RETIREMENT PLANS, PENSIONS AND ANNUITIES

43

RETIREMENT PLANS, PENSIONS AND ANNUITIES

Transcript of RETIREMENT PLANS, PENSIONS AND ANNUITIES

RETIREMENT PLANS, PENSIONS AND ANNUITIES

Published by Fast Forward Academy, LLChttps://fastforwardacademy.com(888) 798-PASS (7277)

© 2021 Fast Forward Academy, LLC

All rights reserved. No part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of the publisher.

2 Hour(s) - Other Federal Tax

NASBA: 116347

CTEC Provider #: 6209CTEC Course #: 6209-CE-0041

IRS Provider #: UBWMFIRS Course #: UBWMF-T-00231-21-S

The information provided in this publication is for educational purposes only, and does not necessarily reflect all laws, rules, or regulations for the tax year covered. This publication is designed to provide accurate and authoritative information concerning the subject matter covered, but it is sold with the understanding that the publisher is not engaged in rendering legal, accounting or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

To the extent any advice relating to a Federal tax issue is contained in this communication, it was not written or intended to be used, and cannot be used, for the purpose of (a) avoiding any tax related penalties that may be imposed on you or any other person under the Internal Revenue Code, or (b) promoting, marketing or recommending to another person any transaction or matter addressed in this communication.

COURSE OVERVIEW.............................................................................................................................................................. 7

Course Description ....................................................................................................................................................................... 7

Learning Objectives ...................................................................................................................................................................... 7

CHAPTER 1 - QUALIFIED RETIREMENT PLANS ................................................................................................................... 7

Introduction................................................................................................................................................................................... 7

Chapter Learning Objectives ....................................................................................................................................................... 8

Defined Benefit Plans................................................................................................................................................................... 8

Defined Contribution Plans ......................................................................................................................................................... 9

CHAPTER 2 - TAX TREATMENT OF QUALIFIED PLANS..................................................................................................... 15

Introduction.................................................................................................................................................................................15

Chapter Learning Objectives .....................................................................................................................................................16

Contributions to Qualified Employee Plans.............................................................................................................................16

Distributions from a Qualified Employee Plan........................................................................................................................19

CHAPTER 3 - ANNUITIES.................................................................................................................................................... 31

Introduction.................................................................................................................................................................................31

Chapter Learning Objectives .....................................................................................................................................................31

Deferred Annuity ........................................................................................................................................................................31

Immediate Annuity .....................................................................................................................................................................31

Qualified Annuity ........................................................................................................................................................................31

Nonqualified Annuity .................................................................................................................................................................32

Death Benefits.............................................................................................................................................................................32

Annuitization Methods...............................................................................................................................................................32

Nonqualified Annuity Income Tax Treatment .........................................................................................................................34

Summary......................................................................................................................................................................................38

GLOSSARY .......................................................................................................................................................................... 39

Glossary .......................................................................................................................................................................................39

Course Description 7

•

•

•

•

•

•

•

•

•

•

COURSE OVERVIEW

COURSE DESCRIPTIONEmployer-sponsored retirement plans, generally referred to in the aggregate as qualified employee plans, constitute one of the important "legs" of the retirement stool that individuals look to for their income in retirement. The other two legs of that stool are personal savings - through investment in securities, deferred annuities, savings accounts, etc. - and Social Security retirement benefits. This course will examine qualified employee plans, their limits and their tax treatment along with a discussion of annuities and their taxation.

Annuities offer their owners the opportunity to systematically liquidate a principal sum or save money for a long-term objective. For many annuity buyers, that objective is to provide income during retirement. As we will see in our examination of annuities, they provide owners with a number of advantages; principal among them is their tax treatment. By purchasing and investing in an annuity, a contract owner can avoid current income taxation of earnings. By avoiding current income taxation, earnings that might have been used to pay current income taxes can be invested to produce additional income.

Annuities' tax advantages aren't limited to tax deferral, however; annuities offer additional tax advantages. For example, an investor purchasing a variable annuity can change his or her investment allocation in the contract's variable subaccounts whenever desired. Typically, such changes are made in order to implement new objectives or to modify the level of risk assumed. From a tax point of view, the important issue is that the contract owner can make these changes without being required to recognize income as would be required if, for example, the investor liquidated his or her stock portfolio in order to purchase bonds. In addition to these tax benefits, a contract owner that elects to annuitize his annuity contract, i.e. to take a periodic income from it, will find that part of each periodic income payment may be tax free as a return of his or her investment in the annuity contract.

LEARNING OBJECTIVESUpon completion of this course, you should be able to:

Distinguish between the types of qualified employee plans;

Recognize the limits imposed on qualified employee plan contributions and benefits;

List the requirements applicable to qualified employee plan loans;

Apply the federal tax laws to qualified employee plan contributions and distributions;

Recognize the tax treatment of nonqualified annuity distributions; and

Identify the tax treatment of annuity contributions and distributions.

CHAPTER 1 - QUALIFIED RETIREMENT PLANS

INTRODUCTIONThe term "qualified retirement plan" generally encompasses a range of qualified employee plans that include an employer's stock bonus, pension and profit sharing plan that meet specific Internal Revenue Code requirements. Among other requirements, such a plan must:

Be established by an employer for the exclusive benefit of employees or beneficiaries;

Be nondiscriminatory in terms of contributions or benefits;

Meet minimum age, service standard, vesting and minimum coverage requirements; and

Contain various other provisions designed to provide fairness and a certain measure of safety for plan participants.

8 Chapter 1 - Qualified Retirement Plans

•

•

•

•

•

•

•

•

A qualified employee plan can be couched in terms of the contribution to be made to it or in terms of the benefit to be received at retirement or at some other time. In the first case, the plan is a defined contribution plan; in the second, it is a defined benefit plan. As we will discuss, this seemingly simple distinction makes an enormous difference.

CHAPTER LEARNING OBJECTIVESUpon completion of this chapter, you should be able to:

Describe the types and characteristics of qualified employee plans;

Explain the limits imposed on qualified employee plan contributions and benefits;

Describe the requirements applicable to qualified employee plan loans; and

Explain the rules governing rollovers to and from qualified employee plans.

Describe the requirements applicable to qualified employee plan loans and their tax treatment;

Apply the federal tax laws to qualified employee plan contributions and distributions;

List the principal types of annuities and their characteristics; and

Describe how annuity contributions and distributions are taxed.

DEFINED BENEFIT PLANSA qualified employee plan that is designed to provide participants with a definite benefit at retirement is known as a defined benefit plan. The benefits that are provided by the plan determine the contributions that must be made to it. In simple terms - and without considering the effects of plan earnings - if an employer must accumulate $100,000 to fund a particular participant's income benefit beginning at his age 65 and the participant enters the plan at age 55, the employer must contribute $10,000 each year to the plan. ($10,000 annual contribution x 10 years = $100,000)

However, if the same participant entered the plan at age 45 (thereby giving the employer 20 years to accumulate the needed funds), the employer's annual contribution is cut in half. ($5,000 annual contribution x 20 years = $100,000) Plan earnings or losses will affect the amount that the employer must contribute to the plan each year. Because of that plan design, the length of the participant's accumulation period before he or she retires has a very significant effect on the size of the required contribution. Clearly, the shorter that the accumulation period is, the larger the contribution must generally be.

Each year, the contribution in a defined benefit plan will change - although, usually, only slightly - from the previous year. As a result of this variability, however, defined benefit plans must calculate the contribution needed to fund each participant's benefit that is promised by the plan. Furthermore, the calculation is repeated each year, taking into account the plan's past investment experience and assumptions about future participant compensation increases and plan investment performance.

Contributions to defined benefit plans are required each year and may change from year to year. Except for changes in the covered participants, the contribution changes are based principally on how well or how poorly plan assets perform and whether or not the performance meets the growth assumptions underlying the annual actuarial calculation. The employer assumes the investment risk in a defined benefit plan, and all contributions are generally made by the employer . The employer is charged with the responsibility to fund the plan adequately, despite the plan's investment experience. As a result, if the investment experience is good, the required employer contributions may decline; if it is bad, they will probably increase.

Since an employer must make the necessary contributions to adequately fund for the stated benefit, regardless of the participant's age at plan entry, a defined benefit plan's contributions are disproportionately higher for older employees than for younger employees. Because older entrants to the plan normally have fewer years of plan participation before they retire, a larger portion of annual contributions goes towards providing benefits for them. Although younger employees will receive their promised benefit, they are clearly not favored in terms of a defined benefit plan's allocation of contributions.

