Retail Payment Systems: What role for the Central...

20

Retail Payment Systems: What role for the Central Bank and other Public Sector Authorities? Jose Antonio Garcia The World Bank Cape Town, April 2009

-

Upload

doannguyet -

Category

Documents

-

view

218 -

download

0

Transcript of Retail Payment Systems: What role for the Central...

Retail Payment Systems: What role for the Central Bank and other Public Sector Authorities?

Jose Antonio GarciaThe World Bank

Cape Town, April 2009

Contents• A few facts and preliminary observations from the

WB Global Payment Systems Survey 2008 and

“Measuring Payment System Development”

• The role of the Central Bank and other authorities in

the development of retail payment systems: the

experience of the World Bank’s PSDG

Retail Payment Systems: where do we stand at the moment?

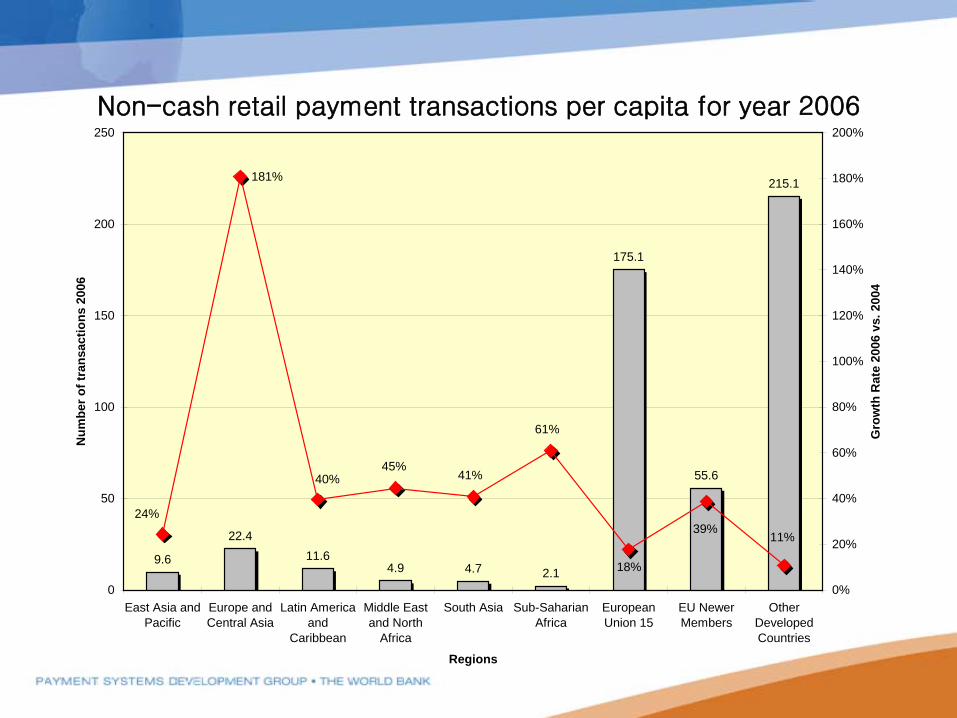

Non-cash retail payment transactions per capita for year 2006

9.6

22.411.6

4.9 4.7 2.1

175.1

55.6

215.1181%

24%

40%45%

41%

61%

18%

39%11%

0

50

100

150

200

250

East Asia andPacific

Europe andCentral Asia

Latin Americaand

Caribbean

Middle Eastand North

Africa

South Asia Sub-SaharianAfrica

EuropeanUnion 15

EU NewerMembers

OtherDevelopedCountries

Regions

Num

ber o

f tra

nsac

tions

200

6

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Gro

wth

Rat

e 20

06 v

s. 2

004

Retail Payment Systems-Subcomponent 1

