Reference Case - Ascension Publishing · Richard Newell, SAIS, December 14, 2009. 1. ... Richard...

24

The Paul H. Nitze School of Advanced International Studies December 14, 2009 Washington, DC Richard Newell, Administrator Annual Energy Outlook 2010 Reference Case

Transcript of Reference Case - Ascension Publishing · Richard Newell, SAIS, December 14, 2009. 1. ... Richard...

Richard Newell, SAIS, December 14, 2009 1

The Paul H. Nitze School of Advanced International Studies December 14, 2009

Washington, DC

Richard Newell, Administrator

Annual Energy Outlook 2010Reference Case

Richard Newell, SAIS, December 14, 2009 2

• Generally assumes current laws and regulations– provisions sunset if specified (e.g., renewable tax credits expire) – excludes potential future laws and regulations (e.g., proposed

greenhouse gas legislation is not included)– some grey areas

• adopts proposed regulations that are not yet final, in order to inform the likely implementation of a statute

• adds a premium to the capital cost of CO2 -intensive technologies to reflect market behavior regarding possible CO2 regulation

• assumes implementation of existing regulations that enable building new energy infrastructure and resource extraction

• Includes technologies that are commercial or reasonably expected to become commercial in the next decade or so– includes cost and efficiency improvements from learning, but not

revolutionary or breakthrough technologies

How does the AEO2010 reference case handle public policy and technology?

Richard Newell, SAIS, December 14, 2009 3

• Extended projection period to 2035• Changes in Federal and State laws and regulations

– revised handling of fuel economy standards to reflect the proposal for light-duty vehicles in model years 2012-2016

– assumes permission will be granted to extend nuclear power unit operating licenses beyond 60 years; no retirements through 2035

• Revised capital costs for capital-intensive projects– overnight costs for nuclear and coal power up 10-20%

• Changes to assumptions about oil and gas resource base– updated characterization of natural gas shales, reflecting evolution

of shale gas resources and technology– new lower-48 onshore oil and gas supply submodule

Key updates included in the AEO2010 reference case

Richard Newell, SAIS, December 14, 2009 4

0

25

50

75

100

125

150

175

200

225

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

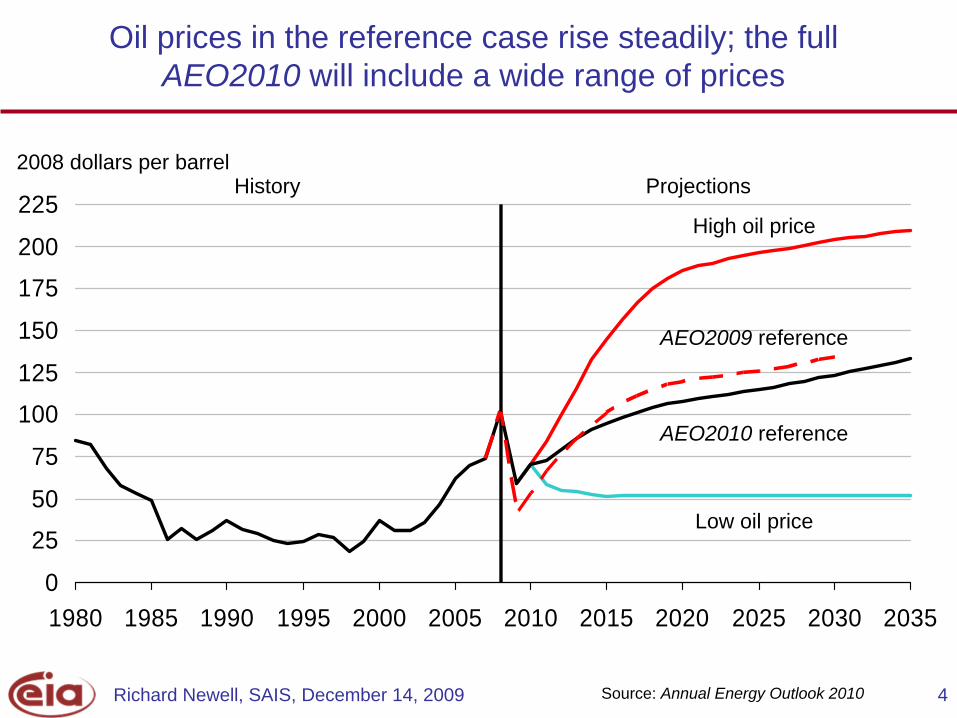

Oil prices in the reference case rise steadily; the full AEO2010 will include a wide range of prices

