Retirement Planning with Voluntary Pension...

17

Retirement Planning with Voluntary Pension Schemes

Transcript of Retirement Planning with Voluntary Pension...

Retirement Planning with

Voluntary Pension Schemes

• The Need for Retirement Planning…………….3

• Introducing Voluntary Pension Schemes ……..7

• How VPS Works ……………………………….11

• Performance and Comparisons …………… 14

Outline

2

The Need for Retirement Planning

3

•“Retirement” is a phase of life where one‟s source of income ceases. While your INCOME stops, your EXPENSES don‟t !

•A Pension is an income that one will NEED at retirement

•While we may be compelled to think of “Retirement” as a tedious phase of our life – it is in fact a stage marked by:

• Limited Income

• Dependency on children

• Sacrifices & hardships

• Difficulty in meeting expenses

• No enjoyment

Therefore, we must ‘Plan’ today for a healthy, happy

retirement tomorrow

The Need for Retirement Planning

4

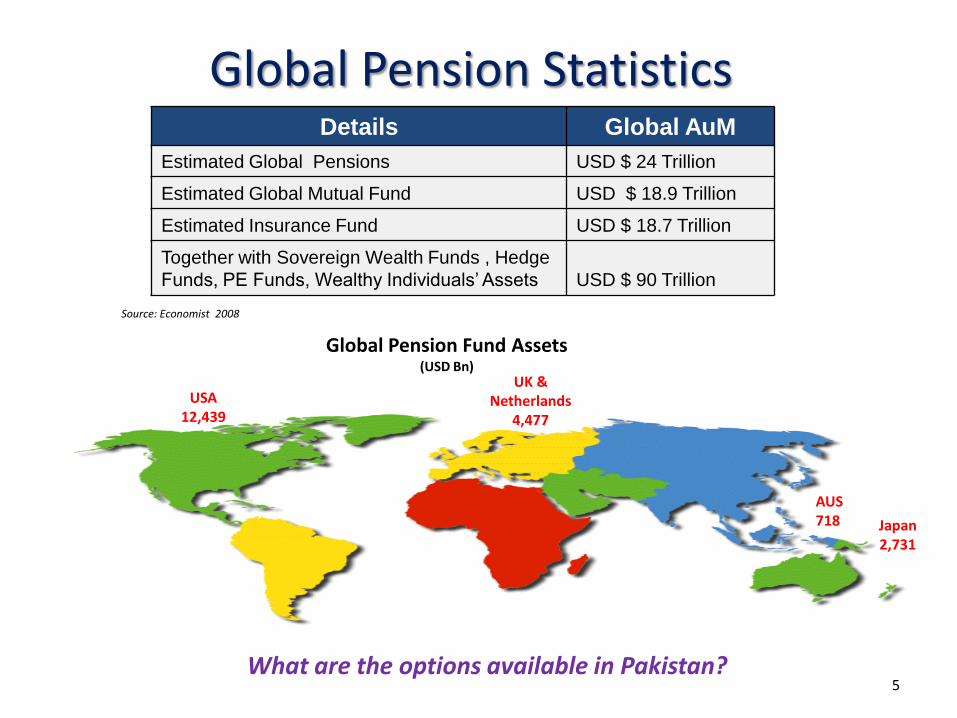

Source: Economist 2008

USA 12,439

Global Pension Fund Assets (USD Bn)

Japan 2,731

UK & Netherlands

4,477

AUS 718

Details Global AuM

Estimated Global Pensions USD $ 24 Trillion

Estimated Global Mutual Fund USD $ 18.9 Trillion

Estimated Insurance Fund USD $ 18.7 Trillion

Together with Sovereign Wealth Funds , Hedge

Funds, PE Funds, Wealthy Individuals‟ Assets

USD $ 90 Trillion

What are the options available in Pakistan?

Global Pension Statistics

5

To date, private citizens of Pakistan have not had access to a pension

plan, which would enable them to plan for their retirement in a

methodical manner.

