REPORTS DESK WITHIN ONE WEEK - World Bank · reports desk within one week document of international...

79

RETURN TO FflY REPORTS DESK WITHIN ONE WEEK DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use C',RCrJL0ATRTG C39Y TO BE RETURNED TO REPORTS DESK Report No. 178-MAS MAURITUS APPRAISAL OF COROMANDEL INDUSTRIAL ESTATE June 6, 1973 Industrial Projects Department This report was prepared for official use only by the Bank Group. It may not be published, quoted or cited without BankGroup authorization. The Bank Group does not accept responsibilityfor the accuracyor completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of REPORTS DESK WITHIN ONE WEEK - World Bank · reports desk within one week document of international...

RETURN TO FflYREPORTS DESK

WITHIN

ONE WEEK

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENTINTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

C',RCrJL0ATRTG C39Y

TO BE RETURNED TO REPORTS DESK Report No. 178-MAS

MAURITUS

APPRAISAL OF

COROMANDEL INDUSTRIAL ESTATE

June 6, 1973

Industrial Projects Department

This report was prepared for official use only by the Bank Group. It may not be published, quotedor cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Currency

1 Rupee - .185 us $1 US $ - 5.4 Rupees

F,puivalents

1 Arpent = 1.043 acres1 square mile = 2.6 square kilometers

Abbreviations

DBM - Development Bank of MauritiusUNCTAD - United Nations Conference on Trade

and DevelopmentDWC - Development Worke CorporationTPT - "Travail Pour Tous" (government work program)

MAURITIUS

COROKANDEL INDUSTRIAL ESTATE

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS

I. INTRODUCTION 1

II. BACKGROUND 1

A. The Problem - Unemployment 1B. Government Strategy 2

1. Employment Targets 22. Industrial Production for Export 33. Export Incentives 4

C. The Manufacturing Sector 51. Present Position and Growth Trends 52. Expected Growth of Manufacturing Employment 63. Industrial Land Requirement Forecast 64. Availability of Industrial Land 7

III. THE PROJECT 8

A. Site Location and Size 8B. Development Plan 9

1. PlotPlani, Factory Buildings and Number ofEnterprises 9

2. Other Infrastructure 10C. Type of Estate Enterprises and Employment 10

IV. PROJECT COST, CONSTRUCTION SCHEDULE AND FINANCING PLAN 11

A. Project Cost and Construction Schedule 11B. Financing Plan 12

V. PROCUREMENT, USE OF CREDIT AND RATE OF DISBURSEMENT 13

VI. PROJECT AND OPERATING CAPABILITY 13

A. DBM - Financial Capability and Estate DevelopmentExperience 13

B. Project Execution 14C. Operations 15

Table of Contents (Continued)

Page No.

VII. FINANCIAL ANALYSIS 16

A. Income 16

B. Income and Cash Flow Forecasts 18

C. Balance Sheet Forecasts 19

D. Financial Return and Viability Tests 19

VIII. ECONOMIC AND SOCIAL BENEFITS 21

A. Acceleration of Industrial Investment 21

B. Employment 22

C. External and Internal Economies 22

D. Social Benefits 22E. Indigenous Entrepreneurship Development 22

F. Fiscal Benefits 23

G. Foreign Exchange Earnings 23

M . SMENTS REACHED AND RECOMMENDATIONS 24

ANNEXES

1. Sectoral Employment and Growth Targets, 1969-1980.2. Numbers of Development Certificates Approved, 1963-1972.

3. Operating Export Processing Enterprises, 1972.4. Projected Manufacturing Employment and Land Requirements, 1970-1980.

5. Planned Industrial Sites.6. Coromandel Industrial Estate - Envirorment.7. Notes on Development Plan.8. Export Processing Enterprises Approved and Under Consideration.9, Capital Cost and Construction Schedule.10. Distribution of Local Currency and Foreign Exchange Expenditure.

1l. Projected Quarterly Disbursements of IDA Credit.

12, Development Bank of Mauritius - Status.13. Note on Capability of S.I.G.M.A.14. Eand and Building Rental Rates.15. Revenue Build-up and Flow.16. Management and General Overhead Cost Estimate.

17. Income Statement.18. Cash Flow Statement.19. Balance Sheets.20. Financial Rate of Return.

Map

This report was prepared by Messrs. C. Goderez and M. Iskander of the

Industrial Projects Department.

MAURITIUS

COROMANDEL INDUSTRIAL ESTATE

SUMMARY AND CONCLUSIONS

i. This report analyzes a project to establish an industrial estateat Coromandel, four miles southwest of Port Louis, the capital and majorcity of Mauritius. The estate, with a total area of about 60 acres wouldprovide, on a rental basis, land and infrastructure for the constructionof individually owned factories as well as space in standard buildings forsmall, medium, and some large scale industry. The total estimated cost ofthe project is about US$8 million equivalent, of which close to half repre-sents foreign exchange expenditures. IDA has been requested by the Govern-ment to provide a credit of US$4 million for the project.

ii. The Mauritian economy, dominated by a single agricultural product(sugar), has been unable to provide sufficient jobs for the expanding work-ing force. Unemployment is estimated to be 41,000 or 17% of the total laborforce of 249,000 (out of a population of 823,000). In addition, there are18,500 relief and development workers (7% of the working force) and under-employment is widespread. Since arable land for all practical purposes isfully under cultivation, agricultural growth and diversification cannot havemore than limited impact, leaving industrial development as the major feasiblelong-term alternative if the unemployment problem is to be solved. Importsubstitution possibilities are limited because of the small national marketand, therefore, industrial growth must be strongly oriented to export pro-cessing activities.

iii. In recent years, stimulated by a generous package of incentives,foreign investment in manufacturing has been entering the country at anaccelerating pace. The first industrial zone at Plaine Lauzun in PortLouis was inaugurated in December 1970 and will be fully developed and occu-pied by early 1974. Approved new industries are having difficulty in find-ing suitable rented quarters or land for factory construction. In responseto the immediate unsatisfied demand for industrial space, which is pro-jected to grow further through the decade, the Government proposes to buildthe industrial estate at Coromandel and in the future others in a dispersedpattern around the island.

iv. The Coromandel Industrial Estate project will be owned and managedby the Development Bank of Mauritius (DBM), a government-owned institutionestablished in 1964 which has gained experience in industrial site planning,development and operation at Plaine Lauzun. The proposed financing consistsof a Government equity contribution in DBM of US$4 million equivalent andthe IDA credit of US$4 million channeled through DBM. The Investment inthe estate would be recovered by rental fees charged the estate occupantsby DBM, which in turn would repay the US$4 million of loan funds to theGovernment over 20 years, including 5 years of grace, at an interest rateof 7.25%. The estate will be developed between 1973 and 1978 and occupancystarting in 1974 is projected to grow in step with the phased developmentof land and buildings. The financial return of the estate project at anassumed 90% occupancy and competitive rentals is 15.4%.

- ii -

v. Among the benefits to be generated by the project are 5,000 jobsby 1980 rising to 8,000 by 1985, most of them involving training and skillupgrading of unskilled and/or unemployed workers. The industries on theestate will represent an estimated capital investment of US$58 million andby the mid-eighties corporate income taxes should approach US$5 million perannum. Net foreign exchange earnings after allowing for profit remittancesand repatriation of imported capital, on the conservative assumption thatall the invested capital is foreign, should approach US$20 million perannum in the late 1980's. The estate is also expected to act as a strongstimulus to indigenous entrepreneurship and small scale industry develop-ment. Finally, national land use as well as industrial and social infra-structure planning and implementation will be greatly facilitated in responseto the guided concentration of industry on the Coromandel estate.

vi. In view of the project's technical and financial feasibility andits economic benefits, and the agreements reached during negotiations onnecessary assurances as summarized at the end of the report, the project issuitable for an IDA credit of US$4 million equivalent.

I. INTRODUCTION

1.01 Since 1970, as part of its development program, the government-owned Development Bank of Mauritius (DBM) has been leasing space to privatefirms in standard manufacturing buildings constructed within the PlaineLauzun industrial zone 1/ at Port Louis, the country's capital and principalharbor (Map). The program has been highly successful and early in 1974the 110 arpents (115 acres) of the zone are expected to be fully occupiedby factories established in these pre-constructed buildings (15 arpents) andindividually-owned factories on leased plots (95 arpents). In line withthe Government's objective of fostering industry and thereby helping reduceunemployment, DBM has been planning further industrial site development onanother 60 arpents at Coromandel, four miles from Port Louis, and in May 1972the Government approached the International Development Association (IDA)for assistance in carrying out the country's first full-fledged industrialestate at this location. The project would consist of the development ofland and the provision of the necessary infrastructure for the settlementof industry including pre-constructed standard buildings to be leased tomanufacturing firms. The project is estimated to cost about US$8 millionequivalent, of which IDA would contribute half or US$4 million.

2/1.02 The consulting firm SCET-International - was selected by DBMin June 1972 to prepare a study to determine: (i) the most suitable locationfor the industrial estate, and (ii) its technical, financial and economicfeasibility. An interim report was submitted in December 1972, and the finalreport, confirming the feasibility of the project, was completed in January1973 3/.