2008 dollars per barrel

Source: Annual Energy Outlook 2010

High oil price

Low oil price

AEO2010 reference

ProjectionsHistory

AEO2009 reference

Richard Newell, SAIS, December 14, 2009 5

0

1

2

3

4

5

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Oil to natural gas price ratio remains high over the projection

ProjectionsHistory

0

5

10

15

20

25

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Oil and natural gas prices

Source: Annual Energy Outlook 2010

Crude oil

U.S. natural gas wellhead

Ratio of oil price to natural gas price 2008 dollars per million Btu

Richard Newell, SAIS, December 14, 2009 6

0

20

40

60

80

100

120

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

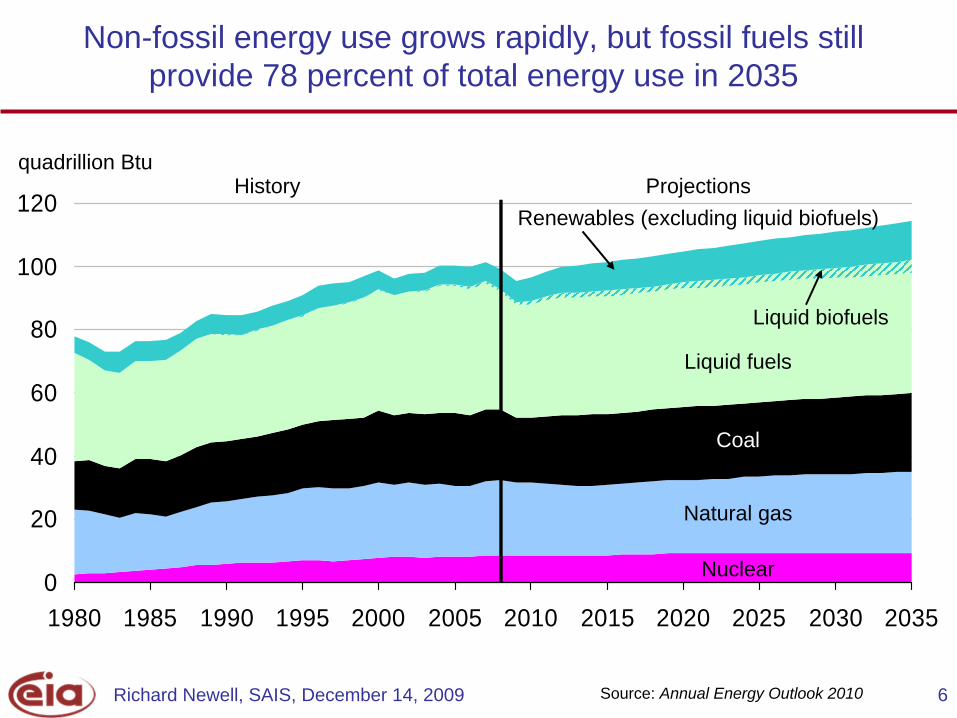

Non-fossil energy use grows rapidly, but fossil fuels still provide 78 percent of total energy use in 2035

quadrillion Btu

Coal

Liquid fuels

Natural gas

ProjectionsHistory

Nuclear

Liquid biofuels

Renewables (excluding liquid biofuels)

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 7

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Energy and CO2 per dollar GDP continue to decline; per capita energy use also declines

index, 2005=1

Energy per capita

Energy per dollar GDP

ProjectionsHistory

CO2 per dollar GDP

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 8

0

50

100

150

200

2005 2010 2015 2020 2025 2030 2035

Energy efficiency gains reduce consumption 15% from where it would otherwise be; structural change is even larger

Constant efficiency

Constant intensity

Efficiency change

Structural change

AEO2010 reference case

192

133

115

quadrillion Btu

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 9

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

U.S. reliance on imported liquid fuels is reduced by increased domestic production and greater fuel efficiency

million barrels per day

Consumption

Production

Net imports

ProjectionsHistory

AEO2010 reference caseUpdated AEO2009 reference case

40% 45%

57%60%

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 10

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Biofuels meet most of the growth in liquid fuels supply

million barrels per dayProjectionsHistory

Natural gas plant liquids

Biofuels including imports

Petroleum supply

Net petroleum imports

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 11

billion gallon-equivalents

0

5

10

15

20

25

30

35

40

45

2008 2022 2022 inAEO2009

2035

Biofuels grow, but fall short of the 36 billion gallon RFS target in 2022, exceed it in 2035

