REPORT 2009 BUSINESS AIRCRAFT FLEET NO … · leader USA saw its fleet decrease by ... AIRBUS...

15

By Nick Klenske No surprise here. 2009 was a slow year for Business Aviation. After declaring 2008 as “One of the Best”, this year we here at BART are hesitant to declare 2009 as “One of the Worse”. But before we tossed in the towel and all but wrote the past year off, we took a closer look at the statistics. And there, buried within the numbers we found good news – and even a hint at what may be the future of Business Aviation. Although the traditional power players have taken a hit – with the United States actually posting a negative rate of growth – the so-called emerging markets are surging like never before. J ust take a brief glance at the numbers and it should be blatant- ly clear: the center of Business Aviation is shifting. For starters, world leader USA saw its fleet decrease by 185 aircraft. On the other hand, Africa, Asia, the Middle East and South America are all growing at exceptional rates. In terms of specific countries, the Top Ten list is nearly split between traditional western nations and such emerging markets as Brazil, Mexico and Venezuela. But again, this really should not come as a surprise. Not only has the market been shifting away from the US for the past several years – compa- nies have been claiming that their sales are now 50 percent US and 50 percent “international” – but these numbers also reflect the economic cri- sis. Whereas the US was hit hard – as was the United Kingdom and, to a lesser extent, Europe – the emerging markets tended to fare better (with Dubai being a major exception). In other words, while companies in the US were having a fire sale trying to quickly get rid of their business air- craft in order to avoid government and public scrutiny, countries like Brazil were turning to Business Aviation as a business solution. The result – well, we think the numbers speak for them- selves. So yes, 2009 was a slow year for Business Aviation – as expected. The World Fleet continued to grow, although at a much slower rate than past years (the world fleet grew by seven percent last year, in comparison to this year’s 4.8 percent). And yes, Europe may have been a surprise as it navigated the crisis fairly well, but only saw a 9.7 percent increase in its fleet, which although strong is almost half the size of last year’s world-lead- ing 18 percent. But the slowdowns in Europe and the US are made up for by the 15.3, 27.1 and 13.3 percent growth rates in Africa, Asia/Middle East and South America respectively. Ok, so we changed our minds about 2009. Business Aviation is not slowing down. Business Aviation is simply changing, shifting and going where business goes – building new economies and ensuring that business gets done. O v e r v i e w Let us start from the end – or as close to the end as the numbers allow: GAMA’s 2009 Third Quarter Report on Shipments. This report traditionally gives us a better idea of what might be expected in 2010. And as we are all for- ward-looking business people, we don’t dwell in the past but simply use it to better navigate the future. According to the GAMA report, in the first three quarters of 2009, total general aviation airplane shipment fell by 46.8 percent, from 2,982 units in 2008 to 1,587 units at the time of the report’s release. Total industry billings were down 23.5 percent, to $13.8 bil- lion. “These shipment and billing figures are a result of this difficult business cycle and reflects the impact of the weak economy,” said GAMA President and CEO Pete Bunce. “However, another contributing factor that has led to the disappointing year-to-date numbers is the unwarranted negative attacks on Business Aviation.” 28 - BART: FEBRUARY - APRIL - 2010 NO SURPRISES HERE SHIFTING The marketplaces are turning towards Europe and the emerging markets of Asia, South America and Africa. REPORT 2009 BUSINESS AIRCRAFT FLEET F L E E T T O T A L S (As of End 2009) W o r l d F l e e t 2 9 , 9 9 2 E u r o p e a n F l e e t 3 , 9 5 9 J e t A i r c r a f t W o r l d w i d e 1 7 , 1 1 8 T u r b o p r o p s W o r l d w i d e 1 2 , 4 9 9

Transcript of REPORT 2009 BUSINESS AIRCRAFT FLEET NO … · leader USA saw its fleet decrease by ... AIRBUS...

By Nick Klenske

No surprise here. 2009 was aslow year for BusinessAviation. After declaring2008 as “One of the Best”,this year we here at BART arehesitant to declare 2009 as“One of the Worse”. Butbefore we tossed in thetowel and all but wrote thepast year off, we took acloser look at the statistics.And there, buried within thenumbers we found goodnews – and even a hint atwhat may be the future ofBusiness Aviation. Althoughthe traditional power playershave taken a hit – with theUnited States actuallyposting a negative rate ofgrowth – the so-calledemerging markets aresurging like never before.

J

ust take a brief glance at thenumbers and it should be blatant-ly clear: the center of Business

Aviation is shifting. For starters, worldleader USA saw its fleet decrease by185 aircraft. On the other hand, Africa,Asia, the Middle East and SouthAmerica are all growing at exceptionalrates. In terms of specific countries,the Top Ten list is nearly split betweentraditional western nations and suchemerging markets as Brazil, Mexicoand Venezuela.

But again, this really should notcome as a surprise. Not only has themarket been shifting away from theUS for the past several years – compa-nies have been claiming that theirsales are now 50 percent US and 50percent “international” – but thesenumbers also reflect the economic cri-sis. Whereas the US was hit hard – aswas the United Kingdom and, to alesser extent, Europe – the emergingmarkets tended to fare better (withDubai being a major exception). Inother words, while companies in the

US were having a fire sale trying toquickly get rid of their business air-craft in order to avoid government andpublic scrutiny, countries like Brazilwere turning to Business Aviation as abusiness solution. The result – well,we think the numbers speak for them-selves.

So yes, 2009 was a slow year forBusiness Aviation – as expected. TheWorld Fleet continued to grow,although at a much slower rate thanpast years (the world fleet grew byseven percent last year, in comparisonto this year’s 4.8 percent). And yes,Europe may have been a surprise as itnavigated the crisis fairly well, butonly saw a 9.7 percent increase in itsfleet, which although strong is almosthalf the size of last year’s world-lead-ing 18 percent. But the slowdowns inEurope and the US are made up for bythe 15.3, 27.1 and 13.3 percent growthrates in Africa, Asia/Middle East andSouth America respectively.

Ok, so we changed our minds about2009. Business Aviation is not slowingdown. Business Aviation is simplychanging, shifting and going wherebusiness goes – building neweconomies and ensuring that businessgets done.

Overview

Let us start from the end – or as closeto the end as the numbers allow:GAMA’s 2009 Third Quarter Report onShipments. This report traditionallygives us a better idea of what might beexpected in 2010. And as we are all for-ward-looking business people, wedon’t dwell in the past but simply useit to better navigate the future.

According to the GAMA report, inthe first three quarters of 2009, totalgeneral aviation airplane shipment fellby 46.8 percent, from 2,982 units in2008 to 1,587 units at the time of thereport’s release. Total industry billingswere down 23.5 percent, to $13.8 bil-lion.

“These shipment and billing figuresare a result of this difficult businesscycle and reflects the impact of theweak economy,” said GAMA Presidentand CEO Pete Bunce. “However,another contributing factor that hasled to the disappointing year-to-datenumbers is the unwarranted negativeattacks on Business Aviation.”

28 - BART: FEBRUARY - APRIL - 2010

NO SURPRISES HERE

SHIFTINGThe marketplaces

are turning

towards Europe

and the emerging

markets of Asia,

South America

and Africa.

