Resetting the regional economic development strategy David Powell, CEO of PTP.

61

Resetting the regional economic development strategy David Powell, CEO of PTP

-

Upload

rudolf-page -

Category

Documents

-

view

214 -

download

0

Transcript of Resetting the regional economic development strategy David Powell, CEO of PTP.

Resetting the regional economic development

strategyDavid Powell, CEO of PTP

How is the economy?

National- Terrible (D & F)

Local- Pretty Good (C)

Business- Even Better (B-C)

U.S. Chamber Small Business Survey

84%

8%8%

54%

27%19%

14%

25%

61%

Headed in Right DirectionOff on Wrong DirectionNot Sure

U.S. Economy

Local Economy

Your Business

Source: U.S. Chamber Small Business Survey, July 2011

Another year of muddling through? Global Weakness

Threatens to undermine US exports Wide variations from continent to continent Europe likely in a recession; China’s growth is slowing

Foreclosure Problem Housing will continue to languish Foreclosures will hold down prices, sales & new construction

Lackluster Job Market Jobs will be added but at a rate too slow to make a dent Only marginal improvement in personal income expected Problem for consumers (especially in gas prices continue to rise!)

Government Belt-Tightening Budget cutting will keep subtracting from growth Congress’s acrimony & propensity for last minute deals will continue

to weigh on business & consumer confidence

4

Are we experiencing a reset?

Unprecedented lack of confidence in Washington

Deloitte survey found >80% of business executives indicated “uncertainty” and “over-regulation” as material reasons for not adding jobs in the U.S.

