Review of Key Criteria for the Successful Development of the Biomedical Sector

44

Review of Key Criteria for the Successful Development of the Biomedical Sector Presented by Frost & Sullivan’s Biotechnology Team 15 th November 2010

-

Upload

frost-sullivan -

Category

Health & Medicine

-

view

2.334 -

download

3

Transcript of Review of Key Criteria for the Successful Development of the Biomedical Sector

Review of Key Criteria for the Successful Development of the Biomedical Sector

Presented by Frost & Sullivan’s Biotechnology Team

15th November 2010

2

Table of Contents

Key success factors for biotech clustersKey success factors for biotech clusters11

A look at International + Singapore Biotech ClustersA look at International + Singapore Biotech Clusters22

Benchmarking with International ClustersBenchmarking with International Clusters33

4

Examples of key biotech clusters

California • San Francisco Bay

Area in North California

• Los Angeles, Orange County, Riverside and San Diego in South California

Boston/ Massachusetts

• Greater Boston Area including Providence and Worcester

Medicon Valley• Zealand in Denmark

and Scania in South Sweden

South Korea• Across the country

Singapore

Israel• Jerusalem, Tel Avi and

Haifa triangle

Taiwan• Medical Technology

Boston and California clusters are leading, mature and old clusters, Medicon Valley is among the successful clusters in

Europe. Israel and Korea are two growing clusters with strong government support and strength in research

5

Setting the stage…

33

44

55

66

22

77

11

To improve Industry Maturity– we need to focus on medical devices, faster commercializable research, proven technologies, clinical trials to leverage healthcare infrastructure

To improve Industry Maturity– we need to focus on medical devices, faster commercializable research, proven technologies, clinical trials to leverage healthcare infrastructure

To improve University and Medical Centre maturity More collaboration activities, TTOs and incubators, More commercial exposure to scientists and international tieups are needed

To improve University and Medical Centre maturity More collaboration activities, TTOs and incubators, More commercial exposure to scientists and international tieups are needed

Promotion of SMEs, Improving skill base and promoting entrepreneurship are desirable to improve the business environment in the overall cluster

Promotion of SMEs, Improving skill base and promoting entrepreneurship are desirable to improve the business environment in the overall cluster

Pre seed funding and steps to develop VC need to be taken to improve funding availability for companiesPre seed funding and steps to develop VC need to be taken to improve funding availability for companies

Singapore performance in the last 10 years has been appreciated by the industry and foreign participants. It compares well on the Business environment. However, it needs to progress on other 3 parameters

Singapore performance in the last 10 years has been appreciated by the industry and foreign participants. It compares well on the Business environment. However, it needs to progress on other 3 parameters

Ways to Promote Entrepreneurship, run TTOs, increase International affiliations, attracting VC can be learned from other international clusters

Ways to Promote Entrepreneurship, run TTOs, increase International affiliations, attracting VC can be learned from other international clusters

Industry Maturity, Medical Centre and University Maturity, Funding Availability and Regulatory and Business Environment are four key attributes of a bio medical cluster

Industry Maturity, Medical Centre and University Maturity, Funding Availability and Regulatory and Business Environment are four key attributes of a bio medical cluster

6

The Magic of Boston and California ClustersStrong science base. Established institutions, Funds from government and VC, strong industry associations and a spirit of entrepreneurship make them sustainable clusters

Strong Science BaseStrong Science Base

• 30+ years of history in Biotech

• 100+ years of successful research

at MIT, Harvard, Stanford, UCSF

• Efficient TLO and networks to drive

commercialization

• Spin offs from successful

companies

• Clarity in IP transfer

• Leading Medical Institutions in the

area

• 30+ years of history in Biotech

• 100+ years of successful research

at MIT, Harvard, Stanford, UCSF

• Efficient TLO and networks to drive

commercialization

• Spin offs from successful

companies

• Clarity in IP transfer

• Leading Medical Institutions in the

area

Funding AvailabilityFunding Availability

• NIH funds of $ 2bn + annually

• VC funds of $ 1bn + annually

• IPO markets, Angel community and

a culture to promote

entrepreneurship and risk taking

• $80mn+ funding for small

businesses

• NIH funds of $ 2bn + annually

• VC funds of $ 1bn + annually

• IPO markets, Angel community and

a culture to promote

entrepreneurship and risk taking

• $80mn+ funding for small

businesses

Business Environment for Biotech

Business Environment for Biotech

• Intellectual environment attract

staff and companies

• Continuous supply of educated

workers

• Industry Associations to

continuously monitor and provide

feedback

• State’s drive to attract companies

• Presence of three generation of

entrepreneurs

• Intellectual environment attract

staff and companies

• Continuous supply of educated

workers

• Industry Associations to

continuously monitor and provide

feedback

• State’s drive to attract companies

• Presence of three generation of

entrepreneurs

• Boston and California face competition from Texas, Los Angeles, Philadelphia for funds. Companies

locating manufacturing facilities elsewhere for low real estate costs, higher tax benefits etc.• Continuous need to Provide space, talent, funds for the expanding cluster• Needs to continue focus on scientific collaboration and innovation• Emerging clusters pose competition due to low cost, high growth potential for companies

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

7

The Secret Sauce of Israel Strong in Research, TTOs and incubators to promote startups, developed VC industry and an entrepreneurship spirit characterize Israel

Strong in Technology/Research

Strong in Technology/Research

• Developed IT industry ; Defense;

• Notable pharma products from

Hebrew, Technion universities

• Israel economy is classified as

Innovation based economy by WEF

• Physicians are early adopter as well

as develop technology

• 2nd in per capita patents granted by

USPTO in biotechnology

• Developed IT industry ; Defense;

• Notable pharma products from

Hebrew, Technion universities

• Israel economy is classified as

Innovation based economy by WEF

• Physicians are early adopter as well

as develop technology

• 2nd in per capita patents granted by

USPTO in biotechnology

Govt SupportGovt Support

• 16 Technology Transfer Offices

• 26 incubators for early stage

companies

• Bi National Funds with US, UK,

Canada, Korea ,Australia and

Singapore

• Associated with EU’s framework

program for R&D1

• Professionally managed funds in

partnership with govt.

• 16 Technology Transfer Offices

• 26 incubators for early stage

companies

• Bi National Funds with US, UK,

Canada, Korea ,Australia and

Singapore

• Associated with EU’s framework

program for R&D1

• Professionally managed funds in

partnership with govt.

Business Environment for Biotech

Business Environment for Biotech

• Eighty VC funds; 20-30% funds to

life sciences.

• Strong in medical devices and early

stage biotech

• Strong networks across the industry

from defense training, being a small

country

• Eighty VC funds; 20-30% funds to

life sciences.

• Strong in medical devices and early

stage biotech

• Strong networks across the industry

from defense training, being a small

country

• 90% of Israeli biotechnology companies have less than 50 employees. • A substantial number of researchers leave the country because of a lack of sufficient attractive

employment opportunities in Israel. • There is too much regulation and bureaucracy as well ; Decades of War conflicts• Late stage funding for life sciences is still scarce. Limited big life sciences companies

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

1 http://ec.europa.eu/research/fp6/index_en.cfm

MATIMOP, the international coordinator for R&D was interested in talks with Singapore

8

The Medicon Valley StoryBenefitted from integrated presence of leading companies and good healthcare infrastructure. The cluster is becoming complacent now

Niche DevelopmentNiche Development

• Novo Nordisk in Diabetes

• Lundbeck in Anti Depressives

• Leo Pharma in Dermatalogy

• Astrazeneca in respiration.

• Integrated Presence for centuries

• Spin off from these companies

• Infrastructure available for clinical

trials

• Novo Nordisk in Diabetes

• Lundbeck in Anti Depressives

• Leo Pharma in Dermatalogy

• Astrazeneca in respiration.

