ResearchAndForecast Jakarta Apartment 2Q2014

11

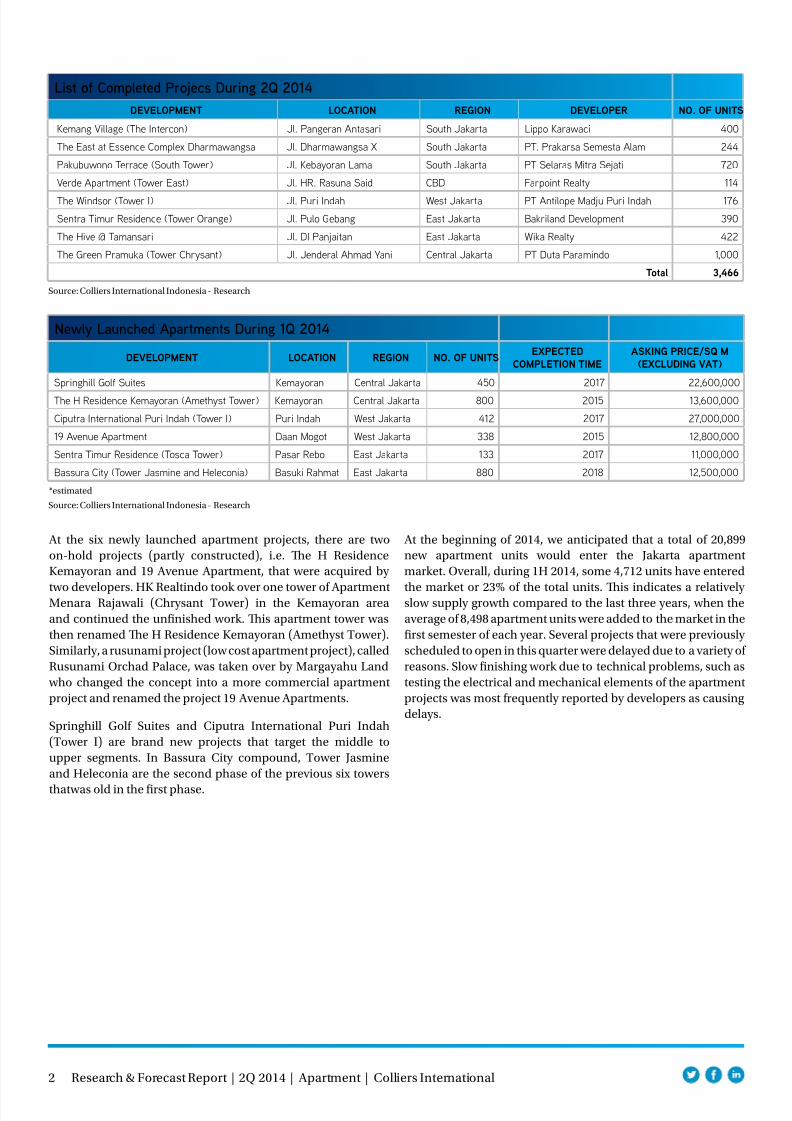

Apartment Sector Apartment for Strata Title Supply As of the end of June 2014, eight apartment projects with 3,466 new apartment units, have been handed over during 2Q 2014. Tis quarter’s additional supply is largely located in South Jakarta, both by number of apartment units and number of projects (1,364 units at three apartment projects). Other regions, like East Jakarta, introduced 812 new units at two apartment projects, while the CBD, West Jakarta and Central Jakarta contributed one project each, accounting for 37.2% of the total units. With the additional new units mentioned above, the total cumulative supply of strata-title apartments was 137,056 units, an increase of 2.6% over the previous quarter . wo upper-class projects, Kemang Village (Te Intercon) and Te East at Essence Darmawangsa, are located in the expatriate community area in South Jakarta, i.e. the Kemang and Darmawangsa areas. Te Intercon tower was the sixth tower at the Kemang Village project being handed over, while Te East tower at Essence Darmawangsa was the last tower being handed over after two previous towers, Eminence (in 2008) and Te South (in 2013), entered the market. Both Kemang Village and Essence Darmawangsa are planning to launch their second phases of development, which focus on residential projects, and will be located adjacent to the existing development. Another project, Pakubuwono errace (South ower) project, which is located on border of South Jakarta and angerang, continues to deliver the second tower which comprises 720 units and targets the middle-low segment. Sentra imur Residence with ower Orange and Te Hive amansari contributed as much as 10.3% of the total stock of apartments in East Jakarta during 2Q 2014. Perumnas (state-owned housing developer) collaborated with Bakrieland to develop Sentra imur Residence, which is located near the bus terminal in Pulo Gebang, in order to accommodate buyers of the low to middle-low segment. Te Hive amansari, which targeted the middle-upper segment is a mixed-use project, located in Cawang and comprised of condotel and apartment components. Locations like West Jakarta, Central Jakarta, and CBD only contributed one project each. Te operation of a brand new project in Puri Indah, Te Windsor (ower I), added an upper segment project to West Jakarta. Verde Apartments (ower East) and Te Green Pramuka (ower Chrysant) are both extensions of the existing projects located in Rasuna Said and Jl. A . Yani and target the upper and low segments, respectively. During this quarter, the Jakarta apartment market saw more additional supply from newly-launched projects. Tere are seven projects with a total potential stock of 2,133 units, 41% less than last quarter. Tis slowing figure indicates that developers tend to take a wait and see attitude, waiting for the results of the presidential election. Research & Forecast Report Jakarta | Apartment 2Q 2014 Accelerating success. “Tere were 3,466 new apartment units which became available during the quarter resulting in a total of 145,390 apartment units in DKI Jakarta. Te average asking price for strata-title apartments in Jakarta climbed by 16% YoY to IDR25.5 million psm. Prices in the CBD were recorded at IDR39.7 million psm, an increase of 17% YoY. ” - Ferry Salanto, Associate Director | Research

description

JLL

Transcript of ResearchAndForecast Jakarta Apartment 2Q2014

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 111

Apartment Sector

Apartment for Strata Title

Supply

As of the end of June 2014 eight apartment projects with 3466

new apartment units have been handed over during 2Q 2014

Tis quarterrsquos additional supply is largely located in South

Jakarta both by number of apartment units and number of

projects (1364 units at three apartment projects) Other regions

like East Jakarta introduced 812 new units at two apartment

projects while the CBD West Jakarta and Central Jakarta

contributed one project each accounting for 372 of the total

units With the additional new units mentioned above the total

cumulative supply of strata-title apartments was 137056 units

an increase of 26 over the previous quarter

wo upper-class projects Kemang Village (Te Intercon) and

Te East at Essence Darmawangsa are located in the expatriate

community area in South Jakarta ie the Kemang and

Darmawangsa areas Te Intercon tower was the sixth tower

at the Kemang Village project being handed over while Te

East tower at Essence Darmawangsa was the last tower being

handed over after two previous towers Eminence (in 2008) andTe South (in 2013) entered the market Both Kemang Village

and Essence Darmawangsa are planning to launch their second

phases of development which focus on residential projects and

will be located adjacent to the existing development Another

project Pakubuwono errace (South ower) project which is

located on border of South Jakarta and angerang continues todeliver the second tower which comprises 720 units and targets

the middle-low segment Sentra imur Residence with ower

Orange and Te Hive amansari contributed as much as 103

of the total stock of apartments in East Jakarta during 2Q 2014

Perumnas (state-owned housing developer) collaborated with

Bakrieland to develop Sentra imur Residence which is located

near the bus terminal in Pulo Gebang in order to accommodate

buyers of the low to middle-low segment Te Hive amansari

which targeted the middle-upper segment is a mixed-use

project located in Cawang and comprised of condotel and

apartment components

Locations like West Jakarta Central Jakarta and CBD onlycontributed one project each Te operation of a brand new

project in Puri Indah Te Windsor (ower I) added an upper

segment project to West Jakarta Verde Apartments (ower East)

and Te Green Pramuka (ower Chrysant) are both extensions

of the existing projects located in Rasuna Said and Jl A Yani and

target the upper and low segments respectively

During this quarter the Jakarta apartment market saw more

additional supply from newly-launched projects Tere are

seven projects with a total potential stock of 2133 units 41 less

than last quarter Tis slowing figure indicates that developers

tend to take a wait and see attitude waiting for the results of the

presidential election

Research ampForecast Report

Jakarta | Apartment2Q 2014

Accelerating success

ldquoTere were 3466 new apartment units which became available

during the quarter resulting in a total of 145390 apartment

units in DKI Jakarta Te average asking price for strata-titleapartments in Jakarta climbed by 16 YoY to IDR255 million

psm Prices in the CBD were recorded at IDR397 million psm

an increase of 17 YoYrdquo

- Ferry Salanto Associate Director | Research

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 211

2 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Source Colliers International Indonesia - Research

List of Completed Projecs During 2Q 2014

DEVELOPMENT LOCATION REGION DEVELOPER NO OF UNITS

Kemang Village (The Intercon) Jl Pangeran Antasari South Jakarta Lippo Karawaci 400

The East at Essence Complex Dharmawangsa Jl Dharmawangsa X South Jakarta PT Prakarsa Semesta Alam 244

Pakubuwono Terrace (South Tower) Jl Kebayoran Lama South Jakarta PT Selaras Mitra Sejati 720

Verde Apartment (Tower East) Jl HR Rasuna Said CBD Farpoint Realty 114

The Windsor (Tower I) Jl Puri Indah West Jakarta PT Antilope Madju Puri Indah 176

Sentra Timur Residence (Tower Orange) Jl Pulo Gebang East Jakarta Bakriland Development 390

The Hive Tamansari Jl DI Panjaitan East Jakarta Wika Realty 422

The Green Pramuka (Tower Chrysant) Jl Jenderal Ahmad Yani Central Jakarta PT Duta Paramindo 1000

Total 3466

Newly Launched Apartments During 1Q 2014

DEVELOPMENT LOCATION REGION NO OF UNITSEXPECTED

COMPLETION TIMEASKING PRICESQ M

(EXCLUDING VAT)

Springhill Golf Suites Kemayoran Central Jakarta 450 2017 22600000

The H Residence Kemayoran (Amethyst Tower) Kemayoran Central Jakarta 800 2015 13600000

Ciputra International Puri Indah (Tower I) Puri Indah West Jakarta 412 2017 27000000

