Retirement Plan Essentials - National Association of Tax ... Retirement... · Retirement Plan...

59

Retirement Plan Essentials

Transcript of Retirement Plan Essentials - National Association of Tax ... Retirement... · Retirement Plan...

Retirement Plan Essentials

Presented By:Jim Vanden Branden, MAS, CPA, CFP

dandTom O’Saben, EA, CFP

Retirement Plans – Why?• Invest for retirement

• Employee retention

• Employee motivationp y

• Reduce income taxes• Reduce income taxes

Retirement Plans – Why Not?

• Administrative costs• Administrative burden headaches• Administrative burden – headaches• Cash flow – employer contributions• Lack of employee appreciation• Owner fiduciary responsibilityy p y• Market loss scapegoating – employee

moralemorale

Retirement Plan TypesA maze of decisions:• IRA based options: SEP SARSEP • IRA-based options: SEP, SARSEP,

SIMPLET lifi d l fi h i • True qualified plans: profit sharing, SIMPLE 401(K), 401(k), safe harbor 401(k) i l 401(k) 401(k), single 401(k), money purchase, target benefit, defined b fi h b l ESOP §457 benefit, cash balance, ESOP, §457, §403(b)

Other Retirement Plan Features

• Cash or deferred arrangement(CODA)• Designated Roth accounts• Designated Roth accounts• Age-weighted• Automatic contribution arrangement

(ACA)• Qualified automatic contribution

arrangement (QACA)g (Q )• Permitted disparity plans (integration)

Today’s Focus:• IRA-Based Options:

SEP– SEP– SIMPLE

Q lifi d Pl O ti • Qualified Plan Options: – Profit sharing– SIMPLE 401(K), safe harbor 401(k),

401(k)Si l 401(k)– Single 401(k)

– Designated Roth accounts

IRA-Based Options: SEP, SIMPLE

• SEP - simplified employee pension plan• SIMPLE savings incentive match plan • SIMPLE – savings incentive match plan

for employeesR i l • Retirement plans – yes

• Qualified plans – no– Lower adoption and on-going costs– Less design flexibility

• Employee establishes and owns IRA

Establishing a SEP - IRAg• Set up and fund by extended due date • Written agreement:• Written agreement:

– IRS model SEP document - Form 5305-SEPSEP

– Prototype SEP document - through a qualified financial institution such as a qualified financial institution such as a mutual fund, insurance company or bank

– Individually designed planIndividually designed plan

• Employer contributions only

Operating a SEP - IRA• No required contribution• No vesting schedule• No vesting schedule• No limit on number of employees• No Form 5500 (in most cases)• No plan withdrawal restrictionsp

– Subject to possible10% penalty

• Employees responsible for investmentsEmployees responsible for investments• Minimal eligibility restrictions

