RESEARCH UNIVERSITY Financial Markets and growth

71

Financial Markets and growth Université Paris-Dauphine International Office 2017-2018 By Yeganeh Forouheshfar [email protected] RESEARCH UNIVERSITY 1

Transcript of RESEARCH UNIVERSITY Financial Markets and growth

FinancialMarketsandgrowth

UniversitéParis-DauphineInternationalOffice

2017-2018By

R E S E A R C HU N I V E R S I T Y

1

Introductiontothiscourse• Outlineofthecourse:

– Ch1:Introduction,keydefinitionsandsomehistory– Ch2:Financeandgrowthnexus– Ch3:Growth,inequality,povertyandfinancialdeepening– Ch4:TheStructureofthefinancialsector– Ch5:Financialrepressionand liberalization– Ch6:Thedomesticfinancialsystem

• Evaluation:50%Finalexam,50%presentation(yourattitudeintheclasscanplayarole!)

• Theslidesareavailableathttp://forouheshfar.com/course-fmg/

2

Readingsuggestions• “DevelopmentFinancedebatesdogmasandnewdirections”-

StephenSpratt(2009)

• “FinancialMarketsandInstitutions”- FredericS.Mishkin &StanleyEakins(8thEdition-2015)

• Worldbank:Globalfinancialdevelopmentreport– annually

• IMF&OECD:workingpapersandreports

3

Chapter1:Introduction,keydefinitionsandsomehistory

FinancialMarkets andGrowth2017-2018

ByYeganehForouheshfar

4

Outlineofthechapter

• WhatarefinancialMarkets• Definingkeyterms• Classificationoffinancialmarkets• Howdofinancialmarketsdifferfromothermarkets

• Majorrolesofthefinancialsystem• Marketorgovernment:Somehistory

5

WhatarefinancialMarkets?• Financialmarketsperformtheessentialfunctionofchanneling

fundsfromeconomicplayersthathavesavedsurplusfundstothosewithashortageoffunds.

• Exchangebetweenthesetwogroupsofagentsissettledinfinancialmarkets.

• Thefirstgroupiscommonlyreferredtoaslenders,thesecondgroupiscommonlyreferredtoastheborrowersoffunds.

6

Featuresofaneffectivefinancialsystem

• Financialtransactionsarebasedontrust

• Stronglegalinfrastructure

• Safe,reliableandefficientpaymentsystem

7

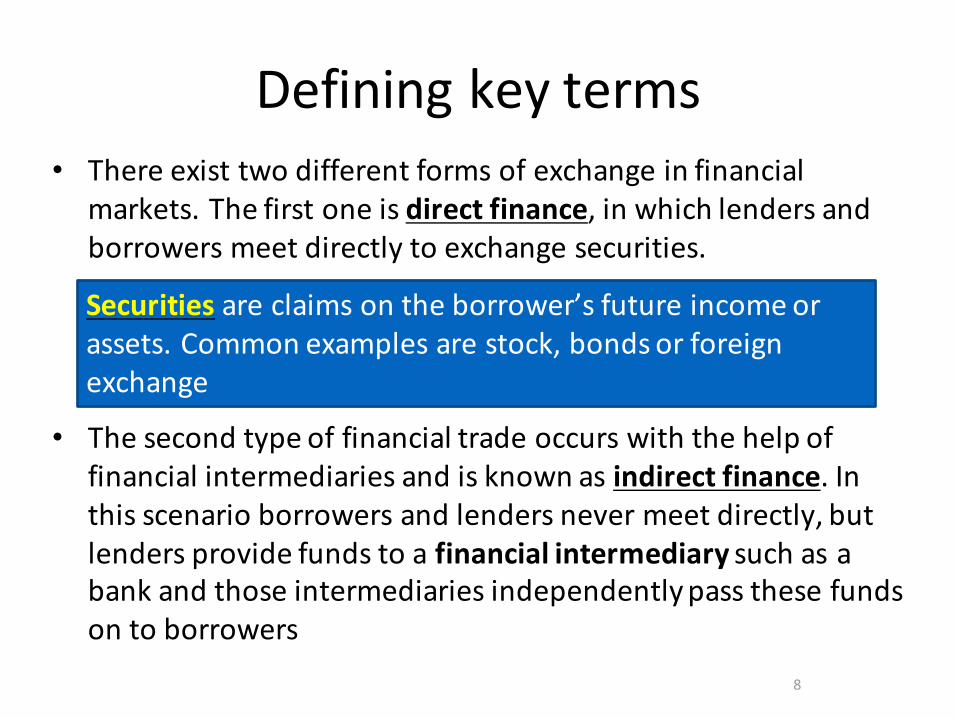

Definingkeyterms• Thereexisttwodifferentformsofexchangeinfinancial

markets.Thefirstoneisdirectfinance,inwhichlendersandborrowersmeetdirectlytoexchangesecurities.

