Reg D Rule 506 Private Offerings: Verifying Accredited...

66

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Presenting a live 90-minute webinar with interactive Q&A Reg D Rule 506 Private Offerings: Verifying Accredited Investors and Identifying "Bad Actors" Navigating New SEC Report on Accredited Investor Definition, Exercising Bad Actor Due Diligence Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific WEDNESDAY, JUNE 22, 2016 Anthony J. Zeoli, Partner, Freeborn & Peters, Chicago Vanessa J. Schoenthaler, Partner, Sugar Felsenthal Grais & Hammer, New York James F. Verdonik, Attorney, Ward and Smith, Raleigh, N.C.

Transcript of Reg D Rule 506 Private Offerings: Verifying Accredited...

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Reg D Rule 506 Private Offerings: Verifying

Accredited Investors and Identifying "Bad Actors" Navigating New SEC Report on Accredited Investor Definition, Exercising Bad Actor Due Diligence

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JUNE 22, 2016

Anthony J. Zeoli, Partner, Freeborn & Peters, Chicago

Vanessa J. Schoenthaler, Partner, Sugar Felsenthal Grais & Hammer, New York

James F. Verdonik, Attorney, Ward and Smith, Raleigh, N.C.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-450-9970 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

REGULATION D RULE 506 PRIVATE OFFERINGS:

Webinar: Navigating New SEC Report on Accredited Investor Definition, Exercising Bad Actor Due Diligence

An Introduction to New Regulation D, Rule 506(c)

Introduction

• Anthony Zeoli

– Partner with the law firm of Freeborn & Peters LLP in Chicago

– Specialize in securities, commercial finance, real estate and general corporate law

– Industry recognized expert in crowdfunding

– Drafted the Illinois Crowdfunding Exemption Bill (Illinois House Bill 3420)

About Me

6

• Rule 506 is a “safe harbor used by privately held (i.e. non-publically traded) companies to sell securities in private offerings which are exempt from the registration requirements of the Securities Act (by virtue of the non-public offering exemption in Section 4(a)(2) of the Securities Act).

• Two types of Rule 506 Offerings – Rule 506(b) (the original) and Rule 506(c) (the new exemption)

Rule 506 - Introduction

7

• Private placements represent the largest source of funding for middle market companies today

– Reg. D Private Offerings represent an over $1.3 Trillion industry (2014)

– Rising trend in # and total amount of Reg. D Private Placements since the 90’s, particularly, within the last 4 years

Charts Taken From “Capital Raising in the U.S.: An Analysis of the Market for Unregistered Securities Offerings, 2009-2014; Division of Economic and Risk Analysis (2015)

Rule 506 - Introduction

8

• Of all Private Offerings, Rule 506 Offerings dominate by far (> 94% of total offerings & > 99% of total amounts raised)

Taken From “Capital Raising in the U.S.: An Analysis of the Market for Unregistered Securities Offerings, 2009-2014; Division of Economic and Risk Analysis (2015)

Rule 506 - Introduction

9

• In General:

– Unlimited Offering Amount;

– May be used by any company (Subject to enhanced “bad actor” disqualification provisions of Rule 506(d))

– May be offered and sold to “accredited investors” and up to 35 “non-accredited investors;”

– Company must verify whether offeree/purchasing investors are “accredited investors” or “non-accredited investors”;

– General advertising / solicitation is NOT permitted;

– Requires filing of Form D with the SEC and applicable State Blue Sky Notice Filings

Rule 506(b) - Rules

10

• Current Test (Section 501 of the Securities Act of 1933): – Earned annual income > $200 K (or $300 K

together with a spouse) in each of the prior (2) years, AND reasonably expects the same for the current year; OR

– net worth > $1 million, either alone or together with a spouse (excluding the value of the person’s primary residence)

• Time for Re-examination of current test: – Section 413(b)(2)(A) of the Dodd-Frank

Wall Street Reform and Consumer Protection Act requires the SEC to re-examine the definition of “accredited investor” every four (4) years

– SEC re-examining the current test; Sparking huge debate

Accredited Investors

11

• JOBS Act: – On March 27, 2012, Congress passed the Jumpstart Our Business Startups (JOBS) Act, a

bipartisan effort in both the House and the Senate to ease the regulatory burdens on smaller companies and facilitate capital formation. President Obama signed the legislation into law on April 5, 2012

• Main Provisions:

– Title I: Creates a transitional "on-ramp" for a new category of issuer, emerging growth companies (i.e. total annual gross revenues of < $1 billion), easing registration requirements in order to encourage them to pursue IPOs

– Title II: Allows for “crowdfunding” by (and public solicitation of) “accredited investors.”

– Title III: Allows for “crowdfunding” by (and public solicitation of) all investors (i.e. accredited and non-accredited)

– Title IV (Regulation A+): Modifying the existing “Regulation A” to provide for, among other things, an expansion of the exemption to cover offerings of securities up to $50 million (versus the previous $5 million) in any 12-month period

JOBS Act & Rule 506(c)

12

• Rule 506(b) and 506(c) are very similar.

