REDACTED VERSION Shipping Conferences: A...

40

REDACTED VERSION Shipping Conferences: A Study of the Impact of FEFC Activity on Prices in the North Europe-Asia Trade By Nils von Hinten-Reed 1 , Tasneem Chipty 2 , and Fiona Scott Morton 3 Charles River Associates June 4, 2004 1 Principal, Charles River Associates 2 Principal, Charles River Associates 3 Professor of Economics, Yale School of Management

Transcript of REDACTED VERSION Shipping Conferences: A...

REDACTED VERSION

Shipping Conferences: A Study of the Impact of FEFC Activity on

Prices in the North Europe-Asia Trade

By Nils von Hinten-Reed1, Tasneem Chipty2, and Fiona Scott Morton3

Charles River Associates

June 4, 2004

1 Principal, Charles River Associates 2 Principal, Charles River Associates 3 Professor of Economics, Yale School of Management

TABLE OF CONTENTS

I. Introduction and Summary of Opinions ........................................................... 1

II. Industry Background ......................................................................................... 3

III. The Economic Principles of Coordinated Behavior ........................................ 7

A. Coordination to Avoid Competition ....................................................... 8 B. Conference versus Non-Conference Members..................................... 9 C. Ability of the FEFC Members to Sustain Collusion ............................. 10

IV. Empirical Framework ....................................................................................... 11

V. Data used for Analysis..................................................................................... 14

A. FEFC Membership.............................................................................. 15 B. FEFC Rate Announcements ............................................................... 16 C. FEFC Capacity Share......................................................................... 17 D. Aggregate Demand............................................................................. 17 E. Exchange Rates ................................................................................. 18 F. Aggregate Capacity ............................................................................ 19 G. Singapore Diesel Spot Price ............................................................... 19

VI. Regression Analysis of Price Levels .............................................................. 19

A. Base Specification, 2000-2003 Sample .............................................. 19 B. Extensions of the Base Specification.................................................. 22 C. 2003 Only Sample .............................................................................. 25 D. First Difference Model......................................................................... 26

VII. Conclusions...................................................................................................... 27

i

I. INTRODUCTION AND SUMMARY OF OPINIONS

1. As part of the on-going DG Competition review of Regulation 4056/86 and the

Article 3 exemption of shipping conferences, we have been asked by outside counsel

for the European Liner Affairs Association (“ELAA”) to study the effect of shipping

conferences on shipping rates in the North Europe-Asia trade. Our goal has been to

study the effects of the Far East Freight Conference (“FEFC”), the conference that

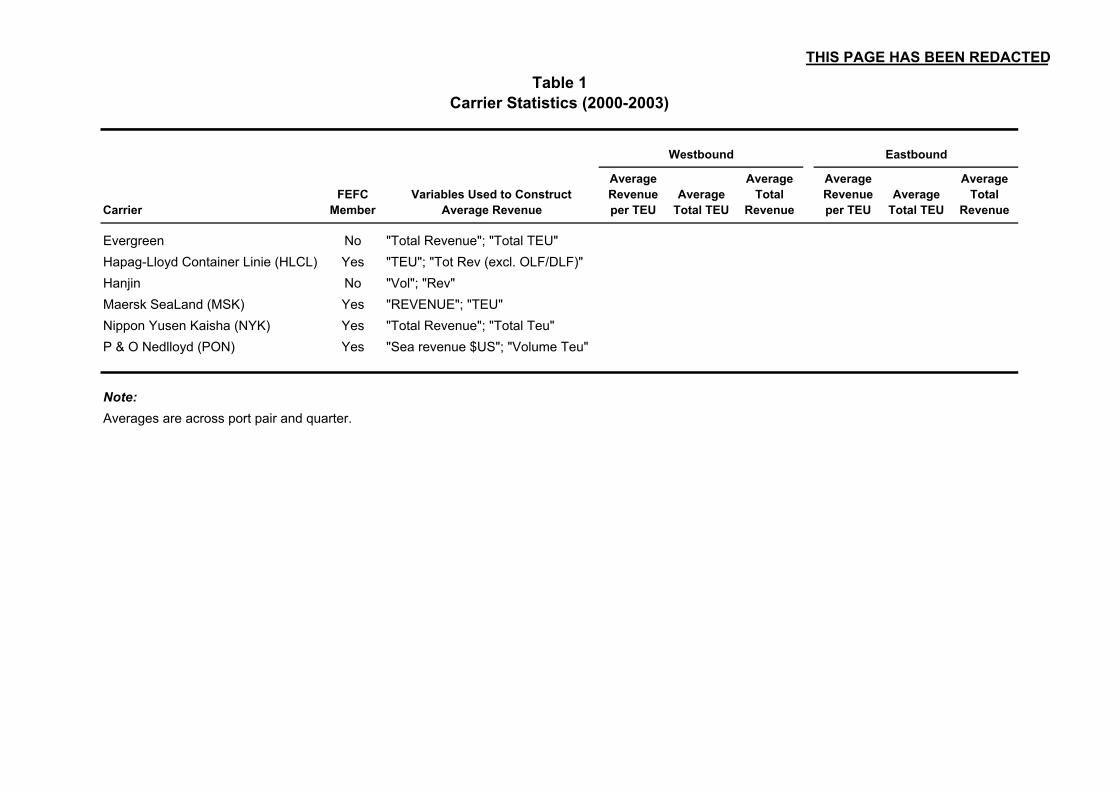

governs the North Europe-Asia trade, on price levels and price volatility. To this end,

we provide a conceptual framework to evaluate the ability of the FEFC to monitor and

enforce an agreement amongst member carriers to raise price above competitive

levels. We also undertake an empirical analysis of the effect of FEFC activity on

price, using historical data.

2. The North Europe-Asia trade is currently served by 23 carriers, 15 of which belong to

the FEFC and control about 60 percent of the available capacity.1 The central

question is whether the FEFC has market power – that is, the ability to raise price

above competitive levels. An important determinant of market power is conference

presence, measured as market share. Unfortunately, these data were unavailable, and

as such, we were unable to collect information on conference market shares by route

over time. Thus, the scope of our empirical analysis is necessarily limited. Given

data availability, we have examined the effects of conference membership and rate

1

1 FEFC members are ANL Container Lines, APL Co Pte Ltd., CMA CGM SA, Egyptian International

Shipping Co., Hapag Lloyd Container Linie GmbH, Hyundai Merchant Marine Co. Ltd., Kawasaki Kisen Kaisha Ltd, A.P. Moller - Maersk SeaLand, Malaysia International Shipping Corporation Berhad, Mitsui O.S.K. Lines Ltd., Nippon Yusen Kaisha, Norasia Container Lines Ltd., Orient Overseas Container Line, P & O Nedlloyd Ltd, and Yangming Transport Corporation.

announcements on price levels. We have also examined the extent to which

conference rate announcements mirror expectations about market conditions.

3. Our principal findings thus far are that FEFC members earn higher revenues per TEU

than non-conference members. We expect that this difference is due in part to

differences in quality of services such as convenient inland transportation and

loading/unloading of cargo.2 This difference may also be due in part to differences in

shipper characteristics, across conference and non-conference carriers.3 In addition,

we find that conference rate announcements contain information about market

fundamentals. Specifically, in our study of westbound cargo movements, rate

announcements appear to be highly correlated with measures of aggregate demand

and fuel prices. Given data limitations, we are unable to estimate the effect of FEFC

market share on price levels, nor are we able to determine the effect of conference

activity on price volatility.

4. Our study of documents and materials relevant to this matter is ongoing. Among the

materials we have reviewed are various issues of “The Drewry Container Market

Quarterly;” materials available on the FEFC website; and various documents provided

2 According to a recent survey conducted by Capital Consulting & Management, Inc. (“CMMI”), Maersk,

APL, and the NYK Line, all three of which are conference carriers, were identified by shippers as “leaders in Trans-Pacific ocean carrier quality.” These shippers described “network and delivery as the most critical performance factors, followed by price….” See CMMI, “Maersk, APL, and NYK Line Are Leaders in Trans-Pacific Ocean Carrier Quality; Pioneering CMMI Survey Uncovers What Quality Means to Shippers, Forwarders,” www.ccmiservices.com, May 26, 2004, p. 1.

