Recruitment Agencies in Switzerland 2018...a recruitment agency to assist companies with recruiting...

24

Recruitment Agencies in Switzerland 2018 How they tick. What they do. How they see themselves in the future.

Transcript of Recruitment Agencies in Switzerland 2018...a recruitment agency to assist companies with recruiting...

Recruitment Agencies in Switzerland 2018How they tick.What they do.How they see themselves in the future.

2

Contents

Executive Summary 3

1. Profile of recruitment agency managers 41.1 Profile 41.2 Function at companies 51.3 Education 51.4 Managers’ motives 61.5 Risk behavior 7

2. The recruitment agencies’ corporate structure 82.1 Networkofbranchoffices,revenue,andapplicantpool 82.2 Personnelconsultantsemployed 92.3 Competitive situation 10

3. Recruitment agencies’ service offerings 11

4. Recruiting and customer acquisition in the staffing industry 13 4.1 Recruitingapplicants 134.2 Acquisition of corporate customers 15

5. Recruitment agencies in the age of digitalization 165.1 Goalsofthedigitalizationprojects 165.2 Stateofdigitalizationatrecruitmentagencies 175.3 Reasonsforthefailureofdigitalizationprojects 185.4 Whodigitizeshow? 19

6. Recruitment agencies look into the future 216.1 Theemploymentworld–todayandtomorrow 216.2 The future of the industry 22

Legalnotices 24

Description of methods

Onbehalfofswissstaffing,themarketresearchinstitutegfs-zürichinvited 308 recruitment agency excecutives to participate in a com-binedonlineandtelephonesurvey.ThesurveywasconductedinFall2018.129managerstookpartinthesurvey.Therefore,thereturnquotaforsurveysis42%,whichishighforavoluntarysurvey.swissstaffingwrotetothemanagersofallitsmembercompanies.1 In view of the high number of surveys returned and a response quota of approxi-mately17%acrosstheentireindustry,theresponsesarerepresentativeforthestaffingindustryinSwitzerland.2

1Thenumberofmanagersapproachedislessthanthetotalnumberofmembercom-paniessincesomemanagersbelongtoseveralrecruitmentagenciesinSwitzerland.Sometimes,theirbranchofficesrepresentalegallyindependentcompany. 2Asiscustomaryforsurveys,certaindistortionsoftheirrepresentativenaturecannotbeexcluded.Accordingtogeneralexperience,managersoflargecompanies,forexam-ple,participatelessoftenforreasonsoftime.Questionsaboutprofessionalethicsmayalsobemorepronouncedthanintheindustryoverall.

3

Executive Summary

Thestaffingindustryischaracterizedbysmallandmedium-sizedcompanies.82%oftheapproximately800recruitmentagenciesinSwitzerlandhavetotalrevenueoflessthanCHF20millionperyear.Atthree-quartersofthecompanies,managementisinthehandsoftheowner,whoispersonallyresponsibleforthesuccessandfailureofthecompany.WhetherownerorCEO,withthemanagementofacompany,themanagersarefulfillingtheirdreamofindependenceandtheystandbehindtheirserviceswithpassion:bringingpeopleseekingjobsandemployerstogethersothattheyfitperfectly.For85%or75%ofrespondents,itisimportantfortheirworkasmanagerofarecruitmentagencytoassistcompanieswithrecruitingandhelppeopleintheirsearchforjobs.

RecruitmentagenciesinSwitzerlandemployapproximately5,000personnelconsultants,whoplace340,000temporaryworkersinpaidjobseachyear.Bycontrast,publicemploymentofficeshave2,700employeesincludingadministrativepersonnel.Thisindicatesthatwithitspersonnelresourcesandplacementexpertise,thestaffingindustrymakesavaluablecontributiontotheexploitationofdomes-ticpotentialandthefunctionalityoftheSwissemploymentmarket–akeyfunctionthathasrecentlybeenthreatenedbyattemptsatpoliticalandsocialrestrictions.

Digitalizationadvancesthestaffingindustry.Strongcompetitionandtheprevalenceofmedium-sizedcompaniesmakecostlyinnovationsdifficult,soit‘snowonderthathighcostsarethemostfrequentreasonwhyadigitalizationprojectisnotimplemented.Nevertheless,approximately60%ofcompanieshaveinitiatedsuchaprojectinthelast5years.However,corecorporateprocessesaredigitalizedatonly49%ofcompanies.Despitethelowdegreeofdigitalization,compa-niesremaincompetitivebecausethepersonalcontactnetworkwithcompaniesandemployeesisthedecisivefactorforrecruitingandcustomeracquisition.Withincreasingdigitalization,itwillbecomeevermoredifficulttosucceedonthemarketwithouttechnicalinno-vations.

Asspecialistsintheperfectplacementofpersonnel,themanagersofstaffingcompanieshaveasenseofcurrentdevelopmentsintheemploymentmarket.Alothasbeenwritteninrecentyearsaboutafuturewithfewerjobsandincreasingunemployment.Themanagersofrecruitmentagenciesseethisdifferently:only22%believetherewillbeincreasingunemployment,17%intherentalandplacementofrobots.Accordingtostaffingindustryestimates,peoplewillstillplayacentralroleintomorrow’seconomy.Intheprocess,workersinSwitzerlandcanbesurethatinphasesofstructuralupheaval,therecruitmentagencieswillstandbytheirsidewiththeircoachingandplacementexpertise,asalsointimesofrecovery.

Dr.MariusOsterfeldDübendorf,January2018

4

1. Profileofrecruitmentagencymanagers

1.1. Profile

Whoarethepeopleattheapproximately800recruitmentagenciesinSwitzerland?Themanagerscomefromalloverthecountry.Thelan-guagedistributionamongswissstaffing’smemberscorrespondstothelanguagedistributionintheoverallpopulation.Thisalsoshowsthatwithregardtoitsmemberstructure,swissstaffingisanationalindustryassociation.

Onaverage,themanagersare49yearsoldandtheyhavebeenemployedintheindustryfor18years.Only17%ofthosesurveyedhavelessthan5years’industryexperience.Thus,themanagersofarecruitmentagencygenerallyhavemanyyears’experienceinthein-dustry and they can incorporate this expertise into the management oftheircompanies.