R E P O R T 2 0 0 9 B U S I N E S S A I R C R A F T F L E E T

FLEET TOTALS

(As of End 2009)

World Fleet 29,992

European Fleet 3,959

Jet Aircraft Worldwide 17,118

Turboprops Worldwide 12,499

30 - BART: FEBRUARY - APRIL - 2010

MFG/MODEL TOTAL EUR

AIRBUS A300 1 0

AIRBUS A310 21 12

AIRBUS A318 ELITE 7 4

AIRBUS A319CJ 44 22

AIRBUS A320 5 1

AIRBUS A340 10 0

ASTRA 1125 32 0

ASTRA 1125SP 36 1

ASTRA 1125SPX 58 3

BAC 1-11 18 1

BAE 146-100 4 1

BAE 146-200 6 4

BAE 146-300 1 0

BAE Avro RJ70 1 1

BEECHJET 400 60 1

BEECHJET 400A 346 25

BOEING 707-120B 4 0

BOEING 707-320 33 5

BOEING 707-C 7 0

BOEING 707-E 5 0

BOEING 720B 3 1

BOEING 727-100 51 3

BOEING 727-200 25 2

BOEING 737 1 0

BOEING 737-100 1 0

BOEING 737-200 36 1

BOEING 737-300 9 1

BOEING 737-400 3 0

BOEING 737-500 4 1

BOEING 737-700 7 0

BOEING 747-300 1 0

BOEING 747-400 10 0

BOEING 747SP 12 1

BOEING 757 4 0

BOEING 757-200 15 2

BOEING 767-200 7 0

BOEING 767-300 4 2

BOEING 777-200 1 0

BOEING BBJ 99 14

BOEING BBJ2 14 4

CANADAIR RJ 24 2

CHALLENGER 300 260 48

CHALLENGER 600 78 5

CHALLENGER 601-1A 63 9

CHALLENGER 601-3A 132 14

CHALLENGER 601-3R 59 4

CHALLENGER 604 363 80

CHALLENGER 605 82 33

CHALLENGER 800 3 1

CHALLENGER 850 43 26

CHALLENGER 870 2 1

CHALLENGER 890 2 0

CITATION 500 271 37

CITATION 525 352 86

CITATION BRAVO 335 81

CITATION CJ1 195 53

CITATION CJ1+ 97 33

CITATION CJ2 239 73

CITATION CJ2+ 153 58

MFG/MODEL TOTAL EUR

CITATION CJ3 329 77

CITATION ENCORE 165 13

CITATION ENCORE+ 55 6

CITATION EXCEL 369 65

CITATION I 24 9

CITATION I/SP 296 33

CITATION II 586 65

CITATION II/SP 73 19

CITATION III 195 14

CITATION MUSTANG 256 65

CITATION S/II 153 10

CITATION SOVEREIGN 279 47

CITATION ULTRA 274 15

CITATION V 258 19

CITATION VI 36 5

CITATION VII 118 13

CITATION X 298 21

CITATION XLS 328 108

CITATION XLS+ 35 10

DIAMOND I 4 1

DIAMOND IA 71 3

DORNIER 328JET ENVOY 53 23

ECLIPSE EA500 256 22

EMBRAER LEGACY 600 164 61

EMBRAER LEGACY SHUTTLE 11 0

EMBRAER LINEAGE 1000 2 0

EMBRAER PHENOM 100 68 6

FALCON 10 152 14

FALCON 100 33 11

FALCON 200 33 4

FALCON 2000 231 49

FALCON 2000DX 4 1

FALCON 2000EX 26 8

FALCON 2000EX EASy 143 55

FALCON 2000LX 4 3

FALCON 20C 93 25

FALCON 20C-5 21 5

FALCON 20D 29 7

FALCON 20D-5 4 0

FALCON 20E 37 14

FALCON 20E-5 15 9

FALCON 20F 87 10

FALCON 20F-5 79 6

FALCON 20G 5 5

FALCON 50 241 40

FALCON 50-40 6 0

FALCON 50EX 101 15

FALCON 7X 49 25

FALCON 900 39 12

FALCON 900B 138 35

FALCON 900C 25 8

FALCON 900DX 21 9

FALCON 900EX 118 35

FALCON 900EX EASy 100 39

FOKKER F100 4 3

FOKKER F28 3 1

GLOBAL 5000 77 18

GLOBAL EXPRESS 149 36

GLOBAL EXPRESS XRS 84 30

MFG/MODEL TOTAL EUR

GULFSTREAM G-100 22 2

GULFSTREAM G-150 78 10

GULFSTREAM G-200 221 28

GULFSTREAM G-300 13 0

GULFSTREAM G-350 11 0

GULFSTREAM G-400 23 0

GULFSTREAM G-450 160 14

GULFSTREAM G-500 9 0

GULFSTREAM G-550 239 60

GULFSTREAM G-II 164 1

GULFSTREAM G-IIB 40 2

GULFSTREAM G-III 183 2

GULFSTREAM G-IV 212 11

GULFSTREAM G-IVSP 286 11

GULFSTREAM G-V 191 19

HAWKER 1000A 44 4

HAWKER 1000B 7 3

HAWKER 125-1A 19 4

HAWKER 125-1AS 9 0

HAWKER 125-1B 11 9

HAWKER 125-3A 3 1

HAWKER 125-3A/RA 7 0

HAWKER 125-3A/RAS 3 0

HAWKER 125-3AS 2 0

HAWKER 125-3B 9 1

HAWKER 125-3B/RAS 1 0

HAWKER 125-3BS 1 0

HAWKER 125-400A 16 0

HAWKER 125-400AS 52 3

HAWKER 125-400B 14 1

HAWKER 125-400BS 3 0

HAWKER 125-600A 20 1

HAWKER 125-600AS 12 1

HAWKER 125-600B 2 0

HAWKER 125-600BS 1 0

HAWKER 125-700A 173 9

HAWKER 125-700B 32 21

HAWKER 4000 25 0

HAWKER 400XP 234 43

HAWKER 750 35 14

HAWKER 800A 226 5

HAWKER 800B 61 14

HAWKER 800XP 423 52

HAWKER 800XPI 51 25

HAWKER 850XP 100 19

HAWKER 900XP 111 19

JET COMMANDER 1121 11 0

JET COMMANDER 1121B 8 1

JETSTAR 6 2 0

JETSTAR 731 16 3

JETSTAR 8 7 0

JETSTAR II 24 1

