Relationship between Ownership Structure and Company Performance: Evidence from Macedonian Companies

39

Relationship between Ownership Structure and Company Performance Evidence from Macedonian companies KIRADZISKA, Snezana October 2010

-

Upload

snezana-kiradziska -

Category

Documents

-

view

925 -

download

1

Transcript of Relationship between Ownership Structure and Company Performance: Evidence from Macedonian Companies

Relationship between Ownership Structure and Company Performance

Evidence from Macedonian companies

KIRADZISKA, Snezana

October 2010

2

Executive Summary

This research project aims at exploring the relationship between ownership structure and

company performance in the Macedonian companies listed on the official market on the

Macedonian Stock Exchange during 2006 - 2009. The proposed hypothesis assumes that

more concentrated ownership structures enforce better monitoring on the professional

managers which results in better company performance.

New advanced econometrics was introduced in testing the hypothesis where endogeneity

of the ownership structure was considered. The empirical findings from the tests did not

support the proposed hypothesis.

To the best knowledge of the author this is originally the first research in this field in

Republic of Macedonia. It contributes in raising the awareness of corporate governance

practices in Macedonia as well as the agency problem in the post transition period.

This research donates the ongoing debate in the finance theory regarding the relationship

between ownership structure and company performance along with the other studies done

throughout the years.

3

Content

1. Introduction ..................................................................................................................6

2. Literature review ..........................................................................................................9

2.1. Theoretical aspects ...................................................................................................9

2.1.1. Corporate Governance and Agency Theory .....................................................9

2.1.2. Ownership structure .........................................................................................10

2.1.3. Company Performance ....................................................................................13

2.1.4. Gaps in knowledge...........................................................................................15

2.2. Previous studies ......................................................................................................15

3. Methodology ................................................................................................................22

3.1. Data requirements ..................................................................................................22

3.2. Research Approach and Methodology....................................................................22

3.2.1. Collecting data .................................................................................................24

3.2.2. Data issues ......................................................................................................25

3.2.3. Selection of estimators.....................................................................................26

3.2.4. Empirical specification ...................................................................................28

3.2.5. Estimation results ............................................................................................32

4. Conclusions and Recommendations ..........................................................................35

5. Reflection on Learning ...............................................................................................37

BIBLIOGRAPHY............................................................................................................38

APPENDIX 1....................................................................................................................42

APPENDIX 2....................................................................................................................43

APPENDIX 3....................................................................................................................44

APPENDIX 4....................................................................................................................45

APPENDIX 5....................................................................................................................46

4

1. Introduction

The relationship between ownership structure and company performance has been

debated for decades in the finance theory. The historic roots lie in the book of Adolf

Berle and Gardiner Means published in 1932. In their book The Modern Corporate and

Private Property authors explore the concentration of economic power by the large

companies in United States of America and the rise of a class of managers exercising

power no matter the shareholders and other stakeholders. This book was a result of the

economic events of 1920s, including the stock market crash of 1929. Furthermore,

Mizruchi (2004, p. 2) refers to the book of Berle and Means (1932) stating the issue that

the managers were seen as having interests not necessarily in line with those of the

shareholders meaning owners preferred that profits be returned to them in the form of

dividends, whereas managers preferred to either reinvest the profits or in more sinister

interpretations to further their own privileges in the form of higher salaries or “perks”.

Consequently their argument was that the unmonitored managers by largely dispersed

ownership structure can lower the value of the company. As the ownership and the

control were separated, the managers grew in those agents who had the power to destroy

or to build value and to distribute the wealth as well. In that time the term managerialism

emerged. As one of the approaches that critiqued managerialism was the agency theory.

According to Mizruchi (2004, p. 6) agency theory more than any approach has focused

on the complexities and difficulties of monitoring that arise when ownership is widely

dispersed. Significant contribution to the agency theory has been given by Jensen and

Meckling by acknowledging that managers have different motives than the owners and

that it is difficult to monitor the managers when the ownership structure is dispersed.

Throughout the years the Berle and Means (1932) argument has been tested by many

authors. Demsetz and Lehn (1985, p. 1176) with their article in the Journal of Political

Economy have openly critiqued the thesis of Berle and Means (1932) stating that the

ownership is structured in a way to maximize the owners value. The ongoing debate and

the number of studies testing the relationship have been a driver for this study as well.

5

This research tests the relationship between ownership structure and performance in

Republic of Macedonia. To the best knowledge of the author, no prior research has been

done on this topic.

Republic of Macedonia as the other countries of Central and Eastern Europe in the last

twenty years has been a subject of the process of privatization. This meant transferring

the ownership structure from state to privately ownership. The companies were to

become key players of the market oriented economy. The ownership structure of the large

companies was not built by investor driven decision but it was enforced by the

circumstances of the process of privatization. Most of the shareholders were the

employees in the previous state owned companies. There was a need for corporate

restructuring and managing in a way companies to be competitive on the domestic and

the global market.

The current corporate governance practices were implemented with the new Company

Law in 1996. Today, the Macedonian market, even though small, is characterized with

the key market players: the Macedonian Stock Exchange (MSE) with its regulation,

Securities Exchange Commission (SEC) as a regulator as well as investors who are

motivated for gaining a profit or a dividend. The real shareholding does exist today in

Republic of Macedonia. Its further development depends on the capability of the

companies, regulators and other institutions to strengthen the corporate governance

issues.

This issue has a social background regarding the accountability of the managers of the

large companies not only towards shareholders but to the society as well. Due to the

recent events of corporate failures, managers’ accountability has raised debates. The

unmonitored managers in the widely dispersed ownership structure can exercise power in

their own benefit and influence politics. Consequently, the personal driver of the author

for research in this field is the importance of corporate governance issues in Republic of

Macedonia in order to motivate higher accountability of the Macedonian managers

towards the shareholders.

6

The research objective of this paper is to examine the relationship between the ownership

structure and performance in the Macedonian companies. The test will be done by using

advanced statistical methods. The assumption is that the more concentrated ownership

structure provides better monitoring of the managers which results in better performance.

Consequently it is testing the Berle and Means (1932) hypothesis as well.

In the beginning, the literature was reviewed by studying theories, exploring definitions

and by analyzing the studies conducted. The studies and tests conducted trough the

decades have shown different results for supporting or critiquing the Berle and Means

(1932) theory. In the theoretical part, the definitions for the ownership structure and

performance will be explained. After the literature review the methodology for testing is

going to be analyzed. The analysis followed the logical pattern of doing the research.

Furthermore, details of the estimators which were used for the tests are presented. The

results achieved are analyzed and compared to theory. At the end, the thesis concludes by

providing recommendations for future studies and research.

7

2. Literature review

2.1. Theoretical aspects

2.1.1. Corporate Governance and Agency Theory

This study is closely related to the corporate governance issues and agency theory.

According to Johnson et al. (2005, p. 165) the governance framework describes whom

the organization is there to serve and how the purposes and priorities of the organization

should be decided upon. Furthermore, it refers to how an organization should function

and the distribution of power among different stakeholders. In recent years this concept

has gained much popularity as many corporate governance failures have emerged in the

finance and business world. The issue that has been observed is the separation of the

ownership and control in the companies. Managers are the agents for the principals

(shareholders) who have to work in maximizing the firm value and the shareholders

value. The agency theory presumes that there should be an incentive as a motivation the

“agents” to work in the best interest of the shareholders. But very often, the professional

managers, according to Johnson et al. (2005, p. 167) become very distant from the

ultimate beneficiaries of the company performance. This is the point where the agents

diverge to work in their own interest and not in the interest of the principal and the

conflict of interest arises.

