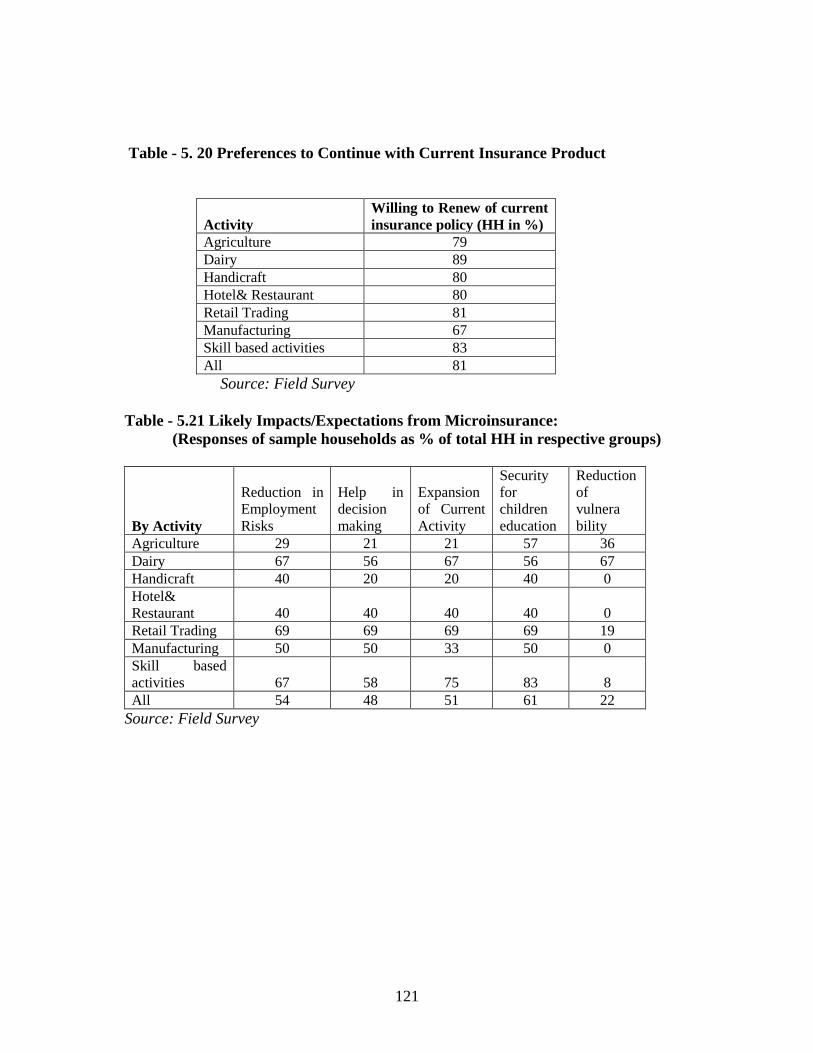

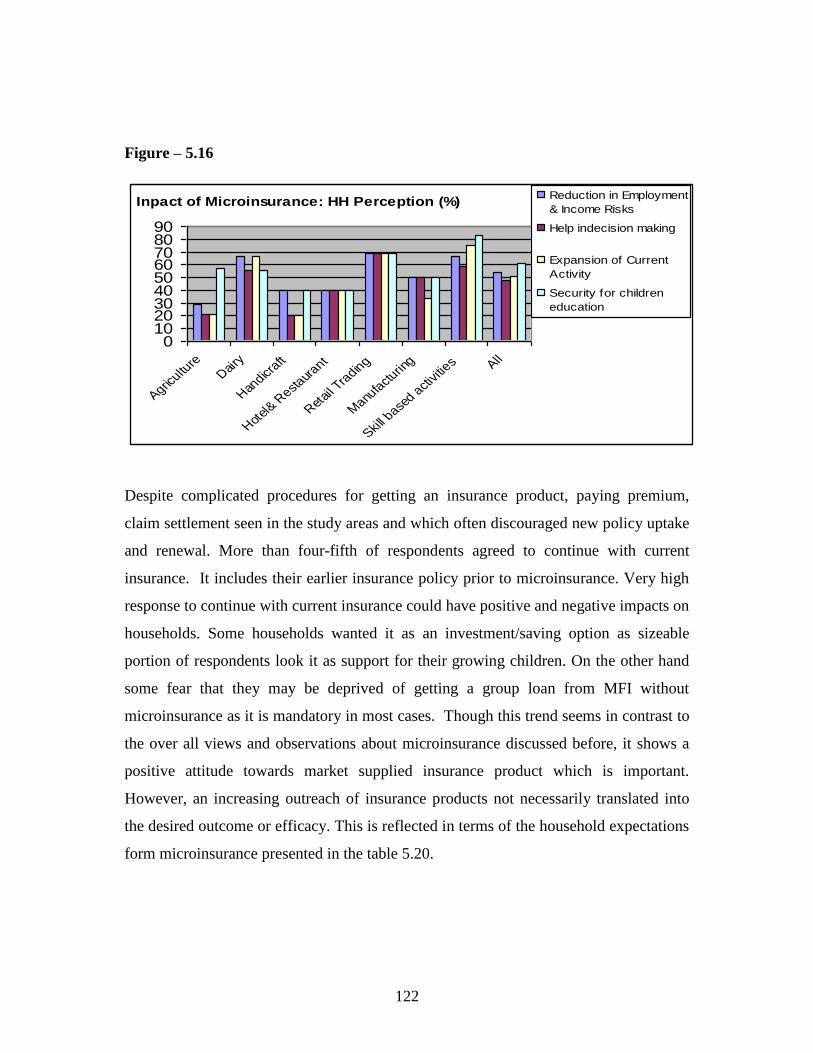

Reoprt on Microinsurance in India _Final

157

1 Microinsurance in India: Outreach & Efficacy Basanta K. Sahu, Researcher Centre for Microfinance Research (CMR) (Main Centre, Lucknow) Bankers Institute of Rural Development (BIRD) Lucknow-226012

-

Upload

farheen-ahmad -

Category

Documents

-

view

35 -

download

3

description

microinsurance report

Transcript of Reoprt on Microinsurance in India _Final

1

Microinsurance in India: Outreach & Efficacy

Basanta K. Sahu,

Researcher

Centre for Microfinance Research (CMR)

(Main Centre, Lucknow)

Bankers Institute of Rural Development (BIRD)

Lucknow-226012

2

ACKNOWLEDGEMENTS

The study benefited from the experiences of members of self-help groups, microcredit

clients, MFIs, insurers (microinsurance), bankers, experts, researchers and others,

particularly from the states of Tamilnadu and Orissa who provided some critical and

interesting insights. Support from MFIs (ASA Gram Vidiyal, Mahasemam and

BISWA) during the field survey was invaluable in covering different groups.

Several rounds of discussions with the Director, BIRD and others at CMR, BIRD,

Lucknow helped me in providing a proper direction to this study. Support from office

staff at BIRD is also duly acknowledged without which the document preparation

would have been difficult.

Thanks are also due to Mr. Arvind Yadav who generously helped with the data

processing work for the study.

Usual disclaimer applies.

3

CONTENTS

Page No

Acknowledgement

Executive Summary

7-10

Chapter - 1

Introduction

Meaning and Definition of Microinsurance

Microinsurance India

Microinsurance & Social Security

Review of Literature

Structure of the study

11-27

Chapter -2 Objectives, Methodology, Data & Study Areas

Partner-Agent Model of Microinsurance

Advantages and Limitation of Agent -Partner Model

Research Questions:

Objectives

Methodology

Selection of Study Area

Data Collection

Sampling & Data Collection Methods

Features of Methodology

Field Visit

Primary Data Analysis

Limitations of the Study

28-39

Chapter -3 Insurance Sector in India and Outreach of

Microinsurance

Performance of Insurance Sector in Post-Reform Period

Obligations of Life insurers

Outreach of Microinsurance in India

Opportunity for Microinsurance in India

40-51

Chapter -4 Introduction to Select MFI & Microinsurance in Study

Areas

Introduction

BISWA, (Sambalpur, Orissa)

Mahasemam, (Madurai, Tamil Nadu)

ASA Gram Vidiyal, (Tiruchirapally

Comparative Observations & Suggestions of MFIs on

Microinsurance

Summary

52-74

4

Chapter -5 Microinsurance, Household Risks and Coping Strategy

in Study Areas

Household Features

House Types

Education & Skills

Household Employment Pattern

Household Income Pattern

Household Borrowing & Saving Pattern

Household Asset Holding Pattern

Household Participation in Microinsurance

Microinsurance and Household‘s Perception and Priority

Demand for Insurance

Summary

75-124

Chapter -6 Conclusions & Policy Suggestions

125-132

References

133-135

Appendix – I: Case Study on Understanding Insurance

Products and its Use

136-137

Appendix - II Some Socio-Economic Features of

Selected States in India

137

Appendix – III Questionnaire for Household

138-150

Appendix – IV Questionnaire for MFI

151-153

Glossary

154-157

5

List of Tables:

Title Page

Table – 1.1 Population Excluded from Insurance in South Asian Countries

Table – 1.2 Key Issues & Findings on Microinsurance: a brief review

Table – 2.1 Sample Size and Study Areas

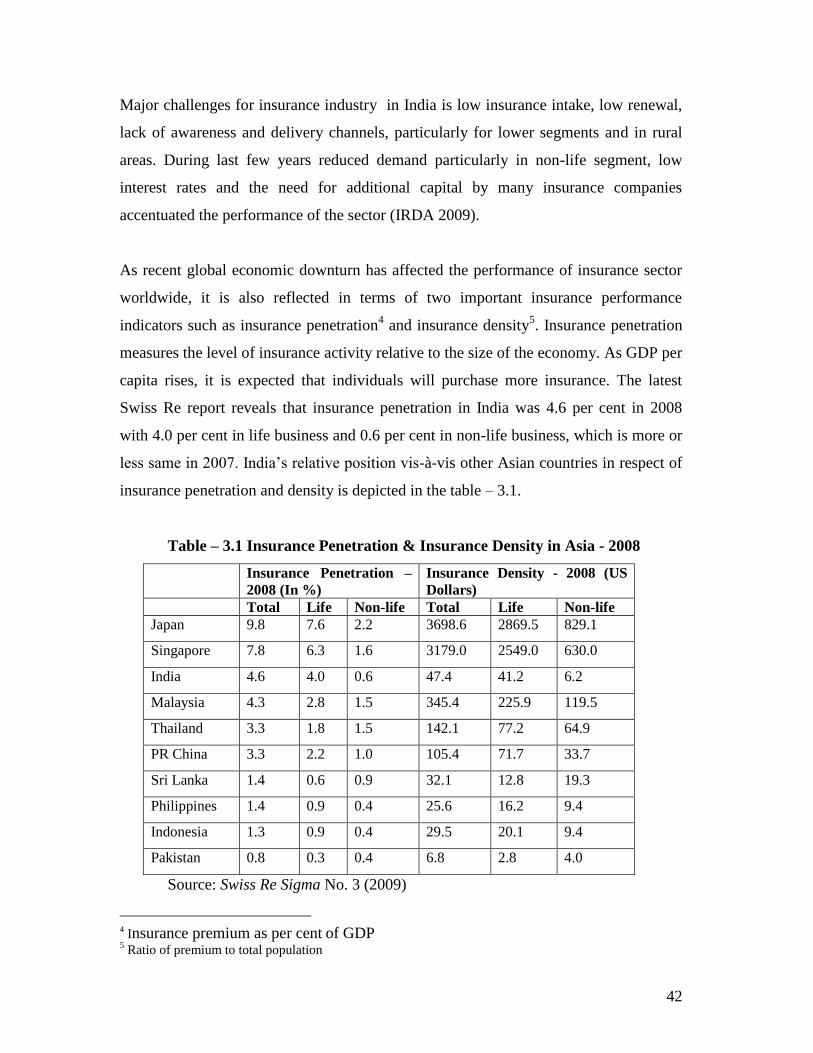

Table – 3.1 Insurance Penetration & Insurance Density in Asia

Table – 3.2 Insurance Policies Issued during 2008-09

Table – 3.3 Microinsurance Business during 2008-09 (LIFE) Table – 3.4 IRDA Prescribed Range of Microinsurance Cover

