Report of the Auditor -General the Fiscal Outturns for Fiscal Years... · Auditor-General’s...

246

On the Fiscal Outturns For the Fiscal Years 2008/09 and 2009/10 Winsley S. Nanka, CPA, CFE Acting Auditor-General, R.L. Report of the Auditor-General

Transcript of Report of the Auditor -General the Fiscal Outturns for Fiscal Years... · Auditor-General’s...

On the Fiscal Outturns For the Fiscal Years

2008/09 and 2009/10

Winsley S. Nanka, CPA, CFE

Acting Auditor-General, R.L.

Report of the Auditor-General

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

2 Promoting accountability, transparency, integrity and fiscal probity

Office of the Auditor-General

Republic of Liberia

13 February 2012

TRANSMITTAL LETTER

AUDITOR-GENERAL’S REPORT ON THE FISCAL OUTTURNS FOR THE FISCAL YEARS

2008/9 AND 2009/10.

1. I am pleased to present my report on the Fiscal Outturns for the fiscal years ended June

30, 2009, and 2010. The report is issued in consonance with the requirements of

Section 37(1, 2) of the Public Financial Management (PFM) Act of 2009, which stipulates

that the Minister of Finance shall prepare the un-audited Final Account of the National

Budget and submit it to the Auditor General for his review and certification not later

than four (4) months after the end of the fiscal year.

2. It worth noting that all the findings conveyed in this report had been formally

communicated to the MoF Management and Desk Officers concerned for their responses

through Audit Observation Memoranda (AOMs) and Management Letter. Where

responses were provided, they were evaluated and incorporated in this report.

3. As indicated in my report, the GOL financial operations for the periods under review

were characterized by financial irregularities. These irregularities which amounted to

US$33,941,455.53 took the form of under-levying of penalty and interest on real

property owners; violation of Government Travel Ordinance (i.e. Executive Ordinance on

Foreign Travel No: 8) and lack of supporting evidence for some expenditures reported

in the fiscal outturns as well as unexplained net variances observed between

expenditures reported in the Fiscal Outturns for 2008/9 and 2009/10, respectively, and

that confirmed by line Mini9stries and Agencies.

4. I noted that internal controls within the Revenue Department of MOF were lax as

exemplified by non-imposition of penalty on all defaulting importers to the tune of

LD151, 400, 000.00, who under-declared their respective CIF’s or goods imported. In

other words, of the 757 defaulting importers involved in under-declaration of their CIF

value as detected and reported on by the BCE Post Clearance Audit Unit the required

penalty was levied only on 146. I considered this matter as very significant risk

impacting on the integrity of revenue assessed and collected by the Bureau of Customs

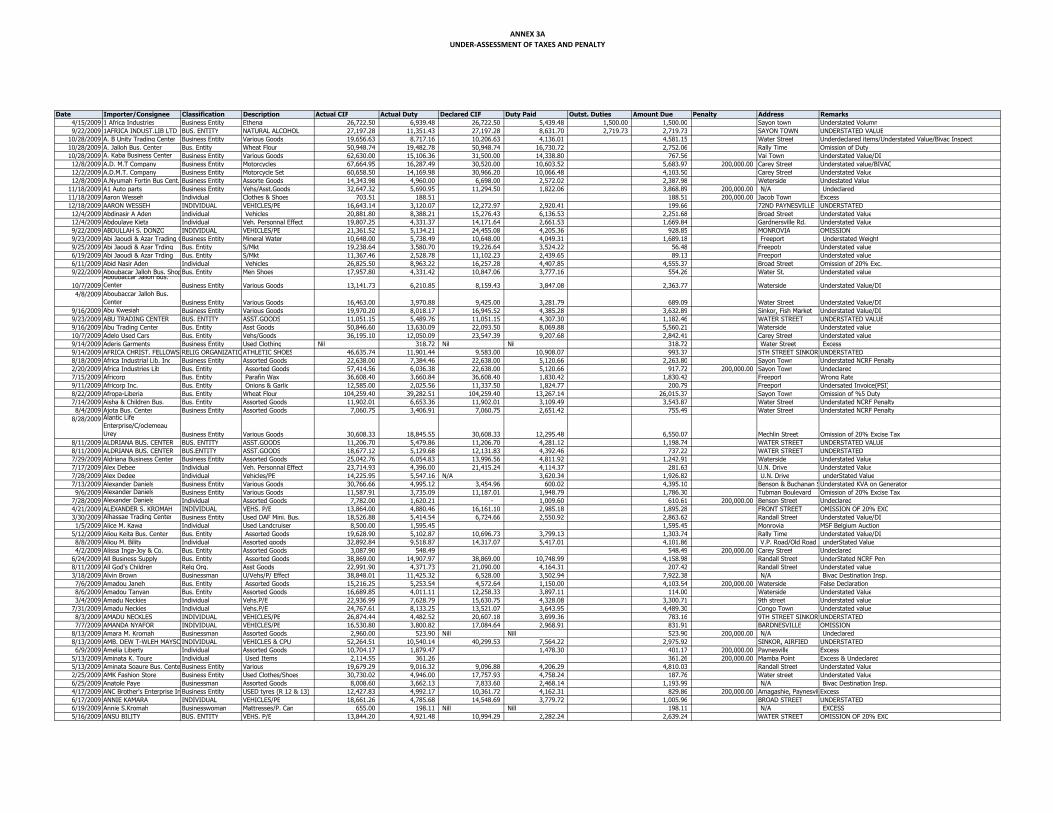

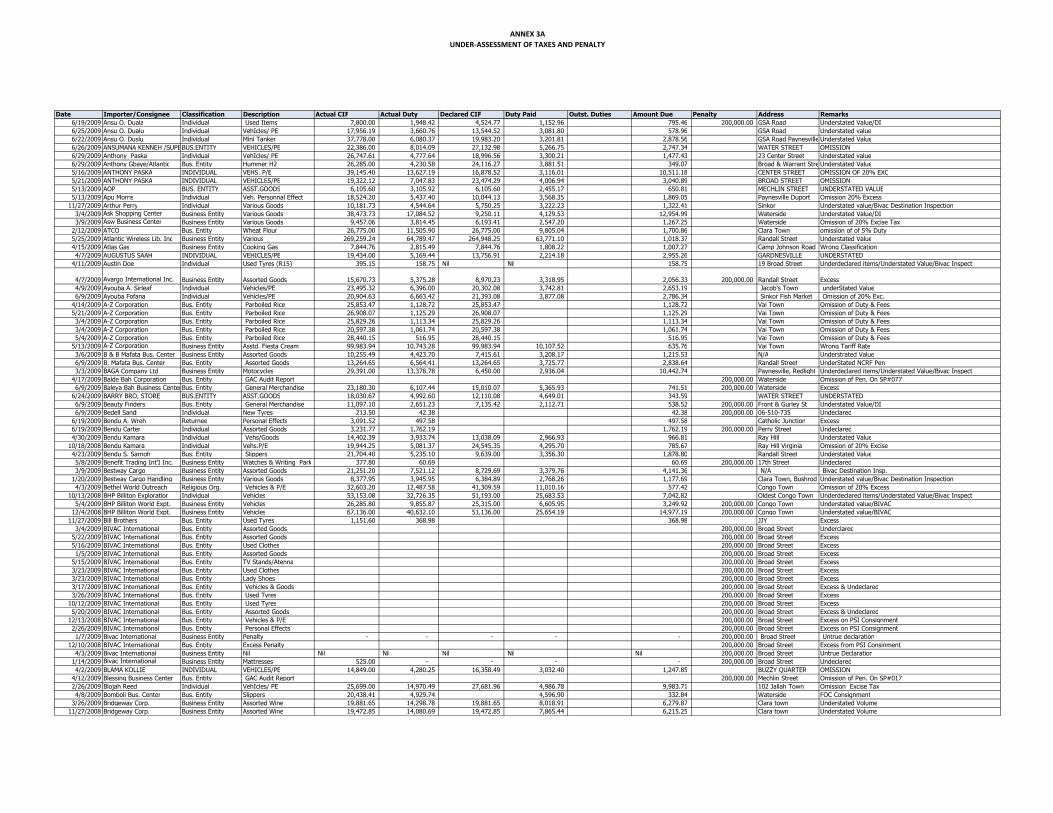

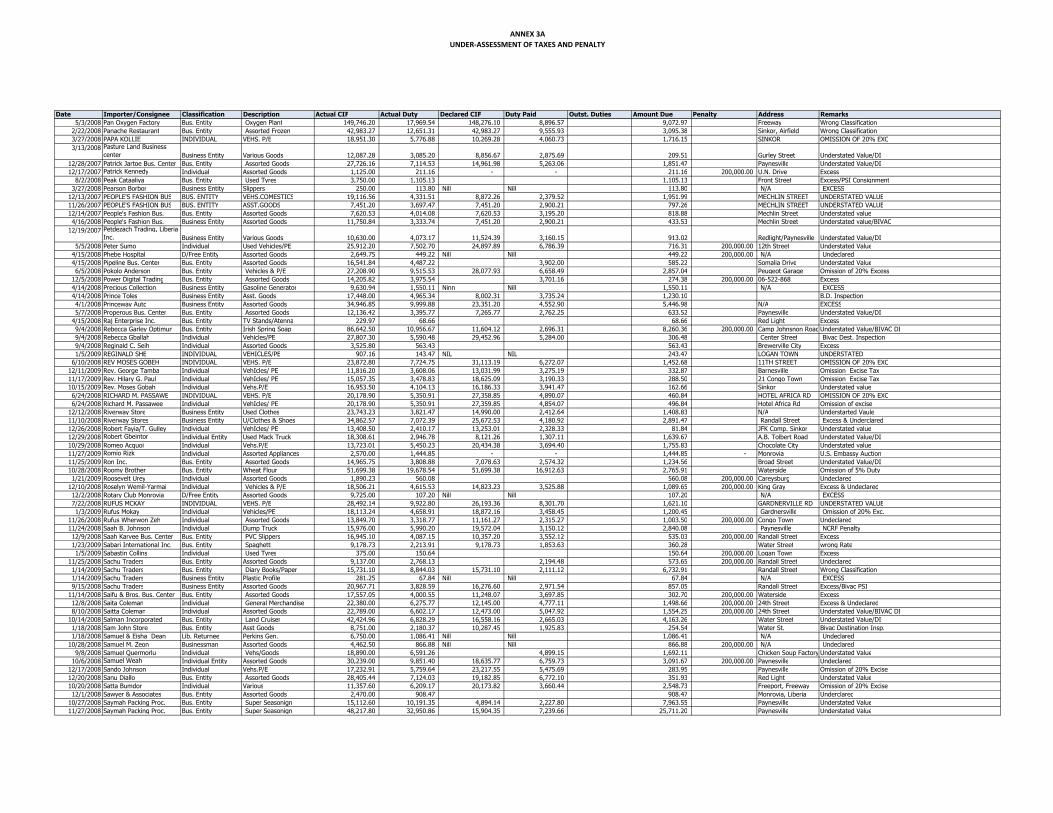

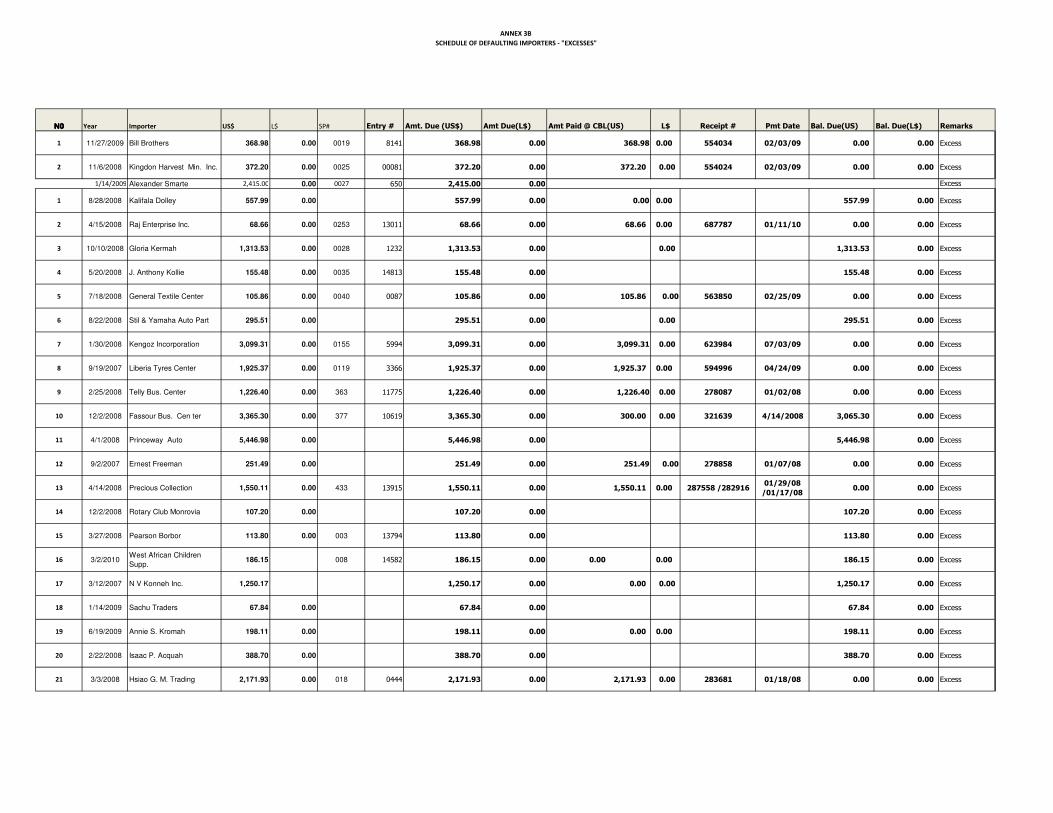

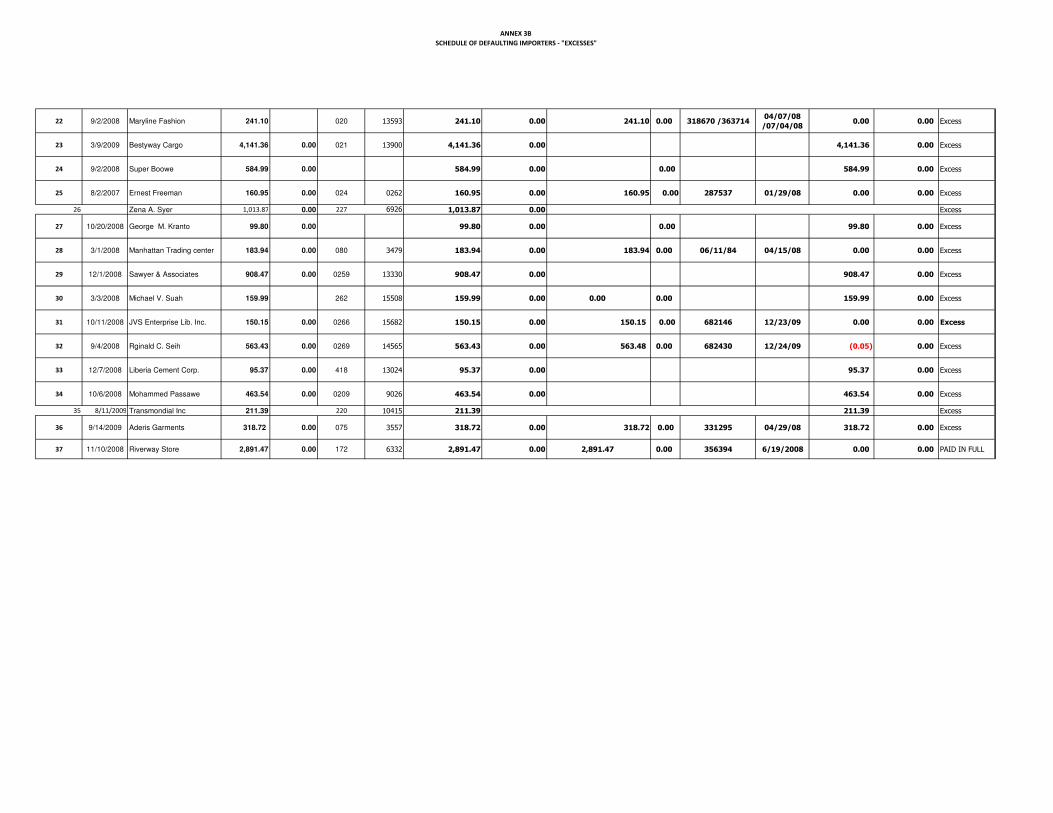

and Excise, and thus I have instructed the Forensic Department of the GAC to carry out

a thorough investigation into each of the cases of the remaining 611 defaulting

importers.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

3 Promoting accountability, transparency, integrity and fiscal probity

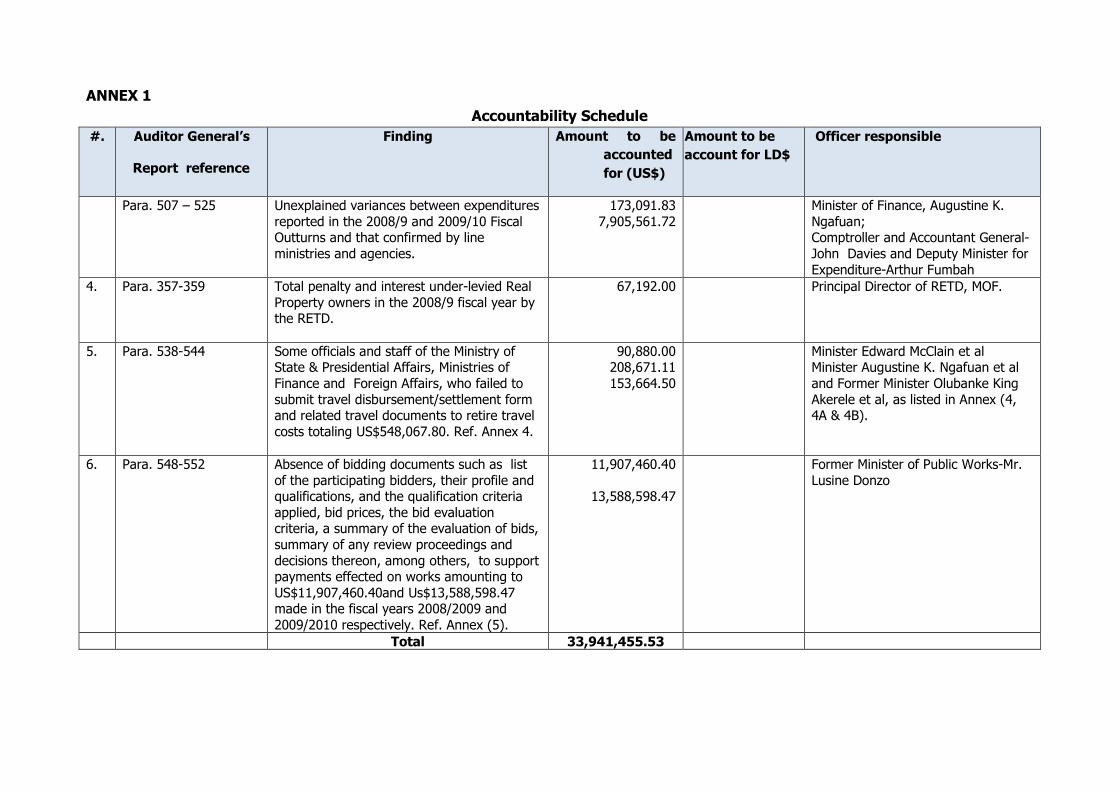

5. Besides the non-payment of related penalty by defaulting importers, it was also

discovered that defaulting importers did not pay additional taxes of US$1,344,816.71

derived from imported goods under-declared by importers. It was established that

BIVAC, Liberia, was partly responsible for the under-assessments and was consequently

billed for the additional taxes payable by the importers. However, there is no evidence

to show that BIVAC had discharged this obligation.