Pike and Neale (2009, p.13) are proposing the ways to minimize the agency problem by

setting up and monitoring managers. Those include the following:

- auditing the accounts of the company;

- conducting management audits and imposing additional reporting requirements;

and

8

- restrictive covenants imposed by lenders, such as ceilings on the dividend payable

on the maximum borrowings.

The above mentioned ways of monitoring the professional managers are called agency

costs which are undertaken in order to resolve the conflict of interest between the

managers and shareholders.

In their book Johnson et al. (2005, p. 210) refer to the Harvard Business School professor

Michael Jensen as to one of the proponents of agency theory which warns that there are

no “perfect agents” in the real world. He argues that either through their own self-interest,

or perhaps by error, managers can not be trusted to maximize shareholders interests.

Furthermore, Professor Michael Jensen explains that the best safeguard is to align

financially the managers’ interests with the shareholder goal of long-run value

maximization.

Today, modern corporations are characterized by very diffuse ownership structure.

According to Ross et al. (2005, p. 15) the diffuse ownership brings with it the separation

of ownership and control in the large corporations. Furthermore, in the literature there are

arguments that if the shareholders ownership is too diffuse and fragmented the effective

control is brought in question. Consequently, the more concentrated ownership structure

the better the monitoring of the professional managers which results in working in the

best interest of the shareholders and higher corporate performance. This is the root of the

many studies done in this field as is for this research which aims to prove whether there is

relationship between the ownership structure and company performance.

2.1.2. Ownership structure

Republic of Macedonia has undergone trough the processes of transition towards

functional market economy. In the socialist times the owner of the company was the

9

state. After the introduction of the new Company Law in 1996 and adoption of the

privatization model in 1994, the previously state owned companies were transformed into

Joint Stock Companies (JSC) owned by various shareholders, which in Macedonian case

turned to be largely the previous managers or the employees. But in that time the

shareholders were not investors in a real sense of the word as they did not paid

adequately for what they received in exchange. There was an evident need for change in

the mentality and behavior of the shareholders and implementing a shareholder’s culture.

The awareness had to be raised that the companies had to generate profit on the market

and not to be seen as social units of the society. The need for improving the corporate

governance practices was more than evident. The next step was putting in place the 2004

Company Law which implemented the world trends and European tendencies mostly

regarding protection of the shareholders rights.

The subject of this empirical study are the Joint Stock Companies in Macedonia listed on

the official market on the Macedonian Stock Exchange. In the observed period of this

research (2006-2009) the number of listed companies is fixed to 36 per year. As the

corporate governance issue has a legal background, the definition of a Joint Stock

Company according the Macedonian Company Law [Article 270] is that it is a company

where the shareholders participate with contributions in the equity, which is divided into

shares. The shareholders are owners of the company and they are entitled to a part of the

annual profit, they have voting rights and they remain last for settlement if there is a

bankruptcy process of the company.

The managing of the JSC’s according to the Macedonian Company Law can be organized

in one or two tier boards. The members of the one tier boards of directors are executive

and non executive. The executives are responsible for the daily operations of the

company. The non executive members are actually supervising the work of the

executives. The two tier board recognizes two managing bodies: the managing board and

supervisory board. Legally the two boards should be complementary. According to

Belicanec and Nedkov (2008, p. 151) the harmonized and coordinated managing and the

supervisory board are responsible for balancing the company interests and the interests of

10

the shareholders. Furthermore, the supervisory board should control the managing board

which should be working in shareholders’ best interest. This addresses the issue of

agency theory in the Macedonian companies as well.

In May 2004 the United States Agency for International Development (USAID)

conducted a research on all active Joint Stock Companies in Macedonia. The objectives

of the research were the current corporate governance practices in Macedonia. The

research addressed the issues like awareness of shareholders rights, need for

modernization of the registration process in Macedonia as well as understanding the new

Company Law as a mean for attracting finance. The interesting fact identified by the

research (2004, p.28) is that the ownership structure has been classified into the following

groups of owners in Macedonia:

- The government;

- Managers;

- Non executive members of the board of directors and supervisory boards;

- Individual investors;

- Employees; and

- The PIOM (Pension fund).

La Porta et al. (1998, p.8) used 10% threshold in his study to describe the controlling of

the company. If the there is a shareholder exceeding the 10% cutoff it is defined as an

ultimate controller. Consequently, the companies are divided into widely held companies

and companies with more concentrated ownership by ultimate controllers. To define a

control of companies, regarding this study a cutoff of 5% of the total shares is used in this

study. This threshold of 5% of the shares is used because legally it is a significant portion

of the voting rights which gives the shareholder right to propose items on the agenda of

the annual general meeting of shareholders that has already been called. Furthermore the

company has obligation for disclosing shareholders holding more than 5%.

11

Given the data in Appendix 4, this research indicates that the average control right held

by the largest shareholders in the companies listed on the official market on the

Macedonian Stock Exchange to be 33% in 2006, 35% in 2007 and 2008 and 36% in

2009. The max values meaning the highest control right by one shareholder in 2006 is

72%, 76% in 2007, 92% in 2008 and 2009. The minimum values are 6% in the four

observed years. This research revealed that there is no Joint Stock Company in

Macedonia without an ultimate controller. These findings indicate concentrated

ownership structure.

2.1.3. Company Performance

The managing board is accountable for the daily operations of the company. Shareholders

expect that the company will achieve higher performance results seen trough the financial

ratios. The hypothesis of the thesis is following: the more concentrated ownership

structure of the company, the higher the performance.

As previously mentioned the researchers have used few performance indicators in their

studies. Demsetz and Lehn (1985) have used the post tax accounting profit / book value

of equity. Many others, such as Mc Connell and Servaes (1990), Hermalin and Weisbach

(1991), Cho (1998) and others have used the Tobin Q. According to Pike and Neale

(2009, p. 585) Tobin’s Q is a ratio which is produced by dividing market value of assets

by replacement value of assets. Ratio greater than 1 indicates that the firm has done well

with its investment decision because of which the company is overvalued by the market.

Demsetz and Villalonga (2001) give different perspectives to the two performance

measurements mostly used in the studies above mentioned: the accounting profit and

Tobin’s Q. In their article, Demsetz and Villalonga (2001, p. 4) explain that the two ratios

differ by the time perspective where the accounting profit is backward-looking and

Tobin’s Q is forward looking. The question is whether it is more reliable to use what the

management has accomplished or what the management will accomplish. The second

12

difference is who actually measures the performance: for the accounting profit rate it is

the accountant who is constrained by the standards of his profession and the Tobin Q is

measured by the group of investors influenced by their optimism or pessimism.

Regarding this study the Return on Ordinary Shareholders’ Funds (ROSF) was used as a

performance measurement. According to Atrill and McLaney (2006, p. 174) the return on

ordinary shareholders’ funds compares the amount of profit for the period available to the

owners, with the owners’ average stake in the business during the same period. It is a

performance measurement showing how much the shareholders’ funds did generate

profit. It is a result of the daily operations of the management board. The shareholders’

want this ratio to be higher. The higher the ratio the higher hypothetically will be the

benefits for the shareholders. The findings in Republic of Macedonia show that after the

2008 crisis, the ROSF ratio has worsened in 2009. As already elaborated, according to

the initial thesis in the research, ROSF should be higher as the concentration of the

ownership is higher. The assumption is that the more concentrated ownership structure

imposes monitoring on the professional managers which tends to work for higher ROSF.

On the other hand widely dispersed ownership structure can not impose monitoring

mechanisms over the management and this situation provides them with a room for

working in their best interest not in shareholders’.

