Research Bulletin - :: Gulf One Bank · Research Bulletin December 2008 ... • Cost-plus trade...

22

Research Bulletin December 2008 Islamic Finance: Opportunities and Challenges 1

Transcript of Research Bulletin - :: Gulf One Bank · Research Bulletin December 2008 ... • Cost-plus trade...

Research Bulletin December 2008

Islamic Finance: Opportunities and Challenges

1

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 2

Gulf One Investment Bank B.S.C. (c) is a Bahrain registered bank whose vision is to be the leading knowledge-based infrastructure investment bank in the MENA (Middle East and North Africa) region. Its mission is to mobilise local and global capital to accelerate the execution of infrastructure projects via innovative custom made financial solutions. This Research Bulletin has been prepared by staff in the Research Department of Gulf One Investment Bank B.S.C. (c) under the general direction of Dr. Nahed Taher, Founder & CEO of Gulf One Investment Bank. The research team comprises: Dr. Mohammed Salisu Chief Economist Gulf One Investment Bank E-mail: [email protected] Ms. Lobna Bousrih Research Analyst Gulf One Investment Bank [email protected] Ms. Sana Harrabi Research Analyst Gulf One Investment Bank [email protected] All comments and enquiries about this Bulletin should be sent to Dr. Mohammed Salisu at the above mentioned e-mail address. ________________________________________________________________________Disclaimer This research bulletin was prepared by Gulf One Investment Bank B.S.C (c), (“Gulf One”) and is of a general nature and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive or to address the circumstances of any particular individual or entity. This material is based on current public information that we consider reliable at the time of publication, but it does not provide tailored investment advice or recommendations. It has been prepared without regard to the financial circumstances and objectives of persons and/or organisations who receive it. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. In addition, the views expressed in this bulletin do not necessarily represent the views of the Management or Board of Directors of Gulf One Investment Bank. This bulletin or any portion hereof may not be reprinted, sold or redistributed without the prior written consent of Gulf One.

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 3

Overview Islamic finance has emerged from the current global financial crisis relatively unscathed largely due to the fundamental principles that govern its operations, such as profit and loss sharing schemes, assets-backed securities, interest-free transactions, and prohibition of speculative activities. Thus, the intrinsic nature of Islamic finance encourages risk management and transparency, which together with the prescribed Islamic injunctions, can play an important role in shielding Islamic finance industry from risks of financial distress associated with excessive leverage and speculative investments that have, for long, bedevilled the global financial system. This can be attested to not just from the present financial crisis but also from previous financial crises, such as the 1997/98 Asian financial crisis, where Islamic financial institutions weathered the storm with relative ease and alacrity. So, what explains the resilience of Islamic finance? The answer lies in the ‘ethical’ nature of Islamic finance. By prohibiting interest-based transactions and speculations and sanctioning assets-backed activities, Islamic law provides a credible basis for wealth creation by linking credit expansion to growth of the real economy, leading to sustainable economic prosperity, equity and social justice. Tying financial transactions to tangible, identifiable underlying assets and interest-free arrangements can eliminate excessive debt obligations and debt burdens. The recent cuts in interest rates to near-zero levels in the US, Japan, and Europe as a panacea for the current financial crisis provide a tacit acknowledgement of the ills of interest-based financing, and thereby provide support to Islamic finance as a credible and viable alternative financing mechanism. Needless to say, therefore, the current global financial crisis has opened a window of opportunity for Islamic finance to blossom, expand beyond its niches and mainstream itself into the global financial system. However, such transformational objectives can only be achieved through innovation and profound changes in mindsets as well as in legal, institutional, and regulatory environments. This is because despite recent floatation of new Islamic products, critics argue that many of the so-called Islamic finance institutions offer products that are hardly distinguishable from those offered by their conventional counterparts. For example, some of the innovative products such as ‘Islamic derivatives’ and ‘Islamic credit cards’ are not only carbon copies of conventional products but they also raise unnecessary controversies regarding their Sharia-compliant characteristics. Similarly, many Islamic finance institutions are increasingly relying on conventional indicators, such as LIBOR (London Inter-Bank Offer Rate – an interest rate), as benchmarks for commissions and service charges. Islamic institutions, particularly Islamic banks, have also been often criticized for inflated margins, over-concentration on a narrow range of sectors, especially real estate, and excessive lending to consumers. There is also the issue of the complex, cumbersome and complicated product approval processes, requiring services of members of the ‘Sharia Boards’, which often tend to unnecessarily slow down Islamic finance deals. Critics have also argued that governments in many predominantly Muslim countries have not been active enough in promoting the growth of Islamic finance. To push Islamic finance to new heights would require active state participation particularly in areas of project financing, creation of a lender of last resort for Islamic finance and provision of financial guarantees, particularly on large-scale capital intensive infrastructure projects. Clearly, there are challenges as well as opportunities for Islamic finance, and so the key questions are: What can be done to maximize the opportunities and mitigate the challenges? In other words,

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 4

how can Islamic finance institutions use their relative strengths and the current windows of opportunities to overcome their weaknesses and potential threats? Can Islamic finance compete effectively with conventional finance? Can it on its own address the overwhelming infrastructure investment requirements that exist in the Gulf Cooperation Council (GCC) countries? The answers to these and other issues relating to modus operandi, size, composition, and mainstreaming of Islamic finance constitute the subject matter of this research bulletin. Modus Operandi of Islamic Finance Islamic finance involves a set of financial contractual relationships that are governed by Islamic law (Sharia) derived from the Holy Qur’an and the sayings and deeds of Prophet Muhammad1 (Sunnah) as well as Islamic jurisprudence (fiqh). The rules and regulations governing Islamic finance encompass both legal and ethical dimensions of Islamic law. One such element of Islamic law is the prohibition of interest or usury (riba) as making money from money is not permitted. Wealth is, however, allowed to be created through trade and investment activities. Islamic law also prohibits risk-free returns, gambling/betting (maisir), and preventable uncertainty (gharar) such as financial derivative instruments. Similarly, Islamic law forbids speculation including exchange of money for debt without an underlying asset transfer. Finally, Islamic law involves prohibition of activities that are considered to be sinful (haram), such as alcohol and pork products. These principles, particularly the prohibition of interest, have necessitated the use of a variety of alternative modes of finance. It is noteworthy that engaging in interest-free transactions does not mean that capital is costless in an Islamic financial system. On the contrary, Islam recognises the important role played by capital in the production process and it encourages capital owners to invest their money and earn profits arising from the business outcomes. What Islamic law frowns at, however, is the fixing of a pre-determined amount for the use of capital2. This means that Islamic finance encourages risks taking and investment of capital in profit-making ventures without recourse to charging interest, which economists regard as the rental cost of capital. Under Islamic finance, there are a number of trade and investment schemes to which capital could be deployed to yield undetermined rates of return. The principal modes of capital deployment in an Islamic finance paradigm include the following:

• Joint ventures involving profit and loss sharing (PLS) schemes (Musharaka) • Financial arrangements involving principal-agent relationship based on profit-sharing and

ingredients of social capital, especially trust (Mudaraba) • Cost-plus trade financing (Murabaha) • Hire-purchase and sale-leaseback agreements (Ijara) • Contractual relationships based on pre-delivery financing and leasing structures (Istisna) • A host of other modes including forward sales of commodities (Salam), deferred payment

sales, risk-free asset with zero real rate of return (Qardh al Hassan), and agency contracts where an agency performs financial transactions on behalf of a client (Wakala).

1 Peace be upon him. 2 Salahuddin Ahmed, Islamic Banking, Finance and Insurance: A Global Overview (Kuala Lumpur: A S Noordeen publications, 2006).

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 5

These are standard, well known vehicles through which Islamic finance has always operated. They can be grouped into three broad classes: (i) equity and profit sharing, (ii) credit purchase, and (iii) leasing. The first category (equity and profit and sharing) consists of both musharaka and mudaraba instruments, while murabaha and Qardh al Hassan fall into the credit purchase category. The remaining types of Islamic finance can be lumped into the leasing mode. The musharaka scheme (joint ventures) is essentially an equity participation arrangement where all parties to the agreement contribute capital towards the financing of a business, and they share profits or losses on a pro rata basis of their equity contributions. It is generally suited for financing specific projects for limited durations due to the high risks involved. In the case of Mudarabah, it is a profit-sharing scheme that brings together physical capital and human capital, involving capital contribution from an investor and knowledge/management contribution from an entrepreneur. Thus, a mudarabah financing arrangement is similar to equity investment by shareholders in a company. Profit is shared according to a pre-determined ratio but financial losses are solely incurred by the investor, except in cases of wilful negligence on the part of the entrepreneur3. Murabaha (cost-plus financing) is an asset-based sale contract for financing products on deferred payment basis. For example, Islamic finance institution, such as a bank, buys goods on behalf of clients and then sells them to the clients at the original price plus a profit margin to cover the cost of purchase and associated risks. The client, in turn, takes the product and pays the ‘cost-plus’ amount on monthly instalment basis, but the financier retains ownership until full amounts have been paid. It is estimated that around 70 percent of existing Islamic finance funds are deployed in short-term low-risk Murabaha transactions4. A variant of murabaha, often used for longer term contracts, is called Bai Bithaman Ajil (BBA), and is very popular in Asian countries particularly in Malaysia. It is noteworthy that international agencies such as the World Bank have Islamic finance instruments based on the BBA framework. Leasing and hire-purchase financing contracts also feature prominently in Islam finance. In the case of leasing (ijara), the client (lessee) rents the product from the financier (lessor) at an agreed rent, whilst in the case of hire purchase the lessee has the option to purchase the leased assets. Both types of financing are commonly used for longer-term credit facilities for products such as capital equipment and home financing. In case of large-scale project financing, Islamic finance relies heavily on the instrument of istisna, which is a pre-production financing tool for financing activities in areas such as mining and manufacturing industries. It is generally believed that Istisna contracts can provide a suitable financing mechanism of public goods and mega infrastructure projects. In recent years, other modes of Islamic financing have been introduced into the industry, including Islamic securitisation and Islamic derivatives, such as Islamic hedging of currency risk. Islamic securitisation can be an ideal financing instrument for emerging capital markets, such as the GCC. The first ever Islamic securitization took place in December 2003 undertaken by Al Manar Financing and Leasing of Kuwait involving the purchase of retail portfolio of more than 1,000 clients from The Investment Dar worth nearly US$19 million. Since then, a number of Islamic securitisation deals in the Gulf region ensued5. 3 In a mudarabah scheme, the financier (investor) is not permitted to interfere in the running of the business. 4 Salahuddin Ahmed, ibid, p.30. 5 Salahuddin Ahmed, ibid, p.34.