United States in the Global Economy

Impact of the “Great Recession”Difference in Real GDP/Person 2007-2012

-5% -3% -3% -1%

4%10%

14%

34%

51%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

UnitedKingdom

UnitedStates

France Japan Germany Russia Brazil India China

Source: The Economist, The World in 2012

GDP Growth 2011

1.7%

-0.6%

9.2%

2.3%1.4% 1.8%

7.6%

3.0%4.0%

-5%

-3%

-1%

1%

3%

5%

7%

9%

US Japan China Canada Euro Area Austrialia India Brazil Russia

Source: Economist Jan 21, 2011

USA Growth in 2012 Projected-

1.1% to 2.0%

Budget Balance as % of GDP 2011

-8.7% -8.3%

-1.8%

-4.0% -4.1%-2.6%

-5.4%

-2.7%-0.8%

-15%

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

US Japan China Canada Euro Area Austrialia India Brazil Russia

Source: Economist Jan 21, 2011

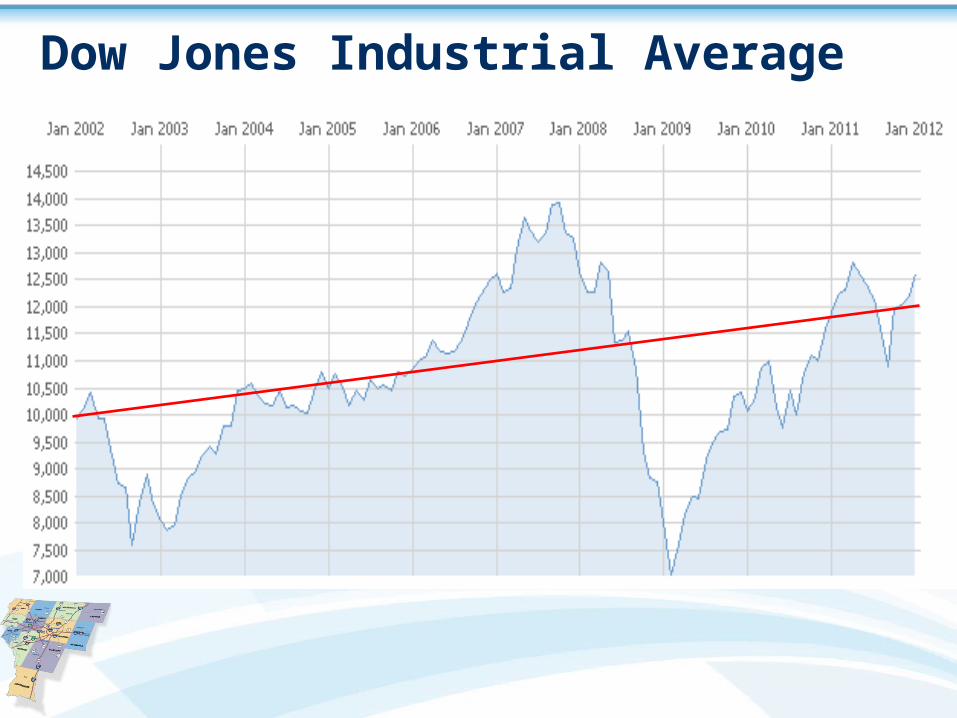

Dow Jones Industrial Average

USA Total Nonfarm Payroll

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1961 1064 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

Source: BLS, Jan 2012

In thousands

Employment Monthly Net Change Jan 2000- 2011

-800

-600

-400

-200

0

200

400

600

2000 2006 2011

Jobs

Source: BLS Jan 2012

125,000 Jobs/Mo. To keep pace with population growth in the USIn thousands

The best year in the last decade averaged

208,000 additional jobs per month…12 years

Unemployment SummaryDecember 2011

13.8%

8.7%7.7%

4.1%

0%

2%

4%

6%

8%

10%

12%

14%

Less thanHS

HS Grad SomeCollege

BA Plus

National unemployment rate in December, 8.5%, down from 9.4% in December 2010

For Men over 20, 8.0%, down from 9.4%

For Women over 20, 7.9%, down from 8.1%

For 16-19 year olds, 23.1%, down from 25.2%

For Whites (7.5%), Blacks (15.8%), Hispanics (11.0%)