Witha78%share,themajorityofstaffingcompaniesaremanagedbyaman.Ascomparedtoallself-employedpeopleinSwitzerland,theshareofmeninmanagementisthusslightlyhigher.

Italian French German

Managers of recruitment agencies by mother tongue as compared to theoverallpopulationNumberofrespondents:129

Additionalsource:BFS,structuralcollection2015,2017

20%

40%

60%

80%

Recruitmentagencymanagers

Overall population

74%

21%

5%

67%

24%

9%100%

0%

Women Men

Managers of recruitment agencies by sex ascomparedtoallself-employed(withemployees)Numberofrespondents:129

Additionalsources:BFS,SAKE,annualvalues2016/Bergmann,H.etal.„BedeutungundPositionierungvonFraueninSchweizerKMU“,KMU-HSG,Universi-tätSt.Gallen,2014.

20%

40%

60%

80%

Recruitmentagencymanagers

Self-employedwithemployees

78%

22%

75%

25%

All self-employed

62%

38%

100%

0%

55-65years 40-54years 25-39years

Managers of recruitment agencies by ageascomparedtoallself-employedinSwitzerlandNumberofrespondents:129

Additionalsource:BFS,SAKE,annualvalues2016

20%

40%

60%

80%

Recruitmentagencymanagers

All self-employed

23%

50%

27%

21%

50%

29%

100%

0%

Managers of recruitment agencies according to their duration of employment in thestaffingindustryNumberofrespondents:129

30%

11

-20

yea

rs

21

-30

yea

rs

5-1

0 y

ears

up

to

5 y

ears

mo

re t

ha

n3

0 y

ears

10%

5%

15%

25%

35%

20%

32

%

15

%

29

%

17

%

7%

0%

5

1.2. Function at companies

74%ofthemanagersarealsotheowneroftheirrecruitmentagency.Theseowner-operatedcompaniesexemplifythesocialidealoftheentrepreneur,whodoesbusinessonhisownaccountandpersonallytendsthebusinessofhiscompany.Withtheirname,theownersrep-resentthesuccessesandfailuresoftheircompanyandbearrespon-sibilitypersonally.

Approximatelyone-quarteroftherecruitmentagenciesaremanagedbyaCEOwhoisentrustedwithmanagementbytheshareholders.Suchanorganizationalformisbeneficialforlargerrecruitmentagencies.HalfoftheoperationswithCEOshaveanetworkofthreeormorebranchofficesacrossSwitzerland.Forcompanieswithoneortwobranchoffices,thesharewithCEOisjust14%.TheincreasedmanagementcomplexityisanessentialreasonforentrustingthemanagementofalargercompanytoaCEO.Furthermore,thelocalbranchofficesofinternationalcorporategroupsaremanagedbyaCEO.Asexchange-listedcompanies,theyareinthespotlightandsubjecttostrictcomplianceregulationsandcorporatesocialrespon-sibility.

1.3. Education

Themanagersofarecruitmentagencygenerallyhaveaprofessionaleducation.One-quarterhavecompletedprofessionaltraining;anotherone-thirdhaveattainedadvancedprofessionaltraining.Thesefiguresreflectafrequently-reportedanecdotalcareerpathofpersonnelcon-sultants.Beforejoiningthestaffingindustry,manycompletetrainingintheindustryinwhichtheylaterworkaspersonnelconsultants.Thankstothisprofessionalbackground,theyareexpertatmakingcontactwithhiringcompanies,theyknowwhattheyaretalkingabout,andcanplacetherequestedworkersexpertly.

One-thirdofthemanagershaveearnedauniversitydegree.Ontheonehand,manymanagershaveacquiredthebusinessandlegalskillsformanagingacompanyinthecourseoftheirstudies.Ontheotherhand,thissharereflectsthedevelopmentoftheindustrytowardtheplace-mentofhighly-qualifiedworkers.PersonnelconsultantsingrowthsectorssuchasIT,finance&accounting,aswellaslifescience,pharma,andchemistryhavegenerallyearnedadegreeinthesesubjects.With-outthisqualification,theywouldnothavethespecializedknowledgerequiredfordiscussionswiththeresponsibleindividualsatthecompa-nies.

CEO Owner

Distribution of survey participants with respect to their function at the companyNumber of respondents: 108

74%

26%

Universitydegree Advancedprofessionaltraining Generaleducation Professionaltrainingincl.apprenticeship Compulsoryschool

Managers of recruitment agencies according to their highest educational attainmentNumberofrespondents:129

