Retirement Withdrawal Strategies

37

Milwaukee Bogleheads® A DIY investment group, followers of John Bogle's Index investing strategies, the Milwaukee local chapter of Bogleheads. This presentation was made November 4, 2014 by Bob Schramm of our chapter.

-

Upload

leemke -

Category

Economy & Finance

-

view

178 -

download

0

Transcript of Retirement Withdrawal Strategies

Milwaukee Bogleheads®

A DIY investment group, followers of John Bogle's

Index investing strategies, the Milwaukee local

chapter of Bogleheads.

This presentation was made November 4, 2014

by Bob Schramm of our chapter.

Disclaimer

All examples are for illustration purposes only and

are not investment recommendations.

The views expressed in the presentation, are

those of the presenter, commenters, guests and

participants and may not reflect the views of the

Bogleheads organization.

Use your discretion in using examples presented

here for your own investment purposes.

Retirement Funds:

Will You Still Love Me Tomorrow?

A look at Otar’s Zones and Guyton’s Rules

Robert Schramm

MKE Bogleheads

November 4, 2014

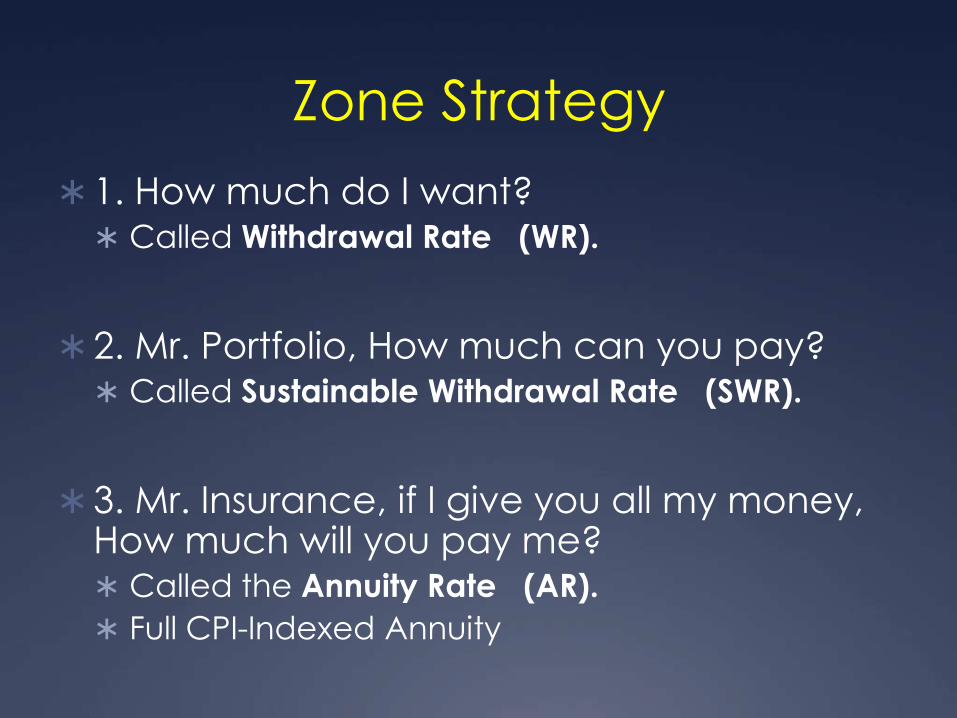

Zone Strategy

1. How much do I want? Called Withdrawal Rate (WR).

2. Mr. Portfolio, How much can you pay? Called Sustainable Withdrawal Rate (SWR).

3. Mr. Insurance, if I give you all my money, How much will you pay me? Called the Annuity Rate (AR).

Full CPI-Indexed Annuity

65 yr male$1,000,000AR: 5.3%

SWR: 3.8%

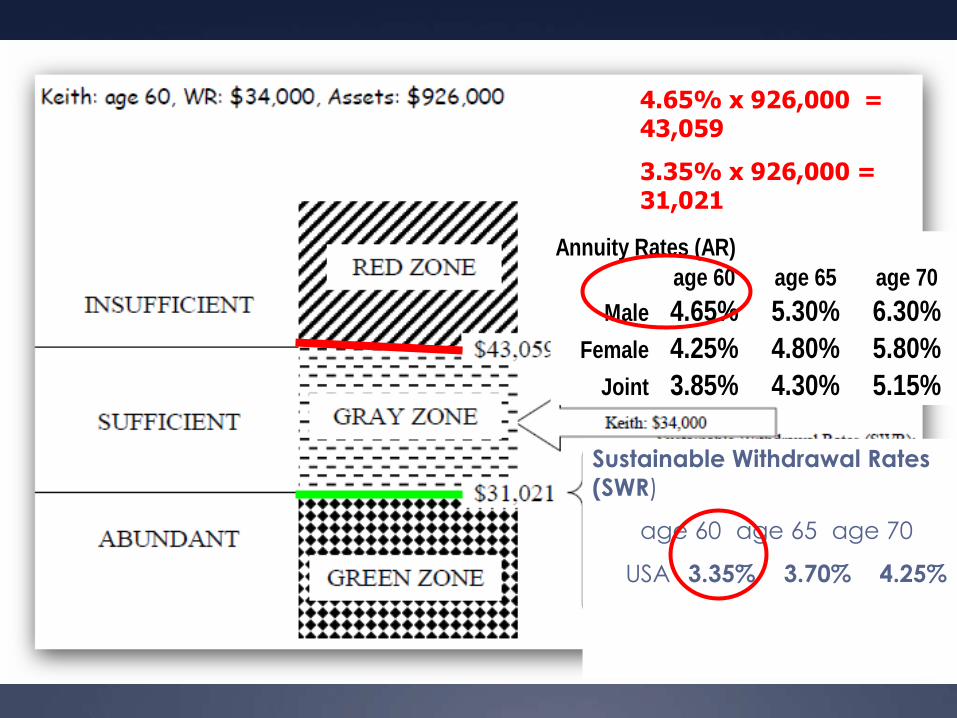

4.65% x 926,000 = 43,059

3.35% x 926,000 = 31,021

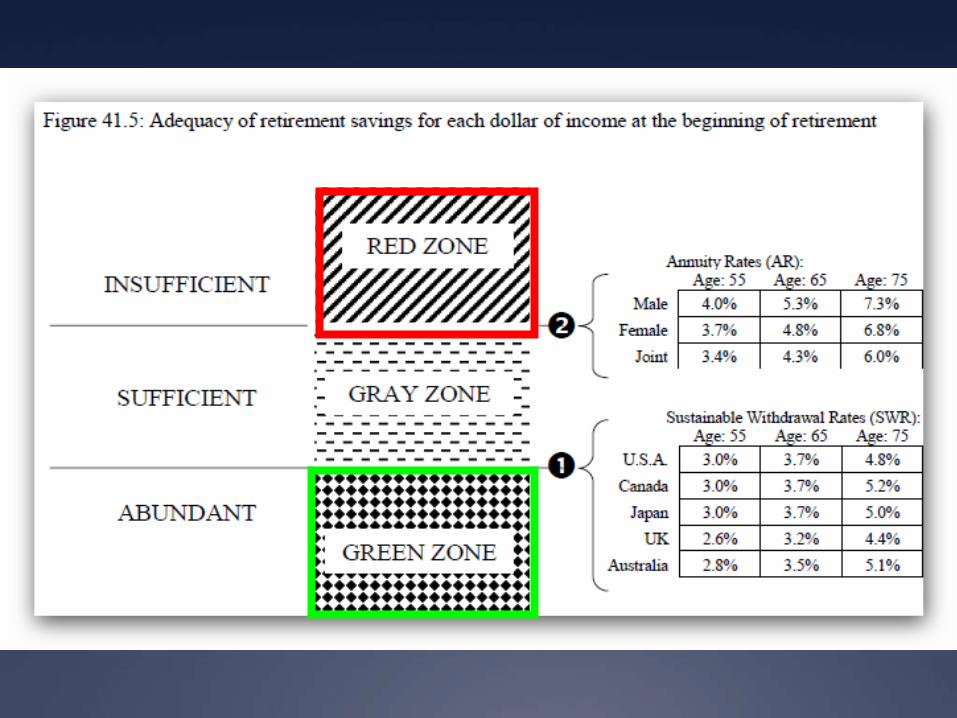

Annuity Rates (AR)

age 60 age 65 age 70

Male 4.65% 5.30% 6.30%

Female 4.25% 4.80% 5.80%

Joint 3.85% 4.30% 5.15%

Sustainable Withdrawal Rates

(SWR)

age 60 age 65 age 70

USA 3.35% 3.70% 4.25%

age 60 age 65 age 70

USA 3.35% 3.70% 4.25%

Annuity Rates (AR)

age 60 age 65 age 70

Male 4.65% 5.30% 6.30%

Female 4.25% 4.80% 5.80%

Joint 3.85% 4.30% 5.15%

5.8% x 385,000 = 223305.80% x 385,000

= 22,330

4.25% x 385,000

= 16,363

Conversion Numbers

% Rate to Multiplier Annuity Rate (AR) to Life Annuity Multiplier (LAM)

