Retail Marketing 2013: Organizational Drift - RSR Research · PDF filefrom price-only strategy...

32

Retail Marketing 2013: Organizational Drift Benchmark Report 2013 Nikki Baird & Steve Rowen, Managing Partners August 2013 Sponsored by: Supported by:

Transcript of Retail Marketing 2013: Organizational Drift - RSR Research · PDF filefrom price-only strategy...

Retail Marketing 2013:

Organizational Drift

Benchmark Report 2013 Nikki Baird & Steve Rowen, Managing Partners

August 2013

Sponsored by:

Supported by:

ii

Executive Summary

Retail marketing has received a tremendous amount of attention over the last 18 months. It has gone from its own department doing its own thing - down to its own technology purchases - to the center of attention in an enterprise-wide omni-channel transformation. Big, rapid changes mean lots of new challenges, and this year's benchmark report shows that retailers are feeling the pressure.

Key findings • Retailers appear to be turning the corner on uncertainty about the economy and

uncertainty about what role marketing should ultimately play within the enterprise - secondary to merchandising? Or primary function that stands on its own?

• Laggards seem to be on the cusp of leaving behind price as their only competitive differentiator. This has enormous implications for marketing, as they attempt to move from price-only strategy and communications, to more brand-oriented marketing.

• Marketing has a lot on its plate already, and the retailers who are moving quickly to consolidate digital and traditional marketing are creating enough pressure on their marketing departments that key digital strategies are getting left behind.

• Marketing is much more important to the retail enterprise, and thus marketing tools have increased in their perceived value to the retailers participating in our survey, almost across the board. However, a showdown is coming as to which platform will ultimately be the single customer interaction platform that retailers are looking for: will it be CRM or will it be the digital marketing platform that ultimately wins?

BOOTstrap Recommendations Because retailers are focused on so much organizational and process change within the marketing department, our recommendations focus on helping retailers ensure they minimize the disruptive nature of their transformation. Most important, retailers need to remember that a shift in strategy - from cost cutting to growth - also necessitates a shift in both marketing strategy and tactics. Such a shift also has big implications for technology investments - if retailers can successfully navigate the uncertain future of retail marketing platforms.

iii

Table of Contents Executive Summary ........................................................................................................................ ii Research Overview ......................................................................................................................... 1

Big Changes in Process for Retail Marketing .............................................................................. 1 Defining Winners and Why They Win .......................................................................................... 2 Methodology ................................................................................................................................ 3 Survey Respondent Characteristics ............................................................................................ 3

Business Challenges ....................................................................................................................... 4 Back to the Future ....................................................................................................................... 4 Answering the Question ............................................................................................................... 5 Containing the Excitement ........................................................................................................... 6

Opportunities ................................................................................................................................... 7 The Barriers Have Fallen ............................................................................................................. 7 As Goes the Strategy, So Go the Channels ................................................................................ 8 Speed is Not Always Good, Even in Marketing ......................................................................... 10

Organizational Inhibitors ................................................................................................................ 13 Old vs. New ............................................................................................................................... 13 Two Different Takes ................................................................................................................... 14 Who’s Driving This Thing? ......................................................................................................... 16

Technology Enablers ..................................................................................................................... 19 No Shortage of Interest .............................................................................................................. 19 Great, But… ............................................................................................................................... 20

BOOTstrap Recommendations ..................................................................................................... 24 Returning to Growth Means Changing the Strategy .................................................................. 24 When Strategy Changes, So Should Tactics ............................................................................. 24 Consolidation Means "Bring Together" ...................................................................................... 24 Platforms Require Careful Evaluation ........................................................................................ 25

Appendix A: RSR’s Research Methodology .................................................................................... a Appendix B: About Our Sponsors ................................................................................................... b Appendix C: About RSR Research ................................................................................................. c

iv

Figures Figure 1: Knowing More but Doing Less ......................................................................................... 1

Figure 2: Doing More - A Winning Behavior .................................................................................... 2

Figure 3: Turning the Corner ........................................................................................................... 4

Figure 4: Some Turn Slower Than Others ...................................................................................... 5

Figure 5: Settling the Ownership Question ...................................................................................... 5

Figure 6: Consensus around Data Is Easy ...................................................................................... 6

Figure 7: Surprise! You Can't Compete On Price Alone ................................................................. 7

Figure 8: A Glimmer of Hope for Laggards ..................................................................................... 8

Figure 9: Things Have Changed While You Were Away ................................................................. 9

Figure 10: Dipping a Toe into Digital Waters ................................................................................... 9

Figure 11: Slow and Steady Wins? ............................................................................................... 10

Figure 12: It's Never Enough ......................................................................................................... 11

Figure 13: Laggards and Strategic Value - Who Knew? ............................................................... 11

Figure 14: The More Things Change, the More They Stay the Same ........................................... 13

Figure 15: Winners Tread Lightly Around Org Change and Culture ............................................. 14

Figure 16: Platform and On-Demand Rule the Roost ................................................................... 15

Figure 17: Laggards Swear They Need To Get Strategic ............................................................. 15

Figure 18: CEO And CMO Win The Customer Experience Battle... ............................................. 16

Figure 19: ...But Have They Won the War? .................................................................................. 17

Figure 20: Winners Say Yes, Laggards Undecided ...................................................................... 18

Figure 21: The Value Stampede ................................................................................................... 19

Figure 22: Winners Have a Different Value Emphasis .................................................................. 20

Figure 23: Still a Lot of Gaps to Fill ............................................................................................... 21

Figure 24: Uneven Adoption .......................................................................................................... 22

Figure 25: Big Appetites, Small Plates .......................................................................................... 22

1

Research Overview

Big Changes in Process for Retail Marketing In retail, the marketing message has long been the front line of customer centricity and omni-channel transformation. When retailers first realized they needed "one face to the customer" across channels, the marketing messages were the first (and easiest) to change. That didn't mean they were good at it, or that they could at all deliver on the cross-channel promises they were making, but that didn't stop them from making those promises. And many retailers, when choosing to take on consolidation across channels, looked to marketing as the starting point for that process - looking to combine traditional and online marketing teams.

At the same time, the relative importance of marketing within the retail enterprise has rapidly been rising, driven largely by the need to actually keep a lot of those cross-channel promises. As RSR found in our last two benchmark surveys on marketing topics, retailers are busy consolidating their marketing activities and elevating marketing leadership from a supporting role for merchandising to a genuine seat at the executive table.

However, just because the future looks bright for the marketing department, retailers are not necessarily well-positioned to deliver on customer expectations, whether in terms of the brand promise, the product value proposition, or the shopping experience. As this year's benchmark will show, while marketing is still the first internal organization to respond to the transformational pressures of omni-channel retailing, it still has a long way to go, and a lot of pitfalls along the way.

As a case in point, we asked retailers to rate the degree to which they agree or disagree with a series of statements related to their overall marketing sophistication. In 2013, more respondents agreed more strongly that their customer loyalty program - a foundational element to collecting and understanding customer data - is critical to their marketing strategy. They also more strongly agreed with the idea that they know who their best shoppers are. But when it comes to execution, the story changes (Figure 1).

Figure 1: Knowing More but Doing Less

Source: RSR Research, August 2013

18%

22%

32%

15%

28%

36%

My company is proficient at targeted marketing across channels.

My company knows who our best shoppers are.

