Return on Knowledge Global Inflation-Linked Bonds 8 February 2011.

17

Return on Knowledge Global Inflation-Linked Bonds 8 February 2011

-

Upload

charlie-mallen -

Category

Documents

-

view

215 -

download

0

Transcript of Return on Knowledge Global Inflation-Linked Bonds 8 February 2011.

Return on Knowledge

Global Inflation-Linked Bonds8 February 2011

2

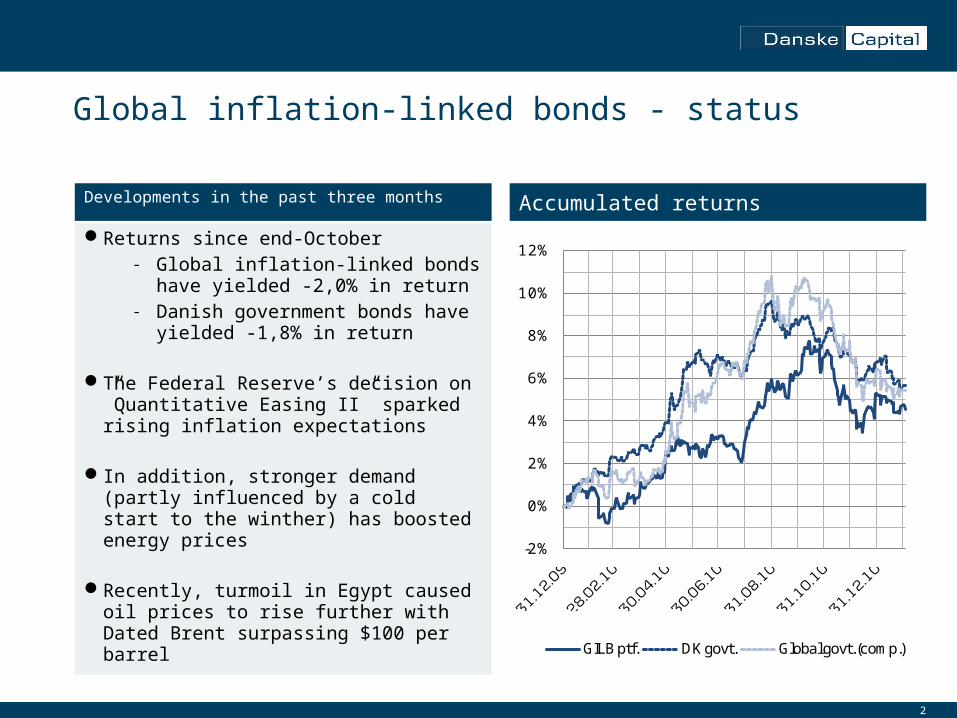

Global inflation-linked bonds - status

Developments in the past three months

Returns since end-October- Global inflation-linked bonds have

yielded -2,0% in return- Danish government bonds have

yielded -1,8% in return

The Federal Reserve’s decision on ”Quantitative Easing II” sparked rising inflation expectations

In addition, stronger demand (partly influenced by a cold start to the winther) has boosted energy prices

Recently, turmoil in Egypt caused oil prices to rise further with Dated Brent surpassing $100 per barrel

Accumulated returns

-2%

0%

2%

4%

6%

8%

10%

12%

GILB ptf. DK govt. Global govt. (comp.)

