REPORTING FOR INSURERS IN ZIMBABWE CLARIFIED

54

REPORTING FOR INSURERS IN ZIMBABWE CLARIFIED

Transcript of REPORTING FOR INSURERS IN ZIMBABWE CLARIFIED

REPORTING FOR INSURERS IN ZIMBABWE CLARIFIED

WHAT IS ON THE MENU

1. Purpose & Scope

2. Background

3. Research methodology

4. Clarification & Use of certain terms

2

4. Clarification & Use of certain terms

5. Research Findings and Recommendations

Purpose & Scope

� To clarify the appropriate financial reporting to insurers in Zimbabwe;

� To achieve uniform, technically correct and globally acceptable financial reporting by all Zimbabwean

3

acceptable financial reporting by all Zimbabwean insurers.

the cause and concerns

Background4

Background

� Lack of uniformity in reporting by insurance

companies: lack of uniformity identified by stakeholders (regulator, analysts, auditors, e.g.)

5

� Technical acceptability: desire to achieve global acceptable and technically sound financial reporting by all insurers.

� Public interest: to protect the interest of all stakeholders vested in the insurance companies (investors, policyholders, e.g.)

Background (continued)6

� In order to address the above the Insurance sub –committee of the Accounting Procedures Committee (APC) of the Institute of Chartered Accountants (ICAZ)(Z) was mandated to research and recommend appropriate financial reporting best recommend appropriate financial reporting best practices for Zimbabwean insurers.

Research participants & expertise, coverage, documentation & evidence.

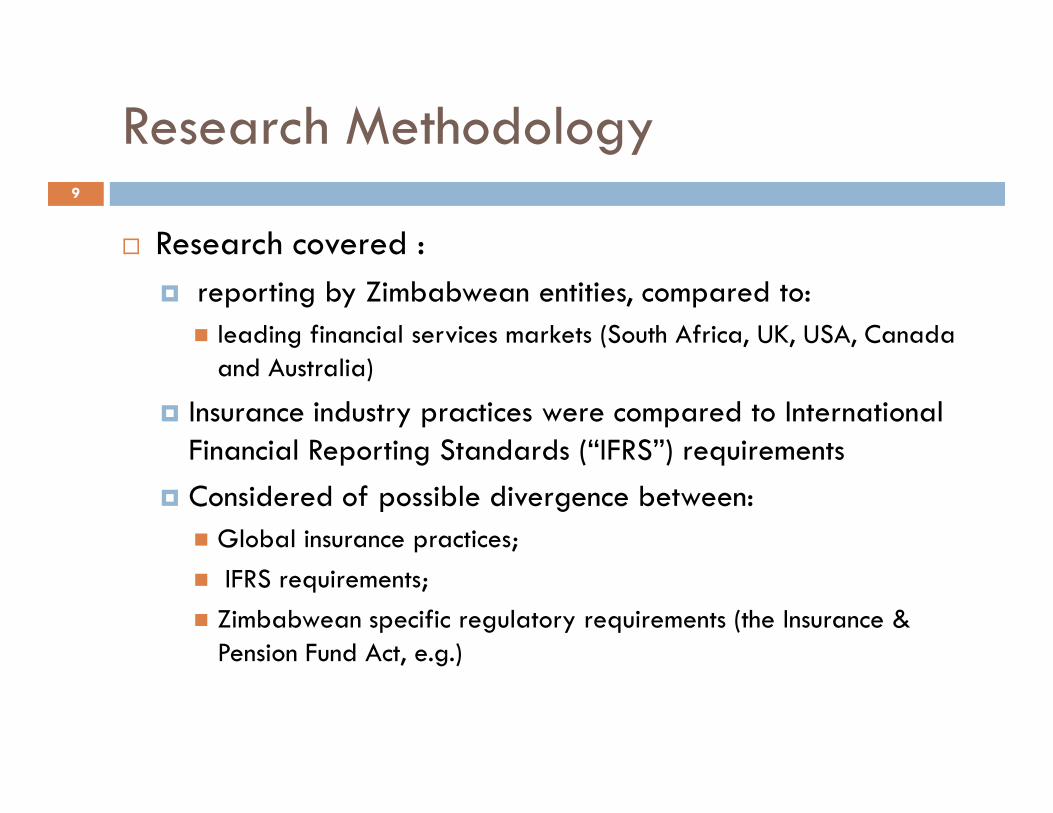

Research Methodology7

documentation & evidence.

Research Methodology

� Who was involved?: � IPEC representatives

� ICAZ Insurance sub committee of Accounting Procedures Committee:� Preparers of insurance financial statements

8

� Preparers of insurance financial statements

� Actuaries

� Auditors of insurance entities

� IFRS technical experts

NB: The researchers worked in teams based on interest and experience.

Research Methodology

� Research covered :

� reporting by Zimbabwean entities, compared to:

� leading financial services markets (South Africa, UK, USA, Canada and Australia)

� Insurance industry practices were compared to International

9

� Insurance industry practices were compared to International Financial Reporting Standards (“IFRS”) requirements

� Considered of possible divergence between:

� Global insurance practices;

� IFRS requirements;

� Zimbabwean specific regulatory requirements (the Insurance & Pension Fund Act, e.g.)

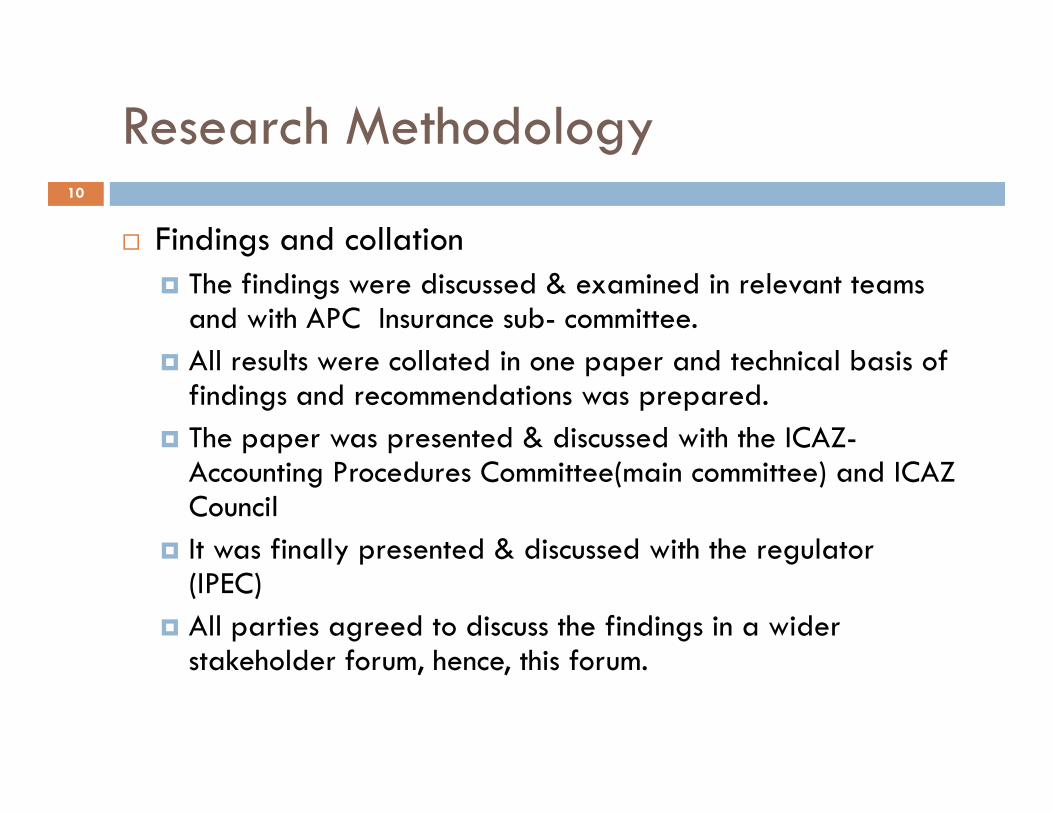

Research Methodology

� Findings and collation

� The findings were discussed & examined in relevant teams and with APC Insurance sub- committee.

� All results were collated in one paper and technical basis of findings and recommendations was prepared.

10

findings and recommendations was prepared.

� The paper was presented & discussed with the ICAZ-Accounting Procedures Committee(main committee) and ICAZ Council

� It was finally presented & discussed with the regulator (IPEC)

� All parties agreed to discuss the findings in a wider stakeholder forum, hence, this forum.

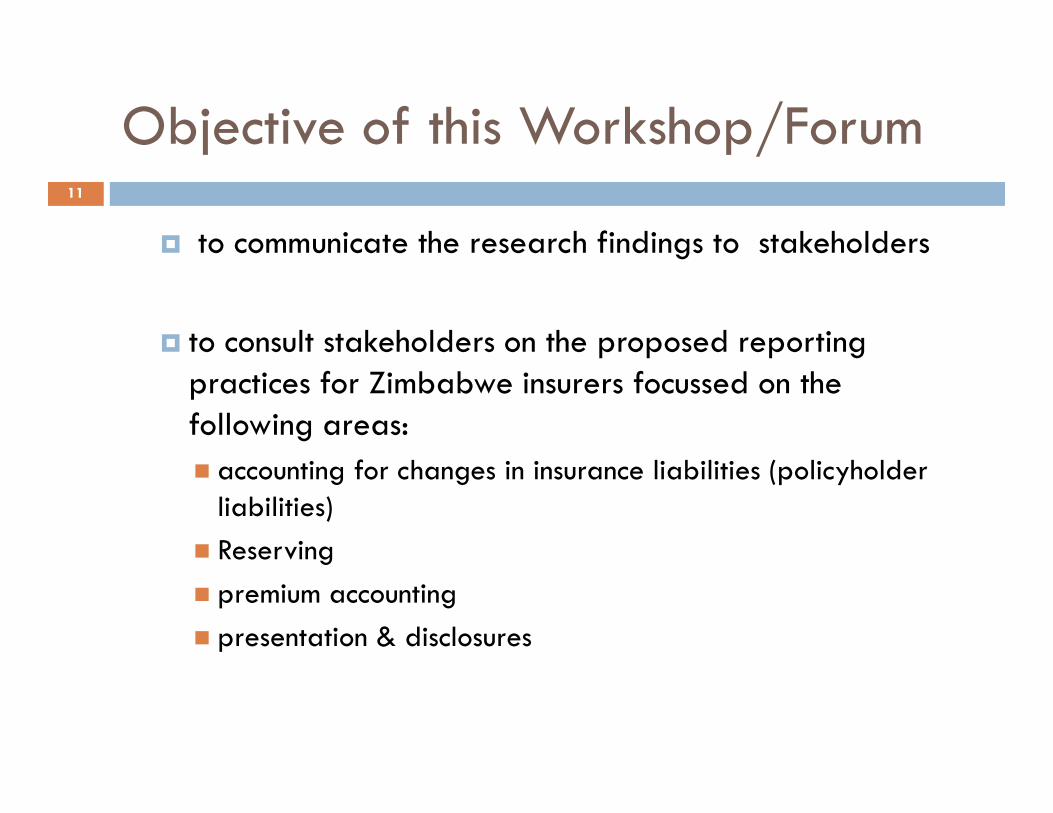

Objective of this Workshop/Forum

� to communicate the research findings to stakeholders

� to consult stakeholders on the proposed reporting practices for Zimbabwe insurers focussed on the following areas:

11

following areas:

� accounting for changes in insurance liabilities (policyholder liabilities)

� Reserving

� premium accounting

� presentation & disclosures

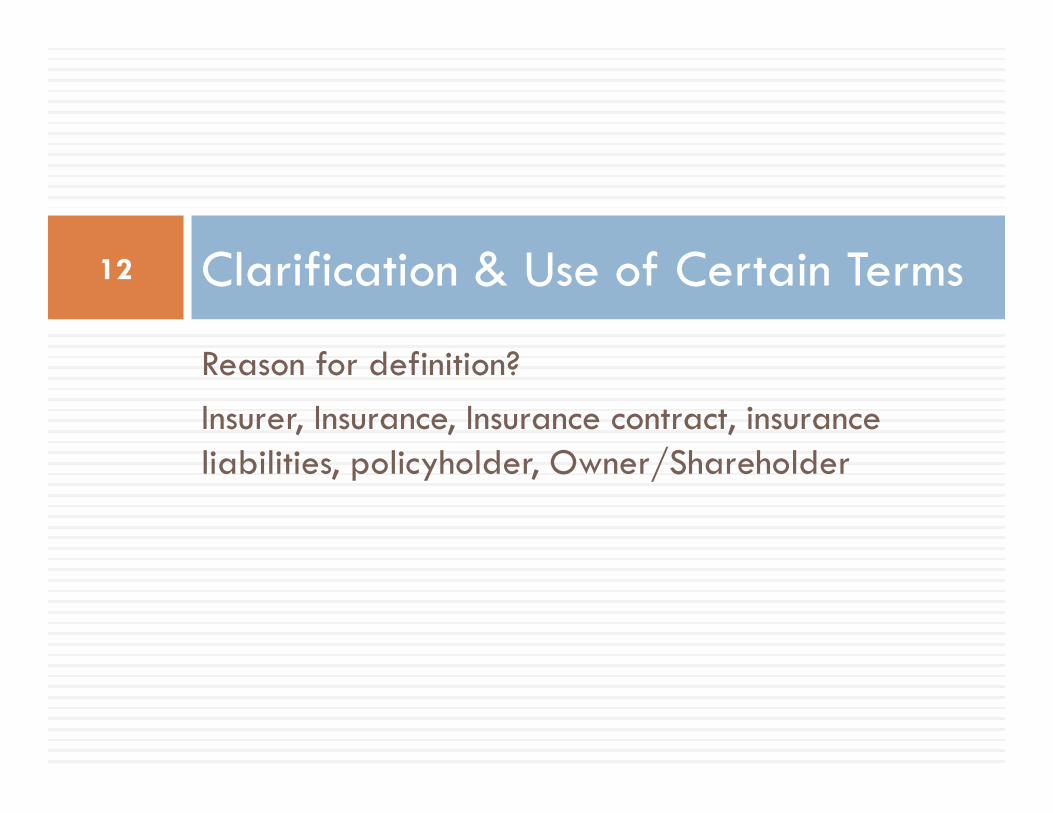

Reason for definition?