1.03 This report is based on the SCET study and the findings of anappraisal mission consisting of Messrs. C. Goderez (chief) and M. Iskander(industrial economist) of the Industrial Projects Department which visitedMauritius from January 31 to February 10, 1973.

II. BACKGROUND

A. The Problem - Unemployment

2.01 Mauritius is a small island (720 square miles) located some 500miles due east of Madagascar in the Indian Ocean. The population of 823,000in 1972, while increasing at a rate of only 1.8% per annum (compared to 3%in the 1950's), makes the island one of the most densely populated areas

1/ An industrial zone is an area reserved for industry but without thecentral management and common service facilities of an industrialestate (see para. 2.20 for further discussion).

2/ Societe Centrale Pour L'Equipement Du Territoire - International(France).

3/ Feasibility Study of Industrial Estates, Main Report and Annexes,January 1973, 420 pages.

-2-

in the worid. The economy is overwhelmingly dependent on a single crop -sugar - which during 1967-1970 contributed 33% of GDP, 40% of total employ-ment and 90% of exports. From 1962 to 1969, the economy stagnated and GNPat market prices was only US$200 million in 1971 or about US$250 per capita.As a result of firm sugar prices worldwide and the determined efforts of theGovernment to accelerate industrial investment, the GNP trend is now rising.Government projections of a 7% annual rate of economic growth up to 1975are not unrealistic provided sugar prices continue firm and industrializationcontinues its upward trend.

2.02 There is, however, a serious problem of unemployment and under-employment. Registered enemployed and relief and development workers totalled59,500 in 1972 or about 24% of the labor force. (Comprehensive registrationof unemployed in the last two years probably picked up a substantial numberof hidden unemployed who were not included in the 1969 statistics given inthe table, para. 2.03). Statistics on the underemployed are unreliable butcannot fail to be very high in a sugar-based seasonal economy. One studyin 1961/62 revealed that 7,000 men during the height of the sugar croppingand milling season and 12,700 during the intercrop season were working lessthan 30 hours per week. Agriculture alone cannot solve the problem, de-spite efforts at diversification into other crops such as tea and ginger,since available arable land is already practically 100% under crop, 95% insugar alone.

B. Government Strategy

1. Employment Targets

2.03 The land constraint and continued population growth have led tothe economic development strategy adopted by the Government designed toaccomplish a major structural change in the econamy to ensure full employ-ment by 1980. Agriculture's share in the economy, at present about 25% ofGDP, is projected to decline to 17% by 1980 while the share of manufacturingis to rise from 15% to 23% of GDP. Industrializatiotn, therefore, is the keylong term factor if the full employment goal set by the Government andtabulated below is to be met (Annex 1):

EMPLOYMENT TARGET i1969-1980 G

Projected Growth1969 1975 1980 Rate 1969-80

(actual) %Employed (Wage earnersand self-employed) 195,000 248,000 325,000 5.3

Relief and DevelopmentWorkers 16,000 20,000 - -Unemployed 20,000 10,500 -

Total 231,000 278,000 325,000 5.3

The table indicates that employment must grow by a total of 130,000 jobsover the decade, or at an annual rate of 5.3%, if the working force, in-creasing at a rate of 3.5% per annum, is to be fully employed by 1980. Toachieve this goal, manufacturing employment will have to increase at 9.4%per annum to compensate for slower growth sectors. (If the unemploymentand relief and development worker figure was as high in 1972 as indicated inpara. 2.02, manufacturing employment will in fact have to grow faster than9.4% per annum between 1973 and 1980 if the government target is to be met.)

2.04 To deal with the problem of interim unemployment, the DevelopmentPlan includes a government work program called "Travail Pour Tous" (TPT)which may receive IDA support through a Rural Development Project currentlybeing appraised. Only projects deemed economically or socially productiveare undertaken and these are typically roads, buildings, land clearing andreforestation, bench terracing to increase land availability and ruralwater supply. Besides providing necessary employment, and added nationalbenefit is derived - upgrading of labor skills such as carpentry, brick-laying and plumbing, creating a resource which will be in growing demand asthe industrialization process accelerates. It is expected that as privateindustrial investment grows, the TPT program will be phased out after apeak in 1975 and disappear by 1980.

2. Industrial Production for Export

2.05 Because of the small national market, import substitution activi-ties have limited potential and in fact the possibilities in this area havebeen substantially exhausted. Production for export, based primarily onimported raw and intermediate goods, appears to be the only feasible alter-native and the main promotional thrust has been aimed at attracting exportprocessing activities of the type that have flourished in Korea, Hong-Kong,Taiwan and Singapore. Mauritius' major comparative advantage is its amplesupply of labor at wage rates about one-third of those in Hong-Kong andSingapore. This advantage is likely to be prolonged for the foreseeablefuture even though some upward pressure on wage levels can and should beexpected because of the predicted economic growth and increasing job opportuni-ties. The same factors are, however, operating in competing countries sothat the relative advantage of Mauritius should continue.

2.06 Additionally, factories already established including gem cutting,carved furniture, packaging products, thread and garments among others, havedemonstrated the high level of trainability inherent in Mauritian workers.But the success of the campaign initiated in the late 1960's to attractindustrial investment to the island must be attributed as well to otherfactors equally as important as the quality and low cost of labor. Theseare embodied in a global program of incentives reflecting the Government'sdetermined and pragmatic approach to industrial promotion.

-.4-

3. Export Incentives

2.07 Among the incentives offered are tax holidays of generally 5 to10 years, no import duties on capital goods and raw materials, credit availa-bility, subsidized power and water rates, free repatriation of capital anddividends, government contributions to the cost of export market surveys,trade fairs and trade missions, and prepared industrial sites offering lowcost rental space in first-class reinforced concrete buildings or, alter-natively, loans of up to 50% of building costs repayable over 10 years. Notthe least important incentive is the Export Processing Zones Act of 1970,which facilitates for government approved and certified industries the in andout movement of goods, based on ex post facto scrutiny by the NationalComptroller.

2.08 The comprehensive incentive "package" offered may perhaps be moreconcessionary than is necessary to achieve the desired stimulation of invest-ment but has been considered justifiable by the Government in order tomaximize the attractions of Mauritius to foreign firms. As noted later inthis report, it appears to have been successful in terms of investment flowand job creation and, therefore, changes in terms and conditions should beapproached with caution. It may be advisable to reconsider whether or notconcessionary rates on power and water, for example, are really necessary.Scheduling of future capital repatriation to help ensure net positive foreignexchange earnings from ̀ e inception of each project might also be feasiblewithout significant deterrent effects on investment. For tile next few years,however, at least until Mauritius becomes better known to the world businesszommunity, it would probably be prudent not to alter significantly the

present package. 1/

2.09 Associate membership in the European Economic Comnunity is pendin-(ratification of this status is expected in May/June 1973) and Mauritiusbased industry is looking forward to easier access to that major market area.Australia has conceded preferential tariff rates on certain Mauritian pro-ducts and exports to that country and to South Africa are growing. Long rangeprospects for export growth to the U.S.A. and other developed countries willbe enhanced once the Generalized System of Preferences of UNCTAD comes intoeffect.

2.0 A potential investor planning to produce for the world market cannot.lo pbut find Mauritius a desirable location. The incentives and advantages

r.merated above, coupled with a pleasant sub-tropical climate, ease of imm'on for expatriate managers and relative political and social stability,3roven to be effective in attracting a growing number of firms. Thisbasic reality -which supports the feasibility of the proposed project

st Coromandei.

/5j + Scott (Oxford) in a report "@The Promotion of Export Processingodus,ries in Mauritius", June 1972, opined that the current system of

.~.s.entives is yielding in net social benefits about 90% of the optimum-:.* could be achieved, indicating that potential incremental social.-.enefits are small in any case.

-5-

C. The Manufacturing Sector

1. Present Position and Growth Trends

2.11 In 1969, manufacturing contributed about 15% to GDP and 13% oftotal employment (25,000 jobs approximately). The sector is dominated bysugar milling and related industries which generate about 60% of value addedand 50% of manufacturing jobs; sugar and tea processing alone in 1969accounted for 26% of the sectoral work force. At the other end of the spec-trum, small scale manufacturing, defined by the Census of Industrial Pro-duction as establishments employing 10 or less, comprises 95% of total enter-prises (3,471 out of 3,660 in 1968), employs about the same number ofworkers as the 189 larger enterprises (over 10 workers per enterprise, notincluding sugar and tea processing) but contributes only 15% of manufacturingoutput. Except for a government owned sack factory and feed mill, the sectoris entirely privately owned.

2.12 During the 1960's, growth in manufacturing was almost entirely inimport substitution, with the exception of the major agricultural basedsugar and tea industries. During the 10-year period 1963-1972, eac1 /year anaverage of 8 primarily import substituting "development companies" - wereestablished, generating at their inception about 50 jobs per enterprise(Annex 2). On the other hand, from 1970 to the end of 1972, following theintroduction of the export incentive system (para. 2.07), an average of 7export processing companies per year were created primarily with foreigninvestment averaging some 100 jobs/enterprise (Annex 3), or double the employ-ment per plant compared to the development companies.