3

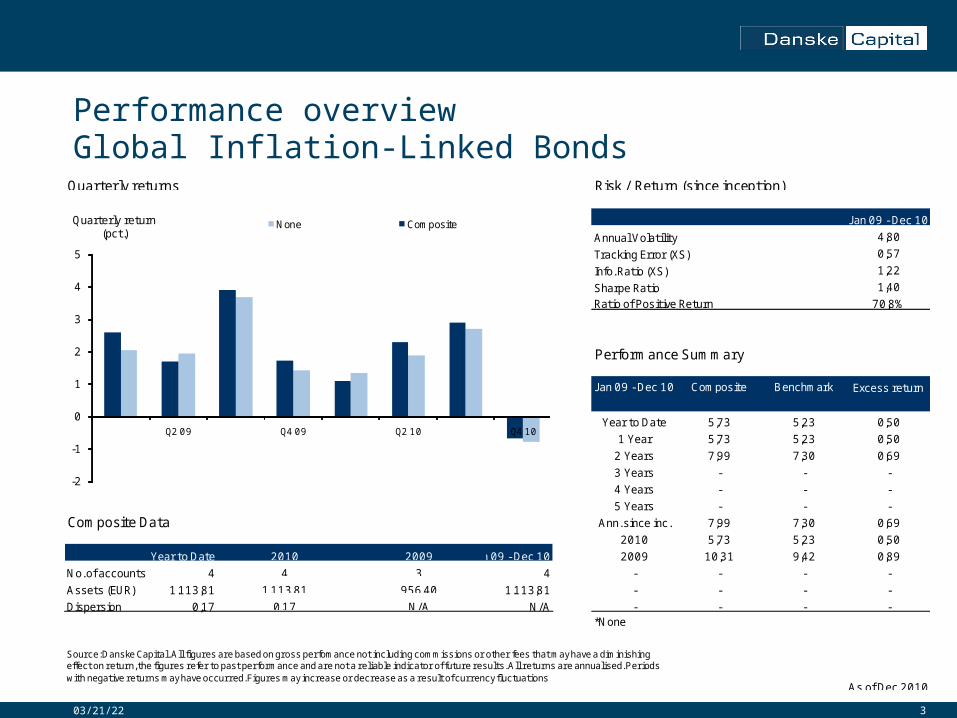

Performance overviewGlobal Inflation-Linked Bonds

04/18/23

J an 09 - Dec 10

Annual Volatility 4,80

Tracking Error (XS) 0,57

Info. Ratio (XS) 1,22

Sharpe Ratio 1,40

Ratio of Positive Return 70,8%

Performance Summary

Composite Return (EUR)

Benchmark return*

Excess return

Year to Date 5,73 5,23 0,50

1 Year 5,73 5,23 0,50

2 Years 7,99 7,30 0,69

3 Years - - -

4 Years - - -

5 Years - - -Composite Data Ann. since inc. 7,99 7,30 0,69

2010 5,73 5,23 0,50

Year to Date J an 09 - Dec 10 2009 10,31 9,42 0,89

No. of accounts 4 4 - - - -

Assets (EUR) 1.113,81 1.113,81 - - - -

Dispersion 0,17 N/A - - - -

2009

*None

Source: Danske Capital. All figures are based on gross perfomance not including commissions or other fees that may have a diminishing effect on return, the figures refer to past performance and are not a reliable indicator of future results. All returns are annualised. Periods with negative returns may have occurred. Figures may increase or decrease as a result of currency fluctuations

As of Dec 2010

Quarterly returns Risk / Return (since inception)

N/A0,17

J an 09 - Dec 10

1.113,81

4

2010

956,40

3

-2

-1

0

1

2

3

4

5

Q4 10Q2 10Q4 09Q2 09

Quarterly return (pct.)

None Composite

4

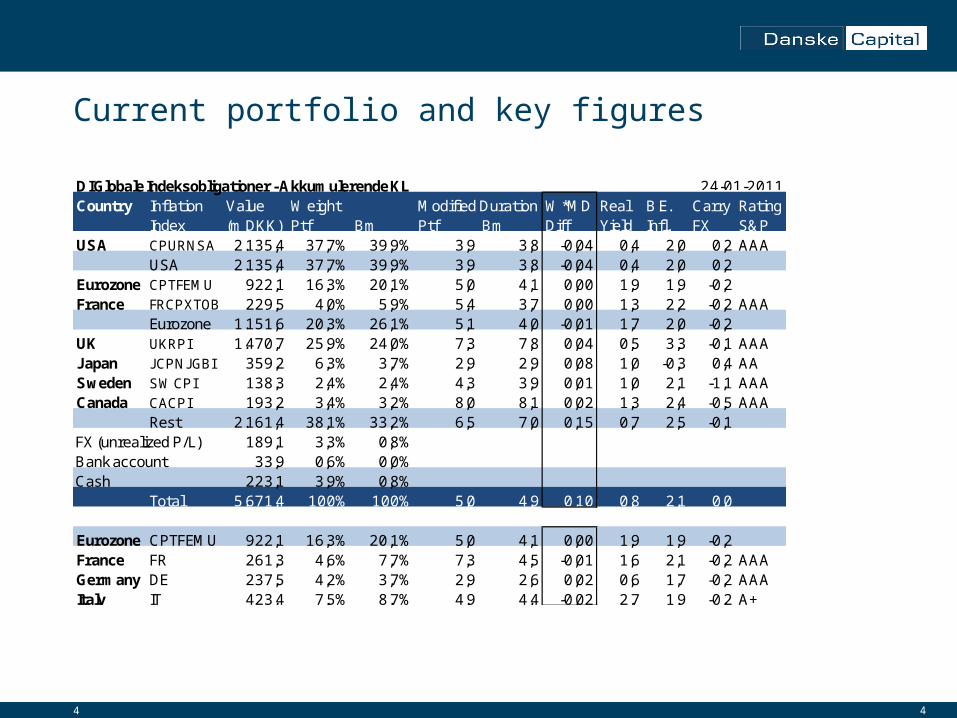

Current portfolio and key figures

4

DI Globale Indeksobligationer - Akkumulerende KLCountry Inflation Value Weight Modified Duration W*MD Real B.E. Carry Rating

