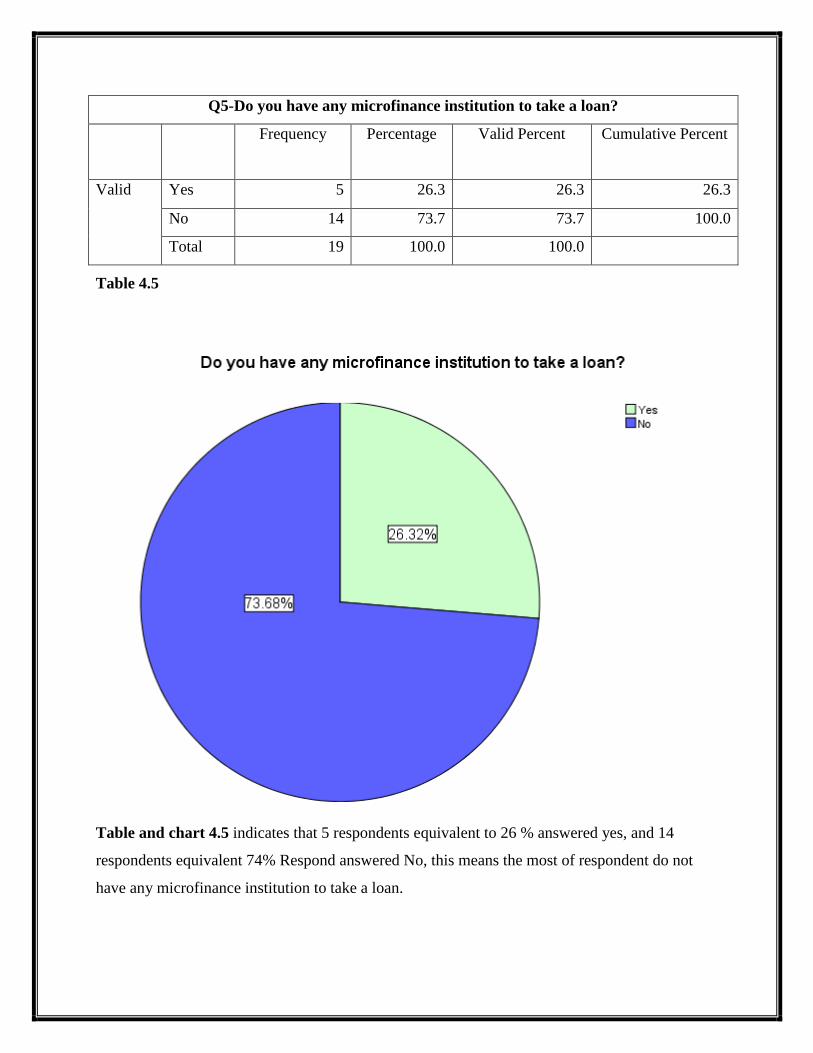

review Advisor: Mustafa Mohamed...

65

1 2 Literatu re review 3 Credit records Pricing data Bibliography UNIVERSITY OF HARGEISA FACULTY OF ECONOMICS HARGEISA, SOMALILAND The Role of Microfinance in Job creation in Hargeisa s/land Introduction Advisor: Mustafa Mohamed Aden By: Farhan Aw-dahir Dugsiiye 4 Conclusion & Analysis &discussion recommendation University of Hargeisa Faculty of Economics July, 2015 UOH “ THE ROLE OF ACCOUNTING FOR INVENTORY MANAGEMENT IN BUSINES

Transcript of review Advisor: Mustafa Mohamed...

1

2

Literatu

re

review

3

Bill

Customers

Credit records

Pricing data Bibliography

UNIVERSITY OF HARGEISA

FACULTY OF ECONOMICS

HARGEISA, SOMALILAND

The Role of Microfinance in Job creation in Hargeisa s/land

Introduction

Advisor: Mustafa Mohamed Aden

By: Farhan Aw-dahir Dugsiiye 4

Conclusion &

Analysis &discussion recommendation

University of Hargeisa

Faculty of Economics

July, 2015 UOH

“ THE ROLE OF ACCOUNTING FOR INVENTORY MANAGEMENT IN BUSINES

Prepared by:

Farhan Aw-dahir Dugsiiye

ID: ECO 114917

Advisor: Pro. Mustafa Mohamed Aden

Project Paper Submitted in Partial Fulfillment of the Requirement for the

Degree of Economics

Research Proposal Submission Form

Project Paper Title: The Role of Microfinance in job creation in Hargeisa Somaliland

Director:

UNIVERSITY OF HARGEISA (UOH)

Faculty of Economics

Dear Sir:

Attached are the following documents for evaluation and approval:

Chapter1: Introduction

Chapter2: Literature review

Chapter3: Research methodology

Chapter4: Data Analysis and interpretation

Chapter 5: Conclusion and Recommendations

I have thoroughly checked by work and I am confident that this is free from grammatical errors,

weaknesses in sentence construction, spelling mistakes, referencing mistakes and others, I have

checked guidelines for writing project paper and I am satisfied that he project paper proposal

satisfied its requirement

Thanks you…………………………….

I have read the student research proposal and I am satisfied that it is in line with the UOH program

guidelines for writing project proposal. It is also free from major grammatical errors, sentence

construction weaknesses, citation and others.

Supervisor signature: ____________ Date: _______________

DECLARATION

Name: Farhan Aw-dahir Dugsiiye

Student number: Eco 114917

I have by declare that this project paper is the result of my own study based on my

Interest to take into this microfinance, aside from parental guidance and my

Friends support to enable me to establish this study. For the internet system of which I conduct research

as one of my source for this study, quotations for the inquiry and summaries

Which have been duly acknowledged?

I hereby verity that this research is not submitted in substance for any other degree

Signature: __________________ Date: __________________

Supervisor name: Pro. Mustafe Mohamed Aden

Application to conduct Research Paper

PART A: STUDENT PARTICULAR

1: Student name: Farhan Aw-dahir Dugsiiye

Student number: Eco 114917

PART B: PARTICULAR ABOUT THE PROJECT

1: Title of the project: The Role of Microfinance in job creation in Hargeisa Somaliland

2: Research Objective: The main objective of this research is to find the role of microfinance in

job creation.

3: Proposed research method.

PART C: FACULTY’S INPUTS

1: Topic chosen: Accepted/ Not Accepted

2: Suggested Supervisor for the student

Dedicated to

MY LOVED PARENT:

Mrs.: Moumina Mahamoud Mr.: Aw-dahir Dugsiiye

My ALLAH rest their souls in the heaven and be merciful to them as they were to me in my

childhood (Amen) and honorable professor who had a great talent teaching method, and brought

beautiful studies.

ACKNOWLEDGEMENTS

First, thanks to “ALLAH” who gave me the power of doing this program and implementing,

who also allowed me to reach my spiral goals?

First of all to complete this research required the assistance, guidance and support of a number of

people to whom I would like to express my deeply appreciation and acknowledge them which

makes this project finally seem uncomplicated.

I would like to thank my supervisor Pro: Mustafa Mohamed Aden for his guidance throughout

the preparation of this study. Realizing this project would not have been achievable without his

support and the encouragement of him this masterpiece would never have been completed.

For his special guidance and un accountable advice for doing the research and extremely diligent

in reviewing text chapters exercise, problem, and their solutions that paves the way in

implementing and preparing this research paper.

I am also would like to thanks many people who guided and supports me throughout the

developing of the text express my sincere appropriation their expert attention that effectively

guided this book through production process.

The text and its sump lent have been enriched by the comments of many reviewers; I am

indebted to each of them, who assisted me.

I am also, thanks to dozen of my colleagues for adopting their encouragement and cooperative

support.

I am also would like to thanks Kaaba Microfinance Institution that has found data and the

students of university of Hargeisa they support the questionnaire to fulfill.

Abstract

The objective of the paper is to investigate the role of microfinance in job creation.

Microfinance consist of micro-loan, saving, insurance, money transfer. It facilities the poor

household income to get easy micro-credit, this encouraged the society, low-income people,

youth and the other parts of society.

Job creation often refers to government policies to reduce unemployment that caused many of

the unemployment workers to work and also eliminate the rate of unemployment.

Therefore it is very necessary to accept an efficient inventory process to give the right status. The

research has chosen known organization to examine which method is efficient of fulfill this type

of operation.

Students of university of Hargeisa and Kaaba Microfinance Institution,

This project is examining most known microfinance method. And then select the most proper

microfinance method in job creation.

The researcher has chosen known Kaaba microfinance institution to find out the data.