Insurer, Insurance, Insurance contract, insurance

Clarification & Use of Certain Terms12

Insurer, Insurance, Insurance contract, insurance liabilities, policyholder, Owner/Shareholder

Clarification & Use of Certain Terms

� Reason for definitions:

� To clarify:

� the affected parties (insurers providing insurance services)

� Certain misused terms:

13

� policyholder liability vs insurance/actuarial reserves vs insurance liability

� Policyholders vs Owners vs Shareholders

Clarification & Use of Certain Terms

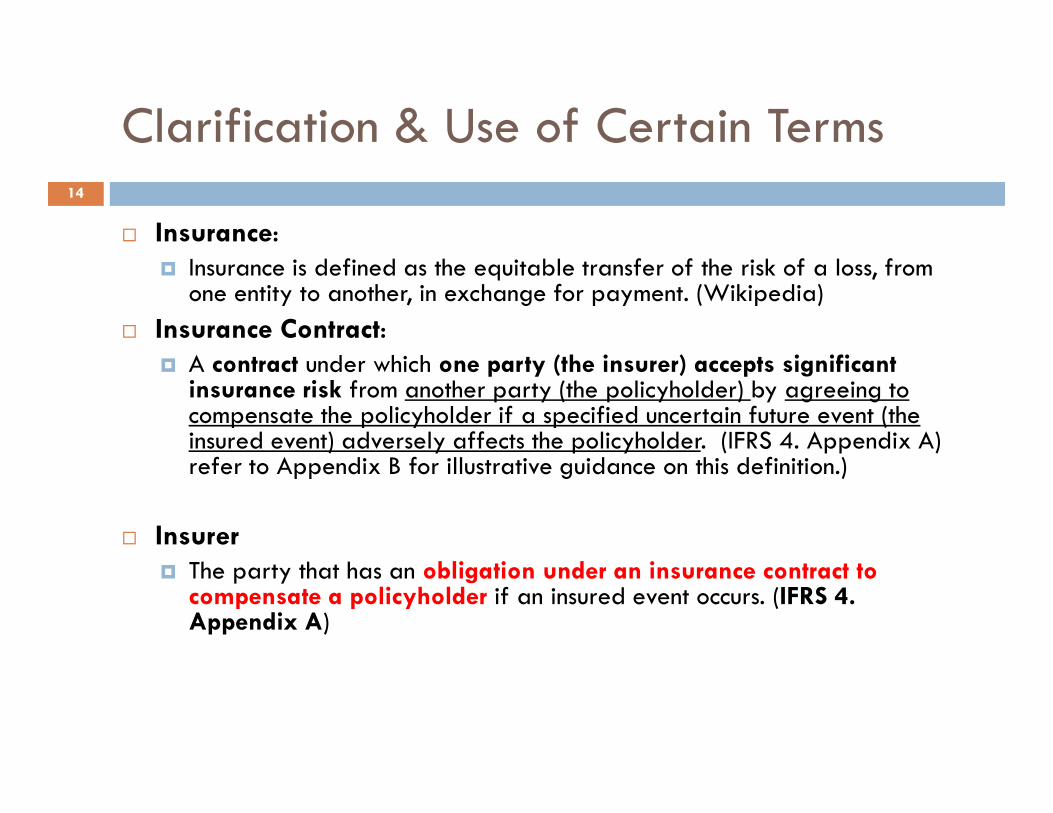

� Insurance:� Insurance is defined as the equitable transfer of the risk of a loss, from

one entity to another, in exchange for payment. (Wikipedia)

� Insurance Contract:� A contract under which one party (the insurer) accepts significant

insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the

14

compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder. (IFRS 4. Appendix A) refer to Appendix B for illustrative guidance on this definition.)

� Insurer

� The party that has an obligation under an insurance contract to compensate a policyholder if an insured event occurs. (IFRS 4. Appendix A)

Clarification & Use of Certain Terms

Insurance is classified into two groups:

� Life insurance: life insurance, annuities and pensions products.

� Non-life: general, or property/casualty insurance

15

� Non-life: general, or property/casualty insurance other types of insurance, e.t.c.

Clarification & Use of Certain Terms

� Types of Insurance:� Auto insurance

� Gap insurance

� Home insurance

� Health insurance

� Accident, sickness and unemployment insurance

16

� Accident, sickness and unemployment insurance

� Casualty

� Life

� Burial/Funeral insurance

� Property

� Liability

� Credit

� Other types

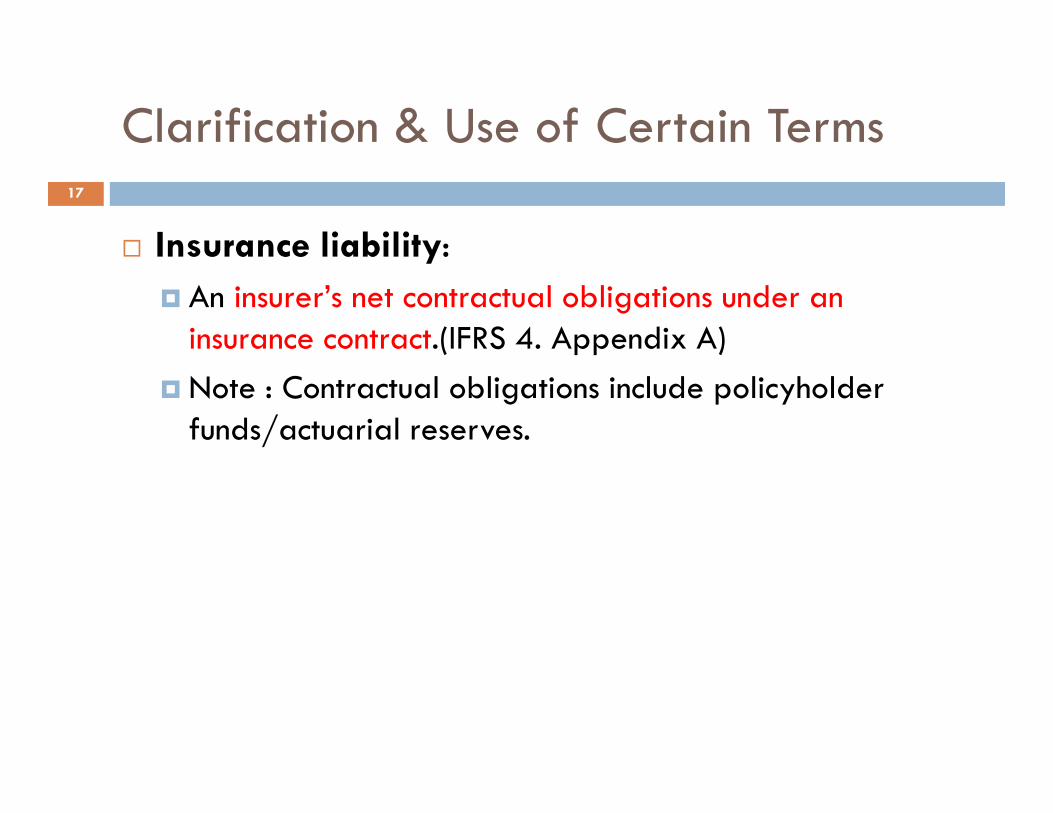

Clarification & Use of Certain Terms

� Insurance liability:

� An insurer’s net contractual obligations under an insurance contract.(IFRS 4. Appendix A)

� Note : Contractual obligations include policyholder

17

funds/actuarial reserves.

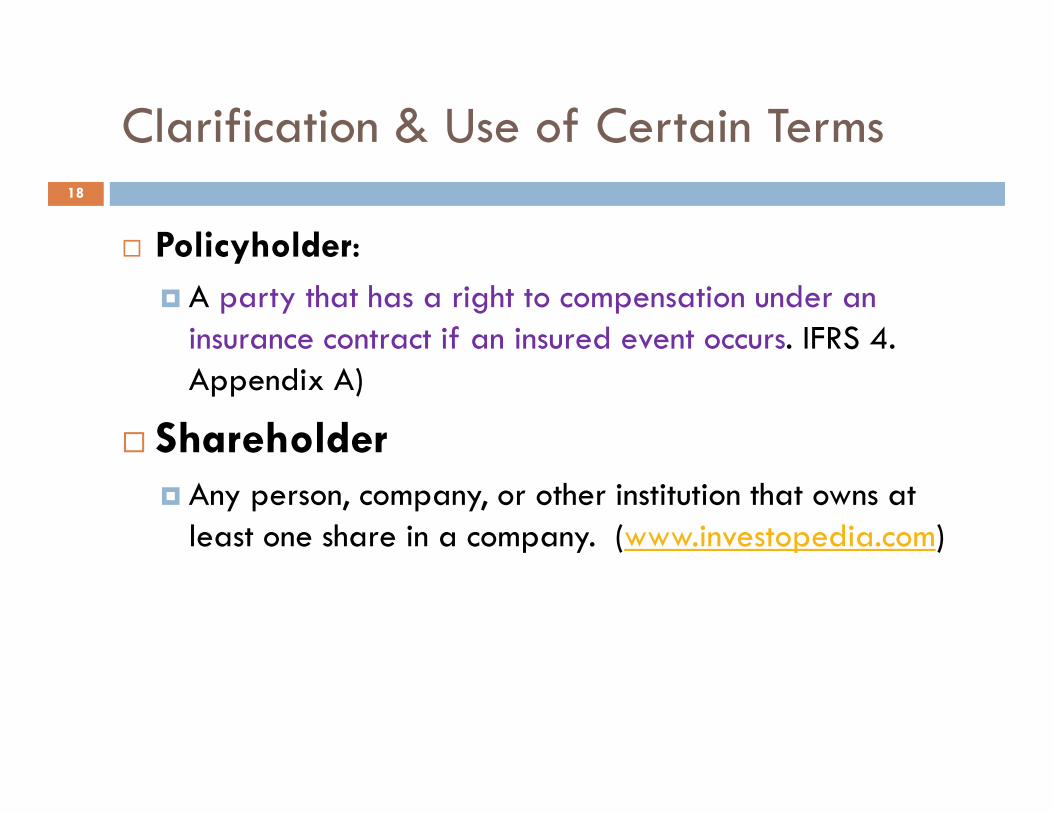

Clarification & Use of Certain Terms

� Policyholder:

� A party that has a right to compensation under an insurance contract if an insured event occurs. IFRS 4. Appendix A)

18

� Shareholder� Any person, company, or other institution that owns at

least one share in a company. (www.investopedia.com)

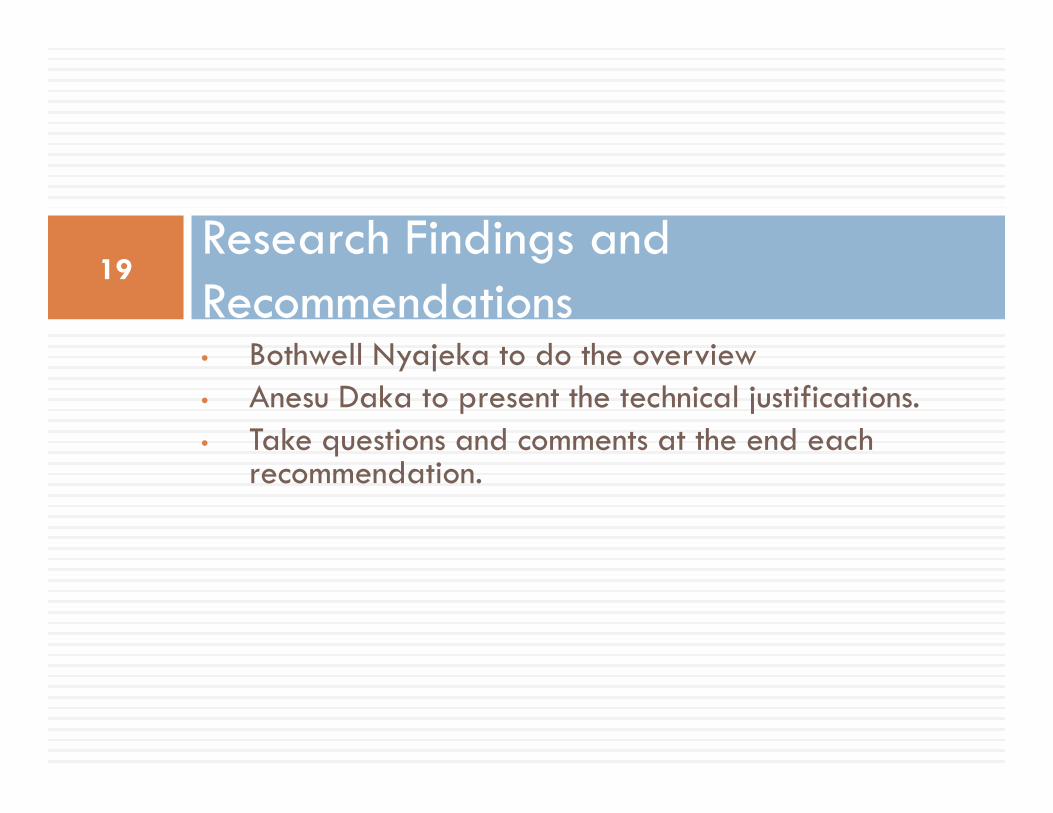

• Bothwell Nyajeka to do the overview

• Anesu Daka to present the technical justifications.