Index (m.DKK) Ptf Bm Ptf Bm Diff Yield Infl. FX S&PUSA CPURNSA 2.135,4 37,7% 39,9% 3,9 3,8 -0,04 0,4 2,0 0,2 AAA

USA 2.135,4 37,7% 39,9% 3,9 3,8 -0,04 0,4 2,0 0,2Eurozone CPTFEMU 922,1 16,3% 20,1% 5,0 4,1 0,00 1,9 1,9 -0,2France FRCPXTOB 229,5 4,0% 5,9% 5,4 3,7 0,00 1,3 2,2 -0,2 AAA

Eurozone 1.151,6 20,3% 26,1% 5,1 4,0 -0,01 1,7 2,0 -0,2UK UKRPI 1.470,7 25,9% 24,0% 7,3 7,8 0,04 0,5 3,3 -0,1 AAAJ apan J CPNJ GBI 359,2 6,3% 3,7% 2,9 2,9 0,08 1,0 -0,3 0,4 AASweden SWCPI 138,3 2,4% 2,4% 4,3 3,9 0,01 1,0 2,1 -1,1 AAACanada CACPI 193,2 3,4% 3,2% 8,0 8,1 0,02 1,3 2,4 -0,5 AAA

Rest 2.161,4 38,1% 33,2% 6,5 7,0 0,15 0,7 2,5 -0,1FX (unrealized P/L) 189,1 3,3% 0,8%Bank account 33,9 0,6% 0,0%Cash 223,1 3,9% 0,8%

Total 5.671,4 100% 100% 5,0 4,9 0,10 0,8 2,1 0,0

Eurozone CPTFEMU 922,1 16,3% 20,1% 5,0 4,1 0,00 1,9 1,9 -0,2France FR 261,3 4,6% 7,7% 7,3 4,5 -0,01 1,6 2,1 -0,2 AAAGermany DE 237,5 4,2% 3,7% 2,9 2,6 0,02 0,6 1,7 -0,2 AAAItaly IT 423,4 7,5% 8,7% 4,9 4,4 -0,02 2,7 1,9 -0,2 A+

24-01-2011

5

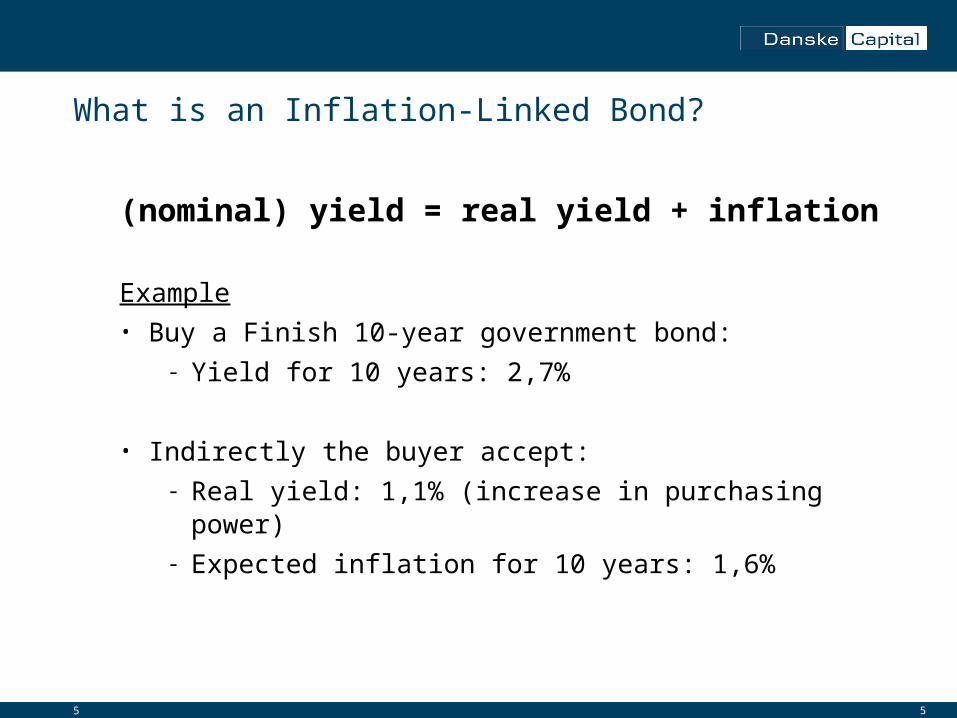

What is an Inflation-Linked Bond?