• Integrated Presence for centuries

• Spin off from these companies

• Infrastructure available for clinical

trials

Business Environment for Biotech

Business Environment for Biotech

• Good Branding , Patient Databases, Developed Healthcare Infrastructure

• International affiliation of companies and institutions; Life Science

ambassador program

• Development of Denmark- Sweden bridge, Management Teams,

• Govt. support to universities, incubators for proof of concepts &

commercializable research by various grants

• Presence of local VCs; 40+ in life sciences

• Good Branding , Patient Databases, Developed Healthcare Infrastructure

• International affiliation of companies and institutions; Life Science

ambassador program

• Development of Denmark- Sweden bridge, Management Teams,

• Govt. support to universities, incubators for proof of concepts &

commercializable research by various grants

• Presence of local VCs; 40+ in life sciences

• Collaboration between universities, hospitals and institutions need to be improved• Lack of capital at later stages recently; Improvement needed to tap US capital markets• The cluster is said to be a little complacent .Not many cluster development efforts specifically• Taxes and an unfavorable weather; high cost of services are growing concerns

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

Singapore can look forward to become a partner in the Life Science Ambassador Program

9

The Growth of Korea Educated and experienced manpower, success in research and clinical trials and the biomedical infrastructure created by the government are the key reasons for growth

Strong Science BaseStrong Science Base

• Biotechnology-related Departments

in 40 Universities

• Strong in clinical trials

• High quality of workforce

• Around 40 technologies or drug

candidates were licensed out to Big

Pharma during 1986-2008 and over

100 new drugs or lead candidates

are under development.

• Biotechnology-related Departments

in 40 Universities

• Strong in clinical trials

• High quality of workforce

• Around 40 technologies or drug

candidates were licensed out to Big

Pharma during 1986-2008 and over

100 new drugs or lead candidates

are under development.

Business Environment for BiotechBusiness Environment for Biotech

• Govt. creating research institutes, 25 biotechnology centers acting as

incubators, specialized biotech parks, providing funds

• The first initiative started in late 1980’s, continued effort in 1994 and 2006

• government investments have grown from $311mn in 2001 to $721mn in

2007. This represents a CAGR of 15%.

• Korea is ranked as 19 by WF Global Competitiveness Report 2009-10

• The Bio-Vision initiative started in 2006 out with a budget of $720 million

for R&D and $230 million for infrastructure in 2007, with a projected rise to

$1.67 billion for R&D and $690 million for infrastructure by 2016. The total

budget for nine years is projected at $15.56 billion

• Govt. creating research institutes, 25 biotechnology centers acting as

incubators, specialized biotech parks, providing funds

• The first initiative started in late 1980’s, continued effort in 1994 and 2006

• government investments have grown from $311mn in 2001 to $721mn in

2007. This represents a CAGR of 15%.

• Korea is ranked as 19 by WF Global Competitiveness Report 2009-10

• The Bio-Vision initiative started in 2006 out with a budget of $720 million

for R&D and $230 million for infrastructure in 2007, with a projected rise to

$1.67 billion for R&D and $690 million for infrastructure by 2016. The total

budget for nine years is projected at $15.56 billion

• Pharmaceutical companies do not have strong experience to enter global markets• Difficulty to source foreign talent• Collaboration needs to improve among universities and industries. Between companies in the clusters• Pharmaceutical industry is mostly generics

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

10

The Rise of Singapore Strong govt. support, a good business climate , healthcare infrastructure has lead to significant growth in last 10 years.

Govt. SupportGovt. Support

• A*Star, EDB, NRF,SPRING key

agencies established

• Biopolis, Tuas Biomedical park

infrastructure lauded by the industry

and foreign participants

• A*Star, EDB, NRF,SPRING key

agencies established

• Biopolis, Tuas Biomedical park

infrastructure lauded by the industry

and foreign participants

Healthcare InfrastructureHealthcare Infrastructure

• 2.6 beds per 1,000 patients , 253 clinical trial certificates approved in 2007

• 4-6 weeks for clinical trial certificate review/approval; applications are made

in parallel to regulatory body and institutional review board.

• No.2 in the world for IP protection

• 3rd in WEF Global Competitiveness Report 2009-10

• Indications of developing medical devices and clinical trials segment

• 2.6 beds per 1,000 patients , 253 clinical trial certificates approved in 2007

• 4-6 weeks for clinical trial certificate review/approval; applications are made

in parallel to regulatory body and institutional review board.

• No.2 in the world for IP protection

• 3rd in WEF Global Competitiveness Report 2009-10

• Indications of developing medical devices and clinical trials segment

• Limited Pre Seed Funding Available, Not sufficient for startup needs• VC investment in the sector less than $200mn annually. Preference given to other sectors, projects with

certain product development plans and clear revenue generation strategy• Low levels of Entrepreneurship even though the business climate is quite suitable. Preference of

Singaporeans towards professional careers and limited need to pursue risky opportunities• Need for improvement in commercialization and collaboration activities of research institutes• Less than 25 startups being created in the sector annually• Potential improvements in availability of experienced top management and in skill base of local workers• Improvements needed in international affiliations and collaboration of SMEs

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

Higher Focus on Areas of Improvement

11

Key Success Factors for Biotech ClustersCompany Base, Science Base and Funding Availability are key capabilities for biomedical clusters

• Thriving spin-out and start up companies.

• Presence of companies to support research, clinical trials and

manufacturing

• More mature ‘role model’ companies.

• Presence of suppliers for raw materials

• Thriving spin-out and start up companies.

• Presence of companies to support research, clinical trials and

manufacturing

• More mature ‘role model’ companies.

• Presence of suppliers for raw materials

Science BaseScience Base

Company BaseCompany Base

Description

• Leading research organizations: University departments,

hospitals/medical schools and charities

• Critical mass of researchers, World leading scientists, Both industry

driven and independent research

• Leading research organizations: University departments,

hospitals/medical schools and charities

• Critical mass of researchers, World leading scientists, Both industry

driven and independent research

Availability of Finance

Availability of Finance

• Venture capitalists, Business angels, Developed public markets

• Availability of cash at all stages of business like venture formation,

pre-seed, seed, second round, mezzanine and opportunities for IPO

• Venture capitalists, Business angels, Developed public markets

• Availability of cash at all stages of business like venture formation,

pre-seed, seed, second round, mezzanine and opportunities for IPO

1

2

3

Source: Frost & Sullivan analysis

Boston, CaliforniaBoston,

California

US,Medicon Valley,

Israel

US,Medicon Valley,

Israel

CaliforniaCalifornia

Example clusters

12

Key Success Factors for Biotech ClustersInfrastructure, supportive policy and business support services are strongly needed during the cluster start and growth phase

• Incubators available close to research organizations

• Premises with wet labs and flexible leasing arrangements

• Space to expand, Motorways, Rail, International airport

• Incubators available close to research organizations

• Premises with wet labs and flexible leasing arrangements

• Space to expand, Motorways, Rail, International airport

Supportive PolicyEnvironment

Supportive PolicyEnvironment

Premises &InfrastructurePremises &

Infrastructure

Description

• National and sector promotion policies, Long term planning

• Proportionate fiscal and regulatory framework

• Transparency, Efficient procedures, Skilled Administration

• National and sector promotion policies, Long term planning

• Proportionate fiscal and regulatory framework

• Transparency, Efficient procedures, Skilled Administration

Business SupportServices

Business SupportServices

• Specialist business, legal, patent, recruitment, property

advisors, Large companies in related sectors (healthcare,

chemical, agrifood)

• Specialist business, legal, patent, recruitment, property

advisors, Large companies in related sectors (healthcare,

chemical, agrifood)