2.13 While the rate of implantation of development companies has beenfalling off significantly, and may be expected to diminish further sincepossibilities for additional import substitution are now virtually exhausted,the trend for export processing companies has been rising sharply. On thebasis of latest estimates available (Dec. 1972), the number of export proces-sing certificates granted, and projected to be converted into operating plantsin 1973 and 1974, totalled 29 corresponding to 14 or 15 new companies per yearif all are indeed installed. Allowing for some slippage, it may conservative-ly be expected that, combined, about 16 development and export processingcompanies will be established annually in the near future.

2.14 An interesting and very significant conclusion of the SCET marketstudy is the high proportion of investments anticipated from firms alreadyestablished in the better known export-processing zones of Hong Kong,Singapore, Taiwan and others. The success of those nations has raised wagesto levels which are progessively more unfavorable compared with those ofMauritius and the politically tense atmosphere of Southeast Asia makes Mauri-tius' relatively remote location - which otherwise would be a disadvantage -appear attractive by comparison.

1/ Locally financed companies which are granted "development certificates";these carry certain incentives such as tax holidays, credit availability,and reduced tariffs on imported capital goods and materials.

- 6 -

2. Expected Growth of Manufacturing Emplo]yent

2.15 In this section, the manufacturing sector will be treated as com-prising all manufacturing (small, medium and large) industries, excludingsugar and tea processing for which zero employment growth is anticipated inthe 1970-1980 decade. Between 1967 and 1970 the total number of manufacturingjobs increased at a rate of approximately 3% per year and it was only from1970 onward that - primarily due to the influx of export-processing companies -the rate tripled to 9% per year. Total manufacturing employment is estimatedto have reached about 22,500 at the end of 1972, of which 11,700 were employedin medium/large scale industry and 10,800 in small establishments and artisanshops. On the basis of the detailed study prepared by SCET, it is furtherestimated that between 1973 and 1980 some 22,300 and 5,200 new jobs will becreated respectively in medium/large and small enterprises so that by the endof the present decade the manufacturing labor force will have reached some50,000 or about 83% of the Government's manufacturing employment target of60,400 in 1980 (Annex 4). Based on the evidence available, there is a highprobability of equaling or exceeding the predicted growth over the nextseveral years and a lower, but still reasonable, probability of maintaining

t *- Awth during the second half of the decade.

2.16 The expected employment creation in medium/large enterprises - ofprime concern to the evaluation of the estate project - is based on thefollowing major assumption: (a) the average number of medium/large enter-prises to be established annually in Mauritius will continue to be about 16as in the recent past; (b) the average employment intensity per plant willbe maintained (i.e. at the start of operations, for development companiesabout 50 persons per plant and for export processing industries about 100per plant); (c.. 'he composition of the mix between development and exportprocessing companies will shift markedly in favor of the latter; and (d)additional employment creation of about 10% per year will occur in the al-ready existing enterprises as tiiey expand. As a consequence, incrementalemployment in this segment of industry is expected to increase from about1,600 per annum to 4,300 per amnunm between 1973 and 1980, or by 15% peryear, and by a total of about 22,300 new jobs as mentioned in para. 2.15.

3. Industrial Land Requirement Forecast

/_.lm Rational land use planning is particularly important in Mauritiussince there is no land reserve to absorb or to mitigate the effects of non-optimal and haphazard land use. A start has been made in land use planningbut a much more comprehensive approach is needed and should involve thevarious relevant government agencies (Ministry of Town and Country Planning,Ministry of Agriculture, DBM and others) in a coordinated program. Thisissue is dealt with in greater detail in the Rural Development ProjectAppraisal 1/. Meanwhile, even in the absence of a comprehensive land useplan, the Coromandel project contributes to the objective of rational landuse for industry.

I/ Rural Development Project Appraisal, Report No. MAS-161, June 5,Annex 2, para. 9.

-7-- 7 -

2.18 Assuming generally accepted average ratios of job creation perunit of land for the types of enterprises likely to be established in Mauri-tius, it is forecast that about 446 arpents of additional factory land willbe required between 1973 and 1980 (Annex 4).

4. Availability of Industrial Land

2.19 Under the current Development Plan (1971-1975), nine primaryand four secondary smaller areas totalling 660 arpents have been reserved forindustry (Annex 5). These include the Coromandel site of 60 arpents butexclude the 110 arpents of the Plaine Lauzun industrial zone which has alreadybeen fully allocated. Even assuming a faster industrial growth than des-cribed in the preceding paragraphs, the above areas will amply satisfy in-dustrial land requirements into the early 1980's. Taking into account thatmany larger enterprises and a significant number of medium-sized establishmentsare likely to purchase land and develop factory sites independently, notwith-standing the overall land limitation in Mauritius, the planned industrialsites provide an adequate reserve well into the 1980's. The above areas areeither unused government-owned Crown Land readily available for developmentor marginally productive private sugar crop land.

2.20 With the exception of Coromandel, all of the reserved areas arestill designated as industrial zones and it is unlikely that all will in factbe converted into estates. An industrial zone is a delineated area reservedfor industry where companies buy or lease land from private or public owners,build factories and individually negotiate supply of services such as powerand water with the public utilities. There are no common services, centralmanagement or special facilities such as pre-constructed standard buildingsready for occupancy, auxiliary power plants, central water storage and sewagetreatment as in industrial estates. The centrally planned and managed estateconcept offers many advantages, especially to smaller firms seeking rentedspace in buildings or small parcels of leased land for construction.

2.21 Nevertheless, as already stated, some firms may be expected toestablish plants independently either because of company preference, orbecause their operations do not meet estate standards. For example, thesestandards normally exclude certain chemical processing industries whicheven with the best available pollution control technology disseminate odorsor irritants and need to be isolated. Generally, the firms preferrringestate locations will be of small to medium size (50 to 200 employees), en-gaged in light manufacturing (apparel, furniture, electronics and other lightassembly activities, packaging products, jewelry and ornaments) and inclinedto limit their investment to equipment and working capital without tying upsubstantial capital in land and buildings. SCET estimated that 80% of thenew companies, and in particular the export processing firms, would preferthe prepared space and services of an estate and be acceptable as occupants.This distribution pattern appears reasonable based on experience in othercountries and the recent history in Mauritius, and implies that of the totalprojected demand of 446 arpents between 1973 and 1980 (Annex 4), 80% or 360arpents should take the form of estates. Coromandel will provide 60 arpentswithin the next few years and the need for further estate projects in theother reserved locations should be continually assessed and implemented as thegrowth in demand justifies the investments needed.

III. THE PROJEC'T'

A. Site Location and Size

3.01 Although the 60 arpents at Coromandel had already been optionedearly i2n 1972 bv DBM on the basis of its own evaluation, the SCET feasibilitystudy started with a comparative analysis of altervaative sites. Availablealternatives were weighed in accordance with the foilowing criteria: landvalues, transportation arteries, proximity to the major center of Port Louis,labor availabiLity, land characteristics (load bearing capacity, surface,and tinderground features affecting construction. costs), c.ost of externalinfrastructure connections (power, water, telephones, drainage and sewagedisposail). A first review narrowed the preferred choices to four - Coro-mandel, Vacoas-Phoenix, Curepipe and La Cure (Map) - which were then surveyedin depth to select the one most suitable. it was conclude- that Coromandelis indeed the most economic and therefore the preferred site. DBM purchasedthe land in February 1973 and preparatory work nas begun to develop it intoan industrial estate. Among its outstanding advantages are:

(a) Land was purchased at a very favorabIL;& -Price of Rs 15,000(US$2,900)0/arpent which is well below the current marketprice of Rs 60,000/arpent (DBM estimate).

(b) It is unoccupied and unexploited and had been considered onlymarginally productive for sugar cane.

(c) Located at the southern edge of the District of Port Louis, it ison'ly 4 miles from the urban center but easily accessible to themajor labor force of Port Louis by regular bus service which canbe expanded as needed.

(d) It is bounded on the east by the pri rr highway connecting PortLouis with the airport, which is 30 uulle,i a .ay, and on the north,west and south by secondary roads (Annex

(e) Land is only slightly sloping (4 to 6'l); grading costs will there-fore be minimal and surface drainage adequate.

(f) High voltage power distribution lines cross the property.

(g) Sufficient water of the requisite quality iS readily available fromnearby sources.

3.02 In view o`t the projected high demand for industrial sites parti-cularly in the proximity of Port Louis, DBM has taken an option on an addi-tional 120 arpents adjacent to Coromandel, at La Tour, parts of which wouldbe allocated to housing and other social infrastructure. No developmentwork will be undertaken at 'a Tour until 1974 at the earliest when DBM willhave to decide whether it wants to expand the Corom&ndel estate through

- 9 -

addition of La.Tour or develop a new estate at some other location. ExpandingCoromandel has obvious advantages in reducing infrastructure costs, but thepossibility of excessive congestion must also be taken into consideration andfinancial savings in developing the larger estate in one continuous projectmight be more than offset by the additional social costs of urban congestion.These aspects require further study and, during negotiations, DBM has agreedto consult IDA before proceeding with development of La Tour.