The second performance measurement used in the research is Sales Growth. This

indicator shows the increase in sales on annual basis. The companies in Republic of

Macedonia demonstrated a decrease in sales growth since 2006. The annual growth

percentages were as follows: 26% in 2006, 13 % in 2007, 12 % in 2008 and there was a

fall of -9% in 2009 as compared with 2008. There should be a positive relationship

between the sales growth and the concentrated ownership structure, as well as positive

impact of sales growth on ROSF.

The third measurement used is debt to equity ratio. According to Gibson (2007, p.241)

the debt ratio indicates the firm’s long term debt paying ability. It is computed as follows:

13

Debt to equity ratio = long-term liabilities / total assets

According to Jensen and Meckling (1976, p.52) even in absence of the tax benefits debt

can be utilized if the ability to exploit potentially profitable investment opportunities is

limited by the resources of the owner. If capital is not raised the owner will suffer

opportunity loss of not undertaking the additional investments. Furthermore they explain

that even though the owner will bear the agency costs because of the debt he will need

the additional capital as long as the marginal wealth increments are greater from the

marginal agency costs of debt. This argues that the debt is increasing the value of the

company, assuming higher ROSF. Regarding the companies in Republic of Macedonia

this research indicates rather steady average debt to equity ratios of the listed companies:

0.21 in 2006, 0.21 in 2007, 0.24 in 2008 and 0.23 in 2009.

2.1.4. Gaps in knowledge

There is no research in Republic of Macedonia focusing on the research objectives from

this proposed study. There are studies related to corporate governance exploring other

issues but never has been the relationship between the ownership structure and

performance tested.

2.2. Previous studies

Many studies have analyzed the relationship between the organizational structure and the

financial performance of the companies.

Among the first authors seeking the relationship between the ownership structure and the

corporate performance are Berle and Means (1932). Berle and Means (1932) in the paper

of Fishman et al. (2008, p. 115) assert that as the ownership becomes increasingly

dispersed shareholders are becoming powerless to control the professional managers as

14

they can not effectively carry out monitoring of management. Furthermore, they suggest

that the diffuseness of ownership and performance should have negative relationship.

Consequently, the more concentrated ownership structure will produce higher financial

performance measures.

In 1976 Jensen and Meckling reinforced the theory of Berle and Means (1932) in regard

to the agency theory, which is arguing against the irrelevance of the capital structure in

determining the market value of the company. Agency theory derives from the fact that

ownership and control in the company are separated where the managers are the agents

and should be working in the best interest of the principals – shareholders. The managers

are delegated the decision making process which require some incentives and control to

work in the best interest of the shareholders. These incentives and the control processes

cause costs which are called agency costs. According to the Jensen and Meckling paper

(1976, p. 5) the agency costs are the monitoring expenditures by the principal, the

bonding expenditures by the agent and the residual loss which is caused by the

divergence between the agents decisions and those decisions which would maximize the

welfare of the principal. Furthermore, the large shareholders can pressure managers not to

undertake activities that lower the value of shareholders and to increase the value of the

company.

In 1985, Harold Demsetz and Kenneth Lehn have provoked the hypothesis of Berle and

Means (1932) by conducting a research including 511 US corporations. They have used

five ownership measures which give an indication for firm’s concentration of the

ownership structure as % of stock held by top 5 shareholders, % of stock held by top 20

shareholders, Herfindahl measure of ownership structure, % of shares controlled by 5

largest families and % of stock controlled by institutional investors. The performance

measures are post tax accounting / book value of equity. The methodology used was the

Ordinary Least Square (OLS) which is not treating the ownership structure as

endogenous variable. The empirical study indicated no significant relationship between

the ownership concentration and the accounting profit rate which does not prove the

Berle and Means (1932) thesis. In their paper, Demsetz and Lehn (1985, p. 1176) are

15

arguing that the structure of corporate ownership varies systematically in ways that are

consistent with value maximization. Furthermore, they are pioneers of the idea that the

ownership structure is endogenous and according to Fishman et al. (2008, p. 115) it

depends on the individual characteristics of the firm.

There are authors that have overlooked the endogeneity of the ownership structure in the

studies conducted. According to Fishman et al. (2008, p.115) those are Morck, Schleifer

and Vishny (1988) who found a significant non-monotonic relationship by using the

Piecewise Linear regression. The ownership measure was percent of stock held by

directors and the Tobin’s Q and accounting profit were used as performance measures.

McConnell and Servaes (1990) by using the OLS have found a significant curvilinear

relationship between the ownership structure and performance. They have analyzed two

samples in 1976 and 1986. They have come up with results indicating that with an

increase in the insider ownership (managerial equity ownership) by 10% the performance

is improved by 30%.

In 1991 Hermalin and Weisbach by using the Tobin’s Q and % of the stock held by

incumbent CEO and former CEOs still on BoD revealed significant non-monotonic

relationship. Welch (2003, p. 290) indicates that during the study they have treated the

ownership as endogenous.

Among the authors treating ownership as endogenous variable are Loderer and Martin

(1997). In their paper Fishman et al. (2008, p.115) state that Loderer and Martin (1997)

have treated both the performance and ownership as endogenous variable by using a

simultaneous equations framework. However the results indicated that insider ownership

fails to predict performance, but performance is a negative predictor of insider ownership.

Furthermore the concern is that the 3-system equation appears to be under-identified as

Martin and Loderer added a binary variable to the model to overcome the lack of

exogenous variables in the system.

16

Another author that controlled the endogeneity of ownership is Cho (1998). He used two

measures: % of stock held by directors and Tobin’s Q. Welch (2003, p.290) in her article

presented that Cho (1998) using the Piecewise Linear Regression found that firm

performance affects ownership structure but not vice versa.

Himmelberg, Hubbard and Palia (1999) addressed the problem of endogeneity of

ownership structure. Using the Quadratic Piecewise Model they have found ownership to

have a quadratic relationship with performance. It is noteworthy that before this study

they did not control the endogeneity of the ownership and revealed that the changes in

ownership do not have a significant impact on the performance.

Similarly, Holderness, Kroszner and Sheehan (1999) conducted a study treating the

ownership as endogenous. They have found a significant positive relationship between

performance and ownership by officers and company directors between 0% and 5%.

In 2001, Demsetz and Villalonga were challenged by the hypothesis of Berle and Means

(1932) that there is an inverse correlation between the diffuseness of the ownership

structure and corporate performance. In their research Demsetz and Villalonga (2001,

p.4) are using the Tobin’s Q and accounting profit rate as performance measurement.

Regarding the agency theory they have taken the fraction of shares owned by the five

largest shareholders to represent the ability to control the professional management and

on the other side the fraction of shares owned by the management to represent the ability

of professional management to ignore the shareholders as an indication on the power held

by the parties that have different interests in the firm. Using the OLS regression and 2-

Stage Least Squares they found no significant relationship which is consistent with their

hypothesis. Consequently, in their article (2001, p.24) they argue that the findings support

the view that the market succeeds in bringing forth ownership structures, whether these

be diffuse or concentrated, that are of approximate appropriateness for the firms they

serve.

17

In 2003 a study was conducted on the Australian companies by Emma Welch. Her

research is challenged by the contrasting hypothesis of Berle and Means (1932) and of

Demsetz and Villalonga (2001). In the first phase (OLS testing) of the research Welch

(2003, p.302) did not take into account the endogeneity of the ownership structure which

revealed that performance is statistically dependant on managerial ownership. However,

when endogeneity is taken into account there is no statistical dependence of performance

on either ownership measure. Welch (2003) fitted the results in the generalized nonlinear

model which is advanced and it indicated a limited evidence of a nonlinear relationship

between managerial share ownership and firm performance. Fishman et al. (2008)

publicized a research conducted on the Australian companies which confirms the

previous Australian study and also recommends more advanced methods for testing the

relationship between structure and ownership.

