REQUEST FORPROPOSAL (RFP)

54

1 REQUEST FOR PROPOSAL (RFP) For Provision of 2016 HACT Financial Audit for UNDP funded Projects (Process 35-44188) Phnom Penh, Cambodia December 13, 2016 Dear Sir / Madam: We kindly request you to submit your Proposal for provision of 2016 HACT Audit for UNDP Projects . Please be guided by the forms attached hereto as Annex B and C, in preparing your Proposal. Your offer, comprising of a Technical and Financial Proposal, in separate sealed envelopes, must be submitted to the following address no later than 3 January 2017 by 11:00 a.m., local time. Late submission shall be rejected. UNDP Cambodia, Registry Office (Building No. 3) No. 18, Pasteur Street, Boeung Keng Kang I PO Box 877, Phnom Penh, Cambodia Attn: Procurement Analyst, Procurement Unit Your Proposal must be expressed in the English, and valid for a minimum period of 90 days In the course of preparing your Proposal, it shall remain your responsibility to ensure that it reaches the address above on or before the deadline. Proposals that are received by UNDP after the deadline indicated above, for whatever reason, shall not be considered for evaluation. If you are submitting your Proposal by email, kindly ensure that they are signed and in the .pdf format, and free from any virus or corrupted files. Services proposed shall be reviewed and evaluated based on completeness and compliance of the Proposal and responsiveness with the requirements of the RFP and all other annexes providing details of UNDP requirements. The Proposal that complies with all of the requirements, meets all the evaluation criteria and offers the best value for money shall be selected and awarded the contract. Any offer that does not meet the requirements shall be rejected. Any discrepancy between the unit price and the total price shall be re-computed by UNDP, and the unit price shall prevail and the total price shall be corrected. If the Service Provider does not accept the final price based on UNDP’s re-computation and correction of errors, its Proposal will be rejected.

Transcript of REQUEST FORPROPOSAL (RFP)

1

REQUEST FOR PROPOSAL (RFP)For Provision of 2016 HACT Financial Audit for UNDP funded Projects

(Process 35-44188)

Phnom Penh, CambodiaDecember 13, 2016

Dear Sir / Madam:

We kindly request you to submit your Proposal for provision of 2016 HACT Audit for UNDPProjects .

Please be guided by the forms attached hereto as Annex B and C, in preparing yourProposal.

Your offer, comprising of a Technical and Financial Proposal, in separate sealedenvelopes, must be submitted to the following address no later than 3 January 2017 by 11:00a.m., local time. Late submission shall be rejected.

UNDP Cambodia, Registry Office (Building No. 3)No. 18, Pasteur Street, Boeung Keng Kang I

PO Box 877, Phnom Penh, CambodiaAttn: Procurement Analyst, Procurement Unit

Your Proposal must be expressed in the English, and valid for a minimum period of 90 days

In the course of preparing your Proposal, it shall remain your responsibility to ensure that itreaches the address above on or before the deadline. Proposals that are received by UNDP after thedeadline indicated above, for whatever reason, shall not be considered for evaluation. If you aresubmitting your Proposal by email, kindly ensure that they are signed and in the .pdf format, and freefrom any virus or corrupted files.

Services proposed shall be reviewed and evaluated based on completeness and complianceof the Proposal and responsiveness with the requirements of the RFP and all other annexes providingdetails of UNDP requirements.

The Proposal that complies with all of the requirements, meets all the evaluation criteria andoffers the best value for money shall be selected and awarded the contract. Any offer that does notmeet the requirements shall be rejected.

Any discrepancy between the unit price and the total price shall be re-computed by UNDP,and the unit price shall prevail and the total price shall be corrected. If the Service Provider does notaccept the final price based on UNDP’s re-computation and correction of errors, its Proposal will berejected.

No price variation due to escalation, inflation, fluctuation in exchange rates, or any othermarket factors shall be accepted by UNDP after it has received the Proposal. At the time of Award ofContract or Purchase Order, UNDP reserves the right to vary (increase or decrease) the quantity ofservices and/or goods, by up to a maximum twenty five per cent (25%) of the total offer, without anychange in the unit price or other terms and conditions.

Any Contract or Purchase Order that will be issued as a result of this RFPshall be subject tothe General Terms and Conditions attached hereto. The mere act of submission 'of a Proposal impliesthat the Service Provider accepts without question the General Terms and Conditions of UNDP, hereinattached as Annex D.

Please be advised that UNDP is not bound to accept any Proposal, nor award a contract orPurchase Order, nor be responsible for any costs associated with a Service Providers preparation andsubmission of a Proposal, regardless of the outcome or the manner of conducting the selectionprocess.

UNDP's vendor protest procedure is intended to afford an opportunity to appeal for personsor firms not awarded a Purchase Order or Contract in a competitive procurement process. In theevent that you believe you have not been fairly treated, you can find detailed information aboutvendor protest procedures in the following link:http://www.undp.org/content/undp/en/home/operations/procurement/protestandsanctions/

UNDP encourages every prospective Service Provider to prevent and avoid conflicts ofinterest, by disclosing to UNDP if you, or any of your affiliates or personnel, were involved in thepreparation of the requirements, design, cost estimates, and other information used in this RFP.

UNDP implements a zero tolerance on fraud and other proscribed practices, and is committedto preventing, identifying and addressing all such acts and practices against UNDP, as well as thirdparties involved in UNDP activities. UNDP expects its Service Providers to adhere to the UN SupplierCode of Conduct found in this link: http://www.un.org/depts/ptd/pdf/conduct english.pdf

Thank you and we look forward to receiving your Proposal.

Sincerely yours,

~rOperations Manager

2

3

Annex A

Description of Requirements

Context of theRequirement

Provision of Audit Services for UNDP Projects under National Implementation(NIM) and NGO Implementation.

The objective is to give UNDP an independent audit opinion on themanagement and performance of the financial, operational, and projectactivities for projects under UNDP’s National Implementation modality (NIM)and NGO Implementation.

Implementing Partner ofUNDP

1. Mine Action for Human Development2. Cambodia Climate Change Alliance (CCCA) Phase II3. Generating, Accessing and Using Information and Knowledge Related

to the Three Rio Conventions (3 Rio)4. Multi-media Initiative for Youth5. Partnership for Development Results Phase 26. A Project to be randomly selected (To be confirmed after selection

process)Brief Description of theRequired Services1

The scope of audit services shall be in accordance with International Standardson Auditing (ISA) and cover the overall management of the project’simplementation, monitoring and supervision. The audit work should include thereview of work plans, progress reports, project resources, project budgets,project expenses, project delivery, recruitment, operational and financial closingof projects (if applicable) and disposal or transfer of assets.

The report to be audited is referred to as the Combined Delivery Report (CDR).This report is prepared by UNDP, using an in-house accounting softwarepackage called ATLAS. The CDR serves as the official financial statement thatmust be certified by the auditors. Project financial statements, if certified, mustreconcile to the expenses appearing in the CDR and must be attached to theaudit report.

A detailed ToR is attached as Annex E.List and Description ofExpected Outputs to beDelivered

Details audit work plan and schedules. Draft audit report by 28 February 2017 Final signed audit report with signed UNDP statements by 31 March

2017.Person to Supervise theWork/Performance of theService Provider

Oversight Analyst, Management Support Unit, UNDP Cambodia

Frequency of Reporting Refer to attached ToR (Annex E)Progress ReportingRequirements

Refer to attached ToR (Annex E)

Location of work☒ Projects’ office/site☒ At Contractor’s Location

1 A detailed TOR may be attached if the information listed in this Annex is not sufficient to fully describe thenature of the work and other details of the requirements.

4

Expected duration ofwork

10 weeks (from 23 January to 31 March 2017)

Target start date 23 January 2017Latest completion date 31 March 2017

Travels ExpectedRefer to attached ToR (Annex E)

Special SecurityRequirements

N/A

Facilities to be Providedby UNDP (i.e., must beexcluded from PriceProposal)

☒ Office space and facilities, if needed

Implementation Scheduleindicating breakdownand timing ofactivities/sub-activities

☒ Required

Names and curriculumvitae of individuals whowill be involved incompleting the services

☒ Required

Currency of Proposal☒ United States Dollars

Value Added Tax on PriceProposal2

☒must be exclusive of VAT and other applicable indirect taxes

Validity Period ofProposals (Counting forthe last day of submissionof quotes)

☒ 90 days

In exceptional circumstances, UNDP may request the Proposer to extend thevalidity of the Proposal beyond what has been initially indicated in this RFP.The Proposal shall then confirm the extension in writing, without anymodification whatsoever on the Proposal.

Partial Quotes☒ Not permitted

Payment Terms3 Outputs Percentage Timing Condition forPayment Release

Details auditwork plan andschedules

20% Within 1week aftercommencingdate ofcontract

Within thirty (30) daysfrom the date ofmeeting thefollowing conditions:a) UNDP’s written

acceptance (i.e.,

2 VAT exemption status varies from one country to another. Pls. check whatever is applicable to the UNDPCO/BU requiring the service.3 UNDP preference is not to pay any amount in advance upon signing of contract. If the Service Provider strictlyrequires payment in advance, it will be limited only up to 20% of the total price quoted. For any higherpercentage, or any amount advanced exceeding $30,000, UNDP shall require the Service Provider to submit abank guarantee or bank cheque payable to UNDP, in the same amount as the payment advanced by UNDP to theService Provider.