19 Avenue Apartment Daan Mogot West Jakarta 338 2015 12800000

Sentra Timur Residence (Tosca Tower) Pasar Rebo East Jakarta 133 2017 11000000

Bassura City (Tower Jasmine and Heleconia) Basuki Rahmat East Jakarta 880 2018 12500000

Source Colliers International Indonesia - Research

estimated

At the six newly launched apartment projects there are two

on-hold projects (partly constructed) ie Te H Residence

Kemayoran and 19 Avenue Apartment that were acquired by

two developers HK Realtindo took over one tower of ApartmentMenara Rajawali (Chrysant ower) in the Kemayoran area

and continued the unfinished work Tis apartment tower was

then renamed Te H Residence Kemayoran (Amethyst ower)

Similarly a rusunami project (low cost apartment project) called

Rusunami Orchad Palace was taken over by Margayahu Land

who changed the concept into a more commercial apartment

project and renamed the project 19 Avenue Apartments

Springhill Golf Suites and Ciputra International Puri Indah

(ower I) are brand new projects that target the middle to

upper segments In Bassura City compound ower Jasmine

and Heleconia are the second phase of the previous six towers

thatwas old in the first phase

At the beginning of 2014 we anticipated that a total of 20899

new apartment units would enter the Jakarta apartment

market Overall during 1H 2014 some 4712 units have entered

the market or 23 of the total units Tis indicates a relativelyslow supply growth compared to the last three years when the

average of 8498 apartment units were added to the market in the

first semester of each year Several projects that were previously

scheduled to open in this quarter were delayed due to a variety of

reasons Slow finishing work due to technical problems such as

testing the electrical and mechanical elements of the apartment

projects was most frequently reported by developers as causing

delays

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 311

3 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

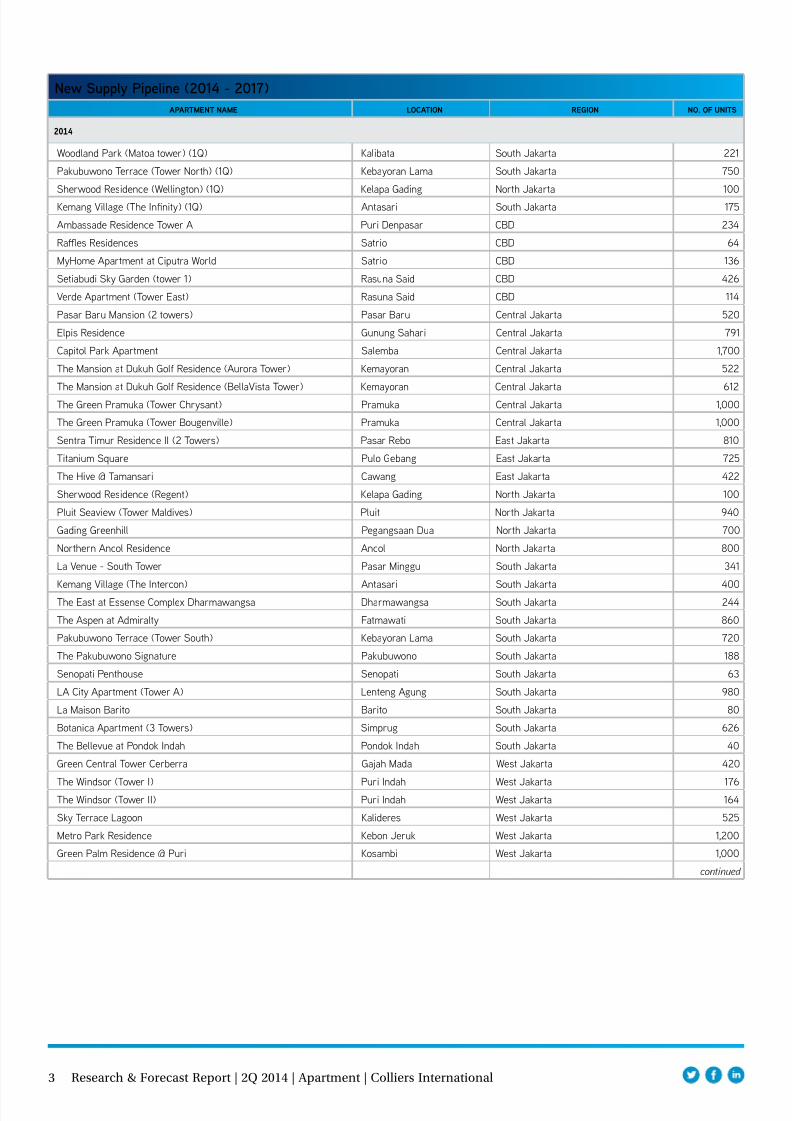

New Supply Pipeline (2014 - 2017)

APARTMENT NAME LOCATION REGION NO OF UNITS

983090983088983089983092

Woodland Park (Matoa tower) (983089Q) Kalibata South Jakarta 221

Pakubuwono Terrace (Tower North) (1Q) Kebayoran Lama South Jakarta 750

Sherwood Residence (Wellington) (1Q) Kelapa Gading North Jakarta 100

Kemang Village (The Infinity) (1Q) Antasari South Jakarta 175

Ambassade Residence Tower A Puri Denpasar CBD 234

Raffles Residences Satrio CBD 64

MyHome Apartment at Ciputra World Satrio CBD 136

Setiabudi Sky Garden (tower 1) Rasuna Said CBD 426

Verde Apartment (Tower East) Rasuna Said CBD 114

Pasar Baru Mansion (2 towers) Pasar Baru Central Jakarta 520

Elpis Residence Gunung Sahari Central Jakarta 791

Capitol Park Apartment Salemba Central Jakarta 1700

The Mansion at Dukuh Golf Residence (Aurora Tower) Kemayoran Central Jakarta 522

The Mansion at Dukuh Golf Residence (BellaVista Tower) Kemayoran Central Jakarta 612

The Green Pramuka (Tower Chrysant) Pramuka Central Jakarta 1000

The Green Pramuka (Tower Bougenville) Pramuka Central Jakarta 1000

Sentra Timur Residence II (2 Towers) Pasar Rebo East Jakarta 810

Titanium Square Pulo Gebang East Jakarta 725

The Hive Tamansari Cawang East Jakarta 422

Sherwood Residence (Regent) Kelapa Gading North Jakarta 100

Pluit Seaview (Tower Maldives) Pluit North Jakarta 940

Gading Greenhill Pegangsaan Dua North Jakarta 700

Northern Ancol Residence Ancol North Jakarta 800

La Venue - South Tower Pasar Minggu South Jakarta 341

Kemang Village (The Intercon) Antasari South Jakarta 400The East at Essense Complex Dharmawangsa Dharmawangsa South Jakarta 244

The Aspen at Admiralty Fatmawati South Jakarta 860

Pakubuwono Terrace (Tower South) Kebayoran Lama South Jakarta 720

The Pakubuwono Signature Pakubuwono South Jakarta 188

Senopati Penthouse Senopati South Jakarta 63

LA City Apartment (Tower A) Lenteng Agung South Jakarta 980

La Maison Barito Barito South Jakarta 80

Botanica Apartment (3 Towers) Simprug South Jakarta 626

The Bellevue at Pondok Indah Pondok Indah South Jakarta 40

Green Central Tower Cerberra Gajah Mada West Jakarta 420

The Windsor (Tower I) Puri Indah West Jakarta 176The Windsor (Tower II) Puri Indah West Jakarta 164

Sky Terrace Lagoon Kalideres West Jakarta 525

Metro Park Residence Kebon Jeruk West Jakarta 1200

Green Palm Residence Puri Kosambi West Jakarta 1000

continued

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 411

4 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

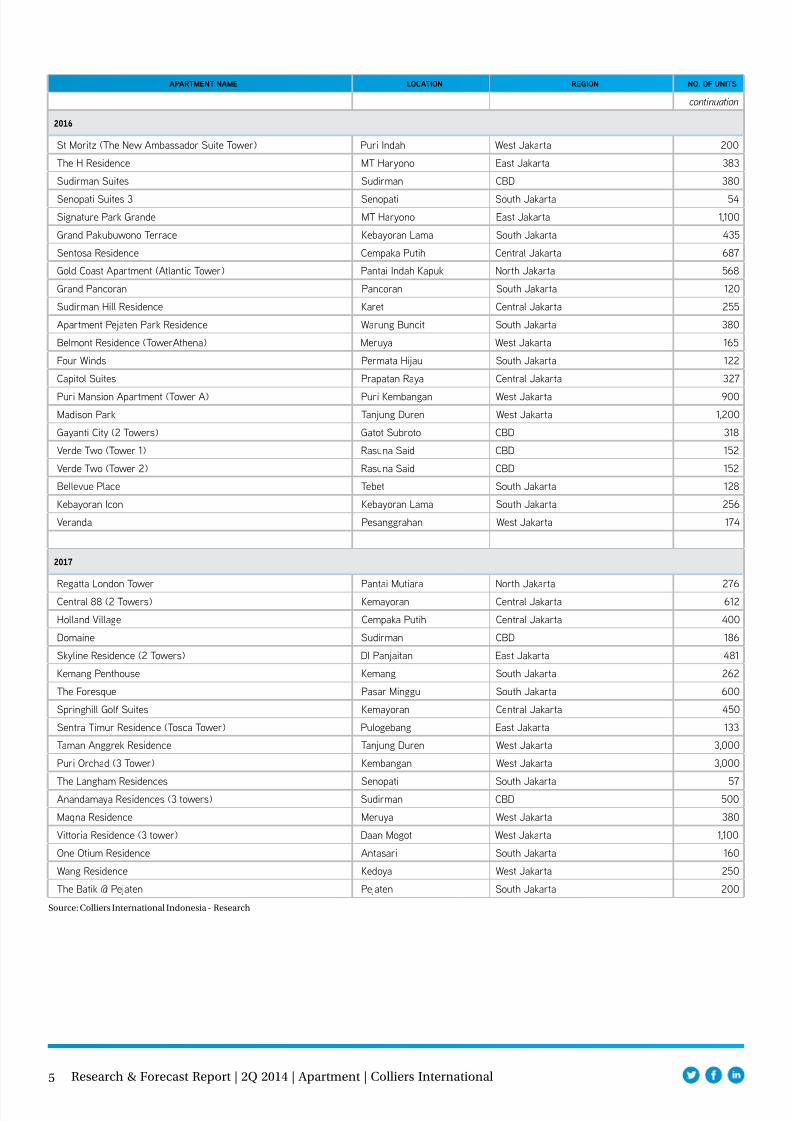

APARTMENT NAME LOCATION REGION NO OF UNITS

continuation

983090983088983089983093

East Park Apartment (Tower C) KRT Radjiman East Jakarta 550

The Residence (CWJ 2) Satrio CBD 119

The Orchad Satrio (CWJ 2) Satrio CBD 349

Setiabudi Sky Garden (tower 2) Setiabudi CBD 160

T - Plaza Residence (Tower B) Pejompongan Central Jakarta 500

Menteng Park Cikini Central Jakarta 756

The Grreen Pramuka (Tower Orchid) Pramuka Central Jakarta 1000

The Grreen Pramuka (Tower Penelope) Pramuka Central Jakarta 1000

The Green Pramuka (Tower Scarlet) Pramuka Central Jakarta 1000

The H Residence Kemayoran (Amethyst) Kemayoran Central Jakarta 800

Green Signature Apartment MT Haryono East Jakarta 800

Bassura City (Tower Flamboyan) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Edelweiss) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Dahlia) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Cattleya) Basuki Rahmat East Jakarta 600