LEARJET 23 15 1

LEARJET 24 37 1

LEARJET 24A 4 0

LEARJET 24B 25 0

LEARJET 24D 66 1

LEARJET 24E 15 0

LEARJET 24F 9 0

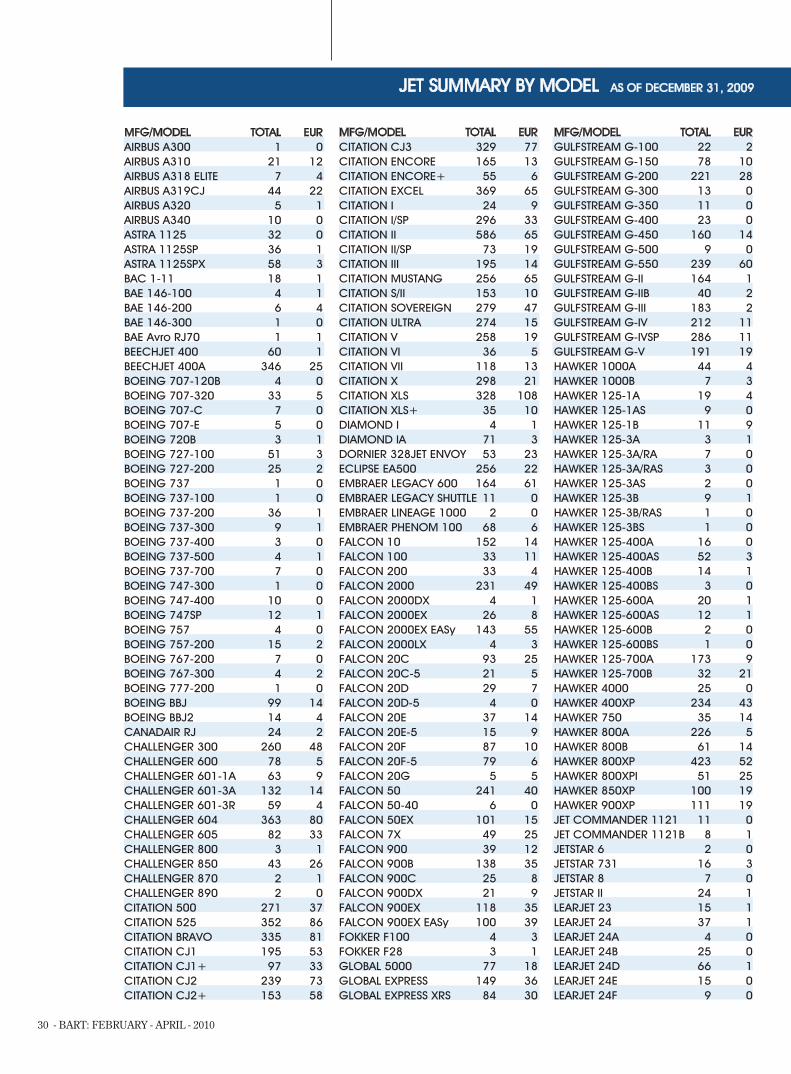

JET SUMMARY BY MODEL AS OF DECEMBER 31, 2009

BART: FEBRUARY - APRIL - 2010 - 31

MFG/MODEL TOTAL EUR

LEARJET 25 30 0

LEARJET 25B 68 1

LEARJET 25C 14 1

LEARJET 25D 138 2

LEARJET 25G 4 0

LEARJET 28 5 0

LEARJET 29 4 0

LEARJET 31 35 4

LEARJET 31A 207 13

LEARJET 35 50 0

LEARJET 35A 479 40

LEARJET 36 15 0

LEARJET 36A 38 4

LEARJET 40 45 16

LEARJET 40XR 74 13

LEARJET 45 239 42

LEARJET 45XR 155 15

LEARJET 55 116 14

LEARJET 55B 8 1

LEARJET 55C 14 2

LEARJET 60 312 54

LEARJET 60XR 54 19

LOCKHEED L1011 3 0

MDD DC8 2 0

MDD DC9 12 0

MDD MD80 14 2

PREMIER I 126 23

PREMIER IA 136 36

SABRELINER 40 24 2

SABRELINER 40A 28 1

SABRELINER 40EL 7 0

SABRELINER 40EX 2 0

SABRELINER 40R 4 0

SABRELINER 40SE 1 0

SABRELINER 50 1 0

SABRELINER 60 43 0

SABRELINER 60A 3 0

SABRELINER 60AELXM 1 0

SABRELINER 60EL 3 1

SABRELINER 60ELXM 33 0

SABRELINER 60EX 4 0

SABRELINER 60SC 2 0

SABRELINER 60SCELXM 2 0

SABRELINER 60SCEX 1 0

SABRELINER 65 75 1

SABRELINER 80 27 0

SABRELINER 80A 3 0

SABRELINER 80SC 7 0

SINO SWEARINGEN SJ30-2 4 1

WESTWIND 1 105 0

WESTWIND 1123 7 0

WESTWIND 1124 54 0

WESTWIND 2 80 0

Total Jets 17.382 2.744

© avdata/JETNET

MFG/MODEL TOTAL EUR

AVANTI II 87 33

AVANTI P180 98 42

CARAVAN 208 390 29

CARAVAN 208B 1.311 81

CHEYENNE 400 40 7

CHEYENNE I 171 15

CHEYENNE IA 17 4

CHEYENNE II 372 48

CHEYENNE III 80 9

CHEYENNE IIIA 54 16

CHEYENNE IIXL 75 6

CONQUEST I 209 16

CONQUEST II 318 9

GULFSTREAM G-I 70 3

JETSTREAM 31 45 9

JETSTREAM 32 31 5

JETSTREAM 41 9 2

KING AIR 100 64 1

KING AIR 200 713 65

KING AIR 200C 32 3

KING AIR 200T 20 2

KING AIR 300 212 2

KING AIR 300LW 21 10

KING AIR 350 623 48

KING AIR 350C 27 4

KING AIR 90 30 1

KING AIR A/B90 13 0

KING AIR A100 112 4

KING AIR A200 236 1

KING AIR A90 77 5

KING AIR A90-1 121 2

KING AIR B100 122 1

KING AIR B200 1.091 134

KING AIR B200C 100 6

KING AIR B200CT 9 0

KING AIR B200GT 86 16

KING AIR B200SE 5 1

KING AIR B200T 23 1

KING AIR B90 113 6

KING AIR C90 445 43

KING AIR C90-1 42 0

KING AIR C90A 226 20

KING AIR C90B 426 34

KING AIR C90GT 97 8

KING AIR C90GTi 98 16

KING AIR C90SE 16 0

KING AIR E90 295 18

KING AIR F90 188 11

KING AIR F90-1 30 3

MALIBU JETPROP 218 56

MERLIN 300 9 2

MERLIN IIA 2 0

MERLIN IIB 37 4

MERLIN III 28 1

MERLIN IIIA 35 5

MERLIN IIIB 59 5

MERLIN IIIC 24 2

MERLIN IV 9 1

MERLIN IV-A 24 5

MFG/MODEL TOTAL EUR

MERLIN IV-C 21 4

MITSUBISHI MARQUISE 98 3

MITSUBISHI MU-2B 3 0

MITSUBISHI MU-2C 16 0

MITSUBISHI MU-2D 1 0

MITSUBISHI MU-2F 39 0

MITSUBISHI MU-2G 6 0

MITSUBISHI MU-2J 47 1

MITSUBISHI MU-2K 43 7

MITSUBISHI MU-2L 22 0

MITSUBISHI MU-2M 19 3

MITSUBISHI MU-2N 26 0

MITSUBISHI MU-2P 32 2

MITSUBISHI MU-2S 17 0

MITSUBISHI SOLITAIRE 42 1

PILATUS PC-12 776 92

PILATUS PC-12 NG 151 24

PIPER MERIDIAN 382 61

SOCATA TBM-700A 105 30

SOCATA TBM-700B 96 30

SOCATA TBM-700C1 8 5

SOCATA TBM-700C2 95 11

SOCATA TBM-850 174 33

STARSHIP 2000A 5 0

TURBO COMMANDER 1000 100 3

TURBO COMMANDER 690 48 1

TURBO COMMANDER 690A 186 9

TURBO COMMANDER 690B 193 4

TURBO COMMANDER 840 105 6

TURBO COMMANDER 900 34 1

TURBO COMMANDER 980 74 3

Total TurboProp 12.499 1.215

Grand Total 29.881 3.959

© avdata/JETNET

TURBOPROPS

JET FLEET

TURBOPROPS FLEET

WORLD TURBINE FLEET

2.697

1.215

3.912

17.118

12.499

29.617

World Europe

World Europe

World Europe

32 - BART: FEBRUARY - APRIL - 2010

EXECUTIVEExecutive

aircraft are

airliner aircraft

converted to

private business

use, excluding

models originally

meant for

business use.

R E P O R T

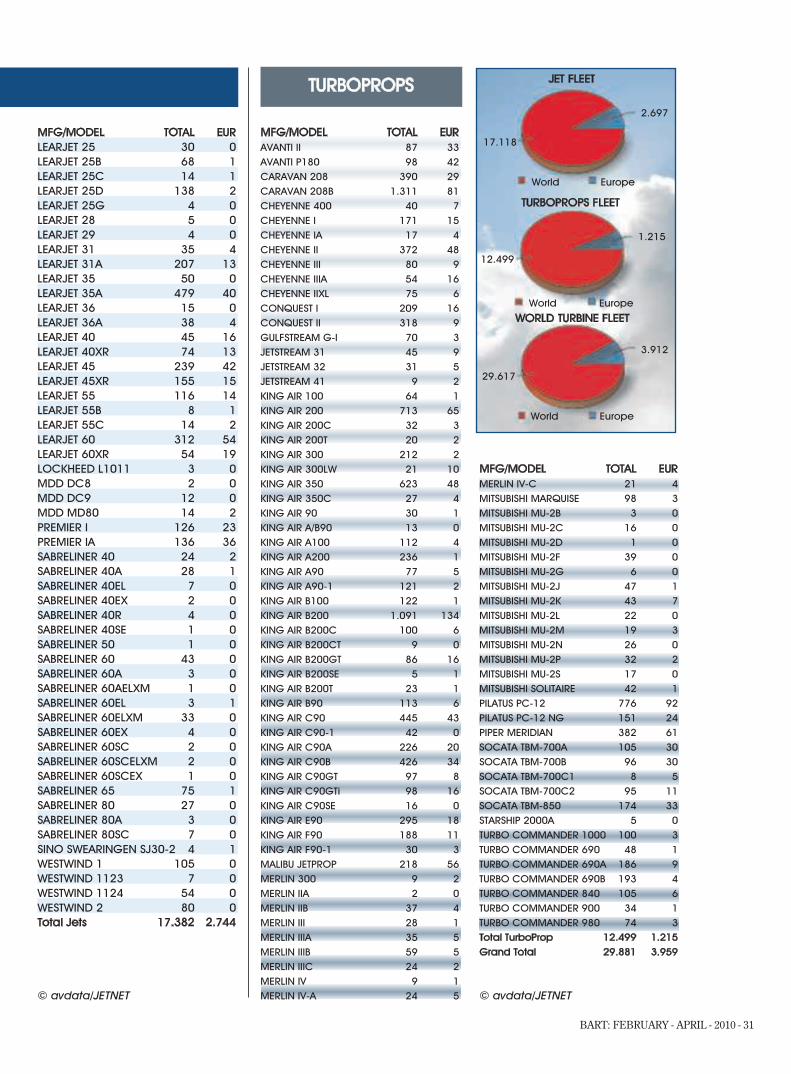

NORTH AMERICA

Country Total Executive Jet Turb.