(nominal) yield = real yield + inflation

Example• Buy a Finish 10-year government bond:

- Yield for 10 years: 2,7%

• Indirectly the buyer accept:- Real yield: 1,1% (increase in purchasing power)- Expected inflation for 10 years: 1,6%

5

6

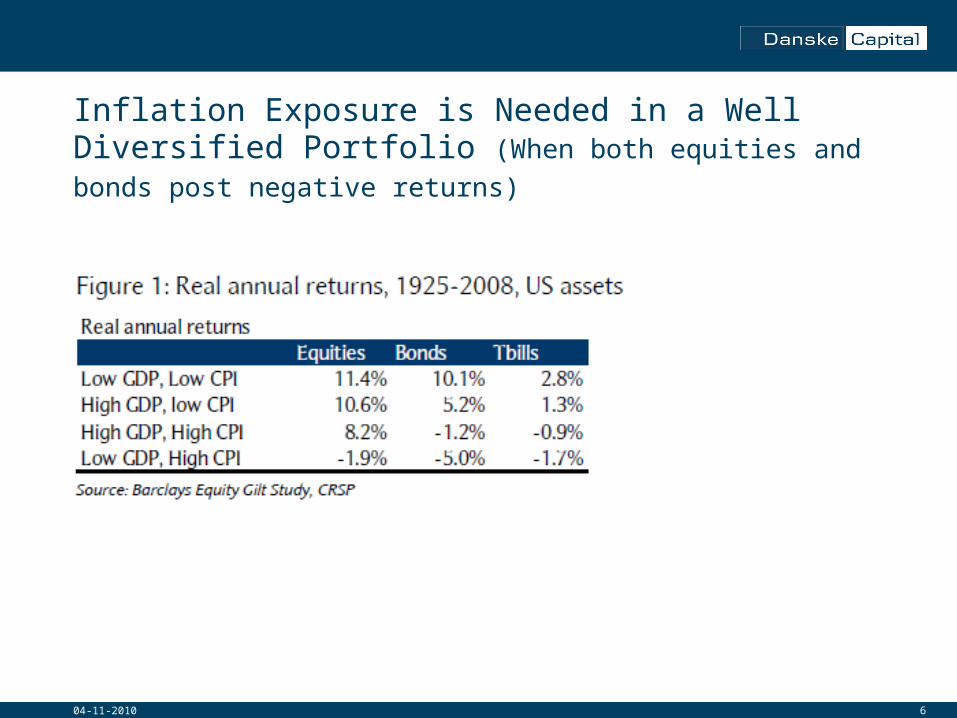

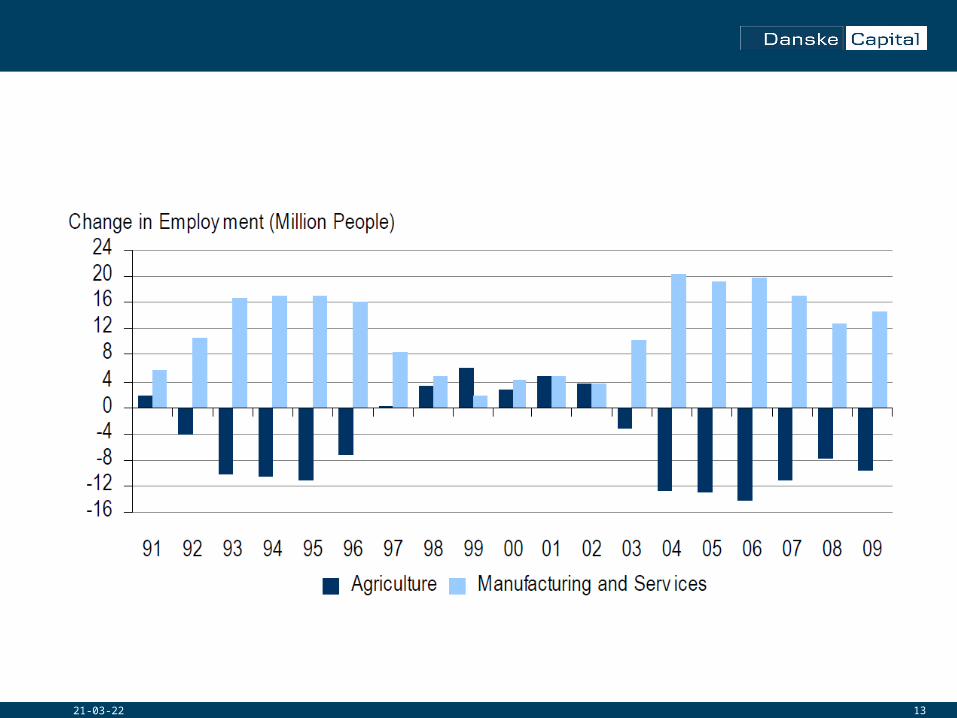

Inflation Exposure is Needed in a Well Diversified Portfolio (When both equities and bonds post negative returns)