The Somaliland government until has not started a plan to developing or improving a society at

side of job creation or economic sector. Because of Somaliland society has living a low living

standard. When the creation microfinance or small business has encouraged a poor people and

youth have a living standard of the society is grow up. The unemployment was bringing a many

of the generations to migration in the European countries, which preferred better life.

CONTEXT PAGE

Title page……………………………………………………………………......i

Research proposal submission form……………………………………………ii

Declaration page………………………………………………………………..iii

Application to conduct research paper………………………………………….iv

Dedication page…………………………………………………………………v

Acknowledgement……………………………………………………………...vi

Abstract………………………………………………………………………...ix

Table of contents………………………………………………………………..x

List of figures…………………………………………………………………..xii

List of abbreviations……………………………………………………………xii

CHAPTER ONE INTRODUCTION.................................................................1

1.1: Background of the study……………………………………………………2

1.2: Statement of the problem…………………………………………………….3

1.3: purpose of study…….………………………………………………..............4

1.4: Research questions and hypothesis……………………………………..…….4

1.5: Objectives of study…………………………………………………………...4

1.6: Scope……………………………………………………………………........4

1.7: significant of study ……….……………………………………………..........5

1.8: description of study area...........................................................................…….5

1.9 limitation of the study…………………………………………………………..6

2: LITERATURE REVIEW:…………………….………………………………7

2.0: Definition of microfinance …….………………….…………………………..7

2.1: Microfinance and microcredit …………………….……………………..........8

2.2: The history of microfinance…………………………….………………..........8

2.3: Characteristics of Microfinance ……………………………………………...9

2.4: Microfinance Service…………………….…………………………………..10

2.5: Microfinance Services in world ….………………………………………….11

2.6: Microfinance Services in Africa ……………………………………………..11

2.7: Impact of Microfinance ……………………………………………….…......12

2.8: Microfinance and its impact in development…………...………………..…...13

2.9: The impact of microfinance on poverty………………………………………14

2.10: Islamic in microfinance………………………………………………………14

2.10.1 Mudarabah………………………………………………………………….14

2.10.2 Musharakah…………………………………………………………….……15

2.10.3 Murabahah……………..……………………………………………………16

2.10.4 Ijarah…………………………………. …………………………………….17

2.10.5: Qard Al-hasan………………………………………………………………18

2.11: Kaaba microfinance institution……………………………………………….18

2.12: definition of job creation……………………………………………………..19

2.13: advantage of job creation………………………………………………………20

2.14: The role of the public sector in job creation…………………………………......21

2.15.0: The role of the private sector in job creation…………………………………..21

2.15.1: Direct action concerning skills development and training…………………….22

2.15.2: Direct actions concerning job creation…………………………………………23

2.15.3. Policy making and advocacy…………………………………………………..23

2.16: social and economic benefits of job creation……………………………………..24

2.16.1: Job creation is the best weapon in the battle against poverty……………………24

2.16.2: Job creation improves income distribution and reduces inequality………………24

2.16.3 Job creation can improve conditions and promote investment in the poorest

communities………………………………………………………………………………24

2.16.4: Job creation can stimulate output, income, consumption and Investment……….24

2.16.5: Job creation supports public and social goods and services………………………24

3.0: RESEARCH METHODOLOGY

3.0: Variable definition……………………………………………………………….25

3.1: Research design…………………………………………………………………..25

3.2: Research population…………………………………………………………….....26

3.3: Sampling Technique………………………………………………………………26

3.4: Sample Size……………………………………………………………………….33

3.5: Sampling Procedure……………………………………………………………….34

3.6: Research instruments………………………………………………………………34

3.7: Data collection procedure………………………………………………………….34

3.8: Data analysis……………………………………………………………………….28

3.9: Ethical issues of the study…………………………………………………………28

4.0: DATA ANALYSING AND INTERPRETATION

4.1 introduction……………………………………………………………...29

List of TABLES AND FIGURES Page

Tab & Fig 4.1…………………………………………………………………30

Tab & Fig 4.2…………………………………………………………………31

Tab & Fig 4.3…………………………………………………………………32

Tab & Fig 4.4…………………………………………………………………33

Tab & Fig 4.5………………………………………………………………....34

Tab & Fig 4.6…………………………………………………………………35

Tab & Fig 4.7…………………………………………………………………36

Tab & Fig 4.8…………………………………………………………………37

Tab & Fig 4.9…………………………………………………………………38

Tab & Fig 4.10………………………………………………………………..39

Tab & Fig 4.11………………………………………………………………..40

Tab & Fig 4.12………………………………………………………………..41

Tab & Fig 4.13………………………………………………………………..42

Tab & Fig 4.14………………………………………………………………..43

Tab & Fig 4.15………………………………………………………………..44

Tab & Fig 4.16………………………………………………………………..45

5.0: CONCLUSION AND RECOMMENDATIONS.................................46

5.1: Conclusion……………………………………………………….………47

5.2: Recommendations………………………………………………………49

6.0 Appendix

6.1 Appendix A

Questionnaire…………………………………………………………………53

Chapter One: Introduction

1.1 Background of the Study

Microfinance consists of the provision of financial services in small increments, typically to very

poor people.

The beginnings of the microfinance movement are most closely associated with the economist

Muhammed Yunus, who in the early 1970's was a professor in Bangladesh. In the midst of a

country-wide famine, he began making small loans to poor families in neighboring villages in an

effort to break their cycle of poverty.(1)

The experiment was a surprising success, with Yunus

receiving timely repayment and observing significant changes in the quality of life for his loan

recipients. Unable to self-finance an expansion of his project, he sought governmental assistance,

and the Grameen Bank was born. In order to focus on the very poor, the Bank only lent to

households owning less than a half-acre of land. Repayment rates remained high, and the Bank

began to spread its operations to other regions of the country. In less than a decade, the Bank was

operating independently from its governmental founders and was advertising consistent

repayment rates of about 98%. In 2006 Yunus was awarded the Nobel Peace Prize.

The success of the Grameen Bank did not go unnoticed. Institutions replicating its model sprang

up in virtually every region of the globe. Between 1997 and 2002, the total number of MFIs grew

from 618 to 2,572. Altogether, these institutions claimed about 65 million clients, up from 13.5

million in 1997 and still growing at 35% a year. The amount of money flowing to clients also

continues to climb rapidly and the Grameen Bank has extended over $750 million worth of credit

in the past two years alone.

Alongside the explosion of the microfinance industry in absolute terms, there has been a steady

growth in private financing for MFIs. The bulk of microfinance funding is still provided by

development-oriented international financial institutions and NGO's. Yet estimates place demand

for unmet financial services at roughly 1.8 billion individuals. Even at its current growth rates, it

is clear that microfinance will only be extended to meet this enormous demand by leveraging

private capital, flows of which dwarf all other potential sources. Commercial financing has

grown most rapidly in Latin America, where regulated financial institutions now serve 54% of

the continent's microfinance clients and, importantly, are now responsible for 74% of the region's

loans. Overall, 2005 saw private lending to MFIs jump from $513 million to $981 million.

The European Progress Microfinance Facility has proved to be a successful tool to create jobs,

particularly amongst groups with difficulties to raise finance from more traditional sources, by

helping start-ups by micro-entrepreneurs, according to the second annual report on its

implementation, published today. Through this Facility twenty microfinance providers

throughout the European Union have received guarantees or funding (debt or equity) to facilitate

their lending to would-be micro-entrepreneurs worth €170 million over the coming two to three

years.(2)

A recent study by the UN office of the Special Adviser on Africa suggests that now is a good

time to reassess the role of microfinance in Africa's development. Drawing from experience

elsewhere, it seems clear that micro-finance is not a magic bullet. On its own it cannot

fundamentally transform African economies held back by many structural constraints. Yet

providing a whole range of financial services to the poor including credit for small and micro-

enterprises, savings facilities, insurance, pensions, and payment and transfer facilities is clearly

desirable and can contribute to the achievement of the Millennium Development Goals.

Africa has seen an increase in such services in recent years. Microfinance institutions offer a

variety of products.(3)

Where such institutions do not reach, traditional and informal providers

such as the tontines in Cameroon, the Susu in Ghana and the banquiers ambulates in Benin

continue to serve the poor. Their informality limits their potential to expand their activities,

however, and they often charge high rates.

Somaliland, a relatively small area in the Northwest, became independent in 1991. Since then, it

has managed to restore many aspects of normal society. However it has lost many citizens,

people who fled to safe countries and took another nationality. (4)

Doses of Hope (DoH) are an

NGO that works in Somaliland. It was started by three refugees in the Netherlands. It now has

two main activities, micro credit and a second section that assists disabled children and adults.