4

5

6

Source: Frost & Sullivan analysis

AllAll

US,Singapore

US,Singapore

US, Medicon Valley

US, Medicon Valley

Example clusters

13

Key Success Factors for Biotech ClustersSkilled workforce, entrepreneurial culture and effective networking develop as clusters mature and are important for sustainability

• Skilled workforce, Training courses at all levels• Skilled workforce, Training courses at all levelsSkilled Workforce

Skilled Workforce

Description

7

• Commercial awareness and entrepreneurship in Universities

and research institutes, presence of anchor companies

• Role models and recognition of entrepreneurs, Presence of

Second generation entrepreneurs

• Commercial awareness and entrepreneurship in Universities

and research institutes, presence of anchor companies

• Role models and recognition of entrepreneurs, Presence of

Second generation entrepreneurs

EntrepreneurialCulture

EntrepreneurialCulture

8

• Critical mass of employment opportunities, Other living

amenities

• Image/Reputation as biotechnology cluster, Climate conditions

• Attractive place to live. Good remuneration. Presence of similar

intellectual class

• Critical mass of employment opportunities, Other living

amenities

• Image/Reputation as biotechnology cluster, Climate conditions

• Attractive place to live. Good remuneration. Presence of similar

intellectual class

Ability to attract key staff

Ability to attract key staff

9

• Shared aspiration to be a cluster. Regional trade associations.

• Efficient TTOs

• Shared aspiration to be a cluster. Regional trade associations.

• Efficient TTOs

Effective collaboration

Effective collaboration

10

Source: Frost & Sullivan analysis

Boston, Israel

Boston, Israel

Boston, Israel

Boston, Israel

Singapore.California

Singapore.California

Boston.CaliforniaBoston.

California

Example clusters

14

Key Attributes of Biotech Clusters Ten factors have been combined into four attributes for simplicity, measurement and to do comparison across clusters. These include all stakeholders and all activities in the value chain

Industry MaturityIndustry Maturity

Funding AvailabilityFunding Availability

• Presence and nature of biotech companies (e.g. Startup, early stage, late development, mature commercial, enabling service)

• Quantity and diversity of lifesciences stakeholders (e.g. R&D, medical devices, clinical trials and manufacturing, supporting industries)

• Growth in Output – stagnated growth, slow growth or faster than industry

• Presence and nature of biotech companies (e.g. Startup, early stage, late development, mature commercial, enabling service)

• Quantity and diversity of lifesciences stakeholders (e.g. R&D, medical devices, clinical trials and manufacturing, supporting industries)

• Growth in Output – stagnated growth, slow growth or faster than industry

• Availability of funding to support early stage company research

• Funding for established biotech companies to invest in additional infrastructure and clinical research to move products into the market place

• Public and Private funding channels

• Availability of funding to support early stage company research

• Funding for established biotech companies to invest in additional infrastructure and clinical research to move products into the market place

• Public and Private funding channels

University/Medical Centre MaturityUniversity/Medical Centre Maturity

Regulatory and Business EnvironmentRegulatory and Business Environment

• Strong research universities and academic medical centers, supported by effective technology transfer offices, as a key source of innovation and talent

• Collaborative relationships between research universities and academic medical centers to sustain invention and innovation

• Areas of Research and Commercialization Success

• Strong research universities and academic medical centers, supported by effective technology transfer offices, as a key source of innovation and talent

• Collaborative relationships between research universities and academic medical centers to sustain invention and innovation

• Areas of Research and Commercialization Success

• Stable and supportive public policy structure• Supportive business environment to retain existing

companies and / or attract new enterprises (e.g., taxes, permitting, costs, IP protection)

• Stakeholder Synergy

• Stable and supportive public policy structure• Supportive business environment to retain existing

companies and / or attract new enterprises (e.g., taxes, permitting, costs, IP protection)

• Stakeholder Synergy

Source: Frost & Sullivan analysis

• Industry Maturity and University/Medical Centre maturity comprises Company and Science Base• Funding Availability Remains Same• Regulatory and Business Environment comprises other seven factors

15

Cluster Current Positioning and Outlook

World ClassEmerging Cluster Capability

Siz

e

SMALL

LARGECalifornia

Boston

Medicon Valley

Korea

Singapore

Israel

• California life sciences $ 75bn in 2008

with a growth of 2% over 2007• Israel life sciences export were $6.5bn

in 2008 and they tripled from 2004

levels• Singapore $15bn in 2009 growing at a

CAGR of 14% during 2000-2009• Korea pharmaceutical was around

$14bn in 2008 growing at a rate of 8-

10%

• Revenues for Boston and Medicon valley clusters not available. Their positioning is approximate in terms of size

16

Comparative Analysis

Cluster Industry Maturity Funding AvailabilityUniversity/Medical Centre Maturity

Business Environment for Life sciences

California

Boston/Massachusetts

Medicon Valley/Sweden/ Denmark

Israel

Korea

Singapore

• Industry maturity – Focus on medical devices, faster commercializable research, proven technologies, clinical trials

to leverage healthcare infrastructure• Funding availability – Higher efficiency of grants being disbursed, development of VC funds • University/Medical Center maturity – More collaboration activities, TTOs and incubators, More commercial exposure

to scientists

Source: Frost & Sullivan AnalysisNote : Two similar circles may not denote complete equality on the parameter.

17

Table of Contents

Key success factors for biotech clustersKey success factors for biotech clusters11

A look at International + Singapore Biotech ClustersA look at International + Singapore Biotech Clusters22

Benchmarking with International ClustersBenchmarking with International Clusters33

18

Boston ClusterStrong Research base, effective networks and entrepreneurship culture leads to startup companies which leverage the available funding and other stakeholders’ support to develop successful products

.

Funding Avalability

Experienced Talent and Effective

Networks

Entrepreneurship Culture

30 +Years of history

Strong Research Base

Diverse Companies

Strong Research base, effective networks and entrepreneurship culture leads to startup companies which leverage the available funding and other stakeholders’

support to develop successful products

Strong Research base, effective networks and entrepreneurship culture leads to startup companies which leverage the available funding and other stakeholders’

support to develop successful products

Source: Frost & Sullivan Analysis

19

Evolution of Boston ClusterGovernment funding promoted research leads to formation of biotech startups that tie up with big pharmaceutical companies.

1. World-class universities and research hospitals (M.I.T., Whitehead, Harvard, Massachusetts General Hospital,

Brigham & Women’s Hospital, Beth Israel Hospital, Boston University, etc., etc.)- Harvard university since

1640 and MIT since 1865

2. Longwood Medical Center in Boston/Brookline started with 26acres in 1906 and grew up around Harvard

Medical School . Kendell Square in Cambridge began in 1915 when MIT moved its campus there.

3. In 1962, Massachusetts Medical Center was found in Worcester.

4. In 1978, Biogen, first biopharma of the region was founded

5. In 1980 Bayh-Dole Act Gave universities title to their patents from federally funded research Allowed

universities to grant licenses, including exclusive licenses Allowed universities to take royalties (and

legislated sharing of royalties with inventors.)