Bassura City (Tower Alamanda) Basuki Rahmat East Jakarta 600

Teluk Intan (Tower Saphire) Teluk Gong North Jakarta 1100

Tifolia Apartment Perintis Kemerdekaan East Jakarta 500

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

Callia Apartment Perintis Kemerdekaan East Jakarta 560

The Oakwood Sky Garden (2 Towers) Pluit North Jakarta 700

Pluit Seaview (Tower Ibiza) Pluit North Jakarta 500

Pluit Seaview (Tower Bahama) Pluit North Jakarta 650

Green Bay Pluit (Sea View) Pluit North Jakarta 2072

Kemang Village - The Bloomington Antasari South Jakarta 150

The Royal Olive Residence Tower I Buncit Raya South Jakarta 225

Woodland Park (Cendana Tower) Kalibata South Jakarta 218

Senopati Suites 2 Senopati South Jakarta 81

1 Park Avenue Gandaria South Jakarta 279

Nine Residence Warung Buncit South Jakarta 246

Providence Park Permata Hijau South Jakarta 114

Kencana Residence Pondok Indah South Jakarta 173

District 8 (Tower Eternity) Senopati South Jakarta 400

District 8 (Tower Infinity) Senopati South Jakarta 280

Izzara Apartment (2 Tower 225 unit) TB Simatupang South Jakarta 450

Lexington Rersidence (Tower 1) Pondok Pinang South Jakarta 270

Lexington Rersidence (Tower 2) Pondok Pinang South Jakarta 270

The Aspen Peak at Admiralty Fatmawati South Jakarta 644

Belmont Residence (Tower Montblanc) Meruya Ilir West Jakarta 350

Gianetti Apartment Kemanggisan West Jakarta 500

St Moritz (New Presidential Tower) Puri Indah West Jakarta 150

Satu8 Residence Kedoya West Jakarta 174

The Nest Apartment Meruya Utara West Jakarta 1100

Point 8 (Air Crew Tower) Daan Mogot West Jakarta 546

Gallery West Kebon Jeruk West Jakarta 280

19 Avenue Apartment Daan Mogot West Jakarta 338

continued

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 511

5 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO OF UNITS

continuation

983090983088983089983094

St Moritz (The New Ambassador Suite Tower) Puri Indah West Jakarta 200

The H Residence MT Haryono East Jakarta 383

Sudirman Suites Sudirman CBD 380

Senopati Suites 3 Senopati South Jakarta 54

Signature Park Grande MT Haryono East Jakarta 1100

Grand Pakubuwono Terrace Kebayoran Lama South Jakarta 435

Sentosa Residence Cempaka Putih Central Jakarta 687

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

Grand Pancoran Pancoran South Jakarta 120

Sudirman Hill Residence Karet Central Jakarta 255

Apartment Pejaten Park Residence Warung Buncit South Jakarta 380

Belmont Residence (TowerAthena) Meruya West Jakarta 165

Four Winds Permata Hijau South Jakarta 122

Capitol Suites Prapatan Raya Central Jakarta 327

Puri Mansion Apartment (Tower A) Puri Kembangan West Jakarta 900

Madison Park Tanjung Duren West Jakarta 1200

Gayanti City (2 Towers) Gatot Subroto CBD 318

Verde Two (Tower 1) Rasuna Said CBD 152

Verde Two (Tower 2) Rasuna Said CBD 152

Bellevue Place Tebet South Jakarta 128

Kebayoran Icon Kebayoran Lama South Jakarta 256

Veranda Pesanggrahan West Jakarta 174

983090983088983089983095

Regatta London Tower Pantai Mutiara North Jakarta 276Central 88 (2 Towers) Kemayoran Central Jakarta 612

Holland Village Cempaka Putih Central Jakarta 400

Domaine Sudirman CBD 186

Skyline Residence (2 Towers) DI Panjaitan East Jakarta 481

Kemang Penthouse Kemang South Jakarta 262

The Foresque Pasar Minggu South Jakarta 600

Springhill Golf Suites Kemayoran Central Jakarta 450

Sentra Timur Residence (Tosca Tower) Pulogebang East Jakarta 133

Taman Anggrek Residence Tanjung Duren West Jakarta 3000

Puri Orchad (3 Tower) Kembangan West Jakarta 3000

The Langham Residences Senopati South Jakarta 57Anandamaya Residences (3 towers) Sudirman CBD 500

Maqna Residence Meruya West Jakarta 380

Vittoria Residence (3 tower) Daan Mogot West Jakarta 1100

One Otium Residence Antasari South Jakarta 160

Wang Residence Kedoya West Jakarta 250

The Batik Pejaten Pejaten South Jakarta 200

Source Colliers International Indonesia - Research

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 611

6 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Source Colliers International Indonesia - Research

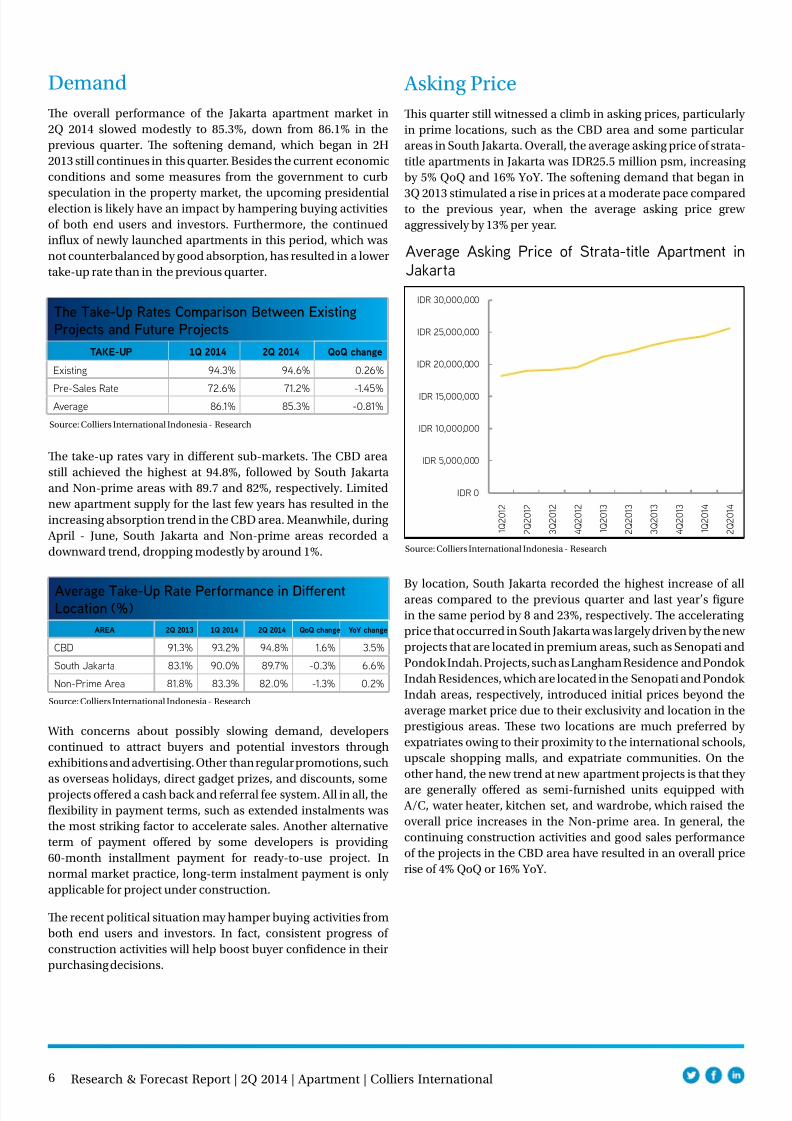

Average Take-Up Rate Performance in DifferentLocation ()

AREA 983090Q 983090983088983089983091 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change YoY change