Additionalsource,SAKE,annualvalues2016

20%

Recruitmentagencymanagers

Resident population 25-65 years

40%

60%

80%

100%

25%

2%

6%

34%

33%

13%

38%

27%

14%

8%

0%

6

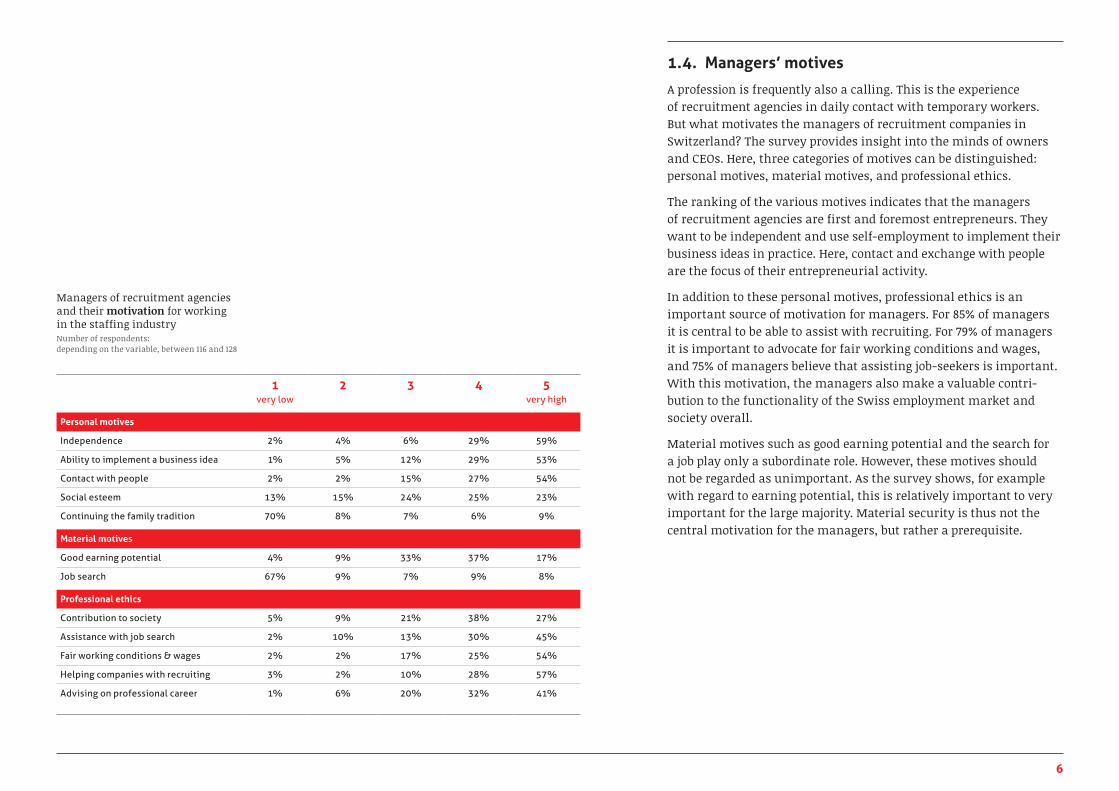

1.4. Managers’ motives

Aprofessionisfrequentlyalsoacalling.Thisistheexperience ofrecruitmentagenciesindailycontactwithtemporaryworkers. ButwhatmotivatesthemanagersofrecruitmentcompaniesinSwitzerland?ThesurveyprovidesinsightintothemindsofownersandCEOs.Here,threecategoriesofmotivescanbedistinguished:personalmotives,materialmotives,andprofessionalethics.

The ranking of the various motives indicates that the managers ofrecruitmentagenciesarefirstandforemostentrepreneurs.Theywanttobeindependentanduseself-employmenttoimplementtheirbusinessideasinpractice.Here,contactandexchangewithpeoplearethefocusoftheirentrepreneurialactivity.

Inadditiontothesepersonalmotives,professionalethicsisanimportantsourceofmotivationformanagers.For85%ofmanagersitiscentraltobeabletoassistwithrecruiting.For79%ofmanagersitisimportanttoadvocateforfairworkingconditionsandwages,and75%ofmanagersbelievethatassistingjob-seekersisimportant.Withthismotivation,themanagersalsomakeavaluablecontri-butiontothefunctionalityoftheSwissemploymentmarketandsocietyoverall.

Materialmotivessuchasgoodearningpotentialandthesearchforajobplayonlyasubordinaterole.However,thesemotivesshouldnotberegardedasunimportant.Asthesurveyshows,forexamplewithregardtoearningpotential,thisisrelativelyimportanttoveryimportantforthelargemajority.Materialsecurityisthusnotthecentralmotivationforthemanagers,butratheraprerequisite.

1very low

2 3 4 5very high

Personal motives

Independence 2% 4% 6% 29% 59%

Ability to implement a business idea 1% 5% 12% 29% 53%

Contact with people 2% 2% 15% 27% 54%

Social esteem 13% 15% 24% 25% 23%

Continuing the family tradition 70% 8% 7% 6% 9%

Material motives

Good earning potential 4% 9% 33% 37% 17%

Job search 67% 9% 7% 9% 8%

Professional ethics

Contribution to society 5% 9% 21% 38% 27%

Assistance with job search 2% 10% 13% 30% 45%

Fair working conditions & wages 2% 2% 17% 25% 54%

Helping companies with recruiting 3% 2% 10% 28% 57%

Advising on professional career 1% 6% 20% 32% 41%

Managers of recruitment agencies and their motivation for working inthestaffingindustryNumber of respondents: dependingonthevariable,between116and128

7

1.5. Risk behavior

Areadinesstoassumeriskisanindispensablepartofbeinganentrepreneur.Theassumptionofliabilitiesandmakingofbigin-vestmentsisfacedwithanuncertaincourseofbusiness.Therefore,it‘snowonderthatthemanagersofrecruitmentagenciesaremuchmorerisk-friendlythantheaverageSwiss.WhileintheSRF/ETHriskstudy2013,23%oftheSwisspopulationclaimedtoberisk-friendlyorveryrisk-friendly,atmorethan51%,thisfigureismorethantwiceashighamongthemanagers.Curiously,intheswissstaffingsurvey,only11%ofthemanagersclaimedtobeveryrisk-friendly.ThisshowsthattheownersandCEOshappilyassumerisks,butonlytoacertainextent.

5veryhigh 4 3 2 1verylow

The risk attitude of the managers of recruitment agencies as compared to theoverallpopulationNumberofrespondents:129

Additionalsource:SRF/ETHriskstudy2013.

0%

20%

Recruitmentagencymanagers

Swiss population

40%

60%

80%

100%

43%

6%

40%

11%

9%

26%

19%

4%

42%

20% 40% 60% 80% 100%

Continuing the family tradition

Job search

Social esteem

Good earning potential

Contribution to society

Advising on professional career

Assistance with job search

Ability to implement a business idea

Helping companies with recruiting

Independence

Fair working conditions & wages

Contact with people

0%

15%

65%

73%

75%

79%

81%

83%

85%

88%

17%

48%

54%

Ranking of the motives for working inthestaffingindustry Scalevalues4&5together

Number of respondents: dependingonthevariable,between116and128

8

2. The recruitment agencies’ corporate structure

2.1. Networkofbranchoffices, revenue,andapplicantpool

Thestaffingindustryischaracterizedbysmallandmedium-sizedcompanies.78%ofswissstaffing’smembercompanieshaveoneortwobranchoffices.7%ofthemembershavemorethan10locations.Assmallandmedium-sizedcompanies,therecruitmentagenciesarefirmlyrootedintheirregionsandtheyassistlocalcompanieswithshort-termpersonnelrequirements.

