Retirement Plans: Managing Your Fiduciary Responsibility

52

Retirement Plans: Managing Your Fiduciary Responsibility

-

Upload

securedocs -

Category

Economy & Finance

-

view

948 -

download

1

Transcript of Retirement Plans: Managing Your Fiduciary Responsibility

Retirement Plans: Managing Your Fiduciary Responsibility

About Pensionmark

Pensionmark Retirement Group provides retirement plan consulting services to employers throughout the nation, with a focus on delivering reliable retirement plan solutions and helping employees retire with dignity.

Firm Statistics

• Established in 1988 and currently serving approximately 650 corporate clients with over $5 billion in retirement plan assets

• Over 71 team members across 21 offices throughout the United States

• Recognized as one of the top retirement plan consulting firms in the nation1

1. PLANSPONSOR Magazine 2007-2012. Nominated by industry professionals and selected based on a quantitative evaluation of service levels and feedback from employer clients.

About AppFolio SecureDocs

AppFolio SecureDocs is a virtual data room for sharing and storing sensitive documents both internally and with outside parties.

AppFolio, Inc. Company Basics

• Founded by the team that created and launched GoToMyPC and GoToMeeting

• Backed by leading technology companies and investors

• Web-based business software for financial and legal professionals

About Devyn Duex

Devyn Duex, MBA, AIF®, CRPS®

Vice President, Client RelationsLPL Registered Administrative Associate

• Mrs. Duex received her Master’s in Business Administration-Marketing (MBA/MKT) from the University of Phoenix and received her Bachelor of Arts degree in Theatre Arts, Magna Cum Laude, from Point Park University in Pittsburgh, PA.

• She has been recognized as one of the nation's most influential retirement plan advisors by 401kWire (2009, 2010). (Based on reader votes, input from distributors and statistics about advisor practice gathered directly from nominees.)

• Mrs. Duex was recently recognized as one of the Top Women in Business in 2012 for the Tri-Counties by Pacific Coast Business Times.

• Mrs. Duex also earned the AIF® (Accredited Investment Fiduciary™) professional designation awarded by the Center for Fiduciary Studies which is associated with the University of Pittsburgh and the CHARTERED RETIREMENT PLANS SPECIALISTSM (CRPS®) certification from the College of Financial Planning.

Key Topics

After today’s session you will have a better understanding of the following:

• Plan Governance—What is it and why you should care. • 401(k), IRS and Department of Labor (DOL) Audit Planning• Fee Disclosure is here, now what? Understanding and determining

reasonableness. • Are your participants ‘Retirement Ready’?

What is Plan Governance?

It is more than just fiduciary responsibility:

Plan governance encompasses all of the duties, responsibilities, and actions connected with the establishment and administration of the Plan and the management of Plan assets.

What Questions Should You Ask?

• Are the right people involved? • Are duties clearly identified and communicated? • Are there formal processes and procedures in place

and documented?• Are activities being routinely monitored?

What Questions Should You Ask?

• Are the right people involved?

Who’s Involved?

The following people may be involved:

• Individuals authorized to act on behalf of the employer as Plan Sponsor

• Fiduciaries• Employees of the Plan Sponsor who carry out ministerial

duties• Service Providers• Financial Professionals

One Role At a Time

The individual can act in only one capacity at any time and must understand which role he or she is in when fulfilling assigned duties.

Settlor Functions

Employer functions which are non-fiduciary in nature including:

•Establishing and amending the retirement plan•Determining fiduciary structure•Determining who will appoint the named fiduciary•Putting risk strategies in place

Who is a Fiduciary?

A Fiduciary is any individual who:

Uses discretion in administering and managing a Plan or controlling the Plan’s assets makes that person a fiduciary to the extent of that discretion or control.

A Plan must have at least one fiduciary (a person or entity) named in the written Plan as the Named Fiduciary (for some Plans, it may be an administrative committee or a company’s board of directors).

Must act in the best interest of Plan participants and beneficiaries, held to ERISAstandard of care:• Follow the prudent person rule • Follow the diversification rule • Follow the exclusive benefit rule • Act in accordance with the plan documents • Provide information to plan participants.