Legislated RFS in 2022

RFS with adjustments under CAA Sec.211(o)(7) Biodiesel

Other feedstocks

Biomass-to- liquids

Net ethanol imports

Cellulosic ethanol

Corn ethanol

Renewable diesel

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 12

0

5

10

15

20

25

30

35

40

45

2000 2005 2010 2015 2020 2025 2030 2035

HistoryAEO2010Updated

New light duty vehicle efficiency reaches 40 mpg by 2035

miles per gallon

AEO2009 reference case

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 13

millions

0123456789

10

2000 2008 2015 2020 2025 2030 2035

Electric/fuel cellPlug-in hybrid electricHybrid electricMild hybrid electricGaseousFlex fuelDiesel

Mild and full hybrid systems dominate new light-duty vehicle sales by 2035

ProjectionsHistory

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 14

0

2

4

6

8

10

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

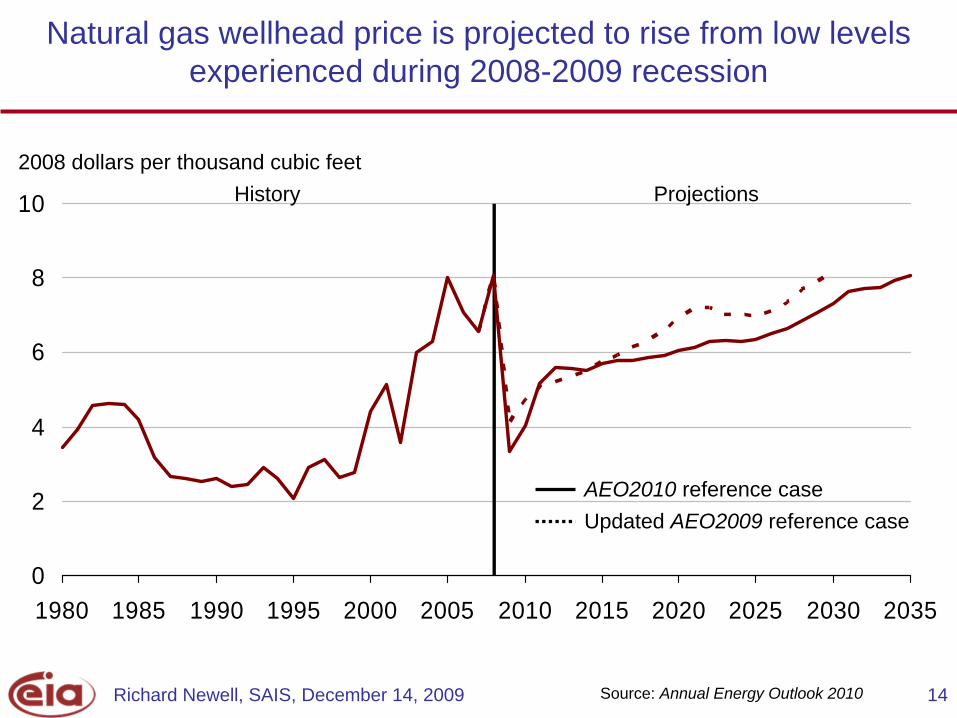

Natural gas wellhead price is projected to rise from low levels experienced during 2008-2009 recession

2008 dollars per thousand cubic feetProjectionsHistory

AEO2010 reference caseUpdated AEO2009 reference case

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 15

10

15

20

25

30

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Import share of natural gas supply declines as domestic supply grows

trillion cubic feet

Consumption

Domestic supply

Net imports

ProjectionsHistory

AEO2010 reference caseUpdated AEO2009 reference case

2%6%

13%

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 16

Shale gas has been the primary source of recent growth in U.S. technically recoverable natural gas resources

0

250

500

750

1000

1250

1500

1750

2000

2250

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

AEO edition

Source: U.S. Geological Service, Mineral Management Service, private data, and EIA.

trillion cubic feet

Unproved shale gas &other unconventional

Unproved conventional(including Alaska*)

Proved reserves(all types & locations)

* Alaska resource estimates prior to AEO2009 reflect resources from the North Slope that were not included in previously published documentation.

