Reinsurance Market Outlook · Insured Losses 140,000 2005 Katrina, Rita, Wilma 120,000 1992...

47

Reinsurance Market Outlook David Simmons, Head of Aon Benfield Publications May 2009 Proprietary & Confidential

Transcript of Reinsurance Market Outlook · Insured Losses 140,000 2005 Katrina, Rita, Wilma 120,000 1992...

Reinsurance Market OutlookDavid Simmons, Head of Aon Benfield Publications

May 2009

Proprietary & Confidential

Market Background

Proprietary & Confidential

2009 Economic Outlook

GDP contraction / low growth

Unemployment

600 Change in Non-Farm Payroll

Unemployment

Government intervention

Low reinvestment yields 200

400

y

Deflationary and inflationary risk

Market volatility200

0

hous

ands

Less leveraged optimal capital structures

Capital markets open but expensive -400

-200ThChanging investor interest

Economic and regulatory capital changes-800

-600

… and/or increased M&A

Source: Bloomberg U S Bureau of Labor Statistics

-800Jan 00 Jan 02 Jan 04 Jan 06 Jan 08

Proprietary & Confidential

Source: Bloomberg, U.S. Bureau of Labor Statistics

2

Financial MarketsEquity marketsJan 2001 = 100

5-year government bond yields

6%

5%

6%

110

130

4%90

2%

3%

50

70

1%

%

Jan Jan Jan Jan Jan Jan Jan Jan Jan30

50

Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan 01

Jan 02

Jan 03

Jan 04

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

UK Eurozone USA

Jan 01

Jan 02

Jan 03

Jan 04

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

S&P 500 FTSE 100Eurotop 100 Nikkei

Proprietary & Confidential 3

Source: Bloomberg

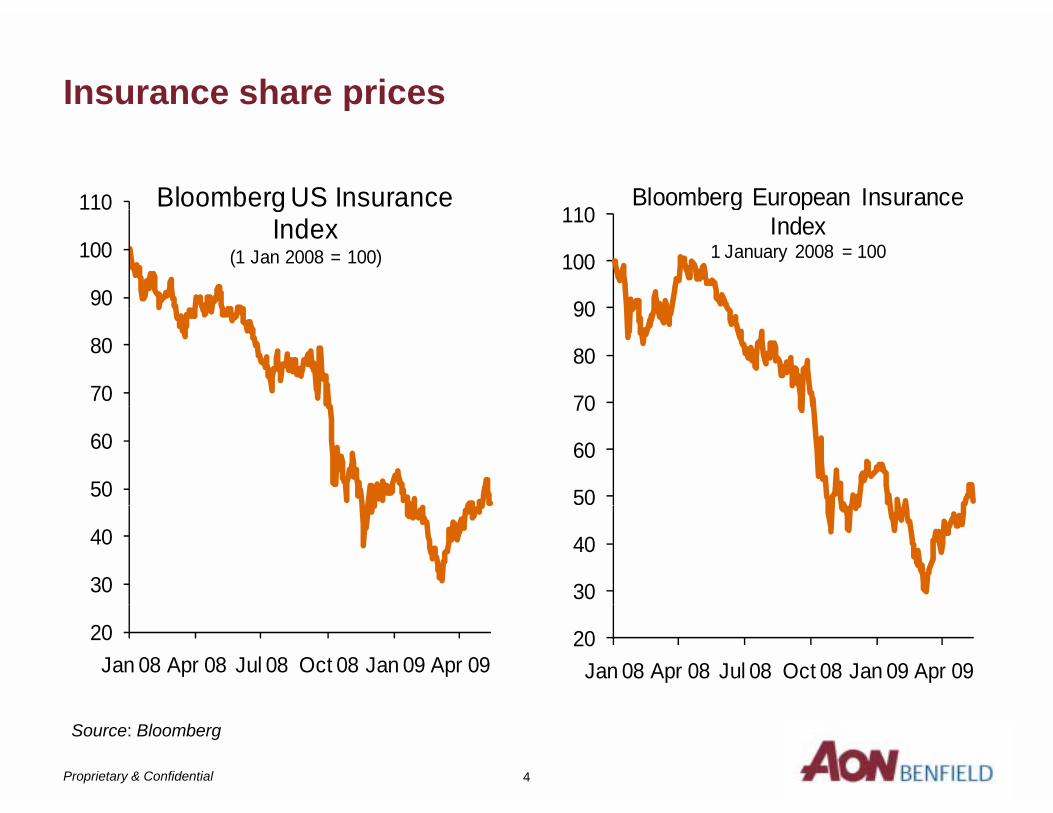

Insurance share pricesp

110 Bloomberg US Insurance 110

Bloomberg European Insurance

90

100

110 gIndex

(1 Jan 2008 = 100)

90

100

110g p

Index1 January 2008 = 100

70

80

70

80

90

50

60

50

60

70

30

40

30

40

20Jan 08 Apr 08 Jul 08 Oct 08 Jan 09 Apr 09

20Jan 08 Apr 08 Jul 08 Oct 08 Jan 09 Apr 09

Proprietary & Confidential 4

Source: Bloomberg

CDS Spreadsp

1,200 900

1,000700

800

600

800

s po

ints

400

500

600

poin

ts

400

Bas

i

200

300

400

Bas

is