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 6

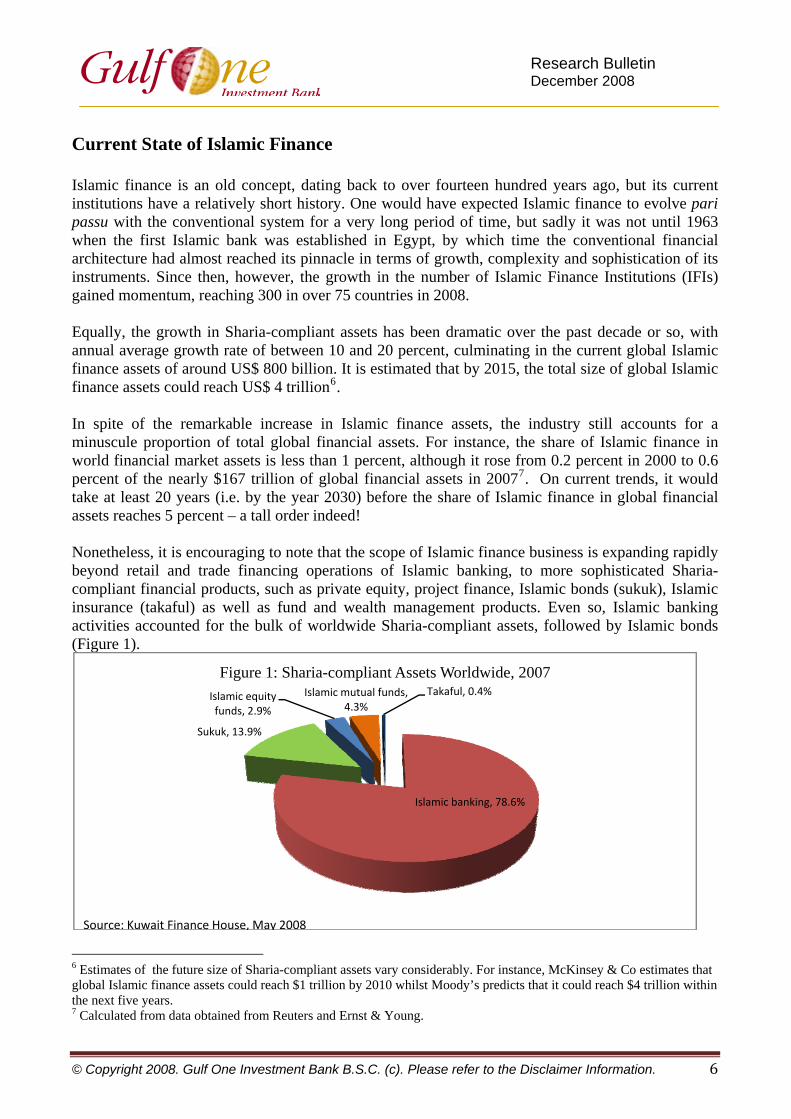

Current State of Islamic Finance Islamic finance is an old concept, dating back to over fourteen hundred years ago, but its current institutions have a relatively short history. One would have expected Islamic finance to evolve pari passu with the conventional system for a very long period of time, but sadly it was not until 1963 when the first Islamic bank was established in Egypt, by which time the conventional financial architecture had almost reached its pinnacle in terms of growth, complexity and sophistication of its instruments. Since then, however, the growth in the number of Islamic Finance Institutions (IFIs) gained momentum, reaching 300 in over 75 countries in 2008. Equally, the growth in Sharia-compliant assets has been dramatic over the past decade or so, with annual average growth rate of between 10 and 20 percent, culminating in the current global Islamic finance assets of around US$ 800 billion. It is estimated that by 2015, the total size of global Islamic finance assets could reach US$ 4 trillion6. In spite of the remarkable increase in Islamic finance assets, the industry still accounts for a minuscule proportion of total global financial assets. For instance, the share of Islamic finance in world financial market assets is less than 1 percent, although it rose from 0.2 percent in 2000 to 0.6 percent of the nearly $167 trillion of global financial assets in 20077. On current trends, it would take at least 20 years (i.e. by the year 2030) before the share of Islamic finance in global financial assets reaches 5 percent – a tall order indeed! Nonetheless, it is encouraging to note that the scope of Islamic finance business is expanding rapidly beyond retail and trade financing operations of Islamic banking, to more sophisticated Sharia-compliant financial products, such as private equity, project finance, Islamic bonds (sukuk), Islamic insurance (takaful) as well as fund and wealth management products. Even so, Islamic banking activities accounted for the bulk of worldwide Sharia-compliant assets, followed by Islamic bonds (Figure 1).

6 Estimates of the future size of Sharia-compliant assets vary considerably. For instance, McKinsey & Co estimates that global Islamic finance assets could reach $1 trillion by 2010 whilst Moody’s predicts that it could reach $4 trillion within the next five years. 7 Calculated from data obtained from Reuters and Ernst & Young.

Islamic banking, 78.6%

Sukuk, 13.9%

Islamic equity funds, 2.9%

Islamic mutual funds, 4.3%

Takaful, 0.4%

Figure 1: Sharia-compliant Assets Worldwide, 2007

Source: Kuwait Finance House, May 2008

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 7

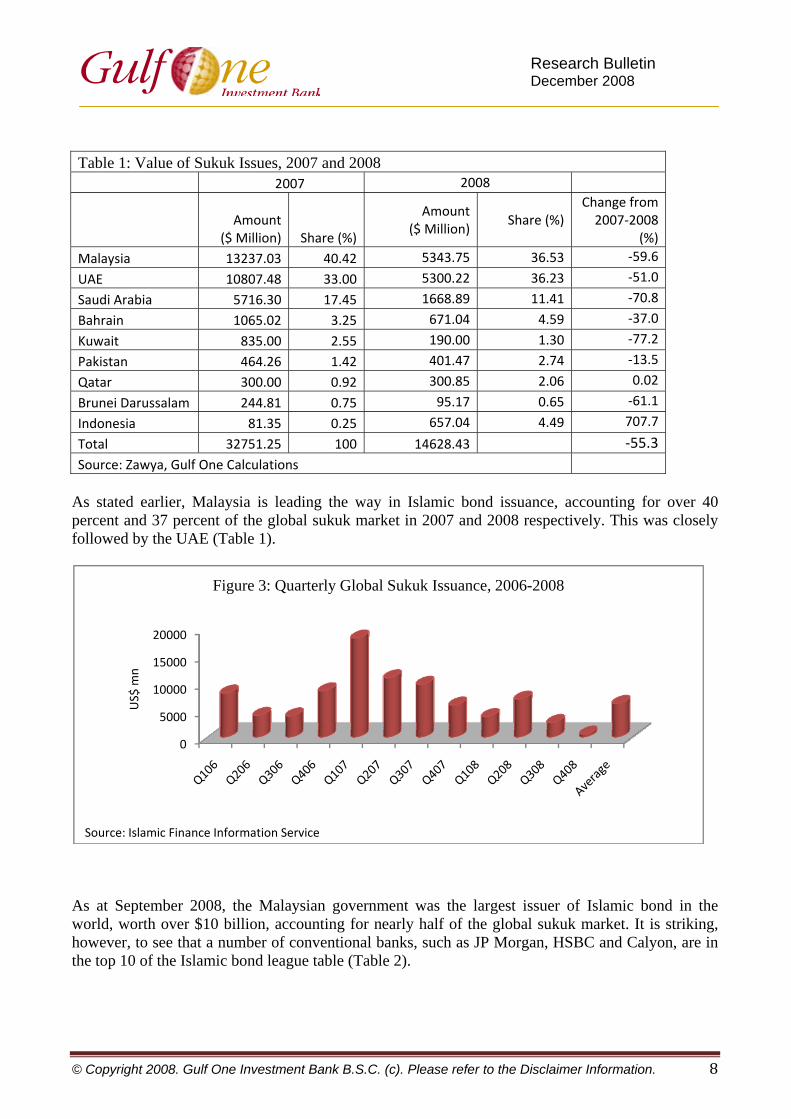

But Islamic bonds are currently the most popular and rapidly growing Islamic finance product, and they have become an important instrument for fund-raising and investment activities around the globe. They are structured on the various Islamic financing modes such as musharaka, murabaha, ijara and istisna, but at least 51 percent of the underpinning assets must be leased-back real assets, not debt instrument8. Over half of the global sukuk transactions in 2008 were based on the ijara mode of financing, followed by musharaka with 17.2 percent (Figure 2).