Provident funds cater to similar needs but provide: • Very low returns • Lack transparency • Lack of premature accessibility (in most cases)

Private citizens primarily depend on: • Yield on property • Interest on bank deposits/NSS • Or alternatively depend on their children for retirement support

Pension Alternatives in Pakistan

6

Introducing ‘The Voluntary Pension Scheme’

(VPS)

7

The Benefits of VPS in Retirement Planning can be countless…

• VPS is a flexible Savings cum Investment Plan that facilitates individuals to

save for retirement in a systematic and disciplined manner

• Participants can define their own Investment Plan through choice of asset

allocation based on their individual risk tolerance and return expectation.

• Investment in Pension Fund grows Tax free

VPS as a Tool for Effective Retirement Planning

8

• Provides Special Tax benefits, not available in any other Investment vehicle

– Annual Tax Savings on up to 20% (or more if one is over 40 yrs.) of your annual

taxable income

– All investment income/gains tax free till retirement

– Reduced Tax Rate when receiving monthly income (pensions) post retirement

• Attractive Options, before, at and after Retirement

– Flexible investment allocations that may be changed once a year

– Withdraw up to 50% cash lump sum tax free at the time of retirement and;

– Receive monthly income by investing remaining balance (or entire balance) in an

annuity plan or you can even invest in an „Income Payment Plan‟

• May invest in Lump sum or at regular frequency

• No penalty on missing any payment

• Conventional and Islamic Options are available

VPS as a Tool for Effective Retirement Planning

9

• Coupled with Insurance/ Takaful benefits, to reduce the uncertainty in your life

• Allows you to choose your own retirement age (between 60 and 70). You may also revise your retirement age at a later date.

• Early Retirement is possible on the unfortunate event of disability. In case of untimely death, the Pension proceeds are transferred to the Nominees

• Portable - can easily switch between available Pension Fund Managers at a later stage, and continues if you switch jobs

• Plan Continuity – with job switches, your pension scheme is

not disbanded

VPS as a Tool for Effective Retirement Planning

10

How VPS Works (Essential Mechanics)

11

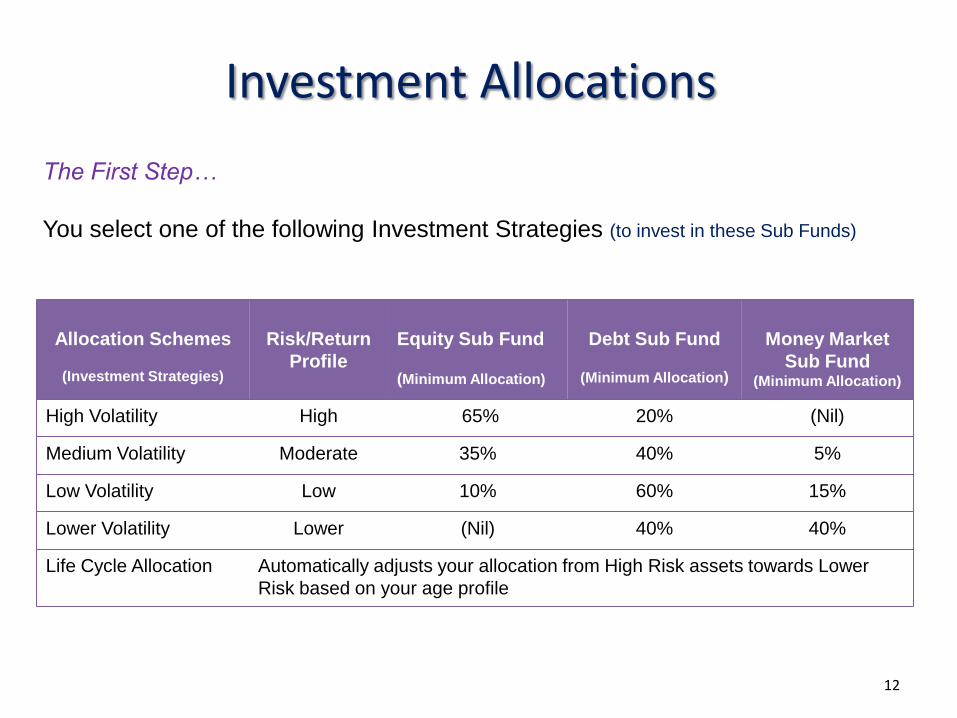

The First Step…

You select one of the following Investment Strategies (to invest in these Sub Funds)