200

0

100

200

0Jan 08 Apr 08 Jul 08 Oct 08 Jan 09 Apr 09

XL Berkshire ACEOdyssey Axis

Jan 08 Apr 08 Jul 08 Oct 08 Jan 09 Apr 09

Swiss Re Munich ReHannover Re SCOR

Proprietary & Confidential

Source: Bloomberg

5

Odyssey Axis Hannover Re SCOR

Insured Losses

140,0002005 Katrina, Rita, Wilma

120,000

1992 Hurricane Andrew 2001 September 11

2004 Charlie, Frances, Ivan, Jean, Songda 2008 Ike

80,000

100,000

8 pr

ices

)

1994 Northridge

1999 Storm Lothar

40,000

60,000

USD

bn (2

00 Earthquake

20,000

,U

01970 1975 1980 1985 1990 1995 2000 2005

Man-made disasters Natural catastrophes

Proprietary & Confidential 6

Source: Swiss Re, sigma no 2/2009

Ike and Top Ten Catastrophe Losses

8 9

7.9

Typhoon Mirelle/No

Hurricane Hugo

11.1

9.2

8.9

Hurricane Rita

Hurricane Charley

Typhoon Mirelle/No …

20 0

14.7

13.8

Hurricane Ike

Hurricane Ivan

Hurricane Wilma

22.8

20.3

20.0

Terror Attack on WTC

Northridge …

Hurricane Ike

71.3

24.6

0 20 40 60 80

Hurricane Katrina

Hurricane Andrew

0 20 40 60 80USDbn

Source: Swiss Re sigma 2/2009 Aon Benfield Analytics Research

Proprietary & Confidential 7 7

Source: Swiss Re, sigma 2/2009, Aon Benfield Analytics Research

Other catastrophe losses in USD indexed to 2008

Insurer Impairment Correlates With Underwritingp g

120%70

110%

115%

50

60

s

105%

110%

40

50

ned

ratio

pairm

ents

95%

100%

20

30

Com

bin

No

of Im

p

85%

90%

0

10

1969 1973 1977 1981 1985 1989 1993 1997 2001 2005

No of Impairments P&C Combined Ratio (RH scale)

Proprietary & Confidential 8

Source: A.M. Best Special Report 6 April 2009

Reasons For Insurer Impairment 1999 – 2008p

0%R d f i i

27%

Reserve def iciency

Rapid growth

Af f ili t bl40%

Aff iliate problems

Catastrophe losses

Mi ll

4%2%

Miscellaneous

Alleged f raud

O t t d t

6%6%

3% Overstated assets

Signif icant changes

U id if i d6%12% Unidentif ied

Reinsurance failure

Proprietary & Confidential 9

Source: A.M. Best Special Report 6 April 2009

2008 Reinsurer Results

Top 10 Concentration: Market Share Of Top 10 Aon Benfield Research P&C Reinsurance Groupsp