It should be noted that the global sukuk market in 2008 suffered a sharp decline with a total value of sukuk issuance of around $15 billion, less than half of the nearly $33 billion recorded in 2007 (Table 1). The decline in sukuk has been global, but the GCC and South East Asia were hit hardest with the former more severely impacted than the latter. In both regions, however, there were considerable variations across countries. Kuwait and Saudi Arabia witnessed the greatest decline in sukuk issuance in 2008, with a drop of more than 70 percent, whilst Qatar recorded no adverse market trend. In the case of South East Asia, however, it is Malaysia, the biggest sukuk market in the world, which experienced the biggest fall in sukuk issuance. In contrast, Indonesia witnessed a 7-fold increase in sukuk transactions in 2008! The sharpest decline in sukuk market in 2008 was on account of the fourth quarter of the year (Figure 3), making it the lowest quarterly sukuk issuance since 2002. A number of factors have contributed to the decline in the global sukuk market, but the principal factor is the global financial crisis, which has dried up liquidity, widened credit spreads, and eroded confidence which introduced a ‘wait-and-see’ attitude among investors9. Standard & Poor’s, however, predicts that the Islamic bond market would pick up by early 2010 when the global financial market is expected to begin to improve. 8 Middle East, Issue 394, November 2008. 9 Some analysts have, however, attributed the ‘deflation in the sukuk bubble’ in 2008 partly to a ruling from the Bahrain-based Accounting & Auditing Organisation for Islamic Finance Institutions (AAOIFI), which appeared to have been critical of some of sukuk structures. It was reported that the chairman of AAOIFI said that “one of the common forms of sukuk issuance, which guarantees the price at which an issuer will buy back an asset, contravenes the principle of risk and reward sharing, which is integral to Islamic finance” (MEED, 14 September 2008).

Ijara, 54.3%

Murabaha, 5.4%

Musharaka, 17.2%

Istisna, 5.4%

Mudaraba, 4.5%

Salam, 1%

Wakala, 12.2%

Figure 2: Composition of Global Sukuk in 2008

Source: Standard & Poor's (September 9, 2008)

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 8

Table 1: Value of Sukuk Issues, 2007 and 2008

2007 2008

Amount ($ Million) Share (%)

Amount ($ Million)

Share (%) Change from 2007‐2008

(%)Malaysia 13237.03 40.42 5343.75 36.53 ‐59.6

UAE 10807.48 33.00 5300.22 36.23 ‐51.0

Saudi Arabia 5716.30 17.45 1668.89 11.41 ‐70.8

Bahrain 1065.02 3.25 671.04 4.59 ‐37.0

Kuwait 835.00 2.55 190.00 1.30 ‐77.2

Pakistan 464.26 1.42 401.47 2.74 ‐13.5

Qatar 300.00 0.92 300.85 2.06 0.02

Brunei Darussalam 244.81 0.75 95.17 0.65 ‐61.1

Indonesia 81.35 0.25 657.04 4.49 707.7

Total 32751.25 100 14628.43 ‐55.3Source: Zawya, Gulf One Calculations

As stated earlier, Malaysia is leading the way in Islamic bond issuance, accounting for over 40 percent and 37 percent of the global sukuk market in 2007 and 2008 respectively. This was closely followed by the UAE (Table 1).

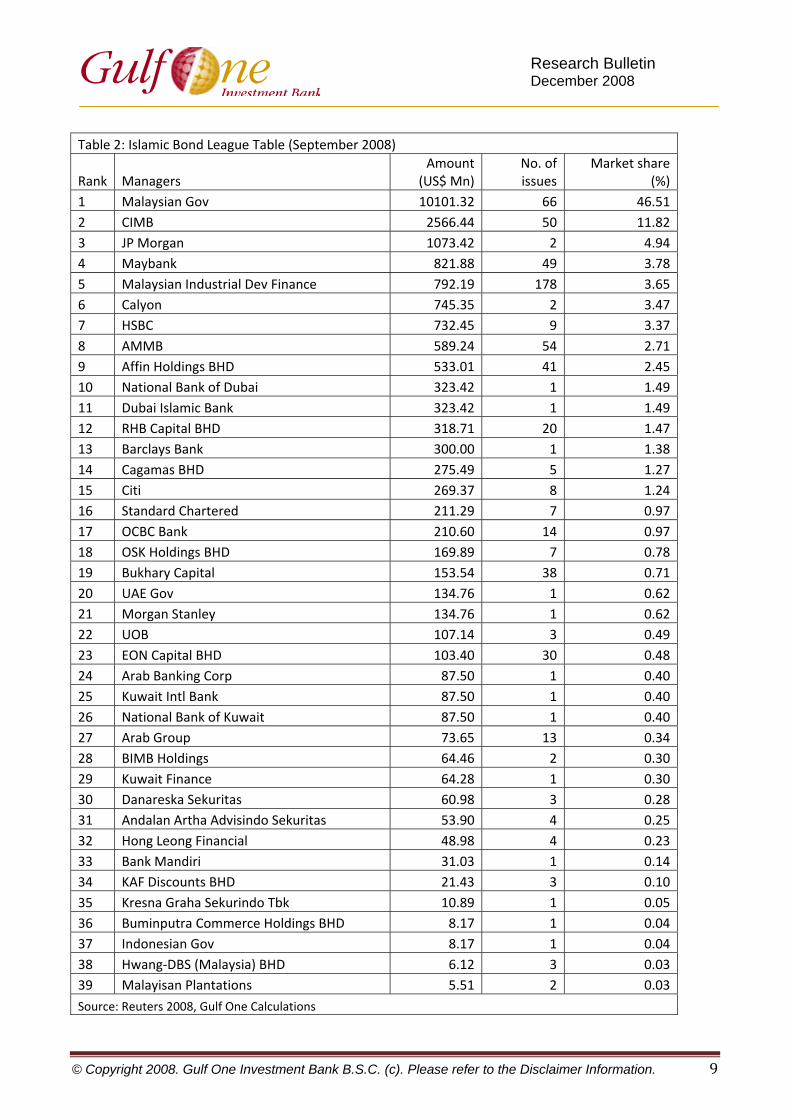

As at September 2008, the Malaysian government was the largest issuer of Islamic bond in the world, worth over $10 billion, accounting for nearly half of the global sukuk market. It is striking, however, to see that a number of conventional banks, such as JP Morgan, HSBC and Calyon, are in the top 10 of the Islamic bond league table (Table 2).

0

5000

10000

15000

20000

US$ mn

Source: Islamic Finance Information Service

Figure 3: Quarterly Global Sukuk Issuance, 2006-2008

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 9

Table 2: Islamic Bond League Table (September 2008)

Rank Managers Amount

(US$ Mn)No. of issues

Market share (%)

1 Malaysian Gov 10101.32 66 46.512 CIMB 2566.44 50 11.823 JP Morgan 1073.42 2 4.944 Maybank 821.88 49 3.785 Malaysian Industrial Dev Finance 792.19 178 3.656 Calyon 745.35 2 3.477 HSBC 732.45 9 3.378 AMMB 589.24 54 2.719 Affin Holdings BHD 533.01 41 2.4510 National Bank of Dubai 323.42 1 1.4911 Dubai Islamic Bank 323.42 1 1.4912 RHB Capital BHD 318.71 20 1.4713 Barclays Bank 300.00 1 1.3814 Cagamas BHD 275.49 5 1.2715 Citi 269.37 8 1.2416 Standard Chartered 211.29 7 0.9717 OCBC Bank 210.60 14 0.9718 OSK Holdings BHD 169.89 7 0.7819 Bukhary Capital 153.54 38 0.7120 UAE Gov 134.76 1 0.6221 Morgan Stanley 134.76 1 0.6222 UOB 107.14 3 0.4923 EON Capital BHD 103.40 30 0.4824 Arab Banking Corp 87.50 1 0.4025 Kuwait Intl Bank 87.50 1 0.4026 National Bank of Kuwait 87.50 1 0.4027 Arab Group 73.65 13 0.3428 BIMB Holdings 64.46 2 0.3029 Kuwait Finance 64.28 1 0.3030 Danareska Sekuritas 60.98 3 0.2831 Andalan Artha Advisindo Sekuritas 53.90 4 0.2532 Hong Leong Financial 48.98 4 0.2333 Bank Mandiri 31.03 1 0.1434 KAF Discounts BHD 21.43 3 0.1035 Kresna Graha Sekurindo Tbk 10.89 1 0.0536 Buminputra Commerce Holdings BHD 8.17 1 0.0437 Indonesian Gov 8.17 1 0.0438 Hwang‐DBS (Malaysia) BHD 6.12 3 0.0339 Malayisan Plantations 5.51 2 0.03

