Report on Risk Management and Capital Adequacy of Bank ... · and Capital Adequacy of Bank...

47

Report on Risk Management and Capital Adequacy of Bank Gospodarstwa Krajowego as at 31 December 2016 (Pillar III)

Transcript of Report on Risk Management and Capital Adequacy of Bank ... · and Capital Adequacy of Bank...

Report on Risk Management

and Capital Adequacy

of Bank Gospodarstwa Krajowego

as at 31 December 2016 (Pillar III)

Page 2 of 47

Table of contents

1. Introduction .............................................................................................................................................................. 3

2. General Information ................................................................................................................................................. 3

2.1. General information about the Bank .............................................................................................................. 3

2.2. Presentation of reporting data ....................................................................................................................... 3

2.3. Risk statement ................................................................................................................................................ 4

3. Risk management principles at the Bank .................................................................................................................. 5

3.1. General risk management principles .............................................................................................................. 5

3.2. Risk management organisational structure .................................................................................................... 7

3.3. Rules for the election of the Bank’s Management Board members ............................................................ 10

3.4. Number of functions in the bodies of other entities, held by members of the Management Board and the

Supervisory Board of the Bank ..................................................................................................................... 11

3.5. Credit, exposure concentration, and counterparty credit risk ..................................................................... 11

3.5.1. Credit and exposure concentration risk .......................................................................................... 11

3.5.2. Counterparty Credit Risk .................................................................................................................. 13

3.5.3. Credit risk mitigation techniques ..................................................................................................... 15

3.5.4. Reduction of a customer’s credit rating .......................................................................................... 16

3.5.5. Tabulated data of credit risk and counterparty credit risk .............................................................. 16

3.6. Liquidity risk .................................................................................................................................................. 23

3.7. Market risk .................................................................................................................................................... 25

3.7.1 Characteristics of interest rate risk in the banking book ................................................................. 26

3.7.2 Financial result sensitivity to changes in interest rates ................................................................... 27

3.7.3 Valuation sensitivity to changes in interest rates ............................................................................ 28

3.8. Operational risk ............................................................................................................................................ 28

3.9. Model Risk .................................................................................................................................................... 30

3.10. Compliance Risk ............................................................................................................................................ 30

3.11. Other risks ..................................................................................................................................................... 30

3.12. Risk reporting ................................................................................................................................................ 30

3.13. Equity exposures not taken into account in the trading book ..................................................................... 32

4. Own funds ............................................................................................................................................................... 33

5. Capital adequacy ..................................................................................................................................................... 35

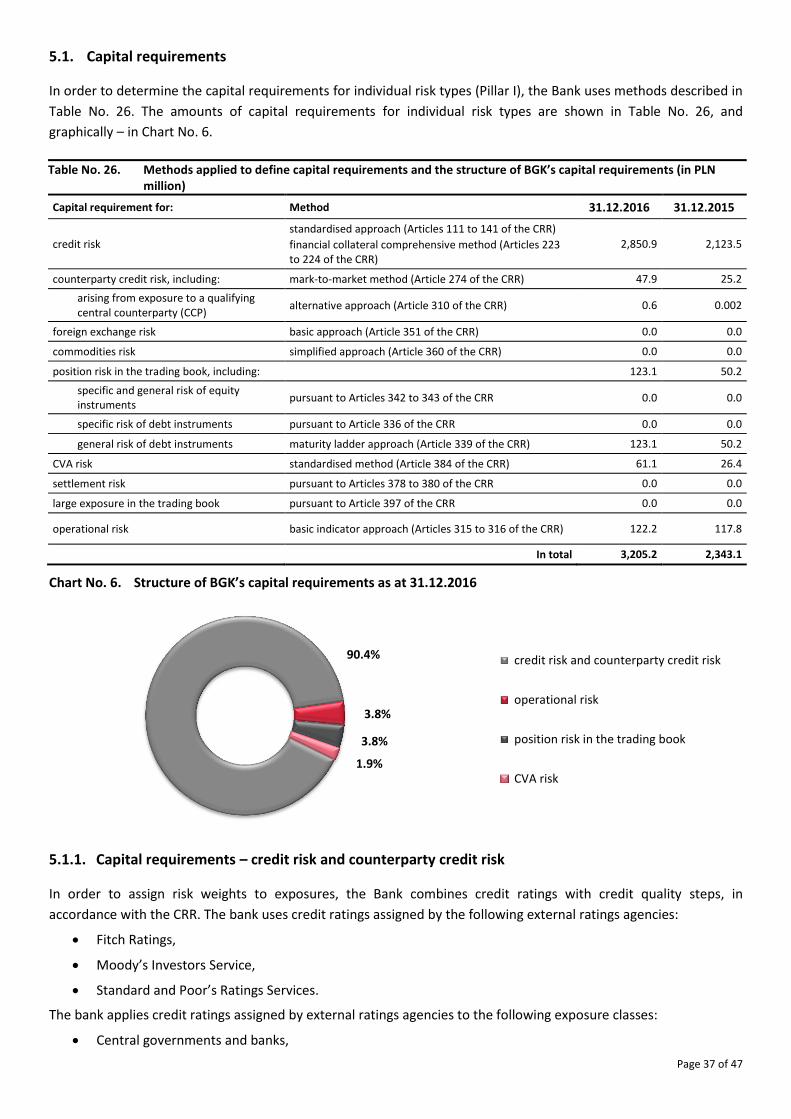

5.1. Capital requirements .................................................................................................................................... 37

5.1.1. Capital requirements – credit risk and counterparty credit risk ..................................................... 37

5.2. Internal capital .............................................................................................................................................. 39

5.3. Capital buffers............................................................................................................................................... 40

6. Financial leverage ................................................................................................................................................... 40

7. Encumbered and unencumbered assets ................................................................................................................ 42

8. Information on the variable remuneration policy towards persons holding managerial positions ....................... 43

Glossary .......................................................................................................................................................................... 46

Statement of the Management Board of Bank Gospodarstwa Krajowego .................................................................... 47

Page 3 of 47

1. Introduction

This document constitutes the implementation, by Bank Gospodarstwa Krajowego, of the provisions specified in

Part Eight of the CRR in relation to disclosing information about risk management and capital adequacy.

This report has been drafted in accordance with “Principles of Information Policy of Bank Gospodarstwa Krajowego

in the scope of publication of qualitative and quantitative information on capital adequacy”1, approved by the

Management Board and the Supervisory Board of the Bank.

Information not covered by the certified auditor’s review of the financial statements and the report on the activities

of the Bank are verified by relevant organisational units of the Bank’s head office.

Before publication, this reports shall be subject to approval by the Bank’s Management Board.

2. General Information

2.1. General information about the Bank

As a highly reliable state financial institution, Bank Gospodarstwa Krajowego specialises in services for the public

sector. The Bank ensures economically efficient and operationally effective support of the economic policy of the

Council of Ministers, government’s social and economic programmes, as well as local governance and regional

development programmes.

The volume of support from the State Treasury is determined by the provisions of the Act on BGK that obligate the

Minister responsible for public finance to provide BGK with means to maintain own funds at a level guaranteeing the

fulfilment of the Bank’s tasks and liquidity.

Moreover, Fitch Ratings has confirmed the high reliability of Bank Gospodarstwa Krajowego by assigning it a credit

rating of “A-”, a level equal to Poland’s rating – the rating was confirmed in a Fitch Ratings’ communication of 21

February 2017.

2.2. Presentation of reporting data

Pursuant to the Act on BGK, the tasks of the Bank – in addition to the activities defined in the Banking Law Act –

includes, inter alia, the administration of funds created, entrusted, or provided to BGK on the basis of separate acts,

constituting so-called “commissioned activities”.

As part of commissioned activities carried out by the Bank through separated funds, one should distinguish:

funds associated with granting credits, loans, or off-balance sheet commitments at the Bank’s risk – “fund

exposed to credit risk”,

funds associated with managing cash flows for specific budgetary targets – “flow funds”.

The financial statements of the Bank include own activities of the Bank and commissioned activities carried out as

part of funds exposed to credit risk. Balance sheets, summaries of off-balance sheet items, and profit and loss

accounts of individual funds associated with commissioned activities (both funds exposed to credit risk as well as

flow funds), are presented in an appendix to the financial statements.