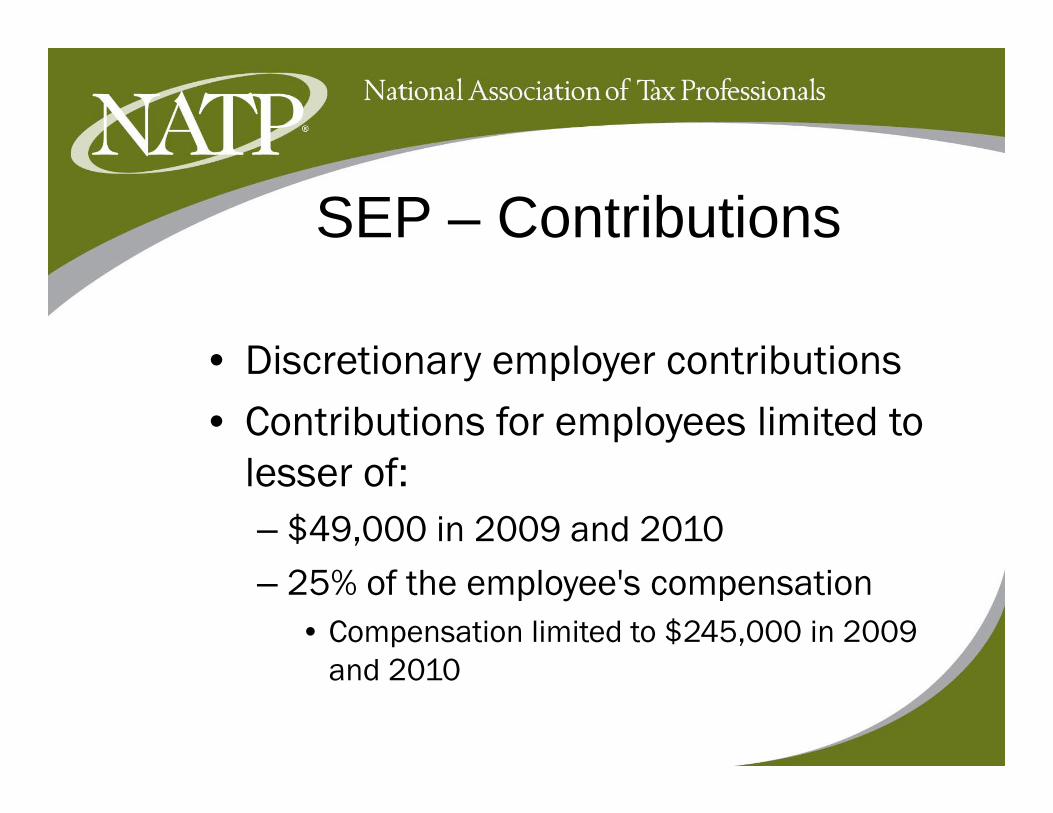

SEP – Contributions

• Discretionary employer contributions• Discretionary employer contributions• Contributions for employees limited to

l flesser of:– $49,000 in 2009 and 2010– 25% of the employee's compensation

• Compensation limited to $245,000 in 2009 d 2010and 2010

SEP – Contributions • Reduced contribution rate for self-

employed:employed:– Compensation is earnings from self-

employment net of ½ SE tax and owner’s employment, net of ½ SE tax and owner s SEP contribution.

– Circular calculation - Maximum = 20%Circular calculation Maximum 20%• [Employee rate / (1+ employee rate)]

– IRS Pub. 560, Chapter 5: rate table, rate , p ,worksheet, deduction worksheet

SEP – Deduction • Lesser of:

– Contributions (including any excess t ib ti )contributions carryover).

– 25% of compensation paid to participants fr th b i th t h th l t from the business that has the plan, not to exceed $49,000 per participant in 2009 and 20102009 and 2010

– Compensation limited to $245,000 per participant, for 2009 and 2010participant, for 2009 and 2010

• Self-employed reduced rate (20% max.)

SIMPLE IRA Features• Inexpensive to set up and operate• Mandatory employer contributions• Mandatory employer contributions• Employees have option to help fund

h i itheir retirement• No discrimination testing required • Lower contribution limits than some

other retirement plansp• Loans not available

Establishing a SIMPLE• New SIMPLE IRA: effective on any date

between January 1 and October 1between January 1 and October 1– If previously maintained SIMPLE IRA, new

SIMPLE IRA effective only on January 1SIMPLE IRA effective only on January 1

• New businesses that comes into existence after October 1:existence after October 1:– Set up SIMPLE IRA plan as soon as

administratively feasibleadministratively feasible.

• Calendar-year only

Establishing a SIMPLEg

• No other retirement plan:• No other retirement plan:– No contributions can be made or benefits

accrued in another plan for service in any accrued in another plan for service in any year beginning with the year the SIMPLE IRA plan becomes effectiveIRA plan becomes effective

– Exception: plan for collectively bargained employeesp y

Establishing a SIMPLEEstablishing a SIMPLE

• 100 or fewer employees• 100 or fewer employees– Count if received $5,000 or more in prior

year compensationyear compensation• Count all employees, regardless of whether

eligibleg

– Include self-employed and leased employees

Establishing a SIMPLEEstablishing a SIMPLE

• Written agreement:• Written agreement:– Form 5304-SIMPLE if each participant to select

the financial institution for his or her SIMPLE IRA the financial institution for his or her SIMPLE IRA contributions

– Form 5305-SIMPLE if all SIMPLE IRA contributions are required to be deposited initially at a designated financial institution

– Prototype document from bank etcPrototype document from bank, etc.– Individually-designed plan

Operating a SIMPLE• Required contribution• No vesting scheduleNo vesting schedule• 100 participant employee limit• No Form 5500• No Form 5500• No plan withdrawal restrictions

subject to possible 25% or 10% penalty– subject to possible 25% or 10% penalty• Employees responsible for investments

Mi i l ligibilit t i ti• Minimal eligibility restrictions

Operating a SIMPLEg• Notify employees of the following

before the beginning of the election before the beginning of the election period: 1) The employee’s opportunity to make or 1) The employee s opportunity to make or

change a salary reduction choice2) The plan’s matching contributions or 2) The plan s matching contributions or

nonelective contributions3) A summary description including the plan 3) su a y desc pt o c ud g t e p a

eligibility and basic features

Operating a SIMPLE• Notification - continued:

4) If using a designated financial institution 4) If using a designated financial institution, written notice that the employee’s SIMPLE IRA balance can be transferred without cost or penalty.