2008 GPW: USD 135bn

16%

Munich Re

Swiss Re

40%

Lloyd's

Hannover Re

Berkshire Hathaway13%

y

SCOR

Transatlantic Re

P t R9%

5%

Partner Re

Everest Re

Mapfre Re5%

4%3%3%3%2%

2% Remainder

Proprietary & Confidential 11

Source: Aon Benfield Analytics Research

Aon Benfield Aggregate Combined Ratiogg g

5.6% 4.6% 95.7%110%

90.8%

70%

90%

65.2%63.8%

50%

29.1% 29.5%10%

30%

-2.0%-10%

10%

2007 COR Expenseratio

Loss ratio G&I losses Prior yearreserve adj

2008 COR

Proprietary & Confidential 12

Source: Company Data, Aon Benfield Analytics Research

2008 Combined Ratios

Paris Re

White Mountains

Transatlantic Holdings

Odyssey

ACE

ABA*

Swiss Re

Allied World

Flagstone Re

40% 50% 60% 70% 80% 90% 100% 110%

IPC Holdings

RenaissanceRe

40% 50% 60% 70% 80% 90% 100% 110%

Combined Ratio (Reporting Currency)

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

13

2008 Prior Year Reserve Adjustmentsj

IPC Holdings

Max Capital

Montpelier Re

Allied World

Odyssey

ABA*

RenaissanceRe

SCOR

Transatlantic Holdings

Odyssey

2% 2% 6% 10% 14% 18% 22% 26% 30%

Everest Re

White Mountains

-2% 2% 6% 10% 14% 18% 22% 26% 30%

Prior Year Reserve Adj as % NPE (Reporting Currency)

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

14

2008 Hurricane Losses

Montpelier Re

IPC Holdings

Validus

Flagstone Re

XL Capital

ABA*

RenaissanceRe

White Mountains

Munich Re

XL Capital

SCOR

ACE

0% 5% 10% 15% 20% 25% 30% 35%

Gustav & Ike Losses as % NPE (Reporting Currency)

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

15

Development of Aon Benfield Aggregate Shareholders’ Fundsp gg g

-5-524

170

-17-5158

150

160

127-1

-9

130

140

US

D b

n

120

130

100

110

31 Dec Additional Net Dividends FX Investment Share Other 31 Dec31 Dec2007 SHF

AdditionalCapital

Net Income

Dividends FX Investmentlosses

Sharebuybacks

Other 31 Dec2008 SHF

Proprietary & Confidential 16

Source: Company Data, Aon Benfield Analytics Research

2008 Shareholders’ Funds, % Changeg

Odyssey

Allied World

Aspen

Validus

Odyssey

ABA*

PartnerRe

XL Capital

Max Capital

Flagstone Re

White Mountains

Swiss Re

XL Capital

-40% -35% -30% -25% -20% -15% -10% -5% 0% 5% 10%

% Change in 2008/2007 Shareholders' Funds (Reporting Currency)

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

17

Aon Benfield Aggregate 2008 Invested Asset Splitgg g p

Total Invested Assets 31 December 2008 USD698bn

14%

5%

Fixed Interest investments

Cash and cash equivalents

Oth i t t9% Other investments

Equity investments

72%

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

18

2008 Invested Asset Leverageg

Swiss Re

SCOR

Munich Re

Hannover Re

ABA*

XL Capital

SCOR

R i R

Montpelier Re

Validus

IPC Holdings

Flagstone Re

RenaissanceRe

0 1 2 3 4 5 6 7 8 9 10

g

Invested Asset Leverage (Reporting Currency)