Claessens and Djankov (1999) conducted an empirical study on ownership and

performance in Czech Republic. Motivating fact of this study was the Czech voucher

scheme privatization. The results of the tests indicate that both profitability and

productivity changes are positively related with ownership concentration in a situation in

which ownership is exogenous to firm performance. In their paper, Claessens and

Djankov (1999, p. 19) explain that the study revealed that certain types of owners such as

foreign strategic investors and non bank funds are more strongly associated with

improvements of performance. Furthermore, Claessens and Djankov (1999, p. 1)

demonstrated that in transition economies, empirical studies found positive relationship

between concentrated ownership and both voucher prices and stock market prices in

Czech Republic and China as well as a positive relation between actual firm performance

and ownership concentration in Russia.

In 2007 Kapopoulos and Lazaretou conducted a research on the Greek companies

regarding the relationship between the ownership structure and performance in the

context of a small European market. Greece has a relatively small stock market in which

the issue of corporate governance does not have a long history and it is dominated by

family controlled firms. Kapopoulos and Lazaretou (2007, p. 153) explain that in their

18

study they have treated the ownership as multidimensional and endogenous. The

empirical findings indicate that there exists a linear positive relationship between

profitability and ownership structure meaning both measures of ownership, managerial

fractions of shares and important shareholdings, positively influence Tobin’s Q.

Perrini, Rossi and Rovetta (2008) conducted a research in Italy which is another

contribution in the context of a small European market. Perrini et al. (2008, p. 312)

pointed out that using the data panel model they found that the ownership concentration

of the five largest shareholders is beneficial to firm valuation. Furthermore, this study

suggests new courses of research having in mind the power of shareholders and managers

as well as exploring the endogeneity of ownership and non-linearity issues.

A recent study has been done in Japan which was examining the influence of the

ownership structure on the corporate performance trough the history in the 20th

century.

According to Miyajima et al. (2009, p. 24) the Japanese experiences suggest that

ownership structure influences corporate performance but not necessarily on a consistent

basis. They show that in the interwar period the ownership structure was an important

determinant of corporate performance. By contrast, they revealed that in the high growth

era and after the oil crises ownership structure influenced performance but to a much

smaller degree. Furthermore, Miyajima et al. (2009, p.1) found that in the bubble period

(the late 80s) and after the collapse of the bubble, performance grew more sensitive to the

ownership.

There are two contrasting theses in the studies conducted in this field. The one is of Berle

and Means (1932) giving arguments for the positive relationship between concentrated

ownership and corporate performance. On the other hand Demsetz and Lehn (1985) were

arguing that performance and ownership are not related. Some studies have been

extending the scope of the research implementing many other variables concerning the

organizational structure. The methods used in evaluating the relationship have been

differently chosen by various researchers. A significant issue in the studies is whether the

ownership structure is treated as an endogenous variable. This issue gives a new course in

19

the research and leads to more consistent estimates. The researchers throughout the years

have been trying to adapt the research on the characteristics of their sample in order to get

the most precise results. The specific characteristics are the sample size, the number of

years for the data, the laws in the country where the research has been done impacting the

ownership structures, corporate governance tradition in the countries, industry sectors in

the country in which the research has been done. All of these factors influence the

determination of the variables and statistically modeling the research. Different authors

have taken different measures regarding ownership and performance as well as methods

used. The results have largely been mixed.

20

3. Methodology

3.1. Data requirements

In order to construct the statistical method for testing the hypothesis, data was needed for

the Joint Stock Companies listed on the official market on the Macedonian Stock

Exchange. On one side, the calculations of performance measures needed data for the

return on ordinary shareholders’ funds, sales growth and debt to equity ratio. On the other

hand, data was needed to construct the ownership structure ratio.

The performance measures were extracted from the annual audited financial statements

that all companies listed on the official market are obliged by law to disclose on the web

site of the Macedonian Stock Exchange (www.mse.org.mk).

The data for the ownership structure of the listed companies on the Macedonian Stock

Exchange was found from the Central Securities Depository (CSD). The CSD is the only

central register of securities which is responsible for the settlement of all tradings done on

the stock exchange. The depository has the data needed for the ownership structure of the

Macedonian companies. As the data were not disclosed anywhere a direct approach to the

CSD registers was needed. Further in the text the ways of collection of data will be

described.

3.2. Research Approach and Methodology

In the development of knowledge the principles of positivism as research philosophy

were used in this study. According to Saunders et al. (2003, p. 83) the researcher in this

tradition assumes the role of an objective analyst, coolly making detached interpretations

about those data that have been collected in an apparently value-free manner.

21

Furthermore, they refer to Gill and Johnson (1997) that this philosophy puts emphasis on

a highly structured methodology on quantifiable observations that lend themselves to

statistical analysis. Positivists favor a scientific approach in using official statistics

because they give objective, reliable quantitative data.

In order to obtain quantitative results from this study the deductive research approach

was used. Sunders et al. (2003, p. 86) refer to Robson (1993) who lists five sequential

stages trough which the deductive research as this will progress:

- deducing a hypothesis from the theory;

- expressing the hypothesis in operational terms meaning identifying variables;

- testing the hypothesis;

- examining the specific outcome of the inquiry; and

- if necessary, modifying the theory in the light of the findings.

Furthermore, this is an explanatory study which analyses the relationship between the

defined variables. When thought of the research approach the author acted as the other

researchers in the previous studies using the deductive method in order to gain

knowledge but there is a difference in the methodological aspects when analyzing the

data gathered which will be explained further in the text.

This research required gathering large amount of data. The steps in which the research

was done were carefully planned. To obtain data from the Macedonian Stock Exchange

was time consuming and the answer from the Central Securities Depository was

unpredictable. The following steps were recognized during this research regarding the

data:

- Collecting data;

- Data issues;

- Selection of estimators;

- Empirical specification;

22

- Estimation results.

3.2.1. Collecting data

For this study performance and ownership measures were needed. The performance

measures needed were Return on Ordinary Shareholders’ Funds, Sales Growth and Debt

to Equity given in appendix 1,2 and 3. As mentioned previously data needed to calculate

these ratios were to be found from the Macedonian Stock Exchange’s published data.

Before defining the number of companies that were subject to the data an explanation of

the organization of the Macedonian Stock Exchange is needed.

A company to be listed on the Macedonian Stock Exchange undergoes a process of

entering a security on the official market. It means being in compliance with the criteria

defined by the stock exchange where the company should disclose continuously price

sensitive information which can be of financial and non-financial nature. The companies

which have clear strategies and are in need for additional capital are listed on the

Macedonian Stock Exchange. As the process of privatization has been completed those

companies have accepted the challenges of the market oriented economy, tried in

changing the mentality of human resources and are aiming towards well structured and

organized companies achieving positive financial results. The management and the

shareholders become aware of the benefits of a listed company such as: possibility for

efficient new issues of shares, efficient system of reporting, higher ratings, higher

liquidity, protection of the shareholders, access to foreign stock exchanges. The criteria to

be listed on the official market is to submit audited financial statements from the last two

years, equity amounting to at least EUR 500,000 and number of shareholders at least 100

(www.mse.org.mk). Actually this is the background of the companies that are subject of

analysis for this study. The number of companies which are listed on the official market

is 36 for the observed period. The other companies which are registered on the stock

exchange are not listed and they undergo specific obligations for reporting according to

the Securities Law.