Many disabilities are the result of the Civil War.

Somaliland is an Islamic country and Islam has serious reservations against the charging of

interest. But a micro-finance project that only gets back what it loans will soon run out of money,

given inflation and the costs of running the project. There had to be a stage when interest or an

alternative is introduced. A dose of Hope does not charge interest; it charges administrative

costs. These are deducted at source: someone borrowing $200 will be given $180 with $20 kept

back for administrative costs.

Some community members, particularly borrowers who have trouble repaying or who just do not

want to repay, complain about the administrative costs, claiming that they are non-Islamic.

1.2 Statement of the Problem

Microfinance is providing financial service to low income people. It refers to a project to create

small business such to beneficiary poor and young people.

Microfinance consist of micro-loan, saving, insurance, money transfer. It facilities the poor

household income to get easy micro-credit, this encouraged the society, low-income people,

youth and the other parts of society.

Job creation often refers to government policies to reduce unemployment that caused many of

the unemployment workers to work and also eliminate the rate of unemployment.

The Government can motivate job creation when it invests in projects that improve or create new

services. These activities could include releasing contracts to the private sector for infrastructure,

defense, engineering, justice, etc. Other ways that the government creates jobs is by issuing

special grants for privately run programs. These are often for special studies and research. Grant

receivers do employ people. However these grants are often connected to special favors called

earmarks. These seemingly good gestures destroy independent innovation that is developed by

unconnected science communities and can cause discouragement to innovate by others.

The Somaliland government until has not started a plan to developing or improving a society at

side of job creation or economic sector. Because of Somaliland society has living a low living

standard. When the creation microfinance or small business has encouraged a poor people and

youth have a living standard of the society is grow up. The unemployment was bringing a many

of the generations to migration in the European countries, which preferred better life.

1.3 Purpose of the Study

The purpose of this study investigates the role of microfinance in job creation in Hargeisa

Somaliland.

1.4 Research questions

1: how does the microfinance reduce the poverty?

2: how does the job creation decrease the credit of youth?

3: what is the relationship between microfinance and job creation?

1.5 Objectives of Study

The specific objectives are:

To establish whether microfinance have the required financial capacity (cost-

effectiveness of credit operation).

To investigate how microfinance increases entrepreneurial competence and culture.

To find out products microfinance institutions employ to enable the Youth access credit

and accumulate savings.

To establish the extent to which microfinance institutions have succeeded in poverty

eradication among the youth.

1.6 Scope

The study will be conducted in Hargeisa the capital city of Somaliland. It will focus Micro-

finance institutions where KAABA, will the specific case for this research. It will cover three

months effective from 26th

April, 2015.

1.7 Significance of study

Upon the completion of this study the following stakeholders will benefits:

Society: is the first beneficiary of the microfinance and also making job creation, because when

the microfinance providing a poor people or young people is increased the employment of the

society.

The provision microfinance or loan they are making in small business that facilities to create

income or other business is very important to society and increased economic of the society.

Institutions: based on the outcome of this study it concerned all institutions to beneficiary this

study to focus on the microfinance, because of this study will eliminate needs toward making

research the role of microfinance in job creation.

Government: if they need information about the microfinance and job creation has received in

this book. Because this study has concerned government, institutions, society and other needed

information. This study will assistance some of the institution of the government and international

institutions such as ministry of social affairs and labor, ministry of trade and investment, banks,

institutions and international organization. Lastly, the study will also intend to add to the existing

literature on microfinance in job creation, to help future researchers interested in the subject matter and as

a basis for further reference.

1.8 Description of the study Area

Population: The total population of Somaliland is estimated 3.5 million; the majority of the

population lived in the rural areas as pastoralist and nomads 50%, while about 35% live in urban

cities or centers. The remaining 15% live outside of the country. (5)

Mainly in Europe and North

America. The average life expectancy for males is 50 years old, and for females 55. The

population is dispersed in Hargeisa, the capital city, and other main towns and cities such as

Burao, Borama, Berbera, Erigabo, Gabiley, Saylac and Las Anod.

Location: The Republic of Somaliland is situated in the Horn of Africa with boundaries defined

by the Gulf of Aden in the North, Somalia in the East and Southeast, the Federal Republic of

Ethiopia in the South and West, and the Republic of Djibouti to the Northwest.

Culture and language: Somali is the official language, including Arabic and English. It is

mandatory that Arabic be taught in schools and mosques, with English too being spoken and

taught in schools around the country. Somali is one of the Cushitic Languages of the Afro-asiatic

family.

Economy: The region’s main source of income comes from the export of livestock (camels,

cattle, goats, and sheep) to Saudi Arabia and the Gulf States through the port of Berbera. Produce

from agriculture are sorghum and maize, with the Hargeisa highland being best suited for dry-

farming, whilst the Haud region is more suitable for animal grazing. The economy of Somaliland

is estimated GDP $1.5 billion and the GDP per capital income $429 and the other sectors to

contribution is agriculture sector is 65%, industry is 10% and service is 25%.

Religious: Majority of the population consists of Sunni Muslims; Islam is the principle faith and

religion. Religion informs social norms and practice, such as women wearing a hijab (a veil

covering the body except for the hands and face) in public, and all Somalis abstaining from

gambling, the eating of pork, or drinking of alcohol, as is discouraged in Islam. 100% is Muslim

pure.

1.9 Limitation of Study

There is some of the limitation in the microfinance. Firstly there are little of institutions to

provide microfinance in Somaliland especially in Hargeisa. The government of our country there

is not making a strategic to developing a low-income people or young people because they bring

a many of family to living a low standard living.

There is not data with concerned microfinance because when visited to the ministry of finance

that was told there is not data of the microfinance.

The second constraint to this research was finance and time. The time allowed for the completion

of this work was short, coupled with the fact that other academic work were in progress.

Chapter two

Literature Review

2.0 What is microfinance?

Microfinance, according to (Otero, 1999) is “the provision of financial services to low-income

poor and very poor self-employed people”. These financial services according to (Ledgerwood,

1999) generally include savings and credit but can also include other financial services such as

insurance and payment services. (Schreiner & Colombet 2001) define microfinance as “the

attempt to improve access to small deposits and small loans for poor households neglected by

banks.” Therefore, microfinance involves the provision of financial services such as savings,

loans and insurance to poor people living in both urban and rural settings who are unable to

obtain such services from the formal financial sector.

“Microfinance is commonly associated with small, working capital loans that are invested in

microenterprises or income-generating activities” (Churchill & Frankiewicz2006). Such

microenterprises are often family owned and have less than five employees, sometimes based out

of the home, as for instance small retail kiosk, sewing workshops, carpentry shops and market

stalls (Whole Planet Foundation, 2009).

Today however microfinance is referred to more generally as the provision of financial services

to those excluded from the formal financial system (UNCDF, 2002). In the beginning the credits

that were given to poor were called micro credits or micro-lending, but soon it became clear that

also other financial services were used and needed by the poor which enlarged the micro credits

to “microfinance” (Kuzu, 2005).

"Microfinance can be broadly defined as: “The provision of small-scale financial services such

as savings, credit and other basic financial services to poor and low-income people”.

According to United Nation (UN)

The term "microfinance institutions (MFI‟s)" now, refers to a wide range of organizations

dedicated to providing these services and includes non-governmental organizations, credit

unions, cooperatives, private commercial banks, non-bank financial institutions and parts of

State-owned banks.”Poor people are not able to access loans from commercial banks normally

because of lack in guarantee and collateral. But there are many other reasons also involved for

which commercial banks were not willing to finance poor. These reasons are included that poor

have less education, no proper experience and training, high expenses on transactions of small

loans and lower rate of profit. (Mazher 2010).

2.1 Microfinance and microcredit.

In the literature, the terms microcredit and microfinance are often used interchangeably, but it is

important to highlight the difference between them because both terms are often confused.

(Sinha 1998) states “microcredit refers to small loans, where as microfinance is appropriate

where NGOs and MFIs supplement the loans with other financial services (savings, insurance,

etc)”. Therefore microcredit is a component of microfinance in that it involves providing credit

to the poor, but microfinance also involves additional non-credit financial services such as

savings, insurance, pensions and payment services (Okiocredit, 2005).