6. In 1985, Genzyme had its first drug Ceradase to treat Gaucher disease

7. In 1996, Wyeth acquires Genetic Institute and became the first large pharma company to establish

manufacturing in the region

8. In 2005, NIH research grants to the region reach $2.2bn

Source: Press Articles

20

Boston ClusterMature Industry–big and small, across sectors and across the value chain; presence of leading medical institutions, venture capital firms and industry associations make it an integrated and mature cluster

Key Cluster Stakeholders

Pharma/Biotech 600

Medical Devices 450

VC Firms (Biotech Focus) 30

Industry Associations 10

72000 employees

21

Boston ClusterStrong Academic Science; Entrepreneurship culture and TLO efforts move products from mind to market

MIT Statistics

• 20+ companies formed using MIT IP every year

• Genzyme, Repligen, Biogen and Amgen founded by MIT faculty

or alumni

• 40+ biotechnology patents every year

• 100 + technology licenses every year

• 9% of undergraduates from Massachusetts only; but 42% of

technology companies founded by graduates are in the state

0

5

10

15

20

25

30

1991 1993 1995 1997 1999 2001 2003 2005

Companies founded with MIT IP

Activities Encouraging Entrepreneurship

• Technology Licensing Office

• Entrepreneurship Center for internships

• Deshpande center for competitive late stage research grants

• Enterprise forum is over 25 years old with 20 chapters and in 3

foreign countries

• $100 K plan contest has led to founding of multiple businesses

• Role models, Venture mentoring and networking seminars

Activities of TLO

• Assess breadth and strength of IP; Negotiate license agreement

• Introduce startups to investors and sector experts

• Set financial terms; milestones and clarify IP position

• Monitor progress and let market forces take over

• MIT does not provide management, board seats, money,

business plan writing, laboratories etc

• Strict conflict of interest rules-e.g. Formal incubation outside

university, no MIT investment in company etc.

Source: Lita Nelsen, Role of Research Institutions in formation of Biotech clusters in Massachusetts 2005

22

Boston ClusterFunding Availability- Developed Public and Private Channels

NIH SBIR and STTR grants 2005

Grant categoryNumber of grants

Total amount($mn)

SBIRPhase 1 114 $21 Phase 2 110 $53 Total 224 $74 STTRPhase 1 20 $3 Phase 2 10 $6 Total 30 $9

Rank Top 10 Grantees of NIH funding 2005Dollars awarded ($ millions)

1 Massachusetts General Hospital 2872 Brigham and Women’s Hospital 2533 Massachusetts Institute Of Technology 1724 Harvard University Medical School 1695 Boston University Medical Campus 1236 Beth Israel Deaconess Medical Center 1237 Dana-Farber Cancer Institute 1178 University of Massachusetts Medical School 1159 Children’s Hospital Boston 10310 Harvard University (School of Public Health) 102

• 10% of US NIH funding equaling $2.25 bn in 2005

• 2nd largest in absolute terms; highest in per capita R&D

funding of $353

• VC investments of more than $1bn in 2006

• $83 mn available to facilitate the commercialization of

novel technology and intellectual property licensed

from universities to small high technology firms

employing less than 500 people

23

Boston ClusterRecent Initiatives in the Cluster

• $500 million is earmarked for the Massachusetts Life Sciences Investment Fund• $250 million for the award of grants and $250 million in tax credits. • Tax incentives for companies to embark on expansions or new initiatives ;• Provide seed money to develop new ideas and provide financial aid for graduate students. • Money for the state's vocational and technical high schools and colleges to purchase new

equipment to train life sciences workers.• Retain Researchers, Develop Stem Cell bank, fund equipment purchase, commercialization

$1 billion Life Sciences

Initiative by Stateover 10 years

$1 billion Life Sciences

Initiative by Stateover 10 years

2015Strategic Plan

Development byMassBio

2015Strategic Plan

Development byMassBio

Six Focus Areas for MassBiotech Association

1. Company Recruitment and Retention

2. Provision of Business Services

3. Promote Scientific Collaboration and Innovation

4. Improve Industry Representation

5. Develop talent at all levels

6. Improve access to capital

Other InitiativesOther Initiatives

• Bio Ready Community –Communities ready for labs or manufacturing plants.• Life Science Talent Initiative -Promote biotechnology methods and inspire scientific curiosity

and understanding at the high school level

Source: Press Articleshttp://www.mass.gov/Agov3/docs/mass_life_sciences_strategy.rtfSource :http://www.boston.com/business/articles/2009/04/30/bio_ready_communities_in_state_named/

24

Israel ClusterStrong govt. support, developed private VC industry, good Business environment and effective networks characterize the Israel cluster

• 16 TTOs Fusion among the universities, hospital systems, businesses, and the military• Blockbuster drugs from Israel Universities.• 23 govt. sponsored incubators for advancing early stage technologies• 50% of incubator companies in life science; Received 25% of $360 million from OCS• 38% of 1175 incubator companies graduate to mature companies• Bi National Funds; Framework to work with EU and other grants available

• 16 TTOs Fusion among the universities, hospital systems, businesses, and the military• Blockbuster drugs from Israel Universities.• 23 govt. sponsored incubators for advancing early stage technologies• 50% of incubator companies in life science; Received 25% of $360 million from OCS• 38% of 1175 incubator companies graduate to mature companies• Bi National Funds; Framework to work with EU and other grants available

• Life science exports nearly tripled from $2.4 billion in 2004 to $6.5 billion in 2008• 8% of GDP on Healthcare;$2088 per capita; 3.5 MD/Physicians per 1000 population• Physicians are early adopter as well as develop technology• Israel classified as Innovation driven economy by WEF 2009• 70-80 companies formed every year; Entrepreneurial culture• 2nd in per capita patents granted by USPTO in biotechnology

• Life science exports nearly tripled from $2.4 billion in 2004 to $6.5 billion in 2008• 8% of GDP on Healthcare;$2088 per capita; 3.5 MD/Physicians per 1000 population• Physicians are early adopter as well as develop technology• Israel classified as Innovation driven economy by WEF 2009• 70-80 companies formed every year; Entrepreneurial culture• 2nd in per capita patents granted by USPTO in biotechnology

• Eighty Funds in 2008; 483 companies raised $2bn; 20-30% funds to Life sciences • Eighty Funds in 2008; 483 companies raised $2bn; 20-30% funds to Life sciences

• Strong Networks across the industry• Two very well known innovations emerged from Rafael, Israel Armament Development

Authority: PillCamTM, a video capsule endoscope (developed by Given Imaging) and cryotherapy for the treatment of cancer (developed by Galil Medical).

• Strong Networks across the industry• Two very well known innovations emerged from Rafael, Israel Armament Development

Authority: PillCamTM, a video capsule endoscope (developed by Given Imaging) and cryotherapy for the treatment of cancer (developed by Galil Medical).

Govt. SupportGovt. Support

Business Environment

Business Environment

Private VCPrivate VC

Defense Community

Defense Community

Source: Israel Export and International Cooperation Institute

25

Israel ClusterStrong in Medical devices ; Biotech Research; Small companies in early research phases

Diagnostic tests

Bioinformatics, drug discovery, proteomics

Gene therapies, molecular biology

Industrial applications

Pharmaceuticals, biopharmaceuticals, biogenerics

0 5 10 15 20 25 30

2825

241919

1411

98

22

Sectors within Israel Biotech industry, 2006

Between 1- 10

Between 11- 20

Between 21-30

Between 31-50

More than 50

0102030405060708090

100

114 1 3 2

88

136

13 9

Employee structure of Biotech companies, 2005

Agrobiotechnology companies

Biotechnology companies

65%8%

13%

11% 2% 1%

Companies By Sector, 2009 (1100+ companies)

Medical DevicesHealthcare ITPharmaBioAg BioOthers

30%

38%

26%

6%

Stage Of Companies, 2009

SeedR&DInitial revenueRevenue Growth

Source: Israel Export and International Cooperation Institute, Israel Biotechnology Sector Paper by Alastair Bell

26

Israel ClusterBrief Snapshot of Various Sectors

Medical DevicesMedical Devices

• Ranked 2nd for Medical Devices solution• Therapeutic devices–both implantable and disposable–

comprise the largest subsector• Insightec works on MRI guided non invasive surgical

procedures• DeepBreeze provides physicians with a dynamic functional

image of the lungs.• Sialo Technology presents an advanced endoscope system

and tools for root canal “direct vision”

• Ranked 2nd for Medical Devices solution• Therapeutic devices–both implantable and disposable–

comprise the largest subsector• Insightec works on MRI guided non invasive surgical

procedures• DeepBreeze provides physicians with a dynamic functional

image of the lungs.• Sialo Technology presents an advanced endoscope system

and tools for root canal “direct vision”

Healthcare ITHealthcare IT

• 100% of primary care physicians in Israel use computerized patient records.

