revenue and Expense: Recognition - David Bean, GASB, John Stanford, IPSASB

22

Page 1 | Proprietary and Copyrighted Information Revenue and Expense: Recognition David Bean Director of Research and Technical Activities, GASB John Stanford Acting Technical Director, IPSASB The views expressed in this presentation are those of Mr. Stanford and Mr. Bean. Official positions of the GASB and IPSASB on accounting matters are reached only after extensive due process and deliberation.

-

Upload

oecd-governance -

Category

Government & Nonprofit

-

view

413 -

download

3

Transcript of revenue and Expense: Recognition - David Bean, GASB, John Stanford, IPSASB

Page 1 | Proprietary and Copyrighted Information

Revenue and Expense:

Recognition

David Bean

Director of Research and Technical

Activities, GASB

John Stanford

Acting Technical Director, IPSASB

The views expressed in this presentation are

those of Mr. Stanford and Mr. Bean. Official

positions of the GASB and IPSASB on

accounting matters are reached only after

extensive due process and deliberation.

Page 2 | Proprietary and Copyrighted Information

• IPSAS 9, Revenue from Exchange Transactions

• IPSAS 11, Construction Contracts

• IPSAS 19, Provisions, Contingent Liabilities and

Contingent Assets

• IPSAS 23, Revenue from Non-Exchange Transactions

(Taxes and Transfers)

IPSASs Potentially Affected

Page 3 | Proprietary and Copyrighted Information

• IPSAS 9 and 11 based on IASB equivalents (IAS 18 and IAS 11).

IASB has issued replacement IFRS 15 (new thinking)

– Consider extent to which performance obligation approach can be

applied in public sector

• IPSAS 19 does not provide specific guidance for non-exchange

expenses

– IPSAS 23 only addresses revenue

• Opportunity to more closely align revenue and expense

recognition guidance

Why Have These Projects Been Initiated?

Page 4 | Proprietary and Copyrighted Information

• Boundary issues between IPSAS 23 and other IPSASs

– Is a transaction considered to be exchange, non-exchange, or both?

• Difficulties in the application of IPSAS 23 and IPSAS 19

– When does a stipulation result in a liability?

– Where can specific guidance be found for non-exchange expenses?

• None of the issues raised are considered to be fatal flaws

Constituent Feedback

Page 5 | Proprietary and Copyrighted Information

Exchange vs. Non-Exchange

Public School Teacher

• Exchange

– Employment contract pays salary in exchange for

services

– Value exchanged is approximately equal

• Non-Exchange

– Benefits of services do not flow to resource

provider

– Value is not approximately equal

Page 6 | Proprietary and Copyrighted Information

Exchange vs. Non-Exchange

License

Non-Exchange Expenses

• A local government requires all motor

vehicles to be licensed and charges a

license fee of CU100 for each license

• The local government estimates that it

costs approximately CU97 to issue

each license

• The license is valid for one year from

the date of issuance

Page 7 | Proprietary and Copyrighted Information

Exchange vs. Non-Exchange

License

Non-Exchange Expenses

• Exchange

– Cost of the license of CU97 is approximately

equal to the amount paid for the license of

CU100

• Non-Exchange

– Value of the license may be difficult to

determine and some jurisdictions may not

know or capture the cost of the license

Page 8 | Proprietary and Copyrighted Information

Exchange vs. Non-Exchange

License for High-Value Vehicle

Non-Exchange Expenses

• Same license and same cost of CU97

• Different rate charged to vehicles that

are valued at over CU50,000

• Owners of those vehicles must pay

CU500 instead of CU100 for the one-

year license

Page 9 | Proprietary and Copyrighted Information

Exchange vs. Non-Exchange

License for High-Value Vehicle

Non-Exchange Expenses

• Amount paid and cost of license are

no longer approximately equal

• Classification as non-exchange,

even though it is the same license

Page 10 | Proprietary and Copyrighted Information

• Determining whether a stipulation is a condition or restriction a key step

– Stipulations without both a performance obligation and a return obligation (including timing

requirements) are restrictions

• Resources received in advance

– Condition—liability of recipient

– Restriction—revenue of recipient

• Concerns about the strictness of IPSAS 23 – is it providing relevant, faithfully

representative, understandable and comparable information?