2.2 The History of Microfinance

Microcredit and microfinance are relatively new terms in the field of development, first coming

to prominence in the 1970s, according to (Robinson 2001) and Otero (1999). Prior to then, from

the 1950s through to the 1970s, the provision of financial services by donors or governments was

mainly in the form of subsidized rural credit programmers’. These often resulted in high loan a

default, high loses and an inability to reach poor rural households (Robinson, 2001). Robinson

states that the 1980s represented a turning point in the history of microfinance in that MFIs such

as Grameen Bank and BRI began to show that they could provide small loans and savings

services profitably on a large scale. They received no continuing subsidies, were commercially

funded and fully sustainable, and could attain wide outreach to clients (Robinson, 2001). It was

also at this time that the term “microcredit” came to prominence in development (MIX, 2005).

The difference between microcredit and the subsidized rural credit programmers of the 1950s

and 1960s was that microcredit insisted on repayment, on charging interest rates that covered the

cost of credit delivery and by focusing on clients who were dependent on the informal sector for

credit (ibid.). It was now clear for the first time that microcredit could provide large-scale

outreach profitably. The 1990s “saw accelerated growth in the number of microfinance

institutions created and an increased emphasis on reaching scale” (Robinson, 2001). (Dichter

1999) refers to the 1990s as “the microfinance decade”. Microfinance had now turned into an

industry according to (Robinson 2001). Along with the growth in microcredit institutions,

attention changed from just the provision of credit to the poor (microcredit), to the provision of

other financial services such as savings and pensions (microfinance) when it became clear that

the poor had a demand for these other services (MIX, 2005). The importance of microfinance in

the field of development was reinforced with the launch of the Microcredit Summit in 1997. The

Summit aims to reach 175 million of the world’s poorest families, especially the women of those

families, with credit for the self-employed and other financial and business services, by the end

of 2015 (Microcredit Summit, 2005). More recently, the UN, as previously stated, declared 2005

as the International Year of Microcredit.

2.3 Characteristics of microfinance

Microfinance gives access to financial and non-financial services to low-income people, who

wish to access money for starting or developing an income generation activity. The individual

loans and savings of the poor clients are small (Kodheka, 2003). Microfinance came into being

from the appreciation that micro-entrepreneurs and some poorer clients can be ‘bankable’, that

is, they can repay, both the principal and interest, on time and also make savings, provided

financial services are tailored to suit their needs. Microfinance as a discipline has created

financial products and services that together have enabled low-income people to become clients

of a banking intermediary. The characteristics of microfinance products include:

i. Little amounts of loans and savings and short- terms loan (usually up to the term of one year).

ii. Payment schedules attribute frequent installments (or frequent deposits) and Installments

made up from both principal and interest, which amortized in course of time.

iii. Higher interest rates on credit (higher than commercial bank rates but lower than loan-shark

rates), which reflect the labor-intensive work associated with making small loans and allowing

the microfinance intermediary to become sustainable overtime.

iv. Easy entrance to the microfinance intermediary saves the time and money of the client and

permits the intermediary to have a better idea about the clients’ financial and social status.

v. Application procedures are simple and short processing periods (between the completion of

the application and the disbursement of the loan).

vi. The clients who pay on time become eligible for repeat loans with higher amounts and the use

of tapered interest rates (decreasing interest rates over several loan cycles) as an incentive to

repay on time. Large size loans are less costly to the MFI, so some lenders provide large size

loans on relatively lower rates.

vii. No collateral is required contrary to formal banking practices. Instead of collateral,

microfinance intermediaries use alternative methods, like, the assessments of clients’ repayment

potential by running cash flow analyses, which is based on the stream of cash flows, generated

by the activities for which loans are taken.

2.4 Micro finance services

Micro finance Services refer mainly to small loans; savings mobilization and training in micro

enterprise investment services extended to poor people to enable them undertake self

employment projects that generate income (Onuaman, 2002). Micro finance came into being

from the appreciation that micro entrepreneurs and some poorer clients can be ‘bankable’, that is,

they can repay both the principal and interest, on time and also make savings, provided financial

services are tailored to suit their needs (Coetze, 2003)). Micro finance is perceived as the

provision of financial and non financial services by micro finance institutions (MFIs) to low

income groups without tangible collateral but whose activities are linked to income generating

ventures (Sinha, 2008). These financial services include savings, credit, payment facilities,

remittances and insurance. The non-financial services mainly entail training in micro enterprise

investment and business skills. There is also a belief that micro finance encompasses micro

credit, micro savings and micro insurance (CGAP, 2004). Micro finance is not a new

development. Its origin can be traced back to 1976, when Muhammad Yunus set up the Grameen

Bank, as experiment, on the outskirts of Chittagong University campus in the village of Jobra,

Bangladesh. The aim was to provide collateral free loans to poor people, especially in rural areas,

at full-cost interest rates that are repayable in frequent installments. Borrowers were organized

into groups and peer pressure among them reduced the risk of default (Khan& Rahaman, 2007).

In many cases, basic business skill training should accompany the provision of micro loans to

improve the capacity of the poor to use funds (UN, 2005).

2.5 Microfinance Services in the World

The current global youth population is very large. Of the world’s more than 3 billion people

estimated to be under the age of 25, approximately 1.3 billion are between the ages of 15 and 24.

Just under half of these young people live on less than two dollars a day, as estimated by the UN

(Youth Save, 2010). Yet young people the world over are aware of the inequities of the global

system, which leaves them vulnerable in many ways. Unemployment, especially amongst them,

also leads to high risk behavior – crime, drugs and spread of HIV/AIDs. Moreover in line with

most cultures in developing countries, the employed have to look after the unemployed extended

family members, thereby reducing their ability to save and opportunities for wealth creation that

is needed to spur economic growth. To this end, microfinance, the provision of a wide range of

financial services, has proved immensely valuable to poor people, especially the youth and

women on a sustainable basis. Access to financial services has allowed many families throughout

the developing world to make significant progress in their own efforts to escape poverty

(Onuman, 2005). The provision of credit has increasingly been regarded as an important tool for

raising the incomes of youths, mainly by mobilizing resources to more productive uses. As

development takes place, one question that arises is the extent to which credit can be offered to

the youths to facilitate their taking advantage of the developing entrepreneurial activities. The

generation of self-employment in non-farm activities for example, requires investment in

working capital. However, at low levels of income, the accumulation of such capital may be

difficult. Under such circumstances, loans, by increasing family income, can help the youth to

accumulate their own capital and invest in employment-generating activities (Schreiner, 2010).

2.6 Microfinance Services in Africa

Many diverse institutional models of micro financing are functioning in Africa, but most clients

are served by credit unions and co-operatives members sell (e.g. coffee, tea, cotton etc.) or the

nature of their employment (Onuman, 2005). In West and Central Africa however, savings and

credit cooperatives are generally more community-based. In contrast to Asia, the lack of

population density means that rural and agricultural finance is particularly challenging, and thus

many MFIs are urban-based and focused. Perhaps as a result the July 2003 Micro Banking

Bulletin identified only 8 sustainable institutions and estimated that only around 25 million

clients are being served throughout the continent. However, these numbers may under-estimate

or ignore the large numbers being served by cooperatives and postal banks. Nonetheless both

international and domestic banks are starting to take an interest in the potential of the low-

income market in Africa. The last twenty years have seen significant improvements in micro

financing through advances in understanding and providing financial services to better advance

development and eradicate poverty. This includes providing the financial means to save, access

credit, and start small businesses, with the potential to enhance community development, as well

as local and national policy making.

2.7 Impact of Microfinance

Microfinance institutions offer several services to their clients who in most cases are the

economically less privileged. According to Bennett (1994) and Ledgerwood (1999) microfinance

clients who are mostly men and women slightly below or above the poverty line can be able to

access variety of products and services which are mostly financial. Microfinance institutions

offer services to the low income earning groups because these groups are ignored by large

financial institutions since they are considered less profitable. Olaitan (2001) and Akanji (2001)

argue that products and services that make microfinance institutions different from large

financial institutions include increased provision of credit, increased provision of savings,

repositories and other financial services to low income earners or poor households.

The impact of microfinance can be described in a triangle where it has effect on financial

sustainability, outreach to the poor, and institutional performance/impact.

2.8 Microfinance and its impact in development

Microfinance has a very important role to play in development according to proponents of

microfinance. UNCDF (2004) states that studies have shown that microfinance plays three key

roles in development. It:

♦ helps very poor households meet basic needs and protects against risks,

♦ is associated with improvements in household economic welfare,

♦ helps to empower women by supporting women’s economic participation and so promotes

gender equity.

Otero (1999) illustrates the various ways in which “microfinance, at its core combats poverty”.