Our customer loyalty program is a foundational element of our marketing

strategy.

Marketing Sophistication: "Strongly Agree"

2013 2012

2

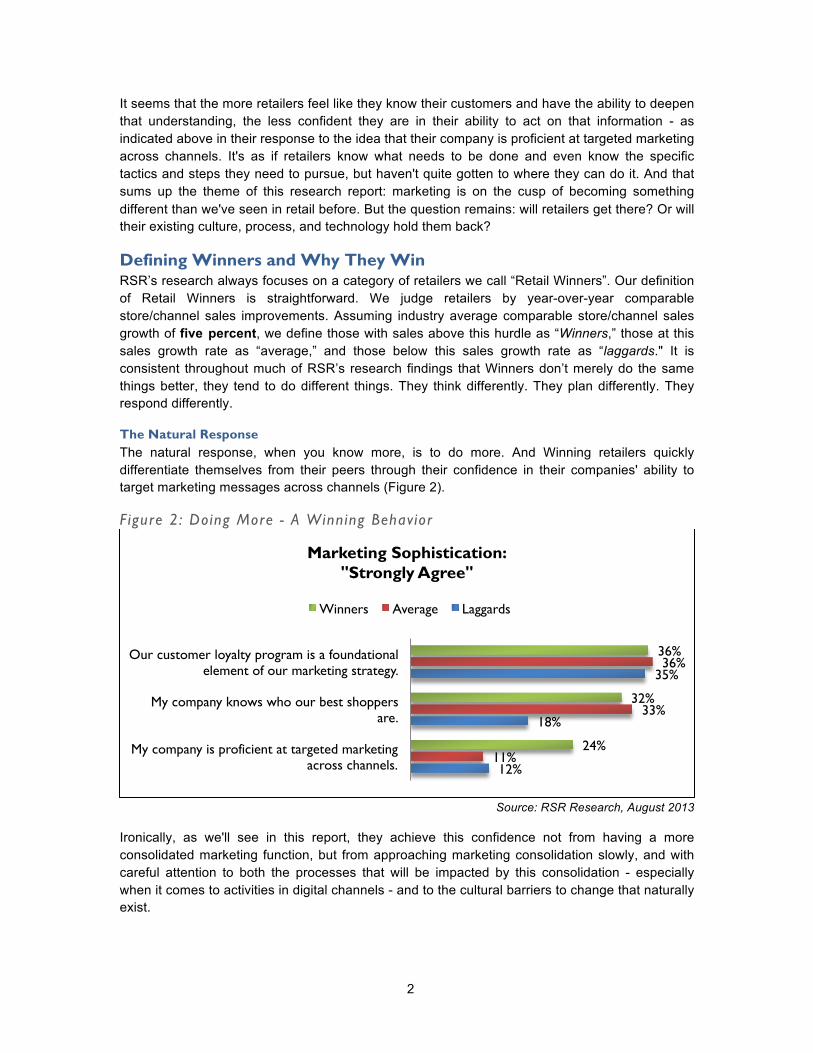

It seems that the more retailers feel like they know their customers and have the ability to deepen that understanding, the less confident they are in their ability to act on that information - as indicated above in their response to the idea that their company is proficient at targeted marketing across channels. It's as if retailers know what needs to be done and even know the specific tactics and steps they need to pursue, but haven't quite gotten to where they can do it. And that sums up the theme of this research report: marketing is on the cusp of becoming something different than we've seen in retail before. But the question remains: will retailers get there? Or will their existing culture, process, and technology hold them back?

Defining Winners and Why They Win RSR’s research always focuses on a category of retailers we call “Retail Winners”. Our definition of Retail Winners is straightforward. We judge retailers by year-over-year comparable store/channel sales improvements. Assuming industry average comparable store/channel sales growth of five percent, we define those with sales above this hurdle as “Winners,” those at this sales growth rate as “average,” and those below this sales growth rate as “laggards." It is consistent throughout much of RSR’s research findings that Winners don’t merely do the same things better, they tend to do different things. They think differently. They plan differently. They respond differently.

The Natural Response The natural response, when you know more, is to do more. And Winning retailers quickly differentiate themselves from their peers through their confidence in their companies' ability to target marketing messages across channels (Figure 2).

Figure 2: Doing More - A Winning Behavior

Source: RSR Research, August 2013

Ironically, as we'll see in this report, they achieve this confidence not from having a more consolidated marketing function, but from approaching marketing consolidation slowly, and with careful attention to both the processes that will be impacted by this consolidation - especially when it comes to activities in digital channels - and to the cultural barriers to change that naturally exist.

12%

18%

35%

11%

33%

36%

24%

32%

36%

My company is proficient at targeted marketing across channels.

My company knows who our best shoppers are.

Our customer loyalty program is a foundational element of our marketing strategy.

Marketing Sophistication: "Strongly Agree"

Winners Average Laggards

3

The end result is that Winners do more marketing across channels, and yet are more confident in their ability to do that marketing well - with a single face to the customer.

Methodology RSR uses its own model, called the “BOOT MethodologySM,” to analyze Retail Industry issues. We build this model with our survey instruments. Appendix A contains a full explanation of the methodology.

In our surveys, we continue to find differences in the thought processes, actions, and decisions made by retailers who outperform their competitors and the industry at large – Retail Winners. The BOOT model helps us better understand the behavioral and technological differences that drive sustainable sales improvements and successful execution of brand vision.

Survey Respondent Characteristics RSR conducted an online survey from May - July 2013 and received answers from 122 qualified retail respondents. Respondent demographics are as follows:

• Job Title: Executive/Senior Management (CEO, CFO, COO, SVP) 19% Middle Management (VP/Director/Manager) 54% Internal Consultant/Staff 20% Other 7%

• 2011 Revenue (US$ Equivalent)

Less than $50 Million 24% $51 - $249 Million 17% $250 - $999 Million 26% $1 - $5 Billion 17% Over $5 Billion 16%

• Products sold:

Fashion / Short Lifecycle / Seasonal 30% Basic / Replenishment Goods 26% Durable Goods / Consumer Electronics 27% Perishable / Food 17%

• Headquarters/Retail Presence:

USA 70% 73% Canada 6% 30% Latin America 0% 16% Europe 7% 17% Middle East 4% 13% Africa 4% 11% Asia/Pacific 10% 23%

• Year-Over-Year Sales Growth Rates (assume average growth of 5%):

Better than average (Retail Winners) 38% Average 46% Worse than average (Laggards) 16%

4

Business Challenges

Back to the Future Retail respondents to this year's marketing benchmark indicated some significant shifts in their perception of their business challenges. And the decreases in challenge areas are just as important as the increases.

Top three on retailers' lists of business challenges include difficulty with customer retention and loyalty, keeping up with the new ways consumers are using technology (new to the list in 2013), and a tie between too many communication channels with unproven effectiveness and keeping up with all the new ways to engage with customers (Figure 3).

Figure 3: Turning the Corner

Source: RSR Research, August 2013

Customer retention and loyalty, and the challenges with maintaining both, have long been on the top-three list for marketing business challenges, but every year it appears to grow in importance. However, the driving reasons behind those increases seem to be shifting. For example, while retailers may be scrambling to keep up with consumers - whether in technology-driven ways or not - they certainly aren't scrambling to deal with a tough business environment: in 2012, 47% of survey respondents said that the uncertain economy constrained their marketing budget. In 2013, that number fell to 30%, putting it second from the bottom of the list.