Source: BLS Jan 2012

Unemployment Rate By Education

Population Growth

Last decade US population grew at the lowest rate

since the great depression

Population Growth

Southern States 5-Year Employment Changes

-114,000-21,200

-762,300

-307,000

-45,900

57,000

-59,800-134,800

-43,000

-222,500

23,000

-85,100-127,200

451,100

-83,700-3,600

-900,000

-700,000

-500,000

-300,000

-100,000

100,000

300,000

500,000

AL AR FL GA KY LA MD MO MS NC OK SC TN TX VA WV

Source: U.S. BLS, Dec, Measured Nov 2006- Nov 2011

Total -1,478,000 lost jobs

Southern States 5-Year Employment Changes

-5.7%

-1.8%

-9.5%

-7.5%

-2.5%

3.0%

-2.3%

-4.9%-3.8%

-5.4%

1.5%

-4.4%-4.6%

4.4%

-2.2%-0.5%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

AL AR FL GA KY LA MD MO MS NC OK SC TN TX VA WV

Source: U.S. BLS, Dec, Measured Nov 2006- Nov 2011

Southern States 1-Year Employment Changes

0.2%0.6%

1.4%

-0.5%

1.2%

2.6%

0.7%

0.1%

1.0%

0.4%

2.8%

1.8%

1.2%

2.2%

0.5%

0.8%

-2%

-1%

0%

1%

2%

3%

AL AR FL GA KY LA MD MO MS NC OK SC TN TX VA WV

Source: U.S. BLS, Dec, Measured Nov 2010- Nov 2011

Southern States 1-Year Employment Changes

3,000 7,400

98,100

-20,300

20,600

46,700

18,3001,400

10,500 19,600

43,00032,700 32,400

226,000

16,900 6,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

AL AR FL GA KY LA MD MO MS NC OK SC TN TX VA WV

Source: U.S. BLS, Dec, Measured Nov 2006- Nov 2011

Total +562,300 gained jobs

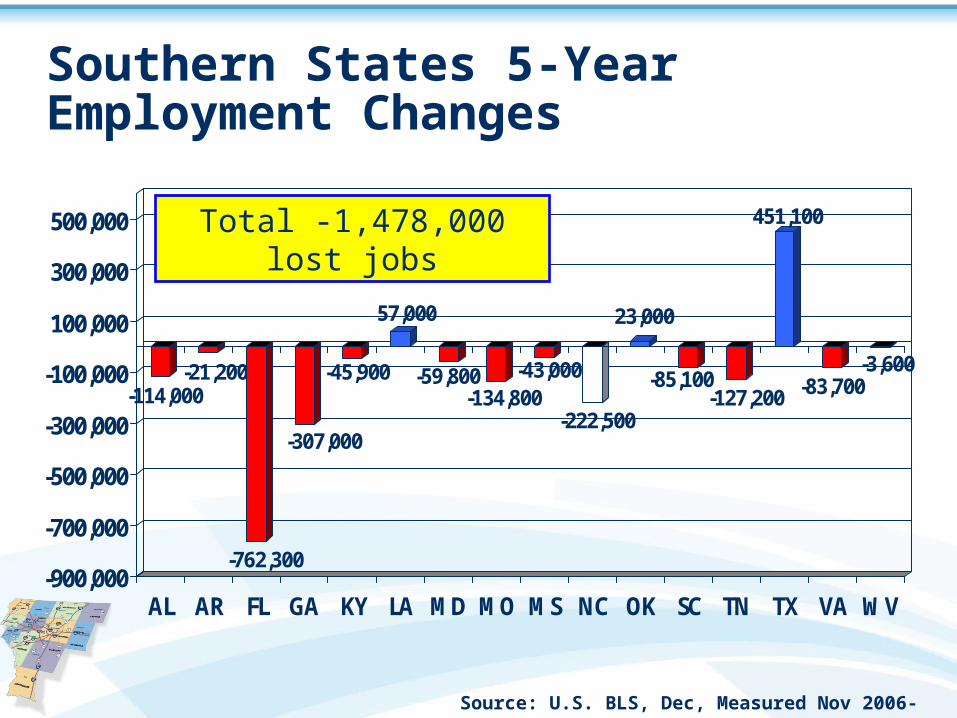

Reset of the Regional Economy90K job loss in Piedmont Triad from 2000 to 2010

22

Employment Change by NC Partnership Region

Advantage West

Charlotte Region

Eastern Region

Northest Region

Southeast Region

Piedmont Triad

Research Triangle

North Carolina

-90,000 -60,000 -30,000 0 30,000 60,000

∆ 10 yr∆ 5 yr∆ 1 yr

Percentage Unemployment By Year By County1990- November 2011

0%

2%

4%

6%

8%

10%

12%

14%

Alamance Forsyth Guilford Davidson Randolph

Source: NCESC

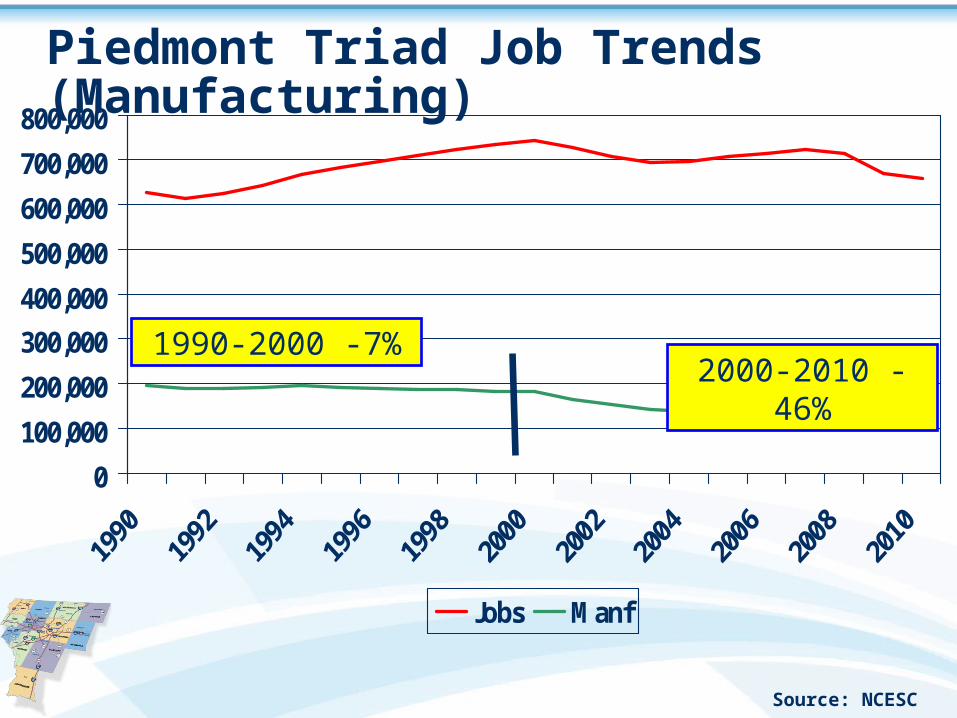

Piedmont Triad Job Trends (Manufacturing)