1

Defined Contribution Plans 9

•

•

•

•

•

•

•

•

•

•

Benefits under defined benefit plans are often, although not always, stated in terms of a percentage of the participant's final compensation. In such a case, the higher the level of the participant's compensation, the greater the plan contribution must be in order to be able to fund the participant's retirement income. To illustrate, assume that two employees, each age 45, participate in a defined benefit plan promising to pay a retirement income of 60% of their final compensation. Employee A earns $50,000 annually, and employee B earns $100,000 annually. Without considering their likely compensation growth, if each of these two employees continued to earn the same income until retirement, employee A could look forward to receiving a monthly retirement income of $2,500. ($50,000 X 60% = $30,000 / 12 months = $2,500) Employee B could expect to receive a monthly retirement income of $5,000 each month. Clearly, the employer would need to make substantially higher contributions - perhaps double the amount - to fund employee B's benefit.

DEFINED BENEFIT/401(K) PLANS

Defined benefit/401(k) hybrid plans are authorized for years after 2009. Under a defined benefit/401(k) hybrid plan, the sponsoring employer guarantees the benefit at retirement under the defined benefit portion of the plan. In addition to the defined benefit, however, the plan participant may increase his or her retirement savings through elective deferrals made to the 401(k) part of the plan.

Under current law, eligibility to sponsor a defined benefit/401(k) plan is limited to employers with at least 2 employees but no more than 500 employees, provided the plan meets certain benefit and contribution requirements. The defined benefit part of the plan must provide a retirement benefit of at least a) 1% of plan participants' final average compensation multiplied by years of service, or b) 20% of final average compensation. Under the 401(k) portion of the plan, the plan must provide for an automatic employer matching contribution arrangement of 4% of participant compensation.

DEFINED CONTRIBUTION PLANSIt is no secret that defined benefit plans tend to be fairly complicated and somewhat more expensive to administer than many other qualified employee plans. In contrast, defined contribution plans are generally simpler than defined benefit plans. For these defined contribution plans, there are generally no actuarial calculations required to determine contributions for each participant, nor is there any stated benefit provided by the plan. Instead of a stated benefit the employer must provide, the plan is couched in terms of the employer's contribution.

Falling into the category of defined contribution plans are:

Money purchase pension plans;

Target benefit plans;

Profit sharing plans;

Thrift plans;

401(k) plans;

403(b) tax sheltered annuity plans;

Stock bonus plans;

Employee stock ownership plans (ESOPs);

Simplified employee pensions (SEPs); and

Savings incentive match plans for employees (SIMPLEs)

Rather than being determined by the benefit that will be provided at retirement—the case in defined benefit plans—contributions to defined contribution plans are simply made as required by the plan formula and are generally based on the participant's compensation. For example, a defined contribution plan's formula may state that the employer is required to make contributions equal to 10% of a participant's compensation. As a result, the ultimate value of the

10 Chapter 1 - Qualified Retirement Plans

retirement benefit provided by the plan is based on the value of the participant's account balance at that time. If the participant has an account balance of $500,000 at retirement and chooses a monthly benefit, the monthly benefit might be $4,000; if the account balance is $625,000, the benefit might be $5,000 a month.

Since the benefit at retirement in a defined contribution plan depends principally on the performance of the plan assets, the participant—rather than the employer—assumes all investment risk. Because it is impossible to determine the future investment performance of the plan assets with any certainty, the defined contribution retirement benefit is unknown. Furthermore, in certain profit sharing plan designs, under which an employer may make discretionary contributions, future contributions are also unknown. In these defined contribution plans to which contributions are discretionary, the ultimate benefit at retirement is impossible even to estimate.

Participants in defined contribution plans may have the option of directing the investment of their own plan account balances; a well-known example of this type of plan is a 401(k), wherein the participant has the right to allocate his or her elective deferrals and matching employer contributions to a wide range of investment options. Regardless of who has the right and duty to direct individual account investment, the defined contribution plan participant's benefit may be higher than he or she expected if the plan investments perform well. If they perform more poorly than expected, ultimate plan benefits may be lower than anticipated.

INDIVIDUAL PARTICIPANT ACCOUNTS CHARACTERIZE DEFINED CONTRIBUTION PLANS

Individual accounts are the defining feature of defined contribution plans, and such an account is established for each participant. One of the benefits of individual account creation is that participants generally have a better understanding and appreciation of the plan. (Because of the nature and complexity of a defined benefit plan, the retirement benefit is often a complete mystery for the majority of participants until just prior to their retirement.) Furthermore, contributions are also easily understood by the defined contribution plan participants. They are typically stated as a fixed dollar amount or a fixed percentage of employee compensation and—except in the case of discretionary contributions—must be made at the same level each year.

Since younger participants at the time the defined contribution plan begins generally have a longer period of time until retirement, the magic of compound earnings can make a substantial difference in the amount accumulated at retirement for them. As a result, the benefits at retirement in a defined contribution plan generally are greater for younger participants. A defined contribution plan does not favor employees who are older at the time that they become covered under the plan; these older employees will usually have fewer years until retirement during which plan assets can grow.

TARGET BENEFIT PLANS

Defined benefit plans are generally preferred by older plan participants because they usually receive the lion's share of the contribution allocation. However, better-than-expected plan investment performance in a defined benefit plan doesn't increase the participant's benefit. Instead, it just reduces the employer's future cost.

A target benefit plan, however, provides much of the benefit to the older participant that he or she finds in a defined benefit plan but also permits the benefit to increase if plan performance exceeds expectations. (The downside of that plan design, from the participant's perspective, is that the actual benefit at retirement may also be less than the "target" benefit if plan assets perform poorly.)

Not unexpectedly, a target benefit plan can be seen as a hybrid of a defined benefit and a defined contribution plan. It begins by looking like a defined benefit plan. At plan inception, an annual contribution level is calculated that, based upon plan assumptions, will provide the target benefit at retirement, much like a defined benefit plan. It is important to remember, however, that this is a target benefit rather than a defined benefit, and this distinction is critical. The

Defined Contribution Plans 11

employer does not guarantee that the target benefit plan will actually produce the target benefit (unlike a defined benefit plan in which the employer does guarantee the benefit).

At plan inception, the actuarial calculation determines the level, fixed contribution that will be made. This contribution will be made to the plan each year for each plan participant. It is important to understand that once this calculation is made to determine the fixed level contributions to the target benefit plan, there are no additional actuarial calculations that are required. Now that the level of contributions is fixed, the target benefit plan behaves like a defined contribution plan rather than a defined benefit plan. The plan simply accumulates funds in individual accounts that are established for the plan participants. Each participant's benefit at retirement depends on the amount in his or her account.

Target Benefit Plan Investment Risk

The investment risk in a target benefit plan is borne by the plan participant just as he or she would bear it in any defined contribution plan, such as a money purchase pension plan. In the event plan investments perform better than at the rate assumed in the actuarial calculation that was made to determine the contribution level, he or she will have a higher benefit than the target benefit stated in the plan. In contrast, if plan investments perform more poorly, the benefit will be lower than the target benefit stated in the plan. An important thing to remember with respect to target benefit plans is that the employer is not required to increase its contributions to make up for poor investment performance, nor may it reduce its contributions in years when investment performance exceeds assumptions (both of which apply to defined benefit plans).

Target Benefit Plans Favor Older Plan Participants

Although target benefit plans have elements of both defined benefit and defined contribution plans, they generally favor older plan participants; however, they also provide some advantages to younger plan participants. Because older plan participants have fewer years in which to accumulate the needed funds, older participants will receive a greater percentage allocation of the fixed annual target benefit plan contribution for each dollar of target benefit at retirement. As we noted earlier, however, actual investment results will determine the benefit at retirement, which may be larger or smaller than the target benefit.

The benefit to younger participants comes from their having a longer period for their contributions to earn tax-deferred interest and compound in a tax-deferred environment. A target benefit plan has favorable elements for every party to the plan: the employer gets a break because it doesn't bear the risk of poor investment performance; the older employee receives a generally greater allocation of each contribution, and the younger employee can look forward to a longer period of tax-deferred accumulation and increased benefits following better-than-anticipated performance.

PROFIT SHARING PLANS

A profit sharing plan is one of the important types of defined contribution plans. For many companies that experience substantial cash flow variations from time to time a profit sharing plan, because of its discretionary contributions, may offer needed flexibility.

Profit sharing plans can also be suitable in situations in which an employer wants to provide an incentive to employees. In such a case, an employer may be able to motivate employees to greater productivity and increase company profits by funding plan contributions based on a particular level of profits. Like all defined contribution plans, benefits under a profit sharing plan depend on the value of the participant's account balance.

Traditional Profit Sharing Plans

A substantial benefit of profit sharing plans, from the point of view of the plan sponsor, is that contributions are not required each and every year as they are in pension plans. Under the law, profit sharing plan contributions simply must be "substantial and recurring" for the plan to retain its qualified status. The amount of profit sharing plan

12 Chapter 1 - Qualified Retirement Plans

contribution to be made may be determined by the plan sponsor each year. As in the case of other defined contribution plans, each participant has an individual account. Frequently, participants may direct the investment of their own account balances—a characteristic normally observed in 401(k) plans.

