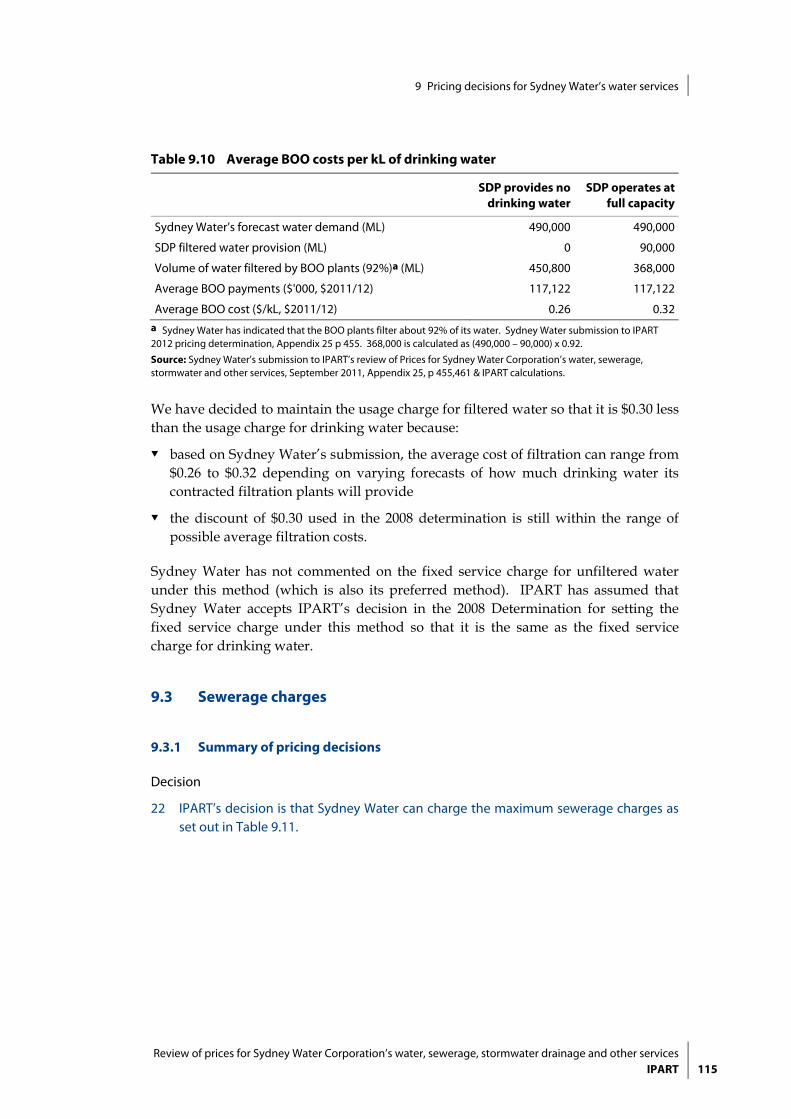

Review of prices for Sydney Water Corporation’s …...Contents Review of prices for Sydney Water...

244

Independent Pricing and Regulatory Tribunal Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services From 1 July 2012 to 30 June 2016 Water — Final Report June 2012

Transcript of Review of prices for Sydney Water Corporation’s …...Contents Review of prices for Sydney Water...

Independent Pricing and Regulatory Tribunal

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesFrom 1 July 2012 to 30 June 2016

Water — Final ReportJune 2012

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services From 1 July 2012 to 30 June 2016

Water — Final Report June 2012

ii IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

© Independent Pricing and Regulatory Tribunal of New South Wales 2012

This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism and review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgement of the source is included.

ISBN 978-1-922127-04-4

The Tribunal members for this review are:

Dr Peter Boxall AO, Chairman

Mr James Cox PSM, Chief Executive Officer and Full Time Member

Ms Sibylle Krieger, Part Time Member

Inquiries regarding this document should be directed to a staff member:

Lucy Garnier (02) 9290 8453

Scott Chapman (02) 9290 8449

Independent Pricing and Regulatory Tribunal of New South Wales PO Box Q290, QVB Post Office NSW 1230 Level 8, 1 Market Street, Sydney NSW 2000

T (02) 9290 8400 F (02) 9290 2061

www.ipart.nsw.gov.au

Contents

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART iii

Contents

1 Executive summary 1 1.1 Overview of determination 1 1.2 Impact on residential customer bills 9 1.3 Impact on non-residential customers 11 1.4 Impact of Sydney Desalination Plant on customers 13 1.5 Impact on Sydney Water 14 1.6 Structure of this report 19

2 Context for this review 20 2.1 Other reviews that have affected our decisions and inputs 21 2.2 IPART’s review process 22 2.3 Matters we are required to consider 23 2.4 Overview of Sydney Water’s submissions 25

3 IPART’s approach to setting prices 29 3.1 Overview of price setting approach 29 3.2 Length of the determination period 30 3.3 Approach for determining the notional revenue requirement 33 3.4 Approach for converting the notional revenue requirement into prices 35 3.5 Approach for addressing the risk of significant variation between actual and

forecast water sales 38 3.6 Approach to addressing uncertainty about SDP’s operating schedule and its

impact on Sydney Water’s costs 40 3.7 Obligations on Sydney Water to report on its progress against output

measures 41

4 Overview of IPART’s findings and decisions on Sydney Water’s revenue requirements 43 4.1 Summary of findings and decisions on revenue requirements 44 4.2 Sydney Water’s proposed notional revenue requirement 44 4.3 IPART’s finding on the notional revenue requirement 45 4.4 IPART’s decision on target revenue 47 4.5 IPART’s finding on revenue from trade waste services and other fees and

charges 48

Contents

iv IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

5 Operating expenditure 52 5.1 Summary of IPART’s finding 52 5.2 Sydney Water’s submission 53 5.3 Stakeholder comments 58 5.4 Atkins Cardno’s review 59 5.5 IPART’s analysis 65

6 Capital expenditure 69 6.1 Summary of IPART’s decisions 70 6.2 Assessing Sydney Water’s past capital expenditure 71 6.3 Assessing Sydney Water’s forecast capital expenditure 75 6.4 Calculating the annual value of the RAB over the determination period 83 6.5 Calculating the allowance for a return on assets 85 6.6 Calculating the allowance for regulatory depreciation 87

7 Sydney Water’s forecast water sales 90 7.1 Decisions 91 7.2 Sydney Water’s Proposed Approach 92 7.3 Alternatives to Sydney Water’s Model 95 7.4 Stakeholder Consultation 96 7.5 IPART’s Analysis 98

8 Outcomes from review of price structures 99 8.1 Price structures review for the 4 water utilities 99 8.2 Price structures for Sydney Water 101 8.3 Impacts on Sydney Water’s customers from proposed price reform 104

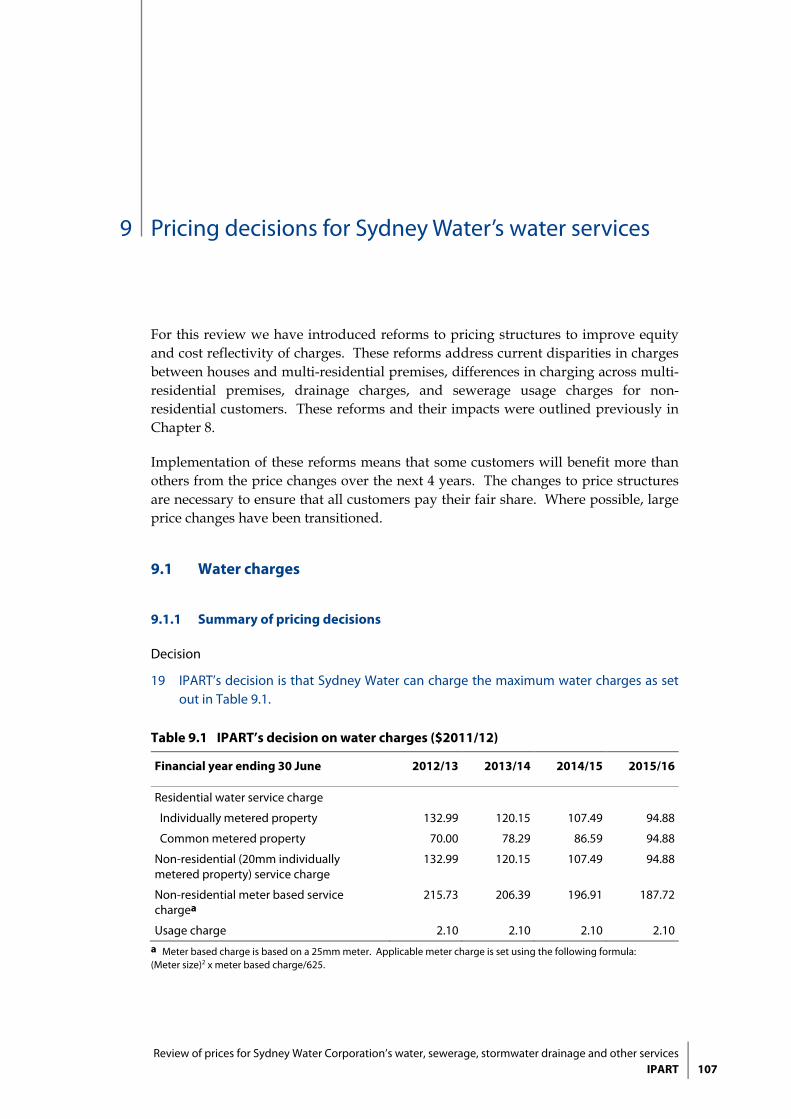

9 Pricing decisions for Sydney Water’s water services 107 9.1 Water charges 107 9.2 Unfiltered water charges 113 9.3 Sewerage charges 115 9.4 Stormwater drainage charges 121 9.5 Charges for the Rouse Hill Area 124 9.6 Recycled water 130 9.7 Trade waste charges 134 9.8 Miscellaneous charges 148 9.9 Minor service extension charges 151 9.10 Exempt land 152 9.11 Combination and mixed development 153 9.12 Unmetered properties 154

Contents

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART v

10 Implications of pricing decisions for Sydney Water customers 156 10.1 Summary of findings on implications for customers 156 10.2 Impact of price restructuring on different customers 157 10.3 Impact on the affordability of services for residential customers 161 10.4 Impact on the affordability of services for non-residential customers 174 10.5 Impact of 2008 decision to limit Sydney Water’s ability to levy developer

charges 179

11 Implications of pricing decisions for Sydney Water’s service standards, financial viability and other issues 181 11.1 Implications for Sydney Water’s service standards 181 11.2 Impact on Sydney Water’s financial viability and shareholders 182 11.3 Implications for general inflation 186 11.4 Implications for the environment 186

Appendices 187 A Matters to be considered by IPART under section 15 of the IPART Act 189 B Sydney Water’s output measures and capital expenditure program 191 C Weighted average cost of capital 197 D Calculating the tax allowance 213 E Long Run Marginal Cost of Water 215 F Water and sewerage bills and disposable income analysis for Sydney Water 225 G List of decisions 229

Glossary 233

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 1

1 Executive summary

The Independent Pricing and Regulatory Tribunal of NSW (IPART) is responsible for regulating the prices Sydney Water Corporation (Sydney Water) can charge for the water supply, sewerage and stormwater drainage services it provides to its residential and non-residential customers, as well as some of its recycled water services and a range of miscellaneous services (including trade waste). We recently completed our review and made our determination on the maximum prices Sydney Water can charge for these services over the 4-year period from 1 July 2012 to 30 June 2016 (the 2012 determination period).