Research Findings and Recommendations

19

• Anesu Daka to present the technical justifications.

• Take questions and comments at the end each recommendation.

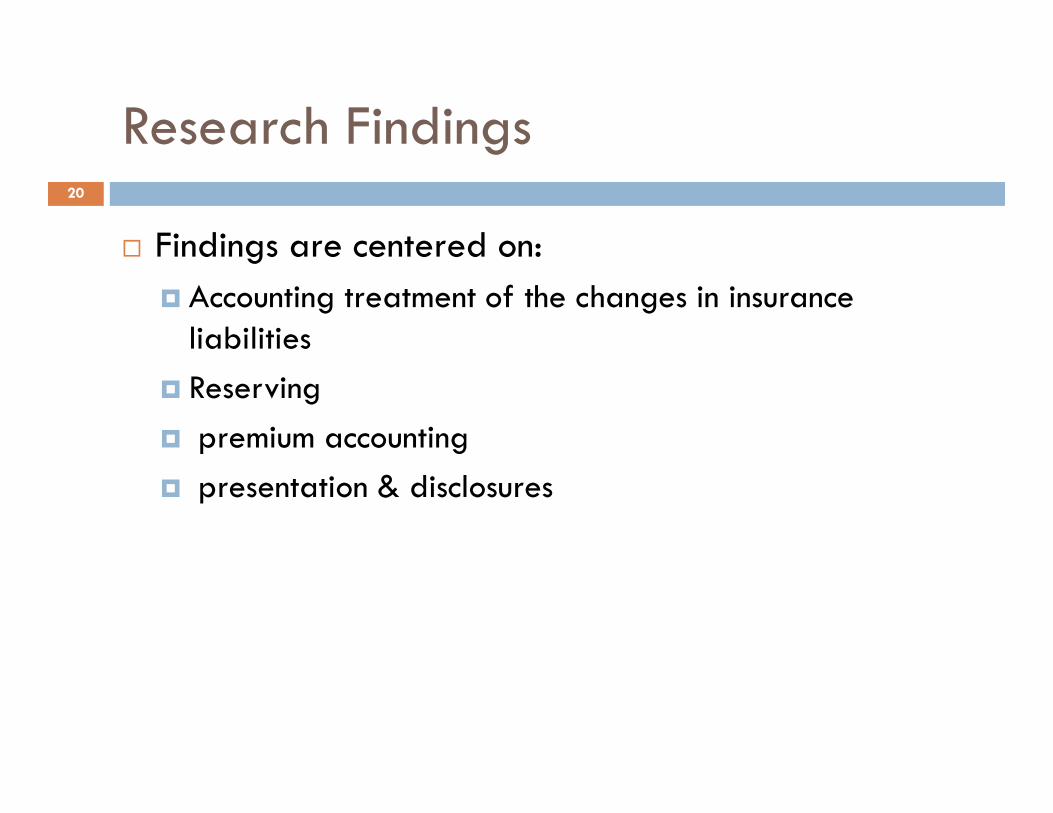

Research Findings

� Findings are centered on:

� Accounting treatment of the changes in insurance liabilities

� Reserving

20

� premium accounting

� presentation & disclosures

Research Finding21

Research Findings

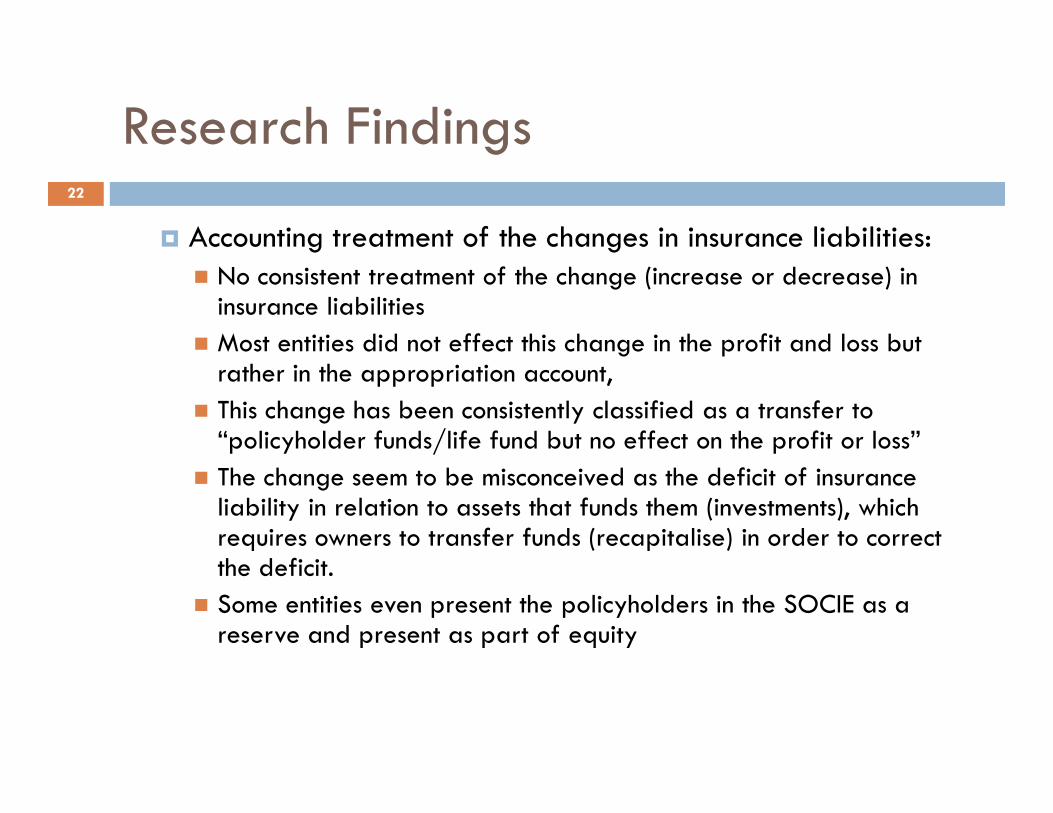

� Accounting treatment of the changes in insurance liabilities

Research Findings

� Accounting treatment of the changes in insurance liabilities:� No consistent treatment of the change (increase or decrease) in

insurance liabilities

� Most entities did not effect this change in the profit and loss but rather in the appropriation account,

� This change has been consistently classified as a transfer to

22

� This change has been consistently classified as a transfer to “policyholder funds/life fund but no effect on the profit or loss”

� The change seem to be misconceived as the deficit of insurance liability in relation to assets that funds them (investments), which requires owners to transfer funds (recapitalise) in order to correct the deficit.

� Some entities even present the policyholders in the SOCIE as a reserve and present as part of equity

Research Findings23

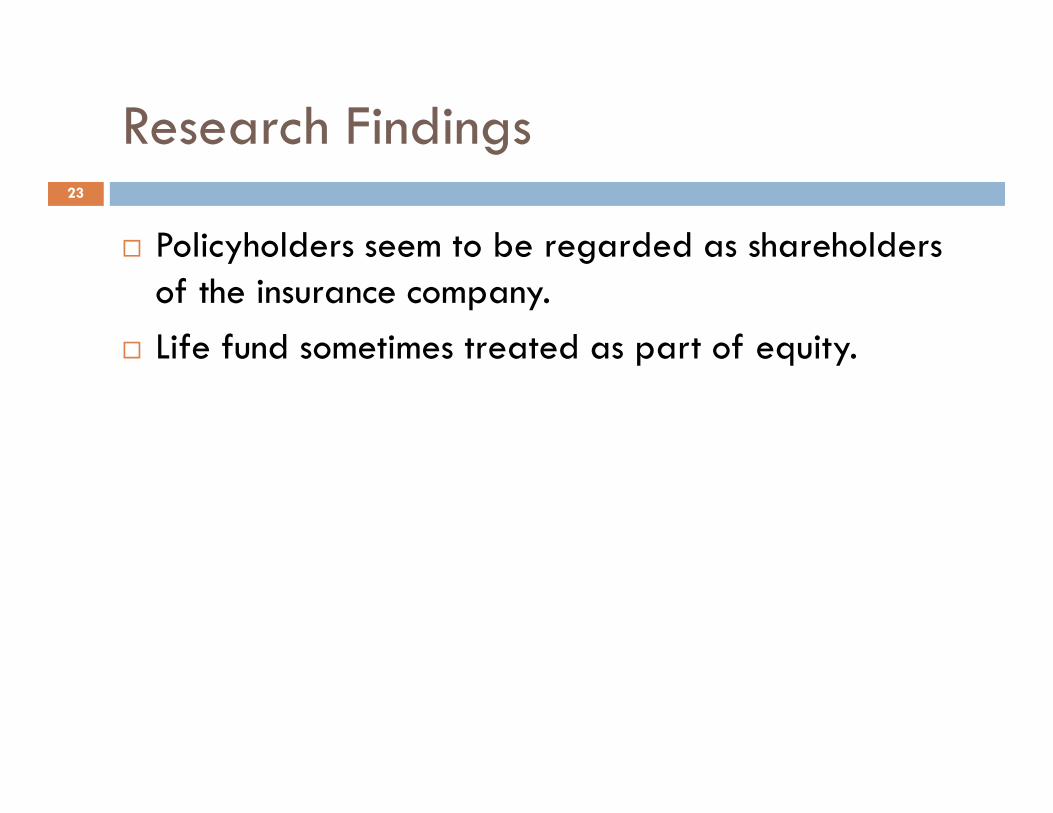

� Policyholders seem to be regarded as shareholders of the insurance company.

� Life fund sometimes treated as part of equity.

Recommendation24

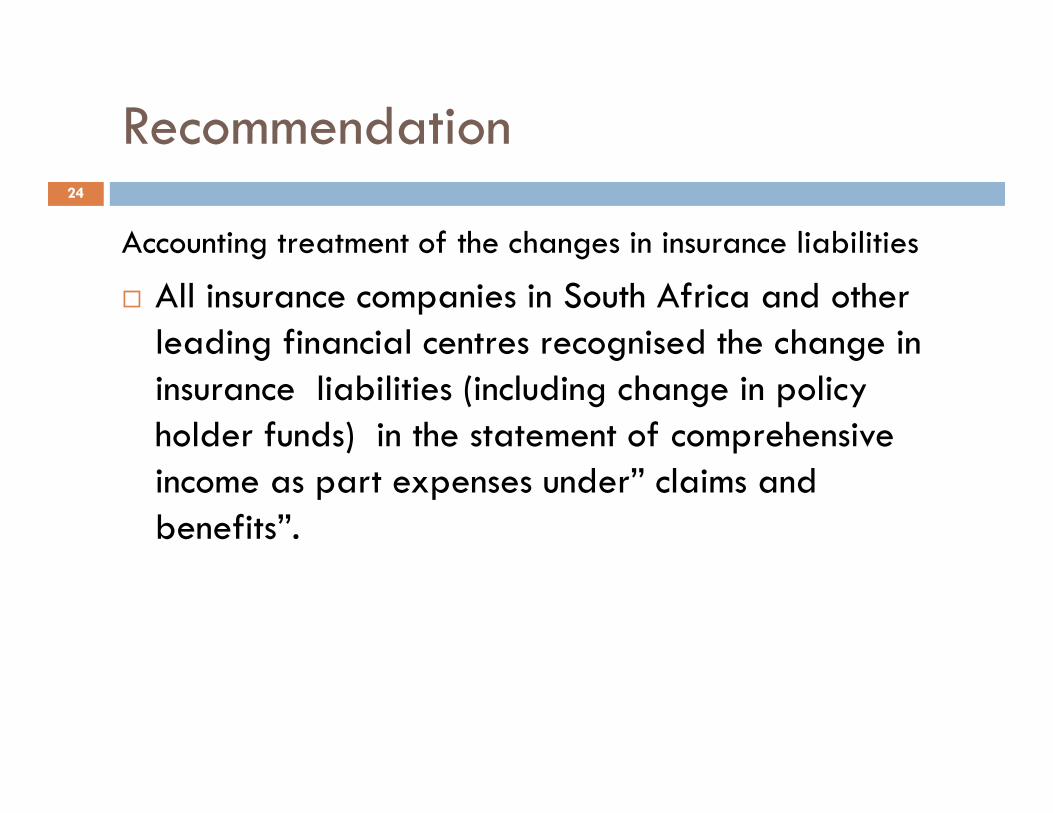

Accounting treatment of the changes in insurance liabilities

� All insurance companies in South Africa and other leading financial centres recognised the change in insurance liabilities (including change in policy insurance liabilities (including change in policy holder funds) in the statement of comprehensive income as part expenses under” claims and benefits”.