Looking at business challenges by performance, it would appear that laggards are singing the same sad song they have been singing since the economic downturn began - laggard respondents are the driving factor behind both the difficulty with customer retention and loyalty and challenges differentiating their brand, while their forward-looking Winning peers are much more interested in the challenges posed by consumer use of technology (Figure 4).

23%

47%

41%

28%

29%

51%

26%

30%

41%

42%

42%

49%

61%

It's hard to differentiate our brand from our competition

The uncertain economy constrains our marketing budget

Customer segments are fragmenting, making it harder to reach our consumers

We can't keep up with all the new ways to engage with consumers

Too many communication channels have unproven effectiveness

We can’t keep up with the new ways consumers are using technologies

Customer retention has become more difficult and building customer loyalty is challenging

Top 3 Marketing Business Challenges

2013 2012

N/A

5

Figure 4: Some Turn Slower Than Others

Source: RSR Research, August 2013

However, as we'll see in the Opportunities section, what laggards are choosing to do about their business challenges appears to have taken a significant shift.

Answering the Question The biggest question over the last two years of RSR's marketing benchmark has been "Who owns the customer experience?" In the past, that answer has been muddled - even in 2012, over a third of respondents said "no one" in answer to that question.

In 2013, the answer has grown much more definitive. Those answering "no one" fell from 35% to 19%, and it wasn't just the CMO who benefited - almost every retail executive has stepped up ownership of the customer experience (Figure 5).

Figure 5: Sett l ing the Ownership Quest ion

Source: RSR Research, August 2013

61% 50%

24%

45%

59%

22% 31%

88%

44%

We can’t keep up with the new ways consumers are using

technologies

Customer retention has become more difficult and building

customer loyalty is challenging

It's hard to differentiate our brand from our competition

Marketing Business Challenges

Winners Average Laggards

8%

35%

6%

8%

8%

11%

25%

28%

19%

19%

23%

24%

25%

35%

38%

43%

eCommerce Executive

No explicit owner

Chief Merchant

COO

Chief Customer Experience Officer

VP Stores

CEO

Chief Marketing Executive

Customer Experience Owners 2013 2012

6

The only cautionary tale that exists in looking from 2012 to 2013 is that if retailers are going to have collective leadership and responsibility for the customer experience, then they need to ensure that everyone is working off of the same vision for what that customer experience should be. Otherwise, "everyone" yields the same results as "no one."

Fortunately, retailers appear to be putting in the foundational elements to make that shared vision possible - certainly, they are consolidating control over that most valuable resource, customer data. The percent of respondents reporting that Marketing is the primary owner of customer data internally nearly doubled from 2012 to 2013, from 33% to 61%, and those reporting "No explicit owner" fell from 33% to 17% (Figure 6).

Figure 6: Consensus around Data Is Easy

Source: RSR Research, August 2013

Other internal areas also have increased ownership over customer data - store operations, eCommerce/direct, and merchandising all showed increased ownership over 2012. However, this increase appears to be driven more from a recognition of the value of customer data that is generated in all aspects of the business (especially customer-facing ones), rather than a diversification of ownership over consolidated data sources.

Containing the Excitement When looking at the winds of change stirring around retail marketing, it's easy to get excited. The impact of the economic downturn is fading away, and while retailers are just as challenged by customer loyalty and retention as ever, it appears to be more in the context of keeping up with their changing expectations and new technology-driven behaviors. At the same time, retailers are getting focused when it comes to their marketing strategy - they are marshaling their executive team to focus on the customer experience, and they are defining that customer experience based on one view of the customer, owned by marketing and fed by all aspects of customer engagement. As we'll see in the next section, the Opportunities are bright. But there are still significant head winds that could blow retailers' marketing plans drastically off course.

5%

33%

7%

13%

14%

19%

33%

33%

10%

17%

20%

20%

22%

23%

34%

61%

Supply Chain / Fulfillment

No explicit owner

Merchandising

eCommerce/Direct Channels

Store Operations

Customer Service / Call Center

IT

Marketing

Customer Data Internal Owners

2013 2012

7

Opportunities

The Barriers Have Fallen Retailers' top marketing opportunity remained relatively unchanged from 2012 to 2013: more effective targeting by capturing more detailed customer preferences. Second on the list also held steady: a greater focus on customer experience, less on product. But after that, all bets were off (Figure 7).

Figure 7: Surprise! You Can't Compete On Pr ice Alone

Source: RSR Research, August 2013

Most dramatic was the shift at the bottom of the list, where interest in raising barriers to entry for competition fell from 35% in 2012 to a measly 8% of respondents rating it a top-three opportunity in 2013. Along with that, the percent of respondents believing that customers themselves could help identify differentiating products, for example through things like crowdsourcing, fell almost by half - from 44% in 2012 to 23% in 2013. And more practical and less ambitious opportunities, like using digital channels to drive traffic to stores, increased from 28% of respondents in 2012 to 44% in 2013.

The result appears to be that retailers now recognize that price and/or product are not enough to differentiate their brand. They need to focus on the customer experience to win, and they need to use digital channels not to build a separate customer experience, but to create links between the physical experience and digital realms.

This shift is where laggards really shine. Winners and laggards both reported an overriding interest in focusing more on the customer experience and less on product (Figure 8).

35%

44%

41%

38%

40%

28%

48%

52%

8%

23%

25%

28%

31%

42%

44%

48%

53%

Raise the barriers to entry for competitors

Develop better products and services through more direct customer input (i.e., crowdsourcing)

Switch our company from primarily traditional marketing tactics to primarily digital marketing

Become more focused on our company's brand promise to consumers

New marketing channels enable us to truly differentiate our brand

Turn customers into brand advocates through social media

Use digital channels to drive traffic to stores

A greater focus on customer experience, less on product

More effective targeting by capturing more detailed customer preferences

Top 3 Marketing Opportunities 2013 2012

N/A

8

Figure 8: A Gl immer of Hope for Laggards

Source: RSR Research, August 2013

But laggards took it one step further, putting emphasis on becoming more focused on the company's brand promise to consumers and developing more customer-focused products. No laggards reported wanting to raise the barriers to entry for competitors, and they were much more skeptical than peers on new marketing channels' ability to help them differentiate their brand.

We're going to take this as a positive sign for laggards, who, since the economic downturn, have been in near-panic mode about conserving existing business and not focusing on trying to grow or acquire new customers. In our most recent Pricing and Store benchmarks, laggards were particularly pessimistic, pursuing low-price-at-any cost pricing strategies, and looking forward to a future where they were closing stores rather than opening new ones.

Given how much the economy has diminished as a business challenge for retailers, it appears that laggards are shifting their strategy from maintain/cut to grow. The question remains - is this because the economy is improving, or is it because they have lived with pervasive economic uncertainty long enough that they've just decided it's time to stop waiting? It's too early to tell, but we will be watching this apparent shift to growth closely to see if it lasts.

