Return on Knowledge Danske Capital Luxembourg Danske Hedge Fixed Income Strategies February 2011.

23

Return on Knowledge Danske Capital Luxembourg Danske Hedge Fixed Income Strategies February 2011

-

Upload

dwain-floyd -

Category

Documents

-

view

215 -

download

0

Transcript of Return on Knowledge Danske Capital Luxembourg Danske Hedge Fixed Income Strategies February 2011.

Return on Knowledge

Danske Capital Luxembourg

Danske Hedge Fixed Income Strategies

February 2011

22

Agenda• The Basics• Examples of current strategies

• Danish government-guaranteed bank issues• Svenske bostäder I (Swedish mortgage bonds)• Svenske bostäder II (Swedish mortgage bonds)• Outright interest-rate call on long EUR swap rates• Relative Value 10s30s yield curve steepening on a forward basis• Relative Value Danish government rich compared to German government bonds• Relative Value USD interest rate curve (5-year vs. 2-year)

• Risk• In general• Scenario analysis• Historical utilisation• Exposure• Current allocation of risk

• 2011 forecast

• Historical returns

3

Portfolio Managers and Strategy Team

19-04-23

Michael Petry is Portfolio Manager of the Danske Invest Hedge Fixed Income Strategies fund. Michael joined Danske Capital in November 2005 from a position as Senior Dealer with Danske Markets where he worked as a market maker in swaps and options. At Danske Markets he has previously worked with derivatives sales. Prior to this, Michael worked as a Portfolio Manager with Danmarks Nationalbank (the Danish central bank). Michael has 17 years’ experience within Fixed Income and bond markets and holds a Graduate Diploma in Business Administration (Economics & Financial Planning) from the Aarhus School of Business.

Michael Petry is Portfolio Manager of the Danske Invest Hedge Fixed Income Strategies fund. Michael joined Danske Capital in November 2005 from a position as Senior Dealer with Danske Markets where he worked as a market maker in swaps and options. At Danske Markets he has previously worked with derivatives sales. Prior to this, Michael worked as a Portfolio Manager with Danmarks Nationalbank (the Danish central bank). Michael has 17 years’ experience within Fixed Income and bond markets and holds a Graduate Diploma in Business Administration (Economics & Financial Planning) from the Aarhus School of Business.

Tom Rosenkrans is associate portfolio manager of the Danske Invest Hedge Fixed Income Strategies fund and primary portfolio manager of the Danske Invest Hedge Mortgage Arbitrage hedge fund that focuses on investment in Danish mortgage bonds. Tom has more than nine years of experience within the financial markets and primarily focuses on Fixed Income and bond markets. Tom was previously employed by the Ministry of Finance. Tom holds a MSc in mathematics and economics from the Copenhagen Business School.

Tom Rosenkrans is associate portfolio manager of the Danske Invest Hedge Fixed Income Strategies fund and primary portfolio manager of the Danske Invest Hedge Mortgage Arbitrage hedge fund that focuses on investment in Danish mortgage bonds. Tom has more than nine years of experience within the financial markets and primarily focuses on Fixed Income and bond markets. Tom was previously employed by the Ministry of Finance. Tom holds a MSc in mathematics and economics from the Copenhagen Business School.

Carsten Cilieborg works as an analyst with the Global Fixed Income dept. of Danske Capital. Carsten is a member of the research team behind the Danske Invest Hedge Fixed Income Strategies fund and is also a member of the research team behind our global bond portfolios. Carsten prepares quantitative and strategic analyses of the global fixed income markets on a regular basis for the Danske Invest Hedge Fixed Income Strategies fund. Carsten has seven years of experience within the financial markets, and prior to joining Danske Capital he worked as an analyst with the Treasury Dept. of Danmarks Skibskreditfond (Danish Ship Finance). Carsten holds a MSc (economics) from the Copenhagen University.