CBD 913 932 948 16 35

South Jakarta 831 900 897 -03 66

Non-Prime Area 818 833 820 -13 02

Demand

Te overall performance of the Jakarta apartment market in

2Q 2014 slowed modestly to 853 down from 861 in the

previous quarter Te softening demand which began in 2H

2013 still continues in this quarter Besides the current economic

conditions and some measures from the government to curb

speculation in the property market the upcoming presidentialelection is likely have an impact by hampering buying activities

of both end users and investors Furthermore the continued

influx of newly launched apartments in this period which was

not counterbalanced by good absorption has resulted in a lower

take-up rate than in the previous quarter

Source Colliers International Indonesia - Research

The Take-Up Rates Comparison Between ExistingProjects and Future Projects

TAKE-UP 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

Existing 943 946 026

Pre-Sales Rate 726 712 -145Average 861 853 -081

Te take-up rates vary in different sub-markets Te CBD area

still achieved the highest at 948 followed by South Jakarta

and Non-prime areas with 897 and 82 respectively Limited

new apartment supply for the last few years has resulted in the

increasing absorption trend in the CBD area Meanwhile during

April - June South Jakarta and Non-prime areas recorded a

downward trend dropping modestly by around 1

Asking Price

Tis quarter still witnessed a climb in asking prices particularly

in prime locations such as the CBD area and some particular

areas in South Jakarta Overall the average asking price of strata-

title apartments in Jakarta was IDR255 million psm increasing

by 5 QoQ and 16 YoY Te softening demand that began in

3Q 2013 stimulated a rise in prices at a moderate pace comparedto the previous year when the average asking price grew

aggressively by 13 per year

With concerns about possibly slowing demand developers

continued to attract buyers and potential investors through

exhibitions and advertising Other than regular promotions such

as overseas holidays direct gadget prizes and discounts some

projects offered a cash back and referral fee system All in all the

flexibility in payment terms such as extended instalments was

the most striking factor to accelerate sales Another alternative

term of payment offered by some developers is providing

60-month installment payment for ready-to-use project In

normal market practice long-term instalment payment is only

applicable for project under construction

Te recent political situation may hamper buying activities from

both end users and investors In fact consistent progress of

construction activities will help boost buyer confidence in their

purchasing decisions

Average Asking Price of Strata-title Apartment inJakarta

IDR 0

IDR 5000000

IDR 10000000

IDR 15000000

IDR 20000000

IDR 25000000

IDR 30000000

1 Q 2 0 1 2

2 Q 2 0 1 2

3 Q 2 0 1 2

4 Q 2 0 1 2

1 Q 2 0 1 3

2 Q 2 0 1 3

3 Q 2 0 1 3

4 Q 2 0 1 3

1 Q 2 0 1 4

2 Q 2 0 1 4

Source Colliers International Indonesia - Research

By location South Jakarta recorded the highest increase of allareas compared to the previous quarter and last yearrsquos figure

in the same period by 8 and 23 respectively Te accelerating

price that occurred in South Jakarta was largely driven by the new

projects that are located in premium areas such as Senopati and

Pondok Indah Projects such as Langham Residence and Pondok

Indah Residences which are located in the Senopati and Pondok

Indah areas respectively introduced initial prices beyond the

average market price due to their exclusivity and location in the

prestigious areas Tese two locations are much preferred by

expatriates owing to their proximity to the international schools

upscale shopping malls and expatriate communities On the

other hand the new trend at new apartment projects is that they

are generally offered as semi-furnished units equipped with AC water heater kitchen set and wardrobe which raised the

overall price increases in the Non-prime area In general the

continuing construction activities and good sales performance

of the projects in the CBD area have resulted in an overall price

rise of 4 QoQ or 16 YoY

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 711

7 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

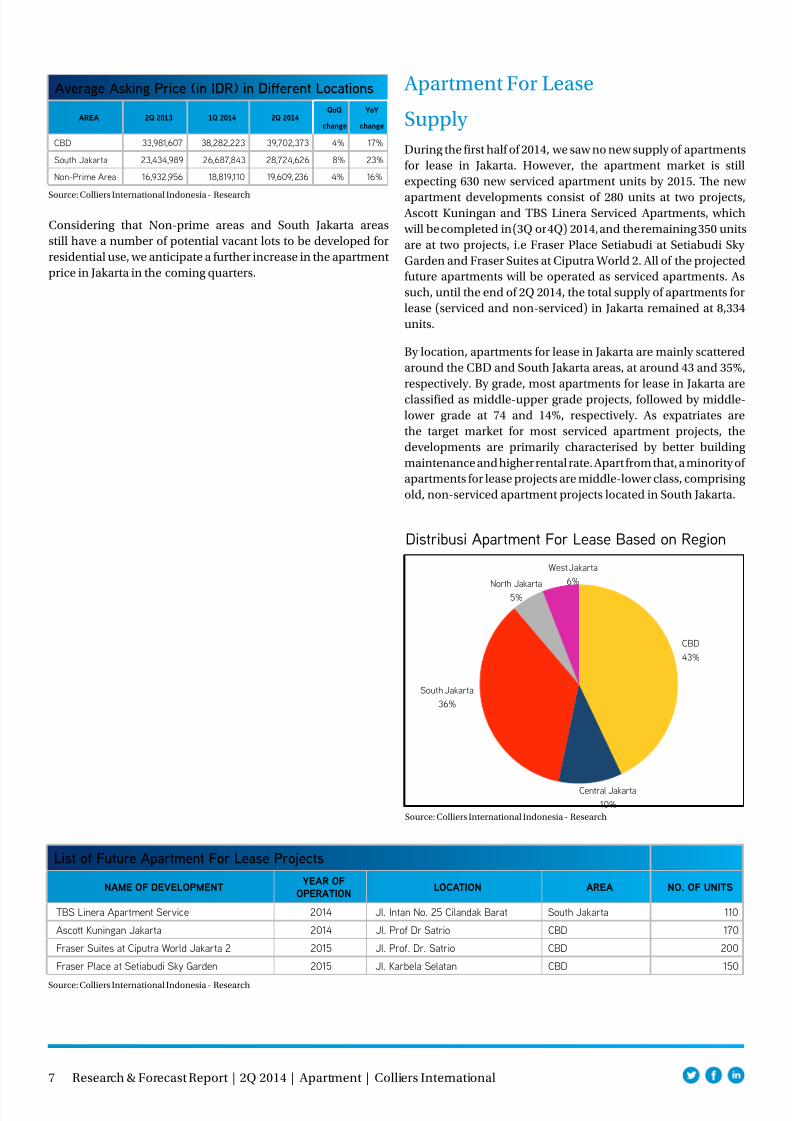

Apartment For Lease

Supply

During the first half of 2014 we saw no new supply of apartments

for lease in Jakarta However the apartment market is still

expecting 630 new serviced apartment units by 2015 Te new

apartment developments consist of 280 units at two projects Ascott Kuningan and BS Linera Serviced Apartments which

will be completed in (3Q or 4Q) 2014 and the remaining 350 units

are at two projects ie Fraser Place Setiabudi at Setiabudi Sky

Garden and Fraser Suites at Ciputra World 2 All of the projected

future apartments will be operated as serviced apartments As

such until the end of 2Q 2014 the total supply of apartments for

lease (serviced and non-serviced) in Jakarta remained at 8334

units

By location apartments for lease in Jakarta are mainly scattered

around the CBD and South Jakarta areas at around 43 and 35

respectively By grade most apartments for lease in Jakarta are

classified as middle-upper grade projects followed by middle-

lower grade at 74 and 14 respectively As expatriates are

the target market for most serviced apartment projects the

developments are primarily characterised by better building

maintenance and higher rental rate Apart from that a minority of

apartments for lease projects are middle-lower class comprising

old non-serviced apartment projects located in South Jakarta

Source Colliers International Indonesia - Research

Average Asking Price (in IDR) in Different Locations

AREA 983090Q 983090983088983089983091 983089Q 983090983088983089983092 983090Q 983090983088983089983092QoQ

change

YoY

change

CBD 33981607 38282223 39702373 4 17

South Jakarta 23434989 26687843 28724626 8 23

Non-Prime Area 16932 956 18819110 19609236 4 16

Considering that Non-prime areas and South Jakarta areas

still have a number of potential vacant lots to be developed for

residential use we anticipate a further increase in the apartment

price in Jakarta in the coming quarters

Source Colliers International Indonesia - Research

List of Future Apartment For Lease Projects

NAME OF DEVELOPMENTYEAR OF

OPERATIONLOCATION AREA NO OF UNITS

TBS Linera Apartment Service 2014 Jl Intan No 25 Cilandak Barat South Jakarta 110

Ascott Kuningan Jakarta 2014 Jl Prof Dr Satrio CBD 170

Fraser Suites at Ciputra World Jakarta 2 2015 Jl Prof Dr Satrio CBD 200

Fraser Place at Setiabudi Sky Garden 2015 Jl Karbela Selatan CBD 150

Distribusi Apartment For Lease Based on Region

Source Colliers International Indonesia - Research

CBD

43

Central Jakarta

10

South Jakarta

36

North Jakarta

5

West Jakarta

6

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 811

8 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Average Rental Rates

Te overall asking rental rates for apartments for lease increased

slightly during 2Q 2014 Te QoQ increase in the rental rate was

mostly due to some old apartments having renovated some of

their units and then offering them at higher prices Te renovation

work created a rent discrepancy between the standard and the

renovated units ranging from USD200 to 400 per unit On theother hand some serviced apartment operators with projects in

the South Jakarta area confidently feel that their high occupancy

rate is the basis for raising the rental rates slightly between

USD100 and 150 unit month

Source Colliers International Indonesia - Research

Average Rental Rates (psmmonth) in Different Areas

RENTAL RATE (PSMMONTH CHANGE

AREA 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ

CBD including SouthJakarta

USD2758 USD2761 01

Non-Prime Areas USD1564 USD1597 21

Overall the average rental rates of serviced apartments in

the CBD (including South Jakarta) and the Non-prime areas

increased modestly by 09 compared to the previous quarter

Serviced apartments in the CBD area (including South Jakarta)

posted an average rent of USD3320 psm month while the

non-serviced apartments quoted a cheaper rate at an average

of USD2670 psm month Serviced apartments located in the

Non-prime areas reached USD1780 psm month while the

non-serviced apartments charged less at USD1320 psm month

Average Rental Rates of Apartment For Lease(Serviced and Non-Serviced)

Source Colliers International Indonesia - Research

USD 000

USD 500

USD 1000

USD 1500

USD 2000

USD 2500

USD 3000

2009 2010 2011 2012 2013 2014 YTD

CBD (including South Jakarta) Non-prime Area

Te increase in the electricity tariff effective 1 July 2014 has

yet to have a substantial impact on serviced and non-serviced

apartments It will not cause apartments for lease to raise their

rental rates or service charges immediately because the tariff will

be charged directly to the tenants

Occupancy Rates

Te dynamic market for Jakarta apartments for lease during 2Q

2014 has made the overall occupancy rate increase by 08 to

766 All apartment submarkets including serviced and non-

serviced have experienced an upward trend compared to the

previous quarter by 02 and 19 respectively

Source Colliers International Indonesia - Research

The Occupancy Rates of Serviced and Non-ServicedApartment

TAKE-UP 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

Serviced 705 724 19

Non-Serviced 784 786 02

Quite a few transactions occurred in the apartment for lease

market in Jakarta during this fiscal period especially in May

when a number of expatriates particularly from Japan relocated

to Indonesia On the other hand newcomers mostly corporatetenants took both short-term and long-term leases