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

19

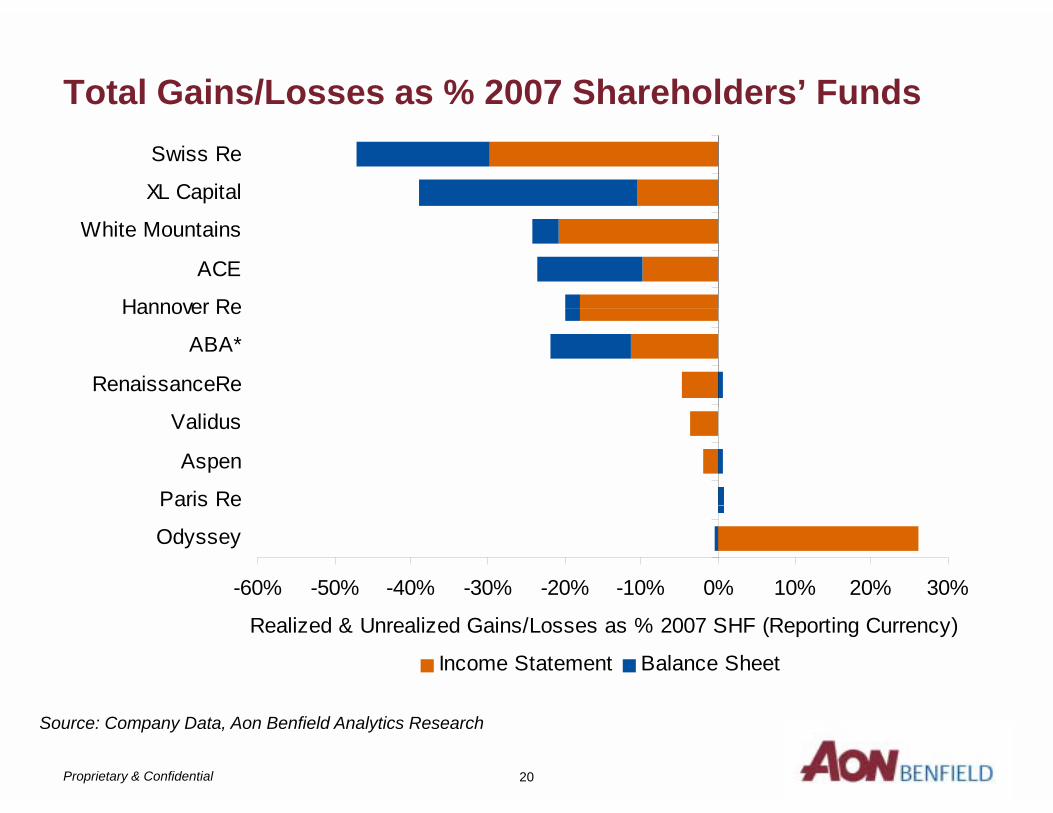

Total Gains/Losses as % 2007 Shareholders’ Funds

XL Capital

Swiss Re

Hannover Re

ACE

White Mountains

RenaissanceRe

ABA*

Hannover Re

Paris Re

Aspen

Validus

-60% -50% -40% -30% -20% -10% 0% 10% 20% 30%

Odyssey

Paris Re

Realized & Unrealized Gains/Losses as % 2007 SHF (Reporting Currency)

Income Statement Balance Sheet

Proprietary & Confidential

Source: Company Data, Aon Benfield Analytics Research

20

Reinsurers 10-year Risk/Return* Comparisony p

WR Berkley

20%

HannoverRe

ACE Everest

RenaissanceRe15%

erag

e

Hannover Re

Swiss RePartnerRe

TransatlanticOdyssey

IPCNat Indemnity

10%

-200

8 A

ve

Munich Re White MountainsXLIPCNat. Indemnity

GeneralRe

0%

5%

RoE

199

9 -

SCOR-5%

0%R

5%0 p.p. 5 p.p. 10 p.p. 15 p.p. 20 p.p. 25 p.p.