As Goes the Strategy, So Go the Channels The biggest caveat to laggards' shift in strategy (from maintain existing customers to acquire new ones) is that their tactics will also need to change. The biggest question remaining from the economic downturn is how much lasting impact will it have on shopper behavior? That's a difficult question to answer when so much shopper behavior was also impacted by technology. Winning retailers appear to recognize the second half of consumer behavior shifts (to more technology

0%

31%

44%

19%

13%

44%

50%

44%

56%

6%

19%

27%

38%

25%

46%

44%

56%

35%

13%

24%

24%

29%

32%

37%

42%

53%

61%

Raise the barriers to entry for competitors

Develop better products and services through more direct customer input (i.e., crowdsourcing)

Become more focused on our company's brand promise to consumers

New marketing channels enable us to truly differentiate our brand

Switch our company from primarily traditional marketing tactics to primarily digital marketing

Turn customers into brand advocates through social media

Use digital channels to drive traffic to stores

More effective targeting by capturing more detailed customer preferences

A greater focus on customer experience, less on product

Top 3 Marketing Opportunities Winners Average Laggards

9

use) and have moved to expand the digital communication channels they use to engage with customers. Laggards have not moved to nearly the same degree (Figure 9).

Figure 9: Things Have Changed While You Were Away

Source: RSR Research, August 2013

Winners and average performing retailers have shifted their focus from traditional media like print, TV, and radio, to search advertising, Facebook or other social networks, Twitter, and even mobile advertising to a lesser extent. Laggards are still primarily focused on traditional media, direct mail, and email. In other words, they are not necessarily in all the places where their shoppers engage.

However, even that is changing to some degree. When we look at the percent of retailers reporting "no plans" to leverage a type of communication channel, we see that laggards are consistent about avoiding digital channels - with one exception, Facebook (Figure 10).

Figure 10: Dipping a Toe into Digital Waters

Source: RSR Research, August 2013

62% 72%

68% 72%

57% 69%

56% 39%

55% 51% 69%

59% 49% 56%

39% 24%

92% 83%

75% 77%

42% 54% 42%

33%

Traditional media

(print, TV, radio)

Direct Mail Email Online advertising

(display, video)

Search advertising

Facebook or other social

network

Twitter Mobile advertising

Communication Channels "Longer Than 1 Year" Winners Average Laggards

10% 7% 7% 10% 14%

3% 7%

11% 10%

19%

2% 2%

15% 10%

20% 17%

8% 8%

0%

15%

33%

0%

17%

25%

Traditional media

(print, TV, radio)

Direct Mail Email Online advertising

(display, video)

Search advertising

Facebook or other social

network

Twitter Mobile advertising

Communication Channels "No Plans"

Winners Average Laggards

10

When it comes to moving into digital channels, for some reason lagging retailers feel most secure about pursuing Facebook as the entrée into digital customer engagement. Oddly, they are least enamored with search advertising - professing no plans there at over twice the rate of their peers. We'll see in the Organizational Inhibitors section that there are reasons why laggards are slow to move into these digital channels - it has a lot to do with their capacity to manage marketing innovations - but it may also have a lot to do with who owns which communication channels, and that is an area still in flux.

Speed is Not Always Good, Even in Marketing It appears that laggards have moved the fastest when it comes to consolidating their cross-channel marketing activities under the umbrella of corporate marketing. Winners have moved the slowest (Figure 11).

Figure 11: Slow and Steady Wins?

Source: RSR Research, August 2013

Retailers have a difficult balancing act to maintain here. Customers aren't going to wait around for retailers to figure out how to use digital channels to engage with them. In fact, by the time retailers figure out one digital channel, consumers are off to the next new one. One of the advantages of having the eCommerce team and/or a digital marketing specialty team focus on some of these emerging channels has been that retailers have been able to engage in a lot of innovation quickly.

The downside has been that retailers haven't been very consistent about telling their brand story across channels, and this confuses customers - thus the move to consolidate marketing channels so that it's easier to present one face to consumers.

If retailers move too fast to consolidate marketing, they risk missing important new engagement channels. And thus, laggards are more highly consolidated into central corporate marketing, but are less involved in more emerging digital channels.

66% 59%

45% 44% 43% 41% 41% 34%

66% 68% 64% 58% 62%

50% 48% 40%

75% 83%

67% 82%

73% 67% 64%

55%

Traditional media

(print, TV, radio)

Direct Mail Facebook or other social

network

Email Twitter Online advertising

(display, video)

Mobile advertising

Search advertising

Communication Channel Owners "Corporate Marketing Owns"

Winners Average Laggards

11

This is reflected in where retailers perceived their marketing departments are spending their time - "not enough time" clearly outweighs "too much time" in the chart below (Figure 12).

Figure 12: I t 's Never Enough

Source: RSR Research, August 2013

And here again, laggards have a lot to say about how their marketing departments need to shift to growth-oriented tactics (Figure 13).

Figure 13: Laggards and Strategic Value - Who Knew?

Source: RSR Research, August 2013

7%

13%

14%

17%

18%

18%

23%

36%

49%

56%

46%

55%

39%

55%

57%

38%

30%

37%

27%

44%

22%

Acquiring new customers

Engaging customers

Driving sales

Driving traffic (stores, website)

Building the brand

Building customer loyalty

Communicating promotions

Marketing Dept Time Spent

Too Much Time Right Amount of Time Not Enough Time

46%

46%

62%

23%

69%

46%

100%

21%

27%

38%

17%

43%

32%

48%

27%

27%

27%

28%

33%

40%

52%

Building the brand

Driving sales

Engaging customers

Communicating promotions

Building customer loyalty

Driving traffic (stores, website)

Acquiring new customers

Marketing Dept Time Spent "Not Enough Time"

Winners Average Laggards

12

An amazing 100% of laggard respondents report that their marketing departments are not spending enough time acquiring new customers. This is a dramatic shift from what we've seen in the past, where laggards were overly focused on communicating promotions, driving traffic, and driving sales. Now, they want to focus on building customer loyalty, engaging with customers, and building the brand.

However, as admirable as these goals are, they too are at risk from moving too aggressively to consolidate cross-channel marketing activities.

Dictionary.com defines "to consolidate" as 1) to bring together separate parts into a unified whole and 2) to discard unused or unwanted items and organize the remaining.1 If retailers treat cross-channel marketing consolidation cutting instead of reorganizing, they're putting themselves at risk of over-balancing more towards not doing enough innovation to keep up with consumers. Marketing consolidation needs to tend more towards definition #1 - bringing together disparate marketing resources so that they can more easily tell a single brand story across multiple touchpoints. But Marketing, as we'll see in the Organizational Inhibitors section below, already has too much on its plate to reduce the number of resources focused on marketing activities while bringing them all under one umbrella.