Just as they do in other defined contribution plans, participants in profit sharing plans bear the investment risk with respect to their plan assets. As a result, benefits received by participants in the plan are affected not only by the level of contributions made over the years but also by the performance achieved by the investments to which the plan participant's account is allocated.

Since the allocation of employer contributions in a traditional profit sharing plan normally depends solely on the participant's compensation level rather than on his or her age, traditional profit sharing plans generally favor younger participants. Although there is a limit to the amount of compensation that is considered for purposes of the contribution allocation, the higher that an individual's compensation is, the greater his or her annual contribution allocation of the employer's contribution will be.

Age-Based Profit Sharing Plans

The defining characteristics of a traditional profit sharing plan include its allocation of contributions based solely on the participants' compensation and the relationship of the compensation to the plan sponsor's overall payroll.

Under a traditional profit sharing plan, an employer could not make a greater allocation of the plan's contributions based on a participant's age; only compensation counted. An age-based profit sharing plan changes that. Age-based profit sharing plans enable a plan sponsor to provide disproportionately higher contributions for older participants.

Thus, age-based profit sharing plans favor older plan participants over younger participants. They accomplish this favoring by using both compensation and age as bases for allocating employer contributions to the plan. Age-based profit sharing plans are very similar in their allocation concept to target benefit plans.

401(K) PLANS

Although the funding of retirement plans has traditionally been seen as the responsibility of employers, the perception of the proper funding responsibility began to change dramatically in the decade of the 1980s. During that period, many employers scrambled to shore up their bottom lines by downsizing their employee population and jettisoning their costly pension plans in favor of the then-new 401(k) plans. These 401(k) plans enable an employer to provide employees with an opportunity to make pre-tax contributions (or after-tax contributions and tax-free qualified distributions in the case of designated Roth accounts) to a plan in which earnings are tax-deferred.

Also referred to as a cash or deferred arrangement (CODA), a 401(k) plan is funded primarily by employee salary deferrals, rather than employer contributions. By installing a 401(k) plan, an employer may limit its costs principally to certain expenses for plan administration. Even these plan administration expenses, however, may be borne by plan participants if the employer allocates these expenses to participant accounts.

Many employers offer to match some percentage of each participant's deferred amount. This employer matching is designed to encourage plan use by employees. Although an employer's matching of employee deferrals is certainly a benefit to participants, it is seldom altruistic. Instead, it helps to increase the amount of salary that may be deferred by higher-paid participants, such as business owners and executives. Various tests that must be performed by 401(k) plan administrators limit the amount that may be deferred by higher-paid participants to a percentage of the amounts deferred by lower-paid participants. Because of this mandated attempt to limit discrimination, business owners generally have a vested interest in encouraging lower-paid employees to participate.

Largely because of the flexibility of 401(k) plans and their complex testing requirements, their administration has been relatively complicated and expensive. The level of required plan administration has been reduced, however, with the introduction of SIMPLE 401(k)s.

Defined Contribution Plans 13

•

•

401(k) plan participants have considerable flexibility in determining annual plan deferral amounts as well as many choices in their investment. These deferral amounts, known as elective deferrals, are expressed as a percentage of each participant's compensation. The plan participant determines the amount of compensation to be deferred within IRS limits that permit a regular deferral of up to $19,500 and a catch-up contribution of up to $6,500 for age 50 and older participants in 2021.

In order to meet the safe harbor requirements that eliminate the plan sponsor's fiduciary responsibility for investment performance, the 401(k) plan must provide at least three diversified investment options. Each of these options must offer plan participants a different risk and return profile.

Because 401(k) plan sponsors cannot make larger matching contributions to older participants based on age, these plans tend to favor younger employees. As we noted in our discussion of other defined contribution plans, younger employees benefit from having a longer period of time over which their deferrals and the employer's matching contributions can grow and compound in a tax-deferred environment.

The plan's limitation on contributions severely curtails the highly-paid participant's use of a 401(k) plan to accumulate the needed retirement income, since a lower-paid employee may make deferrals of a larger percentage of compensation than a higher-paid one. For example, if the current elective deferral limit is $19,500 in 2021, an employee earning $95,000 could defer 20% of salary and meet the deferral limit. A key employee earning $195,000 can defer the same $19,500 in 2021. However, for that key employee, the deferral is only 10% of his or her pay.

403(B) TAX SHELTERED ANNUITY PLANS

A tax sheltered annuity plan, often referred to as a 403(b) plan, is a retirement plan for employees of:

State and local governments, but only for employees that are performing services for an educational organization, such as a public school; and

Certain income tax-exempt organizations, usually referred to as "501(c)(3) organizations," described in the Internal Revenue Code.

Eligible employees electing to participate in their employer's 403(b) plan sign a salary reduction agreement to make elective deferrals to their plan, very similar to the elective deferral agreement used by 401(k) plan participants. Similar to a 401(k) plan participant, a 403(b) plan participant determines the amount of compensation to be deferred within IRS limits that permit a regular deferral of up to $19,500 and a catch-up contribution of up to $6,500 for age 50 and older participants in 2021.

Although the reference to an "annuity" in the plan's name might suggest that a 403(b) plan participant's elective deferral may be allocated only to an annuity, such is not the case. In fact, tax sheltered annuity plan participants may allocate elective deferrals to either an annuity or a custodial account. If allocated to a custodial account, the funds may be used to purchase mutual fund shares.

SIMPLIFIED EMPLOYEE PENSION (SEP)

A simplified employee pension (SEP) is nothing more than an employer's agreement to contribute to its employees' IRAs that are maintained by them. The plan can be adopted by an employer by completing a fairly simple IRS form, rather than the much more complicated procedure involved in installing a qualified retirement plan. As in all such tax-favored plans, the plan must be non-discriminatory.

A SEP, because of its utter simplicity, is significantly easier and less expensive to install and administer than a qualified retirement plan. As a result, the need for the various consultants normally associated with the establishment of a qualified retirement is minimized; further reducing the employer's cost. Furthermore, the employer's contribution is discretionary, enabling the employer to discontinue contributions in times of reduced cash flow.

14 Chapter 1 - Qualified Retirement Plans

1.

2.

A SEP allows for higher contribution levels than traditional or Roth IRAs, has fewer restrictions than qualified retirement plans and, unlike SIMPLEs—the tax-favored plan next addressed—there is no limit on the number of employees in the plan. Employer contributions are entirely discretionary, and employees are immediately 100% vested in their accounts.

SAVINGS INCENTIVE MATCH PLAN FOR EMPLOYEES (SIMPLE)

The fundamental concept behind savings incentive match plans for employees (SIMPLEs) is identical to that for SEPs: plan design and administrative convenience result in a plan that is relatively inexpensive to implement and produces employer savings when compared to traditional qualified employee plans. Unlike SEPs, however, eligibility to establish a SIMPLE is restricted to small employers.

In the context of SIMPLE plans, the term "small employer" means an employer with 100 or fewer employees earning at least $5,000 annually. For purposes of this small employer limitation, all employees who are employed at any time during the calendar year are considered, even those employees who are excludable or ineligible to participate. In addition to regular employees that must be counted towards the 100 or fewer employee limitation, certain self-employed individuals who received earned income from the employer during the year must also be counted. However, an employer that ceases to be eligible—because of an increase in the number of employees, for example—after having installed and maintained a SIMPLE for at least 1 year will continue to be treated as eligible for the following 2 years.

The eligible employer must not only meet the "small employer" definition, the SIMPLE must generally be the employer's sole retirement plan. A SIMPLE is not subject to nondiscrimination or top-heavy rules and may be in the form of a SIMPLE IRA or a SIMPLE 401(k).

Contributions to a SIMPLE may come from two sources:

Elective contributions by employees, and

Employer contributions.

Employee elective contributions are made under a qualified salary reduction arrangement, which is a written arrangement under which employees that are eligible to participate may elect to receive payments in cash or contribute them to the plan.

Elective contributions to a SIMPLE are limited to no more than $13,500 and catch-up contributions for employees age 50 or older are limited to no more than $3,000 in 2021. Elective contributions to a SIMPLE are counted in the overall limit on elective deferrals that may be made by any individual. The practical result of the overall limit on elective deferrals is to limit the amount that may be contributed by an employee who is covered under the plans of two or more employers. For example, an employee, age 45, in a SIMPLE would be able to make elective contributions of $13,500 in 2021. However, if that employee was also employed by an employer that maintained a 401(k) plan, he or she would be permitted only to defer up to $6,000 ($19,500 overall limit – $13,500 SIMPLE contributions) in the 401(k) plan in 2021, because of the $19,500 overall limit on elective deferrals in 2021.