Source: Reuters 2008, Gulf One Calculations

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 10

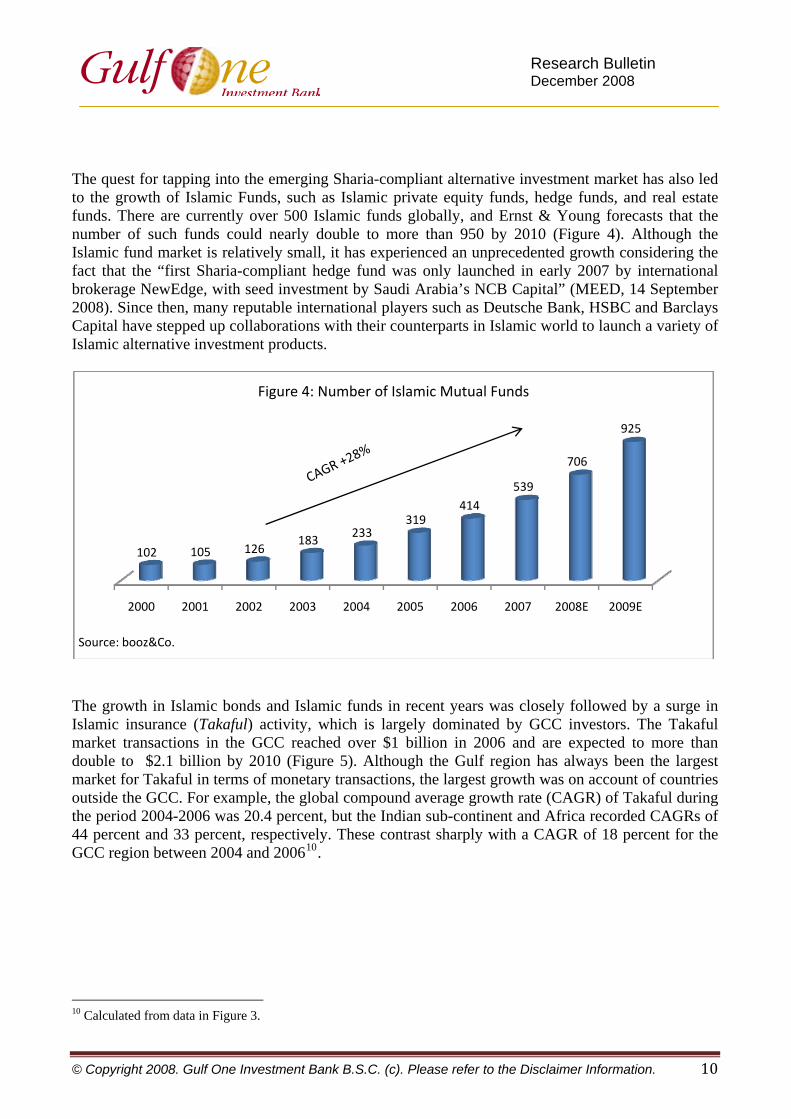

The quest for tapping into the emerging Sharia-compliant alternative investment market has also led to the growth of Islamic Funds, such as Islamic private equity funds, hedge funds, and real estate funds. There are currently over 500 Islamic funds globally, and Ernst & Young forecasts that the number of such funds could nearly double to more than 950 by 2010 (Figure 4). Although the Islamic fund market is relatively small, it has experienced an unprecedented growth considering the fact that the “first Sharia-compliant hedge fund was only launched in early 2007 by international brokerage NewEdge, with seed investment by Saudi Arabia’s NCB Capital” (MEED, 14 September 2008). Since then, many reputable international players such as Deutsche Bank, HSBC and Barclays Capital have stepped up collaborations with their counterparts in Islamic world to launch a variety of Islamic alternative investment products.

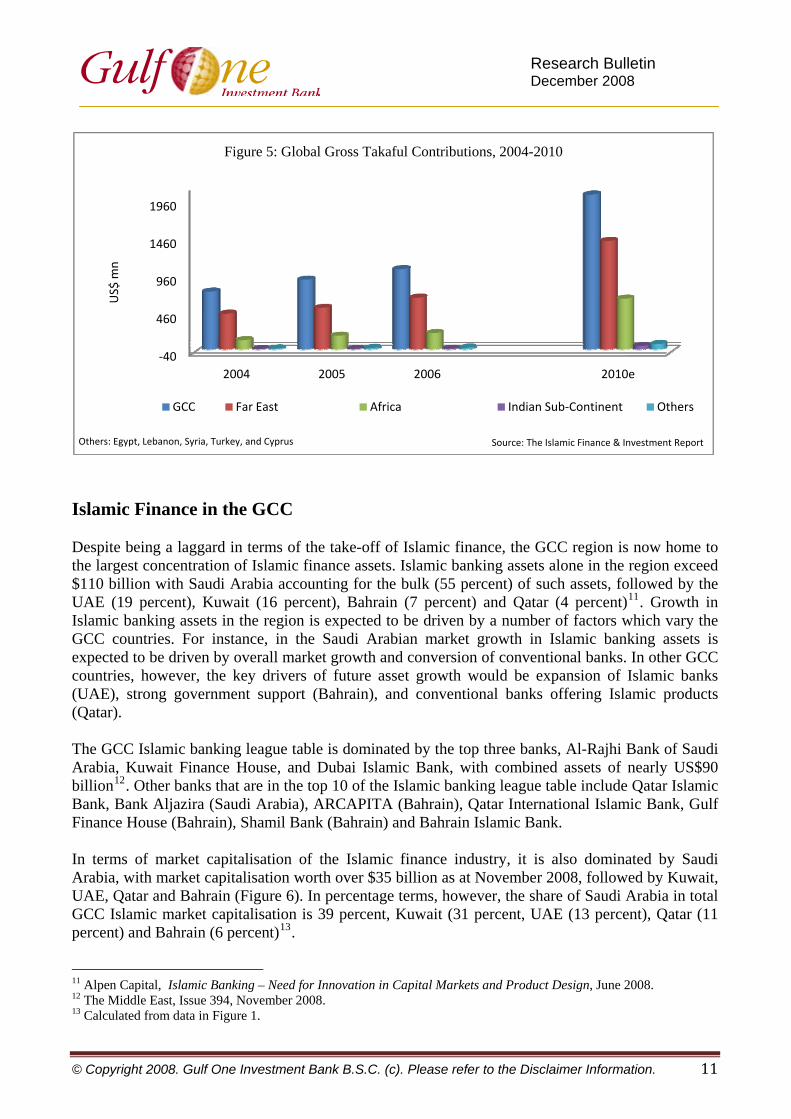

The growth in Islamic bonds and Islamic funds in recent years was closely followed by a surge in Islamic insurance (Takaful) activity, which is largely dominated by GCC investors. The Takaful market transactions in the GCC reached over $1 billion in 2006 and are expected to more than double to $2.1 billion by 2010 (Figure 5). Although the Gulf region has always been the largest market for Takaful in terms of monetary transactions, the largest growth was on account of countries outside the GCC. For example, the global compound average growth rate (CAGR) of Takaful during the period 2004-2006 was 20.4 percent, but the Indian sub-continent and Africa recorded CAGRs of 44 percent and 33 percent, respectively. These contrast sharply with a CAGR of 18 percent for the GCC region between 2004 and 200610.

10 Calculated from data in Figure 3.

2000 2001 2002 2003 2004 2005 2006 2007 2008E 2009E

102 105 126183 233

319414

539

706

925

Source: booz&Co.

Figure 4: Number of Islamic Mutual Funds

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 11

Islamic Finance in the GCC Despite being a laggard in terms of the take-off of Islamic finance, the GCC region is now home to the largest concentration of Islamic finance assets. Islamic banking assets alone in the region exceed $110 billion with Saudi Arabia accounting for the bulk (55 percent) of such assets, followed by the UAE (19 percent), Kuwait (16 percent), Bahrain (7 percent) and Qatar (4 percent)11. Growth in Islamic banking assets in the region is expected to be driven by a number of factors which vary the GCC countries. For instance, in the Saudi Arabian market growth in Islamic banking assets is expected to be driven by overall market growth and conversion of conventional banks. In other GCC countries, however, the key drivers of future asset growth would be expansion of Islamic banks (UAE), strong government support (Bahrain), and conventional banks offering Islamic products (Qatar). The GCC Islamic banking league table is dominated by the top three banks, Al-Rajhi Bank of Saudi Arabia, Kuwait Finance House, and Dubai Islamic Bank, with combined assets of nearly US$90 billion12. Other banks that are in the top 10 of the Islamic banking league table include Qatar Islamic Bank, Bank Aljazira (Saudi Arabia), ARCAPITA (Bahrain), Qatar International Islamic Bank, Gulf Finance House (Bahrain), Shamil Bank (Bahrain) and Bahrain Islamic Bank. In terms of market capitalisation of the Islamic finance industry, it is also dominated by Saudi Arabia, with market capitalisation worth over $35 billion as at November 2008, followed by Kuwait, UAE, Qatar and Bahrain (Figure 6). In percentage terms, however, the share of Saudi Arabia in total GCC Islamic market capitalisation is 39 percent, Kuwait (31 percent, UAE (13 percent), Qatar (11 percent) and Bahrain (6 percent)13.