IPSAS 23 Application Issues—Stipulations

Page 11 | Proprietary and Copyrighted Information

New Approach vs. Traditional Approach

Performance Obligations

Approach

Two broad approaches to recognition

Exchange and

Non-Exchange Approach

Page 12 | Proprietary and Copyrighted Information

Performance Obligation: The IFRS 15 Definition

• A promise to transfer distinct goods or services, or a series

of distinct goods or services that are substantially the

same and have the same pattern of transfer, to a customer

• Performance obligations are satisfied when (or as) control

of the goods or services is transferred to the customer

• Revenue is recognized when (or as) the performance

obligations are satisfied

Page 13 | Proprietary and Copyrighted Information

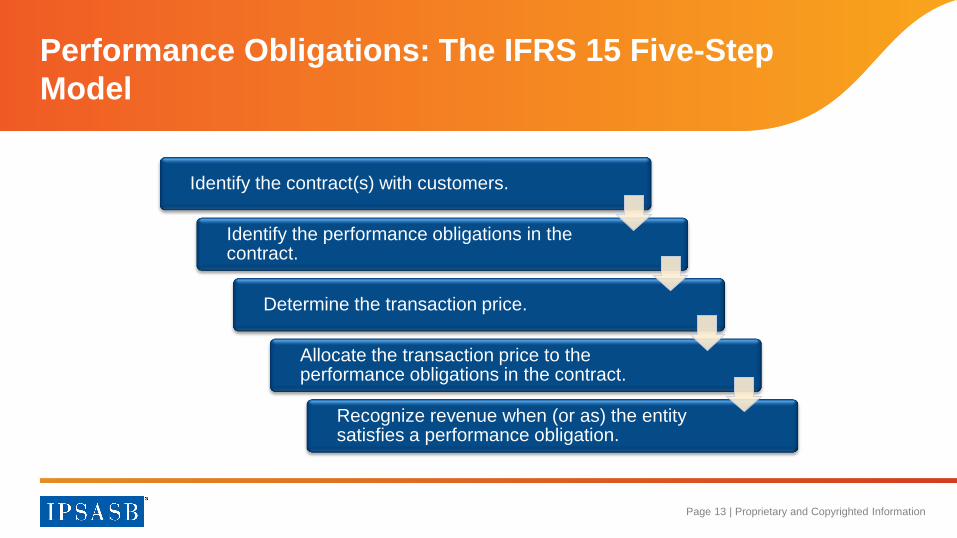

Performance Obligations: The IFRS 15 Five-Step

Model

Identify the contract(s) with customers.

Identify the performance obligations in the contract.

Determine the transaction price.

Allocate the transaction price to the performance obligations in the contract.

Recognize revenue when (or as) the entity satisfies a performance obligation.

Page 14 | Proprietary and Copyrighted Information

Applying the IPSAS 15 performance based approach

in the public sector

Page 15 | Proprietary and Copyrighted Information

Performance Obligation Approach

Transactions

With performance

obligations

With no performance

obligations

A modified IFRS 15

performance obligation

approach

IPSAS 23 modified to

address expenses and

current revenue issues

IPSAS 23—modified to

address revenue issues

IPSAS 19—modified to

address expense issues

Page 16 | Proprietary and Copyrighted Information

Applying the IPSAS 15 performance based approach

in the public sector

Break Out Session – Revenue: Performance obligations Approach and IPSAS 23 Issues

Page 17 | Proprietary and Copyrighted Information

Performance Obligation Approach

Advantages

• Continued alignment with IASB

• Reduces need to classify transactions as exchange or non-exchange

• In some cases identifying performance obligations straightforward so accounting

may be more understandable

Disadvantages

• Performance obligation approach developed by IASB for certain exchange

revenues (potential unintended consequences when applied to broader range of

revenue and expense)

• Could be trading one set of implementation issues for another set

• Still need to address transactions without performance obligations

Page 18 | Proprietary and Copyrighted Information

Exchange and Non-Exchange Approach

Transactions

Exchange

Revenue

Non-exchange

IFRS 15 performance

obligation approach

IPSAS 23 modified to

address expenses and

current revenue issues

IPSAS 23—modified to

address revenue issues

IPSAS 19—modified to

address expense issues

Page 19 | Proprietary and Copyrighted Information

Exchange and Non-exchange Approach

Advantages

• Familiar

• No fatal flaws

Disadvantages

• Classification of transactions as

exchange or non-exchange

• IPSAS 19—not consistent with

the conceptual framework-

recognition

• Challenges regarding treatment

of stipulations

Page 20 | Proprietary and Copyrighted Information

• Alignment with Social Benefits Guidance

– Definition and scope

• Social Benefits CP focus on ‘social risk’

– Non-exchange expense without a performance obligation

• Comments on Social Benefits consultation in IPSASB

Chairs

Other Challenges

Page 21 | Proprietary and Copyrighted Information

• Has the Board identified all of the viable alternatives?

• Are there any fatal flaws to the two approaches that have

been identified?

Feedback and discussion