Ministerial Duties

These functions are non-discretionary in nature and are necessary to carry out the day-to-day operation of the Plan:

• Enrolling employees in the retirement Plan as a part new employee orientation

• Processing employee deferrals through payroll

• Conducting employee meetings emphasizing the importance of planning for retirement

Accidental Fiduciary

Following a process is one thing; making a decision or interpreting how a process should be done is another

• An employee or other individual who exercises discretionary authority over the Plan and becomes a fiduciary, even if not appointed.

Service Providers & Financial Professionals

Important to establish, understand, and monitor your process around organizations providing services to the Plan.

What Questions Should You Ask?

• Are the right people involved?

• Are duties clearly identified and communicated?

Roles & Responsibilities

• Communication of roles and responsibilities—and an understanding of those roles and responsibilities by the individuals assigned—are keys to successful Plan governance

• Document, Document, Document!

What Questions Should You Ask?

• Are the right people involved? • Are duties clearly identified and communicated?

• Are there formal processes and procedures in place and documented?

Processes and Procedures

Critical in helping both fiduciaries and non-fiduciaries carry out their responsibilities, assisting in keeping your plan in compliance, and will result in greater efficiency and preparedness in the event of an IRS or DOL plan audit.

Manage Your Risk by Using a Disciplined Process

Clear and deliberate methodology is key How you arrived at a decision can be more important than thedecision itself.Common processes to address: • Selecting and monitoring investments• Administering loan program• Qualification process of DROs• Determining claims for benefits• Required disclosures to participants• Determining Eligibility• Plan compliance testing• Contribution timing• Participant withdrawal transactions and distributions

Document…

…Document, Document.

What Questions Should You Ask?

• Are the right people involved? • Are duties clearly identified and communicated? • Are there formal processes and procedures in place and

documented?

• Are activities being routinely monitored?

It doesn’t end at the set-up…

Routinely monitor both fiduciary and non-fiduciary activities, and make changes as needed.

ERISA Compliance is Important

ERISA compliance is important. Failure can result in serious penalties.• Bear personal liability for breaches• Subject to fines of 5% to 100% of the amount of losses

incurred, as well as excise taxes, and civil or criminal sanctions• The plan may be disqualified

Poll 1

Have you already established Plan governance regarding your Retirement benefit(s)?

• YES

• NO

• A Process is in place, but not officially documented

Audit Planning

• 401k Required Independent Audit• IRS Audit• DOL Investigation

401(k) Required Audit

• Over 100 participants as of the first day of the Plan Year• Participant definition: Any individual eligible to make

elective contributions under a Plan, Nonvested individuals who are earning or retaining credited service, and current and former employees and beneficiaries eligible for or receiving benefits

• 80/120 Participant Rule; small Plan filer exception

• Independent Qualified Public Accountant

Poll 2

Is your Plan currently under random selection for an audit/investigation by the IRS or DOL?

• YES, currently in process

• YES, a letter was received but the process has not yet started

• YES, a previous Plan year, not currently.