Each year, each employee that is eligible to participate in a SIMPLE can elect, during the 60-day period preceding that year, to participate in the salary reduction arrangement or modify the amount of his or her elective contribution.

SUMMARY

Qualified employee plans are classified as either defined benefit plans or defined contribution plans. A defined benefit plan guarantees a definitely determinable benefit at retirement. In contrast, a defined contribution plan does not guarantee a particular level of benefit at retirement. Instead, a defined contribution plan is couched in terms of the sponsoring employer's contributions to the plan.

Introduction 15

A participant's compensation and age are the principal determinants of employer contributions under a defined benefit plan. Because of that characteristic of the plan, a defined benefit plan generally requires disproportionately-larger employer contributions for older, higher paid employees. Significantly larger portions of the employer's annual contributions will go toward providing benefits for older employees with fewer years of plan participation over which to accrue their benefits. In plain terms, these defined benefit plans favor older, higher paid employees.

Defined contribution plans generally produce higher benefits at retirement for longer-service employees. Thus, such plans tend to favor younger participants (who are likely to have longer periods of service by the time they retire). Since they have a longer period of employment and plan participation, their accounts can grow and compound in a tax-deferred environment for a greater time period.

A target benefit plan, by offering benefits characteristic of both defined benefit and defined contribution plans, can be seen as a hybrid plan. Although a target benefit plan is technically a defined contribution plan, it begins by resembling a defined benefit plan through its greater allocation of contributions to older employees. However, the target benefit plan acts like a defined contribution plan in accumulating individual account balances.

Generally similar to other defined contribution plans, younger plan participants are favored in traditional profit sharing plans since they have a longer period during which to accumulate benefits. Furthermore, their contribution allocation is not reduced because of their younger age as it is in defined benefit plans.

A profit sharing plan variation, known as an age-based profit sharing plan, generally provides greater contributions to older plan participants than traditional profit sharing plans. In these age-based profit sharing plans, a disparity in the participants' ages is used to provide a larger portion of the allocation of employer profit sharing plan contributions to older plan participants.

A popular qualified employee plan for employers interested in providing employees an opportunity to make their own pre-tax contributions (or after-tax contributions and tax-free qualified distributions) to a tax-favored plan is a 401(k) plan. A 401(k) plan is funded principally by employee salary deferrals, rather than employer contributions, although the plan may call for the employer to match certain participant contributions. This characteristic moves the burden of funding retirement to employees and limits employer costs.

A tax sheltered annuity plan, also referred to as a 403(b) plan, is similar in operation and contribution limits to a 401(k) plan. Participation in a 403(b) plan is limited to employees of 501(c)(3) tax-exempt organizations and public schools. Under the plan, employees choosing to participate make elective deferrals that are allocated to the purchase of annuities and/or mutual funds.

Simplified employee pension plans permit employers of any size to sponsor a tax-favored retirement plan. These plans are comprised of employee-owned individual retirement accounts to which an employer may make discretionary contributions. Their principal attractiveness to employers is their inexpensiveness to install and their lack of an annual contribution commitment.

Savings Incentive Match Plans for Employees—plans better known as SIMPLEs—enable employers with no more than 100 employees to establish and maintain a tax-favored retirement plan at minimal administrative cost. Although the employer is required to make annual contributions (rather than discretionary contributions as under a SEP), it is allowed a certain flexibility to make either matching or nonelective contributions. The principal attractiveness of a SIMPLE to an employer is its lower administrative costs and its modest level of required contributions.

CHAPTER 2 - TAX TREATMENT OF QUALIFIED PLANS

INTRODUCTIONAlthough qualified employee plans meet several important non-tax employee and employer objectives, their tax-favored status weighs heavily on decisions of employers to offer such plans and on the decisions of employees to participate in them. In this chapter we will examine the tax benefits of qualified plans.

16 Chapter 2 - Tax Treatment of Qualified Plans

•

•

•

•

•

•

CHAPTER LEARNING OBJECTIVESUpon completion of this chapter, you should be able to:

Describe the tax treatment of loans from qualified plans; and

Apply the federal tax laws to qualified employee plan contributions and distributions.

List the principal types of annuities and their characteristics; and

Describe how annuity contributions and distributions are taxed.

CONTRIBUTIONS TO QUALIFIED EMPLOYEE PLANSFunding plan participants' income in retirement requires contributions. Depending on the qualified employee plan, those contributions may be made by employers and/or plan participants. However, regardless of by whom made, the tax benefits resulting from qualified employee plan contributions are important motivating factors in the decision of an employer to sponsor such a plan and the desire of an employee to participate.

EMPLOYER PLAN CONTRIBUTIONS

Although 401(k) plans and 403(b) plans have moved much of the responsibility for funding retirement income from the shoulders of employers to those of employees, many plans rely heavily or entirely on employer contributions. Such employer contributions are deductible by the employer within specified limits. The limits on deductible employer contributions vary, however, depending on whether the contributions are made to a defined benefit plan or a defined contribution plan.

An employer's contribution to a qualified employee plan generally is deductible only in the taxable year paid. However, employers are deemed to have made a contribution to a plan in the preceding tax year if the payment is on account of that year and is made no later than the due date, including extensions, of the employer's tax return.

Defined Benefit Plan Limit on Deductible Employer Contributions

As noted in Chapter 1, a defined benefit plan promises the plan participants a specified benefit at retirement. The contribution to the plan—except in the case of a defined benefit/401(k) plan—is normally made entirely by the employer.

In order for the employer to meet its defined benefit plan promises, the employer must contribute to the plan an amount that is sufficient to fully fund the plan participants' benefits at retirement. As long as the benefits being funded do not exceed the IRS-imposed limits, the employer's contribution to the plan is entirely deductible.

Deductible contributions to a defined benefit plan are structured to provide level funding over an employee's service with the employer. Although the plan actuary provides a plan valuation to the employer that specifies the amount of its annual contribution, the maximum employer contribution to fund any participant's benefit at normal retirement cannot exceed the lesser of:

100% of the plan participant's compensation; or

A specified dollar amount that generally increases annually based on a cost of living adjustment.

The maximum specified dollar amount of benefit that may be funded in a defined benefit plan in 2021 is $230,000.

Defined Contribution Plan Limit on Deductible Employer Contributions

Employer deductible contributions to a defined contribution plan are generally limited to no more than 25% of the compensation paid during the employer's taxable year to the employees participating in the plan. Employee salary deferrals are not included in the 25% of compensation limitation.

2

Contributions to Qualified Employee Plans 17

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

You may recall from Chapter 1 that the category of qualified employee plans that are defined contribution plans include:

Money purchase pension plans;

Target benefit plans;

Profit sharing plans;

Thrift plans;

401(k) plans;

403(b) tax-sheltered annuity plans;

Stock bonus plans;

Employee stock ownership plans (ESOPs);

Simplified employee pensions (SEPs); and

Savings incentive match plans for employees (SIMPLEs).

With the exception of contributions to SIMPLE plans, contributions to SIMPLE plans are limited to no more than $13,500 in 2021, the deductible contribution to a defined contribution plan for a plan participant may not exceed:

100% of the plan participant's compensation; or

A specified dollar amount that generally increases annually based on a cost of living adjustment.

The specified dollar amount for employer contributions to a defined contribution plan in 2021 is $58,000.

EMPLOYEE PLAN CONTRIBUTIONS

Employee contributions to employer retirement plans are generally known as "elective deferrals" and are characteristic of 401(k) plans and 403(b) tax-sheltered annuity plans. Unless elective deferrals are directed to a designated Roth account in the plan, the funds deferred are allocated to the plan before income taxes are paid.

Plan participants are limited in the amounts they may defer under a 401(k) or 403(b) plan in any year to the lesser of:

100% of the plan participant's compensation; or

A specified dollar amount that generally increases annually based on a cost of living adjustment.

The specified dollar amount in 2021 is $19,500. The applicable limit on elective deferrals generally applies to the total of all elective deferral contributions (in the aggregate) made to such plans. Thus, the maximum elective deferral applies to the contributions made to 401(k) plans, 403(b) tax-sheltered annuity plans, and other plans to which a plan participant may make such contributions. Contributions to a designated Roth account (see Designated Roth Accounts below) are subject to the same elective deferral limit.

403(b) Plan Contribution Limit Increased for Long-Service Employees

The limit on elective deferrals may be increased for certain 403(b) tax-sheltered annuity participants. An employee may make additional elective deferrals provided he or she has had at least 15 years of service with:

An educational institution;

A hospital;

A home health service agency;

A church;

A convention or association of churches; or

A health and welfare agency.