3 In addition to quality differences, there may also be different compositions of demand served by FEFC conference and non-conference members. We understand that within containerized cargo, conference carriers handle more cargo controlled by European importers who typically negotiate carrier rate agreements with longer-term commitments than their Asian counterparts. Thus, FEFC member carriers may be able to sustain higher rates in a falling market, as in the 2000 to 2001 time period, because of their shipper’s lesser ability to adjust rates in response to fluctuating market conditions.

2

by the ELAA. We have also reviewed proprietary data provided by eight carriers

serving the North Europe-Asia trade.

5. In the next section, we provide some industry background. Section III presents the

economic principles of coordination, including a discussion of whether the market

structure on the North Europe-Asia trade is likely to satisfy the elements necessary for

successful coordination. Section IV describes the empirical framework used to assess

the impact of the FEFC. Section V describes the data, and Section VI the regression

results. Section VII summarizes our conclusions.

II. INDUSTRY BACKGROUND

6. Shipping conferences have existed since the late 19th century with the stated goal of

insulating the marketplace from destructive competition.4 A shipping conference is a

group of member carriers serving a particular trade that regularly meets to discuss

trade and industry outlook.5 In contrast to a trade association, the members of a

shipping conference are permitted to discuss prices. Different trades are governed by

different conferences. For example, routes between North Europe and Asia are

governed by the FEFC, while routes between Europe and the US are governed by the

Trans-Atlantic Conference Association (“TACA”).6

7. According to David Jeffries, the General Manager of TACA, TACA representatives

have policy meetings about 10 times a year. Jefferies says, “The carriers come

4 William Sjostrom, “Antitrust Immunity for Shipping Conferences: An Empty Core Approach,” The

Antitrust Bulletin, Summer 1993, pp. 419-423. 5 Conferences, as stated above, are regulated by the Block Exemption contained in Regulation 4056/86. 6 OECD, “Competition Policy in Liner Shipping: Final Report” April 16, 2002, p.22.

3

together and they are able to consider the general state of the trade, and look at issues

of common interest -- rules and regulations, the regulatory scenes in Europe and in

Washington. The carriers can look at their general market share, the state of the trade,

how they see the market developing and consider means of creating and maintaining

stability in the market. If you can pool knowledge, pool views, you have a general

feel for the trade. Then you don't have people acting irrationally and you can

engender a degree of stability.”7 Similarly, the FEFC Principals representatives meet

about 8 times a year.8

8. Historically, carriers within a conference agree to adopt a common rate structure and a

regular schedule of service on specific routes, even during periods of low volume.9,10

Following the Carrier group discussions and Revised TACA decision of the

Commission in 1999, however, the FEFC – like many other conferences – has

reduced dramatically in both size and scope. It is our understanding that while the

FEFC must publish a tariff, it can no longer require a common rate structure.11

Instead, the FEFC engages in a “rate restoration” program whereby it periodically

announces desired rate increases. Since 1999, the FEFC has not policed its

7 Chris Dupin, “Why TACA Has Survived,” Journal of Commerce, Monday, January 29, 2001.

8 FEFC announcement archives, http://www.fareasternfreightconference.com/Press_and_Notices?archive=true.

9 OECD, op. cit., p. 18 10 See Fiona Scott Morton, “Entry and Predation: British Shipping Cartels 1879-1929,” Journal of Economics

and Management Strategy, Vol. 6, No. 4, Winter 1997, pp. 686-687, for a historical description of shipping conferences.

411 Interview with Rod Riseborough, Chief Executive Officer of the FEFC Secretariat, April 8, 2004

members’ relationships with shippers to determine or enforce compliance with its

suggested conference rate and/or announced rate increases.12

9. Over the last several years, containerized cargo between North Europe and Asia has

been transported at individually negotiated rates, whether they are spot rates or rate

agreements with longer-term commitments.13 Carriers typically charge an “all-in-

rate”, which includes sea transport charges, ancillary charges, and surcharges.14 Some

carriers are vertically integrated, owning certain equipment and facilities at ports that

can facilitate the loading or unloading of cargo.15 We also understand that certain

carriers offer better forms of inland transportation.16 To the extent that conference

members offer better services, in terms of loading/unloading cargo or inland

transportation, relative to non-conference members, conference members may be able

to charge higher prices.

10. Containerized cargo refers to cargo transported in standard containers that are loaded

onto container ships, and can include merchandise such as consumer electronics,

apparel, and paper.17 Containers come in two standard sizes: 20-foot boxes and 40-

12 Interview with Rod Riseborough, op. cit. 13 Due in part to the fact that there are no Federal Maritime Commission requirements outside of the US, rate

agreements in the FEFC are less formal than the rate contracts found in the North Atlantic. 14 This “all-in” rate contains at least 3 legs (maritime, two ports) and sometimes 5 if the inland rates are

included. The data set received from the FEFC lines was port to port. 15 For example, MSC in Antwerp, CMA CGM in Marseille, and Hapag Lloyd each have partial ownership in

Alterswerder, APM Terminal, P&O Ports. 16 For example, European Rail Shuttle is owned by Maersk Sealand and P & O Nedlloyd Ltd. 17 In 2000, about 60 percent of worldwide non-bulk cargo was containerized cargo. Joseph Sussman,

Introduction to Transportation Systems, Norwood, MA: Artech House, Inc., 2000, p. 264.

5

foot boxes. Volume is typically measured in terms of TEUs or “twenty-foot

equivalent units”. Thus, a 40-foot box contains 2 TEUs.18

11. Industry supply and demand needs have been generally increasing over time.19 As

manufactured products, such as consumer electronics, are produced primarily in Asia

(not in Europe), westbound demand for scheduled service is much greater than the

eastbound demand. As a result, there is less excess capacity going westbound,

relative to eastbound, and the lines’ principal problem is getting as many boxes back

to the Far East as quickly as possible in order to satisfy the westbound demand.20

12. In addition to shipping conferences, the industry attempts to balance its supply and

demand needs through the use of shipping consortia. Shipping consortia refer to

arrangements among carriers, conference and non-conference carriers alike, to share

current fleet capacity.21 If one carrier has sold too many slots, it can buy the excess

from another member of the consortia. By allowing carriers access to the same

vessels, shipping consortia dilute potential asymmetries that might otherwise arise

across conference and non-conference carriers.

18 Typically, a 40-foot bay cannot accommodate two 20-foot boxes. 19 World Trade Organization, Annual Report 2004, p. 3. 20 This has been particularly acute in 2003 and 2004 with the growth of exports from China. See World Trade

Organization, op. cit., p. 3. 21 Competition rules for consortia are contained in Regulation 823/2000.

6

III. THE ECONOMIC PRINCIPLES OF COORDINATED BEHAVIOR

13. Shipping conferences can provide the mechanism to orchestrate coordination among

carriers serving the routes in the trade. In principle, carriers may coordinate (either

explicitly or tacitly) on a number of different decisions – including sea prices, inland

haulage rates, schedules, capacity investments, and reactions to regulations. We focus

in this paper on the periodic conference announcements of suggested rate increases.

To the extent that these rate announcements are commensurate with changing supply

and demand conditions, they are simply precursors to independent price increases that

would have occurred anyway. However, to the extent that the rate announcements are

attempts by the conference to raise price above the competitive level, the magnitude

of their impact will depend largely on the mechanisms available to implement and

police the announced rates.

14. Firms can coordinate to raise prices above competitive levels through either explicit

collusion or through a form of behavior commonly called “tacit collusion,”

“conscious parallelism,” or “oligopolistic rationality.” In both tacit and explicit

collusion, successful coordination is characterized by firms' ability to agree on terms

of collusion, to monitor members’ compliance with the terms of the collusive

agreement, and to punish firms that deviate from the collusive agreement.22

15. In this section, we describe the mechanisms that have been known to facilitate and

hinder coordination. We also discuss the apparent asymmetry between conference

22 Phillip E. Areeda, et al., Antitrust Law: An Analysis of Antitrust Principles and Their Application, 1995,

Vol. IIA, ¶ 405.

7

and non-conference carriers. Finally, we describe aspects of the marketplace that

suggest that the FEFC may not be able to implement and police coordinated behavior.

A. COORDINATION TO AVOID COMPETITION 16. It is a well-known proposition in economics that firms have an incentive to coordinate

their behavior to avoid competition. An equally well-known proposition is that in the

face of a collusive agreement, firms have an incentive to cheat.