Carsten Cilieborg works as an analyst with the Global Fixed Income dept. of Danske Capital. Carsten is a member of the research team behind the Danske Invest Hedge Fixed Income Strategies fund and is also a member of the research team behind our global bond portfolios. Carsten prepares quantitative and strategic analyses of the global fixed income markets on a regular basis for the Danske Invest Hedge Fixed Income Strategies fund. Carsten has seven years of experience within the financial markets, and prior to joining Danske Capital he worked as an analyst with the Treasury Dept. of Danmarks Skibskreditfond (Danish Ship Finance). Carsten holds a MSc (economics) from the Copenhagen University.

The team has a solid and well-balanced mixture of experience from different areas of the financial markets as well as a sound theoretical and educational background. The combination of experience and theoretical knowledge adds value to the investment process.

The team has a solid and well-balanced mixture of experience from different areas of the financial markets as well as a sound theoretical and educational background. The combination of experience and theoretical knowledge adds value to the investment process.

Michael Petry, Chief Portfolio Manager. Born 1970. Tom Rosenkrans, Senior Portfolio Manager. Born 1974.

Carsten Cilieborg, Portfolio Manager. Born 1978.

4

Risk Management Team

19-04-23

Per Søgaard-Andersen is Chief Analyst with the Alternative Solutions and Risk Measurement team in Danske Capital. The team is responsible for development of risk models for a number of Danske Capital’s products, including hedge funds. Per has more than 22 years of experience within the financial markets. Before joining Danske Capital, he worked at SimCorp, ABN-AMRO, Nordea and SAMPENSION. Per Søgaard-Andersen holds a Ph.D. from DTU (the Technical University of Denmark).

Rasmus Majborn is Risk Analyst with the Alternative Solutions and Risk Measurement team in Danske Capital. The team is responsible for development of risk models for a number of Danske Capital’s products, including hedge funds. Rasmus has seven years of experience within the financial markets and holds a MSc in mathematics and economics from the Copenhagen Business School.

The team is highly dedicated with the monitoring and managing of portfolio risk. The state of the art Value-at-Risk based risk management model is so superior, that the portfolio managers use the model actively in the decision-making process to evaluate portfolio impact in terms of diversification effects.

The team is highly dedicated with the monitoring and managing of portfolio risk. The state of the art Value-at-Risk based risk management model is so superior, that the portfolio managers use the model actively in the decision-making process to evaluate portfolio impact in terms of diversification effects.

Per Søgaard-Andersen, Chief Analyst. Born 1957. Rasmus Majborn, Risk Analyst. Born 1973.

5

The Basics

19-04-23

Per Søgaard-Andersen is Chief Analyst with the Alternative Solutions and Risk Measurement team in Danske Capital. The team is responsible for development of risk models for a number of Danske Capital’s products, including hedge funds. Per has more than 22 years of experience within the financial markets. Before joining Danske Capital, he worked at SimCorp, ABN-AMRO, Nordea and SAMPENSION. Per Søgaard-Andersen holds a Ph.D. from DTU (the Technical University of Denmark).

Rasmus Majborn is Risk Analyst with the Alternative Solutions and Risk Measurement team in Danske Capital. The team is responsible for development of risk models for a number of Danske Capital’s products, including hedge funds. Rasmus has seven years of experience within the financial markets and holds a MSc in mathematics and economics from the Copenhagen Business School.

5

To generate attractive absolute returns by investing in primarily Scandinavian and European Fixed Income Markets. The value is mainly created through relative-value and convergence strategies

To generate attractive absolute returns by investing in primarily Scandinavian and European Fixed Income Markets. The value is mainly created through relative-value and convergence strategies

Objectives Objectives

Target return = risk free rate + 4%Attractive Sharpe ratioLow correlation with other asset classes

Target return = risk free rate + 4%Attractive Sharpe ratioLow correlation with other asset classes

TargetsTargets

Danske Capital’s long expertise and experience as one of the leading managers in the Scandinavian Fixed Income Markets

Danske Capital’s long expertise and experience as one of the leading managers in the Scandinavian Fixed Income Markets

MeansMeans

Risk not exceeding 125% of a 10-year Danish government bond measured by Value-at-RiskThe investment universe as described later