1 http://dictionary.reference.com/browse/consolidate?s=t

13

Organizational Inhibitors

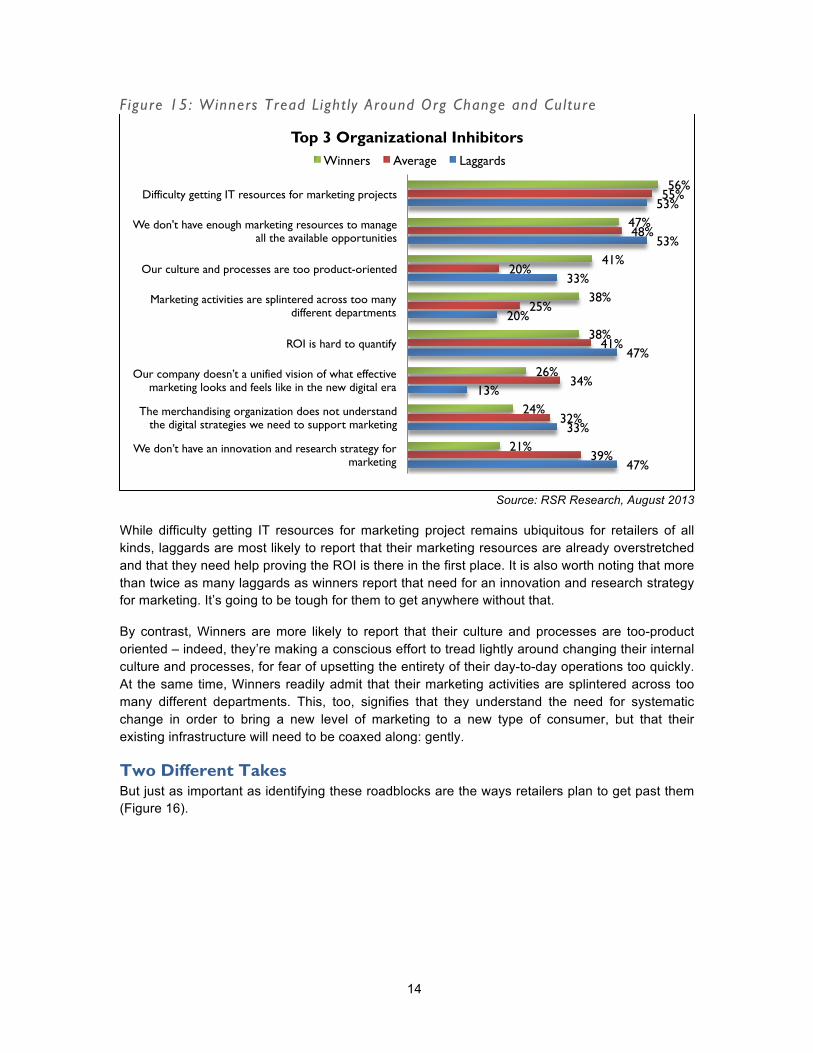

Old vs. New At the beginning of this report, we talked about how marketing is on the cusp of becoming something different, but expressed concern that retailers’ existing culture, technologies and processes may have the power to hold them back. Figure 14 confirms just how plausible that concern is.

Figure 14: The More Things Change, the More They Stay the Same

Source: RSR Research, August 2013

Last year’s top three organizational inhibitors take their exact place at the top of the list again – only this time, all three (difficulty getting IT resources, a lack of resources to manage new opportunities, and difficulty proving ROI in the first place) are even greater obstacles to retailers. In fact, at a time when respondents to many of our most recent topic-specific benchmark reports are telling us that the need to prove ROI is waning, it appears that marketing functions still require quite a bit of convincing and education when pushing them up the ranks. For some retailers (some more than others, as we’ll see in just a moment), just because Marketing now has a space at the big table doesn’t mean everyone there has bought in yet.

We were also very surprised to see that in, aggregate, “we don’t have an innovation and research strategy for marketing” – a first time option, was identified as a roadblock by 1 in 3 retailers.

However, when viewed by performance, we can see that laggards are the driving force behind many of these trends (Figure 15).

23%

33%

28%

27%

37%

38%

28%

29%

29%

30%

33%

41%

48%

55%

Our company doesn’t a unified vision of what effective marketing looks and feels like in the new digital era

Marketing activities are splintered across too many different departments

The merchandising organization does not understand the digital strategies we need to support marketing

Our culture and processes are too product-oriented

We don’t have an innovation and research strategy for marketing

ROI is hard to quantify

We don't have enough marketing resources to manage all the available opportunities

Difficulty getting IT resources for marketing projects

Top 3 Organizational Inhibitors 2013 2012

N/A

N/A

14

Figure 15: Winners Tread Light ly Around Org Change and Culture

Source: RSR Research, August 2013

While difficulty getting IT resources for marketing project remains ubiquitous for retailers of all kinds, laggards are most likely to report that their marketing resources are already overstretched and that they need help proving the ROI is there in the first place. It is also worth noting that more than twice as many laggards as winners report that need for an innovation and research strategy for marketing. It’s going to be tough for them to get anywhere without that.

By contrast, Winners are more likely to report that their culture and processes are too-product oriented – indeed, they’re making a conscious effort to tread lightly around changing their internal culture and processes, for fear of upsetting the entirety of their day-to-day operations too quickly. At the same time, Winners readily admit that their marketing activities are splintered across too many different departments. This, too, signifies that they understand the need for systematic change in order to bring a new level of marketing to a new type of consumer, but that their existing infrastructure will need to be coaxed along: gently.

Two Different Takes But just as important as identifying these roadblocks are the ways retailers plan to get past them (Figure 16).

47%

33%

13%

47%

20%

33%

53%

53%

39%

32%

34%

41%

25%

20%

48%

55%

21%

24%

26%

38%

38%

41%

47%

56%

We don’t have an innovation and research strategy for marketing

The merchandising organization does not understand the digital strategies we need to support marketing

Our company doesn’t a unified vision of what effective marketing looks and feels like in the new digital era

ROI is hard to quantify

Marketing activities are splintered across too many different departments

Our culture and processes are too product-oriented

We don't have enough marketing resources to manage all the available opportunities

Difficulty getting IT resources for marketing projects

Top 3 Organizational Inhibitors Winners Average Laggards

15

Figure 16: Platform and On-Demand Rule the Roost

Source: RSR Research, August 2013

In aggregate, retailers point to better coordination between the marketing department and selling channels, solutions that don’t further strain the IT department, and increased investment in a streamlined marketing technology platform as the best ways to overcome the inhibitors they identified in Figure 15. However, this data becomes even more interesting when viewed by who’s saying what (Figure 17).

Figure 17: Laggards Swear They Need To Get Strategic

Source: RSR Research, August 2013

Winners identify – at an inordinate rate – that an executive tasked with managing and improving the overall customer experience is key to ensuring new marketing techniques have relevance.

26%

19%

48%

46%

31%

35%

30%

43%

16%

17%

39%

40%

43%

45%

45%

47%

A savvy cross-channel agency to help manage our brand

Case studies/success stories in my vertical

Design a more differentiating value proposition and customer experience

An executive tasked with managing and improving the overall customer experience

More experimentation with new technologies

Investment in a streamlined marketing technology platform or infrastructure

Solutions that don't burden our IT department

More coordination between selling channels and marketing

Overcoming Inhibitors 2013 2012

52% 39% 36% 36%

50%

30% 27% 33%

73%

An executive tasked with managing and improving the overall customer experience

More experimentation with new technologies

Design a more differentiating value proposition and customer

experience

Overcoming Inhibitors

Winners Average Laggards

16

They know that absent this role, there is no master set of eyes at the front of the house. They’ve already told us they’re cognizant of the fact their internal organizational structures were built at a time when product-focused marketing was king. They’ve also told us they can’t upend those fractured systems and processes overnight without risking the dynamic that’s already made their culture and team members successful. What they can do, however, is ensure that even if the left hand can’t always see what the right hand is doing, this master set of eyes sees the finished product from the customer’s point of view. It is their absolute best chance of rectifying imperfections while they transition to newer marketing techniques.