Thecorporateenvironmentinthestaffingindustry,whichischarac-terizedbysmallandmedium-sizedcompanies,isalsoevidentfromthedistributionofmembers’revenues.67%ofthecompaniessur-veyedhadrevenueoflessthanCHF10millionin2016.Hereitmustbeconsideredthattheserevenuefiguresincludewagepaymentstotemporaryworkersincludingallsocialinsurancecontributions.Overheadandpersonnelcosts,aswellasanymargin,representonlyafractionofthisrevenue.Incontrasttothesmallandmedium-sizedcompaniesarethelargeplayers.18%ofswissstaffing’smembersrecordedannualrevenueofmorethanCHF20millionin2016;theseincludetheSwisssubsidiariesoflargeinternationalstaffingcompa-nies.

Theheartofasuccessfulrecruitmentagencyisitsapplicantpool.Duetopersonnelrequirements,whichoftenariseonshortnotice,temporaryagenciescontinuallyrecruitnewapplicants.Thisallowsthemtoplacequalifiedworkersatthecompaniesthatneedthemwithindays.Forthelargemajorityofmembercompanies,thecan-didatepoolincludes1,000orfewerapplicants.14%ofmemberscanaccessmorethan10,000applicantsonshortnotice.

swissstaffingmembercompanies by their revenue Number of respondents: 120

5% 10% 15% 20% 25% 30%

2.5 to 5 million

1 to 2.5 million

up to 1 million

10 to 20 million

5 to 10 million

more than 20 million

0%

16%

27%

18%

18%

9%

12%

CHF

swissstaffingmembercompaniesbythesizeof their talent poolNumberofrespondents:129

10% 20% 30% 40% 50%

2500 to 5000

1000 to 2500

up to 1000

10000 to 15000

5000 to 10000

more than 15000

0%

2%

4%

12%

15%

25%

42%

size of talent pool

10% 20% 30% 40% 50% 60%

3 to 5

2

1

more than 10

6 to 10

0%

7%

5%

10%

18%

60%

number ofbranch offices

swissstaffing member companies bysizeoftheirbranch office networkNumberofrespondents:129

9

2.2. Personnel consultants employed

Short-termplacementofpersonnelisthecoreserviceofarecruit-mentagency.Despiteincreasingdigitalizationintheindustry,personnelconsultantsplayacentralroleinprovidingthisservice.58%ofswissstaffing’smembercompaniesemployupto5personnelconsultants.15%ofmembersemploymorethan10personnelcon-sultants.Atthelargestparticipatingcompany,thereare250.

At87%ofswissstaffing’smembercompanies,personnelconsultantsworkinofficeteamsofupto5people.Thissuggeststhatregardlessofthesizeofarecruitmentagency,theteamsaresmallandenableclose,personalcooperation.However,preciselybecausetheteamsaresmall,itiseasyforpersonnelconsultantstoloseperspectiveonthemarket,whichiswheremarketindicatorssuchastheSwissStaffingindexcomeintoplay.Inthevolatilestaffingindustry,theseindicatorsofferpersonnelconsultantsanimpressionofhowthecompanyorthebranchofficeisdevelopingascomparedtotheover-allmarket.

Startingwithanaveragenumberof5personnelconsultantspercompanyandtakingintoaccountthelargecompanies,giventhe800recruitmentagenciesinSwitzerland,itissafetoassumethatthereareatotalof5,000personnelconsultants.Incomparisontotheap-proximately2,700employeeswhoworkatpublicemploymentofficesaccordingtoSeco’sestimates,thesheernumberofpersonnelcon-sultantsinthestaffingindustryisnearlytwiceashighasinpublicpersonnelplacement.Thisshowsthatduetoitsextensivepersonnelresources,privatejobplacementmakesanimportantcontributiontotheexploitationofdomesticpotentialinSwitzerland.3

3Inthesurvey,therecruitmentagencieswereaskedexplicitlyaboutthenumberofpersonnelconsultants.IntheSecoreport“WirksamkeitundEffizienzderöffentlichenArbeitsvermittlung”[“Effectivenessandefficiencyofpublicworkplacement”],itisestimatedthereare2,700employeesatpublicemploymentoffices.Thisfigureincludestheadministrativepersonnelandisthusonlypartiallycomparabletothefiguresforthestaffingindustry.

1000 2000 3000 4000 5000

Public employmentoffice employees

Personnel consultantsat recruitment agencies

0

2700

5000 The estimated number of personnel consultants employed industry- wide ascomparedtoallpublicemploymentofficeemployeesNumberofrespondents:129

Additionalsource:Seco,«Wirk-samkeitundEffizienzderöffentli-chenArbeitsvermittlung,»2016

swissstaffingmemberscompanies by number of personnel consultants per branch officeNumberofrespondents:129

0% 5% 10% 15% 20% 25% 30%

3

2

1

more than 5

4 to 5

13%

21%

22%

29%

15%

Personnelconsultants

5% 10% 15% 20% 25% 30%

3 to 5

2

1

11 to 250

6 to 10

0%

15%

27%

29%

19%

10%

Personnelconsultants

swissstaffingmemberscompanies by the number of personnel consultants employedNumberofrespondents:129

10

2.3. Competitive situation

InSwitzerland,thestaffingindustryisacompetitivemarketwithmanyregionalandnationalactors.AccordingtofiguresfromtheSwissFederalStatisticalOffice,thereareapproximately800compa-nieswhosemainbusinessistemporaryemployeeplacement.Accord-ingtoswissstaffing’sestimates,thesixlargestrecruitmentagenciesaccountforamarketshareofjust25%.Thehighnumberofcompeti-torsandthelowmarketconcentrationspeakinfavorofstiffcompeti-tion.Addedtothis:providerchangesareeasilypossibleonthevolatiletemporary market and hiring companies can obtain comparative bids withoutalotofeffort.

swissstaffing’smembercompaniesregardthecompetitivesitua-tiononthemarketasintense.Two-thirdsofthemanagersspecifythatthecompetitionfortheircompaniesisstifforevenverystiff.One-quarterregardthemselvesassubjecttorelativelystrongcompet-itivepressure.Only8%ofthecompaniesare,accordingtostatementsbytheirmanagers,subjecttolittlecompetitivepressureandhavefoundanicheinordertoescapethecompetition,atleasttemporarily.Duetothecomparativelysmallscalingeffects 4,newcompetitorscanpenetrateaformernicherelativelyquickly.