Antigua and Barbuda 1 0 0 1

Aruba 15 0 13 2

Bahamas 23 1 7 15

Barbados 4 0 3 1

Belize 14 0 1 13

Bermuda 40 1 35 4

Canada 1068 8 400 660

Cayman Islands 28 2 23 3

Costa Rica 30 0 10 20

Dominica 1 1 0 0

Dominican Republic 37 0 17 20

El Salvador 7 1 2 4

Greenland 1 0 0 1

Guadeloupe 3 0 0 3

Guatemala 68 0 22 46

Haiti 3 2 0 1

Honduras 14 0 4 10

Jamaica 5 0 3 2

Martinique 1 0 0 1

Mexico 960 11 635 314

Netherlands Antilles 5 0 2 3

Nicaragua 7 0 0 7

Panama 86 0 25 61

Puerto Rico 59 0 28 31

St Vincent-Grenadines 3 0 2 1

Trinidad and Tobago 1 0 1 0

Turks and Caicos Isl. 2 0 1 1

United States 17905 122 10787 6996

Virgin Islands (British) 16 1 11 4

Virgin Islands (U.S.) 11 0 7 4

West Indies 7 0 7 0

Total 20425 150 12046 8229

SOUTH AMERICA

Country Total Executive Jet Turb.

Argentina 233 1 105 127

Bolivia 15 0 3 12

Brazil 1010 3 463 544

Chile 78 2 28 48

Colombia 228 0 21 207

Ecuador 23 0 9 14

Guyana 8 0 0 8

Paraguay 23 1 5 17

Peru 37 1 5 31

Suriname 3 0 0 3

Uruguay 8 0 2 6

Venezuela 560 1 200 359

Total 2226 9 841 1376

EUROPE

Country Total Executive Jet Turb.

Austria 267 2 236 29

Belarus 1 0 1 0

Belgium 85 2 49 34

Bosnia and Herzegovina 3 0 2 1

Bulgaria 28 1 21 6

Croatia 11 0 6 5

Cyprus 11 0 10 1

Czech Republic 46 0 28 18

Denmark 102 0 71 31

Estonia 9 0 8 1

Finland 41 0 27 14

France 398 4 195 199

Germany 644 7 420 217

Gibraltar 2 0 2 0

Greece 56 3 35 18

Hungary 7 0 5 2

Iceland 8 0 4 4

Ireland 45 1 34 10

Isle of Man 42 0 37 5

Italy 230 0 151 79

Latvia 8 0 6 2

Liechtenstein 3 0 2 1

Lithuania 5 0 3 2

Luxembourg 72 1 34 37

Macedonia 2 0 2 0

Malta 6 1 5 0

Moldova 1 0 1 0

Monaco 5 0 4 1

Montenegro 5 0 5 0

Netherlands 89 1 51 37

Northern Ireland 4 0 4 0

Norway 59 0 15 44

Poland 32 0 18 14

Portugal 194 0 187 7

Romania 16 1 12 3

Russian Federation 128 1 106 21

San Marino 6 0 5 1

Scotland 2 0 1 1

Serbia 19 0 15 4

Slovak Republic 14 0 9 5

Slovenia 15 0 12 3

Spain 193 4 141 48

Sweden 85 0 50 35

Switzerland 313 4 227 82

Ukraine 36 2 29 5

United Kingdom 611 12 411 188

Total 3959 47 2697 1215

UNKNOWN

Country Total Executive Jet Turb.

Unknown 93 2 49 42

Total 93 2 49 42

Likewise, a recently released study shows the powerfulconnection between well-run companies and those that useBusiness Aviation. For example, Business Week maga-zine’s 2009 “25 Best Customer Service Companies” and theCorporate Responsibility Officer’s list of 2009 “100 BestCorporate Citizens” both show that 90 percent of the identi-fied S&P 500 companies are business aircraft users –which hints that as the economy recovers so too willBusiness Aviation.

“When America’s most responsible and best-run compa-nies use Business Aviation to create jobs and share holdervalue, attacks on this segment of general aviation are

2 0 0 9 B U S I N E S S A I R C R A F T F L E E T

BART: FEBRUARY - APRIL - 2010 - 33

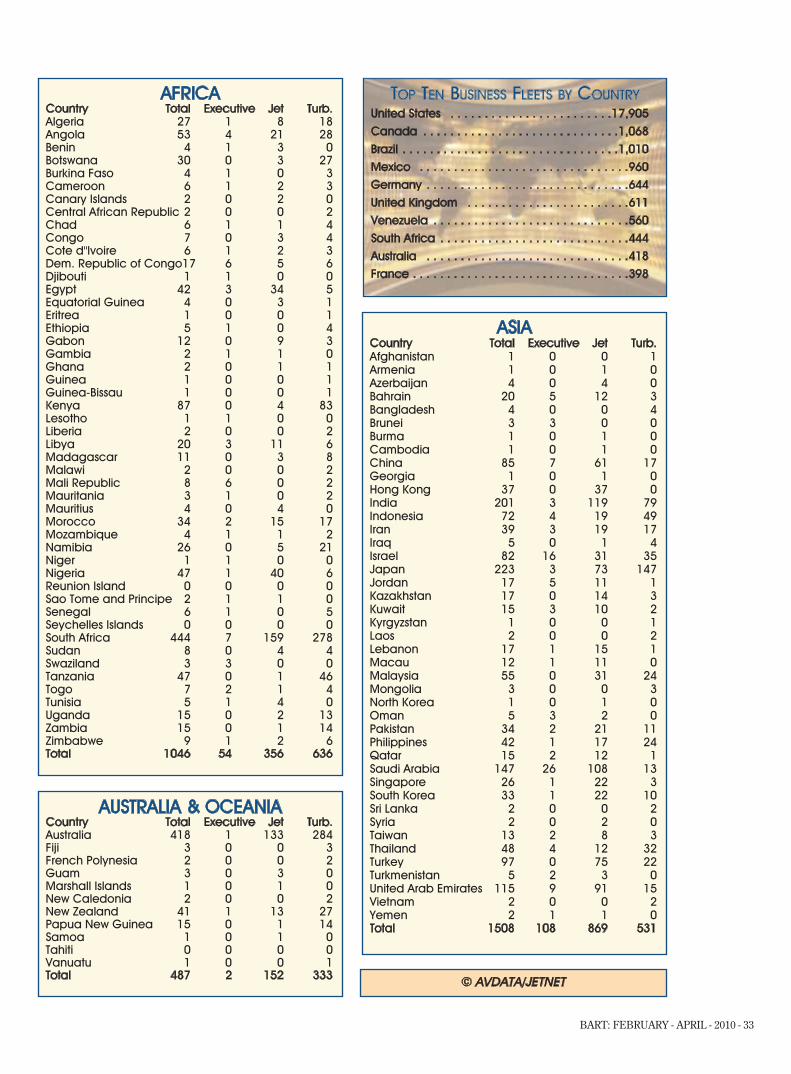

ASIA

Country Total Executive Jet Turb.

Afghanistan 1 0 0 1

Armenia 1 0 1 0

Azerbaijan 4 0 4 0

Bahrain 20 5 12 3

Bangladesh 4 0 0 4

Brunei 3 3 0 0

Burma 1 0 1 0

Cambodia 1 0 1 0

China 85 7 61 17

Georgia 1 0 1 0

Hong Kong 37 0 37 0

India 201 3 119 79

Indonesia 72 4 19 49

Iran 39 3 19 17

Iraq 5 0 1 4

Israel 82 16 31 35

Japan 223 3 73 147

Jordan 17 5 11 1

Kazakhstan 17 0 14 3

Kuwait 15 3 10 2

Kyrgyzstan 1 0 0 1

Laos 2 0 0 2

Lebanon 17 1 15 1

Macau 12 1 11 0

Malaysia 55 0 31 24

Mongolia 3 0 0 3

North Korea 1 0 1 0

Oman 5 3 2 0

Pakistan 34 2 21 11

Philippines 42 1 17 24

Qatar 15 2 12 1

Saudi Arabia 147 26 108 13

Singapore 26 1 22 3

South Korea 33 1 22 10

Sri Lanka 2 0 0 2

Syria 2 0 2 0

Taiwan 13 2 8 3

Thailand 48 4 12 32

Turkey 97 0 75 22

Turkmenistan 5 2 3 0

United Arab Emirates 115 9 91 15

Vietnam 2 0 0 2

Yemen 2 1 1 0

Total 1508 108 869 531

© AVDATA/JETNET

AUSTRALIA & OCEANIA

Country Total Executive Jet Turb.