• However, there are 3 main differences between Rule 506(b) and Rule 506(c):

– Manner of Offering & General Solicitation;

– Offeree & Investor Requirements / Limitations; and

– Investor Verification

Rule 506(b) Vs. Rule 506(c)

13

• Manner of Offering & General Solicitation:

Rule 506(b) Vs. Rule 506(c)

14

• Offeree & Investor Requirements / Limitations:

Rule 506(b) Vs. Rule 506(c)

15

• Investor Verification

Rule 506(b) Vs. Rule 506(c)

16

• Rule 506(b) is still the most popular, but use of Rule 506(c) is increasing significantly:

Taken From “Capital Raising in the U.S.: An Analysis of the Market for Unregistered Securities Offerings, 2009-2014; Division of Economic and Risk Analysis (2015)

Rule 506(b) Vs. Rule 506(c)

17

QUESTIONS?? Contact Info:

Anthony J. Zeoli, Esq. Freeborn & Peters LLP (312) 360-6798 [email protected] www.freeborn.com Blog: www.CrowdfundingLegalHub.com Twitter: @ajzeoli

18

© 2016 WARD AND SMITH, P.A.

James F. Verdonik Ward and Smith, P.A. P: 919.277.9100 F: 919.277.9177 E: [email protected]

Verifying Accredited Investors in SEC Rule 506 (c) Offerings

Overview

• Who are Accredited Investors?

• SEC Proposals to Change Accredited Investor Definition

• Difference between Traditional Rule 506 (b) Test and Rule 506 (c)'s Reasonable Steps Requirement

• Rule 506 (c) Safe Harbor for Individual Investors

• Verifying Outside the Safe Harbor

• Reasonable Steps to Verify Entities

• Integration Issues: Verification Issues when Switching from 506 (b) to 506 (c)

20

Whose Decision?

• Issuer

• Platform or Other Intermediary

• Future Investors

• Securities Regulators When File Form D

• Plaintiffs

21

What if are Wrong?

• Section 12 (a) (1) Liability for Violating Section 5 of 1933 Act because Have No Federal Exemption from Registration

• Cannot rely on Section 4 (a) (2) exemption if conduct a general solicitation

• Violate Section 12 (a) (2) of 1933 Act because fail to disclose that investors have rescission rights

• Violate state securities laws because state registration laws are not preempted

• Violate state disclosure requirements because fail to disclose rescission rights

• Liability is to all investors not just to the investors you fail to verify

• Liability for failing to disclose rescission rights from an earlier offering can cause cascading liability to investors in later offerings

22

Individual Accredited Investors

• Net Worth – Greater than $1 Million

• Residences – Only count primary residence and mortgage in determining net worth if the home is "underwater"

• What is Primary Residence vs Vacation Home or r4ental Property Affects Net Worth Calculation

• Income - $200,000 each of past 2 years and expect $200,000 in year investment is made

• Spouses – Can choose to include spouse in the net worth test or the income test, but the income test increases to $300,000 if include spouse's income in the income test

• Executive Officers, Directors and general partners are automatically accredited investors without regard to income or net worth

23

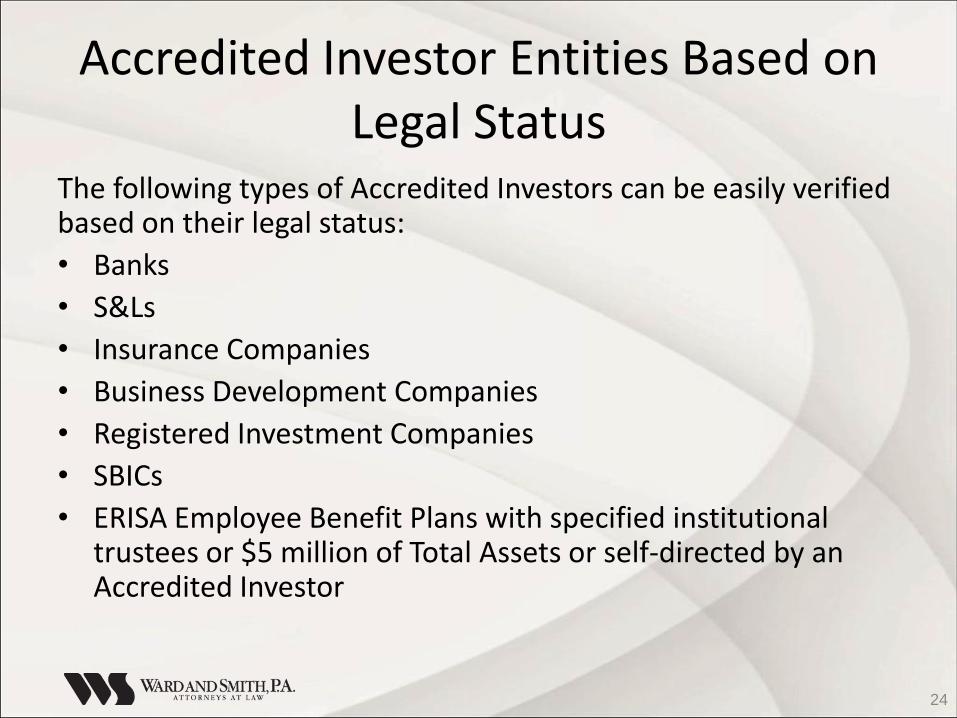

Accredited Investor Entities Based on Legal Status

The following types of Accredited Investors can be easily verified based on their legal status:

• Banks

• S&Ls

• Insurance Companies

• Business Development Companies

• Registered Investment Companies

• SBICs

• ERISA Employee Benefit Plans with specified institutional trustees or $5 million of Total Assets or self-directed by an Accredited Investor

24

Accredited Investor Entities Based on Other Criteria

The following Accredited Investors present verification issues beyond verifying their legal status:

• Entities not formed for the purpose of the investment and having more than $5 million of total assets: – Trusts if directed by a sophisticated person

– 501 (c) (3) non-profits

– Corporations and other entities

• Employee benefit plans with $5 million in assets

• Any entity all of whose owners are Accredited Investors

25

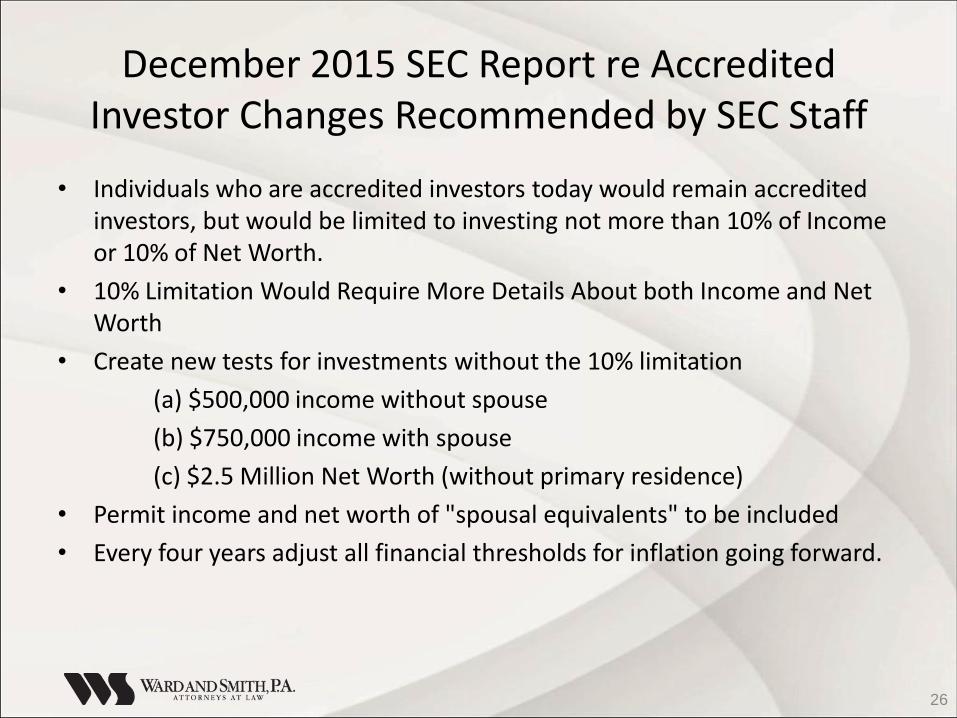

December 2015 SEC Report re Accredited Investor Changes Recommended by SEC Staff

• Individuals who are accredited investors today would remain accredited investors, but would be limited to investing not more than 10% of Income or 10% of Net Worth.

• 10% Limitation Would Require More Details About both Income and Net Worth

• Create new tests for investments without the 10% limitation

(a) $500,000 income without spouse

(b) $750,000 income with spouse

(c) $2.5 Million Net Worth (without primary residence)

• Permit income and net worth of "spousal equivalents" to be included

• Every four years adjust all financial thresholds for inflation going forward.