Richard Newell, SAIS, December 14, 2009 17

0

5

10

15

20

25

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

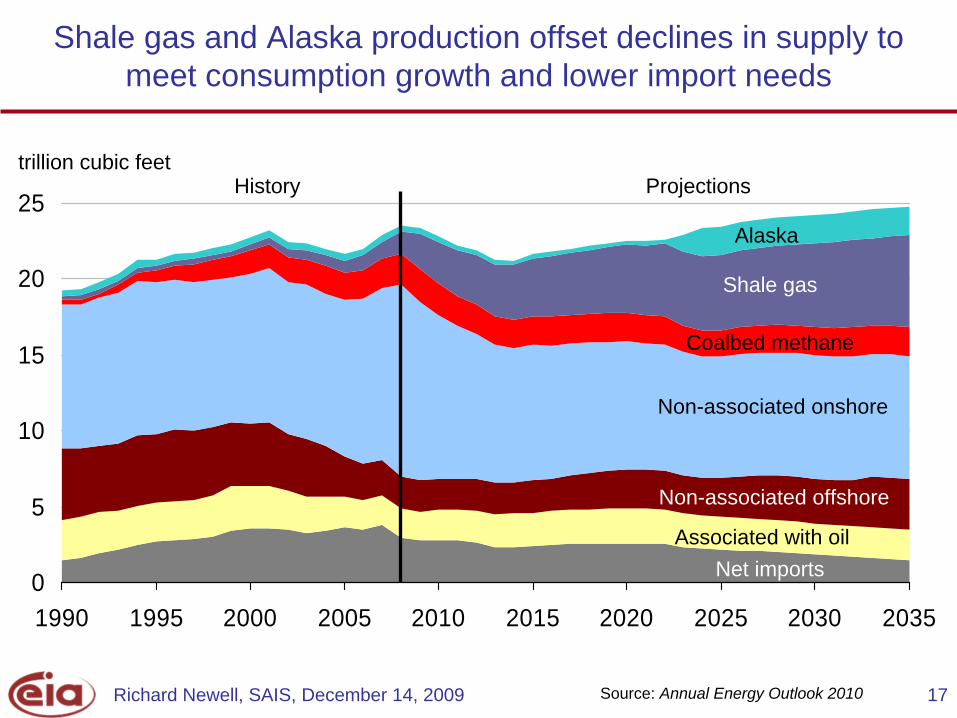

Shale gas and Alaska production offset declines in supply to meet consumption growth and lower import needs

trillion cubic feet

Alaska

Non-associated offshore

ProjectionsHistory

Associated with oil

Coalbed methane

Net imports

Non-associated onshore

Shale gas

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 18

-2

0

2

4

6

8

10

12

14

1950 1960 1970 1980 1990 2000 2010 2020 2030

Growth in electricity use continues to slow

3-year rolling average percent growth

Projections

HistoryPeriod Annual Growth1950s 9.81960s 7.31970s 4.71980s 2.91990s 2.42000-2008 0.92008-2035 1.0

Structural Change in Economy - Higher prices - Standards - Improved efficiency

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 19

Natural gas and renewables account for the majority of capacity additions from 2008 to 2035

Coal312 (31%)

Natural gas338 (33%)

Hydropower*99 (10%)

Nuclear101 (10%)

Other renewables

40 (4%)

Other119 (12%)

* Includes pumped storage

Coal31 (12%)

Natural gas116 (46%)

Hydropower*1 (0.4%)

Nuclear8 (3%)

Other renewables92 (37%)

Other2 (1%)