Regular tenants of apartments for lease particularly in the

South Jakarta area were still dominated by Asian expatriates

such as Japanese and Koreans Furthermore the increase in

the occupancy rate during the quarter was underpinned by

corporate tenants from big local banks that occupied a number

of units for training purposes Tis contributed to the increase

in the occupancy rate in South Jakartarsquos serviced apartments

Active industries that generate demand for apartments for lease

continue to be oil and gas construction banking and financial

manufacturing and embassies

Source Colliers International Indonesia - Research

Average Occupancy Level of Apartment For Lease

(Non-Serviced)OCCUPANCY 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

CBD 841 846 05

South Jakarta 781 783 03

Non-prime area 759 759 01

Source Colliers International Indonesia - Research

Average Occupancy Level of Apartment For Lease(Serviced)

OCCUPANCY 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

CBD 788 820 32

South Jakarta 761 838 77

Non-prime area 519 527 09

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 911

9 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Concluding Tought

Te political circumstances has been the most stirring

factor affecting buyer sentiment Te apprehension over the

presidential election led to a wait-and-see attitude for apartment

buyers who may postpone their buying decisions in the short

term Tis is evidenced by the softening demand since 1Q 2014

that impacted the slowing growth in asking prices On the otherhand the high interest rate depreciation of rupiah and stricter

mortgage regulations remain the concerns of developers in

their attempts to keep sales at a healthy level In fact quite a

few developers are initiating various creative strategies that will

likely boost sales of apartments

Te apartment for lease market will grow moderately until 2015

with a total of four projects in the pipeline located in the CBD

and South Jakarta areas In addition massive new stock of new

strata-title apartments located in close proximity to the CBD can

potentially put downward pressure on occupancy levels of both

serviced and non-serviced apartments

Te hike in the electricity tariff in July has not immediately caused

apartments for lease to raise their service charges or rental rates

In fact the serviced and non-serviced apartments charge a rental

rate based on daily services quality of furnishings and facilities

in the apartments Te electricity tariff is charged directly to the

tenants based on their usage

In anticipation of tougher competition from strata-title

apartment units offered for lease and operated like non-serviced

apartments the serviced apartments offered more benefits and

facilities to entice tenants In addition to the standard facilities

such as 24-hour security system and swimming pool many

serviced apartment projects offered various plus points that

cater to the needs of residents Tese include special facilities

like a lounge library or free breakfast and daily services such asfree school bus for the children personal grocery delivery and

daily maid services which are not normally available with non-

serviced apartments or strata-title apartments

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 1011

10 Research amp Forecast Report | 2Q 2014 | Office | Colliers International

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 1111

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 211

2 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Source Colliers International Indonesia - Research

List of Completed Projecs During 2Q 2014

DEVELOPMENT LOCATION REGION DEVELOPER NO OF UNITS

Kemang Village (The Intercon) Jl Pangeran Antasari South Jakarta Lippo Karawaci 400

The East at Essence Complex Dharmawangsa Jl Dharmawangsa X South Jakarta PT Prakarsa Semesta Alam 244

Pakubuwono Terrace (South Tower) Jl Kebayoran Lama South Jakarta PT Selaras Mitra Sejati 720

Verde Apartment (Tower East) Jl HR Rasuna Said CBD Farpoint Realty 114

The Windsor (Tower I) Jl Puri Indah West Jakarta PT Antilope Madju Puri Indah 176

Sentra Timur Residence (Tower Orange) Jl Pulo Gebang East Jakarta Bakriland Development 390

The Hive Tamansari Jl DI Panjaitan East Jakarta Wika Realty 422

The Green Pramuka (Tower Chrysant) Jl Jenderal Ahmad Yani Central Jakarta PT Duta Paramindo 1000

Total 3466

Newly Launched Apartments During 1Q 2014

DEVELOPMENT LOCATION REGION NO OF UNITSEXPECTED

COMPLETION TIMEASKING PRICESQ M

(EXCLUDING VAT)

Springhill Golf Suites Kemayoran Central Jakarta 450 2017 22600000

The H Residence Kemayoran (Amethyst Tower) Kemayoran Central Jakarta 800 2015 13600000

Ciputra International Puri Indah (Tower I) Puri Indah West Jakarta 412 2017 27000000

19 Avenue Apartment Daan Mogot West Jakarta 338 2015 12800000

Sentra Timur Residence (Tosca Tower) Pasar Rebo East Jakarta 133 2017 11000000

Bassura City (Tower Jasmine and Heleconia) Basuki Rahmat East Jakarta 880 2018 12500000

Source Colliers International Indonesia - Research

estimated

At the six newly launched apartment projects there are two

on-hold projects (partly constructed) ie Te H Residence

Kemayoran and 19 Avenue Apartment that were acquired by

two developers HK Realtindo took over one tower of ApartmentMenara Rajawali (Chrysant ower) in the Kemayoran area

and continued the unfinished work Tis apartment tower was

then renamed Te H Residence Kemayoran (Amethyst ower)

Similarly a rusunami project (low cost apartment project) called

Rusunami Orchad Palace was taken over by Margayahu Land

who changed the concept into a more commercial apartment

project and renamed the project 19 Avenue Apartments

Springhill Golf Suites and Ciputra International Puri Indah

(ower I) are brand new projects that target the middle to

upper segments In Bassura City compound ower Jasmine

and Heleconia are the second phase of the previous six towers

thatwas old in the first phase

At the beginning of 2014 we anticipated that a total of 20899

new apartment units would enter the Jakarta apartment

market Overall during 1H 2014 some 4712 units have entered

the market or 23 of the total units Tis indicates a relativelyslow supply growth compared to the last three years when the

average of 8498 apartment units were added to the market in the

first semester of each year Several projects that were previously

scheduled to open in this quarter were delayed due to a variety of

reasons Slow finishing work due to technical problems such as

testing the electrical and mechanical elements of the apartment

projects was most frequently reported by developers as causing

delays

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 311

3 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

New Supply Pipeline (2014 - 2017)

APARTMENT NAME LOCATION REGION NO OF UNITS

983090983088983089983092

Woodland Park (Matoa tower) (983089Q) Kalibata South Jakarta 221

Pakubuwono Terrace (Tower North) (1Q) Kebayoran Lama South Jakarta 750

Sherwood Residence (Wellington) (1Q) Kelapa Gading North Jakarta 100

Kemang Village (The Infinity) (1Q) Antasari South Jakarta 175

Ambassade Residence Tower A Puri Denpasar CBD 234

Raffles Residences Satrio CBD 64

MyHome Apartment at Ciputra World Satrio CBD 136

Setiabudi Sky Garden (tower 1) Rasuna Said CBD 426

Verde Apartment (Tower East) Rasuna Said CBD 114

Pasar Baru Mansion (2 towers) Pasar Baru Central Jakarta 520

Elpis Residence Gunung Sahari Central Jakarta 791

Capitol Park Apartment Salemba Central Jakarta 1700

The Mansion at Dukuh Golf Residence (Aurora Tower) Kemayoran Central Jakarta 522

The Mansion at Dukuh Golf Residence (BellaVista Tower) Kemayoran Central Jakarta 612

The Green Pramuka (Tower Chrysant) Pramuka Central Jakarta 1000

The Green Pramuka (Tower Bougenville) Pramuka Central Jakarta 1000

Sentra Timur Residence II (2 Towers) Pasar Rebo East Jakarta 810

Titanium Square Pulo Gebang East Jakarta 725

The Hive Tamansari Cawang East Jakarta 422

Sherwood Residence (Regent) Kelapa Gading North Jakarta 100

Pluit Seaview (Tower Maldives) Pluit North Jakarta 940

Gading Greenhill Pegangsaan Dua North Jakarta 700

Northern Ancol Residence Ancol North Jakarta 800

La Venue - South Tower Pasar Minggu South Jakarta 341

Kemang Village (The Intercon) Antasari South Jakarta 400The East at Essense Complex Dharmawangsa Dharmawangsa South Jakarta 244

The Aspen at Admiralty Fatmawati South Jakarta 860

Pakubuwono Terrace (Tower South) Kebayoran Lama South Jakarta 720

The Pakubuwono Signature Pakubuwono South Jakarta 188

Senopati Penthouse Senopati South Jakarta 63

LA City Apartment (Tower A) Lenteng Agung South Jakarta 980

La Maison Barito Barito South Jakarta 80

Botanica Apartment (3 Towers) Simprug South Jakarta 626

The Bellevue at Pondok Indah Pondok Indah South Jakarta 40

Green Central Tower Cerberra Gajah Mada West Jakarta 420

The Windsor (Tower I) Puri Indah West Jakarta 176The Windsor (Tower II) Puri Indah West Jakarta 164

Sky Terrace Lagoon Kalideres West Jakarta 525

Metro Park Residence Kebon Jeruk West Jakarta 1200

Green Palm Residence Puri Kosambi West Jakarta 1000

continued

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 411

4 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO OF UNITS

continuation

983090983088983089983093

East Park Apartment (Tower C) KRT Radjiman East Jakarta 550

The Residence (CWJ 2) Satrio CBD 119

The Orchad Satrio (CWJ 2) Satrio CBD 349

Setiabudi Sky Garden (tower 2) Setiabudi CBD 160

T - Plaza Residence (Tower B) Pejompongan Central Jakarta 500

Menteng Park Cikini Central Jakarta 756

The Grreen Pramuka (Tower Orchid) Pramuka Central Jakarta 1000

The Grreen Pramuka (Tower Penelope) Pramuka Central Jakarta 1000

The Green Pramuka (Tower Scarlet) Pramuka Central Jakarta 1000

The H Residence Kemayoran (Amethyst) Kemayoran Central Jakarta 800

Green Signature Apartment MT Haryono East Jakarta 800

Bassura City (Tower Flamboyan) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Edelweiss) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Dahlia) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Cattleya) Basuki Rahmat East Jakarta 600