0

100,000

200,000

300,000400,000

500,000

600,000

700,000

800,000

Jobs Manf

1990-2000 -7%2000-2010 -46%

Source: NCESC

Piedmont Triad Manufacturing Job Shifts 1990-2010

-38,222

-19,625 -19,084

-3,550 -2,737

431 1,651 207

-50,000

-40,000

-30,000

-20,000

-10,000

0

10,000

Textiles

Apparel

Furniture

Comp/Elect

Elec/Appl

Food

Plast/Rub

Transport

Source: NCESC

North Carolina Metro Job Growth Nov 2010 to Nov 2011

0.2% 0.2%

-0.2%

0.5%

2.4%

0.2%

2.1%

0.7%

-1.5% -1.3%

1.9%

-1.0%-1.5%

2.7%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

Ashville

Burlington

Charlotte

Durham

Fayettenille

Goldsboro

Greensboro

Greenville

Hickory

Jacksonville

Raleigh

Rocky Mount

Wilm

ington

Winston Salem

Source: Garner Economics LLC Jan 2012

% Employment Growth Last 12 MonthsNov 2010-Nov 2011

1.1%

0.4%

1.1%

0.3%

0.9%

2.2%

1.5%

0%

1%

1%

2%

2%

3%

Advantage West Charlotte Eastern Northeast Southeast Piedmont Triad ResearchTriangle

Every PTP County More People Employed in Nov

2011 than in 2010

Source: NCESC

Annual Population Growth

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011

USA NC

Source: Brookings Jan 20, 2012

Annual Population % Change Rates2001-2010

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Greensboro Winston-Salem National

Source: U.S. Bureau Intercensal Population Estimates, SYNEVA Economics, Nov 2011

Solutions

Four Interconnected Processes

EconomicDevelopment

Market Readiness

Organizational Context

Workforce Pipeline

Business Environment

Factors

• Reciprocating System

• Non-Economic Factors

Resetting the Piedmont Triad Partnership

Key Issues

Economic Development

Market Readiness

Organizational Context

Workforce Pipeline

Business Environme

nt

• CEO Engagement

• Urban Collaboration

• The “PTP Region”

Collaborative Regional Model

High Point Partners

Winston Salem Alliance

PiedmontTriad Partnership

GreensboroPartnership

Shared StrategyLeveraged Resources

Joint Fundraising

Piedmont Triad Region(as determined by the State of NC)

Piedmont TriadEconomic Developer’sCouncil (PTEDC)

Manages marketing, working with our 13 local economic development organizations

MARKETING LEADERSHIP

Piedmont Triad Partnership

Promotes the region and its assets through marketing and outreach to potential relocation candidates

CEO leadership group made up of top regional business investors

Contributes expertise, funding and influence to catalytic projects in key sectors of opportunity