6. It was also noted during the audit that spending agencies were not disclosing to the

Ministers of Finance and Planning and Economic Affairs, all information related to donor

funding (i.e grants and Aid to Liberia). As a result, inflows reported in the Fiscal

Outturns and the National Budgets for the two periods did not contain any information

on Grants and Aid. The non-incorporation and disclosure of donor inflows in the

respective National Budgets and Fiscal Outturns distorts the total income figure reported

in the Fiscal Outturns for the years under review. I have thus advised appropriately in

this report that the Ministers of Finance and Planning and Economic Affairs should

ensure compliance with all requirements on grants and aid, as provided for under the

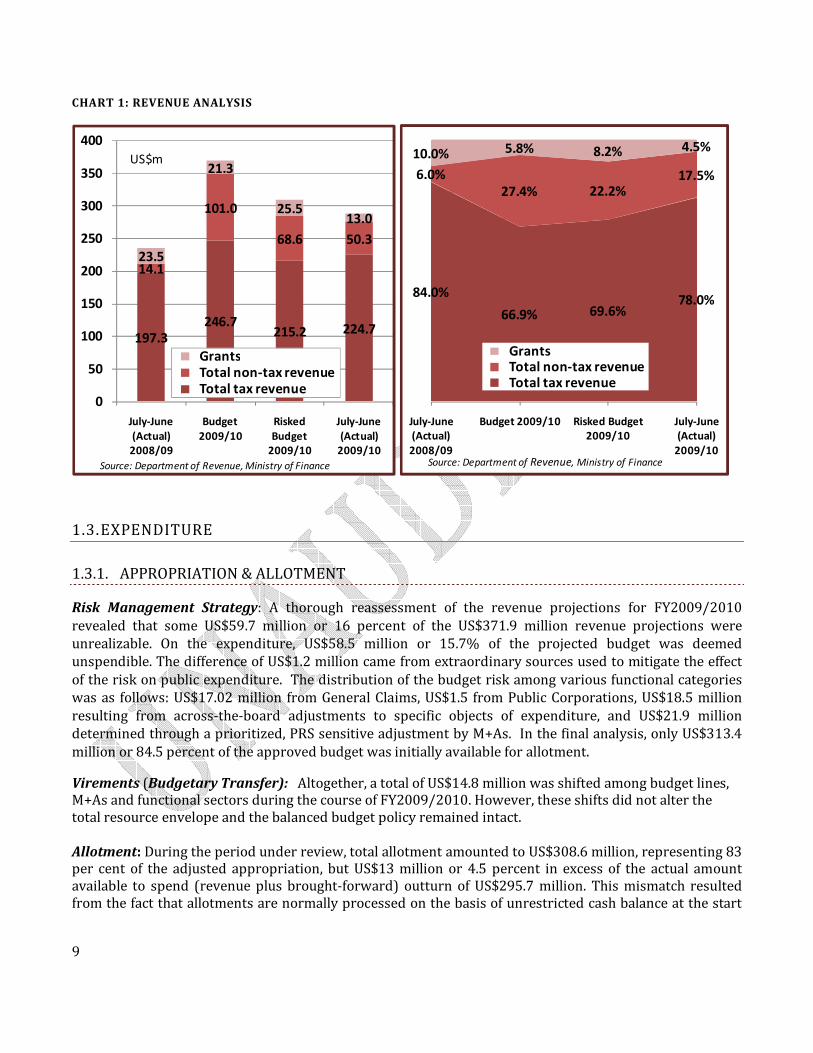

extant reguatory framework by incorporating and disclosing all information on grants

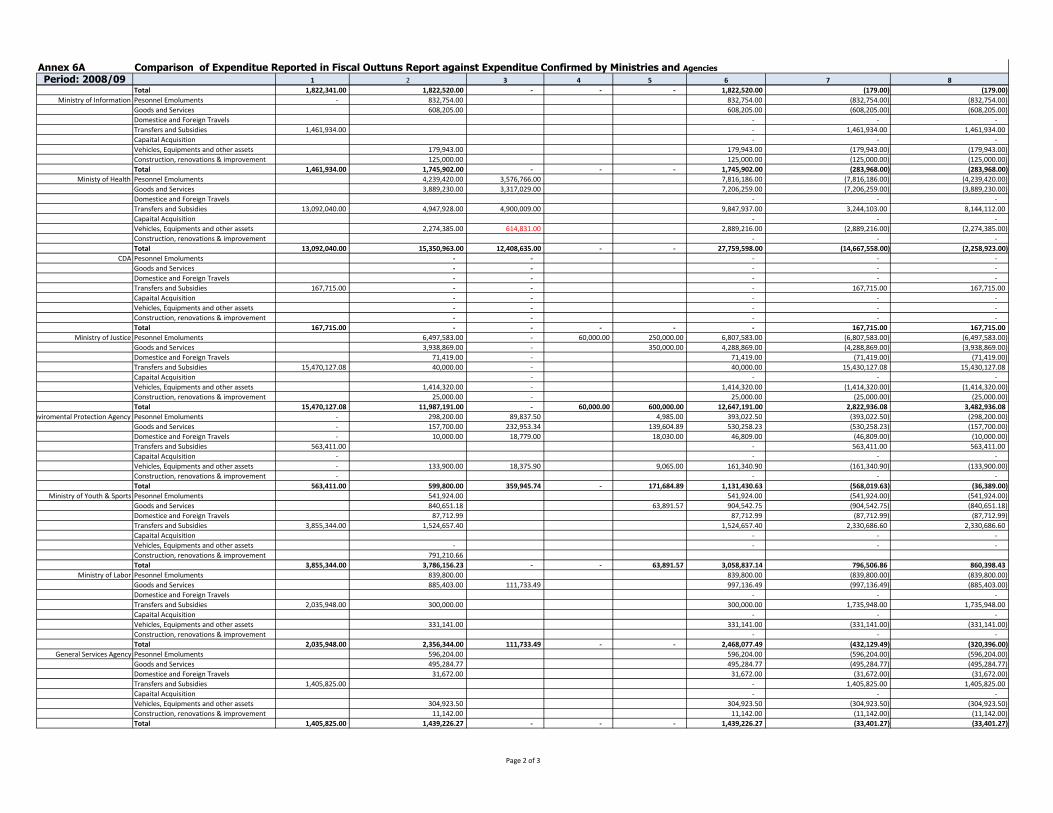

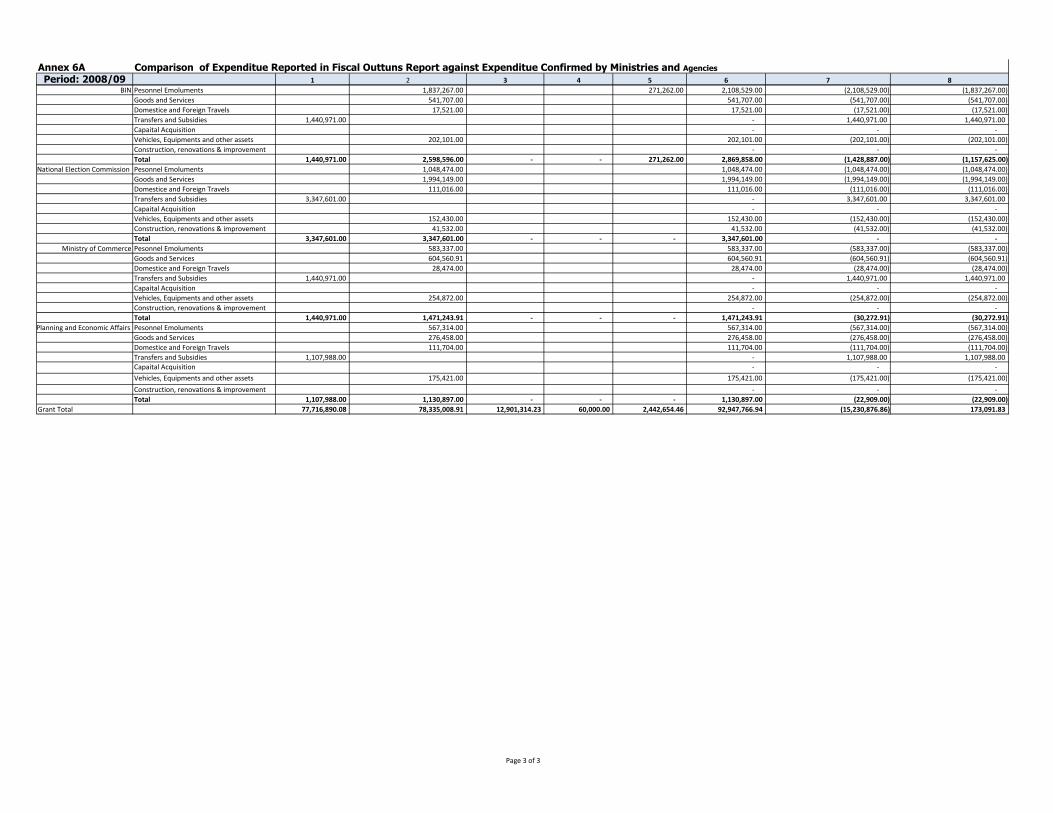

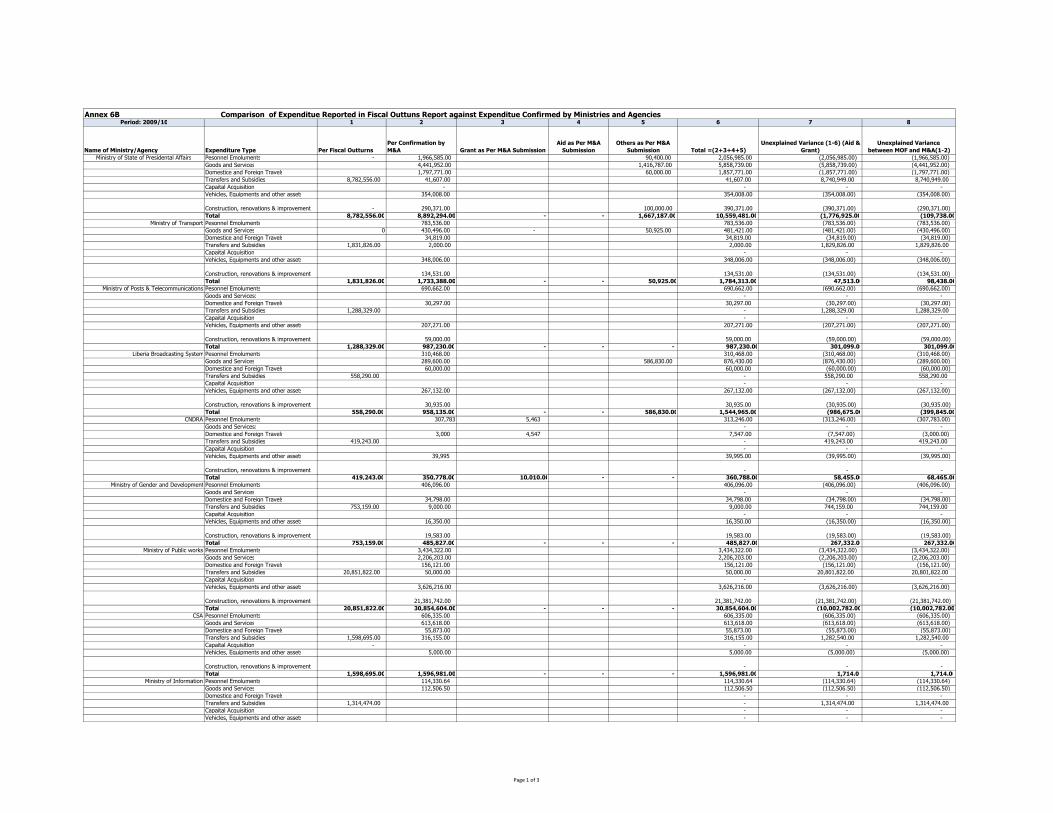

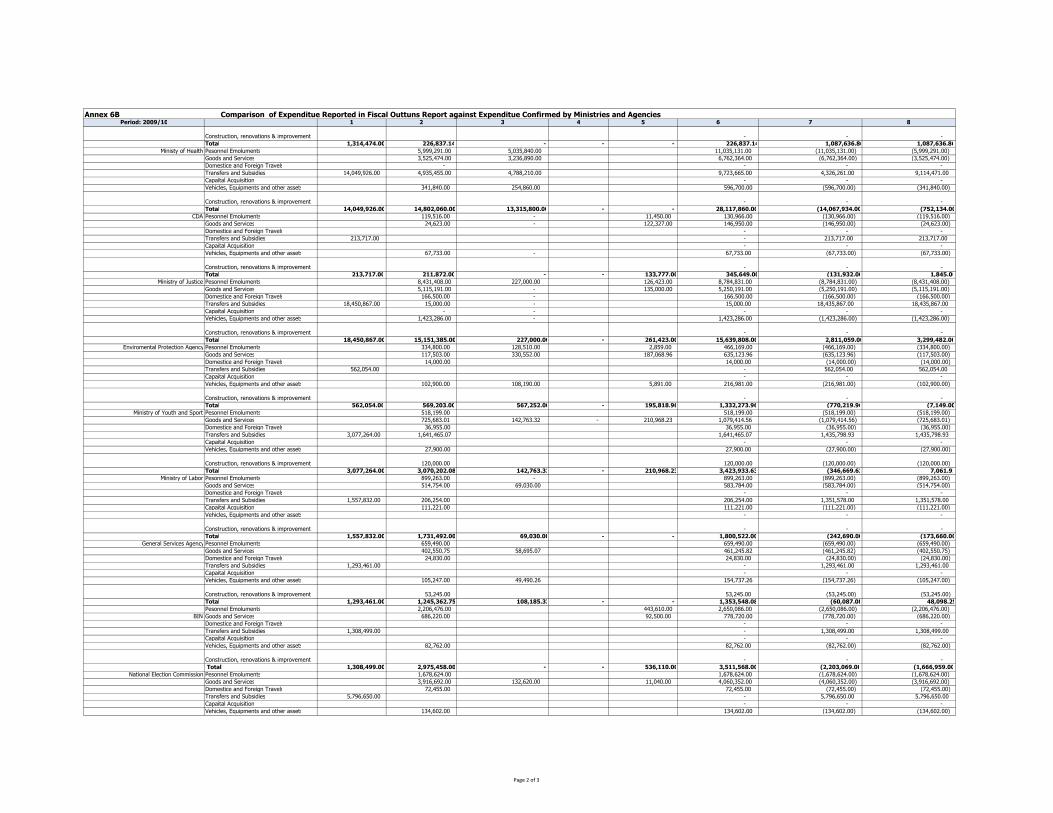

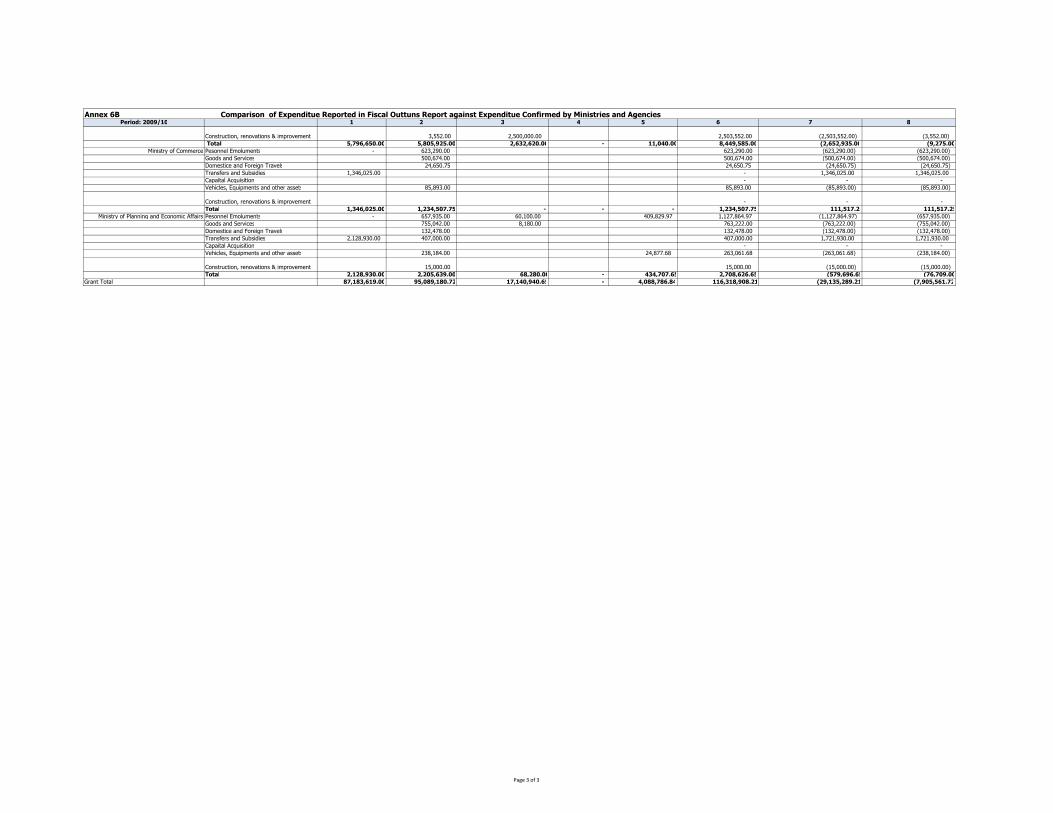

and aid in the National Budgets and Consolidated Fund Account.