26

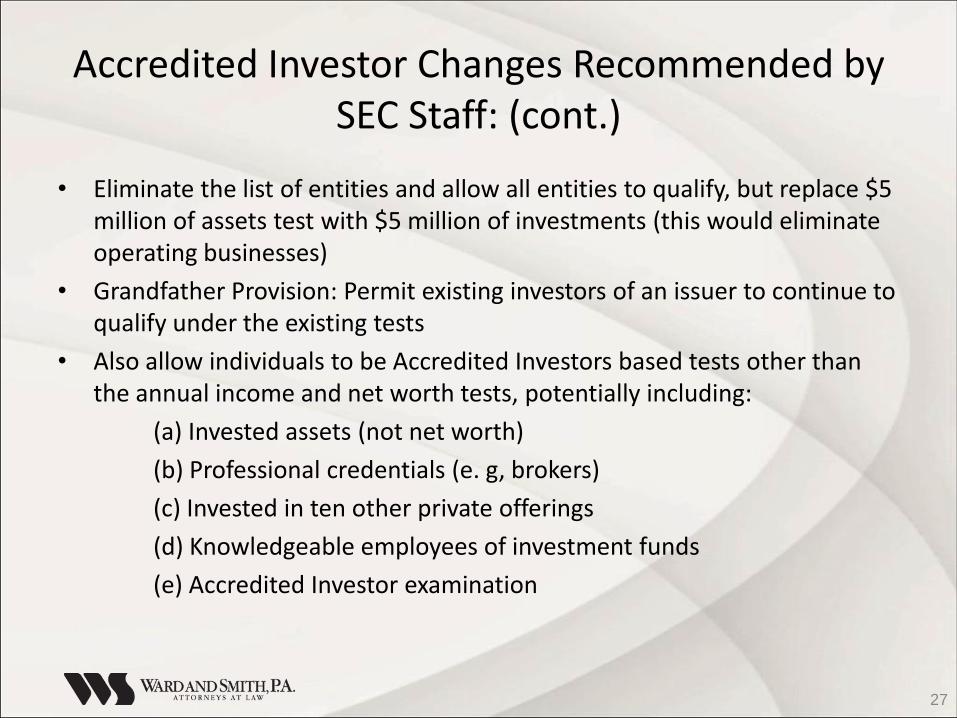

Accredited Investor Changes Recommended by SEC Staff: (cont.)

• Eliminate the list of entities and allow all entities to qualify, but replace $5 million of assets test with $5 million of investments (this would eliminate operating businesses)

• Grandfather Provision: Permit existing investors of an issuer to continue to qualify under the existing tests

• Also allow individuals to be Accredited Investors based tests other than the annual income and net worth tests, potentially including:

(a) Invested assets (not net worth)

(b) Professional credentials (e. g, brokers)

(c) Invested in ten other private offerings

(d) Knowledgeable employees of investment funds

(e) Accredited Investor examination

27

Increase in Numbers of Individual Accredited Investors

28

New Financial Thresholds for Individuals

29

Rule 506 (b) Test in Rule 501 (a):

• Is an Accredited Investor

• OR

• Issuer has Reasonable Belief is an Accredited Investor

30

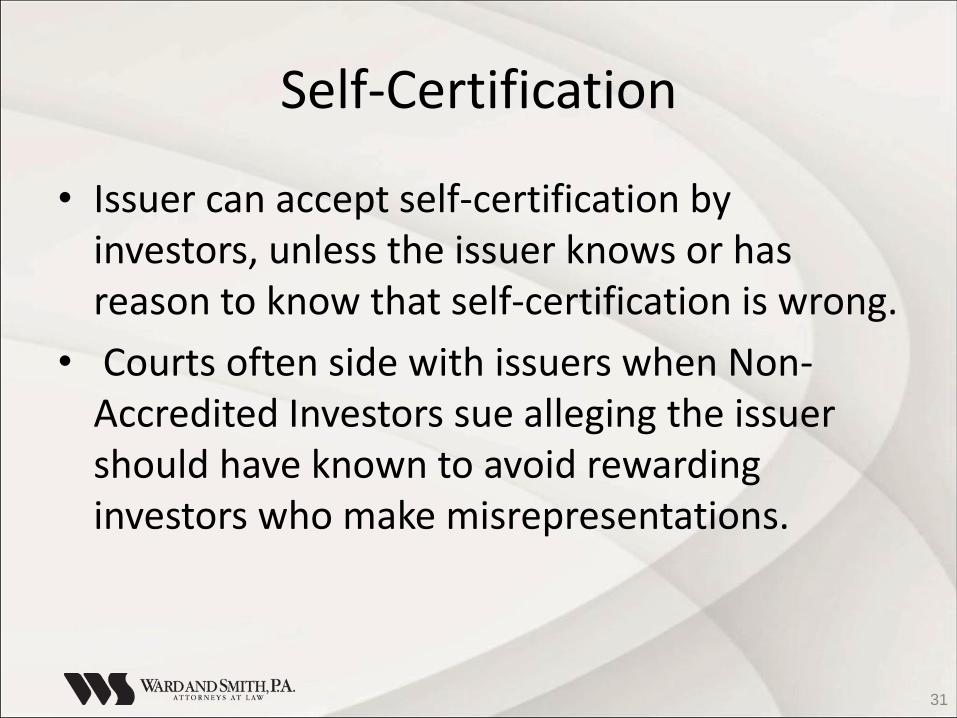

Self-Certification

• Issuer can accept self-certification by investors, unless the issuer knows or has reason to know that self-certification is wrong.

• Courts often side with issuers when Non-Accredited Investors sue alleging the issuer should have known to avoid rewarding investors who make misrepresentations.

31

Rule 506 (c) Test

Must satisfy 506 (b) Test

AND

Must take "reasonable steps" to verify Accredited Investor status.