B. Development Plan

3.03 A detailed analysis of the physical part of the estate is containedin the SCET Study; the layout of the estate and a brief description of itsinfrastructure are given in Annex 7.

1. Plot Plan, Factory Buildings and Number of Enterprises

3.04 The site will be subdivided into 25 plots for industry and one plotfor a management and commercial center. Average plot size will be 1.9 arpentsbut the layout provides optimum flexibility for plot sizes to range from 0.5to 4 arpents per enterprise, or even more, depending on individual require-ments. Following the strong demand for ready-made factory buildings at PlaineLauzun, over one third of the estate will be reserved for this type of factorybuilding, i.e. primarily for small scale enterprises. Also for these the floorarea per factory can be kept very flexible from a minimum size of 2,000 sq. ft.to a multiple thereof. All plots and subdivisions have access to the internalroad network and to the various utilities (para. 3.05) that will be providedon the estate. The projected pattern of land usage and of the number of fac-tories expected to settle on the estate is given below:

PATTERN OF LAND USAGE, AVERAGE FACTORY SPACE, AND NUMBER OF ENTERPRISES

Land Estimated Average Floor Number ofArea Floor Space Space Per Factory Factories

(arpents) (sq.ft.) (sq. ft.)

(a) 12 to 15 StandardBuildings (small/medium scaleindustries) 27 900,000 7,500 120

(b) Individual Factories(medium/large scale indus-tries) 1/ 20 300,000 30,000 10

(c) Management/CommercialCenter 4 60,000 - -

(d) Roads, Utilities and Landfor Common Use 9 -_ _

Total 60 1,260,000 130

1/ Owner financed, although DBM may extend construction loans out of itsgeneral funds.

- 10 -

3.05 The number of factories that will in fact locate on the estate isdifficult to predict and the above total of 130 enterprises must be considereda rough approximation only. While the number is based on experience gainedat the Plaine Lauzun industrial zone, it will vary with the type of industrythat will actually settle on the estate. The individual and the standardfactory buildings will be of reinforced concrete construction to withstandthe cyclonic winds of the area of velocities of 160 miles/hour and more. Thestandard factory buildings will have one to three floors and will largelyfollow the design that at Plaine Lauzun has proved satisfactory both from thepoint of view of utility and low cost of construction. Individual factorybuildings will have to comply with certain architectural guidelines to pre-serve the aesthetic character of the estate.

3.06 The Management/Commercial Center will be a building to houseDBM's on-site operating staff, a canteen, bank, post office, and possiblyseveral retail stores. A building and grounds maintenance shop would alsobe included to store maintenance equipment, tools and materials. Productionshops such as foundries and forges are not envisaged as estate-owned facili-ties, but might appear as privately-owned ancillary industries.

2. Other Infrastructure

3.07 Provision of utilities (water, sewage, power and telecommunications)and responsibility for their implementation will rest with the respectivepublic utilities and will therefore not form part of the cost of the project;an exception is the sewage treatment plant which will be constructed by theestate and on its account. Preliminary design standards as included in theSCET study are in line with normal practice in Mauritius and, as they willgenerally follow those at Plaine Lauzun, are already known to be acceptableto foreign private investors. These standards were discussed during negoti-ations and agreement was reached on satisfactory arrangements to be enteredinto with the utility companies on the timely construction of their facilities.

C. Type of Estate Enterprise and Employment

3.08 The type of export-oriented industries that can be expected to cometo the estate will be determined by two principal factors: (a) the availabil-ity of low-cost and quickly trainable labor and (b) the relatively high trans-portation costs overseas. Production therefore will be geared to the manu-facture or partial processing of a wide variety of products, from electroniccomponents to toys, with a high value added, where labor inputs are signifi-cant and where the value of imported materials and components and of the ex-ported product is high as compared to their weight and/or volume. Most ofthe processes therefore can be expected to be highly labor-intensive. Annex 8gives a spectrum of the type of products that might be expected to be manu-factured on the estate, together with the countries from which the technicalknow-how would be supplied. Using the same industry mix as at Plaine Lapzunand the same average ratio of 6.7 workers per 1,000 sq. ft. of floor space asexperienced there, Coromandel when fully occupied could employ some 8,000 people.

IV. PROJECT COST, CONSTRUCTION SCHEDULE AND FINANCIAL PLAN

A. Project Cost and Construction Schedule

4.01 The cost of the project, detailed in Annex 9, is summarizedbelow:

CAPITAL COST ESTIMATES

Local Foreign Total Local Foreign Total %(Rs. million) (US$ million)

Land 0.90 - 0.90 0.17 - 0.17 2.1Infrastructure 1.51 0.97 2.48 0.28 0.18 0.46 5.8Buildings 12.22 13.18 25.40 2.26 2.44 4.70 59.2Engineering andSupervision 0.65 - 0.65 0.12 - 0.12 1.5

Sub-total 15.28 14.15 29.43 2.83 2.62 5.45 68.6

Contingencies- Physical 1.44 1.42 2.86 0.28 0.27 0.55 6.8- Price Escalation 6.48 4.00 10.48 1.20 0.74 1.94 24.6

Total 23.20 19.57 42.87 4.31 3.63 7.94 100.0

4.02 The cost estimates were prepared by SCET in January 1973 on thebasis of actual costs incurred in the ongoing construction of similar workson the Plaine Lauzun industrial zone. Land was purchased by DBM in February1973 and construction is expected to commence by mid-1973 and to end byDecember 1978. Initial contracts for construction will be let for onlyportions of the total work, including 40% of the standard buildings between(about 300,000 sq. ft. of leasable floor space), the Management/CommercialCenter (60,000 sq. ft.), and 60% of leasable land (12 arpents) plus 60% ofroads and other infrastructure. As presently planned this contractual phasewill be completed by the end of 1975 and the remainder of the buildings andthe infrastructure will be built between 1976 and 1978. Phasing constructionover a 5-year period is designed to insure full occupancy of land and build-ings as soon as they are ready. Given current forecasts of supply and demandfor industrial land and buildings, the construction period is somewhatlengthy. However, the construction plan is flexible enough to allow the estatemanagement to adjust the speed of construction in the light of realized andprospective rates of occupancy.

4.03 Physical contingencies of 10% of project costs (before contingen-cies) - and excluding land which has already been purchased - are includedin the above estimate. Price escalation (starting with Jan. 1, 1974) hasbeen based on current trends, i.e. 12% per year on local currency expendituresand 8% per year on foreign exchange expenditures. With these contingenciesand particularly since it is likely that the overall construction period

- 12 -

can be compressed, cost estimates are considered realistic. Nevertheless,during negotiations assurances were obtained from the Government that itwtll supply any funds - both local and foreign - that may be needed to com-plete the project, on terms satisfactory to IDA.

4.04 Various estimates have been made by DBM and SCET (Annex 10) of theforeign exchange and local currency components of the building constructionand infrastructure works. The above split of about 54% local and 46% foreignprobably underestimates the foreign exchange requirements which may be ashigh as half of total project cost. The IDA credit of US$4.0 million isbased on the assumption that the foreign exchange component will be a maxi-mum of 50% of project cost.

B. Financing Plan

4.05 The project will be financed as follows:

FINANCING PLAN

Rs million US$ million

Government equity contribution 21.4 4.0

Proceeds of IDA credit 21.4 4.0

Total 42.8 8.0

The US$4.0 million equivalent contribution by the Government would takethe form of an equity subscription in DBM.

4.06 The IDA credit would be made to the Government, which would onlendthe proceeds to DBM at an interest rate of 7.25% per annum and repayable over20 years including 5 years grace, the latter corresponding to the approxi-mate duration of construction. T'o avoid putting additional risks on DBM onaccount of its agency role of executing the project on behalf of the Govern-ment, during negotiations the Government proposed and it was agreed that itwould guarantee DBM against project losses. This would be accomplished bythe Government reimbursing DBM for project operating losses incurred in anyfiscal vear in excess of cumulative earned surplus from project operations.

- 03 -

V. PROCUREMENT, USE OF CREDIT AND RATE OF DISBURSEMENT

5.01 The proceeds of the IDA credit will be used for expenditures onthe construction of roads, standard buildings and other infrastructure works,but not for the purchase of the estate land and the engineering contract.The land has already been acquired and the engineering contract will benegotiated with S.I.G.M.A., a local firm of engineers, at a fee of 2% of thevalue of civil works. S.I.G.M.A. is well known to DBM as competent firmwhich has successfully carried out important public works in Mauritius andis considered qualified by IDA.

5.02 Tender notices for goods and services contracts (excluding theengineering contract) will be made known to all local embassies and consulatesof the Association's member countries and Switzerland, in addition to adver-tisement in Mauritius.