11 Alpen Capital, Islamic Banking – Need for Innovation in Capital Markets and Product Design, June 2008. 12 The Middle East, Issue 394, November 2008. 13 Calculated from data in Figure 1.

‐40

460

960

1460

1960

2004 2005 2006 2010e

US$ mn

Others: Egypt, Lebanon, Syria, Turkey, and Cyprus

Figure 5: Global Gross Takaful Contributions, 2004-2010

GCC Far East Africa Indian Sub‐Continent Others

Source: The Islamic Finance & Investment Report

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 12

In spite of the tremendous progress made by Islamic finance industry in the GCC in recent years, the industry still accounts for a small proportion (15 percent) of total regional market capitalisation. A breakdown of such a ratio for individual countries in the region puts Bahrain in the driving seat, with 25 percent, followed by Kuwait with 21 percent whilst UAE and Saudi Arabia have the lowest ratios (Figure 7).

Yet another striking feature of Islamic finance in the GCC is its concentration in a handful of sectors dominated largely by real estate, followed by financial services largely in the form of consumer loans and credits. Figure 8 shows that real estate accounts for nearly a quarter of Islamic finance

Bahrain, 5.6

Kuwait, 27.08

Qatar , 9.92

Saudi Arabia, 35.07

UAE , 11.78

Figure 6: Islamic Finance Market Capitalization (US$ bn), November 2008

Source: Global Investment House

25

21

15 14

10

15

Bahrain Kuwait Qatar Saudi Arabia UAE Total GCC

Source: Global Invesment House

Figure 7: Share of Islamic Finance in Total Market Capital in the GCC (%), 2008

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 13

transactions, ahead of financial services (16 percent), transport (13 percent) and government sector (12 percent)14.

International Dimension of Islamic Finance Recently, Islamic finance has been gaining considerable momentum in non-Muslim countries. In Europe, the UK is leading the way with the establishment of the Islamic Bank of Britain, a stand-alone Islamic bank, in 2004. According to MEED (14 September 2008), the Islamic Bank of Britain has over 40,000 customers with more than $250 million in savings. Since then, two more Sharia-compliant banks have been established in the UK: the European Islamic Investment Bank and the Bank of London & the Middle East (BLME). The establishments of these Islamic banks are timely, as the UK has a sizeable population of Muslims (around 3 million) who are increasingly clamouring for Islamic finance products. As a result, conventional banks desirous of tapping into such a niche market have recently introduced Islamic windows, and there are currently around 23 conventional banks in the UK offering a variety of Islamic products, dominated by real estate. It is estimated that the total value of Islamic mortgage in 2007 rose to $900 million, a 50 percentage increase over the preceding year. The rise and growth of Islamic finance in the UK has been largely attributed to the unwavering UK government support by creating a conducive environment for Sharia-compliant products. First, the UK government changed the law in 2003 to facilitate Sharia-compliant mortgages. This was followed, two years later, by changes to the taxation law to create “a level playing field for savings products using mudaraba (trust financing) and wakala (agency contract) structures, as well as asset finance through murabaha (sale at pre-determined mark-up)” (MEED, 14 September 2008). Similarly, in 2007, the government introduced new measures to facilitate the sukuk (Islamic bond)

14 Although the information in Figure 8 relates to the sectoral composition of global Islamic finance, it mirrors the situation in the GCC given the considerable weight of the region in the industry.

0.005.0010.0015.0020.0025.00

16.14

24.30

9.58 9.6113.21

9.2611.29

3.410.92 1.12 0 0.25 0.50 0.41

%

Figure 8: Composition of Global Islamic Finance by Sectors (%), 2008

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 14

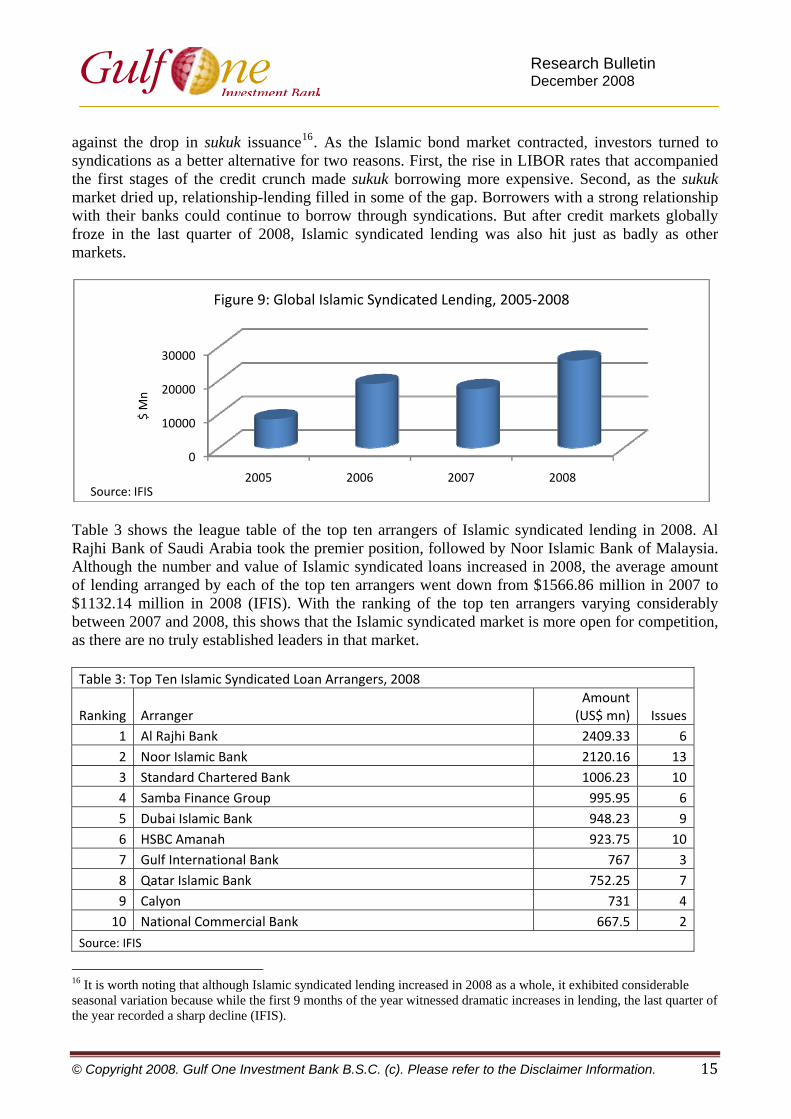

market. In 2008, after the UK government undertook an impact assessment of Islamic bond legislation, it was speculated that the government would start issuing sovereign Islamic bond within a year, but this was later denied by officials. In addition, the UK Financial Services Authority (FSA), which is the banking sector regulatory body, has specialists in Islamic banking in its deposit-taking division aimed at supervising Islamic institutions. The UK is also leading the way in terms of professional training related to Islamic finance. For instance, both the UK Securities & Investment Institute and the Chartered Institute of Management Accountants are now offering Islamic finance qualifications that are recognised globally. Islamic finance in other European countries is also making significant progress albeit at a much slower pace than in the UK. France and Germany, currently with estimated Muslim populations of 6 million and 3.5 million, respectively, have relatively few offerings of Islamic finance products. Both countries have no stand-alone Islamic banks, but Sharia-compliant products are being provided by conventional banks. There are 4 such conventional banks in France whilst Commerzbank and Deutsche Bank provide Islamic finance services in Germany. Sharia-compliant products also have strong presence in other European countries, such as Holland, Luxembourg, Denmark, and Switzerland. Many believe that Islamic finance would not make significant inroads in Europe unless the governments introduce radical reforms, similar to those in the UK, to create favourable climate for the development and growth of Islamic finance institutions. Outside Europe, Islamic finance has a sizeable presence in the US, which boasts of around 20 Islamic banks that offer Sharia-compliant products. Critics have, however, argued that many of these banks largely focus on domestic retail operations rather than large transactions (MEED). Even so, the US is the second largest country in the western world, besides the UK, in terms of Islamic finance activities and it has more promising prospects than many European countries. Islamic Syndications and Project Finance One area where Islamic finance institutions, particularly Islamic banks, are relatively less visible is project financing, partly due to the long gestation periods of some of the projects, such as mega infrastructure projects, and partly due to the complexity of structuring Sharia-compliant project finance. As a result, most Islamic finance institutions appeared to be largely motivated by short-term financing, particularly in areas such as real estates and personal consumables, at the expense of infrastructure projects. This is a worrisome phenomenon for a couple of reasons. First, the continued focus of Islamic banks on short-term trade financing will inevitably cause their relegation to the periphery of the financial system15. Second, whilst Islamic financing of real estates and consumables performs a very important economic function, it has little direct bearing on expansion of the production possibility frontier of an economy. Only financing of activities in the productive sector, such as infrastructure projects, can accelerate productivity growth, boost income and create jobs that could sustain economic and social prosperity. Having said that, Islamic syndicated lending performed better than the sukuk market in 2008, with borrowing expanding from nearly $20 billion in 2007 to over $27 billion in 2008, a 32% increase (Figure 9). In the GCC, Islamic syndicated lending provided the debt market with some buffer

15 Without taking centre stage, Islamic banking would always remain in the shadows, as A. H. Pramanik argues in his book, Islamic Banking: How Far Have We Gone? (International Islamic University Malaysia, 2007).