Allocation Schemes

(Investment Strategies)

Risk/Return

Profile

Equity Sub Fund

(Minimum Allocation)

Debt Sub Fund

(Minimum Allocation)

Money Market

Sub Fund (Minimum Allocation)

High Volatility High 65% 20% (Nil)

Medium Volatility Moderate 35% 40% 5%

Low Volatility Low 10% 60% 15%

Lower Volatility Lower (Nil) 40% 40%

Life Cycle Allocation Automatically adjusts your allocation from High Risk assets towards Lower

Risk based on your age profile

Investment Allocations

12

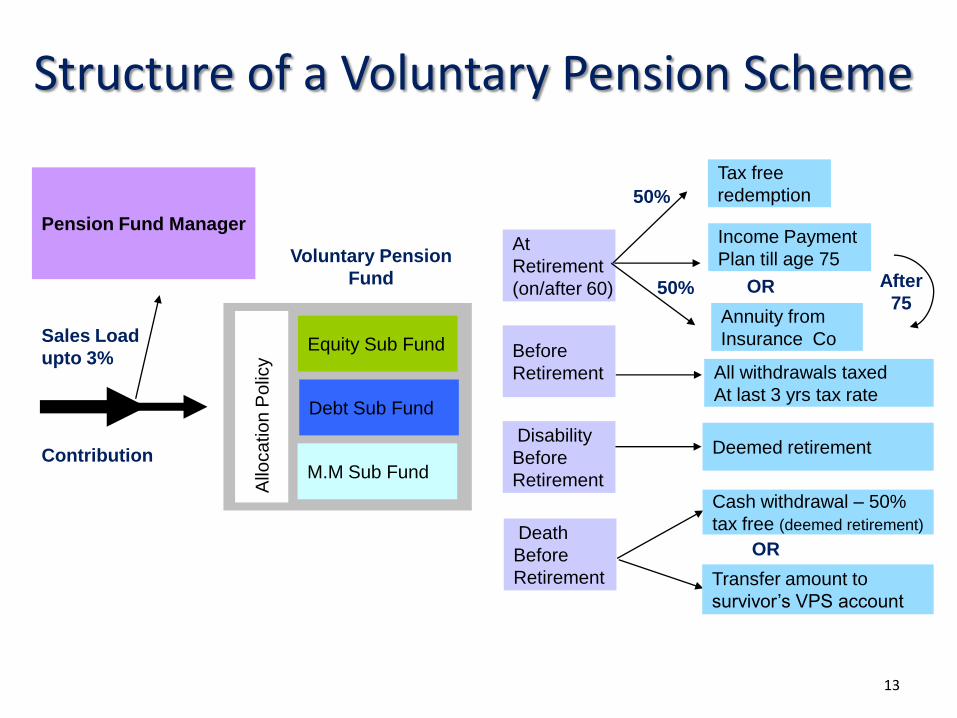

Equity Sub Fund

Debt Sub Fund

M.M Sub Fund

Voluntary Pension

Fund

Contribution

Allo

ca

tio

n P

olic

y

Pension Fund Manager

Sales Load

upto 3%

At

Retirement

(on/after 60)

Before

Retirement

Disability

Before

Retirement

50%

50%

OR

Annuity from

Insurance Co

Income Payment

Plan till age 75

OR

Tax free

redemption

After

75

All withdrawals taxed

At last 3 yrs tax rate

Deemed retirement

Cash withdrawal – 50%

tax free (deemed retirement)