This report explains our determination, including our key decisions and the analysis and rationale that underpin those decisions.

1.1 Overview of determination

While Sydney Water proposed average price increases of around 15% in real terms1 over the determination period, our determination means that water supply prices will go down in real terms over this period. As a result, most customers will experience a slight decrease in their annual water and sewerage bills in real terms (and a slight increase once inflation is incorporated into prices). For example, the annual bill for a typical residential customer living in a freestanding house will fall by $29 in real terms between 2012 and 2016. The main reason for this is that our decision that Sydney Water’s revenue requirement over this period is lower than it proposed.

However, some customers will experience larger decreases and others real increases in their annual water and sewerage bills. This is due to our decision to restructure water, sewerage and stormwater prices to remove cross-subsidies between customer groups and improve the cost-reflectivity of these prices. This price restructuring will not increase the total revenue Sydney Water receives for services. Rather, it removes inequities and improves the balance between fixed service charges and variable usage charges so customers in all groups pay bills that better represent the costs they impose on Sydney Water. The price restructuring also ensures that Sydney Water’s prices send efficient price signals.

1 That is, before inflation is applied.

1 Executive summary

2 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

To mitigate the impacts of these price changes on Sydney Water and its customers, we have adopted a glide path approach in setting prices. That is, we have calculated the prices required in the final year and set prices in the interim years to transition to those prices. This smooths out the price fluctuations that would otherwise occur.

1.1.1 Our decision on Sydney Water’s revenue requirement

Sydney Water estimated that its revenue requirement will increase by an average of 4.2% per year over the determination period,2 and therefore proposed average price increases of around 15% (in real terms). However, based on our analysis and calculations, we decided that its revenue requirement will remain fairly stable during the period, increasing by an average of only 0.7% per year (real terms).

There are 4 main reasons why our decision on the revenue requirement is lower than Sydney Water’s estimate, the first 2 of which are methodological:

1. We used a real post-tax Weighted Average Cost of Capital (WACC) in calculating the allowances for returns on and of assets and included tax liabilities as a separate cost building block, in line with our recent decision on our approach for determining water utilities’ revenue requirements.3 In its submission, Sydney Water used a real pre-tax WACC, in line with our previous approach.

2. We set prices based on the assumption that the Sydney Desalination Plant (SDP) will be in water security mode for the full 4 years of the determination period, and any costs associated with periods of plant operation will be passed through to customers in the next year.4 Sydney Water proposed prices on the basis that SDP will be in full operation mode, and any savings associated with periods of shutdown will be passed through in the next year.

3. We decided that the appropriate level of post-tax WACC for Sydney Water is 5.6%, which is lower than Sydney Water proposed. This decision is consistent with, and similar to, the WACC we used in determining prices for the Sydney Desalination Plant (although we used a pre-tax WACC for SDP’s determination, in line with our approach at that time).5 In reaching this decision, we took account of the current uncertainties in the market by considering long-term averages and selecting a WACC at the top end of the range.

2 Sydney Water proposed an increase of $401 million (around 17%) over its 2011/12 revenue for

2015/16. 3 IPART, The incorporation of company tax in price determinations, June 2011. 4 Our determination allows for any additional bulk water costs incurred by Sydney Water due to

SDP operating and supplying water (in accordance with the Metropolitan Water Plan) to be passed through to customers’ bills in the following year. This will increase typical residential bills by around $30 in 2015/16. Quoted bills include approximately $100 per year to cover payments to SDP operating in water security mode.

5 Our decision was that the real pre-tax WACC for SDP is 6.7%. Our calculations indicated that our decision that the real post-tax WACC of 5.6% for Sydney Water is equivalent to a real pre-tax WACC of approximately 6.6% (using the same input parameters for both calculations). For more information about these parameters see Appendix C.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 3

4. We allowed for lower capital and operating expenditure than Sydney Water proposed, in line with our view that there are opportunities for it to make efficiency savings in some areas of its proposed expenditure.

To illustrate the impact of our decisions for the final determination (including those discussed above), Table 1.1 shows how a typical residential bill would have changed under Sydney Water’s proposal and compares it to the change under our draft and final determinations.

Table 1.1 Change in a typical residential water and sewerage bill between 2011/12 and 2015/16 under Sydney Water’s proposal and IPART’s draft and final determinations ($2011/12)

$2011/12

Change in current bill under Sydney Water’s proposal +166 +166

Impact of IPART decisions: Draft Final

Use post-tax rather than pre-tax WACCa -54 -52

Use of post-tax WACC of 5.5% (draft determination) 5.6% (final determination)

-89 -64

Set prices on basis that SDP is in water security shutdown mode -38 -38

Update proposed SDP-related costs to reflect our final determination on SDP’s pricesb

-12 -12

Apply efficiency savings to proposed operating expenditure -9 -9

Apply efficiency savings to proposed capital expenditurec -19 -18

Other (including changes to price structures) -3 -3

Total impact of IPART decisions on bill on Sydney Water’s proposal -223 -195

Total change in current bill under IPART’s determination -57 -29a The change between the draft and final reports incorporates a correction to our calculation to include a tax allowance on Assets Free of Charge. b As Sydney Water made its submission before we completed our determination on SDP’s prices, it included SDP’s proposed prices. These proposed prices were higher than those we subsequently determined. c The change between the draft and final reports is due to our decision to allow additional stormwater capital expenditure and the avoided costs of Rouse Hill recycled water plant.

Note: Assumes 200kL consumption. Totals may vary due to rounding.

1.1.2 Our decision to restructure prices

In making our 2012 determination, we considered the findings of our recent broad review of the price structures of Sydney Water and the other metropolitan water utilities we regulate.6 This review found that under the current price structures, the fixed charges that some Sydney Water customers pay do not reflect the cost of making the services available to them. As a result, other customer groups are paying more than the cost of providing their service.

6 IPART, Review of price structures for metropolitan water utilities – Final Report, March 2012.

1 Executive summary

4 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

To remove these cross-subsidies and improve the equity and cost-reflectivity of Sydney Water’s prices for all customers, we made decisions to:

Introduce a standard water service charge of $94.88 per year for all residential customers, regardless of their property type. Currently, there is no standard water service charge for residential customers with a unit in a multi-dwelling property with a shared meter. On average, these customers pay around $70 per year, but some pay as little as $5 to $10 a year.7 In contrast, residential customers with a single-dwelling property or a unit with an individual meter pay a standard water service charge of $144.79 per year.

We consider all residential customers impose similar costs on Sydney Water in having a water supply service to their home, and so should all pay the same price for this availability. We note that differences in customers’ water usage are already accounted for through the variable water usage charge. Therefore, we have decided to introduce a standard water service charge for all residential customers.

As a result of this decision, many households in units with a shared meter will pay a higher service charge than currently, while all those in houses and units with an individual meter will pay a lower service charge. To minimise the impacts of this price restructuring on customers and Sydney Water, we have set water services charges so they transition towards the standard charge over several years. All customers will pay the standard charge by 1 July 2015.

Remove the standard sewerage service charge for non-residential customers with a strata unit in a property with a shared meter, and replace it with a meter-based charge. These customers currently pay a service charge equal to the sewerage service charge for customers with an individual 20mm meter. In contrast, those in single-owner properties with a shared meter pay a pro-rata share of the applicable sewerage service charge for the property’s meter size.8 This means that non-residential customers in properties with the same size meter can pay very different charges for the same service, depending on the property’s title. It also means that collectively, those in strata units contribute more than their share of Sydney Water’s fixed sewerage costs, and thus cross-subsidise those in non-strata properties.

To remove this cross-subsidisation, we have decided to restructure sewerage service charges so that all non-residential customers in a property with a shared meter pay a pro-rata share of charge applicable to the property’s meter size. This results in increases in the total building charge for single owner properties with a meter size of 25mm or larger. However, once this charge is shared, the charge applicable to many non-residential customers within those properties will decrease as they will no longer be subject to the standard charge.

7 This is because Sydney Water charges these customers on the basis of a share of a meter based

charge. 8 Sydney Water invoices the property owner a single charge based on the meter size.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 5

Reduce the sewerage usage charge for non-residential customers so it moves towards a level that reflects the short run marginal cost of treating sewage. Currently, the level of Sydney Water’s sewerage usage charge is above the estimated unit cost of collection, treatment and disposal of sewage. We are concerned that this provides a poor pricing signal and could provide perverse incentives for some large customers to adopt on-site recycling where this is not efficient. If this were to occur, Sydney Water may lose some of its sewerage revenue stream and need to recover costs through higher charges to its remaining customers. As the estimated unit cost of collection, treatment and disposal of sewage is significantly less that the current usage charge, we have decided to transition the charge towards this cost over the determination period. As a result, the sewerage usage charge decreases by 32% over the period.