7. There were significant variances between the Expenditures as confirmed by the

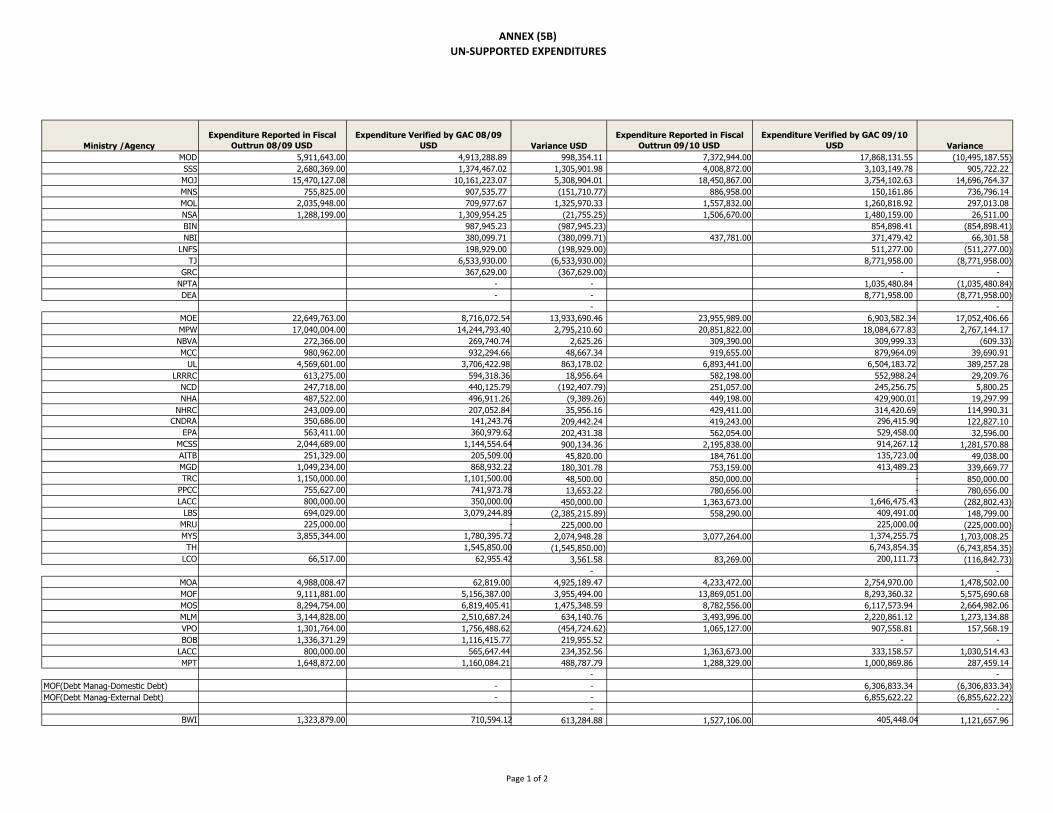

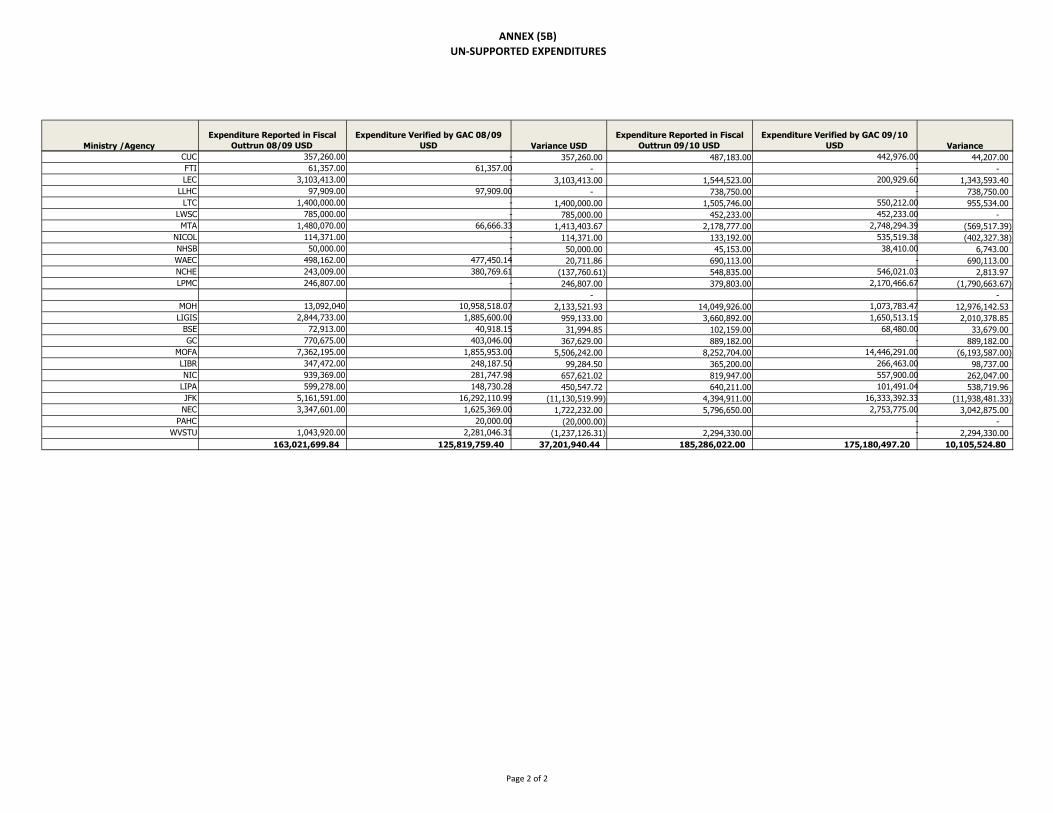

Ministries and Agencies and that conveyed in the Fiscal Outturn Reports for 2008/9 and

2009/10, which the Minister of Finance could not account for. I noted net variances