She states that microfinance creates access to productive capital for the poor, which together

with human capital, addressed through education and training, and social capital, achieved

through local organization building, enables people to move out of poverty (1999). By providing

material capital to a poor person, their sense of dignity is strengthened and this can help to

empower the person to participate in the economy and society (Otero, 1999). The aim of

microfinance according to (Otero 1999) is not just about providing capital to the poor to combat

poverty on an individual level, it also has a role at an institutional level. It seeks to create

institutions that deliver financial services to the poor, who are continuously ignored by the

formal banking sector. (Littlefield & Rosenberg 2004) states that the poor are generally excluded

from the financial services sector of the economy so MFIs have emerged to address this market

failure. By addressing this gap in the market in a financially sustainable manner, an MFI can

become part of the formal financial system of a country and so can access capital markets to fund

their lending portfolios, allowing them to dramatically increase the number of poor people they

can reach (Otero, 1999).while acknowledging the role microfinance can have in helping to

reduce poverty, concluded from their research on microfinance that “most contemporary

schemes are less effective than they might be” (1996). They state that microfinance is not a

panacea for poverty-alleviation and that in some cases the poorest people have been made worse-

off by microfinance. (Rogaly 1996) finds five major faults with MFIs. He argues that:

♦ They encourage a single-sector approach to the allocation of resources to fight poverty,

♦ Microcredit is irrelevant to the poorest people,

♦ an over-simplistic notion of poverty is used,

♦ there is an over-emphasis on scale,

♦ there is inadequate learning and change taking place.

2.9The impact of microfinance on poverty

There is a certain amount of debate about whether impact assessment of microfinance projects is

necessary or not according to (Simanowitz 2001). The argument is that if the market can provide

adequate proxies for impact, showing that clients are happy to pay for a service, assessments are

a waste of resources (ibid.). However, this is too simplistic a rationale as market proxies mask

the range of client responses and benefits to the MFI (ibid.) Therefore, impact assessment of

microfinance interventions is necessary, not just to demonstrate to donors that their interventions

are having a positive impact, but to allow for learning within MFIs so that they can improve their

services and the impact of their projects (Simanowitz, 2001). Poverty is more than just a lack of

income. (Wright 1999) highlights the shortcomings of focusing solely on increased income as a

measure of the impact of microfinance on poverty. He states that there is a significant difference

between increasing income and reducing poverty (1999). He argues that by increasing the

income of the poor, MFIs are not necessarily reducing poverty. It depends what the poor do with

this money, often times it is gambled away or spent on alcohol (1999), so focusing solely on

increasing incomes is not enough.

2.10.0 Islamic in microfinance

2.10.1 Mudarabah

Mudarabah has the potential to be adapted as Islamic microfinance scheme. Mudarabah is where

the capital provider or microfinance institution (rabbul mal) and the small entrepreneur

(mudarib) become a partner. The profits from the project are shared between capital provider and

entrepreneur, but the financial loss will be borne entirely by the capital provider. This is due to

the premise that a mudarib invests the mudarabah capital on a trust basis; hence it is not liable for

losses except in cases of misconduct. Negligence and breach of the terms of mudarabah contract,

the mudarib becomes liable for the amount of capital.Mudarabah structure could be based on a

simple or bilateral arrangement where Islamic bank provides capital and the micro-entrepreneur

acts as an entrepreneur.Mudarabah structure may also be based on two-tier structure or re-

mudarabah where 3 parties i.e. capital provider (public, government, zakat, waqf etc.),

intermediate mudarib (Islamic Bank) and final mudarib (micro entrepreneur).The profit-sharing

ratio on mudarabah is pre-determined only as a percentage of the businessprofit and not a lump

sum payment. The profit allocation ratio must be clearly stated and must be on the basis of an

agreed percentage. Profit can only be claimed when the mudarabah operations make a profit.

Any losses must be compensated by profits of future operations.After full settlement has been

made, the business entity will be owned by the entrepreneur. The entrepreneur will exercise full

control over the business without interference from the Islamic bank but of course with

monitoring. On the practical side, there is a problem to determine the actual total profit to be

shared because micro entrepreneurs normally do not have proper accounts or financial statement

(Dhumale & Sapcanin 1999).Meanwhile, muzara’ah is a form of mudarabah contract in farming

where Islamic bank can provide land or monetary capital for farming product in return for a

share of the harvest according to the agreed profit sharing ratio. In the context of microfinance,

the capital provider may need huge capital and expertise to manage such initiative and may need

to manage higher risk because the Islamic bank need to involve directly in the farming sector

through provision of asset such as land.In the case of mudarabah, the Islamic bank may face

capital impairment risk as loss makingoperations of micro entrepreneurs expose the Islamic bank

to the risk of capital erosion. In addition, since in mudarabah the Islamic bank should not request

collateral may expose Islamic bank to credit risk on these transactions. As part of risk mitigation,

even though the entrepreneur exercises full control, Islamic bank can still undertake supervision

(Iqbal & Mirakhor 1987).

2.10.2 Musharakah

Musharakah can also be developed as a micro finance scheme where Islamic bank will enter into

a partnership with micro entrepreneurs. If there is profit, it will be shared based on pre-agreed

ratio, and if there is loss, it will then be shared according to capital contribution ratio.

The most suitable technique of musharakah for microfinance could be the concept diminishing

partnership or musharakah mutanaqisah.

Musharakah Mutanaqisah

A: (Islamic Bank 80%) B: (Micro Entrepreneur 20%)

Another form of Musharakah is musaqat. Musaqat is a profit and loss sharing partnership

contract for orchards. In this case, the harvest will be shared among all the equity partners

(including entrepreneur as a partner) according to the capital contributions. All the Musharakah

principles will be applicable for this form of Musharakah.

This scheme, however, could be of high risk, since it needs the capital and expertise to directly

involve in the business especially in managing the orchards. Musharakah capital may also be

subjected to capital impairment risk, where the capital may not be recovered, as it ranks lower

than debt instruments upon liquidation (Haron & Hock 2007).

The normal risk mitigation techniques that can be adopted by Islamic banks are also applicable

in the case of microfinance i.e. through a third-party guarantee. This guarantee can be obtained

and structured for the loss of capital of some or all partners through the active role of the so

called Credit Guarantee Corporation (CGC) as practiced in the case of SME financing in

Malaysia.

2.10.3 Murabahah

Using murabahah as a mode of microfinance requires Islamic bank to acquire and purchase asset

or business equipment then sells the asset to entrepreneur at mark-up. Repayments of the selling

price will be paid on installment basis. The Islamic bank will become the owner of the asset until

the full settlement. This scheme is the most appropriate scheme for purchasing business

equipment. This mode of financing has already been introduced in Yemen in 1997.

In 1999, there are more than 1000 active borrowers [Dhumale & Sapcanin 1999]. Borrowers

must form a group of 5 micro entrepreneurs where all members will act as guarantor if there is

default among their group members. The benefit of this mode of financing is continuous

monitoring, and entrepreneurs with a good reputation of repayment will be offered extra loan

found to be more practical and most suitable scheme for Islamic microfinance to be provided by

Islamic banks. This is due to the fact that the buy-resell model which allows repayments in equal

installment is easier to administer and monitor. The above diagram indicates the application of

the extended concept of murabahah i.e. Murabahah to the Purchase Orderer. This is where a

micro-entrepreneur enters into a sale and purchase agreement, or memorandum of understanding

to purchase a specific kind of goods or equipments needed by the micro-entrepreneur with the

Islamic bank.

The Islamic bank then sells the goods to the entrepreneur at cost plus mark-up, and entrepreneur

can pay back later in lump sum or by installments (bai muajal). A number of shari’ah principles

must be met for the contract to be valid (Haron & Hock 2007).

Such as the goods must in existence at the time of sale; ownership of the goods must be with the

bank; the goods must have the commercial value; the goods are not be used for a “haram”

purpose; the goods must be specifically identified and known; the delivery of goods is certain

and not conditional upon certain other events; and, the selling price is fixed at cost plus mark up

Murabahah could be easily implemented for microfinance purposes and can be further

exemplified by the used of deferred payment sale (bai’ al-muajal). Murabahah, however, May

expose Islamic bank as in the case conventional lending to credit risk.

This, however, can be mitigated by requesting for an urboun, a third party financial guarantee, or

pledge of assets. In addition, Islamic bank can also institutes direct debit from the entrepreneur’s

account, centralizes blacklisting system, and minimum non-compounded penalty to deter

delinquent entrepreneurs. Murabahah to the Purchase Ordered also exposes Islamic banks to

delivery risk where goods are not delivered, goods not delivered on time, or goods delivered not

according to specification by the entrepreneur after payment is made by the Islamic bank. To

mitigate delivery risks, Islamic bank may request a performance guarantee from the seller to give

assurance on the delivery of goods.