In order to limit the regulatory risk measures and to draw up obligatory reporting resulting from CRR provisions, the

Bank takes into account both Bank’s own activities and commissioned activities carried out as part of funds exposed

to credit risk as well as flow funds. In view of the above, the data presented in this document include both the own

activities and the commissioned activities of the Bank.

1 document available on the Bank’s website: www.bgk.pl

Page 4 of 47

As at 31 December 2016, Bank Gospodarstwa Krajowego was neither subject to consolidation for accounting

purposes nor to prudential consolidation pursuant to CRR provisions.

2.3. Risk statement

In Table no. 1, key risk-related ratios and figures are presented, and in Charts No. 1 and 2, the structure of the

Bank’s balance sheet. Together, they reflect the risk profile of the Bank.

Table No. 1. Key ratios and figures2

Regulatory limit As at 31.12.2016 As at

31.12.2015

Bank’s balance sheet figures

Total assets presented in the financial statements in PLN million 67,258.2 43,419.1

Total assets with flow funds included in PLN million 121,063.2 90,057.1

Net result in PLN million 349.2 362.7

Capital adequacy

Own funds in PLN million 12,257.5 9,445.8

Capital requirements in PLN million 3,205.2 2,343.1

Internal capital in PLN million 3,811.8 3,008.3

CET1 ratio 4.5% 30.11% 31.35%

Capital adequacy ratio (total capital ratio) 8% 30.59% 32.25%

Internal capital ratio 100% 31.10% 31.85%

Risk of excessive leverage

Leverage ratio 9.13% 9.26%

Credit risk and counterparty credit risk

Exposure taken into account in the standardised approach of determining the capital requirement for credit risk and counterparty credit risk in PLN million

146,954.3 113,909.6

Capital requirement for credit risk and counterparty credit risk in PLN million

2,898.8 2,148.8

Specific risk provisions in PLN million 723.2 620.9

Liquidity Risk

M1 in PLN million 0 15,503.8 6,095.0

M4 1.00 1.24 1.18

LCR 70% in 2016, 60% in 2015

252% 212%

Market risk

VaR(1D) for Bank’s currency position in PLN million 1.6 1.8

BPV for trading book in PLN million 0.01 0.01

Capital requirement for market risk in PLN million 123.1 50.2

Interest rate risk in the banking book

Change in interest result given a change in interest rates by -2 p.p. in the scope of banking book in PLN million

-110.3 -202.5

Change in interest result given a change in interest rates by +2 p.p. in the scope of banking book in PLN million

99.5 67.9

Operational Risk

Net loss on operational risk events in PLN million 0.3 5.1

Capital requirement for operational risk in PLN million 122.2 117.8

2 Risk ratios data and comparable data are presented jointly for the Bank’s own activities and commissioned activities

Page 5 of 47

Chart No. 1. Bank’s balance sheet structure in the financial statements

Chart No. 2. Bank’s balance sheet structure with flow funds included

3. Risk management principles at the Bank

3.1. General risk management principles

The internal objective of risk management at the Bank is to maintain high quality of assets within an acceptable risk

level.

The main risk management guidelines at BGK are defined in the Bank’s Strategy and policies for managing particular

types of risks. The risk appetite is determined by the acceptable level of Tier 1 ratio, capital adequacy ratio, and

internal capital ratio, as well as the acceptable level of individual risk types. In the allocation process, the required

capital is distributed among individual risk types, with limit levels defined for individual risks at BGK.

Diagram no. 1 presents a general scheme of areas covered by limits.

3 Other assets of the Bank with flow funds include also receivables of the National Road Fund

37.6 3.0

1.1

5.8

26.6

5.8

3.9

12.1

31.0

2.9

4.6

0 20 40 60 80 100 120 140

Liabilities

Assets

in PLN billion

37.6 30.5

1.1

28.8

26.6

5.8

3.9

12.1

35.0

6.3

54.4

0 20 40 60 80 100 120 140

Liabilities

Assets

in PLN billion

A1 – Interbank deposits L1 – Clients’ deposits

A2 – Net loans L2 – Loans incurred

A3 – Reverse repo and buy-sell-back transactions L3 – Liabilities under securities issuance

A4 – Debt securities L4 – Repo and sell-buy-back transactions

A5 – Other assets3

L5 – Total capital (excluding current year’s result and retained

profit/accumulated loss)

L6 – Other liabilities

A1 A2 A3 A4 A5

L6 L5 L4 L3 L2 L1

A5 A4 A3 A2 A1

L6 L5 L4 L3 L2 L1

Page 6 of 47

Diagram No. 1. Areas covered by limits

The Bank’s risk management is based on:

BGK Capital Management Policy and BGK Internal Capital Adequacy Assessment Process Principles approved

by the Supervisory Board,

risk management policies, principles, and procedures related to risk identification, measurement/assessment,

monitoring, reporting, and control, developed in written form and approved by the Supervisory Board or the

Management Board of the Bank,

corporate governance principles and variable remuneration policy towards persons holding managerial

positions at BGK, approved by the Supervisory Board or the Management Board of the Bank.

Internal regulations are subject to regular reviewing to adjust them to changes in the Bank’s risk profile, the Bank’s

economic environment, and prudent banking practices.

The risk management system is designed to ensure a uniform and efficient process of identification,

measurement/assessment, monitoring, reporting, and controlling of risks, and to take safety measures.

The risk identification process includes determination of risk types, their sources (risk factors), significance and

relationships between individual types of risk.

The risk measurement/assessment process includes methods of risk quantification, determination of the acceptable

risk level, identification of relationships, patterns, and trends, as well as estimation of the costs of the risk borne,

and stress tests.

The risk monitoring and control process includes supervision of the level of risk taken, reviews of relevance and

accuracy of the methods of risk assessment applied, and evaluation of efficiency of the tools used.

The risk reporting process includes information on the risk profile, identification of possible threats, and information

on the measures adopted.

The safety measures include regulations (policies, principles, instructions, procedures, by-laws, and contingency

plans), internal limits, planning ratios levels and deviations from the plan, recommendations for organisational units

of the Bank’s head office and branches, as well as insurance and risk transfer.

The Bank supervises the risk associated with the activities of its subsidiaries, including, in particular, in the area of

liquidity, capital, operational, and compliance risk.

RISK APPETITE

Capital adequacy

Credit and concentration

risk

Liquidity risk

Interest rate risk

Foreign exchange risk

Operational risk

Page 7 of 47

The organisation of risk management at the Bank is shown in Diagram No. 2.

Diagram No. 2. Organisation of selected types of risk at the Bank

3.2. Risk management organisational structure

The composition, scope of activity, and competences of the Bank’s bodies and the corporate object of the Bank are

defined in the Act on BGK, the Bank’s Articles of Association, and the rules of procedure of the said bodies.

Below, the Bank’s bodies, Committees of the Supervisory Board, committees appointed by the Bank’s Management

Board are presented, as well as leading organisational units of the Bank’s head office that participate in the risk

management process at the Bank.

Supervisory Board of the Bank

The Supervisory Board supervises the compliance of the Bank’s policy on risk-taking with the long-term

development plan – strategy and financial plan of the Bank.

Risk Committee

The Risk Committee supports operations of the Bank’s Supervisory Board, overseeing the management system for

all risks identified in the Bank’s operations, in particular by providing opinions as to the Bank’s overall ongoing and

future risk appetite. The Risk Committee includes persons appointed from among the members of the Bank’s

Supervisory Board. In 2016, 6 meetings of the Risk Committee were held.

Risk management supervision

Risk appetite Tactical

management Strategic

management Risk monitoring

Credit risk Management

Board

CC

CC CRD

CRMD DLD

Supervisory Board Supervisory Board

Management

Board

Market risk Management

Board

ALCO

TD

FMSD FRD Supervisory Board

Supervisory Board

Management

Board

Liquidity risk Management

Board

ALCO

TD FRD Supervisory Board Supervisory Board

Management

Board

Operational risk Management

Board

ORC

Each organisational unit

FRD Supervisory Board Supervisory Board

Management

Board

Compliance Risk Management

Board

ORC

Each organisational unit

Compliance unit Supervisory Board Supervisory Board

Management

Board

Capital adequacy Management

Board

ALCO

Each business unit FRD Supervisory Board Supervisory Board

Management

Board

Page 8 of 47

Audit Committee

The Audit Committee supports the Bank’s Supervisory Board, in particular through oversight of the internal audit

area and monitoring the financial and management reporting process, as well as financial audit activities carried out

at the Bank. The Audit Committee includes persons appointed from among the members of the Bank’s Supervisory

Board.