• Thesecondtypeoffinancialtradeoccurswiththehelpoffinancialintermediariesandisknownasindirectfinance.Inthisscenarioborrowersandlendersnevermeetdirectly,butlendersprovidefundstoafinancialintermediarysuchasabankandthoseintermediariesindependentlypassthesefundsontoborrowers

Securities areclaimsontheborrower’sfutureincomeorassets.Commonexamplesarestock,bondsorforeignexchange

8

Anoverviewofthefinancialsystem

Source:Mishkin &Eakins(2015) 9

Definingkeyterms (cont.)• Asset:Anypossessionthathasvalueinanexchange.

– Tangibleassets:Itsvaluedependsonparticularphysicalproperties:Ex.buildings,land,machinery,…

– Intangibleassets:Legalclaimstosomefuturebenefit(itsvaluebaresnorelationtotheform,physicalorotherwise,inwhichtheseclaimsarerecorded):Financialassets/instruments

• Issuer (ofthefinancialinstrument):Entitythathasagreedtomakefuturecashpayments.

• Investor:Ownerofthefinancialinstrument.

10

ExamplesoffinancialinstrumentsContext Issuer Investor Termsoftheloan

AloanbyBNP Theindividualwhobuysacar

Commercialbank

Specifiedpaymentsovertime=repaymentoftheloan+interest

Abond issuedbytheFrenchgovernment

Frenchgovernment

Buyerofthebond

Interestpaymentseverysixmonth tillmaturitydate->amountborrowed

Abond issuedbyTotalInc.

Corporation Sameasabove!

Abond issuedbythegovernment ofAustralia

Acentralgovernment

Sameasabove!

AshareofcommonstockissuedbyL’Oréal

Corporation Receivedividends+aclaimtoaproratashareofthenetassetvalueincaseofliquidation

AshareofcommonstockissuedbyToyotaMotorCorporation

TheJapaneseCorporation

Sameasabove!

11

Definingkeyterms(cont.)• Globallywecanidentify2typesofFinancialinstruments(identifiedbytypeofclaimthattheholderhasontheissuer):

1. Debtinstrument:Theissueragreestopayinterestandrepaytheamountborrowed

2. Equityinstrument:Obligatestheissuerofthefinancialinstrumenttopaytheholderanamountbasedonearnings,ifany,aftertheholdersofthedebtinstrumentshavebeenpaid.Ex:commonstock,apartnershipshareinabusiness

12

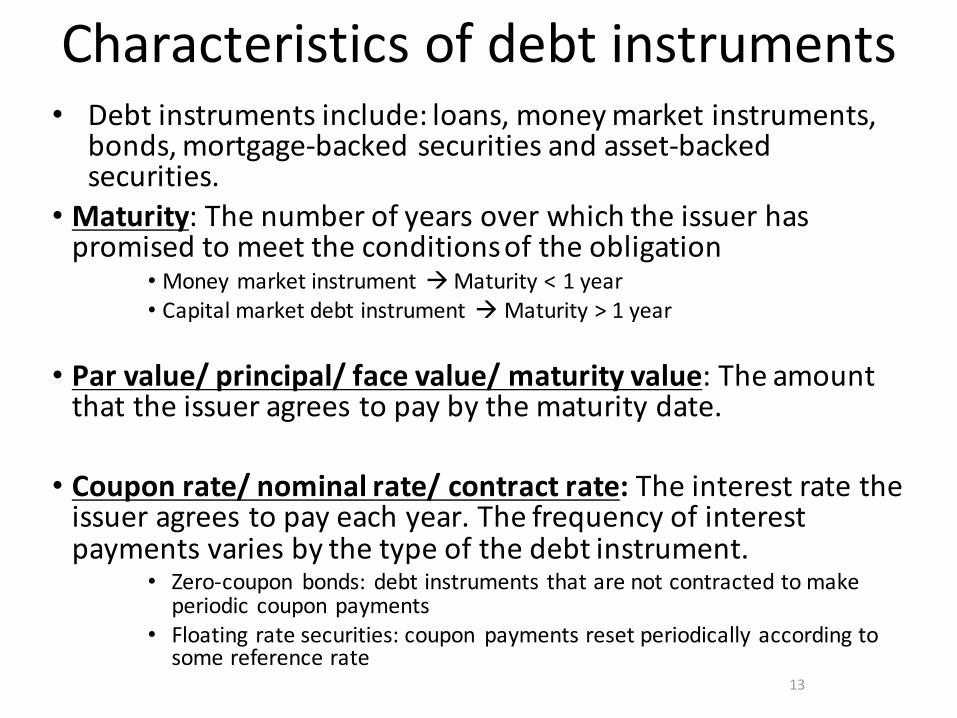

Characteristicsofdebtinstruments• Debtinstrumentsinclude:loans,moneymarketinstruments,

bonds,mortgage-backedsecuritiesandasset-backedsecurities.

• Maturity:Thenumberofyearsoverwhichtheissuerhaspromisedtomeettheconditionsoftheobligation

• MoneymarketinstrumentàMaturity<1year• CapitalmarketdebtinstrumentàMaturity> 1 year

• Parvalue/principal/facevalue/maturityvalue:Theamountthattheissueragreestopaybythematuritydate.