2.10.4 Ijarah

Ijarah by definition is a long term contract of rental subject to specified conditions as prescribed

by the shari’ah. Unlike conventional finance lease, the less or (Islamic bank) not only

owned the asset but takes the responsibility of monitoring the used of asset and discharges its

responsibility to maintain and repair the asset in case of mechanical default those are not due to

wear and tear.

Ijarah Muntahia Bitamleek is an elaborate concept of ijarah where the transfer of ownership

will take place at the end of the contract and pre-agreed between the lessor and the lessee. The

title of the asset will be transferred to the lessee either by way of gift, token price and pre-

determined price at the beginning of the contract or through gradual transfer of ownership.

Ijarah Muntahia Bitamleek is more suitable for micro finance scheme especially for micro

entrepreneurs who are in need of assets or equipments. Islamic bank will purchase the assets

required by the entrepreneurs and rent the assets to qualified entrepreneurs.

In this case, the entrepreneurs can just rent the asset over a period of time and pay the rentals at

regular intervals. The entrepreneur as a lessee will be responsible to safeguard the asset whereas

the lessor will monitor their usage. For ijarah, the Islamic bank may be exposed to settlement risk

where the entrepreneur as a lessee is unable to service the rental as and when it falls due.

Similarly, the Islamic bank can request an urboun from the entrepreneur which can also be taken

as an advance payment of the lease rental. Alternatively, the Islamic bank as the owner of the

asset should has the right to repossess the asset.

2.10.5 Qard Al hasan

Qard al-hasan or interest free loan is one of the most advanced and suitable tools for

microfinance purposes. In principle, “Qard al-hasan” is a kind of borrowing of money that lender

does not have any expectation from borrower except the receiving the principle. In fact, Muslims

would use“Qardhul al-hasan” to help one another when they need financial help in order to

please Allah (Mirakhor & Iqbal, 2007). The only different between” Qard al-

hasan” and sadaqahis that sadaqah is pure charity and the giver does not have any expectation of

money but in qard al-hasan borrower must return back the principle within the agreed period of

time (Mirakhor & Iqbal, 2007).Qard al-hasan can be used as an instrument to provide fund for

micro financing to support small business and start-ups as it is less expensive compared to other

source of Islamic finance. The term of repayment can be agreed by installment in the certain

agreed period of time. The only extra charge for qard al-hasan is the service charge fee that

micro-finance institution is allowed to receive (Mirakhor & Iqbal, 2007).

2.11 Kaaba microfinance

Kaaba Micro finance Institution’s (K-MFI) is a financial service provider that aims to strengthen

the economic base of the low-income women and youth in Somaliland through loans and savings

service. The institution offers different kinds of help and combines cost-efficient methodologies

with a very high level of customer service.

K-MFI has been operating under Doses of Hope Foundation (DHF) a non-governmental

development foundation operating in Somaliland since 1998. The first micro finance began in

1999 micro finance project with 150 women beneficiaries; from 1999 to 2007 the microfinance

program has directly reached out 7000 beneficiaries, and has indirectly benefited another 38,000

out of which 80% are low-income women and youth. In partnership with Oxfam Novib, DHF

has in 2008 begun the transformation of the microfinance program into an independent

microfinance institution now known as Kaaba Micro finance institution (K-MFI).

The transformation process started with a seed capital of Euro 150,000 from Oxfam Novib and

culminated in the legal existence of K-MFI as a separate organization with its own registration,

management and structure in 2009. Since then K-MFI has gone through profound transformation

and has accessed financial services to 5076 clients from 2010 & 2013 alone, which is more than

double of its 2008 & 2009 of 1559 clients, thus fulfilling its overall objective to empower its

clients economically, and to contribute positively to the high unemployment rate of the country

through self-employment opportunities. K-MFI’s main goal is to provide financial services

primarily to the low-income women and youth in Somaliland to become self-reliant and serve as

agents of change in their respective communities. (Kaaba 2013).

2.12 What is meant by Job Creation?

Job creation is difficult to evaluate because it is difficult to measure. This report attempts to

survey a wide range of job creation strategies that policy makers can implement during times of

economic recession. The proverbial golden egg of job creation policies is the “net new job”—the

job that is created without displacing any other economic activity. While it is easy enough to

measure whether a new job has been created at the macroeconomic scale by looking at aggregate

data from the Bureau of Labor Statistics, it is very difficult to determine if

(1) The jobs created didn’t merely displace jobs in other locations or sectors, and

(2) If the jobs were created because of a specific policy. Throughout this report, this dilemma

emerges frequently; the theoretical mechanism for how a policy creates jobs may be well

understood, but data showing that it actually did create net new jobs is ambivalent at best or,

more commonly, simply nonexistent.

The process by which the number of jobs in an economy increases, Job creation often refers to

government policies intended to reduce unemployment. Job creation programs may take a

variety of forms. For example, a government may lower taxes and reduce regulation to make

hiring less expensive. On the other hand, a government may hire workers itself, for example, to

build a road.

2.13 Advantages of job creation

Shifting the focus to job creation has four advantages:

Employment is much easier to measure than unemployment. Measuring unemployment

involves subtle distinctions between individuals who are in the labor force and those

who are not: those counted as unemployed must say they are actively looking for a job;

yet in high-unemployment countries in particular, so-called discouraged workers stop

looking for work and remain uncounted. Conversely, many who claim to be looking

for work may be half-hearted about it, the more so as their prospects dwindle.

A second reason for trying to understand job creation better is that for any given level

of unemployment, faster job creation increases a country's output, and, among other

things, raises the ratio of workers to pensioners, thereby lowering the cost of its social

safety net.

Third, the insights gained from studying unemployment do not necessarily hold up

when the focus shifts to job creation. For example, laws, programs, or labor

agreements making it relatively difficult or expensive to lay off workers seem to have

no effect one way or the other on the unemployment rate. However, strong systems of

job protection appear to have a big effect in holding down job creation.

Finally, analyzing employment growth instead of experience with unemployment

offers richer results. Data on unemployment, for example, tell us nothing about the

kinds of jobs available in the workplace, or the terms under which workers hold them,

such as whether they are permanent or temporary, or full-time as opposed to part-time.

A look at these factors lets us assess, among other things, whether faster job creation in

the United States than in Continental Europe comes from historical conditions, such as

a much lower proportion of farm jobs or traditional manufacturing jobs, which have

been stagnant or declining in all advanced countries. This approach can also examine

the effects of women entering the workforce in larger numbers in recent years, and can

shed light on important policy questions, such as whether promoting part-time work

leads to higher overall job creation or merely cannibalizes full-time jobs.

2.14 The role of the public sector in Job creation

The current debates on job creation focus on various policy measures that essentially add up to

attempts to tinker with the market in a capitalist system, hoping to unlock resources and open up

initiatives for creating employment. Whilst such attempts are not too he dismissed, we should be

mindful of their shortcomings.

Public sector

The only source of capital reserves great enough to make a significant dent in the unemployment

statistics of our country, apart from what is in the hands of the largest capitalist enterprises lies

with the state. The public sector, which includes the parastatals, the public service and local

government, already makes up almost 50% of the economy. The crisis of the public sector is well

documented, but to argue that privatization and contracting out are measures that will assist in

solving this crisis is simply ridiculous. All this will lead to is reduced employment levels, and

will thus add to the burden of the government in terms of job creation.

Measures to reform the public sector must include:

Policy to reform the running state enterprises; and

Policy to inform the transformation of the public service and local government

administration

2.15 The Role of the Private Sector

Improving employment opportunities for young people requires a broad and concerted effort

from all stakeholders. While governments are primarily responsible for creating an enabling

environment for youth employment, employers – as major providers of jobs, and workers – as

direct beneficiaries, have an important role in the process. Action by employers and their

organizations to support youth employment can take several forms, which varies across countries

depending on national circumstances. These include:

2.16.1 Direct action concerning skills development and training

Employers and their organizations have a central role in the identification (and subsequent

design and implementation) of the appropriate education, training and general skills requirements

that economies need. Business has a clear interest in ensuring that education and training creates

the skilled labour force they will need for the future. As key customers of the education and

training system, business can help inform policy and practice across a variety of related issues.

Traditionally a great deal of efforts of employers worldwide have focused on equipping school

leavers, first-time jobseekers and young unemployed with the technical skills and attitudes that

are required from them to become more “employable” or “suitable” for the labour market.