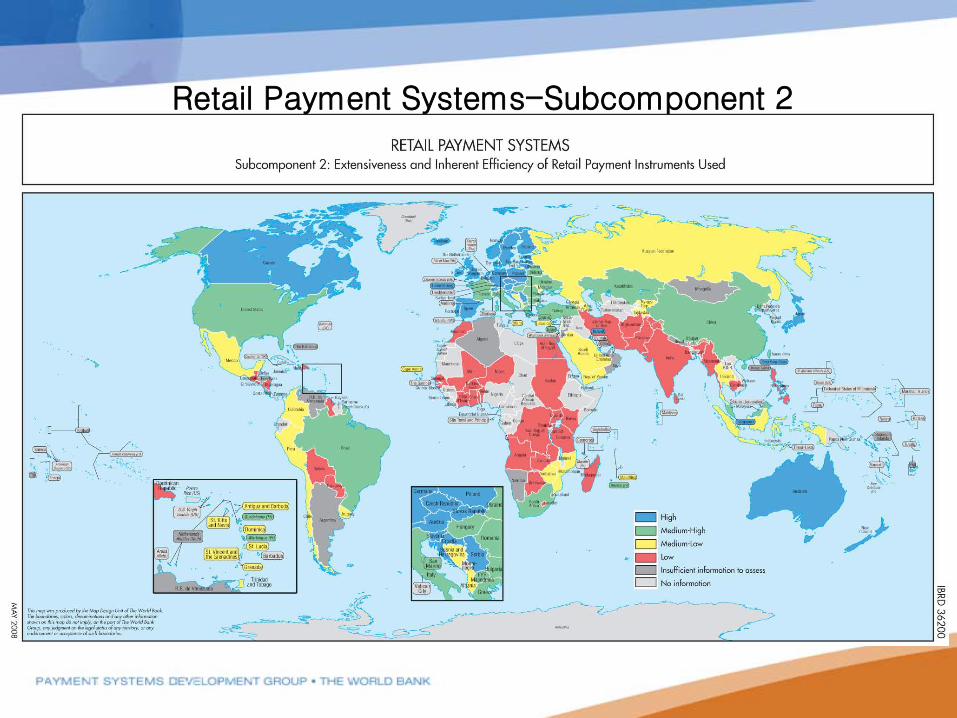

Retail Payment Systems-Subcomponent 2

Preliminary Observations

• “Measuring Payment System Development” shows that a country’s level of development in the area of retail payment systems has a very strong correlation with that country’s overall stage of developmentFew minor exceptions

• In areas such as Large-value systems and the Legal Framework, this is not necessarily the case. Many countries have already achieved a “high” or “medium-high” level of development in these areas despite their status as low-income or lower-middle income countries

Preliminary Observations (cont.)

• While Legal reforms and improvements to Large-value systems are coordinated/undertaken by a central agent (i.e. the Central Bank), for the most part the development of retail payment systems has been left to so-called “market forces”

• Based on all the above:

Can the Central Bank (and other authorities) influence the development of retail systems?

Should they?

If so, how?

The role of the Central Bank and other authorities in the development

of Retail Payment Systems: the experience of the WB’s PSDG

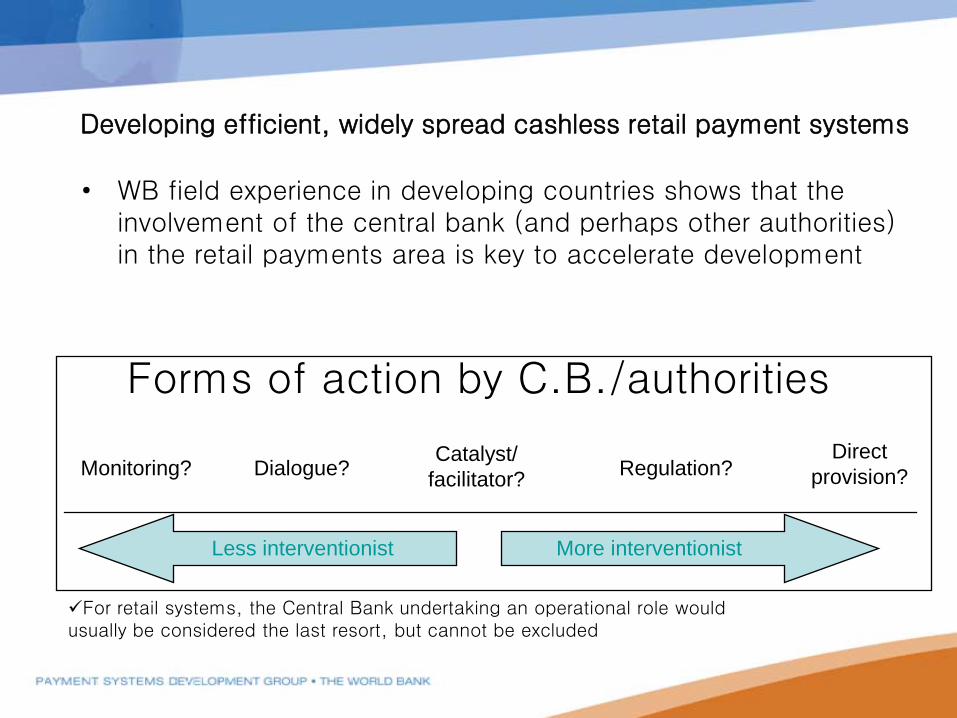

Developing efficient, widely spread cashless retail payment systems

• WB field experience in developing countries shows that the involvement of the central bank (and perhaps other authorities) in the retail payments area is key to accelerate development

Direct provision?