• Couponrate/nominalrate/contractrate:Theinterestratetheissueragreestopayeachyear.Thefrequencyofinterestpaymentsvariesbythetypeofthedebtinstrument.

• Zero-coupon bonds:debtinstruments thatarenotcontractedtomakeperiodiccouponpayments

• Floating ratesecurities:coupon paymentsresetperiodicallyaccordingtosomereferencerate

13

Definingkeyterms(cont.)• Financialmarkets:Wherefinancialinstrumentsareexchanged

3majoreconomicfunctions• Interactionofbuyerandsellersdeterminethepriceoftradedasset(pricediscoveryprocess)

• Amechanismforaninvestortosellafinancialinstrument(offeringliquidity)

• Reducingthetransactioncosts– Searchcost :Ex.advertising– Informationcost:tocalculatethemeritsofafinancialinstrument

14

Classificationoffinancialmarkets1. Type offinancialclaim

• Debtmarkets• Equitymarkets

2. Maturity oftheclaim• Moneymarket• Capitalmarkets

3. Issuance:• Primarymarket (newlyissued)• Secondarymarket (previouslyissued)

4. Time ofthetransaction:• Cashmarket• Derivativesmarket(Thecontractholderbuysorsellsafinancial

instrumentatsomefuturetime)5. Organizational structure:

• Auctionmarket/organizedExchange• Over-the-countermarket 15

Debtvs.Equity• Debttitlesarethemostcommonlytradedsecurity.Inthese

arrangements,theissuerofthetitle(borrower)earnssomeinitialamountofmoney(suchasthepriceofabond)andtheholder(lender)subsequentlyreceivesafixedamountofpaymentsoveraspecifiedperiodoftime,knownasthematurityofadebttitle

• Debttitlescanbeissuedon:– shortterm(maturity<1yr.)– longterm(maturity>10yrs.)– intermediateterms(1yr.<maturity<10yrs.)

• Theholderofadebttitledoesnotachieveownershipoftheborrower’senterprise

• Commondebttitlesare bondsormortgages16

Debtvs.Equity(cont.)• Themostcommonequitytitleis(common)stock

• Anequityinstrumentsmakesitsbuyer(lender)anowneroftheborrower’senterprise

• Formallythisentitlestheholderofanequityinstrumenttoearnashareoftheborrower’senterprise’sincome,butonlysomefirmsactuallypay(moreorless)periodicpaymentstotheirequityholdersknownasdividends.Oftenthesetitles,thus,areheldprimarilytobesoldandresold

• Equitytitlesdonotexpireandtheirmaturityis,thus,infinite.Hencetheyareconsideredlongtermsecurities

17

Debtvs.Equity(cont.)Twoformsofequitymarket:

1)Publicequitymarket(sharemarkets/stockexchanges):Wherecompanieslist theirsharesfortradingpurposes.Totalvalueofthecompany’soutstandingsharesàMarketCapitalization (Ex:acompanywith100millionshares&eachsharehasamarketvalueof10$àcap.=?) Investorsreceivedividends

2)Privateequity:Sharesarenotlistedonapublicmarket,theyaresolddirectlytotheinvestors

18

Moneymarketsvs.capitalmarkets• Moneymarketsaremarketsinwhichonlyshorttermdebt

titlesaretradedEx:Banker’sacceptances,commercialpaper,governmentbills

withshortmaturities

• Capitalmarketsaremarketsinwhichlongerterm debtandequityinstrumentsaretraded:Bondmarkets:Ø EnableInc.orgov. toborrowdirectlyfrominvestorsinthecapital

markets)Ø Regularstreamofincomepaymentsthroughcoupons.(interest

payments)Ø Paymentofthedebt’sprincipal uponmaturity

19

20

Primarymarketvs.secondarymarkets• Primarymarketsaremarketsinwhichfinancialinstruments

arenewlyissuedbyborrowersØ Theyarenotveryknowntothepublic(sellingbehindcloseddoors)Ø Animportantinstitution:investmentbanks

• SecondarymarketsaremarketsinwhichfinancialinstrumentsalreadyinexistencearetradedamonglendersØ Ex:TheNewYorkStockExchangeØ Ex:NASDAQ

Themagnitudeofthecouponissetatthetimeofissuanceà Fixedinterest

Inthesecondarymarkets,afallinthepriceofthebondresults inanincreaseintherateofinterest,oryield paid.

21

Cashvs.Derivativesmarket

Derivativesmarkets:2typesofbasicinstruments:

» Futures/forwardcontract:transactionofafinancialinstrumentatapredeterminedpriceataspecifiedfuture.

»Optioncontract:Ownerofthecontracthastherightbutnottheobligationtobuy/sellafinancialinstrumentataspecificpricefromanotherparty.