Set area-based stormwater drainage charges. Sydney Water supplies stormwater drainage services to a small proportion of its customers.9 These customers currently pay a fixed charge, based on whether they are residential or non-residential. However, as the area of land serviced is a key determinant of the costs of a drainage system, a customer’s property size can be used as a simple proxy for their contribution to these costs.10 Given this, we have decided to introduce area-based stormwater drainage charges over the determination period to make the charges more cost reflective.

Residential customers will pay fixed charges ($/year) based on their property type (single or multi-dwelling) as a proxy for property size. Non-residential customers will pay fixed charges depending on which of 5 property-size bands they fall into. As a result of this decision, customers with relatively small properties (such as units) will pay lower charges, while those with larger properties will pay higher charges.

1.1.3 Price outcomes

Under the determination, the prices for some services for most customers decrease over the determination period, while those for others increase or stay the same (in real terms).11

For water supply services (Table 1.2):

The fixed service charges ($ per year) decrease in each year of the period. For residential customers with individual meters, the standard charge falls by 34.5% from its current level by 2015/16. For non-residential customers, it falls by 17% by 2015/16.

9 There are just over 500,000 customers, mostly located in the inner west and inner south west of

Sydney who receive stormwater drainage services from Sydney Water. For the remaining customers, stormwater drainage services are supplied by their local council.

10 There are also other determinants such as such as slope of the ground, the percentage of impervious ground, the percentage of water that drains off the property, on-site retention and storage devices and the nature of the land usage that also drive costs.

11 That is, the price before adjusting for inflation.

1 Executive summary

6 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

The variable usage charge ($ per kilolitre) for drinking water does not change over the determination period, and the charge for unfiltered water increases by only 1.4% compared to its current level.

Table 1.2 Prices for water supply services ($2011/12)

Current (2011/12) 2012/13 2013/14 2014/15 2015/16

Total change

Service charges ($/year) Residential - individual meter

144.79 132.99 120.15 107.49 94.88 -34.5%

Residential - common meter

N/A a 70.00 78.29 86.59 94.88 NA

Non residential

20mm individual meter 144.79 132.99 120.15 107.49 94.88 -34.5%

20mm meter 144.79 138.07 132.09 126.02 120.14 -17.0%

25mm meter 226.24 215.73 206.39 196.91 187.72 -17.0%

32mm meter 370.66 353.45 338.15 322.62 307.56 -17.0%

40mm meter 579.17 552.27 528.36 504.09 480.56 -17.0%

50mm meter 904.95 862.92 825.56 787.64 750.88 -17.0%

80mm meter 2,317 2,209 2,113 2,016 1,922 -17.0%

100mm meter 3,620 3,452 3,302 3,151 3,004 -17.0%

150mm meter 8,145 7,766 7,430 7,089 6,758 -17.0%

200mm meter 14,479 13,807 13,209 12,602 12,014 -17.0%

300mm meter 32,579 31,065 29,720 28,355 27,032 -17.0%

Usage charges ($/kilolitre)

Usage - drinking water 2.10 2.10 2.10 2.10 2.10 0%

Usage - unfiltered water 1.78 1.80 1.80 1.80 1.80 1% a Customers with a shared meter such as apartments currently pay a share of the service charge which is based on the size of the meter. This share depends on the number of units being served by the meter and the size of the meter. Under our determination, all apartments will now pay a set annual service charge.

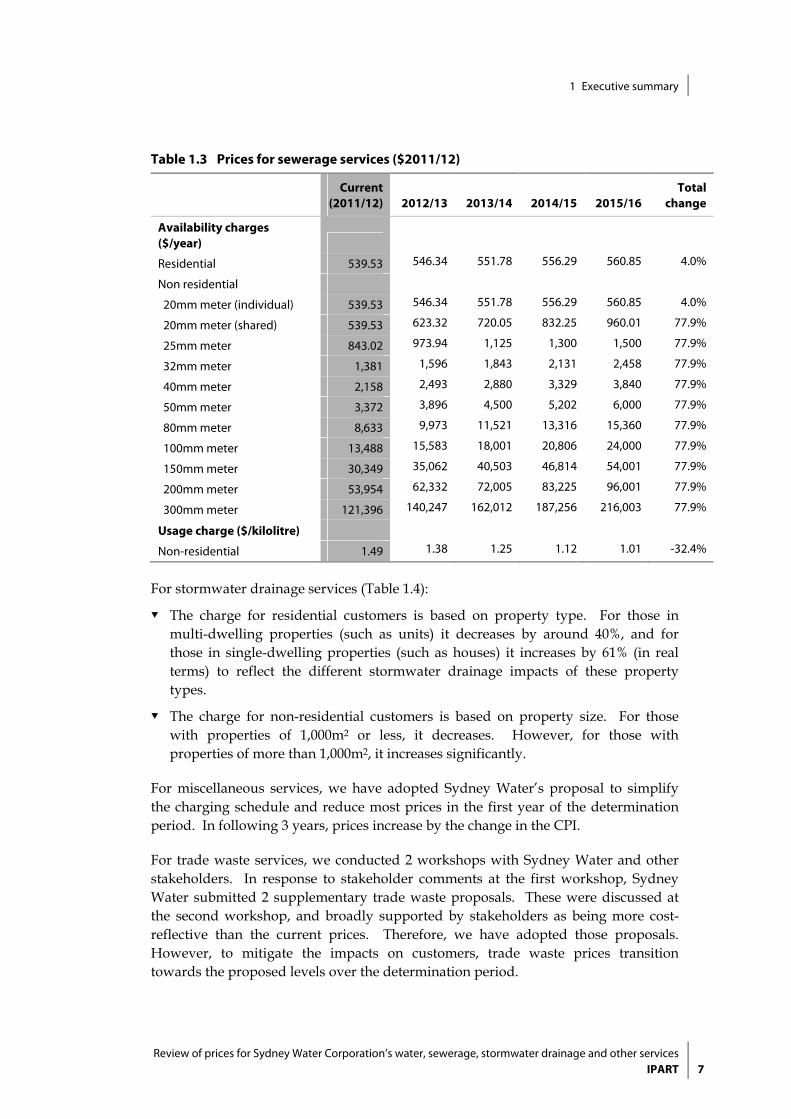

For sewerage services (Table 1.3):

The fixed service charge ($ per year) for residential customers and for almost half of non-residential customers increases by 4% over the determination period. For other non-residential customers – those with individual meters of 25mm diameter or greater – this charge increases by around 78%.

The variable usage charge ($ per kilolitre) for non-residential customers decreases by around one-third over the period. However, the threshold volume of sewerage discharge above which non-residential customers are liable to pay the charge also decreases by 50 kL per year to 300kL in 2015/16.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 7

Table 1.3 Prices for sewerage services ($2011/12)

Current(2011/12) 2012/13 2013/14 2014/15 2015/16

Total change

Availability charges ($/year)

Residential 539.53 546.34 551.78 556.29 560.85 4.0%

Non residential

20mm meter (individual) 539.53 546.34 551.78 556.29 560.85 4.0%

20mm meter (shared) 539.53 623.32 720.05 832.25 960.01 77.9%

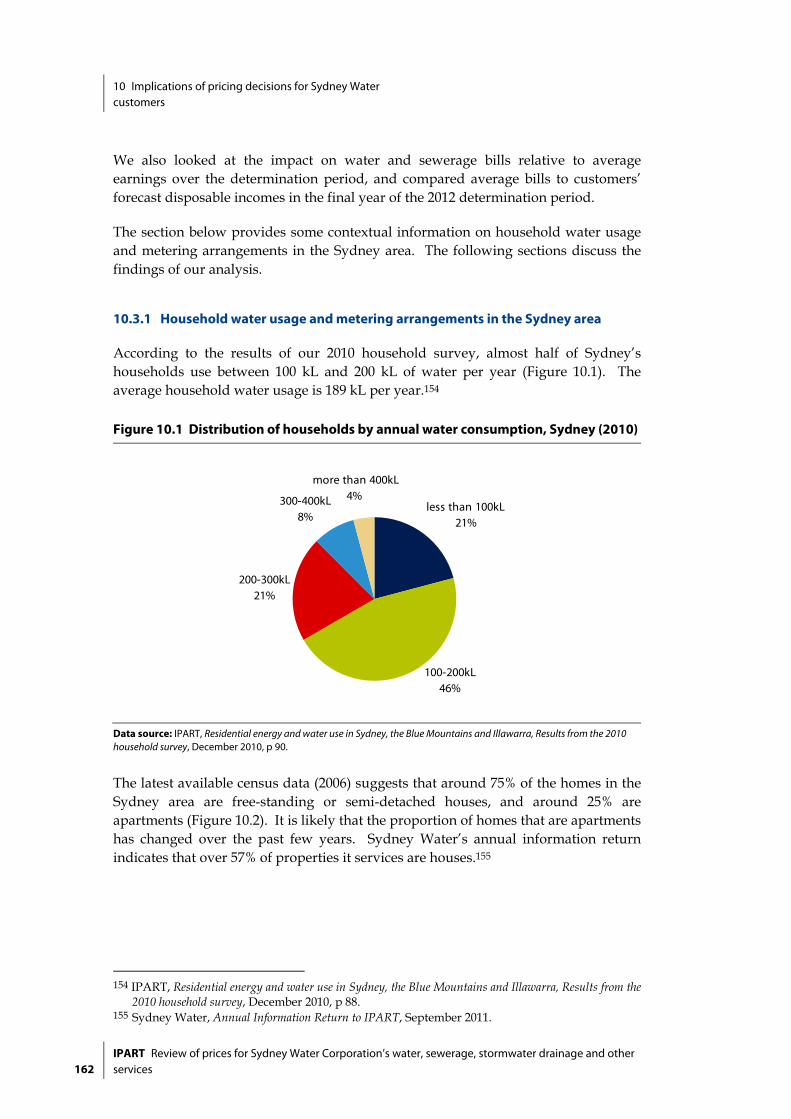

25mm meter 843.02 973.94 1,125 1,300 1,500 77.9%

32mm meter 1,381 1,596 1,843 2,131 2,458 77.9%

40mm meter 2,158 2,493 2,880 3,329 3,840 77.9%

50mm meter 3,372 3,896 4,500 5,202 6,000 77.9%

80mm meter 8,633 9,973 11,521 13,316 15,360 77.9%

100mm meter 13,488 15,583 18,001 20,806 24,000 77.9%

150mm meter 30,349 35,062 40,503 46,814 54,001 77.9%

200mm meter 53,954 62,332 72,005 83,225 96,001 77.9%

300mm meter 121,396 140,247 162,012 187,256 216,003 77.9%

Usage charge ($/kilolitre)

