THE HARD QUESTIONS! ANSWERED. COMMENTS - QUESTIONS - TESTIMONIES.

Upload

melvyn-harrisCategory

view

214download

0

REMINDER:

The audience is in listen-only mode

Please e-mail questions via the Q&A panel box

Select questions will be answered during the last 10 minutes of the program

Please answer poll questions

Webex customer support at: 866-229-3239

&

Welcome You to Our Webcast:Private Equity Deal Review

INTRODUCTION

Moderator:David Carey Senior WriterThe Deal LLC

EXPERT PANEL

John M. PollackPartnerSchulte Roth & Zabel

EXPERT PANEL

Howard D. MorganCo-presidentCastle Harlan Inc.

EXPERT PANEL

Robert Landis PartnerRiverside Co.

EXPERT PANEL

David E. RosewaterPartnerSchulte Roth & Zabel

Current state of U.S. M&A deal activity: Where are we now?

Observation of a “market practice” based on the

treatment/inclusion of key deal terms

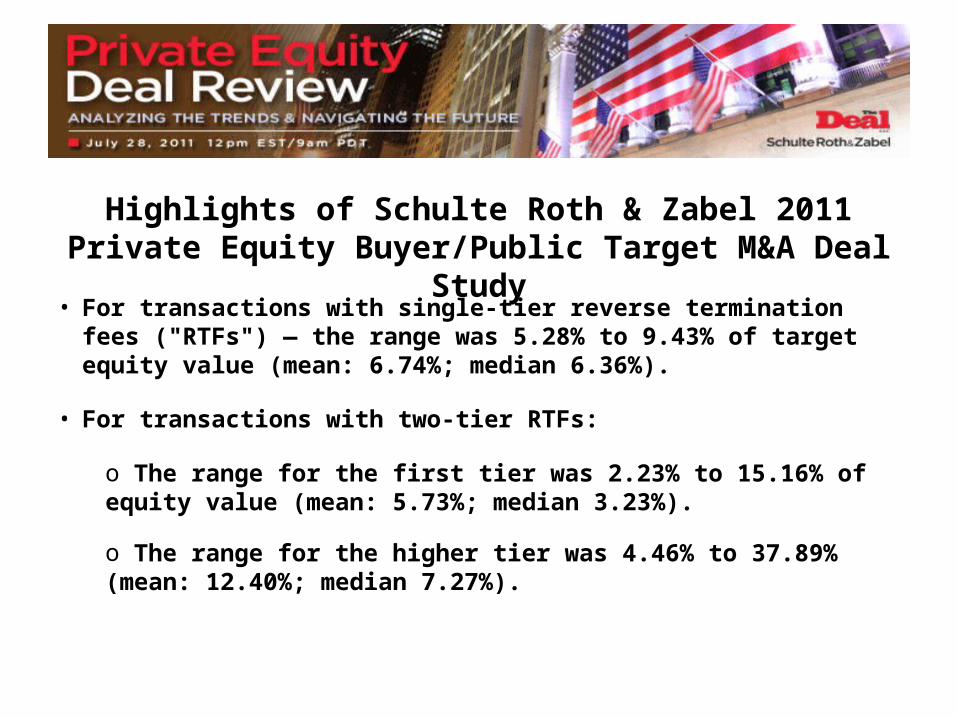

Highlights of Schulte Roth & Zabel 2011 Private Equity Buyer/Public Target M&A Deal

Study

Highlights of Schulte Roth & Zabel 2011 Private Equity Buyer/Public Target M&A Deal

Study

Highlights of Schulte Roth & Zabel 2011 Private Equity Buyer/Public Target M&A Deal

Study• For transactions with single-tier reverse termination fees

("RTFs") — the range was 5.28% to 9.43% of target equity value (mean: 6.74%; median 6.36%).

• For transactions with two-tier RTFs:

o The range for the first tier was 2.23% to 15.16% of equity value (mean: 5.73%; median 3.23%).

o The range for the higher tier was 4.46% to 37.89% (mean: 12.40%; median 7.27%).

Highlights of Schulte Roth & Zabel 2011 Private Equity Buyer/Public Target M&A Deal Study

“While ‘go-shop’ provision are not ‘market practice,’ they are widely used and not exceptions to the rule”

“While there recently have been innovations in deal terms in strategic acquisitions of U.S. public companies, these innovations have not spread to transactions involving private equity

buyers”

Highlights of Schulte Roth & Zabel 2011 Private Equity Buyer/Public Target M&A Deal Study

Macroeconomic andsocioeconomic

issues that are on the radar of dealmakers

Dealmaking Evolution Post-2008 Credit Crisis

Length of time for deals to be signed Duration of owning portfolio companies Future prospects in financing Biggest changes in deal terms

Outlook of dealmaking in the near term

AUDIENCE Q&A

Closing thoughts

Thank You for Joining Our Webcast

&