5.03 IDA funds will be disbursed against certified progress paymentson eligible contracts. The ratio of IDA to government contributions in thesecontracts will be 52/48; this takes account of the Government's additionalpayments for land and the engineering contract. Quarterly disbursementforecasts of the credit are shown in Annex 11. As indicated in para. 4.04,a minimum of 91% of the credit is expected to be used for foreign exchangepurchases but this could possibly reach 100%.

VI. PROJECT AND OPERATING CAPABILITY

A. DBM - Financial Capability and Estate Development Experience

6.01 DBM, the proposed owner and executing agency of the project, isan autonomous public sector institution, established in 1964 to fosterindustrial and tourism development and agricultural diversification. Sharecapital of Rs. 10 million (US$1.85 million) is owned 80% by the Governmentand 20% by the Bank of Mauritius (Central Bank). As of June 30, 1972, totalresources of DBM were Rs. 71 million (US$13.2 million), consisting of Rs. 22million capital and reserves; Rs. 18 million debentures and bonds outstanding;Rs. 29 million government loans; and Rs. 2 million deposits. Annual dis-bursements have increased at an average rate of 20% between 1965 and 1972.In mid-1972, DBM obtained a US$3.5 million IDA credit of which US$400,000was allocated to the construction of standard buildings at Plaine Lauzunand US$100,000 to finance the Coromandel industrial estate feasibility study.Industrial building construction and leasing has been underway at PlaineLauzun for some years and DBM has gained considerable experience in planning,executing and management of standard buildings as well as in general super-vision of the industrial zone at Plaine Lauzun. Annex 12 gives more back-ground on DBM's activities, financial position and prospects.

- 14 -

6.02 Management of the estate by DBM is, furthermore, advantageousbecause of the combination with possible loan financing of individuallyowned factory buildings and equipment for estate enterprises. Assumingthat estate enterprises will borrow as much as 60% of the value of theirequipment and up to 50% of the cost of buildings, total loan requirementsbetween 1974 and 1980 could reach approximately Rs. 162 million (US$30 mil-lion) or an average of about Rs. 23 million (US$4.3 million) per year. Theaverage figure, however, would follow a growth curve so that annual require-ments in the mid-1970's will be lower, perhaps in the US$2 to 3 millionrange, and may rise to US$5 million or more late in the decade. Approvalsof .1ans to medium/large scale enterprises by DWI were US$1 million inFY1971 (ended June 30, 1971), US$1.5 million in FY1972 and are expected to reachUS$4 million in FY1973, a probably exceptionally high figure. Assuming thata current "normal" rate of lending is about US$3.5 million per year, and con-sidering that about 70% of DBN's portfolio is in manufacturing, DBM seems nowto be lending to this sector at about the rate predicted for the immediateyears ahead at Coromandel - US$2-3 million per year.

6.03 Although DBM is the primary source of development lending, in addi-tion the six conmercial banks in Mauritius have recently begun to participatewith DBM on a 50:50 basis in development loans of up to 7 years to medium/largescale industry at the same interest rate as DBM's (8.5%). Commrrcial bankcredits to industry, including short-term, increased by 70% in FY1971 andanotlher 58% in F9Y1972, reaching Rs. 55 million in June 1972, corresponding to17.8% of total credits outstanding (Rs. 308 million). 1/ If we assume that10% of this industrial credit is medium-long term development finance, itwould appear that Rs. 5.5 million (US$1 million) has been channeled into in-dustrial development finance by the commercial banks out of total resourcesof i's. 308 million (US$57 million). This activity has started only in thelast two to three years and can be expected to grow. The resources of DBMplus the resources and growing involvement of the commercial banks appearto be adeeuate to meet the estimated demand for industrial equipment andfactory building finance at Coromandel.

B. Project Execution

6.04 Additional staff is needed for the project and a separate unit willbe established within DBM with prime responsibilities for project implementa-tion. DBM plans to recruit a civil engineer as a full-time Project Managerand a project accountant, responsible for the day-to-day management of theproject. Both will work under the overall supervision of the Head of DBM'sIndustrial Section and be supported by other DBM staff as may be required

1/ Bank Supervision Report, March 11, 1973, "The Development Bank ofMauritius."

- 15 -

from time to time. An important function of the accountant will be toset up separate project bookkeeping and accounts to facilitate financialcontrol and future evaluation of the estate's performance.

6.05 As in the past at Plaine Lauzun, further technical expertise willbe supplied by a Mauritian architect who will be responsible for buildingdesign, preparation of building tender documents, evaluation of bids andsupervision of construction. The architect would report to the ProjectManager and act as the owner's (DBM) representative in all dealings with thecontractors. S.I.G.M.A. will provide engineering design services, i.e.detailed engineering of the Coromandel development plan. The five partnersare experts in land surveying and land use planning, structural design andengineering, soil mechanics, hydraulics, road building and factory, commercialand residential building design (Annex 13).

C. Operations

6.06 As early as possible but not later than mid-1974, a Manager ofPromotion and Sales, and later in that year, when the first occupants areexpected to enter Coromandel, an Estate General Manager will be added tothe management team with the necessary staff. These arrangements, togetherwith the overall support of DBM, are expected to provide adequate assurancesthat the project will be executed properly, and were confirmed duringnegotiations. Further competence of DBM in estate management is plannedto be acquired through study trips to Singapore, Hong Kong, Taiwan and Israel,among others. DBM's Industrial Section Head has already undertaken thefirst of such trips.

6.07 Despite the encouraging demand forecast, DBM plans to start addition-al promotional efforts to attract foreign investment and thereby help ensurefull occupancy of the estate as quickly as possible. Such efforts wouldinclude: (i) preparation of up-to-date promotion brochures; (ii) interna-tional and national advertising of the Coromandel estate and the investmentincentives; (iii) enlisting the cooperation of chambers of commerce, interna-tional banks, foreign government trade promotion organizations, and interna-tional development institutions (e.g. African Development Bank and UNIDO),in order to maximize contact with the world business community. Attendanceat trade fairs and visits to foreign countries together with private Mauritianbuisnessmen are intended to be arranged to make contact with possible invest-ors. Occasionally, it might also be justified to contract consultants incertain priority target countries such as Hong Kong, Taiwan, Singapore,Australia, South Africa, Germany, France, England, Japan and the U.S.A., toconduct promotional programs.

6.08 Admittance to the estate will require DBM approval. DBM willappraise the viability of each applying company as it does in its otheroperations, independently of whether or not it will be asked to provide

- 16 -

financing for equipment purchases. Since one of the prime objectives ofthe estate is to overcome the unemployment problem in the country, preferencewill be given to the establishment of labor over capital-intensive manufac-tures. Furthermore, criteria for settlement on the estate, including theestablishment of ecologicalistandards, architectural guide-lines and buildingregulations as well as standard lease contracts and general estate rules,are being developed and will be submitted in a form satisfcory to IDAbefore end-1973.

6.09 Although special assistance to occupant firms in training theiremployees to higher skills is a feature of some estate projects in otherdeveloping countries, no similar activity is planned at Coromandel. Foreignfirms have been training specialized staff as needed at company expense andthere does not seem to be any strong pressure to increase the already at-tractive incentive package (para. 2.07) by a government supported trainingprogram tied to either Coromandel or Plaine Lauzun. Industrial trainingprograms do exist under the aegis of the Ministries of Education, Labor andImmigration with, in some cases, support from UNDP and the ILO and additionalprograms are being planned.1/ These training programs have been providing aflew o~f i^ntice skilled workers (carpenters, bricklayers, plumbers) aswelw, as more skilled personnel (technicians including draftsmen, machinists,instrument mechanics). Training in commercial administration is availableon the university level. In view of the existing and apparently broadlybased national training effort, it was concluded that no special programwas needed as part of the project.

VII. FINANCIAL ANALYSIS

A. Income

7.01 Land and buildings will only be leased. Currently, undevelopedland, to the limited extent available in the Port Louis area, is being leasedat an annual rental of Rs. 6,000 to 8e,00 per arpent. By mid-1974, whenoccupancy will begin, a land lease rate at Coromandel of Rs. 10,000 perarpent cf developed land is assumed; this is considered a conservative assump-tion and competitive with alternative sites in the Port Louis area. Basedon past trends and projected demand, the annual lease rate can reasonablybe expected to increase by at least 8% per year for the foreseeable future.Lease rates will be fixed for a three-year term (the customary period alreadyestablished at Plaine Lauzun) and at each three-year renewal thereafter itIs assumed for purposes of the financial projections that the rate will beincreased by 25%. By way of comparison, at the most recently establishedexport processing zones in Taiwan, occupants have to pay an annual land rentalof about Rs. 35,000 per arpent.

1/ Bank/IDA report AE-30a, "Mauritius: 4-Year Development Plan - AnAssessment", October 24, 1972, p. 14-25.

- 17 -

7.02 Building rentals are projected to start at Rs. 5.0/sq.ft/year.Rentals at Plaine Lauzun have recently been increased to about Rs. 4.0/sq.ft./year, and DBM plans to increase this to Rs. 4.5-5.0/sq.ft. during thecourse of 1973. Starting rentals at Coromandel can therefore be reasonablyset at Rs. 5.0/sq.ft. in 1974. As with land leasing, building rental contractswill be at fixed rates for three years, renewable thereafter every threeyears with an assumed 25% increase in rent for each three-year period. Thisis a conservative assumption when compared to the inflation assumed in esti-mating project cost (Annex 14).