• Election period: Generally, the 60-day p y, yperiod immediately preceding January 1 of a calendar year (November 2 to December 31of the prior calendar year)

SIMPLE Contributions

• Two Normal Employer Contribution • Two Normal Employer Contribution Options:

M t hi l ’ t ib ti d ll– Matching employees’ contributions dollar-for-dollar up to 3% of pay, orA 2% nonelective contribution for each – A 2% nonelective contribution for each eligible employee, regardless of employee contributioncontribution

SIMPLE Contributions• Special lower matching percentage:

Employer can match less than 3% but at – Employer can match less than 3%, but at least 1%

– Employee notification required within a Employee notification required within a reasonable period of time before the 60-day election periody p

– Match less than 3% is not allowed for more than 2 years during the last 5-year period

SIMPLE ContributionsContribution Limits:• Employee• Employee

– $11,500 in 2009 and 2010 Employees age 50 or over; “catch up” – Employees age 50 or over; catch-up contribution for 2009 and 2010 of $2,500

• EmployerEmployer– Dollar-for-dollar match up to 3% of pay, or– 2% nonelective contribution per eligible p g

employee

SIMPLE Contributions• Employee deferrals:

Must be forwarded to the financial – Must be forwarded to the financial institution no later than the close of the 30-day period following the last day of the 30 day period following the last day of the month in which they were withheld from the employees’ paychecks.

• Employer matching or nonelectivecontributions:– No later than extended due date

True Qualified PlansTrue Qualified Plans

– Profit SharingProfit Sharing– SIMPLE 401(K), safe harbor 401(k),

401(k)401(k)– Single 401(k)– Designated Roth accountsDesignated Roth accounts

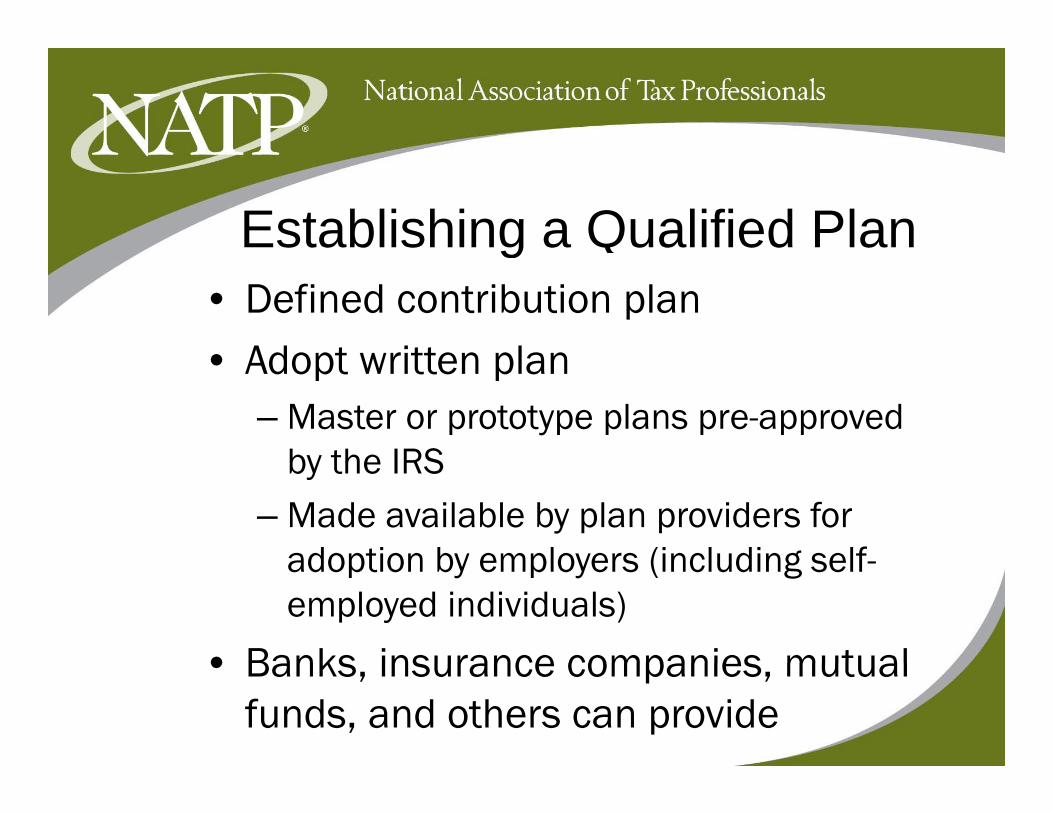

Establishing a Qualified Plang• Defined contribution plan • Adopt written plan • Adopt written plan