5

Draft auditreport

30% 28 February2017

not mere receipt)of the quality ofthe outputs; and

b) Receipt ofinvoice from theService Provider.

Final signedaudit reportwith certifiedstatements

50% 31 March2017

Person(s) toreview/inspect/ approveoutputs/completedservices and authorize thedisbursement of payment

Country Director, UNDP Cambodia

Type of Contract to beSigned

☒ Contract for Professional Services

Preliminary Examination UNDP shall examine the Proposals to determine whether they are complete withrespect to minimum documentary requirements, whether the documents havebeen properly signed, whether or not the Proposer is in the UN Security Council1267/1989 Committee's list of terrorists and terrorist financiers, and in UNDP’slist of suspended and removed vendors, and whether the Proposals aregenerally in order, among other indicators that may be used at this stage.

The below requirements will be reviewed under Preliminary Examination beforeproceeding with the evaluation. UNDP may reject any Proposal at this stage.

1. Legally registered audit firm with Certificate of Registration of thebusiness, including Articles of Incorporation, or equivalent document.

2. Form for Submitting Service Provider’s Technical Proposal is dulycompleted and signed as per Annex-B (completion in the template inAnnex-B is mandatory for bidder as the form would allow bidders to confirmits conformity with the requirements defined in the Request for Proposaland all its attachments, as well as the provision of UNDP General ContractTerms and Conditions required under this process). Bidders may choose touse its own template and acceptable if it is duly signed by authorized personand confirm the same as Annex-B.

3. Technical and Financial Proposals are submitted in separate sealedenvelopes.

4. Proposer is not in the UN Security Council 1267/1989 Committee's list ofterrorists and terrorist financiers, and in UNDP’s list of suspended andremoved vendors.

Criteria for ContractAward

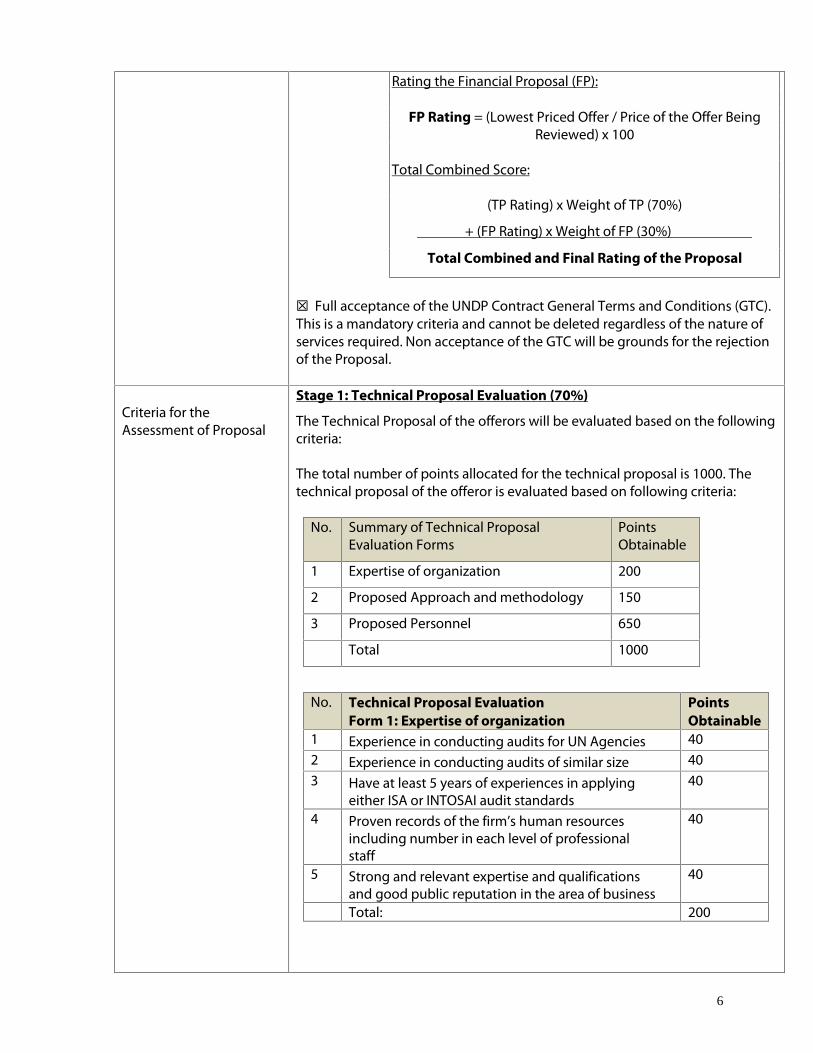

☒ Having received the Highest Combined Score (based on the 70%technical weight and 30% price weight distribution)

The total score for each proposal will be calculated independently by thefollowing formula:

Rating the Technical Proposal (TP):

TP Rating = (Total Score Obtained by the Offer / Max.Obtainable Score for TP) x 100

6

Rating the Financial Proposal (FP):

FP Rating = (Lowest Priced Offer / Price of the Offer BeingReviewed) x 100

Total Combined Score:

(TP Rating) x Weight of TP (70%)

+ (FP Rating) x Weight of FP (30%)

Total Combined and Final Rating of the Proposal

☒ Full acceptance of the UNDP Contract General Terms and Conditions (GTC).This is a mandatory criteria and cannot be deleted regardless of the nature ofservices required. Non acceptance of the GTC will be grounds for the rejectionof the Proposal.

Criteria for theAssessment of Proposal

Stage 1: Technical Proposal Evaluation (70%)

The Technical Proposal of the offerors will be evaluated based on the followingcriteria:

The total number of points allocated for the technical proposal is 1000. Thetechnical proposal of the offeror is evaluated based on following criteria:

No. Summary of Technical ProposalEvaluation Forms

PointsObtainable

1 Expertise of organization 200

2 Proposed Approach and methodology 150

3 Proposed Personnel 650

Total 1000

No. Technical Proposal EvaluationForm 1: Expertise of organization

PointsObtainable

1 Experience in conducting audits for UN Agencies 402 Experience in conducting audits of similar size 403 Have at least 5 years of experiences in applying

either ISA or INTOSAI audit standards40

4 Proven records of the firm’s human resourcesincluding number in each level of professionalstaff

40

5 Strong and relevant expertise and qualificationsand good public reputation in the area of business

40

Total: 200

7

No. Proposed Approach PointsObtainable

1 To what degree does the Offeror understand thetask? Have the important aspects of the task beenaddressed in sufficient detail?

50

2 Is the scope of task well defined and does itcorrespond to the TOR?

50

3 Is the presentation clear and is the sequence ofactivities and the planning logical, realistic andpromise efficient implementation to the project?

50

Total 150

No. Proposed personnel PointsObtainable

1 Audit manager (1 person): Master of Business Administration with

specialization in accounting, finance or relatedfield or ACCA/CPA accredited (10 points)

At least 10 year experiences of managing auditexercise of similar size (30 points)

Experience in supervising and instructing auditteams, certifying financial statements, reviewingprocurement process, providing audit ratings andconducting quality control (10 points)

Experience in audits of Development Projects inCambodia is an advantage (10 points)

60

2 Senior auditor (1 person): Having ACCA/CPA accreditation (30 points) At least 8 years of experience in the field of audit

(20 points) Experience in supervising and instructing audit

teams, certifying financial statements, reviewingprocurement process, providing audit ratings andconducting quality control (10 points)

Experiences in managing audits of developmentprojects in Cambodia (10 points)

70

3 National Accredited auditors (6 persons): (70 x 6persons) Having ACCA/CPA accreditation (30 points) At least 5 years of experience in the field of audits

(20 point) Experience in audits of development projects in

Cambodia (20 points)

420

8

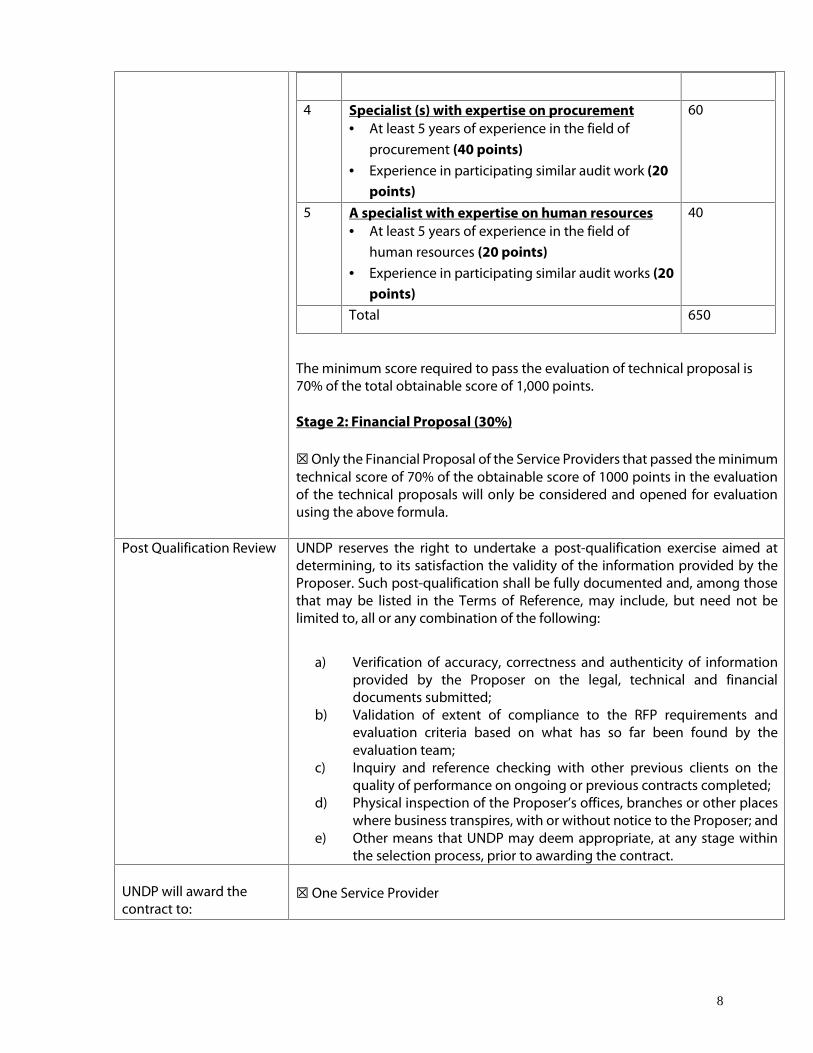

4 Specialist (s) with expertise on procurement At least 5 years of experience in the field of

procurement (40 points) Experience in participating similar audit work (20

points)