7.03 The starting land lease and building rental rates, being competitivewith other rates in the Port Louis area, are readily acceptable to potentialoccupants. Although the assumed increases of 25% every three years are con-sidered conservative, the actual lease terms need not necessarily contain sucha rigid formula, but rather provide for a reassessment in the light of actualexperience. The guiding criterion should be competitiveness. In addition,to protect the financial position of the estate, agreement was reachedduring negotiations that there will be consultation with IDA, whenever, forany reason, the return on total capital employed falls below 10% per annum.This leaves open the question of what measures should be adopted if theproject fails to yield such a return. Corrective action might involve measuresquite distinct from changes in rentals. This rate of return test, in effect,establishes a revenue "floor" which assures coverage of debt service andoperating costs as well as the use of capital in the project in as productivea way as elsewhere in the economy.

7.04 The total revenue build-up and flow from land leases and buildingrentals is detailed in Annex 15. Although the demand forecast indicatesthat 100% occupancy is a reasonable likelihood, all projections of incomehave been set at 90% occupancy of developed land and buildings.

7.05 Annex 16 lists the management and general overhead breakdown under(i) salaries and general overhead, (ii) insurance, (iii) building and groundmaintenance and (iv) international promotion. These expenses will start in1974 and build up to Rp. 930,000 per year by 1979, the first year of "normal"operation after completion of construction, corresponding to 15% of revenuein that year. Thereafter, it was assumed that operating costs could bemaintained at the same rate, (i.e. 15% of revenue). A special provision ofRs. 100,000 per year for international promotion is limited to the five-yearperiod 1974-1978, although this activity may have to be continued if occupancyruns significantly lower than predicted. Additional operating costs are(i) depreciation of 5% per year on infrastructure and buildings and (ii) 7.25%interest on the outstanding loan. The depreciation rate of 5% per year - aconservative building depreciation rate - has been applied to the totalproject (less land, which is not depreciated) since buildings account forover 90% of the project cost and any adjustment for differing rates applic-able to other infrastructure items would have been insignificant.

- 18 -

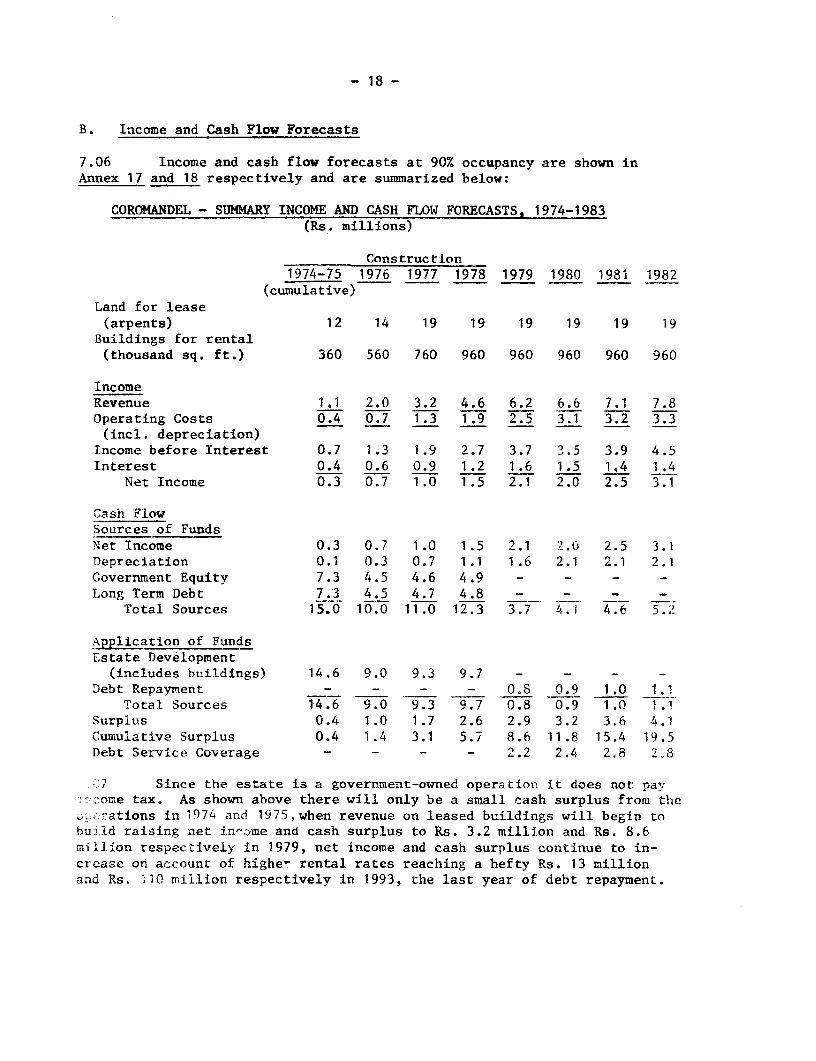

B. Income and Cash Flow Forecasts

7.06 Income and cash flow forecasts at 90% occupancy are shown inAnnex 17 and 18 respectively and are summarized below:

COROMANDEL - SUMMARY INCOME AND CASH FLOW FORECASTS, 1974-1983(Rs. millions)

Construction1974-75 1976 1977 1978 1979 1980 1981 1982

(cumulative)Land for lease(arpents) 12 14 19 19 19 19 19 19

Buildings for rental(thousand sq. ft.) 360 560 760 960 960 960 960 960

IncomeRevenue 1.1 2.0 3.2 4.6 6.2 6.6 7.1 7.8Operating Costs 0.4 0.7 1.3 1.9 2.5 3.1 3.2 3.3(incl. depreciation)

Income before Interest 0.7 1.3 1.9 2.7 3.7 _3.5 3.9 4.5Interest 0.4 0.6 0.9 1.2 1.6 1.5 1.4 1.4

Net Income 0.3 0.7 1.0 1.5 2.1 2.0 2.5 3.1

Cash FlowSources of FundsNet Income 0.3 0.7 1.0 1.5 2.1 2.0 2.5 3.1Depreciation 0.1 0.3 0.7 1.1 1.6 2.1 2.1 2.1Government Equity 7.3 4.5 4.6 4.9 - - -

Long Term Debt 7.3 4.5 4.7 4.8 - -

Total Sources 15.0 10.0 11.0 12.3 3.7 4.1 4.6 a.2

Application of FundsEstate Development(includes buildings) 14.6 9.0 9.3 9.7 - - - -

Debt Repayment _- - - 0.8 0.9 1,0 1.1Total Sources 14.6 9.0 9.3 9.7 0.8 0.9 1.0 1.1

Surplus 0.4 1.0 1.7 2.6 2.9 3.2 3.6 4.1Cumulative Surplus 0.4 1.4 3.1 5.7 8.6 11.8 15.4 19.5Debt Service Coverage - - - - 2.2 2.4 2,8 2.3

%i7 Since the estate is a government-owned operation it does not pay,,come tax. As shown above there will only be a small cash surplus from the

-- ations in 1974 and 1975,when revenue on leased buildings will begin tobuild raising net in-ome and cash surplus to Rs. 3.2 million and Rs. 8.6million respectively in 1979, net income and cash surplus continue to in-crease on account of highe- rental rates reaching a hefty Rs. 13 millionand Rs. M10 million respectively in 1993, the last year of debt repayment.

- 19 -

7.08 Debt service coverage starts at a comfortable 2.2 in 1979, thefirst year of debt amortization, and increases thereafter to 3.0 in 1983 and6.2 in 1993, the last year of debt amortization.

C. Balance Sheet Forecasts

7.09 Projected balance sheets of the estate operation are summarizedbelow from Annex 19. The starting year corresponds to the beginning of thesecond and last construction contract period (para. 4.02):

COROMANDEL - SUMMARIZED BALANCE SHEETS, 1976-1982(Rs. million)

1976 1977 1978 1979 1980 1981 1982

AssetsCurrent 1.4 3.1 5.7 8.6 11.8 15.4 19.5Fixed (Net) 23.2 31.8 40.4 38.8 36.7 34.6 32.5Total Assets 24.6 34.9 46.1 47.4 48.5 50.0 52.0

Liabilities and EquityCurrent - - 0.8 0.9 1.0 1.0 1.1Long Term Debt 11.8 16.4 20.5 19.6 18.6 17.6 16.5Equity 12.8 18.5 24.8 26.9 28.9 31.1 34.4Total Liabilitiesand Equity 24.6 34.9 46.1 47.4 48.5 50.0 52.0

Current Ratios - - 6.7 9.6 11.8 15.4 17.8Debt/Equity Ratio 48/52 47/53 45/55 45/55 42/58 39/61 36/64

7.10 Liquidity, or the current ratio, of the project is satisfactorythroughout the period of repayment of debt. The earned surplus credited tothe project will accrue in the total earnings of DBM from all its operationsand be rolled over in its normal lending program.