• Toolsforhandlingoffinancialrisk:Derivativescanbeusedforanumberofpurposes,includinginsuringagainstpricemovements(hedging),increasingexposuretopricemovementsforspeculationorgettingaccesstootherwisehard-to-tradeassetsormarkets.

Timeofthetransaction!

22

Exchangevs.over-the-countermarkets• Secondarymarketscanbeorganizedas:

Ø OrganizedExchange,inwhichbuyersandsellersofsecuritiesmeetinonecentrallocation,suchasastockexchange(Avisiblemarketplaceforsecondarymarkettransactions)

ØOver-the-counter(OTC)marketsinwhichdealersatdifferentlocationswhohaveaninventoryofsecuritiesstandreadytobuy&sellsecuritiestoanyonewhocomestothem.(Atelecommunicationnetwork)üTitlesaresoldinseverallocationsüVerycompetitivesinceOTCdealerareincomputercontactandknowthepricessetbyanother

23

Nationalorinternational?

• Capitalandmoneymarkets National

• Forex andderivativesmarkets International

FXmarkets:(Foreignexchangemarket/Forex)Amarketfortradingcurrenciesinternationally

24

• Internationalizationofthefinancialmarketsà importanttrend

• Americancorporationsarenowmorelikelytotapinternationalcapitalmarketstoraisefunds

• Foreignersbecomeimportantinvestors(inUS,France,…)

25

InternationalBondMarket• Foreignbonds:aresoldinaforeigncountryanddenominatedinthatcountry’scurrencyEx:ifPorschesellsabondinUSdenominatedin$àforeignbond

• Foreignbondhavebeenanimportantinstrumentforcenturies:alargepercentageofUSrailroadsbuiltisthe19th centurywerefinancedbysalesofforeignbondsinBritain

• Arecentinnovationintheinternationalbondmarket:Eurobond 26

• Eurobonds:AbondissuedinacurrencyotherthanthecurrencyofthecountryormarketinwhichitisissuedEx:AbondthatisdenominatedinU.S.dollarsandissuedinJapanbyanAustraliancompany

• AvariantoftheEurobondàEurocurrencies:foreigncurrenciesdepositedinbanksoutsidethehomecountry

• ThemostimportantEurocurrenciesareEurodollars:US$depositedinforeignbanksoutsidetheUS

AbonddenominatedineurosiscalledaEurobondonlyif itissoldoutsidethecountriesthathaveadoptedtheeuro

27

Commercialfinancialinstitutions• Commercialbanks:

• Investmentbanks:

• Universalbanks:

• Mortgagebanks:

• Contractualsavings:

• Assetmanagementcompanies:

• Venturecapitalists/Privateequitycompanies:

28

Commercialfinancialinstitutions• Commercialbanks:Takedepositfrompublicandlendto

individualsandcorporateborrowers.ü Differencebetweentheinterestratepaidtosaversandthatchargedto

borrowers Spreadü Thesebankstransformshorttermliabilitiesintolongtermassets

• Investmentbanks:Financialservicesthataregenerallyrelatedtothebusinesses(findingandstructuringvariousformsoffinance,issuanceofcorporatebonds,arrangementofmergersandacquisitions,…)

• Universalbanks:Combinefunctionsofcommercialandinvestmentbanks

29

• Mortgagebanks:Providefinanceforthepurchaseofproperty.

• Contractualsavings:Institutionssuchaspensionfundsandinsurancecompanies.

Assetmanagement:Ø In-houseØ Out-sourced

• Assetmanagementcompanies:provide“Portfoliomanagement”servicesbyaccessingpublicandprivatefinancialmarkets

• Venturecapitalists/Privateequitycompanies:ProvidecapitalforneworexpandingbusinessInthelast2decades,wehaveseenaconsiderabledestructionofthe‘functionalboundaries’betweendifferenttypesofbankandnon-bankfinancialinstitutions. 30

Quasi-commercialfinancial institutions

• Statedevelopmentbanks:Ownedbygovernments,directcredittoprioritiesofthegovernment.

• Mutualcooperativebanks:Collectivelyownedbytheirmembers.(higherinterest,lowercharges)

• Postofficesavingsbanks:Basicfinancialservices(lowincome)

• Creditunions:Ownedbytheirmembers,creditgrantedtomembersonlowincomes

• Microfinanceinstitutions:Providingthepoorwithaccesstofinancialservices,informofbank,cooperative,creditunionetc.

31

Governmentalfinancialinstitutions• Centralbanks:Havethemonopolyoffiatmoney

issuance.– Provideliquidity(controlmoneysupply)– LOLR:actasalender-of-lastresorttothedomesticbankingsystem

Mainfeatures:ØNationalpaymentsandsettlementsystemØ Prudentialregulation/supervisionØ InsurancefordepositsØ Executemonetarypolicyà inflationtargetingØ Exchangeratepolicy

32

TypesoffinancialIntermediaries

1. Depositoryinstitutions:Financialintermediariesthatacceptdepositsfromindividualsandinstitutionsandmakeloans.

2. Contractualsavingsinstitutions:Financialintermediariesthatacquirefundsatperiodicintervalsonacontractualbasis.

3. Investmentintermediaries

33

34

Financial

Intermediaries

Contractual savings

Institutions

Investment Intermedari

es

Depository Institutions

Commercial Bank

Mutual Funds (Investment Funds)

Finance Companies

Pension Funds

Credit Unions

Insurance Companies

Savings and Loans Associations (S&L)

Mutual Saving Banks

Money market Mutual Funds

Specialized Banks

35

36

Howdofinancialmarketsdifferfromothermarkets?

