Regulatory roadmap in retail finance Monika Halan 4 June 2015, Mumbai.

59

Regulatory roadmap in retail finance Monika Halan 4 June 2015, Mumbai

-

Upload

kerrie-ramsey -

Category

Documents

-

view

214 -

download

0

Transcript of Regulatory roadmap in retail finance Monika Halan 4 June 2015, Mumbai.

Regulatory roadmap in retail finance

Monika Halan4 June 2015, Mumbai

2 disruptors

Technology

Regulation

1. Technology

• Do-it-yourself options are disrupting advice• Apps will allow investors to make comparisons• Machine readable disclosures will make

products transparent• And the robots are coming!

Robots are coming!

Robots.....

Google Maps

• GPS on our phones has come from data disclosure by the US government

• US defence initiative for sending up satellites• Clinton decided to make data public• Now you don’t get lost!

What will disclosure do to finance

• Machine readable data will change the world of finance

• Hidden behind obfuscation instead of disclosure• When product costs, returns and benefits are

truly comparable, advisors will have to add real value – right now they are product decoders

Machine readable

• Machine readable is not a soft copy• It is data that can be read by a computer• Re-imagine finance with data disclosure

requirements that include the words: machine readable

Role of wealth managers

• Will change from being well paid product decoders to solving people’s financial problems

• Will have to upgrade on quality of advice• Will have to brace for much more scrutiny

2. Regulation

I. Post 2008 rush towards increased regulationII. How did we get here?III. What lies ahead?

I. Post 2008, increased global focus on consumer protection

• UK: Fines on mis-selling have totalled GBP 9 billion, commissions banned

• Australia: commissions banned 2012 – front, trail, exit

• USA: $140 billion in fines in 2 years. CPFB has been set up, but regulations remain weak

Indian regulatory eye on consumer protection

• Focus on mis-selling of retail finance• Sebi: mis-selling funds came under FUTP

regulations in 2012• RBI: put out a charter of consumer rights 2014• Irda: reworked its Protection of Policyholder

interest regulation in 2014

Why increased focus on protection?

• Investors lost Rs 1.5 trillion in the ULIP mis-selling scam by FY 2012

• Another Rs 60,000 crore lost by investing in traditional policies in FY12 and FY13

• Hidden cost in mutual funds cost investors Rs 2,200 crore in 22 months

II. Why protect consumers of finance?

• Universe is bigger than just investors• Financial products are across banking, credit,