Examples of interventions by employers in this area include:

Enterprises’ participation in national vocational training systems and training

programmers through interventions aimed at facilitating the transition of young people to

the world of work (e.g. enterprise-based training)

Measures to increase the number and scope of training opportunities for young people

within the private sector (e.g. campaigns geared towards businesses to create or expand

training places; joint efforts by employers and educational authorities to increase

vocational training places and apprenticeship places in enterprises)

Special training schemes organized by employers, individually or collectively, outside the

framework of national training systems in order to generate the skills required by a

specific industry or company, including schemes targeting disadvantaged youth.

Establishment of school-industry partnership arrangements in order to enhance the

relevance of education and easing young people transition from school to work (e.g.

workplace learning initiatives within the educational framework) (Anderson,2005)

2.16.2 Direct actions concerning job creation

Private sector growth is a key engine of job creation and more than ad hoc measures are required

to enable employers to create jobs for young people on a sustainable basis. In many countries,

however, employers, often through their organizations, are also implementing or pioneering a

number of initiatives to expand job opportunities for young workers, and to facilitate their

integration into the labour market. Examples of action in this area include:

Job facilitation and placement schemes to match young jobseekers with job offers from

companies (e.g. a job bank by an organization)

Use of government programmers’ and incentives to create new jobs for young people

(e.g. a Fund)

Mentoring of young entrepreneurs and business start-up assistance

Establishment of young entrepreneurs’ networks or support to ease access to enterprise

networks

2.16.3. Policy making and advocacy

The participation of employers and their organizations in the design, implementation and

evaluation of policies and programmers’ for youth employment has proven critical for enhancing

the relevance of interventions and make them more respondent to labour market requirements.

Employers, through their organizations, can also play an important role in raising-awareness,

generating and disseminating information, and mobilizing support around youth employment

issues. Some actions undertaken by employers in this regard include:

Participation in national tripartite policy-making bodies dealing with vocational

education and training and job creation (e.g. boards of educational and training

institutions; funding bodies for grant allocation to young entrepreneurs)

Contribution to policy and programmer’s development and implementation through

social dialogue and collective bargaining

Research into and dissemination of information on youth employment issues,

specifically with regard to private sector needs concerning skills and job requirements.

Promotional campaigns and other initiatives targeting different groups depending on

circumstances (e.g. young people, parents, schools, industry partners, etc.) using tools such as

advertisements, radio spots, television chat shows, videos, newspaper articles, job fairs In the

real word, action in each of the three main areas highlighted above is often intertwined, as the

examples contained in this tool show.

2.17 SOCIAL AND ECONOMIC BENEFITS OF JOB CREATION

2.17.1 Job creation is the best weapon in the battle against poverty. Unemployment is a major cause of poverty. Those who are unemployed are much more likely to be living

below the poverty line. Job creation is the best antidote for poverty—as cited above, it support saving,

diminishes debt accumulation, and supports spending.

2.17.2 Job creation improves income distribution and reduces inequality.

There is a direct relation between unemployment and inequality. Job creation promises to improve

income distribution and reduce inequality. The social benefits of decreased inequality have been well-

documented. Of particular significance are the ways in which inequality makes everyone worse off,

including the rich. Increased inequality can threaten democratic institutions and damage social cohesion.

Even the symbolic value of job creation at this time should not be underestimated.

2.17.3 Job creation can improve conditions and promote investment in the

poorest communities.

Job creation can result in improved economic and social conditions in the poorest areas. It is known that

low-wage workers tend to live in poorer communities and spend a larger portion of their income locally.

Thus, job creation will result in increased spending in the neediest regions, which can further increase

employment where unemployment is the highest and most burdensome. Lowering poverty rates will

increase the inducement to invest in poor neighborhoods, with a positive impact on economic and social

conditions.

2.17.4 Job creation can stimulate output, income, consumption and

Investment. Unemployment means lower output, income, consumption and investment. Job creation will increase

output and income, which will result in more consumption spending, and ultimately increase the

inducement to invest.

2.17.5 Job creation supports public and social goods and services.

As already stated, unemployment decreases tax revenues and puts extra demands on government

budgets as well as private agencies, resulting in less public and social goods and services. This

includes fewer people employed in these types of positions. By supporting healthy government

budgets, job creation supports public and social goods and services. In addition, some of the new

jobs can (and should!) directly support such services.

Chapter three

Research Methodology

3.0Variable defections

Microfinance is the provision of savings accounts, loans, insurance, money transfers and other

banking services to customers that lack access to traditional financial services, usually because of

poverty. Making small loans to individuals who lack the necessary resources to secure traditional

credit is known as microcredit.

Job creation the process by which the number of jobs in an economy increases. Job creation

often refers to government policies intended to reduce unemployment. Job creation programs

may take a variety of forms. For example, a government may lower taxes and reduce regulation

to make hiring less expensive. On the other hand, a government may hire workers itself, for

example, to build a road.

3.1Research design

The study will engage a descriptive correlation? Design in order to describe the role of

microfinance in job creation in Somaliland small and medium sized microfinance institutions

mainly in Hargeisa. This design is chosen because it will be easier and less time to the

researchers. Descriptive correlation research? Is popular in social science enables to show the

relationship between the variable of the study (dependent variable and in dependents variable).

Therefore, this design deeply interacts in describing the respondents in a form of qualitative and

quantitative approaches. This research will be analyzed in quantitative method and qualitative

method as well, because quantitative method is more objective in measuring data as

comprehensive way in forms of graphical methods.

3.2 Research population

The target population of this study will be 20 from the KAABA microfinance institution and

University of Hargeisa; these are project managers which this study directly affects, 9 of the

target population will be managers and workers, Also, a portion of this target population of 10

will be the students that study in the University of Hargeisa, where social development projects

are implemented, including local microfinance institutions.

The target population used in this study was drawn out the reports of KAABA microfinance

institutions and University of Hargeisa.

3.3 Sampling Technique

Systematic sampling technique will be employed when selecting respondents of this study. In the

University of Hargeisa and KAABA microfinance institution, the researcher will select one out

of every five students who cross the main gate of the University of Hargeisa, and the KAABA

microfinance the researcher will select one out of every two workers or managers.

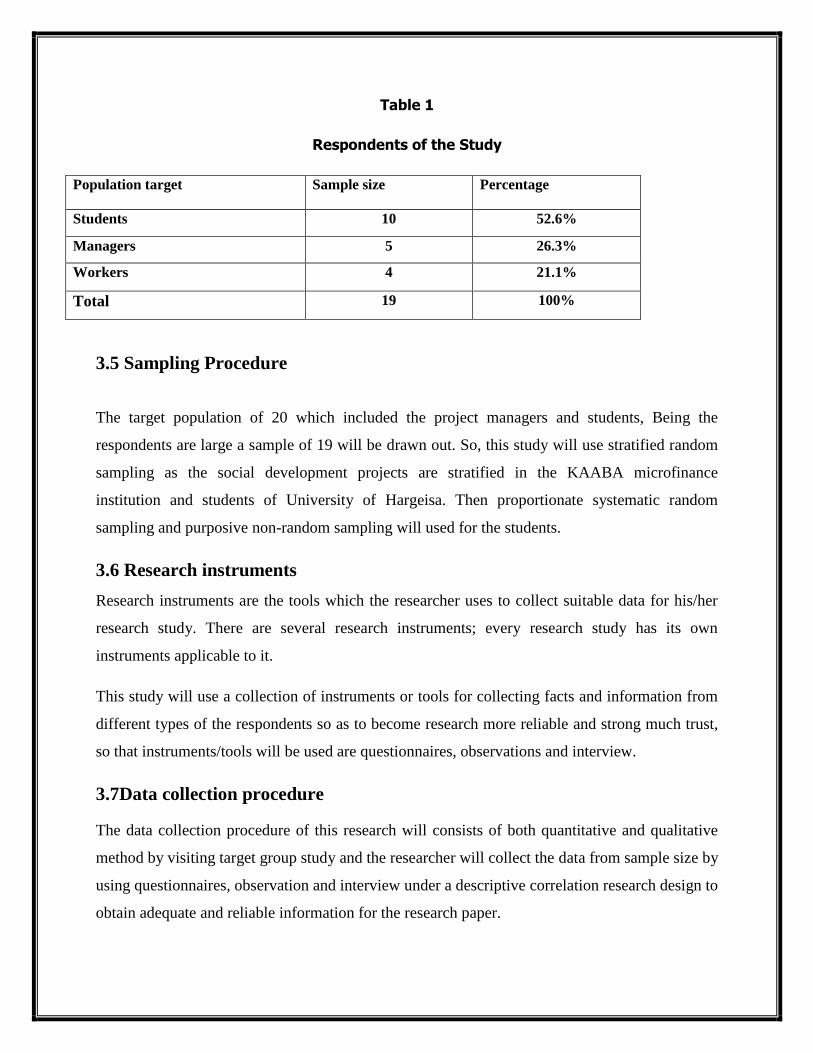

3.4Sample Size

As the target populations of the study were many, a sample will be chosen from each category of

the population Table 1 below shows the respondents of the study with the following categories:

target population and sample size, percentage. The Slovenes formula is used to determine the

minimum sample size.