Management Board of the Bank

The Management Board of the Bank is responsible for organising and administering the risk management process

and ensuring the efficiency of the risk management system. One of the Management Board members, who has

obtained consent of the Polish Financial Supervision Authority to be appointed as a Management Board member,

supervises the banking risk area that covers organisational units managing credit, financial, operational, and other

risks.

Asset and Liability Committee

The Committee offers opinions and participates in the decision-making process. The primary objective of the

Committee is to define the current, mid-, and long-term management policy for the Bank’s assets and liabilities. The

aim of the policy is to optimise results and allocate the Bank’s capital efficiently. It takes into account the relevant

level of exposure to risk and the nature of public tasks commissioned to the Bank. These include tasks fulfilled by the

Bank as part of the management of funds created, entrusted, or transferred to the Bank under separate regulations

or other legal acts.

Operational Risk Committee

The main objective of the Committee is to ensure efficient management of the operational and compliance risks.

The Committee offers opinions and participates in the decision-making process. It is responsible for reducing the

operational and compliance risks, in particular through: initiation and coordination of activities aimed to identify,

measure, and monitor the operational and compliance risks; providing opinions on the level of limits reducing the

operational risk; and assessment of the risk mitigation techniques applied for such risks. The Committee coordinates

the activities aimed to identify, measure, and monitor the reputation risk and the related reporting.

Credit Committee

The primary tasks of the Committee include: appraisal of loan applications and applications for restructuring or

enforcement. It also provides recommendations to the Bank’s Management Board on matters reserved for the

competence of the Board, performing reviews of the credit portfolio, annual reviews of industry sectors and

deciding on their classification to relevant investment risk categories.

Change Committee

The Committee offers opinions and participates in the decision-making process. The basic tasks of the Committee

include managing the portfolio of undertakings within the authorisation limits granted to the Committee and

accepting, in connection with the objectives provided for in the Bank’s Strategy, basic rules for banking products and

services, processes, applications, and IT infrastructure.

Page 9 of 47

Financial Risk Department

The Financial Risk Department is responsible for creation and development of an efficient management system for

the financial risk (liquidity, market, financial leverage risk, and capital adequacy) and non-financial risks (operational

and model risk), creating and improving system solutions limiting the risk of country of operation and the risk of

cooperation with domestic and foreign banks and insurance companies, supervising transactions on financial

markets, measuring capital requirements for market risk, CVA risk, and operational risk, estimating the internal

capital and coordinating the ICAAP process.

Credit Risk Department

The Credit Risk Department is responsible for the individual credit risk management and the classification of:

clients or groups of entities associated with a client which is not a financial institution and is not included in

the portfolio managed by the Distressed Loans Department,

credit transactions

and verifying the value of collaterals accepted by the Bank for individual credit transactions, exclusive of collaterals

provided to financial institutions as part of the exposure limits for banks set by the Bank.

Credit Risk Management Department

The Credit Risk Management Department is in charge of designing the directions and principles of the Bank’s credit

policy, credit risk management for the credit exposure portfolio of the Bank, developing principles of credit risk

assessment and methods of credit risk mitigation, preparation of data concerning assets bearing credit risk,

calculation of the capital requirement for credit risk and counterparty credit risk, coordination of the process of

creating and releasing specific risk provisions, developing analyses of the Bank’s credit exposure portfolio, as well as

optimisation of credit processes.

Distressed Loans Department

The Distressed Loans Department is responsible for recovery of receivables requiring a restructuring or debt

collection procedure as well as for correct classification of credit receivables.

Internal Audit Department

The Internal Audit Department reports directly to the President of the Management Board and is responsible for the

independent assessment of the internal control system and risk management processes at the Bank and its

subsidiaries, including the relevance and effectiveness of the existing control mechanisms. It is also responsible for

consulting in the form of recommendations on improvements in the control mechanisms, or implementation of new

solutions increasing the efficiency of the internal control system.

Compliance Unit

The Compliance Unit is responsible for development and coordination of the compliance and reputation risk

management process, compliance tests in key compliance risk areas, and qualified support in matters of compliance

risk. The Compliance Unit’s operations are supervised and managed by the Compliance Officer reporting directly to

the President of the Management Board.

Below, the general outline of the Bank’s organisational structure is presented with distribution of tasks carried out in

the Bank, which ensures independence of the functions of risk measurement, monitoring, and control of the

operating activities from which the risk taken by the Bank ensues.

Page 10 of 47

Diagram No. 3. General outline of the Bank’s organisational structure as at 31 December 2016

3.3. Rules for the election of the Bank’s Management Board members

The composition and term of office of the Management Board as well as the rules for appointing, reasons for

mandate expiry, and rules for suspending of Management Board members are specified in Articles 10 and 11 of the

Act on BGK.

The Management Board is comprised of 6 members, including President, First Vice-President, and Vice-President.

The Prime Minister appoints and dismisses:

President of the Management Board – upon request of the minister responsible for the economy,

First Vice-President of the Management Board – upon request of the minister responsible for financial

institutions,

Vice-President of the Management Board – upon request of the minister responsible for transport,

one Management Board member each – upon request of, respectively, minister competent for regional

development, minister competent for the economy, and minister competent for public finance.

Appointment of the President and one member of the Management Board is subject to consent of the Polish

Financial Supervision Authority. The provisions of Articles 22a.2 and 22b of the Banking Law Act shall be applied

accordingly.

For serious reasons, the Supervisory Board may suspend individual or all members of the Management Board for a

period not longer than 3 months.

For a period not longer than 3 months, the Supervisory Board may delegate Supervisory Board members to perform

duties of Management Board members:

who have been dismissed, tendered resignation, or are unable to perform their duties for other reasons,

Supervisory Board

Member of the

Management Board

Areas: sales, banking

product management,

investment project

financing

Member of the

Management Board

Areas: banking

operations, IT, EU funds,

security

President of the

Management Board

General management

area

Compliance Officer

Internal Audit Department

ChC

Vice-President of the

Management Board

Areas: commissioned

activities, social housing,

logistics and

administration

First Vice-President

of the Management

Board

ALCO

Areas: finance, capital

investments, financial markets

Member of the

Management Board

CC, ORC

Risk management

Independent Model

Validation Specialist

Remuneration Committee

Risk Committee

Audit Committee

Page 11 of 47

if, in the Supervisory Board’s opinion, it is a necessary solution for the purposes of prudent and sustainable

management of the Bank.

The mandate of Management Board member shall expire with the expiry of the term of office, death, or dismissing

from the Management Board. If the mandate of a Management Board members expires during the term of office of

the Management Board, another member shall be appointed to serve until the end of the Management Board’s

term of office.

3.4. Number of functions in the bodies of other entities, held by members of the Management Board and the Supervisory Board of the Bank

Table No. 2 presents information about the number of functions held by members of the Bank’s Management Board

and Supervisory Board in the bodies of other entities.

Table No. 2. Number of functions held in bodies of other entities as at 31.12.2016

BGK Supervisory Board

members BGK Management Board members

Number of functions held in supervisory boards of other entities 0 4

Number of functions held in management boards of other entities 4* 0

In total 4 4

* including one function of President in a foundation

3.5. Credit, exposure concentration, and counterparty credit risk

3.5.1. Credit and exposure concentration risk

Credit risk constitutes one of the most important risk types to which the Bank is exposed in its operations and it is

defined as a threat of a borrower’s failure to pay the liability under an agreement, i.e. failure to repay receivables

under credit exposure along with the Bank’s fee within time limits defined in the agreement.

Main credit risk management purposes are as follows:

identification of credit risk areas and risk mitigation to a level accepted by the Bank,

regular review of actions adopted in this risk area,

shaping balance-sheet and off-balance-sheet items of the Bank to minimise the risk of unfavourable

deviation of the financial result from the Bank’s financial plan.

The credit risk management process is carried out at the level of customer risk with individual credit exposure and

credit portfolio risk taken into account, on the basis of:

planned, targeted actions defined in the credit policy,

internal regulations,

available support systems and tools,

recommendations for branches and other units of the Bank.

The Bank formalised its credit risk management approach in the Credit and Concentration Risk Management Policy

of BGK and the procedure Credit Risk Management Principles of BGK. The Principles define the manner of credit risk

assessment and measurement as at the moment of entering into transactions bearing the risk and during the

transactions’ life. The Principles also describe controls for the level of this risk in relation to individual transactions

and the whole credit portfolio, including controls for the level of exposure concentration risk.