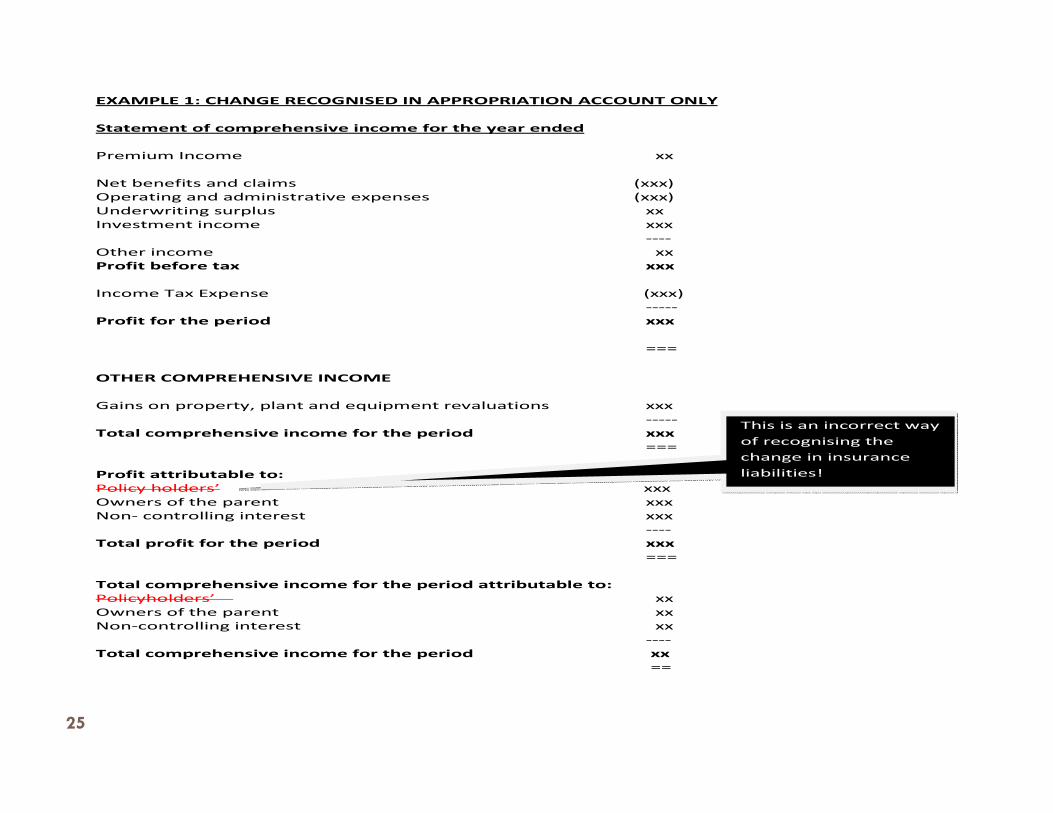

EXAMPLE 1: CHANGE RECOGNISED IN APPROPRIATION ACCOUNT ONLY

Statement of comprehensive income for the year ended

Premium Income xx

Net benefits and claims (xxx)

Operating and administrative expenses (xxx)

Underwriting surplus xx

Investment income xxx

----

Other income xx

Profit before tax xxx

Income Tax Expense (xxx)

-----

Profit for the period xxx

===

OTHER COMPREHENSIVE INCOME

Gains on property, plant and equipment revaluations xxx

25

Gains on property, plant and equipment revaluations xxx

-----

Total comprehensive income for the period xxx

===

Profit attributable to:

Policy holders’ xxx

Owners of the parent xxx

Non- controlling interest xxx

----

Total profit for the period xxx

===

Total comprehensive income for the period attributable to:

Policyholders’ xx

Owners of the parent xx

Non-controlling interest xx

----

Total comprehensive income for the period xx

==

This is an incorrect way

of recognising the

change in insurance

liabilities!

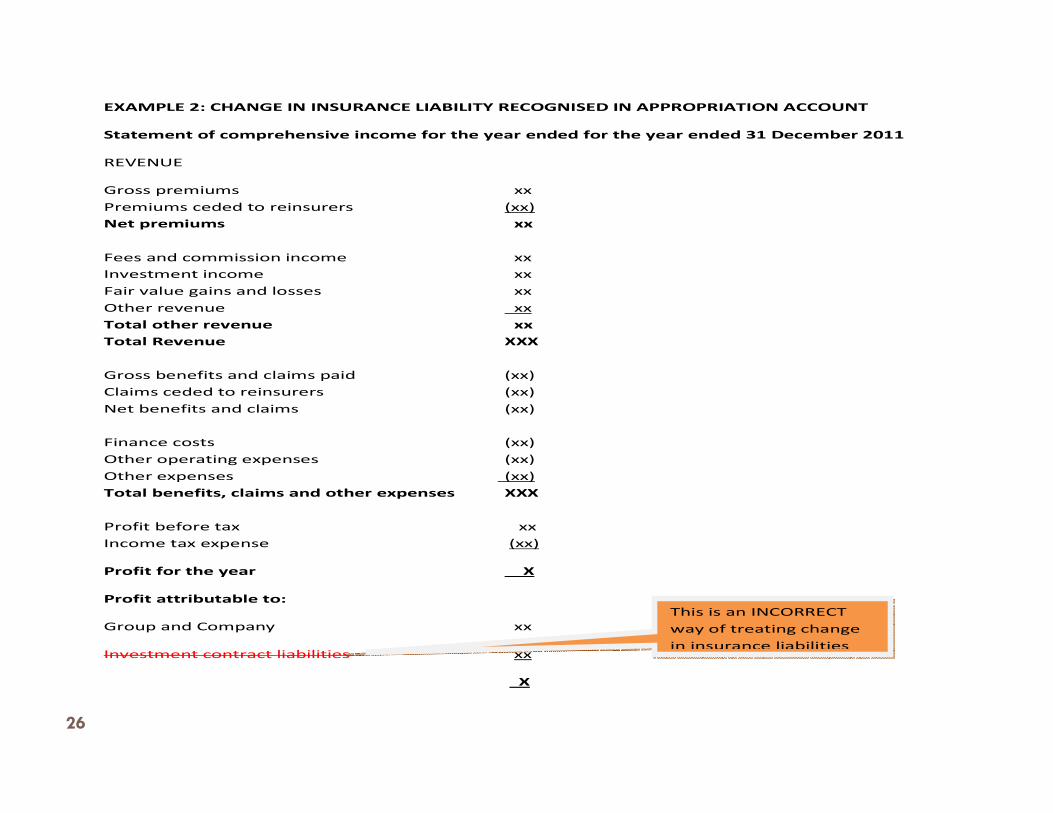

EXAMPLE 2: CHANGE IN INSURANCE LIABILITY RECOGNISED IN APPROPRIATION ACCOUNT

Statement of comprehensive income for the year ended for the year ended 31 December 2011

REVENUE

Gross premiums xx

Premiums ceded to reinsurers (xx)

Net premiums xx

Fees and commission income xx

Investment income xx

Fair value gains and losses xx

Other revenue xx

Total other revenue xx

Total Revenue XXX

Gross benefits and claims paid (xx)

Claims ceded to reinsurers (xx)

Net benefits and claims (xx)

26

Net benefits and claims (xx)

Finance costs (xx)

Other operating expenses (xx)

Other expenses (xx)

Total benefits, claims and other expenses XXX

Profit before tax xx

Income tax expense (xx)

Profit for the year X

Profit attributable to:

Group and Company xx

Investment contract liabilities xx

X

This is an INCORRECT

way of treating change

in insurance liabilities

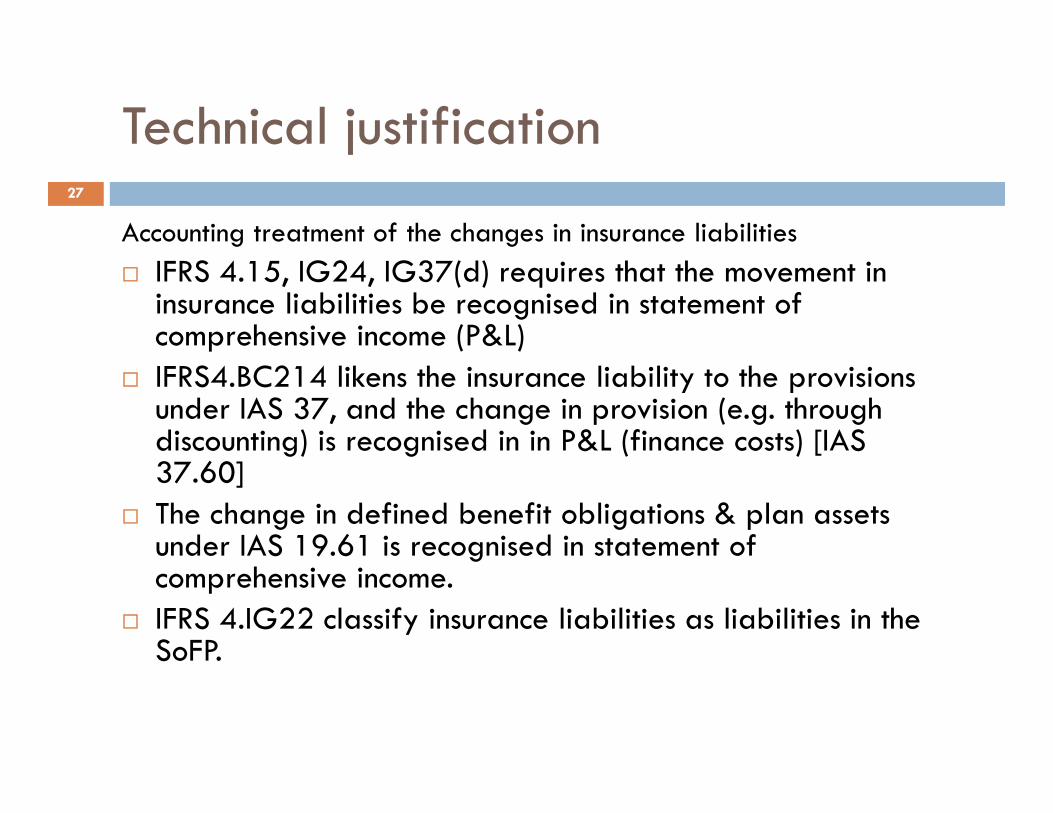

Technical justification27

Accounting treatment of the changes in insurance liabilities

� IFRS 4.15, IG24, IG37(d) requires that the movement in insurance liabilities be recognised in statement of comprehensive income (P&L)

� IFRS4.BC214 likens the insurance liability to the provisions under IAS 37, and the change in provision (e.g. through under IAS 37, and the change in provision (e.g. through discounting) is recognised in in P&L (finance costs) [IAS 37.60]

� The change in defined benefit obligations & plan assets under IAS 19.61 is recognised in statement of comprehensive income.

� IFRS 4.IG22 classify insurance liabilities as liabilities in the SoFP.

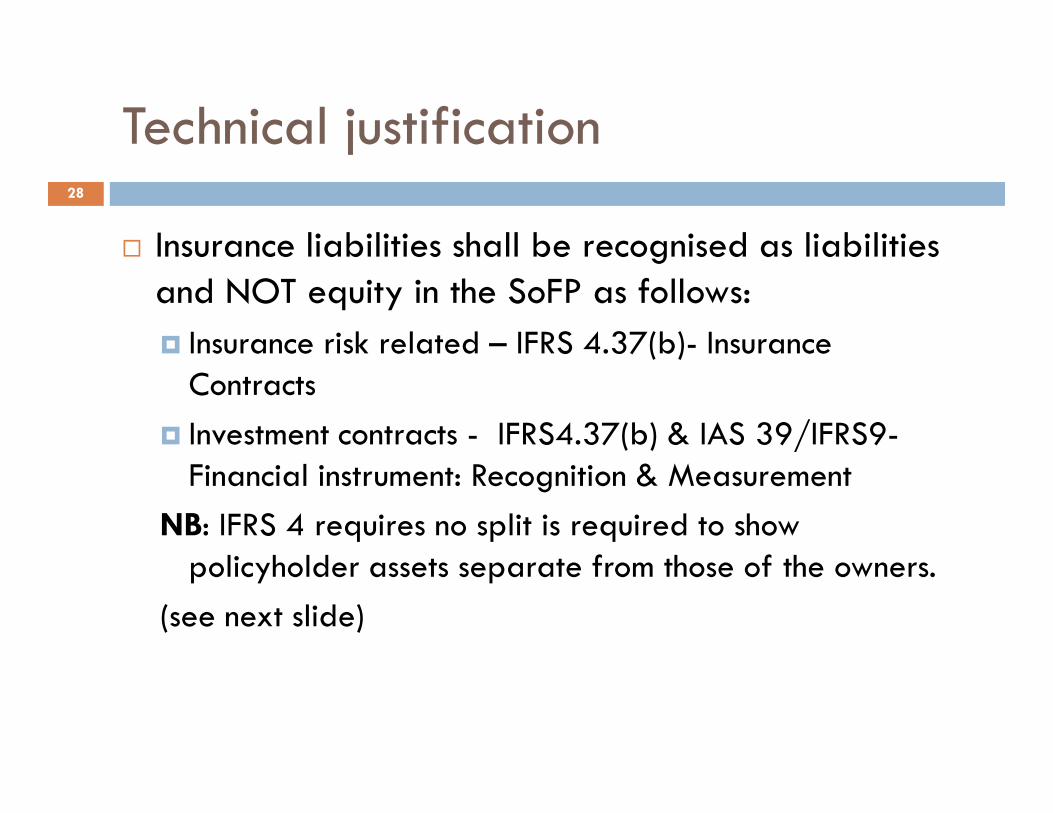

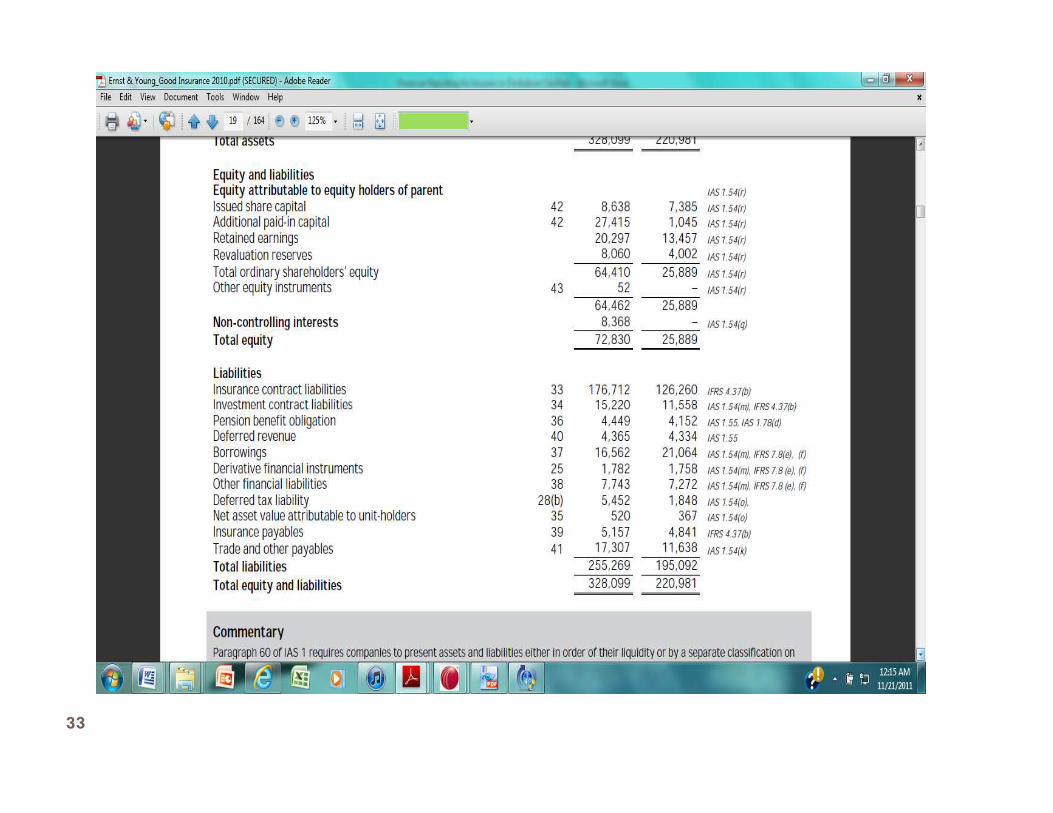

Technical justification28

� Insurance liabilities shall be recognised as liabilities and NOT equity in the SoFP as follows:

� Insurance risk related – IFRS 4.37(b)- Insurance Contracts

� Investment contracts - IFRS4.37(b) & IAS 39/IFRS9-Financial instrument: Recognition & Measurement

NB: IFRS 4 requires no split is required to show policyholder assets separate from those of the owners.