04-11-2010

7

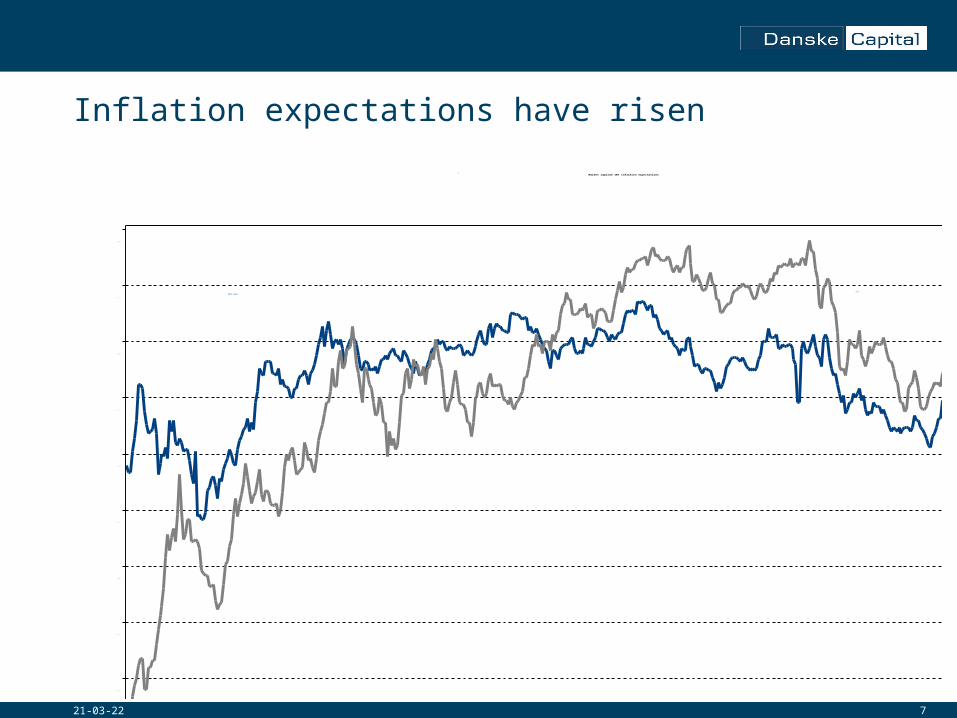

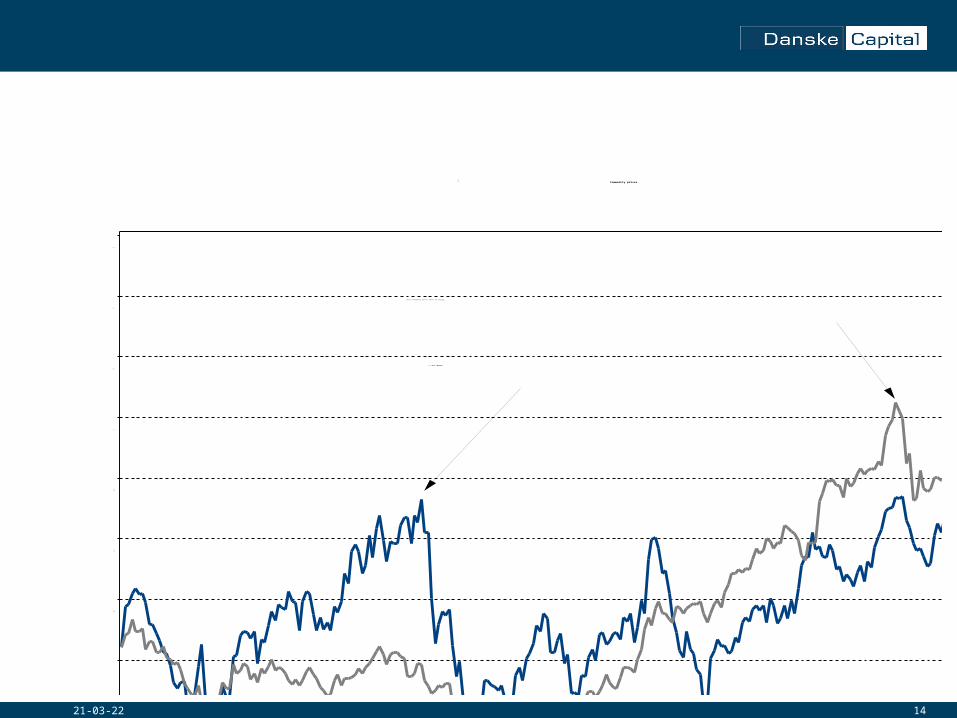

Inflation expectations have risen

18-04-23

Market implied 10Y inflation expectations

jan

09

mar maj jul sep nov jan

10

mar maj jul sep nov jan

11

Perc

ent

0,00

0,25

0,50

0,75

1,00

1,25

1,50

1,75

2,00

2,25

2,50

Euro area

USA