Less interventionist More interventionist

Monitoring? Dialogue?Catalyst/

facilitator? Regulation?

Forms of action by C.B./authorities

For retail systems, the Central Bank undertaking an operational role would usually be considered the last resort, but cannot be excluded

Strategies and Actions

• WB experience shows that one of the most (if not the most) important accelerators of retail payment sytem development is the “full inclusion and buy-in” of government entities that handle large volumes of payment transactions National Treasury and Tax Collection Agency (if different)

Social Security Institution

Utilities

...

• Indeed, strong partnerships with these entities are key to:1. Reduce the use of cash and/or paper-based instruments

2. Achieve a “critical mass” of transaction volumes in new or planned systems to make them financially viable/profitable

3. Accelerate the adoption of modern payment instruments by broader segments of the population (which may, in some cases, also result in higher bancarization levels)

Strategies and Actions: Government Payments & Collections

• Discussions on, and work towards the development of new retail systems should therefore include the active participation from key government stakeholders If applicable, better to include them during the design phase

Keep in mind the “big picture”: the potential savings in efficiency for government payments & collections are usually far much greater than the cost of the new system(s)

To the extent possible, tailor the new systems to the needs of relevant public sector entities in order to include as many transactions as possible and, especially, achieve high STP ratios

All this will also require major changes on the side of the government: from an operational standpoint, but also changes in the overall mentality and business paradigm

When difficulties arise and the situation becomes stagnant, the Central Bank is usually the only effective facilitator/mediator

• Ensure that the Central Bank has sufficient powers and resources to exercise its oversight function over retail payment systems This includes a clear definition of the objective of its involvement and

the tools it intends to use to achieve those objectives

• However, experience shows that Central Banks do not necessarily need to wait for legal empowerment in order to carry out some “basic” oversight activities for retail payment systems like monitoring, collecting statistics, engaging in dialogue, etc.

Strategies and Actions: Central Bank Oversight

A “light approach” for Central Banks in retail payments:

1. Monitor developments, including collection of statistics and opinions from market participants, consumers, etc.

2. Ensuring the legal and regulatory framework are adequate for the proper development of retail payment instruments, services and systems

3. Ensure that an appropriate cooperative framework is in place among market participants and between market participants and regulators

Strategies and Actions: Central Bank Oversight (cont.)

A “light approach” for Central Banks in retail payments (cont.):

4. Set up appropriate mechanisms to detect and contain frauds in the use of retail instruments

5. The Central Bank making available its settlement services to payment service providers For example, settlement services in central bank money

Strategies and Actions: Central Bank Oversight (cont.)

A “less than light approach” for Central Banks in retail payments:

6. Exercising the CB’s catalyst role effectively Facilitate agreements between service providers (e.g. interoperability,

participation of government entities, balanced regulations, etc.)

In general, foster cooperation on infrastructure and competition on value added services

7. Identify (and then promote the adoption of) incentives for individuals and business to start/increase their usage of modern payment instruments and services These incentives are usually linked to pricing policies

8. Carry out an effective payment system oversight that ensures fair competition and access, transparency in prices & terms and conditions of services, proper consumer protection, etc.

Strategies and Actions: Central Bank Oversight (cont.)