60

5 A specialist with expertise on human resources At least 5 years of experience in the field of

human resources (20 points) Experience in participating similar audit works (20

points)

40

Total 650

The minimum score required to pass the evaluation of technical proposal is70% of the total obtainable score of 1,000 points.

Stage 2: Financial Proposal (30%)

☒Only the Financial Proposal of the Service Providers that passed the minimumtechnical score of 70% of the obtainable score of 1000 points in the evaluationof the technical proposals will only be considered and opened for evaluationusing the above formula.

Post Qualification Review UNDP reserves the right to undertake a post-qualification exercise aimed atdetermining, to its satisfaction the validity of the information provided by theProposer. Such post-qualification shall be fully documented and, among thosethat may be listed in the Terms of Reference, may include, but need not belimited to, all or any combination of the following:

a) Verification of accuracy, correctness and authenticity of informationprovided by the Proposer on the legal, technical and financialdocuments submitted;

b) Validation of extent of compliance to the RFP requirements andevaluation criteria based on what has so far been found by theevaluation team;

c) Inquiry and reference checking with other previous clients on thequality of performance on ongoing or previous contracts completed;

d) Physical inspection of the Proposer’s offices, branches or other placeswhere business transpires, with or without notice to the Proposer; and

e) Other means that UNDP may deem appropriate, at any stage withinthe selection process, prior to awarding the contract.

UNDP will award thecontract to:

☒ One Service Provider

9

Annexes to this RFP4 Form for Submission of Technical Proposal (Annex B) Form for Submission of Financial Proposal (Annex C) General Terms and Conditions / Special Conditions (Annex D) Terms of Reference (Annex E)

Contact Person forInquiries(Written inquiries only)5

UNDP CambodiaRegistry Office (located in Building No. 3, Ground Floor)No. 53, Pasteur Street,PO Box 877, Phnom Penh, CambodiaTel: 023 216 167, Fax: 023 216 257Attn: Procurement Unit,E-mail: [email protected]

Any delay in UNDP’s response shall be not used as a reason for extending thedeadline for submission, unless UNDP determines that such an extension isnecessary and communicates a new deadline to the Proposers.

4 Where the information is available in the web, a URL for the information may simply be provided.5 This contact person and address is officially designated by UNDP. If inquiries are sent to other person/s oraddress/es, even if they are UNDP staff, UNDP shall have no obligation to respond nor can UNDP confirm thatthe query was received.

10

Annex B

FORM FOR SUBMITTING SERVICE PROVIDER’S TECHNICAL PROPOSAL6

(This Form must be submitted only using the Service Provider’s OfficialLetterhead/Stationery7)

[insert: Location].[insert: Date]

To: [insert: Name and Address of UNDP focal point]

Name of Proposing Organization / Firm:Country of Registration:Name of Contact Person for thisProposal:Address:Phone / Fax:Email:

Dear Sir/Madam:

We, the undersigned, hereby offer to render the following services to UNDP inconformity with the requirements defined in the Request for Proposal (RFP) Process No. 35-44188, and all of its attachments, as well as the provisions of the UNDP General Contract Termsand Conditions.

A. Qualifications of the Service Provider

This section should describe the organizational unit that will be responsible for the contract,and the general management approach towards this project. This should fully explain theBidder’s resources in terms of personnel and other resources necessary for achieving projectresults. The Service Provider must describe and explain how and why they are the best entitythat can deliver the requirements of UNDP by indicating the following:

a) Profile – provide description of the organization/firm including the year, staffs structure,and state/country of incorporation and a brief description of the Bidder’s presentactivities (focusing on the services related to the Proposal). The Bidder should describe itsexperience in similar projects;

b) Business Licenses – Registration Papers, Tax Payment Certification, etc.;c) Track Record – list of clients for similar services indicating description of contract scope,

contract duration, contract value, and contact references within the last 5 years;

6 This serves as a guide to the Service Provider in preparing the Proposal.7 Official Letterhead/Stationery must indicate contact details – addresses, email, phone and fax numbers – forverification purposes

11

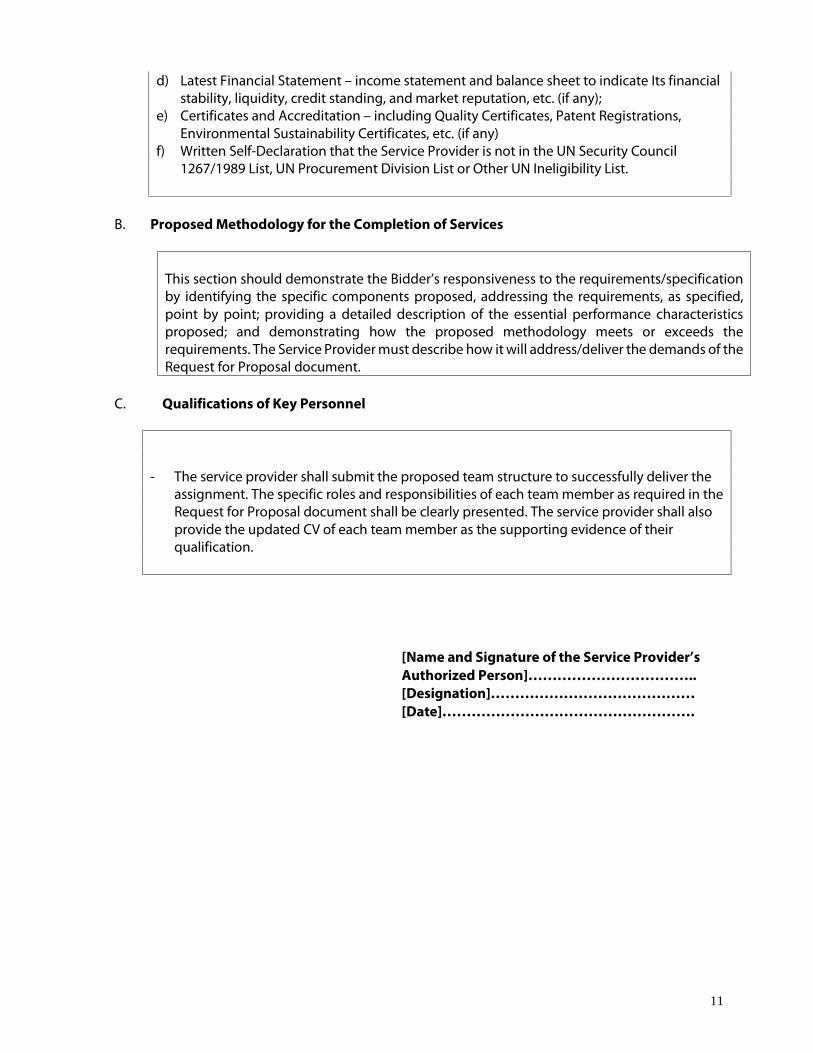

d) Latest Financial Statement – income statement and balance sheet to indicate Its financialstability, liquidity, credit standing, and market reputation, etc. (if any);

e) Certificates and Accreditation – including Quality Certificates, Patent Registrations,Environmental Sustainability Certificates, etc. (if any)

f) Written Self-Declaration that the Service Provider is not in the UN Security Council1267/1989 List, UN Procurement Division List or Other UN Ineligibility List.

B. Proposed Methodology for the Completion of Services

This section should demonstrate the Bidder’s responsiveness to the requirements/specificationby identifying the specific components proposed, addressing the requirements, as specified,point by point; providing a detailed description of the essential performance characteristicsproposed; and demonstrating how the proposed methodology meets or exceeds therequirements. The Service Provider must describe how it will address/deliver the demands of theRequest for Proposal document.

C. Qualifications of Key Personnel

- The service provider shall submit the proposed team structure to successfully deliver theassignment. The specific roles and responsibilities of each team member as required in theRequest for Proposal document shall be clearly presented. The service provider shall alsoprovide the updated CV of each team member as the supporting evidence of theirqualification.

[Name and Signature of the Service Provider’sAuthorized Person]……………………………..[Designation]……………………………………[Date]…………………………………………….