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 15

against the drop in sukuk issuance16. As the Islamic bond market contracted, investors turned to syndications as a better alternative for two reasons. First, the rise in LIBOR rates that accompanied the first stages of the credit crunch made sukuk borrowing more expensive. Second, as the sukuk market dried up, relationship-lending filled in some of the gap. Borrowers with a strong relationship with their banks could continue to borrow through syndications. But after credit markets globally froze in the last quarter of 2008, Islamic syndicated lending was also hit just as badly as other markets.

Table 3 shows the league table of the top ten arrangers of Islamic syndicated lending in 2008. Al Rajhi Bank of Saudi Arabia took the premier position, followed by Noor Islamic Bank of Malaysia. Although the number and value of Islamic syndicated loans increased in 2008, the average amount of lending arranged by each of the top ten arrangers went down from $1566.86 million in 2007 to $1132.14 million in 2008 (IFIS). With the ranking of the top ten arrangers varying considerably between 2007 and 2008, this shows that the Islamic syndicated market is more open for competition, as there are no truly established leaders in that market. Table 3: Top Ten Islamic Syndicated Loan Arrangers, 2008

Ranking Arranger Amount (US$ mn) Issues

1 Al Rajhi Bank 2409.33 62 Noor Islamic Bank 2120.16 133 Standard Chartered Bank 1006.23 104 Samba Finance Group 995.95 65 Dubai Islamic Bank 948.23 96 HSBC Amanah 923.75 107 Gulf International Bank 767 38 Qatar Islamic Bank 752.25 79 Calyon 731 4

10 National Commercial Bank 667.5 2

Source: IFIS

16 It is worth noting that although Islamic syndicated lending increased in 2008 as a whole, it exhibited considerable seasonal variation because while the first 9 months of the year witnessed dramatic increases in lending, the last quarter of the year recorded a sharp decline (IFIS).

0

10000

20000

30000

2005 2006 2007 2008

$ Mn

Figure 9: Global Islamic Syndicated Lending, 2005‐2008

Source: IFIS

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 16

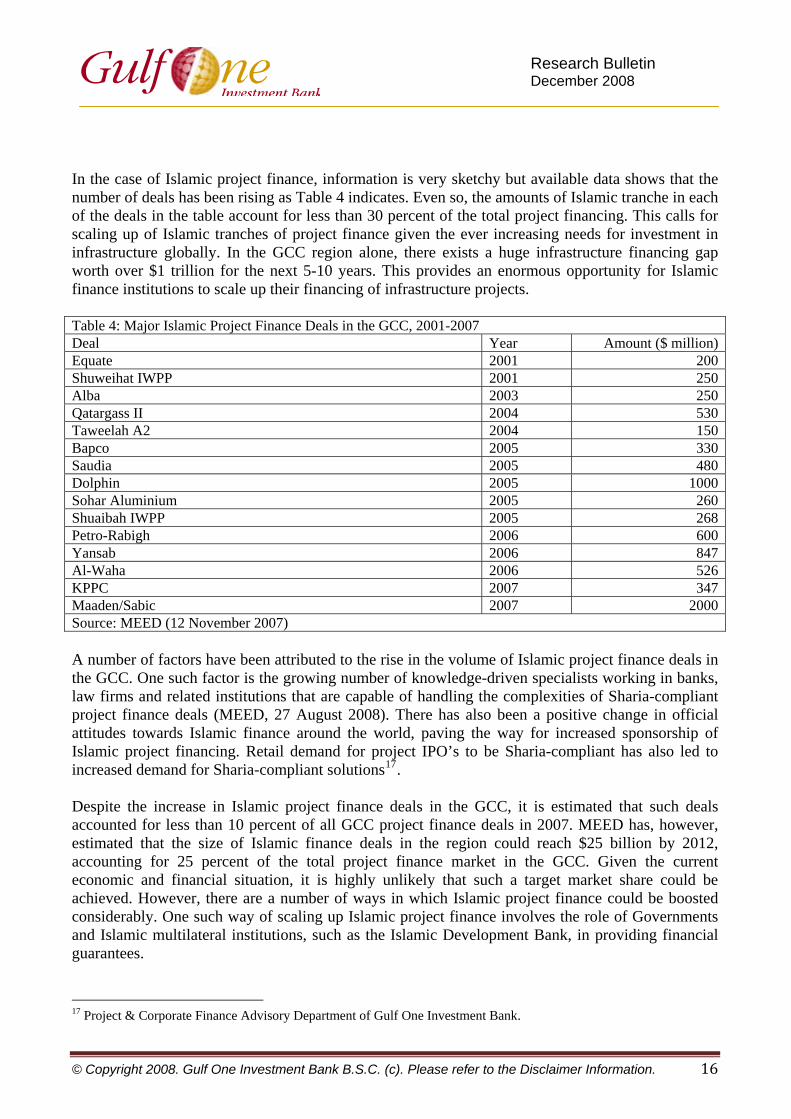

In the case of Islamic project finance, information is very sketchy but available data shows that the number of deals has been rising as Table 4 indicates. Even so, the amounts of Islamic tranche in each of the deals in the table account for less than 30 percent of the total project financing. This calls for scaling up of Islamic tranches of project finance given the ever increasing needs for investment in infrastructure globally. In the GCC region alone, there exists a huge infrastructure financing gap worth over $1 trillion for the next 5-10 years. This provides an enormous opportunity for Islamic finance institutions to scale up their financing of infrastructure projects. Table 4: Major Islamic Project Finance Deals in the GCC, 2001-2007 Deal Year Amount ($ million)Equate 2001 200Shuweihat IWPP 2001 250Alba 2003 250Qatargass II 2004 530Taweelah A2 2004 150Bapco 2005 330Saudia 2005 480Dolphin 2005 1000Sohar Aluminium 2005 260Shuaibah IWPP 2005 268Petro-Rabigh 2006 600Yansab 2006 847Al-Waha 2006 526KPPC 2007 347Maaden/Sabic 2007 2000Source: MEED (12 November 2007) A number of factors have been attributed to the rise in the volume of Islamic project finance deals in the GCC. One such factor is the growing number of knowledge-driven specialists working in banks, law firms and related institutions that are capable of handling the complexities of Sharia-compliant project finance deals (MEED, 27 August 2008). There has also been a positive change in official attitudes towards Islamic finance around the world, paving the way for increased sponsorship of Islamic project financing. Retail demand for project IPO’s to be Sharia-compliant has also led to increased demand for Sharia-compliant solutions17. Despite the increase in Islamic project finance deals in the GCC, it is estimated that such deals accounted for less than 10 percent of all GCC project finance deals in 2007. MEED has, however, estimated that the size of Islamic finance deals in the region could reach $25 billion by 2012, accounting for 25 percent of the total project finance market in the GCC. Given the current economic and financial situation, it is highly unlikely that such a target market share could be achieved. However, there are a number of ways in which Islamic project finance could be boosted considerably. One such way of scaling up Islamic project finance involves the role of Governments and Islamic multilateral institutions, such as the Islamic Development Bank, in providing financial guarantees.

17 Project & Corporate Finance Advisory Department of Gulf One Investment Bank.

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 17

It is noteworthy that the role of financial guarantee is critical since financing mega projects generally involves a huge amount of capital outlay and a considerable risk exposure. The complexity of structuring Islamic project financing together with a relatively high default risk potential make Islamic project finance a daunting challenge, which might deter investors. One way to reduce the default risk and to attract Islamic project financiers is to introduce government financial guarantees. It is worth mentioning that financial guarantees have played an important role in conventional project financing, which undoubtedly serves to improve the credit rating and debt capacity of firms, thereby giving them access to more and cheaper funds. Multilateral organisations such as the World Bank have for long been providing financial guarantees to support large-scale project financing in developing countries18. However, in the case of GCC countries, the active involvement of governments in providing financial guarantees would be welcome from a number of perspectives. First, the overwhelming carbon-based wealth of the region has enabled it amass substantial foreign exchange resources, which put governments in good stead to act as credible financial guarantors of Islamic project finance contracts. Second, from socio-economic perspectives, governments in the region have an obligation to provide key infrastructure facilities for sustainable prosperity of the region. But, as is well known, the huge infrastructure financing gap in the GCC suggests that governments alone cannot meet all the infrastructure requirements. Government efforts have to be complemented by private sector investment. Therefore government financial guarantee could build confidence and enhance the creditworthiness of Sharia-compliant projects, and would attract private sector investors to the Islamic project finance industry. Third, active involvement of governments in Islamic project finance would provide incentive for countries in the region to speed up the process of reforming the legal, institutional, and regulatory environment for effective operations of Islamic finance. Fourth, scaling up the volume of Islamic financed projects through government guarantees would boost fiscal position through increased tax revenues associated with the projects. Performance of Islamic Finance

There is no doubt that Islamic finance has witnessed an unprecedented growth in recent years, and it is expected to grow at exponential rates in the future as the industry continues the process of mainstreaming itself into the international financial system. Lessons from the current global financial crisis also provide considerable support to Islamic finance philosophy which helped the sector to weather the storm of the crisis relatively easily. These and other factors would continue to make Islamic finance an attractive concept. The key question is what is the performance of Islamic finance during the current global financial crisis in terms of key financial ratios and indices? What lessons can both Islamic and conventional systems of finance learn from each other?