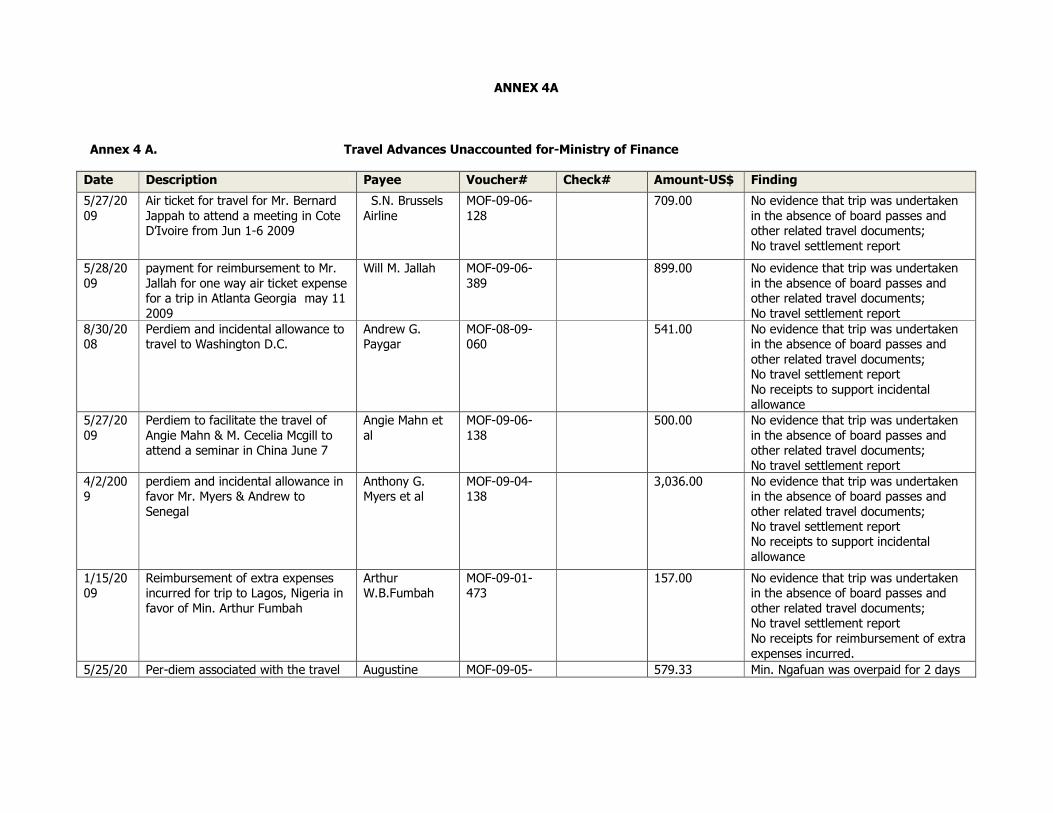

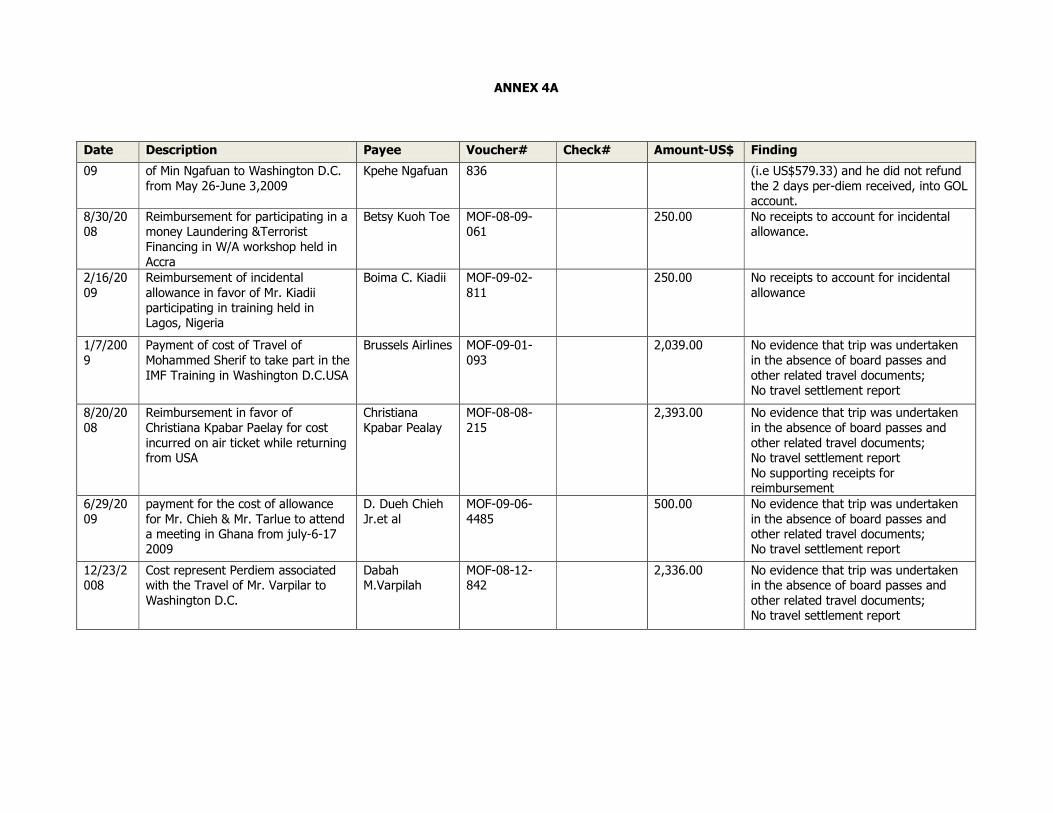

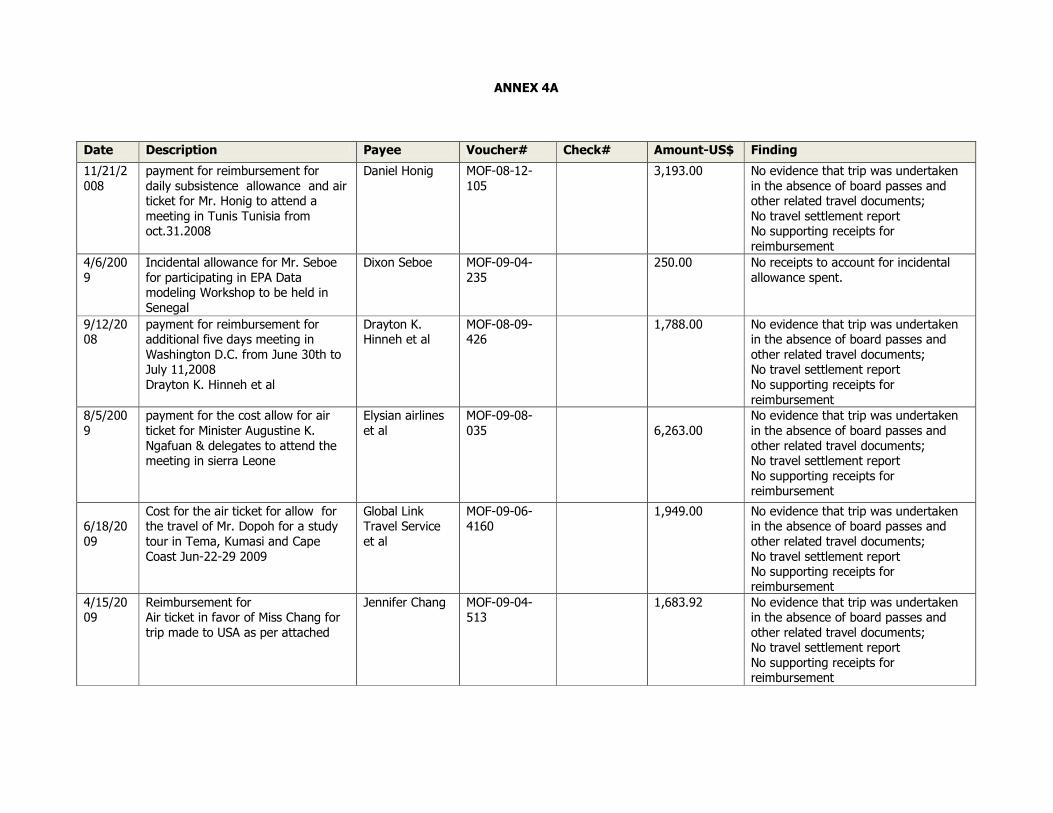

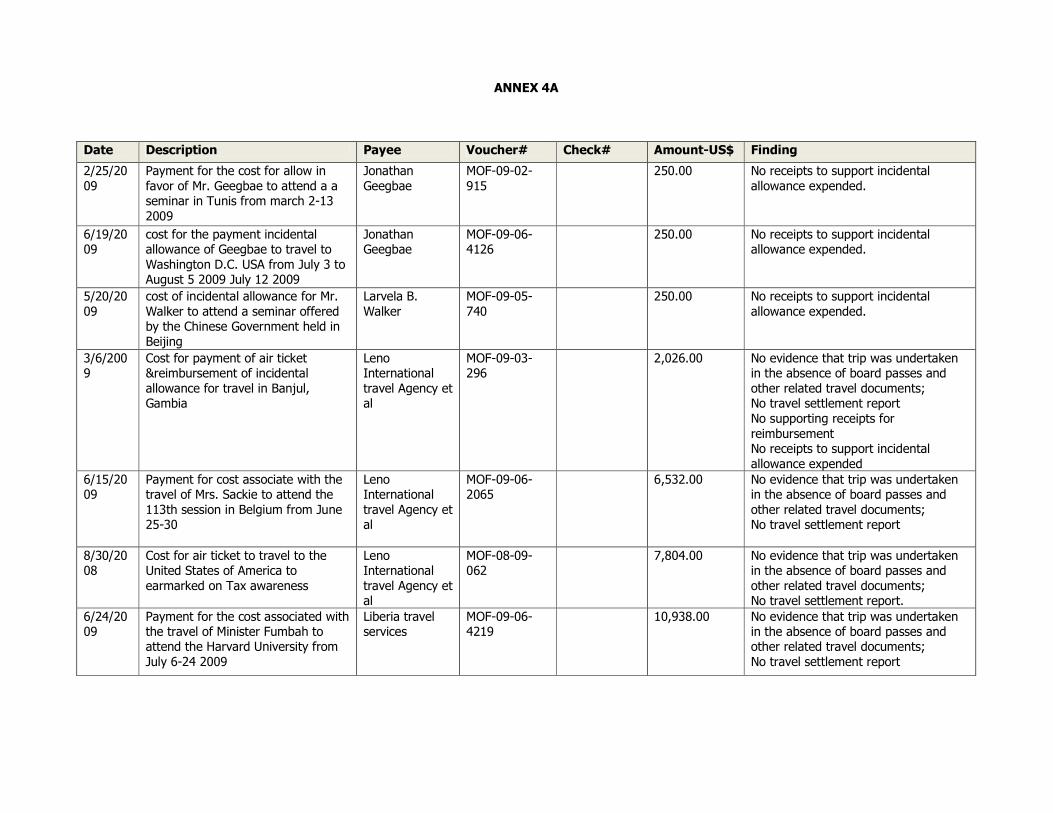

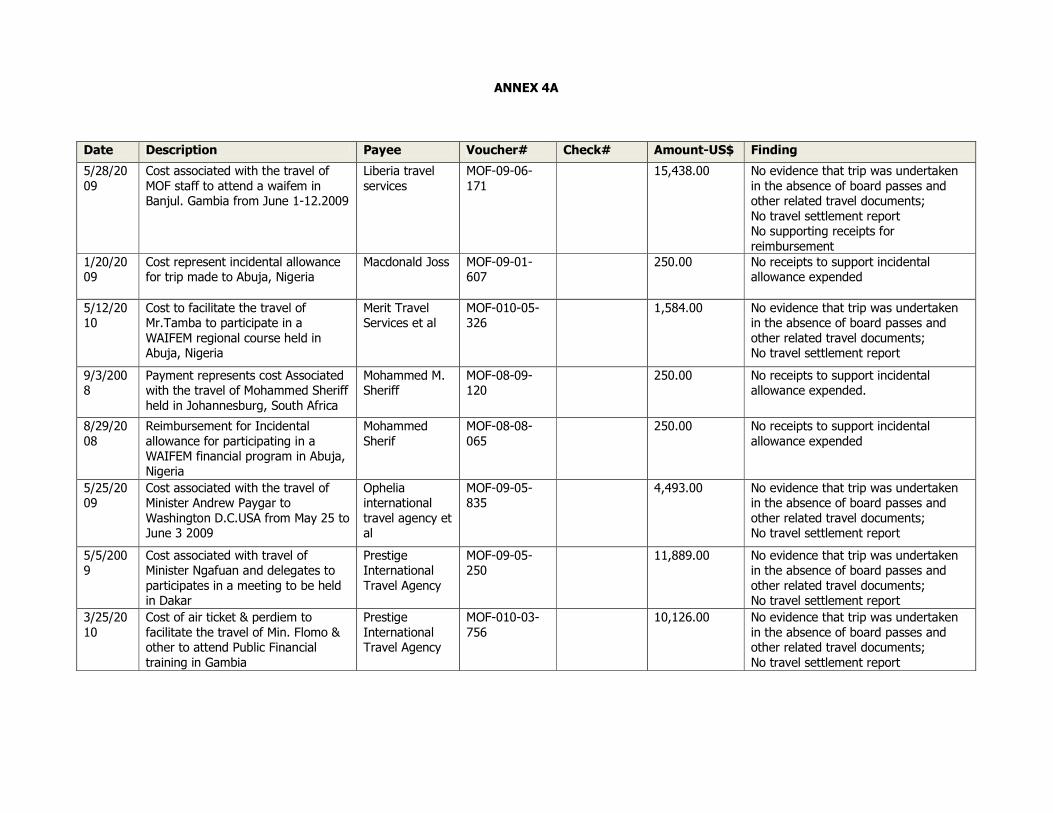

amounting to US$173,091.83 and US$ 7,905,561.72 for the fiscal years 2008/9 and

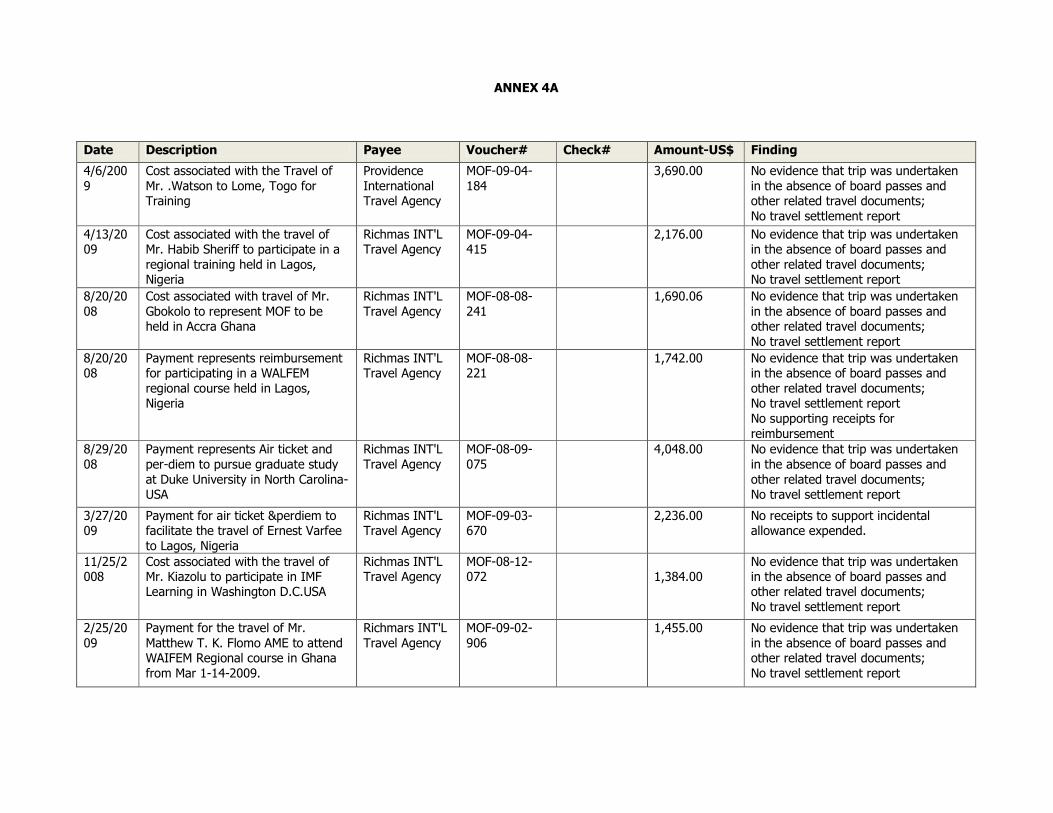

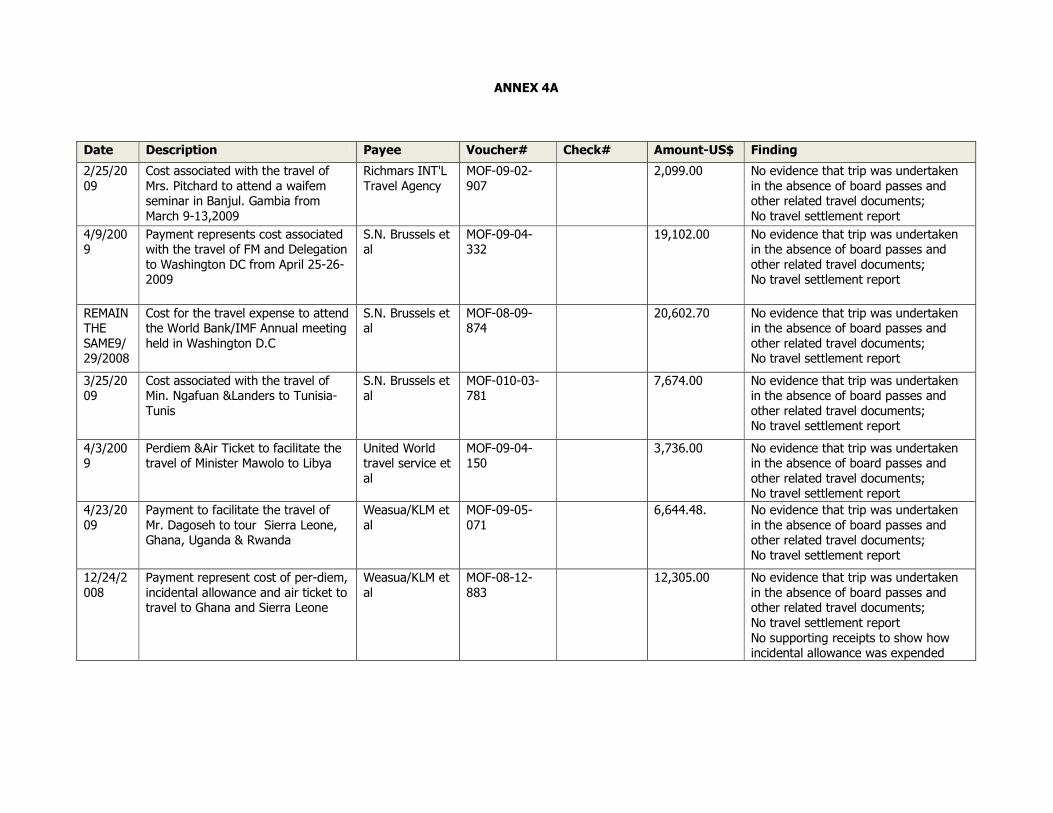

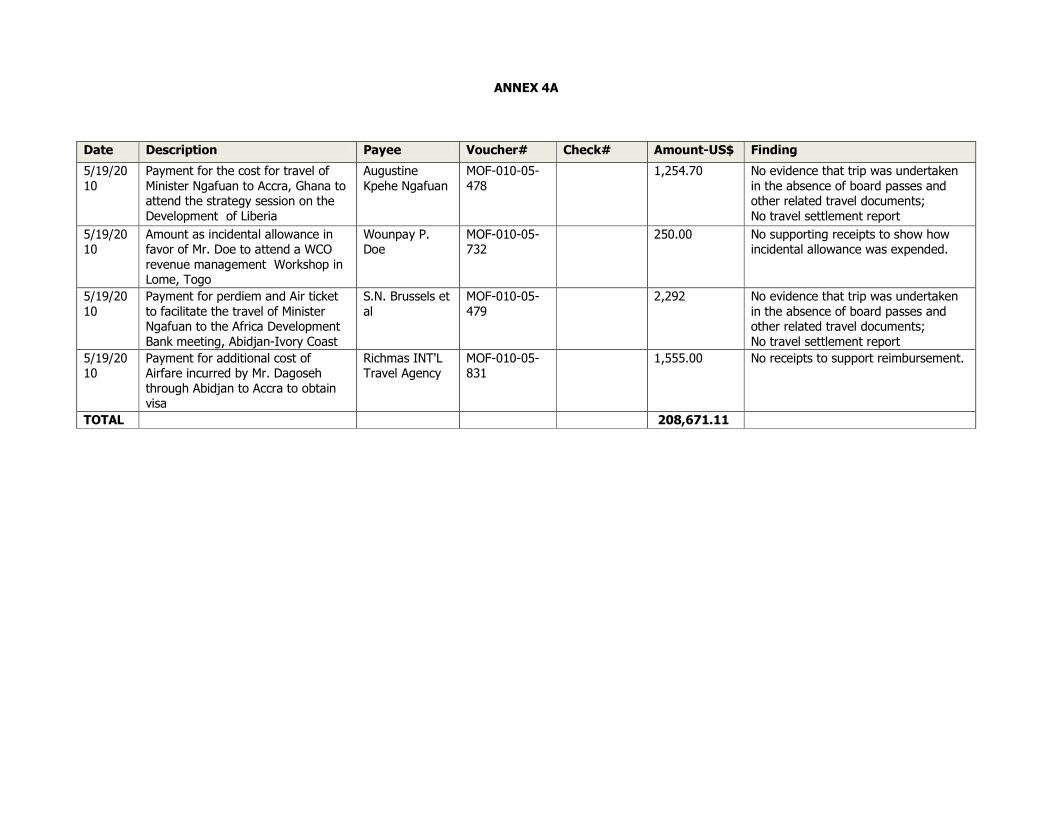

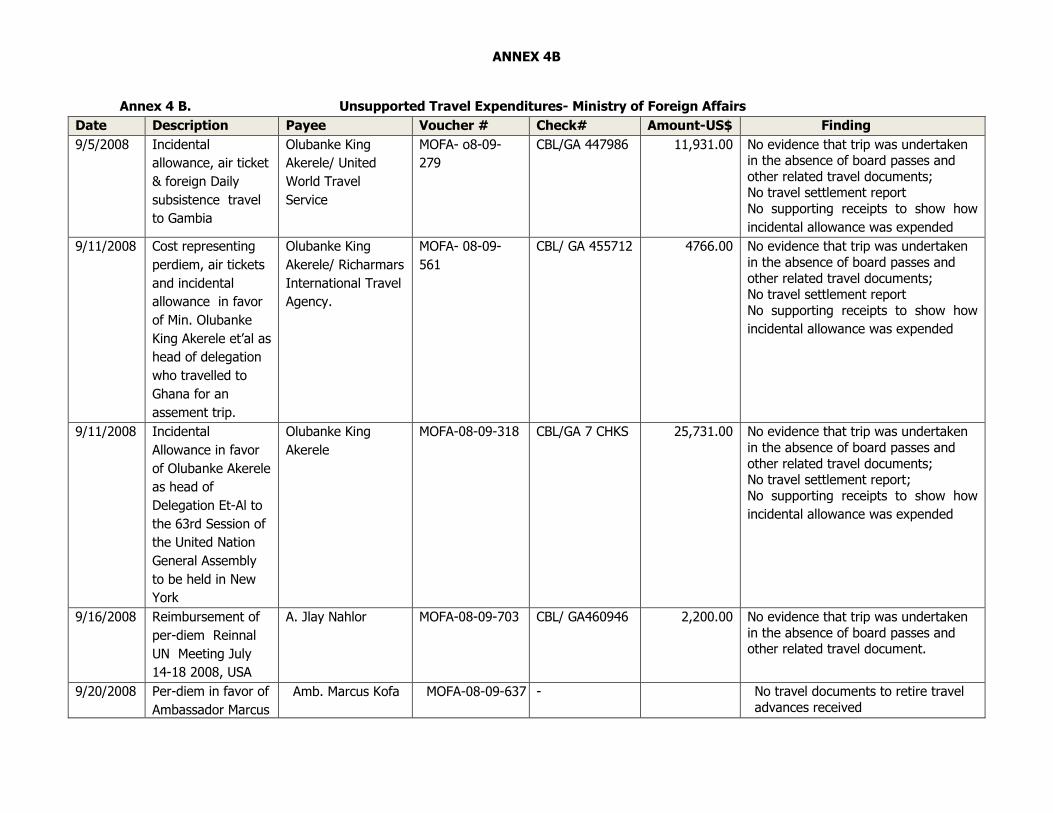

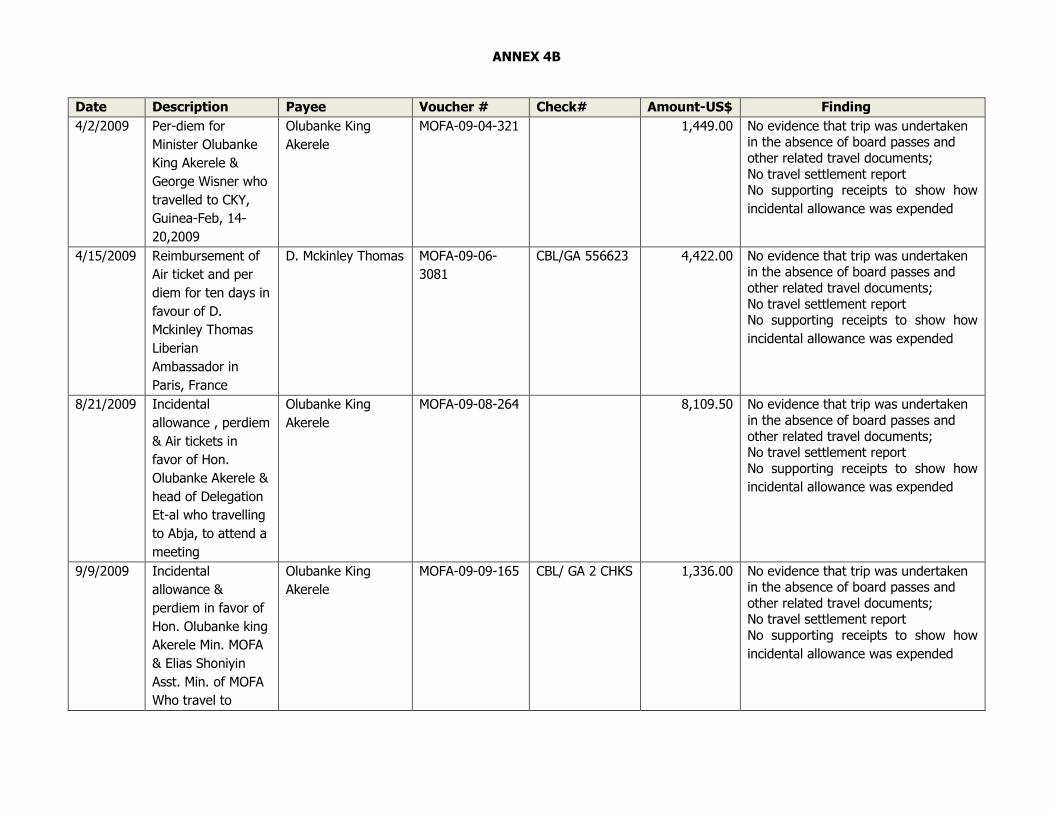

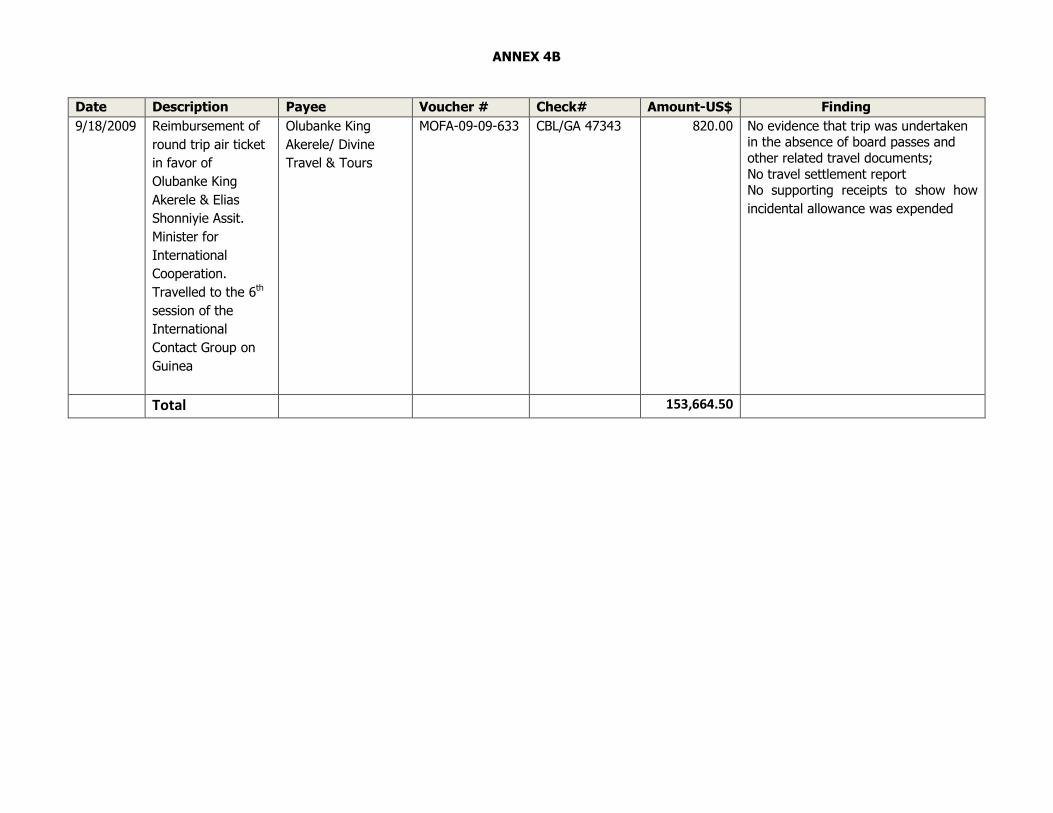

2009/10, respectively, when I sought third- party confirmation from 27 selected line