The exposure concentration risk is an important credit risk factor. The Bank has introduced relevant internal

principles and procedures applied to exposure concentration with particular emphasis on large exposures to

individual customers and customer groups of the Bank. Portfolio concentration is monitored for individual

Page 12 of 47

borrowers, entities associated by capital or management, industries, etc. Exposure concentration principles concern

various activities of the Bank (not only lending activity, but also investment activity or money market transactions).

In terms of concentration risk, the Bank follows external regulations. Furthermore, pursuant to a resolution by the

Bank’s Management Board, additional exposure limits are in place at the Bank – apart from the statutory

concentration limits – that apply at the credit decision stage.

The Bank applies methodologies of creditworthiness assessment for individual entities taking into account the

nature of their operation and uses defined principles of acceptance and evaluation of legal collaterals.

The Bank monitors timeliness of repayment of liabilities under exposures bearing credit risk and performs regular

reviews of economic and financial standing of the borrowers. It classifies individual exposures and creates relevant

specific risk provisions. It also maintains an adequate level of capital ensuring solvency in case of default on part of

the debtors.

The Bank controls the credit risk exposure level:

in aggregate and for its own activities, as well as activities connected with the administration of funds

established, entrusted, or transferred on the basis of separate acts,

for exposure concentration to one entity and/or entities associated by capital or management, or in

organisational terms, including exposure concentration with account taken of the activities carried out by

the Bank’s subsidiaries,

for large exposures,

in relation to individual economic sectors,

separately under mortgage-backed exposures,

in relation to selected segments and products,

under currency or currency-indexed transactions,

under off-balance sheet liabilities granted by the Bank (guarantees, sureties, and letters of credit).

In May 2009, the Bank withdrew the offer of loan products for individuals. The only loans granted to individuals by

the Bank as part of the implementation of the government programme are loans with interest subsidies for removal

of the consequences of flood disasters, landslides, and hurricanes (pursuant to the Act of 8 July 1999 on the interest

subsidies for bank loans granted for removal of flood disaster consequences (Polish Journal of Laws No. 62, item

690, as amended), among others.

The Management Board of the Bank defines the credit policy taking into account the Bank’s risk appetite and

Strategy as well as the existing level of credit risk borne by the Bank, the structure of credit portfolio, the structure

of legal collaterals, repayments of the transactions bearing credit risk, and external macroeconomic factors. Among

other elements, the credit policy indicates the acceptable level of risk for the credit portfolio, credit purposes and

recommendations, credit profile for individual customer and product segments, risk management process, and the

related prudent practices.

Pursuant to applicable regulations, the Bank performs - at least once a year - stress tests of credit exposure

sensitivity to changes in the exchange rates, interest rate and the value of the existing mortgage collaterals.

The main instrument used to reduce the credit risk is legal collateralisation of the Bank’s receivables. The Bank

applies an internal procedure for the establishment and evaluation of legal collateralisation for receivables as at the

conclusion of the transactions bearing credit risk and for monitoring the collaterals during the transaction’s life.

The basis for calculation of the value of real (in-kind) collaterals is the measurement value verified by the Bank using

the indicators adjusting the value of the collaterals. In the case of unfunded credit protection, the economic and

financial standing of the collateral issuer is examined. Moreover, the fulfilment of formal and legal conditions for

Page 13 of 47

collateral acceptance is verified each time, as well as whether it is funded and liquid, and also its correlation to the

economic and financial standing of the debtor.

In the life period of a transaction bearing credit risk, the legal collateral is periodically monitored. The condition and

value of the collateral are examined along with the possibility of satisfying the Bank’s receivables from the collateral,

and the proportion of the current collateral value to the actual amount of receivables. The frequency of collateral

monitoring depends on the form of collateral, the amount of credit exposure, and risk assessment of the credit

transaction.

For credit risk, BGK uses a system of limits as one of its credit risk management tools. The limits are applied both on

the operational as well as strategic level, in accordance with relevant competences. Depending on the risk profile of

the exposure, the Bank applies the following limits:

industry limits that reflect the risk stemming from the type of activity of the customer,

objective limits, resulting from the risk borne by the purpose of the loan,

subjective limits, defined depending on the customer type,

and product limits.

The internal limit types and amounts are approved by the Bank’s Management Board. In internal procedures, the

Bank defines the principles for setting and updating internal limit amounts as well as the frequency of monitoring

their observance and reporting the monitoring results.

The portfolio credit risk monitoring process consists in a cyclical review of the values of limited parameters and

analysis of the limit usage.

Current monitoring and reporting are of key importance for the credit risk management process. The risk profile

information, as well as information on the possible threats and actions undertaken, is regularly prepared and

communicated.

The distribution of credit decision powers at the Bank is an additional credit risk reducing factor.

3.5.2. Counterparty Credit Risk

The following procedures are applicable at the Bank:

assessment of the financial standing of the counterparty bank,

definition and monitoring of exposure limits granted for the counterparty bank and the country,

monitoring, classification, and reporting of the current exposure to the counterparty bank and the country.

The exposure limits are set to limit the risk and should be understood as:

in relation to counterparty banks:

○ settlement risk connected with a possible default on BGK receivable by the counterparty bank on

the settlement date, where the total amount of a contract (agreement) is at risk, whereas the risk

covers all cash flows taking place between BGK and the counterparty bank,

○ pre-settlement risk, connected with a possible counterparty bank’s partial or full default on a

payment obligation within a given lifetime, as a result of which the Bank can incur losses.

in relation to countries:

○ political risk – risk connected with a possible negative impact of political decisions, conditions, or

events in a given country on the financial sector, as a result of which investors will incur losses or

lose profits,

○ economic risk – risk that the receivables will not be recovered as a result of a deteriorated economic

situation in a given country.

Page 14 of 47

This risk is reduced with the use of relevant limits:

in the case of banks, these are:

○ settlement limit for interbank market transactions,

○ pre-settlement limit for interbank market transactions,

○ trade finance transaction limit,

○ banking group limit,

in the case of countries:

○ country exposure limit,

○ treasury securities issuer limit.

The current exposure affecting the limits for banks and other counterparties takes account of the positive valuation

and volatility of market parameters.

Chart No. 3 shows the credit quality distribution of banks on the basis of a rating of BGK’s existing exposures.

Chart No. 3. Credit quality of counterparty banks on the basis of the Bank’s exposures as at 31.12.20164

In order to arrive at the exposure value under derivative transactions when calculating the capital requirement for

credit risk and counterparty credit risk, the Bank uses the mark-to-market method referred to in Article 274 of the

CRR.

The value of exposures under derivative transactions is determined as the sum of:

the current replacement cost equal to the current market value, where the latter is positive,

the potential future credit exposure equal to nominal amounts (or delta equivalent in case of options),

multiplied by the percentages specified in the CRR depending on the nature of the derivative transaction.

As at 31 December 2016, the Bank did not use offsetting of transactions to estimate the capital requirement for

credit risk and counterparty credit risk.

Table no. 3 shows data of the positive fair value of derivatives.

Table No. 3. Positive fair value of derivatives as at 31.12.2016 (in PLN million)

positive gross fair value total collateral provided net value

In total 429.3 438.1 -8.8

In order to mitigate counterparty bank credit risk, the Bank concludes master agreements and collateral

agreements, which make it possible to offset mutual receivables in justified events (“event of default” and

“termination event”) and provide for the exchange of margins to cover the exposures arising from derivatives. The

agreements concluded are based on the commonly used ISDA, CSA or PBA standards. In addition, in almost all cases

where there is such a possibility, the Bank settles transactions using a central counterparty (CCP).

4 account based on external ratings by Moody’s, Standard&Poor’s, and Fitch Ratings, mapped onto a uniform AAA-B scale

AA and higher 4.7%

A 78.4%

BBB 13.2%

BB and lower 1.4%

no rating 2.2%

Page 15 of 47

The amount of variation margin exchanged with counterparties under the signed agreements that hedge the risks

associated with derivative transactions does not depend on a deterioration of credit quality. On the other hand,

a deterioration of credit quality could result in the need to establish an initial margin.

3.5.3. Credit risk mitigation techniques

The Bank uses the following instruments and methods to limit or reduce the credit risk:

risk diversification,

risk hedging,

risk distribution,

risk compensation.

The Bank uses the Financial Collateral Comprehensive Method in order to determine the capital requirement for

credit risk.