23

The 36 companies according to the transparency principals publish their annual financial

statements on the web page on the Macedonian Stock Exchange (www.mse.org.mk and

www.seinet.com.mk). Every year they publish the audited financial statements which

include the Balance Sheet, Income Statement, Cash Flow Report, Report for Changes in

the Equity and the accompanying Notes. This was the source of data for the performance

measures: Return on Ordinary Shareholders’ Funds, Sales Growth, Debt to Equity Ratio.

The data extracted from the financial reports was for the years 2006, 2007, 2008 and

2009. They are divided into several sectors: industry – 13 companies, construction - 2,

agriculture – 1, hospitality and tourism – 3, services – 7, trade – 5, banking – 5. The

process of collecting the data from the financial statements was time consuming as

manually for the 36 companies the performance measures were calculated. The

calculation was according the theoretical formulation given in the literature which was

previously explained in the text.

Regarding the collection of data for the ownership structure of those 36 companies a

direct contact was needed to the Central Securities Depository. A letter was written to the

officials in CSD explaining the purpose of the required data. The information required

was first, the number of shareholders owning shares under 5% and the shareholders of the

companies owning more than 5% of the companies given in appendix 4. The information

needed was for the years 2006, 2007, 2008 and 2009 in order to match the data for the

performance measures. In a week the official in the Central Securities Depository

positively answered to the requirement and gave the data on a CD to the author of this

research. Ethical issues were considered in accessing the data from this institution. The

confirmation from CSD is given in appendix 5.

3.2.2. Data issues

The empirical study is based on annual data for 36 companies listed on the Macedonian

Stock Exchange during the 2006-2009 period. Panel data analysis has been a commonly

used technique in microeconometrics and its popularity is often attributed to the use of

24

the full information content of both the time and spatial dimension. In accordance with

the theoretical guidance, data relate to four variables (ownership concentration ratio,

Return on ordinary shareholders’ funds, sales growth and debt to equity). Furthermore,

Gujarati (2003, p. 637) underscores that panel data estimation can take into account the

heterogeneity by allowing for individual -specific variables, provide more informative

data, more variability, less collinearity among variables, more degrees of freedom and

more efficiency. By studying the behavior of the cross-sectional units across time, panel

data analysis can provide valuable information on the dynamics of change, detect and

measure effects that simply cannot be observed in pure cross-section or pure time series

data.

3.2.3. Selection of estimators

The main empirical strategy to conduct the analysis is based on the generalized method of

moments (GMM). In particular, it is a dynamic panel-data estimator offering a variety of

advantages. GMM has large sample properties that are easy to characterize in ways that

facilitate comparison and can be used even with relatively short time series. The method

provides a natural way to construct tests which take account of both sampling and

estimation error.

In contrast with the first-differenced Arellano and Bond (1991) specification, the system

GMM creates a system of two equations for each time period: the first one is based on the

Arellano and Bond (1991) model in differences, in which differences are instrumented by

levels, and an additional one in which the original levels are instrumented with

differences (Roodman, 2006). One of the important innovations brought by the system

GMM is that it circumvents the main problem of difference GMM, which is associated

with the weak assumption that past levels of the variable are good instruments for first

differences. More precisely, for variables that may display a random walk, past changes

may be more predictive of current levels than past levels are of current changes. The

system GMM uses more moment conditions, because the explanatory variables expressed

25

in first differences are instrumented with lags of their own levels, and the explanatory

variables in levels are instrumented with lags of their own first differences.

Another advantage of the dynamic panel data models is their ability to address potential

endogeneity problems. In particular, relevant empirical studies (e.g. Demsetz and Lehn,

1985) identified the problem of endogeneity of ownership structure and company

performance. This implies that the ownership structure influences the performance, but

also the ownership affects company performance. An additional argument for favoring

the GMM estimation is that “even when coefficients on lagged dependent variable are not

of direct interest, allowing for the dynamics in the underlying process may be crucial for

recovering consistent estimates of other parameters” (Bond, 2002).

For the purpose of comparing results, an ordinary least squares (OLS) regression was

used in the empirical analysis. According to Lucey (2002, p.133) the method of finding

the line of best fit mathematically in which the line minimizes the total of the squared

deviations of the actual observation from the calculated line, is called least squares

method. According to Gujarati (2003, p. 58) the method of least squares under certain

assumptions has some very attractive statistical properties that have made it one of the

most powerful and popular methods of regression analysis. But as a strong argument in

limitation of using the OLS technique is that it does not address the problem of

endogeneity.

This study departs from the existing literature by employing a more advanced

econometric technique. In the previous studies the OLS technique has been used as an

estimator. Demsetz and Lehn (1985), McConnell and Servaes (1990), Demsetz and

Villalonga (2001) and Welch (2003) has used the OLS in testing their hypothesis. Morck,

Schleifer and Vishny (1988), Hermalin and Weisbach (1991) Craswell, Taylor and

Saywell (1997), Cho (1998) Himmelberg, Hubbard and Palia (1999) and Holderness,

Kroszner and Sheehan (1999) has used the Piecewise Regression. As well in their studies

Cho (1998), Demsetz and Villalonga (2001) and Welch (2003) are using the method of

two-stage least squares.

26

3.2.4. Empirical specification

Given the previously discussed theoretical concepts between the ownership structure and

performance the empirical formulation takes the following form:

itDummyititDummyFIRSTFIRSTit

itDummySALESSALESitDummyDEitDEitROSFit

µββ

βββββ

+++

+++++=

76

54321

Where subscripts i and t denote the cross sectional units and the time period, respectively,

so that i = 1, 2,….36 (N=36) and t = 2006, 2007, 2008, 2009 (T=4). The beta 1

coefficient is the intercept and the remaining betas are denoting the slope coefficients.

The first variable is the Return on ordinary shareholders’ funds. The data as previously

mentioned was extracted from the audited financial reports. The calculation followed to

derive the indicator is, as follows: net profit at the end of the year/ ordinary shareholders’

funds. The ratio shows the ability of the management to generate profit on the funds from

the ordinary shareholders. According to the hypothesis that will be tested in this research

the more concentrated ownership structure the higher is the Return on ordinary

shareholders’ funds. Furthermore, the concentrated structure imposes closer monitoring

to the professional management for better results than the more diffuse ownership

structure. The more diffuse ownership leaves space for the professional management to

work for their best interest not for the shareholders.

Another variable used in the model as part of the performance measures is the Sales

growth. The variable measures the growth in sales in regard to the previous year

contemporaneous sales growth. Regarding the hypothesis, the expected movement of the

sales growth is positive with the more concentrated ownership structure. As with the

ROSF, the more closely monitored management by the more concentrated structure will

27

result in higher sales. Consequently, the higher sales growth the higher expected is the

return on ordinary shareholders’ funds.

The third variable employed in the statistical method was the Debt to equity ratio for the

Macedonian companies. The expected sign according to Jensen and Meckling (1976)

theory is positive. According to their theory the debt can be positively utilized and bring

benefits to the shareholders but to the point where the benefits exceed the costs.

Consequently, the concentrated ownership structure can oppose better monitoring in

utilizing the debt. This is also expected to influence positively on the Return on ordinary

shareholders’ funds.