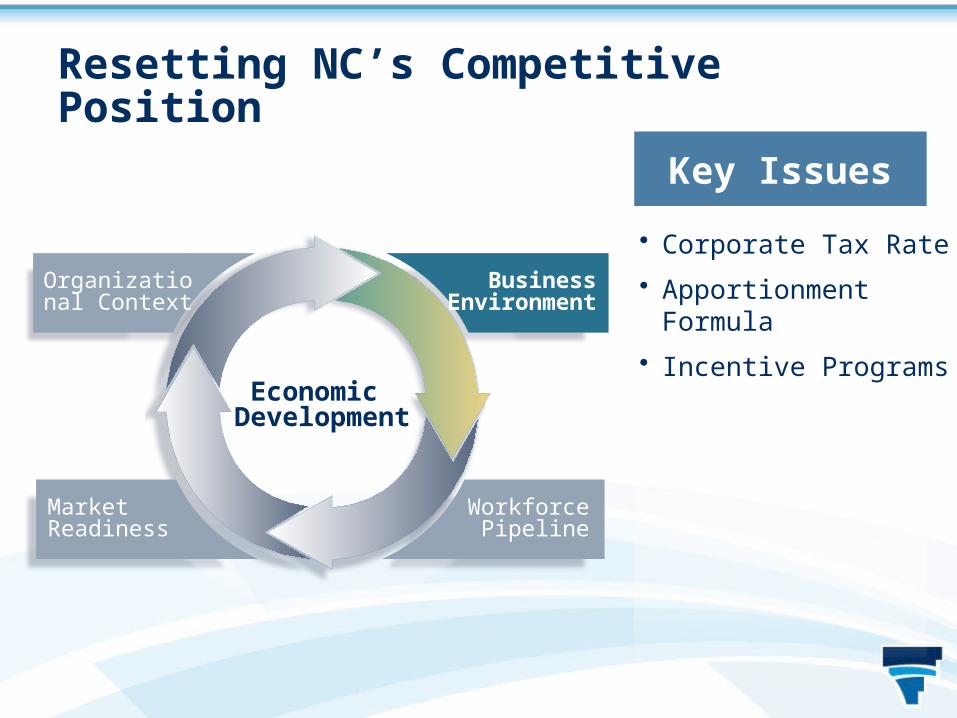

Resetting NC’s Competitive Position

Key Issues

Economic Development

Market Readiness

Organizational Context

Workforce Pipeline

Business Environme

nt

• Corporate Tax Rate

• Apportionment Formula

• Incentive Programs

Tax and incentive reforms are necessary to effectively compete

Most Southeastern states (including SC, GA & VA) have: Lower tax rates Much more favorable tax apportionment formulas Sizeable incentive programs not requiring special legislation

For large exporters, NC’s corporate income tax is many times greater than the income tax than competitor states.

In 2011 the Tax Foundation ranked North Carolina among the 10 states with the worst business tax climate. Virginia ranked 12th

South Carolina ranked 24th

37

U.S. Exports 2000-2011

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

2000Feb

2000Sep

2001Apr

2001Nov

2002Jun

2003Jan

2003Aug

2004Mar

2004Oct

2005May

2005Dec

2006Jul

2007Feb

2007Sep

2008Apr

2008Nov

2009Jun

2010Jan

2010Aug

2011Mar

2011Oct

42% Increase since 2009

Source: BEA Jan 2012

NC Exports as a % of GMP- 2010

5.7% 5.6%4.6%

7.5%

1.5%2.6%

12.0%

8.1%

10.7%

3.4%

13.5%

8.1% 7.5%

0%

2%

4%

6%

8%

10%

12%

14%

Ashville

Burlington

Charlotte

Durham

Fayetteville

Goldsboro

Greensboro

Greenville

Hickory

Raleigh

Rocky Mount

Wilm

ington

Winston Salem

Source: US Metro Economies. HIS Insight, Jan 2012

PTP 2005 to 2010

Greensboro/HP- 10.5% to 12.0%

Winston-Salem- 5.9% to 7.5%

Burlington- 2.5% to 5.6%

Competitor states have discretionary programs for large scale economic development projects

Adding to their advantage, our competitor states have established discretionary grant programs allowing them to make large upfront cash grants. Based on the project’s projected rate of return Without the necessity and delay of special legislation

NC has in place a mechanism for making such grants, the Site Infrastructure Development Fund (SIDF). Legislature has not appropriated any funds since it was

created to induce Merck to locate a vaccine facility in Durham County in 2003.

40

More competitive recruitment program needed for large scale economic development projects

To eliminate the disadvantages inherent in NC’s current business recruitment tools:

1. Offer upfront cash grants where individual grant decisions are made without the necessity of special legislation

2. Reduce the corporate income tax rate to the median rate in the Southeast region

3. Adopt a single sales factor corporate income tax apportionment formula

Remember: Our closest competitors have done all of these things and continue to offer tax credits and other incentives for attracting jobs and investment.