Risk not exceeding 125% of a 10-year Danish government bond measured by Value-at-RiskThe investment universe as described later

RestrictionsRestrictions

66

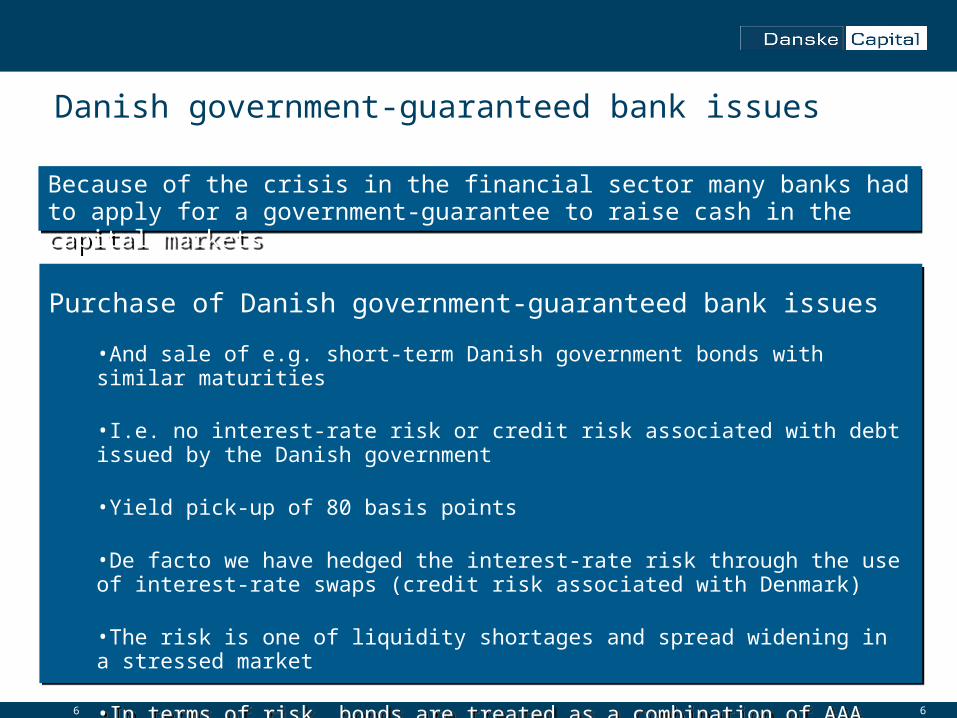

Danish government-guaranteed bank issues

Purchase of Danish government-guaranteed bank issues

•And sale of e.g. short-term Danish government bonds with similar maturities

•I.e. no interest-rate risk or credit risk associated with debt issued by the Danish government

•Yield pick-up of 80 basis points

•De facto we have hedged the interest-rate risk through the use of interest-rate swaps (credit risk associated with Denmark)

•The risk is one of liquidity shortages and spread widening in a stressed market

•In terms of risk, bonds are treated as a combination of AAA rated covered bonds and government bonds

Purchase of Danish government-guaranteed bank issues

•And sale of e.g. short-term Danish government bonds with similar maturities

•I.e. no interest-rate risk or credit risk associated with debt issued by the Danish government

•Yield pick-up of 80 basis points

•De facto we have hedged the interest-rate risk through the use of interest-rate swaps (credit risk associated with Denmark)

•The risk is one of liquidity shortages and spread widening in a stressed market

•In terms of risk, bonds are treated as a combination of AAA rated covered bonds and government bonds

Because of the crisis in the financial sector many banks had to apply for a government-guarantee to raise cash in the capital marketsBecause of the crisis in the financial sector many banks had to apply for a government-guarantee to raise cash in the capital markets

77

Swedish bostäder IThe figure shows the yield pickup on a 4-year AAA rated Swedish mortgage bond (Stadshypotek)

The bond is trading at a relatively high premium in a historical perspective

The red dots indicate how much the yield spread may rise on a 3, 6 and 12-month horizon before leading to a negative return on the investment