• No, never been through this process

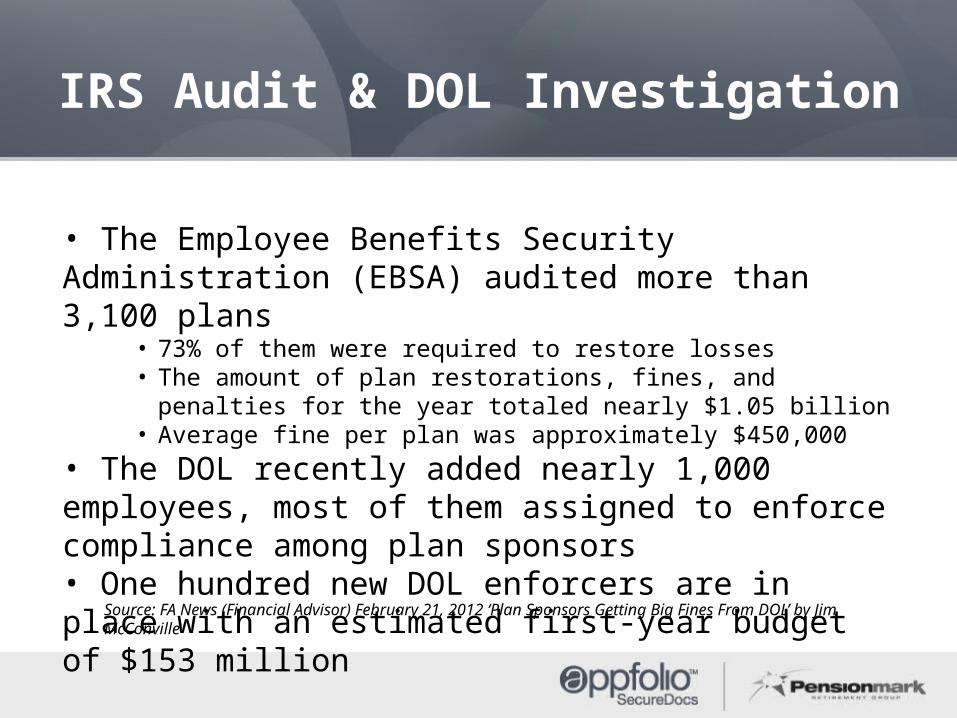

IRS Audit & DOL Investigation

• The Employee Benefits Security Administration (EBSA) audited more than 3,100 plans

• 73% of them were required to restore losses• The amount of plan restorations, fines, and penalties for the year totaled

nearly $1.05 billion• Average fine per plan was approximately $450,000

• The DOL recently added nearly 1,000 employees, most of them assigned to enforce compliance among plan sponsors• One hundred new DOL enforcers are in place with an estimated first-year budget of $153 million

Source: FA News (Financial Advisor) February 21, 2012 ‘Plan Sponsors Getting Big Fines From DOL’ by Jim McConville

DOL Investigation

Responsibility to review Plans for Fiduciary breaches

Reminder; Basic Fiduciary Duties• Acting solely in the interests of the participants and their beneficiaries

• Being prudent

• Paying only reasonable and necessary expenses of the plan

• Following the terms of the plan

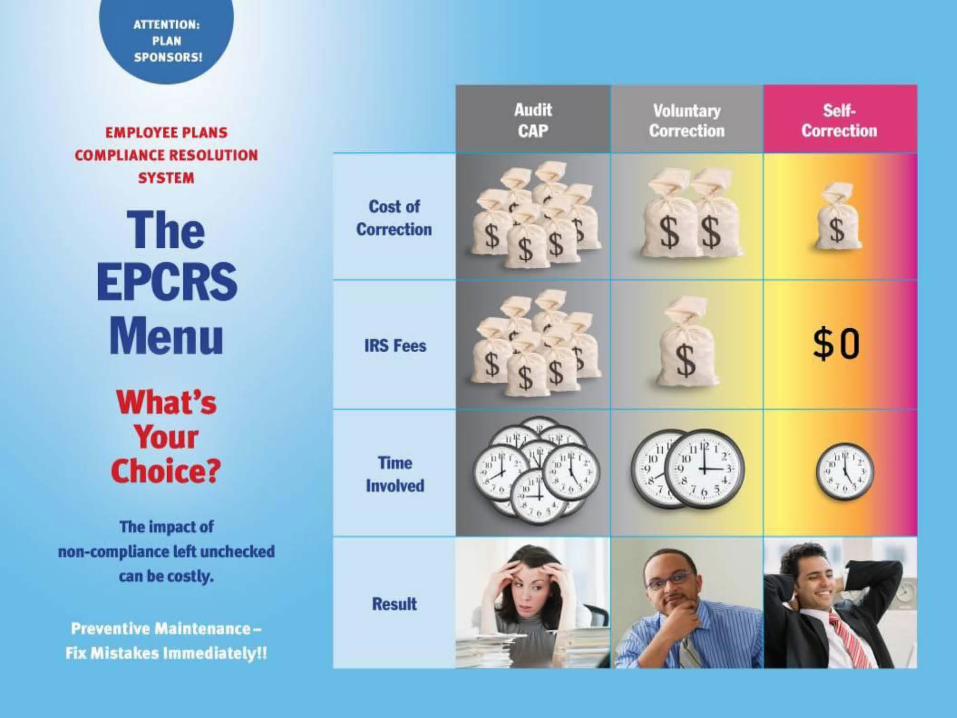

DOL Investigation

Steps to help address common problems

1. Understand your plan and your responsibilities 2. Carefully select service providers

3. Make timely contributions

4. Avoid prohibited transactions

IRS Audit

How 5500’s are Selected for Examination:

Project Cases •Large or Unusual Assets or Entries on Form 5500 •Inconsistencies in Answers •Inaccurate Answers •Referrals from IRS Divisions, PBGC, DOL, Interested Parties

IRS Audit

How 5500’s are Selected for Examination:

Project Cases •Large or Unusual Assets or Entries on Form 5500 •Inconsistencies in Answers •Inaccurate Answers •Referrals from IRS Divisions, PBGC, DOL, Interested Parties

IRS Audit

IRS Audit

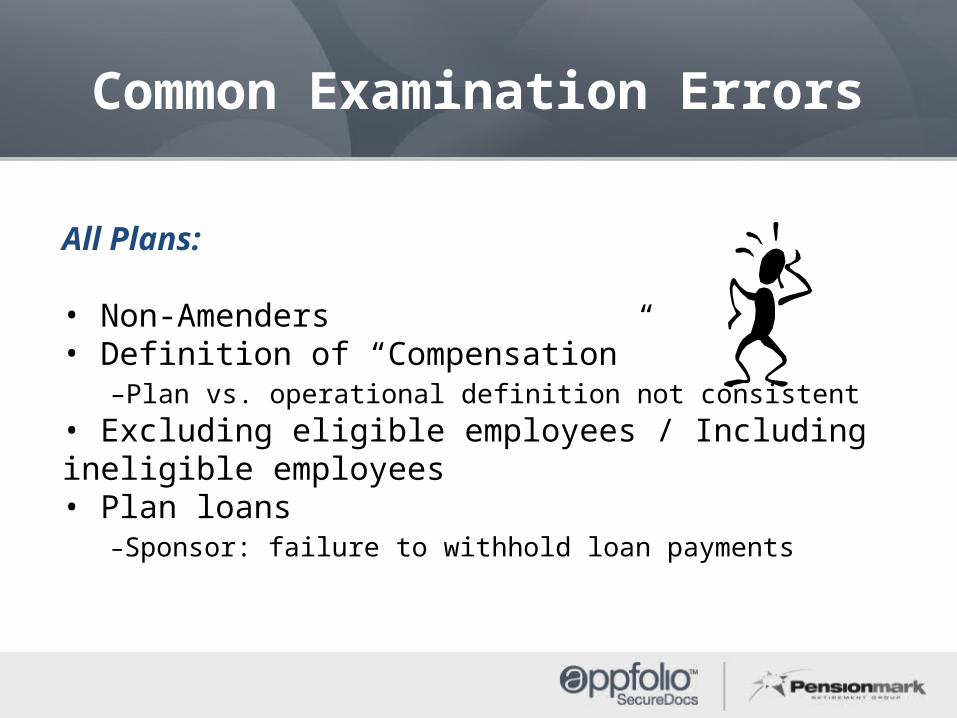

Common Examination Errors

All Plans:

• Non-Amenders • Definition of “Compensation”

–Plan vs. operational definition not consistent • Excluding eligible employees / Including ineligible employees • Plan loans