2008 capacity Capacity additions 2008 to 2035

1,008gigawatts

250gigawatts

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 20

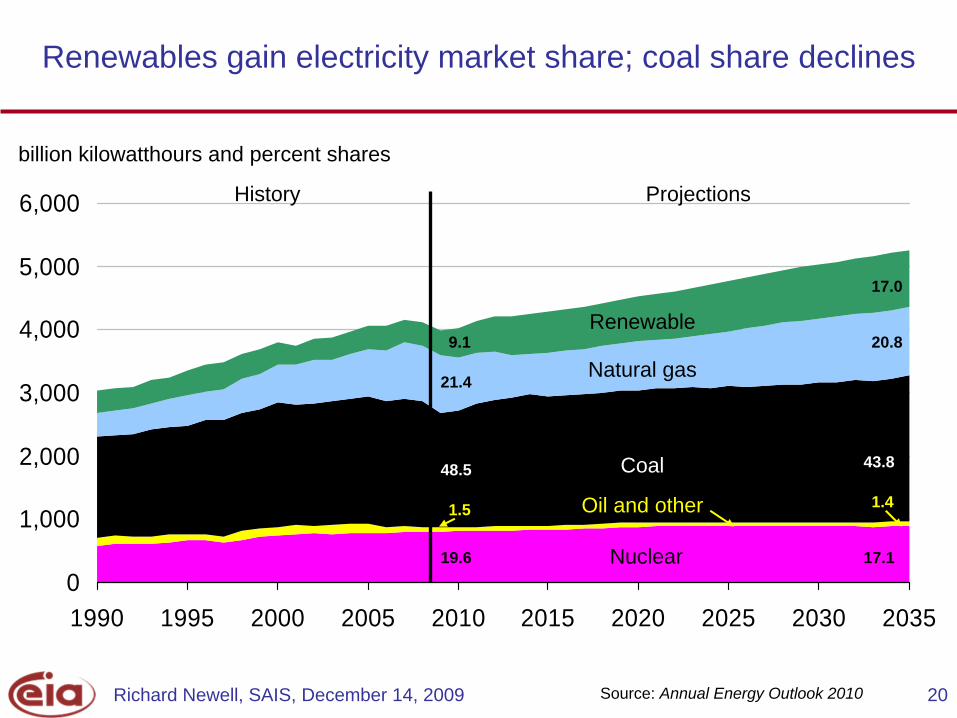

Renewables gain electricity market share; coal share declines

0

1,000

2,000

3,000

4,000

5,000

6,000

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

billion kilowatthours and percent shares

Natural gas

Renewable

ProjectionsHistory

Nuclear

Oil and other

Coal48.5 43.8

21.4

20.8

19.6 17.1

9.1

17.0

1.41.5

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 21

0

100

200

300

400

500

600

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

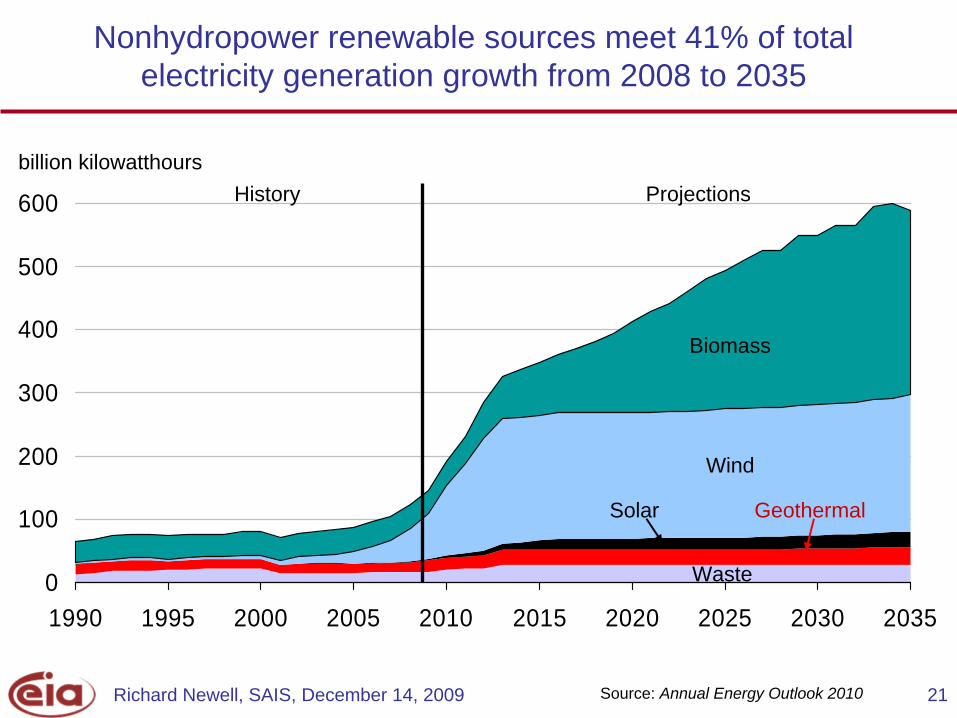

Nonhydropower renewable sources meet 41% of total electricity generation growth from 2008 to 2035