4Here,scalingeffectsarecostbenefitsthatariseduetothecompany’ssize.Sincetheoperationofarecruitmentagencyrequireshardlyanymachinesorsuch,newentrantsandsmallrecruitmentagenciescanquicklybecomecompetitive.Servicessuchassalaryaccountingandspecialsoftwaresolutionsfortheindustrycanbepurchased.Onefinancialobstacleforestablishmentofarecruitmentagencyarethedepositsthatmustbemadewiththestateforthehiringpermit.

0% 5% 10% 15% 20% 35%25% 30%

3

2

4

very low competition 1

very high competition 5 33%

35%

24%

6%

2%

swissstaffingmembercompanies by the way their managers perceive the competitive situationNumberofrespondents:125

11

3. Recruitmentagencies’serviceofferings

Inthepast30years,thestaffingindustryhasundergoneenormouschange.Ifatthebeginningofthe1990sthemainbusinesswasplacingtemporaryemployees,anincreasingneedforflexibility,specializedworkers,anddigitalizationhaveresultedinfundamentalchange,whichisstillongoing.Outoftherecruitmentagencieshavecomestaff-ingcompaniesthatprovidetheircustomerswithextensiveHRservices.

Theindustry’sdevelopmentisreflectedintheservicesthatswissstaff-ing’smembercompaniesoffer.Nowasbefore,placementoftemporaryemployeesisthemembers’coreservice.98%ofthecompaniessurveyedofferthisservice.88%ofthecompaniesprovidepermanentjobplace-mentsasapartoftheirrangeofservices.Inadditiontothesetwocoreservices,withtry&hireandpayrolling,twomixedformsbetweentemporaryandpermanentjobplacementhavebeenestablished;theseareanunmistakablesignofthedevelopmentofrecruitmentagenciesintostaffingcompanies.

Inthecourseoftry&hire,acompanycaninitiallyemploysomebodytemporarilyforthreemonths,thenafterthisget-to-know-youphase,hiretheemployeeatthecompanywithoutaplacementfee.83%ofswissstaffing’smembercompaniescounttry&hireamongtheirser-vices.Withthisoffering,recruitmentagenciesarebuildingvaluablebridgestotheworldofwork.Inparticular,forapplicantswhowanttochangeindustries,whohavegapsintheirresumesorwhodonotyethavealltherequiredskills,try&hireopensupnewopportunitiesontheemploymentmarket.

0% 20% 40% 60% 100%80%

Try & Hire

Permanent job placement

Temporary work

Headhunting

Outplacement

RPO / MSP

Online platform

Payrolling

88%

83%

82%

33%

29%

21%

16%

98%

swissstaffingmembercompanieswith their service offerings, double-countingpossibleNumberofrespondents:125

No Yes

swissstaffingmember companies with supplier-function for a RPO/MSPNumber of respondents: 108

77%

23%

12

82%oftherecruitmentcompaniesoffertheircustomerspayrolling.Foraslimmargin,withthisservicetherecruitmentagencyassumesresponsibilityforpayingpartorallofacompany’sstaffandalsoaccountsforallsocialinsurancecontributions.Animportantbene-fitforcustomers:includedinthepackageareallHRservicesforthestaff,suchasassistinganemployeeincaseofillnessoraccident.Theexampleofpayrollingdemonstrateshowcompaniesintheindustryhavedevelopedintocomprehensivestaffingcompanies.

ThetworelativelynewservicesRecruitmentProcessOutsourcing(RPO)andManagedServiceProvision(MSP)arethefurtherlogicaldevelopmentofcomprehensivepersonnelconsulting.Approximately21%ofmembercompaniesareactiveinthissector.InthecourseofRPO,therecruitmentagencytakesoverparticularpartsofthere-cruitingprocess–forexample,pre-selectingincomingapplications,conductingtheinitialroundofinterviewsorcreatingassessmentcenters.Ifarecruitmentagencytakesovertheentiremanagementofacompany’sflexibleworkforce,theindustryspeaksofManagedServiceProvision(MSP).Thisfuture-orientedservicerepresentsthemostextensiveHRoutsourcingtoastaffingcompany.Fromthese-lectionoftherecruitmentagencytothefinalplacementofworkers,thestaffingcompanyisresponsibleforeachHRstepfortheflexibleworkforce.Whiletodaythereareonlyafewfull-serviceMSPsinSwitzerland,digitalizationwilllikelyreducethecostofthisserviceandmakeitmorefeasibleforcustomers.Thankstobothdevelop-ments,newcustomergroupsforthisserviceareanticipatedinthecomingyears.

Asspecialistsforpersonnelquestions,one-thirdoftherecruitmentagenciesassisttheircustomerswiththegreatestchallengesintheHRsector:theyactasheadhuntersfortheircustomers,searchingforrarespecialistsorassistingemployeeswhohavebeenletgowithoutplacementduringthesearchforanewjob,includingdetermina-tionoflocation,coaching,andplacementservices.

Inthefuture,onlineplatformsandcrowdsourcingwillbeenginesofjobdevelopmentandwilllikelyleveloutthepathtowardtheso-calledgigeconomy.Theword“gig”comesfromthemusicscene,whereartistsreceivetheirfeeafterashortappearanceinaclubandthencontinuetotheirnextcustomer.UberandAirbnbareexam-plesoftheseformsofwork.However,recruitmentagencieshavealreadyrecognizedthegrowthmarketofthegigeconomy.16%ofswissstaffing’smembercompaniesalreadyofferonlineplatformsforworkplacement.Theadvantageforpotentialemployees:thankstoplacementviaarecruitmentagency,theirsocialcontributionsarecompletelyensuredandtheyareprotectedbytheGAVPersonalverleih[CLAoftheSwissStaffingIndustry].