– Master or prototype plans pre-approved by the IRSby the IRS

– Made available by plan providers for adoption by employers (including selfadoption by employers (including self-employed individuals)

• Banks insurance companies mutual • Banks, insurance companies, mutual funds, and others can provide

Establishing a Qualified Plang Q• Individually designed plan is also

acceptable if customization is requiredacceptable if customization is required• Determine plan's investment vehicle:

E t bli h t t (l l i t t) – Establish trust (legal instrument) or custodial account to invest the fundsThe owner the trust or the custodial – The owner, the trust, or the custodial account can purchase an annuity contract from an insurance companyfrom an insurance company

Establishing a Qualified PlanEstablishing a Qualified Plan• Custodial account can be set up with a bank Custodial account can be set up with a bank,

savings and loan association, credit union, or other person who can act as the plan trustee

• Trust or custodial account not required to invest the plan's funds in annuity contracts or face-amount certificates

• For non-trustee holders the contracts must state they are not transferable

Qualified Plan Common Features

• Can have other retirement plans• Can be a business of any size• Need to annually file a Form 5500y• Testing to avoid discrimination in favor

of highly compensated employeeof highly compensated employee

Profit-Sharing Plan FeaturesProfit Sharing Plan Features

• Employer contributions only• Employer contributions only• Contributions are strictly discretionary • Good plan if cash flow is an issue• Employees not allowed to contribute, p y ,

but W-2 pension box checked

Operating a Profit-Sharing p g gPlan

• Pre approved profit sharing plans are • Pre-approved profit-sharing plans are available to cut down on administrative headachesheadaches

• Custom plan document• Test that benefits do not discriminate

in favor of the highly compensated employees

Profit-Sharing Plan Contributions

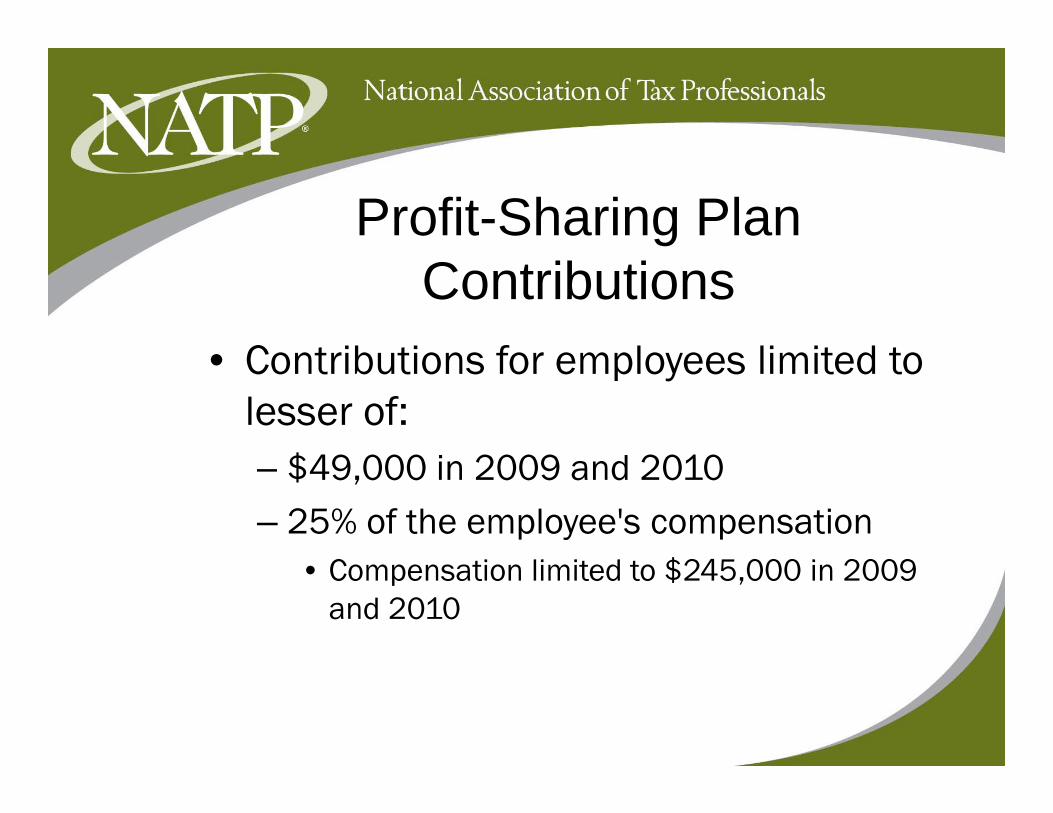

• Contributions for employees limited to • Contributions for employees limited to lesser of:

$49 000 i 2009 d 2010– $49,000 in 2009 and 2010– 25% of the employee's compensation

C i li i d $245 000 i 2009 • Compensation limited to $245,000 in 2009 and 2010

Profit-Sharing Plan C t ib tiContributions

• Reduced contribution rate for self• Reduced contribution rate for self-employed:

C ti i i f lf– Compensation is earnings from self-employment, net of ½ SE tax and owner’s SEP contributionSEP contribution

– Circular calculation - Maximum = 20%• [Employee rate / (1+ employee rate)][Employee rate / (1+ employee rate)]

401(k) Plan Features• Employee deferrals

• Employer match

• Employer discretionaryp y y

• Loans• Loans

Operating a 401(k) Planp g ( )

• Higher administrative costs

• Ongoing discrimination testingg g g

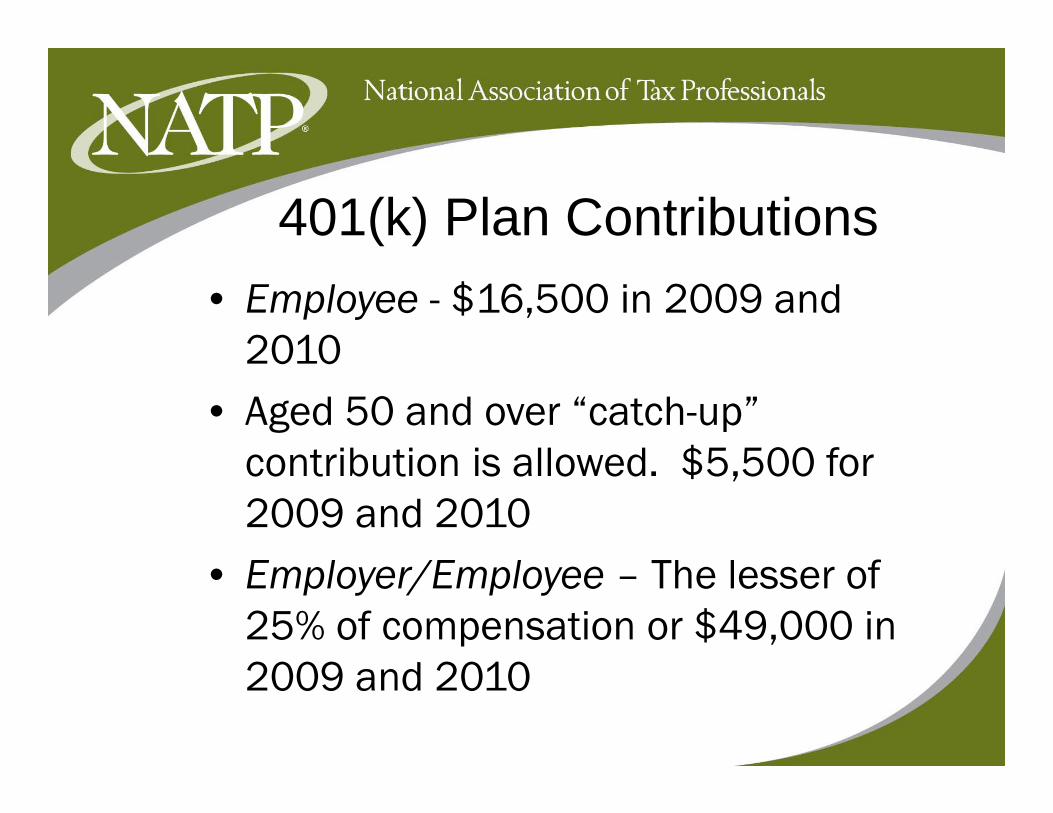

401(k) Plan Contributions• Employee - $16,500 in 2009 and

20102010• Aged 50 and over “catch-up”

contribution is allowed $5 500 for contribution is allowed. $5,500 for 2009 and 2010E l /E l Th l f • Employer/Employee – The lesser of 25% of compensation or $49,000 in 2009 d 20102009 and 2010