41

Resetting the Triad’s Educational Priorities

Key Issues

Economic Development

Market Readiness

Organizational Context

Workforce Pipeline

Business Environme

nt

• Skills Gap

• STEM Pipeline

• Aviation Workforce

Critical workforce pipeline expected to hamper the region’s growth

Estimated over 3,000 jobs currently cannot be filled in the region due to a skills gap Average salary is >$50,000 Annual economic impact is >$5 billion

These jobs require highly skilled technicians or/and professionals 20% = 4+ year degree 70% = Associate or technical degree 10% (and declining) = Certificate

43

Educational Attainment-% BA plus

24%

26%32%

23%

27%24% 24%

30%27%

41%

31%

0%

10%

20%

30%

40%

50%

Piedmont Triad

Birmingham

Charlotte

Greenville/Spartan

Jacksonville

Louisville

Mem

phis

Nashville

VA Beach

Raliegh/Durham

Richmond

Source: US Census, 2009, PTP Research

Goal: Unite education and training efforts for careers in logistics and distribution to prepare and maintain a superior workforce

Managed by Guilford Technical Community College in partnership with Davidson County Community College, Forsyth Technical Community College, and Randolph Community College.

(NCCGL)

45

TriSTEMScience, Technology, Engineering & Mathematics

Goal: Raise the number of graduates in the region (from <7,000 to >20,000) Connect existing STEM

programming, by distributing the ‘best practices’ of programs to all school systems

Involve private businesses in STEM education program input and execution

Direct grant and foundation funding

46

Specialized Training Centers for Advanced Manufacturing

Goal: Provide world class training to increase the availability of skilled workers to support a decision to expand or relocate Establish a collaboration between

private sector and region’s universities and community colleges

Devise an innovative mechanism to raise the competitive position by offering training to any employer or student in the state of NC

47

“ATEC Example” - Aviation Training and Education Center

Resetting the Triad’s Economic Drivers

Key Issues

Economic Development

Market Readiness

Organizational Context

Workforce Pipeline

Business Environme

nt

• New Industrial Base

• PTI Airport

• Industrial Product

Competitive Mega Sites

PACCARSeverCorr

Toyota

Dow Corning/ HemlockVolkswagen

AvailableOccupied

Mega Site: Location Requirements

Site must be large (between 1,000 to 3,300 acres) Site must be served by rail Site must be adjacent to interstate or 4-lane controlled

access highway Site must be in an attainment area Site must be available for immediate use Site must be eligible for expedited permitting Site must have reasonable access to commercial airport Labor must be available and capable of being trained

50

Mega Site: Location Requirements

Exceptional training facilities must be provided Site must be located in areas of low levels of unionization Site must be located in area with right-to-work laws Utilities must be provided within 18 months Site must be provide to end user at no cost Site must be located in a favorable tax environment

51

Four Interconnected Processes

EconomicDevelopment

Market Readiness

Organizational Context

Workforce Pipeline

Business Environment

Benchmarks

• Volkswagen (TN)

• Mercedes Benz (AL)

• Boeing 787 (SC)

Volkswagen Assembly Plant, Chattanooga, TN

Project Scope: Jobs: 2,000 direct Investment: $1.4 billion Incentives: $577.4 million ($289,000/job) Site: 1,350 acres

Announced in 2008; opened in May 2011 Most recent recruitment of an automotive assembly

plant Represents high water mark in incentive dollars offered

for an automotive assembly plant

53

Volkswagen Assembly Plant, Chattanooga, TNIncentive Package

$200 MM: Super jobs tax credits of $5,000 per job per year for up to 20 years.

$81 MM: Estimated value of 1,350 acres provided to VW at no cost.

$100 MM: Property tax abatements over a 10 year period.

$156.4 MM: Training costs, road, rail and utility improvements, low interest loans, grants and additional tax credits.

$40 MM: Specialized training facilities and programs Total: $577.4 million

54

VW Incentive Justification“Didn’t want to lose another one. . .”

Alabama also had a finalist site in the VW competition. Alabama offered $385MM in incentives – the largest

package Alabama had ever offered for an automotive plant.

Tennessee’s VW package was more than $190MM greater than Alabama’s offer.

On a cash flow basis: For each dollar spent on a one time basis, the state and

local governments will receive $1 in new tax revenues annually for 30 years

Results in a net cash benefit to Tennessee of $526.9 million and $557 million for the local governments

55

Mercedes Benz Assembly Plant, Vance, Alabama

Project Scope: Jobs: 1,500 Investment: $300 Million Incentive: $253 Million ($160,000/job) Site: 1,000 acres

In 1993, Alabama offered a then unheard of $253MM in incentives.