(see next slide)

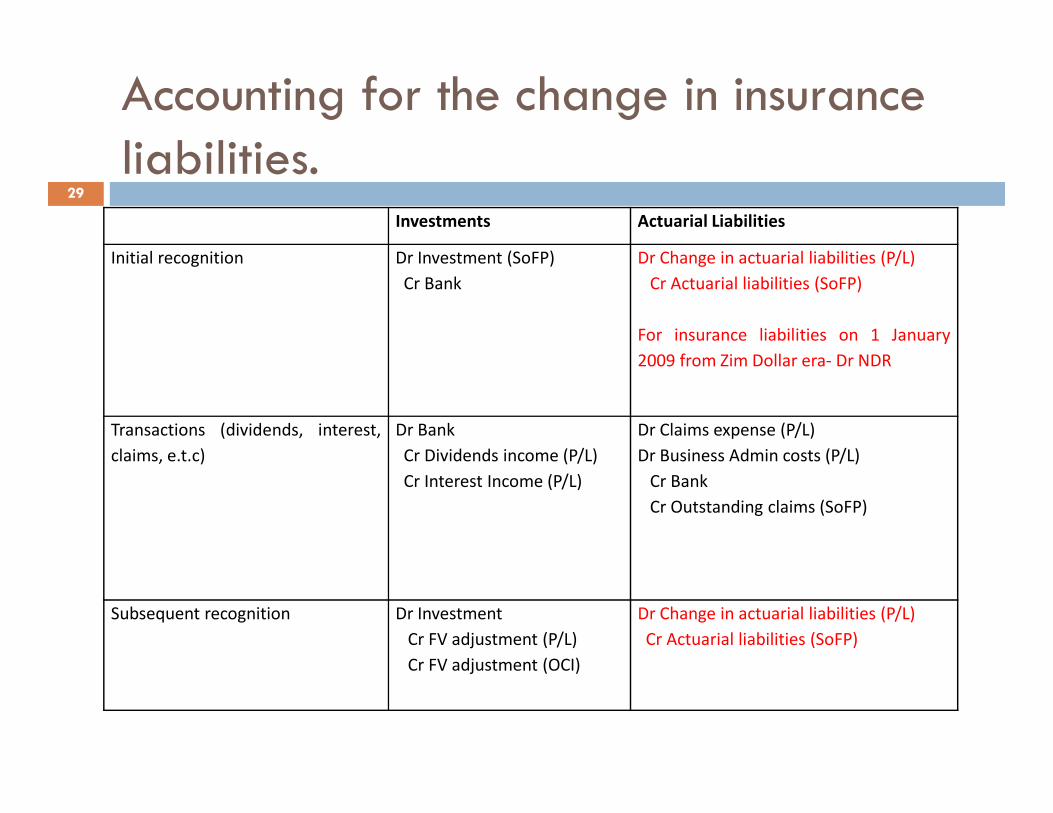

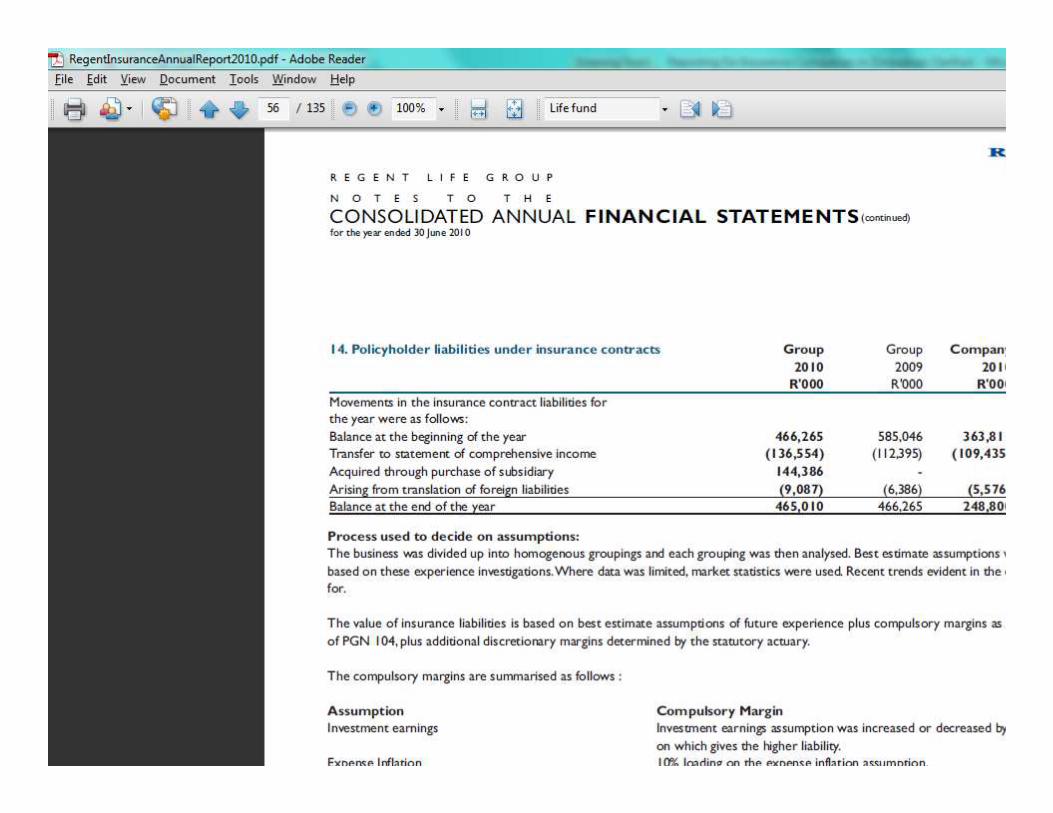

Accounting for the change in insurance liabilities.

29

Investments Actuarial Liabilities

Initial recognition Dr Investment (SoFP)

Cr Bank

Dr Change in actuarial liabilities (P/L)

Cr Actuarial liabilities (SoFP)

For insurance liabilities on 1 January

2009 from Zim Dollar era- Dr NDR

Transactions (dividends, interest,

claims, e.t.c)

Dr Bank

Cr Dividends income (P/L)

Cr Interest Income (P/L)

Dr Claims expense (P/L)

Dr Business Admin costs (P/L)

Cr Bank

Cr Outstanding claims (SoFP)

Subsequent recognition Dr Investment

Cr FV adjustment (P/L)

Cr FV adjustment (OCI)

Dr Change in actuarial liabilities (P/L)

Cr Actuarial liabilities (SoFP)

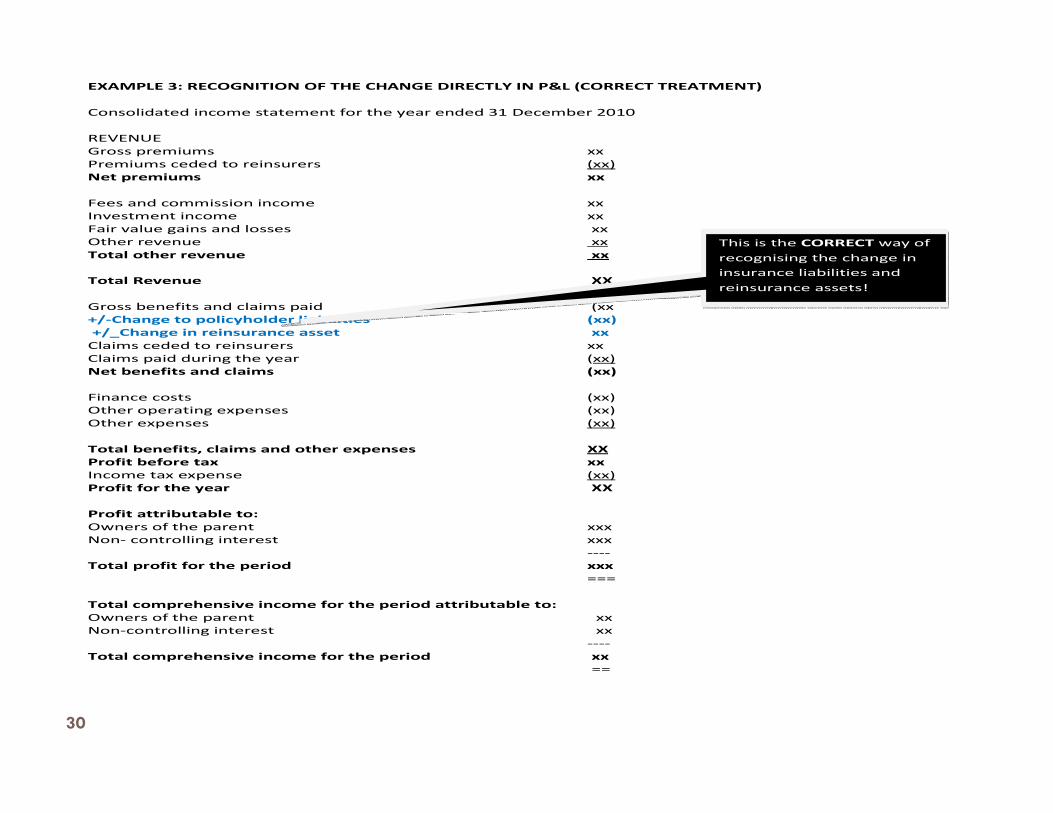

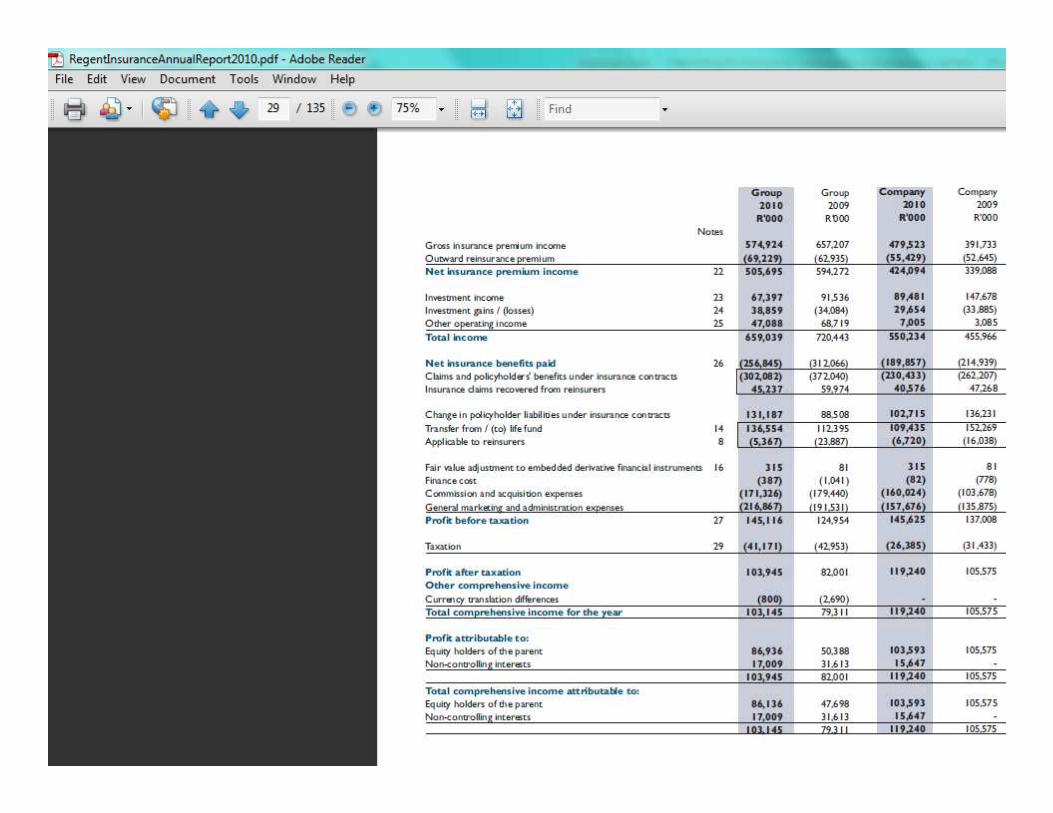

EXAMPLE 3: RECOGNITION OF THE CHANGE DIRECTLY IN P&L (CORRECT TREATMENT)

Consolidated income statement for the year ended 31 December 2010

REVENUE

Gross premiums xx

Premiums ceded to reinsurers (xx)

Net premiums xx

Fees and commission income xx

Investment income xx

Fair value gains and losses xx

Other revenue xx

Total other revenue xx

Total Revenue XX

Gross benefits and claims paid (xx

+/-Change to policyholder liabilities (xx)

+/_Change in reinsurance asset xx

Claims ceded to reinsurers xx

Claims paid during the year (xx)

Net benefits and claims (xx)

Finance costs (xx)

Other operating expenses (xx)

This is the CORRECT way of

recognising the change in

insurance liabilities and

reinsurance assets!