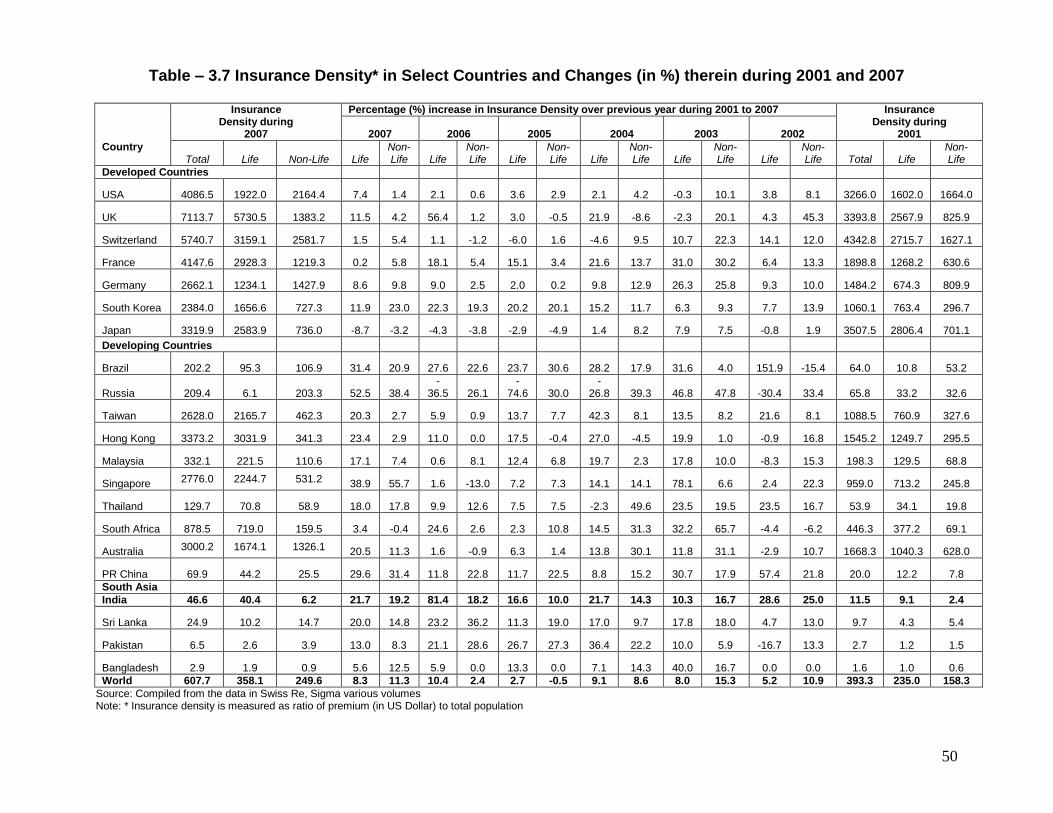

Table – 3.5 Insurance Penetration in Select Countries & Changes -2001-07

Table – 3.6 Insurance Density in Select Countries and Changes -2001-07

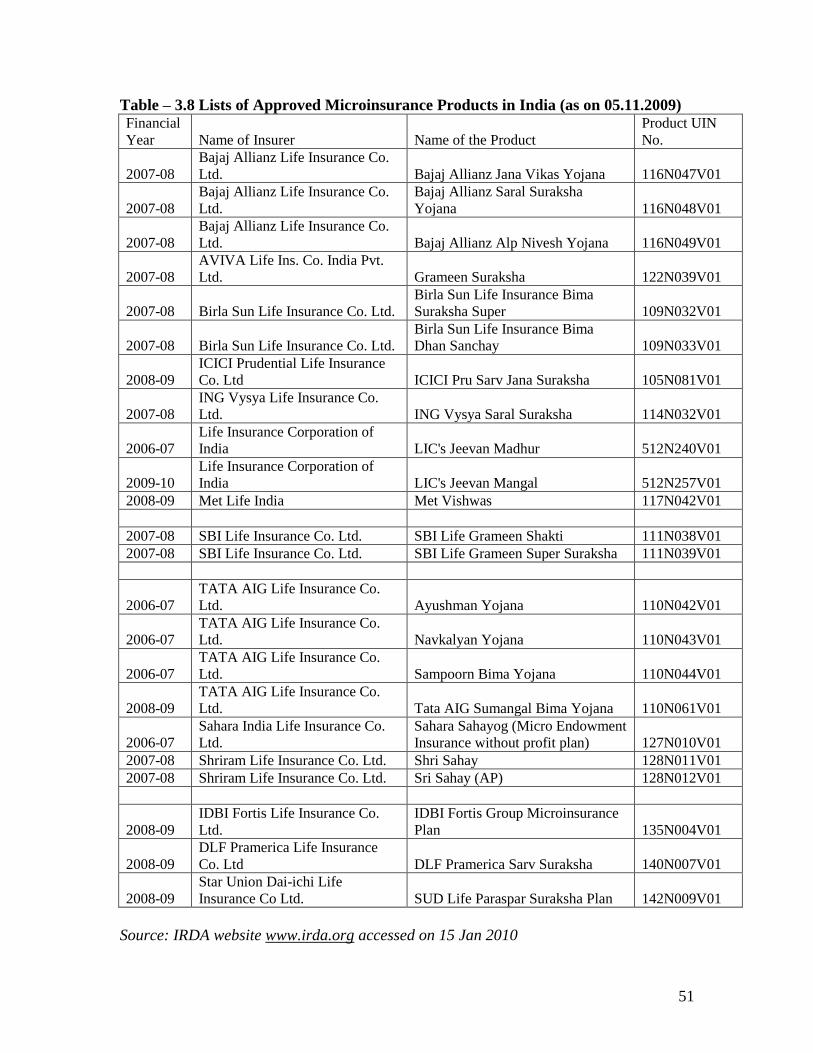

Table – 3.7 Lists of Approved Microinsurance Products in India

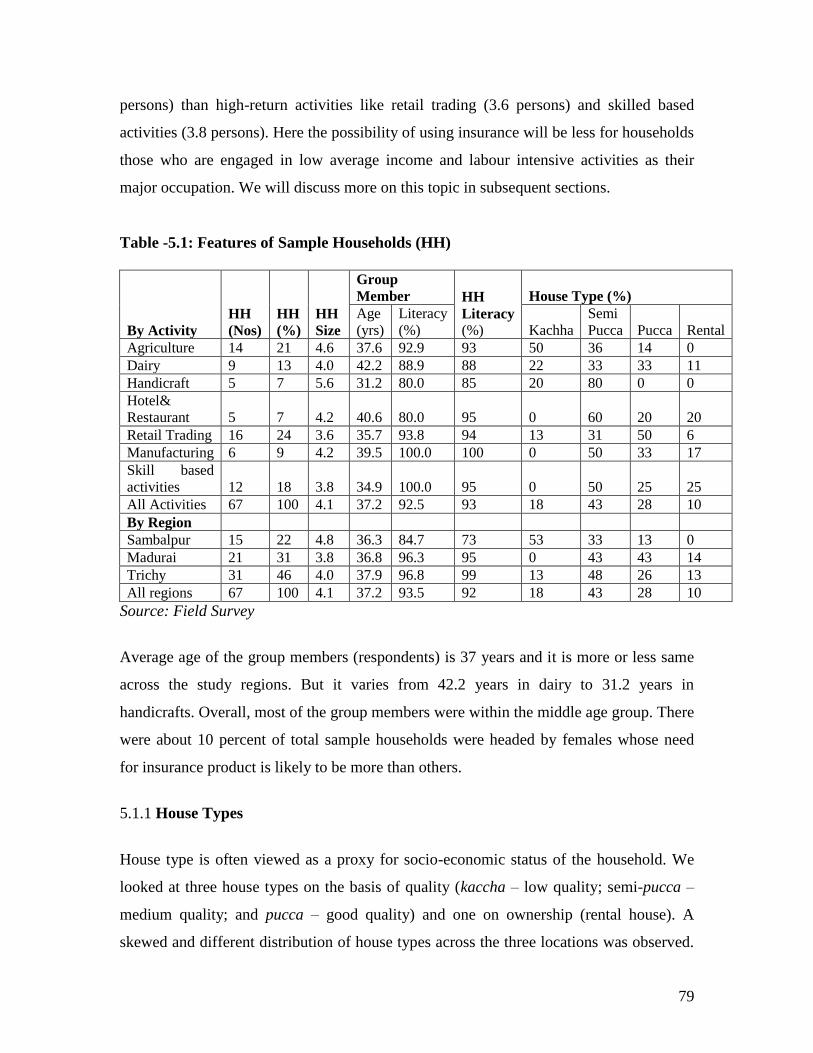

Table – 5.1 Features of Sample Households

Table – 5.2 Level of Education of Group Members (in %)