12

Annex C

FORM FOR SUBMITTING SERVICE PROVIDER’S FINANCIAL PROPOSAL8

(This Form must be submitted only using the Service Provider’s OfficialLetterhead/Stationery9)

[insert: Location].[insert: Date]

To: [insert: Name and Address of UNDP focal point]

The Financial Proposal must provide a detailed cost breakdown. Provide separate figures for eachfunctional grouping or category.

A. Cost Breakdown of Outputs/Tasks [This is only an Example]:

The Proposers are requested to provide the cost breakdown for each project based on the followingformat. UNDP shall use the cost breakdown for the price reasonability assessment purposes as wellas the calculation of price in the event that both parties have agreed to add new deliverables to thescope of Services.

No Cost Breakdown of Project Amount

1 Mine Action for Human Development

2 Cambodia Climate Change Alliance (CCCA) Phase II

3 Generating, Accessing and Using Information andKnowledge Related to the Three Rio Conventions (3Rio)

4 Multi-media Initiative for Youth

5 Partnership for Development Results Phase 2

6 A Project to be randomly selected (To be confirmedafter selection process)Total Lump Sum Amount

8 This serves as a guide to the Service Provider in preparing the Proposal.9 Official Letterhead/Stationery must indicate contact details – addresses, email, phone and fax numbers – forverification purposes

13

B. Cost Breakdown by Cost Component [This is only an Example]:

Description of ActivityTotal Period of

Engagement

Total PersonRemuneration/Unit

Rate

Total

I. Personnel Services1. Services from Home Office

a. Expertise 1b. Expertise 2

2. Services from Field Officesa. Expertise 1b. Expertise 2

II. Other Related Costs1. Travel Costs2. Daily Allowance3. Communications4. Reproduction5. Equipment Lease6. Others

[Name and Signature of the Service Provider’sAuthorized Person][Designation][Date]

NOTE: WHEN SUBMITTING YOUR BID DOCUMENTS, PLEASE CAREFULLY PLACE THETECHNICAL AND FINANCIAL PROPOSALS IN SEPARATE SEALED ENVELOPES.

14

Annex D

General Terms and Conditions for Services

1.0 LEGAL STATUS:

The Contractor shall be considered as having the legal status of an independent contractorvis-à-vis the United Nations Development Programme (UNDP). The Contractor’s personneland sub-contractors shall not be considered in any respect as being the employees or agentsof UNDP or the United Nations.

2.0 SOURCE OF INSTRUCTIONS:

The Contractor shall neither seek nor accept instructions from any authority external to UNDPin connection with the performance of its services under this Contract. The Contractor shallrefrain from any action that may adversely affect UNDP or the United Nations and shall fulfillits commitments with the fullest regard to the interests of UNDP.

3.0 CONTRACTOR'S RESPONSIBILITY FOR EMPLOYEES:

The Contractor shall be responsible for the professional and technical competence of itsemployees and will select, for work under this Contract, reliable individuals who will performeffectively in the implementation of this Contract, respect the local customs, and conform toa high standard of moral and ethical conduct.

4.0 ASSIGNMENT:

The Contractor shall not assign, transfer, pledge or make other disposition of this Contract orany part thereof, or any of the Contractor's rights, claims or obligations under this Contractexcept with the prior written consent of UNDP.

5.0 SUB-CONTRACTING:

In the event the Contractor requires the services of sub-contractors, the Contractor shallobtain the prior written approval and clearance of UNDP for all sub-contractors. The approvalof UNDP of a sub-contractor shall not relieve the Contractor of any of its obligations underthis Contract. The terms of any sub-contract shall be subject to and conform to the provisionsof this Contract.

6.0 OFFICIALS NOT TO BENEFIT:

The Contractor warrants that no official of UNDP or the United Nations has received or will beoffered by the Contractor any direct or indirect benefit arising from this Contract or the awardthereof. The Contractor agrees that breach of this provision is a breach of an essential termof this Contract.

7.0 INDEMNIFICATION:

The Contractor shall indemnify, hold and save harmless, and defend, at its own expense,UNDP, its officials, agents, servants and employees from and against all suits, claims,

15

demands, and liability of any nature or kind, including their costs and expenses, arising out ofacts or omissions of the Contractor, or the Contractor's employees, officers, agents or sub-contractors, in the performance of this Contract. This provision shall extend, inter alia, toclaims and liability in the nature of workmen's compensation, products liability and liabilityarising out of the use of patented inventions or devices, copyrighted material or otherintellectual property by the Contractor, its employees, officers, agents, servants or sub-contractors. The obligations under this Article do not lapse upon termination of this Contract.

8.0 INSURANCE AND LIABILITIES TO THIRD PARTIES:

8.1 The Contractor shall provide and thereafter maintain insurance against all risks inrespect of its property and any equipment used for the execution of this Contract.

8.2 The Contractor shall provide and thereafter maintain all appropriate workmen'scompensation insurance, or the equivalent, with respect to its employees to coverclaims for personal injury or death in connection with this Contract.

8.3 The Contractor shall also provide and thereafter maintain liability insurance in anadequate amount to cover third party claims for death or bodily injury, or loss of ordamage to property, arising from or in connection with the provision of services underthis Contract or the operation of any vehicles, boats, airplanes or other equipmentowned or leased by the Contractor or its agents, servants, employees or sub-contractors performing work or services in connection with this Contract.

8.4 Except for the workmen's compensation insurance, the insurance policies under thisArticle shall:

8.4.1 Name UNDP as additional insured;8.4.2 Include a waiver of subrogation of the Contractor's rights to the insurance

carrier against the UNDP;8.4.3 Provide that the UNDP shall receive thirty (30) days written notice from the

insurers prior to any cancellation or change of coverage.8.5 The Contractor shall, upon request, provide the UNDP with satisfactory

evidence of the insurance required under this Article.

9.0 ENCUMBRANCES/LIENS:

The Contractor shall not cause or permit any lien, attachment or other encumbrance by anyperson to be placed on file or to remain on file in any public office or on file with the UNDPagainst any monies due or to become due for any work done or materials furnished underthis Contract, or by reason of any other claim or demand against the Contractor.

10.0 TITLE TO EQUIPMENT:

Title to any equipment and supplies that may be furnished by UNDP shall rest with UNDP andany such equipment shall be returned to UNDP at the conclusion of this Contract or when nolonger needed by the Contractor. Such equipment, when returned to UNDP, shall be in thesame condition as when delivered to the Contractor, subject to normal wear and tear. TheContractor shall be liable to compensate UNDP for equipment determined to be damaged ordegraded beyond normal wear and tear.

16

11.0 COPYRIGHT, PATENTS AND OTHER PROPRIETARY RIGHTS:

11.1 Except as is otherwise expressly provided in writing in the Contract, the UNDP shallbe entitled to all intellectual property and other proprietary rights including, but notlimited to, patents, copyrights, and trademarks, with regard to products, processes,inventions, ideas, know-how, or documents and other materials which the Contractorhas developed for the UNDP under the Contract and which bear a direct relation toor are produced or prepared or collected in consequence of, or during the course of,the performance of the Contract, and the Contractor acknowledges and agrees thatsuch products, documents and other materials constitute works made for hire for theUNDP.

11.2 To the extent that any such intellectual property or other proprietary rights consist ofany intellectual property or other proprietary rights of the Contractor: (i) that pre-existed the performance by the Contractor of its obligations under the Contract, or (ii)that the Contractor may develop or acquire, or may have developed or acquired,independently of the performance of its obligations under the Contract, the UNDPdoes not and shall not claim any ownership interest thereto, and the Contractorgrants to the UNDP a perpetual license to use such intellectual property or otherproprietary right solely for the purposes of and in accordance with the requirementsof the Contract.

11.3 At the request of the UNDP; the Contractor shall take all necessary steps, execute allnecessary documents and generally assist in securing such proprietary rights andtransferring or licensing them to the UNDP in compliance with the requirements ofthe applicable law and of the Contract.

11.4 Subject to the foregoing provisions, all maps, drawings, photographs, mosaics, plans,reports, estimates, recommendations, documents, and all other data compiled by orreceived by the Contractor under the Contract shall be the property of the UNDP, shallbe made available for use or inspection by the UNDP at reasonable times and inreasonable places, shall be treated as confidential, and shall be delivered only toUNDP authorized officials on completion of work under the Contract.

12.0 USE OF NAME, EMBLEM OR OFFICIAL SEAL OF UNDP OR THE UNITED NATIONS:

The Contractor shall not advertise or otherwise make public the fact that it is a Contractorwith UNDP, nor shall the Contractor, in any manner whatsoever use the name, emblem orofficial seal of UNDP or THE United Nations, or any abbreviation of the name of UNDP orUnited Nations in connection with its business or otherwise.

13.0 CONFIDENTIAL NATURE OF DOCUMENTS AND INFORMATION:

Information and data that is considered proprietary by either Party and that is delivered ordisclosed by one Party (“Discloser”) to the other Party (“Recipient”) during the course ofperformance of the Contract, and that is designated as confidential (“Information”), shall beheld in confidence by that Party and shall be handled as follows:

13.1 The recipient (“Recipient”) of such information shall:

17

13.1.1 use the same care and discretion to avoid disclosure, publication ordissemination of the Discloser’s Information as it uses with its own similarinformation that it does not wish to disclose, publish or disseminate; and,

13.1.2 use the Discloser’s Information solely for the purpose for which it wasdisclosed.