30

Other operating expenses (xx)

Other expenses (xx)

Total benefits, claims and other expenses XX

Profit before tax xx

Income tax expense (xx)

Profit for the year XX

Profit attributable to:

Owners of the parent xxx

Non- controlling interest xxx

----

Total profit for the period xxx

===

Total comprehensive income for the period attributable to:

Owners of the parent xx

Non-controlling interest xx

----

Total comprehensive income for the period xx

==

Anesu Daka CA(SA) Chartered Accountants Academy31

Anesu Daka CA(SA) Chartered Accountants Academy32

33

Research Finding34

Reserving � Reserving

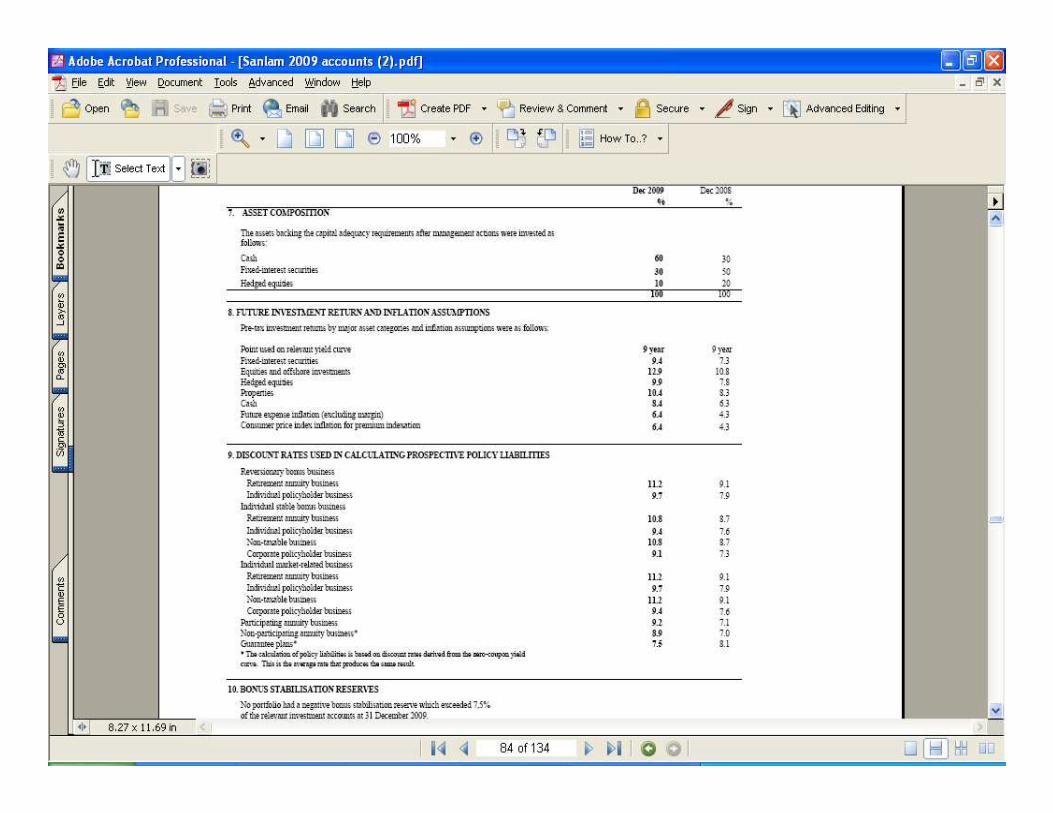

Research Findings

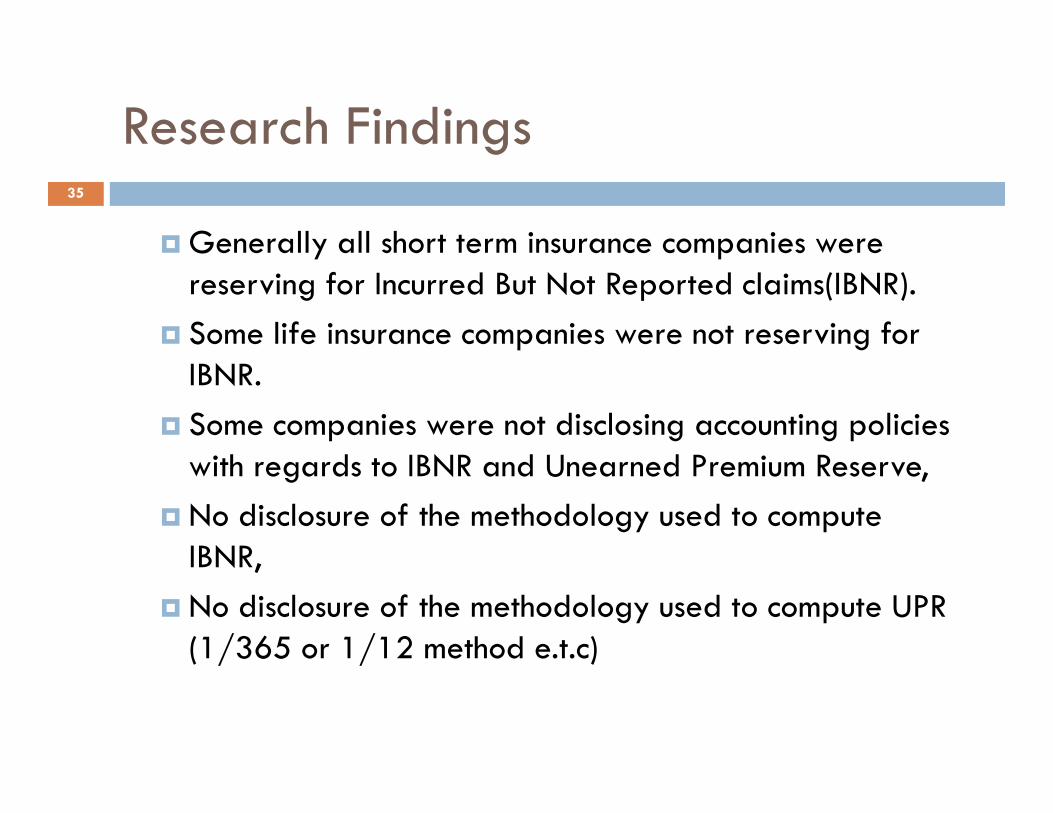

� Generally all short term insurance companies were reserving for Incurred But Not Reported claims(IBNR).

� Some life insurance companies were not reserving for IBNR.

Some companies were not disclosing accounting policies

35

� Some companies were not disclosing accounting policies with regards to IBNR and Unearned Premium Reserve,

� No disclosure of the methodology used to compute IBNR,

� No disclosure of the methodology used to compute UPR (1/365 or 1/12 method e.t.c)

Research Findings

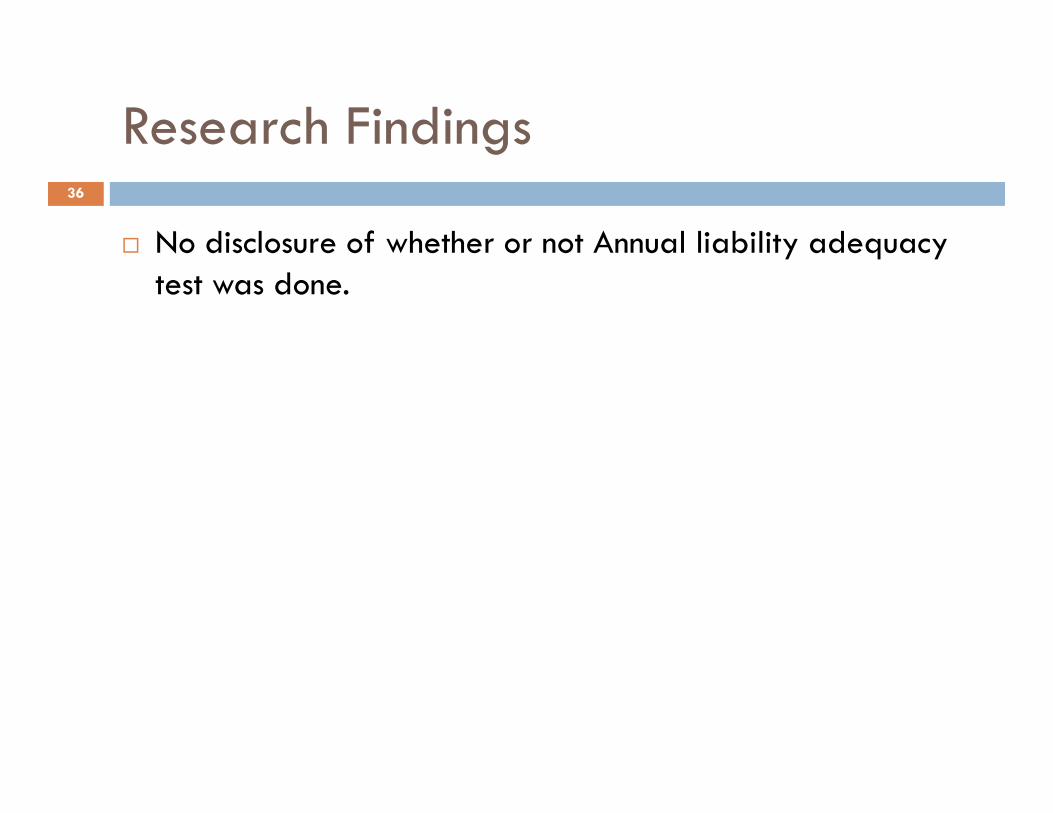

� No disclosure of whether or not Annual liability adequacy test was done.

36

Recommendation and Technical justification

Reserving

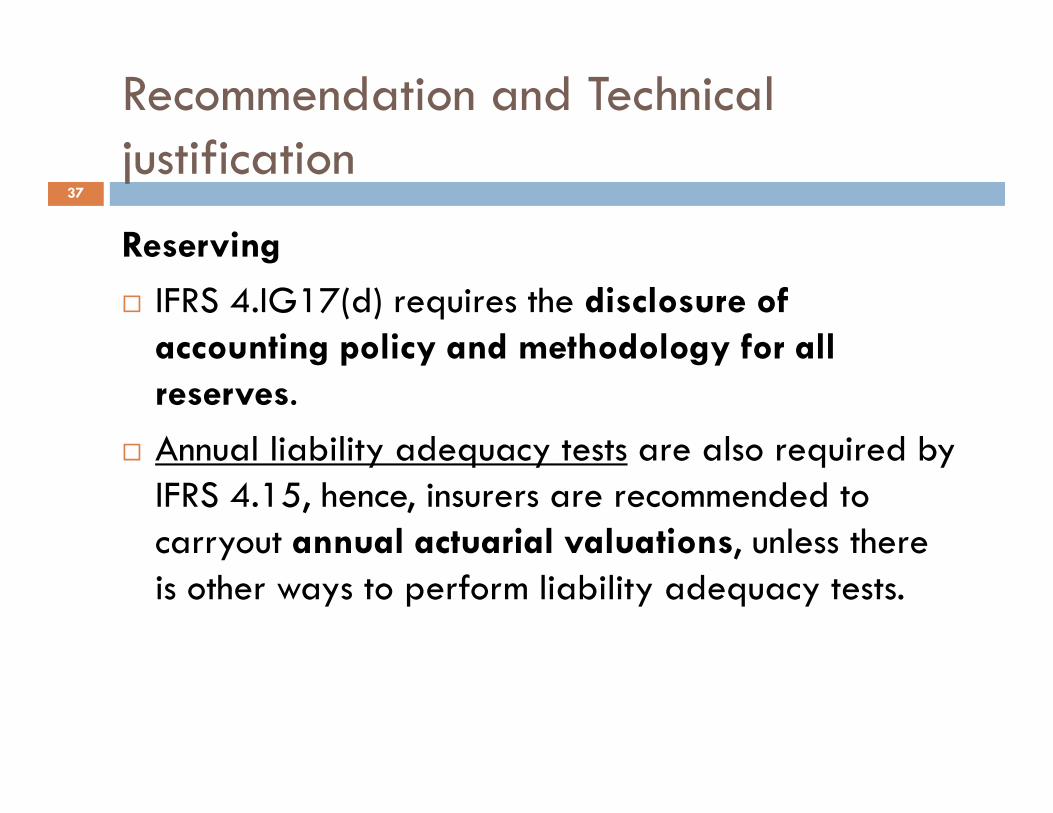

� IFRS 4.IG17(d) requires the disclosure of

accounting policy and methodology for all

reserves.

37

reserves.

� Annual liability adequacy tests are also required by IFRS 4.15, hence, insurers are recommended to carryout annual actuarial valuations, unless there is other ways to perform liability adequacy tests.