–Sponsor: failure to withhold loan payments

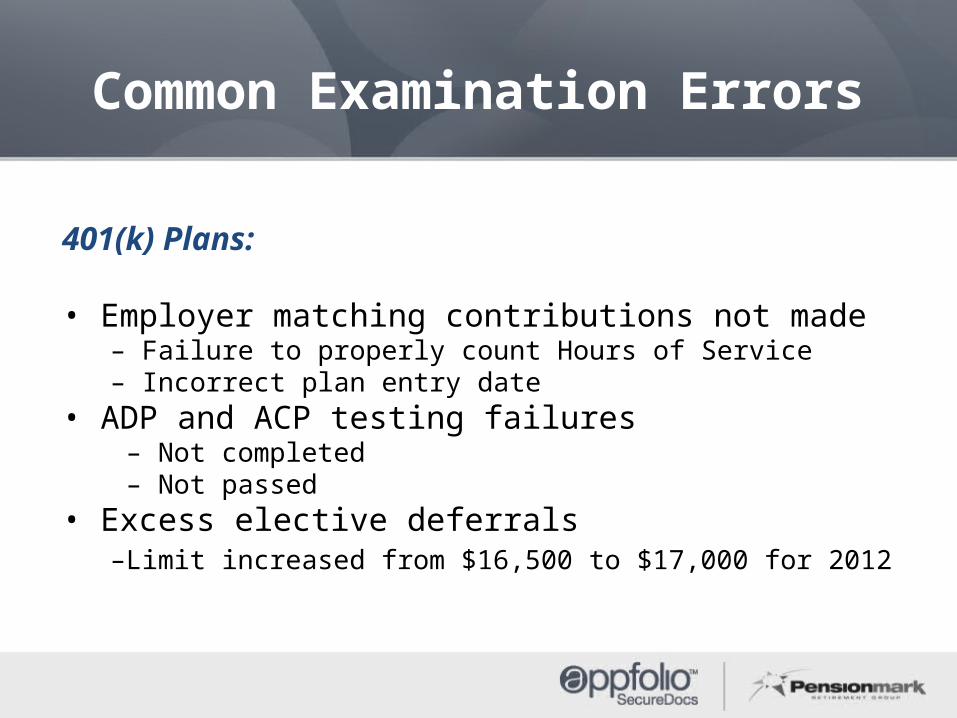

Common Examination Errors

401(k) Plans:

• Employer matching contributions not made – Failure to properly count Hours of Service – Incorrect plan entry date

• ADP and ACP testing failures – Not completed – Not passed

• Excess elective deferrals –Limit increased from $16,500 to $17,000 for 2012

Common Examination Errors

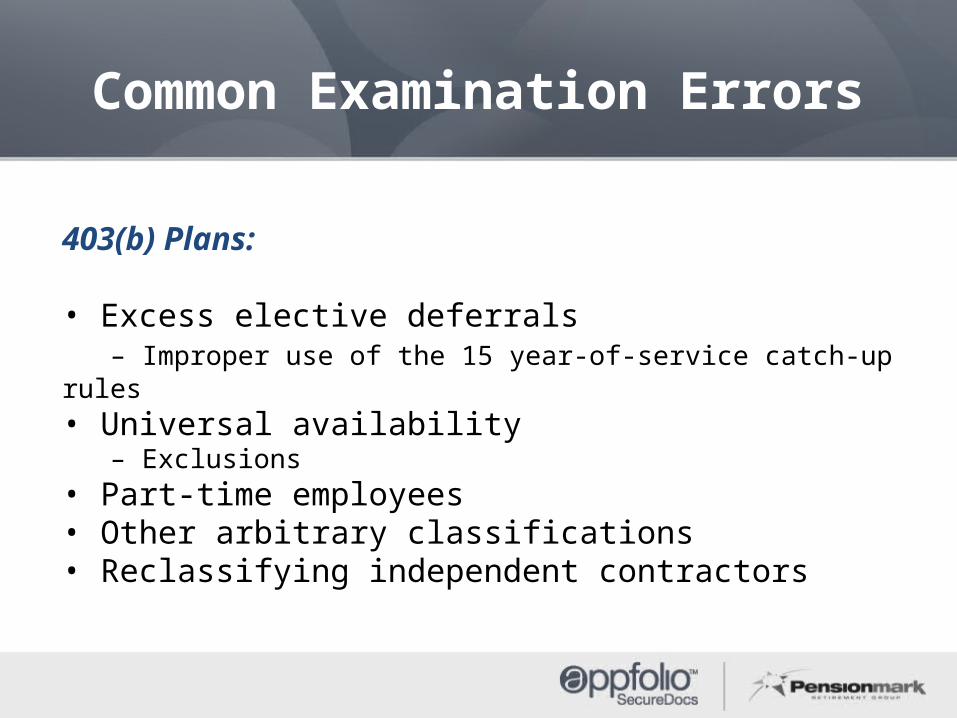

403(b) Plans:

• Excess elective deferrals – Improper use of the 15 year-of-service catch-up rules • Universal availability

– Exclusions • Part-time employees • Other arbitrary classifications • Reclassifying independent contractors