13

4. Recruiting and customer acquisition inthestaffingindustry

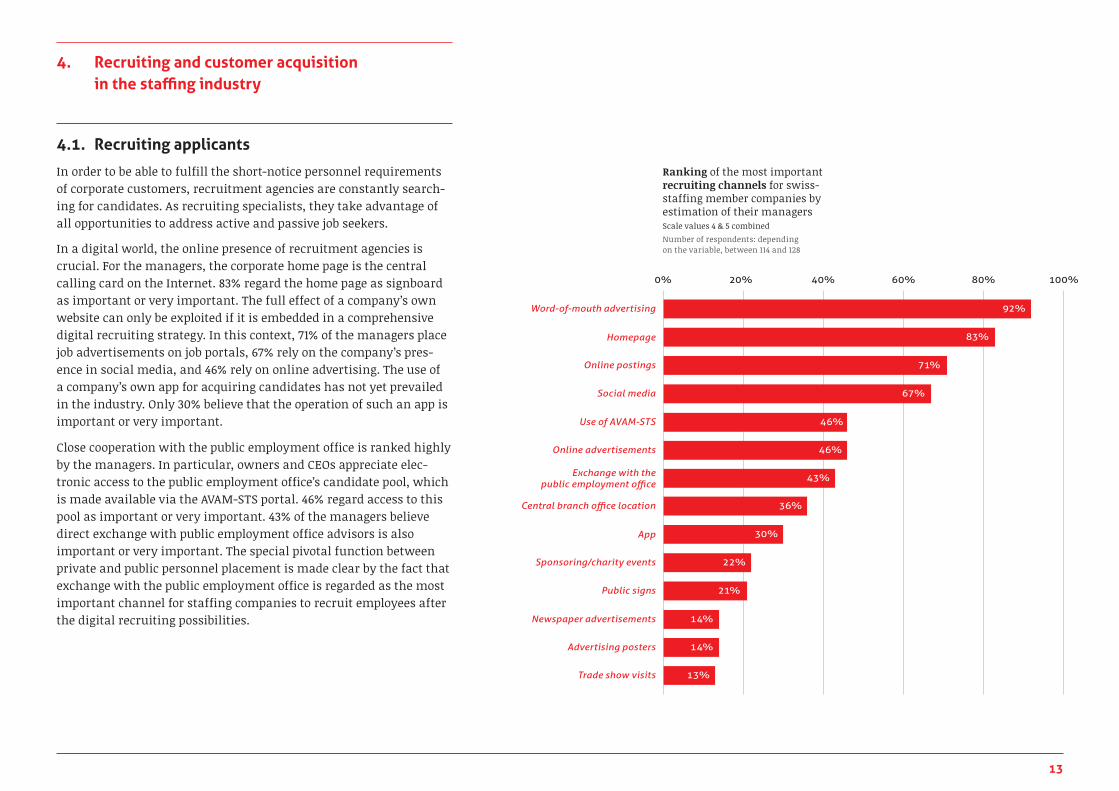

4.1. Recruiting applicants

Inordertobeabletofulfilltheshort-noticepersonnelrequirementsofcorporatecustomers,recruitmentagenciesareconstantlysearch-ingforcandidates.Asrecruitingspecialists,theytakeadvantageofallopportunitiestoaddressactiveandpassivejobseekers. Inadigitalworld,theonlinepresenceofrecruitmentagenciesiscrucial.Forthemanagers,thecorporatehomepageisthecentralcallingcardontheInternet.83%regardthehomepageassignboardasimportantorveryimportant.Thefulleffectofacompany’sownwebsitecanonlybeexploitedifitisembeddedinacomprehensivedigitalrecruitingstrategy.Inthiscontext,71%ofthemanagersplacejobadvertisementsonjobportals,67%relyonthecompany’spres-enceinsocialmedia,and46%relyononlineadvertising.Theuseofacompany’sownappforacquiringcandidateshasnotyetprevailedintheindustry.Only30%believethattheoperationofsuchanappisimportantorveryimportant.

Closecooperationwiththepublicemploymentofficeisrankedhighlybythemanagers.Inparticular,ownersandCEOsappreciateelec-tronicaccesstothepublicemploymentoffice’scandidatepool,whichismadeavailableviatheAVAM-STSportal.46%regardaccesstothispoolasimportantorveryimportant.43%ofthemanagersbelievedirectexchangewithpublicemploymentofficeadvisorsisalsoimportantorveryimportant.Thespecialpivotalfunctionbetweenprivateandpublicpersonnelplacementismadeclearbythefactthatexchangewiththepublicemploymentofficeisregardedasthemostimportantchannelforstaffingcompaniestorecruitemployeesafterthedigitalrecruitingpossibilities.

20% 40% 60% 80% 100%

Online postings

Homepage

Word-of-mouth advertising

Use of AVAM-STS

Social media

Online advertisements

Exchange with thepublic employment office

Sponsoring/charity events

App

Central branch office location

Newspaper advertisements

Public signs

Advertising posters

Trade show visits

0%

46%

67%

46%

43%

71%

83%

92%

14%

21%

14%

13%

22%

30%

36%

Ranking of the most important recruiting channels for swiss-staffingmembercompaniesbyestimation of their managers Scalevalues4&5combined