Ownership concentration ratio is another important variable accentuated by the theory. It

measures the concentration of the first ownership owning more than 5% of the shares in

the company. When the data was received from the Central Securities Depository, an

investigation was made to check whether a company listed on the official market on the

Macedonian stock exchange for the period of 2006 – 2009 has a shareholder owning

more than 5% of the shares. The analysis showed that some of the companies in the

period of 2006 – 2009 had a second, third and even fourth shareholder owning more than

5% of the shares. But in order the research to be consistent the concentration ratio in this

research indicates the percentage of shares owned by the first shareholder with more than

5% of the shares. Demsetz and Lehn (1985) for the purpose in their research are taking

the % of shares held by top 5 shareholders and by top 20 shareholders, Morck, Schleifer

and Vishny (1988) took the percentage of shares controlled by company directors,

McConnell and Servaes (1990) took the percentage of shares held by insiders,

blockholders, institutional investors, Cho (1998) employed the percentage of shares held

by company directors, Demsetz and Villalonga (2001) took the shares hold by the top

management, the CEO and company directors. Regarding the research the concentration

ratio depends on the sample and the information that can be provided.

Furthermore, dummy variables are introduced in the statistical model. According to

Gujarati (2003, p. 298) these variables usually indicate the presence or absence of a

28

“quality” or an attribute and are essentially nominal scale variables. They are used to

classify data into mutually exclusive categories. For the purpose of this research the

dummies were used in order to introduce a distinction between data for the financial and

non-financial sector. In the past year, the financial sector in Macedonia particularly the

banking sector has attracted many investors. The financial sector also hosts some of the

most profitable companies in the country. Given the particular interest in the performance

of the financial sector, dummies were introduced for each variable such as for ROSF,

First shareholder, Sales growth and Debt to Equity.

For presentational convenience, Table 1 offers a short description of the symbols,

variables employed and the expected sign of the relationship with the dependent variable.

Table 1 – Description of variables

Symbol Description Expected sign

first

First shareholder owning shares more than

5% plus

sales Sales growth plus

de Debt to Equity ratio plus

d2first

Dummy for first shareholder owning shares

more than 5% in the banking sector plus

d2sales

Dummy for sales growth in the banking

sector plus

d2de Dummy for debt to equity ratio plus

In Table 2 a descriptive statistics is given for the sample in the period of 2006-2009. The

results indicate average high concentration ratio of 0.35 but as well a high standard

deviation arising from the fact that the maximum concentration ratio is 0.92. The ROSF

ratio on average shows negative results but as well the standard deviation is higher. An

interesting fact is that the minimum for the debt to equity ratio is 0.00 meaning that there

are companies that do not employ debt at all. The standard deviation is high for the debt

to equity ratio. The sales growth has a very high standard deviation as the minimum

shows negative sign and the maximum indicates high results. It can be concluded that the

29

sample is heterogenic, meaning it is consisted of companies achieving highly different

performance results. One more reason is that they are from different industries which are

differently developed in Macedonia. Another possible explanation is that the sectors were

differently impacted by the financial crisis and that influenced the financial results in

2008 and 2009.

Table 2 – Descriptive statistics

First

shareholder >

5%

ROSFDEBT to

EQUITYSALES Growth

Average 0.35 -0.03 0.22 0.10

Standard deviation 0.22 0.38 0.30 0.64

Maximum 0.92 0.34 1.92 6.10

Minimum 0.06 -3.98 0.00 -0.96

30

3.2.5. Estimation results

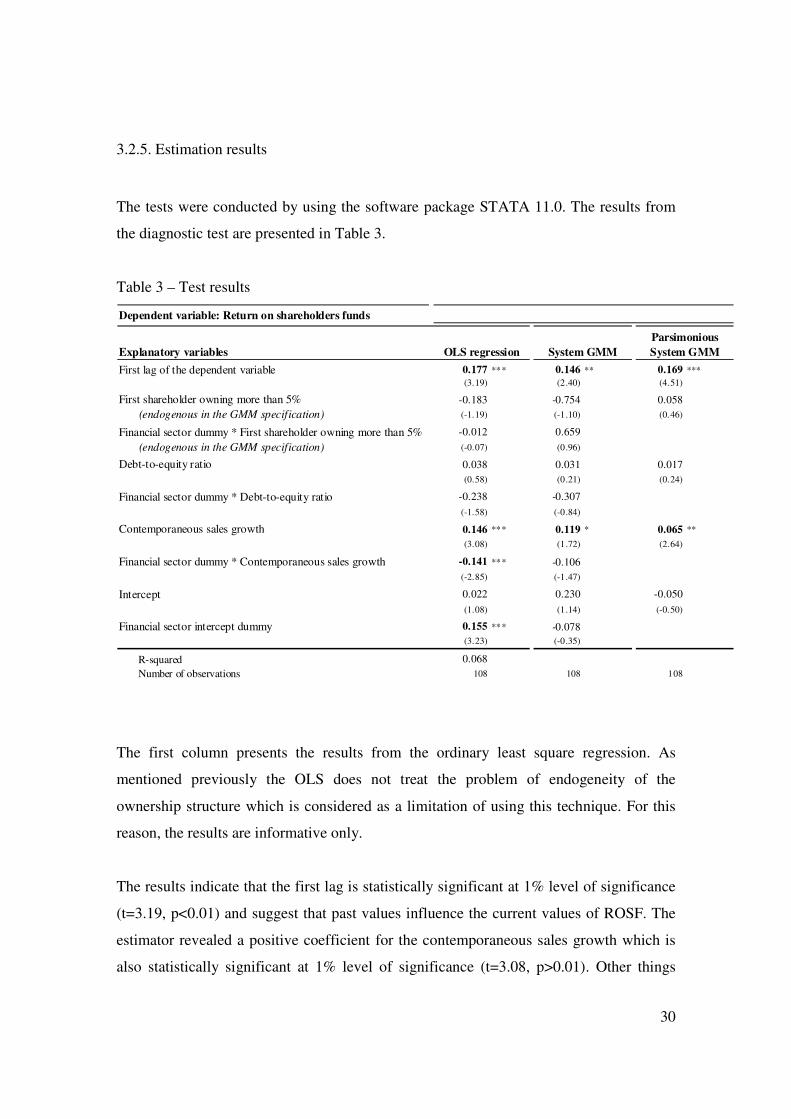

The tests were conducted by using the software package STATA 11.0. The results from

the diagnostic test are presented in Table 3.

Table 3 – Test results

Explanatory variables

First lag of the dependent variable 0.177 *** 0.146 ** 0.169 ***

(3.19) (2.40) (4.51)

First shareholder owning more than 5% -0.183 -0.754 0.058

(endogenous in the GMM specification) (-1.19) (-1.10) (0.46)

Financial sector dummy * First shareholder owning more than 5% -0.012 0.659

(endogenous in the GMM specification) (-0.07) (0.96)

Debt-to-equity ratio 0.038 0.031 0.017

(0.58) (0.21) (0.24)

Financial sector dummy * Debt-to-equity ratio -0.238 -0.307

(-1.58) (-0.84)

Contemporaneous sales growth 0.146 *** 0.119 * 0.065 **

(3.08) (1.72) (2.64)

Financial sector dummy * Contemporaneous sales growth -0.141 *** -0.106

(-2.85) (-1.47)

Intercept 0.022 0.230 -0.050

(1.08) (1.14) (-0.50)

Financial sector intercept dummy 0.155 *** -0.078

(3.23) (-0.35)

R-squared 0.068

Number of observations 108 108 108

Parsimonious

System GMM

Dependent variable: Return on shareholders funds

OLS regression Random-effects System GMM

The first column presents the results from the ordinary least square regression. As

mentioned previously the OLS does not treat the problem of endogeneity of the

ownership structure which is considered as a limitation of using this technique. For this

reason, the results are informative only.