401(k) Plan Contributions• Self Employed - $16,500 in 2009 and

20102010• Self Employed - Aged 50 and over

“catch up” $5 500 for 2009 and 2010catch-up $5,500 for 2009 and 2010• Discretionary: Reduced contribution

f lf l d C i rate for self-employed: Compensation is earnings from self-employment, net

f ½ SE d ’ SEP of ½ SE tax and owner’s SEP contribution

SIMPLE 401(k)• Employer mandatory contributions• Discrimination testing not requiredDiscrimination testing not required• Less flexibility, less expensive to operate• Must have 100 or fewer employers• Must have 100 or fewer employers• Cannot have any other retirement plans• Eligible employees: $5 000 or more in • Eligible employees: $5,000 or more in

compensation from the employer for the preceding calendar yearpreceding calendar year

SIMPLE 401(k) Plan FeaturesSIMPLE 401(k) Plan Features

• Employee deferralsEmployee deferrals• Mandatory employer match• Employer discretionary NOT allowed• Employer discretionary NOT allowed• Employees are totally vested in any and all

contributionscontributions• Loans allowed• No contributions or benefit accruals under • No contributions or benefit accruals under

any other plans of the employer

SIMPLE 401(k) Plan Contributions

• ER matching contribution of 3% or• ER matching contribution of 3%, or• ER non-elective contribution of 2%• Employee contributions $11,500 in

2009 and 2010• Age 50 and over, an additional “catch-

up” of $2,500 in 2009 and 2010p ,

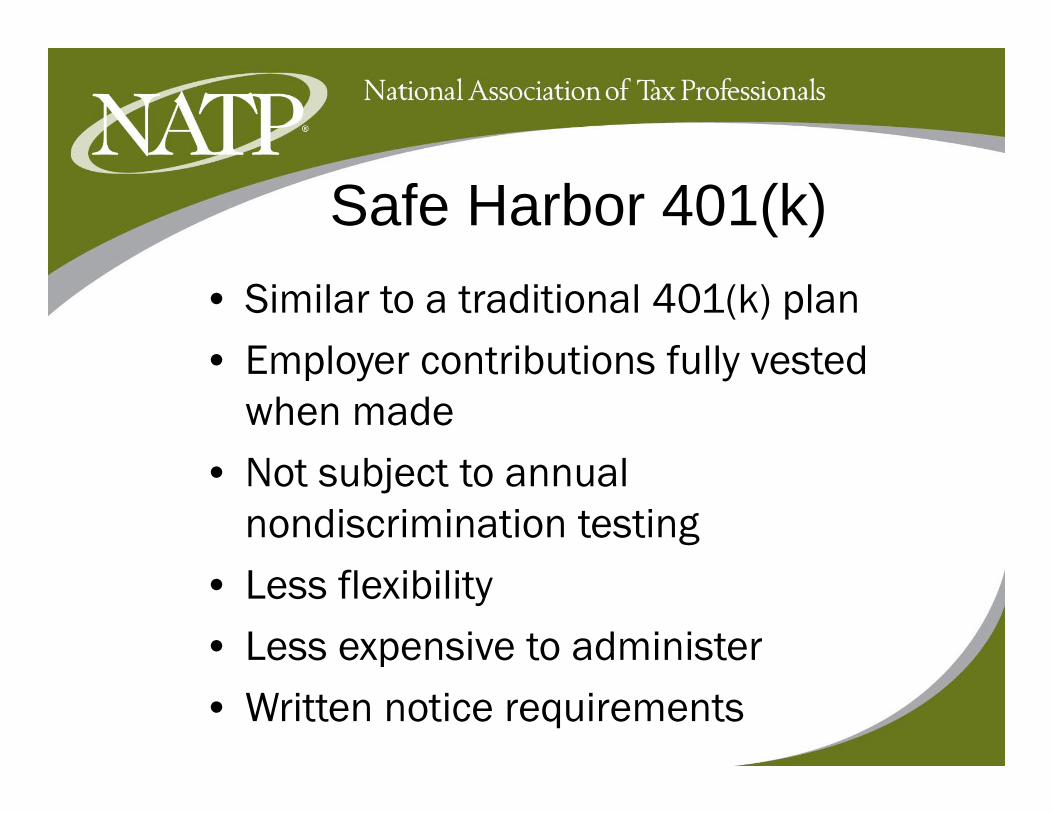

Safe Harbor 401(k)• Similar to a traditional 401(k) plan• Employer contributions fully vested • Employer contributions fully vested

when madeN bj l • Not subject to annual nondiscrimination testing

• Less flexibility• Less expensive to administerp• Written notice requirements

Safe Harbor 401(k)• Contributions: employer matching or

employer contribution regardless of employer contribution regardless of employee elective deferrals allowed