Number of respondents: depending onthevariable,between114and128

14

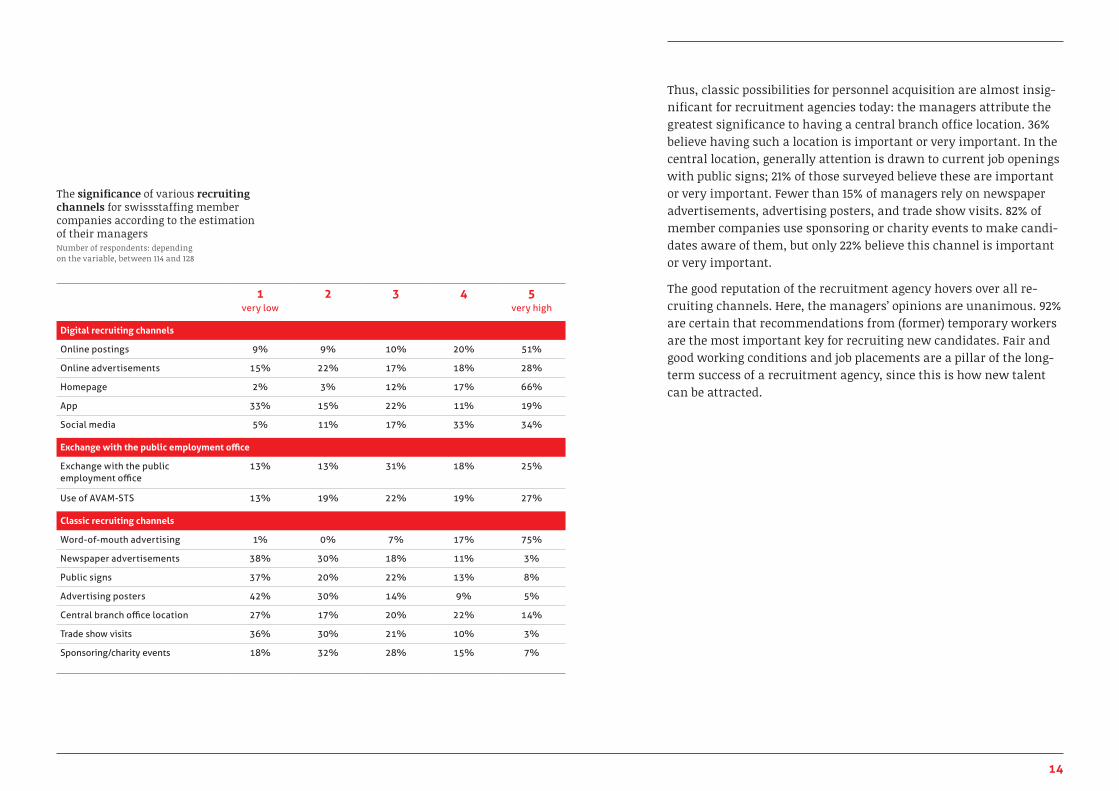

Thus,classicpossibilitiesforpersonnelacquisitionarealmostinsig-nificantforrecruitmentagenciestoday:themanagersattributethegreatestsignificancetohavingacentralbranchofficelocation.36%believehavingsuchalocationisimportantorveryimportant.Inthecentrallocation,generallyattentionisdrawntocurrentjobopeningswithpublicsigns;21%ofthosesurveyedbelievetheseareimportantorveryimportant.Fewerthan15%ofmanagersrelyonnewspaperadvertisements,advertisingposters,andtradeshowvisits.82%ofmember companies use sponsoring or charity events to make candi-datesawareofthem,butonly22%believethischannelisimportantorveryimportant.

Thegoodreputationoftherecruitmentagencyhoversoverallre-cruitingchannels.Here,themanagers’opinionsareunanimous.92%arecertainthatrecommendationsfrom(former)temporaryworkersarethemostimportantkeyforrecruitingnewcandidates.Fairandgoodworkingconditionsandjobplacementsareapillarofthelong-termsuccessofarecruitmentagency,sincethisishownewtalentcanbeattracted.

1very low

2 3 4 5very high

Digital recruiting channels

Online postings 9% 9% 10% 20% 51%

Online advertisements 15% 22% 17% 18% 28%

Homepage 2% 3% 12% 17% 66%

App 33% 15% 22% 11% 19%

Social media 5% 11% 17% 33% 34%

Exchangewiththepublicemploymentoffice

Exchange with the public employment office

13% 13% 31% 18% 25%

Use of AVAM-STS 13% 19% 22% 19% 27%

Classic recruiting channels

Word-of-mouth advertising 1% 0% 7% 17% 75%

Newspaper advertisements 38% 30% 18% 11% 3%

Public signs 37% 20% 22% 13% 8%

Advertising posters 42% 30% 14% 9% 5%

Central branch office location 27% 17% 20% 22% 14%

Trade show visits 36% 30% 21% 10% 3%

Sponsoring/charity events 18% 32% 28% 15% 7%

The significance of various recruiting channelsforswissstaffingmembercompanies according to the estimation of their managers Number of respondents: depending onthevariable,between114and128