Standard Deviation 10 Year

Proprietary & Confidential

*Pre-tax operating return on average equity

Source: Company Data, Aon Benfield Analytics Research21

Reinsurer Rating Changesg g

Everest ReEverest Re

Transatlantic Re

Atradius

S i RSwiss Re

SCOR

Secura

NR

2001 2008 Mar 2009

NR BBB A AA AAA

Proprietary & Confidential 22

Source: Standard & Poor’s, Aon Benfield Analytics Research

Reinsurer Rating Changesg g

60

50

30

40

D bn

20

USD

0

10

0AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- NR

2001 2008 Mar 2009

Proprietary & Confidential 23

Source: Standard & Poor’s, Aon Benfield Analytics Research

2008 Lloyd’s Results2008 Lloyd’s Results

2003-2008 Results

GBPmn 2004 2005 2006 2007 20082008/7

% chGross written premiums 14,614 14,982 16,414 16,366 17,985 10%Reinsurance as % GWP 20% 21% 24.1% 19.0% 21.0% 2ppNet written premiums 11,734 11,770 13,201 13,256 14,217 7%Net earned premiums 11 797 11 785 12 688 13 097 13 796 5%Net earned premiums 11,797 11,785 12,688 13,097 13,796 5%Net claims incurred 7,646 9,505 6,219 6,547 8,464 29%Net operating expenses 3,755 3,668 4,327 4,451 4,134 -7%Underwriting result 396 -1,388 2,142 2,099 1,198 -43%C bi d i 96 6% 111 8% 86 0% 84 0% 91 3%Combined ratio 96.6% 111.8% 86.0% 84.0% 91.3% 7ppProfit before tax 1,367 -103 3,662 3,846 1,899 -51%Net resources (incls sub debt) 12,169 10,992 13,333 14,461 15,264 6%Equity 11,663 10,491 12,836 13,449 14,182 5%q y , , , , ,Central assets 1,663 1,850 2,054 2,465 2,608 6%Pre tax return on average net resources 12.3% -0.9% 31.4% 29.3% 13.7% -16pp

Proprietary & Confidential

Source: Lloyd’s, Aon Benfield Analytics Research

25

Proforma Results

4

4.5

30%

35%

3

3.5

n 20%

25%

30%

1 5

2

2.5

GBP

bn

10%

15%

20%

0.5

1

1.5

5%

10%

-0.5

0

2004 2005 2006 2007 2008-5%

0%

2004 2005 2006 2007 2008

Profit before tax (LH scale) Pre-tax return on capital (RH scale)

Proprietary & Confidential

Source: Lloyd’s, Aon Benfield Analytics Research

26

Combined Ratio by Business Liney

123.8%140%

99.6% 96.7% 95.1%86 8%

100%

120%

d ra

tio

86.8% 84.6% 83.8%80%

r com

bine

d

40%

60%

enda

r yea

r

0%

20%Cale

0%Energy Motor Property Casualty Aviation Marine Reinsurance

2007 2008

Proprietary & Confidential

Source: Lloyd’s, Aon Benfield Analytics Research

27

Prior Year Reserve Adjustmentsj

-1.3%

0%

p.p.

-6.5%7 8%

-5%

mov

emen

t p

-7.8% -8.2%

-12.1%

-8.8%-10%

rese

rve

m

20%

-15%

Prio

r yea

r

-23.7%-25%

-20%

Motor Property Marine Energy Casualty Reinsurance Aviation

2007 2008

Proprietary & Confidential

Source: Lloyd’s, Aon Benfield Analytics Research

28

2009 Outlook

Proprietary & Confidential

1Q 2009 Changes in Shareholders’ Fundsg

GAAP Equity Change, Investment Losses and Invested Asset Ratio - Reinsurers Net Net Total realized Investment

Change realized unrealized & unrealized losses Invested Invested GAAP GAAP in investment investment investment as % of Total Total assets assets equity equity GAAP losses losses losses GAAP equity investments investments leverage leverage