Australia 418 1 133 284

Fiji 3 0 0 3

French Polynesia 2 0 0 2

Guam 3 0 3 0

Marshall Islands 1 0 1 0

New Caledonia 2 0 0 2

New Zealand 41 1 13 27

Papua New Guinea 15 0 1 14

Samoa 1 0 1 0

Tahiti 0 0 0 0

Vanuatu 1 0 0 1

Total 487 2 152 333

AFRICA

Country Total Executive Jet Turb.

Algeria 27 1 8 18

Angola 53 4 21 28

Benin 4 1 3 0

Botswana 30 0 3 27

Burkina Faso 4 1 0 3

Cameroon 6 1 2 3

Canary Islands 2 0 2 0

Central African Republic 2 0 0 2

Chad 6 1 1 4

Congo 7 0 3 4

Cote d''Ivoire 6 1 2 3

Dem. Republic of Congo17 6 5 6

Djibouti 1 1 0 0

Egypt 42 3 34 5

Equatorial Guinea 4 0 3 1

Eritrea 1 0 0 1

Ethiopia 5 1 0 4

Gabon 12 0 9 3

Gambia 2 1 1 0

Ghana 2 0 1 1

Guinea 1 0 0 1

Guinea-Bissau 1 0 0 1

Kenya 87 0 4 83

Lesotho 1 1 0 0

Liberia 2 0 0 2

Libya 20 3 11 6

Madagascar 11 0 3 8

Malawi 2 0 0 2

Mali Republic 8 6 0 2

Mauritania 3 1 0 2

Mauritius 4 0 4 0

Morocco 34 2 15 17

Mozambique 4 1 1 2

Namibia 26 0 5 21

Niger 1 1 0 0

Nigeria 47 1 40 6

Reunion Island 0 0 0 0

Sao Tome and Principe 2 1 1 0

Senegal 6 1 0 5

Seychelles Islands 0 0 0 0

South Africa 444 7 159 278

Sudan 8 0 4 4

Swaziland 3 3 0 0

Tanzania 47 0 1 46

Togo 7 2 1 4

Tunisia 5 1 4 0

Uganda 15 0 2 13

Zambia 15 0 1 14

Zimbabwe 9 1 2 6

Total 1046 54 356 636

TOP TEN BUSINESS FLEETS BY COUNTRY

United States . . . . . . . . . . . . . . . . . . . . . . . .17,905

Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1,068

Brazil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1,010

Mexico . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .960

Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .644

United Kingdom . . . . . . . . . . . . . . . . . . . . . . . .611

Venezuela . . . . . . . . . . . . . . . . . . . . . . . . . . . . .560

South Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . .444

Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .418

France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .398

34 - BART: FEBRUARY - APRIL - 2010

unwarranted,” says Bunce. “We arenow seeing some encouraging signsthat policymakers all around the USare recognizing the vital contributionour industry makes to the economy.”

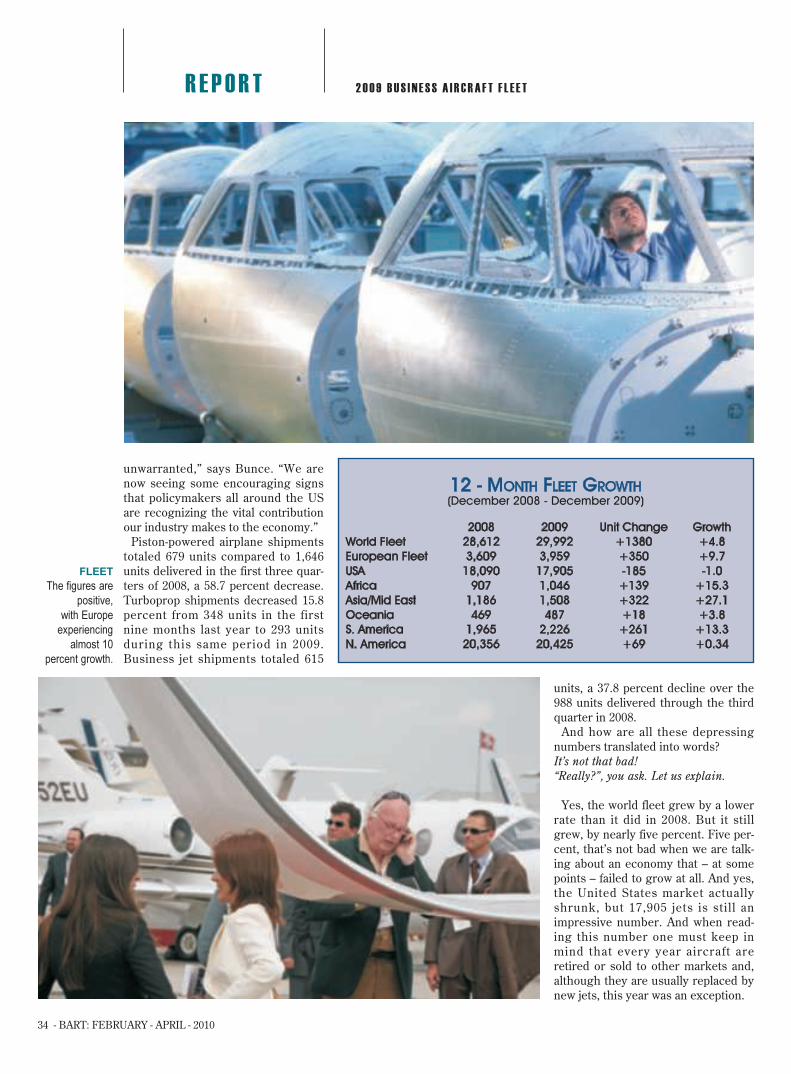

Piston-powered airplane shipmentstotaled 679 units compared to 1,646units delivered in the first three quar-ters of 2008, a 58.7 percent decrease.Turboprop shipments decreased 15.8percent from 348 units in the firstnine months last year to 293 unitsduring this same period in 2009.Business jet shipments totaled 615

units, a 37.8 percent decline over the988 units delivered through the thirdquarter in 2008.

And how are all these depressingnumbers translated into words?It’s not that bad!“Really?”, you ask. Let us explain.

Yes, the world fleet grew by a lowerrate than it did in 2008. But it stillgrew, by nearly five percent. Five per-cent, that’s not bad when we are talk-ing about an economy that – at somepoints – failed to grow at all. And yes,the United States market actuallyshrunk, but 17,905 jets is still animpressive number. And when read-ing this number one must keep inmind that every year aircraft areretired or sold to other markets and,although they are usually replaced bynew jets, this year was an exception.

FLEETThe figures are

positive,

with Europe

experiencing

almost 10

percent growth.

R E P O R T 2 0 0 9 B U S I N E S S A I R C R A F T F L E E T

12 - MONTH FLEET GROWTH

(December 2008 - December 2009)

2008 2009 Unit Change Growth

World Fleet 28,612 29,992 +1380 +4.8

European Fleet 3,609 3,959 +350 +9.7

USA 18,090 17,905 -185 -1.0

Africa 907 1,046 +139 +15.3

Asia/Mid East 1,186 1,508 +322 +27.1

Oceania 469 487 +18 +3.8

S. America 1,965 2,226 +261 +13.3

N. America 20,356 20,425 +69 +0.34

36 - BART: FEBRUARY - APRIL - 2010

That’s right – an exception. The num-bers, when held up against the eco-nomic and political facts, make 2009an exception, not a rule. The US econ-omy was hit hard and, as Bunce states,Business Aviation was unfairly heldout as the scapegoat. But, thanks tothe concerted efforts by GAMA andNBAA, this perception is changingand with it, business aircraft are onceagain being bought. So expect to seethe US back in the black next year atthis time.

What about Europe? It’s the oppositesituation here as 2008 was an excep-tion – with an 18 percent growth rate.Perhaps because of the economy ormaybe simply a result of a leveling offof the business scene, Europe is backto a more reasonable 9.7 percent rateof growth.