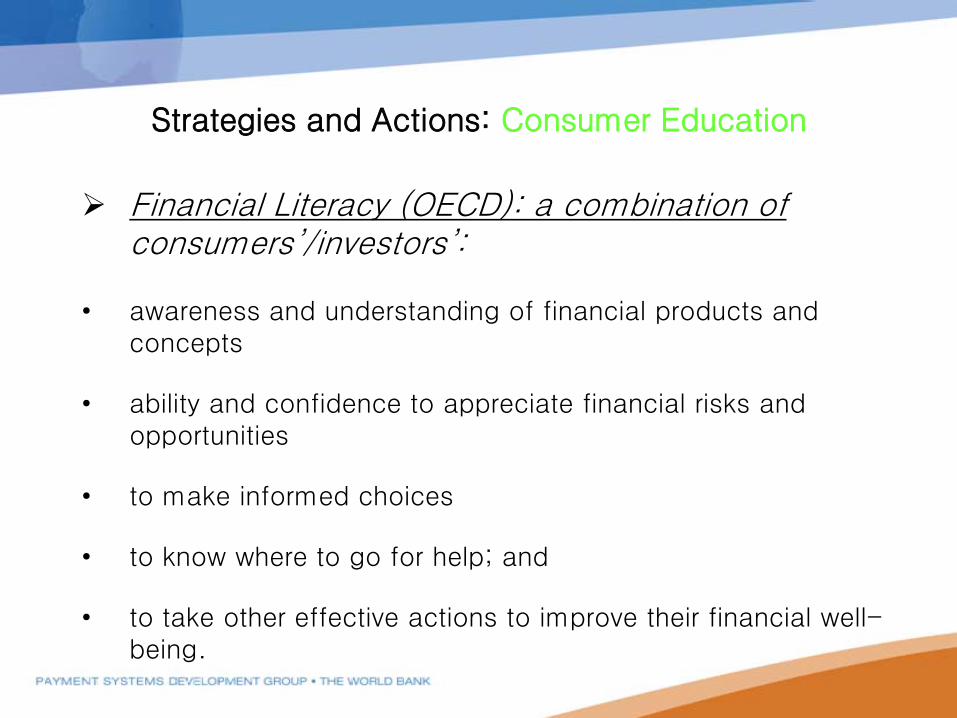

Financial Literacy (OECD): a combination of consumers’/investors’:

• awareness and understanding of financial products and concepts

• ability and confidence to appreciate financial risks and opportunities

• to make informed choices

• to know where to go for help; and

• to take other effective actions to improve their financial well-being.

Strategies and Actions: Consumer Education

... a combination that leads to consumer/investor:

Knowledge – Action - Empowerment

Strategies and Actions: Consumer Education (cont.)

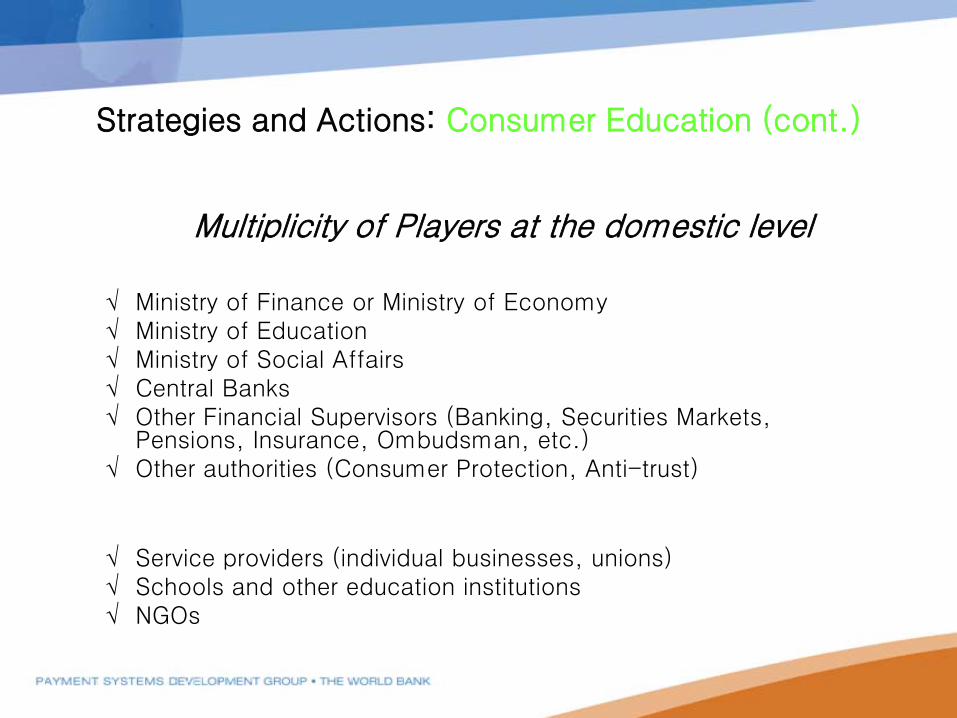

Multiplicity of Players at the domestic level

Public SectorAgencies√ Ministry of Finance or Ministry of Economy√ Ministry of Education√ Ministry of Social Affairs√ Central Banks√ Other Financial Supervisors (Banking, Securities Markets,

Pensions, Insurance, Ombudsman, etc.)√ Other authorities (Consumer Protection, Anti-trust)

Private Sector Agents√ Service providers (individual businesses, unions)√ Schools and other education institutions√ NGOs

Strategies and Actions: Consumer Education (cont.)

Thank you!

Jose Antonio [email protected]

Payment Systems Development GroupThe World Bank

www.worldbank.org/paymentsystems

PPP Goals