The results indicate that the first lag is statistically significant at 1% level of significance

(t=3.19, p<0.01) and suggest that past values influence the current values of ROSF. The

estimator revealed a positive coefficient for the contemporaneous sales growth which is

also statistically significant at 1% level of significance (t=3.08, p>0.01). Other things

31

being equal, the estimates suggest that an increase of the sales growth by 1 % would be

associated with an improvement of the ROSF by 0.15%. The OLS estimator also reveals

a positive relationship between ROSF and sales growth in the financial sector, but the

impact is of a smaller magnitude. This coefficient is statistically significant at 1% level of

significance. The most important finding is that the estimator does not show a statistically

significant coefficient for the first shareholder owning more than 5% of the shares. This

fact confronts the theoretical assumption that the greater ownership concentration leads to

higher performance presented by the return on ordinary shareholders funds.

The second column of Table 3 reports the results produced by the GMM estimator. As

previously mentioned the GMM estimator addresses the problem of endogeneity. This

technique indicates that two coefficients are statistically significant. The first one is the

first lag of the dependant variable. This is consistent with the OLS estimator. Again, the

past values influence the current values of ROSF. The coefficient is statistically

significant at the 5% level of significance. The other statistically significant coefficient at

10% level of significance is the contemporaneous sales growth. This indicates a positive

relationship between the sales growth and ROSF in this sample (t=1.72, p>0.1). The

GMM estimator does not reveal a statistically significant coefficient of the first

shareholder owning more than 5% of the shares. Consistent with the results of the OLS,

again using the GMM estimator the results are not in compliance with the theoretical

assumptions. The dummies did not show any statistically significant coefficient so they

were excluded from the test using the parsimonious system GMM. The results in the third

column revealed consistency with the system GMM and produced statistically significant

coefficient with the first lag of the return on ordinary shareholders funds and the

contemporaneous sales growth. Again, there was no statistically significant coefficient

for the first shareholder owning more than 5%.

The tests in the previous empirical studies, using the OLS and other estimators that treat

the problem of endogeneity, present mixed evidence. Demsetz and Lehn (1985, p. 1175)

in their article used the OLS estimator which revealed no significant relationship between

ownership concentration and accounting profit rate and especially no significant positive

32

relationship. Using a piecewise linear regression Morck, Schleifer and Vishny (1988)

revealed significant non-monotonic relation (increasing between 0% and 5%, decreasing

between 5 and 25%, and increasing beyond 25%), McConnell and Servaes (1990) found

a positive relation for insider ownership with the Tobin’s Q, Hermalin and Weisbach

(1991) revealed significant non-monotonic relation between managerial ownership and

performance, Loderer and Martin (1997) by using simultaneous equations and addressing

the problem of endogeneity revealed that ownership fails to predict performance but

performance is a negative predictor of ownership. Cho (1998) using the system of three

equations estimates that Tobin’s Q affects ownership structure but not vice versa. In 2003

Demsetz and Villalonga (2001) did tests with the two equation method and revealed no

significant relationship. The recent empirical findings of Kapopoulos and Lazaretou

(2007) suggests that more concentrated ownership structure positively relates to higher

firm profitability and also found that higher firm profitability requires less diffused

ownership. The research of Perrini, Rosssi and Rovetta (2008) provides empirical support

for the agency theory in finding that ownership concentration of the five largest

shareholders is beneficial to firm valuation.

This research has investigated the validity of the agency theory by using data for the

Macedonian companies listed on the official market on the stock exchange. The

hypothesis was that more concentrated ownership is associated with better performance

indicators. Unlike the previous studies, it addresses the problem of potential endogeneity.

Both estimators, OLS and system GMM, did not reveal any significant coefficients

regarding the relation between ownership structure and performance. Hence, the evidence

from the listed companies in the Republic of Macedonia does not support the Berle and

Means (1932) hypothesis.

33

4. Conclusions and Recommendations

The more concentrated ownership structure tends to lead to better monitoring of the

professional managers which produces better company performance. This is the

hypothesis in this research that was tested on the evidence from the Macedonian

companies listed on the Macedonian Stock Exchange. The test results using the ordinary

least square regression and generalized method of moments produced results that were

not supporting the hypothesis.

More advanced statistical estimators are used in this research than the previous studies

that have been conducted in the finance theory. The results depend on the data available

for the research. Regarding the data for the Macedonian companies there are issues that

should be considered for any future research. Namely, the sample for this research is

relatively small having 36 companies that are listed on the Macedonian Stock Exchange.

However, the covered period can be extended if there is an opportunity to get the data.

For this research the period used in extracting data for the ownership structure and

performance was 2006 to 2009. Higher number of observations can give more precise

results in a future research. Furthermore, the group of companies (36) is heterogenic

having companies classified in a number of sectors. The variability of performance ratios

is high not just between the sectors but within the sectors as well. In this research

dummies were used for the financial sector as the most profitable and influential one in

the economy. In future research other sectors can be controlled as well. The following

authors that will be interested in this field can use other variables in their studies if they

have available data. Namely, the percent of stock held by CEO’s can as well be

implemented in the research.

The root of the tested hypothesis is the agency theory explaining the conflict of interest

between the managers and shareholders. Despite the results produced, the awareness of

the agency problem should rise in better improvement of the corporate governance

practices in the Macedonian companies. Even thought, corporate governance discipline is

34

relatively young in this country there are many institutions and tools which have been

used for its promotion. A company should put in place practices that will in the same

time preserve and provide return on the investment of the shareholders but will also

enable the professional managers to achieve the company strategy. Furthermore, this

should motivate managers’ accountability towards the shareholders and the society as

whole.

35

5. Reflection on Learning

The greatest challenge in writing the thesis was the fact that this was originally the first

research in Republic of Macedonia addressing the agency problem in this manner. Every

aspect of the whole process was very demanding. The literature had to be reviewed

regarding the theory and the number of studies done in this field. The interesting part was

the historical development of the ownership – performance issue that has been researched

for decades by many authors. This indicates the significance of this field of study in the

finance theory. Collecting the data was a time consuming process which gave a dose of

unpredictability to the whole study regarding the willingness of the institutions that

provided the data. The knowledge gained related to the statistics part is very valuable. A

lot of reading was done regarding the complex estimators used in conducting the tests. It

gave the author a new perspective in further researches in other fields regarding the data,

variables employed and new statistical methods used.

The period of six months was testing the knowledge and skills gained in the previous

period of studying as well as developing new. It is a great feeling that this piece of study

is a contribution to an ongoing debate for decades as well it is a basis for this field of

research in Republic of Macedonia. However, the experience and knowledge gained

during the whole process of this research will open new perspectives for other studies in

the future.

36

BIBLIOGRAPHY

Atrill, P. and McLaney, E. (2006). Accounting and Finance for Non – Specialists, fifth

ed. England: Prentice Hall.

Claessens, S. and Djankov, S. (1999). Ownership Structure and Corporate Performance

in Czech Republic. The William Davidson Institute, Working Paper Number 227.

Available at:

http://deepblue.lib.umich.edu/bitstream/2027.42/39613/3/wp227.pdf

Accessed: 15/05/2010

Demsetz, H. and Lehn, K. (1985). The Structure of Corporate Ownership: Causes and

Consequences. Journal of Political Economy; Dec85, Vol. 93 Issue 6.

Available at:

http://web.ebscohost.com/ehost/pdfviewer/pdfviewer?vid=16&hid=15&sid=ae13a96a-

f7c9-4463-a940-907f88447d9b%40sessionmgr4

Accessed: 15/05/2010

Demsetz, H. and Villalonga, B. (2001). Ownership Structure and Corporate

Performance. Journal of Corporate Finance, Vol. 7, Issue. 3, p. 209-33.