• More than 70 companies are developing products for healthcare IT.

• Developed communication technologies provides strong base for developing healthcare IT and telemedicine solutions

• Roshtov is a leader in enterprise wide medical information systems,

• 100% of primary care physicians in Israel use computerized patient records.

• More than 70 companies are developing products for healthcare IT.

• Developed communication technologies provides strong base for developing healthcare IT and telemedicine solutions

• Roshtov is a leader in enterprise wide medical information systems,

Therapeutics and Stem CellsTherapeutics and Stem Cells

• 17% annual growth of biotechnology sector in last decade• 20 active stem cell companies• Breakthrough therapeutics in the treatment of cancer,

multiple sclerosis, Parkinson’s and Alzheimer’s diseases, diabetes, and more

• Weizmann Institute of Science and Technion are leading institutes

• 17% annual growth of biotechnology sector in last decade• 20 active stem cell companies• Breakthrough therapeutics in the treatment of cancer,

multiple sclerosis, Parkinson’s and Alzheimer’s diseases, diabetes, and more

• Weizmann Institute of Science and Technion are leading institutes

Drug Delivery and DiagnosticsDrug Delivery and Diagnostics

• 70 companies developing new drug delivery platforms• Intecpharma’s Accordion Pill improves drug absorption• BioSight develops targeted chemotherapy drugs• 120 companies developing diagnostic kits for testing

diseases, birth defects, microorganisms etc• Smart Biotech stimulates antibody production (in vitro) for

early and more complete detection of HIV• Exalenz Bioscience assess a range of liver and

gastrointestinal disorders via molecular analysis of the patient’s breath.

• 70 companies developing new drug delivery platforms• Intecpharma’s Accordion Pill improves drug absorption• BioSight develops targeted chemotherapy drugs• 120 companies developing diagnostic kits for testing

diseases, birth defects, microorganisms etc• Smart Biotech stimulates antibody production (in vitro) for

early and more complete detection of HIV• Exalenz Bioscience assess a range of liver and

gastrointestinal disorders via molecular analysis of the patient’s breath.

Source: Israel Export and International Cooperation Institute

27

Singapore StrengthsGovt. Support, Healthcare Infrastructure and Friendly Business Environment are key strengths. However, entrepreneurial culture needs to be encouraged.

Source: Frost & Sullivan Primary Research

28

SPRING Policies & InitiativesFinancing Schemes and Capability Building Schemes for SMEs

Business Capability Programs

BrandPact

To increase companies’ awareness of brand development, we work with the business associations and brand experts to offer branding workshops, online branding resources, and forums to inform and educate companies on their branding journey. Recognition platforms such as Singapore Prestige Brand Award and Singapore Brand Award

Customer Centric Initiative (CCI) The Customer-Centric Initiative (CCI) aims to encourage companies to be committed to service excellence and to take the lead in raising service standards in their industry.

Design Engage Programme With this businesses can learn how to integrate strategic design thinking into every step of their business process.

HR Capability Programme This offers SMEs tools, templates and guidelines in 6 strategic areas - manpower planning, recruitment and selection, compensation and benefits, performance management, learning and development and career development.

Intellectual Property Management Programme (IPM)

This provides consultancy advice and funding support to develop and protect your intellectual property.

SME Management Action for Results Initiative (SMART)

This provides Singapore-based SMEs with consultancy advice and funding support to develop management systems and processes.

Financing Schemes

Business Angel FundsProvides innovative Singapore-based young companies a co-investment financing option from pre-approved angel groups, up to S$1.5 million in matching capita

Spring Startup Enterprise Development Scheme

Provides innovative Singapore-based young companies a co-investment financing option from independent investor(s), up to S$1 million in matching capital

Young Entrepreneurs' Scheme for Startups (YES! Startups)

Provides youths with grants of up to S$50,000 to start their innovative business

Source: http://www.spring.gov.sg/entrepreneurship/fs/pages/programmes-start-ups.aspx

29

SPRING Policies & InitiativesTechnology Innovation Schemes and Business Leadership Development Schemes

Business Leadership

Business Leaders InitiativeThe Business Leaders Initiative is a comprehensive effort to develop SME business leaders, both present and future.

Advanced Management Programme (AMP)

This focuses on training SME business owners, CEOs and senior executives through customized management and leadership courses

Management Development Scholarship (MDS)

This grooms promising young SME executives by co-sponsoring their MBA programmes with their employers.

Executive Development Scholarship (EDS)

It provides local under-graduates who are passionate about setting up their own businesses or working in SMEs with full sponsorship of their studies and work attachments in local SMEs and SPRING.

Technology Innovation

Innovation Voucher Scheme (IVS)

The Innovation Voucher Scheme (IVS) connects public Knowledge Institutions (KI) with SMEs to encourage SMEs in adopting technology to develop their innovative ideas

Technology Enterprise Commercialization Scheme (TECS)

This aims to catalyze the formation and growth of such start-ups based on strong technology Intellectual Property and a scalable business model.

Source: http://www.spring.gov.sg/entrepreneurship/fs/pages/programmes-start-ups.aspx

30

Singapore–Opportunities and ThreatsOpportunities in individual sectors; threats from neighboring clusters

OpportunitiesOpportunities

• Biogenerics and vaccines are the key growth areas in

pharmaceuticals. Other opportunities are Volume

manufacturing of commodities, translational medical

research and the generic drugs market.

• For biotech, stem cell research, genetic screening and

gene therapy are promising areas for the future.

• Healthcare services industry can see growth in medical

tourism and chronic diseases.

• Government focus on clinical trials to drive CRO growth

• In the medical devices section do it at home products and

development of measurement devices for the affluent

section of the people holds significant potential.

• Biogenerics and vaccines are the key growth areas in

pharmaceuticals. Other opportunities are Volume

manufacturing of commodities, translational medical

research and the generic drugs market.

• For biotech, stem cell research, genetic screening and

gene therapy are promising areas for the future.

• Healthcare services industry can see growth in medical

tourism and chronic diseases.

• Government focus on clinical trials to drive CRO growth

• In the medical devices section do it at home products and

development of measurement devices for the affluent

section of the people holds significant potential.

ThreatsThreats

• China’s health biotech segment had maintained an annual

growth rate of 30% since 2005

• Biopharmaceutical production rose from US$860 million in

2000 to US$4.2 billion in 2005, and is forecast to exceed

US$12.5 billion in 2015

• Venture capitalists committed US$337 million to Chinese

life sciences projects during 2008.

• Indian biotech sector could reachUS$5 billion by 2010

• Biopharmaceutical segment has more than 40% of the 325

biotech companies in India

• Few larger Indian companies have begun acquiring foreign

entities in the US and Europe to better retail their products

• China’s health biotech segment had maintained an annual

growth rate of 30% since 2005

• Biopharmaceutical production rose from US$860 million in

2000 to US$4.2 billion in 2005, and is forecast to exceed

US$12.5 billion in 2015

• Venture capitalists committed US$337 million to Chinese

life sciences projects during 2008.