There are a number of indices that track the performances of Islamic finance markets. These include the Dow Jones Islamic Market Indices, Morgan Stanley Capital Index (MSCI), Investment House Islamic Index, Indonesia Islamic Index, and a host of other indices. The Dow Jones Islamic Market index in particular is more diverse and tracks Islamic markets in different regions (GCC, Asia/Pacific, BRIC19, and Global Emerging Markets) and has an index on Islamic Market

18 For a succinct summary of the literature on financial guarantees, see M.K. Hassan and I. Soumare, Financial Guarantee as Innovation Tool in Islamic Project Finance, University of New Orleans Discussion Paper, 2006. 19 BRIC stands for Brazil, Russia, India and China.

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 18

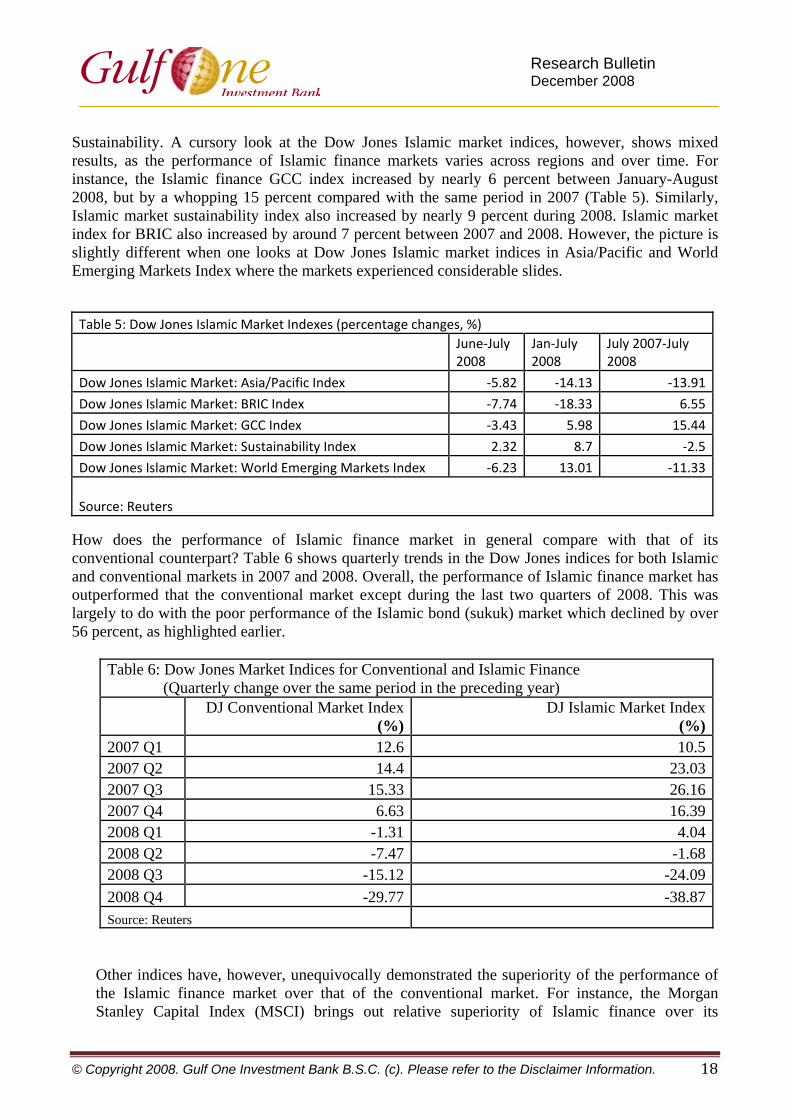

Sustainability. A cursory look at the Dow Jones Islamic market indices, however, shows mixed results, as the performance of Islamic finance markets varies across regions and over time. For instance, the Islamic finance GCC index increased by nearly 6 percent between January-August 2008, but by a whopping 15 percent compared with the same period in 2007 (Table 5). Similarly, Islamic market sustainability index also increased by nearly 9 percent during 2008. Islamic market index for BRIC also increased by around 7 percent between 2007 and 2008. However, the picture is slightly different when one looks at Dow Jones Islamic market indices in Asia/Pacific and World Emerging Markets Index where the markets experienced considerable slides.

Table 5: Dow Jones Islamic Market Indexes (percentage changes, %)June‐July 2008

Jan‐July 2008

July 2007‐July 2008

Dow Jones Islamic Market: Asia/Pacific Index ‐5.82 ‐14.13 ‐13.91

Dow Jones Islamic Market: BRIC Index ‐7.74 ‐18.33 6.55

Dow Jones Islamic Market: GCC Index ‐3.43 5.98 15.44

Dow Jones Islamic Market: Sustainability Index 2.32 8.7 ‐2.5

Dow Jones Islamic Market: World Emerging Markets Index ‐6.23 13.01 ‐11.33 Source: Reuters

How does the performance of Islamic finance market in general compare with that of its conventional counterpart? Table 6 shows quarterly trends in the Dow Jones indices for both Islamic and conventional markets in 2007 and 2008. Overall, the performance of Islamic finance market has outperformed that the conventional market except during the last two quarters of 2008. This was largely to do with the poor performance of the Islamic bond (sukuk) market which declined by over 56 percent, as highlighted earlier.

Table 6: Dow Jones Market Indices for Conventional and Islamic Finance (Quarterly change over the same period in the preceding year)

DJ Conventional Market Index(%)

DJ Islamic Market Index(%)

2007 Q1 12.6 10.52007 Q2 14.4 23.032007 Q3 15.33 26.162007 Q4 6.63 16.392008 Q1 -1.31 4.042008 Q2 -7.47 -1.682008 Q3 -15.12 -24.092008 Q4 -29.77 -38.87Source: Reuters

Other indices have, however, unequivocally demonstrated the superiority of the performance of the Islamic finance market over that of the conventional market. For instance, the Morgan Stanley Capital Index (MSCI) brings out relative superiority of Islamic finance over its

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 19

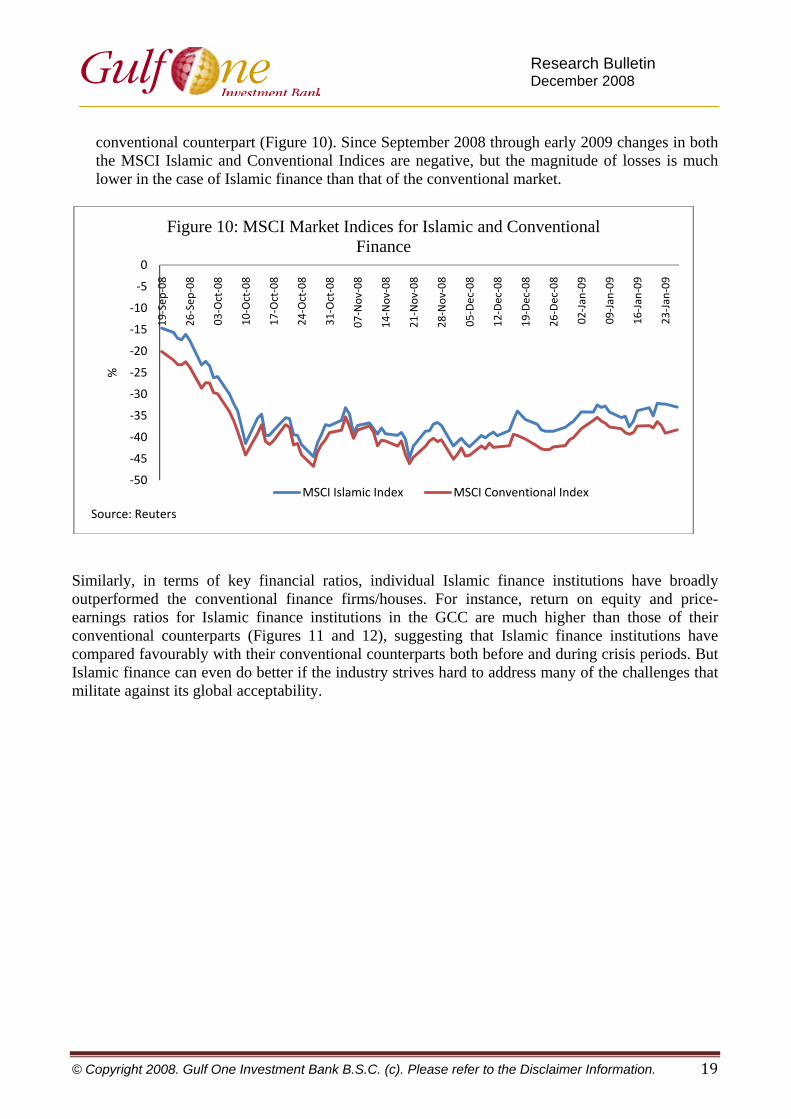

conventional counterpart (Figure 10). Since September 2008 through early 2009 changes in both the MSCI Islamic and Conventional Indices are negative, but the magnitude of losses is much lower in the case of Islamic finance than that of the conventional market.