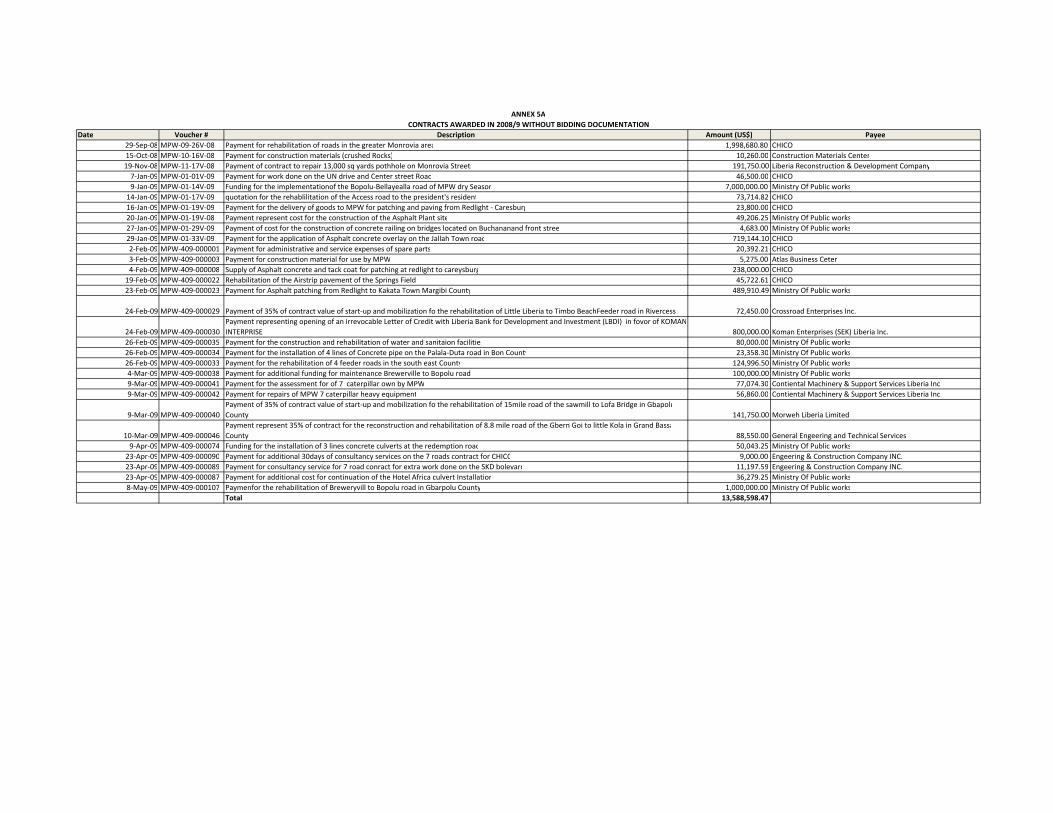

Ministries and Agencies of Government to confirm their Expenditures as reported in the

Fiscal Outturns. To resolve the issue of the non-reconciliation, I have advised that the

Minister of Finance should ensure that reconciliation between the Ministry of Finance

and the line Ministries and Agencies is pursued, as these variances impact negatively on

the fair presentation of the Fiscal Outturn reports for 2008/09 and 2009/10.

8. Similarly, I noted expenditure variances between 2008/9 and 2009/10 Expenditures in

the Fiscal Outturns and those substantiated from the supporting vouchers submitted to

the GAC to the tune of US$37,201,940.44 and US$10,105,524.80 respectively.

9. As indicated in Annex 8, the Minister of Finance own analysis of the variances reported

produced yet another un-explained variances of US$3,091,113.56 and US$3,954,378.31

for FY 2008/09 and 2009/10, of expenditure unsupported, respectively.

10. There were also instances of non adherence to the travel ordinances. I reviewed travel

expenditure made to government officials and employees for foreign travels in order to

obtain the assurance that the requirements of the Executive Ordinances No. 9 on the

application for advance and retirement of travel advances were complied with. I

however noted that some of the officials to whom travel advances totalling

US$453,215.61 were paid, did not retire their advances to show how the monies were

spent.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

4 Promoting accountability, transparency, integrity and fiscal probity

11. Non-preparation in timely fashion by the Controller and Accountant General of the

Financial Statements of the Consolidated Fund of Liberia, as required by Regulation

I.12, Public Financial Management Regulations was also noted during my audit. The

Minister of Finance compiled and submitted to me Fiscal Outturn Reports for the

respective periods instead of Financial Statements of the Consolidated Fund Account.

12. It worth noting however that after the issuance of the Draft Auditor-General’s Report

on the fiscal outturns for 2008/9 and 2009/10, Minister of Finance submitted Financial

Statements of the Consolidated Fund of Liberia for the fiscal year ended June 30, 2010,

compiled on IPSAS cash basis accounting, to GAC on November 21, 2011. Because the

Statements were presented at the virtual end of the audit (i.e. after I have completed

my audit on the Fiscal Outturns), I thus planned that the audit of the 2010/11 fiscal

year financial statements on the Consolidated Fund will cover as well the 2009/2010

financial statements.

13. It is also important to note that significant steps are being taken by the Minister of

Finance to improve public sector financial management in Liberia. The improvements

noted include the migration from a legacy system to an Integrated Financial

Management System (IFMIS), the introduction of a chart of accounts, the preparation of

financial statements based on cash basis International Financial Reporting Standards

(IPSAS), the development of an internal audit strategy and the establishment of an

Internal Audit Oversight Board which will provide oversight in the implementation of the

internal audit strategy, among others.

14. The issues listed above are quite significant because of their impact on public financial

management. Therefore, I urge Her Excellency, the President of the Republic of Liberia,

the Honourable Speaker of the House of Representatives, the President Pro-Tempore of

the Liberian Senate and Members of the National Legislature to consider their resolution

urgently.

Winsley S. Nanka, CPA, CFE

Acting Auditor General, R.L.

Her Excellency, the President of the Republic of Liberia

The Executive Mansion

Monrovia

The Hon. Speaker

The House of Representatives

Capitol Hill, Monrovia

The President Pro-Tempore of the Senate

The House of Senate

Capitol Hill, Monrovia

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

5 Promoting accountability, transparency, integrity and fiscal probity

Table of Contents

ACRONYMS .................................................................................................................................................. 8

EXECUTIVE SUMMARY .............................................................................................................................. 9

Background ................................................................................................................................................. 9

Limitation of Responsibility ..................................................................................................................... 10

Scope Limitation ....................................................................................................................................... 10

SUMMARY OF SIGNIFICANT FINDINGS ............................................................................................... 11

GOVERNANCE MATTERS ......................................................................................................................... 11

Non-Preparation of Financial Statements of the Consolidated Fund and Public Funds for the

Fiscal Years 2008/09 and 2009/10 ........................................................................................................ 11

Internal control operating within ministries and agencies of GOL .................................................... 11

Control Environment ................................................................................................................................ 11

Code of Conduct ....................................................................................................................................... 12

Disaster Recovery Plan or Business Continuity plans ......................................................................... 12

Human Resource Policies ........................................................................................................................ 12

Staff Performance Evaluation ................................................................................................................. 13

Risk Assessment Process......................................................................................................................... 13

Information and Communication ........................................................................................................... 13

Control activities ....................................................................................................................................... 13

Monitoring ................................................................................................................................................. 14

Internal Audit function............................................................................................................................. 14

REVENUES OF THE CONSOLIDATED FUND ......................................................................................... 14

Consolidated Fund, Cash and Bank: Current composition of the Consolidated Fund .................... 14

Non-Distinction among accounts constituting the Consolidated Fund ............................................. 15

Monitoring and control of Consolidated Fund Accounts ..................................................................... 15

Consolidated Fund balance reported as at the close of 2008/9 and 2009/10 fiscal years ........... 15

Effects of application of MOUs entered into by MOF with other parties. ........................................ 16

Duties and Taxes from International Trade ......................................................................................... 16

Fees from Real Property .......................................................................................................................... 17

Revenue from Motor Vehicles................................................................................................................. 18

Maritime Revenue .................................................................................................................................... 19

Grants and Aid .......................................................................................................................................... 20

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

6 Promoting accountability, transparency, integrity and fiscal probity

EXPENDITURES OF THE CONSOLIDATED FUND ................................................................................ 21

Statement of Accountability .................................................................................................................... 22

AUDITOR-GENERAL’S OPINION ON THE 2008/9 AND 2009/10 FISCAL OUTTURNS .................... 22

Basis of Disclaimer Opinion .................................................................................................................... 22

Auditor-General’s Disclaimer Opinion .................................................................................................... 23

DETAILED REPORT .................................................................................................................................. 24

Introduction............................................................................................................................................... 24

MOF Responsibility ................................................................................................................................... 24

Audit Objectives ........................................................................................................................................ 26

Audit Scope and Methodology ................................................................................................................ 27

Limitation of Responsibility ..................................................................................................................... 27

Scope Limitation ....................................................................................................................................... 28

Internal Control Operating in Ministries and Agencies of GOL .......................................................... 32

Control Environment ................................................................................................................................ 33

Disaster Recovery Plan or Business Continuity Plans ......................................................................... 35

Human Resource Policies ........................................................................................................................ 36

Staff Performance Evaluation ................................................................................................................. 37

Risk Assessment Process......................................................................................................................... 38

Information And Communication ........................................................................................................... 38

Control Activities ....................................................................................................................................... 39

Monitoring ................................................................................................................................................. 40

Internal Audit Function ............................................................................................................................ 40

Audit Planning ........................................................................................................................................... 41

REVENUES OF THE CONSOLIDATED FUND ......................................................................................... 42

Consolidated Fund, Cash and Bank: Current composition of the Consolidated Fund .................... 42

Non-Distinction Among Accounts Constituting the Consolidated Fund ............................................ 46

Monitoring and Control of Consolidated Fund Accounts .................................................................... 47

Consolidated Fund Balance as at the Close of 2008/9 and 2009/10 Fiscal Years .......................... 51

Opening and Monitoring of Transitory Accounts ................................................................................. 53

Effects of Application Of MOUs Entered Into by MOF With Other Parties ....................................... 56

Duties and Taxes From International Trade ........................................................................................ 59

Inordinate delays in payment of GOL share of BIVAC Inspection Fees ........................................... 59

Under-Assessment of Imports and Non-Recovery of Related Penalties And Forfeitures .............. 60

Validation of Fiscal Outturns’ Representations on Duties and Taxes on International Trade ...... 64

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

7 Promoting accountability, transparency, integrity and fiscal probity

Fees From Real Property ......................................................................................................................... 65

Non-Maintenance of Databases on Real Properties in Liberia ........................................................... 65

Non-Compliance With Provisions of the Revenue Code in the Assessment Of Real Property by

RETD .......................................................................................................................................................... 68

Penalty and Interest Not Appropriately Charged on Late Payment of Taxes Assessed ................ 71

Inadequate Records Maintained on Personnel Files ........................................................................... 73

Variance Between Tax Collected/Paid and that of the Fiscal Outturn Reports For 2008/9 And

2009/10 ..................................................................................................................................................... 75

Revenue From Motor Vehicles ................................................................................................................ 77

Maintenance of Databases on Taxpayers by Divisions of MOT ......................................................... 77

Time it Took Taxpayers to Register Motor Vehicles and Obtain License Plates ............................. 79

Documentation Underpinning Fees Collected by the MOT Divisions And Reconciliation of the

Fees Collected With MOF and CBL......................................................................................................... 80

Land and Rail Division ............................................................................................................................. 81

Vehicle Dealership .................................................................................................................................... 81

Garages ...................................................................................................................................................... 81

Transport Unions ...................................................................................................................................... 82

Operations Undertaken by the Insurance Division of MOT ............................................................... 83

Representations Contained in the Fiscal Outturns For 2008/9 And 2009/10 For Revenue Derived

From MOT Operations ............................................................................................................................. 85

Maritime Revenue .................................................................................................................................... 86

Small Watercraft Fund ............................................................................................................................. 86

Analysis of Fiscal Outturns, LMA Remittance & Revenue Report, DCRARS Report and CBL

Revenue Bank Statements ...................................................................................................................... 89

Minister of Finance Response ................................................................................................................. 92

Direct, Payroll and Business Profit Taxes ............................................................................................. 92

Penalty for failure to file and failure to pay taxes ............................................................................... 92

EXPENDITURES OF THE CONSOLIDATED FUND ................................................................................ 98

Policies and Procedures ......................................................................................................................... 107

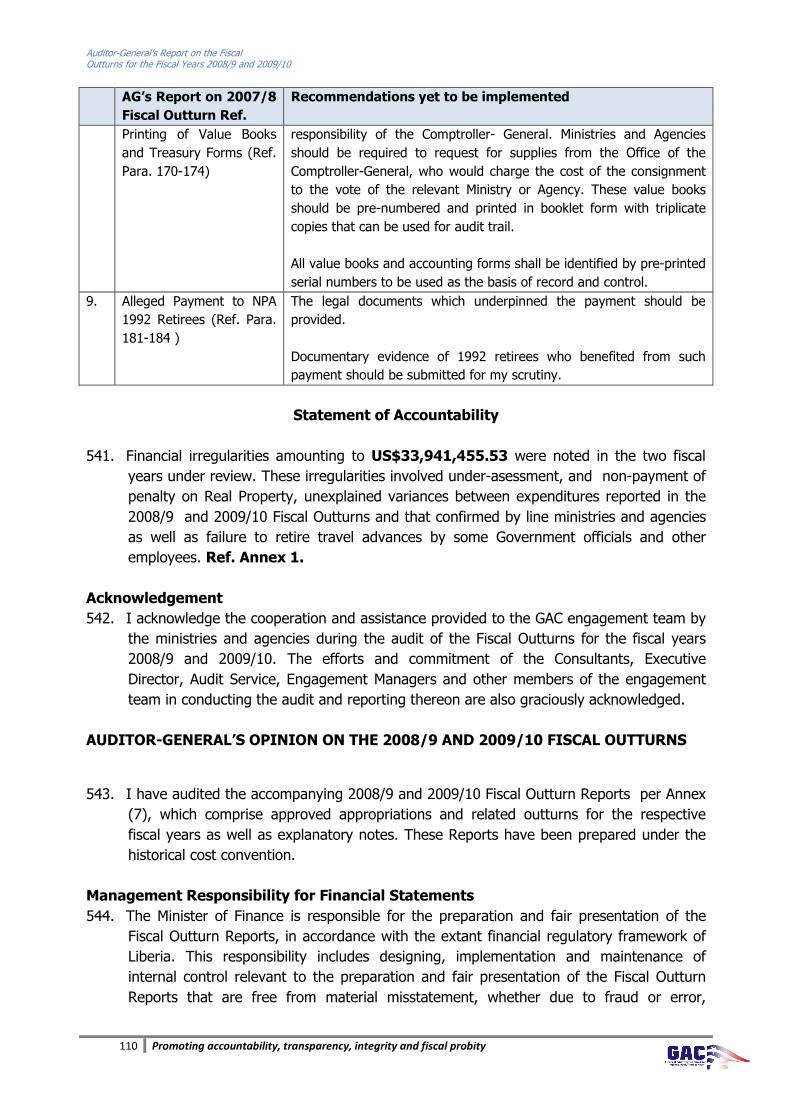

Acknowledgement .................................................................................................................................. 110

Management Responsibility for Financial Statements 110

Basis of Disclaimer Opinion .................................................................................................................. 111

Auditor-General’s Disclaimer Opinion .................................................................................................. 112

Accountability Schedule (Annex 1)………………………………………………………………………………….113

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

8 Promoting accountability, transparency, integrity and fiscal probity

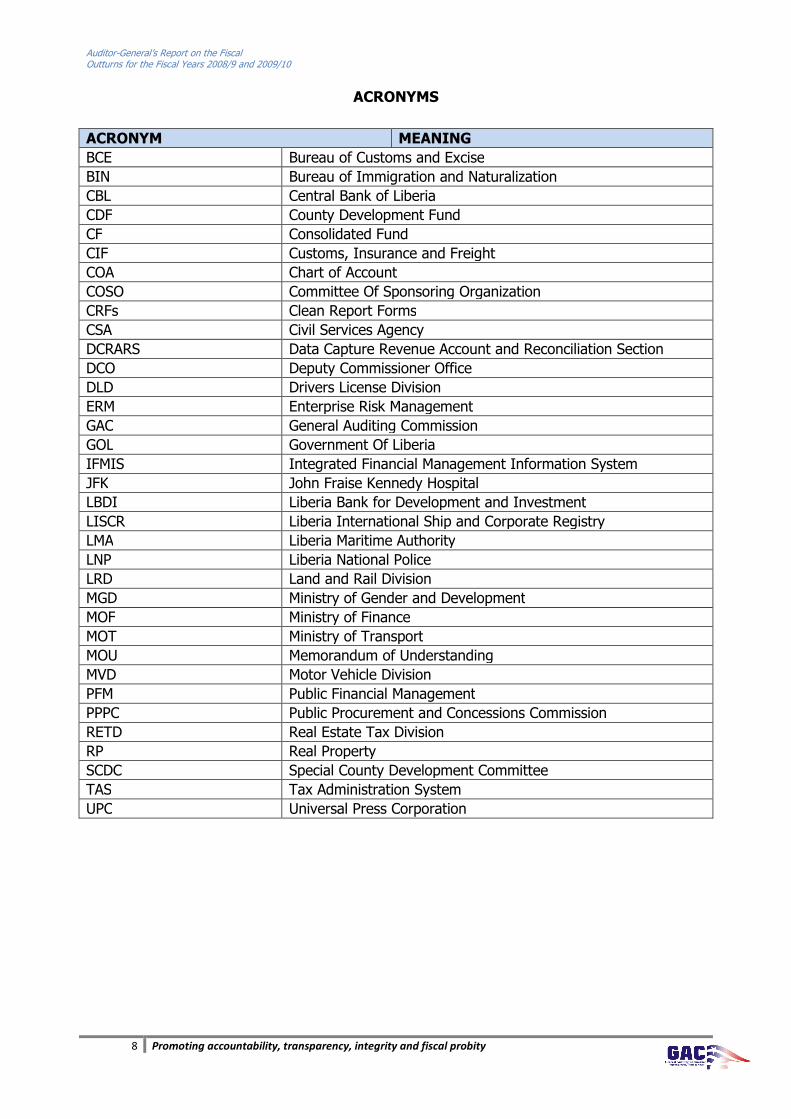

ACRONYMS

ACRONYM MEANING

BCE Bureau of Customs and Excise

BIN Bureau of Immigration and Naturalization

CBL Central Bank of Liberia

CDF County Development Fund

CF Consolidated Fund

CIF Customs, Insurance and Freight

COA Chart of Account

COSO Committee Of Sponsoring Organization

CRFs Clean Report Forms

CSA Civil Services Agency

DCRARS Data Capture Revenue Account and Reconciliation Section

DCO Deputy Commissioner Office

DLD Drivers License Division

ERM Enterprise Risk Management

GAC General Auditing Commission

GOL Government Of Liberia

IFMIS Integrated Financial Management Information System

JFK John Fraise Kennedy Hospital

LBDI Liberia Bank for Development and Investment

LISCR Liberia International Ship and Corporate Registry

LMA Liberia Maritime Authority

LNP Liberia National Police

LRD Land and Rail Division

MGD Ministry of Gender and Development

MOF Ministry of Finance

MOT Ministry of Transport

MOU Memorandum of Understanding

MVD Motor Vehicle Division

PFM Public Financial Management

PPPC Public Procurement and Concessions Commission

RETD Real Estate Tax Division

RP Real Property

SCDC Special County Development Committee

TAS Tax Administration System

UPC Universal Press Corporation

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

9 Promoting accountability, transparency, integrity and fiscal probity

EXECUTIVE SUMMARY

Background

1. I present this report on the Fiscal Outturns of the Republic of Liberia for the fiscal years

2008/9 and 2009/10, as required under Section 37(5,6), PFM Act; this being the third

audit conducted by the GAC on the respective Fiscal Outturns of the Republic of Liberia

in accordance with the provision of Chapter 53.3 of the 1972 Executive Law of Liberia.