Bassura City (Tower Alamanda) Basuki Rahmat East Jakarta 600

Teluk Intan (Tower Saphire) Teluk Gong North Jakarta 1100

Tifolia Apartment Perintis Kemerdekaan East Jakarta 500

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

Callia Apartment Perintis Kemerdekaan East Jakarta 560

The Oakwood Sky Garden (2 Towers) Pluit North Jakarta 700

Pluit Seaview (Tower Ibiza) Pluit North Jakarta 500

Pluit Seaview (Tower Bahama) Pluit North Jakarta 650

Green Bay Pluit (Sea View) Pluit North Jakarta 2072

Kemang Village - The Bloomington Antasari South Jakarta 150

The Royal Olive Residence Tower I Buncit Raya South Jakarta 225

Woodland Park (Cendana Tower) Kalibata South Jakarta 218

Senopati Suites 2 Senopati South Jakarta 81

1 Park Avenue Gandaria South Jakarta 279

Nine Residence Warung Buncit South Jakarta 246

Providence Park Permata Hijau South Jakarta 114

Kencana Residence Pondok Indah South Jakarta 173

District 8 (Tower Eternity) Senopati South Jakarta 400

District 8 (Tower Infinity) Senopati South Jakarta 280

Izzara Apartment (2 Tower 225 unit) TB Simatupang South Jakarta 450

Lexington Rersidence (Tower 1) Pondok Pinang South Jakarta 270

Lexington Rersidence (Tower 2) Pondok Pinang South Jakarta 270

The Aspen Peak at Admiralty Fatmawati South Jakarta 644

Belmont Residence (Tower Montblanc) Meruya Ilir West Jakarta 350

Gianetti Apartment Kemanggisan West Jakarta 500

St Moritz (New Presidential Tower) Puri Indah West Jakarta 150

Satu8 Residence Kedoya West Jakarta 174

The Nest Apartment Meruya Utara West Jakarta 1100

Point 8 (Air Crew Tower) Daan Mogot West Jakarta 546

Gallery West Kebon Jeruk West Jakarta 280

19 Avenue Apartment Daan Mogot West Jakarta 338

continued

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 511

5 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO OF UNITS

continuation

983090983088983089983094

St Moritz (The New Ambassador Suite Tower) Puri Indah West Jakarta 200

The H Residence MT Haryono East Jakarta 383

Sudirman Suites Sudirman CBD 380

Senopati Suites 3 Senopati South Jakarta 54

Signature Park Grande MT Haryono East Jakarta 1100

Grand Pakubuwono Terrace Kebayoran Lama South Jakarta 435

Sentosa Residence Cempaka Putih Central Jakarta 687

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

Grand Pancoran Pancoran South Jakarta 120

Sudirman Hill Residence Karet Central Jakarta 255

Apartment Pejaten Park Residence Warung Buncit South Jakarta 380

Belmont Residence (TowerAthena) Meruya West Jakarta 165

Four Winds Permata Hijau South Jakarta 122

Capitol Suites Prapatan Raya Central Jakarta 327

Puri Mansion Apartment (Tower A) Puri Kembangan West Jakarta 900

Madison Park Tanjung Duren West Jakarta 1200

Gayanti City (2 Towers) Gatot Subroto CBD 318

Verde Two (Tower 1) Rasuna Said CBD 152

Verde Two (Tower 2) Rasuna Said CBD 152

Bellevue Place Tebet South Jakarta 128

Kebayoran Icon Kebayoran Lama South Jakarta 256

Veranda Pesanggrahan West Jakarta 174

983090983088983089983095

Regatta London Tower Pantai Mutiara North Jakarta 276Central 88 (2 Towers) Kemayoran Central Jakarta 612

Holland Village Cempaka Putih Central Jakarta 400

Domaine Sudirman CBD 186

Skyline Residence (2 Towers) DI Panjaitan East Jakarta 481

Kemang Penthouse Kemang South Jakarta 262

The Foresque Pasar Minggu South Jakarta 600

Springhill Golf Suites Kemayoran Central Jakarta 450

Sentra Timur Residence (Tosca Tower) Pulogebang East Jakarta 133

Taman Anggrek Residence Tanjung Duren West Jakarta 3000

Puri Orchad (3 Tower) Kembangan West Jakarta 3000

The Langham Residences Senopati South Jakarta 57Anandamaya Residences (3 towers) Sudirman CBD 500

Maqna Residence Meruya West Jakarta 380

Vittoria Residence (3 tower) Daan Mogot West Jakarta 1100

One Otium Residence Antasari South Jakarta 160

Wang Residence Kedoya West Jakarta 250

The Batik Pejaten Pejaten South Jakarta 200

Source Colliers International Indonesia - Research

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 611

6 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Source Colliers International Indonesia - Research

Average Take-Up Rate Performance in DifferentLocation ()

AREA 983090Q 983090983088983089983091 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change YoY change

CBD 913 932 948 16 35

South Jakarta 831 900 897 -03 66

Non-Prime Area 818 833 820 -13 02

Demand

Te overall performance of the Jakarta apartment market in

2Q 2014 slowed modestly to 853 down from 861 in the

previous quarter Te softening demand which began in 2H

2013 still continues in this quarter Besides the current economic

conditions and some measures from the government to curb

speculation in the property market the upcoming presidentialelection is likely have an impact by hampering buying activities

of both end users and investors Furthermore the continued

influx of newly launched apartments in this period which was

not counterbalanced by good absorption has resulted in a lower

take-up rate than in the previous quarter

Source Colliers International Indonesia - Research

The Take-Up Rates Comparison Between ExistingProjects and Future Projects

TAKE-UP 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

Existing 943 946 026

Pre-Sales Rate 726 712 -145Average 861 853 -081

Te take-up rates vary in different sub-markets Te CBD area

still achieved the highest at 948 followed by South Jakarta

and Non-prime areas with 897 and 82 respectively Limited

new apartment supply for the last few years has resulted in the

increasing absorption trend in the CBD area Meanwhile during

April - June South Jakarta and Non-prime areas recorded a

downward trend dropping modestly by around 1

Asking Price

Tis quarter still witnessed a climb in asking prices particularly

in prime locations such as the CBD area and some particular

areas in South Jakarta Overall the average asking price of strata-

title apartments in Jakarta was IDR255 million psm increasing

by 5 QoQ and 16 YoY Te softening demand that began in

3Q 2013 stimulated a rise in prices at a moderate pace comparedto the previous year when the average asking price grew

aggressively by 13 per year

With concerns about possibly slowing demand developers

continued to attract buyers and potential investors through

exhibitions and advertising Other than regular promotions such

as overseas holidays direct gadget prizes and discounts some

projects offered a cash back and referral fee system All in all the

flexibility in payment terms such as extended instalments was

the most striking factor to accelerate sales Another alternative

term of payment offered by some developers is providing

60-month installment payment for ready-to-use project In

normal market practice long-term instalment payment is only

applicable for project under construction

Te recent political situation may hamper buying activities from

both end users and investors In fact consistent progress of

construction activities will help boost buyer confidence in their

purchasing decisions

Average Asking Price of Strata-title Apartment inJakarta

IDR 0

IDR 5000000

IDR 10000000

IDR 15000000

IDR 20000000

IDR 25000000

IDR 30000000

1 Q 2 0 1 2

2 Q 2 0 1 2

3 Q 2 0 1 2

4 Q 2 0 1 2

1 Q 2 0 1 3

2 Q 2 0 1 3

3 Q 2 0 1 3

4 Q 2 0 1 3

1 Q 2 0 1 4

2 Q 2 0 1 4

Source Colliers International Indonesia - Research

By location South Jakarta recorded the highest increase of allareas compared to the previous quarter and last yearrsquos figure

in the same period by 8 and 23 respectively Te accelerating

price that occurred in South Jakarta was largely driven by the new

projects that are located in premium areas such as Senopati and

Pondok Indah Projects such as Langham Residence and Pondok

Indah Residences which are located in the Senopati and Pondok

Indah areas respectively introduced initial prices beyond the

average market price due to their exclusivity and location in the

prestigious areas Tese two locations are much preferred by

expatriates owing to their proximity to the international schools

upscale shopping malls and expatriate communities On the

other hand the new trend at new apartment projects is that they

are generally offered as semi-furnished units equipped with AC water heater kitchen set and wardrobe which raised the

overall price increases in the Non-prime area In general the

continuing construction activities and good sales performance

of the projects in the CBD area have resulted in an overall price

rise of 4 QoQ or 16 YoY

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 711

7 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Apartment For Lease

Supply

During the first half of 2014 we saw no new supply of apartments

for lease in Jakarta However the apartment market is still

expecting 630 new serviced apartment units by 2015 Te new

apartment developments consist of 280 units at two projects Ascott Kuningan and BS Linera Serviced Apartments which

will be completed in (3Q or 4Q) 2014 and the remaining 350 units

are at two projects ie Fraser Place Setiabudi at Setiabudi Sky

Garden and Fraser Suites at Ciputra World 2 All of the projected

future apartments will be operated as serviced apartments As

such until the end of 2Q 2014 the total supply of apartments for

lease (serviced and non-serviced) in Jakarta remained at 8334

units

By location apartments for lease in Jakarta are mainly scattered

around the CBD and South Jakarta areas at around 43 and 35

respectively By grade most apartments for lease in Jakarta are

classified as middle-upper grade projects followed by middle-

lower grade at 74 and 14 respectively As expatriates are

the target market for most serviced apartment projects the

developments are primarily characterised by better building

maintenance and higher rental rate Apart from that a minority of

apartments for lease projects are middle-lower class comprising

old non-serviced apartment projects located in South Jakarta

Source Colliers International Indonesia - Research

Average Asking Price (in IDR) in Different Locations

AREA 983090Q 983090983088983089983091 983089Q 983090983088983089983092 983090Q 983090983088983089983092QoQ

change

YoY

change

CBD 33981607 38282223 39702373 4 17

South Jakarta 23434989 26687843 28724626 8 23

Non-Prime Area 16932 956 18819110 19609236 4 16

Considering that Non-prime areas and South Jakarta areas

still have a number of potential vacant lots to be developed for

residential use we anticipate a further increase in the apartment

price in Jakarta in the coming quarters

Source Colliers International Indonesia - Research

List of Future Apartment For Lease Projects

NAME OF DEVELOPMENTYEAR OF

OPERATIONLOCATION AREA NO OF UNITS

TBS Linera Apartment Service 2014 Jl Intan No 25 Cilandak Barat South Jakarta 110