Non-residential 1.49 1.38 1.25 1.12 1.01 -32.4%

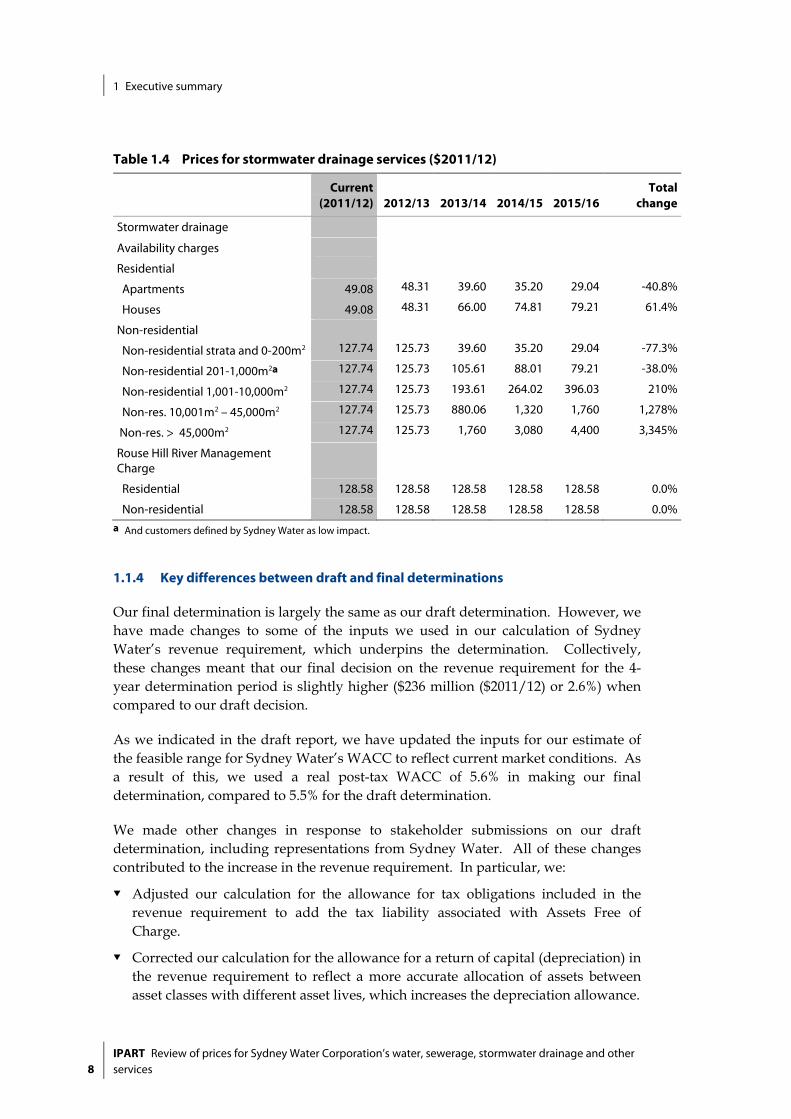

For stormwater drainage services (Table 1.4):

The charge for residential customers is based on property type. For those in multi-dwelling properties (such as units) it decreases by around 40%, and for those in single-dwelling properties (such as houses) it increases by 61% (in real terms) to reflect the different stormwater drainage impacts of these property types.

The charge for non-residential customers is based on property size. For those with properties of 1,000m2 or less, it decreases. However, for those with properties of more than 1,000m2, it increases significantly.

For miscellaneous services, we have adopted Sydney Water’s proposal to simplify the charging schedule and reduce most prices in the first year of the determination period. In following 3 years, prices increase by the change in the CPI.

For trade waste services, we conducted 2 workshops with Sydney Water and other stakeholders. In response to stakeholder comments at the first workshop, Sydney Water submitted 2 supplementary trade waste proposals. These were discussed at the second workshop, and broadly supported by stakeholders as being more cost-reflective than the current prices. Therefore, we have adopted those proposals. However, to mitigate the impacts on customers, trade waste prices transition towards the proposed levels over the determination period.

1 Executive summary

8 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Table 1.4 Prices for stormwater drainage services ($2011/12)

Current

(2011/12) 2012/13 2013/14 2014/15 2015/16 Total

change

Stormwater drainage

Availability charges

Residential

Apartments 49.08 48.31 39.60 35.20 29.04 -40.8%

Houses 49.08 48.31 66.00 74.81 79.21 61.4%

Non-residential

Non-residential strata and 0-200m2 127.74 125.73 39.60 35.20 29.04 -77.3%

Non-residential 201-1,000m2a 127.74 125.73 105.61 88.01 79.21 -38.0%

Non-residential 1,001-10,000m2 127.74 125.73 193.61 264.02 396.03 210%

Non-res. 10,001m2 – 45,000m2 127.74 125.73 880.06 1,320 1,760 1,278%

Non-res. > 45,000m2 127.74 125.73 1,760 3,080 4,400 3,345%

Rouse Hill River Management Charge

Residential 128.58 128.58 128.58 128.58 128.58 0.0%

Non-residential 128.58 128.58 128.58 128.58 128.58 0.0%a And customers defined by Sydney Water as low impact.

1.1.4 Key differences between draft and final determinations

Our final determination is largely the same as our draft determination. However, we have made changes to some of the inputs we used in our calculation of Sydney Water’s revenue requirement, which underpins the determination. Collectively, these changes meant that our final decision on the revenue requirement for the 4-year determination period is slightly higher ($236 million ($2011/12) or 2.6%) when compared to our draft decision.

As we indicated in the draft report, we have updated the inputs for our estimate of the feasible range for Sydney Water’s WACC to reflect current market conditions. As a result of this, we used a real post-tax WACC of 5.6% in making our final determination, compared to 5.5% for the draft determination.

We made other changes in response to stakeholder submissions on our draft determination, including representations from Sydney Water. All of these changes contributed to the increase in the revenue requirement. In particular, we:

Adjusted our calculation for the allowance for tax obligations included in the revenue requirement to add the tax liability associated with Assets Free of Charge.

Corrected our calculation for the allowance for a return of capital (depreciation) in the revenue requirement to reflect a more accurate allocation of assets between asset classes with different asset lives, which increases the depreciation allowance.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 9

Adjusted the operating expenditure included in the revenue requirement to incorporate additional filtration costs12 and account for lower forecast revenue from the Rosehill-Camellia recycled water scheme.

Increased the value of the Regulatory Asset Base used to calculate the allowances for a return on assets and depreciation to allow for higher stormwater capital expenditure over the determination period and include the value of avoided costs arising from the Rouse Hill recycled water scheme.

Updated trade waste revenues and costs to reflect our final decision to adopt Sydney Water’s supplementary trade waste proposals and allow it to recover the under-recovery due to the transition period from all sewerage customers.

In addition, we considered stakeholder submissions on the move to area based stormwater drainage charges and replaced the variable charge for very large properties with an additional fixed price band.

1.2 Impact on residential customer bills

As a result of the determination, most residential customers’ water and sewerage bills will decrease slightly in real terms over the determination period, and increase modestly in nominal terms. For example, the bill for a household with an individual water meter and water usage of 200kL per year13 will decrease in real terms by 2.6% (or $29) over the 4-year period, or by an average of 0.7% per year. When inflation is included in prices, this bill will increase by 6.5% (or $72) over 4 years, or by an average of 1.6% per year.14 This means that water and sewerage bills will increase at a slower rate than other household items, and typically income.

However, households with a shared water meter (such as many of those with a unit in a multi-dwelling property) will experience different changes to their bill, due to our decision to set a standard water service charge of $94.88 ($2011/12) for all residential customers by 2015/16 (see section 1.1.2 above). The impact of this decision will depend on the customer’s current water service charge, which varies from property to property. For example, the bill for a household with a current water service charge of $70 (the average for customers in units with a shared meter) and water usage of 135kL per year15 will increase in real terms by 5.1% (or $45.80) over the determination period, or an average of 1.3% per year. However, this increase will be offset by the reduction in the stormwater drainage charge for those customers who receive this service.

12 As a result of the Sydney Desalination Plant operating assumptions. 13 This is the average water usage for residential customers in houses. 14 Assuming forecast change in the CPI of 2.5% from 2013/14 onwards, in line with the midpoint

of the Reserve Bank of Australia’s inflation target range. 15 Based on our household survey 135 kL is the median consumption for residential customers in

flats and units.

1 Executive summary

10 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Table 1.5 shows the indicative impact of the determination on residential water and sewerage bills for customers with individual meters and various levels of water usage (with and without inflation).

Table 1.5 Impact of determination on annual water and sewerage bills for residential customers with individual meters

Water usage pa

Current (2011/12)

2012/13 2013/14 2014/15 2015/16 Total change

Without inflation

100 kL 895 889 882 874 866 -29

change -0.6% -0.8% -0.9% -0.9% -3.2%

200 kL 1,105 1,099 1,092 1,084 1,076 -29

change -0.5% -0.7% -0.7% -0.7% -2.6%

300 kL 1,315 1,309 1,302 1,294 1,286 -29

Change -0.4% -0.6% -0.6% -0.6% -2.2%

With inflation

100 kL 895 904 918 933 947 53

Change 1.0% 1.6% 1.6% 1.6% 5.9%

200 kL 1,105 1,117 1,137 1,157 1,177 72

Change 1.1% 1.8% 1.7% 1.7% 6.5%

300 kL 1,315 1,330 1,356 1,381 1,407 92

Change 1.1% 1.9% 1.9% 1.9% 7.0%

Note: Totals may vary due to rounding.