Mercedes’ initial investment was $300MM. Invested an additional $80 MM in 1998 Invested an additional $2 Billion in 2011 Created an additional 1,500 jobs since 1993

56

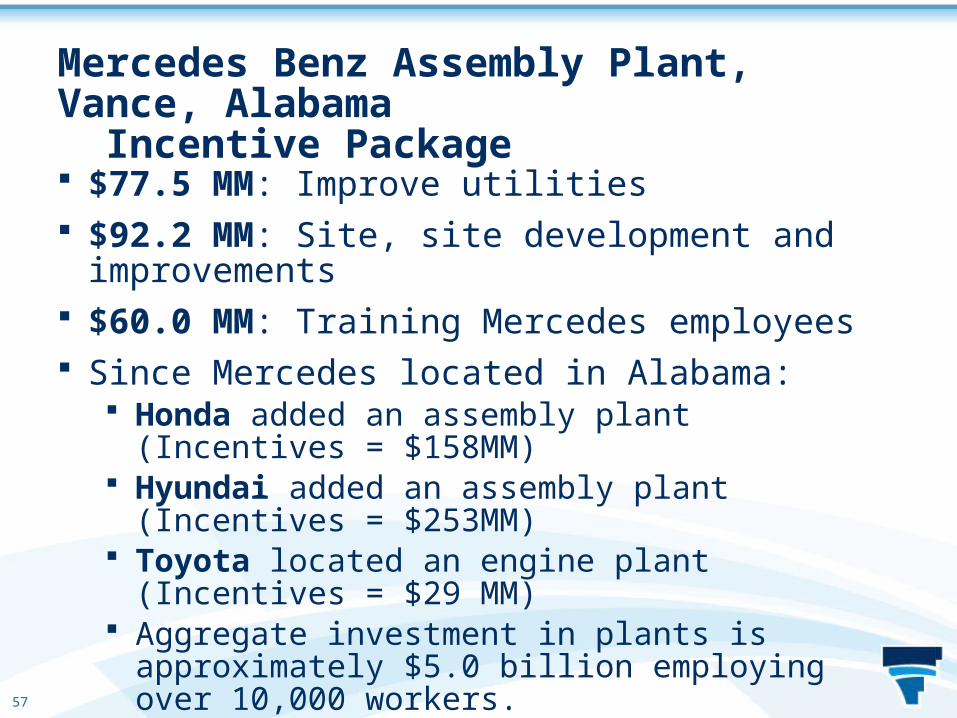

Mercedes Benz Assembly Plant, Vance, AlabamaIncentive Package

$77.5 MM: Improve utilities $92.2 MM: Site, site development and improvements $60.0 MM: Training Mercedes employees Since Mercedes located in Alabama:

Honda added an assembly plant (Incentives = $158MM) Hyundai added an assembly plant (Incentives = $253MM) Toyota located an engine plant (Incentives = $29 MM) Aggregate investment in plants is approximately $5.0

billion employing over 10,000 workers.

57

Boeing 787 Dreamliner Plant North Charleston, SC

SC officials have refused to quantify Estimated by the Charleston Post and Courier, to exceed

$900 million and quite likely exceed $1 billion. Boeing’s investment is variously reported to be between

$750 million and $1.025 billion. The plant is reported to involve the creation of 3,800

direct jobs and 5,971 additional indirect jobs.

58

$361.8MM: Principal and interest on General Obligation Economic Development Bonds

$306MM: Property tax abatements (Fee-In-Lieu) $150MM: Sales tax exemptions $33MM: Training Total: $850,839,350 Tax credits and other grants will easily increase the total

package to an amount in excess of $900 million

59

Boeing 787 Dreamliner Plant North Charleston, SCIncentive Package

Estimated Impacts from a mid-sized Automotive Assembly Plant

Impact Value

Employment 9,526

Labor Income $642,752,280

Value Added $1,274,430,596

Output $4,271,237,688

Total State & Local Taxes $101,708,714

Property Taxes $25,148,418

Sales Taxes $32,631,225

Income Taxes $18,442,011

Other Taxes $25,487,060

Source: UNC-G Bryan School of Business

In conclusion. . .

EconomicDevelopment

Market Readiness

Organizational Context

Workforce Pipeline

Business Environment

Priorities

• Catalytic Projects

• Tax & Incentive Reform

• Specialized Centers

• Industrial Product