• If no additional contributions are made • If no additional contributions are made in a year, exempted from the top-heavy rules of §416rules of §416

Automatic Enrollment 401(k)Automatic Enrollment 401(k)

• Employer automatically reduces employee’s Employer automatically reduces employee s wages by a fixed percentage or amount and contributes to plan

• Unless the employee has affirmatively chosen not to or has a different percentage

• These contributions qualify as elective deferrals, increase participation in plan

Automatic Enrollment 401(k)Automatic Enrollment 401(k)

• Eligible automatic contribution • Eligible automatic contribution arrangement (EACA)M ll l i hd • May allow employees to withdraw automatic enrollment contributions ( d i ) b l i (and earnings) by election

Automatic Enrollment 401(k)Automatic Enrollment 401(k)

• Qualified automatic contribution Qualified automatic contribution arrangement (QACA)

• Additional “safe harbor” provisionsAdditional safe harbor provisions• Exempt from annual discrimination testing

requirementsq• Matching or nonelective employer

contributions required• 100% vesting within 2 years

Single Owner / Employee 401(k)

• Not a special type of 401(k)Not a special type of 401(k)• Written plan document, within the provisions

of qualified plan rulesq p• Less administrative costs, no testing• 401(k) rules and definitions allow for a 401(k) rules and definitions allow for a

maximum addition of $49,000 with the lowest amount of compensation (2010)

• 130,000 x 25% = 32,500 + 16,500 = 49,000

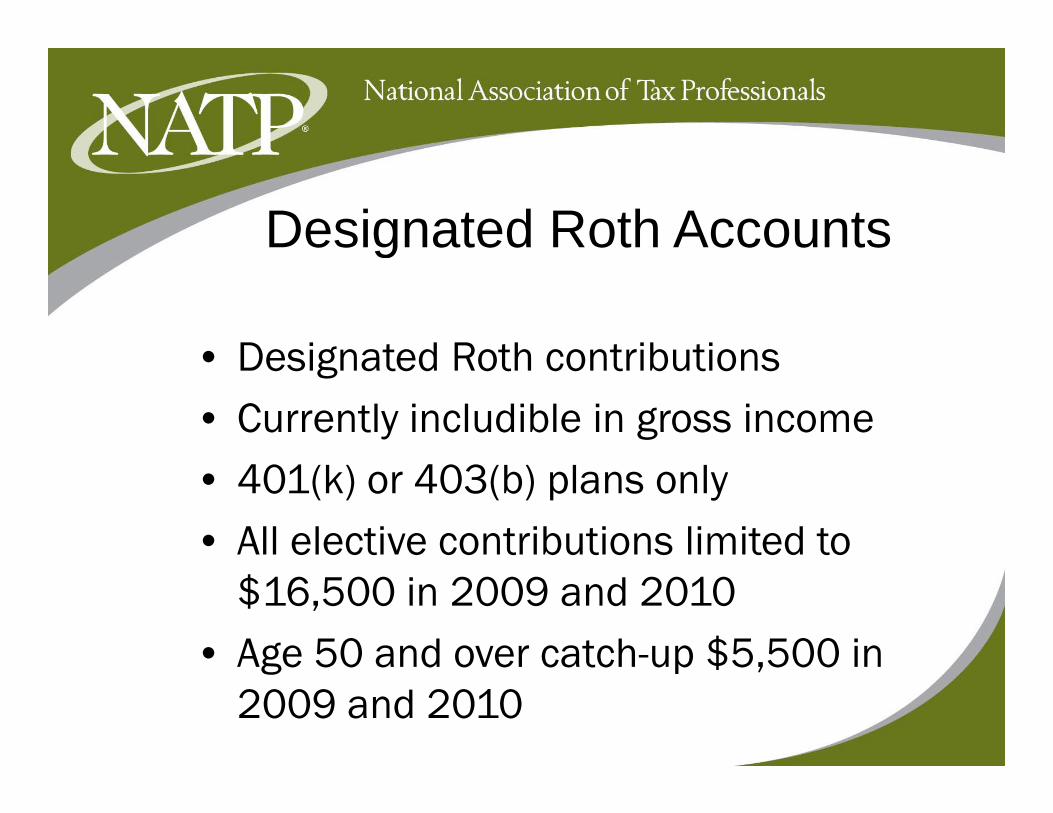

Designated Roth Accountsg

• Designated Roth contributions• Designated Roth contributions• Currently includible in gross income• 401(k) or 403(b) plans only• All elective contributions limited to