The investment has been hedged. Thus the return will be inde-pendent of the underlying trend in interest rates

Turbulence in the SEK money market has been the driver of the recent spread widening

The figure shows the yield pickup on a 4-year AAA rated Swedish mortgage bond (Stadshypotek)

The bond is trading at a relatively high premium in a historical perspective

The red dots indicate how much the yield spread may rise on a 3, 6 and 12-month horizon before leading to a negative return on the investment

The investment has been hedged. Thus the return will be inde-pendent of the underlying trend in interest rates

Turbulence in the SEK money market has been the driver of the recent spread widening

Strategy: Purchase of bostad bonds funded through repo trades . Hedging of interest-rate risk through a matching interest-rate swap

Strategy TotalBuy/Sell Bond YTM, bond YTM, swap 3M REPO 3M Stibor yield

Buy SM1576 (4½-årig) 3.86 -3.16 -1.90 2.02 0.82

Fixed leg Floating leg

-20

0

20

40

60

80

100

120

-20

0

20

40

60

80

100

120

dec-97 dec-98 dec-99 dec-00 dec-01 dec-02 dec-03 dec-04 dec-05 dec-06 dec-07 dec-08 dec-09 dec-10 dec-11 dec-12

yiel

d pi

ck-u

p (b

p)

yile

d pi

ck-u

p (b

p)

3 mth

6 mth

12 mth

4-yearbostad (Swedish mortgage bond)

Rich >>

Cheap>>

88

Swedish bostäder IIThe figure shows the ASW structure for Swedish bostäder

Bonds with shorter maturities are more expensive (lower risk premium) than bonds with longer maturities

However, this trend is reversed around a maturity of 5-6 years

10-year bostäder appear relatively expensive compared to 5-year bonds

Primarily because of the lack of issuance of 10-year maturities and heavy issuance of 5-year maturities

In our opinion investors are not sufficiently compensated for the (spread) risk in the 10-year segment

The figure shows the ASW structure for Swedish bostäder

Bonds with shorter maturities are more expensive (lower risk premium) than bonds with longer maturities

However, this trend is reversed around a maturity of 5-6 years

10-year bostäder appear relatively expensive compared to 5-year bonds

Primarily because of the lack of issuance of 10-year maturities and heavy issuance of 5-year maturities

In our opinion investors are not sufficiently compensated for the (spread) risk in the 10-year segment

Strategi: Buy 5-year bonds and sell 10-years (on an ASW basis) in a spread risk neutral ratio (2:1)Risk: The price of 10-year bonds will exceed that of 5-year bonds on an ASW basis

Buy/Sell Bond YTM, bond YTM, swap 3M REPO 3M STIBOR TotalBuy (2x) 5-year 4,07 -3,37 -1,95 2,11 1,72

Sell 10-year -4,68 3,82 1,75 -2,11 -1,22Strategi (2 x 5 year - 10 year) 3,46 -2,91 -2,15 2,11 0,50

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

0 2 4 6 8 10 12 14

yiel

d pi

ck-u

p

yiel

d pi

ck-u

p

Time To Maturity (years)

10-year SwedishMortgage Bond

5-year SwedishMortgage Bond

<<SwedishMortgage Bonds spread-to-swap curve

99

Outright: Long-term EUR forward rates are considered overbought

The figure shows the development in the level of 20-year rates in 20 years in Euroland since 2004. Long-term EUR forward rates appear overbought. The reason for this is the risk aversion caused by the South European sovereign debt crisis and fears of recession which have prompted/led to a demand for long-term swap rates by European pension funds.

The figure shows the development in the level of 20-year rates in 20 years in Euroland since 2004. Long-term EUR forward rates appear overbought. The reason for this is the risk aversion caused by the South European sovereign debt crisis and fears of recession which have prompted/led to a demand for long-term swap rates by European pension funds.

Source: Danske Analytics and Danske Capital. Historical performance is not indicative of future performance

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

apr-04 okt-04 apr-05 okt-05 apr-06 okt-06 apr-07 okt-07 apr-08 okt-08 apr-09 okt-09 apr-10 okt-10

20y20y average 2 x std. dev.