Table – 5.3 Household Employment by Activity, Region & Sex

Table – 5.4 Household Income by Activity, Region and Sex

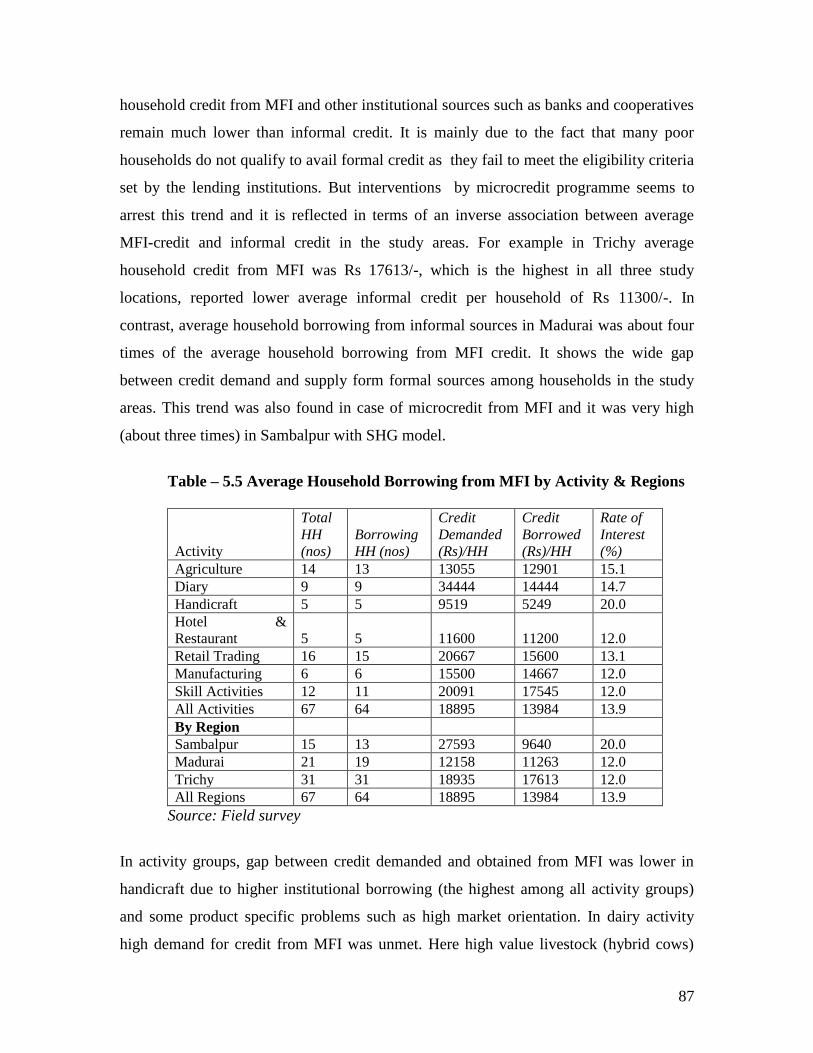

Table – 5.5 Household Borrowing from MFI by Activity & Regions

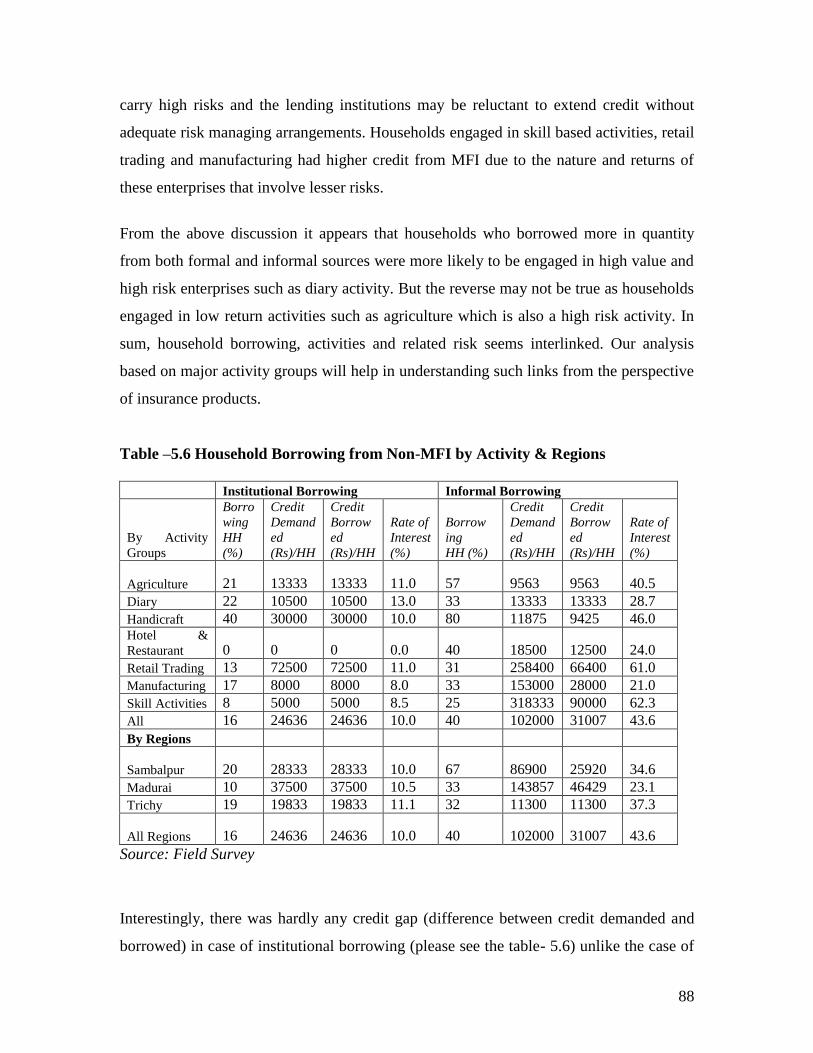

Table – 5.6 Household Borrowing from Non-MFI by Activity & Regions

Table – 5.7 Household Saving Pattern by Activities & Regions

Table – 5.8 Asset Holding Pattern of Sample Households in Study Areas

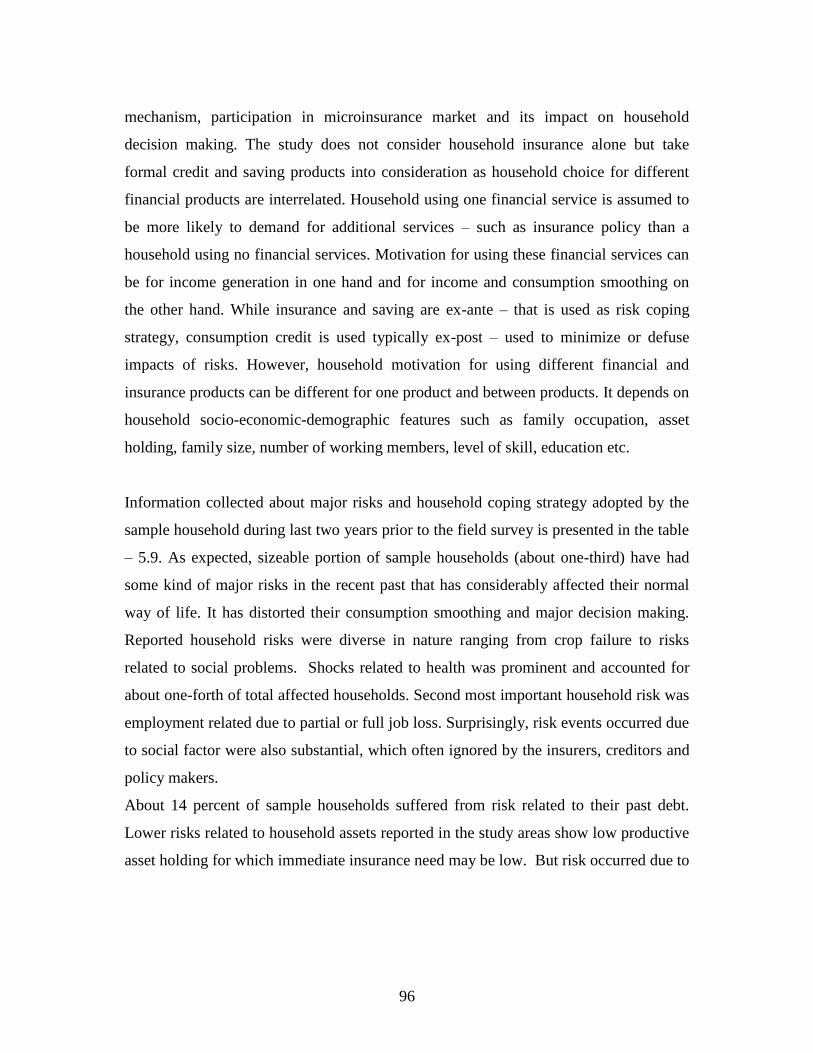

Table – 5.9 Types of Household Risks & Coping Strategy in Study Areas

Table- 5.10 Household Perception about Insurance & Risks Management

Table- 5.11 Intra-Household Risk Management

Table- 5.12 Intra-Household Risk Strategy: Reduction in Food Expenditure

Table- 5.13 Insurance Awareness & Insurance Related Problem

Table- 5.14 Household‘s Insurance Holding Pattern by Activity & Regions

Table- 5.15 HH Preference to Continue with Current Insurance Product

Table- 5.16 Distribution of Demand for Insurance by Type of Risks

Table–5. 17 Correlation table

Table- 5.18 Distribution of Demand for Insurance by Activity Group

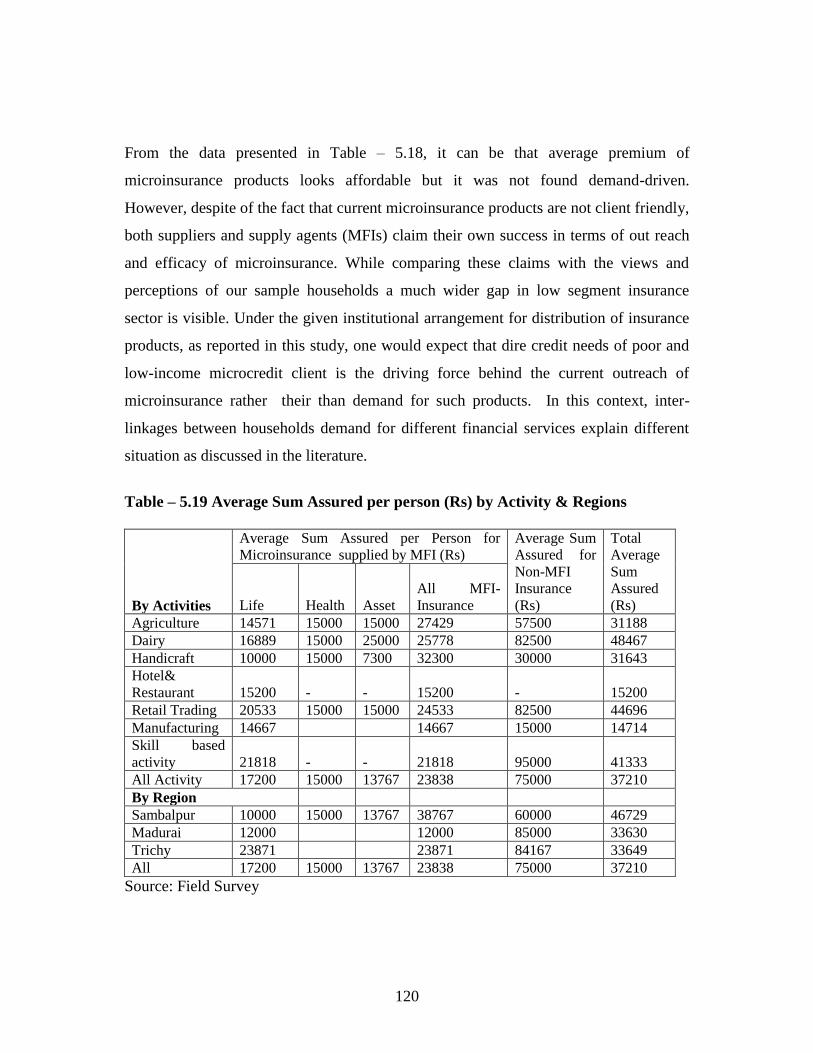

Table- 5.19 Average Sum Assured per person (Rs) by Activity & Regions

Table- 5.20 Average Premium per Person (Rs) by Activity & Regions

Table- 5.21 Impact of Microinsurance: Expectations of Sample Households

6

List of Charts

Title Page-No.

Chart –3.1 Insurance Density in Select Countries in World

Chart –3.2 Insurance Density in South Asian Countries 2001-07

Chart- 3.3: Change in Insurance Density in South Asian Countries

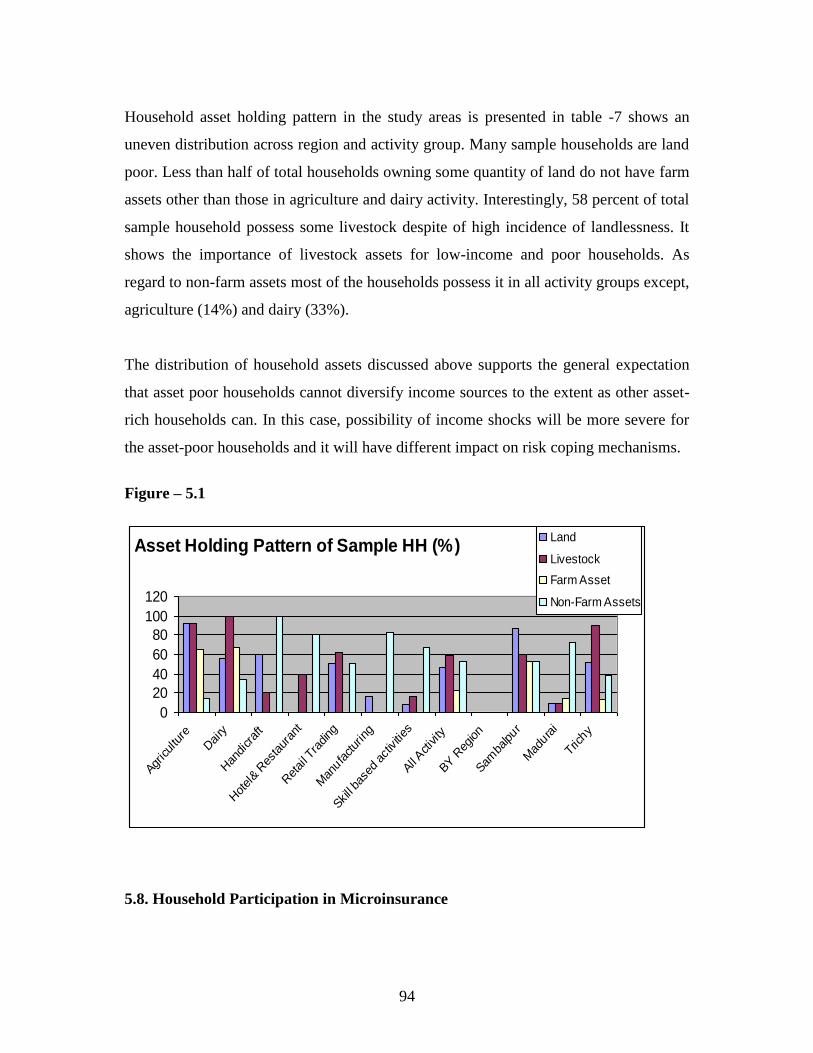

Chart –5.1: Asset Holding Pattern of HH

Chart –5.2 – Type of Household Risks in Study Areas

Chart –5. – Household Risks Coping Strategy in Study Areas

Chart –5.4 – Who gets Affected worse without insurance

Chart –5.5 – Can Insurance Manage HH Risks

Chart–5.6 – Intra-Household Risk Management: Increase in

Working Hours

Chart–5.7 Intra-Household Risk Management: Health Exp

Chart–5.8 Intra-Household Risk Management: Education Exp.

Chart–5.9 Intra-Household Risk Management: Food Exp.