• Indian biotech sector could reachUS$5 billion by 2010

• Biopharmaceutical segment has more than 40% of the 325

biotech companies in India

• Few larger Indian companies have begun acquiring foreign

entities in the US and Europe to better retail their products

Source: Frost & Sullivan Primary Research, Expert Interviews

31

Table of Contents

Key success factors for biotech clustersKey success factors for biotech clusters11

A look at International + Singapore Biotech ClustersA look at International + Singapore Biotech Clusters22

Benchmarking with International ClustersBenchmarking with International Clusters33

32

Comparative Analysis

California Boston Medicon Valley Israel Korea Singapore

Year 1978 1978 1995; Previous Presence 1978 1982 & then 2000 2000

No. of companies 2000 1300 500 1000 in 2008700 pharma , 600 biotech 2000 medical devices

Over 130 global biomedical companies

Sector size and growth

Lifesciences contributed $ 75bn in 2008, a growth of 2% over 2007

Biotechnology annual growth rate of 7% during 2003-2007

N/A Life Sciences was $6.5 bn in 2008

Pharmaceutical was $14bn in 2007 growing at 10% during 2001-2007. Biotech was $3.3 bn in 2006 growing at 18% during 2001-2006

Biomedical sector was $15bn (S$20.7 bn) in 2009 a CAGR of 14% during 2000-2009

Venture Capital Funding (Private Funds)

$3.4 bn in 2009 $1.1 bn in 2006 $940 mn in 2006 $270 mn in 2009 N/A $100-$200 mn in 2009

Employment 274,000 72,000 40,000 12,000 63,000 16,000

Population7.4 mn ( SF Bay Area)2.7 mn (San Diego)

4mn (Greater Boston) 3.2 mn 7 mn 48 mn 4mn

Region Area (sq km)

18000 (SF Bay Area) 840 (San Diego)

12105(Greater Boston)

1788 (Zealand)10939 (Scania)

1788 ( Cluster triangle)

98,480 ( country area) 682

Source: Frost & Sullivan Analysis

33

Comparative Analysis

Cluster Industry Maturity Funding AvailabilityUniversity/Medical Centre Maturity

Business Environment for Life sciences

California

Boston/Massachusetts

Medicon Valley/Sweden/ Denmark

Israel

Korea

Singapore

• California and Boston are leading clusters • Singapore is rated high in Business Environment. It needs to improve on Industry Maturity, Funding Availability,

and University & Medical Centre maturity.• Singapore is a young cluster compared to other clusters. So, this comparison is indicative when compared with

other clusters. The industry has lauded Singapore’s’ biomedical progress over the last ten years

Source: Frost & Sullivan Analysis

34

Comparative Analysis- Industry Maturity (1/2)Successful clusters have critical mass; strong in research; successful in commercialization and have companies across the value chain

ClusterIndustry Maturity

Rationale

California• Northern California has more than 2000 life sciences companies• 560 products on the market and 463 products in Phase II and Phase III clinical trials.

Boston/Massachusetts

• 600+ pharmaceutical/biotech companies, 450 in medical devices• 21 of top 50pharma have manufacturing , 7% of global drug pipeline of 1800+ drugs• 32% in research ,20% in clinical, 33% in commercialization

Medicon Valley/Sweden/ Denmark

• 480 life sciences companies, 209 Biotech, 128 in Medical Devices, 16 Pharma Companies (7

of the largest in the world)• 38% of products in pre-clinical stage• Core competences in therapeutic areas like diabetes/ metabolism, neuroscience, cancer,

inflammation and allergy

Israel

• 750 life science companies, 400 in medical, 160 in Biotechnology, 100 in pharmaceuticals.

Only few big companies like Teva Pharma. Most of the companies are sold once research

gets proven• 27% companies are revenue generating, 36% companies in seed stage, 37% of the

companies are equally divided between clinical and preclinical stages of research• Biotech had $1.8bn in revenues in 2003 with a $4bn target for sector in 2010• Approximately 70 new companies are established every year in the biomedical sector

Source: Frost & Sullivan Analysis

35

Comparative Analysis- Industry Maturity (2/2)Singapore needs critical mass of companies; focus on medical devices, clinical trials increase research commercialization; continue on its growth path

ClusterIndustry Maturity

Rationale

Korea

• Korea Pharmaceutical industry was $14 billion in 2007 growing at 10% during 2001-07• The biotech industry grew rapidly from a worth of US$1.2 billion in 2000 to US$3.3 billion

in 2006, or 0.38% of GDP• In 2006, 708 companies in the life sciences sectors ; 509 are companies focusing both on

R&D and Sale of Bio-products; remaining 199 focused only on R&D.• Companies fall into three general categories: conglomerates (diversified groups), ~30;

mid-size companies (pharmaceuticals, food), ~70, and; small new companies (R&D driven,

often VC financed), more than 500• Tradition in bio-technology and DNA fermentation industry and is the second largest

country in fermentation industry.• Attractive for clinical trials due to its supportive environment, market size, high enrollment

rate and speed, well-equipped facilities, quality data and experienced investigators• Clinical trials in Korea have increased 9 times from 45 in 2001 to 400 in 2008.

Singapore

• BMS manufacturing output was S$21 bn ($15.1 bn) in 2009; CAGR of 14% since 2000;

2.5% growth over 2008• Medtech contributed S$3bn and pharma contributed S$18 bn in 2009• 253 approved clinical trial studies of which 53% are in stage 3• In 2007, GERD in biomedical sciences S$1143.7 mn, 19% of total GERD

Source: Frost & Sullivan Analysis

36

Comparative Analysis- Funding Availability (1/2)Successful clusters have developed private funding channels with strong government support for research and starting up; funding across value chain

ClusterFunding Availability

Rationale

California

• Northern California is home to 34% of active US VCs. California region receives highest NIH

funding of $3.2 bn in 2007 and $800mn in 2009• 28% of biotechnology funding comes from VCs. $1bn in life sciences VC investment in 2009

equally distributed between biotech and medical devices

Boston/Massachusetts

• $2bn funding available in 2005 from NIH for medical research centers• $83 mn funding available in 2005 for small businesses• $1 bn + available in VC funding in 2006 with 70% in Biotech, 3% in Healthcare services and

27% in Medical Devices• Angel Capital available as well ; developed capital markets • Lately VC investment in the sector is being adjusted to find the right set of focus areas

Medicon Valley/Sweden/ Denmark

• 3% of GDP spent by government on research. Govt. spend is mainly on universities and

startups in incubators• Dedicated biotech investors ; in 2007, they had a total of EUR 1 billion funds under

management; made more than 120 biotech/life science investments in their portfolio – local

as well as international

Source: Frost & Sullivan Analysis

37

Comparative Analysis- Funding Availability (2/2)Singapore needs to improve its private funding, pre-seed funding for enterprises

ClusterFunding Availability

Rationale

Israel

• $270 mn in VC funding in 2009• Developed VC industry because of the high technology sector, good science base, presence

of startups and the government funds in partnership with professional VCs• Main modes of domestic support include grants of up to 50% for market-driven competitive

R&D projects, up to 66% for start-up companies, up to 66% for advanced generic

technology, and up to 85% for technological incubators.• Not enough in early stage funding and the very late stages, in the middle it's quite fine.• Not enough options in later stages in Israel and therefore many companies that reach the

late stage have to raise funds overseas

Korea

• Government funding initiatives have given Korea a sound research base.• The Bio-Vision initiative started out with a budget of $720 million for R&D and $230 million

for infrastructure in 2007, with a projected rise to $1.67 billion for R&D and $690 million for

infrastructure by 2016. The total budget for nine years is projected at $15.56 billion.