The audit was commissioned on February 28, 2011 and completed on July 29, 2011.

2. Section 37(1,2), Public Financial Management (PFM) Act of 2009, mandates the

Minister of Finance to prepare the un-audited Final Account of the National Budget and

submit it to the Auditor General no later than four (4) months after the end of the fiscal

year. Section 37(5,6) of the PFM Act, requires me to review the Final Account of the

National Budget produced by the Minister of Finance and forward an audit report, along

with the Final Account, to the Legislature no later than four (4) months after receipt of

the un-audited Final Account from the Minister.

3. Additionally, Regulation I.12 of the PFM Regulations, 2009, requires the Comptroller-

General, within a period of four months after the end of each fiscal year, or such other

period as the Legislature may by resolution appoint, to prepare the Annual Accounts of

the Consolidated Fund (CF) for the Minister’s transmittal to the Auditor-General.

Furthermore, Regulation I.13 of the PFM Regulations, requires the Comptroller-General

to prepare, within a period of four months or such other period as the Legislature may

by resolution appoint, prepare Annual Accounts of the Public Fund for the Minister’s

transmittal to the Auditor General. The Annual Public Accounts shall not be prepared

only where there are no other funds established outside the Consolidated Fund.

4. The above statutory provisions mean that, commencing 2009/10, the Minister of

Finance is mandated to issue three (3) financial reports to the Auditor-General for

review, certification and submission to the National Legislature for the fiscal year then

ended. These reports are:

i. Un-audited Final Account of the National Budget (Ref. Section 37(1,2),

PFM Act, 2009);

ii. Annual Accounts of the Consolidated Fund (Ref. Regulation I.12, PFM

Regulations, 2009); and

iii. Annual Accounts of the Public Fund (Ref. Regulation I.13, PFM

Regulations, 2009).

5. The MOF compiled the Fiscal Outturns for the fiscal years 2008/9 and 2009/10 and

submitted to me for purposes of my audit, instead of Financial Statements of the

Consolidated Fund and Public Fund for 2008/09 and 2009/10 fiscal years. It was after

the issuance of the Draft Auditor-General’s Report on the fiscal outturns for 2008/9

and 2009/10, Ministry of Finance submitted Financial Statements of the Consolidated

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

10 Promoting accountability, transparency, integrity and fiscal probity

Fund of Liberia for the fiscal year ended June 30, 2010, compiled on IPSAS cash basis

accounting, to GAC on November 21, 2011. Thus, the submission of the Financial

Statements comes some twelve (12) months after the deadline stipulated by the extant

regulatory framework.

6. GAC’s enabling enactment – i.e. Executive Law of 1972. Section 53(7) of the Executive

Law requires me to call the attention of the National Legislature to any officer or

employee who has wilfully or negligently failed to collect or receive monies belonging to

the Government; any public monies not duly accounted for and paid into an authorized

depository; any appropriation that was exceeded or applied to an account; any

deficiency or loss through fraud, default, or mistake of any person; and inadequate or

ineffective internal control of public monies and assets. I am also required to include in

my report, where appropriate, recommendations for executive action or legislation

deemed necessary to improve the receipt, custody, accounting and disbursement of

public monies and other assets.

7. My audit was conducted in accordance with the requirements of the International

Standards on Auditing of Supreme Audit Institutions (ISSAIs). These standards require

me to plan and perform the audit so as to obtain reasonable assurance whether the

Fiscal Outturns are free of material misstatement. The audit thus involved reviews as

would enable me to appropriately report on the attainment of the audit objectives.

8. The outcomes from my review were conveyed through Audit Observation Memoranda

(AOMs) to respective desk officers, their supervising officers and line Ministers, whose

comments to my findings, where provided, were evaluated in arriving at my

conclusions. Thereafter, a Draft Report incorporating all the unresolved findings was

submitted to the Minister of Finance for his response. This report thus, where

appropriate, encompassed responses received from the Minister.

Limitation of Responsibility

9. I reviewed the systems and management controls operated by the Ministries and

Agencies only to the extent I considered necessary for the effective performance of this

audit. As a result, my review may not have detected all weaknesses that existed or all

improvements that could have been made.

Scope Limitation

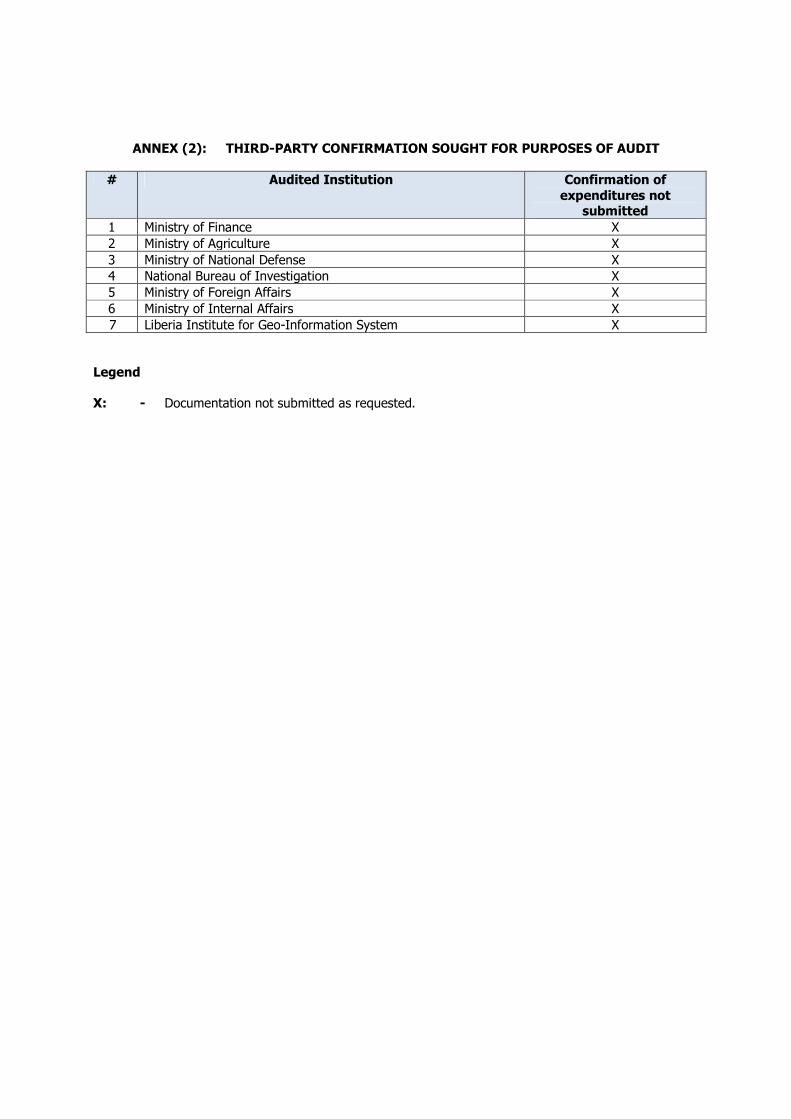

10. My audit scope was limited by the fact that seven (7) of the Ministries and Agencies did

not provide confirmation of funds received and disbursed during the periods under

review. The effect of these omissions created uncertainties in the substantiation of

representations contained in the Fiscal Outturns for 2008/9 and 2009/10. Particulars of

the Ministries and Agencies that did not confirm total funds received and disbursed are

provided in Annex (2).

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

11 Promoting accountability, transparency, integrity and fiscal probity

SUMMARY OF SIGNIFICANT FINDINGS

11. I present hereunder, summary of significant findings borne out of my review. For

purposes of brevity, this segment of the report catalogues only noted deviations.

Recommendations proffered to address the significant findings are provided in the

detailed report.

GOVERNANCE MATTERS

Non-Preparation of Financial Statements of the Consolidated Fund and Public Funds

for the Fiscal Years 2008/09 and 2009/10

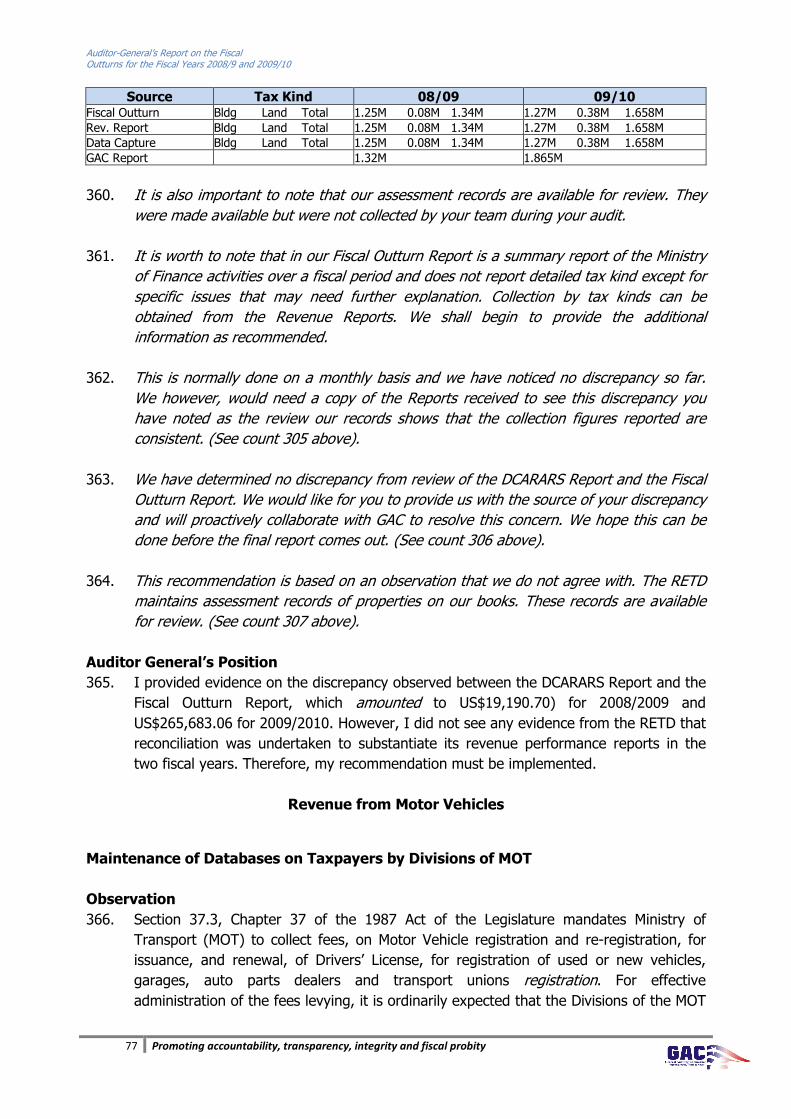

12. Contrary to the requirements of Regulations I.12 and I.13 of the PFM Regulations of

2009, that the Comptroller-General should prepare the Annual Accounts of the

Consolidated Fund and Public Funds for the Minister of Finance’s transmittal to the

Auditor-General within a period of four months after the end of each fiscal year, or such

other period as Legislature may by resolution appoint, for the fiscal years 2008/9 and

2009/10, the MOF did not compile these Annual Accounts. Instead, only the Fiscal

Outturn Reports were compiled for the respective periods.

13. It should be noted that the issue of non-preparation of Annual Accounts of the

Consolidated Fund was conveyed in my report on the 2007/8 Fiscal Outturns submitted

to the Legislature, Executive and the MOF.

14. The Fiscal Outturn Report produced by MOF is deficient in information on the assets,

liabilities and fund balances, and for that matter the report does not portray GOL’s

financial performance, position and cash flows. Thus, stakeholders in Liberia, including

the National Legislature, policy makers, civil society and Liberia’s international partners

as well as the general public would be deprived of crucial information they would

require to assess GOL performance in the area of public financial management.

Internal control operating within ministries and agencies of GOL

15. I reviewed the effectiveness of internal control operating in ministries and agencies of

GOL on the basis of the Committee of Sponsoring Organization of the Treadway

Commission (COSO) framework. The COSO framework is an internal control standard

that sets the benchmark for an effective internal control system. In terms of the

framework, an effective internal control system should consist of five elements which

are, the control environment, risk assessment, information and communication, control

activities and monitoring. Because of the urgency attached to the audit, a limited

number of GOL’s ministries and agency were selected for purposes of the review. The

outcomes from my review of the various elements of internal control on J. F. K.

Hospital, Ministries of Internal Affairs, Public Works and Education are presented below.

Control Environment

16. The COSO internal control framework requires management of any organization to

provide a framework within which the internal control operates. This is set by the tone

of management, its philosophy and operating style, organizational structure, and the

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

12 Promoting accountability, transparency, integrity and fiscal probity

way in which authority is delegated, staff is organized and developed (human resource

policies and procedures) and the commitment of those charged with governance.

17. I did not see evidence that the environment in which the internal controls operated

within Ministries of Internal Affairs, Education and JFK Hospital complied with the

requirements of the COSO framework. This is because these entities were not operating

with an approved organizational structure; had not developed a strategic plan and

operational plan for use in the allocation of resources during the periods under review

and there was no evidence that the entities had developed mission statements

encompassing vision, values and objectives.

18. Lack of approved organizational structure that established a clear line of authority and

responsibility within the institutions denied assurance that the organizations would be

able to assign accountability for the actions of individuals in the entities.

Code of Conduct

19. The COSO framework demands that code of conduct should be established to guide

staff in their conduct or behaviour during the performance of their responsibilities within

each entity. The code must be distributed to all members of staff and on regular basis,

awareness programs should be undertaken to sensitize staff on the code.

20. The Civil Service Agency (CSA) has Standing Orders (i.e. code of conduct) which are

applicable to all ministries of GOL. However, there was no evidence that the Ministers of

Internal Affairs and Education had obtained and distributed the Standing Orders to all

staff in their ministries. There was also no evidence that JFK Hospital’s Management

had developed and distributed a code of conduct to its staff. Staff of entities without

code of conduct may not be aware of acts incompatible with the norms of their

establishments.

Disaster Recovery Plan or Business Continuity plans

21. Management of an entity should draw up a disaster recovery plan to recover

information in the event of loss or mishap. There was no evidence that the Ministers of

Internal Affairs and Education as well as the General Administrator of the JFK Hospital

had disaster recovery plans to help recover transaction data and information and to

ensure business continuity, in the event of mishap.

Human Resource Policies

22. Management of entity must interpret regulations/instructions related to human resource

and establish policies and procedures providing for, among others, regulation of matters

such as orientation, training, promotions, compensation, and experience criteria for

recruiting skilled and competent staff as well as skills retention and monitoring of the

competency of staff. Such policies and procedures must be properly communicated to

all staff.

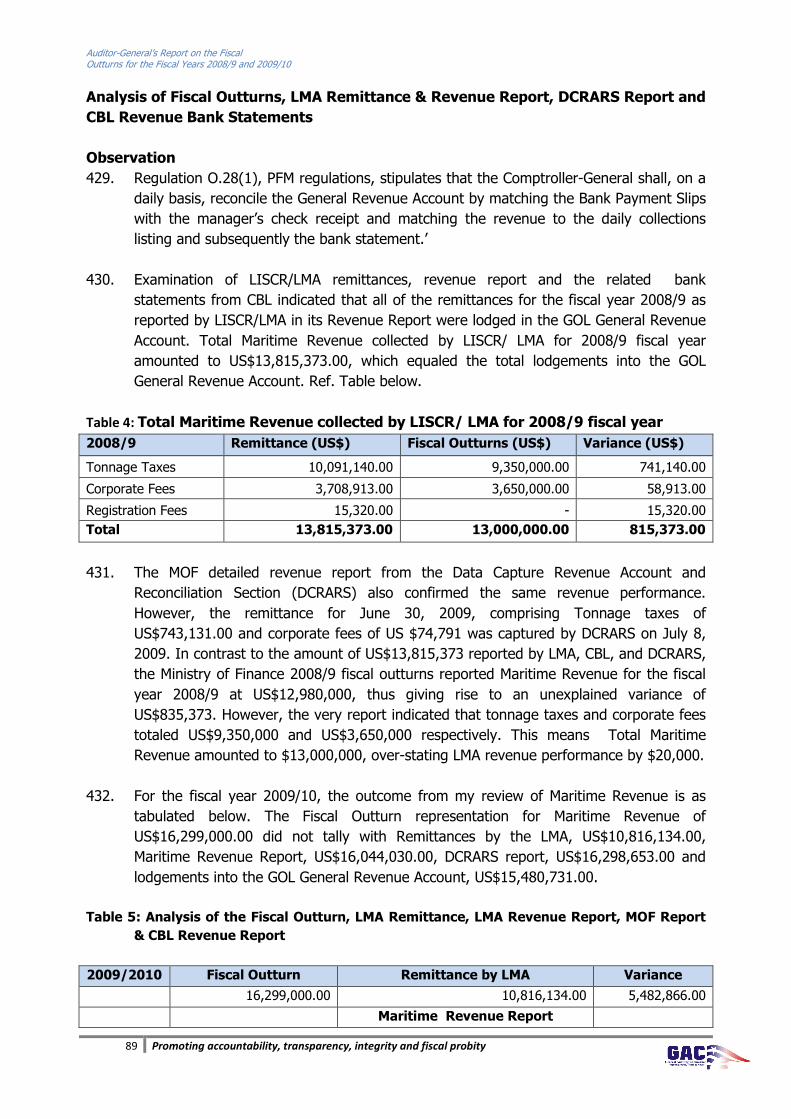

23. However, I did not see evidence that the Ministers of Internal Affairs and Education and

the General Administrator of the JFK Hospital had interpreted relevant regulations and