Violate the rule even if the investor actually is accredited. Being lucky is not a defense.

32

Safe Harbor for Individual Investors

Relies on Reviewing Investor's Financial Documents:

• Income – non-exclusive list includes Form W-2, Form 1099, Schedule K-1 to Form 1065, and Form 1040 for two most recent years and representations about current year.

• Net Worth Documentation for Assets: bank statements, brokerage statements and other statements of securities holdings, certificates of deposit, tax assessments, and appraisal reports issued by independent third parties; and

• Net Worth Documentation for Liabilities: a consumer report from at least one of the nationwide consumer reporting agencies; and

• Written statement from investor that all liabilities have been disclosed.

33

Safe Harbor for Individuals (cont.)

• Timing: Must be dated within three months before the investment date

• Named Persons can provide written statements that they have taken reasonable steps to verify Accredited Investor status within the prior three months (Note This Is Broader than Reviewing Safe Harbor Documents):

– A registered broker-dealer

– A investment adviser registered with the SEC (not states)

– A licensed attorney in good standing in all jurisdictions where licensed

– A certified public accountant registered and in good standing under the laws of their residence or principal office

• Must have a reasonable basis to rely on others not named in the Safe Harbor.

• Platforms use Sub-Contractors for Verification

34

"Reasonable Steps" to Verify Outside the Safe Harbor

WHY? Is Most Important Question for Understanding Reasonable Steps.

"An issuer that solicits new investors through a website available to the general public, through a widely disseminated email or social media solicitation, or through print media, such as a newspaper, will likely be obligated to take greater measures to verify accredited investor status than an issuer that solicits new investors from a database of pre-screened accredited investors created and maintained by a reliable third party."

• 506 (b) Offerings:

– Issuer usually has contacts and knowledge of Investors other than the self-certification

OR

– Registered Broker or Other Intermediary has contacts and knowledge of Investors other than the self-certification

• In Rule 506(c) Offerings on Internet, often no one has information about investors other than the self-certification.

• There is no reasonable basis for believing self-certifications by Unknown Investors

35

Something More than Self Certification

• How much more is required is a facts and circumstances test.

• Examples in SEC Release No. 33-9415 (July 10, 2013)

– the nature of the purchaser and the type of accredited investor that the purchaser claims to be;

– the amount and type of information that the issuer has about the purchaser;

– the nature of the offering, such as the manner in which the purchaser was solicited to participate in the offering

– the terms of the offering, such as a minimum investment amount.

36

Interpreting Facts and Circumstances

• "After consideration of the facts and circumstances of the purchaser and of the transaction, the more likely it appears that a purchaser qualifies as an accredited investor, the fewer steps the issuer would have to take to verify accredited investor status, and vice versa." SEC Release No. 33-9415 (July 10, 2013)

• High Minimum Investment Amount

• Publicly available information about the investor, including in government filings (E. g proxy statement information)

• Knowledge of Prior Investment Transactions

• Issuers must prove they have an exemption. Create written record of the reasonable steps taken to verify Accredited Investor status and why the steps were reasonable.

37

SEC Action Against Platform

SEC Enforcement Against Eureeca Capital November 10, 2014:

• Offshore platform

• Accepted US Investors before Rue 506 (c) permitted general solicitation

• Accepted US Investors after Rule 506 (c) became effective without taking reasonable steps to verify Accredited investor status

• Failed to register as a broker in the US

38

Grandfather Provision of 506 (c) (2) (ii) (D)

• Investors who invested in a Rule 506 (b) offering before September 23, 2016 as Accredited Investors can self-certify continued Accredited investor status in later Rule 506 (c) offerings

• Based on premise that the early investor could be harmed if the issuer excludes the investor from a later capital-raising round and first refusal rights obligations of issuers

39

Angel Capital Association http://www.angelcapitalassociation.org/data/Established%20Angel

%20Group/EAG%20Tools/ACAEAGCertificationProgram09-14.pdf

Established Angel Group

"Certification criteria include six required criteria and three other recommended, but not required, factors."