Singapore

• Approximately $10.6 billion for its phase-two development plan of its Biomedical Science

Initiative from 2006 to 2010• Private VC industry underdeveloped for the sector ; Only around $100-$200 mn of funds • Limited pre seed funding

Source: Frost & Sullivan Analysis

38

Comparative Analysis- University/Medical Centre Maturity (1/2)Successful clusters have startups and products emerging from universities; besides noble laureates, efficiently running TTOs and incubators

Cluster

University/Medical CentreMaturity

Rationale

California• Northern California is home to four major research universities with over $500 million in

research funding: University of California at Davis, University of California at San Francisco

(UCSF), University of California at Berkeley, Stanford University.

Boston/Massachusetts

• 16 Academic Medical Centers• Nation’s highest density of world-renowned medical research facilities• Strong history of startups springing from universities and noble laureates

Medicon Valley/Sweden/ Denmark

• 12 universities, 150,000 university students, of which 45,000 study life science,33 hospitals• 5 TTOs within universities and hospitals, 5 other TTOs in the region• Most significant contribution within cancer research and immunology

Korea

• Korea has Biotechnology-related Departments in 40 Universities• 30 University-associated Research Institutes on the Genetic Engineering, Institute of

Molecular Biology and Genetics, over 20 centers in Biotechnology Area in the Universities

Seoul National University, Korea University, Hanyang University, etc.• Prominent center for clinical trials. 400 trials in 2008 including 216 international trials. 90%

in Phase2 and Phase3• Strong interaction between the universities, research centers and startups.

Source: Frost & Sullivan Analysis

39

Comparative Analysis- University/Medical Centre Maturity (2/2)Singapore needs to focus on research commercialization; have efficient TTOs and incubators; continue its focus on research excellence

Cluster

University/Medical CentreMaturity

Rationale

Israel

• 35% of all academic research in Israel focuses on life science but it receives 50% of total

academic research funding• 7 tech transfer organizations (TTOs) within the universities, 5 TTOs at hospitals• Over the past 40 years Yissum (the TTO of the Hebrew University in Jerusalem) has granted

more than 400 technology licenses and is responsible for commercializing an array of

successful products that generate nearly $1 billion in worldwide sales every year.• Research pioneer Haim Aviv founded Biotechnology General (taken over by Ferring in 1995),

Diatech Diagnostics (taken over by Healthcare Technologies in 1991), Assutech (1990, today:

HerbiMed) and Peptor (1993), which merged with the German biotech company Develogen

in 2004. • Other example of novel Israeli drugs Rebif (Weizmann-Serono) – annual sales $550M ,

GonalF (Weizmann-Serono) - $450M, Doxil (Hadsit/Hebrew U.- J&J) – $350M, Copaxone

(Weizmann-Teva) - $540M, Exelon (Hebrew University-Novartis) - $340M

Singapore

• 2 major Universities, NUS and NTU. Also there are other Tertiary institutes like Duke-NUS

Graduate Medical School• 15 research institutes; 1.41 papers published per 1,000 people• 7 public and 16 private hospitals; 1.7 doctors per 1000 population• GERD: 2.61% of GDP in 2007 less than Korea (3.22% in 2006), USA 2.68% in 2006), Sweden

(4.1% in 2008), Israel (4.8% in 2008)Source: Frost & Sullivan Analysis

40

Comparative Analysis- Business Environment(1/2)Successful clusters have associations, steady stream of workers; high diffusion of knowledge; infrastructure in place and supporting business policies

ClusterBusiness Environment

Rationale

California

• Biggest state by GSP of $1.8 trillion. 6 times that of Massachusetts• Cetus, the world’s first biotech company was founded in 1971 and Genentech in 1976. • Anchor companies’ founders present who mentor next generation entrepreneurs• 100,000 employees, San Francisco metro area has population of 7 mn, San Diego region

has population of 2.9 million• Baybio is an active organization with 450 members;• Clear, strong and highly responsive regulatory bodies

Boston/Massachusetts

• Massachusetts ranks 13 among US states by nominal GSP of $351bn• 70,000 people employed, Boston metro area has population of 5.8 million• Operation costs are high, Housing and transportation problems• Massbio is a leading biotech association. Several forums for networking and collaboration

Medicon Valley/Sweden/ Denmark

• 3.5 Million inhabitants, 40000 employees; Minimal regulations imposed on startups• Sweden and Denmark rank 4th and 5th of 133 economies in WEF- Global Competitiveness

Report 2009 respectively. • Both Denmark and Sweden rank high in innovation, education, goods market stability,

macroeconomic stability and technology readiness.• High personal taxes and weather discourage foreign talent, Small local market

Source: Frost & Sullivan Analysis

41

Comparative Analysis- Business Environment(2/2)Singapore can improve on knowledge diffusion; availability of more skilled workers

Cluster

Business Environment

Rationale

Israel

• High level of entrepreneurship, Strong networks because of a small country and people undergoing

military training in common• Few Life Science Industry and startup associations; Bureaucratic Red tape, Lack of transparency, High

taxes; History of years of war• Good Regulatory standards, Israel is ranked as an Innovation based economy by WEF 2009• Israel ranks high in higher education achievements

Korea

• 21000 employees, Educated and experienced R&D manpower• Government has a dedicated effort towards the sector since 1982; picked up pace in 2000’s• Several initiatives to connect universities to industry and create focused clusters• Pharmaceutical companies do not have strong experience to enter global markets• South Korean economy's long term challenges include a rapidly aging population, inflexible labor

market, and overdependence on manufacturing exports to drive economic growth

Singapore

• Population is 4.8 million;12450 employed in biomedical manufacturing sector• Ranked 2nd in IP protection; Singapore ranks 3rd in WEF report 09-10, slightly ahead of Denmark and

Sweden• Participants have mentioned the lack of few niche facilities• World’s Top Logistics Hub (World Bank 2007); Well-connected through its airport• Concluded 19 FTAs that cover 60% of the world’s GDP

Source: Frost & Sullivan Analysis

42

Develop private VC industry in long term – Learning from Israel professional funds with government participation

Yozma program in Israel started in 1992 with a govt. funding of $100 mn ($80 mn in 10 startup focused VC funds and $20mn as direct investments in startups.

Yozma program in Israel started in 1992 with a govt. funding of $100 mn ($80 mn in 10 startup focused VC funds and $20mn as direct investments in startups.

Target Level of Capital Aimed was 200-250M$ (Government Support- 100M$)- this was the ‘Critical Mass’ of effort required for VC industry ‘emergence’

Target Level of Capital Aimed was 200-250M$ (Government Support- 100M$)- this was the ‘Critical Mass’ of effort required for VC industry ‘emergence’

Government Participation in each Fund-8 million dollars (in most Funds this represented 40% of the 20 M$ raised)

Government Participation in each Fund-8 million dollars (in most Funds this represented 40% of the 20 M$ raised)

Strong Incentive to the “Upside”- the possibility, within a 5 year period, of purchasing Government’s share at approx. at cost with 5-7% interest rate(all Funds except 3 made

use of this option). There was no downside 'guarantee‘.

Strong Incentive to the “Upside”- the possibility, within a 5 year period, of purchasing Government’s share at approx. at cost with 5-7% interest rate(all Funds except 3 made

use of this option). There was no downside 'guarantee‘.