Households that include pensioners will be largely unaffected by our determination, regardless of their property type.16 Their water and sewerage bills will stay fairly constant, increasing by $3 in real terms over the determination period.

Households that receive stormwater drainage services from Sydney Water will experience other changes to their bills, due to our decision to transition to area-based charges for these services (see section 1.1.2):

For households in units, these charges will decrease over the determination period, moving from $49 in 2012/13 to $29 in 2015/16 (in real terms). On average, this will offset almost half of the increase in their water and sewerage bills due to our decision to introduce a standard water service charge for residential customers (discussed above). As a result, the combined water, sewerage and stormwater drainage bill for a typical household in a unit should increase only slightly over the determination period in real terms.

16 See chapter 10 for an explanation of the concessions for pensioners.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 11

For households in houses, these charges will increase over the determination period, moving from $49 in 2012/13 to $79 in 2015/16 (in real terms). To mitigate the impact on these households, we decided to transition to the new stormwater drainage charges over this determination period.

1.3 Impact on non-residential customers

Non-residential customers with individual, 20mm meters – who make up nearly half of Sydney Water’s non-residential sewerage customers – will experience a reduction in their total water and sewerage bills.17 This is largely due to decreases in the water service and sewerage usage charges applicable to these customers.

However, those with individual, 25mm or larger meters will face higher bills. This is due to our decision to restructure sewerage service charges, which resulted in increases in these charges per property (see section 1.1.2). The customers most affected are those with relatively low sewage discharge volumes.18 For those with large sewage volumes, the impact of higher sewerage service charges is offset by lower usage charges, so their bill increases are lower in percentage terms.

Table 1.6 shows the indicative impact of the determination on non-residential water and sewerage bills for customers with individual meters, various levels of water usage and average sewerage discharge volumes (in real terms).

Table 1.6 Impact of determination on annual water and sewerage bills for non-residential customers with individual meters ($2011/12)

Water usage pa

Meter size

Current(2011/12)

2012/13 2013/14 2014/15 20/1516 Total change

260 kL 20mm 1,231 1,225 1,218 1,210 1,202 -29

%increase -0.5% -0.6% -0.7% -0.7% -2.4%

350 kL 25mm 1,628 1,720 1,830 1,959 2,108 479

%increase 5.6% 6.4% 7.0% 7.6% 29.4%

1,000 kL 40mm 4,820 5,090 5,391 5,729 6,107 1,287

%increase 5.6% 5.9% 6.3% 6.6% 26.7%

10,000 kL 100mm 46,354 47,028 47,886 49,075 50,605 4,251

%increase 1.5% 1.8% 2.5% 3.1% 9.2%

Note: Totals may vary due to rounding.

Note: Average sewage discharge factors used.

17 We have assumed water usage of 260 kL per year, which is the average water consumption by

this customer group as reported by Sydney Water. 18 Customers may elect to move from a larger meter size to a 20mm meter if an assessment of their

requirements confirms that a 20mm meter is adequate. Customers requesting to move from a larger meter to a 20mm meter will pay a charge to move to a smaller meter.

1 Executive summary

12 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Non-residential customers with a shared meter will experience varied impacts on their bills, depending on whether or not they are in a strata property, the number of customers that share the property’s meter, and their sewage volumes. Most customers in strata properties will see decreases in their bills, due to our decision to remove the minimum sewerage service charge currently applicable to them (see section 1.1.2). For example, a typical19 non-residential strata premises will see its bill decrease by around $4,000 ($2011/12) or 40%. Strata properties likely to experience increases are larger users, whose current sewerage service charge exceeds the minimum charge, due to the decrease in the sewerage discharge allowance for strata properties.

Table 1.7 shows the indicative impact of the determination on non-residential water and sewerage bills for customers with shared meters, various levels of water usage and average sewerage discharge volumes (in real terms).

Table 1.7 Indicative annual water and sewerage charges for strata units sharing a meter ($2011/12)

Water use (kL pa)

Meter size

Equal strata connections

2011/ 12

2012/ 13

2013/ 14

2014/ 15

2015/ 16

Change 2011/12 to 15/16

75 kL pa per unit

25mm 3 773 486 523 566 615 -158

% increase -37% 8% 8% 9% -20%

350 kL pa per unit

25mm 3 1,351 1,238 1,279 1,323 1,370 20

% increase -8% 3% 3% 4% 1%

75 kL pa per unit

25mm 8 726 285 306 328 351 -375

% increase -61% 7% 7% 7% -52%

350 kL pa per unit

40mm 8 1,348 1,354 1,368 1,388 1,415 67

% increase 0% 1% 2% 2% 5%

75 kL pa per unit

40mm14 739 375 396 420 447 -292

% increase -49% 6% 6% 6% -40%

Note: Non-residential customers on shared maters will not actually receive a bill from Sydney Water for the amounts shown above. They will receive an invoice from Sydney Water directly for their water and sewerage service charges, but will be paying for their water usage charge via their strata levies.

We have applied an average discharge factor of 79%, calculated from information submitted by Sydney Water in early November 2011 in response to requests from IPART. We have also distributed the free threshold allowance for sewerage evenly between strata units.

Note: Totals may vary due to rounding.

Source: IPART analysis.

19 Sydney Water email 22 May 2012. Typical property is 14 units connected to a 40mm meter and

water consumption of around 1,050kL per year.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 13

Non-residential customers who receive stormwater drainage services from Sydney Water will also experience varied impacts, depending on the size of their property. Those whose property area is 1,000m2 or less – who make up the majority of these customers – will pay lower stormwater drainage charges over the determination period. In 2015/16, they will pay up to $99 less than in 2012.

Those whose property area is 10,001m2 or more – who number around 500 – will pay increasingly higher stormwater drainage charges over the period. We recognise that these price increases are large, and may have a significant impact on some customers. However, after considering the submissions received from stakeholders in response to our draft report, we have replaced the variable charge applicable to the very largest properties (those with property areas greater than 45,000m2) with a capped fixed charge.

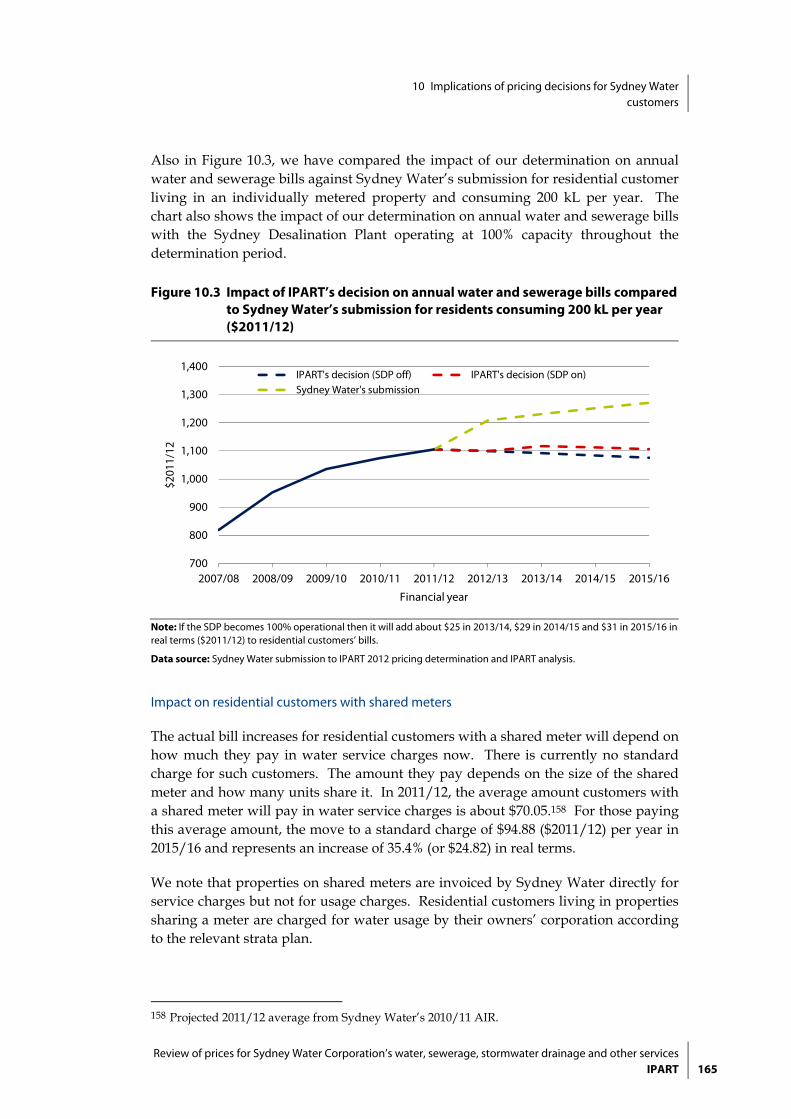

1.4 Impact of Sydney Desalination Plant on customers

As section 1.1.1 above discussed, in making the determination we assumed that SDP will be in water security mode over the full 4-year determination period. If this is not the case, and Sydney Water is required to purchase drinking water from the SDP in any year of this period, we have provided for Sydney Water to pass through the associated costs to customers by adjusting prices in the following year.

The size of these costs and their impact on customers will depend on SDP’s actual operating schedule. However, as an indication, if SDP operates at 100% capacity for any full year it will cost Sydney Water an additional $50 million to $65 million ($2011/12).20 For residential customers and most non-residential customers (those with a 20mm individual meter), this will add an additional $25 to $31 ($2011/12) to their annual water and sewerage bill in the following year. For other non-residential customers, it will add varied amounts to their annual bill, depending on their meter size and whether that meter is shared with other customers. However, those with an individual 25mm meter will pay an additional $44 to $61 ($2011/12) each year and those with larger meters will pay proportionately higher amounts.21

Table 1.8 shows the likely impact on residential water and sewerage bills if SDP is required to operate at full capacity for the full 4 years.

20 The actual amount varies from approximately $50 million ($2011/12) in the first year to

approximately $65 million ($2011/12) in 2015/16. 21 If SDP has to restart and/or shut down over the period, Sydney Water will incur large one-off

charges of up to $5.5 million. If this occurs, this will also add to customer bills.