Chart–5.10 Problem Related to Microinsurance

Chart–5.11 Household Awareness about Insurance

Chart–5.12 Household Insurance Holding

Chart–5.13 Household Demand for Life & Health Insurance

Chart–5.14 Distribution of HH Demand for Insurance (%HH)

Chart–4.15 Average Premium of HH

Chart–5.16 Impact of Microinsurance

7

Executive Summary

1. Coping with risks such as health problems, crop failure, loss of livestock, death of a

family member, loss of asset, income and employment is much harder on the part of

poor and low income groups than others. Many poor households involve in activities of

smaller scale but carrying higher degree of risk and uncertainty and hence prone to

financial and income risks.

2. Microinsurance is believed to work as a powerful risk management tool for low income

and vulnerable groups by preventing them from falling into the poverty trap. But not

much is known about outreach and efficacy of microinsurance across regions and

groups.

3. In India, though government plays a proactive role in providing insurance cover to the

poor through subsidized insurance schemes and other programmes. The size and

potential of microinsurance market is enormous due a sizeable portion of poor and low

income population who live without any formal insurance.

4. A recent UNDP study (2007) found that about 90% of the Indian population (950

million people) is not covered by insurance and it constituted an untapped market of

about US$2 billion. India has lower insurance penetration of 4.7 percentage (ratio of

premium to GDP) and insurance density of USD 46.6 (ratio of premium to population)

compared to world average of 7.5 percent and USD 607.7 respectively. However,

within South Asian region, India has experienced a positive and faster change in

insurance density in recent years.

5. More than 50 microinsurance schemes are in operation in India and most of them have

been launched during last 4-5 years. Around 43 schemes cover 5.2 million people and

about 66% insurance schemes are linked with micro finance services provided by

specific institutions (ILO, 2004a). Life and health insurance risk related products are

generally demanded by people. Most of these insurance schemes (74%) operate in 4

southern states: Andhra Pradesh (27%), Tamil Nadu (23%), Karnataka (17%) and

Kerala (8%). The microinsurance sector in India is characterized by uneven

development and limited to a few products.

6. The present study has attempted to analyze microinsurance in India under Partner -

Agent Model where, insurers utilize MFI as intermediary or delivery channel to provide

sales and basic services to the clients with lower administrative cost.

8

7. The present study is based on primary field survey covering 75 women micro credit

clients randomly selected from 23 centers in 11 development blocks in three districts of

two states (Trichy and Madurai in Tamil Nadu and Sambalpur in Orissa). The analysis

of microinsurance has been made mainly on the basis of information collected from

select MFIs and household data with focus on enterprise/occupation, groups and

regions.

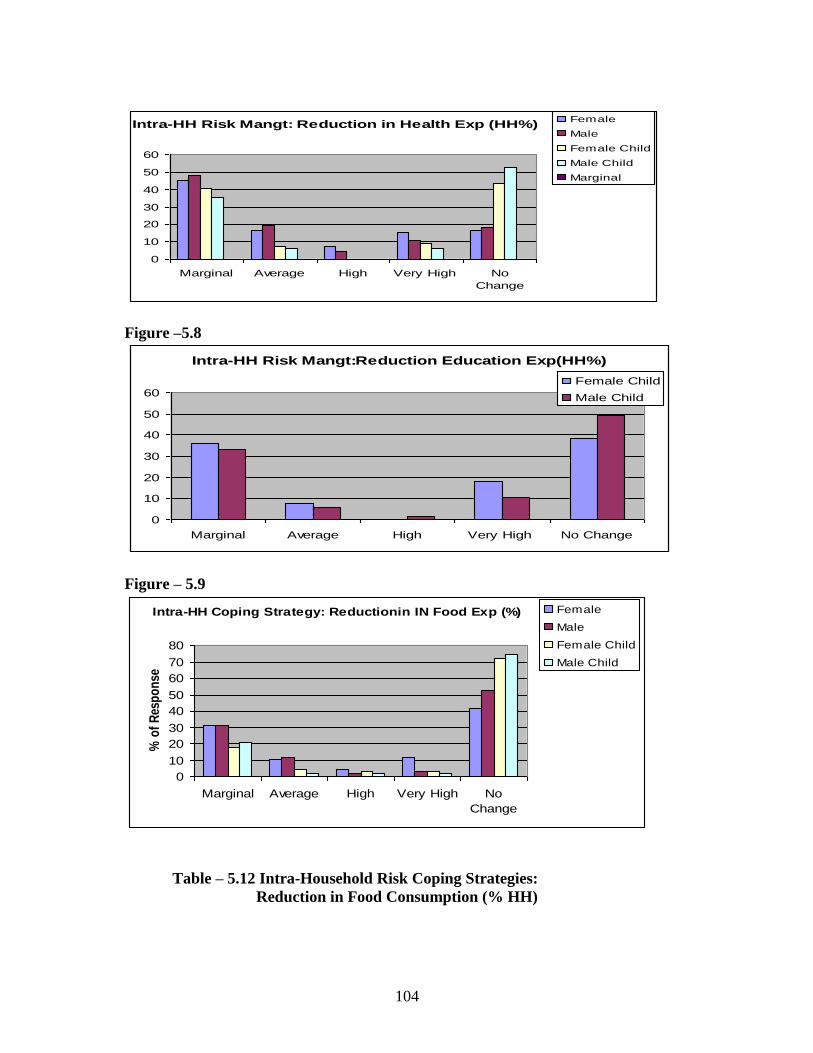

8. About a quarter of the sample households reported had faced some adverse (risk)

during last two years (prior to the date of field survey) that severely affected their

financial condition and economic situation. Common Risks observed among sample

household ranged from major health related expenditure, health problems of females,

accidents, crop loss, loss of livestock, market related problems, and other problems

such as divorce.

9. Common risk coping strategies adopted by households were reduction in household

expenditure ( on food, education and health), borrowing from informal sources, dis-

saving (in kind/cash), migrating out, distress sale of produce and other assets,

increasing average working hours (observed mainly among females), postponement of

social expenditures etc. However, these coping strategies were no longer found

adequate and effective to manage sharp fluctuations in household income and

consumption, especially when faced with multiple risk events.

10. Over and above the microinsurance product, (mostly life insurance of microcredit

clients comes with microcredit loan) the priority accorded to various risk coping

strategy among households varied across occupation groups and regions. About 42

percent households resorted to borrowing from informal sources, 18 percent

households used dis-saving, 16 percent households undertook supplementary non-farm

activity and about 14 percent undertook distress sale of assets as coping mechanism. To

some degree, this underscores the importance of linkage between savings, formal credit

and insurance in risk avoidance behavior of households.

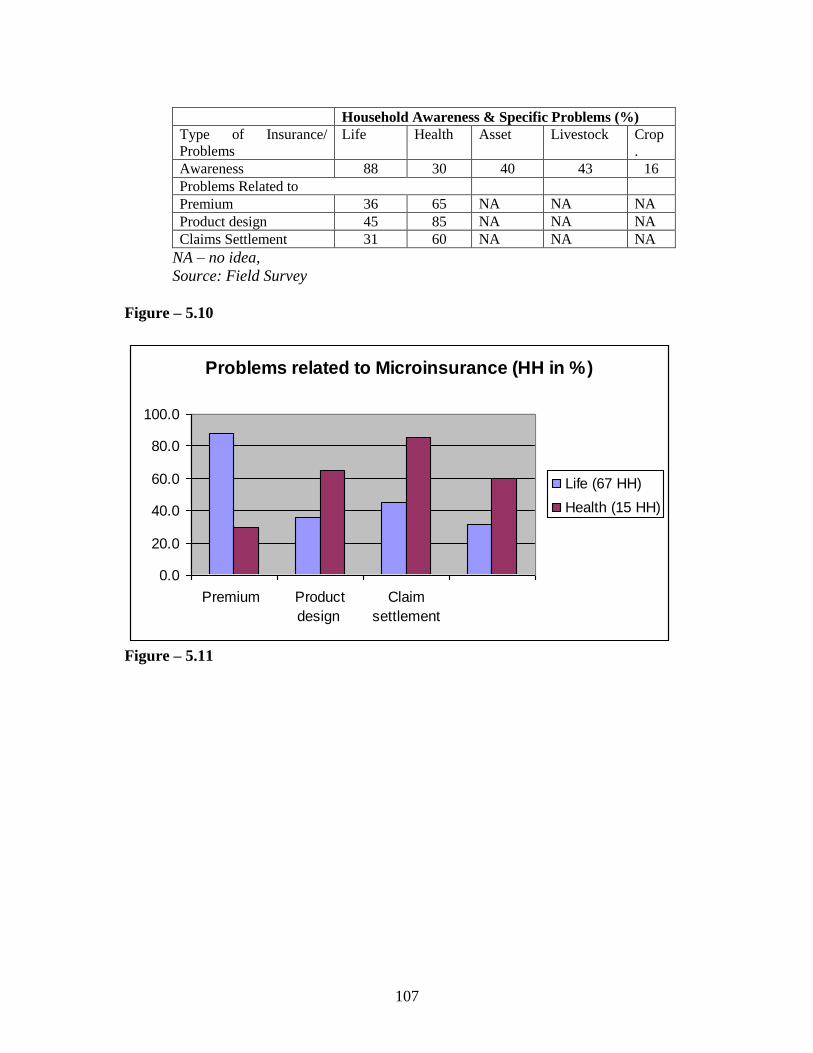

11. Though about 88 percent of sample households in the study had some idea about life

insurance their understanding was inadequate, unclear and very different. However,

lack of understanding, information and options for insurance products was found one of

the key constraints for wider outreach of insurance. About 44 percent of households

had heard about livestock and asset insurance but they did not possess any further

information. Surprisingly, only 30 percent households knew about health insurance and

only a few of them had tried it at least once. Preference for health insurance was more.

9

It reflects the gap between supply of microinsurance and potential demand for the same

among the poor households.

12. Similarly, households‘ complaints against existing insurance products were found to be

very high and it varied with different aspects of insurance products and household

characteristics. About 85 percent of households were not happy with the design of

insurance product offered to them. A sizeable proportion of households reported having

problems related to insurance premium (65 percent) and claim settlement (60 percent).

Non-coverage of spouse and other family members in life and health insurance scheme

was one of the main cause of dissatisfaction among households.

13. High male mortality rate (two to four times higher than female) was believed to be one

of the key factors for not providing coverage to spouse of the female group members,

especially when premium under microinsurance has been kept low.

14. However, findings of our analysis do not support the argument that a household‘s risk

assessment and experience of shocks has a direct correlation on household decision to

participate in insurance market. Households exposed more to risks are less likely to use

available formal insurance products than others. Some lower income groups feel that

use of insurance product as an additional risk as they have to pay premium regularly.

Their poor understanding about the functioning of insurance services and lack of trust

on the staff of insurers drives them away from insurance.

15. Household borrowing, saving, family size, level of education, asset holding etc. did not

reflect much association with household participation in insurance or continuance.

Many low income households reported using borrowing from informal sources in the

event of crisis such as illness, crop loss, livestock loss and death of a earning member

rather than participating in any formal insurance scheme.

16. However, household participation in insurance, through microcredit programme by

MFIs was found to be mostly involuntary in nature. Many microcredit clients believed

that it is difficult to pay premium out of their small loan amount from MFIs. Under the

given arrangement and conditions of household borrowing from MFIs, insurance

uptake did not appear to be very effective.

17. It appears that there is a vicious circle of uptake and renewal of insurance products in

operation. The situation of inability to pay premium led to a position of no insurance

cover (no risk cover – more vulnerable to risks of income and expenditure – high cost

of coping with risks - borrowing and liquidation of asset – low capacity and

productivity – low income - inability to pay premium/- no insurance).

10

18. In many cases, what poor households are willing to pay and able to pay for the

insurance was led to inability to cover risks adequately. Under this situation, dire credit

need of poor households often surpasses their need for insurance.

19. Demand for insurance found to be dependent on household income flows, nature of

enterprise or activities undertaken.

20. On supply side, constraints of the insurers and intermediaries (MFIs) help to explain

why there has been so little development of the microinsurance market. While insurers

look to experiment and explore the large client base of MFIs and to fulfill the social

and rural obligations imposed by the regulator, the intermediaries (MFIs) are keen to

protect their credit. It also partly explains the low voluntary demand for insurance and

wide gaps between the client‘s needs and insurance products on offer.

21. MFIs as distribution channel of microinsurance can prove to be useful in reducing

administrative costs of penetrating rural markets, but underutilization of this

distribution channels is visible. Though MFIs enjoy flexibility to choose insurance

partner through bargaining process, some of them change insurance partners frequently

which further affects the insurance activity.