But let’s go out on a limb here andsay “who cares about the US andEuropean markets”? Yes, they’veslowed but they are still strong. Whatwe should care about is where thegrowth is because – going back to theconcept of using the past to predict thefuture – this year’s statistics arescreaming that the future of BusinessAviation is in the emerging markets.Africa is up by 15.3 percent, withSouth Africa leading the way. Asia andthe Middle East enjoyed a 27.1 percentincrease in fleet size. Think about that.27.1 percent – in an economic crisisnonetheless. And South America,home of Top Ten players Brazil andVenezuela, enjoyed a 13.3 percent rateof growth.

Although the Top Ten list saw nochanges in position since 2008, wemay predict a new number two in2011. Last year, Brazil trailed Canadaby almost exactly 100 aircraft. Overthe course of the past year, Brazil hasclosed this gap to 58 aircraft – somaybe a BRIC country will move tonumber two in next year’s list?

Let’s not forget there are plenty ofcountries looming in the shadows ofthis prestigious list: Argentina (233),Columbia (228), Japan (223), India(201), Saudi Arabia (147), Russia(128), China (122) and the UAE (115)are all creeping their way up. Andguess where these countries are alllocated? That’s right, the emergingregions of Asia, the Middle East andSouth America.

R E P O R T 2 0 0 9 B U S I N E S S A I R C R A F T F L E E T

BART: FEBRUARY - APRIL - 2010 - 37

GROWTHBoth turboprops

and jets showed

a strong year.

Where the Growth Is

Turboprops vs. JetsBolstered by the surge in emerg-

ing markets and steady sales inbush countries like Australia andthe safar i region of Afr ica ,Turboprops continue to grow. Thisyear the turboprop fleet increasedfrom 12,127 to 12,499, for anincrease of 372 – slightly down fromlast year’s increase of 457 aircraft.But this is st i l l up from severalyears ago when turboprops wereviewed as a thing of the past. If yourecall, in 2007 the number of newturboprops entering the marketplummeted from 794 in 2006 to just325.

Likewise, all things considered,jets too enjoyed another strongyear. This sector closed out the yearwith a fleet total of 17,118 aircraftworldwide. In 2008, the worldwidejet fleet was at 16,240, which repre-sents an 878 aircraft increase (com-pared to a 970 increase in jet fleetlast year). Of the total jet fleet, 2,697are based in Europe, meaning thatthe continent’s love affair with thebusiness jet continues.

Models and MakesOn the jet side, as to the overall

contribution to the worldwide jetfleet, there is no change in the lead-ing OEMs with Cessna staying atthe top spot with 5,769 jets flying,followed by Bombardier (3,672) andHawker Beechcraft (2,113). Thisyear Gulfstream bumped Dassaultout of the number four spot with its1,852 jets (compared to Dassault’s1,834). And Embraer – a companywho continues to surge with newaircraft – comes in with 245 jets.

In terms of specifics, like last year,the Citation reigns supreme, claim-ing six of the top ten spots. At thetop remains the Citation II, whichactually dropped two aircraft fromits fleet to end the year with 586.Other leading Citations include theExcel (369), 525 (352), Bravo (335)and CJ3 (329). Dropped from thelist are the XLS and I/SP, which had328 and 296 respectively.

At the number two spot was onceagain the Learjet 35A, which, likethe Citation II, dropped in numbersfrom 485 aircraft to 479 in 2009. Thenumber three spot went to theHawker 800XP, which accounts for423 aircraft, up one jet from last

year . Other leaders include theChallenger 604 (363 jets), Beechjet400A (346 jets) and the Learjet 60(312 jets).

Once again turning to numbers topredict the future, according toGAMA’s reports the above listedtrends look to stay on track. As ofthe close of the Third Quarter 2009,Cessna has shipped 512 units, withHawker Beechcraf t a t 173,Bombardier at 140, Gulfstream at

74, Embraer at 56 and Dassault at51. In terms of total billings year-to-date 2009 the list turns a bit:Bombardier ($3,948,000,000),Gulfstream ($3,054,000,000),Dassault ($2,000,665,000),Cessna ($1,828,523,634),Hawker Beechcraft ($1,221,618,700),and Embraer ($523,975,000).

On the turboprop side, thingsremained pretty much the same. Theleading aircraft continues to be the

38 - BART: FEBRUARY - APRIL - 2010

Caravan 208B at 1,311 aircraft. Theother leaders include the King AirB200 (1,091), Pilatus PC-12 (776),King Air 200 (713), King Air 350 (623)and Cheyenne II (372). In Europe,which favors the jet, the King Air B200is the most popular turboprop, at 134.The Pilatus PC-12 and PC-12 NGremain popular in North America, with583 and 98 respectively.

Regional Performance

As previously mentioned, unlike lastyear, in 2009 not all regions experi-enced an increase in total fleet size,with the United States seeing adecrease of 185 aircraft, or a one per-cent decrease in rate of growth. Butoverall, the net growth of all otherregions remains positive. In 2006 allregions were reported as showing adecrease in level of annual growth.More in line with last year’s trend,most regions saw an increase,although which regions experiencehow much growth varied (with

Europe falling and Asia/Middle Eastsurging).

At the same time, 2009 can be com-pared to 2007, where regions saw alimited level of growth. At the time,the lower levels were explained bysuch international issues asincreased oil prices and greater reg-ulations making it more difficult forBusiness Aviat ion to sustain i tsupward growth. In 2009, the lowerlevels of growth can simply beexplained by the often quoted BillClinton quote: “It’s the economy, stu-pid”. Where the economy is strug-gling (US, Europe), the numbersstagnated. Where the economy didbetter (Asia, Middle East, SouthAmerica), the numbers surged.

Europe

Europe continues to be one of theworld’s most successful markets,with growth continuing over the lastseveral years. In 2006, the totalEuropean fleet was at 2,851. By 2007

it grew by 7.2 percent to 3,054. Andin 2008 i t boomed to 3,609 – anincrease of 552 aircraft, or an 18.0percent rate of growth in overall fleetsize. So things cooled off a bit, butthis year’s 9.7 percent increase infleet size (350 aircraft) is still higherthan the impressive 2006 – 2007 7.2percent increase.

Top individual countries remain theusual suspects, with Germany, theUnited Kingdom and France all rep-resenting the continent on the TopTen Business Fleets by Country list.All three countries saw their fleetsgrow, with Germany going from 570to 644, the United Kingdom from 536to 611 and France from 330 to 398.

Other European countries that sawconsiderable growth over the pastyear include:Austria (+26),Bulgaria (+9),Czech Republic (+10),Denmark (+7),Finland (+8),

AREAEurope

continues to be

one of the most

promising

regions.

R E P O R T 2 0 0 9 B U S I N E S S A I R C R A F T F L E E T

BART: FEBRUARY - APRIL - 2010 - 39

LEADERSRussia +55,

Austria +26 and

Switzerland +23

were the

leading countries

last year.

Greece (+15),Italy (+17),Luxembourg (+9),Netherlands (+21),Norway (+16),Poland (+9),Russia (+55),Spain (+31)and Switzerland (+23).

Interestingly, the Isle of Man saw 29new aircraft on its registry, whereasCyprus lost four, Ireland went downeight, Lichtenstein by 11 and Monacoby 35 aircraft. 2009 also welcomedMoldova to the Business Aviation club.

The Americas

Usually this space is dedicated to theUnited States and Canada, with therest of the America filling in whitespace. But this year let’s change thefocus. Yes, the US and Canadian fleetsstill dominate – and will probably doso for some years to come. However,the focus has shifted to SouthAmerica.

This isn’t anything new. Even lastyear in our Fleet Report we discussednot only how the slowing of theAmerican economy and the weaken-ing of the US dollar both contribute tothis trend, but that it is also the resultof a larger trend – namely the growingimportance of the global economy.And that trend continues to strength-en.

In North America, the three mainplayers – US, Canada and Mexico –are all Top 10 Players, with bothCanada and Mexico seeing their fleetsgrow. Other North American coun-tries enjoying a net growth include:Bahamas, Cayman Islands, Domincan

40 - BART: FEBRUARY - APRIL - 2010

Republic (with an impressive 10 air-craft added to the fleet), Guatamalaand Puerto Rico. Other tropicalnations did not fare as well, withBelize, El Salvador, Turks and Caicosand both the US and British VirginIslands losing aircraft. AlthoughAnguilla fell of this year’s list, its spotwas taken by Martinique.