17. Factors that are known to facilitate collusion include: (1) the existence of mechanisms

to monitor and enforce adherence to an announced pricing scheme; (2) the ability to

punish deviations from the collusive agreement, including the extent to which the

same firms repeatedly encounter each other over time or in multiple markets;23 and

(3) the ability to backlog orders or maintain inventories. The first of these is required

to detect cheating. Absent detection and the associated threat of punishment, there

exists a strong incentive for at least some firms to unilaterally deviate from a collusive

agreement and undercut the agreed upon pricing scheme. Repeated interaction, either

over time or in multiple geographic markets, can provide opportunities to punish

cheaters, thereby raising the implicit cost of cheating from a collusive agreement. For

example, when it is detected that a firm has cheated in one geographic market, other

firms can retaliate and punish the cheating firm in any one or all of the markets in

which they interact. Thus, the possibility of retaliation in many markets can reduce

the incentives to “cheat” in any one market. The ability to backlog orders or maintain

inventories allows firms to adjust to unexpected fluctuations in market conditions.

23 B. Douglas Bernheim and Michael D. Whinston, “Multimarket Contact and Collusive Behavior,” RAND

Journal of Economics, Vol. 21, No. 1, Spring 1990.

8

Absent this ability, firms may have to raise or lower prices (thus deviating from their

collusive agreement) in order to clear the market.

18. Factors that are known to hinder implementation of a collusive agreement include: (1)

large number of sellers; (2) ease of entry; (3) the use of confidential contracts or rate

agreements between buyers and sellers; (4) infrequent or lumpy orders; and (5)

fluctuating market conditions. The first of these is intended to capture the scope of

the coordination problem. While there is no single number for all circumstances,

textbook wisdom suggests that collusion becomes unwieldy to implement as the

number of firms “exceeds 10 or 12.”24 Ease of entry can erode any potential gains

from raising prices above competitive levels. The use of confidential contracts and

fluctuating market conditions impede detection of deviations from the collusive

agreement. In addition, infrequent or lumpy demand can raise the incentive to cheat.

B. CONFERENCE VERSUS NON-CONFERENCE MEMBERS 19. FEFC member carriers handle approximately 60 percent of the trade between North

Europe and Asia, while non-conference carriers handle the remaining 40 percent.25

As a general rule, economic theory predicts that similarly situated non-conference

carriers will mimic conference prices. This symmetry should hold regardless of

whether the conference’s principal function is to process and relay information about

market fundamentals or to coordinate member firms in raising price above

competitive levels. To the extent that non-conference and conference carriers

24 F.M. Scherer, Industrial Market Structure and Economic Performance, Hopewell, NJ: Houghton Mifflin

Company, 2nd edition, p. 199.

25 Based on estimates of non-FEFC capacity, in Rod Riseborough, Chief Executive Officer of the FEFC Secretariat to the FEFC Principals, “Non-Conference Vessel Capacity”, December 17, 2003.

9

compete for the same shippers on the same routes, they should respond in the same

way to information about market fundamentals. Similarly, if the conference succeeds

in enforcing an increase in price above the competitive levels, then non-conference

carriers would find it in their interest to match this price increase.26 Therefore,

systematic differences in conference and non-conference prices, if any, must be

explained by underlying differences in service quality or composition of demand.

C. ABILITY OF THE FEFC MEMBERS TO SUSTAIN COLLUSION 20. As explained above, the operation of the FEFC conference secretariat has changed

dramatically over time. Over the last several years, the FEFC has reduced

dramatically in both size and scope. While conference carriers regularly convene to

discuss prices, the use of confidential rate agreements between shippers and carriers

has become the prevalent practice in the North Europe-Asia trade. Further the FEFC

does not – indeed, cannot – police its members’ relationships with shippers to

determine or enforce compliance with its conference rate and/or announced prices.

Thus, it is unclear whether the FEFC as it currently functions is able to sustain prices

above competitive levels.

21. A number of factors are likely to hinder the FEFC’s ability to sustain its conference

rates. The trade is served by a large number of carriers. Barriers to entry are

26 An industry that has both a cartel and non-cartel firms might be characterized by the “dominant firm-

competitive fringe” model. In this case, the cartel is a dominant firm and the competitive fringe firms are price takers, taking as given the price set by the cartel. (See Dennis Carlton and Jeffrey Perloff, Modern Industrial Organization, New York: HarperCollins College, 2nd edition, p. 200.) To the extent that some of the fringe are large firms able to influence the market, they will best respond to prices set by the cartel. In this case, the fringe firms will still prefer to match the cartel price.

10

relatively low.27 The use of confidential rate agreements between shippers and

carriers is prevalent. Demand for scheduled service can be infrequent and lumpy.

Market conditions have been known to fluctuate over time, and there is little ability to

backlog or inventory.

22. On the other hand, the carriers have multi-market contact – across different routes

within the same trade, across different trades, and over time. To the extent that multi-

contact improves carriers’ ability to punish deviators, it can facilitate collusive

arrangements. Further, even though rate agreements are confidential and the FEFC

does not itself engage in policing, it may be possible for the carriers to monitor each

other’s activity in other, more creative ways. For example, lines within a consortia

have information on the volume of business handled by each other.28

23. In practice, whether the FEFC or its member carriers are engaging in coordinated

behavior to raise prices above competitive levels is an empirical question. In the

remainder of this report, we describe our empirical framework and results of our

analysis of historical data on conference activity and market prices.

IV. EMPIRICAL FRAMEWORK

24. We employ regression analysis to study the effect of FEFC activity on price levels.

Regression analysis is a useful way of understanding the relationship between a

variable of interest – the average price of containerized cargo movement, in this case

– and a set of independent variables that play a role in its determination. Our basic 27 Expansion by an existing carrier entails acquiring additional capacity. We understand that de novo entry

requires capital up to 800 million Euros. Assuming that capital markets function properly, it is difficult to imagine significant barriers to entry.

1128 It is unclear whether on most trades these consortia are of a size that would facilitate collusion.

empirical model relates the average price of containerized cargo movement, defined

as revenue per TEU, to both a set of demand and supply factors that we understand

are widely believed to be important determinants of prices and measures of FEFC

presence. Controlling for observable determinants of market prices, we can use the

model to infer the impact, if any, of FEFC activity.

25. Given the substantial difference in “excess capacity” between westbound and

eastbound movements, we estimate the effects of FEFC activity on price levels

separately for the two directions. Ideally, the FEFC variables should include an

indicator for whether the carrier is a member of the FEFC, a measure of FEFC share

of capacity or volume, and FEFC rate increase announcements. A key demand factor

is the total demand for containerized cargo in the Far East trade. Key supply factors

are the price of fuel and the availability of capacity. Specifically, the model takes the

form:

ijt

tt

jtR

εββββ

ββββ

ββββ

+++++

++++

+++=

j11t10t92t8

7t654

jt32it10ijt

ControlsPair -Port Trends Time Rate ExchangeCapacity

CapacityPrice FuelDemand t Annoucemen Rate FEFC * Membership FEFC

tAnnoucemen Rate FEFCShare FEFCMembership FEFCTeuPer ev

where i indexes the carrier; j indexes the port-pair; and t indexes the time period. εijt

is a stochastic disturbance term, common to regression models, that captures the net

effect of all factors omitted from the empirical specification.

26. FEFC Membership varies by carrier and time.29 FEFC Share of volume or capacity

and FEFC Rate Announcement vary by port-pair and time. The interaction term,

between FEFC Membership and FEFC Rate Announcement, allows FEFC members 29 While in principle FEFC Membership can vary over time, the carriers in our analysis sample have not

changed their membership status over the years for which we have data.

12

to have a differential response from the non-members to the suggested rate increase.

In principle, this model allows us to investigate whether FEFC membership affects

the rate that a line charges; whether FEFC concentration affects all rates on a route;

and whether rate announcements represent information about expected

supply/demand conditions. A technical requirement of the analysis is variation in

conference presence either over time or on different port-pairs, for a given point in

time. We expect our variation to stem from varying degrees of conference presence

across the different port-pairs in our analysis sample.30

27. Measures of Demand, Fuel Price, Capacity, and Capacity Squared vary by time.

Demand and Fuel Price can include either contemporaneous or lagged values,

depending on the structure of the industry. If shipping rates at time t are determined

in a previous period, say t-1, then the information available in the previous period

may explain the average revenues in period t. In principle, revenue per TEU should

be increasing in both demand and fuel price. We expect that as capacity increases,

average revenue decreases, though it is unclear apriori whether this is likely to occur

at an increasing or decreasing rate. Thus, Capacity is allowed to enter as a quadratic;

that is, we include both the level and the squared term, to permit a more flexible

functional form with average revenue.