The value of a collateral is periodically monitored during the lifetime of a transaction bearing credit risk. Should an

unfavourable change occur in the value of the collateral, the Bank implements adequate procedures.

The Bank accepts the following main types of collaterals:

real property mortgage,

bank guarantee and State Treasury guarantee,

KUKE S.A. guarantee or insurance,

surety of a local government unit,

registered pledge on movables,

promissory notes.

Specific types of collaterals are established depending on the total Bank’s exposure to the customer, economic and

financial standing of the customer, customer and product type, and other factors.

The main guarantors in the Bank’s lending activity include local government units offering loan sureties, as well as

State Treasury, or KUKE S.A.

Each time before a collateral is established in the form of a local government unit’s surety, the economic and

financial standing of the entity is examined in accordance with the rating and creditworthiness methodology for

local government units applicable at the Bank. As a rule, only those local government units may be guarantors which

are deemed creditworthy and have been positively assessed by the Regional Audit Chamber in terms of budget

implementation and accuracy of the total debt.

Export credit transactions with counterparty banks as part of the Financial Exports Support Government Programme

are fully protected under insurance agreements concluded by the Bank with Korporacja Ubezpieczeń Kredytów

Eksportowych S.A. (KUKE S.A.). The credit protection of KUKE S.A. is carried out in line with the general conditions of

export credit insurance guaranteed by the State Treasury.

Table no. 4 shows credit protection forms for individual exposure classes.

Page 16 of 47

Table No. 4. Exposures covered with credit protection under the standardised approach for capital requirements as at 31 December 2016 (in PLN million)

5

Exposure classes Exposure amount*

Credit protection

in % Guarantees and sureties

Financial collaterals

In total

Central governments and central banks 95,576.3 0.0 0.0 0.0 0.0%

Regional governments and local authorities 5,989.7 0.0 0.0 0.0 0.0%

Public sector entities 610.3 144.0 1.2 145.2 23.8%

Institutions, including banks 7,663.6 567.8 1,700.3 2,268.2 29.6%

Corporates 23,743.3 3,107.1 2,016.9 5,124.1 21.6%

Retail 834.2 0.0 0.6 0.6 0.1%

Secured by mortgages on immovable property 5,688.2 274.1 25.9 300.0 5.3%

In default 2,302.5 77.5 4.5 82.0 3.6%

Associated with particularly high risk 2,329.5 143.5 0.0 143.5 6.2%

Equity exposures 1,344.6 0.0 0.0 0.0 0.0%

Other items 872.2 0.0 0.0 0.0 0.0%

In total 146,954.3 4,314.0 3,749.5 8,063.5 5.5%

* value of balance-sheet exposures and balance-sheet equivalent of off-balance sheet liabilities, and derivative transactions, without taking into account the effects of credit risk mitigation

A predominant credit protection that ensures maximum risk reduction applies to transactions with other corporates,

secured with sureties or guarantees whose main issuers are local government units and the State Treasury.

Primarily, local government units offer sureties for exposures of affiliated Social Housing Associations, hospitals, and

municipal companies. Healthcare entities constitute a significant share of local government’s sureties as well. The

risk for transactions with banks can be reduced owning to treasury securities.

3.5.4. Reduction of a customer’s credit rating

If the credit rating of a customer is reduced, or the value of their collateral decreases, the Bank may demand from

the debtor, during the lifetime of the transaction bearing credit risk, to provide an additional collateral or to replace

the existing collateral, depending on the individual risk rating. Such actions are provided for in debtor agreement

templates.

3.5.5. Tabulated data of credit risk and counterparty credit risk

Definitions

Definition of past due receivables

In its lending activities, the Bank defines past due receivables and acts in line with the regulation of the Minister of

Finance on provisioning principles.

Definition of impaired receivables

In its lending activities, the Bank defines impaired receivables and acts in line with the approach defined in the

regulation of the Minister of Finance on provisioning principles. Impaired receivables are exposures classified under

“substandard”, “doubtful”, and “loss” categories. Exposures are classified under individual categories on the basis of

the assessment of the economic and financial standing of the customer and timeliness of repayment of their

liabilities.

5since the figures in the tables are rounded, differences in totals and percentages may occur

Page 17 of 47

Definition of value and provision adjustments

The Bank applies the special provisioning principles for the banking book, defined in the regulation of the Minister of

Finance on provisioning principles. There is also an internal instruction applicable at the Bank to regulate credit

exposure classification principles and specific risk provisions that defines the rules and procedures for decisions

taken in this field. The decisions under consideration are taken on a quarterly basis, by way of a detailed credit

portfolio review taking account of repayment timeliness and economic and financial standing of the entities, and

also the condition of legal collaterals taken into account in reduction of the basis for special provisioning. In the case

of negative phenomena, the Bank reclassifies the receivables and special provisioning also in periods between the

quarterly portfolio reviews.

In the case of counterparty banks, the Bank assigns categories to the exposures (pursuant to the regulation of the

Minister of Finance on provisioning principles) on the basis of the economic and financial standing of the banks or a

repayment timeliness analysis. The Bank sets economic and financial standing categories for banks on the basis of

two criteria: rating and the amount of the banks’ own funds.

Moreover, a general risk provision is created at the Bank based on the parameters of the Probability of Default (PD),

the loss on the exposure affected by the default (Loss Given Default, LGD), and the probability that the counterparty

will use the off-balance sheet portion of the exposure within the time horizon of the provision creation (Credit

Conversion Factor, CCF).

The write-down amount is determined in accordance with the following formula: (Balance-sheet exposure + Off-

balance-sheet exposure*CCF)*PD*LGD.

Due to the non-cancellable nature of the exposures in the Bank’s portfolio, a CCF of 100% is used.

The PD parameter is determined on the basis of the rating system used at the Bank, and in the case of portfolios not

covered by rating – on the basis of the history of changes in the level of the exposures in default.

The LGD parameter is determined on the basis of a historical analysis of recovery levels, and for the portfolios with

no sufficient history of recovery levels available – on the basis of an expert judgement.

Irrespectively of the write-down amount determined in accordance with the above formula, additional write-downs

associated with the identified elevated risk of certain portfolios of e.g. coal companies or housing enterprises with

very remote maturity dates are created.

General information

The total amount of exposure under credit risk (after accounting adjustments), excluding the results of credit risk

mitigation effects, totalled PLN 146,954.3 million as at 31 December 2016.

The amount of exposures presented in tables in section 3.5.5 has been determined as the sum of balance-sheet

exposures and a balance-sheet equivalent of off-balance sheet commitments and derivative transactions, without

taking into account the effects of credit risk mitigation.

The average amount of exposure by classes is shown in Table no. 5 (exposure classes with zero values have been excluded).

Page 18 of 47

Table No. 5. Average exposure amount in 2016 by classes (in PLN million)6

Amount of exposure Average exposure

amount

Central governments and central banks 95,576.3 2,572.4

Regional governments and local authorities 5,989.7 6.2

Public sector entities 610.3 8.0

Institutions, including banks 7,663.6 133.2

Corporates 23,743.3 106.8

Retail 834.2 0.1*

Secured by mortgages on immovable property 5,688.2 11.5

In default 2,302.5 2.3

Associated with particularly high risk 2,329.5 97.9

Equity exposures 1,344.6 79.6

Other items 872.2 92.7

In total 146,954.3

* does not include aggregated items concerning off-balance-sheet exposures arisen as a result of sureties or guarantees granted by BGK as part of the implementation of government programmes, those resulting from sureties or guarantees for the loan portfolio referred to in Article 128b.2 (1) of the Banking Law Act and meeting, in the loan-granting bank, the conditions of classification to the retail exposure class, specified in Article 123(a) and (b) of the CRR

The Bank’s financial administration of government institutions’ ventures results in very high exposures both in the

class of “central governments and central banks” and the class of “institutions, including banks”.

Table No. 6 shows geographic distribution of credit exposures by countries, while Table no. 7 – geographic

distribution of domestic exposures by regions.