3

4

18 Chapter 2 - Tax Treatment of Qualified Plans

•

•

•

•

•

•

•

•

•

The increase to the regular limit on elective deferrals is limited to the least of the following three amounts:

$3,000;

$15,000 less any amounts taken under this special increase rule in prior years; or

The amount by which $5,000 multiplied by the participant's years of service exceeds the total of salary reduction or elective deferrals made in prior years to a 403(b), 401(k) plan, SIMPLE IRA, or a SEP and, for years after 1988, to a Section 457 (deferred compensation for state and local governments and tax-exempt organizations) plan.

Catch-up Contributions for Participants Age 50 or Older

Participants in 401(k) plans and 403(b) tax-sheltered annuity plans that are age 50 or older by the end of the year may make catch-up contributions. The catch-up provision in the law permitting increased contributions by age 50 and older participants increases the otherwise applicable dollar limit on elective deferrals.

Accordingly, the additional elective deferral that age 50 and older participants in a 401(k) or 403(b) tax-sheltered annuity plan are permitted is equal to the lesser of:

The applicable catch-up dollar amount; or

The amount of the participant's compensation (reduced by any other elective deferrals for the year).

The applicable dollar amount for 2021 catch-up contributions for a 401(k) or 403(b) tax-sheltered annuity plan is $6,500 and is indexed for inflation in subsequent years.

Note: The applicable dollar amount for 2021 catch-up contributions for a SIMPLE plan is $3,000 and is indexed for inflation in subsequent years.

Designated Roth Accounts

401(k) plans and 403(b) plans may offer plan participants the opportunity to allocate some or all their elective deferrals to a designated Roth account. These plans are authorized, but employers are not required to offer such accounts.

Employee elective deferrals to a 401(k) or 403(b) plan are contributed to the plan on a before-tax basis unless directed to a designated Roth account in the plan. If directed to a designated Roth account, the amount so directed is currently taxable to the plan participant. As will be discussed later in this chapter, qualified distributions from Roth accounts are tax-free.

LIFE INSURANCE IN A QUALIFIED EMPLOYEE PLAN

A qualified employee plan may contain life insurance on the plan participant. Using life insurance in a plan:

Requires that certain requirements be met; and

Affects taxation.

Requirements for Plan Life Insurance

The primary function of a qualified employee plan is to provide retirement benefits. Thus, in order for life insurance to be included in a qualified employee plan, it must be "incidental" to the plan's principal purpose. In order to meet the incidental test, life insurance contained in a qualified employee plan must meet one of the following requirements:

The cost of the life insurance must be less than 25% of the cost to provide all benefits under the plan; or

The death benefits provided under the life insurance do not exceed 100 times the monthly retirement income provided by the plan.

Life Insurance Premiums

If life insurance that meets one of the incidental tests is included in the plan, the premiums for the coverage are paid on a before-tax basis. The insured plan participant is required each year to include the value of the pure death benefit,

Distributions from a Qualified Employee Plan 19

•

•

•

•

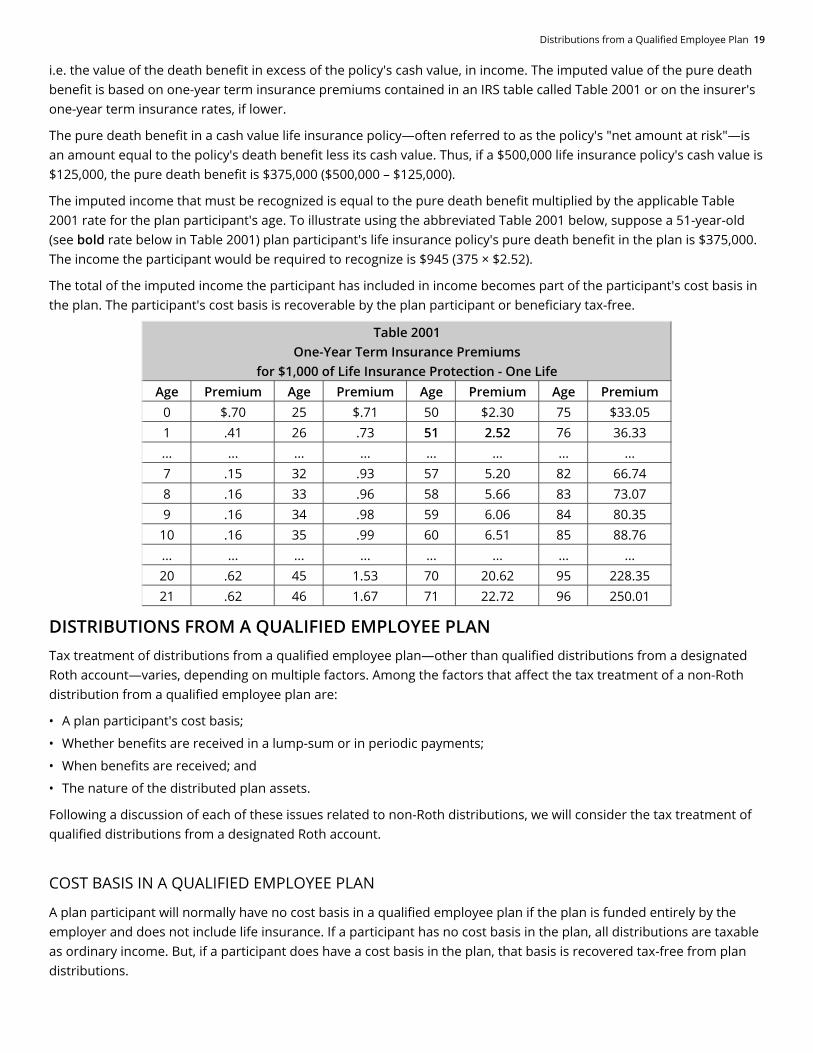

i.e. the value of the death benefit in excess of the policy's cash value, in income. The imputed value of the pure death benefit is based on one-year term insurance premiums contained in an IRS table called Table 2001 or on the insurer's one-year term insurance rates, if lower.

The pure death benefit in a cash value life insurance policy—often referred to as the policy's "net amount at risk"—is an amount equal to the policy's death benefit less its cash value. Thus, if a $500,000 life insurance policy's cash value is $125,000, the pure death benefit is $375,000 ($500,000 – $125,000).

The imputed income that must be recognized is equal to the pure death benefit multiplied by the applicable Table 2001 rate for the plan participant's age. To illustrate using the abbreviated Table 2001 below, suppose a 51-year-old (see bold rate below in Table 2001) plan participant's life insurance policy's pure death benefit in the plan is $375,000. The income the participant would be required to recognize is $945 (375 × $2.52).

The total of the imputed income the participant has included in income becomes part of the participant's cost basis in the plan. The participant's cost basis is recoverable by the plan participant or beneficiary tax-free.

Table 2001One-Year Term Insurance Premiums

for $1,000 of Life Insurance Protection - One LifeAge Premium Age Premium Age Premium Age Premium

0 $.70 25 $.71 50 $2.30 75 $33.051 .41 26 .73 51 2.52 76 36.33... ... ... ... ... ... ... ...7 .15 32 .93 57 5.20 82 66.748 .16 33 .96 58 5.66 83 73.079 .16 34 .98 59 6.06 84 80.35

10 .16 35 .99 60 6.51 85 88.76... ... ... ... ... ... ... ...20 .62 45 1.53 70 20.62 95 228.3521 .62 46 1.67 71 22.72 96 250.01

DISTRIBUTIONS FROM A QUALIFIED EMPLOYEE PLANTax treatment of distributions from a qualified employee plan—other than qualified distributions from a designated Roth account—varies, depending on multiple factors. Among the factors that affect the tax treatment of a non-Roth distribution from a qualified employee plan are:

A plan participant's cost basis;

Whether benefits are received in a lump-sum or in periodic payments;

When benefits are received; and

The nature of the distributed plan assets.

Following a discussion of each of these issues related to non-Roth distributions, we will consider the tax treatment of qualified distributions from a designated Roth account.

COST BASIS IN A QUALIFIED EMPLOYEE PLAN

A plan participant will normally have no cost basis in a qualified employee plan if the plan is funded entirely by the employer and does not include life insurance. If a participant has no cost basis in the plan, all distributions are taxable as ordinary income. But, if a participant does have a cost basis in the plan, that basis is recovered tax-free from plan distributions.

20 Chapter 2 - Tax Treatment of Qualified Plans

•

•

•

•

•

1.

2.

3.

•

•

•

•

A participant's cost basis in a qualified employee plan generally consists of the sum of the following amounts:

The total nondeductible contributions made by the employee;

The sum of the annual one year term costs of life insurance protection included by the participant as taxable income;

Any other employer contributions that have already been taxed to the participant;

Certain employer contributions attributable to foreign services performed before 1963; and

The amount of any plan loans included in a participant's income as a taxable distribution.