28. Exchange Rates are used to control for potential effects of currency fluctuations that

may affect the dependent variable, which is reported in USD in the proprietary data.

Time Trends include a set of indicator variables controlling for movements from year

30 According to 2003 FEFC capacity shares, conference share of capacity varies from 50 to 100 percent on the

different port-pairs in our analysis sample.

13

to year that are not otherwise captured by the other regressors discussed above. Port-

Pair Controls include a set of indicator variables controlling for the port-pair involved

in the movement. These variables control for differences in loading/unloading

technology, inland transportation, and regulations that are port or port-pair specific.

V. DATA USED FOR ANALYSIS

29. We have assembled an analysis dataset of containerized cargo movements in the

North Europe-Asia trade on both the eastbound and westbound legs. We use a

combination of proprietary and publicly available data to construct this dataset. The

proprietary data come from four FEFC conference and two non-conference

members.31 These data, which are summarized in Table 1, contain information on

revenues and total volume, measured in TEUs, for the years 2000-2003.32 We

construct revenue per TEU by dividing revenue by volume. Table 1 also presents the

variables contained in the carrier-provided data files. Based on communication with

carriers, our analysis assumes that revenues are sea only revenues and do not includes

revenues for other ancillary services such as inland transportation.

30. The proprietary data vary by month for four of the six carriers and by quarter for the

other two. The demand, fuel price, and capacity data – which are described in more

detail below – are available quarterly. Thus, our analysis dataset is quarterly, where

the monthly proprietary data are aggregated appropriately. 31 These data were collected in response to our information request submitted to the ELAA via outside

counsel. We understand that this request was sent to all ELAA member carriers, and the carriers who responded represent a random selection of ELAA members. We analyze data from Evergreen, HLCL, Hanjin, MSK, NYK, and PON (see Table 2). We also received data from MOL and CP Ships, but for different reasons these data were incompatible for use in our study.

32 The proprietary data are available from 1999-2003, but due to data limitations on aggregate demand and capacity, our analysis data begins in 2000.

14

31. The analysis data includes a total of 60 different port-pair combinations, with six ports

in Europe and five ports in Asia.33 Table 2 shows the different port-pair combinations

along with average revenues, 2003 FEFC market share, and carriers serving those

port-pairs. The final analysis data set contains 2,147 complete westbound records and

1,909 complete eastbound records of quarterly data for specific carrier and port-pair

combinations. Table 3 presents summary statistics (means and standard deviations)

for the variables of interest, separately for eastbound and westbound. The table also

presents summary statistics for the full sample (2000 to 2003) as well as for the

reduced sample looking only at 2003.

32. The remainder of this section describes the construction of the FEFC, demand, fuel

price, capacity, and exchange rate variables. We highlight concerns or limitations of

the data in the discussion.

A. FEFC MEMBERSHIP 33. We collected information on FEFC membership since 2000 from the FEFC website.34

While FEFC membership has fluctuated over time, the six carriers for which we have

proprietary data have not changed their member status. Thus, we are unable to

separately estimate carrier-specific effects from FEFC membership effects.35

33 The ports in Europe include: Hamburg, Antwerp, Bremerhaven, Felixstowe, Rotterdam, and Southampton.

The ports in Asia include: Hong Kong, Shanghai, Pusan, Yokohama/Tokyo/Kobe, and Yantian/Shekou. The port groupings (e.g. Yokohama/Tokyo/Kobe) reflect the aggregation present in the carrier data.

34 http://www.fareasternfreightconference.com.

35 In this case, the inclusion of both carrier-specific indicator variables and the FEFC membership indicator variable would result in a serious misspecification of the regression model. Specifically, the two sets of variables would be perfectly collinear.

15

B. FEFC RATE ANNOUNCEMENTS 34. We collected information about the FEFC rate restoration program from three

separate data sources: Drewry Shipping Consultants (“Drewry”), the FEFC website,36

and files received from the FEFC. Drewry publishes conference rate increases and

surcharge announcements.37 The announcements are also archived on the FEFC

website. Upon compiling the available information, we found the three sources to be

generally compatible, yet there were instances where one source contained more

announcements than the others. Thus, we collected all unique announcements across

the three sources.

35. The westbound rate announcements appear separately for 20-foot and 40-foot boxes,

and the 40-foot increases are systematically twice their 20-foot counterpart. As such,

the rate increase on a per TEU basis is the same, regardless of box size. The

eastbound rate announcements, however, appear to be the same for both the 20- and

40-foot boxes. We compute the rate increase on a per TEU basis assuming an equal

number of 20 and 40- foot boxes.

36. We calculate a “suggested conference rate” as the sum of the announced rate increase

and the average FEFC market rate during the month prior to the effective date of the

desired increase. For example, announcements of 200 USD in April and 150 USD in

June indicate that the conference suggested rate for period from April 1 to May 31

would be 200 USD higher than the average FEFC carrier rate in March, while the

suggested rate from June 1 onward would be 150 USD higher than the average FEFC

36 http://www.fareasternfreightconference.com/Press_and_Notices

37 Drewry Shipping Consultants, “The Drewry Container Market Quarterly”, various issues.

16

carrier rate in May. Figure 1 illustrates average monthly FEFC rate along with our

calculated suggested conference rate.

37. We constructed a quarterly suggested conference rate variable as the value during the

middle month of each quarter. For example, we use the February rate for the first

quarter of a given year.

C. FEFC CAPACITY SHARE 38. We obtained information on non-conference capacity serving the trade from a

confidential memo titled “Non-Conference Vessel Capacity.”38 The memo provides

estimates of non-conference carrier capacity on specific routes serving the trade.

Using the information from the March issue of Drewry’s “Container Market

Quarterly” on ports visited on each route and total nominal capacity on the route39, we

constructed conference capacity share for each port-pair.

39. A serious limitation of these data is that they are only available for 2003. As such,

when we include FEFC capacity share in the regression specification, we are limited

to a 2003 only sample. This is particularly limiting because most of our key

regressors, including demand, fuel price, and capacity, are only available at the

quarterly level.

D. AGGREGATE DEMAND 40. We employ two alternative measures of aggregate demand. The first is an estimate of

total TEUs shipped by route, separately for the eastbound and westbound legs, from

38 Rod Riseborough, Chief Executive Officer of the FEFC Secretariat to the FEFC Principals, “Non-

Conference Vessel Capacity”, December 17, 2003.

39 The table detailing this information is dated January 1, 2004 making it contemporaneous with the nonconference capacity data.

17

Drewry.40 Prior to 2000, Drewry reported this information twice a year; since 2000,

the information is available quarterly. (This same limitation applies to our data for

aggregate capacity.) Thus, our analysis sample begins in the year 2000, even though

our proprietary data are available going back to 1999.

41. Second, we measure aggregate demand using the growth in imports of key consumer

goods that account for the majority of containerized cargo. We understand that these

goods are electronics and paper goods, on the westbound and eastbound legs,

respectively.

42. On the westbound leg, we construct quarterly growth in the volume (measured in

USD) of consumer electronics41 imported to North Europe 42 from the Far East, using

trade data from a proprietary database known as TradStat.43 Similarly, on the

eastbound leg, we construct quarterly growth in the volume (measured in USD) of

paper goods imported to China, Hong Kong, Japan, and Korea, from North Europe.44

E. EXCHANGE RATES 43. In our westbound model, we use the average over the quarter of the daily Euro-USD

exchange rate. Similarly, in our eastbound model, we use a set of exchange rates one

40 Drewry Shipping Consultants, “The Drewry Container Market Quarterly”, March 2004, p. 102. 41 Consumer electronics includes goods such as domestic appliances and home entertainment equipment. 42 We define North Europe as Belgium, Denmark, Finland, Germany, Norway, Sweden, and the United

Kingdom. Data for the Netherlands are not available. 43 These data are obtained from Thompson Dialog’s TradStat database (http://www.tradstatweb.com). 44 This includes all origin countries in Europe with the exception of Belgium, due to the fact that the data for

Belgium are incomplete.