1 Executive summary

14 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Table 1.8 Impact of determination on annual water and sewerage bills for residential customers with individual meters if SDP operates at full capacity ($2011/12) – SDP operating at full capacity

Water usage pa

Current (2011/12)

2012/13 2013/14 2014/15 2015/16 Total change SDP on

100 kL 895 889 907 902 896 1

change -0.6% 2.0% -0.5% -0.7% 0.1%

200 kL 1,105 1,099 1,117 1,112 1,106 1

change -0.5% 1.6% -0.4% -0.5% 0.1%

300 kL 1,315 1,309 1,327 1,322 1,316 1

change -0.4% 1.3% -0.3% -0.5% 0.1%

Note: Totals may vary due to rounding.

Note: The 2012/13 bills are the same for whether SDP is operating or not because the cost pass-through is implemented in the year following the year of operation. If SDP is operating in 2015/16 this will be accounted for in the first year of the next determination.

1.5 Impact on Sydney Water

Under our determination, Sydney Water is expected to generate a total of $9,150.4 million ($2011/12) in revenue over the 4-year determination period. We consider this is sufficient to recover its efficient costs and earn a reasonable rate of return on its assets over this period. This is approximately $145 million more than the target revenue for the draft determination, and approximately $1,176 million (or 11%) less than Sydney Water’s proposed revenue requirement.

In its submission, Sydney Water indicated that its revenue requirement will increase over the determination period, due to forecast increases in the costs of maintaining and renewing its assets, servicing urban growth, implementing the Priority Sewerage Program, and other factors including the carbon price. However, based on our views of the efficiency and prudence of its past and forecast expenditures and the market cost of capital, we found that its revenue requirement should remain fairly stable (within 1% to 2%) over determination period.

Table 1.9 compares our final decision on the notional revenue requirement with our draft decision and Sydney Water’s proposal.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 15

Table 1.9 Notional revenue requirement ($million, 2011/12)

2012/13 2013/14 2014/15 2015/16

Sydney Water’s proposal

Return on assets 955.5 995.5 1,034.9 1,069.4

Return of assets (depreciation) 211.1 226.4 241.4 255.1

Operating expenditurea 1,361.7 1,372.1 1,374.3 1,374.3

Total notional revenue requirement 2,528.3 2,594.0 2,650.7 2,698.8

IPART’s draft decision

Return on assetsb 721.9 751.5 781.6 804.0

Return of assets (depreciation) 207.1 219.8 232.0 242.6

Operating expenditure 1,268.5 1,265.8 1,259.6 1,252.5

Total notional revenue requirement 2,197.5 2,237.1 2,273.2 2,299.0

IPART’s final decision

Return on assetsb 761.7 791.8 822.4 844.9

Return of assets (depreciation) 213.1 226.6 239.4 250.3

Operating expenditure 1,283.5 1,276.2 1,270.6 1,263.4

Total notional revenue requirement 2,258.3 2,294.6 2,332.4 2,358.5a Includes costs of bulk water and desalinated water, and an allowance for a return on working capital. b Includes an allowance for a return on working capital and an allowance for tax obligations.

Note: Totals may not add due to rounding.

Note: Figures differ slightly from those presented in Sydney Water’s submission because IPART includes income from some activities that Sydney Water has excluded from its calculation of notional revenue requirement.

Source: Sydney Water submission to IPART’s Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services, 16 September 2011, p109.

We consider that our determination will allow Sydney Water to deliver its services to the required standard and earn a real post-tax rate of return of at least 5.6%. Our modelling shows that the determination will allow Sydney Water to maintain its financial viability, and pay a 70% dividend, and pay a proportion of its capital expenditure in cash in each year of the determination period, assuming that it operates at efficient costs.

1.5.1 Service standards

Our decision on Sydney Water’s revenue requirement assumes that it will maintain its current services levels, and not reduce these levels to achieve cost reductions and efficiency savings. We consider that our prices will continue to allow Sydney Water to meet the service standards required by its operating licence while reducing the potential for price increases to fund over-performance.

1 Executive summary

16 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

1.5.2 Rate of return

As section 1.1.1 discussed, in determining the revenue requirement we used a real post-tax WACC to calculate the allowances for a return on assets and depreciation, and calculated a separate allowance for tax liability. Our recent research22 indicates that this approach leads to a more accurate estimate of a water utility’s tax liability than using a real pre-tax WACC (as we have in previous determinations). We estimate that the move to a post-tax WACC and separate tax allowance has reduced Sydney Water’s notional revenue requirement by around $95 million per annum (or 4%).23

In determining the appropriate level for Sydney Water’s post-tax WACC, we estimated that the feasible range for this level is 4.0% to 5.6%, with a midpoint of 4.6%. We decided that a WACC of 5.6% – the top of this range – is appropriate, largely due to the current market uncertainties with reference to the longer term averages for market parameters.

We consider that our pricing decisions will allow Sydney Water to achieve at least the total notional revenue requirement in each year of the determination period, and thus earn a real post-tax rate of return of 5.6% on its Regulatory Asset Base (RAB) in each year.24

1.5.3 Efficiency savings

In reaching our decision on Sydney Water’s notional revenue requirement, we allowed for lower levels of operating and capital expenditure than it proposed, in line with our view that there are opportunities for it to improve the efficiency of its forecast expenditure programs. This view reflects the findings and recommendations of our consultants, WS Atkins International Ltd and Cardno (Atkins Cardno), who conducted a rigorous review of Sydney Water’s forecast expenditures.25

We allowed for $32.8 million (or around 0.9%) less operating expenditure than Sydney Water proposed over the determination period, to reflect opportunities for making efficiency savings through innovation and technological development, and the catch up efficiency required for Sydney Water to achieve the performance of a Frontier Company over time. However, our final decision on forecast operating expenditure is higher than our draft decision, as it includes the higher filtration expenses Sydney Water incurs when purchasing water from Sydney Catchment Authority rather than the Sydney Desalination Plant.

22 IPART, The incorporation of company tax in price determinations, June 2011. 23 Our calculation of Sydney Water’s allowance for tax liability is set out in Appendix D. 24 If it delivers its services at efficient costs and delivers its capital expenditure program. 25 WS Atkins International and Cardno, Detailed review of Sydney Water’s operating and capital

expenditure, Final Report November 2011.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 17

We allowed for $468 million (or 15.6%) less capital expenditure than Sydney Water proposed. This decision reflects a rephasing of capital programs to beyond the end of the determination period, as well as a slight change in the growth assumptions and the introduction of stretch efficiency targets for Sydney Water, in line with Atkins Cardno’s recommendations. Our final decision on capital expenditure is $16.1 million higher than our draft decision, as we allowed for higher capital expenditure on stormwater assets (as discussed further below).

We also incorporated $65 million less past capital expenditure into Sydney Water’s RAB than it proposed. This reflects our findings that Sydney Water did not consider all the potential options for Priority Sewerage Program projects, some of its expenditure on IT and meter replacement was imprudent, and its property-related expenditure was higher than necessary. We also adjusted Sydney Water’s proposal to reflect the timing of payments made through Developer Commercial Agreements.

Prior to the release of our draft report, Sydney Water wrote to us contesting a number of findings in Atkins Cardno’s report. It argued that at least $285 million of the identified efficiency savings be reinstated and expressed concerns about future service quality. Atkins Cardno provided a response, which can be found on our website. In summary, it put the view that:

Sydney Water’s proposal to increase spending on renewing existing water mains is overly ambitious. It considers it more realistic to increase this spending steadily each year, rather than step it up as Sydney Water proposed. Atkins Cardno reiterated that its recommended expenditure on these programs is still significantly higher than Sydney Water’s actual expenditure since 2008.

Sydney Water’s proposed expenditures for system reliability works and wet weather overflow abatement were not fully developed.

Some of Sydney Water’s proposed expenditure on providing infrastructure for growth could be deferred due to the uncertainty of future growth rates.

Sydney Water could achieve capital efficiency savings of $143 million over the determination period.

Some of Sydney Water’s proposed spending on IT and water meters was not adequately justified.

We considered the arguments put forward by Sydney Water and Atkins Cardno and, for our draft report, decided to adopt the forward capital expenditure program proposed by Atkins Cardno, subject to 2 arithmetical corrections confirmed by Atkins Cardno.

1 Executive summary

18 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Since the release of our draft report, Sydney Water has made a number of further representations with respect to the capital efficiency savings. We have reconsidered its arguments and have maintained our draft decisions with respect to water and sewerage capital expenditure. However, we decided to reinstate Sydney Water’s capital expenditure for stormwater assets. This decision was based on a commitment by Sydney Water to improve the condition of stormwater assets. We note that Sydney Water has proposed and we have allowed for higher stormwater capital expenditure under previous determinations, but it has not delivered its proposed program. In order to monitor this, we have included an output measure to be considered at the next price review.

We note that Atkins Cardno found little evidence of Sydney Water having either a long-term investment plan or a long-term business plan in place. We are concerned by this and the implications for Sydney Water’s asset management and efficient expenditure. We expect Sydney Water to have developed these long-term plans over the 2012 determination period.

1.5.4 Financial viability

We assessed the impact of our final determination we considered Sydney Water’s likely financeability in each year of the determination period using its forecast cash flows under this determination and its actual gearing ratio to compute the following financial ratios:

funds from operations interest cover

funds from operations/total debt

debt gearing.

For this modelling, we applied a 70% dividend payout ratio rather than the fixed dividend assumptions contained in Sydney Water’s submission. We consider that this approach reflects NSW Treasury’s standard reference point of a dividend payout ratio of 70% of post-tax profit for Government businesses.26

However, we note that our decisions on the inputs to the revenue calculations, such as the rate of return on assets, are based on market conditions and are independent of the revenue requirements generated by dividend agreements.

In addition, we considered the financial ratios and dividend payments of other comparable organisations to ensure that the outcomes for Sydney Water were consistent with industry standards.

26 NSW TC 09/11, Treasury Circular – Distribution Policy.

1 Executive summary

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 19

Overall, our financial modelling indicates that Sydney Water’s financial ratios will continue to be sound under the final determination and are improved over the draft determination. We also considered the forecast cash flows and are confident that revenues under our determination are sufficient for Sydney Water to pay a 70% dividend and a proportion of capital expenditure, consistent with a benchmark company. Our conclusions partly depend on whether Sydney Water delivers its services at efficient costs and on demand forecasts. The outcomes of our financial modelling are included in Chapter 11.