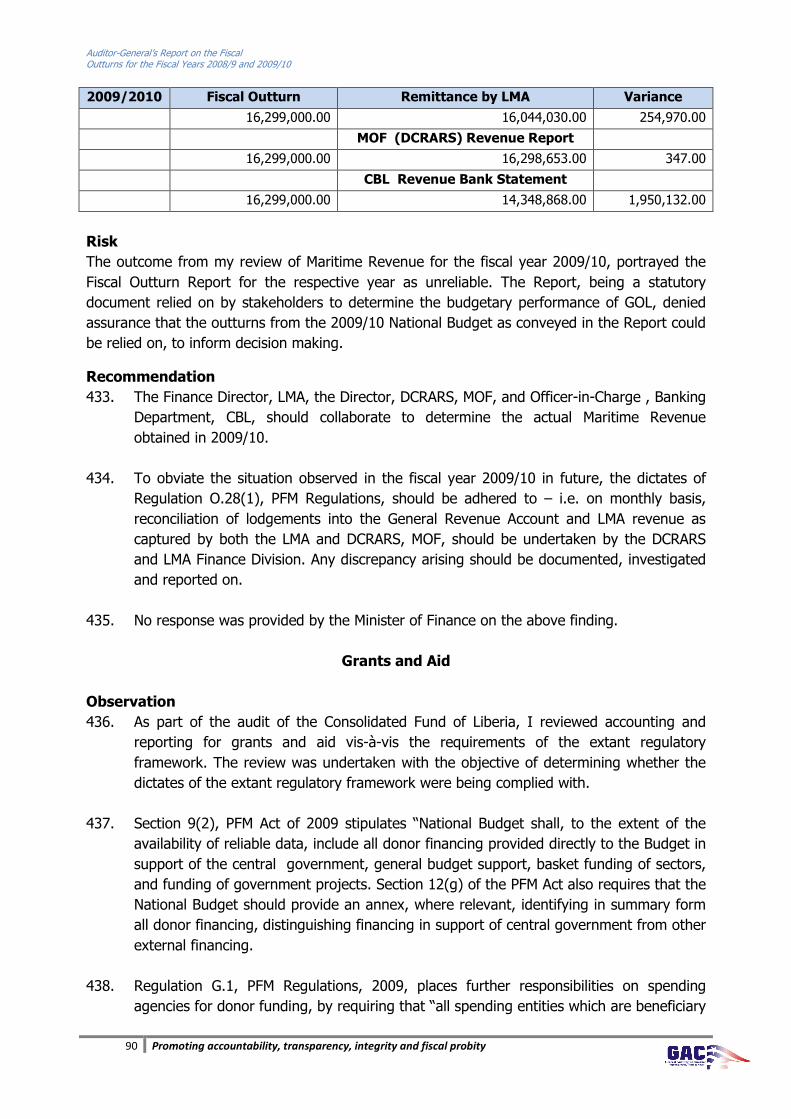

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

13 Promoting accountability, transparency, integrity and fiscal probity

included the requirements in its own documented and approved policies and

procedures. These omissions denied assurance that the entities are using policies and

procedures that do address their unique human resource needs.

Staff Performance Evaluation

24. The COSO framework requires management of an entity to evaluate the performance of

each individual staff on a regular basis. There was however, no evidence that the

Ministries of Internal Affairs and Education as well as the JFK Hospital’s Managements

were conducting performance appraisals of their staff on a regular basis. I could

therefore not ascertain the basis of placement of various staff and how grading and

promotion were done within each entity. Non-conduct of performance appraisal of staff

denied assurance that the entities were aware of staff deficiencies and this may impact

negatively on their ability to deliver quality services.

Risk Assessment Process

25. Managements of entities must establish a risk management policy, which sets the basis

for conducting risk assessment within the entities. Risk assessment process entails

identifying and analysing the risk that may impact negatively on the achievement of

each entity’s objectives. However, my review of some selected Ministries and Agencies

did not see evidence that the Ministers of Internal Affairs and Education as well as the

General Administrator of the JFK Hospital had developed a risk management policy and

were conducting risk assessment procedures that enable the entities to identify risk and

formulate mitigating strategies to the risk. Prevalence of the above omission may

impact the entities’ ability to provide quality service.

Information and Communication

26. The COSO framework requires that institutions must produce accurate and timely

information and communicate it to the stakeholders, such as the Legislature, GAC,

international partners, and their clients, on a regular basis, as required under extant

regulatory framework. This requirement was not being complied with by the Ministers of

Internal Affairs and Education as well as the General Administrator, JFK Hospital. Failure

to provide periodic reporting as required under extant regulatory framework would deny

stakeholders of these institutions valuable information needed for informed decision-

making.

Control activities

27. Under the COSO framework, institutions must interpret relevant financial regulations

and develop its own written policies and procedures, to enable it to be effective in the

management of key processes of each entity. The policies and procedures should be

able to guide staff in key processes such as recording, utilization of the entity’s

resources, reporting and monitoring.

28. There was no evidence that the Ministers of Internal Affairs and Education and the

General Administrator, JFK Hospital had interpreted their regulations to develop policies

and procedures (i.e. operational manual) to guide key processes in areas such as

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

14 Promoting accountability, transparency, integrity and fiscal probity

accounting, human resource and other resource utilization operations. This omission

could lead to waste, commissioning of errors and pursuit of ill-advised activities by staff.

Monitoring

29. Management of an entity should establish procedures that ensure regular monitoring of

internal controls and other activities within the entity, in order to identify control

deficiencies within a reasonable time. Internal auditors play an important role in

evaluating the effectiveness of control systems. However, the Ministers of Internal

Affairs and Education as well as the General Administrator, JFK Hospital had not

established procedures to monitor the effectiveness of internal controls on a regular

basis. There was no evidence that the internal audit units of the entities had produced

any reports regarding the effectiveness of internal controls operating in their respective

institutions. Prevalence of the above situation may result in waste, error and/or abuse in

institution’s operations. This is because management may not be aware of the

deficiencies within its operations.

Internal Audit function

30. Internal Auditing Standard 1000 stipulates that the purpose, authority, and

responsibility of the internal audit activity must be formally defined in an internal audit

charter, consistent with the Definition of Internal Auditing, the Code of Ethics, and the

Standards. There was no evidence that the internal audit units in the Ministries of

Internal Affairs, Education and the JFK Hospital were operating under respective

internal audit charter. The above omission denied assurance that these entities’ internal

audit units did know their roles and responsibilities and understand the scopes of their

work.

REVENUES OF THE CONSOLIDATED FUND

Consolidated Fund, Cash and Bank: Current composition of the Consolidated Fund

31. Despite the requirements of Regulations B.2, H.6(1), PFM Regulations, of 2009, and

Section 34(4), PFM Act, that the CF shall comprise specified inflows, Operations

Accounts of ministries and agencies, Transitory Accounts and Accounts of Liberia

Foreign Missions, my review from both the perspectives of the CBL and Comptroller and

Accountant-General indicated that the CF, as currently constituted, comprised five (5)

main accounts, namely Central Revenue Account (USD), Central Revenue Account (LD),

Operation Account (USD), Operation Account (LD) and Payroll Account (LD).

32. No subsidiary accounts for each of the main inflows of the Bureaus of Customs and

Excise and Internal Revenue and other agencies’ collections as well as subsidiary

accounts for the Operations and Payroll Accounts were maintained, to facilitate

monitoring and reconciliation. The CF accounts maintained by Data Capture Revenue

Accounts and Reconciliation Section (DCRARS) of the MOF, and accounts maintained by

the CBL for the CF did not coincide. This is contrary to the dictates of Regulation H.6

(f), PFM Regulations, that the CF accounts maintained by the CBL and the Comptroller

and Accountant-General should follow the same classifications as prescribed in the

government’s Chart of Accounts.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

15 Promoting accountability, transparency, integrity and fiscal probity

33. For effective determination of CF balance, monitoring and reconciling inflows and

outflows of the Fund, the CF, as currently constituted, is not adequate. The non-

provision of subsidiary accounts for the five main accounts, into which main inflows and

outflows would first hit before being transferred into the five main accounts, would

prohibit effective determination of CF balance, monitoring, reconciliation and control of

the Fund.

Non-Distinction among accounts constituting the Consolidated Fund

34. Funds of the CF are not being managed in a fashion whereby distinction is drawn

between funds that are committed and uncommitted. Uncommitted Accounts are

accounts whose funds are available to support the National Budget, whilst Committed

Accounts are those earmarked for specific purposes. The current approach for

managing the CF could result in earmarked funds being applied for purposes not

intended. Such misapplication could embarrass GOL, when it happens, causing

donors/development partners of Liberia to lose trust in the GOL, thus putting in

jeopardy subsequent inflows from the donors/development partners.

Monitoring and control of Consolidated Fund Accounts

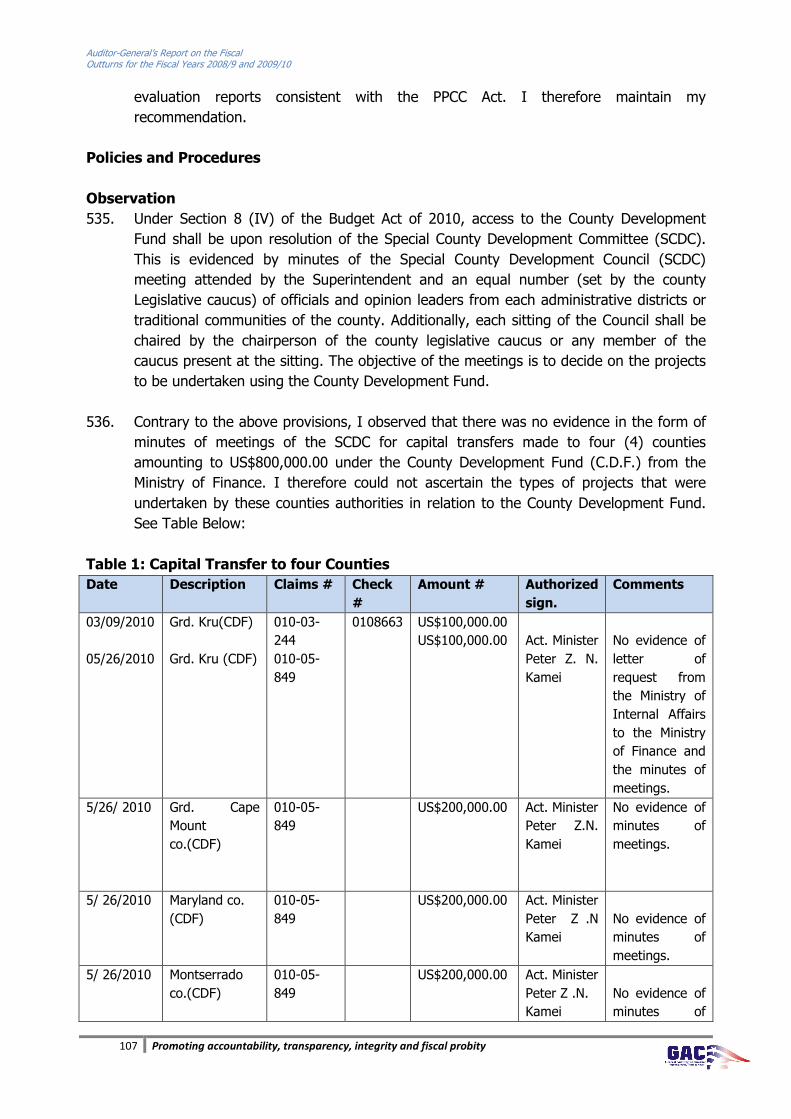

35. I did not sight evidence of monitoring of the CF accounts by both MOF and CBL, to

provide assurance on regularity of dealings on the accounts. I noted that the

reconciliation of collections and lodgements undertaken by DCRARS was ineffective

because of a number of factors. Significant among these factors being the non-

maintenance of definitive listing of subsidiary accounts underpinning the GOL’s General

Revenue Accounts that the daily collections captured by the Section can be compared.

The Section neither undertakes reconciliation on daily basis. Though the monthly report

of DCRARS matches GOL daily collections as captured by the Section against daily

lodgements at CBL, these were no near reconciling. On daily basis, significant variances

between collections and lodgements were recorded and there was no indication that

these variances were reconciled daily. The control period of one month observed, within

which the DCRARS reconciles revenue collections with lodgements into the CF at the

CBL, is inordinately long. Other factors contributing to the ineffective monitoring and

reconciliation of the CF accounts are expatiated on in the detailed report. Ineffective

monitoring and control of subsidiary accounts statutorily constituting the CF could limit

funds considered available on the CF for disbursement on GOL’s programs.

Consolidated Fund balance reported as at the close of 2008/9 and 2009/10 fiscal

years

36. The Fiscal Outturns for 2008/9 and 2009/10 reported respectively uncommitted CF Cash

balances of US$1.6 million and US$10.73 million at the close of the respective fiscal

years. These balances were arrived at on the basis of the five main accounts of the CF,

as currently constituted, as well as the dictates of Regulation B.26 (2), PFM Regulations,

which stipulates that “any unpaid balances on commitments will also lapse at the end of

the year, unless goods and services have already been delivered, in which case,

settlement must be made within 90 days after the end of the fiscal year”. The CF

balances of the two fiscal years under review thus excluded balances of Transitory

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

16 Promoting accountability, transparency, integrity and fiscal probity

Accounts, Accounts of Liberia Foreign Missions and those of operations accounts of

ministries and agencies of GOL.

37. Another factor impacting the determination of the CF Balance was the change in

accounting basis – i.e. from commitment basis in 2007/8 to cash basis in 2008/9 and a

further change in 2009/10 to “Budget Cash Expenditures’’. The change from one

accounting basis to another was not annotated, to give indication of what the CF cash

position would have been but for the changes.

38. As the CF Cash Positions at the close of 2008/9 and 2009/10 fiscal years were based

only on the CF’s five main accounts (i.e. GOL General Revenue Accounts, Operations

Accounts and Payroll account), to the exclusion of other balances of transitory accounts,

accounts of Liberia Foreign Missions and those of operations accounts of Ministries and

Agencies of GOL, the CF Cash Positions reported in the respective Fiscal Outturn

Reports were not valid.

Effects of application of MOUs entered into by MOF with other parties.

39. The MOF entered into three Memorandum Of Understandings (MOUs). The first MOU

was entered into with EcoBank (Liberia) Limited and Ministry of Transport; the second

MOU was entered into with Liberia Bank for Development and Investment (LBDI) and

Ministry of Labour and the third MOU was entered into with LBDI and Bureau of

Immigration and Naturalization (BIN). Under the MOUs, the banks involved pre-financed

specified quantum of Assorted License Plates and value books production under

contracts with Monrovia Development and Management Corporation (MDMC) and

Universal Press Corporation of Liberia (UPC). Thus, for every payment made by the

public for a license number plate or value book (i.e. permits, stickers etc), the GOL,

banks and other parties involved would receive portion of the specified fees paid.

40. I found the provisions in the MOUs so elaborate that they expose GOL collections to

risks. This is because, by the dictates of the MOUs, funds supposedly paid into the CF,

as acknowledged by issuance of Treasury Counterfoil/Flag Receipts, are deducted

before lodgement into the Fund. As what is paid into the CF is not what accrues to the

CF, GOL collections cannot be reconciled with lodgements into the CF, and that is the

position that pertains currently.

Duties and Taxes from International Trade 41. BIVAC, Liberia, failed to subscribe to a provision in its contract with GOL that

government share of pre-shipment fees shall be brought to the account at the end of

the calendar month and paid within 10 working days to the GOL. Fees due GOL and

subjected to delays before transfer were US$297,552.11 and US$702,783.14 for 2008/9

and 2009/10 respectively. The delays observed between the due dates of payment and

actual dates of payment ranged from one (1) to twenty-eight (28) days.

42. Though the Post Clearance Audit Unit of BCE duly reported the under-assessments of

taxes on goods imported into Liberia and consequent additional taxes payable, the

requirements of Section 1608(c), Revenue Code of Liberia (2000,) were not fully met.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

17 Promoting accountability, transparency, integrity and fiscal probity

This is because Penalty of L$ 200,000.00 required by this Revenue Code provision to be

levied on each defaulting importer was not effected. Of the 757 defaulting importers

noted, the required penalty was levied on 146. Total required penalty amounted to L$

151,400,000.00, but L$ 29,200,000.00 was levied. Also, though the goods which were

the subject matter of the under-assessments are required to be forfeited, this was not

done. No evidence was sighted that consideration was given to the idea of

implementing this requirement. The total CIF value of the goods involved was

US$17,586,705.40. Ref. Annex (3).

43. Because of significant risk impacting the integrity of revenue assessed and collected by

the BCE and the urgency attached to the completion of this report, I have instructed the

Forensic Audit Department of GAC to conduct thorough investigation into each of the

cases of the defaulting importers.

44. Limited documentation was provided by the BCE on its operations within the fiscal years

2008/9 and 2009/10. As a result, I could not substantiate the representation in the

respective Fiscal Outturns that US$88.546 million and US$91.835 million respectively

were derived from Duties and Taxes from International Trade during the fiscal years.

Fees from Real Property

45. Section 2003, Revenue Code of Liberia, 2000, requires that, at the minimum, the Real

Property Assessment Record Books (i.e. databases on Real Property) should be

maintained on all Real Property (RP) in Liberia. The Real Property Assessment Record

Books, according to the provision, should provide for location, area, lot number

designation, any use classification, date of inspection of Real Property for the purpose

of determining its market value, its assessed value and annual tax assessed thereon.

The Real Estate Tax Division, MOF, was yet to maintain these databases. The non-

maintenance of the databases made it impossible to determine the extent to which all

RPs subject to tax were levied in the fiscal years 2008/9 and 2009/10. This omission

denied assurance that all RPs in Liberia that qualified to be assessed for tax were

assessed in the periods under review.