In South America, BusinessAviation continues to boom. In 2008its total fleet came in at 1,965. At theend of 2009 the number was 2,226,for an addition of 261 aircraft. In

terms of growth rates, this convertsto an impressive 13.2 percent.Individual country leaders continueto be Brazil, Venezuela, Argentinaand Columbia, but one should keepan eye on such countries as Chileand Paraguay, both of whom contin-ue to steadily increase their fleetsizes. Interestingly, Ecuador saw itsf leet decrease and Peru saw nochange at all.

Asia and the Middle East

If you were to hedge your bets onwhere the future of Business Aviationis, put your money on Asia and theMiddle East. With an increase in fleetsize of 322 aircraft and a whopping27.1 percent increase in rate of growth– this region is booming. This mayexplain why in 2011 NBAA will returnto its relationship with ABACE aftercanceling the show last year.

Breaking down this diverse regioninto countries, it again becomes clearthat the vast majority of this businessis within the Middle East. It should benoted that this could be severly effect-ed by the late 2009 debt crisis in Dubai– but we’ll have to wait and see.

In the Middle East, the big playersare Israel (82), Bahrain (20), Iran (39),Qatar (15), Saudi Arabia (147), Turkey(97), and the UAE (115). On the Asianside, the leaders include China/HongKong (122), Indonesia (72), Japan(223), Malaysia (55), Pakistan (34),Philippines (42), Singapore (26),South Korea (33), and Thailand (48).India also continues to grow as aBusiness Aviation center. With a totalfleet of 201, this is a 33 aircraftincrease from 2008.

Australia, Oceania and Africa

Australia and Oceania continued itstrend of posting a slow but steadyincrease, with a total increase of 18 air-craft, which is down from the 38 air-craft added last year. Countries thatenjoyed an increase include Australia(+8), Fiji (+2), New Zealand (+9), andPapua New Guinea (+4). Those withdecreases include French Polynesia,New Caledonia and Tahiti.

Africa, on the other hand, continuesto enjoy significant growth. Coming offan 8.9 percent increase in growth over2008, in 2009 Africa topped itself byadding 139 aircraft for a 15.3 percentincrease in rate of growth. The leadercontinues to be South Africa, who is aTop Ten member, but such countriesas Angola, Botswana, Egypt, Kenya,Morocco, Nigeria and Tanzania contin-ue to add to their fleets.

Looking Ahead

2009 was a rough year – and chancesare 2010 will be slow going too as theeconomy struggles to pull itselftogether. Yet the future of BusinessAviation continues to look promising.New markets are opening and othersare seeing new benefits for BusinessAviation. How will our 2010 FleetReport read? It’s hard to say, but we’reguessing the world fleet will continueto climb.

REGIONSBusiness

Aviation is

booming in India,

the Middle East

and Africa.

R E P O R T 2 0 0 9 B U S I N E S S A I R C R A F T F L E E T

BART: FEBRUARY - APRIL - 2010 - 41

For the sixth year in a row,BART International hasteamed up with the expertsat Avinode, an independentEuropean online charternetwork, to provide an in-depth statistical overview ofthe European BusinessAviation Industry.

2

009 can best be summarized as ayear of slow recovery for thecharter industry. In 2008, 585,000

searches and 500,000 requests weresent. In comparison, 2009 saw thesenumbers drop to 473,572 request, withdemand hovering slightly below 2008levels (see charts). But this is not nec-essarily bad news as, if one looks atthe numbers, it becomes clear thatthings are getting better – as bothdemand and requests saw a steadyincrease as the year progressed.

In fact, at the close of 2009 demandactually exceeded 2008 levels withsearches peaking over 180,000 inDecember. This is slightly up from theroughly 170,000 made during thesame month in 2008. Also, the patternof searches and requests remained thesame, with both years showing a sharpincrease during the summer months(mainly July) and a gradual increase toclose the year.

Needless to say, the reason for thisoverall drop is the global financial cri-sis and its significant affect on thecharter industry. Out of the BusinessAviation sector, perhaps the charterindustry took the quickest hit, with anumber of charter companies goingout of business, particularly in Europeand the US. However, the late increasein numbers is also proof that therecovery has begun and – although itmay be slow – the worse is likelybehind us.

Year Month Total Sent Requests

2009 Jan 26,734

2009 Feb 26,550

2009 Mar 31,372

2009 Apr 34,460

2009 May 39,315

2009 Jun 45,807

2009 Jul 51,420

2009 Aug 47,608

2009 Sep 41,827

2009 Oct 42,561

2009 Nov 41,691

2009 Dec 44,227

RECOVERYCharter demand

exceeded 2008

levels at the end

of the year.

R E P O R T C H A R T E R I N D E X

PULLING THROUGH

2009 2009 2009 2009 2009 2009 2009 2009 2009 2009 2009 2009

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

60,000

50,000

40,000

30,000

20,000

10,000

0

NUMBER OF CHARTER REQUESTS SENT PER MONTH

42 - BART: FEBRUARY - APRIL - 2010

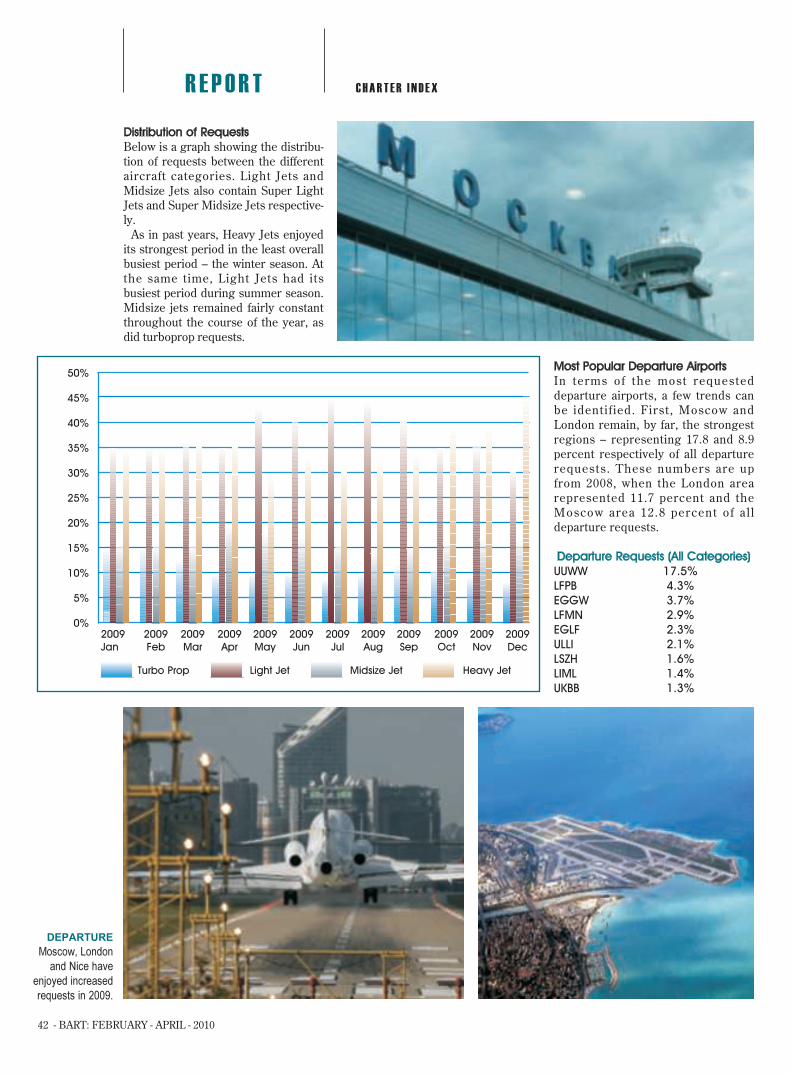

Distribution of Requests

Below is a graph showing the distribu-tion of requests between the differentaircraft categories. Light Jets andMidsize Jets also contain Super LightJets and Super Midsize Jets respective-ly.

As in past years, Heavy Jets enjoyedits strongest period in the least overallbusiest period – the winter season. Atthe same time, Light Jets had itsbusiest period during summer season.Midsize jets remained fairly constantthroughout the course of the year, asdid turboprop requests.