13.2 Provided that the Recipient has a written agreement with the following persons orentities requiring them to treat the Information confidential in accordance with theContract and this Article 13, the Recipient may disclose Information to:

13.2.1 any other party with the Discloser’s prior written consent; and,13.2.2 the Recipient’s employees, officials, representatives and agents who have a

need to know such Information for purposes of performing obligations underthe Contract, and employees officials, representatives and agents of any legalentity that it controls controls it, or with which it is under common control,who have a need to know such Information for purposes of performingobligations under the Contract, provided that, for these purposes a controlledlegal entity means:

13.2.2.1 a corporate entity in which the Party owns or otherwise controls,whether directly or indirectly, over fifty percent (50%) of votingshares thereof; or,

13.2.2.2 any entity over which the Party exercises effective managerialcontrol; or,

13.2.2.3 for the UNDP, an affiliated Fund such as UNCDF, UNIFEM and UNV.

13.3 The Contractor may disclose Information to the extent required by law, provided that,subject to and without any waiver of the privileges and immunities of the UnitedNations, the Contractor will give the UNDP sufficient prior notice of a request for thedisclosure of Information in order to allow the UNDP to have a reasonableopportunity to take protective measures or such other action as may be appropriatebefore any such disclosure is made.

13.4 The UNDP may disclose Information to the extent as required pursuant to the Charterof the UN, resolutions or regulations of the General Assembly, or rules promulgatedby the Secretary-General.

13.5 The Recipient shall not be precluded from disclosing Information that is obtained bythe Recipient from a third party without restriction, is disclosed by the Discloser to athird party without any obligation of confidentiality, is previously known by theRecipient, or at any time is developed by the Recipient completely independently ofany disclosures hereunder.

13.6 These obligations and restrictions of confidentiality shall be effective during the termof the Contract, including any extension thereof, and, unless otherwise provided inthe Contract, shall remain effective following any termination of the Contract.

14.0 FORCE MAJEURE; OTHER CHANGES IN CONDITIONS

14.1 In the event of and as soon as possible after the occurrence of any cause constitutingforce majeure, the Contractor shall give notice and full particulars in writing to the

18

UNDP, of such occurrence or change if the Contractor is thereby rendered unable,wholly or in part, to perform its obligations and meet its responsibilities under thisContract. The Contractor shall also notify the UNDP of any other changes inconditions or the occurrence of any event that interferes or threatens to interfere withits performance of this Contract. On receipt of the notice required under this Article,the UNDP shall take such action as, in its sole discretion; it considers to be appropriateor necessary in the circumstances, including the granting to the Contractor of areasonable extension of time in which to perform its obligations under this Contract.

14.2 If the Contractor is rendered permanently unable, wholly, or in part, by reason of forcemajeure to perform its obligations and meet its responsibilities under this Contract,the UNDP shall have the right to suspend or terminate this Contract on the sameterms and conditions as are provided for in Article 15, "Termination", except that theperiod of notice shall be seven (7) days instead of thirty (30) days.

14.3 Force majeure as used in this Article means acts of God, war (whether declared or not),invasion, revolution, insurrection, or other acts of a similar nature or force.

14.4 The Contractor acknowledges and agrees that, with respect to any obligations underthe Contract that the Contractor must perform in or for any areas in which the UNDPis engaged in, preparing to engage in, or disengaging from any peacekeeping,humanitarian or similar operations, any delays or failure to perform such obligationsarising from or relating to harsh conditions within such areas or to any incidents ofcivil unrest occurring in such areas shall not, in and of itself, constitute force majeureunder the Contract..

15.0 TERMINATION

15.1 Either party may terminate this Contract for cause, in whole or in part, upon thirty (30)days notice, in writing, to the other party. The initiation of arbitral proceedings inaccordance with Article 16.2 (“Arbitration”), below, shall not be deemed a terminationof this Contract.

15.2 UNDP reserves the right to terminate without cause this Contract at any time upon 15days prior written notice to the Contractor, in which case UNDP shall reimburse theContractor for all reasonable costs incurred by the Contractor prior to receipt of thenotice of termination.

15.3 In the event of any termination by UNDP under this Article, no payment shall be duefrom UNDP to the Contractor except for work and services satisfactorily performed inconformity with the express terms of this Contract.

15.4 Should the Contractor be adjudged bankrupt, or be liquidated or become insolvent,or should the Contractor make an assignment for the benefit of its creditors, or shoulda Receiver be appointed on account of the insolvency of the Contractor, the UNDPmay, without prejudice to any other right or remedy it may have under the terms ofthese conditions, terminate this Contract forthwith. The Contractor shall immediatelyinform the UNDP of the occurrence of any of the above events.

16.0 SETTLEMENT OF DISPUTES

19

16.1 Amicable Settlement: The Parties shall use their best efforts to settle amicably anydispute, controversy or claim arising out of this Contract or the breach, terminationor invalidity thereof. Where the parties wish to seek such an amicable settlementthrough conciliation, the conciliation shall take place in accordance with theUNCITRAL Conciliation Rules then obtaining, or according to such other procedure asmay be agreed between the parties.

16.2 Arbitration: Any dispute, controversy, or claim between the Parties arising out of theContract or the breach, termination, or invalidity thereof, unless settled amicablyunder Article 16.1, above, within sixty (60) days after receipt by one Party of the otherParty’s written request for such amicable settlement, shall be referred by either Partyto arbitration in accordance with the UNCITRAL Arbitration Rules then obtaining. Thedecisions of the arbitral tribunal shall be based on general principles of internationalcommercial law. For all evidentiary questions, the arbitral tribunal shall be guided bythe Supplementary Rules Governing the Presentation and Reception of Evidence inInternational Commercial Arbitration of the International Bar Association, 28 May1983 edition. The arbitral tribunal shall be empowered to order the return ordestruction of goods or any property, whether tangible or intangible, or of anyconfidential information provided under the Contract, order the termination of theContract, or order that any other protective measures be taken with respect to thegoods, services or any other property, whether tangible or intangible, or of anyconfidential information provided under the Contract, as appropriate, all inaccordance with the authority of the arbitral tribunal pursuant to Article 26 (“InterimMeasures of Protection”) and Article 32 (“Form and Effect of the Award”) of theUNCITRAL Arbitration Rules. The arbitral tribunal shall have no authority to awardpunitive damages. In addition, unless otherwise expressly provided in the Contract,the arbitral tribunal shall have no authority to award interest in excess of the LondonInter-Bank Offered Rate (“LIBOR”) then prevailing, and any such interest shall besimple interest only. The Parties shall be bound by any arbitration award rendered asa result of such arbitration as the final adjudication of any such dispute, controversy,or claim.

17.0 PRIVILEGES AND IMMUNITIES:

Nothing in or relating to this Contract shall be deemed a waiver, express or implied, of any ofthe privileges and immunities of the United Nations, including its subsidiary organs.

18.0 TAX EXEMPTION

18.1 Section 7 of the Convention on the Privileges and Immunities of the United Nationsprovides, inter-alia that the United Nations, including its subsidiary organs, is exemptfrom all direct taxes, except charges for public utility services, and is exempt fromcustoms duties and charges of a similar nature in respect of articles imported orexported for its official use. In the event any governmental authority refuses torecognize the United Nations exemption from such taxes, duties or charges, theContractor shall immediately consult with the UNDP to determine a mutuallyacceptable procedure.

18.2 Accordingly, the Contractor authorizes UNDP to deduct from the Contractor's invoiceany amount representing such taxes, duties or charges, unless the Contractor hasconsulted with the UNDP before the payment thereof and the UNDP has, in each

20

instance, specifically authorized the Contractor to pay such taxes, duties or chargesunder protest. In that event, the Contractor shall provide the UNDP with writtenevidence that payment of such taxes, duties or charges has been made andappropriately authorized.

19.0 CHILD LABOUR

19.1 The Contractor represents and warrants that neither it, nor any of its suppliers isengaged in any practice inconsistent with the rights set forth in the Convention onthe Rights of the Child, including Article 32 thereof, which, inter alia, requires that achild shall be protected from performing any work that is likely to be hazardous or tointerfere with the child's education, or to be harmful to the child's health or physicalmental, spiritual, moral or social development.

19.2 Any breach of this representation and warranty shall entitle UNDP to terminate thisContract immediately upon notice to the Contractor, at no cost to UNDP.

20.0 MINES:

20.1 The Contractor represents and warrants that neither it nor any of its suppliers isactively and directly engaged in patent activities, development, assembly,production, trade or manufacture of mines or in such activities in respect ofcomponents primarily utilized in the manufacture of Mines. The term "Mines" meansthose devices defined in Article 2, Paragraphs 1, 4 and 5 of Protocol II annexed to theConvention on Prohibitions and Restrictions on the Use of Certain ConventionalWeapons Which May Be Deemed to Be Excessively Injurious or to Have IndiscriminateEffects of 1980.

20.2 Any breach of this representation and warranty shall entitle UNDP to terminate thisContract immediately upon notice to the Contractor, without any liability fortermination charges or any other liability of any kind of UNDP.

21.0 OBSERVANCE OF THE LAW:

The Contractor shall comply with all laws, ordinances, rules, and regulations bearing upon theperformance of its obligations under the terms of this Contract.