7.11 During negotiations assurances have been obtained that independentaudits will be conducted of the estate operations in a manner satisfactoryto IDA.

D. Financial Return and Viability Tests

7.12 The financial rate of return of the project was calculated withcosts and revenues in constant 1973 rupees (Annex 20). Based on 90% occu-pancy over a 20-year project life and a residual value equal to the bookvalue of investment, i.e. land valued at the actual price paid in 1973(Rs. 900,000) and no residual values for the buildings and infrastructure,the rate of return is 10.3%. Compared to the most recent estimate of op-portunity cost of capital of 8%1/, the project is acceptable. However, landvalues, which have more than doubled since DBM optioned Coromandel in early

1/ M.F.G. Scott, "Estimates of Accounting Prices in Mauritius", April 1972(mimeographed paper), p. 14.

- 20 -

1972, will continue to increase, and the re4z.:)-ocejl. gs will have auseful life far beyond 20 years especially if they are properly maintained,as is assumed in the project operating costs. If we assume a realistic netpresent value of Rs. 900,000 for the land and a residual value of half theinitial investment cost for buildings and infrastruicture, the rate of returnincreases to 12.4%. In addition, if we assume that rental rates will in-crease by 3% per year to reflect the increased scarcity of industrial landand buildings, the internal rate of return is 1534ZO This last case is themost realistic one, since it accounts for both residia; values in the build-ings and the scarcity value of the land.

7.13 Actually, there are two important interdependent variables whichaffect income and profitability. These are (i) rate of occupancy and (ii)land lease and rental levels. Assuming 80% occupancy and a rental rateof Rs. 5.0 per sq. ft. (equivalent in total revenue to '10X occupancy anda rental rate of Rs. 4.0 per sq. ft.), the rate of return is 13.0%. Thisis regarded as a realistic lower bound, for the fol.owving reasons: (a)DBM has a long waiting list for buildings at Plaine Lauzun at rental ratesof Rs. 4.0/sq. ft./year and soon to rise to 3s, s 45-5.01sq, lt,year; (b) theCoromandel estate will meet only about 13% of thie estimated demand forstandard buildings for the period 1973-1980, and no other estate projectsare currently planned.

7.14 Although considered very unlikely to occur, a further return testwas made assuming that construction ceases after the initial contract period(1973-75) because of lagging investment and lower than expected occupancy.Based on a reduced cost of US$2.7 million and 75% occupancy over 20 years,the financial return is 8% indicating that even on this basis the projectis feasible.

7.15 The projections based on constant terms not only show favorablerates of return but the projected debt service and current ratios arealso more than adequate.

DEBT SERVICE AND CURRENT RATIOS IN CONSTA.'NT TERMS PROJECTIONS

1980 1981 1982 1983 1984

Debt Service Coverage 2.4 2.4 2<4 2.4 2.4

Current Ratio 12.2 13.7 16.1 17.3 18.6

7.16 In reality, the return of 10.3% derived from the constant rupeeprojections (Annex 20) understates the financial return of the project.On the basis of current rupee projections outlined in para. 7.01-7.10, andagain assuming only 90% occupancy over 20 years of project life and no residualvalue, the return would be 15.0%.

- 21 -

7.17 In conclusion, the analytical tests of project profitabilitydemonstrate that the project is viable and justifiable. The sensitivity ofthe project to occupancy rates lower than projected is apparent, but it isvery unlikely that occupancy would in fact drop to a point at which thefinancial return would be less than 8Z (assumed opportunity cost of capital).In any case the project yields substantial economic and social benefits asdescribed in the following chapter.

VIII. ECONOMIC AND SOCIAL BENEFITS

8.01 A rigorous measure of the national benefits generated by the projectwould require a "with and without" ("with the project" and "without the proj-ect") comparative analysis. This in turn would require credible estimatesof the effect of the project on the rate of factory investment from which allcosts and benefits are derived - and this cannot really be quantified withany degree of accuracy. Undoubtedly, many industries have been and wouldcontinue to be established in Mauritius even if no estate were ever built.Prepared sites and services accelerate the investment decision process andin some cases might be a plus factor inducing a company "go" decision oninvestment which otherwise might have been "no go" or "wait". In the absenceof an accepted methodology to quantify the incremental benefits of the "with"situation, the paragraphs following will make qualitative judgements of thehard-to-quantify benefits and numbers will be used only for reasonablycredible estimates.

A. Acceleration of Industrial Investment

8.02 The project will facilitate and accelerate factory investment,particularly by foreign firms acting alone or in joint ventures with localcapital. Assuming (i) an average capital/output ratio of 3.5 1/ for thetype of industries foreseen and (ii) output (value added) of US$3,000 2/ peremployee at full occupancy in 1979, capital invested in the estate industrieswill be US$58 million and value added per annum US$17 million. Although thefull amounts cannot be attributed wholly to the estate, it is clear that manyof the foreign firms are specifically attracted to the ready availability ofstandard buildings and the infrastructure services. Since the bulk of theinvestment will be foreign capital inflow, a substantial part of the totalnew investment can be attributed to the estate. It is also reasonable toassume that local capital, which otherwise might leave the country in wholeor in part, will be a significant fraction of the whole.

1/ The current ratio for existing export processing industries in Mauritius.2/ Currently, value added per employee is under US$2,000 but this will be

increasing as efficiency improves and more sophisticated processes andproducts are introduced.

- 22 -

B. Employment

8.03 The completed project will house industries providing employmentfor 5,000-6,000 by 1979, rising to a peak in 1985 and beyond of perhaps8,000. Approximately 14% of the new factory jobs needed nationally between1973 and 1980 (38,000) would, therefore, be created on the estate 11. Thesituration level by 1985, equal to 170 jobs per arpent, is high in comparisonto usually accepted criteria and can be explained by the high allocation ofland (57%) to multi-level standard factory buildings for smaller and morelabor intensive activities. A very high percentage of workers will be trainedto higher skills and earning power than they have had in the past. Construc-tion workers may average 1,000 to 1,200 during the construction period of1973 to 1978. As in the case of investment, a substantial part of the newinvestment is directly the result of the establishment of the estate.

C. External and Internal Economies

8.04 The concentration of industries on the estate, as opposed to thehaphazard and dispersed pattern which would occur otherwise, greatlyfacilitates rational planning and installation of external infrastructure(power, water, sewage, roads, etc.). Costs will be lower since externalnetworks will be less dispersed and time schedules for planning and imple-mentation compressed. Within the estate, there will be internal economiesresulting from lover cap'tal investment per factory because of commonutilities and services.

D. Social Benefits

3.05 With estate management in control of the quality, cleanliness andappearance of factories as well as standards of employee services, theworking environment will be greatly improved. Among the common facilitiesforeseen are (i) a central canteen (many small firms make no provision forlunch facilities), (ii) an employees association and athletic field. Airpollution control standards will be enforceable and the common sewage treat-ment complex will eliminate liquid and solid waste problems. Town planning,including housing and transportation, schools, hospitals, and other socialinfrastructure can be developed efficiently for the concentration of workerswhich might correspond by 1985 to a family population of about 35,000.

E. Indigenous Entrepreneurship Development

,..<.6., A number of the industries already established are joint ventureso; -mixed foreign and local capital. Future growth can be expected to showa --7sing trend in local participation as domestic capital accumulationand .ocal management tapabilities grow. In the small scale industry sector,growth will assuredly accelerate in response to the need for ancillary supply

1f! As noted in para. 8.01, a more meaningful figure would be the jobaation i"with" the estate less the job creation "without" the estate,the incremental jobs attributable to the estate.

- 23 -

of services, parts and components to the larger industries. DBM is alreadyimplementing an organized program of small scale industry development by meansof a special lending program (maximum loan is Rs. 10,000 at a concessionalinterest rate of 4.5% per annum and pay-back of up to 10 years) and the Coro-mandel estate, by concentrating a large number of small enterprises at onelocation, will provide a framework for more efficient transfer of technicaland financial assistance, management training and marketing guidance. With-out the establishment of Coromandel as a focal point for these programs,these programs would not be as successful or, at the least, would be moreexpensive for an equivalent result.

F. Fiscal Benefits

8.07 Industries will generally be certified as "development" or "exportprocessing" and these enjoy income tax exemptions of 5-8 years and 10 ormore years respectively. Fiscal income in the form of taxes on profits,therefore, will not be realized until the 1980's. Assuming a 4/1 ratio ofgross product value (GPV) to added value or GPV of approximately US$100 millionin the mid-1980's 1/ and taxable profits of 10% on sales of US$10 million,corporate income taxes at 45% would equal US$4.5 million per year. Ofcourse, without the expense of the estate some increase in tax revenues wouldoccur from those enterprises that would be established anyway. The questionis whether the net benefits (i.e. tax revenues minus estate expenses, capitaland operating) are greater with the estate or without it. Since it hasearlier been indicated that the bulk of new investment will be in the form offoreign capital inflow and that many enterprises are specifically attractedby the advantages of the estate, it is probable that the net benefits withthe estate are greater; notional estimates under several assumptions tendto confirm that conclusion. Personal income taxes will add to the fiscalincome but no effort has been made to estimate this amount. Finally, theestate is projected to yield an operating profit and this will accrue to theGovernment as the owner of DBM.