1010

Relative Value (RV): 10s30s steepening 4y forward

Strategy: Pay 30s and receive 10s with a 4-year forward start. Beta-neutral ratio no underlying interest-rate risk. Strategy has positive roll-down/carry Risk: The curve (10s30s) is flattening further because of increased risk aversion

-120

-100

-80

-60

-40

-20

0

20

40

60

80

-120

-100

-80

-60

-40

-20

0

20

40

60

80

apr-04 apr-05 apr-06 apr-07 apr-08 apr-09 apr-10

stee

pnes

s 10s3

0s

(bp)

stee

pnes

s 10s3

0s

(bp)

10s30s spot10s30s 4yr forward

1111

Danish long dated bonds (30 year) rich compared to Germany

-15

-10

-5

0

5

10

15

20

25

30

35

40

-15

-10

-5

0

5

10

15

20

25

30

35

40

nov-08 feb-09 maj-09 aug-09 nov-09 feb-10 maj-10 aug-10 nov-10 feb-11

yiel

d sp

read

(bp)

yiel

d sp

read

(bp)

30-yearyield spread Denmark vs.Germany

Denmark cheap vs. Germany>>

Denmark rich vs. Germany>>

1212

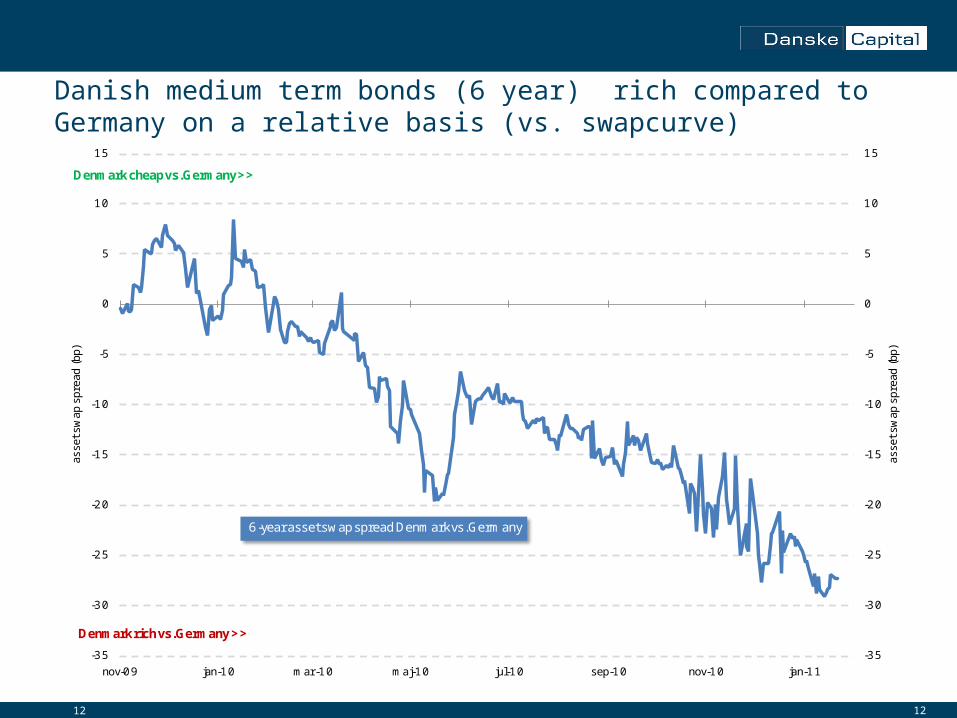

Danish medium term bonds (6 year) rich compared to Germany on a relative basis (vs. swapcurve)

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

nov-09 jan-10 mar-10 maj-10 jul-10 sep-10 nov-10 jan-11

asse

t sw

ap s

prea

d (b

p)

asse

t sw

ap s

prea

d (b

p)

6-yearasset swap spread Denmark vs.Germany

Denmark cheap vs. Germany>>

Denmark rich vs. Germany>>

1313

On the USD curve 5-year looks cheap compared to 2-year. We believe the curve is to steep and position for a flatter curve