22. The microcredit-linked insurance business is one of the key factors for growth of the

microfinance sector in India. For the insurers, it is beneficial to gain access to the huge

rural client base of MFIs and there is enormous market potential for customized

insurance products and dire need for innovation. In this regard, a comprehensive

health-cum- livestock insurance product, particularly in lower segment may offer better

opportunity.

23. Creation of complete awareness, flexibility for premium payment options, efficient

claims processing system, trained and trustworthy insurance agents or staff and

effective client redressal system are some core areas for policy intervention. Role of

MFIs along with involvement of local institutions (Gram Panchayat, Gram Sabha and

other community based institutions) could be useful in addressing insurance related

matters such as, claim settlement, premium payment, client identification in

consultation with the insurers. The documentation and submission of proof of claim

need to be standardized. Insurers should involve MFIs and representatives of clients in

product design and development. MFIs may obtain clients feed-back and use it in

negotiations with the insurers. Better incentives for intermediaries and training for field

staff are also suggested.

11

Chapter - 1

Introduction

Risk is pervasive in the lives of poor and low-income groups. Economic, social, natural,

and other factors distort household‘s risk management capability and their struggle to

come out of poverty. Faced with multiplicity of risks, poor and weaker sections are

often forced to deplete their financial, physical, social and human assets just to cope

with the contingencies. Some common risks they confront with are unemployment,

illness, accident, death of main earning members of the family, crop loss, loss of

livestock, fire, theft, drought, flood, and loss in petty trading activity due to market

factors. Some groups are more vulnerable to many of these risks than the others and

unable to cope with risk events. Hence, uninsured risk leaves many poor households

more vulnerable to the losses from negative shocks. However, impact of such risks

lingers for a longer period depending on the nature and severity of risks and strategy

adopted by the household for coping. On the other hand, household exposure to risks

not only results in substantial financial losses but also the suffering accentuates the fear

and uncertainty relating to the risk. Because of this perpetual apprehension, many poor

households are less likely to take advantage of income-generating opportunities which

could be a way out of poverty.

Risk pooling and informal insurance are not entirely new to many low income

households. Informal risk-sharing practices have been around for generations. Options

for protecting against risks includes diversifying household resources and income,

building assets, stocking food, investing in livestock, renewing & strengthening social

networks, saving and borrowing from informal sources, participating in public social

security programme, enrolling in insurance schemes etc. The risk management

approaches differ under socio-economic and agro-climatic conditions and also

depending upon its exposure to risk. Unfortunately, risk coping mechanisms are limited

in assuring benefits and typically cover only a small portion of the total loss of income

and income generating opportunity. Household‘s informal means to manage risks may

12

not provide adequate and long term protection, especially to poor and low income

groups who are prone to loss of entitlements incurred due to variety of risks.

Households follow variety of coping strategies to manage different kind and nature of

risks that affect their income and consumption smoothing. But many informal risk

coping strategies come at a cost, as assets are depleted when trying to cope with risk

such as distress sale during crises, reduction of household expenditure on food,

withdrawing children from school, postponing or avoiding expenditure on health, social

functions etc. It has both short term and long-term adverse impacts on households.

Though household diversification often viewed as positive response against risk events

many such coping strategies followed by the poor do compensate the entire loss. If

household risks are not carefully designed and strategically handled it may result in

bigger welfare losses. The situation would be worse when risks to life and livelihoods

recur more frequently and there is limited risk managing options. So provision of

formal insurance cover to these vulnerable groups could be useful to protect them

against risks and supplement their risk managing capacity. As formal insurance can

directly impact on households‘ ex-post risk coping mechanisms, it is believed that

households participation in insurance would help to maintain income and consumption

soothing and avoid asset loss.

But access to and provision of formal insurance is limited for the poor and low income

groups. State-provided social security measures are inadequate to cover all kinds of

household risks. Under this condition many poor households may tend to behave as

resilient to risk events or their risk coping behaviour may result in huge welfare loss

due to wrongly managed or unable to manage risks. It may also induce many poor

households to focus on low risk and low return activities or rely on a range of informal

ex-post options, relief measures, public social security measures etc. It provides huge

scope for policy interventions as well as business opportunity.

Therefore, it is important from policy point of view to understand different household

risks and risk-management strategies in one hand and the need and demand for

13

insurance products, particularly for low income groups. On the other hand, interestingly

microinsurance has drawn attention of the policy makers, insurers, business leaders and

others in recent years. Microinsurance has been seen as one of the major risk managing

tools for the poor and low income groups and a potential market for business.

Experiences across countries in the world show that microinsurance has potential to

reduce household risk impacts and to provide business opportunity. By offering a

payout after the loss, it may avoid more costly ways of risk coping by the poor

household and leaves their future income earning opportunities intact. The sense of

security linked to being insured through microinsurance augment household welfare

with positive impacts.

Poverty and vulnerability among low income groups mainly stems from their poor risk

management capacity and exclusion from the financial markets. Hence it is important to

understand their need as well as demand for financial products including insurance.

Many poor and low income households may involve in activities or enterprises of

smaller scale but higher risk and uncertainty. It makes them disadvantageous because

they are more prone to economic and financial collapse. Under this situation it is

interesting to analyze how microinsurance can play a meaningful role in household risk

managing efforts, in rural credit and insurance market and providing business

opportunity. In this regard we like to focus on current scenario of outreach and efficacy

of microinsurance in India, major factors that encourage and prevent growth of

microinsurance and other related issues for achieving broader objectives such as

financial inclusion and inclusive development.

Meaning and Definition of Microinsurance:

Microinsurance, commonly called as insurance for the poor, has recently drawn the

attention of practitioners in developing countries. In common parlance, microinsurance

is the provision of insurance services to low-income households, which serves as an

important tool to reduce risks for the already vulnerable population. There is no

unanimously accepted definition of microinsurance despite its profound use and

understanding across stakeholders and others. A simple definition of microinsurance is

14

offered by Churchill (2006) is that it is an insurance that (i) operates by risk-pooling (ii)

financed through regular premiums and (iii) tailored to the poor who would otherwise

not be able to take out insurance. Microinsurance is defined as ―...insurance that is

accessed by the low-income population, provided by a variety of different entities, but

run in accordance with generally accepted insurance practices ... Importantly this means

that the risk insured under a microinsurance policy is managed based on insurance

principles and funded by premiums‖ (International Association of Insurance

Supervisors, 2007).

Microinsurance is different from usual form of insurance. A macro definition of

microinsurance states that it is the provision of financial protection contingent on the

occurrence of predefined risk in exchange for an ex-ante premium payment affordable

to the clients. In terms of micro definition, microinsurance is more complicated as there

are different approaches. ―Micro‖ as reference to low premium and low benefits may be

affordable but it may not be effective enough to manage risks of different types of

different categories of clients. Microinsurance is often believed to be an important

component of a broader set of financial services under microfinance – making available

financial services for poor households and enterprises to sustain their livelihoods.

Basically there are two broad categories of microinsurance often commonly understood

– one focused on extending social protection to the poor in the absence of appropriate

government schemes and the other offering a vital financial service to low-income

households by developing an appropriate business model that enables the poor to be a

profitable (or sustainable) market segment for commercial or cooperative insurers.

Microinsurance is also taken as group insurance that can cover thousands of customers

under one contract. It requires an intermediary between the customer and the insurance

company. This intermediary role has been played mainly by non-governmental

organization (NGO) and microfinance institutions (MFI). The role of intermediaries in

growth of microinsurance in India is well documented.

15

Currently around 135 million, or 5%, of low income people in developing countries are

using microinsurance products. But the size of insurance market for low income groups

is large and it constitutes about 1.5 to 3 billion potential clients (Microinsurance Centre,

2007). According to a research carried out by Swiss Re in 2007, most growth in the

insurance industry over the past decade has come from the wealthy and middle income

markets in emerging economies. Premiums grew by 3.3% globally and by 11.8% in the

emerging markets in that year. Though partly this was due to a growing number of

clients moving into the wealthy and middle income brackets in these countries, it is also

attributable to insurance expanding into new markets. The number of people covered

under microinsurance is estimated about 78 millions in 77 countries out of 100 less

developed countries (Roth et al 2007).

Microinsurance in India

In India development of microinsurance sector and related policy discussions has

started few years back. Within very short period, the sector has drawn attention of

policy makers due to its importance both at household level and the economy as a

whole. Two major and recent studies by the ILO (2004a and 2004b) depict broad

picture of microinsurance sector in India. As regard to the microinsurance products the

study highlights that out of 80 listed insurance products 45 cover only a single risk and

only two or three products cover multiple risks. Majority of the insurance products

cover life (52%) or accident-related risks and addressed to individuals. Out of the 12

currently available health insurance products seven products have been designed and

restricted to groups and five products have chosen to coverage to some critical illness at

individual level but not the reimbursement of hospitalization expenses. Most of the

products require a single payment of premium (i.e., a one-time payment) upon

subscription. Private insurers had three times more products than their public

counterparts.

Some important observations about the demand for microinsurance in India are made in

a recent study by ILO (2004b). The study provides details of micro-insurance schemes

operational in India. Out of 51 schemes that are operational in India most schemes

16

have started operations during the last few years. As regards to beneficiaries, about 43

schemes, for which the information is available, cover 5.2 million people. About 66%

of the microinsurance schemes are linked with micro finance services provided by

specialized institutions (17 schemes) or non-specialized organizations (17 schemes).

Twenty two percent of the schemes are implemented by community based

organizations, and 12% by health care providers. Life and health are the two most

popular risks for which insurance is demanded. Twenty-five out of 37 schemes received

some external funds to initiate their schemes. Twenty out of 32 schemes received

external technical assistance in the form of advisory services, technical services,

training or even referral services for their schemes. As regard, to the regional

distribution of microinsurance outreach about 74 % of total schemes operate in 4

southern states constituting Andhra Pradesh (27%), Tamil Nadu (23%), Karnataka

(17%) and Kerala (8%). Two western states Maharashtra (12%) and Gujarat (6%)

account for 18% of the schemes. About 56% of schemes deal with one single risk. This

shows low outreach and unequal distribution of microinsurance in the country. The

study also reflect the linkage between micro-insurance and micro-finance.

Development of microinsurance is often related to microcredit, particularly in

developing countries like India. Though microcredit has dominated in microfinance

market the entry of microinsurance is only in recent past. In India microinsurance is a

relatively new financial service and its outreach is rather limited and unevenly

distributed across states. The over all performance of microinsurance in India is not

very encouraging. According to a recent study by UNDP (2007), the outreach of

microinsurance is around 5 million people covering only 2 percent of the poor in the

country. It shows there is huge potential for microinsurance market in the country. A

conservative estimation of size of microinsurance market (both life and non life) in

India ranges between INR 62,304.70 to 84,267.55 million (US$ 1,384.55 to 1,872.61

million). In case of life insurance, the market potential is estimated to be between

INR15,393 to 20,141 million (US$ 342.07 to 447.58 million) and in case of non-life

insurance, it is between INR46,911.70 to 64,126.55 million (US$1,042.48 to 1,425.03

million). The non-life insurance estimation is limited to four types of coverage – milch

17

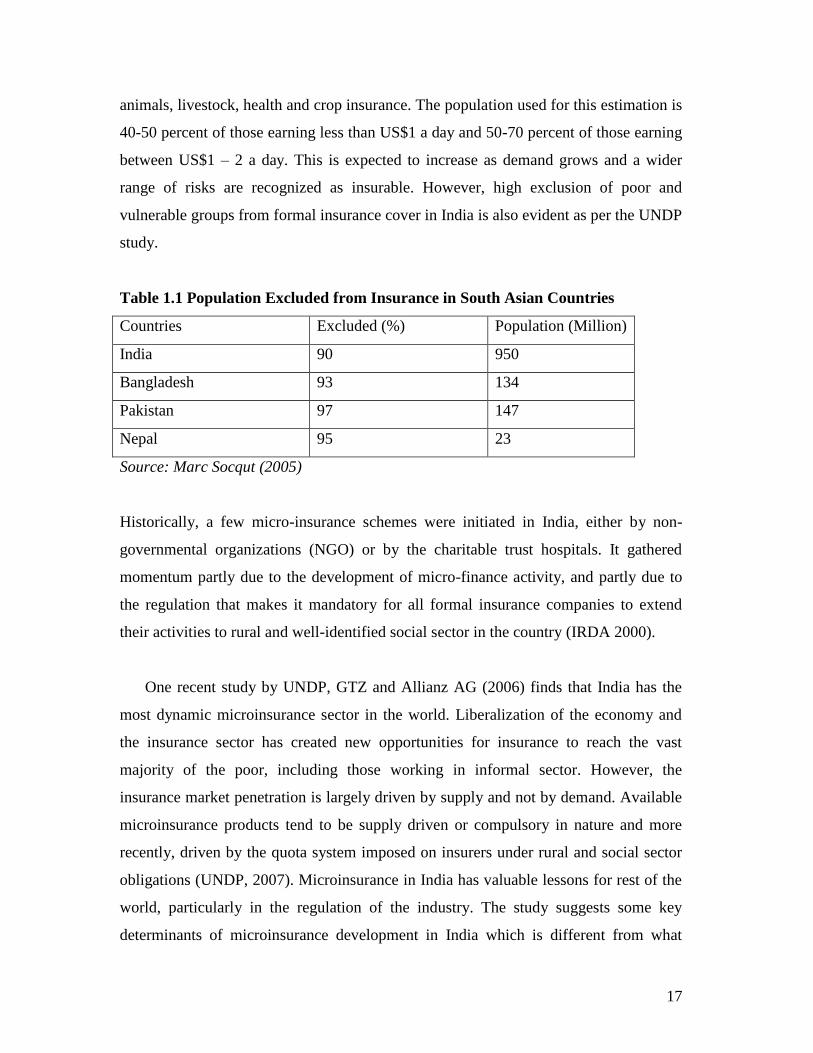

animals, livestock, health and crop insurance. The population used for this estimation is

40-50 percent of those earning less than US$1 a day and 50-70 percent of those earning

between US$1 – 2 a day. This is expected to increase as demand grows and a wider

range of risks are recognized as insurable. However, high exclusion of poor and

vulnerable groups from formal insurance cover in India is also evident as per the UNDP

study.