Company 31/03/2009 31/12/2008 equity 31/03/2009 31/03/2009 31/03/2009 31/12/2008 31/03/2009 31/12/2008 31/03/2009 31/12/2008Arch 3,630 3,433 6% (41) 58 17 0% 11,109 10,800 3.1 3.1Aspen 2,832 2,779 2% (12) 1 (11) 0% 6,063 5,754 2.1 2.1AXIS 4,493 4,461 1% (40) (58) (98) -2% 10,841 10,925 2.4 2.4Endurance 2,254 2,207 2% (10) (8)** (18) -1% 5,606 5,502 2.5 2.5Endurance 2,254 2,207 2% (10) (8) (18) 1% 5,606 5,502 2.5 2.5Everest 5,040 4,960 2% (48) 47 (2) n.a. 13,737 13,863 2.7 2.8Flagstone 1,224 1,183 3% 6* - 6 0% 1,777 1,708 1.5 1.4Hannover Re 4,526 4,696 -4% (17)* (294) (311) -7% 42,602 42,404 9.4 9.0IPC 1,849 1,851 0% (36)* - (36) -2% 2,218 2,263 1.2 1.2Max 1,263 1,280 -1% 18 (66) (48) -4% 5,036 5,410 4.0 4.2Montpelier 1,437 1,358 6% (5)* 9 4 0% 2,451 2,365 1.7 1.7Munich Re 28 660 29 965 4% 50* (212) (162) 1% 230 308 242 614 8 0 8 1Munich Re 28,660 29,965 -4% 50 (212) (162) -1% 230,308 242,614 8.0 8.1Odyssey 2,714 2,828 -4% (65) (87)** (151) -5% 7,534 7,959 2.8 2.8PartnerRe 4,282 4,199 2% (5)* (64)* (69) -2% 11,901 12,236 2.8 2.9Platinum 1,829 1,809 1% 15* (2)** 13 1% 4,347 4,289 2.4 2.4RenaissanceRe 3,121 3,033 3% 3* (5)* (2) 0% 6,307 6,244 2.0 2.1SCOR 4,764 4,816 -1% (171)* (447) (618) -13% 22,748 23,924 4.8 5.0Swiss Re 17,876 22,585 -21% (2,094)* (1,584) (3,678) -16% 167,466 171,356 9.4 7.6T tl ti 3 321 3 198 4% (61)* 105 44 1% 11 014 10 660 3 3 3 3Transatlantic 3,321 3,198 4% (61)* 105 44 1% 11,014 10,660 3.3 3.3Validus 2,023 1,939 4% (23)* 22* (1) 0% 3,483 3,302 1.7 1.7White Mountains 3,482 3,513 -1% (23)* (21)* (45) -1% 9,569 9,474 2.7 2.7Total 100,622 106,093 -5% (2,559) (2,606) (5,165) -5% 576,118 593,052 5.7 5.6

As at 8 May 2009USD mn Foreign exchange at balance sheet date*Pre-tax realized/unrealized **Other CompreInvestments include cash and securities lendingSource: Company data

Proprietary & Confidential 30

Reinsurance 2009 Projectionsj

M&A activity

N t tNew entrants

Cat bond issuance

Share buybacks

Tax environments

Some existing players very well placed• High business diversification• Focus on traditional reinsurance business• Prudent and conservative asset management policy• Limited leverage through medium term capital management strategy• Focus on liquidity and operational cash flow

Proprietary & Confidential 31

Some Challenges and Opportunities g pp

Demand• Certainty of demand • Reduction in economic activity• Reinsurance diversification

S lSupply• Healthy financial situation• Capital management• Product innovation• Product innovation

Pricing• Recessionary claimsy• Inflation and deflation• Prior year adjustments• Investment returns