40

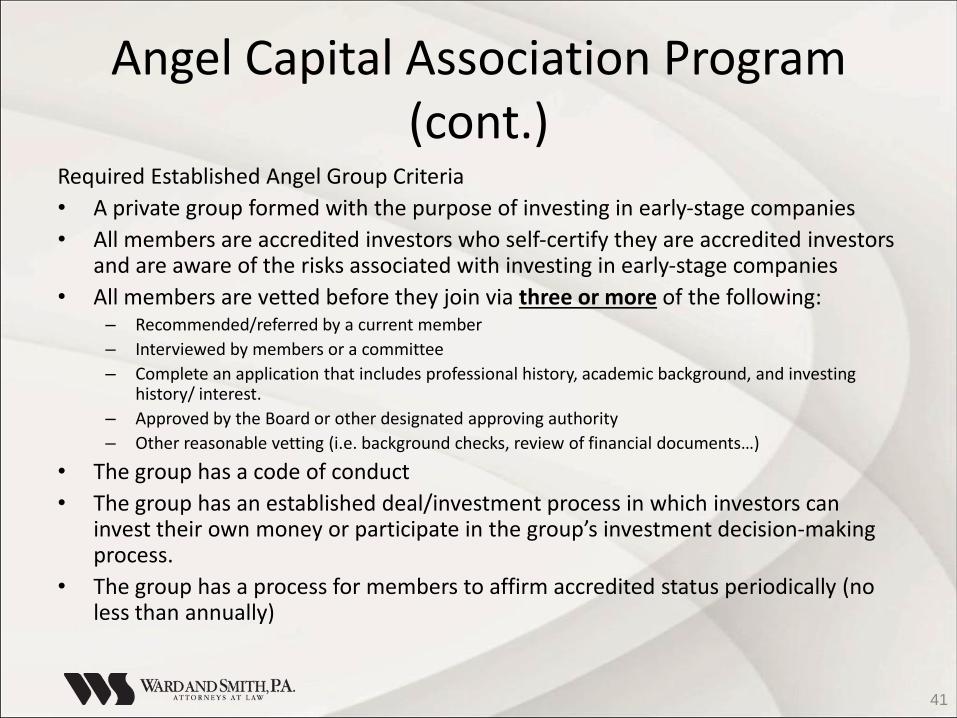

Angel Capital Association Program (cont.)

Required Established Angel Group Criteria

• A private group formed with the purpose of investing in early‐stage companies

• All members are accredited investors who self‐certify they are accredited investors and are aware of the risks associated with investing in early‐stage companies

• All members are vetted before they join via three or more of the following: – Recommended/referred by a current member

– Interviewed by members or a committee

– Complete an application that includes professional history, academic background, and investing history/ interest.

– Approved by the Board or other designated approving authority

– Other reasonable vetting (i.e. background checks, review of financial documents…)

• The group has a code of conduct

• The group has an established deal/investment process in which investors can invest their own money or participate in the group’s investment decision‐making process.

• The group has a process for members to affirm accredited status periodically (no less than annually)

41

Angel Capital Association Program (cont.)

Other Recommended Practices (not required) for Established Angel Group:

• The group convenes or participates in regular education sessions for members about facets of early stage investing

• At least one group member has invested in a Rule 506 deal in the past

• The organization or person is a member of a professional organization, such as ACA

Cannot be an EAG if pay fees for investment advice.

42

Angel Capital Association Program (cont.)

• Reasonable Steps to Verify Outside the Safe Harbor

• Facts and Circumstances Test Means Issuer Cannot Blindly Rely on A Certification

• Does the Issuer have a Reasonable Basis to Believe the Particular Angel Group is an Accredited Investor at the time of the investment?

• Timing: Is Annually Often Enough?

• Most Angel Groups Lack Staff to Check Members

43

Problem Verifying Other Entities

• Investment Funds and other entities with $5 Million or more in total assets not formed to invest in this offering

OR

• All owners are accredited investors

OR

• Operating businesses with $5 million of total assets

44

Investment Funds

• $5 million Total Assets Test means do not have to worry about liabilities

• All owners are Accredited Investors

• Does Fund Have Verification Procedures

• How Often Does the Fund Check

• Is It Reasonable to Rely on the Manager

45

Investment Funds (cont.)

• Determining Asset Value of Private Investments is Difficult

• Reliance on Valuations Used for Other Purposes Provides Comfort (E. g. Fund's Financial Statements)

• Timing of Valuation: Has Value Changed?

• How Should Issuer Value Earlier Round of Same Issuer?

• If formed for purpose of first round, does the Fund qualify for not being formed for the purpose of the second round?

46

Operating Businesses

• Vendors may contribute products and services.

• Less likely to have appraisal.

• Balance Sheet will not value Intellectual Property, Customers etc.

• Should you accept a value based on EBITDA or Revenue Multiple or other formula?

• Do these measures really reflect Asset Value?

• Who established value: CEO, Board of Directors or others?

• Timing: How recent?

47

Integrating Rule 506 (b) Offerings and Rule 506 (c) Offerings

• Rule 506 (b) and Rule 506 (c) offerings can be integrated

• If the Two Offerings are Integrated:

- General solicitation in the Rule 506 (c) offering destroys the Rule 506 (b) exemption

- Lack of "reasonable steps" to verify Accredited Investor status in the Rule 506 (b) offering destroys the Rule 506 (c) exemption

48

CDI Question 260.12

• Question: If an issuer commenced an offering in reliance on Rule 506(b), may the issuer determine, prior to any sales of securities in the offering, to rely on Rule 506(c) for the offering?