Table 1.1 Population Excluded from Insurance in South Asian Countries

Countries Excluded (%) Population (Million)

India 90 950

Bangladesh 93 134

Pakistan 97 147

Nepal 95 23

Source: Marc Socqut (2005)

Historically, a few micro-insurance schemes were initiated in India, either by non-

governmental organizations (NGO) or by the charitable trust hospitals. It gathered

momentum partly due to the development of micro-finance activity, and partly due to

the regulation that makes it mandatory for all formal insurance companies to extend

their activities to rural and well-identified social sector in the country (IRDA 2000).

One recent study by UNDP, GTZ and Allianz AG (2006) finds that India has the

most dynamic microinsurance sector in the world. Liberalization of the economy and

the insurance sector has created new opportunities for insurance to reach the vast

majority of the poor, including those working in informal sector. However, the

insurance market penetration is largely driven by supply and not by demand. Available

microinsurance products tend to be supply driven or compulsory in nature and more

recently, driven by the quota system imposed on insurers under rural and social sector

obligations (UNDP, 2007). Microinsurance in India has valuable lessons for rest of the

world, particularly in the regulation of the industry. The study suggests some key

determinants of microinsurance development in India which is different from what

18

commonly assumed that a microinsurance policy is simply a low-premium insurance

policy. Some of the key factors that hinder growth of microinsurance are remote

location of clients, illiteracy and unfamiliar with the insurance products, illness due to

poor food consumption pattern, work conditions and lack of regular medical check-ups

and lack of access to formal financial services. Higher transaction costs on the part of

policyholders in terms of premium deposit, claim settlement and other matters is often

considered as major factor preventing growth of microinsurance in the country.

In a pioneering study by UNDP (2007), pro-poor insurance sector growth in India

was discussed with some key issues and constraints, pertinent to the growth of the

microinsurance sector.

(1) There are specific reasons for low demand for insurance in spite of intense

need. Suppliers have their own concerns, which help to explain why there has been

slow development in microinsurance market. The rural financial markets characterized

by limited and inappropriate services, inadequate information and capacity gaps also

hinder growth of rural insurance market.

(2) There are challenges in insurance product design, which result in a mismatch

between client‘s needs and standard products on offer. Inadequate effort in product

development could be due to different perspective of stakeholders.

(3) Absence of adequate and suitable insurance data is a major concern. In the

absence of a suitable insurance database calculation of premium, costs, benefits,

willingness to pay, based on macro aggregates may not give actual insights. Building

and sharing claims histories can help in aligning pricing decisions with actuarial

calculations, thereby reducing price.

(4) Difficulty in distribution is one of the most cited reasons for absence of rural

insurance. The high costs of penetrating rural markets, combined with under utilization

of available distribution channels, hinder the growth of rural insurance services.

(5) Cumbersome and inappropriate procedures inhibit the development of this

sector.

(6) Contrasting perspectives of the insured and the insurers, lead to low customiza-

tion of products and low demand for what is available.

19

Microinsurance & Social Security

Social protection measure is often related with microinsurance for the poor and low

income groups. Microinsurance can play a crucial role as a comprehensive tool to

reduce poverty, inequality and vulnerability, particularly where public social protection

measures are inadequate and unevenly distributed. Unfortunately, more than half of the

world‘s total poor do not benefit from any form of social protection measures. Since

microinsurance is designed for the protection of low-income people to cope with

common risks, it can also strive to cover the excluded such as poor, women and

workers in informal sector. In many developing countries like India, the proportion of

informal workforce in total workforce is substantial and there is increasing tendency

towards casual nature of labour. Under this situation, it becomes daunting task on the

part of the government to provide social security to all. About 90 percent of the

working population of India is employed in the informal sector and about thirty percent

of the unorganized workers are very poor who needs public social security supports.

Although current social protection measures consist of health, disability, death, old age

and economic risks are prioritized, its funding and implementation remain challenging.

In India social protection being a concurrent subject, it has its own political economy.

So in the absence of a dependable social protection, the importance of microinsurance

becomes interminable.

With inherent limitations of the existing social protection measures in the country, there

is also a high demand to combat the adverse impacts of natural disasters such as

drought, floods, cyclone etc. Unfortunately, the ex-post coping mechanisms primarily

supported by the Government are not sufficient and do not cover all groups in all

sectors. Though India has exhibited with series of pro-poor anti-poverty measures

oriented towards reduction of risks and vulnerability, microinsurance can contribute

indirectly as it often exclude covariant risks from their portfolio.

There are a wide range of developmental programmes being supported by the

Government like Swarna Jayanti Gram Swarojgar Yojana (SGSY), National Rural

20

Employment Guarantee Scheme (NREGS), Rastriya Swasthya Bima Yojana (RSBY),

Rastriya Health Mission (RHM), Aam Aadmi Bima Yojana (AABY), Indira Awas

Yojana (IAY), Public Distribution (PDS), old age allowances, drought relief etc. which

have facilitated the improvement of income levels of poor households. The public-

package of ―Doubling Flow of Agricultural Credit‖ has also enabled greater

institutional credit flow for agriculture and allied activities. However, all these policy

interventions, though ambitious in stated intent, only incidentally address household

risks. The most vulnerable rural population, particularly women, older people and rural

people are mostly excluded from the insurance market. It implies the need of this

segment of population for protection of their lives / income-generating assets against

various perils. At present, Personal Accident Insurance Scheme (PAIS) which is being

provided as a bundled offering along with the Kisan Credit Card (KCC) Scheme and

the Rashtriya Krishi Bima Yojana (RKBY) for insuring crops, are, probably, the only

borrowed-linked risk mitigation mechanisms available to rural households. Similarly,

the progress in enrolment of the poor in the Rashtriya Swasthya Bima Yojana1 (RSBY)

in its third year of operation does not seem to meet the target to cover all poor by 2012 (

Narayana, 2010).

Under this situation, prospect of microinsurance is expected to be much wider and

challenging, especially with huge network of financial infrastructure in the country. For

instance, many commercial banks have partnered foreign insurance companies for

providing life insurance policies. Thus, banking outlets (which number close to 70,000)

and more than 1 lakh cooperative societies could provide the needed outreach to purvey

micro-insurance facilities without much addition to transaction costs. Unfortunately, the

desired outreach and efficacy of microinsurance sector in India has not been achieved.

Review of Literature:

In this section, we have summarized findings and major issues of some important

studies and reports on microinsurance in general and in India in particular with focus on

1 Prior to launch of RSBY in 2003, Universal Health Insurance Scheme was introduced in 2003 to

provide a health benefit package to poor with sum assured of Rs 30000/-

21

household risks and risk managing strategy, outreach of microinsurance products,

major policy regulation and constraints. It helps us to develop a framework for analysis

of the present study which is presented in subsequent chapters. Available literature

evaluating the impact of insurance in low-income countries is limited. There is also

unbalance between different types of insurance products. Overall, the emphasis is

concentrated on different health insurance schemes, and their impact on health care-

utilization, out-of-pockets expenditure or social inclusion. Very few studies evaluate

the impact of insurance on household income, nutrition, or other dimensions of welfare

than those directly related to the insurance. Study on other insurance products are also

limited and hindered by the lack of systematic baseline data on individual beneficiaries

and groups.

Cohen and Sebstad (2006) highlighted the need to carefully study of clients‘ insurance

needs before introducing a new product, where market research can include studying (i)

clients‘ needs, (ii) specific products, or (iii) the size of the potential market. Analyzing

insurance demand from Uganda, Malawi, Philippines, Vietnam, Indonesia, Lao P.D.R.,

Georgia, Ukraine and Bolivia they found that the most prevalent risks relate to health

and loss of wage earners. In a recent study by Ito and Kono (2010) on health

microinsurance in Karnataka, India found that take-up rates of microinsurance have

been low despite its perceived need and the enthusiasm of microfinance practitioners.

They found some evidence that people behave in a risk-loving way when facing the risk

of losses.

However, despite these patterns, households‘ priorities regarding demand for insuring

risks are nevertheless context specific. More research is essential to understand and

identify the means for increasing insurance take-up rates and decreasing dropout rates.

A general understanding about attributes of microinsurance products from a client

perspective is awareness, easy to understand, simple, affordable, valuable and trust.

These factors are determinants of uptake and therefore, determine the impact of

microinsurance at household level.

22

In case of weather insurance, some recently studies have attempted to asses its impacts

on household incomes and also on risk-taking behaviour (Gine et al., 2007a; 2007b;

Gine and Yang, 2007). The findings do not show substantial impacts; for example,

Gine and Yang (2007) undertake a study in Malawi and shows that those with

insurance did not increase the uptake of risky technologies, one of the expected

outcomes. In terms of the impact of new schemes on existing mechanisms, Jowett et al.

(2003) found that social cohesion and informal financial networks are negatively

associated with insurance uptake, suggesting that the former crowd out public voluntary

health insurance. Dercon and Krishnan (2003) present evidence that suggests a

crowding out effect of informal risk-sharing arrangements by food aid. On the other

hand, Morduch (2006) argues towards a possible negative price effect of insurance

during times of shocks when insured individuals drive up the price of goods, for

example food products.

On the other hand, more educated households have been found to be more likely to take

up insurance (Chankova et al., 2008; Gine et al., 2007b). It emphasizes on effort to

improve communication and financial education on risk-pooling, insurance and rights

of policyholders tailored to low-educated and illiterate individuals and simplify

policies. Similarly, households with a sick household head are less likely to purchase

insurance. This might capture the fact that households with a sick household head have less

income flow and have difficulty in financing the insurance premium (Ito and Kono, 2010)

Clients‘ understanding of insurance products and ability and willingness to pay are key

to take up of insurance.

As regard, to constraints of microinsurance products it could be region and group

specific. Some common constraints already documented in literature are low take-up

rates, high claim rates, low renewal rates, poor delivery channels, high transaction costs

and poor insurance literacy. Another serious constraint to the uptake of insurance is

trust on each other. The contrast of microinsurance with microcredit helps to see the

difference between these two activities. Lenders have to trust borrowers; while insurers

have to be trusted by clients. Radermacher et al. (2006) underline the importance of

23

trust along these two dimensions: first, that the insurer is willing to make payments to

clients; and second, that the insurer is able to deliver the payments. The demand, uptake

and renewal of insurance clients also depend on the market conditions and constraints

to insurance provision.

Willingness to pay for insurance is crucial in promoting enrolment by low-income

households (Chankova, 2008). Paying premiums should be in line with households‘

cash flows (Cohen and Sebstad, 2006). Dror et al. (2007) study households‘ willingness

to pay, analyzing data on households in India find a higher level of nominal willingness

to pay and household income and nominal willingness to pay are positively correlated,

while household income and willingness to pay as a percentage of household income is

negatively correlated. Household size is the most important determinant of willingness

to pay levels.