Most Popular Departure Airports

In terms of the most requesteddeparture airports, a few trends canbe identified. First, Moscow andLondon remain, by far, the strongestregions – representing 17.8 and 8.9percent respectively of all departurerequests. These numbers are upfrom 2008, when the London arearepresented 11.7 percent and theMoscow area 12.8 percent of al ldeparture requests.

Departure Requests (All Categories)

UUWW 17.5%

LFPB 4.3%

EGGW 3.7%

LFMN 2.9%

EGLF 2.3%

ULLI 2.1%

LSZH 1.6%

LIML 1.4%

UKBB 1.3%

DEPARTUREMoscow, London

and Nice have

enjoyed increased

requests in 2009.

R E P O R T C H A R T E R I N D E X

2009 2009 2009 2009 2009 2009 2009 2009 2009 2009 2009 2009

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Turbo Prop Light Jet Midsize Jet Heavy Jet

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

BART: FEBRUARY - APRIL - 2010 - 43

ARRIVALCosta Smeralda,

Malaga (left) and

Rome show up in

the arrival top ten.

Trends

In the turboprop sector, the top ten listis dominated by western and northernEuropean cities. However, for light jets,the list for departures is mixed – cover-ing both European staples asBordeaux, Nice and Geneva, along withMoscow’s Vnukovo and Kula Lumpur.Eastern Europe continues to develop asa prominent location for midsize jets,where the numbers far outpace thoseof smaller aircraft categories. Moscow,St. Petersberg and Kiev are all repre-sented on this years top ten list – alongwith Dubai at the number six position.Heavy jets remain international inscope, with Teterboro, St. Martin,London, Moscow and Dubai represent-ed in the top ten. In terms of overallpercentage, the Moscow region domi-nates in both the mid and heavy cate-gories, checking in at 29.4 and 28 per-cent respectively.

Turbo Props

LFPB 5.8%

EHRD 2.1%

EGGW 2.1%

LSGG 2.1%

EBAW 1.9%

LOWW 1.8%

EHAM 1.8%

LSZH 1.8%

LFMN 1.8%

EBBR 1.8%

Light Jets

LFPB 5.8%

LFMN 4.2%

LSGG 4.0%

UUWW 3.7%

EGGW 3.4%

EGLF 2.8%

LIML 2.5%

LSZH 2.1%

EGKB 1.8%

LFMD 1.7%

Mid-Size

UUWW 29.0%

ULLI 3.5%

EGGW 2.8%

LFPB 2.6%

LFMN 2.4%

OMDB 2.0%

LSGG 2.0%

KTEB 1.9%

UKBB 1.5%

EGLF 1.4%

Heavy

UUWW 27.6%

EGGW 4.5%

LFPB 3.9%

LFMN 2.8%

ULLI 2.8%

LSGG 2.7%

KTEB 2.1%

EGLF 1.8%

OMDB 1.8%

LSZH 1.5%

Most Popular Arrival Airports

As an overall trend, people typical-ly f ly from North to South, withsuch c i t ies as Costa Smera lda ,Malaga and Rome showing up inthe arrival top ten. Turbos signifi-cantly follow this North to Southf ly ing pat tern , whereas in theheavy jets sector one sees moremajor city destinations as Dubaiand New York.

When compared to departure air-ports, Moscow’s overall 4.9 percentof all arrivals shows that once againMoscow remains a popular regionfor departing. A similar pattern canbe seen in London, although not assignificant.

44 - BART: FEBRUARY - APRIL - 2010

All Categories

UUWW 4.8%

LFMN 3.8%

LFPB 2.9%

LSGG 2.6%

EGGW 1.9%

LIEO 1.6%

OMDB 1.4%

LSZH 1.3%

LEMG 1.2%

LIRA 1.2%

Turboprops

LFPB 2.5%

LFMN 2.2%

LSGG 1.7%

EDDV 1.4%

LFTZ 1.2%

LIRA 0.9%

EDDM 0.9%

EBBR 0.8%

EIDW 0.8%

LIEO 0.8%

Light Jets

LFMN 4.1%

LFPB 3.6%

LSGG 2.9%

LIEO 2.3%

UUWW 2.1%

LEIB 1.5%

LIRA 1.5%

EGGW 1.4%

LFMD 1.4%

LSZH 1.3%

Mid Size

UUWW 6.6%

LFMN 3.9%

LFPB 2.3%

OMDB 2.2%

LSGG 2.2%

EGGW 1.8%

ULLI 1.6%

LEMG 1.5%

LTAI 1.4%

UKBB 1.2%

Heavy Jets

UUWW 5.2%

LFMN 3.5%

OMDB 2.8%

VRMM 2.7%

EGGW 2.7%

LFPB 2.6%

LSGG 2.5%

KTEB 1.8%

LSZH 1.3%

KMIA 1.2%

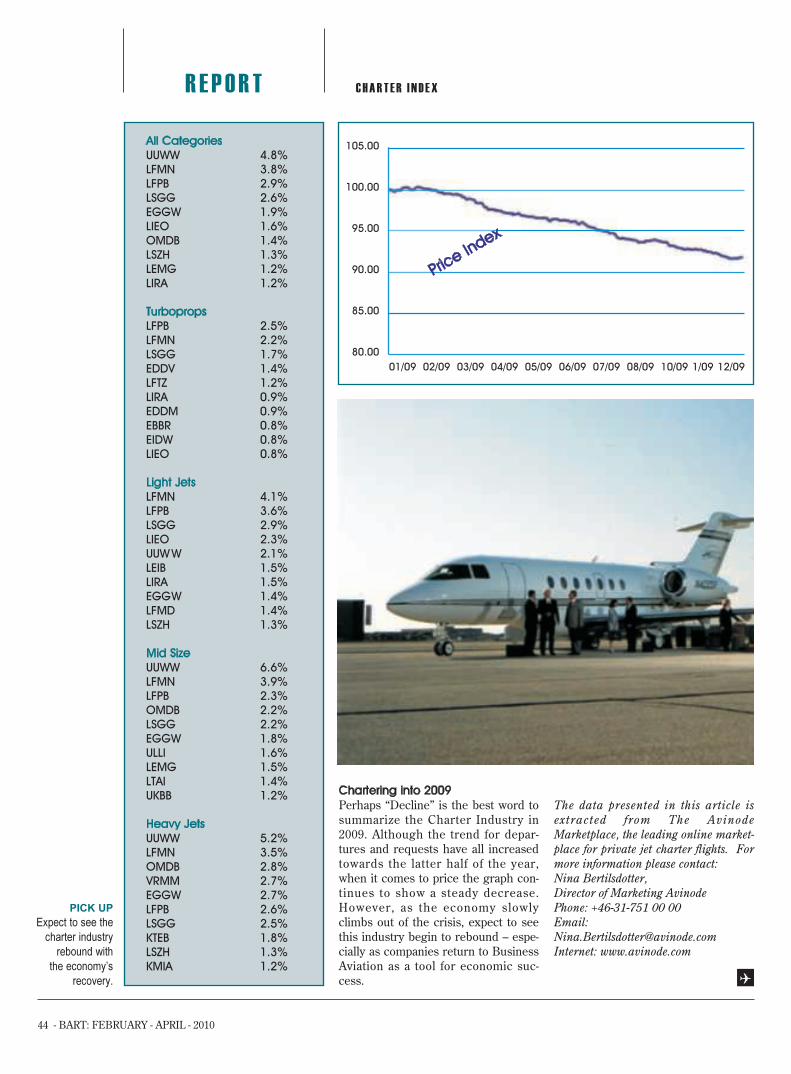

Chartering into 2009

Perhaps “Decline” is the best word tosummarize the Charter Industry in2009. Although the trend for depar-tures and requests have all increasedtowards the latter half of the year,when it comes to price the graph con-tinues to show a steady decrease.However, as the economy slowlyclimbs out of the crisis, expect to seethis industry begin to rebound – espe-cially as companies return to BusinessAviation as a tool for economic suc-cess.

The data presented in this article isextracted from The AvinodeMarketplace, the leading online market-place for private jet charter flights. Formore information please contact:Nina Bertilsdotter,Director of Marketing AvinodePhone: +46-31-751 00 00Email:[email protected]: www.avinode.com

PICK UPExpect to see the

charter industry

rebound with

the economy’s

recovery.

R E P O R T C H A R T E R I N D E X

01/09 02/09 03/09 04/09 05/09 06/09 07/09 08/09 10/09 1/09 12/09

105.00

100.00

95.00

90.00

85.00

80.00

Price

Index