• Answer: Yes, as long as the conditions of Rule 506(c) are satisfied with respect to all sales of securities in the offering. To the extent the issuer already filed a Form D indicating its reliance on Rule 506(b), it must amend the Form D to indicate its reliance on Rule 506(c) instead, as that decision represents a change in the information provided in the previously-filed Form D. [Nov. 13, 2013]

• Timing Issue: If you sell securities in the Rule 506 (b) offering, can you verify Accredited Investor status after the investment is made in the Rule 506 (b) offering and before you start the Rule 506 (c) offering?

49

Integrating 506 (b) Offerings and 506 (c) Offerings (cont.)

• Rule 502 (a)'s 6 months "safe harbor" six months applies.

• If safe harbor does not apply, consider the follow factors:

– Whether the sales are part of a single plan of financing;

– Whether the sales involve issuance of the same class of securities;

– Whether the sales have been made at or about the same time;

– Whether the same type of consideration is being received; and

– Whether the sales are made for the same general purpose.

• Rule 155 for public and private offerings has a more sensible thirty-day safe harbor.

50

Integrating 506 (b) Offerings and 506 (c) Offerings (cont.)

• Checking the type of offering box on Form D alerts the SEC and the states you switched offering exemptions

• Preserve ability to switch by verifying Accredited Investor status in the Rule 506 (b) offering

• Easier if Hold One Closing and Know Will Need to Switch

• Requirement for More than Self-Certification by Clicking on an Internet Platform is just an Extension of Rule 506 (b)'s Reasonable Basis Standard.

• If Have Personal Contact with Rule 506 (b) Offering Investors, Reasonable Steps Test is Easier to Satisfy than if Only Sell Through Platform

51

Integration with Other Types of Offerings

• Section 4 (a) (2), Rule 504 and Rule 505 Have Same Issues as in Switching from Rule 506 (b) to Rule 506 (c)

• Regulation A offerings will not be integrated with: – Any prior offers or sales

– Later registered offers or sales

– Later Rule 701 employee offerings or foreign offerings

• Regulation Crowdfunding offerings will not be integrated with any other offering (including a concurrent offering provided each offering meets the exemption criteria for that offering).

52

www.wardandsmith.com 800.998.1102

ASHEVILLE GREENVILLE NEW BERN RALEIGH WILMINGTON

© 2016 WARD AND SMITH, P.A. 53

“BAD ACTOR” PROVISIONS

Vanessa J. Schoenthaler

Sugar Felsenthal Grais & Hammer LLP

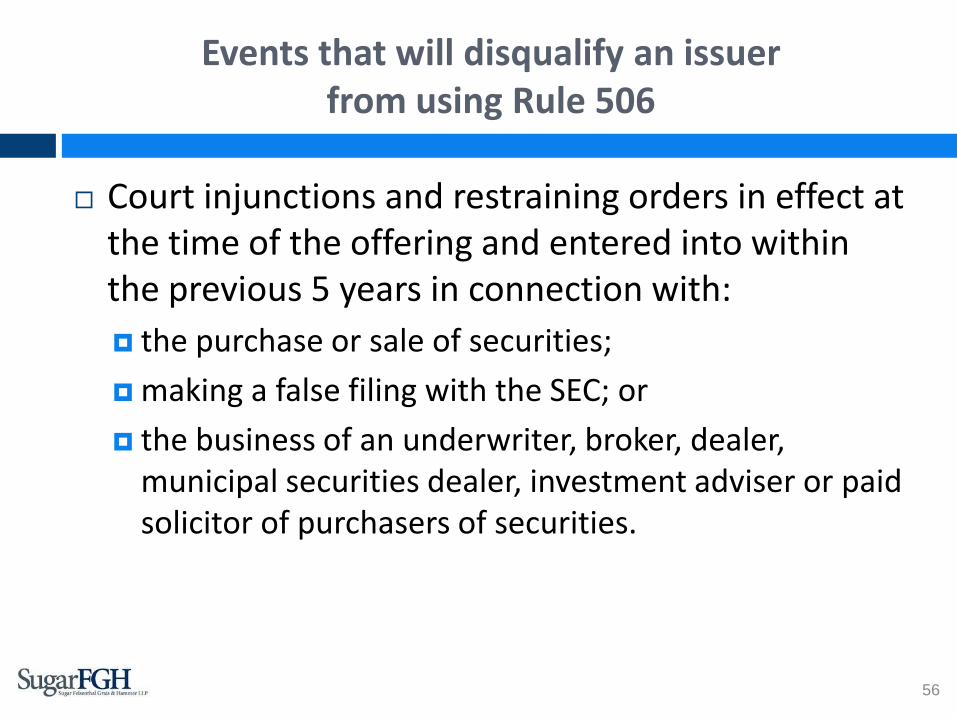

Events that will disqualify an issuer from using Rule 506

Certain criminal convictions (occurring within 10 years of the offering, or 5 years in the case of the company, or a predecessor or affiliated company) in connection with:

the purchase or sale of securities;

making a false filing with the SEC; or

the business of an underwriter, broker, dealer, municipal securities dealer, investment adviser or paid solicitor of purchasers of securities.