-20

0

20

40

60

80

100

120

140

160

180

-20

0

20

40

60

80

100

120

140

160

180

dec-99 dec-00 dec-01 dec-02 dec-03 dec-04 dec-05 dec-06 dec-07 dec-08 dec-09 dec-10

5yr

-2

yr U

SD

(bp)

5 yr -2

yr U

SD

(bp

)

Steepcurve >>

<<Flat curve

1414

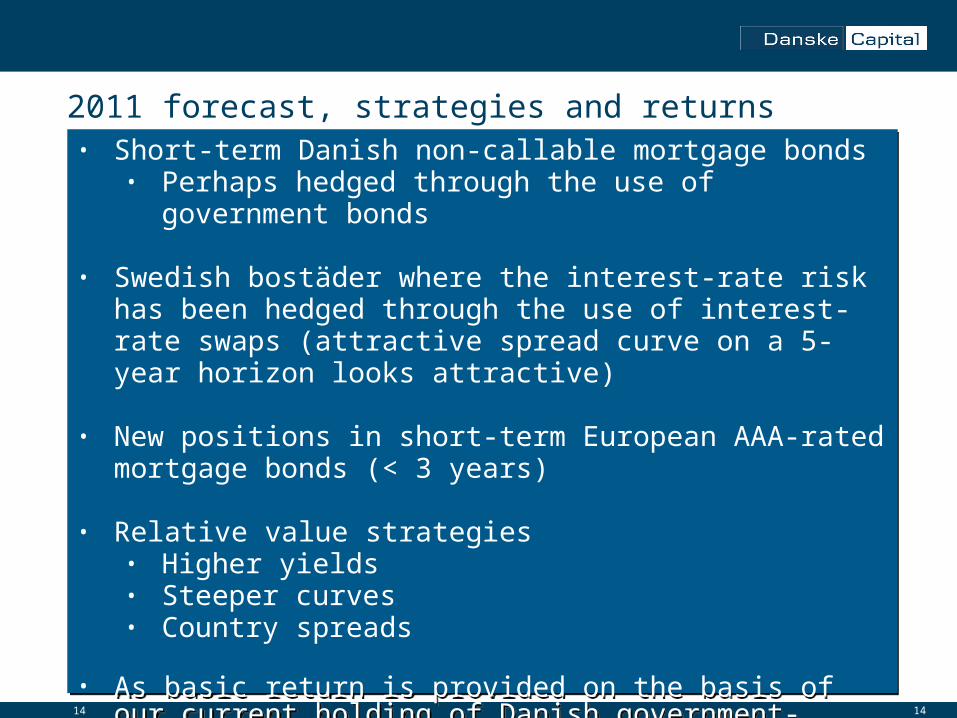

2011 forecast, strategies and returns• Short-term Danish non-callable mortgage bonds

• Perhaps hedged through the use of government bonds

• Swedish bostäder where the interest-rate risk has been hedged through the use of interest-rate swaps (attractive spread curve on a 5-year horizon looks attractive)

• New positions in short-term European AAA-rated mortgage bonds (< 3 years)

• Relative value strategies• Higher yields • Steeper curves • Country spreads

• As basic return is provided on the basis of our current holding of Danish government-guaranteed bank issues and EUR covered bonds

• Short-term Danish non-callable mortgage bonds• Perhaps hedged through the use of government

bonds

• Swedish bostäder where the interest-rate risk has been hedged through the use of interest-rate swaps (attractive spread curve on a 5-year horizon looks attractive)

• New positions in short-term European AAA-rated mortgage bonds (< 3 years)

• Relative value strategies• Higher yields • Steeper curves • Country spreads

• As basic return is provided on the basis of our current holding of Danish government-guaranteed bank issues and EUR covered bonds