As regard, to supply of microinsurance products some common findings are emerged

from across studies. While different perspective of different stakeholders constitutes as

a major supply constraint, availability of suitable distributive channel, pricing and

regulation determine the overall supply of microinsurance products. Interestingly, most

of the low segment insurance markets are supply driven. From the insurers‘

perspective, microinsurance opens a huge market, especially for the ones facing market

saturation. Insurers aim to develop new business models that create mechanisms which

cater to this low-income market who will be future high-income clients. Unfortunately,

standardized insurance product may not respond to client needs.

As regard to the designing of microinsurance products, Brown and Churchill (2000a)

argues for some criteria,

(i) a large number of similar units exposed to risk,

(ii) limited policyholder control over the insured event,

(iii) the existence of insurable interest,

(iv) losses can be identified and measured,

(v) losses should not be catastrophic,

24

(vi) chance of loss is calculable and

(vii) Premiums are economically affordable.

Potential demand for insurance may get influenced by type and nature of risks and

vulnerability. Leftley and Mapfumo (2006) highlight, the importance of demand side

factors for developing a successful product depending on the operational and regulatory

environment as well as risk carrier options. The risk coverage-premium tradeoff by

providing a menu of choices and letting clients chose their desired coverage and

corresponding premium has been developed (Dror, 2007). In Ethiopia, it was found that

the risk inherent in a modern high-return input (fertiliser) caused lower than optimal

uptake (Dercon and Christiaensen, 2007). Unable to insure agricultural risk, aversion to

risk led to choices that suppressed expected returns. The UNDP (2007) study on India,

found that health insurance was perhaps in most demanded products but short in

supply, because of operating such insurance schemes.

Managing moral hazard is another key constraint in microinsurance sector. Households

with a higher ratio of sick members are more likely to purchase insurance (Ito and

Kono 2010), showing some evidence of presence of moral hazard. To manage moral

hazard and adverse selection problems composite insurance products is recommended

by Cohen and McGuinness (McCord 2008). But Roth and Chamberlain (2006), warn

that in practice the potential benefit of bundled microinsurance in terms of lower

premium is hardly passed on to its clients.

As regard, to delivery channel of microinsurance using intermediaries such as NGOs

and MFIs is common, particularly in rural areas. However, within institutional models

and delivery channels there are four major delivery models such as (1) partner-agent

model, (2) community based model, (3) full-service model, and (4) public insurance

provider model. Partner-agent model found referred in many cases (McCord 2006, Roth

and Athreye, 2005). Number of studies evaluated different microinsurance insurance

schemes and focus on several aspects beyond just the purchase of insurance. Some of

the general findings of these studies are complied and presented below.

25

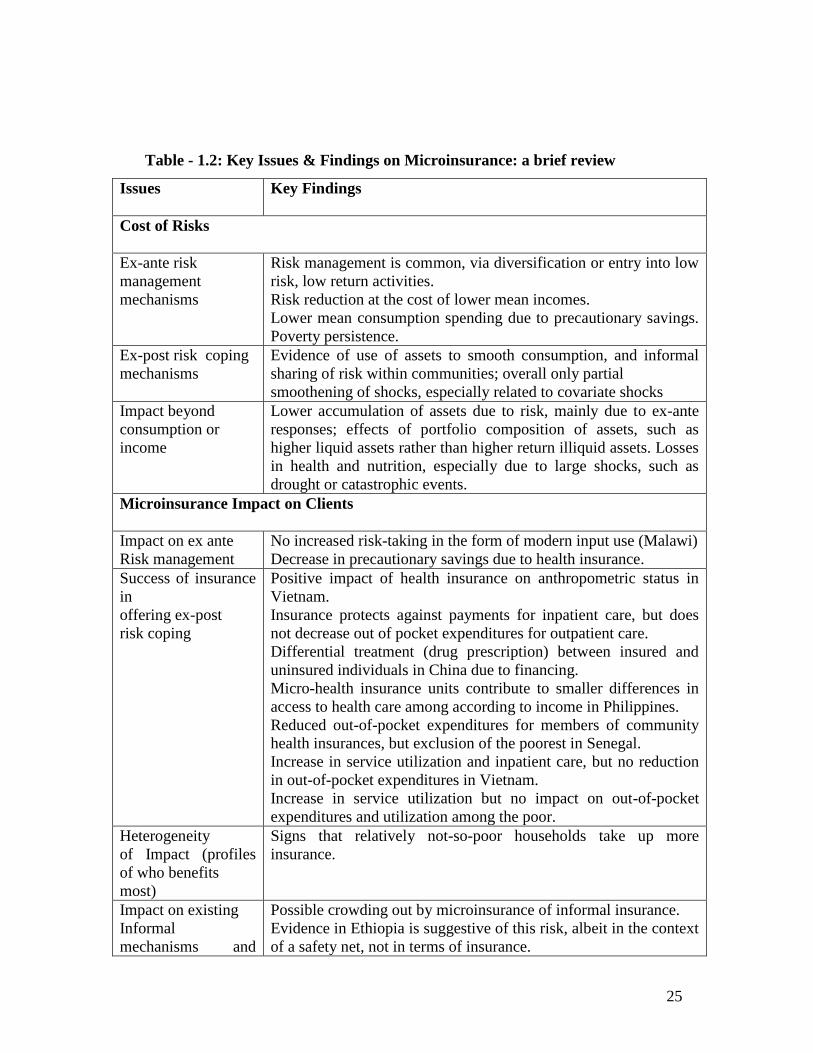

Table - 1.2: Key Issues & Findings on Microinsurance: a brief review

Issues Key Findings

Cost of Risks

Ex-ante risk

management

mechanisms

Risk management is common, via diversification or entry into low

risk, low return activities.

Risk reduction at the cost of lower mean incomes.

Lower mean consumption spending due to precautionary savings.

Poverty persistence.

Ex-post risk coping

mechanisms

Evidence of use of assets to smooth consumption, and informal

sharing of risk within communities; overall only partial

smoothening of shocks, especially related to covariate shocks

Impact beyond

consumption or

income

Lower accumulation of assets due to risk, mainly due to ex-ante

responses; effects of portfolio composition of assets, such as

higher liquid assets rather than higher return illiquid assets. Losses

in health and nutrition, especially due to large shocks, such as

drought or catastrophic events.

Microinsurance Impact on Clients

Impact on ex ante

Risk management

No increased risk-taking in the form of modern input use (Malawi)

Decrease in precautionary savings due to health insurance.

Success of insurance

in

offering ex-post

risk coping

Positive impact of health insurance on anthropometric status in

Vietnam.

Insurance protects against payments for inpatient care, but does

not decrease out of pocket expenditures for outpatient care.

Differential treatment (drug prescription) between insured and

uninsured individuals in China due to financing.

Micro-health insurance units contribute to smaller differences in

access to health care among according to income in Philippines.

Reduced out-of-pocket expenditures for members of community

health insurances, but exclusion of the poorest in Senegal.

Increase in service utilization and inpatient care, but no reduction

in out-of-pocket expenditures in Vietnam.

Increase in service utilization but no impact on out-of-pocket

expenditures and utilization among the poor.

Heterogeneity

of Impact (profiles

of who benefits

most)

Signs that relatively not-so-poor households take up more

insurance.

Impact on existing

Informal

mechanisms and

Possible crowding out by microinsurance of informal insurance.

Evidence in Ethiopia is suggestive of this risk, albeit in the context

of a safety net, not in terms of insurance.

26

other external

effects

Evidence in Vietnam shows that strong informal insurance hinders

uptake of new insurance products.

Demand for Microinsurance

Most important risk

management

needs

- health

- loss of income earner

- highly context specific, require careful market

research

Successful product

attributes

- simple

- affordable

- valuable

Factors influencing

uptake

- education of household head

- wealth

- family size

Literacy gaps - lack of understanding of mechanisms behind

insurance

- lack of effort by insurance agents to explain

- products in a way that is understandable for low education,

illiterate groups

Improving trust and

credibility in

insurance

providers

- building on existing structures

- education

- careful marketing and sales strategies

- arguments for subsidizing insurance premium for vulnerable

groups

Willingness to pay - nominal willingness to pay is higher than estimated in previous

studies

- importance of household size as determinant of nominal

willingness to pay

Supply of MI

Developing and

pricing

microinsurance

products

Detailed suggestions on balancing inclusion, premiums, benefits

and sustainability; need for professionalization for pricing:

involvement of insurance professionals.

Institutional models

and

delivery channels

Arguments on agnosticism regarding institutional models is

required; issues related to incentive contracts for agents.

Source: Dercon et. al (2008)

27

Structure of the Study Report:

The present study is divided into five chapters. Chapter 1 contains introduction and

statement of the problem followed by review of literature to offer a general framework

to understand the link between risk and risk coping behaviour, need and potential

demand for insurance and other aspects of microinsurance.

Chapter 2 discusses objectives, research methodology, data, scope and limitations of

the study.

Chapter 3 highlights some aspects of insurance industry in India, development of

microinsurance and insurance regulation.

Chapter 4 summarizes profile of select MFIs and their experiences in microinsurance

and suitable case studies.

Chapter 5 presents an analysis of original primary data, findings and some emerging

issues on microinsurance. The field data based on household survey direct interactions

with current and potential clients are suitably presented. This chapter constitutes brief

introduction to study areas, features of sample household including income,

employment, borrowing, saving and asset holding pattern. It discusses some major risks

faced by the sample households, their risk coping mechanism; impact of risk and intra-

household risk management; how sample households perceived risks and prioritized

insurance need. Household participation in insurance, demand for specific insurance

product, expectation and suggestions etc are highlighted in this chapter.

Chapter 6 concludes with some suitable policy suggestions based on the findings of the

study. It contains specific recommendations regarding product design, pricing, claim

settlements and strategies for further improvement. Specific recommendations for

different stakeholders: service suppliers and regulators and Government, including the

IRDA, are proposed.

28

Chapter-2

Objectives, Methodology, Data and Study Areas

The literature on microinsurance generally focuses on two major aspects of

microinsurance i) reduction of vulnerability and poverty ii) saving for future

contingency. While reaching out the potential clients through MFIs could be an

opportunity for the insurers to scale up insurance activity, the role of intermediaries

such as MFI cannot be undermined as regard to outreach and efficacy of

microinsurance products in developing populous countries like India. It is well captured

in three different dimensions of outreach based on the framework developed by

Schreiner (2002): depth, quality and scope of outreach. The present study, however,

does not attempt to measure it rather focus on microinsurance products delivered by

MFIs – quite popular in recent years. This is one of the limitations of the study.

There are different microinsurance models and delivery structures used by

microinsurers across the countries. Some important models are given below.

– Partnerships between insurers and distribution agents such as cooperatives and MFIs

– Regulated insurance companies that serve the low-income market directly

– Healthcare providers offering a financing package and absorbing the insurance risk

– Community-based programmes that pool funds, carry risk and manage a relationship

with a healthcare provider

– Government-sponsored or -subsidized insurance schemes

– Self-insuring MFIs that assume the risk of offering insurance to their clients

The present study aims to analyze outreach and efficacy of microinsurance under

partner agent model because of its increasing popularity in the country and elsewhere.

In the partner-agent model, the insurer teams up with a local agent, for example, a

microfinance institution, informal savings institution or other grass-root organizations.

Under this setup, the comparative advantage of the insurer in developing and pricing

policies is combined with the comparative advantage of the local agent by having

experience in reaching the poor, with networks already in place, and enjoying the trust

of large numbers of clients. For example, In India, Tata-AIG has developed a model of

29

micro-agents in addition to MFIs as agents. As microfinance interventions has been

widening, deepening and upscaling in the country, it has provided the institutional

precincts on which the edifice of micro-insurance could be built in rural areas. It also

justify selecting this model of microinsurance for the present study.

Therefore, the study is based on microcredit clients of select MFI to discuss the nature,

structure and outreach of microinsurance product among low income poorer groups and

learn how to improve and supplement their risk-management options using

microinsurance products. The study also attempts to highlight on current practice &

coverage select microinsurance products in select study areas, household risk-

management strategy & options and potential benefits and the impact of the insurance

on low-income groups etc. Although scope of the study is limited to the microcredit

clients of selected MFIs in two states (Tamilnadu and Orissa) it aims at to offer some

specific policy suggestions for better outreach and efficacy of microinsurance frontier

in India.