insurance and managed investment• Our worry is more about non stock market

consumers of financial products

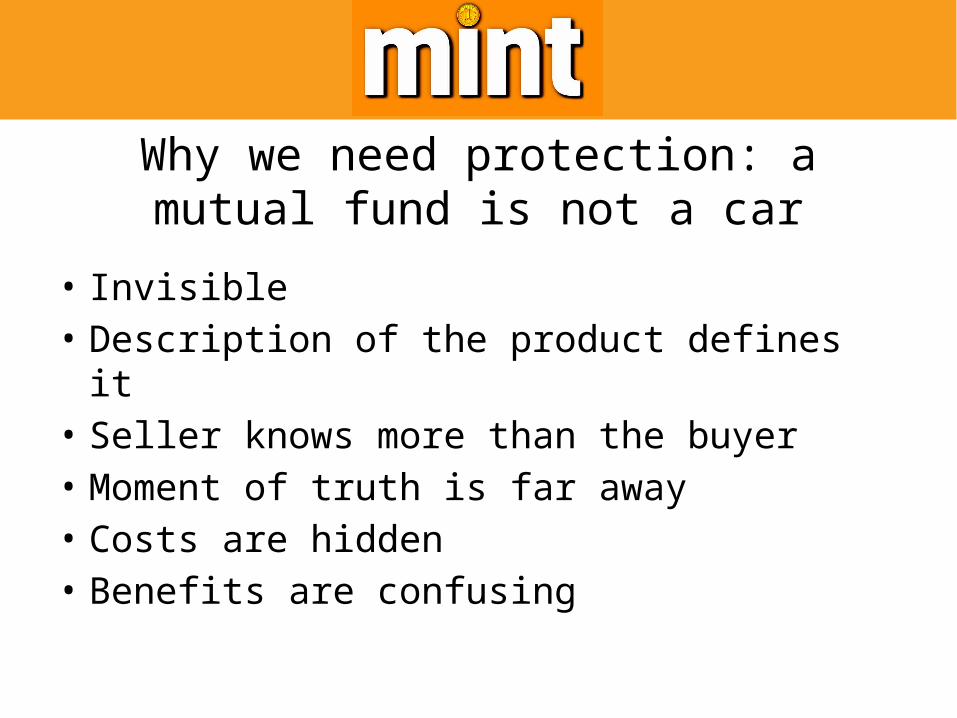

Why we need protection: a mutual fund is not a car

• Invisible• Description of the product defines it• Seller knows more than the buyer• Moment of truth is far away• Costs are hidden• Benefits are confusing

What is so harmful?

• Financial products are not bad in their own right

• But the wrong financial product is harmful• Selling high cost insurance to a 70 year old is

like forcing a diabetic to eat sugar• Sector fund to a first time equity investor

Regulators make it worse

• Confusion in the market place – similar products with different rules

• Regulators fight over turf• Push market• Buyer beware

Impact of cheating

• Households lose faith in the system• Low reach of financial products• Households stay in low return gold and

deposits• Stay under-insured• Lose money to ponzi schemes or to inflation

III. How did we get here?

• Regulatory thought is imported• Based on a disclosure + financial literacy +

buyer beware model• This rests on basic tenants of Economics– Rational economic agents– Utility maximisation– Making optimal choices from a free marketplace

Econs vs Humans

• Textbook market places are unreal– Where there is perfect information to all market

players– Where every economic agent maximises utility– Where prices rise and fall precisely to changes in

demand and supply– Economic agents are always rational

Market outside econ books is very different

• People are not rational and do not make ‘perfect’ economic choices

• People make emotional decisions• People get swayed by anchoring• People are loss averse• People have money illusion• None of this reflects in the way regulation

looks at the world

What goes on in the brain of an investor?

Economic theory vs real life

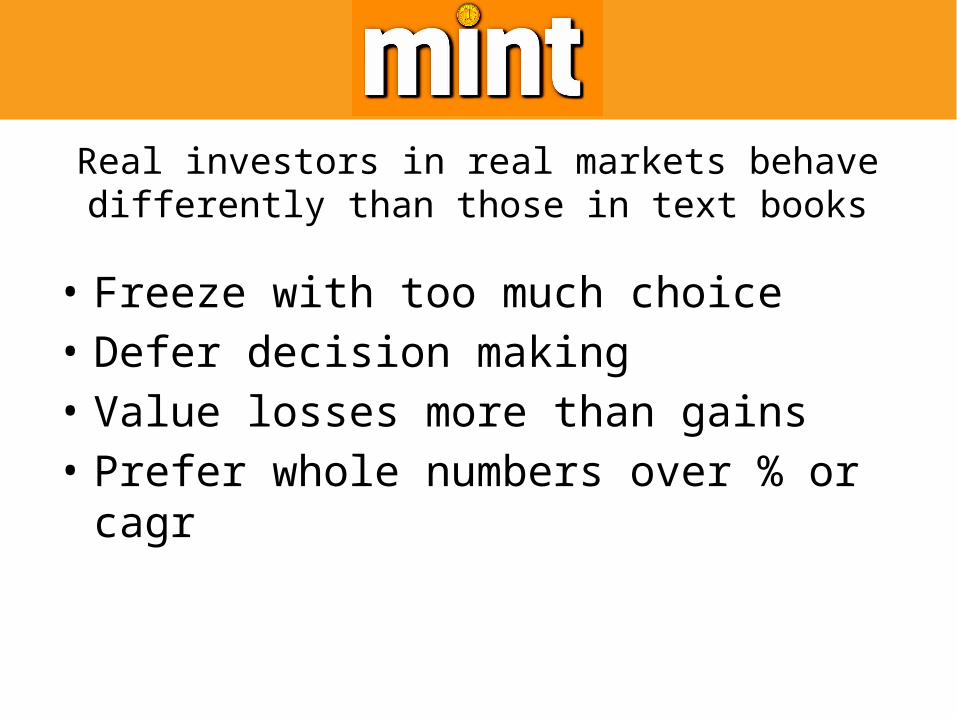

Real investors in real markets behave differently than those in text books

• Freeze with too much choice• Defer decision making• Value losses more than gains• Prefer whole numbers over % or cagr

1. Lots of choice: good or bad?

Good to have at least one product over none

More choice is good

Better to have some choice

But how much choice is too much?