Transfer amount to

survivor‟s VPS account

Death

Before

Retirement

Structure of a Voluntary Pension Scheme

13

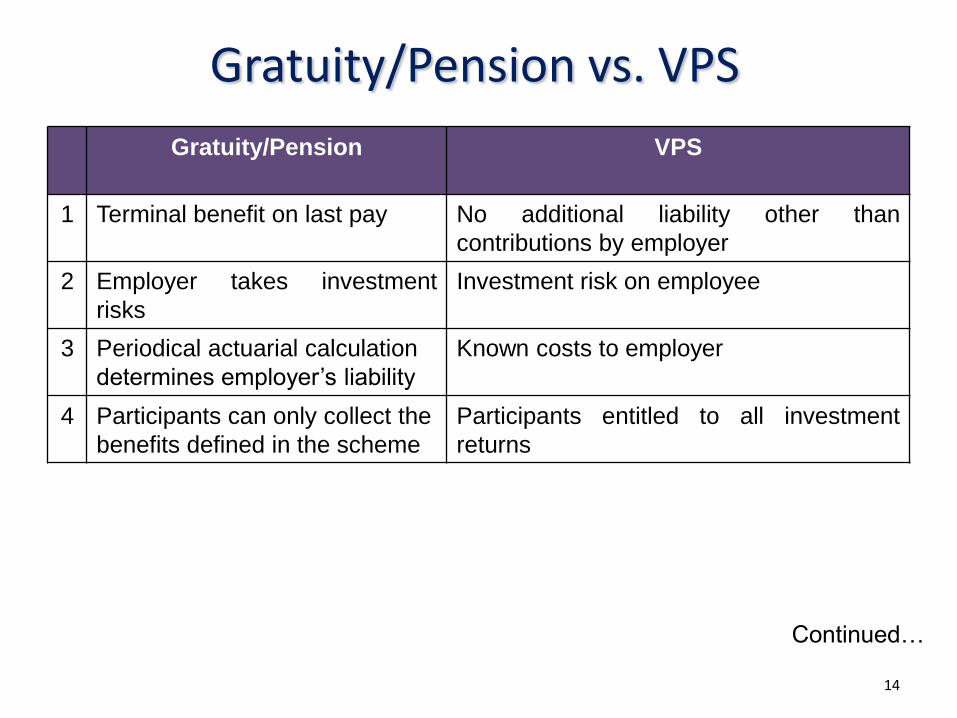

Gratuity/Pension

VPS

1 Terminal benefit on last pay No additional liability other than

contributions by employer

2 Employer takes investment

risks

Investment risk on employee

3 Periodical actuarial calculation

determines employer‟s liability

Known costs to employer

4 Participants can only collect the

benefits defined in the scheme

Participants entitled to all investment

returns

Gratuity/Pension vs. VPS

Continued…

14

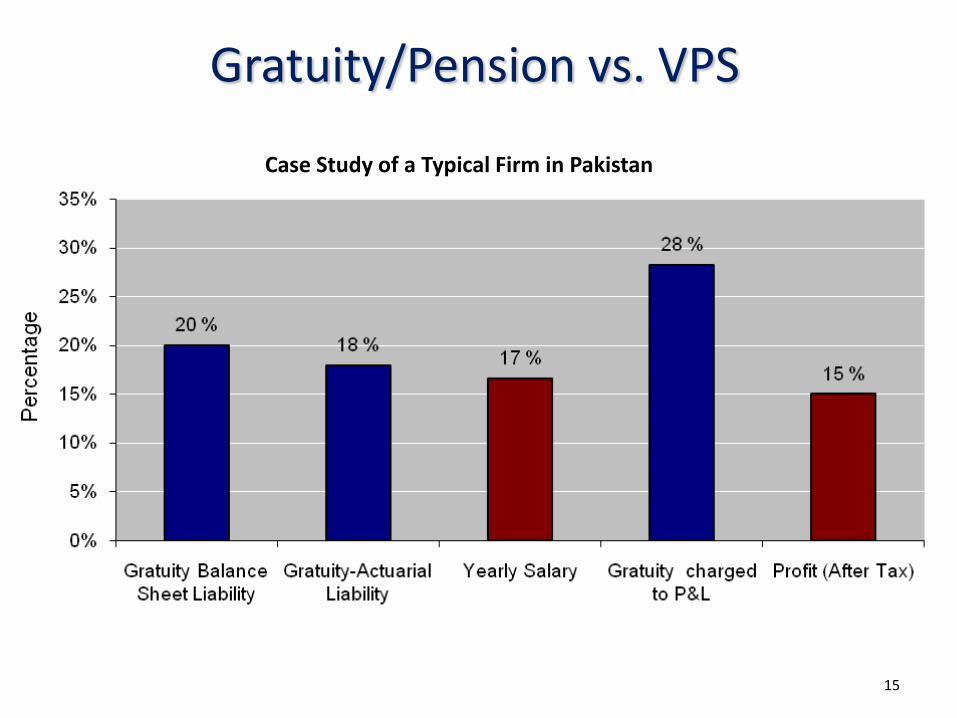

Gratuity/Pension vs. VPS

Case Study of a Typical Firm in Pakistan

15

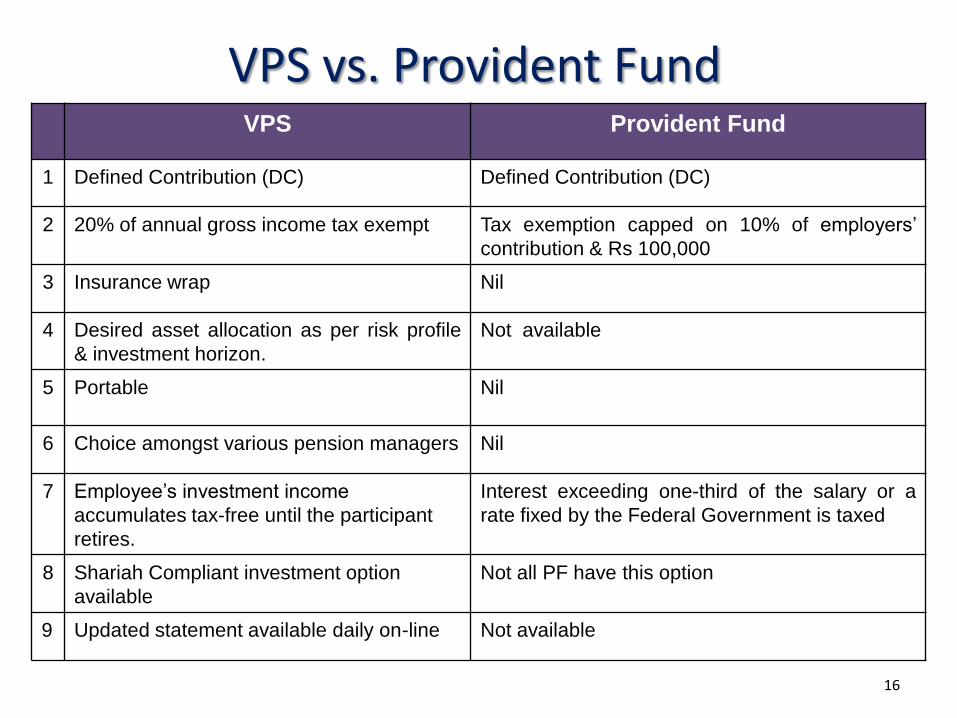

VPS Provident Fund

1 Defined Contribution (DC) Defined Contribution (DC)

2 20% of annual gross income tax exempt Tax exemption capped on 10% of employers‟

contribution & Rs 100,000

3 Insurance wrap Nil

4 Desired asset allocation as per risk profile

& investment horizon.

Not available

5 Portable Nil

6 Choice amongst various pension managers Nil

7 Employee‟s investment income

accumulates tax-free until the participant

retires.

Interest exceeding one-third of the salary or a

rate fixed by the Federal Government is taxed

8 Shariah Compliant investment option

available

Not all PF have this option

9 Updated statement available daily on-line Not available

VPS vs. Provident Fund

16

Thank You

17