55

Events that will disqualify an issuer from using Rule 506

Court injunctions and restraining orders in effect at the time of the offering and entered into within the previous 5 years in connection with:

the purchase or sale of securities;

making a false filing with the SEC; or

the business of an underwriter, broker, dealer, municipal securities dealer, investment adviser or paid solicitor of purchasers of securities.

56

Events that will disqualify an issuer from using Rule 506

Final orders of certain federal and state regulators of securities, insurance, banking, savings associations or credit unions; federal banking agencies; the CFTC and the NCUA that: bar the covered person from associating with a

regulated entity, engaging in the business of securities, insurance or banking, or engaging in savings association or credit union activities; or

are based on fraudulent, manipulative, or deceptive conduct and were issued within 10 years of the offering.

57

Events that will disqualify an issuer from using Rule 506

SEC disciplinary orders relating to brokers, dealers, municipal securities dealers, investment companies, and investment advisers and their associated persons under Section 15(b) or 15B(c) of the Securities Exchange Act, or Section 203(e) or (f) of the Investment Advisers Act that: suspend or revoke the person’s registration as a broker,

dealer, municipal securities dealer or investment adviser; place limitations on the person’s activities, functions or

operations; or bar the person from being associated with any entity or

from participating in the offering of any penny stock

58

Events that will disqualify an issuer from using Rule 506

Certain SEC cease and desist orders from violations and future violations of:

scienter-based anti-fraud provisions of the federal securities laws, including, without limitation:

Section 17(a)(1) of the Securities Act;

Section 10(b) of the Securities Exchange Act and Rule 10b-5;

Section 15(c)(1) of the Securities Exchange Act; and

Section 206(1) of the Investment Advisers Act; or

Section 5 of the Securities Act

59

Events that will disqualify an issuer from using Rule 506

Suspension or expulsion from self-regulatory organization membership or association with a self-regulatory organization member for any act or omission constituting conduct inconsistent with just and equitable principles of trade.

Refusal orders, stop orders or order suspending a registration statement or Regulation A offering statement filed by a covered person within the previous 5 years (or the subject of a pending proceeding to determine whether such an order should be issued).

USPS false representation orders

60

Effect of previous disqualifying events

Bad actor disqualification will not arise as a result of disqualifying events that occurred prior to the September 23, 2013 effective date of the rule amendments.

However, matters that existed prior to September 23, 2013 that would otherwise give rise to disqualification must be disclosed to investors in writing.

Disclosure must be furnished at a reasonable time prior to the sale.

Failure to make the required disclosure will render Rule 506 unavailable, unless the issuer can demonstrate that it did not know and, in the exercise of reasonable care, could not have known that a disqualifying event was required to be disclosed.

61

How issuers are exercising reasonable care in complying with the bad actor provisions

Issuer should consider conducting additional due diligence to satisfy reasonable care requirements, such as: reviewing public databases; or

running background checks.

Issuers seeking to reasonably rely on representations by covered persons should consider: revising D&O questionnaires;

requiring placement agent questionnaires or additional representations and covenants in engagement agreements;

requiring other offering participants that may be covered persons to complete a questionnaire or provide a certification; or

implementing bylaw requirements obligating disclosure.

If an offering is continuous, delayed or long-lived, the issuer must update its factual inquiry periodically through bring-down of representations, questionnaires and certifications, negative consent letters, periodic re-checking of databases, and other steps, depending on the facts and circumstances.

62

The waiver process, and selected examples of waivers

The SEC may waive bad actor disqualifications upon a showing of good cause that the disqualification is not necessary under the circumstances.

Waiver requests must be submitted in writing and manually signed and must: discuss the background of the matter, including facts

and legal issues involved;

suggest grounds for granting the waiver; and

show good cause that disqualification is not necessary under the circumstances.

63

The waiver process, and selected examples of waivers

Factors relevant to the SEC’s granting of a waiver request may include, among others: the nature of the violation or conviction and whether it involved the

offer and sale of securities;

whether the conduct involved a criminal conviction or scienter based violation, as opposed to a civil or administrative non-scienter based violation;

who was responsible for the misconduct;

how long did the misconduct go on for;

remedial action taken; and

the impact of denying the waiver.

Granted waivers are publicly available on the SEC’s website (https://www.sec.gov/divisions/corpfin/cf-noaction.shtml#3b), although confidential treatment of information contained in a waiver may be requested.

64

Curing the bad actor disqualification

Seek a waiver, pursuant to the SEC’s waiver process;

Terminate the relationship the bad actor. If the bad actor is a placement agent, the engagement

should be terminated and the bad actor should not receive payment for future sales.

If the bad actor disqualification only affects control persons of the placement agent, such persons should be terminated or removed from any roles with respect to the placement agent that would cause them to be covered persons.

In addition, provide disclosure and take other remedial steps to address the disqualification.

65

Thank You

Vanessa J. Schoenthaler

Sugar Felsenthal Grais & Hammer LLP

230 Park Avenue

Suite 460

New York, NY 10169

www.sugarfgh.com

66