Table No. 6. Geographic distribution of BGK’s exposures by countries as at 31.12.2016 (in PLN million)

Country

Cen

tral

gove

rnm

ents

an

d

cen

tral

ban

ks

Reg

ion

al

gove

rnm

ents

an

d

loca

l au

tho

riti

es

Inst

itu

tio

ns,

incl

ud

ing

ban

ks

Co

rpo

rate

s

Secu

red

by

mo

rtga

ges

on

imm

ova

ble

pro

per

ty

Ass

oci

ated

wit

h

par

ticu

larl

y h

igh

ris

k

Oth

er c

lass

es

In t

ota

l

Austria 0.0 0.0 204.4 0.0 0.0 0.0 0.0 204.4

Belgium 0.0 0.0 235.8 0.0 0.0 0.1 0.0 235.9

Belarus 0.0 0.0 496.2 121.7 0.0 143.9 0.0 761.8

Russian Federation 0.0 0.0 75.8 259.3 0.0 0.0 0.0 335.1

France 45.7 0.0 2,347.0 0.0 0.0 0.0 0.0 2,392.7

Luxembourg 0.0 0.0 22.1 0.0 0.0 263.5 8.3 294.0

Germany 0.0 0.0 636.9 60.3 0.0 0.0 0.0 697.3

Poland 95,530.6 5,989.7 3,085.1 23,116.6 5,688.2 1,920.2 5,888.8 141,219.3

United Kingdom 0.0 0.0 475.6 24.2 0.0 0.0 0.0 499.8

Other 0.0 0.0 84.5 161.3 0.0 1.7 66.6 314.0

In total 95,576.3 5,989.7 7,663.6 23,743.3 5,688.2 2,329.5 5,963.7 146,954.3

Exposures to foreign entities result first of all from transactions with foreign banks as well as implementation of the

Financial Exports Support programme.

6 average value calculated on the basis of quarterly data of exposures to individual customers of the Bank under a given class

Page 19 of 47

Table No. 7. Geographic distribution of BGK’s exposures by regions as at 31.12.2016 (in PLN million)

Province

Cen

tral

gove

rnm

ents

an

d

cen

tral

ban

ks

Reg

ion

al

gove

rnm

ents

an

d

loca

l au

tho

riti

es

Inst

itu

tio

ns,

incl

ud

ing

ban

ks

Co

rpo

rate

s

Secu

red

by

mo

rtga

ges

on

imm

ova

ble

pro

per

ty

In d

efau

lt

Oth

er c

lass

es

In t

ota

l

Dolnośląskie 0.0 1,133.3 211.8 819.7 497.1 152.1 242.3 3,056.2

Kujawsko-Pomorskie 0.0 310.5 14.6 40.6 301.3 151.0 31.9 849.8

Lubelskie 0.0 262.0 0.0 208.7 100.7 220.2 18.3 809.9

Lubuskie 0.0 222.1 0.0 8.5 124.5 38.0 12.4 405.5

Łódzkie 0.0 324.8 0.0 143.9 123.5 83.6 48.7 724.4

Małopolskie 0.0 585.4 36.0 1,143.9 419.5 60.5 94.2 2,339.5

Mazowieckie 95,529.2 504.1 2,393.0 14,471.9 1,467.3 560.7 4,867.5 119,793.6

Opolskie 0.0 228.7 0.0 28.8 29.2 7.0 14.8 308.5

Podkarpackie 0.0 266.5 0.0 429.9 48.3 32.3 8.9 785.8

Podlaskie 0.0 206.2 0.0 52.0 257.0 12.3 29.0 556.5

Pomorskie 1.4 396.5 53.0 714.2 398.8 142.4 35.2 1,741.3

Śląskie 0.0 386.1 376.9 2,863.4 540.2 650.4 15.1 4,832.0

Świętokrzyskie 0.0 170.6 0.0 33.1 65.6 3.5 10.1 282.9

Warmińsko-Mazurskie 0.0 353.5 0.0 54.4 175.2 21.2 41.2 645.5

Wielkopolskie 0.0 401.4 0.0 1,993.6 737.9 48.5 57.2 3,238.5

Zachodniopomorskie 0.0 238.3 0.0 110.1 402.2 52.3 46.4 849.2

In total 95,530.6 5,989.7 3,085.1 23,116.6 5,688.2 2,235.9 5,573.2 141,219.3

Approximately 85% of the exposures are for Mazowieckie. This is because of the concentration of central

government bodies in this province, the exposures to which constitute the greatest part of the Bank’s portfolio.

Table no. 8 shows the structure of BGK’s impaired exposures by regions.

Table No. 8. Structure of impaired exposures and specific risk provisions of BGK’s exposures by regions as at 31.12.2016 (in PLN million)

Province

Exposures in default

Specific risk provisions

Impaired exposures, not

past due Structure in %

Impaired exposures, past

due Structure in %

Dolnośląskie 151.9 6.9% 0.2 1.1% 19.5

Kujawsko-Pomorskie 151.0 6.8% 0.0 0.1% 27.2

Lubelskie 220.2 9.9% 0.0 0.0% 9.6

Lubuskie 38.0 1.7% 0.0 0.0% 7.0

Łódzkie 82.3 3.7% 1.3 6.2% 42.1

Małopolskie 54.2 2.4% 6.3 29.8% 65.8

Mazowieckie 555.3 25.1% 5.3 25.3% 131.2

Opolskie 7.0 0.3% 0.0 0.0% 2.7

Podkarpackie 32.3 1.5% 0.0 0.0% 41.6

Podlaskie 12.3 0.6% 0.0 0.0% 10.8

Pomorskie 138.7 6.3% 3.7 17.5% 53.9

Śląskie 649.9 29.3% 0.5 2.3% 243.3

Świętokrzyskie 3.5 0.2% 0.0 0.0% 5.2

Warmińsko-Mazurskie 21.2 1.0% 0.0 0.0% 8.9

Wielkopolskie 48.1 2.2% 0.4 1.8% 36.8

Zachodniopomorskie 48.9 2.2% 3.3 15.9% 14.8

Foreign exposures 0.0 0.0% 66.6 76.0% 2.8

In total 2,214.8 100.0% 87.6 100.0% 723.2

Page 20 of 47

Most impaired exposures occur in the provinces of Śląskie, Mazowieckie, and Lubelskie. Impaired exposures in

Śląskie are first and foremost a result of financing entities from the coal extraction industry. In the case of

Mazowieckie, to a large extent this results from a substantial share of historic developer exposures of 2006–2009,

and then from exposures of the former National Housing Fund (NHF). In the case of Lubelskie, the main reason for

the substantial level of impaired credits are exposures of the former NHF and transactions with corporates.

Table no. 9 shows the structure of BGK’s exposures by sectors (exposure classes with zero values have been

excluded).

Table No. 9. Structure of BGK’s exposures by sectors as at 31.12.2016 (in PLN million)

Sector Exposure classes*

In total E1 E2 E3 E4 E5 E6 E7 E8 E9 E10 E11

Public administration and defence, compulsory social security

76,454.8 5,978.9 6.1 0.0 0.0 0.0 0.0 153.9 0.0 245.6 0.0 82,839.4

Construction 0.9 0.0 0.0 0.0 454.3 2.1 3,911.4 621.8 0.0 20.4 0.0 5,010.9

Financial activities 19,069.1 0.0 33.6 3,085.1 3,969.6 0.3 125.9 0.3 1,884.0 1,039.5 8.8 29,213.2

Professional, scientific, technical, and educational activities

3.8 0.0 44.4 0.0 167.1 1.2 73.9 1.6 0.3 0.0 0.0 295.2

Mining and extraction 0.0 0.0 0.0 0.0 951.2 0.5 3.1 609.2 0.0 0.0 0.0 1,563.9

Wholesale trade 0.0 0.0 0.0 0.0 297.5 8.1 21.0 5.8 0.0 0.0 0.0 332.3

Hotels and restaurants 1.0 0.0 0.0 0.0 32.5 2.8 18.3 6.7 0.0 0.0 0.0 61.3

Real estate market, management

0.0 0.0 0.1 0.0 739.9 1.7 562.3 13.2 0.0 16.0 0.0 1,333.2

Health care and social assistance

0.0 0.0 500.3 0.0 25.9 3.7 68.8 50.6 0.0 0.0 0.0 649.3

Other services, sports, entertainment, and recreation

1.0 5.1 16.8 0.0 16.5 0.3 5.9 73.4 0.0 0.0 0.0 119.0

Industrial processing 0.0 0.0 0.0 0.0 3,632.2 7.1 435.6 66.8 0.0 7.5 0.0 4,149.2

Transport, storage and communication

0.0 0.0 5.6 0.0 5,743.0 2.0 116.5 474.1 0.0 0.0 0.0 6,341.2

Electricity, gas and water supply

0.0 5.7 3.4 0.0 7,086.9 5.5 337.1 136.4 0.0 7.2 0.0 7,582.2

Other (e.g. individuals, no Polish Classification of Activity (PKD) number)

45.7 0.0 0.0 4,578.4 626.7 798.9 8.6 88.8 445.2 8.3 863.4 7,464.0

In total 95,576.3 5,989.7 610.3 7,663.6 23,743.3 834.2 5,688.2 2,302.5 2,329.5 1,344.6 872.2 146,954.3

* E1 – central governments and central banks E2 – regional governments and local authorities E3 – public sector entities E4 – institutions, including banks E5 – corporates E6 – retail exposures

E7 – secured by mortgages on immovable property E8 – in default E9 – associated with particularly high risk E10 – equity exposures E11 – other items

The portfolio structure is dominated by public administration and finance as a result of well-developed cooperation

of BGK with central and local government units, which triggers the need to cooperate with financial entities to

ensure funding and liquidity. A relatively large group of exposures is also constituted by the construction industry,

mainly because of loans granted as part of the former NHF. The Bank also engages in funding ventures which are

strategic from the point of view of the State Treasury, including in the sectors of energy, fuel and chemistry, and

transport. Such ventures are implemented in the form of large investment projects.