Available at:

http://www.sciencedirect.com/science?_ob=ArticleURL&_udi=B6VFK-4435022-

1&_user=10&_coverDate=09%2F30%2F2001&_rdoc=1&_fmt=high&_orig=search&_or

igin=search&_sort=d&_docanchor=&view=c&_searchStrId=1479633253&_rerunOrigin

=scholar.google&_acct=C000050221&_version=1&_urlVersion=0&_userid=10&md5=c

ecc8bbf644ab03ee4ac962f14a56c25&searchtype=a

Accessed: 15/05/2010

Dess, G.G., Lumpkin, G.T. and Taylor, L.M. (2005). Strategic Management: Creating

Competitive Advantages, second ed. New York: McGraw-Hill/Irwin.

Fishman, J., Gannon, G. and Vinning, R. (2008). Ownership Structure and Corporate

Performance: Australian Evidence. Corporate Ownership & Control, Volume 6, Issue 2.

Available at:

http://www.lib.academy.sumy.ua/library/C_O_C%5CVolume%206,%20issue%202,%20

Winter%202008.pdf#page=112

Accessed: 15/05/2010

Friend, G. and Zehle, S. (2004). Guide to Business Planning. UK: The Economist.

Gibson, H.C. (2007). Financial Reporting and Analysis. Using Financial Accounting

Information, tenth ed. USA: Thomson Higher Education.

Griffin, W.R. (2005). Management, eight ed. New York: Houghton Mifflin Company.

37

Gujarati, D.N. (2003). Basic Econometrics, fourth ed. New York: McGraw-Hill/Irwin.

Hannagan, T. (2008). Management Concepts and Practices, fifth ed. England: Prentice

Hall.

Hansen, L.P. (2007). Generalized Methods of Moments Estimation. University of

Chicago, Department of Economics.

Available at:

http://home.uchicago.edu/~lhansen/palgrave.pdf

Accessed: 20/05/2010

Jensen C. M. (1986). Agency Costs of Free Cash Flow, Corporate Finance and

Takeovers. American Economic Review, May, 1986, Vol. 76, No.2, pp. 323-329.

Available at:

http://www.xbzhu.cn/jlq/upfile/upattachment/2009-4/200942010211.pdf

Accessed: 20/06/2010

Jensen, C. M. and Meckling H.W. (1976). Theory of the Firm: Managerial Behavior,

Agency Costs and Ownership Structure. Journal of Financial Economics, October, 1976,

V.3, No. 4, pp. 305-360. Available at:

http://www.sfu.ca/~wainwrig/Econ400/jensen-meckling.pdf

Accessed: 20/06/2010

Johnson,G., Scholes, K. and Whittington, R. (2005). Exploring Corporate Strategy,

seventh ed. England: Pearson Education Limited.

Kapopoulos, P. and Lazaretou, S. (2007). Corporate Ownership Structure and Firm

Performance: evidence from Greek firms. Corporate Governance, Volume 2, Volume 15.

Available at:

http://web.ebscohost.com/ehost/pdfviewer/pdfviewer?vid=18&hid=15&sid=ae13a96a-

f7c9-4463-a940-907f88447d9b%40sessionmgr4

Accessed: 15/05/2010

La Porta, R., Lopez-de-Silanes, F. and Shleifer, A. (1998). Corporate Ownership around

the World. Working Papers -- Yale School of Management's Economics Research

Network.

Available at:

http://mba.tuck.dartmouth.edu/pages/faculty/rafael.laporta/publications/LaPorta%20PDF

%20Papers-ALL/Corp%20Ownership.pdf

Accessed: 15/05/2010

Lucey, T. (2004). Quantitative Techniques, sixth ed. UK: Thomson Learning.

Maassen, F.G. and Carson, T. (2004). Corporate Governance in Macedonia: A Census of

All Active Joint Stock Companies in Macedonia. USAID Corporate Governance and

Company Law Project.

38

Available at:

http://www.developmentwork.net/publications/studies/90-corporate-governance-survey-

2003-2004-macedonia

Accessed: 15/05/2010

Miyajima, H., Kawamoto, S., Omi. Y. and Saito, N. (2009). Corporate Ownership and

Performance in Twentieth Century Japan. WIAS Discussion Paper No.2009-001.

Available at:

http://www.waseda.jp/wias/achievement/dp/pdf/dp2009001.pdf

Accessed: 15/05/2010

Mizruchi, M.S. (2004). Berle and Means Revisited: The Governance and Power of Large

U.S. Corporations. Shareholder – Value, Capitalism and Globalization, Bad Homburg,

Germany 2001.

Available at:

http://club.fom.ru/books/tsweb.pdf

Accessed: 15/05/2010

Недков, М. и Беличанец, Т. (2008). Право на друштвата. Скопје: Проект за

деловно окружување на УСАИД. Nedkov, M. and Belicanec, T. (2008). Law on

Companies. Skopje: Business Environment Project – USAID.

Perrini, F., Rossi, G. and Rovetta, B. (2008). Does Ownership Structure Affect

Performance? Evidence from the Italian Market. Corporate Governance: An International

Review; Vol. 16, Issue 4, p312-325.

Available at:

http://web.ebscohost.com/ehost/detail?vid=4&hid=15&sid=ae13a96a-f7c9-4463-a940-

907f88447d9b%40sessionmgr4&bdata=JnNpdGU9ZWhvc3QtbGl2ZQ%3d%3d#db=buh

&AN=34528045

Accessed: 15/05/2010

Pike, R. and Neale, B. (2009). Corporate Finance and Investment: Decision and

Strategies, sixth ed. UK: Pearson Education Limited.

Roodman, D. (2006). How to Do xtabond2 An Introduction to “Difference” and

“System” GMM in Stata. Working Paper Number 103.

Available at:

http://www.nuffield.ox.ac.uk/users/bond/file_HowtoDoxtabond8_with_foreword.pdf

Accessed: 20/06/2010

Ross, A.S, Westerfield, W.R. and Jaffe, J. (2005). Corporate Finance, second ed. New

York: McGraw-Hill/Irwin.

Saunders, M., Lewis, P. and Thornhill, A. (2003). Research Methods for Business

Students, third ed. England: Prentice Hall.

39

Sloman, J. (2006). Economics, sixth ed. UK: Pearson Education Limited.

Thomsen, S. and Pedersen, T. (2000). Ownership Structure and Economic Performance

in the Largest European Companies. Strategic Management Journal, Vol. 21, Issue 6.

Available at:

http://onlinelibrary.wiley.com/doi/10.1002/(SICI)1097-0266(200006)21:6%3C689::AID-

SMJ115%3E3.0.CO;2-Y/abstract

Accessed: 15/05/2010

Welch, E. (2003). The Relationship between Ownership Structure and Performance

Structure and Performance in Listed Australian Companies. Australian Journal of

Management, Vol. 28, No. 3.

Available at:

http://www.agsm.edu.au/eajm/0312/pdf/welch.pdf

Accessed: 15/05/2010

Williams, R.J., Haka, S.F and Bettner, S.M. (2005). Financial and Managerial

Accounting, thirteen ed. New York: McGraw-Hill/Irwin.

Wood, F. and Sangster, A. (2007). Business Accounting, tenth ed. England: Pearson

Education Limited.

Wyld, J. and Hussain, A. (2008). Managing Trough Information for Postgraduates. Great

Britain: Pearson Education Limited.

Yeh, Y., Ko,C. and Su, Y. (2003). Ultimate Control and Expropriation of Minority

Shareholders: New Evidence from Taiwan. Academia Economic Papers.

Available at:

http://www.econ.sinica.edu.tw/upload/file/enaep31-3-2-abs.pdf

Accessed: 15/05/2010