18

for each of the Far East countries in our analysis. These data are obtained from the

U.S. Federal Reserve.45

F. AGGREGATE CAPACITY 44. We obtained information on aggregate capacity, in 1000 TEUs, by route from

Drewry.46 As described above, these data are available quarterly as of 2000.

G. SINGAPORE DIESEL SPOT PRICE 45. To control for supply costs, we included a fuel price variable – the diesel spot price in

Singapore, measured in USD per metric ton47. We use the average over the quarter of

the midpoint between the daily high and low prices.

VI. REGRESSION ANALYSIS OF PRICE LEVELS

46. Using the method of ordinary least squares (OLS), we have estimated the parameters

of the base specification described above, and we have performed a series of

specification tests to determine the set of relevant variables and their functional form

that have resulted in extensions of the base model. Results for the full sample, 2000

to 2003, are presented in Tables 4A and 4B. Results for the 2003 only sample are

presented in Table 5. For each table, extensions are presented across the columns.

We discuss each specification in turn.

A. BASE SPECIFICATION, 2000-2003 SAMPLE 47. The estimation results for the full sample, 2000-2003, are presented in Tables 4A and

4B, for the westbound and eastbound legs, respectively. The regressors in the base

45 http://www.federalreserve.gov/releases/h10/Hist/

46 Drewry Shipping Consultants, “The Drewry Container Market Quarterly”, March 2004, p. 102.

47 Platt's Bunkerwire, Platt's Energy Prices, DRI-WEFA Webstract.

19

specification along with their expected signs (to the extent economic theory alone can

predict) are as follows:

• FEFC membership. The coefficient on this variable represents the price

differential charged by FEFC members, all else held equal.48

• Suggested Conference Rate. This variable shows the correlation, if any, of

suggested conference rate with average revenue. A finding of positive correlation

may indicate either that the FEFC is successful at elevating price above

competitive levels or that the FEFC is simply transmitting information about

expected market outlook, or both.

• FEFC membership interacted with suggested conference rate. This variable

illustrates whether the suggested conference rates affect FEFC members’ rates

differently than those of non-FEFC members.

• Aggregate demand. Aggregate westbound demand is used in the westbound

specification and aggregate eastbound demand, in the eastbound specification.

This variable is expected to have a positive effect on rates.

• Aggregate capacity and aggregate capacity squared. We expect capacity to have

a negative effect on rates, although perhaps at a decreasing rate. Thus, we may

find a small but negative coefficient on the squared term.49

• Singapore diesel spot price. The fuel price is a principal component of variable

cost and is expected to be positively associated with average revenues.

48 As explained earlier, we are unable to estimate separate carrier specific effects.

49 Aggregate capacity rather than carrier specific capacity is used since there appears to be a good deal of capacity sharing, through shipping consortia as well as individually negotiated rentals of excess capacity on vessels.

20

• Exchange rate. This variable (or set of variables) is used to control for

fluctuations in the currency of the region receiving the containerized cargo. We

expect this variable to be positively correlated with average revenues – that is, all

else equal, westbound revenue per TEU expressed in USD will increase as the

Euro appreciates vis a vis the U.S. dollar.

• Year Indicator Variables. These variables are used to control for fluctuations in

price over time due to external factors such as inflation.

• Port-Pair Indicator Variables. These variables are used to account for port

specific costs such as port handling charges.

48. The estimation results for the westbound sample are presented in Column 1 of Table

4A. The regression specification has an adjusted R2 of 0.65.50 We find that the

coefficient of the FEFC indicator is positive and statistically significant, suggesting

that FEFC members charge on average 215 USD more per TEU than non-conference

members. This result is generally stable over the extensions considered (across

Columns 1 through 5 in Table 4A), though the level of the premium fluctuates

between 44 USD to 240 USD, depending on the specification. In addition, the

suggested conference rate has a positive and statistically significant effect on actual

realized rates. The interaction term between FEFC membership and the suggested

conference rate has a small, negative coefficient that is statistically significant,

suggesting that the FEFC members have a somewhat smaller response to

announcements.

21

50 Adjusted R2 is a widely used measure of goodness of fit that can range from 0 to 1, where 1 represents a perfect fit.

49. Aggregate demand and capacity have the wrong sign, though the former is not

statistically significant. By contrast, the fuel price and the U.S. dollar to Euro

exchange rate are statistically significant and have the expected signs.

50. The estimation results for the eastbound sample are presented in Column 1 of Table

4B. This regression has a much lower adjusted R2 and has estimated coefficients that

are less statistically significant. We believe this pattern is driven in large part by the

low utilization of eastbound capacity. Nonetheless, it is noteworthy that the FEFC

membership indicator is never statistically significant, while the FEFC suggested

conference rate is positive and statistically significant across Columns 1 through 3.

B. EXTENSIONS OF THE BASE SPECIFICATION 51. We have examined various extensions to the base specification and have found that

there are several important omitted variables in the original specification. These

extensions are presented in the Columns of 2 through 5 of Tables 4A and 4B. We

discuss each in turn.

52. The first extension involves replacing the aggregate demand regressor with an

alternative measure of demand for containerized cargo. The reason for this change is

the concern that total volume in TEUs may not be an exogenous regressor – that is, it

may itself be determined, at least in part, by the dependent variable. In situations

where a regressor is jointly determined with the dependent variable, the estimates

obtained from OLS are no longer reliable. Thus, we replace aggregate demand in the

westbound model with our measure of electronics import growth, and we replace

aggregate demand in the eastbound model with our measure of paper import growth.

Electronics growth is statistically significant and has the expected sign in all of the

22

westbound specifications.51 (See Columns 2 through 5 of Table 4A.) Paper growth is

not statistically significant and has the wrong sign in the eastbound regressions. (See

Columns 2 through 5 of Table 4B).

53. The second extension is to add as an additional regressor the aggregate demand in the

opposite direction. This is important because the effective average cost of the

westbound cargo falls when the vessel is also used in the eastbound direction. Thus,

competition on the westbound routes may generate a lower rate in the high-demand

direction when demand in the opposite direction increases. Similarly, as demand for

westbound capacity increases, the capacity imbalance grows and there is more

capacity chasing very little cargo on the eastbound route. Because of the low

marginal costs in liner shipping, we expect that as westbound demand increases, the

eastbound average revenue decreases. As expected, we find that demand in the

opposite direction is an important predictor of average revenue, although this variable

has the wrong sign in the westbound model. (See Column 3 of Table 4A.) Aggregate

demand in the opposite direction in the eastbound model has the expected sign and is

statistically significant. (See Columns 3 through 5 of Table 4B.)

54. The third extension is to consider a lag structure for demand and the fuel price. If

rates in this period were determined in a prior period – due to long-term contracts,

then lagged demand and lagged fuel prices may explain at least a portion of today’s

average revenues. Given that long-term contracts between shippers and carriers last

51 In place of growth in the volume (measured in USD) of consumer electronics, we have also estimated the

westbound model using growth in volume (measured in kilograms). Both specifications yield the same qualitative results.

23

between one and six months, a one quarter lag structure is likely to be appropriate.52

Thus, we add as additional regressors lagged demand in the opposite direction and

lagged fuel price. Lagged fuel price is statistically significant and has the expected

sign in the westbound model (See Column 4 of Table 4A.) The lagged fuel price is

statistically significant and has the expected sign in the eastbound model. (See

Column 4 of Table 4B.)

55. Finally, we investigate the effect of dropping the FEFC announcement variables on

the coefficients associated with the demand and supply factors included in the

regression specifications. If it is the case that the FEFC simply serves the function of

transmitting market information, then the FEFC announcements should be highly

correlated with the demand and supply factors, resulting in inflated standard errors.

Upon dropping the announcement variables, we find that the explanatory power of

other market factors increases. In the westbound model, lagged aggregate demand in

the opposite direction and contemporaneous fuel price, neither of which were

statistically significant in the fully specified model, gain significance. Aggregate

demand in the other direction now has the expected sign and is statistically

significant. (See Column 5 of Table 4A.)

56. This finding suggests strongly that the FEFC announcements reflect market

conditions and draw away the explanatory power of those demand variables.