Table no. 10 show structure of exposures to small and medium-sized enterprises (SMEs) by industry.

Page 21 of 47

Table No. 10. Structure of BGK’s exposures to SMEs by sectors as at 31.12.2016 (in PLN million)

Industry

Exposures to SME

In total Structure

in % Corporates Retail

Secured by mortgages on

immovable property

Public administration and defence, compulsory social security

0.0 0.0 0.0 0.0 0.0%

Construction 0.0 1.8 1.0 2.8 0.6%

Financial activities 0.0 0.3 0.0 0.3 0.1%

Professional, scientific, technical, and educational activities

0.0 1.2 0.0 1.2 0.2%

Mining and extraction 0.0 0.5 0.0 0.5 0.1%

Wholesale trade 0.0 8.0 1.5 9.5 1.9%

Hotels and restaurants 0.0 2.8 0.0 2.8 0.6%

Real estate market, management 0.1 1.7 0.0 1.8 0.3%

Health care and social assistance 3.2 3.5 2.6 9.3 1.8%

Other services, sports, entertainment, and recreation

0.0 0.3 0.0 0.3 0.1%

Industrial processing 2.8 7.1 3.4 13.3 2.6%

Transport, storage and communication 5.2 2.0 0.0 7.2 1.4%

Electricity, gas and water supply 0.0 5.5 2.2 7.7 1.5%

Other (individuals, no Polish Classification of Activity (PKD) number)

0.0 448.3 0.0 448.3 88.8%

In total 11.3 482.9 10.7 504.9 100.0%

Exposures to SMEs are classified under three classes: corporates, retail exposures, and exposures secured by

mortgages on immovable property.

Table no. 11 shows the quality of BGK’s exposures by industry .

Table No. 11. Quality of BGK’s exposures by sectors as at 31.12.2016 (in PLN million)

Industry

Exposures in default Specific risk provisions

Impaired exposures, not

past due Structure in %

Impaired exposures, past

due Structure in %

Public administration and defence, compulsory social security

153.9 7.0% 0.0 0.0% 36.1

Construction 610.5 27.6% 11.4 13.0% 199.7

Financial activities 0.3 0.0% 0.0 0.0% 0.4

Professional, scientific, technical, and educational activities

1.6 0.1% 0.0 0.0% 2.5

Mining and extraction 606.7 27.4% 2.5 2.8% 269.0

Wholesale trade 4.7 0.2% 1.1 1.3% 28.4

Hotels and restaurants 6.6 0.3% 0.1 0.1% 18.8

Real estate market, management 11.8 0.5% 1.4 1.6% 5.2

Health care and social assistance 50.6 2.3% 0.0 0.0% 53.1

Other services, sports, entertainment, and recreation

73.4 3.3% 0.0 0.0% 1.2

Industrial processing 64.6 2.9% 2.2 2.5% 20.2

Transport, storage and communication 474.1 21.4% 0.0 0.0% 23.8

Electricity, gas and water supply 136.4 6.2% 0.0 0.0% 40.8

Other (individuals, no Polish Classification of Activity (PKD) number)

19.8 0.9% 68.9 78.7% 23.9

In total 2,214.8 100.0% 87.6 100.0% 723.2

Construction industry has the worst quality structure in the BGK’s portfolio, which results from the set-up of the

industry, comprising mostly credits for developers (in a substantial part at risk), and also credits of the former NHF

Page 22 of 47

with a large share of impaired exposures – reclassified as a result of financial assessment of the customers. Another

sector having a weak quality structure is mining and extraction industry, due to a significant share of exposures to

entities extracting coal, classified to higher risk groups because of their financial condition.

Table no. 12 shows the general risk provision by activity type.

Table No. 12. General risk provision by activity type as at 31.12.2016 (in PLN million)

Activity type General risk

provision

Charges under general risk

provisions in 2016.

Commercial activities, of which: 233.3 95.1

large entities 171.8 126.6

small and medium-sized entities, individuals, other entities 61.5 -31.4

Local government units 10.5 -0.6

Surety activities, commissioned 13.1 -19.6

Residential construction programme 9.7 -94.0

In total 266.6 -19.1

Table 13 shows BGK’s exposure by residual maturity (exposure classes with zero values have been excluded).

Table No. 13. Structure of BGK’s exposures by residual maturity as at 31.12.2016 (in PLN million)

Residual maturity

Exposures

In total up to 1 month

more than

1 month up to 3 months

more than

3 months

to 6

months

more than

6 months

up to 1 year

more than

1 year up to 3

years

more than

3 years up to 5 years

more than

5 years past due

Central governments and central banks

20,379.6 1,497.2 148.8 755.7 5,987.1 795.1 66,012.8 0.0 95,576.3

Regional governments and local authorities

0.8 3.6 12.3 161.7 915.6 1,137.1 3,758.5 0.0 5,989.7

Public sector entities 3.7 3.0 0.2 11.5 62.8 164.6 364.5 0.0 610.3

Institutions, including banks 4,211.3 19.1 1,314.5 129.6 310.6 518.3 1,160.2 0.0 7,663.6

Corporates 2,752.8 1,157.1 393.2 727.2 5,216.8 2,479.6 11,014.6 1.8 23,743.3

Retail exposures 1.8 1.1 0.9 442.5 13.7 16.0 358.0 0.2 834.2

Secured by mortgages on immovable property

0.0 11.7 250.0 295.9 336.6 192.2 4,600.0 1.9 5,688.2

In default 16.8 37.7 2.7 20.6 155.7 392.5 1,593.4 83.1 2,302.5

Associated with particularly high risk

0.0 2.0 29.1 34.5 31.6 46.6 2,185.6 0.0 2,329.5

Equity exposures 0.0 0.0 0.0 0.0 0.0 47.8 1,296.8 0.0 1,344.6

Other items 8.8 0.0 0.0 0.0 0.0 0.0 863.4 0.0 872.2

In total 27,375.6 2,732.5 2,151.7 2,579.3 13,030.6 5,789.7 93,207.8 87.0 146,954.3

Structure in % 18.6% 1.9% 1.5% 1.8% 8.9% 3.9% 63.4% 0.1% 100.0%

The largest group of exposures are central governments and central banks exposures maturing within more than 5

years and resulting from the service of flow funds by the Bank. Also exposures to corporates have a large share in

the portfolio. These are mainly exposures maturing within more than 5 years, which results from the Bank financing

large investment projects with long-term implementation and repayment periods. In addition, a significant group in

terms of size are loans whose residual maturity exceeds 5 years and which were granted to Social Housing

Associations and housing cooperatives as part of the former NHF, as well as loans to local government units.

Page 23 of 47

Provisions

Tables 14 and 15 present the balance of provisions and adjustments in 2016.

Table No. 14. Reconciliation of adjustments and specific risk provisions of BGK for 2016 (in PLN million)

Item As at 01.01.2016 Write-offs

created Write-offs released

Charged to write-offs

Other adjustments

As at 12.31.2016

Specific risk provision 620.9 531.0 -402.2 -26.5 0.0 723.2

regular 0.0 0.0 0.0 0.0 0.0 0.0

watched 8.3 52.4 -10.4 0.0 3.1 53.4

substandard 31.2 71.9 -16.0 0.0 -0.4 86.7

doubtful 204.4 382.5 -327.1 0.0 -4.2 255.6

loss 377.0 24.2 -48.7 -26.5 1.5 327.5

In 2016, the Bank recovered receivables amounting to PLN 87.3 million.