AR 5.3% = LAM 20 100% / 5.3% = 20 5.3% x 20 = 106%

Sustainable Withdrawal Rate (SWR) to Sustainable Asset

Multiplier (SAM)

SWR 3.7% = SAM 27 100% / 3.7% = 27 3.7% x 27 = 99.9%

Mike Box

40,000 – 20,540 = 19,360

Red Zone Strategies

You must export risk

If Retired: Slow down withdrawals

Cut expenses Part-time work

CPI-indexed Annuity to cover inflation risk

If Working: Delay Retirement A few extra years might be enough to buy

annuity

Decision Rules and Maximum

Initial Withdrawal Rates

By Jonathan T. Guyton, CFP, and William J. Klinger

Cornerstonewealthadvisors.com/files/08-06_Websitearticle.pdf

Guyton Withdrawal Rules

Portfolio Management Rule

Inflation Rule

Withdrawal Rule

Capital Preservation Rule

Prosperity Rule

Guyton Withdrawal Rules

Portfolio Management rules

If an asset class exceeds its target allocation, invest

excess in cash.

Withdraw first from excess equities, then from

excess bonds, then from excess cash.

Do not withdraw equity following a year of declining stock market.

Guyton Withdrawal Rules

Inflation rules

Withdrawals increase by the annual rate of inflation, measured by the CPI, to maintain

purchasing power up to a maximum of 6%.

There is no make-up for a missed increase.

Guyton Withdrawal Rules

Withdrawal rule

Withdrawals increase from year to year in

accordance with the inflation rule, except there is

no increase following a year where the portfolio’s

return is negative and when that year’s withdrawal rate would be greater than the original

withdrawal rate.

There is no makeup for missed increases.

Guyton Withdrawal Rules

Capital Preservation rule

For the first 15 years, reduce

withdrawal rate by 10% if it

would have risen by 20%over initial rate.

Expires 15 years before the

maximum age.

This decreased withdrawal

becomes the basis for the

following year’s withdrawal.

Guyton Withdrawal Rules

Prosperity rule

In years with a withdrawal rate more than 20% below the

initial withdrawal rate, the current year’s withdrawal rate is

increased by 10%.

Other decision rule in effect are applied to this increased

amount.

This increased withdrawal amount becomes the basis for determining the next year’s amount.

Guyton Withdrawal RulesProsperity Rule Example

Year Inflation WR Withdrawal Account Balance

Start 4.00% $ 20,000 $ 500,000

1 3.00% 4.12% $ 20,600

7 3.00% 4.92% $ 24,600 $ 820,000

24600 / 820000 = 3%

4% - 20% = 3.2%

4.92% + 10% = 5.41%

7 new 5.41% $ 27,050

Decision Rule Summary

Condition:

Prior year ‘s return is negative

Current WD rate w/I 20% of initial WD rate

Current WD rate > initial WD by 20%

Current WD rate < initial WD rate by 20%

Action:

Apply Withdrawal Rule

Increase prior year WD by CPI

Apply Capital Preservation Rule

Apply Prosperity Rule

Guyton Withdrawal Rules

Conclusions

Withdrawal rates of 5.2%-5.6% sustainable with 99% confidence with 65% equities.

80% equities provides greater purchasing power with lower success rates.

50% equities drops maximum initial withdrawal rates as low as 4.6%.

Aside: 65yo couple 17.6% probability of 30 years-life expectancy just under 24 years.

http://www.retirementoptimizer.com/ Jim Otar’s site for his

book and sample his retirement program

http://cornerstonewealthadvisors.com/files/08-06_WebsiteArticle.pdf Guyton and Klinger’s decision rules

and withdrawal rates

http://www.forbes.com/sites/lawrencelight/2014/04/24/how-to-withdraw-your-retirement-money/ Article and sample link

to a Withdrawal Policy Statement

http://www.kitces.com/?s=annuities+versus+saf Comparing

annuities with safe withdrawal rates

http://assetbuilder.com/SCOTT_BURNS/HOW_TO_OVERCOME_FEAR_OF_REQUIRED_DISTRIBUTIONS?utm_source=feedburner&utm_medium

=feed&utm_campaign=Feed%3A+Assetbuilder+%28AssetBuilder+Inc.%29 Using RMD’s as a way of annuitizing retirement income.

Links to RMD calculators.

http://www.bogleheads.org/wiki/Required_Minimum_Distribution_vs_annuitization A look at IRA minimum distributions in the light of

annuities.

http://www.bogleheads.org/wiki/Safe_Withdrawal_Rates

Considerations of safe withdrawal rates

http://www.esplanner.com/ Economic security planner from

Lawrence Kotlikoff (Try free version)

http://firecalc.com/ Retirement Calculator