Ascott Kuningan Jakarta 2014 Jl Prof Dr Satrio CBD 170

Fraser Suites at Ciputra World Jakarta 2 2015 Jl Prof Dr Satrio CBD 200

Fraser Place at Setiabudi Sky Garden 2015 Jl Karbela Selatan CBD 150

Distribusi Apartment For Lease Based on Region

Source Colliers International Indonesia - Research

CBD

43

Central Jakarta

10

South Jakarta

36

North Jakarta

5

West Jakarta

6

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 811

8 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Average Rental Rates

Te overall asking rental rates for apartments for lease increased

slightly during 2Q 2014 Te QoQ increase in the rental rate was

mostly due to some old apartments having renovated some of

their units and then offering them at higher prices Te renovation

work created a rent discrepancy between the standard and the

renovated units ranging from USD200 to 400 per unit On theother hand some serviced apartment operators with projects in

the South Jakarta area confidently feel that their high occupancy

rate is the basis for raising the rental rates slightly between

USD100 and 150 unit month

Source Colliers International Indonesia - Research

Average Rental Rates (psmmonth) in Different Areas

RENTAL RATE (PSMMONTH CHANGE

AREA 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ

CBD including SouthJakarta

USD2758 USD2761 01

Non-Prime Areas USD1564 USD1597 21

Overall the average rental rates of serviced apartments in

the CBD (including South Jakarta) and the Non-prime areas

increased modestly by 09 compared to the previous quarter

Serviced apartments in the CBD area (including South Jakarta)

posted an average rent of USD3320 psm month while the

non-serviced apartments quoted a cheaper rate at an average

of USD2670 psm month Serviced apartments located in the

Non-prime areas reached USD1780 psm month while the

non-serviced apartments charged less at USD1320 psm month

Average Rental Rates of Apartment For Lease(Serviced and Non-Serviced)

Source Colliers International Indonesia - Research

USD 000

USD 500

USD 1000

USD 1500

USD 2000

USD 2500

USD 3000

2009 2010 2011 2012 2013 2014 YTD

CBD (including South Jakarta) Non-prime Area

Te increase in the electricity tariff effective 1 July 2014 has

yet to have a substantial impact on serviced and non-serviced

apartments It will not cause apartments for lease to raise their

rental rates or service charges immediately because the tariff will

be charged directly to the tenants

Occupancy Rates

Te dynamic market for Jakarta apartments for lease during 2Q

2014 has made the overall occupancy rate increase by 08 to

766 All apartment submarkets including serviced and non-

serviced have experienced an upward trend compared to the

previous quarter by 02 and 19 respectively

Source Colliers International Indonesia - Research

The Occupancy Rates of Serviced and Non-ServicedApartment

TAKE-UP 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

Serviced 705 724 19

Non-Serviced 784 786 02

Quite a few transactions occurred in the apartment for lease

market in Jakarta during this fiscal period especially in May

when a number of expatriates particularly from Japan relocated

to Indonesia On the other hand newcomers mostly corporatetenants took both short-term and long-term leases

Regular tenants of apartments for lease particularly in the

South Jakarta area were still dominated by Asian expatriates

such as Japanese and Koreans Furthermore the increase in

the occupancy rate during the quarter was underpinned by

corporate tenants from big local banks that occupied a number

of units for training purposes Tis contributed to the increase

in the occupancy rate in South Jakartarsquos serviced apartments

Active industries that generate demand for apartments for lease

continue to be oil and gas construction banking and financial

manufacturing and embassies

Source Colliers International Indonesia - Research

Average Occupancy Level of Apartment For Lease

(Non-Serviced)OCCUPANCY 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

CBD 841 846 05

South Jakarta 781 783 03

Non-prime area 759 759 01

Source Colliers International Indonesia - Research

Average Occupancy Level of Apartment For Lease(Serviced)

OCCUPANCY 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

CBD 788 820 32

South Jakarta 761 838 77

Non-prime area 519 527 09

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 911

9 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Concluding Tought

Te political circumstances has been the most stirring

factor affecting buyer sentiment Te apprehension over the

presidential election led to a wait-and-see attitude for apartment

buyers who may postpone their buying decisions in the short

term Tis is evidenced by the softening demand since 1Q 2014

that impacted the slowing growth in asking prices On the otherhand the high interest rate depreciation of rupiah and stricter

mortgage regulations remain the concerns of developers in

their attempts to keep sales at a healthy level In fact quite a

few developers are initiating various creative strategies that will

likely boost sales of apartments

Te apartment for lease market will grow moderately until 2015

with a total of four projects in the pipeline located in the CBD

and South Jakarta areas In addition massive new stock of new

strata-title apartments located in close proximity to the CBD can

potentially put downward pressure on occupancy levels of both

serviced and non-serviced apartments

Te hike in the electricity tariff in July has not immediately caused

apartments for lease to raise their service charges or rental rates

In fact the serviced and non-serviced apartments charge a rental

rate based on daily services quality of furnishings and facilities

in the apartments Te electricity tariff is charged directly to the

tenants based on their usage

In anticipation of tougher competition from strata-title

apartment units offered for lease and operated like non-serviced

apartments the serviced apartments offered more benefits and

facilities to entice tenants In addition to the standard facilities

such as 24-hour security system and swimming pool many

serviced apartment projects offered various plus points that

cater to the needs of residents Tese include special facilities

like a lounge library or free breakfast and daily services such asfree school bus for the children personal grocery delivery and

daily maid services which are not normally available with non-

serviced apartments or strata-title apartments

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 1011

10 Research amp Forecast Report | 2Q 2014 | Office | Colliers International

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 1111

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 311

3 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

New Supply Pipeline (2014 - 2017)

APARTMENT NAME LOCATION REGION NO OF UNITS

983090983088983089983092

Woodland Park (Matoa tower) (983089Q) Kalibata South Jakarta 221

Pakubuwono Terrace (Tower North) (1Q) Kebayoran Lama South Jakarta 750

Sherwood Residence (Wellington) (1Q) Kelapa Gading North Jakarta 100

Kemang Village (The Infinity) (1Q) Antasari South Jakarta 175

Ambassade Residence Tower A Puri Denpasar CBD 234

Raffles Residences Satrio CBD 64

MyHome Apartment at Ciputra World Satrio CBD 136

Setiabudi Sky Garden (tower 1) Rasuna Said CBD 426

Verde Apartment (Tower East) Rasuna Said CBD 114

Pasar Baru Mansion (2 towers) Pasar Baru Central Jakarta 520

Elpis Residence Gunung Sahari Central Jakarta 791

Capitol Park Apartment Salemba Central Jakarta 1700

The Mansion at Dukuh Golf Residence (Aurora Tower) Kemayoran Central Jakarta 522

The Mansion at Dukuh Golf Residence (BellaVista Tower) Kemayoran Central Jakarta 612

The Green Pramuka (Tower Chrysant) Pramuka Central Jakarta 1000

The Green Pramuka (Tower Bougenville) Pramuka Central Jakarta 1000

Sentra Timur Residence II (2 Towers) Pasar Rebo East Jakarta 810

Titanium Square Pulo Gebang East Jakarta 725

The Hive Tamansari Cawang East Jakarta 422

Sherwood Residence (Regent) Kelapa Gading North Jakarta 100

Pluit Seaview (Tower Maldives) Pluit North Jakarta 940

Gading Greenhill Pegangsaan Dua North Jakarta 700

Northern Ancol Residence Ancol North Jakarta 800

La Venue - South Tower Pasar Minggu South Jakarta 341

Kemang Village (The Intercon) Antasari South Jakarta 400The East at Essense Complex Dharmawangsa Dharmawangsa South Jakarta 244

The Aspen at Admiralty Fatmawati South Jakarta 860

Pakubuwono Terrace (Tower South) Kebayoran Lama South Jakarta 720

The Pakubuwono Signature Pakubuwono South Jakarta 188

Senopati Penthouse Senopati South Jakarta 63

LA City Apartment (Tower A) Lenteng Agung South Jakarta 980

La Maison Barito Barito South Jakarta 80

Botanica Apartment (3 Towers) Simprug South Jakarta 626

The Bellevue at Pondok Indah Pondok Indah South Jakarta 40

Green Central Tower Cerberra Gajah Mada West Jakarta 420

The Windsor (Tower I) Puri Indah West Jakarta 176The Windsor (Tower II) Puri Indah West Jakarta 164

Sky Terrace Lagoon Kalideres West Jakarta 525

Metro Park Residence Kebon Jeruk West Jakarta 1200

Green Palm Residence Puri Kosambi West Jakarta 1000

continued

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 411

4 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO OF UNITS

continuation

983090983088983089983093

East Park Apartment (Tower C) KRT Radjiman East Jakarta 550

The Residence (CWJ 2) Satrio CBD 119

The Orchad Satrio (CWJ 2) Satrio CBD 349

Setiabudi Sky Garden (tower 2) Setiabudi CBD 160

T - Plaza Residence (Tower B) Pejompongan Central Jakarta 500

Menteng Park Cikini Central Jakarta 756

The Grreen Pramuka (Tower Orchid) Pramuka Central Jakarta 1000

The Grreen Pramuka (Tower Penelope) Pramuka Central Jakarta 1000

The Green Pramuka (Tower Scarlet) Pramuka Central Jakarta 1000

The H Residence Kemayoran (Amethyst) Kemayoran Central Jakarta 800

Green Signature Apartment MT Haryono East Jakarta 800

Bassura City (Tower Flamboyan) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Edelweiss) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Dahlia) Basuki Rahmat East Jakarta 1000