52 In addition, an analysis done by CapAnalysis (found on the DG Competition website) shows that the BAF

surcharge for fuel dictated by the FEFC is highly correlated with a lag in fuel prices.

24

C. 2003 ONLY SAMPLE 57. A serious omission of the specifications shown in Tables 4A and 4B is a variable

measuring FEFC presence on the different routes. The FEFC suggested conference

rate, for example, is likely to have a more noticeable effect on routes that have

stronger conference presence. Typical measures of concentration include market

share of volume or market share of capacity. However, to construct this variable with

our analysis sample we require data on total volume or total capacity by route, by

quarter. We have data on total capacity by quarter for 2003 only. What is evident

from these data is that FEFC market share varies noticeably from route to route,

ranging from 100 percent on some routes down to about 50 percent on others.

58. Thus, we have re-estimated our base specification using the 2003 sample. See

Columns 1 and 5 of Table 5. Notable omissions from the specifications shown in

Table 5 are demand in the opposite direction, the lagged variables, capacity, and the

exchange rate – all of which were important explanatory variables in Tables 4A and

4B and all of which vary by the calendar quarter. The reason for these omissions is

that the 2003 sample, by construction, has only four quarters and thus, permits at most

three variables that vary by quarter.53

59. Nonetheless, we re-estimated our regression specification including FEFC capacity

share, instead of these demand and supply factors. The coefficient on the capacity

share variable can show whether routes with higher FEFC presence have higher

prices. However, this variable does not appear to have any explanatory power. We

53 We were unable to include three quarterly variables in our specification because of near singularity. Thus,

the specifications shown in Table 5 include only two quarterly variables: electronics or paper growth and fuel price.

25

expect that this is likely due to the lack of sufficient data and the resulting omission of

important explanatory variables.

D. FIRST DIFFERENCE MODEL 60. In addition to the extensions discussed above, we have also re-estimated the

parameters of our regression model using a method known as first-difference

estimation. First difference estimation involves regressing the one-quarter change in

the dependent variable on the one-quarter changes in the independent variables. This

transformation of the original regression model has two potential benefits. First,

differencing the model in this manner eliminates the potential influence of time-

invariant, route-specific factors that may otherwise be omitted from the regression

specification. Second, the first-differenced data series can have desirable statistical

properties even in instances where the original data series may not.54 A potential

disadvantage of first difference estimation is that the differencing eliminates much of

the meaningful variation from the data.55

61. Assuming that the underlying model is well-specified and that the data series exhibit

the necessary statistical properties, the estimation of the model in levels is preferred to

first difference estimation. However, serious differences between the first difference

and levels results are an indicator of specification error in the levels model. As such,

estimation of the first difference model is appropriately viewed as a specification test

of the validity of the underlying model.

54 Andrew Harvey, The Econometric Analysis of Time Series, Cambridge, MA: The MIT Press, 1990, p. 29. 55 As such, overall measures of fit from first differenced estimation tend to be much lower than the

corresponding measures of fit from estimation of the model in levels.

26

62. Tables 6 and 7 present our first difference analysis. Table 6 shows the means and the

standard deviations of the first differenced data used in the regression analysis. Table

7 presents the estimation results. As expected, the adjusted R2 decrease from

approximately 0.6 to 0.29 or 0.21 in the westbound specification, depending on

whether or not the conference announcement variable is included. A similar pattern is

found in the eastbound specification. As with the levels regressions, the eastbound

regression has a much lower adjusted R2 and has estimated coefficients that are

persistently insignificant. We believe this pattern is driven in large part by the low

utilization of eastbound capacity.

63. The first difference westbound regression results are generally compatible with the

levels results. As with the levels results, the suggested conference rate has a positive

and statistically significant effect on average revenue per TEU. In addition, demand,

demand in the other direction, lagged fuel prices, capacity, and the exchange rate have

the expected signs and statistically significant effects on the revenue per TEU. We

also find that fuel price and lagged demand in the opposite direction take on the

expected signs and are statistically significant upon dropping the suggested

conference rate variable. As with the levels model, this pattern of results suggests that

the suggested conference rate and the supply and demand factors are likely to be

highly correlated.

VII. CONCLUSIONS

64. Using an analysis dataset of containerized cargo movements in the North Europe-Asia

trade, we have attempted to estimate a model that explains movements in average

revenue across routes and over time. Our analysis suggests very clearly that demand,

27

demand in the opposite direction, fuel prices, lagged demand and fuel prices, capacity,

and exchange rates are important determinants of average revenues.

65. Our analysis also suggests that conference activity has some effect on market

outcomes. In particular, we find fairly consistently that FEFC members receive

higher rates on westbound routes, as compared to non-members. Though the

empirical analysis is unable to identify the reason for this higher price, economic

principles suggest that this premium is likely due to a quality differential. To see this,

suppose hypothetically that the conference is successful at raising price above

competitive levels, then one would expect that the non-members would follow suit

and raise their price to match that of the FEFC members. It cannot be the case,

therefore, that a price differential is evidence of conspiracy. Rather, it is more likely

that this price differential reflects a service differential. For example, if it were the

case that conference members tend to offer better in-land transportation, shippers

would be willing to pay higher sea prices to ship with conference carriers.

66. In addition, our results suggest that suggested conference rates reflect information on

market fundamentals. It is noteworthy that lagged aggregate demand in the opposite

direction and contemporaneous fuel price, neither of which were statistically

significant in the fully specified model, gain significance in the westbound

specification that drops the announcement variables. In addition, contemporaneous

aggregate demand in the other direction takes on the correct sign and is statistically

significant in that model. Finding that one set of variables becomes statistically

significant when another, potentially related set is omitted, is symptomatic of

multicollinearity – that is when two or more variables in a regression model contain

28

29

essentially the same information, perhaps in different forms. Thus, these findings

support the proposition that the FEFC’s suggested conference rates are commensurate

with changing supply and demand conditions.

67. Finally, we temper these conclusions with the important caveat that we are unable to

control adequately for conference market share – inclusion of which can potentially

alter the results discussed above. Our 2003 only analysis suffers from insufficient

data – as evidence by the general lack of statistical significance. We would require a

longer time series of capacity or total volumes by trade routes to address this concern.

Figure 1: Westbound Suggested Conference Rates

0

500

1000

1500

2000

2500

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04

U.S

. Dol

lars

Average FEFC Revenue per TEU

Suggested Conference Rate

* For the purpose of illustration, this Figure omits data for cargo movements originating in Japan after December 2002, when the Japan-Europe trade came under the control of the Japan Europe Freight Conference.

THIS PAGE HAS BEEN REDACTED

Table 1Carrier Statistics (2000-2003)

Westbound Eastbound

CarrierFEFC

MemberVariables Used to Construct

Average Revenue

Average Revenue per TEU

Average Total TEU

Average Total

Revenue

Average Revenue per TEU

Average Total TEU

Average Total

Revenue

Evergreen No "Total Revenue"; "Total TEU"Hapag-Lloyd Container Linie (HLCL) Yes "TEU"; "Tot Rev (excl. OLF/DLF)"Hanjin No "Vol"; "Rev"Maersk SeaLand (MSK) Yes "REVENUE"; "TEU"Nippon Yusen Kaisha (NYK) Yes "Total Revenue"; "Total Teu"P & O Nedlloyd (PON) Yes "Sea revenue $US"; "Volume Teu"

Note:Averages are across port pair and quarter.