In standard economics, more choice is always better because I can simply ignore the less desirable choices

< <

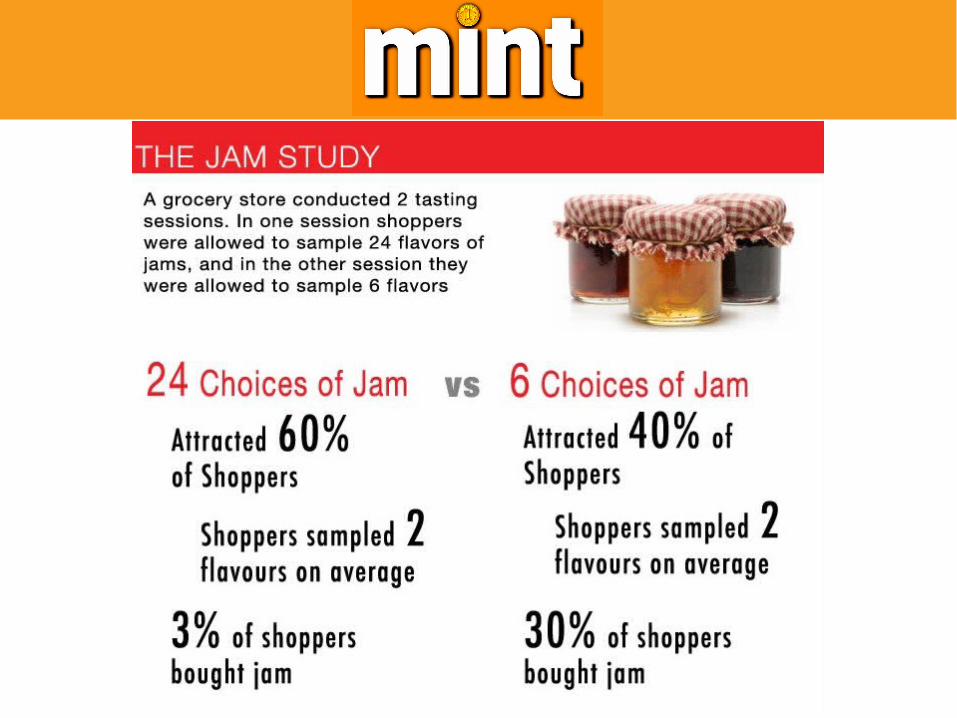

Too much choice freezes consumers

• A corpus building investor will have to decide if she wants to:– Invest in PPF, NPS, insurance linked investment,

mutual funds– Within insurance and funds there are multiple

options and choices– Result: consumer freeze – financial assets of

households < 8% of GDP

Too much choice freezes consumers

• Choice set for income funds in India

2. Investors hate taking decisions

• Ideally investors would like to leave the decision making to somebody else

• The use of defaults have been used smartly by corporations to get people to buy more or buy stuff they don’t need

• Ticking a box is taking a decision and most times investors don’t want to do take the call if they don’t need to

Organ donation rates in Europe

28% and 98%

Did they spend more?

• Extensive campaigning in the Netherlands• Resulted in a 28% rate of organ donation

• Belgium spent NOTHING

The Belgian Secret

3. Investors hate to lose• Old Econ says: Re 1 = Re 1• Old Econ says: Gain of Re 1 = Loss of Re 1• Old Econ says: If the payoff is the same, it does

not matter whether you are gaining or losing – investors will choose rationally in both situations