Common Examination Errors

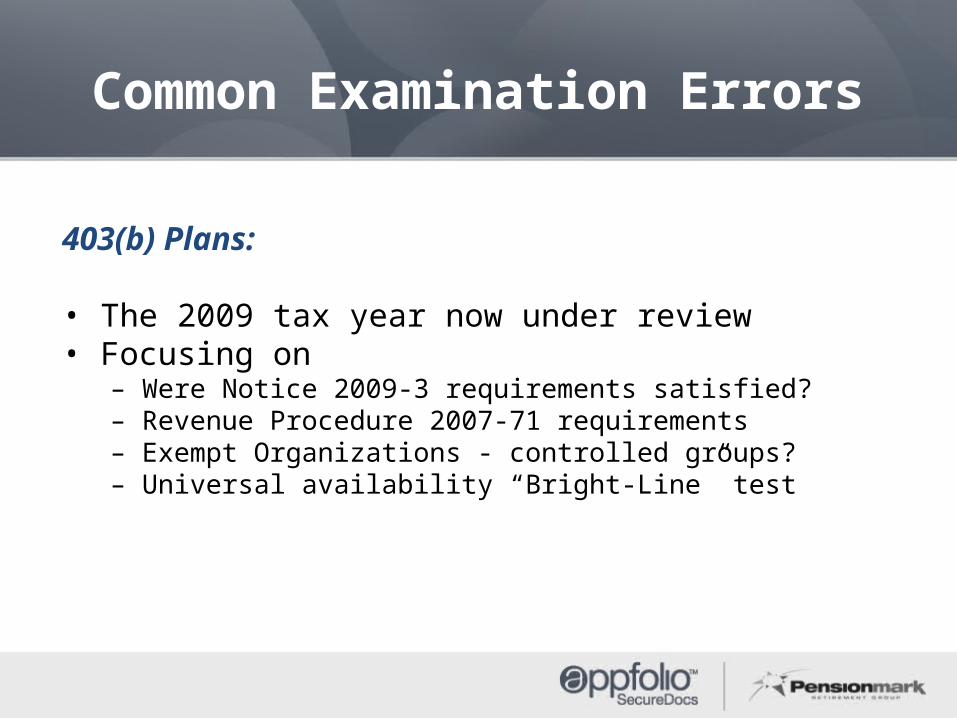

403(b) Plans:

• The 2009 tax year now under review • Focusing on

– Were Notice 2009-3 requirements satisfied? – Revenue Procedure 2007-71 requirements – Exempt Organizations - controlled groups? – Universal availability “Bright-Line” test

IRS Audit

How Do You Improve Compliance?

This is where proper Plan Governance pays off…it is critical to have disciplined process & internal controls!

15, 17, 18

Fee Disclosure, Now What?

Fee Disclosure in Summary

• ERISA 404(a)(5) and 408(b)(2), along with enhancements to the 5500-Schedule C are part of a three-pronged DOL disclosure strategy

• DOL’s intent is to improve on the disclosure of fees and any conflicts of interest

• Designed to assist Plan Sponsor in maintaining reasonableness of fees and allow employees to make better decisions

Poll 3

Has your Plan gone through a fee analysis to determine reasonableness of fees?

• YES

• NO

• NO, but we plan to analyze this, this year

Fee Disclosure- 408(b)(2) Value Proposition

• The Department believes that plan fiduciaries need this information, when selecting and monitoring service providers, to satisfy their fiduciary obligations under ERISA section 404(a)(1) to act prudently and solely in the interest of the plan’s participants and beneficiaries and for the exclusive purpose of providing benefits and defraying reasonable expenses of administering the plan.

Number of times “Reasonableness” or “Reasonable” is mentioned in the regulation: 49