1515

Return

1616

Return relative to the FI Arbitrage Hedge Fund Index

17

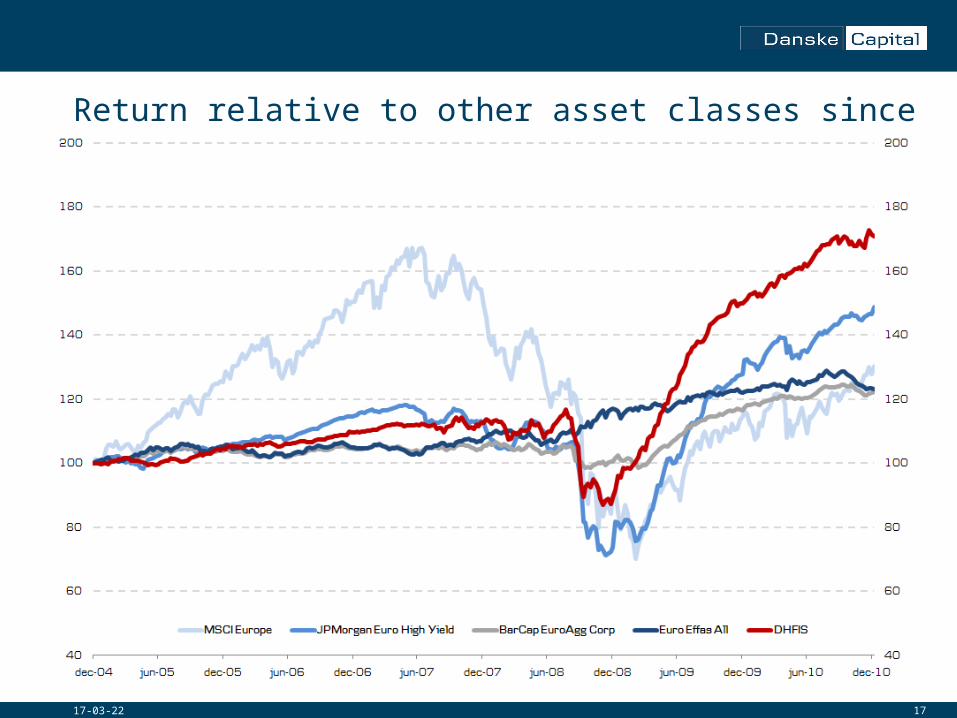

Return relative to other asset classes since inception aktivklasser siden etablering

19-04-23

18

Performance ratios

19-04-23

Rasmus Majborn is Risk Analyst with the Alternative Solutions and Risk Measurement team in Danske Capital. The team is responsible for development of risk models for a number of Danske Capital’s products, including hedge funds. Rasmus has seven years of experience within the financial markets and holds a MSc in mathematics and economics from the Copenhagen Business School.

Performance Measures

Year Annual Returns FUM €Start Date J an 2005 2010 YTD 12.44% € 192.08 M

Last Reported ROR Sep 2010 2009 68.09% € 142.18 M

Minimum Investment DKK 1000 K 2008 -21.06% € 131.73 M

Management Fee 0.50% 2007 2.75% € 134.42 M

Incentive Fee 20.00% 2006 4.63% € 59.90 M

Lock up 7 days 2005 4.81% € 7.04 M

Total Return 68.1% -0.08

Compound Annual Return 9.45% 0.54

Average Monthly Return 0.81% 0.51

W orst Drawdown -22.40 % 0.38

Monthly Standard Deviation 3.25 0.43

Sharpe Ratio 0.62 0.31

Alpha vs S&P 500 0.76 0.32

Beta vs S&P 500 0.26 -0.33

R2 vs S&P 500 0.14 0.42

Up Capture vs S&P 500 0.48 -0.14

Down Capture vs S&P 500 0.06 0.41

Administrative Information

Performance Analysisvs Barclay CTA Index

vs Barclay Hedge Fund Index

vs Barclay FOF Index

vs J PMorgan

vs MSCI W orld

Correlation Analysis

vs S&P 500

vs NASDAQ

vs Dow J ones Industrial

vs Russell 2000

vs Lehman Brothers Treasury

vs FT-SE 100

All data hedged to EUR

1919

Management and performance fee /issuance / home page

• Performance fee- 20% of the return above the risk free rate

• Management fee-1,10% (63,5 bp to Luxembourg)