THIS PAGE HAS BEEN REDACTED

Table 2Port Pair Statistics

Port PairAverage Rev.

per TEU2003 FEFC

Capacity Share Carriers Serving

Antwerp-Hong Kong Evergreen, Hanjin, MSK, NYK, PONAntwerp-Pusan Evergreen, Hanjin, MSK, NYK, PONAntwerp-Shanghai Evergreen, Hanjin, MSK, NYK, PONAntwerp-Yokohama/Kobe/Tokyo Evergreen, Hanjin, MSK, PONAntwerp-Yantian/Shekou Evergreen, Hanjin, MSK, NYK, PONBremerhaven-Hong Kong HLCL, Hanjin, MSK, NYK, PONBremerhaven-Pusan HLCL, MSK, NYK, PONBremerhaven-Shanghai HLCL, MSK, NYK, PONBremerhaven-Yokohama/Kobe/Tokyo HLCL, Hanjin, MSK, PONBremerhaven-Yantian/Shekou MSK, PONFelixstowe-Hong Kong Hanjin, MSKFelixstowe-Pusan Hanjin, MSKFelixstowe-Shanghai Hanjin, MSKFelixstowe-Yokohama/Kobe/Tokyo Hanjin, MSKFelixstowe-Yantian/Shekou Hanjin, MSKHamburg-Hong Kong Evergreen, HLCL, Hanjin, MSK, NYK, PONHamburg-Pusan Evergreen, HLCL, Hanjin, MSK, NYK, PONHamburg-Shanghai Evergreen, HLCL, Hanjin, MSK, NYK, PONHamburg-Yokohama/Kobe/Tokyo Evergreen, HLCL, Hanjin, MSK, NYK, PONHamburg-Yantian/Shekou Evergreen, HLCL, Hanjin, MSK, NYK, PONHong Kong-Antwerp Evergreen, Hanjin, MSK, NYK, PONHong Kong-Bremerhaven Evergreen, HLCL, Hanjin, MSK, NYK, PONHong Kong-Felixstowe Evergreen, Hanjin, MSKHong Kong-Hamburg Evergreen, HLCL, Hanjin, MSK, NYK, PONHong Kong-Rotterdam Evergreen, HLCL, Hanjin, MSK, NYK, PONHong Kong-Southampton Evergreen, HLCL, NYK, PONPusan-Antwerp Evergreen, Hanjin, MSK, NYK, PONPusan-Bremerhaven Evergreen, HLCL, Hanjin, MSK, NYK, PONPusan-Felixstowe Evergreen, Hanjin, MSKPusan-Hamburg Evergreen, HLCL, Hanjin, MSK, NYK, PONPusan-Rotterdam Evergreen, HLCL, Hanjin, MSK, NYK, PONPusan-Southampton HLCL, Hanjin, NYK, PONRotterdam-Hong Kong Evergreen, HLCL, Hanjin, MSK, NYK, PONRotterdam-Pusan Evergreen, HLCL, Hanjin, MSK, NYK, PONRotterdam-Shanghai Evergreen, HLCL, Hanjin, MSK, NYK, PONRotterdam-Yokohama/Kobe/Tokyo Evergreen, HLCL, Hanjin, MSK, NYK, PONRotterdam-Yantian/Shekou Evergreen, HLCL, Hanjin, MSK, NYK, PONShanghai-Antwerp Evergreen, Hanjin, MSK, NYK, PONShanghai-Bremerhaven Evergreen, HLCL, Hanjin, MSK, NYK, PONShanghai-Felixstowe Evergreen, Hanjin, MSKShanghai-Hamburg Evergreen, HLCL, Hanjin, MSK, NYK, PONShanghai-Rotterdam Evergreen, HLCL, Hanjin, MSK, NYK, PONShanghai-Southampton Evergreen, HLCL, Hanjin, NYK, PONSouthampton-Hong Kong HLCL, NYK, PONSouthampton-Pusan HLCL, NYK, PONSouthampton-Shanghai HLCL, NYK, PONSouthampton-Yokohama/Kobe/Tokyo HLCL, NYK, PONSouthampton-Yantian/Shekou HLCL, NYK, PONYokohama/Kobe/Tokyo-Antwerp Evergreen, Hanjin, MSK, NYK, PONYokohama/Kobe/Tokyo-Bremerhaven Hanjin, MSK, NYK, PONYokohama/Kobe/Tokyo-Felixstowe Hanjin, MSKYokohama/Kobe/Tokyo-Hamburg Evergreen, HLCL, Hanjin, MSK, NYK, PONYokohama/Kobe/Tokyo-Rotterdam Evergreen, HLCL, Hanjin, MSK, NYK, PONYokohama/Kobe/Tokyo-Southampton HLCL, NYK, PONYantian/Shekou-Antwerp Evergreen, Hanjin, MSK, NYK, PONYantian/Shekou-Bremerhaven Evergreen, HLCL, Hanjin, MSK, NYK, PONYantian/Shekou-Felixstowe Evergreen, Hanjin, MSKYantian/Shekou-Hamburg Evergreen, HLCL, Hanjin, MSK, NYK, PONYantian/Shekou-Rotterdam Evergreen, HLCL, Hanjin, MSK, NYK, PONYantian/Shekou-Southampton Evergreen, HLCL, Hanjin, NYK, PON

Table 3Means and Standard Deviations (in Parentheses) of Quarterly Analysis Data

Westbound Eastbound

2000 - 2003 2003 2000 - 2003 2003

Revenue per TEU 1,365 1,525 647 657(301) (250) (263) (191)

FEFC Membership 62% 61% 71% 71%(0.49) (0.49) (0.45) (0.45)

Suggested Conference Rate 1,613 1,680 877 873(240) (135) (93) (86)

Aggregate Demand (000 TEU) 1,044 732(273) (55)

Growth Rate of Electronics Imports 10.04 12.99(27) (31)

Growth Rate of Paper Imports 2.53 1.71(13) (12)

Singapore Diesel Spot Price 226 240 226 239(30) (23) (30) (23)

FEFC Capacity Share 73% 71%(0.18) (0.17)

Aggregate Capacity (000 TEU) 1,264 1,023(109) (94)

Aggregate Capacity Squared 1,610,700 1,054,769(278,037) (193,013)

Euro Exchange Rate ($ / Euro) 0.97(0.10)

China Exchange Rate ($ / 1000 Yuan) 121(0.01)

Japan Exchange Rate ($ / 1000 Yen) 9(0.54)

Korea Exchange Rate ($ / 1000 Won) 0.82(0.05)

Observations 2,147 537 1,909 484Number of Liners 6 6 6 6Number of Port Pairs 30 30 30 30

Notes:1. Values for "Growth Rate of Electronics Imports" for Q1 2000 are missing because the volume data for Q4 1999 are not available. The reported figures for 2000-2003 are based on a sample size of 2,007.2. Values for "Growth Rate of Paper Imports" for Q1 2000 are missing because the volume data for Q4 1999 are not available. The reported figures for 2000-2003 are based on a sample size of 1,791.

Table 4ADependent Variable: Revenue per TEU (Westbound, 2000 to 2003)

(1) (2) (3) (4) (5)

214.763 239.869 237.502 236.702 44.450(3.99)** (4.41)** (4.40)** (4.39)** (5.14)**

0.742 0.691 0.796 0.686(19.96)** (18.13)** (18.47)** (12.03)**

-0.103 -0.122 -0.121 -0.120(3.12)** (3.64)** (3.62)** (3.61)**

-0.010(0.49)

0.993 1.043 1.096 0.894(4.19)** (4.43)** (4.66)** (3.68)**

1.182 1.213 -0.894(5.12)** (3.50)** (2.93)**

-0.078 -1.846(0.21) (5.32)**

1.163 0.448 -0.113 0.006 1.882(6.13)** (2.12)* (0.48) (0.02) (7.08)**

1.140 2.698(3.20)** (7.91)**

4.991 -4.971 -3.813 -12.318 -26.537(2.78)** (2.46)* (1.89) (3.31)** (7.31)**

-0.002 0.002 0.001 0.004 0.010(2.79)** (2.10)* (1.43) (3.11)** (7.37)**

1,268.957 1,140.168 893.567 377.350 1,068.402(8.65)** (7.64)** (5.73)** (0.96) (2.66)**

-4,747.812 2,873.754 1,525.288 7,527.693 18,985.449(3.66)** (1.96) (1.03) (2.95)** (7.78)**

Port Pair Indicators Included Included Included Included IncludedYear Indicators Included Included Included Included Included

Observations 2147 2007 2007 2007 2007Adjusted R2 0.65 0.67 0.67 0.67 0.65

Note:Absolute value of t statistics in parentheses (* significant at 5%; ** significant at 1%).