Table No. 15. Reconciliation of adjustments and provisions of BGK for 2016 (in PLN million)

Item Deferred tax

liability provision

Provisions for litigation

Provisions for pensions and

other employee benefits

Provisions for off-balance

sheet (financial and guarantee)

liabilities

General risk provisions

In total

Opening balance 56.3 13.9 15.0 144.8 285.6 515.6

1. Provisions established 0.0 0.8 3.7 121.5 157.8 283.8

2. Provisions released 0.0 -0.2 0.0 -50.6 -176.9 -227.7

3. Other value changes, of which:

13 -0.3 -1.7 -7.9 0.0 3.1

- deferred tax provision increase

25.6 0.0 0.0 0.0 0.0 25.6

- deferred tax provision decrease

-12.6 0.0 0.0 0.0 0.0 -12.6

Closing balance 69.3 14.2 17.0 207.8 266.6 574.8

The Bank records each provision established and released on the basis of the purposes underlying their

establishment or release – without compensation of the related costs and incomes, by individual events.

3.6. Liquidity risk

Definition

The liquidity risk is a threat of losing the ability to pay liabilities in a timely fashion as a result of unfavourable

changes in assets and liabilities, off-balance-sheet transactions, maturity mismatch of current cash flows, and

possible losses resulting from the foregoing.

The liquidity risk is also dealt with in the context of:

market (product) liquidity risk understood as a threat of losing the ability to convert certain products on the

market into cash within the required time frame, resulting in the need to incur financial losses on these

products,

funding risk understood as a threat of shortage of stable funding sources in mid- and long-term, resulting in

real or potential risk of default by the Bank in regard to financial obligations such as payments and

collaterals at their maturity in mid- and long-term, either in whole or involving unacceptable funding costs to

be incurred,

liquidity concentration risk understood as a threat of default in current liabilities due to dependence (lack of

diversification) or overexposure to one entity or associate entities,

Page 24 of 47

liquidity risk in individual currencies in which the Bank carries out its activities, understood as inability to

fulfil the Bank’s liabilities in a given currency due to limitations in convertibility of currencies.

The Bank applies liquidity risk management procedures which define how the risk is monitored and managed.

Liquidity risk management aims to:

ensure and maintain the Bank’s ability to meet its current and future liabilities, taking account of liquidity

costs and return on equity,

prevent contingencies,

define solutions which will enable the Bank to survive a potential crisis (contingency plan).

Measurement

The Bank’s liquidity risk measurement system comprises the following methods:

liquidity ratios (both regulatory and internal), contractual and adjusted liquidity gap analysis, fund stability

analyses, daily monitoring of the deposit base,

stress tests.

The liquidity measures used allow to monitor liquidity in various time horizons. The Bank monitors intraday liquidity

measures developed on the basis of “Monitoring tools for intraday liquidity management” by the Basel Committee7.

Regulatory liquidity measures are calculated in accordance with definitions specified in Resolution No. 386/2008 of

the PFSA and Delegated Regulation 2015/618. As part of internal ratios, the Bank monitors, in particular, ratios

expressing the difference between liquid assets and funds unstable in various time horizons (30 days, 3 months, and

12 months), measures determining the level of long-term funding, concentration and stability of funding source

ratios.

Regulatory liquidity measures are shown in Table No. 16.

Table No. 16. Regulatory liquidity measures limit 31.12.2016

M1 – short-term liquidity gap (in PLN million) 0.00 15,503.8

M2 – short-term liquidity ratio 1.00 1.55

M3 – coverage ratio of non-liquid assets with own funds 1.00 5.03

M4 – coverage ratio of non-liquid and limited-liquidity assets with own funds and stable external funds

1.00 1.24

LCR – liquidity coverage ratio 70% 252%

M1 – the difference between the sum of the primary and supplementary liquidity reserve amount and the amount of external non-stable funds,

M2 – the quotient of the sum of the primary and supplementary liquidity reserve amount to the amount of external non-stable funds,

M3 – the quotient of the Bank’s own funds decreased by the total amount of capital requirements for market risk, delivery settlement risk, and counterparty risk to the non-liquid assets,

M4 – the quotient of the sum of the Bank’s own funds decreased by the total amount of capital requirements for market risk, delivery settlement risk, and counterparty risk and stable external funds to the sum of non-liquid assets and limited-liquidity assets,

LCR – the quotient of the liquidity buffer to net outflows.

As part of liquidity risk measurement, the Bank calculates contractual and adjusted liquidity gap. The liquidity gap

consists in a summary of assets and liabilities by time intervals between the date of the information and the date of

repayment of the bank receivable (assets) and the date of fulfilment of the liabilities by the Bank. The contractual

liquidity gap is calculated in accordance with contractual maturities/due dates, while as part of the adjusted liquidity

gap the following are adjusted to their market values, in particular: deposit values (on the basis of estimated core

7 http://www.bis.org/publ/bcbs248.pdf

8 in resolution no. 386/2008 of 17 December 2008 on the establishment of liquidity standards binding for banks (Official Journal of the PFSA

No. 8, item 40, as amended) measures M1 to M4 were defined

in Commission Delegated Regulation (EU) 2015/61 of 10 October 2014 to supplement Regulation (EU) No 575/2013 of the European Parliament and the Council with regard to liquidity coverage requirement for Credit Institutions (OJ L 11, 17.1.2015, p. 1), the LCR was defined

Page 25 of 47

deposits), liquid securities (presented in the amounts that can be realised in specific time periods), and financial and

guarantee off-balance sheet liabilities granted (in the scope of estimated amounts and realisation dates).

The selected liquidity measures are monitored also in the case of individual significant currencies for which the

amount of liabilities in a given currency exceeds 5% of total liabilities. The market (product) liquidity is reflected in

liquidity measures by taking into account liquid assets with an appropriate haircut.

To assess the impact of adverse conditions on the liquidity level, the Bank regularly carries out stress tests. As part

of stress tests, the Bank develops scenario analyses, sensitivity analyses, and reverse stress tests which take into

account both internal as well as systemic factors. Stress tests are carried out for scenarios covering, among others,

withdrawal of deposits, reduction of securities liquidity, and realisation of off-balance sheet liabilities. Results of

stress tests are used in the liquidity risk management process, including in particular as part of liquidity contingency

plans and in the strategic planning process.

Risk reduction methods

A system of limits is an important liquidity risk management tool at BGK. Both limits and threshold values for

liquidity ratios are applied. The risk monitoring process consists in a cyclical review of the values of limited

parameters and analysis of the limit usage. In 2016, regulatory liquidity measures and the internal limits of liquidity

ratios were not breached.

In order to reduce risk and secure liquidity, the Bank applies the following measures:

transactions on the money market, including deposit transactions, reverse repo, repo, purchase/sale of NBP

money market bills, Treasury bills, bonds, and other instruments,

maintaining a portfolio of liquid securities,

daily monitoring of the money balance and financing possibilities from the NBP,

facilities securing liquidity of the Bank,

own bond issuances and deposit level management to optimise the structure of the sources of funding,

having a mechanism for determining and applying transfer pricing (a FTP system) in place, with regulation of

the liquidity margin included,

modelling, forecasting, and planning liquidity conducted within the framework of forecasting and planning

processes,

plans in case of emergency situations of reduced or endangered liquidity.

In order to hedge the liquidity risk, the Bank maintains a relevant surplus of liquid assets characterised, among other

things, by high credit quality, high tradability, and high liquidity on the repo transaction market. As part of the

excess liquidity, Treasury bonds and NBP money market bills are taken into account, among other things.

The main source of funding for the Bank are deposits, including in particular deposits from the public sector. The

Bank also obtains funding through issuances of own bonds and incurs loans from international financial institutions.

Stable funding sources of the Bank’s own activities (core deposits with maturity dates above one year) are

diversified – the percentage of each category of liabilities as at 31 December 2016 is as follows: deposits represent

71%, bonds issued 16%, and loans 13% of the liabilities.

3.7. Market risk

Definition

Market risk is understood as a threat of possible deterioration in the value of the Bank’s financial instruments

portfolio or Bank’s financial result as a consequence of unfavourable changes in market parameters (exchange rates,