)(1 2eN

Nn

Where:

n = the required sample size

N = the known population size &

e = the level of significance (Which is given = 0.05)

Table 1

Respondents of the Study

Population target Sample size Percentage

Students 10 52.6%

Managers 5 26.3%

Workers 4 21.1%

Total 19 100%

3.5 Sampling Procedure

The target population of 20 which included the project managers and students, Being the

respondents are large a sample of 19 will be drawn out. So, this study will use stratified random

sampling as the social development projects are stratified in the KAABA microfinance

institution and students of University of Hargeisa. Then proportionate systematic random

sampling and purposive non-random sampling will used for the students.

3.6 Research instruments

Research instruments are the tools which the researcher uses to collect suitable data for his/her

research study. There are several research instruments; every research study has its own

instruments applicable to it.

This study will use a collection of instruments or tools for collecting facts and information from

different types of the respondents so as to become research more reliable and strong much trust,

so that instruments/tools will be used are questionnaires, observations and interview.

3.7Data collection procedure

The data collection procedure of this research will consists of both quantitative and qualitative

method by visiting target group study and the researcher will collect the data from sample size by

using questionnaires, observation and interview under a descriptive correlation research design to

obtain adequate and reliable information for the research paper.

3.8 Data analysis

The study will use quantitative data analysis at the end of each section; the data will be

summarized in one of the major appropriate applications, SPSS (Scientific Package for Social

Science). Also the data will be displayed in a calculated table and percentages as statistics

approaches the method of analyze the research strongly show descriptive relationship between

the variables of the study.

3.9 Ethical issues of the study

The study will take into account some of the following ethical issues which would lead the

researcher to be disqualified from conducting the research. Firstly, the issue of plagiarism, fraud,

confidentiality, voluntary consent among others was keenly observed by the researcher so that

the research conducted would be of value to the researcher and also the information obtained to

be of significant to the public in general.

Chapter Four

4.0 Data Analysis and interpretation

4.1 Introduction

This chapter explains analysis of the collected information and it concerned the questionnaires

and interviews that the researcher collect from the respondents during the data collection and it

shows in tables and graphs which is pie chart, par chart, the tables will contain numbers as well

as percentage of the alternative, and interpretation will be evaluating the finding and comparing

the results.

The questionnaires of this chapter are 20 questions and it mainly focuses on the role of

microfinance in employment creation there are 4 questions which have not directly related the

topic and the researcher didn’t illustrate as a table or graph because it does not give a more sense

about the topic and the analysis are as follows.

1. Gender of respondents

Shows that 58% of the respondents were male where as 42% of the respondents were female;

this shows that my questionnaires mostly were distributed male due to the randomly selected

method.

2. Age of the respondents

The respondent answered in different ages which are between 58% less than 25yrs, where 26-

35yrs.is 16%, were is 10% 36-45yrs, over 56yrs 10% and 5% 46-55yrs.

3. Marital Status

53% of the respondents were single and 47% were married, the most of respondents answered

single.

4. Level of Educations

58% of the respondents were university level where as 37% of the respondents were secondary

level. While the remaining respondents are others 5%

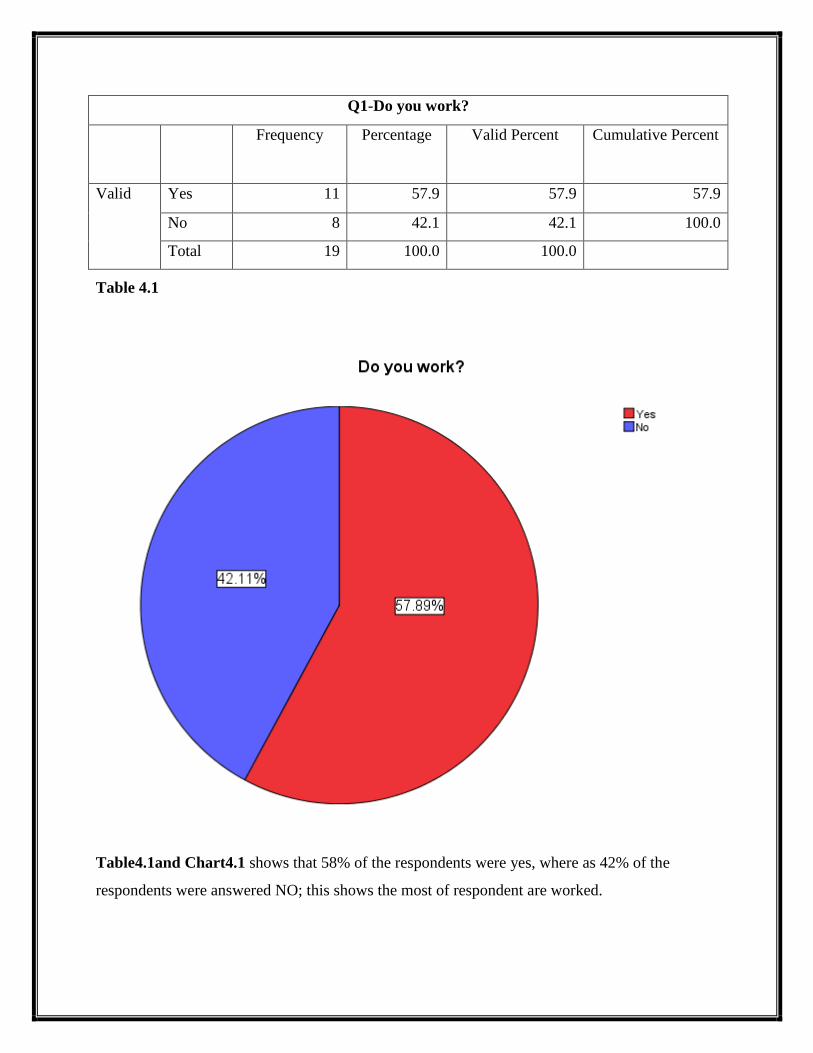

Q1-Do you work?

Frequency Percentage Valid Percent Cumulative Percent

Valid Yes 11 57.9 57.9 57.9

No 8 42.1 42.1 100.0

Total 19 100.0 100.0

Table 4.1

Table4.1and Chart4.1 shows that 58% of the respondents were yes, where as 42% of the

respondents were answered NO; this shows the most of respondent are worked.

Q2-Do you take enough salary?

Frequency Percentage Valid Percent Cumulative Percent

Valid Yes 9 47.4 47.4 47.4

No 10 52.6 52.6 100.0

Total 19 100.0 100.0

Table 4.2

This above chart and table 4.2 explains that 47% of the respondents answering Yes that they

take enough salary, where as 53% of the respondents were answering No they are not taking

enough salary. This means that mostly of the people are not taking enough salary.

Q3-what is your work?

Frequency Percentag

e

Valid Percent Cumulative

Percent

Valid manager 3 15.8 15.8 15.8

assistance 3 15.8 15.8 31.6

work 6 31.6 31.6 63.2

Others (please specify) 7 36.8 36.8 100.0

Total 19 100.0 100.0

Table 4.3

As the table and chart 4.3 above shows the respondents as managers16%, while 16% assistance,

where as 31% work and the remaining 37% were answering others, which means not work.

What is your level of experience?

Frequency Percent Valid Percent Cumulative

Percent

Valid Less than one year 7 36.8 36.8 36.8

1-3yrs 7 36.8 36.8 73.7

4-5yrs 2 10.5 10.5 84.2

over8yrs 3 15.8 15.8 100.0

Total 19 100.0 100.0

Table 4.4

As the table and chart 4.4 above shows that 8 respondents equivalent 42% less than one year

experience, while 6 respondents equivalent 32% answered 1-3yrs, where as 2 respondents

equivalent11% answered 4-5yrs, and 3 respondents 15% were answering over 8ys experience.

The most of respondents answered less than one year.