Israel Yozma Program to develop local VC industry

Israel Yozma Program to develop local VC industry

Each fund managed by a local management company& involving at least one Reputable Foreign Financial Institution (and one important Domestic Financial

Institution)

Each fund managed by a local management company& involving at least one Reputable Foreign Financial Institution (and one important Domestic Financial

Institution)

• Rapid entry of non Yozma VC funds was seen in Israel in1996• Significant increase in number of startups seen in Israel • Growth of (gross) accumulated numbers of new VC-backed SU companies from 110 in 1993 to 730 in 1998

Source: Ministry of Finance, Israel Presentation on Life Science Funds Dec 2009, Venture Capital Policy in Israel , A paper by Gil AvniMelech, Hebrew University 2002

43

Two round of reviews; Scoring Criteria established for determining scientific and technical merit; Applications receive a written critique, Interviews of key people – Learning from US Small Business Grants Criteria

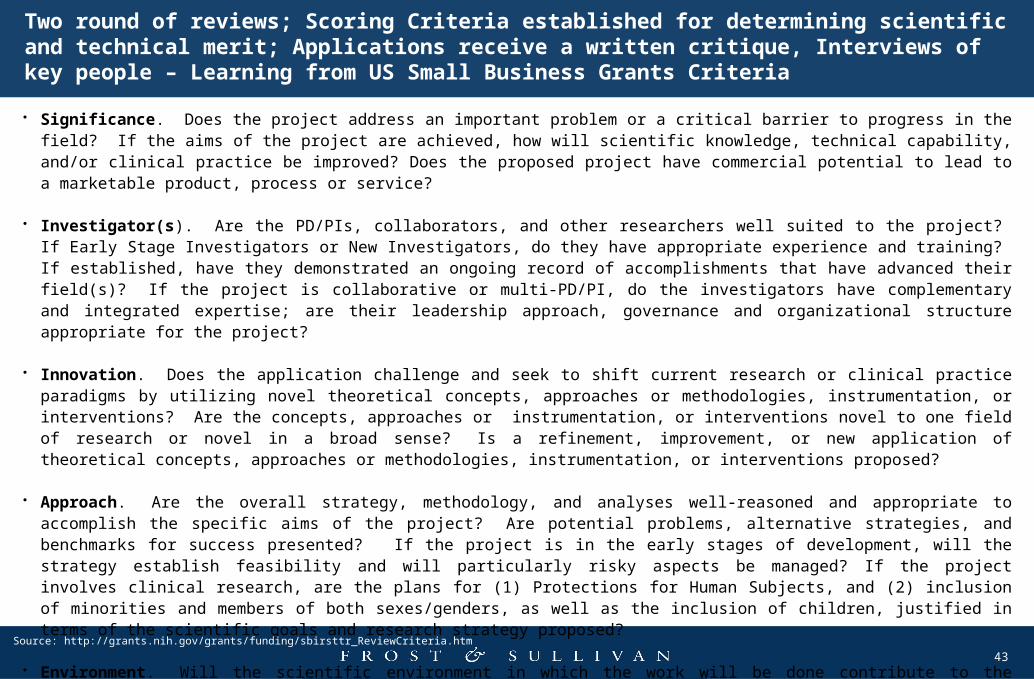

• Significance. Does the project address an important problem or a critical barrier to progress in the field? If the aims of the project are achieved, how will scientific knowledge, technical capability, and/or clinical practice be improved? Does the proposed project have commercial potential to lead to a marketable product, process or service?

• Investigator(s). Are the PD/PIs, collaborators, and other researchers well suited to the project? If Early Stage Investigators or New Investigators, do they have appropriate experience and training? If established, have they demonstrated an ongoing record of accomplishments that have advanced their field(s)? If the project is collaborative or multi-PD/PI, do the investigators have complementary and integrated expertise; are their leadership approach, governance and organizational structure appropriate for the project?

• Innovation. Does the application challenge and seek to shift current research or clinical practice paradigms by utilizing novel theoretical concepts, approaches or methodologies, instrumentation, or interventions? Are the concepts, approaches or instrumentation, or interventions novel to one field of research or novel in a broad sense? Is a refinement, improvement, or new application of theoretical concepts, approaches or methodologies, instrumentation, or interventions proposed?

• Approach. Are the overall strategy, methodology, and analyses well-reasoned and appropriate to accomplish the specific aims of the project? Are potential problems, alternative strategies, and benchmarks for success presented? If the project is in the early stages of development, will the strategy establish feasibility and will particularly risky aspects be managed? If the project involves clinical research, are the plans for (1) Protections for Human Subjects, and (2) inclusion of minorities and members of both sexes/genders, as well as the inclusion of children, justified in terms of the scientific goals and research strategy proposed?

• Environment. Will the scientific environment in which the work will be done contribute to the probability of success? Are the institutional support, equipment and other physical resources available to the investigators adequate for the project proposed? Will the project benefit from unique features of the scientific environment, subject populations, or collaborative arrangements?

Source: http://grants.nih.gov/grants/funding/sbirsttr_ReviewCriteria.htm

44

Proactive commercialization in Research and Academic Centers – Learning from Yale University

Technology Transfer at Yale University

Technology Transfer at Yale University ImpactImpact

• Only six biotech companies in 1993• The hard work of seeking appropriate investors

eventually paid off, and in 1998, after two years

of effort, the first round of financing was

concluded with $20 million for five companies.• Today the Connecticut cluster employs 17,985

people directly and 35,857 through indirect and

induced employment. It consists of 49

biotechnology companies. Five of the biotech

companies are publicly traded: Alexion

Pharmaceuticals, Neurogen, Curagen,

Gennesiance, and Vion Pharmaceuticals. Of

the biotech companies, 24 companies, or 49%,

of the biotechnology cluster in New Haven

were created after 1996 with technology, ideas,

or founders from Yale and with the help of the

OCR.

• Only six biotech companies in 1993• The hard work of seeking appropriate investors

eventually paid off, and in 1998, after two years

of effort, the first round of financing was

concluded with $20 million for five companies.• Today the Connecticut cluster employs 17,985

people directly and 35,857 through indirect and

induced employment. It consists of 49

biotechnology companies. Five of the biotech

companies are publicly traded: Alexion

Pharmaceuticals, Neurogen, Curagen,

Gennesiance, and Vion Pharmaceuticals. Of

the biotech companies, 24 companies, or 49%,

of the biotechnology cluster in New Haven

were created after 1996 with technology, ideas,

or founders from Yale and with the help of the

OCR.

• High support–high selectivity policies needed for entrepreneurially

underdeveloped environments• Provided facilities like creation of business plan, providing mentoring

support, promotion of success stories, having entrepreneurial

courses in curriculum, incentives for starting up, getting

entrepreneurs to set up in the region and chasing VCs• Gregory Gardiner, a former Pfizer executive took charge of Office of

Cooperative Research in 1982• An important goal for the Yale OCR was to identify new ideas,

cultivate venture funding for them, and facilitate their development

into companies that become part of the New Haven economy. • Increased exposure of researchers to commercial ideas• The renewed OCR established direct contacts with venture capital

firms. The goal was not only to persuade venture capital firms of the

relevance of university technology but also to convince them to

create ventures in New Haven

• High support–high selectivity policies needed for entrepreneurially

underdeveloped environments• Provided facilities like creation of business plan, providing mentoring

support, promotion of success stories, having entrepreneurial

courses in curriculum, incentives for starting up, getting

entrepreneurs to set up in the region and chasing VCs• Gregory Gardiner, a former Pfizer executive took charge of Office of

Cooperative Research in 1982• An important goal for the Yale OCR was to identify new ideas,

cultivate venture funding for them, and facilitate their development

into companies that become part of the New Haven economy. • Increased exposure of researchers to commercial ideas• The renewed OCR established direct contacts with venture capital

firms. The goal was not only to persuade venture capital firms of the

relevance of university technology but also to convince them to

create ventures in New Haven

Source: University Commercialization Strategies in the Development of Regional Bioclusters , Shiri M. Breznitz, Rory P. O’Shea, and Thomas J. Allen published in Journal of Product Innovation Management 2008

45

THANK YOU

Rhenu BhullerVice PresidentFrost & Sullivan Biotechnology Group

rbhuller@ frost.comContact: +65 6890 0986