22.0 SEXUAL EXPLOITATION:

22.1 The Contractor shall take all appropriate measures to prevent sexual exploitation orabuse of anyone by it or by any of its employees or any other persons who may beengaged by the Contractor to perform any services under the Contract. For thesepurposes, sexual activity with any person less than eighteen years of age, regardlessof any laws relating to consent, shall constitute the sexual exploitation and abuse ofsuch person. In addition, the Contractor shall refrain from, and shall take allappropriate measures to prohibit its employees or other persons engaged by it from,exchanging any money, goods, services, offers of employment or other things ofvalue, for sexual favors or activities, or from engaging in any sexual activities that areexploitive or degrading to any person. The Contractor acknowledges and agrees thatthe provisions hereof constitute an essential term of the Contract and that any breachof this representation and warranty shall entitle UNDP to terminate the Contract

21

immediately upon notice to the Contractor, without any liability for terminationcharges or any other liability of any kind.

22.2 The UNDP shall not apply the foregoing standard relating to age in any case in whichthe Contractor’s personnel or any other person who may be engaged by theContractor to perform any services under the Contract is married to the person lessthan the age of eighteen years with whom sexual activity has occurred and in whichsuch marriage is recognized as valid under the laws of the country of citizenship ofsuch Contractor’s personnel or such other person who may be engaged by theContractor to perform any services under the Contract.

23.0 AUTHORITY TO MODIFY:

Pursuant to the Financial Regulations and Rules of UNDP, only the UNDP Authorized Officialpossesses the authority to agree on behalf of UNDP to any modification of or change in thisContract, to a waiver of any of its provisions or to any additional contractual relationship ofany kind with the Contractor. Accordingly, no modification or change in this Contract shall bevalid and enforceable against UNDP unless provided by an amendment to this Contractsigned by the Contractor and jointly by the UNDP Authorized Official.

2

ANNEX E - TERMS OF REFERENCE FOR HACT FINANCIAL AUDIT

Period: 01 January to 31 December 2016

TABLE OF CONTENTS

PageINTRODUCTION .......................................................................................................................................... 3

A. Background .................................................................................................................................. 6

B. Project Management.................................................................................................................... 7

C. Consultations with concerned parties......................................................................................... 8

D. Description of Financial Reports (UNDP CDR) to be audited...................................................... 8

E. Audit Services Required ............................................................................................................. 10

F. The Audit Report and Management Letter ............................................................................... 11

NNEX : UDIT S D ..................................................................................... 16

............................................................................. 18

................................................................................................ 19

................................................................................. 24

............................................. 25

ANNEX 6: Priority of Audit Observations and Recommendations.............................................. 26

........................................ 24

.................................................... 25

. 27

............................................. 29

............................................................................ 31

3

INTRODUCTION

Throughout this document the term "implementing partner" is used to refer to the institution designated tomanage the project. Where the project is nationally implemented (NIM), this will refer to a governmentinstitution. Where the project is NGO executed, this will refer to an NGO. The term "government co-ordinatingauthority" refers to the Cambodia Rehabilitation and Development Board/ Council for the Development ofCambodia (CRDB/CDC), which is the official UNDP counterpart.

This TOR has been revised to highlight requirements in the audit services required (Part E and Annex 1) as wellas areas to be covered in the audit report and management letter (Part F and Annex 3), as follows:

Auditors must certify, express an opinion, and quantify the Net Financial Impact ( N F I ) on eachof the following:

(i) UNDP Statement of Expenses - the Combined Delivery Report (CDR) - for the period1 January to 31 December 2016

(ii) Statement of Cash Position reported by the project as at 31 December 2016(iii) Statement of Assets and Equipment as at 31 December 2016

Auditors must indicate the risks associated with their findings and provide a categorization by risk:High, Medium, or Low.

Auditors must provide the monetary value of the NFI of the qualification if the audit opinion on theCDR is Qualified, Adverse or Disclaimer.

Follow-up to resolve Audit Observations

1. The United Nations Board of Auditors (UN BoA) has commented on the NGO/NIM audit results and thecases where they noted a lack of conclusive actions to properly address an audit qualification in the previousyear audit and the related NFI. They also commented on the recurrence of the same significant audit issues inthe same projects without being duly resolved.

A Critical Audit Requirement

2. Following the International Standards on Auditing (ISA 450 and ISA 710), there is a requirementregarding a previous year modified audit opinion.1 This audit standard requires that auditors, when expressingan opinion on this year’s statements, take into account the possible effect of a prior year modified opinion thathas not been properly corrected or resolved.

3. Consequently, a previous year modified opinion that has not been properly resolved may cause theauditors to issue a modified opinion in their current year audit report. If proper attention is not paid to thisaspect, the risk could be a significant accumulation of unresolved modified opinions from previous years thatwould lead the UN BoA to issue a modified audit opinion on UNDP financial statements. (Refer to Annex 5)

4. Country offices (COs) must ensure the audit services are adequately covered as specified in thepresent TOR and CDRs are duly certified by the implementing partners and auditors and signed by UNDP COmanagement and attached to the audit reports; the same applies for the Statement of Cash Position (cash andbank balances of the project) and Statement of Assets and Equipment. If the project does not hold any assetsor equipment or there is no cash at hand or bank account, the auditors must clearly indicate this in theopinion page and certify it.

Annex 1 provides the audit services required and standard scope of audit.

Annex 2 describes the qualifications of an auditor and may help in the process ofselecting auditors.

1 A “modified” audit opinion means either a qualified opinion, a disclaimer of opinion or an adverse opinion.

4

Where the TOR is being supplied to a short list of firms as part of a request for proposals(RFP) and the firms short listed have been pre-qualified, then the list of qualificationswould not be needed.

Annex 3 is a sample audit report that needs to be submitted by the auditor (ISA 705, 706). Amanagement letter needs to be attached to the audit report.

Annex 4 provides a definition of audit opinions (ISA 700).

Annex 5 provides guidance on Reporting Prior Year Modified opinion not corrected (ISA 450 and710).

Annex 6 defines the three risk categories of audit observations and recommendations.

Annex 7 provides a template sample of certified prior year updated action plan (FY2014) thatneeds to be uploaded in CARDS.

Annex 8 provides a template for audit data and observations for FY2016 audits that auditorsneed to submit and the CO copy paste in CARDS the information.

Annex 9 provides guidance on formulating audit observations and recommendations.

Annex 10 provides guidance on Audit Materiality (ISA 320 and 450).

Annex 11 provides

6

A. Background

HACT Financial Audit is the annual audit exercise on UNDP programmes/projects which are implemented byour Implementing Partners within the framework of Harmonized Approach to Cash Transfer (HACT) of theUnited Nations system. Country Programme Action Plan 2016-18 agreed between the Cambodian Governmentand UNDP lays out the scope of the UNDP’s support to development in Cambodia. As Cambodia transitionsinto the next stage of development, the focus of UNDP’s intervention is to foster partnerships that address theimpediments to sustainable development, particularly in the areas of human capital formation and economicvulnerability, critical for LDC graduation. UNDP will be a partner for policy, knowledge and innovation throughevidence-based research for articulating policy options, and mobilizing knowledge and resources for policychoices that better people’s lives.

In this audit exercise the UNDP Country Office wishes to engage an independent audit firm to conduct auditof six projects, namely, the Mine Action for Human Development; Cambodia Climate Change Alliance Phase 2;Multi-media Initiative for Youth; Partnership for Development Results Phase 2; Generating, Accessing andUsing Information and Knowledge Related to the Three Rio Conventions projects; and another project to beselected on a random basis.

Background information on projects to be audited:

Mine Action for Human Development: The project seeks to support the government in the development ofholistic approaches that could help maximizing mine action results on human development. In particular, theproject seeks to support: (1) the development of performance monitoring systems that could link mine actionto human development in a systematic manner and ensure gender disaggregated and poverty relatedindicators are factored in; (2) conduct of land release activities that in respect of gender equality principle andthe Gender Mainstreaming in Mine Action Plan 2013-15 would involve poor communities in responsible andeffective land release, and contractors in effective and efficient use of new technologies that allow for therelease of bigger areas at the minor cost.

Cambodia Climate Change Alliance Phase 2: The Overall Objective of the project is to strengthen nationalsystems and capacities to support the coordination and implementation of Cambodia’s climate changeresponse, contributing to a greener, low carbon, climate-resilient, equitable, sustainable and knowledge-basedsociety. The Specific Objective will be to contribute to the implementation of the Cambodia Climate ChangeStrategic Plan. CCCA programme focus on three main drivers of change: (1) strengthening the governance ofclimate change, (2) harnessing public and private, domestic and external resources in support of the CCCSPvision and (3) Developing human and technological capital for the climate change response.

Generating, Accessing and Using Information and Knowledge Related to the Three Rio Conventions: Thisproject aims harmonize existing environmental information systems, integrating internationally acceptedmeasurement standards and methodologies, as well as develop a more consistent reporting on the globalenvironment. The project will support the development of national capacities to effectively and efficientlystandardize environmental related information that is generated on the implementation of the Rio Conventionsin Cambodia, and give open-access to this information. In parallel, the project will support the strengthening ofCambodia’s capacity to better engage stakeholders and better coordinate the implementation of the RioConventions in the country. In addition, project resources will be used to improve the use of environmentalrelated information for the development of innovative tools supporting decision-making processes related tothe implementation of the Rio Conventions. Project support will also include capacity development in usingthis environmental related knowledge of national institutions involved in international negotiations atConventions COPs, as well as using this knowledge to produce national reports meeting Conventions reportingobligations.