By way of comparison, laggards say their best chance is to get strategic: 73% say that the ability to design a more differentiating value proposition and customer experience is what will get them over their organizational inhibitors. While it was encouraging to see laggards finally abandoning the notion that price could be their ultimate competitive differentiator earlier in this report, here we see a return to their more familiar territory: using hope as a strategy. Winners know that a differentiated customer experience is an outcome – not an ingredient.

Who’s Driving This Thing? At first blush, it appears marketing leaders have been steadily reclaiming control of setting marketing strategies (Figure 18).

Figure 18: CEO And CMO Win The Customer Experience Batt le . . .

Source: RSR Research, August 2013

However, it is important to determine who is driving this change. In fact, this data is heavily driven by the worst-performing retailers, who, as we’ve already seen, are far more likely to have consolidated their marketing departments (in the poorer definition of the word) beyond reason (Figure 19).

7%

17%

25%

16%

28%

23%

71%

52%

8%

13%

21%

23%

27%

32%

68%

73%

Supply Chain Leader

CIO

CFO

eCommerce/Direct Channels

COO/Store Operations

Merchandising Leader

CEO

Marketing Leader

Marketing Strategy Influencers

2013 2012

17

Figure 19: . . .But Have They Won the War?

Source: RSR Research, August 2013

In fact, 85% of laggards say their marketing leader influences their marketing strategy (compared to Winners’ 72%), but at the same time, 62% of laggards say their merchandising leader influences their marketing strategy (compared to only 28% of Winners). This begs the question: when both Winners and laggards told us one of their top marketing opportunities was to focus more on the customer experience and less on product, how is it that only laggards are enabling merchandising to continue to play such a dominant role in determining marketing’s direction?

The answer only becomes even clearer when we ask our retail respondents about who needs more influence in the overall marketing strategy: to no surprise, Winners have little interest in handing control over to anyone beyond marketing leaders and the CEO. Laggards are all over the road, though, with 33% wanting to get merchandising more involved than they already are, and another 33% saying that eCommerce and direct channels should have more say in marketing initiatives than they do today (Figure 20).

8%

15%

0%

38%

62%

15%

85%

54%

7%

26%

10%

17%

26%

29%

69%

64%

10%

17%

24%

24%

28%

31%

72%

79%

Supply Chain Leader

CFO

CIO

eCommerce/Direct Channels

Merchandising Leader

COO/Store Operations

Marketing Leader

CEO

Marketing Strategy Influencers

Winners Average Laggards

18

Figure 20: Winners Say Yes, Laggards Undecided

Source: RSR Research, August 2013

This is a misstep on the part of retailers whose sales are already struggling. If marketing functions are to move forward – not backwards – it’s going to take strong leadership from the person who knows the most about marketing, in the first place: they should be charged (and held accountable) for marketing’s overall effectiveness, with an eye towards providing one view to the customer. Haphazard marketing techniques by varying departments - who will undoubtedly take a product-focuses approach - will only hurt this cause, as will attempts to achieve big-picture consensus by committee.

11%

0%

33%

0%

33%

33%

33%

56%

3%

10%

31%

15%

23%

31%

44%

51%

7%

14%

14%

14%

21%

32%

39%

50%

CFO

CIO

eCommerce/Direct Channels

Supply Chain Leader

Merchandising Leader

COO/Store Operations

CEO

Marketing Leader

Marketing Strategy Influencers "Needs More Influence" Winners Average Laggards

19

Technology Enablers

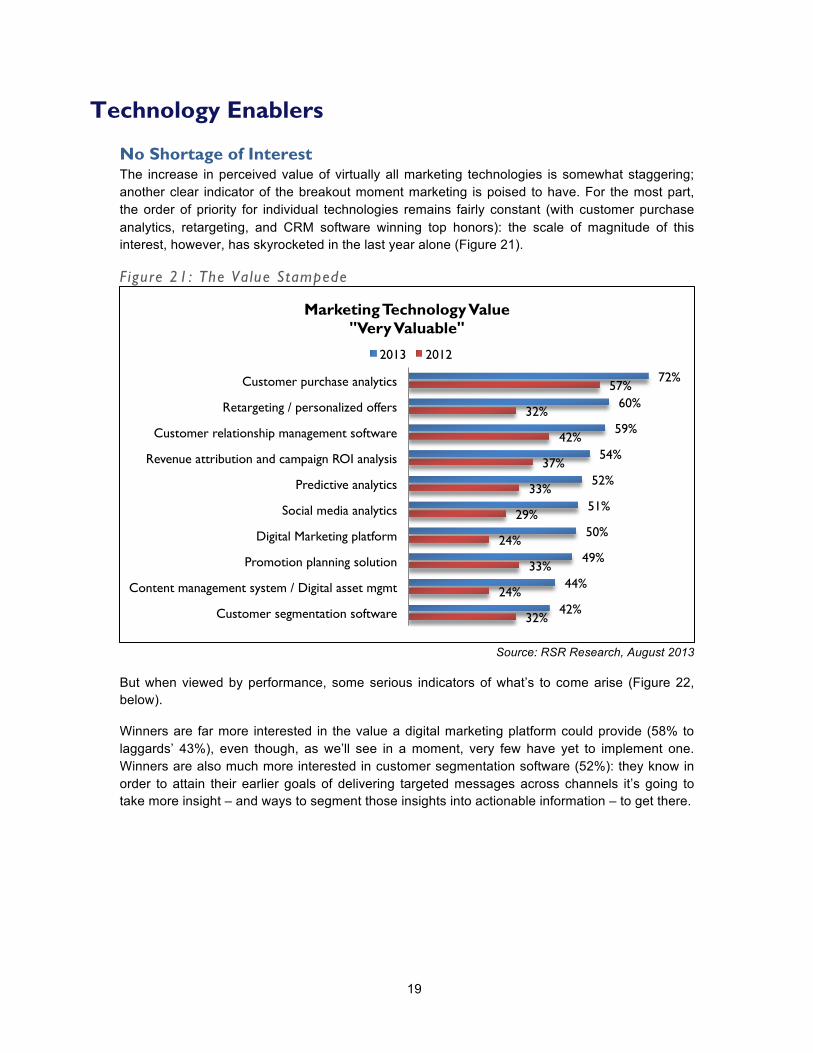

No Shortage of Interest The increase in perceived value of virtually all marketing technologies is somewhat staggering; another clear indicator of the breakout moment marketing is poised to have. For the most part, the order of priority for individual technologies remains fairly constant (with customer purchase analytics, retargeting, and CRM software winning top honors): the scale of magnitude of this interest, however, has skyrocketed in the last year alone (Figure 21).

Figure 21: The Value Stampede

Source: RSR Research, August 2013

But when viewed by performance, some serious indicators of what’s to come arise (Figure 22, below).

Winners are far more interested in the value a digital marketing platform could provide (58% to laggards’ 43%), even though, as we’ll see in a moment, very few have yet to implement one. Winners are also much more interested in customer segmentation software (52%): they know in order to attain their earlier goals of delivering targeted messages across channels it’s going to take more insight – and ways to segment those insights into actionable information – to get there.