HOW BENEFITS ARE DISTRIBUTED

Benefits payable under a qualified employee plan may be received by the plan participant in a lump-sum or in periodic payments. The tax treatment varies, depending on the manner in which the distribution is received.

Lump Sum Plan Distributions

A distribution from a qualified employee plan is a lump sum distribution if it meets all of the following conditions:

It is made in one taxable year;

It consists of the entire plan balance to the credit of an employee; and

It is payable on account of the employee's death, after the employee attained age 59 1/2, or on account of the employee's separation from service.

Certain eligible employees may elect to be taxed on the plan distribution in excess of cost basis by electing ten-year averaging and special treatment of certain capital gains. An employee eligible for this special tax treatment is one who attained age 50 before January 1, 1986.

An eligible plan participant choosing 10-year averaging is required to make a special averaging election by filing Form 4972 with his or her tax return. The election may be made only once and must apply to all lump sum distributions received during the year. In addition, an eligible participant may elect capital gain treatment for the portion of a lump sum distribution allocable to pre-974 plan participation.

A plan participant who elects to receive a lump sum distribution but who is ineligible for special tax treatment must include in income in the year received the amount of his or her distribution that exceeds basis, if any.

Plan Distributions as Periodic Payments

Taxation of periodic payment distributions—distributions as an annuity, in other words—from a qualified plan may vary, depending on whether the plan participant has a cost basis in the plan. In general, a plan participant can recover his or her cost basis tax-free over the period he or she receives periodic payments. The amount of each periodic payment that exceeds the portion representing the participant's cost basis is taxable as ordinary income.

Thus, based on whether or not a participant has a cost basis, periodic payments may be:

Fully taxable; or

Partly taxable.

Fully Taxable Periodic Payments

For most taxpayers receiving periodic payments from a qualified plan, the payments are fully taxable because they have no cost basis in the plan. Plan participants for whom periodic payments are fully taxable are those who:

Paid nothing for their qualified plan benefits;

Made contributions to the qualified plan only on a tax-deferred basis; or

Distributions from a Qualified Employee Plan 21

•

1.

a.

b.

c.

2.

a.

b.

Already recovered all their after-tax contributions tax-free in prior years.

Partly Taxable Periodic Payments

A taxpayer who has a cost basis in the qualified plan under which periodic payments are being received can exclude part of each periodic payment from income as a tax-free recovery of his or her cost. The part of each periodic payment that is tax-free is figured when the taxpayer's periodic payments begin and remain the same amount each year even if the amount of the periodic payments changes.

If the taxpayer's annuity starting date—the date on which periodic payments began, in other words—is after 1986, the total amount of the income he or she can exclude over the years as a tax-free recovery of cost is limited to the participant's cost basis in the plan. When the total cost basis has been recovered, all further periodic payments are fully taxable. In contrast, if the taxpayer's annuity starting date is 1986 or earlier the part of each periodic payment that is tax-free will continue even after the taxpayer has recovered his or her entire cost basis.

Regardless of the taxpayer's annuity starting date, any unrecovered cost at the taxpayer's death is allowed as a miscellaneous itemized deduction on the decedent's final tax return. The miscellaneous itemized deduction for the balance of cost, however, is not a deduction that was subject to the 2% of AGI limit.

Figuring the Tax-Free Part of Periodic Payments - Simplified Method

Taxpayers must use the simplified method of figuring the tax-free part of periodic payments if the annuity starting date is after November 18, 1996, and the taxpayer meets both of the following conditions:

The taxpayer receives his or her pension or annuity payments from a:

Qualified employee plan,

Qualified employee annuity, or

403(b) tax-sheltered annuity plan; and

On the taxpayer's annuity starting date, he or she was:

Younger than age 75, or

Entitled to less than 5 years of guaranteed payments.

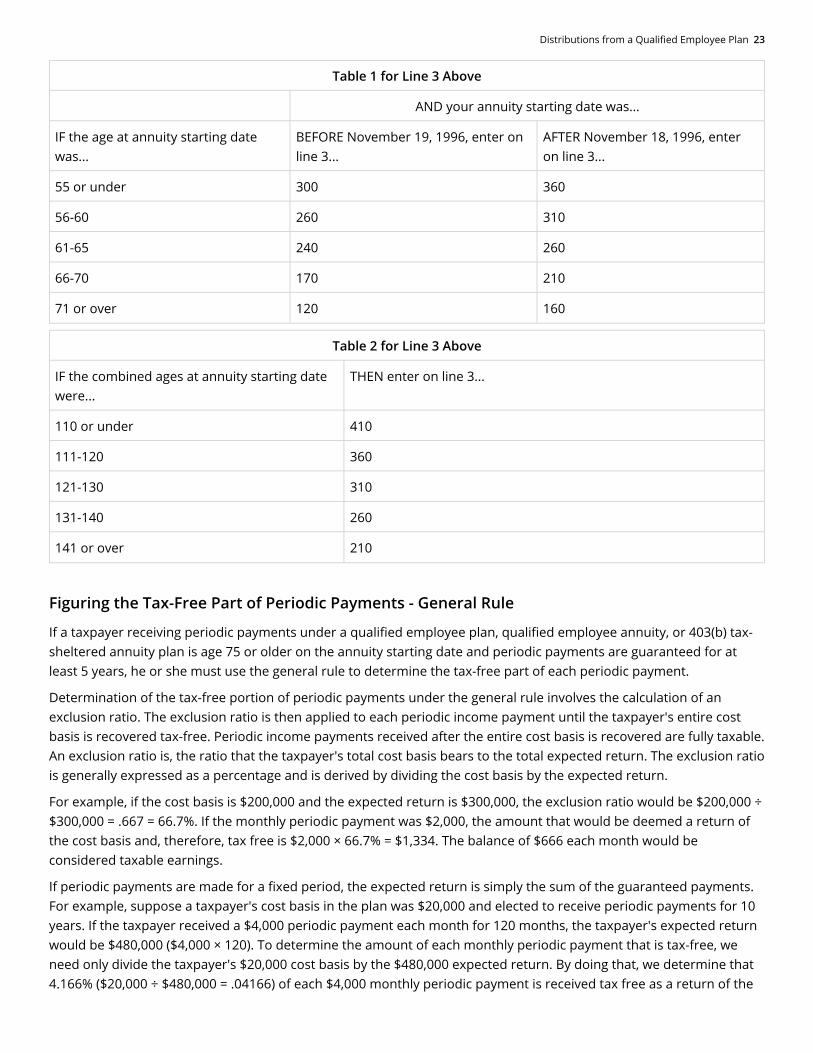

Under the simplified method, a taxpayer figures the tax-free part of each periodic payment received by dividing his or her cost by the total number of anticipated payments. If periodic payments will be made for a specified period—5 or 10 years, for example—the taxpayer's cost should simply be divided by the number of monthly payments to be received. The result is the part of each monthly payment that is tax-free as a recovery of basis.

For periodic payments that are payable for the life or lives of a taxpayer or taxpayers, the number by which the taxpayer's cost must be divided depends on the taxpayer's age at the annuity starting date and whether the periodic payments continue for one or two lives. The applicable numbers to use are given on the simplified method worksheet that is contained in Publication 575, Pension and Annuity Income, and reproduced below. Determining the part of lifetime periodic payments that is tax-free is simple if the worksheet is used.

Simplified Method Worksheet:

22 Chapter 2 - Tax Treatment of Qualified Plans

1.Enter the total pension or annuity payments received this year. Also add this amount to the total for Form 1040, 1040-SR, or 1040-NR line 5a.

1. ____________

2. Enter your cost in the plan (contract) at the annuity starting date plus any death benefit exclusion.*

Note: If your annuity starting date was before this year and you completed this worksheet last year, skip line 3 and enter the amount from line 4 of last year's worksheet on line 4 below (even if the amount of your pension or annuity has changed). Otherwise, go to line 3.

2. ____________

3. Enter the appropriate number from Table 1 below. But if your annuity starting date was after 1997 and the payments are for your life and that of your beneficiary, enter the appropriate number from Table 2 below.

3. ____________

4. Divide line 2 by the number on line 3. 4. ____________

5. Multiply line 4 by the number of months for which this year's payments were made. If your annuity starting date was before 1987, enter this amount on line 8 below and skip lines 6, 7, 10, and 11. Otherwise, go to line 6.

5. ____________

6. Enter any amounts previously recovered tax-free in years after 1986. This is the amount shown on line 10 of your worksheet for last year.

6. ____________

7. Subtract line 6 from line 2. 7. ____________

8. Enter the smaller of line 5 or line 7. 8. ____________

9. Taxable amount for year. Subtract line 8 from line 1. Enter the result, but not less than zero. Also, add this amount to the total for Form 1040, 1040-SR, or 1040-NR line 5b.

Note: If your Form 1099-R shows a larger taxable amount, use the amount figured on this line instead. If you are a retired public safety officer, see Insurance Premiums for Retired Public Safety Officers, earlier, before entering an amount on your tax return.

