Understanding Europe- A Cultural Mosaic. West-Central Europe.

Upload

thomas-edwardsCategory

view

214download

0

Results of CFO Survey in Central EuropeThe only way is up

Gavin Hill Partner, Central Europe

© 2013 Deloitte Central Europe2 Central European CFO Survey

Deloitte Q1 2013 CE CFO Survey

4th CE CFO survey

8+ IndustriesFinancial services, TMT, Transport, Real Estate, Pharmaceutical, Manufacturing, Energy, Consumer Business and other industries participated

14 geographies

668 CFOs respondedKosovo

© 2013 Deloitte Central Europe3 Central European CFO Survey

Key findings from the Q1 2013 CE CFO surveyCut, minimise, grow

• Are less cautious than 6 months ago

• Remain cautious about gearing

• Focus on revenue growth on current & new markets, followed by cost cutting and improvement of liquidity

• Are quite risk averse

• Do not expect talent shortage in finance

• Forecast that financing costs will increase

CFOs in Central Europe

• CFOs feel the same way or somewhat more optimistic regarding financial prospect for their companies than they did 6 months ago.

• This mild decrease of pessimism is consistent with the results of the recent Deloitte survey of Private Equity executives.

• There is a significant north/south split in the sentiment of CFOs (south being more negative and north positive in most questions).

© 2013 Deloitte Central Europe4 Central European CFO Survey

CFO survey results CE x UKGreater risk averseness and cautiousness in Central Europe

Compared to the results of CFO Survey in the United Kingdom, Central European CFOs are more risk averse and are not expecting significant improvements, unlike their UK based counterparts.

The availability of Credit

is highest in 5 years in UK

On average, credit is normally available for majority of CFOs in CE, the exception is southern part of the region

Around 40% of the UK CFOs claim that now is a good time to be taking risk onto their balance sheets.

Only around 20% of CE CFOs claim that now is a good time to be taking risk

Risk

Credit

Uncertainty

Around 20% of CFOs in UK evaluate external economic uncertainty as normal

Even though majority of CFOs claim that external economic uncertainty levels are above normal or high, 21% of CFOs see the conditions as normal

Detailed Results

© 2013 Deloitte Central Europe6 Central European CFO Survey

Financial prospects for companiesMild return of optimism

Slovenia Slovakia Poland Croatia Bulgaria Serbia Romania Hungary Albania Estonia Lithuania Czech Republic

Latvia0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

30% 30%21% 18% 17% 16% 15% 14% 12% 10% 10% 8% 6%

43%36%

35% 40% 43%

32%

45%55%

39%51%

39%

58%

39%

27%

27%43%

26%

34%

50%

40%26%

42%

38%

52%

33%

32%

7%2%

16%

6% 3% 5% 7% 2%

24%

Financial prospects for companies, compared to 6 months ago

Very Optimistic

Somewhat Optimistic

Unchanged

Less Optimistic

Majority of CFOs feel the same way about the financial prospects for their companies, as they did 6 months ago. However significant part of CFOs also feels somewhat optimistic. Especially CFOs in Baltic countries and Serbia.

© 2013 Deloitte Central EuropeCentral European CFO Survey

GDP growth predictionsExpectation of stagnation

7

Real GDP growth, forecast 2013 (%)

2,4

-1,3

Source: Eurostat & IMF

Slovenia Croatia Hungary Czech Republic

Albania Slovakia Serbia Romania Poland Bulgaria Estonia Lithuania Latvia0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

70%

42% 40%

28%

13% 11% 10% 10%5% 3%

30%

58% 58%

66%

52%66% 72% 70%

43%

85%

7% 10% 11%

2%7%

33%18%

18% 20%

52%

12%

77%

84% 76%

2% 5%

16%7%

12%

CFOs GDP growth expectations for 2013

Growth (>3%)

Moderate Growth (1,5-3%)

Stagnation (0 - 1,5%)

Recession

1,4-0,4 -0,1 2,00,0 1,21,1-2,0 1,6 3,0 3,1 3.81,8

Again, the north/south split is clearly visible. Majority of CFOs expect growth between 0-1,5%. The only positive exception are CFOs from Baltic states and Poland, where CFOs expect moderate growth for the year ahead.