Timeandmanagementofrisk• Deliveryinfutureasopposedtothepresent,futureis

uncertainà Riskyà interestpayment(timevalueofamoney)

• Transfersacrosstime:smoothingconsumptionandinvestment

• Transferandmanagerisk• Creditrisk:dangerofdefault• Marketrisk:lossbysuddenchangesinassetprices• Liquidityrisk:unabletosellassetsquicklywithoutloss• Systemicrisk:contagionfromanotherbank

37

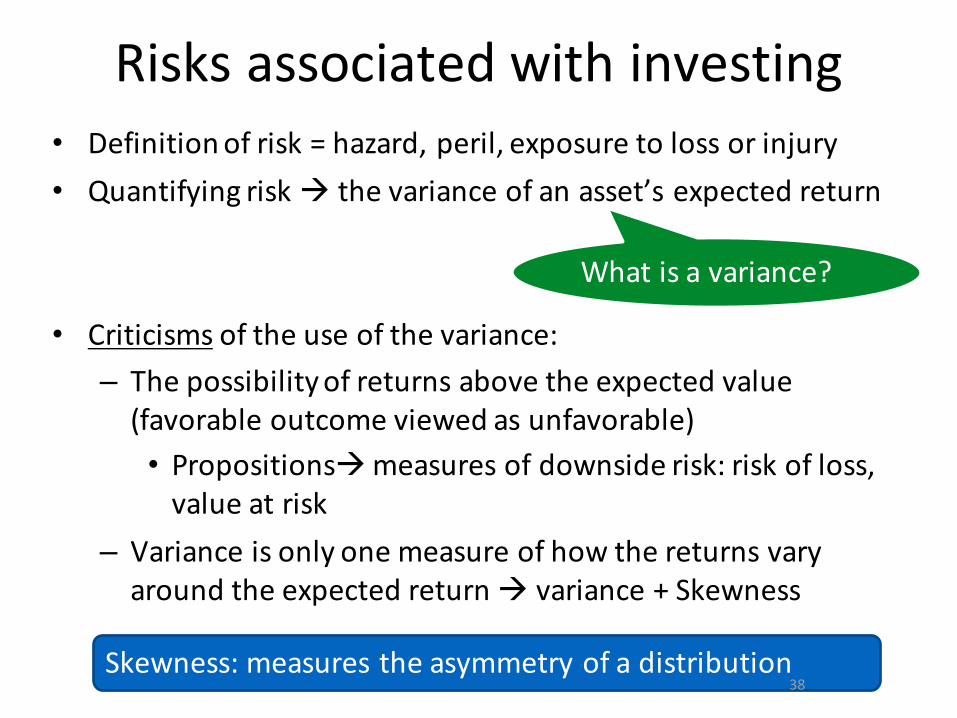

Risksassociatedwithinvesting• Definitionofrisk=hazard,peril,exposuretolossorinjury• Quantifyingriskà thevarianceofanasset’sexpectedreturn

• Criticisms oftheuseofthevariance:– Thepossibilityofreturnsabovetheexpectedvalue(favorableoutcomeviewedasunfavorable)• Propositionsàmeasuresofdownsiderisk:riskofloss,valueatrisk

– Varianceisonlyonemeasureofhowthereturnsvaryaroundtheexpectedreturnà variance+Skewness

What isavariance?

Skewness:measurestheasymmetryofadistribution38

Mainrolesofthefinancialsystem(Levine,2005)

1. Producinginformationandallocatingcapital:

Ø Largecostsof:Evaluatingfirms,managersandmarketconditionsàHighinformationcostsmaykeepcapitalfromflowingtoitshighestvalueuse

Ø Improveresourceallocation

Ø Leadstoamoreefficientallocationofcapital

39

Mainrolesofthefinancialsystem(cont.)

2. Monitoringfirmsandexertingcorporategovernance:

Ø Shareholdersmayexerteffectivegovernancedirectly byvotingoncrucialissues(mergers,liquidations,…)orindirectly byelectingboardsofdirections.

Ø Wellfunctioningstockmarkets:Linkingstockperformancetomanagercompensationhelpsaligntheinterestofmanagerswiththoseofowners

Ø Debtcontracts:reducetheamountoffreecashavailabletofirmsà reducesmanagerialslackAcceleratestherateofadoptionofnewtechnologies

40

3.Riskamelioration:Ø Cross-sectionalriskdiversification:high-returnprojectstendtoberiskierthanlow-returnprojectsà financialmarketsmakeiteasierforpeopletodiversifyriskandshiftportfoliostowardshigherexpectedreturns.