Proprietary & Confidential 32

Consolidation

Proprietary & Confidential

Top 20 Nations by GDPInsurance company domestic non life market sharep y

India100%Japan

ChinaFranceSouth Korea

T k

Sweden

80%ket

shar

e

UKItaly

CanadaAustralia

TurkeyBelgium

60%e co

mar

k

USAGermanySpain

CanadaBrazil

RussiaNetherlands

Indonesia60%

nsur

ance

y

Mexico40%

Top

10 i

20%0.1 1.0 10.0

GDP USD trillions (Log scale)

Proprietary & Confidential

Source: International Monetary Fund, Aon Benfield ResearchGDP USD trillions (Log scale)

Selected countriesInsurance company domestic non life market sharesp y

77.6%78.8%80%

90%

51.8%60%

70%

29.9%30.8%30.2%40%

50%

10%

20%

30%

0%

10%

USA Japan Germany China UK Netherlands

Market leader # 2 # 3 # 4 # 5

Proprietary & Confidential

Source: International Monetary Fund, Aon Benfield Research

Consolidation

1

1.2

50

60

0.8

1

40

50

rers

0.6

W U

SDbn

30

of R

eins

u

0.4

NPW

20

Num

ber

0.2 10

01995 1997 1999 2001 2003 2005 2007

0

Average NPW (LH scale) RAA Reinsurers (RH Scale)

Proprietary & Confidential 36

Source: Reinsurance Association of America, Aon Benfield Research

Lloyd’s Average Syndicate Capacity & Numbery g y p y300

400

450

200

250

300

350

400

er

150

200

BPm

n 250

300

ate

num

be

100

GB

150

200

Synd

ica

5050

100

01989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

0

Average syndicate capacity (LH scale) No. of syndicates (RH scale)

Proprietary & Confidential 37

Source: Lloyd’s, Moody’s, Aon Benfield Research

Lloyd’s M&AyDate Acquirer Target Price

GBPmnSyndicates

May 2007 Validus Holdings Talbot Underwriting 200e 1183

Jul 2007 Ariel Re Atrium Underwriting 193 570, 609

Jul 2007 Sagicor Gerling at Lloyd's n.a. 1209

Oct 2007 Munich Re MSP Underwriting 52 318

Dec 2007 Tokio Marine & Nichido Fire Kiln Ltd 442 308, 510, 557, 807

Dec 2007 American Financial Group Marketform 37 2468

Apr 2008 Argo Group Heritage Underwriting Agency 137 1200, 3245g g g g y

Jul 2008 Ironshore Pembroke 17 4000

Jul 2008 AIG Ascot n/a 1414

Aug 2008 Max Capital Imagine Group (UK) Ltd 101 1400, 2525, 2526g p g p ( ) , ,

Aug 2008 Fairfax Advent 67.2 2, 780

Sep 2008 Beazley Momentum Underwriting Management Ltd. (MUM)

Up to USD37.5mn

3623, 3622

Oct 2008 Flagstone Re Marlborough Underwriting Agency Ltd

n/a 1861

Feb 2009 Beazley First State Management Group Inc

24 623,2623

Proprietary & Confidential 38

Inc

Source: Lloyd’s, Company information, Aon Benfield Research

Desaparición o cierre de reaseguradores en los últimos 10 añosDesaparición o cierre de reaseguradores en los últimos 10 años

H tf d R •Gerling Re•Hartford Re

•Lexington

•AIU Re

Gerling Re

•Chiyoda

•Reliance•AIU Re

•REAC

•New Cap

Reliance

•CNA Re

•Nationwide Re•New Cap

•Signet Star

•American Re

•Kemper Re

•CopenhagenAmerican Re

•Rhine Re •F&G Re

•GIO Re

Proprietary & Confidential

Compras o fusiones de reaseguradores

C

Brockbank Synd

Cat ReACE

Capital Re

Tempest Re

AXAGroupe Victorie

AXAGRE Re

General Re

Cologne Re BerkshireCologne Re

Global Aviation

Berkshire Hathaway

Proprietary & Confidential

Compras o fusiones de reaseguradores

Transcontinentale Re

Skandia AmericaFairfax FinancialSphere Drake

Ranger Re

Christiania GeneralFolksamericaUSF Re

ScorSorema Scor

Proprietary & Confidential

Compras o fusiones de reaseguradores

Aachen Re

Cigna Re (Japan & K )