1.6 Structure of this report

The following chapters explain our review and determination in detail, including our key decisions and the analysis that guided these decisions:

Chapter 2 outlines the scope and context for the review, including our review process, Sydney Water’s operating and regulatory environment, and Sydney Water’s submission and proposed prices

Chapter 3 outlines our price setting approach and decisions related to the regulatory framework

Chapter 4 explains the ‘building block’ approach we used to establish Sydney Water’s notional revenue requirement, and provides an overview of our decisions on this revenue requirement and its individual components

Chapters 5 and 6 discuss our decisions on these individual components in more detail:

– Chapter 5 explains the decisions on Sydney Water’s efficient operating expenditure

– Chapter 6 explains the decisions on the allowances for a return on assets and regulatory depreciation

Chapter 7 discusses our decisions on Sydney Water’s forecast water sales

Chapters 8 and 9 explain the decisions on Sydney Water’s price structure and set out the price levels

Chapter 10 assesses the implications of our pricing decisions on customers

Chapter 11 assesses the implications of our pricing decisions on Sydney Water, general inflation and the environment.

2 Context for this review

20 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

2 Context for this review

The purpose of this review is to determine the maximum prices Sydney Water can charge for the water, sewerage and stormwater drainage services it provides to residential and non-residential customers in the Sydney, Illawarra and Blue Mountains areas. It is also to determine maximum prices for some recycled water services, trade waste services and the range of miscellaneous services Sydney Water provides.

The review is being conducted in an environment that is significantly different from the one in which we undertook the previous 2 determinations for Sydney Water. Those determinations were made in a time of severe drought in the Sydney area which saw dam levels falling and water restrictions introduced. With the passing of the drought and the commissioning of the SDP, dam levels are currently at, or close to 100%, and water restrictions have been replaced with less stringent Water Wise Rules. The changed environment has some important implications for Sydney Water’s costs, sales, pricing, and financial position. These implications are discussed in the relevant chapters throughout this report.

The sections below outline some other contextual issues that have influenced our review, including other recent reviews that have affected our decisions and inputs, our review process, the matters we are required to consider in making our determination, and Sydney Water’s pricing submissions to the review. Appendix A provides some background information on Sydney Water’s operating and regulatory environment.

2 Context for this review

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 21

2.1 Other reviews that have affected our decisions and inputs

We have recently completed or are concurrently conducting 3 reviews that affect the inputs of our calculations of Sydney Water’s costs and prices. These are:

the review of prices to be charged by the Sydney Catchment Authority27 (SCA) for its bulk water services

the review of prices to be charged by SDP Pty Limited28 for its bulk water services

the review of price structures for metropolitan water utilities.29

Sydney Water purchases most of the bulk water it needs to supply its customers from SCA. For this determination, we have calculated Sydney Water’s bulk water costs on the basis of our determination of SCA’s prices.30

The SDP was built to increase the security of Sydney’s water supply in times of low rainfall, rather than to operate continuously. Under contractual arrangements, it is obliged to operate when Sydney’s dam storage levels fall below 70% of their capacity and continue to operate until they return to 80%. Sydney Water is obliged to purchase the water produced by SDP during such times.

The prices in our determination are set on the basis of SDP being in water security shutdown mode throughout the determination period. If it operates in a different mode and produces water, we have provided that Sydney Water can pass through to customers in the following year the additional costs it incurs. These costs will be calculated on the basis of our 2011 determination on SDP’s prices.

In addition to these reviews, we recently completed a review of price structures for the metropolitan water utilities we regulate. We have decided to restructure Sydney Water’s prices to remove cross-subsidies and improve cost reflectivity for all customer groups. These findings are discussed briefly in Chapter 8. However, for detailed information on the principles, please see the final report on this review on our website.31

27 This review is being conducted concurrently with our Sydney Water review, see IPART, Review

of Sydney Catchment Authority’s Operating Licence and Prices from 1 July 2012. 28 This review was completed in November 2011, see IPART, Review of water prices for Sydney

Desalination Plant Pty Limited from 1 July 2012, November 2011. 29 This review was completed in March 2012, see IPART, Review of price structures for metropolitan

water utilities, March 2012. 30 IPART, Review of prices for Sydney Catchment Authority - Final Report, June 2012. 31 IPART, Review of price structures for Metropolitan Water Utilities, March 2012.

2 Context for this review

22 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

2.2 IPART’s review process

As part of our review process, we have undertaken an extensive investigation and public consultation process. We have:

released an Issues Paper in June 2011 to assist in identifying and understanding the key issues for review

invited Sydney Water to make a submission to the review detailing its pricing proposal, and requiring it to provide extensive financial and performance data on the future capital and operating expenditure necessary to maintain service levels and respond to regulatory demands32

invited other interested parties to make submissions on the Issues Paper and Sydney Water’s submission33

held a public hearing on 22 November 2011 to discuss a wide range of issues raised by Sydney Water and other stakeholders

engaged an independent consultant, W.S. Atkins International Ltd in association with Cardno (Atkins Cardno), to review Sydney Water’s capital expenditure, asset planning and operating expenditure proposals34

engaged an independent consultant, Deloitte Touche Tohmatsu Ltd (Deloitte), to review Sydney Water’s proposals for Trade Waste charges35

conducted public workshops to consider the method for forecasting water sales and Trade Waste charges

released a draft report and draft determination and invited stakeholders to make submissions in response to the drafts.

IPART’s Issues Paper, stakeholder submissions, the transcript from the public hearing, information on the public workshops and Atkins Cardno’s report and Deloitte’s report are available on our website (www.ipart.nsw.gov.au).

In making our final determination for Sydney Water, we have considered the matters raised in submissions in response to the issues paper and the draft report and determination. The new charges are expected to apply from 1 July 2012.

32 Sydney Water’s submission was received on 16 September, 2011. 33 A total of 25 written submissions were received from other interested parties. 34 Atkins Cardno’s final report was received in November 2011. 35 Deloitte’s final report was received on 16 December 2011.

2 Context for this review

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 23

2.3 Matters we are required to consider

Our power to determine prices is derived from our governing Act, the Independent Pricing and Regulatory Tribunal Act 1992 (IPART Act). This review is being conducted under Section 11 of the IPART Act. Section 11 provides IPART with a standing reference to conduct investigations and make reports to the Minister on the determination of the pricing for a government monopoly service supplied by a government agency.36

Section 15 of this Act requires IPART to consider a broad range of matters when making determinations.37 These matters include:

consumer protection – the protection of consumers from abuses of monopoly power; the quality, reliability and safety standards of the services concerned; and the social impact of pricing decisions and their effect on inflation

economic efficiency – the need for greater efficiency in the use and supply of services; the need to promote competition; and the need to consider demand management and least-cost planning

financial viability – the cost of providing the services concerned, the appropriate rate of return on public sector assets; and the impact of pricing decisions on the agency’s borrowing, capital and dividend requirements

environmental protection – the need to promote ecologically sustainable development through appropriate pricing policies.

In considering these matters, we aim to balance the diverse needs and interests of stakeholders (including customers), while also ensuring that Sydney Water is adequately recompensed for the services it provides. We also take into account the principles issued by the Council of Australian Governments (COAG) and contained in the National Water Initiative.38

With these requirements in mind, we have developed a general approach to determining monopoly prices for water agencies. That approach is set out in Figure 2.1 below. We have followed this approach in our review of Sydney Water’s prices.

36 The government agency must be specified in Schedule 1 of the IPART Act. Sydney Water is

listed as a government agency for the purposes of Schedule 1 of the IPART Act. 37 The Section 15 requirements are listed in full in Appendix A. 38 The National Water Initiative has built on the principles established in the 1994 COAG Water

Reform Framework.

2 Context for this review

24 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Figure 2.1 IPART’s determination process

Obligations for service provision

Regulatory framework

What is the most appropriate approach to regulating the revenue and prices of agencies in this industry?

Given accuracy of forecasts and current industry dynamics, over what period should prices be set?

Revenue requirements

What are the efficient costs of providing these services?

How much will costs differ with variations in the levels of service provided?

What is an appropriate rate of return on the investment in the agency?

Will the agency have adequate access to capital to fund works that meet required standards and maintain services in the long term?

Price structure

How should the costs of delivering services be spread amongst customer groups?

How prices should be structured to encourage consumer and agency responses that best achieve sustainability objectives?

What are the likely impacts of prices on the affordability of services for different groups of consumers?

What are the potential environmental impacts?

What does the proposed outcome imply for the ongoing viability of the agency and its credit ratings?

What are the likely impacts on competition?

Determining a regulatory balance

What are the services that water agencies are required to deliver to customers and to what standard?

What are consumers' expectations about the level of service to be provided?

What are the broader environmental and operational constraints within which water agencies must operate and what impacts do these have on their capacity to deliver services?

2 Context for this review

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 25

2.4 Overview of Sydney Water’s submissions

Sydney Water provided its initial pricing submission to this review on 16 September 2011. Its submission proposes a real increase in prices of around 15% over the period from 1 July 2012 to 30 June 2016. For a typical residential household consuming 200 kL of water a year, this represents a $166 increase ($2011/12) in their water and sewerage bill over the period (Table 2.1).

Table 2.1 Annual water and sewerage bill for a residential customer consuming 200 kL per year under Sydney Water’s proposal ($2011/12)

2011/12 2012/13 2013/14 2014/15 2015/16 Total

Annual Bill ($) 1,105 1,208 1,231 1,252 1,271

Annual Increase ($) - 103 23 21 19 166

Annual Increase (%) - 9.3% 1.9% 1.7% 1.5% 15.0%

Note: Excludes stormwater charges.

Source: Sydney Water submission to IPART’s Review of prices for Sydney Water Corporation’s water, sewerage, stormwater and other services, September 2011, p 125.

Sydney Water’s submission identifies a range of cost pressures contributing to the proposed increase including:

increased capital expenditure on renewing existing assets

capital expenditure on servicing growth areas which is currently not recovered from developer charges39

reduced water demand40

the impact of growth on the Regulatory Asset Base (RAB) over recent determinations.