32%

24%

33%

24%

29%

33%

37%

42%

32%

57%

42%

44%

49%

50%

51%

52%

54%

59%

60%

72%

Customer segmentation software

Content management system / Digital asset mgmt

Promotion planning solution

Digital Marketing platform

Social media analytics

Predictive analytics

Revenue attribution and campaign ROI analysis

Customer relationship management software

Retargeting / personalized offers

Customer purchase analytics

Marketing Technology Value "Very Valuable"

2013 2012

20

Figure 22: Winners Have a Different Value Emphasis

Source: RSR Research, August 2013

But laggards place an inordinately low value on these same customer segmentation tools (14%), begging the question, “How can one expect to deliver a targeted and personalized message to shoppers when you can’t even segment those shoppers on the most basic level?” It is a prime example of how laggards tend to prioritize the end goal (a more relevant and differentiated customer experience) over the required means to attain it.

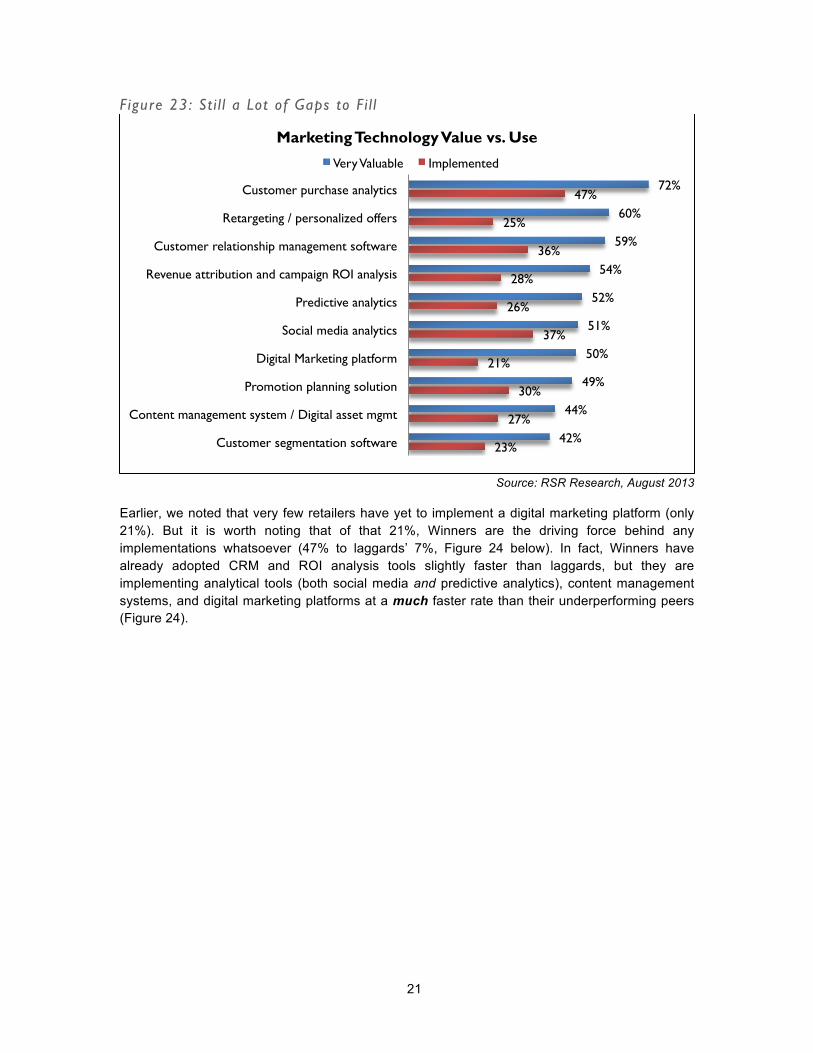

Great, But… As Figure 23 shows, retailers are still a long ways off from deriving the value from new marketing tools; the standard ratio of the gap from valued to implemented is roughly 2 to 1.

14%

43%

50%

57%

14%

64%

64%

43%

43%

71%

53%

53%

55%

49%

44%

52%

60%

46%

64%

70%

43%

45%

48%

50%

52%

52%

53%

58%

61%

74%

Content management system / Digital asset mgmt

Promotion planning solution

Predictive analytics

Social media analytics

Customer segmentation software

Revenue attribution and campaign ROI analysis

Customer relationship management software

Digital Marketing platform

Retargeting / personalized offers

Customer purchase analytics

Marketing Technology Value "Very Valuable"

Winners Average Laggards

21

Figure 23: St i l l a Lot of Gaps to Fi l l

Source: RSR Research, August 2013

Earlier, we noted that very few retailers have yet to implement a digital marketing platform (only 21%). But it is worth noting that of that 21%, Winners are the driving force behind any implementations whatsoever (47% to laggards’ 7%, Figure 24 below). In fact, Winners have already adopted CRM and ROI analysis tools slightly faster than laggards, but they are implementing analytical tools (both social media and predictive analytics), content management systems, and digital marketing platforms at a much faster rate than their underperforming peers (Figure 24).

23%

27%

30%

21%

37%

26%

28%

36%

25%

47%

42%

44%

49%

50%

51%

52%

54%

59%

60%

72%

Customer segmentation software

Content management system / Digital asset mgmt

Promotion planning solution

Digital Marketing platform

Social media analytics

Predictive analytics

Revenue attribution and campaign ROI analysis

Customer relationship management software

Retargeting / personalized offers

Customer purchase analytics

Marketing Technology Value vs. Use Very Valuable Implemented

22

Figure 24: Uneven Adoption

Source: RSR Research, August 2013

What is problematic, however, is that for all retailers, the list of planned projects that have yet to be backed with real money is still quite long (Figure 25).

Figure 25: Big Appetites, Smal l P lates

Source: RSR Research, August 2013

7%

21%

57%

21%

7%

14%

29%

7%

50%

29%

26%

26%

19%

26%

26%

26%

36%

10%

47%

34%

26%

30%

32%

32%

32%

33%

39%

42%

45%

45%

Customer segmentation software

Content management system / Digital asset mgmt

Promotion planning solution

Revenue attribution and campaign ROI analysis

Retargeting / personalized offers

Predictive analytics

Customer relationship management software

Digital Marketing platform

Customer purchase analytics

Social media analytics

Marketing Technology Use "Implemented More Than 1 Year"

Winners Average Laggards

11%

17%

18%

19%

20%

21%

22%

23%

24%

29%

11%

16%

11%

10%

20%

13%

18%

15%

13%

9%

Customer purchase analytics

Content management system / Digital asset mgmt

Promotion planning solution

Social media analytics

Retargeting / personalized offers

Predictive analytics

Customer segmentation software

Revenue attribution and campaign ROI analysis

Customer relationship management software

Digital Marketing platform

Marketing Technology Plans

Budgeted Project Planned, Not Yet Budgeted

23

What all of this data tells us is that when it comes to the next generation of technologies designed to take retailers from old-world marketing into the digital age, technologists won’t have a very hard time leading them to water – it’s the getting them to drink part that will be the challenge. Per usual, Winners already have a jump start on their competitors, putting higher priority on more useful technologies, making sure their internal marketing departments have the required ability to take on new systems, and in small part, they’re already starting to roll those technologies out. What will be interesting to see next year is this: If retailers’ perception of the economic outlook finally has turned a corner, will the loosening of budgets serendipitously line up – timing wise – with the other half of the equation: the unavoidable easing of internal challenges (consolidation, culture, and old-world marketing processes) that must occur in order to facilitate real progress?