Ø Intertemporal risksharing:Someriskscannotbediversifiedataparticularpointintime,suchasmacroeconomicshocks,theycanbediversifiedacrossgenerations.Long-livedintermediariescanfacilitateintergenerationalrisksharingbyinvestingwithalong-runperspective.

41

ØLiquidityrisk:Liquidityreflectsthecostandspeedwithwhichagentscanconvertfinancialinstruments intopurchasingpoweratagreedprice.Liquidityrisk uncertaintiesassociatedwithconvertingassetsintoamediumofexchangeLinkbetweenliquidityandeconomicdevelopment:High-returnprojectsrequirealong-runcommitmentofcapital,notsavors’favorite!(Ex.Industrialrevolutionandliquidcapitalmarketsin18thcenturyinEngland)

Anotherformofliquidity:accesstocreditduringtheproductionprocess

42

4.Mobilizeandpoolsavings:

Ø Theprocessofagglomeratingcapitalfromdisparateinvestorsiscostly

Ø Financialarrangementsthatmobilizesavingsfrommanydiverseindividualsandinvestinadiversifiedportfolioofriskyprojectsfacilitatereallocationofinvestmenttowardhigherreturnactivitieswithpositiveeffectsoneconomicgrowth.

43

5.Easetheexchangeofgoodsandservices

Ø Financialarrangementslowertransactioncost

ØMorespecializationrequiresmoretransactions,sinceeachtransactioniscostlyà financialdevelopmentleadstomorespecialization àpositiveimpactongrowth

44

Roleoffinancialmarkets:aSummary

• Althoughinapureneoclassicalframeworkthefinancialsystemisirrelevanttoeconomicgrowthinpracticeanefficientfinancialsystemcan:

• Lowerthecostofexternalborrowing• Raisethereturntosavors• Ensurethatthesavingsareallocatedtoprojectsthatpromisehighestreturns

45

Financialsectorandthegovernment

• Governmentsregulate theactivitiesofthefinancialsystem

• Governmentsborrowfromthefinancialsystem:issuanceofsovereignbonds

• Governmentsmaytakemoredirectroleinthesystem:Intervenedirectlyinthefunctioningofthesystem,e.g.directingtheallocationofcreditthroughdevelopmentbanks,owningorcontrollingasectionofacommercialbank

46

Shouldit?Towhatextent?

Marketorgovernment:Somehistory• BeforeKeynes:Althoughmarketscanfailthesefailuresare

justanomalouseventsà PeriodoffreecapitalmovementsOptimismaboutthenatureandroleoffreemarkets

47

• Keynes(1936):imperfectionsareinherentinmarketsandthereisnonaturaltendencytowardstheproductionofoptimaloutcomesà Toensurethedesirableoutcomesofhighlevelsofgrowthandemployment,governmentsshouldnecessarilyinterveneintheeconomy.

• (WithouttheGreatDepressionKeynesviewswouldnothavetheimpactthattheydid!)

48

49

50

• IrvingFisher,thegreatdepressionandBrettonWoods:

Ø Anotherstrandofthoughinthisperiod:viewingfinancialcrisisasanintegralpartofthebusinesscycle(notanomaliesorrationalresponsetodeterioratingeconomiccircumstances)

51

Ø Fisher(1933)attemptedtodeterminetherootcauseoftheGreatDepressionà Acrucialfactor:levelofdebtintheeconomy§ Upswingsintheeconomyencourageincreasingdebtlevels(appearanceofgreaterinvestmentopportunities)

§ Higherinvestmentà higherdebtà growthofspeculationinassetmarket(gainsthroughrisingassetprices)à raiseininflationrate(increaseinborrowingincreasesmoneysupply)àreducesthevalueofdebtàencouragingmoreborrowing

§ Atacrucialpoint:CRISISà borrowersarenolongertomeettheirliabilities,theyliquidatetheirassets(distressselling)à deflationà debtincreasesà fearofbankinsolvencyàbankrunsà activitydeclinesàunemploymentrises 52

• IrvingFisher,thegreatdepressionandBrettonWoods(cont.):

Ø TheGreatDepression(1929-1939),shookpeople’sfaithintheabilityoffreefinancialmarketstodeliveroptimaloutcomes.