8

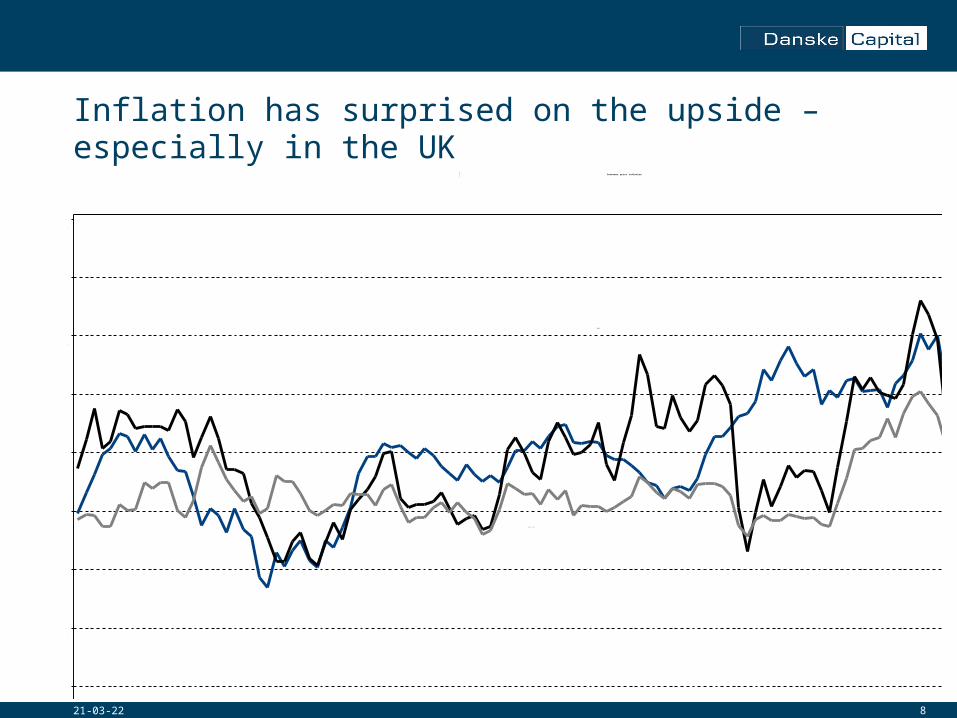

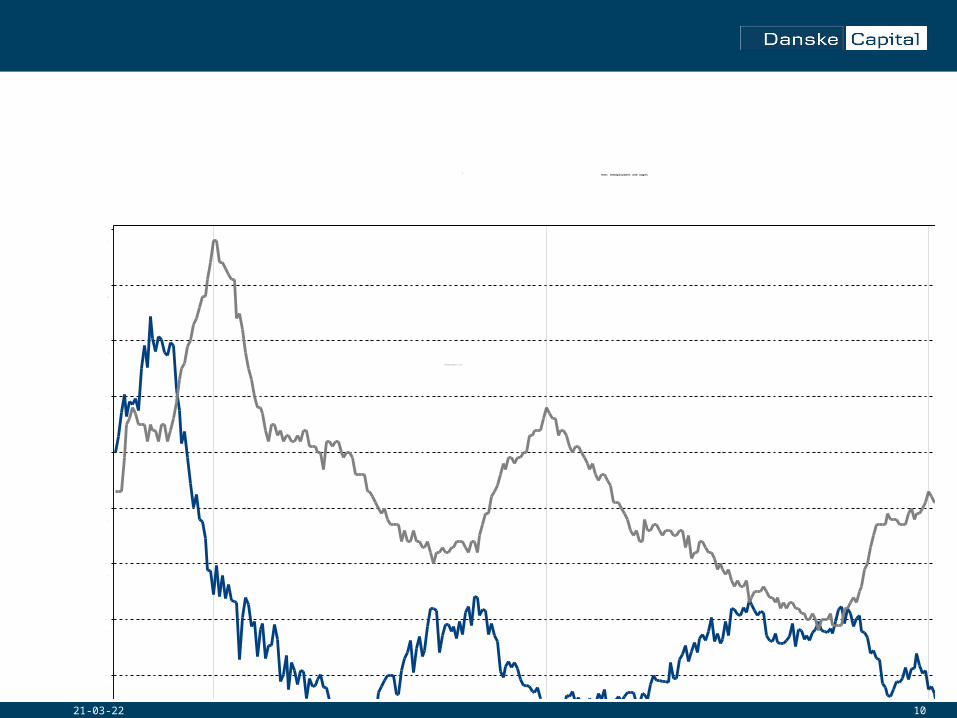

Inflation has surprised on the upside – especially in the UK

18-04-23

Consumer price inflation

00 01 02 03 04 05 06 07 08 09 10 110

1

2

3

4

5

6

7

8

9

10

Perc

enta

ge c

hang

e, Y

oY

-3

-2

-1

0

1

2

3

4

5

6

7

USA

Euro zone

UK (RPI)