$16,500 in 2009 and 2010• Age 50 and over catch-up $5,500 in Age 50 and over catch up $5,500 in

2009 and 2010

Designated Roth AccountsDesignated Roth Accounts

• Roth automatic enrollment OKRoth automatic enrollment OK• No allocation of forfeitures and matching

contributionscontributions• Loans OK• Contributions not limited by incomeContributions not limited by income• Pre-tax elective contributions may not be

converted to a designated Roth accountconverted to a designated Roth account

Summary of Limits• Maximum total annual contributions - the lesser of

$49,000 or 100% of compensation in 2009 and 20102010

• All elective contributions limited to $16,500 in 2009 and 2010

• Age 50 and over catch-up $5,500 in 2009 and 2010

• Compensation considered $245 000 in 2009 and • Compensation considered $245,000 in 2009 and 2010

• Employer contribution limited to lesser of 25% of p ycompensation or $49,000 in 2009 and 2010– 20% for self-employed

Summary of Limits –$50 000 (Self employed)$50,000 (Self-employed)

Age 55, 2009 Contributions:Employee Catch-up Employer Totalp y p p y

SEP-IRANot

AllowedNot

Allowed 9,294 9,294

SIMPLE-IRA 11,500 2,500 1,385 15,385

Profit Sharing Not

AllowedNot

Allowed 9,294 9,294

SIMPLE 401(k) 11,500 2,500 1,385 15,385

401(k) 16 500 5 500 9 294 31 294 401(k) 16,500 5,500 9,294 31,294

Summary of Limits –$150 000 (Self employed)$150,000 (Self-employed)

Age 55, 2009 Contributions:Employee Catch-up Employer Totalp y p p y

SEP-IRANot

AllowedNot

Allowed 28,274 28,274

SIMPLE-IRA 11,500 2,500 4,236 18,236

Profit SharingNot

AllowedNot

Allowed 28,274 28,274

SIMPLE 401(k) 11,500 2,500 4,236 18,236

401(k) 16 500 5 500 28 274 50 274 401(k) 16,500 5,500 28,274 50,274

Summary of Limits –$300 000 (S lf l d)$300,000 (Self-employed)

Age 55, 2009 Contributions:E l C t h E l T t lEmployee Catch-up Employer Total

SEP-IRANot

AllowedNot

Allowed 49,000 49,000

SIMPLE-IRA 11,500 2,500 8,671 22,671

Profit SharingNot

AllowedNot

Allowed 49 000 49 000 Profit Sharing Allowed Allowed 49,000 49,000

SIMPLE 401(k) 11,500 2,500 8,671 22,671

401(k) 16,500 5,500 32,500 54,500

Summary of Limits –$50 000 (Employee)$50,000 (Employee)

Age 55, 2009 Contributions:Employee Catch-up Employer Total

SEP-IRA 12,500 12,500

SIMPLE IRA 11 500 2 500 1 500 15 500 SIMPLE-IRA 11,500 2,500 1,500 15,500

Profit Sharing 12,500 12,500 SIMPLE SIMPLE 401(k) 11,500 2,500 1,500 15,500

401(k) 16,500 5,500 12,500 34,500 0 ( ) 6,500 5,500 ,500 3 ,500

Summary of Limits –$150 000 (Employee)$150,000 (Employee)

Age 55, 2009 Contributions:Employee Catch-up Employer TotalEmployee Catch-up Employer Total

SEP-IRA 37,500 37,500

SIMPLE-IRA 11,500 2,500 4,500 18,500

Profit Sharing 37,500 37,500 gSIMPLE 401(k) 11,500 2,500 4,500 18,500

401(k) 16,500 5,500 32,500 54,500

Summary of Limits –$300 000 (Employee)$300,000 (Employee)

Age 55, 2009 Contributions:Employee Catch-up Employer Totalp y p p y

SEP-IRA 49,000 49,000

SIMPLE-IRA 11,500 2,500 9,000 23,000 Profit Sharing Plan 49,000 49,000

SIMPLE 401(k) 11,500 2,500 9,000 23,000

401(k) 16 500 5 500 32 500 54 500 401(k) 16,500 5,500 32,500 54,500

Other Issues:• Hiring a Spouse

• When To Adopt?p

• Updating or Changing Plans

Other Issues:

• More Than One PlanPer Employee– Per Employee

– Per Employer

• Rollovers as Business Start-Ups Rollovers as Business Start Ups (ROBS)

Thank You!!