Multi-media Initiative for Youth: Started in November 2014, the project was initially aimed at improving theknowledge and efficacy of young people (aged 15-30) especially young women in negotiating with decision

7

makers for better employment opportunities and livelihood enhancement through multi-media. Building onthis success, the project has extended to give young people particularly urban and rural youth and especiallyyoung women, who are in unemployment or in vulnerable employment the knowledge, soft skills and theconfidence they need to be able to both identify alternative jobs and mobilize support from their influencers(such as family members) to apply for these jobs or apply for training that will enable them to get such roles.

Partnership for Development Results Phase 2: The project supports the Royal Government of Cambodia tostrengthen capacities and systems for managing multiples sources of development finance in the context ofattaining Middle Income Country status. The project supports the production, analysis and management ofdata, information and knowledge that can inform resource allocation and programme implementation toensure increased support to targeting of expenditure towards programmes that promote poverty reductionand inclusive sustainable growth, specifically in support of the RS-3 and NSDP as well as the localization of theSDGs.

No. Project Name Implementing Partner (IP)

ApproximateExpenditure by IP for

FY 2016

1Mine Action for HumanDevelopment

Mine Action and Victim AssistanceAuthority

$1,951,760

2Cambodia Climate Change Alliance(CCCA) Phase II

Ministry of Environment$1,544,549

3

Generating, Accessing and UsingInformation and KnowledgeRelated to the Three RioConventions (3 Rio)

Ministry of Environment$ 230,000

4 Multi-media Initiative for Youth BBC Media Action$ 915,186

5Partnership for DevelopmentResults Phase 2

Cambodia Rehabilitation andDevelopment Board/CDC

$ 236,364

6 A Project to be randomly selectedBetween $240,000 to

460,000

The TOR is directed to the audit of UNDP financial statements, which are referred to as Combined DeliveryReports (CDR).

B. Project Management

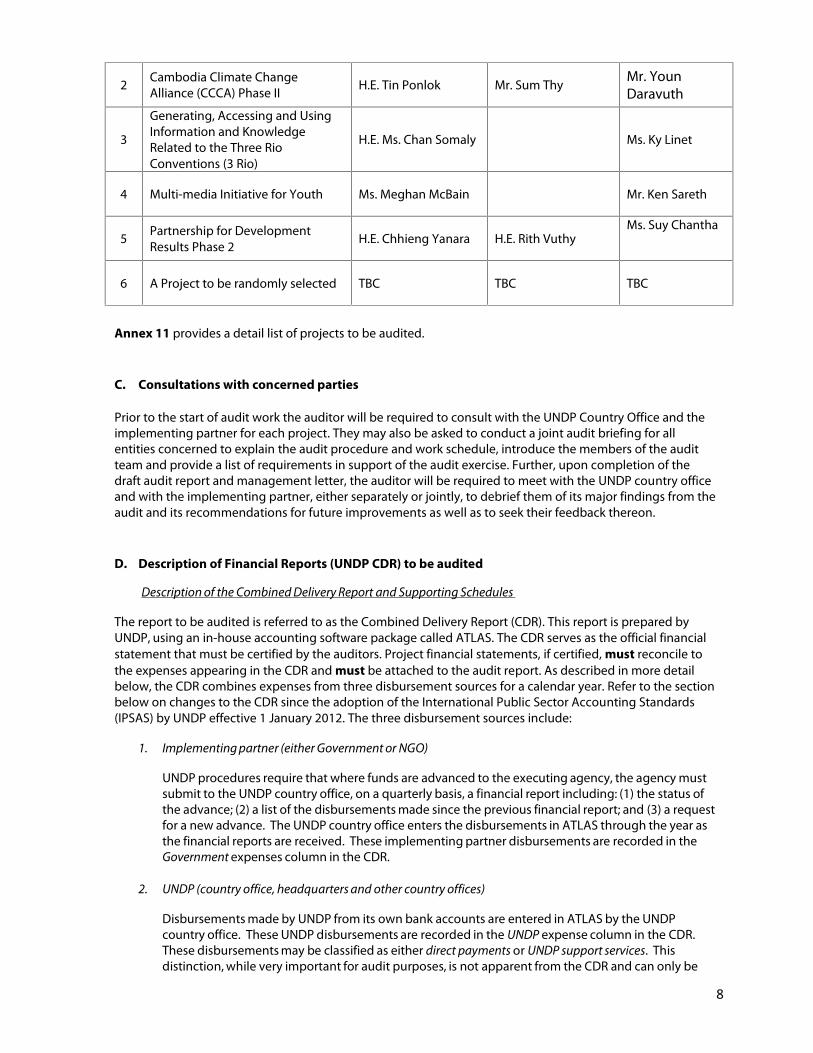

As indicated above, various entities are responsible for implementing UNDP-assisted projects. The relevantofficials responsible for the projects are listed below. They act as primary contact persons in the implementingpartner agencies for this audit exercise.

Project Name National ProjectDirector

National ProjectManager orequivalent

Project Finance

1Mine Action for HumanDevelopment

H.E. Ly Thuch H.E. Ly Panharith Ms. Sreng Sophea

8

2Cambodia Climate ChangeAlliance (CCCA) Phase II

H.E. Tin Ponlok Mr. Sum ThyMr. YounDaravuth

3

Generating, Accessing and UsingInformation and KnowledgeRelated to the Three RioConventions (3 Rio)

H.E. Ms. Chan Somaly Ms. Ky Linet

4 Multi-media Initiative for Youth Ms. Meghan McBain Mr. Ken Sareth

5Partnership for DevelopmentResults Phase 2

H.E. Chhieng Yanara H.E. Rith VuthyMs. Suy Chantha

6 A Project to be randomly selected TBC TBC TBC

Annex 11 provides a detail list of projects to be audited.

C. Consultations with concerned parties

Prior to the start of audit work the auditor will be required to consult with the UNDP Country Office and theimplementing partner for each project. They may also be asked to conduct a joint audit briefing for allentities concerned to explain the audit procedure and work schedule, introduce the members of the auditteam and provide a list of requirements in support of the audit exercise. Further, upon completion of thedraft audit report and management letter, the auditor will be required to meet with the UNDP country officeand with the implementing partner, either separately or jointly, to debrief them of its major findings from theaudit and its recommendations for future improvements as well as to seek their feedback thereon.

D. Description of Financial Reports (UNDP CDR) to be audited

Description of the Combined Delivery Report and Supporting Schedules

The report to be audited is referred to as the Combined Delivery Report (CDR). This report is prepared byUNDP, using an in-house accounting software package called ATLAS. The CDR serves as the official financialstatement that must be certified by the auditors. Project financial statements, if certified, must reconcile tothe expenses appearing in the CDR and must be attached to the audit report. As described in more detailbelow, the CDR combines expenses from three disbursement sources for a calendar year. Refer to the sectionbelow on changes to the CDR since the adoption of the International Public Sector Accounting Standards(IPSAS) by UNDP effective 1 January 2012. The three disbursement sources include:

1. Implementing partner (either Government or NGO)

UNDP procedures require that where funds are advanced to the executing agency, the agency mustsubmit to the UNDP country office, on a quarterly basis, a financial report including: (1) the status ofthe advance; (2) a list of the disbursements made since the previous financial report; and (3) a requestfor a new advance. The UNDP country office enters the disbursements in ATLAS through the year asthe financial reports are received. These implementing partner disbursements are recorded in theGovernment expenses column in the CDR.

2. UNDP (country office, headquarters and other country offices)

Disbursements made by UNDP from its own bank accounts are entered in ATLAS by the UNDPcountry office. These UNDP disbursements are recorded in the UNDP expense column in the CDR.These disbursements may be classified as either direct payments or UNDP support services. Thisdistinction, while very important for audit purposes, is not apparent from the CDR and can only be

9

provided by the UNDP country office as a supporting schedule. A brief description of each categoryis provided below.

a) Direct Payments - This is where the implementing partner is responsible for the expenses butrequested UNDP to effect payment to the vendor/consultant on its behalf. The implementingpartner is accountable for the disbursement and maintains all supporting documentation.UNDP simply effects payments on the basis of properly authorized requests and gives theimplementing partner a copy of the related disbursement voucher as evidence that paymentwas made.

b) UNDP Support Services - This is where the government and UNDP have agreed that UNDP willprovide support services to the project and signed a Letter of Agreement. These supportservices must be described in the Letter of Agreement (LOA). UNDP is fully responsible andaccountable for these expenses and, accordingly, maintains all supporting documentation forthe disbursement. These expenses are outside the scope of audit and, therefore, will not bereviewed by the auditors. This scope limitation should not be used as a reason for issuing aqualified audit opinion on the CDR. Where there is no signed Letter of Agreement for UNDPSupport Services or a Country Programme Action Plan (CPAP) with the respective clauses of theLOA for UNDP Support Services, the audit should also cover the UNDP expenses under COsupport. The CO must include this information in the TOR/contract for the auditors.

3. UN agencies

The UN agency reports its expenses to UNDP and to the government. The UNDP country officeenters the expenses in ATLAS. These UN agency expenses are recorded in the UN agenciesexpense column in the CDR. Note: Any expenses under this column are outside the auditors’scope of audit. UN entities are audited under their own audit arrangement, following the ‘SingleAudit’ principle and are not covered by UNDP’s audit regime.