Bassura City (Tower Cattleya) Basuki Rahmat East Jakarta 600

Bassura City (Tower Alamanda) Basuki Rahmat East Jakarta 600

Teluk Intan (Tower Saphire) Teluk Gong North Jakarta 1100

Tifolia Apartment Perintis Kemerdekaan East Jakarta 500

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

Callia Apartment Perintis Kemerdekaan East Jakarta 560

The Oakwood Sky Garden (2 Towers) Pluit North Jakarta 700

Pluit Seaview (Tower Ibiza) Pluit North Jakarta 500

Pluit Seaview (Tower Bahama) Pluit North Jakarta 650

Green Bay Pluit (Sea View) Pluit North Jakarta 2072

Kemang Village - The Bloomington Antasari South Jakarta 150

The Royal Olive Residence Tower I Buncit Raya South Jakarta 225

Woodland Park (Cendana Tower) Kalibata South Jakarta 218

Senopati Suites 2 Senopati South Jakarta 81

1 Park Avenue Gandaria South Jakarta 279

Nine Residence Warung Buncit South Jakarta 246

Providence Park Permata Hijau South Jakarta 114

Kencana Residence Pondok Indah South Jakarta 173

District 8 (Tower Eternity) Senopati South Jakarta 400

District 8 (Tower Infinity) Senopati South Jakarta 280

Izzara Apartment (2 Tower 225 unit) TB Simatupang South Jakarta 450

Lexington Rersidence (Tower 1) Pondok Pinang South Jakarta 270

Lexington Rersidence (Tower 2) Pondok Pinang South Jakarta 270

The Aspen Peak at Admiralty Fatmawati South Jakarta 644

Belmont Residence (Tower Montblanc) Meruya Ilir West Jakarta 350

Gianetti Apartment Kemanggisan West Jakarta 500

St Moritz (New Presidential Tower) Puri Indah West Jakarta 150

Satu8 Residence Kedoya West Jakarta 174

The Nest Apartment Meruya Utara West Jakarta 1100

Point 8 (Air Crew Tower) Daan Mogot West Jakarta 546

Gallery West Kebon Jeruk West Jakarta 280

19 Avenue Apartment Daan Mogot West Jakarta 338

continued

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 511

5 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO OF UNITS

continuation

983090983088983089983094

St Moritz (The New Ambassador Suite Tower) Puri Indah West Jakarta 200

The H Residence MT Haryono East Jakarta 383

Sudirman Suites Sudirman CBD 380

Senopati Suites 3 Senopati South Jakarta 54

Signature Park Grande MT Haryono East Jakarta 1100

Grand Pakubuwono Terrace Kebayoran Lama South Jakarta 435

Sentosa Residence Cempaka Putih Central Jakarta 687

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

Grand Pancoran Pancoran South Jakarta 120

Sudirman Hill Residence Karet Central Jakarta 255

Apartment Pejaten Park Residence Warung Buncit South Jakarta 380

Belmont Residence (TowerAthena) Meruya West Jakarta 165

Four Winds Permata Hijau South Jakarta 122

Capitol Suites Prapatan Raya Central Jakarta 327

Puri Mansion Apartment (Tower A) Puri Kembangan West Jakarta 900

Madison Park Tanjung Duren West Jakarta 1200

Gayanti City (2 Towers) Gatot Subroto CBD 318

Verde Two (Tower 1) Rasuna Said CBD 152

Verde Two (Tower 2) Rasuna Said CBD 152

Bellevue Place Tebet South Jakarta 128

Kebayoran Icon Kebayoran Lama South Jakarta 256

Veranda Pesanggrahan West Jakarta 174

983090983088983089983095

Regatta London Tower Pantai Mutiara North Jakarta 276Central 88 (2 Towers) Kemayoran Central Jakarta 612

Holland Village Cempaka Putih Central Jakarta 400

Domaine Sudirman CBD 186

Skyline Residence (2 Towers) DI Panjaitan East Jakarta 481

Kemang Penthouse Kemang South Jakarta 262

The Foresque Pasar Minggu South Jakarta 600

Springhill Golf Suites Kemayoran Central Jakarta 450

Sentra Timur Residence (Tosca Tower) Pulogebang East Jakarta 133

Taman Anggrek Residence Tanjung Duren West Jakarta 3000

Puri Orchad (3 Tower) Kembangan West Jakarta 3000

The Langham Residences Senopati South Jakarta 57Anandamaya Residences (3 towers) Sudirman CBD 500

Maqna Residence Meruya West Jakarta 380

Vittoria Residence (3 tower) Daan Mogot West Jakarta 1100

One Otium Residence Antasari South Jakarta 160

Wang Residence Kedoya West Jakarta 250

The Batik Pejaten Pejaten South Jakarta 200

Source Colliers International Indonesia - Research

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 611

6 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Source Colliers International Indonesia - Research

Average Take-Up Rate Performance in DifferentLocation ()

AREA 983090Q 983090983088983089983091 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change YoY change

CBD 913 932 948 16 35

South Jakarta 831 900 897 -03 66

Non-Prime Area 818 833 820 -13 02

Demand

Te overall performance of the Jakarta apartment market in

2Q 2014 slowed modestly to 853 down from 861 in the

previous quarter Te softening demand which began in 2H

2013 still continues in this quarter Besides the current economic

conditions and some measures from the government to curb

speculation in the property market the upcoming presidentialelection is likely have an impact by hampering buying activities

of both end users and investors Furthermore the continued

influx of newly launched apartments in this period which was

not counterbalanced by good absorption has resulted in a lower

take-up rate than in the previous quarter

Source Colliers International Indonesia - Research

The Take-Up Rates Comparison Between ExistingProjects and Future Projects

TAKE-UP 983089Q 983090983088983089983092 983090Q 983090983088983089983092 QoQ change

Existing 943 946 026

Pre-Sales Rate 726 712 -145Average 861 853 -081

Te take-up rates vary in different sub-markets Te CBD area

still achieved the highest at 948 followed by South Jakarta

and Non-prime areas with 897 and 82 respectively Limited

new apartment supply for the last few years has resulted in the

increasing absorption trend in the CBD area Meanwhile during

April - June South Jakarta and Non-prime areas recorded a

downward trend dropping modestly by around 1

Asking Price

Tis quarter still witnessed a climb in asking prices particularly

in prime locations such as the CBD area and some particular

areas in South Jakarta Overall the average asking price of strata-

title apartments in Jakarta was IDR255 million psm increasing

by 5 QoQ and 16 YoY Te softening demand that began in

3Q 2013 stimulated a rise in prices at a moderate pace comparedto the previous year when the average asking price grew

aggressively by 13 per year

With concerns about possibly slowing demand developers

continued to attract buyers and potential investors through

exhibitions and advertising Other than regular promotions such

as overseas holidays direct gadget prizes and discounts some

projects offered a cash back and referral fee system All in all the

flexibility in payment terms such as extended instalments was

the most striking factor to accelerate sales Another alternative

term of payment offered by some developers is providing

60-month installment payment for ready-to-use project In

normal market practice long-term instalment payment is only

applicable for project under construction

Te recent political situation may hamper buying activities from

both end users and investors In fact consistent progress of

construction activities will help boost buyer confidence in their

purchasing decisions

Average Asking Price of Strata-title Apartment inJakarta

IDR 0

IDR 5000000

IDR 10000000

IDR 15000000

IDR 20000000

IDR 25000000

IDR 30000000

1 Q 2 0 1 2

2 Q 2 0 1 2

3 Q 2 0 1 2

4 Q 2 0 1 2

1 Q 2 0 1 3

2 Q 2 0 1 3

3 Q 2 0 1 3

4 Q 2 0 1 3

1 Q 2 0 1 4

2 Q 2 0 1 4

Source Colliers International Indonesia - Research

By location South Jakarta recorded the highest increase of allareas compared to the previous quarter and last yearrsquos figure

in the same period by 8 and 23 respectively Te accelerating

price that occurred in South Jakarta was largely driven by the new

projects that are located in premium areas such as Senopati and

Pondok Indah Projects such as Langham Residence and Pondok

Indah Residences which are located in the Senopati and Pondok

Indah areas respectively introduced initial prices beyond the

average market price due to their exclusivity and location in the

prestigious areas Tese two locations are much preferred by

expatriates owing to their proximity to the international schools

upscale shopping malls and expatriate communities On the

other hand the new trend at new apartment projects is that they

are generally offered as semi-furnished units equipped with AC water heater kitchen set and wardrobe which raised the

overall price increases in the Non-prime area In general the

continuing construction activities and good sales performance

of the projects in the CBD area have resulted in an overall price

rise of 4 QoQ or 16 YoY

7212019 ResearchAndForecast Jakarta Apartment 2Q2014

httpslidepdfcomreaderfullresearchandforecast-jakarta-apartment-2q2014 711

7 Research amp Forecast Report | 2Q 2014 | Apartment | Colliers International

Apartment For Lease

Supply

During the first half of 2014 we saw no new supply of apartments

for lease in Jakarta However the apartment market is still

expecting 630 new serviced apartment units by 2015 Te new

apartment developments consist of 280 units at two projects Ascott Kuningan and BS Linera Serviced Apartments which

will be completed in (3Q or 4Q) 2014 and the remaining 350 units

are at two projects ie Fraser Place Setiabudi at Setiabudi Sky

Garden and Fraser Suites at Ciputra World 2 All of the projected

future apartments will be operated as serviced apartments As

such until the end of 2Q 2014 the total supply of apartments for

lease (serviced and non-serviced) in Jakarta remained at 8334

units

By location apartments for lease in Jakarta are mainly scattered

around the CBD and South Jakarta areas at around 43 and 35

respectively By grade most apartments for lease in Jakarta are

classified as middle-upper grade projects followed by middle-

lower grade at 74 and 14 respectively As expatriates are

the target market for most serviced apartment projects the

developments are primarily characterised by better building

maintenance and higher rental rate Apart from that a minority of

apartments for lease projects are middle-lower class comprising

old non-serviced apartment projects located in South Jakarta

Source Colliers International Indonesia - Research

Average Asking Price (in IDR) in Different Locations

AREA 983090Q 983090983088983089983091 983089Q 983090983088983089983092 983090Q 983090983088983089983092QoQ

change

YoY

change

CBD 33981607 38282223 39702373 4 17

South Jakarta 23434989 26687843 28724626 8 23

Non-Prime Area 16932 956 18819110 19609236 4 16

Considering that Non-prime areas and South Jakarta areas

still have a number of potential vacant lots to be developed for

residential use we anticipate a further increase in the apartment

price in Jakarta in the coming quarters

Source Colliers International Indonesia - Research

List of Future Apartment For Lease Projects

NAME OF DEVELOPMENTYEAR OF

OPERATIONLOCATION AREA NO OF UNITS

TBS Linera Apartment Service 2014 Jl Intan No 25 Cilandak Barat South Jakarta 110

Ascott Kuningan Jakarta 2014 Jl Prof Dr Satrio CBD 170

Fraser Suites at Ciputra World Jakarta 2 2015 Jl Prof Dr Satrio CBD 200

Fraser Place at Setiabudi Sky Garden 2015 Jl Karbela Selatan CBD 150

Distribusi Apartment For Lease Based on Region

Source Colliers International Indonesia - Research

CBD

43

Central Jakarta

10

South Jakarta

36

North Jakarta

5