46. Bills issued by the RETD in the fiscal years 2008/9 and 2009/10 did not contain such

documentation as required for effective assessment of the properties involved. Also, the

RETD did not comply with Sections 2001(b) and 2004 of the Revenue Code of Liberia

2000, in that there were no indications that RPs were assessed and their assessed

values informed tax assessments made on the related RPs. The five-year term provision

which demands that RPs, once assessed for value, those values should be kept on the

Real Property Assessment Record Books and informed assessments made on the related

RPs, was neither evident. The requirement that after the expiration of the five-year

term, there should be re-assessment of RPs values for purposes of taxation was neither

adhered to. Owners of RPs did not file prescribed schedule providing all relevant details

of their properties after acquisition, as stipulated. These omissions denied assurance

that assessments made on RPs were as required under extant regulations.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

18 Promoting accountability, transparency, integrity and fiscal probity

47. Sections 11 and 2002 of the Revenue Code of Liberia (2000) stipulate that penalty and

interest shall be assessed and added to the tax due or to any underpayment thereof if

such tax is not paid from January 1 to July 31 of the year in which it is levied. However,

I noted that penalty and interest charged for late payments in the fiscal years under

review were not in keeping with this requirement. In some instances, penalty and

interest were calculated below or above the required rate. As a result, for 2008/9 fiscal

year, total penalty and interest charged by the RETD was US$18,820.00 as opposed to

US$86,012.00, required under the above quoted provisions. GOL thus forfeited

US$67,192.00.

48. The RETD is charged with responsibility to assess and collect taxes on RPs across the

fifteen counties of Liberia. Personnel files of 18 personnel assigned to the RETD as well

as the Division’s work plans and extent of attainment of these plans for the periods

under review, were not provided to me so as to permit the determination of the

effectiveness of the RETD. The absence of those documentation denied assurance that

its personnel possessed the requisite competencies for the Division’s functions.

49. Limited documentation was provided by the RETD on its operations within the fiscal

years 2008/9 and 2009/10. As a result, I could not substantiate the representations in

the respective Fiscal Outturns that US$2,940,000.00 respectively was derived from Fees

on RPs during the two fiscal years under review.

Revenue from Motor Vehicles

50. MOT is mandated under Section 37.3, Chapter 37 of the 1987 Act of the Legislature to

collect fees, on Motor Vehicle registration and re-registration, for issuance, and renewal,

of Drivers’ License, for registration of used or new vehicles, garages, auto parts dealers

and transport unions registration. For effective administration of the fees levying, it is

ordinarily expected that the Divisions of the MOT charged with the administration of

these fees, would maintain respective databases on their taxpayers. Of the four

Divisions of MOT, Motor Vehicle Division (MVD) and Drivers’ License Division (DLD)

maintained a limited database on their taxpayers. The other two Divisions, Land and

Rail (LRD) and Insurance Divisions, did not have database on its taxpayers. There was

no evidence that collection of fees by the MVD and DLD was informed by their existing

databases.

51. My review of 38 applications for license number plates selected at random indicated

that it took between one (1) and eight (8) months for vehicle owners to obtain their

license number plates after registration, and on the average, a duration of 3.91 months

for each one of the 38 vehicles involved to obtain the license plates. Contrary to this

observation, the MVD Director indicated that it took on the average three to four (3-4)

days to obtain the number plate, after an application for registration. Delays in

submission of license plates to motor vehicles owners meant that those registered

motor vehicles would be on the roads in Liberia without license number plates. Such a

situation constitutes a serious risk to public security and safety.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

19 Promoting accountability, transparency, integrity and fiscal probity

52. The Divisions of the MOT, namely MVD, DLD, Land and Rail and Insurance Divisions,

did not provide me the documentation underpinning the fees the Divisions collected

during the fiscal years 2008/9 and 2009/10. The non-submission of the documentation

denied assurance that fees charged taxpayers during the periods under review were

those required, as stipulated in the extant regulatory framework. The implication is that

GOL might not have derived the required fees for the fiscal years under review.

53. The Commissioner of Insurance (i.e. the Head of the Insurance Division/Bureau, MOT)

is required to enforce the registration of insurance firms operating in Liberia. Under the

Administrative Regulation PG/ NO. 002/82997 Section 4.1, the Insurance Bureau is also

required to ensure that all motor vehicles, bikes and other specified categories of assets

are covered, at the minimum, by third-party insurance. My review did not indicate that

the Commissioner of Insurance was enforcing the provisions of the Division’s regulatory

framework. The Division neither maintained documentation on its activities.

54. The non-enforcement of the provisions of the Revised Insurance Act of 1973, Section

5.5 (E), constitutes a significant violation, as by these omissions, the Commissioner of

Insurance is not informed on the regularity of insurance firms’ operations in Liberia, the

extent of compliance with the requirement that all insurance firms must renew their

operating license annually and whether fees authorized to be paid by MOF were duly

accounted for in the periods under review. Another significant risk occasioned by the

omissions of the Insurance Division is that motor vehicles, bikes and other categories of

assets required to be insured are currently left uncovered with insurance. The

implication is that currently, those assets are exposed to risks such as accidents and

other unpredictable events without the prospects of retrieving them after the events.

55. Limited documentation was provided by the MOT Divisions on their operations within

the fiscal years 2008/9 and 2009/10. As a result, I could not substantiate the

representation in the respective Fiscal Outturns that US$2,151,148.01 and

US$2,614,025.76 respectively were derived from Motor Vehicles during the fiscal years

under review.

Maritime Revenue

56. The Liberia Maritime Authority (LMA) did not undertake periodic reconciliation of its

revenues remitted to the GOL Revenue Accounts from its operations, contrary to the

dictates of Regulation 8, MOF Administrative Regulation No. PFMA-01/MOF/R/02 2010,

Regulation O.28 (1), PFM Regulations, as well as Regulation O.1.(1,2), PFM Regulations.

These categories of revenue are the tonnage taxes, cooperate fees, surplus from the

Deputy Commissioner Office’s operation (DCO’s) and the small watercraft fund. The

LMA justified its stand on the non-reconciliation on the grounds that it is the Ministry of

Finance responsibility to reconcile account(s) for all monies paid into the Consolidated

Fund. Non-reconciliation of remittances notified to the LMA from DCO and LISCR

operations with lodgements effected into the GOL Revenue Accounts denies assurance

that all earnings from LMA’s operations were accounted for.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

20 Promoting accountability, transparency, integrity and fiscal probity

57. For the fiscal year 2009/10, my review indicated that Maritime Revenue of

US$16,299,000.00 reported in the respective Fiscal Outturn did not tally with

Remittances by the LMA, US$10,816,134.00, Maritime Revenue Report,

US$16,044,030.00, DCRARS report, US$16,298,653.00 and lodgements into the GOL

General Revenue Account, US$15,480,731.00. In other words, there were

inconsistencies noted with reports generated from different sources on the Maritime

Revenue. The outcome of my review thus portrayed the 2009/10 Fiscal Outturn Report

as unreliable.

Registration and Assessment of Small, Medium and Large Taxpayers, Payment and

Filing of Turnover Tax Returns, Tax Evasion and Delinquent Taxes

58. Review of 530 taxpayers’ files out of 609 indicated that the BIR failed in many instances

to associate penalties and fines imposed on specific tax kinds and state the taxable

amounts on the basis of which taxes were determined. I observed that about 25

percent of taxpayers, especially those in both small and medium tax categories, whose

files were made available for review, paid taxes far beyond due dates, ranging from one

week to two years. Account statements or revenue detailed reports of tax returns filed

by taxpayers, which listed tax kinds, did not include declaration and period of default

(period between due date and actual date of payment).

59. Also, I noted that taxpayers made declarations of turnover, which did not show

consistent trends over time. These declarations, in my view, smacked of untruthfulness.

Despite these declarations, I did not see evidence that any of the review mechanisms

within the BIR followed up on such taxpayers to ascertain the truthfulness of their

declarations.

60. Additionally, I observed that enforcement provisions were not swiftly applied to

delinquent taxpayers, many of whom are in Monrovia and its environs. For example, in

both fiscal periods, 2008/9 & 2009/10, I noted that 25 taxpayers were delinquent, while

15 were only delinquent in 2008/9 and 36 in 2009/10. BIR did not provide evidence, in

terms of documentation, of prompt enforcement measures against these entities. These

omissions could lead to loss of tax revenue to GOL.

Grants and Aid

61. Spending agencies were not disclosing to the Ministers of Finance and Planning and

Economic Affairs all information related to donor funding not channelled through the

National Budget. Also, I did not sight evidence that the two Ministers had put in place a

mechanism to ensure that all information on grants and aid are gathered, inventoried,

analyzed and reported on. The requirement under the extant regulatory framework for

the Minister of Finance to “maintain a full database of aid flows and produce reports on

statistical records of aid flows data, including progressively bringing off-budget aid flows

onto the budget” neither appeared to have been implemented. I further noted that

neither the Minister of Finance nor the Minister of Planning and Economic Affairs were

in possession of all information on all grants and aid inflows to Liberia, as none of the

Ministers provided same.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

21 Promoting accountability, transparency, integrity and fiscal probity

62. The Fiscal Outturns for 2008/9 and 2009/10 reported grants of US$23,512,814.00 and

US$13,009,000.00 respectively. I observed that the inflows reported in the Fiscal

Outturns were direct budgetary support. However, the National Budgets and Fiscal

Outturns for the two periods did not contain any information on grants and aid that

were not channelled through the Consolidated Fund.

EXPENDITURES OF THE CONSOLIDATED FUND

Variances noted between Expenditures of Government Ministries and Agencies and

that of the Fiscal Outturn Reports for 2008/9 and 2009/10

63. Variances were observed between the Expenditures confirmed by the Ministries and

Agencies as incurred and that conveyed in the Fiscal Outturn Reports for 2008/9 and

2009/10. The variances amounted to US$173,091.83 and US$ 7,905,561.72 for the

respective fiscal years. In addition, there were variances amounting to

US$15,230,876.86 and US$29,135,289.21 for the respective fiscal years on grants and

aid, as reported by the Ministries and Agencies. Details of the variances noted are

expatiated in Annex 6A & B.

64. I also noted that the representations in the Fiscal Outturn Reports for 2008/9 and

2009/10 were not presented showing the details of Expenditures on a line by line item.

Ordinarily, it is required that the representations reported in the Fiscal Outturn Report

should be as detailed as the National Budget, to facilitate analysis. These omissions

denied assurance that financial records underpinning the Consolidated Fund for the two

fiscal years under review were complete and thus, impacted the truth and fairness of

the Fiscal Outturn Reports for 2008/9 and 2009/10.

Un-Supported Expenditures

65. My examination of payment vouchers (PVs) and related supporting documents provided

by the Minister of Finance in relation to Expenditures reported in the fiscal outturns for

2008/2009 and 2009/2010 revealed that Expenditures totalling US$37,201,940.44 and

US$ 10,105,524.80 were not supported by PVs and corresponding supporting

documentation. Details of the variances noted are expatiated on in Annex 5B.

66. Minister of Finance own analysis of the variances reported produced yet another un-

explained variances of US$3,091,113.56 and US$3,954,378.31 for FY 2008/09 and

2009/10, of expenditure unsupported respectively . Ref. Annex 8. On account of the far

reaching nature of the matters raised by MOF on the un-supported expenditures, I have

therefore instructed the GAC Forensic Audit Department to investigate and analyze all

disbursement vouchers, which are the subject of contention by MOF, and all related

matters giving rise to the variances observed.

Failure to account for Foreign Travel Advances paid to Officials of the Ministry of

State (MOS), Ministry of Foreign Affairs (MOFA) and the Ministry of Finance (MOF)

67. Some officials and staff of the Ministry of State & Presidential Affairs, as listed in Annex

(4), failed to submit travel disbursement/settlement form and related travel documents

to retire travel advances totalling US$90,880.00.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

22 Promoting accountability, transparency, integrity and fiscal probity

68. Similarly, also some officials and staff of the Ministries of Finance and Foreign Affairs,

listed in Annexes (4A & 4B) did not submit travel disbursement/settlement form and

related travel documents to account for advances totalling US$208,671.11 and

US$153,664.50 respectively received for their trips. These omissions implied that upon

returning to base, the officials and staff did not account for and report on the foreign

travels and no controls were exercised by the Foreign Travel Section of the Ministry of

Finance, to ensure that the retirement of travel advances were undertaken. Non-

retirement of travel advances could result in non-accountability for travel advances

granted to officials of GOL, thus posing a drain on GOL resources.

Failure to maintain bid documentation and Budget Performance Report

69. Bid documentation supporting Payment Vouchers for works paid by Ministry of Public

Works in 2008/9 and 2009/10 and amounting to US$13,588,598.47 and

US$11,907,460.40 respectively were observed to be absent. Ref. Annex (5A).

Progress reports were neither attached to the Payment Vouchers. I could not therefore

ascertain the validity of the Expenditures incurred by the Ministry of Public Works on

those works.

Status of implementation of prior audit recommendations

70. Recommendations conveyed in my previous report on the 2007/8 Fiscal Outturn were

yet to be implemented. Details of these recommendations are provided in the detailed

report.

Statement of Accountability

71. Financial irregularities amounting to US$33,941,455.53 were noted in the two fiscal

years under review. These irregularities involved under-asessment, and non-payment of

penalty on Real Property, unexplained variances between expenditures reported in the

2008/9 and 2009/10 Fiscal Outturns and that confirmed by line ministries and agencies

as well as failure to retire travel advances by some Government officials and other

employees. Ref. Annex 1.

AUDITOR-GENERAL’S OPINION ON THE 2008/9 AND 2009/10 FISCAL OUTTURNS

Basis of Disclaimer Opinion

72. The following considerations underpinned my opinion on the 2008/9 and 2009/10 Fiscal

Outturn Reports:

i. Variances were noted between the Expenditures confirmed by the Ministries and

Agencies as incurred and respective Expenditures conveyed in the Fiscal Outturn

Reports for 2008/9 and 2009/10. The variances amounted to US$ 173,091.83

and US$7,905,561.72 for the fiscal years 2008/9 and 2009/10 respectively. In

addition, there were variances amounting to US$15,230,876.86 and

US$29,135,289.21 for the respective fiscal years on grants and aid, as reported

by the Ministries and Agencies on one hand, and the Fiscal Outturn reports, on

the other. The variances observed denied assurance that the Fiscal Outurns

Reports for 2008/9 and 2009/10 were reliable.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

23 Promoting accountability, transparency, integrity and fiscal probity

ii. Seven (7) Mnistries and Agencies of GoL, as listed in Annex 2, failed to respond

to my confirmation request to provide information on the Revenues and

Expenditures received and disbursed by them within the fiscal years 2008/9 and

2009/10. As a result of the insufficient evidence had, I was thus not able to

validate representations made in the Fiscal Outturn Reports on Revenue from

Real Property, Duties and Taxes from International Trade, Revenue from Motor

Vehicles, Sales and related Taxes, Direct, Payroll, Bisiness Profit Taxes and

Stumpage and related Taxes as well as the Expenditures of the Minisitries and

Agencies.

iii. 2008/9 and 2009/10 Fiscal Outturn Reports’ representations on Consolidated

Fund Closing Balance as of June 30, 2009 and 2010 were not valid because

other accounts such as Transitory Accounts, Balances on Operations of Ministries

and Agencies and Liberia Foreign Missions Accounts, constituting part of the

Consolidated Fund, were excluded. Additionally, the accounting basis for

recognition of Expenditures was changed from commitment basis in 2007/8 to

cash basis in 2008/9. This basis was changed again in 2009/10 to “Budget cash

Expenditures”. The change from one accounting basis to another was not

annotated, to give indication of what the CF cash position would have been but

for the changes. As the CF cash position is an integral component of the Fiscal

Outturns Reports, it rendered the Reports not reliable.

iv. Financial irregularities amounting to US$33,941,455.53 were noted in the two

fiscal years under review. These irregularities involved under-asessment, and

non-payment of penalty on Real Property, unexplained variances between

expenditures reported in the 2008/9 and 2009/10 Fiscal Outturns and that

confirmed by line ministries and agencies as well as failure to retire travel

advances by some Government officials and other employees. The irregularities

rendered the respective Outturns in the 2008/9 and 2009/10 Fiscal Outturn

Reports not fairly stated in all material respects. Ref. Annex 1.

Auditor-General’s Disclaimer Opinion

73. In my opinion, because of the significant uncertainties inherent in the matters listed in

the basis for disclaimer of opinion above, I am unable to express an opinion as to

whether the Fiscal Outturns for 2008/9 and 2009/10, submitted by the Minister of

Finance and set out in Annexes 7A & 7B, present fairly in all material respects the

outturns achieved in the respective fiscal years and are in compliance with extant

Financial Management Regulatory Framework of Liberia.

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10

24 Promoting accountability, transparency, integrity and fiscal probity

DETAILED REPORT

Introduction

74. I have undertaken the audit of the Fiscal Outturn Reports of the Republic of Liberia for

the fiscal years 2008/9 and 2009/10; this being the third audit commissioned on the

respective Fiscal Outturns of the Republic of Liberia in accordance with the provision of

Chapter 53.3 of the 1972 Executive Law of Liberia. The audit was commissioned on

February 28, 2011 and completed on July 29, 2011.

MOF Responsibility

75. Under Section 37(1,2) of the Public Financial Management (PFM) Act of 2009, it is

stipulated that “the Minister shall prepare the un-audited Final Account of the National

Budget and submit it to the Auditor General no later than four (4) months after the end

of the fiscal year. The un-audited Final Account of the National Budget shall be in

accordance with the content and classifications of the budget. The content, format,

timeframe and procedures for the preparation and submission of the Final Account of

the National Budget shall be determined by accounting regulations under this Act”.

76. Section 37(5,6) of the PFM Act, requires me to review the Final Account of the National

Budget produced by the Minister of Finance and forward an audit report, along with the

Final Account, to the Legislature no later than four (4) months after receipt of the un-

audited Final Account from the Minister. My audit report shall include response and

clarifications furnished by the Minister on the observations and comments raised by me

on the un-audited Account. I am required to publish my report on the Final Account of

the National Budget (i.e. Fiscal Outturn Report) in the Official Gazette and submit it to

the Legislature and public within one month of the completion of the said audit report.

77. Additionally, Regulation I.12 of the PFM Regulations, states that “the Comptroller-

General shall within a period of four months after the end of each fiscal year, or such

other period as Legislature may by resolution appoint, prepare the Annual Accounts of

the Consolidated Fund (CF) for the Minister’s transmittal to the Auditor-General. The

Annual Accounts of the CF shall comprise:

i. A balance sheet showing the assets and liabilities of the CF at the close of the

financial year, annotated with such qualifying information as may affect the

significance of figures shown in the statement;

ii. A summary statement of the receipts into and payments from the CF in

comparison with the budget summary for the financial year;

iii. A statement of the revenue and expenditures for the financial year in

comparison with the approved and revised estimates for the year;

iv. A statement of transactions during the year and an analysis of the position at

the end of the year for:

• The public debt;

Auditor-General’s Report on the Fiscal Outturns for the Fiscal Years 2008/9 and 2009/10