918-04-23

1018-04-23

USA: Unemployment and wages

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

Perc

ent

1

2

3

4

5

6

7

8

9

10

11

Average hourly earnings, YoY

Unemployment rate

1118-04-23

As Share of GDP

USA: Federal Reserve Total Assets

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Perc

enta

ge

5

6

7

8

9

10

11

12

13

14

15

16

17

Perc

enta

ge

5

6

7

8

9

10

11

12

13

14

15

16

17

1218-04-23

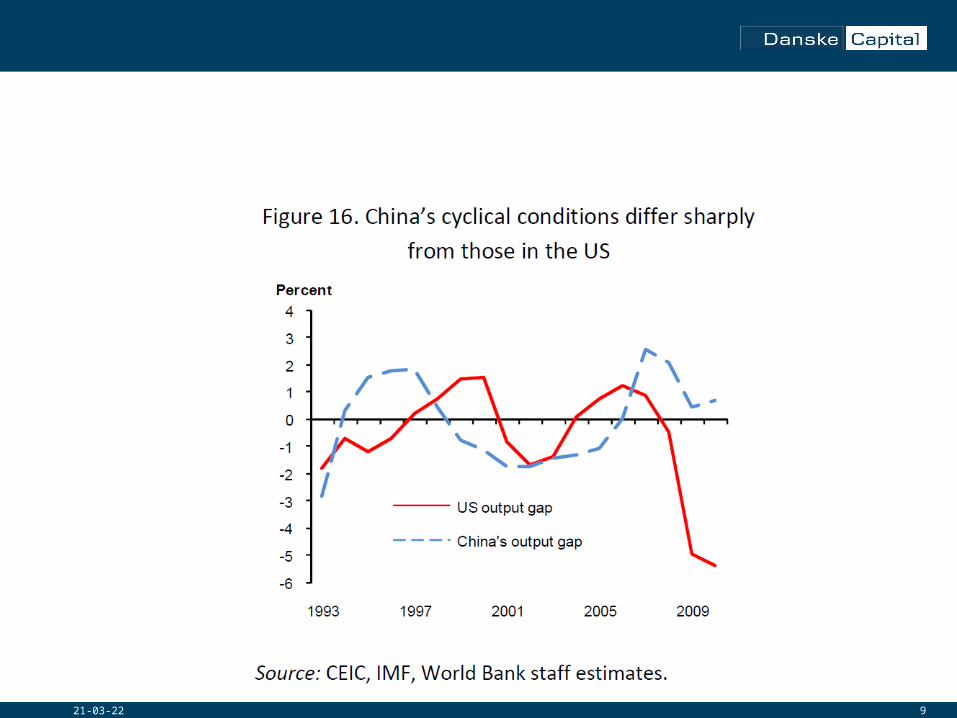

Absolute annual change in USD GDP (at market exchange rates)

Global: USA vs China

00 01 02 03 04 05 06 07 08 09 10

USD

(th

ousa

nd b

illio

ns)

-0,2

-0,1

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

1,0

USD

(th

ousa

nd b

illio

ns)

-0,2

-0,1

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

1,0

USA

China

1318-04-23

1418-04-23

Commodity prices

jan

10

feb mar apr maj jun jul aug sep okt nov dec jan

11

Inde

x

300

325

350

375

400

425

450

475

500

525

USD/

Barre

l

65

70

75

80

85

90

95

100

105

110

<< Oil (Brent)