Why the main issue is NOT disclosure, it is Reasonableness

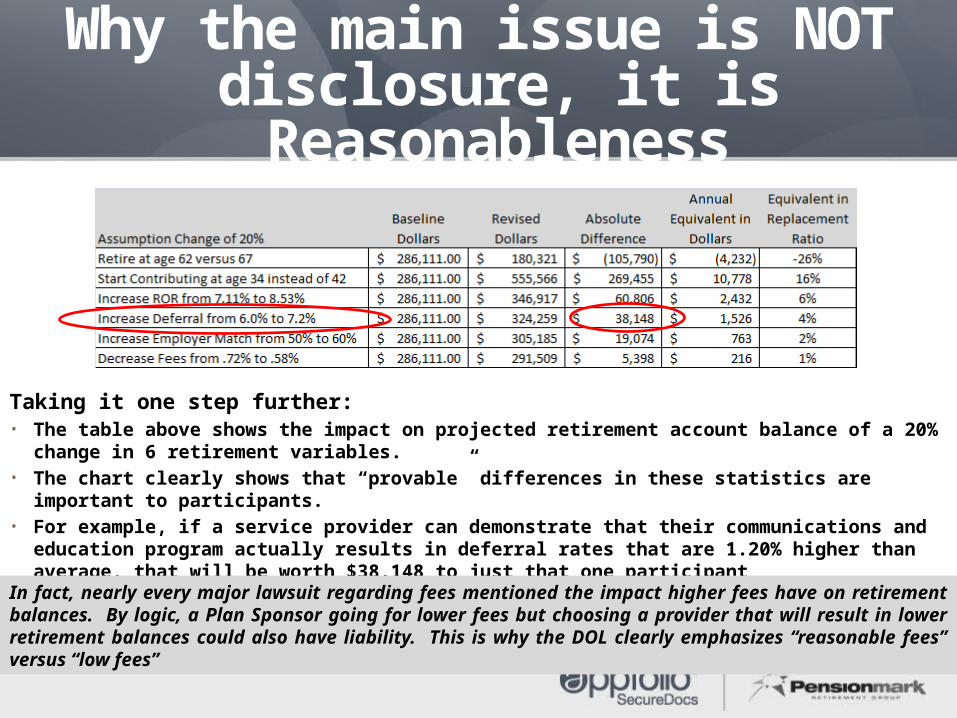

Taking it one step further:• The table above shows the impact on projected retirement account balance of a 20% change in 6 retirement variables.• The chart clearly shows that “provable” differences in these statistics are important to participants.• For example, if a service provider can demonstrate that their communications and education program actually results

in deferral rates that are 1.20% higher than average, that will be worth $38,148 to just that one participant• By contrast a 20% reduction in fees (15 bps) is worth only $5,398 to that one participant

In fact, nearly every major lawsuit regarding fees mentioned the impact higher fees have on retirement balances. By logic, a Plan Sponsor going for lower fees but choosing a provider that will result in lower retirement balances could also have liability. This is why the DOL clearly emphasizes “reasonable fees” versus “low fees”