The research agenda is divided into three main areas: 1) Type of risks and risk aversion

behaviour of poor households 2) Nature of MFI loan-linked, microinsurance products

and its impact on the microcredit clients, 3) understanding difficulties, demand, supply

and other aspects of microinsurance in the study areas. Since most of the risks are

associated with the household‘s occupation and activities and its asset holding and asset

use pattern most of the research questions in the study (listed below) are generic and

concern with broad activity groups and regions. However, individual response, views

and suggestions and its implications are given importance wherever possible.

The association between household features and its risk aversion behaviour and demand

for insurance product across activity groups and regions are specially focused in this

study to understand the client value (potential benefit) of different microinsurance

products in different contexts. Demand for microinsurance, in terms of appropriateness

(demanded protection coverage), affordability (willing and ability to pay total cost

including premium) and accessibility (simplicity, physical access, convenience) are also

30

attempted to analyze with risk-management mechanisms of sample households

(including informal borrowing and savings, insurance, intra-household risk

management, participation in anti-poverty and social security programme). The study

aims at to discuss on household participation in insurance with focus on current credit-

saving linked microinsurance products (life insurance in Madurai & Trichy and life,

health and asset insurance in Sambalpur). Efforts are made to highlight on supply side

information collected from major stakeholders with focus on product design, selection

of partners & negotiation process, overall performance, major difficulties, use of

technology, and other issues.

Partner-Agent Model of Microinsurance

It is a partnership between an insurer and an agent that provides some kind of financial

service to large numbers of low-income people. This could be a microfinance

organization, an NGO, or a business that supplies products to large numbers of low-

income people, such as a fertilizer supplier. This party is an agent, selling insurance

policies to the clients on behalf of the insurance provider (usually) in exchange for a

commission or fee. The insurance provider utilizes the established distribution channels

of this agent and its financial transactions with low-income groups that would

otherwise be too costly to set up. The partnership model uses the comparative

advantage of each partner so that each can focus on its core business, the insurance

provider is responsible for designing and pricing the product, the final claims

management, and the investment of reserves, and absorbs all the insurance risks. In

addition to selling the policies, the agent offers its infrastructure for product servicing

such as marketing the product, premium collection, and assists in claims management.

Advantages and Limitation of Agent -Partner Model of insurance delivery

The delivery system under this model is argued works better because the synergies are

maximized, enabling both organizations to focus on their core business and expertise.

With a single partnership agreement it is possible to sell microinsurance to more

number of clients with fewer skills for the agent than other models. Like other formal

31

insurance product delivery system, it is legally recognized insurance companies and

operates under the insurance laws and regulation. Possibility of reduction of the

overhead costs of both the agent and the insurance company is better as the agent can

use its infrastructure. Information asymmetries are minimized as the agent is familiar

with the needs of clients and their situations, which reduces the time needed for claims

verification and settlement, while receiving feedback on client satisfaction and product

design. There is some incentive for the agent to earn as commission without risk, while

the insurer earns profits. Major limitation of this model is that the insurers depend on

the quality of the agent. So reputation and performance of the agents is crucial.

Conflicts of interest may occur, especially when working with non-financial

institutions. NGOs or MFIs staff or management may develop sympathy for a client

and be lax about underwriting or claims verification. It should be noted that this is less

likely to occur with an MFIs partner that is used to financial discipline with its lending

activities

Research Questions:

The primary research questions are: What are the nature and structure of risks and risk

aversion behaviour of poor households? What is the outreach and efficacy of MFI loan

linked microinsurance? Are intermediaries such as MFIs and their partners able to meet

the insurance need of these clients? What are major difficulties and suggestions offered

by different stakeholders, particularly by the potential clients, to improve the efficacy

and outreach of microinsurance?

Specific questions:

What are major risks/shocks poor and low income groups mostly confronted with?

What is the understanding and practice of formal insurance among microcredit clients?

How risk and risk management behavior are different across groups & other contexts?

What are the nature and benefits of existing microinsurance product in study areas?

32

How do poor household combine microinsurance with their existing risk management

strategies? To what extent does having insurance coverage promote undertaking higher-

risk, more productive economic activities?

Would they like to continue with existing insurance policy?

What are major difficulties and suggestions for microinsurance reported in the study

areas?

What is the room for market-based insurance that enhances household welfare?

Objectives:

The thrust of the study is to analyze the outreach, efficacy and prospect of

microinsurance, particularly among microcredit clients currently under the cover of

insurance and suggest the ways in which microinsurance services can become more

inclusive to enhance pro-poor risk management capability. Some Specific objectives of

the study are :

- Examine different risks faced by the poor and low income groups, their current

coping mechanisms, categorization and prioritization of risks by the client

population. This is expected to help in identifying factors that inhibit demand.

- identifying major issues of outreach and efficacy of microinsurance and the

demand and supply sides constraints.

- To understand perception of the target groups about microinsurance through

direct interactions and to explore the market potential for microinsurance in In-

dia.

- To identify activity and group specific problems and issues relating to

microinsurance such as product design, pricing, claim settlements etc.

- To suggest some implementable policy suggestions for facilitation of desired

growth and outcome of the microinsurance sector.

Methodology:

To study outreach and efficacy of microinsurance, the present study has focused on

select microcredit clients and the areas where spread of microcredit is better. Selection

33

of MFIs for the study was based on their coverage and overall performance in delivery

of financial services such as microcredit and microinsurance. The study primarily

looked at experiences in South India, especially in TamilNadu where spread of

microcredit is relatively better. Selection of Orissa was considered on the basis of

incidence of microfinance, level of poverty and variety of microinsurance products in

operation. Out of different microcredit group models2 and microinsurance delivery

structures3 partnerships between insurers and distribution agents such as MFIs was

selected as it is popular within and out of the study areas.

Keeping in mind limited variety of microinsurance products/schemes and most of are

only recently launched, we selected the study areas and microcredit clients of some

known MFI in Tamilnadu & Orissa, deal in microinsurance for fairly longer period, for

detail study. As most of the insurers have focused on the simplest insurance products

such as life insurance, attempt was made to capture some important features of the

product design, premium, coverage, and benefits, acceptability, difficulties and

suggestions made by the respondents. Detail information about household such as

demographic feature, occupation, income, employment, borrowing, saving, asset

holding, participation in insurance etc were netted out through using a structured

questionnaire. Some of intermediaries other than selected MFIs and local organizations

were identified and contacted before selecting the study areas. A pilot field visit was

undertaken before finalizing for field survey. Respondents were randomly selected

from rural, semi-urban and urban centres of the operation areas under select MFIs.

Random selection of households was mostly done during their centre meeting at early

morning. Prior information about the centre was collected from the concern branch

2 Gramin Bank model having 5 members in a group and 4-5 groups constitute a centre and Self-Help

Group (SHG) model having 10-20 members 3 Different microinsurance models are - Partnerships between insurers and distribution agents such as

MFIs, Regulated insurance companies that serve the low-income market directly, Healthcare providers

offering a financing package and absorbing the insurance risk, Community-based programmes that pool

funds, carry risk and manage a relationship with a healthcare provider, Government-sponsored or -

subsidized insurance schemes, self-insuring MFIs that assume the risk of offering insurance to their

clients

34

mangers and analyzed prior to visit to the centre and selection of the respondents for

detail interview to gather household level information.

The study employed both secondary and primary method of research.

(a) Secondary research based mainly on a review of the literature and secondary data

analysis relating to risks, insurance, credit, poverty and household behaviour.

(b) Primary research based on field survey in three districts in two states in India. This

included field investigations in three selected states of India - Orissa, Rajasthan and

Tamil Nadu - covering different geographic regions. These states also capture

differences in stages of microfinance development in the country, with Tamil Nadu

being relatively advanced. The investigations were in the form of focused group

discussions among the target population, complemented by in-depth interviews among

selected stakeholders.

Selection of Study Areas

With given constraints, the states of Tamil Nadu and Orissa were selected as they are

quite distinct in socio-economic development, allowing us to capture considerable

variability of circumstance relevant for rural insurance, as well as the different stages of

development of this industry. Field investigations were supplemented by number of

consultation with local organization, experts and stakeholders covering operational,

strategic and policy level issues. All this provides clarity on (a) the differing

perspectives of clients, insurers and intermediaries, (b) need and willingness to pay for

customized insurance products. As most vulnerable groups - in particular, women - are

largely excluded from the insurance market, this study is designed to focus on female

microcredit clients who are covered under some microinsurance scheme to analyze its

impacts.

The present study attempts to cover part of the total microinsurance sector in India by

focusing on insurance for microfinance clients in two districts (Madurai and

Tiruchirapally) in Tamil Nadu and one district (Sambalpur) in Orissa. The study is

based on primary field surveys and investigations, focus group discussion, consultation

with local experts, institutions and major stakeholders. Prior to field survey relevant

35

secondary data and information from different published and unpublished sources are

collected analyzed. Selection of Tamil Nadu was based on its better performance and

progress in the field of microfinance. It was also found to be relatively developed in

terms of higher overall insurance coverage in comparisons to other states (UNDP

2007).

Data Collection:

Secondary data were collected from different published reports and document, IRDA

Annual Reports and relevant online sources.

In this study, multiple sources of both qualitative and quantitative information are used

to answer the key research questions raised above. They are grouped in three main

categories:

(a) Contextual information on household including information on the household

features, loaned activity, income, employment, borrowing, saving, household assets.

(b) Information about household risks and risk coping mechanism such as formal

insurance, informal borrowing, distress sale, intra-household risk management etc.

(c) Views and observations about current insurance products, its impacts, major

difficulties and suggestions are gathered from sample households, selected

representative MFIs and concern insurers.

Sampling & Data Collection Methods

The research questions are addressed through a structured schedule for collection of

household level data. Despite of time constraint, to cover larger sample and more

regions, the current contents and coverage of data for the study has extensive

exploratory goals. However, the results of the study may not be amenable to

generalization, but the theory building exploration may be used in subsequent studies.

The field survey inquiry relies on multiple information and sources of evidence. Detail

of the study location and sample size presented in subsequent chapter (Table-2.1).

Primary data was gathered from randomly selected microcredit clients of selected MFIs

one each, located and operated in Trichurapally, Madurai and Sambalpur across

36

economic activities and social groups. Cluster of groups called ‗center‘ consists of 20-

45 group members was the unit of selection for household survey. After their regular

centre meeting early at morning we selected 4-6 members randomly for complete

interview and collect information with the help of structured questionnaire. Selection of

centres was made randomly at branch level with consultation with concerned branch

managers and other field staffs at branch. Branches were selected one each from rural,

semi-urban and urban areas depending on the nature of activities and period of

implementation of microinsurance products. Relevant information and discussions

were also made at headquarter of respective MFIs with the concerned staffs about the

selected sample units at each level.

Participatory approach of data collection was also followed by applying ‗cooperative-

cum-cross-checked‘ method among the group members in order to neutralizing and

minimizing personal errors and biases of the respondents. Similar procedure was

followed for conducting focus group discussions (FGDs), among the current members

and potential clients randomly selected during their centre/group meetings. Field data

was gathered through primary survey method using mixed method for data collection as

explained below.

Methods of primary data collection was done using following methods:

1. Household survey method

2. Focus Group Discussion

3. Interview with Key informants

4. Interview with local organization/institutions

5. Case Study

Features of Methodology:

(1) use of multidimensional quantitative data on household activities to show whether

microinsurance influence household risk aversion behaviour or not.

(2) use of mixed data collection methods (household survey, focus group discussion,

case study, interview with key informants) mostly quantitative, (to link household‘s

ability and its own coping strategy against risks with formal insurance products)

37

(3) use of purposive sampling to explore some new and innovative primary findings

and better understanding about household‘s behaviour on coping strategy with

insurance products.

(4) use of multidimensional data on microinsurance intermediaries (MFI)

Focused group discussions (FGDs) among current and potential clients were carried out

in all locations in each state. The FGDs were based on a pre-designed survey

instruments and check list that provided qualitative information to help assess client

perspectives on the efficacy and constraints of microinsurance.

Use of mixed methods consists of surveys with 75 group members (current clients of

three selected MFIs), 6 focus group discussions with about 60 current group members

(two each in select districts), interviews with 6 senior staffs of MFI and 4

representatives of insurance companies and two case studies.

Field Visit

The field visit consisted of two phases. The first phase was pilot survey involved two