Research Finding38

Premium � Premium Accounting

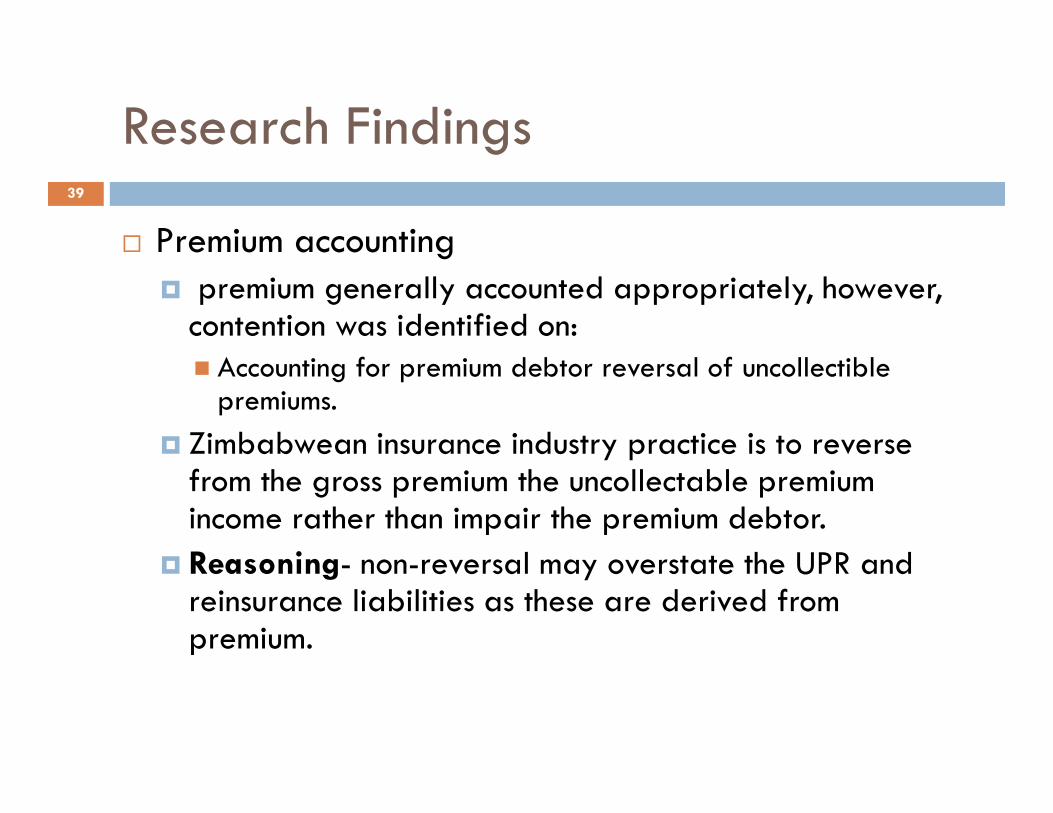

Research Findings

� Premium accounting� premium generally accounted appropriately, however,

contention was identified on:� Accounting for premium debtor reversal of uncollectible

premiums.

39

premiums.

� Zimbabwean insurance industry practice is to reverse from the gross premium the uncollectable premium income rather than impair the premium debtor.

� Reasoning- non-reversal may overstate the UPR and reinsurance liabilities as these are derived from premium.

Recommendation

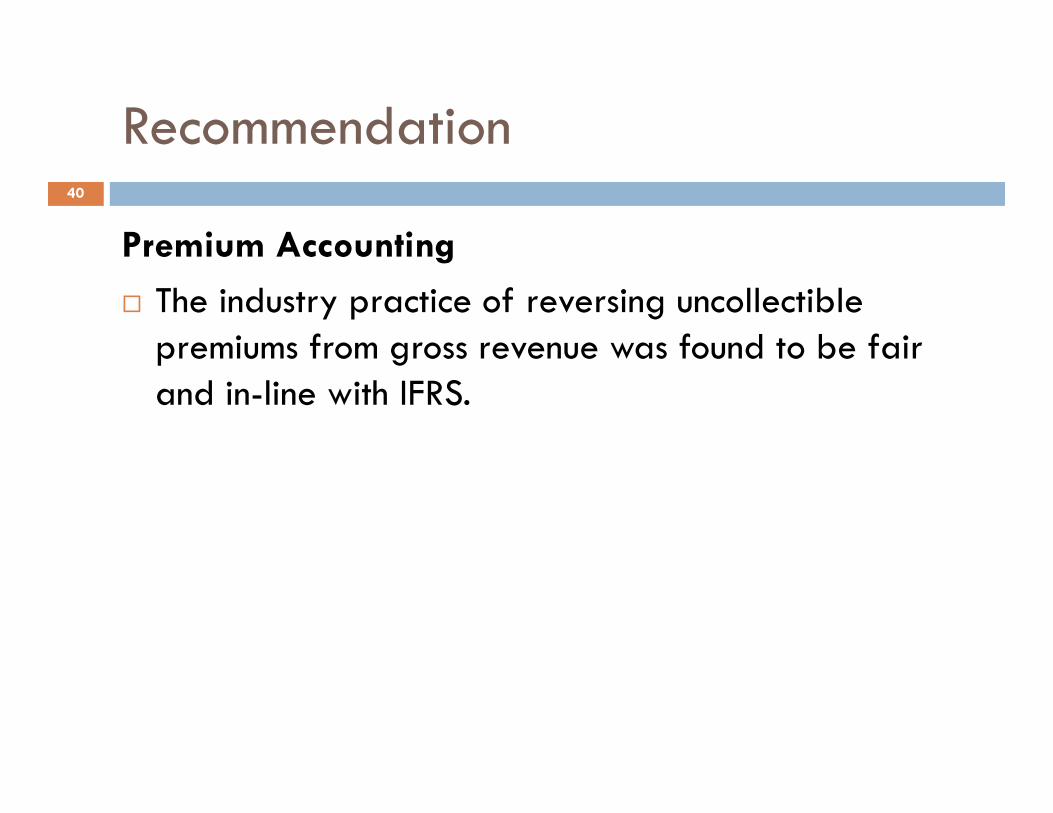

Premium Accounting

� The industry practice of reversing uncollectible premiums from gross revenue was found to be fair and in-line with IFRS.

40

and in-line with IFRS.

Technical justification

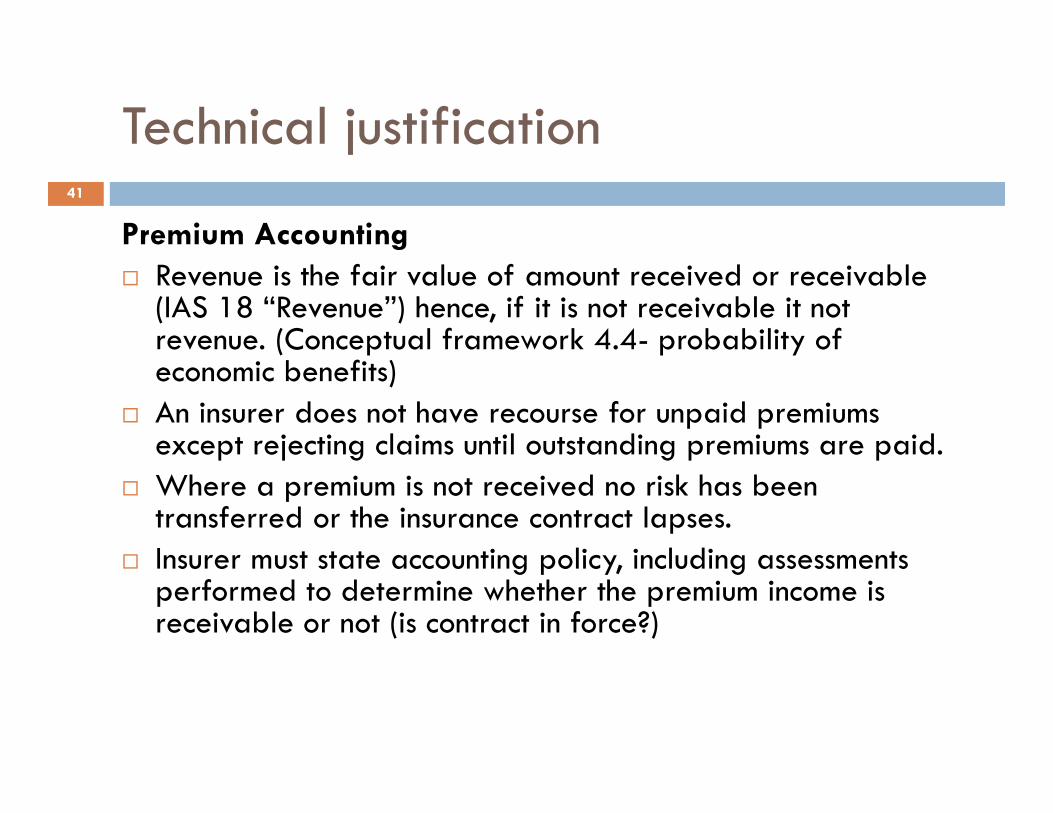

Premium Accounting

� Revenue is the fair value of amount received or receivable (IAS 18 “Revenue”) hence, if it is not receivable it not revenue. (Conceptual framework 4.4- probability of economic benefits)

� An insurer does not have recourse for unpaid premiums

41

� An insurer does not have recourse for unpaid premiums except rejecting claims until outstanding premiums are paid.

� Where a premium is not received no risk has been transferred or the insurance contract lapses.

� Insurer must state accounting policy, including assessments performed to determine whether the premium income is receivable or not (is contract in force?)