Ø BrettonWoodsinNewHampshirein1944:§ Representativesof44countries§ Aim:toconstructaninternationaleconomicsystemthatwouldreduce

theinstabilityofthefinancialsystem§ Thesereformscausedlongperiodofstability§ Currenciesholdingtotheirpeg§ Internationalmovementofcapitalwasgreatlyrestricted§ Keynesarguedthatcapitalcontrolsshouldbeobligatoryonall

countriesà IMFwouldallowsuchcontrolsbutnotinsistsuponthem

53

54

• Structuralism:

Ø Destructionofmarketswasnotlimitedtoindustrialcountries

Ø InLatinAmericathestructuralismdevelopedwithintheEconomicCommissionforLatinAmerica(ECLAC)in1947§ Structuralist approach:“center-periphery”paradigm:UnequalnatureoftheworldeconomicsystemTheindustrialrevolutionin“center”à increasetheproductivityofthefactorsofproductionDevelopingcountries,“periphery”,havetoexportmoreandmorethesefactors(commodities)tobeabletoimportthesamequantityofcapitalgoodsà trappedincommodityproductionandexporttoservethecenter

55

• Structuralism(cont.):

§ “Import-substitutionindustrialization”/ISM:Hightariffsonindustrialimports,exceptforessentialhigh-techcapitalgoods

Aim:movetheeconomyontoavirtuouscircleofindustrialization,risingproductivity,wagesandemployment.

§ Encouragecapitalinflowstofundthisdevelopment§ Criticismin60s:keyindustrializingsectorscontrolledbyforeigninvestors

§ Sweptawayin70s:authoritarianmilitaryregimesandmonetaristpolicies

56

• Monetarismandreturnoffaithinmarkets:Ø Kindleberger (1978)distinguished2differentschoolsofthoughts:modernschoolsofmonetarismandKeynesianism(Currencyschool vs.Bankingschool)

ØCurrencyschool:ControlthemoneysupplyØBankingschool:Expandit

Ø Monetarists:Moneysupply(M)isexogenoustorealincome(Y),prices(P)andinterestrate(R)i.e.anincreaseinMà increaseinPbutnochangetoYFaithinabilityoffreemarketsandpriceadjustmentmechanismandlittlefaithinstate’sabilitytotakethisrole

Ø Keynesians:“quantitytheoryofmoney”:increasingMcouldincreaseY,Misendogenousandaresponsetocreditneeds

ØDominanceofeachschoolindifferentperiodsØPost-war:BankingschoolØ1970s:collapseofthefixedexchangeratesàMonetarist

57

• Neo-liberalism:Ø ChicagoSchoolofEconomics:efficiencyofmarketsandfree

competitionvs.governmentinterventionsinmarketsthatdistortmarketsandpreventoptimaloutcome

Ø Noneedforgovernmenttointerveneintheeconomytoensurefullemployment,inafreemarketsituationpriceswilladjusttoensurethatallfactorsofproductionareemployed

ØMarketsautomatically adjusttofullemploymentmonetaryorfiscalpolicymerelycreateinflation

Ø ElectionofMargaretThatcher(1979)andRonaldReagan(1980)à ideologicalperspectivecametothefore

Ø Neverthelessearlypuremonetaristpoliciessuchascontrolforthemoneysupplyweresoonabandoned 58

• Neo-liberalism(cont.)Ø Relevantdomesticpolicyproposals

Ø Thederegulation ofdomestic financialmarketsØ PrivatizationØ Reduction inthepoweroftradeunionsØ SmallergovernmentØ LowertaxratesØ Opening theinternationalgoodsandcapitalmarkets

Ø In1990,thebirthadriseofthe“WashingtonConsensus”:Ø PrivatizationØ FreetradeØ Export-ledgrowthØ FinancialcapitalmobilityØ Deregulated labormarketsØMacroeconomicprudence

Ø Interventioninmarketsisusuallycounterproductive;regulationsshouldbelightandmarketsshouldbefreed

59

• Financialfragility,uncertaintyandasymmetricinformation

ØKindleberger (1978)distinguishedbetween“upswings”(maniabehavior)and“downturns”(panicbehavior)intheeconomy

ØInupswingà demandforcreditincreasesà riseinbankloansà assetpricesriseà encouragemoreborrowingà thebubble expands