General Electric / ERC

Korea)

Eagle Star

Frankona Re

Industrial Risk Insurance

Medical Protective

National Re

NRG Victory

Nordisk Re

Skandia InternationalSkandia InternationalHannover Re

ClarendonClarendonHannover Re

Proprietary & Confidential

Compras o fusiones de reaseguradoresp g

Equus ReKKR

Equus Re

Rhine Re

American Re

Munich ReNew Re

Real Riassicurazione

SAFRSAFR

Winterthur RePartner Re

Proprietary & Confidential

Compras o fusiones de reaseguradoresCompras o fusiones de reaseguradores

St. Paul ReCigna Re (Asia, Europe & LA)

F&G Re

Mercantile & General

Swiss Re

Reaseguros Alianza

Reaseguradora de Colombia Swiss Re

Unione Italiana de Riassicurazione

Union Re

Lincoln Life

Proprietary & Confidential

Compras o fusiones de reaseguradoresCompras o fusiones de reaseguradores

Chartwell ReTrenwick Re

Chartwell Re

La Salle Re

Sorema UK

Latin American Re

XL CapitalLe Mans Re

Mid Ocean

Nac ReNac Re

Guardian Re Transatlantic Re

Proprietary & Confidential

ContactsDavid Simmons T: +44 (0)20 7522 4177

Aon Benfield T: +44 (0)20 7522 3823Analytics Research E: [email protected]

© Aon Limited trading as Aon Benfield (for itself and on behalf of each subsidiary company of Aon Corporation) (“Aon Benfield”) reserves allrights to the content of this document. This document is provided exclusively for the use of the directors and employees of the organisation towhich it was originally delivered. Copies may be made by that organisation for its own internal purposes, but no part of this document may bewhich it was originally delivered. Copies may be made by that organisation for its own internal purposes, but no part of this document may bemade available to any third party without both (i) Aon Benfield’s prior written consent and (ii) that third party having first signed a “recipient ofreport” letter in a form acceptable to Aon Benfield. Aon Benfield will accept no liability to any third party to whom this document is disclosedwhether in compliance with the preceding sentence or otherwise. This document does not constitute any form of legal, accounting, taxationregulatory or actuarial advice. Without prejudice to the generality of the preceding sentence this document does not constitute an opinion ofreserving levels or accounting treatment. The recipient acknowledges that in preparing this document Aon Benfield may have based analysis ondata provided by the recipient and/or from third party sources. This data may have been subjected to mathematical and/or empirical analysisand modelling. Aon Benfield has not verified, and accepts no responsibility for, the accuracy or completeness of any such data. In addition, theand modelling. Aon Benfield has not verified, and accepts no responsibility for, the accuracy or completeness of any such data. In addition, therecipient acknowledges that any form of mathematical and/or empirical analysis and modelling (including that used in the preparation of thisdocument) may produce results which differ from actual events or losses. Where this document includes a recommendation or an assessmentof risk, the recipient acknowledges that such recommendation or assessment of risk is an expression of Aon Benfield’s opinion only and not astatement of fact. Any decision to rely upon any such recommendation or assessment will be solely at the risk of the recipient, for which AonBenfield accepts no liability, and the recipient acknowledges that this document does not replace the need for the recipient to make its ownassessment. Aon Benfield will not be liable, in any event, for any special, indirect or consequential loss or damage of any kind (including, but notlimited to, loss of profit and business interruption) arising from any use of the information contained in this document. Aon Limited is authorised

Proprietary & Confidential 46

ted to, oss o p o t a d bus ess te upt o ) a s g o a y use o t e o at o co ta ed t s docu e t o ted s aut o sedand regulated by the Financial Services Authority in respect of insurance mediation activities only.