• Weekly NAV / weekly issuance / weekly redemptions (1 week notice)

• www.danskehedge.com / www.danskehedge.dk

20

Awards / nominations

19-04-23

DIHFIS winner of hedgeweek Best Fixed Income Hedgefund award -Hedgeweek - March 2009“The fund posted a positive return over the financial crisis with more than 40% and also managed to maintain low volatility” www.hedgeweek.com

DIHFIS ranked 6th best Fixed Income Hegdefund by Barclayshedge based on a 3 year-period return- Barclays Hedge - November 2010

DIHFIS nominated by EuroHedge/Euromoney as best Fixed Income Hedgefund in 2010 -Eurohedge/Euromoney – December 2010

2121

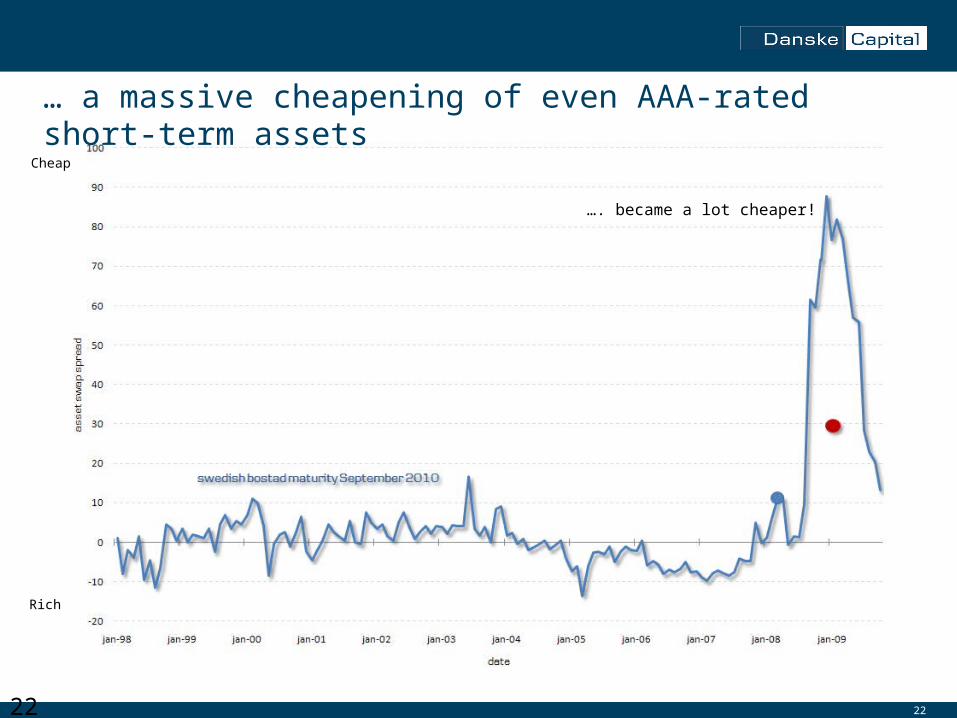

What happened …. ?

What appeared cheap …

Cheap

Rich

2222

… a massive cheapening of even AAA-rated short-term assets

…. became a lot cheaper!

Cheap

Rich

23

Disclaimer & contact information

19-04-23

Danske Capital

Strødamvej 46

DK 2100 Copenhagen

Tel. +45 45 13 96 00

Fax +45 45 14 98 03

http://www.danskecapital.com

This publication has been prepared to be read exclusively in conjunction with the oral presentation provided by Danske Capital. Readers should not replace their own judgement with any information or opinions herein and should contact their investment advisor whenever necessary. Any information or opinions contained herein are not intended for distribution to or use by any person in any jurisdiction or country where such distribution or use would be unlawful and, specifically, are not intended for distribution to or use by any "US Person" within the meaning of the United States Securities Act of 1933, nor any personal customer in the United Kingdom.