ØDistinguish:ØInsiders:areawareofthesituation,selloutatthetopofthemarket

ØOutsiders:attractedbythemania60

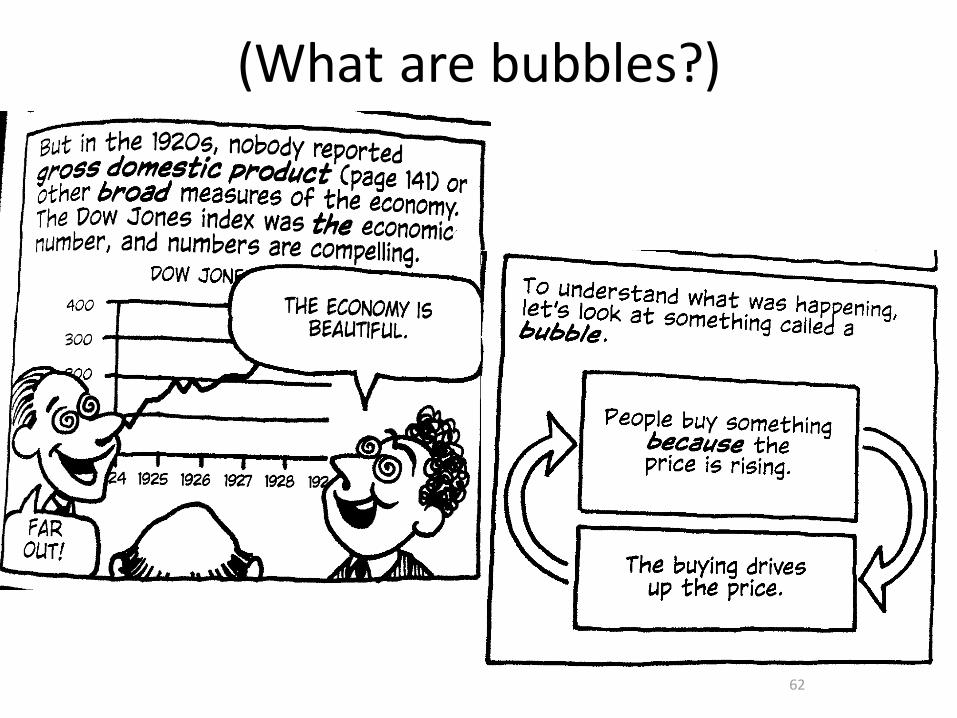

• Financialfragility,uncertaintyandasymmetricinformation(cont.)

ØBubblecancontinuetoexpandifoutsidersoutnumberinsidersà atsomepoint:Periodof“distress”whennatureofbubbleisrecognizedandinfluxofoutsidersceaseà untilsometriggersetsoffapanicandinvestorsrushtowithdrawtheirfunds(likeabankrun)

ØE.g.dotcomboomoflate1990sortheDutchTulipmaniain1637(Atthepeakoftulipmania,inMarch1637,somesingletulipbulbssoldformorethan10timestheannualincomeofaskilledcraftsman!!!!)

61

(Whatarebubbles?)

62

63

64

65

• Financialfragility,uncertaintyandasymmetricinformation(cont.)

Ø Keynes(1936):FutureisinevitablyuncertainThereisnowaytodeterminethevalueofatrueassetintoday’smarketà thetruevalueisthediscountedfutureprofitsàtheseprofitscannotbeknown

Ø Davidson(1998):Agentsanalyzepastandpresentmarketdatainformingrationalexpectationsasabasisformakingutilitymaximizingdecisionsà awaytoobjectivelyobtain“fundamentalprice”thatthemarketcanconvergeon

Ø Allnewinformationisinstantlydiscountedintothecurrentmarketpriceà nopossibilityofspeculativeprofit,boomsandcrashes! 66

• Financialfragility,uncertaintyandasymmetricinformation(cont.)

Ø Newstrandoftheoryin1980s:Asymmetricinformation(JosephStiglitz - Nobelprize):lendersandborrowersdonothaveaccesstoequalinformation(usuallyborrowersarebetterinformed!)

67

• Financialfragility,uncertaintyandasymmetricinformation(cont.)

ØMishkin (1996):2problemsofasymmetricinformation:ØAdverseselection(beforethetransactionoccurs):Indebtandequitymarketslendershavenowaytodistinguishgoodborrowersfrombadonesà thepricetheyarewillingtopayrepresentsthequalityofthefirmbutlow-qualityfirmswillbeeagertoissuesecuritiesatapricethatinflatestheirvalueandhigh-qualityfirmsareunwillingtoissuesecuritiesataverageprice.

ØMoralhazard (afterthetransactionoccurs):Theborrowerhasanincentivetoengageinhigh-riskstrategies.

– Banksarelesssubjecttoasymmetricinformationproblemsthansecuritiesmarketsà relationshipwiththecustomersandknowledgeoflocalmarket

68

• Returnofpsychologyandbehavioralfinance:Ø Foundationoffinancialtheory:assumptionofrational,utility-maximizingagentsà banishpsychologyfromthestudyofeconomicbehavior

Ø 1970sPioneersbehavioraleconomists:Ø AmosTversky,Ø DanielKahneman

ØActualbehaviorsystematicallyviolatesthepreceptofrationaloptimizingbehaviorà theseanomaliescouldbepredicted

Ø Supportersofmarketefficiency:deviationsfromrationalbehaviorarerandomanduncorrelated

ØNewschoolofthough“Behavioralfinance”:peopleemploypsychologicalshort-cutsintheirdecisionmaking.

69

• Returnofpsychologyandbehavioralfinance(cont.)Ø Someconceptsofbehavioralfinance:Emotionsareakey

driverofaperson’sbehavior.Peoplehavebeenshowntobelossaverse,generallyappearingtodislikelosingsomethingroughlytwiceasmuchastheylikegainingit.

Ø Prospecttheory(Kahneman &Tversky):

70

References• “DevelopmentFinancedebatesdogmasandnewdirections”-

StephenSpratt(2009)

• Financeandgrowth:theoryandevidence– RossLevine(2005)

• Financialmarketsandinstitutions– Mishkin&Eakins(8thedition,2015)

• Handbookoffinance(2008)Volume1- Chapter1

• Economix:HowOurEconomyWorks(andDoesn'tWork)byMichaelGoodwin

71