• Real life is different

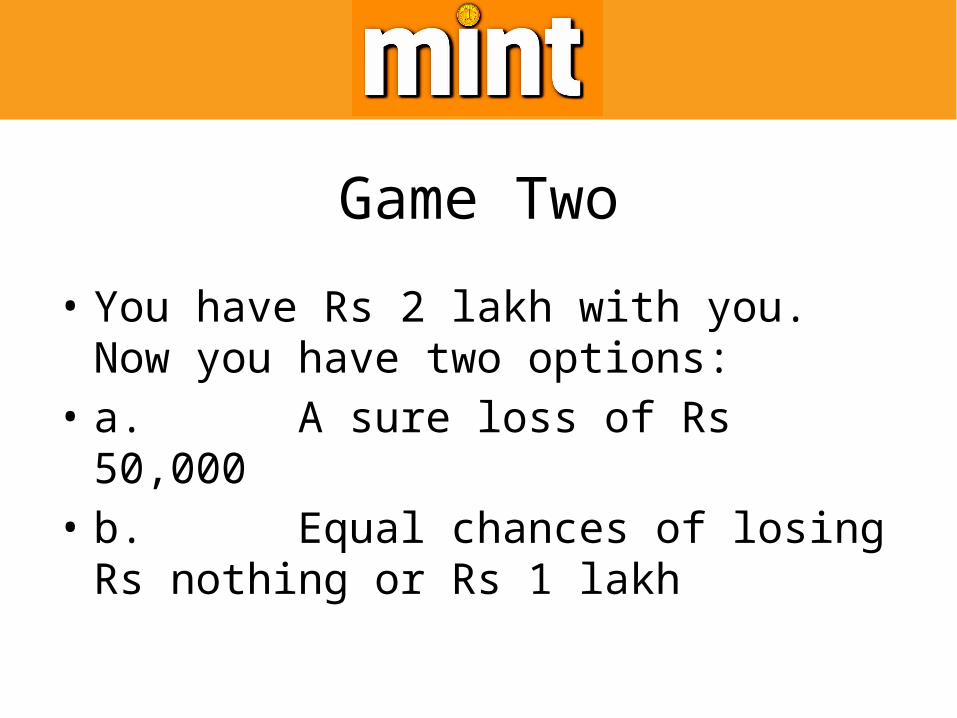

Game One

• You have Rs 1 lakh with you. Now you have two options:

• a. A sure gain of Rs 50,000• b. Equal chances of gaining Rs 1 lakh or

nothing

Game Two

• You have Rs 2 lakh with you. Now you have two options:

• a. A sure loss of Rs 50,000• b. Equal chances of losing Rs nothing or Rs

1 lakh

Results: loss aversion

• Most people choose the sure gain in Game One and choose to gamble in Game Two.

• Their economic choice set changes even though the final result of the two games is exactly the same: – Rs 1.5 lakh in option a– either Rs 1 lakh or Rs 2 lakh in option b

4. Investors don’t do the math

• Deal 1: Invest Rs 1 lakh a year for 10 years15 years later take home Rs 20 lakh

• Deal 2: The CAGR of an equity fund over 20 years= 23%

Whole numbers over %

• Deal 1: Investors make 6.6% a year• Deal 2: Investors made 23.25% a year• But deal 1 looks more attractive in the way it is

framed

Framing meant to cheat

Unfairness and how we respond

• Active miscommunication and cheating by one part of the market

• But how do investors react to unfairness and cheating?

How we react to unfairness• The usual auto fare is Rs 50 between your

office and home• It rains heavily and the metro is flooded• Autos charge Rs 200 for the same ride• Fair or unfair?• How we are programmed to react to

unfairness!• Unfair!

Behavioural Econ getting hard wired

• Machine readable• Comparable• Tax letters in the UK• Save More Tomorrow in the US• Focus on product design in Australia

UK’s FSA leads the way• FSA chief said in May 2015:• “The FCA wants to make sure customers are

far more easily able to compare product prices and to assess their value”.

• “We want the regulatory system to use behavioural economics to ascertain whether people are being put off switching products through inertia, inattention or even the simple fear of regret from making a wrong decision”

NPS and defaults

• NPS has used defaults to nudge people into lifecycle funds

• The choice set is restricted so as to not freeze people

• But NPS has not taken off• Badly designed products and incentives in

insurance are causing market failure

Regulatory changes

• Regulatory changes– FSLRC and the Indian Finance Code– Consumer protection at heart of the new IFC– Fiduciary system– Regulatory pointers in this framework

• Use of behavioural finance by policy makers– Very low cost interventions can have dramatic

effects– Willingness to experiment?