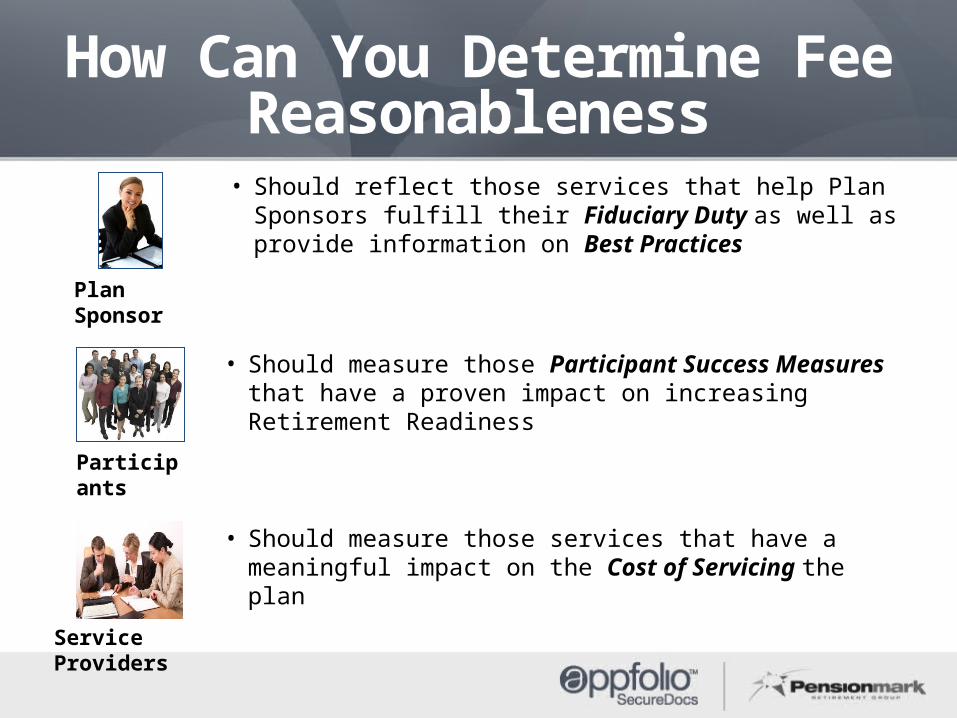

How Can You Determine Fee Reasonableness

Plan Sponsor

Participants

Service Providers

• Should reflect those services that help Plan Sponsors fulfill their Fiduciary Duty as well as provide information on Best Practices

• Should measure those Participant Success Measures that have a proven impact on increasing Retirement Readiness

• Should measure those services that have a meaningful impact on the Cost of Servicing the plan

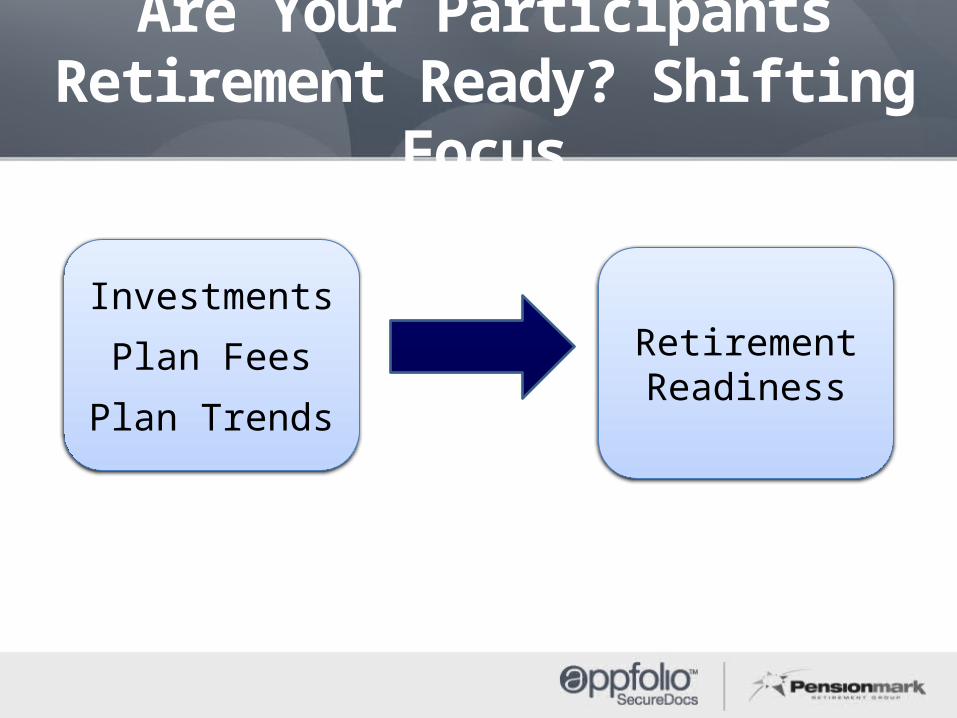

Are Your Participants Retirement Ready? Shifting Focus

Investments

Plan Fees

Plan Trends

RetirementReadiness

Plan Success Cycle

Poll 4

If your organization works with a retirement Plan Advisor, does your Advisor provide fiduciary services to the Plan?

• YES

• NO

• I am not sure

• Currently do not work with an Advisor

Contact Us

Pensionmark Retirement Group24 E. Cota Street, Suite 200Santa Barbara, CA 93101Phone: (888) [email protected]

AppFolio SecureDocs50 Castilian DriveGoleta, CA 93117Phone: (866) [email protected]@securedocs.comwww.securedocs.com

Securities offered through LPL Financial, Member FINRA/SIPC. Financial Representatives of Pensionmark provide investment advice through Independent Financial Partners, a Registered Investment Advisor and separate entity from LPL Financial.APPFOLIO is not affiliated with LPL Financial.

QUESTIONS?

Thank You

Confidential ©2012 AppFolio, Inc.