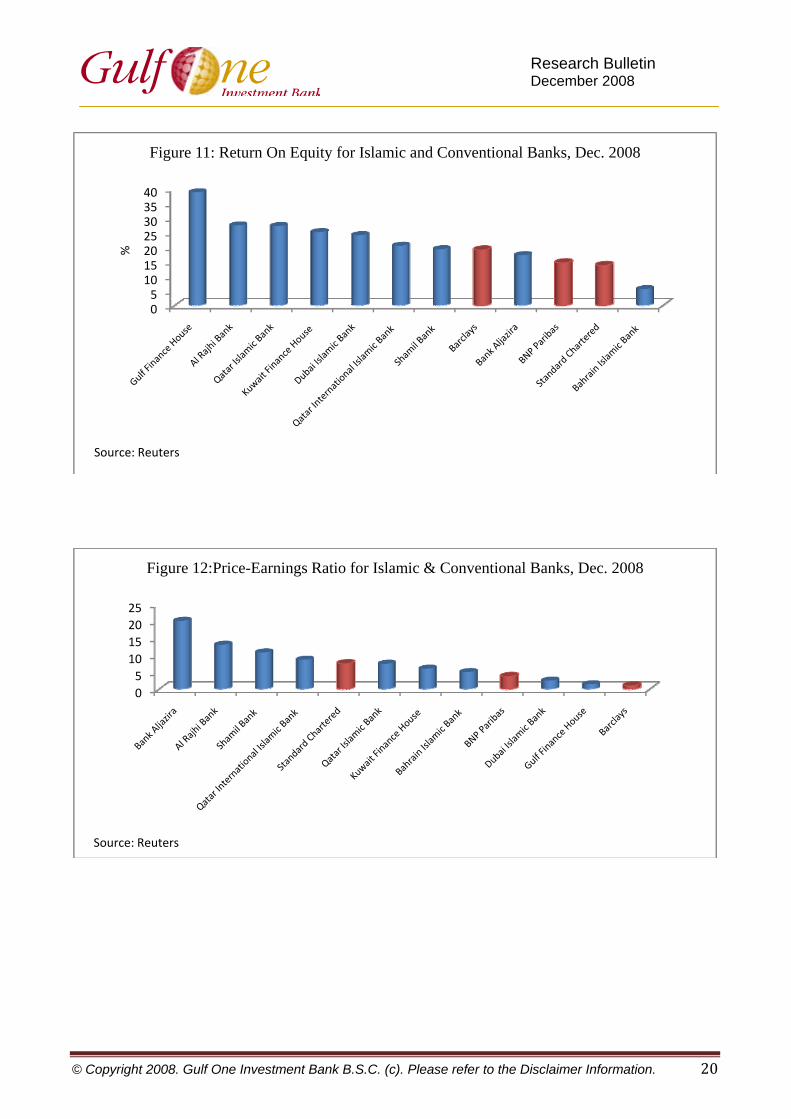

Similarly, in terms of key financial ratios, individual Islamic finance institutions have broadly outperformed the conventional finance firms/houses. For instance, return on equity and price-earnings ratios for Islamic finance institutions in the GCC are much higher than those of their conventional counterparts (Figures 11 and 12), suggesting that Islamic finance institutions have compared favourably with their conventional counterparts both before and during crisis periods. But Islamic finance can even do better if the industry strives hard to address many of the challenges that militate against its global acceptability.

‐50

‐45

‐40

‐35

‐30

‐25

‐20

‐15

‐10

‐5

0

19‐Sep

‐08

26‐Sep

‐08

03‐Oct‐08

10‐Oct‐08

17‐Oct‐08

24‐Oct‐08

31‐Oct‐08

07‐Nov

‐08

14‐Nov

‐08

21‐Nov

‐08

28‐Nov

‐08

05‐Dec‐08

12‐Dec‐08

19‐Dec‐08

26‐Dec‐08

02‐Jan

‐09

09‐Jan

‐09

16‐Jan

‐09

23‐Jan

‐09

%

Source: Reuters

Figure 10: MSCI Market Indices for Islamic and Conventional Finance

MSCI Islamic Index MSCI Conventional Index

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 20

0510152025303540

%

Source: Reuters

Figure 11: Return On Equity for Islamic and Conventional Banks, Dec. 2008

05

10152025

Source: Reuters

Figure 12:Price-Earnings Ratio for Islamic & Conventional Banks, Dec. 2008

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 21

Challenges Islamic finance has made tremendous progress in recent years, but it has also faced many challenges, which unless addressed urgently, would continue to act as a cog in the wheels of its progress. Principal among these challenges are the following:

• Islamic financial products are devoid of depth and breadth that characterised conventional products. This can act to hamper the creation of a critical mass that is needed to attract a large number of transactors.

• The legal, institutional and regulatory environment which Islamic finance operates is generally weak and problematic, which serves to hinder financial innovation in Islamic finance industry. The Sharia compliance of products and activities often constitutes a major challenge for the Islamic finance, and the multiplicity of Sharia boards with varying judgements tends to undermine the creation of a consistent regulatory framework and governance structures. It is noteworthy that efforts at mainstreaming Islamic finance into the global financial system hinge largely on the existence of appropriate legal framework couple with efficient and transparent capital markets.

• The dearth of skilled labour force in Muslim countries militates against the much needed innovation as well as managerial and analytical abilities required to move Islamic finance to new heights.

• The fragmented nature of Islamic finance market and its high concentration on a narrow range of sectors, particularly in real estate, make it vulnerable to sector-specific shocks, such as the current global financial crisis which has disproportionately affected the real estate and construction industries.

• Islamic finance faces challenges posed by limited or absence of widespread Sharia-compliant short-term Islamic money market and highly under-developed Islamic repurchase markets.

• Over reliance of Islamic finance on conventional financial instruments such as LIBOR as benchmarks for mark-ups and fees makes it highly susceptible to whims and caprices of global financial system.

Next Steps In order to move the frontier of Islamic finance into the mainstream of global financial systems, solutions must be found to the above mentioned challenges.

• There is an urgent need to promote Islamic financial architecture that encourages standardization of legal structure and contracts, prudential regulation, and supervision supported by appropriate risk management of the special features and structure of the new products, and accounting practices in line with AAOIFI standards20.

• Efforts must be made towards harmonization and convergence of religious views emanating from differences in interpretation Islamic jurisprudence.

• Overcoming the challenges of fragmentation calls for efforts towards consolidation and restructuring of Islamic financial institutions, including mergers. Such a move is likely to enhance the scale, scope, efficiency, and effectiveness of Islamic finance institutions.

20 Speech by the Governor of Central Bank of Pakistan, at a Conference on Globalisation, May 2008.

Research Bulletin December 2008

© Copyright 2008. Gulf One Investment Bank B.S.C. (c). Please refer to the Disclaimer Information. 22

• There is a further need for proper financial engineering and innovation to support project and infrastructure financing, and private equity. The fact that the share of Islamic tranche in most project financing deals is less than 30% questions the ‘Islamicness’ of a project. Part of the financial engineering should include development of appropriate framework that would enhance the profit-and-loss sharing schemes.

• To ally transactors’ concerns, governments especially in Muslim countries should redouble their efforts to play a critical role in promoting Islamic finance by providing financial guarantees, creating and strengthening legal and institutional environment as well as creating more effective monetary and supervisory role of Islamic finance.

• Islamic finance industry should endeavour to find alternative benchmarks, rather than relying on conventional instruments such as LIBOR. This calls for in-depth studies on the way forward, not only on alternative indicators but also on all the plethora of challenges facing Islamic finance.

Conclusion Without a doubt, the long-term outlook for Islamic finance is promising, and the industry will continue to grow from strength to strength. However, the Islamic finance industry also faces important challenges. Developing and improving the proper enabling environment will go a long way in helping the Islamic finance industry to deal with these challenges. Once such environment becomes sufficiently workable, the Islamic finance industry can become more capable of handling sophisticated financing techniques and instruments. It can then accomplish more successes, especially in the areas of designing market based instruments for monetary control and government financing that satisfy the Islamic principles and promote greater reliance on equity finance. The current global financial crisis presents a window of opportunity for Islamic finance to blossom and accelerate the process of expanding itself across global frontiers. Financial institutions in the GCC, Pakistan, Malaysia and other countries have made great strides in promoting Sharia-compliant products, and are constantly creating more Sharia-compliant financial instruments and structured finance. But more remains to be done to push the industry to greater heights. As it is now, the bulk of the Islamic financial transactions are heavily tilted towards short-term, unproductive sectors of the economy. In order to use Islamic finance to create jobs, boost income and promote sustainable socio-economic prosperity, Islamic finance must shift its focus to financing mega-infrastructure projects. ________________________________________________________________________Disclaimer This research bulletin was prepared by Gulf One Investment Bank B.S.C (c), (“Gulf One”) and is of a general nature and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive or to address the circumstances of any particular individual or entity. This material is based on current public information that we consider reliable at the time of publication, but it does not provide tailored investment advice or recommendations. It has been prepared without regard to the financial circumstances and objectives of persons and/or organisations who receive it. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. In addition, the views expressed in this bulletin do not necessarily represent the views of the Management or Board of Directors of Gulf One Investment Bank. This bulletin or any portion hereof may not be reprinted, sold or redistributed without the prior written consent of Gulf One.