Sydney Water considers that the consequence of IPART not granting the proposed increase will be a significant reduction in Sydney Water’s financial viability:

Failure to achieve full cost recovery will put Sydney Water under financial stress and make its financial position unsustainable.41

39 Revenue from developer charges was used to fund the capital cost of providing services to new

developments in Sydney Water’s operating area. On 17 December 2008, the NSW Government decided to set developer charges in the Sydney Water area at zero.

40 The level of prices is influenced by the forecast demand for water ie, the higher the demand the lower the prices needed to recover the costs (particularly the fixed costs) and vice-versa.

41 Sydney Water submission to IPART’s Review of prices for Sydney Water Corporation’s water, sewerage, stormwater and other services, September 2011, p 25.

2 Context for this review

26 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

2.4.1 Sydney Water’s proposed annual revenue requirement

Sydney Water’s submission sets out its proposed annual revenue requirements over the 4 years to 2015/16 (Table 2.2).

Table 2.2 Sydney Water’s proposed annual revenue requirement ($million, 2011/12)

2011/12a 2012/13 2013/14 2014/15 2015/16

Return on assetsb 955.5 995.5 1,034.9 1,069.4

Return of assets (depreciation) 211.1 226.4 241.4 255.1

Operating costsc 1,361.7 1,372.1 1,374.3 1,374.3

Adjustments -36.0 -36.5 -37.9 -37.0

Total Annual Revenue Requirement 2,451 2,492.3 2557.5 2,612.7 2,661.9 a This is an estimate for the period 1 July 2011 to 30 June 2012. b Includes return on working capital. c Includes bulk water purchase costs.

Note: Totals may vary due to rounding.

Source: Sydney Water submission to IPART’s Review of prices for Sydney Water Corporation’s water, sewerage, stormwater and other services, September 2011, p 109.

Sydney Water argues its revenue requirements for price setting purposes need to increase in each of these years, partly because in the period since 2005/06, its actual revenue has failed to achieve the levels forecast in IPART’s determinations. In its submission Sydney Water estimated that, in nominal terms, its total revenue over this period will be $920 million short of that forecast. Table 2.3 compares the revenue forecast in IPART’s past determinations to Sydney Water’s actual revenue since 2005/06.

Table 2.3 Sydney Water forecast revenue versus actual revenue ($million, nominal)

Revenue 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 Total

Forecast in IPART’s determinations

1,548 1,630 1,704 1,903 2,204 2,332 2,451 13,773

Actual 1,417 1,503 1,528 1,831 2,080 2,202 2,292 12,852

Difference -131 -127 -176 -73 -124 -131 -160 -920

Note: Totals may vary due to rounding.

Source: : Sydney Water submission to IPART’s Review of prices for Sydney Water Corporation’s water, sewerage, stormwater and other services, September 2011, p 27.

In addition to receiving revenue levels less than forecast, Sydney Water argues that it has forgone a further $238 million in contributions toward capital expenditure because of the decision of the previous NSW government to set some developer charges to zero in December 2008.

2 Context for this review

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 27

2.4.2 Sydney Water’s estimates for water demand

Sydney Water explains that another reason for it not achieving forecast levels of revenue in the past was the lower than forecast sales of water. Over the current determination period, water consumption was below that forecast in the 2008 determination as a result of water restrictions continuing for longer than expected and forecast changes in customer consumption patterns not eventuating. In total, in the 4 years to June 2012, Sydney Water forecasts that the cumulative volumetric difference in water sales between the 2008 determination estimates and the actual demand will be 182 gigalitres (GL).

2.4.3 Other proposals

Other proposals put forward in Sydney Water’s submission include:

Using a pass-through mechanism to take account of the uncertainty about whether and for how long the Sydney Desalination Plant will operate over the 2012 determination period. In its forecasts for the volume of bulk water it will need to purchase, Sydney Water has set its proposed prices on the basis that the desalination plant will operate at 100% capacity at all times during the determination period, and that Sydney Water will take all of the output. This adds around $64 million a year to its forecast operating costs (or $33 a year per customer) in comparison to assuming that the plant will be in shutdown mode. Sydney Water also proposes that if the plant does shutdown at any time during the determination period, any cost savings will be passed through to consumers at the end of each financial year. Sydney Water suggests that this pass-through would be calculated and applied to prices at the beginning of each financial year from 1 July, 2013. This issue is discussed in section 5.5.

Restructuring some liquid trade waste charges. This proposal is discussed in section 9.7.

Reducing the number of miscellaneous charges it levies, and reducing the charge for a number of those services. Sydney Water has completed a comprehensive review of its miscellaneous charges, which has resulted in a reduction in the number of charges, number of transactions, and revenue generated from miscellaneous service charges. These proposals are discussed in section 9.8.

Allocating the costs associated with the Rouse Hill River Management function to all sewerage customers. This proposal is discussed in section 9.5.

2 Context for this review

28 IPART Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other services

Addressing issues from the last pricing review. Following the 2008 determination, we identified a number of issues requiring further analysis. In the lead-up to this review, IPART and Sydney Water have conducted a program of quarterly meetings to discuss the results of this analysis, particularly the analysis of price structures. Sydney Water’s submission includes a range of proposals for addressing the issues and responding to the analysis,42 including:

– Levying the standard residential water service charge on each unit in multi-residential dwellings. Most of these units currently pay a proportion of the building’s water service charge.

– Levying the standard residential water service charge on each unit in non-residential strata properties.

Regulating recycled water prices for Rouse Hill development area and including $21.6 million in avoided costs arising from the Rouse Hill recycled water scheme.

2.4.4 Sydney Water’s submission on the draft report and determination

Sydney Water provided a submission on our draft report and determination on 13 April 2012. The submission explains Sydney Water’s concern regarding its financial position and financeability. Sydney Water argues that the WACC has been set too low in the draft determination and that our draft prices may put its long term financial viability at risk. These issues are discussed in sections 6.5 and 11.2.

While Sydney Water broadly accepts the operating and capital expenditures included in the draft determination, it believes that:

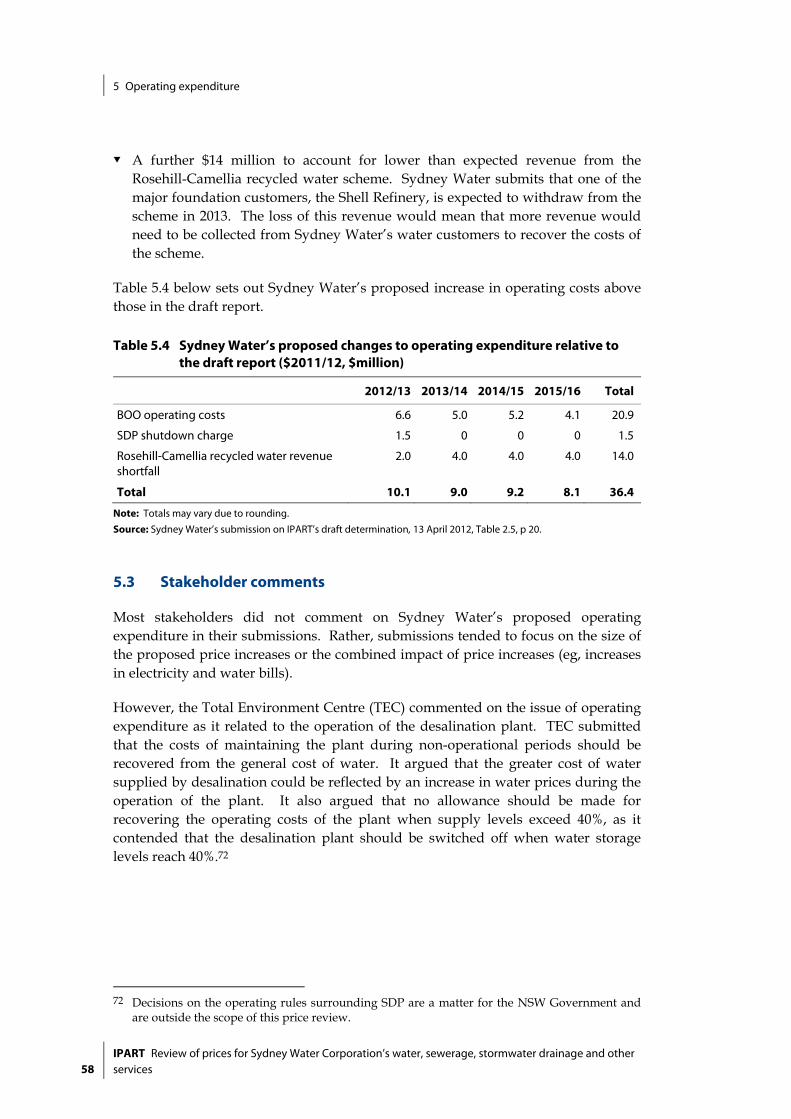

The operating expenditure should be increased by $36.4m to reflect higher costs for the Build Own Operate water filtration plants, SDP shutdown costs, and lower than expected revenue from the Rosehill-Camellia recycled water scheme. These issues are discussed in Section 5.5.

The stormwater drainage capital expenditure should be increased from $9m to $33m to maintain the condition of these assets and ensure service standards are met. This issue is considered in Section 6.3.5.

In relation to tariff reforms, Sydney Water has accepted most of the proposed tariff structures in the draft determination but considers that implementation will be challenging. However, it has requested that:

The area based charges for stormwater drainage be either removed; or simplified and delayed by 12 months. This issue is discussed in section 9.4.

The Rouse Hill Land Charge for new customers in Rouse Hill be removed and the capital costs recovered from all Sydney Water’s sewerage customers. This issue is considered in section 9.5.

42 IPART completed a review of this issue in March 2012, see IPART, Review of price structures for

Metropolitan Water Utilities, March 2012. Sydney Water implemented many of the results of the review in its pricing submission.

3 IPART’s approach to setting prices

Review of prices for Sydney Water Corporation’s water, sewerage, stormwater drainage and other servicesIPART 29

3 IPART’s approach to setting prices