Constant

Euro Exchange Rate

Aggregate Capacity Squared

Aggregate Capacity

Lagged Singapore Diesel Spot Price

Singapore Diesel Spot Price

Lagged Aggregate Demand in Other Direction

Aggregage Demand in Other Direction

FEFC Membership

Growth Rate of Electronics Imports

Aggregate Demand

FEFC Membership * Suggested Conference Rate

Suggested Conference Rate

Table 4BDependent Variable: Revenue per TEU (Eastbound, 2000 to 2003)

(1) (2) (3) (4) (5)

144.005 145.311 147.766 150.940 8.331(1.42) (1.40) (1.43) (1.47) (0.70)

0.535 0.423 0.571 0.092(4.74)** (3.26)** (4.15)** -0.54

-0.155 -0.155 -0.158 -0.162(1.35) (1.33) (1.36) (1.40)

0.354(0.93)

-0.373 -0.597 -0.974 -0.928(0.69) (1.09) (1.68) (1.84)

-0.096 -0.078 -0.080(3.17)** (2.55)* (2.86)**

0.059 0.056(1.19) (1.22)

-0.305 0.150 -0.036 1.663 1.625(0.68) (0.43) (0.10) (3.43)** (3.74)**

2.646 2.597(4.79)** (5.52)**

12.063 -1.634 0.117 -43.689 -42.724(3.21)** (0.34) (0.02) (4.42)** (5.43)**

-0.006 0.000 0.000 0.020 0.020(3.31)** (0.21) (0.21) (4.34)** (5.32)**

-3,305.658 679.570 1,094.907 9,210.732 8,971.351(1.53) (0.41) (0.65) (3.39)** (3.87)**

283.331 125.710 166.627 -515.166 -499.436(4.01)** (1.75) (2.29)* (3.35)** (4.18)**

-576.282 477.611 856.819 4,591.890 4,515.236(0.85) (0.82) (1.44) (4.80)** (5.36)**

391,204.365 -82,123.695 -133,726.078 -1,089,179.635 -1,060,733.266(1.51) (0.41) (0.67) (3.35)** (3.82)**

Port Pair Indicators Included Included Included Included IncludedYear Indicators Included Included Included Included Included

Observations 1909 1791 1791 1791 1791Adjusted R2 0.34 0.35 0.35 0.36 0.36

Note:Absolute value of t statistics in parentheses (* significant at 5%; ** significant at 1%).

FEFC Membership

Suggested Conference Rate

FEFC Membership * Suggested Conference Rate

Aggregate Demand

Growth Rate of Paper Imports

Aggregage Demand in Other Direction

Lagged Aggregate Demand in Other Direction

Singapore Diesel Spot Price

Japan Exchange Rate

Korea Exchange Rate

Constant

Lagged Singapore Diesel Spot Price

Aggregate Capacity

Aggregate Capacity Squared

China Exchange Rate

Table 5Dependent Variable: Revenue per TEU (2003 Only)

Westbound Eastbound

(1) (2) (3) (4) (5) (6) (7) (8)

396.088 384.931 392.861 -16.418 59.005 59.859 59.663 29.694(1.87) (1.79) (1.82) (0.92) (0.37) (0.38) (0.37) (1.76)

0.488 0.495 0.494 0.146 0.149 0.148(3.79)** (3.76)** (3.76)** (0.72) (0.73) (0.73)

-0.243 -0.240 -0.244 -0.032 -0.035 -0.034(1.94) (1.88) (1.91) (0.18) (0.19) (0.19)

138.978 141.766 -8.320 -10.782(1.28) (1.29) (0.09) (0.11)

1.983 1.975 1.974 3.021(4.72)** (4.60)** (4.60)** (10.28)**

-0.517 -0.462 -0.466 -1.152(0.49) (0.44) (0.44) (1.87)

-1.039 -1.018 -1.025 -1.465 -1.535 -1.534 -1.535 -1.695(2.61)** (2.50)* (2.52)* (3.77)** (4.15)** (4.12)** (4.12)** (5.38)**

856.699 984.232 845.425 1,768.384 787.888 797.262 803.014 976.086(3.28)** (3.73)** (2.97)** (11.90)** (3.48)** (3.40)** (3.29)** (9.64)**

Port Pair Indicators Included IncludedIndividual Port Indicators Included Included Included Included Included Included

Observations 537 537 537 537 484 484 484 484Adjusted R2 0.43 0.4 0.4 0.39 0.34 0.33 0.33 0.33

Note:Absolute value of t statistics in parentheses (* significant at 5%; ** significant at 1%).

Growth Rate of Electronics Imports

Growth Rate of Paper Imports

Singapore Diesel Spot Price

Constant

FEFC Membership

Suggested Conference Rate

FEFC Membership * Suggested Conference Rate

FEFC Capacity Share

Table 6Means and Standard Deviations (in Parentheses) of First-Differenced Data

Westbound (2000 - 2003)

Eastbound (2000 - 2003)

Change in Revenue per TEU 10 -5(184) (173)

Change in Suggested Conference Rate 10 -1(151) (111)

Change in Growth Rate of Electronics Imports 3.64(42)

Change in Growth Rate of Paper Imports -1.18(18)

Change in Aggregate Demand in Other Direction (000 TEU) 9 16(33) (374)

Change in Singapore Diesel Spot Price 2 2(35) (35)

Change in Aggregate Capacity (000 TEU) 26 23(33) (30)

Change in Aggregate Capacity Squared 69,070 48,246(88,552) (65,156)

Change in Euro Exchange Rate ($ / Euro) 0.02(0.04)

Change in China Exchange Rate ($ / 1000 Yuan) 0.00(0.01)

Change in Japan Exchange Rate ($ / 1000 Yen) -0.01(0.36)

Change in Korea Exchange Rate ($ / 1000 Won) 0.00(0.03)

Observations 1,808 1,639Number of Liners 6 6Number of Port Pairs 30 30

Table 7Dependent Variable: First-Difference of Revenue per TEU (2000 to 2003)

Westbound Eastbound

(1) (2) (3) (4)

0.574 0.164(12.11)** (1.66)

-0.104 0.030(2.10)* (0.37)

0.861 0.447(6.38)** (3.22)**

0.243 -0.146(0.74) (0.52)

0.821 -0.837 -0.059 -0.035(3.83)** (4.42)** (2.96)** (2.06)*

-0.362 -1.531 0.004 0.042(1.58) (6.78)** (0.12) (1.59)

0.149 1.223 1.595 1.827(0.79) (6.78)** (4.99)** (6.00)**

0.908 1.609 2.593 2.773(4.33)** (7.49)** (7.49)** (8.21)**

-8.009 -18.059 -33.876 -37.871(3.31)** (7.42)** (5.84)** (6.84)**

0.003 0.007 0.016 0.018(3.02)** (7.28)** (5.78)** (6.76)**

676.228 967.098(2.64)** (3.59)**

5,084.774 6,976.581(3.34)** (5.41)**

-381.020 -469.872(4.66)** (6.50)**

3,669.540 4,316.063(6.11)** (8.11)**

-28.245 -128.406 -176.537 -187.842(0.54) (2.36)* (3.80)** (4.06)**

-1.852 -1.893 107.461 115.296(0.05) (0.05) (3.93)** (4.25)**

17.013 -20.704 41.990 33.483(0.63) (0.73) (2.30)* (1.87)

Observations 1808 1808 1639 1639Adjusted R2 0.29 0.21 0.07 0.07

Note:Absolute value of t statistics in parentheses (* significant at 5%; ** significant at 1%).

Change in Year 2002 Indicator

Change in Year 2001 Indicator

Change in Year 2000 Indicator

Change in Korea Exchange Rate

Change in Japan Exchange Rate

Change in China Exchange Rate

Change in Euro Exchange Rate

Change in Growth Rate of Paper Imports

FEFC Membership * Change in Suggested Conference Rate

Change in Suggested Conference Rate

Change in Aggregate Capacity Squared

Change in Aggregate Capacity

Change in Growth Rate of Electronics Imports

Lagged Change in Singapore Diesel Spot Price

Change in Singapore Diesel Spot Price

Lagged Change in Aggregate Demand in Other Direction

Change in Aggregate Demand in Other Direction

![dastan-e-kakaka by iqbal chaudhary - Sameer Rawal...efce[ue keäueeme FefC[Ùee 9 neF&-]HeâeF& FefC[Ùee 21 peneB-leneB ceeref[Ùeesef›eâšer 36 hegjeves Deceerj 61 efnvogmleeve](https://static.fdocuments.net/doc/165x107/610548314a22960de83e26a9/dastan-e-kakaka-by-iqbal-chaudhary-sameer-rawal-efceue-keueeme-fefcee.jpg)