9. ____________

10. Was your annuity starting date before 1987?

Yes. STOP. Do not complete the rest of this worksheet.

No. Add lines 6 and 8. This is the amount you have recovered tax-free through 2021. You will need this number if you need to fill out this worksheet next year.

10. ___________

11. Balance of cost to be recovered. Subtract line 10 from line 2. If zero, you will not have to complete this worksheet next year. The payments you receive next year will generally be fully taxable.

* A death benefit exclusion (up to $5,000) applied to certain benefits received by employees who died before August 21, 1996.

11. ___________

Distributions from a Qualified Employee Plan 23

Table 1 for Line 3 Above

AND your annuity starting date was...

IF the age at annuity starting date was...

BEFORE November 19, 1996, enter on line 3...

AFTER November 18, 1996, enter on line 3...

55 or under 300 360

56-60 260 310

61-65 240 260

66-70 170 210

71 or over 120 160

Table 2 for Line 3 Above

IF the combined ages at annuity starting date were...

THEN enter on line 3...

110 or under 410

111-120 360

121-130 310

131-140 260

141 or over 210

Figuring the Tax-Free Part of Periodic Payments - General Rule

If a taxpayer receiving periodic payments under a qualified employee plan, qualified employee annuity, or 403(b) tax-sheltered annuity plan is age 75 or older on the annuity starting date and periodic payments are guaranteed for at least 5 years, he or she must use the general rule to determine the tax-free part of each periodic payment.

Determination of the tax-free portion of periodic payments under the general rule involves the calculation of an exclusion ratio. The exclusion ratio is then applied to each periodic income payment until the taxpayer's entire cost basis is recovered tax-free. Periodic income payments received after the entire cost basis is recovered are fully taxable. An exclusion ratio is, the ratio that the taxpayer's total cost basis bears to the total expected return. The exclusion ratio is generally expressed as a percentage and is derived by dividing the cost basis by the expected return.

For example, if the cost basis is $200,000 and the expected return is $300,000, the exclusion ratio would be $200,000 ÷ $300,000 = .667 = 66.7%. If the monthly periodic payment was $2,000, the amount that would be deemed a return of the cost basis and, therefore, tax free is $2,000 × 66.7% = $1,334. The balance of $666 each month would be considered taxable earnings.

If periodic payments are made for a fixed period, the expected return is simply the sum of the guaranteed payments. For example, suppose a taxpayer's cost basis in the plan was $20,000 and elected to receive periodic payments for 10 years. If the taxpayer received a $4,000 periodic payment each month for 120 months, the taxpayer's expected return would be $480,000 ($4,000 × 120). To determine the amount of each monthly periodic payment that is tax-free, we need only divide the taxpayer's $20,000 cost basis by the $480,000 expected return. By doing that, we determine that 4.166% ($20,000 ÷ $480,000 = .04166) of each $4,000 monthly periodic payment is received tax free as a return of the

24 Chapter 2 - Tax Treatment of Qualified Plans

•

•

•

•

•

•

1.

2.

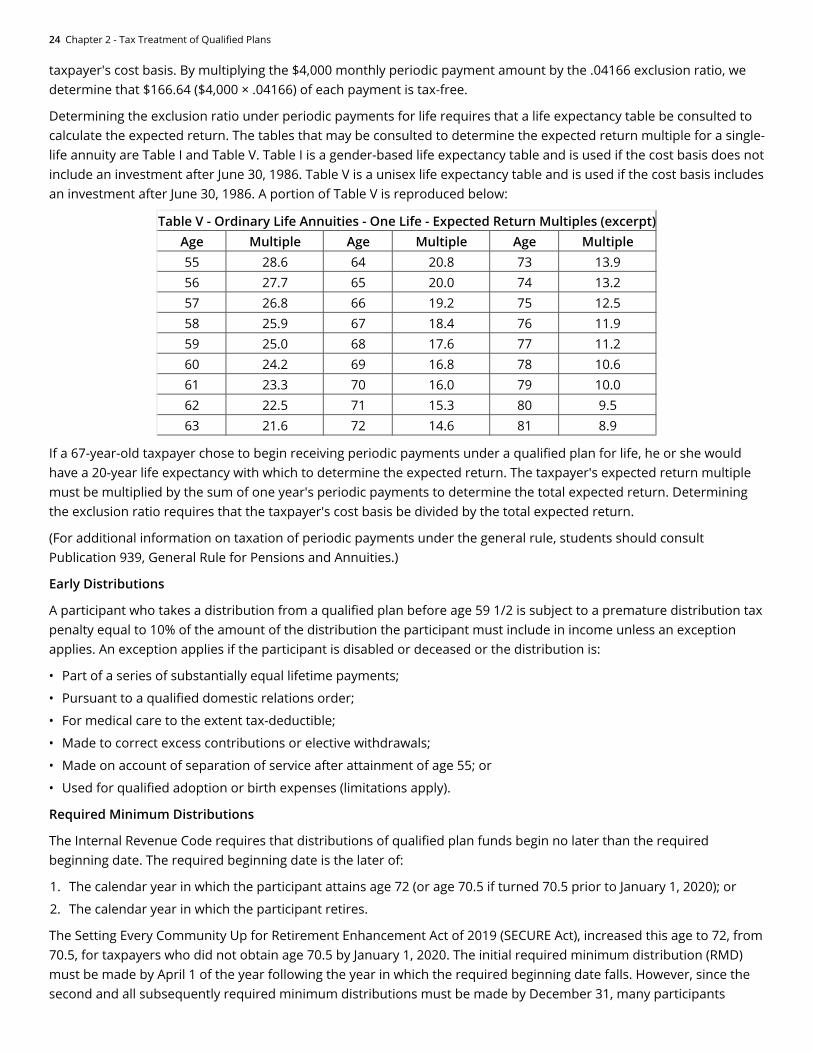

taxpayer's cost basis. By multiplying the $4,000 monthly periodic payment amount by the .04166 exclusion ratio, we determine that $166.64 ($4,000 × .04166) of each payment is tax-free.

Determining the exclusion ratio under periodic payments for life requires that a life expectancy table be consulted to calculate the expected return. The tables that may be consulted to determine the expected return multiple for a single-life annuity are Table I and Table V. Table I is a gender-based life expectancy table and is used if the cost basis does not include an investment after June 30, 1986. Table V is a unisex life expectancy table and is used if the cost basis includes an investment after June 30, 1986. A portion of Table V is reproduced below:

Table V - Ordinary Life Annuities - One Life - Expected Return Multiples (excerpt)Age Multiple Age Multiple Age Multiple55 28.6 64 20.8 73 13.956 27.7 65 20.0 74 13.257 26.8 66 19.2 75 12.558 25.9 67 18.4 76 11.959 25.0 68 17.6 77 11.260 24.2 69 16.8 78 10.661 23.3 70 16.0 79 10.062 22.5 71 15.3 80 9.563 21.6 72 14.6 81 8.9

If a 67-year-old taxpayer chose to begin receiving periodic payments under a qualified plan for life, he or she would have a 20-year life expectancy with which to determine the expected return. The taxpayer's expected return multiple must be multiplied by the sum of one year's periodic payments to determine the total expected return. Determining the exclusion ratio requires that the taxpayer's cost basis be divided by the total expected return.

(For additional information on taxation of periodic payments under the general rule, students should consult Publication 939, General Rule for Pensions and Annuities.)

Early Distributions

A participant who takes a distribution from a qualified plan before age 59 1/2 is subject to a premature distribution tax penalty equal to 10% of the amount of the distribution the participant must include in income unless an exception applies. An exception applies if the participant is disabled or deceased or the distribution is:

Part of a series of substantially equal lifetime payments;

Pursuant to a qualified domestic relations order;

For medical care to the extent tax-deductible;

Made to correct excess contributions or elective withdrawals;

Made on account of separation of service after attainment of age 55; or

Used for qualified adoption or birth expenses (limitations apply).

Required Minimum Distributions

The Internal Revenue Code requires that distributions of qualified plan funds begin no later than the required beginning date. The required beginning date is the later of:

The calendar year in which the participant attains age 72 (or age 70.5 if turned 70.5 prior to January 1, 2020); or

The calendar year in which the participant retires.

The Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act), increased this age to 72, from 70.5, for taxpayers who did not obtain age 70.5 by January 1, 2020. The initial required minimum distribution (RMD) must be made by April 1 of the year following the year in which the required beginning date falls. However, since the second and all subsequently required minimum distributions must be made by December 31, many participants

Distributions from a Qualified Employee Plan 25

•

•

•

choose to begin taking their initial RMD by December 31 of the year in which their required beginning date falls in order to avoid having to take two distributions in the same tax year.