© 2013 Deloitte Central Europe8 Central European CFO Survey

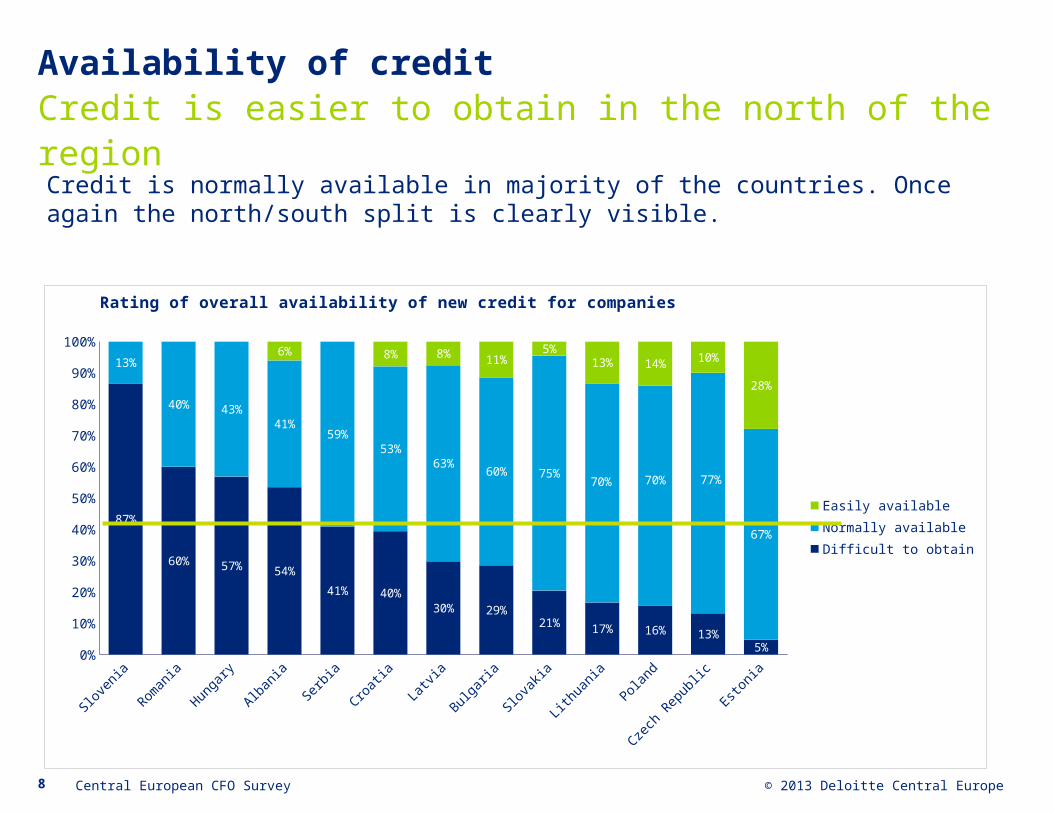

Availability of creditCredit is easier to obtain in the north of the region

Slovenia Romania Hungary Albania Serbia Croatia Latvia Bulgaria Slovakia Lithuania Poland Czech Republic

Estonia0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

87%

60% 57% 54%

41% 40%

30% 29%21%

17% 16% 13%5%

13%

40% 43%

41%59%

53%

63%60% 75%

70% 70% 77%

67%

6% 8% 8%11%

5%

13% 14%10%

28%

Rating of overall availability of new credit for companies

Easily available

Normally available

Difficult to obtain

Credit is normally available in majority of the countries. Once again the north/south split is clearly visible.

© 2013 Deloitte Central Europe9 Central European CFO Survey

Willingness to take riskStaying on the safe side

Slovenia Bulgaria Serbia Slovakia Croatia Albania Romania Hungary Lithuania Latvia Poland Czech Republic

Estonia0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

100%91% 90%

82% 82% 81% 80%73% 72% 71% 69% 67% 64%

9% 10%18% 18% 20% 20%

27% 28% 29% 31% 33% 36%

Is now a good time to be taking greater risk onto company’s balance sheets?

Yes

No

The entire region shares the opinion that now is still not a good time to take risk. Slovenia remains most risk averse from the region with all CFOs surveyed feeling, that now is not a good time to take more risk onto companies’ balance sheets.

© 2013 Deloitte Central Europe10 Central European CFO Survey

Levels of uncertaintyTime to accept the new normal?

• CFOs in CE feel that the levels of external financial uncertainty are above normal / high in most of the countries.

• Only Slovak and Estonian CFOs evaluate the external conditions as normal.

• The question is, whether the

uncertainty will ever decrease or it is time to accept the current state as the new normal.

Normal

Above normal

High

Very high

Rating of general level of external financialand economic uncertainty

“Deloitte” is the brand under which tens of thousands of dedicated professionals in independent firms throughout the world collaborate to provide audit, consulting, financial advisory, risk management, and tax services to selected clients. These firms are members of Deloitte Touche Tohmatsu Limited (DTTL), a UK private company limited by guarantee. Each member firm provides services in a particular geographic area and is subject to the laws and professional regulations of the particular country or countries in which it operates. DTTL does not itself provide services to clients. DTTL and DTTL member firm are separate and distinct legal entities, which cannot obligate the other entities. DTTL and each DTTL member firm are only liable for their own acts or omissions, and not those of each other. Each of the member firms operates under the names "Deloitte," "Deloitte & Touche," "Deloitte Touche Tohmatsu," or other related names. Each DTTL member firm is structured differently in accordance with national laws, regulations, customary practice, and other factors, and may secure the provision of professional services in their territories through subsidiaries, affiliates, and/or other entities. Deloitte Central Europe is a regional organization of entities organized under the umbrella of Deloitte Central Europe Holdings Limited, the member firm in Central Europe of Deloitte Touche Tohmatsu Limited. Services are provided by the subsidiaries and affiliates of Deloitte Central Europe Holdings Limited, which are separate and independent legal entities. The subsidiaries and affiliates of Deloitte Central Europe Holdings Limited are among the region’s leading professional services firms, providing services through more than 3,800 people in 41 offices in 17 countries.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and deep local expertise to help clients succeed wherever they operate. Deloitte's approximately 200,000 professionals are committed to becoming the standard of excellence.

© 2013 Deloitte Central Europe