If that answer is indeed yes, we may be looking at a brand new, digitally-enabled world of marketing sooner than we anticipated.

24

BOOTstrap Recommendations

The retail marketing organization is at the center of a lot of internal and external challenges all at the same time. The good news is, retailers are aware of the challenges, and they know that something needs to be done. But as they embark on transforming their marketing organizations, the pitfalls, as ever, are more cultural and change-related than technological. Our advice? Take it top-down, one step at a time:

Returning to Growth Means Changing the Strategy Even retailers who typically are focused on growth (a.k.a., Retail Winners) had to take a breather during the economic downturn. Especially during the darkest depths, everyone was focused on preserving the customers they already had, not on acquiring new ones.

Times have changed, according to our survey respondents, and growth is back on the menu. But that means that everything else must change as a result, and it all has to start at the top, with the retailer's marketing strategy. A focus on growth means re-evaluating the brand value proposition and making sure that it's aligned with the overall objective. An easy example: for the last five years, the housing market has been miserable. DIY retailers responded with "make your home livable." Now that the housing market is coming back, DIY isn't about living in your existing house, it's about fixing it up to maximize your opportunity to sell it. A DIY retailer focused on growth needs to shift the message - and the tactics that spread that message - in order to stay aligned with what consumers need.

A growth strategy means shifting from an emphasis on retaining existing customers to a focus on acquiring new ones. And in this day and age, acquiring new customers may actually mean that you can't afford to take your eye off the target when it comes to keeping existing customers happy - because they can so easily share their dissatisfaction in social spheres and thereby chase new customers away.

When Strategy Changes, So Should Tactics The environment where retailers are going to execute this shift in strategy has changed too - the same tools that were effective in acquiring new customers twenty years ago are not going to be as effective today, because there are a whole slew of new tools waiting to be leveraged. The good news is that no one else really knows how to leverage them any better than anyone else, certainly not in a holistic sense.

The bad news is, no ROI exists for a lot of these new tools, or when retailers talk about benefits, it's still not certain whether those benefits are unique to that retailer or repeatable across brands. For laggards, this is particularly problematic because they are the least likely among our survey respondents to have an innovation program that helps them experiment with new channels and marketing tools.

The bottom line is this: You won't know which tools work best for you if you don't try them. You can't win if you don't play. And if you wait for someone else to figure out what works and what doesn't, you'll have missed the boat.

Consolidation Means "Bring Together" On the organizational side, this year's benchmark presents a cautionary tale. Does universal consensus exist that every marketing activity ought to be owned by the marketing department?

25

According to our survey respondents, that verdict is not yet in. The reality is that retailers need to manage a balancing act between a unified face to customers and marketing campaigns and tactics that take advantage of the unique elements of the communication channel being leveraged - Pinterest requires a different objective, content, and approach than Twitter, and trying to tell the exact same story through both channels won't resonate with consumers.

Unfortunately, it appears that some retailers (laggards in particular) have moved almost too quickly to consolidate their marketing teams. When traditional corporate marketing was constrained to begin with, consolidation without consideration for the team that is truly needed leads only to balls being dropped and opportunities missed. "Marketing consolidation" needs to be about expanding corporate marketing to absorb new capabilities that might have once lived on an eCommerce team. The retailers who yank channels away without bringing along the people who know how to use those channels are building a road to disaster.

Platforms Require Careful Evaluation Finally, retailers in this year's benchmark expressed a lot of frustration with existing IT departments and the need to "single solutions" like digital marketing platforms. However, there are two big horses already in that race: traditional CRM tools, and digital platforms. Which one should be the platform that carries forward a retailer's goal of one face to the customer, one view of the customer? The answer is, it's too early to tell. Each system knows something different about customers, and can enable different things based on what it knows.

For retailers trying to navigate this solution space, the implication is that they are not going to find everything they're looking for out of one box. And so they must be prepared to evaluate vendors not just on what they can do today, but where they're headed for the future. If a solution provider can't see beyond improvements to existing capabilities as part of their roadmap, they're not going to be a platform provider that is prepared to cross the bridge between traditional and digital marketing.

That bridge will need to be crossed - not today, and not tomorrow, but soon. The retailers who have struck partnership relationships with their solution providers will have an easier time navigating to that future than those with arms-length transactions.

a

Appendix A: RSR’s BOOT MethodologySM The BOOT MethodologySM is designed to reveal and prioritize the following:

• Business Challenges – Retailers of all shapes and sizes face significant external challenges. These issues provide a business context for the subject being discussed and drive decision-making across the enterprise.

• Opportunities – Every challenge brings with it a set of opportunities, or ways to change and overcome that challenge. The ways retailers turn business challenges into opportunities often define the difference between Winners and “also-rans.” Within the BOOT, we can also identify opportunities missed – and describe leading edge models we believe drive success.

• Organizational Inhibitors – Even as enterprises find opportunities to overcome their external challenges, they August find internal organizational inhibitors that keep them from executing on their vision. Opportunities can be found to overcome these inhibitors as well. Winning Retailers understand their organizational inhibitors and find creative, effective ways to overcome them.

• Technology Enablers – If a company can overcome its organizational inhibitors it can use technology as an enabler to take advantage of the opportunities it identifies. Retail Winners are most adept at judiciously and effectively using these enablers, often far earlier than their peers.

A graphical depiction of the BOOT MethodologySM follows:

b

Appendix B: About Our Sponsors

Revionics delivers the industry’s most powerful End-to-End Merchandise Optimization solution, enabling retailers of all sizes to execute a fact-based omni-channel merchandising strategy utilizing the most comprehensive set of shopper demand signals to enhance financial performance with improved customer satisfaction. Revionics’ solutions leverage advanced predictive analytics and demand-based science to ensure retailers have the right product, price, promotion, placement and space allocation for optimal results across all touch points in the omni-channel shopping episode – online, in-store, social and mobile. Revionics has been recognized as a 2012 Deloitte Technology Fast 500™ company and has more retail locations under optimization management than any other vendor. Visit us at www.revionics.com.

Teradata products and services provide retailers with the ability to analyze, predict and act quickly on big decisions related to market conditions or a variety of little decisions, the kind sales associates encounter with customers daily. Built on the powerful foundation of a Teradata Database, Teradata provides insight into:

1. Supply and demand patterns so that you can quickly respond to out of stock or overstock situations

2. Customer segments so that you can better understand who they are and which ones are valuable to your business

3. Promotions and offers so that you can optimize for higher redemption and response 4. Assortments so that the you can localize for different markets and customer segments 5. Key cost drivers in your operation, so that you can operate more efficiently

For more information, please visit http://www.teradata.com/industry-expertise/retail/

c

Appendix C: About RSR Research

Retail Systems Research (“RSR”) is the only research company run by retailers for the retail industry. RSR provides insight into business and technology challenges facing the extended retail industry, providing thought leadership and advice on navigating these challenges for specific companies and the industry at large. We do this by:

• Identifying information that helps retailers and their trading partners to build more efficient and profitable businesses;

• Identifying industry issues that solutions providers must address to be relevant in the extended retail industry;

• Providing insight and analysis about a broad spectrum of issues and trends in the Extended Retail Industry.

Copyright© 2013 by Retail Systems Research LLC • All rights reserved.

No part of the contents of this document August be reproduced or transmitted in any form or by any means without the permission of the publisher. Contact [email protected] for more information.A