If the plan participant fails to take a distribution at least equal to the required minimum distribution, a tax penalty equal to 50% of the insufficiency is payable. For example, if the required minimum distribution in a particular year was $20,000 but the participant received a distribution of only $15,000, the difference of $5,000 would be subject to a 50% tax, resulting in a penalty tax of $2,500.

Plan Distributions of Non-Cash Assets

Sometimes assets other than cash may be distributed from a qualified plan. Such a non-cash distribution may involve the distribution of:

A life insurance policy;

An annuity contract; or

Employer securities.

The tax consequences of the distribution vary, depending on the type of asset.

If the plan distributes a cash value life insurance policy to the participant, the cash value of the policy must be recognized as ordinary income in the year in which the policy is distributed, whether or not the policy is subsequently surrendered. Simple distribution of the policy is sufficient to require recognition. Since a term life insurance policy has no cash value, its distribution from the plan will not require any income recognition.

An annuity contract's distribution, however, receives different tax treatment than that given to a cash value life insurance policy. If the plan distributes a deferred annuity contract, its simple distribution does not trigger immediate tax liability. Instead, there is no recognition of income until the contract is surrendered.

The distribution from a qualified plan of qualifying employer securities in a lump-sum distribution also differs from the distribution of other non-cash assets. Qualifying employer securities distributed from a qualified plan are eligible for deferral of taxes on the net unrealized appreciation (NUA), i.e. the increase in the value of the shares following their contribution to the plan. Only the value of the securities at the time they were contributed to the plan is taxable to the recipient in the year of distribution.

Thus, the NUA continues to be tax-deferred until the stock is subsequently liquidated. When liquidated, the stock value in excess of the taxable amount recognized on distribution is taxed at capital gains rates.

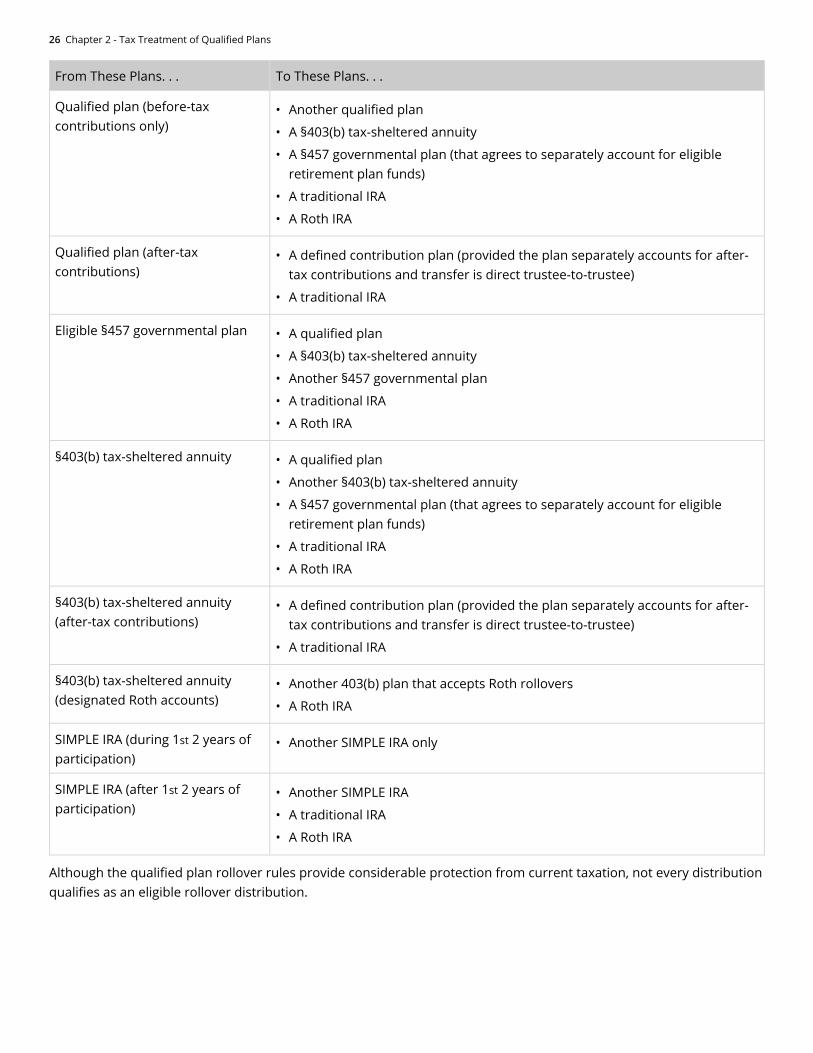

Rollovers

When a participant in a qualified plan leaves the employ of the plan sponsor, the participant may roll over the assets to his or her credit in the plan and avoid current taxation of the funds. A rollover is the transfer of a distribution from certain qualified plans that follows the rules set out in the Internal Revenue Code and Regulations. Distributions that are rolled over pursuant to these rules are not includible in the taxpayer's gross income until they are received at some time in the future.

Qualified plan distributions may be rolled over from and to several types of plans as illustrated in the following chart:

26 Chapter 2 - Tax Treatment of Qualified Plans

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

From These Plans. . . To These Plans. . .

Qualified plan (before-tax contributions only)

Another qualified plan

A §403(b) tax-sheltered annuity

A §457 governmental plan (that agrees to separately account for eligible retirement plan funds)

A traditional IRA

A Roth IRA

Qualified plan (after-tax contributions)

A defined contribution plan (provided the plan separately accounts for after-tax contributions and transfer is direct trustee-to-trustee)

A traditional IRA

Eligible §457 governmental plan A qualified plan

A §403(b) tax-sheltered annuity

Another §457 governmental plan

A traditional IRA

A Roth IRA

§403(b) tax-sheltered annuity A qualified plan

Another §403(b) tax-sheltered annuity

A §457 governmental plan (that agrees to separately account for eligible retirement plan funds)

A traditional IRA

A Roth IRA

§403(b) tax-sheltered annuity (after-tax contributions)

A defined contribution plan (provided the plan separately accounts for after-tax contributions and transfer is direct trustee-to-trustee)

A traditional IRA

§403(b) tax-sheltered annuity (designated Roth accounts)

Another 403(b) plan that accepts Roth rollovers

A Roth IRA

SIMPLE IRA (during 1st 2 years of participation)

Another SIMPLE IRA only

SIMPLE IRA (after 1st 2 years of participation)

Another SIMPLE IRA

A traditional IRA

A Roth IRA

Although the qualified plan rollover rules provide considerable protection from current taxation, not every distribution qualifies as an eligible rollover distribution.

Distributions from a Qualified Employee Plan 27

•

•

•

•

•

•

1.

2.

3.

4.

•

Distributions Ineligible for Rollover

An eligible rollover distribution is any distribution made to an employee of the funds to his or her credit in a qualified trust EXCEPT for a distribution that is:

Part of a series of substantially equal payments made over the employee's life expectancy;

Made for a specified period of 10 years or more;

A required minimum distribution; or

A hardship distribution.

Direct and Indirect Rollovers

There are two types of rollovers:

Trustee to participant to trustee—known as an "indirect rollover," and

Trustee to trustee—known as a "direct rollover".

A trustee can make the rollover directly to another trustee—for example, a pension plan trustee can send the funds directly to a traditional IRA trustee or to another qualified plan trustee by wire transfer or some other means—or it can pay the funds to the individual. Unfortunately, when qualified plan rollover funds are paid to the individual for subsequent payment to the new plan trustee, they come with some serious strings attached.

Any distribution to a participant from a qualified plan, §457 governmental plan, or §403(b) tax-sheltered annuity—even if that distribution will be rolled over to another plan—requires that the trustee of the distributing plan withhold 20% of the distribution for taxes. The amount withheld is itself considered a distribution and subject to taxation and possible premature withdrawal penalties. Furthermore, the indirect rollover must be completed within 60 days of distribution or the entire distribution may be subject to taxation.

The way to avoid mandatory tax withholding and the resulting tax liability is through a trustee-to-trustee rollover, a transfer of funds made directly from the trustee of the existing plan to the trustee of the new plan. By using a trustee-to-trustee rollover of the funds from the plan, the participant can avoid the mandatory 20% withholding by the transferring trustee. The entire account balance can be quickly and efficiently transferred from one plan to another.

Plan Loans

While not all qualified plans permit participants to take loans from their accounts, they may provide for them as long as they meet specific requirements. The participant's meeting these requirements is vital because a failure to meet the requirements may cause the intended loan to be deemed a distribution and, therefore, taxable in the year in which the loan was made. The requirements that must be met for a qualified loan to avoid being considered a distribution are:

The loan must provide for a specific repayment term

The loan repayment must provide for substantially level amortization

The loan must be within certain dollar limitations

The loan must involve a loan agreement that can be enforced