GSCI Commodity price index ex energy

1515

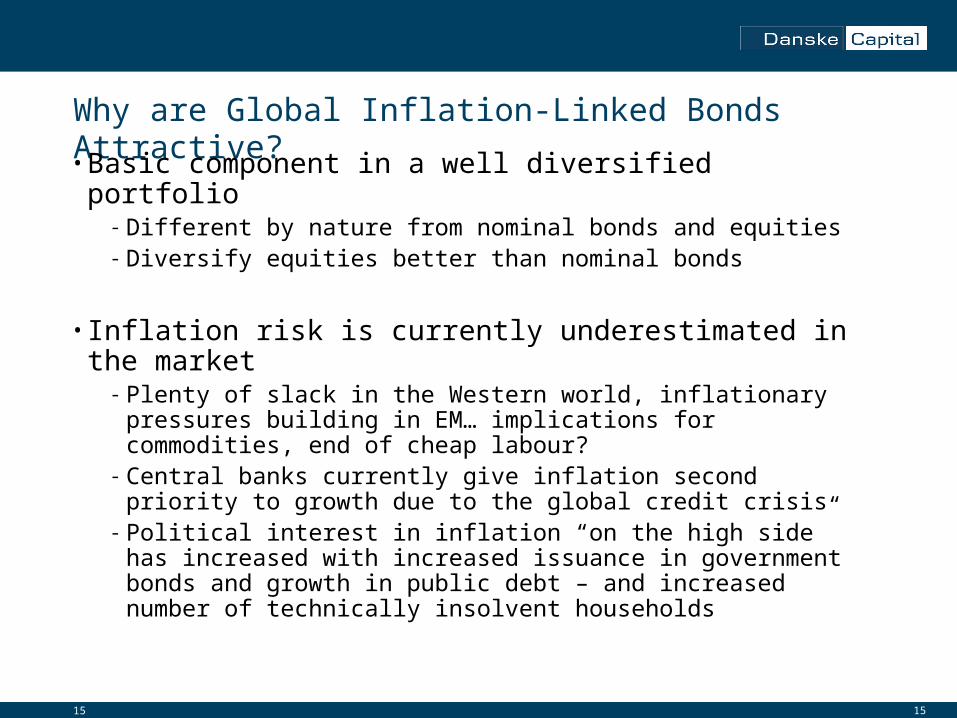

Why are Global Inflation-Linked Bonds Attractive?

•Basic component in a well diversified portfolio- Different by nature from nominal bonds and equities- Diversify equities better than nominal bonds

• Inflation risk is currently underestimated in the market

- Plenty of slack in the Western world, inflationary pressures building in EM… implications for commodities, end of cheap labour?

- Central banks currently give inflation second priority to growth due to the global credit crisis

- Political interest in inflation “on the high side” has increased with increased issuance in government bonds and growth in public debt – and increased number of technically insolvent households

16

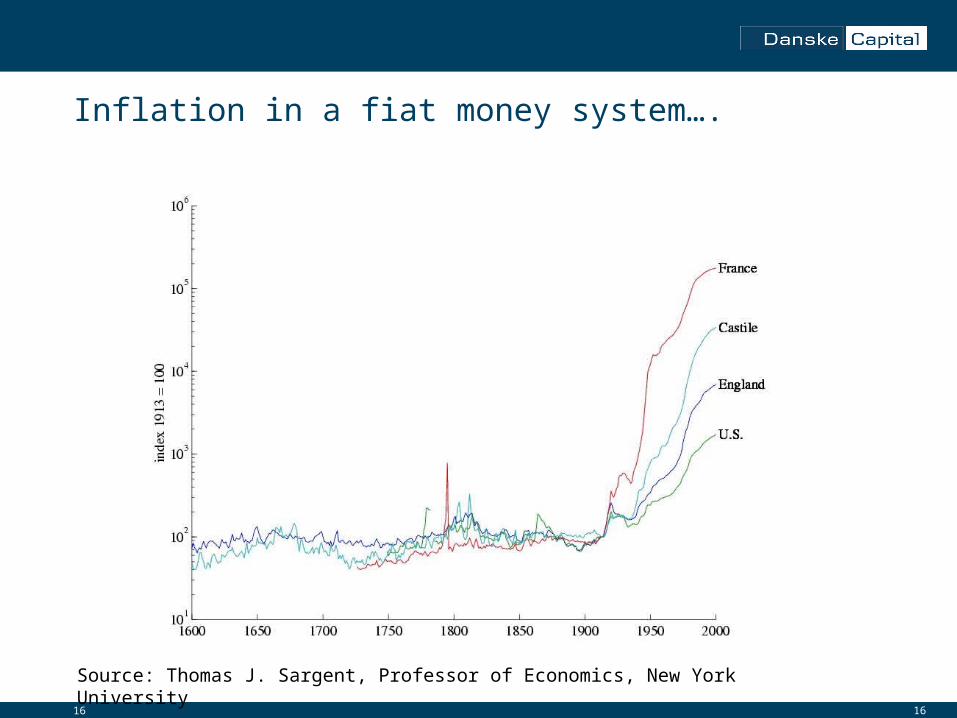

Inflation in a fiat money system….

16

Source: Thomas J. Sargent, Professor of Economics, New York University

1718-04-23

Disclaimer

This publication has been prepared to be read exclusively in conjunction with the oral

presentation provided by Danske Capital. Readers should not replace their own judgement with

any information or opinions herein and should contact their investment advisor whenever

necessary. Any information or opinions contained herein are not intended for distribution to or

use by any person in any jurisdiction or country where such distribution or use would be unlaw-

ful and, specifically, are not intended for distribution to or use by any "US Person" within the

meaning of the United States Securities Act of 1934, nor any personal customer in the United

Kingdom.