G. Foreign Exchange Earnings

8.08 Net foreign exchange (FE) inflow attributable to the estate basedindustries can only be roughly estimated. The basic assumptions are (i)that profits after taxes will be entirely repatriated and (ii) capitalinvestment will be repatriated over time as permitted by the incentivesgranted. The estimate implies that all investment is foreign capital. If,in reality, some portion of the investment were to be indigenous, profitrepatriation and capital repatriation would be reduced and the net foreignexchange inflow would be increased. Value added approximately representsthe foreign exchange earned over the above the cost of imported materials.The inflow and outflow estimates for the post construction operating periodis tabulated below;

1/ GPV in 1980 would be an *stimated US$68 million; allowing for dollarescalation and increasing productivity, GPV rises to US$100 million(estimated) in the mid-1980's.

- 24 -

ANNUAL NET FOREIGN EXCHANGE EARNINGS, 1980-1990(US$ million)

Inflow 1980 1985 1990

Added Value /1 19.0 28.0 45.0

OutflowProfit Repatriation /2 11.0 18.0 20.0Equity Capital Repatriation /3 6.0 6.0 3.0

Net FE earned 2.0 4.0 22.0

/1 Assumes constant growth rate of 10% per year./2 Assumes that most tax holidays have run out by 1990; profits in

that year therefore reflect tax paymenits./3 Assumes 10 year capital recovery on average; for companies esta-

in the mid-1970's this outflow will cease by the late 1980's.

IX. AGREEMENTS REACHED AND RECOMMENDATIONS

9.01 During negotiations, the Government of Mauritius agreed to:

(a) Consult with the Association prior to taking a decision to expandthe Coromandel estate at La Tour (para. 3.02);

(b) Onlend the proceeds of the IDA credit of US$4.0 million to DBMon terms satisfactory to IDA (para. 4.06);

(c) Provide local currency finance of US$4.0 million equivalent toDBM as equity and in a timelv manner as required by the progress ofthe project (para. 4.05);

(d) Finance any cost overrun of the project, both local and foreigncurrency expenditures, on terms satisfactory to IDA (para. 4.03);

(e) Arrange to finance and cause to be implemented in a timely mannerthe necessary external and internal infrastructure installationsspecified as public utility responsibilities (para. 3.07);

(f) Cause DBM to establish a management unit with the necessary outsideassistance for execution and operation of the estate and supportit with additional DBM staff as required (paras. 6.04-6.06);

(g) Arrange for DBM to set up separate project accounts (para. 6.04)and have them audited by independent auditors acceptable to theAssociatior (para. 7.11);

- 25 -

th) Set initial land lease and building rentals acceptable to IDA,maintain these rentals at competitive levels and consult withIDA whenever the rate of return on total capital. employed inthe project falls below 10% per annum (para. 7.03);

(i) Reimbure DBI in any fiscal year for losses in excess of thecumulative earned surplus from estate operations (para. 4.06);and

(j) Prepare, prior to December 31, 1973, tormal criteria governingacceptability of industries as estate occupants and estate buildingstandards satisfactory to TDB (para. 3.07 and 6.06).

9.02 In view of the foregoing agreements, the project provides a suit-able basis for an IDA credit of US$4.0 million equivalent to the Gover,amelntof M'auritius on normal IDA terms.

Industrial Projects DepartmentJune 6, 1973

MAURITIUS

COROMANDEL INDUSTRIAL ESTATE

SECTIORAL EMPLOJYMENT AND) GROWTH TARGETS, 1969-19Fak

Employment Eiployment Employment Emloyment Employment % of total1969 Creation Targets Creation Targets Employment

Activities (actuall) 10-1975 1975 1970-1980 1980 1980

Agriculture including live-stock, forestry, fisheries 76,200 16,600 92,700 32,900 109,000 33.5

Mining and Quarrying. 400 250 650 600 1,000 0.3

Manuf actui5ngsugar and tea processing 6,600 0 6,600 0 6,600 2.0other (enqloying 10 or more) 9,000 8,000 17,000 35,400 44,400 13.7other (artisans) 9.4o 2,00 11.400 _6 16,000 J .9

Sub-Total 25,000 10,000 35,000 42,000 67,000 20.6

Construction, and Public works 13,000 7,500 20,500 17,000 30,000 9.2

Public Utilities 1,300 750 2,050 1,700 3,00 0.9

Transport and C0fflVnicatiofns 13,400 2,700 16,700 6,600 20,000 6.2

Trade 19,800 4,100 23,900 8,200 28,000 8.6

Services (including tourism) 32,100 8,800 4°,900 17,900 50,000 15.b

Government adiistration 13,900 1,600 15,500 3,100 17,000 5.3

TOTAL 195,000 52,300 247,900 130,000 325,000 100 %

* Source: 4-Year Plan/1971-197 5

Industrial Projects Department

Jur.e f, 1973

ANhE 2

MA'JRITIUS

COROMANDEL INDVSTRIAL ESTATE

NUMBERS OF DEVELOPMENT CERTIFICATES APPROVED 1963-1972

13E+ 129 (Octobre 1972)

12t _

110 (A) _ _ - q f ,' 1 -110 (Octobre 1972)

10 ___ ____ ___ __ __ ____/)/

* __ ____ I ____ ___ __ -IN~~~~~~~~I

t -[~~~~~~~~~~~~Dvloenn eriiae

-i | t -, . -f ui j2I 1

SoLMS MIISR OF COMRC,N INDUSTRY

Iustria Pro t e e n

June c I !97,3(,, inciusivt)i a /// ' ,1 , i ' --- i-DOv6iOp9mrent ctrttitcagss____ ____ , __ ____ .o n 1 l nutucturlng indus -1 / | T t---- - I ---- I i - J t ---- ~~~~~~~tri.sC.xcIatig ho1els ,tou-it -, f lens ndshpngcrnu

$~~~5 641&18 67 61 1 70 71 72 (*s) d whech92Qre opmrtiv

SOI.RCES: MlhlSTRY OF COMM1ERCE ANO INDUSTRY

Induistri al ?rojZects D)epartment

June E, 1973

ANNEX 3

MAURIrIUS

COROMANDEL INDUSTRIAL ESTATE

OPERATING EXPORT PROCESSING ENTEPRISES - 1972

Name & Address of ComPpary Products Employees

1. LSP Ltd.c/o Poncini & Alls Ltd., Diamond Cutting & Polishing 75Port Louis

2. Resultant Co. (Mtius) Ltd., Industrial gloves 80Plaine Lausun

3. Cie des Maquettes Boat Models n.a.Jose Ramar Ltee

4. Vettex (Mtius) Ltd., Garments 125Plaine Lauzun

5. Suzie Toys Ltd.Chapman Hill. Toys and games 75Beau Bassin

6. Floreal Knitwear (Mtius) Ltd., Knitwear 1269Floreal

7. Maritius Foods Ltd. Tomato relish, soups, vegetableTrianon. pickles, etc. n.a.

8. Classic Design (Pty) Ltd. Reproduction of antique 35c/o Poncini & Fils Ltd. furniture

9. Elcom Ltd., Electronic Industry n.a.G.R.N.W.

10. Career Co. (Mtius) Ltd.18, Queen Street Wigs 100Port Louis

11. Orkay Synthetics (M) Ltd. Processing of fibres 30Plaine Lausun

12. Overseas Glove Factory Ltd.Industrial Estate, Block A 1st Floor Gloves 70Plaine Lauzun

13. Southern Cross Diamond Co., Ltd. Synthetic Diamond abrasive grit 30Plaine Lauzun

14. C.M.M.R,G.R.N.W. Port Louis Rattan Furniture n.a.

15. International Wigsc/o Knitting Fabrics Industries Wigs 100Bonne Terre, Vacoas

16. Textile Industries Garments 700P.O. Box 648, Port Louis

17. Compagnie Mauricicnne Comrmerciale Garments for ladius and children h5

lo. ?roton Ltd. Peanut flour 60

19. Micro Electronics Co. Electronics 113

20. Overseas Marine Products Marine Products 45

21. BATA Shoes Shoes 100

Sub-Total 3,052

Add estimate for "n.s.tsls 148

Total 1972 Smploynentz 3,200

1/ InUtial employment before grcwth of these industries sveraged about 100 jobsper enterprise or 2,100 jobs total.

Indu trial Projectt DepertmentJune 6, 1973

MAURITIUS

COROMANDEL INDUSTRIAL ESTATE

PROJECTED MANUFACTURING EMPLnY1MNT AND LAND REQUIRTSIS, 1970-198U-/

Cumnlative1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1931980)

Actul - ----- --- Estimate ---- - ibers

New mlomnt (Numbers)- 300 1,000 1,400 1,630 1,870 2,150 2,470 2,840 3,270 3,760 4,330 22,320

-all Scale Inhustvy - 400 500 500 600 600 600 600 700 700 700 700 5200