Research Finding42

Presentation and Disclosure

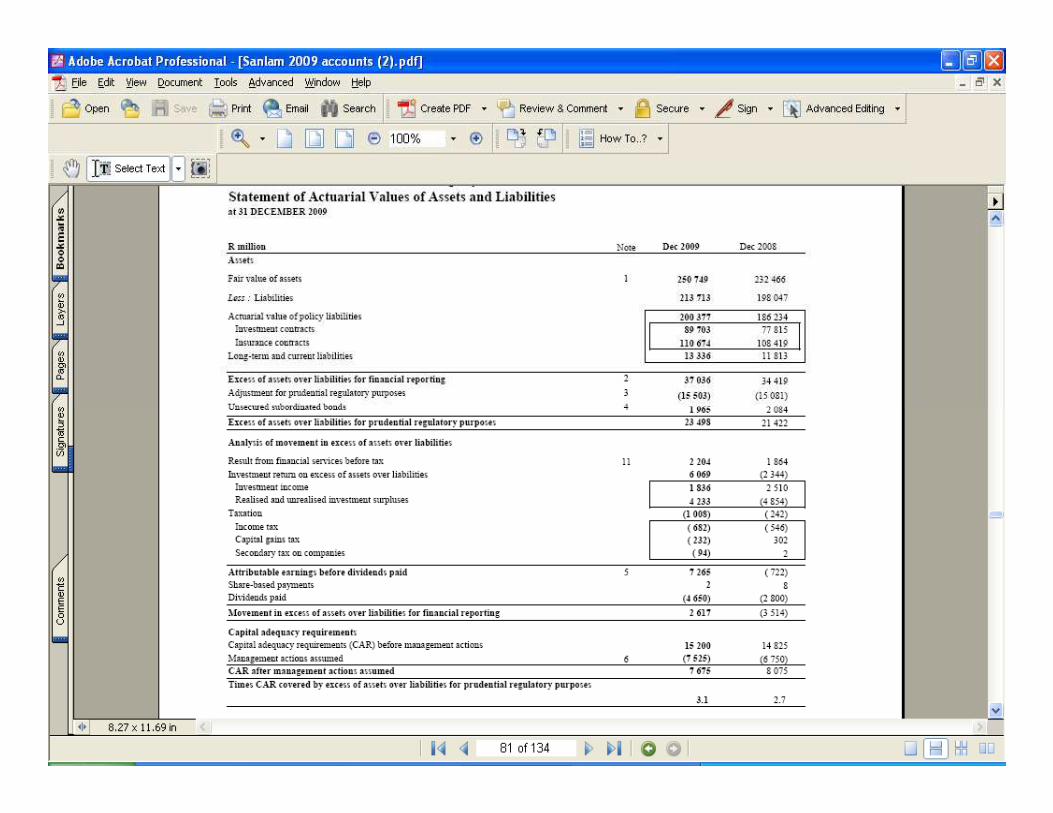

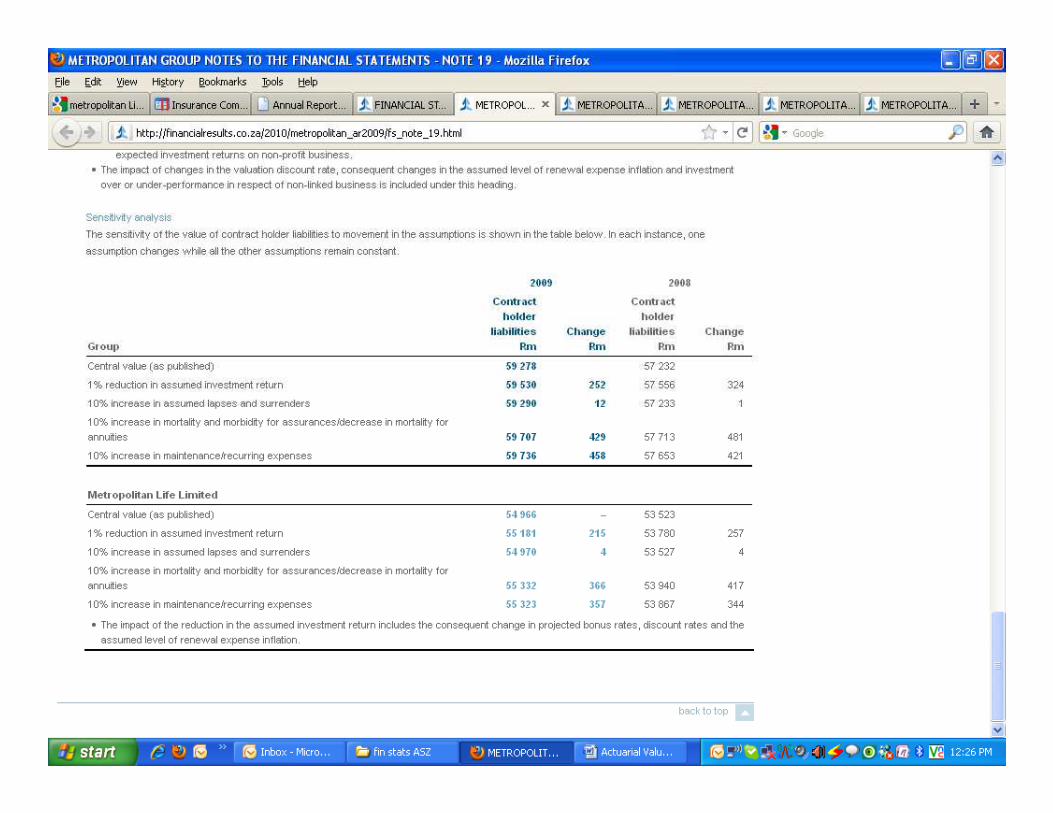

� Presentation and Disclosure

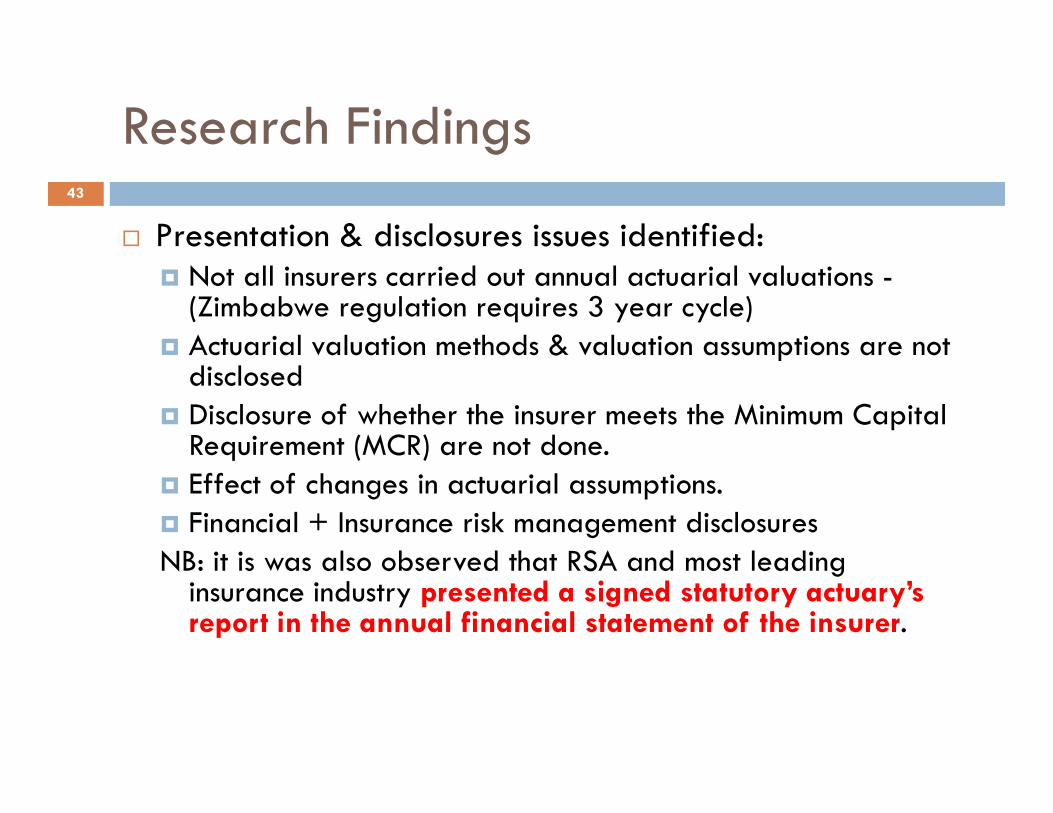

Research Findings

� Presentation & disclosures issues identified:� Not all insurers carried out annual actuarial valuations -

(Zimbabwe regulation requires 3 year cycle)� Actuarial valuation methods & valuation assumptions are not

disclosed� Disclosure of whether the insurer meets the Minimum Capital

43

� Disclosure of whether the insurer meets the Minimum Capital Requirement (MCR) are not done.

� Effect of changes in actuarial assumptions.� Financial + Insurance risk management disclosuresNB: it is was also observed that RSA and most leading

insurance industry presented a signed statutory actuary’s report in the annual financial statement of the insurer.

Recommendation

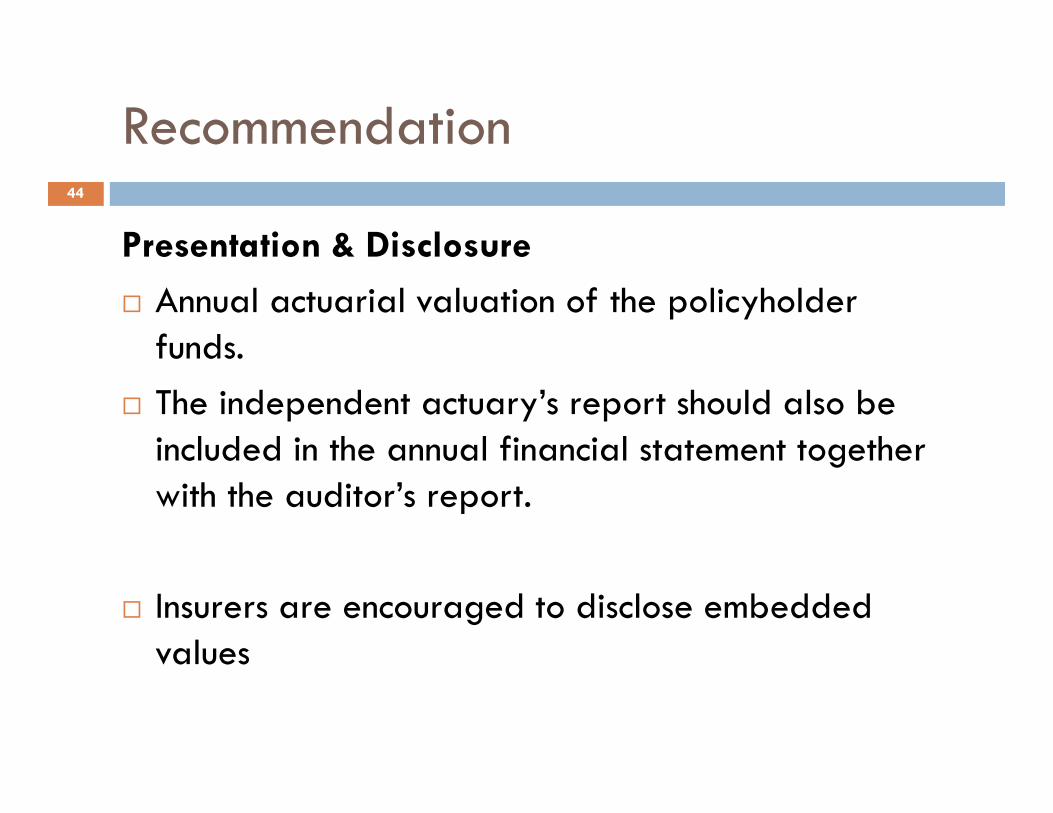

Presentation & Disclosure

� Annual actuarial valuation of the policyholder funds.

� The independent actuary’s report should also be

44

� The independent actuary’s report should also be included in the annual financial statement together with the auditor’s report.

� Insurers are encouraged to disclose embedded values

Technical justification

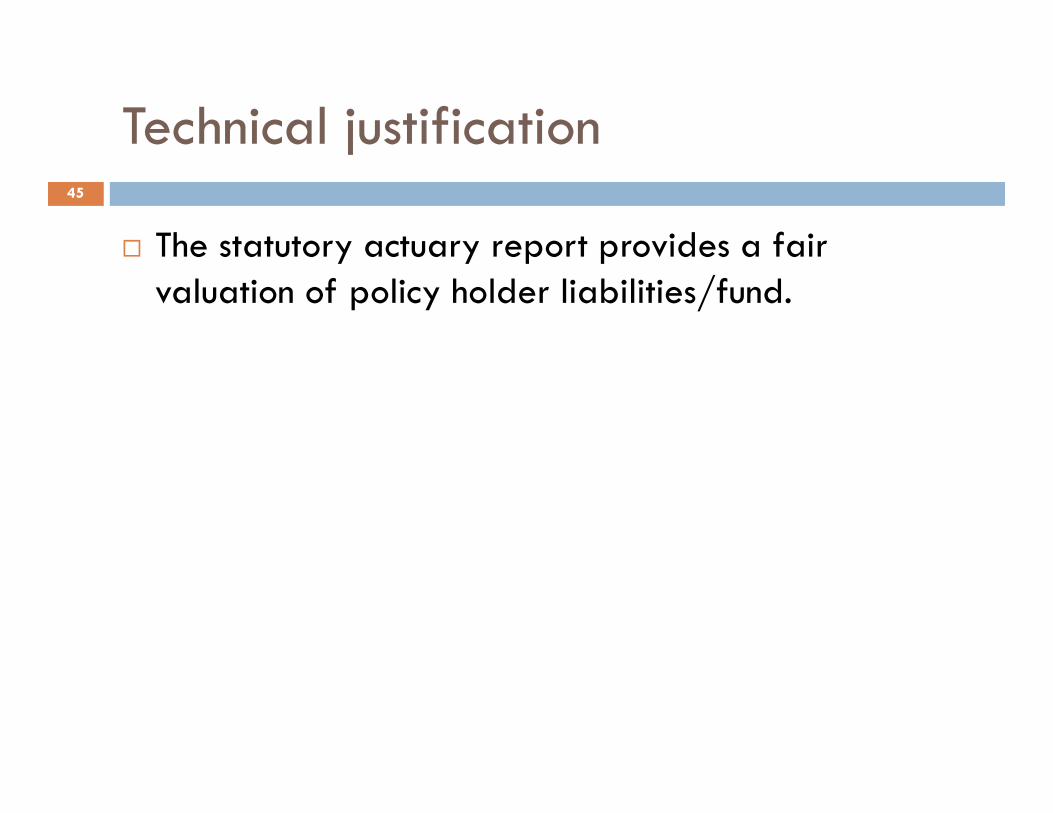

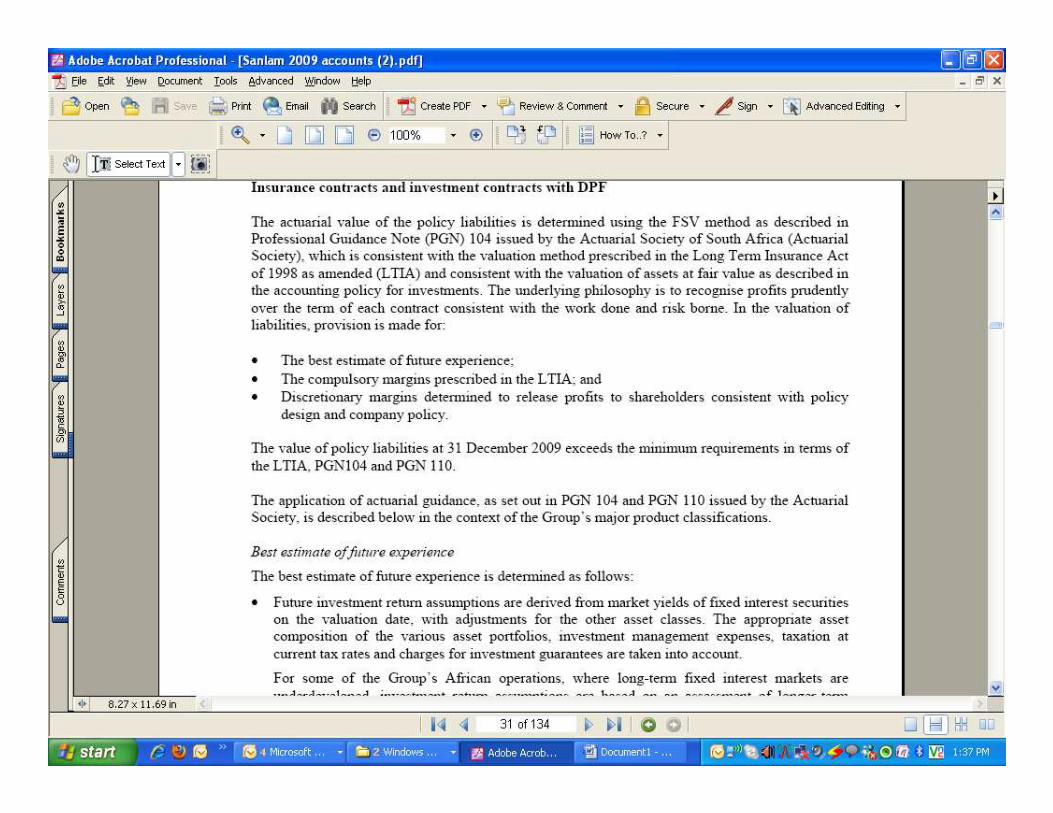

� The statutory actuary report provides a fair valuation of policy holder liabilities/fund.

45

Anesu Daka CA(SA) Chartered Accountants Academy46

Anesu Daka CA(SA) Chartered Accountants Academy47

Anesu Daka CA(SA) Chartered Accountants Academy48

Insurer’s Investments Vs Liabilities49

Anesu Daka CA(SA) Chartered Accountants Academy50

Anesu Daka CA(SA) Chartered Accountants Academy51

Anesu Daka CA(SA) Chartered Accountants Academy52

53

Presenters:

Anesu Daka CA(SA)

Chartered Accountants Academy Director

[email protected] /cell: 0775344635

54

Bothwell Nyajeka CA (Z)

TA Holdings Chief Finance Officer

[email protected] /cell : 0772 422 784