India to have a seller-beware system

• India will have a fiduciary system that puts the onus on the seller and manufacturer of a financial product to look after the financial health of the consumer

• The regulatory cost and intrusion of such a system will be prohibitive unless we work on

• A 3-part market structure that cleans up the road that leads to a fiduciary system

Role of a fiduciary

• One who looks after the customers’ interest• Australia – financial planning regulation• UK – all financial products are now no-load• Big ticket payouts by banks mis-selling

insurance and other products have happened• Most markets have strict rules around

suitability

What is suitability

• Selling insurance to a 70 year old is like forcing a diabetic to eat sugar

• Matching a financial product to the financial need of the customer

• Financial products are not bad in their own right

• But the wrong financial product can kill

Market structure

• Level playing field• Regulation by function• Suitability• Machine readable disclosures• OTC + Advisory market place• Seller Beware

Pre-fiduciary steps: 1. product structure

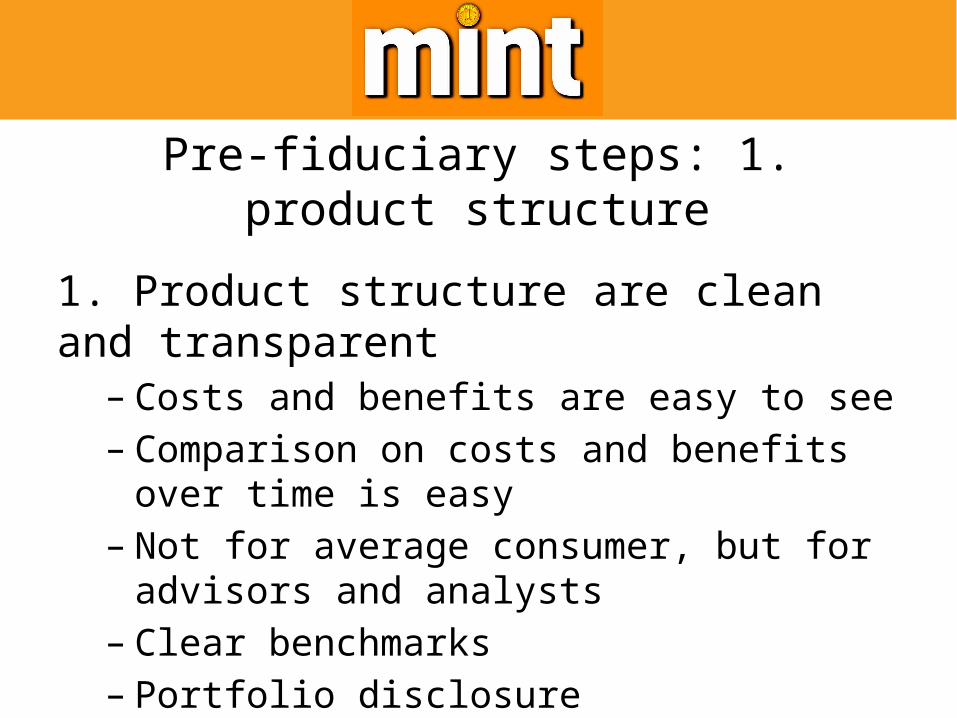

1. Product structure are clean and transparent– Costs and benefits are easy to see– Comparison on costs and benefits over time is

easy– Not for average consumer, but for advisors and

analysts– Clear benchmarks– Portfolio disclosure– Portability

Pre-fiduciary steps: 2. incentives

. Incentives. Align incentives across the investment chain– Producers and sellers “follow the money”– Use money to drive better behaviour– Fix incentives so that producers, seller and

consumers are incentivised towards ‘right’ choices– No loads, trail commissions, use of exit loads to

drive tenure, preference to fee income

Readings

• Richard Thaler: Nudge• David Kahneman: Thinking fast and slow• Dan Airely• Helaine Olen: Pound Foolish• FSLRC Report• Indian Financial Code

Consumer Protection

Issues across regulatorsMonika Halan

8 January 2015, Mumbai