billion kilowatthours

Wind

ProjectionsHistory

Solar

Biomass

Geothermal

Waste

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 22

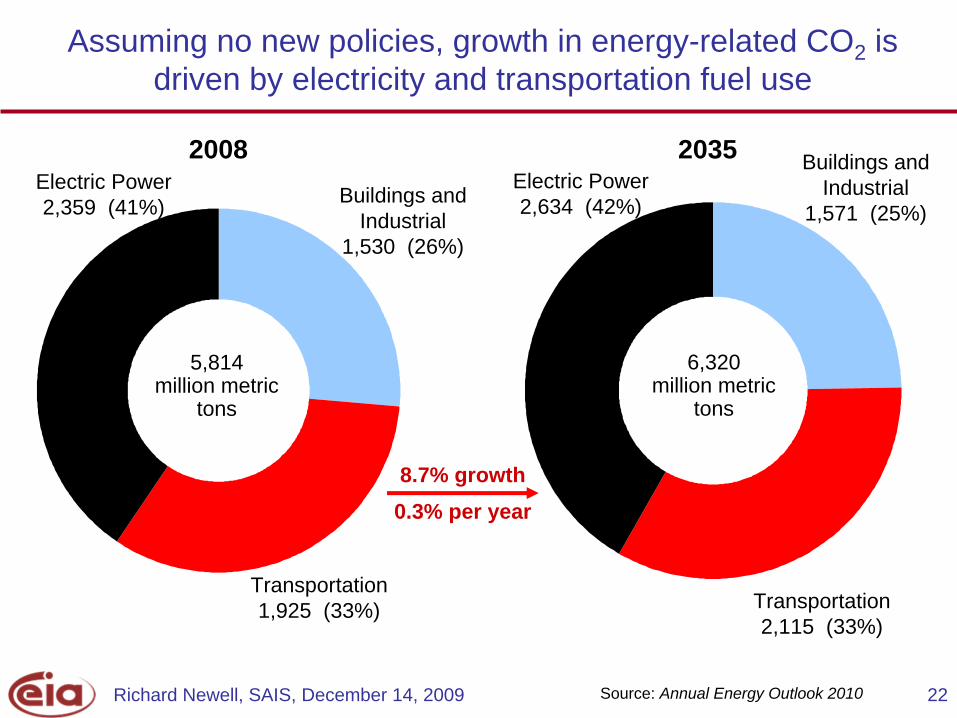

0.3% per year8.7% growth

Assuming no new policies, growth in energy-related CO2 is driven by electricity and transportation fuel use

Transportation1,925 (33%)

Buildings and Industrial

1,530 (26%)

Electric Power2,359 (41%)

2008

5,814million metric

tons

2035

6,320million metric

tons

Transportation2,115 (33%)

Buildings and Industrial

1,571 (25%)Electric Power2,634 (42%)

Source: Annual Energy Outlook 2010

Richard Newell, SAIS, December 14, 2009 23

• Recent Federal and State policies, and rising energy prices, moderate growth in energy consumption and shift it to renewable fuels

• U.S. oil use remains near its present level through 2035– growth in overall liquids demand is met by biofuels, and ethanol

accounts for >17% of gasoline consumption by 2035

– U.S. reliance on imported oil as a share of U.S. liquids use, declines to 45% over the next 25 years

• Shale gas provides the majority of growth in gas supply

• Energy-related CO2 emissions grow 0.3% per year, absent any new policies to limit emissions

Key results from the AEO2010 reference case

Richard Newell, SAIS, December 14, 2009 24

For more information

U.S. Energy Information Administration home page www.eia.gov

Short-Term Energy Outlook www.eia.gov/emeu/steo/pub/contents.html

Annual Energy Outlook www.eia.gov/oiaf/aeo/index.html

International Energy Outlook www.eia.gov/oiaf/ieo/index.html

Monthly Energy Review www.eia.gov/emeu/mer/contents.html

U.S. Energy Information Administrationwww.eia.gov