At the end of the year, after receiving the fourth quarter financial report from the implementing partner andthe year-end expense report from the UN agency, UNDP prepares the CDR and submits it to theimplementing partner for signature. UNDP will provide the auditor with the signed CDR together with thefollowing supporting documentation.

1. The quarterly financial reports submitted by the implementing partner.2. A list of the direct payments processed by UNDP at the request of the implementing partner.3. A list of the disbursement made by UNDP as part of support services provided to the

implementing partner.4. The UN agency expenses statement for the year.5. Letter of Agreement for UNDP support services signed between UNDP and the Government (or

CPAP with relevant clauses regarding UNDP support services).7. Relevant financial reports that show expenses of UNDP CO support, if there is no Letter

of Agreement.

Note: With the adoption of the International Public Sector Accounting Standards (IPSAS) by UNDPeffective 1 January 2012, the CDR is now prepared in two sections; the first section containing thetotal expense information as explained above (by Implementing Partner, UNDP and UN Agencies) andthe second section showing the following information:

Outstanding NEX advances Un-depreciated Fixed Assets Inventory Prepayments Commitments

In addition to the verification of the total project expense reflected in the CDR, the auditors will nowbe responsible for validating certain areas of the information appearing in the Funds Control section

10

of the CDR as shown above.

Outstanding NEX advances – If there is an amount appearing under this category, the auditors shouldreconcile it to the cash at hand at the project level. In principle, this amount should represent thebalance of any advances transferred to the implementing partner minus the total expenses reportedin the quarterly financial reports submitted by the implementing partner to UNDP.

Un-depreciated Fixed Assets – There could be cases where fixed assets that belong to or are used bythe project are under UNDP’s control (i.e. in situations where UNDP is providing support services tothe project and there is no signed Letter of Agreement, as an example). If there is an amountappearing on the CDR under this category, the auditors should investigate and determine that theseassets are project related or not and, if project related, should perform the same audit procedures tovalidate the assets as those undertaken for the certification of the Statement of Assets andEquipment. Please refer to the Programme and Operations Policies and Procedures (POPP) section on“Administrative Services/Asset Management/Property Plan and Equipment/Furniture and EquipmentAcquisition and Maintenance” for information regarding the custody/control/ownership of assets.

Inventory – Similar to the case of Un-depreciated Fixed Assets, there may be situations where certainitems of inventory that were acquired for the project are temporarily under UNDP’s control/custody.If there is an amount under this category, the auditors should determine the nature of the inventoryand whether or not it is intended for the project. If it is determined that the inventory is projectrelated, then the same audit procedures fort the certification of the Statement of Assets andEquipment should be applied. Please refer to the aforementioned section of the POPP on assetmanagement as well as the section on “Financial Resources/Inventory Management” for additionalguidance as necessary.

Prepayments – The auditors should validate any amount appearing under this category, i.e.determine what it represents and if it is in any way project related.

Commitments – Any amounts appearing under this category would be provided for informationalpurposes only and, therefore, the auditors would not be required to undertake any audit proceduresrelated to the verification or validation of same.

E. Audit Services Required

The scope of audit services required is as the following:

The auditors are expected to conduct the audit in the institutions of the above-mentioned audit list,with the scope limited to the UNDP assistance through a specific project implemented by saidinstitution.

The audit will be carried out in offices of selected UNDP projects in Phnom Penh, except for MineAction for Human Development Project where auditors are required to conduct physical assetverification in project offices in provinces as specified in Annex 11.

The audit will be carried out in accordance with either ISA2 or INTOSAI3 auditing standards. The audit period is 1 January to 31 December of the year 2016. The scope of the audit is limited to the implementing partner expenses, which are defined as

including: (1) all disbursements listed in the quarterly financial reports submitted by theimplementing partner; and (2) the direct payments processed by UNDP at the request of theimplementing partner.

The auditor is required to verify the mathematical accuracy of the CDR by ensuring that the expensesdescribed in the supporting documentation (the quarterly financial reports, the list of directpayments processed by UNDP at the request of the government) are reconciled to the expenses, bydisbursing source, in the CDR.

The auditor is required to state in the audit report the amount of expenses excluded from the scope

2 . International Standards on Auditing (ISA) published by the International Auditing and Assurance Standards Boardof theInternational Federation of Accountants3 International Organization of Supreme Audit Institutions

11

of the audit because they were made by UNDP as part of direct support services and the amount oftotal expenses excluded because they were made by a UN agency. This scope limitation is not a validreason for the auditors to issue a qualified audit opinion on the CDR.

The auditor is required to state in the audit report if the audit was not in conformity with any of theabove and indicate the alternative standards or procedures followed.

The auditor is required to express an opinion as to the overall financial situation of the project for theperiod 1 January to 31 December 2016 and will certify:

1. The Statement of Expenses (CDR) for the period from 1 January to 31 December 2016;

2. The Statement of Cash Position (cash and bank balances of the project) reported by theproject as at 31 December 2016; and

3. The Statement of Assets and Equipment held by the project as at 31 December 2016.

The auditor is required to, as applicable, report in monetary value, the net financial impact of anymodified audit opinion (modified opinions can be qualified, adverse, or disclaimer) on the Statementof Expenses (CDR) where applicable. This should also include prior year non resolved NFI.

The auditor is required to review and sign the updated action plans for prior year auditobservations and recommendations.

The auditor/audit firm is required to submit a draft audit report by 28 February 2017 and a final signedaudit report with signed UNDP statements by 31 March 2017.

Note: Audit opinions must be one of the following: (a) unmodified, (b) qualified, (c) adverse, or (d)disclaimer. If the audit opinion is other than “unmodified”, the audit report must describe both thenature and amount of the possible effects on the financial statements.

The report should also make a reference to the section of the management letter with regard to therelated audit observation number and the action taken or planned to be taken to address and conclusivelycorrect the issues underlying the qualification. A definition of audit opinions is provided in Annex 4.

F. The Audit Report and Management Letter

The expected contents of the audit report and management letter and the topics/areas to becovered by the auditors are as follow.

Audit Report – VERY IMPORTANT

The audit report should clearly indicate the auditor’s opinion (Refer to Annex 3 for a sample AuditReport). This would include at least the following:

That it is a special purpose and confidential report The audit standards that were applied (ISAs, or national standards that comply with one of the ISAs

in all material respects) The period covered by the audit opinion The amount of expenses audited The amount of the net financial impact of the modified audit opinion on the CDR, if modified The reason(s) resulting in the issuance of a modified audit opinion, qualified, adverse or

disclaimer of opinion (the reason(s) must be also included in the management letter as an auditobservation(s))

The scope limitation (description and value) for those transactions that are the responsibility ofUNDP (as part of direct CO support services to NIM) or a UN agency. Important to note: Suchscope limitation should not be reason for a qualified audit opinion as such transactions would be,in general, excluded from the audit scope

Whether the UNDP CDR - for the period from 1 January to 31 December 2016] is adequately andfairly presented and whether the disbursements are made in accordance with the purpose forwhich funds have been allocated to the project.

12

(a) A Financial Audit to express an opinion on the project’s financial statements that includes:

Expression of an opinion on whether the statement of expenses presents fairly theexpense incurred by the project over a specified period in accordance with UNDPaccounting policies and that the expenses incurred were: (i) in conformity with theapproved project budgets; (ii) for the approved purposes of the project; (iii) in compliancewith the relevant regulations and rules, policies and procedures of the Government orUNDP; and (iv) supported by properly approved vouchers and other supportingdocuments. The CDR is the mandatory and official statement of expenses to be certified.Other forms of statement of expenses that may be prepared by a project office are notaccepted.

Whether the result of the prior year’s audits resulting in modified audit opinions on theCDR had conclusive actions to properly address an audit qualification in the previous yearaudit and the related NFI. If there is a lack of conclusive actions, the auditors must takeinto account the possible effect of a prior year modified opinion that has not beenproperly corrected or resolved.

Note: Consequently, a previous year modified opinion that has not been properly resolvedmay cause the auditors to issue a modified opinion in their current year audit report. Ifproper attention is not paid to this aspect, the risk could be a significant accumulation ofunresolved modified opinions from previous years.

Expression of an opinion on the value and existence of the project’s statement of assetsand equipment as at a given date. This statement must include all assets and equipmentavailable as at 31 December 2016, and not only those purchased in a given period. Wherea project does not have any assets or equipment, it will not be necessary to express suchan opinion; however, this should be disclosed in the audit report.

Express an opinion on the value and existence of the cash held by the project as at a givendate, i.e. 31 December 2016. The Audit Firm is required to express and opinion on theStatement of Cash Position where a dedicated bank account for the project has beenestablished and/or the project holds petty cash. Where the project does not hold anycash, this should be disclosed in the audit report.

The Financial Audit will be conducted in accordance with International Standards on Auditing (ISA).

(b) An audit to assess and express an opinion on the project’s internal controls and systems.

The deliverable will be an audit report similar to a long form management letter that covers theinternal control weaknesses identified and the audit recommendations to address them.

The management letter should be attached to the audit report and cover the following topics/issues:

A general review of a project’s progress and timeliness in relation to progress milestones andthe planned completion date, both of which should be stated in the project document orAnnual Work Plan (AWP). This is not intended to address whether there has been compliancewith specific covenants relating to specific performance criteria or outputs. However, generalcompliance with broad covenants such as implementing the project with economy andefficiency might be commented upon but not with the legal force of an audit opinion.