15

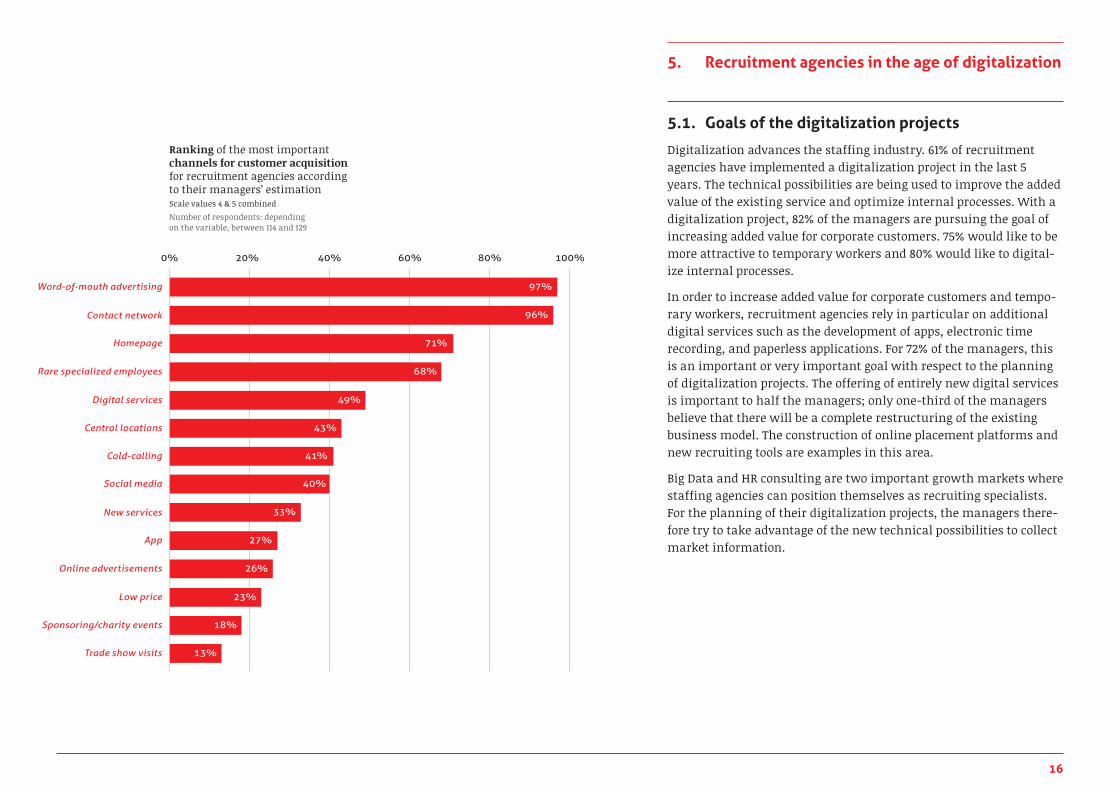

4.2. Acquisition of corporate customers

Accordingtothemanagers’estimation,recommendationsfromex-istingcustomersandthepersonalcontactnetworkarecrucialforac-quiringnewcorporatecustomers.For97or96%,thispathtoacquiringnewcustomersisimportantorveryimportant.ThisisfollowedbythehomepageascallingcardontheInternet(71%)andtheavailabilityofrarespecializedworkers(68%).

Inadditiontothesefourpossibilitiesfornewcustomeracquisition,themanagersrelyondifferentwaysofcomingintocontactwithnewcustomers.Manymanagersusethepossibilitiesofthedigitalworld.49%considerdigitalservicesimportantorveryimportantforcustomeracquisition.40%relyonadvertisingviasocialmedia,and27%or26%stilltrytopositionthemselvesonthemarketwithonlineadvertisingortheoperationofanapp.

Theindustryusesmanyclassicpathstomakecontactwithnewcorporatecustomers:one-thirdoftherecruitmentagenciestrytoap-proachpotentialbusinesspartnerswiththecompany’snewservices.For41%oftherecruitmentagencies,cold-callingcustomersplaysanimportantorveryimportantrole.43%believehavingabranchofficenearcustomersisimportant.Surprisingly,thisgeographicproximityappears to be more important for acquiring corporate customers than forrecruitingcandidates.

Onlyslightvaluewasascribedtosponsoring,charityevents,andtradeshowvisits.Fewerthan20%ofthemanagersbelievetheseareimportantorveryimportant.Interestingly,pricealsodoesnotseemtobethedecisiveelementforcustomeracquisition.Justone-quarterofthemanagersbelievethisisimportantorveryimportant.Giventhestiffcompetitiononthestaffingmarket,thisinsightinitiallyseemssurprising.Ontheotherhand,itshowsthat,givenstiffcompetition,thecompaniesmustdistinguishthemselvesfromtheircompetitorsthroughcharacteristicsotherthanprice.

1very low

2 3 4 5very high

Digital services

Homepage 2% 8% 19% 27% 44%

Digital services 14% 11% 26% 23% 26%

Social media 10% 20% 29% 24% 16%

Online advertisements 24% 21% 29% 16% 10%

App 34% 21% 18% 12% 15%

Productdifferentiation

New services 24% 19% 24% 20% 13%

Rare specialized employees 7% 8% 17% 27% 41%

Low price 17% 22% 39% 15% 7%

Classic methods of customer advertising

Contact network 0% 0% 4% 12% 84%

Word-of-mouth advertising 0% 0% 3% 16% 81%

Cold-calling 19% 13% 27% 21% 20%

Trade show visits 35% 25% 27% 7% 6%

Sponsoring/charity events 24% 31% 27% 8% 10%

Central locations 22% 14% 20% 26% 18%

The significance of various channels for customer acquisition by recruitment agencies according to their managers’ estimates Number of respondents: depending onthevariable,between114and129

16

5. Recruitment agencies in the age of digitalization

5.1. Goals of the digitalization projects

Digitalizationadvancesthestaffingindustry.61%ofrecruitmentagencieshaveimplementedadigitalizationprojectinthelast5years.Thetechnicalpossibilitiesarebeingusedtoimprovetheaddedvalueoftheexistingserviceandoptimizeinternalprocesses.Withadigitalizationproject,82%ofthemanagersarepursuingthegoalofincreasingaddedvalueforcorporatecustomers.75%wouldliketobemoreattractivetotemporaryworkersand80%wouldliketodigital-izeinternalprocesses.

Inordertoincreaseaddedvalueforcorporatecustomersandtempo-raryworkers,recruitmentagenciesrelyinparticularonadditionaldigitalservicessuchasthedevelopmentofapps,electronictimerecording,andpaperlessapplications.For72%ofthemanagers,thisisanimportantorveryimportantgoalwithrespecttotheplanningofdigitalizationprojects.Theofferingofentirelynewdigitalservicesisimportanttohalfthemanagers;onlyone-thirdofthemanagersbelievethattherewillbeacompleterestructuringoftheexistingbusinessmodel.Theconstructionofonlineplacementplatformsandnewrecruitingtoolsareexamplesinthisarea.

BigDataandHRconsultingaretwoimportantgrowthmarketswherestaffingagenciescanpositionthemselvesasrecruitingspecialists.Fortheplanningoftheirdigitalizationprojects,themanagersthere-foretrytotakeadvantageofthenewtechnicalpossibilitiestocollectmarketinformation.

20% 40% 60% 80% 100%

Homepage

Contact network

Word-of-mouth advertising

Digital services

Rare specialized employees

Central locations

Cold-calling

App

New services

Social media

Low price

Online advertisements

Sponsoring/charity events

Trade show visits

0%

49%

68%

43%

41%

71%

96%

97%

23%

26%

18%

13%

27%

33%

40%

Ranking of the most important channels for customer acquisition for recruitment agencies according to their managers’ estimation Scalevalues4&5combined

Number of respondents: depending onthevariable,between114and129

17

5.2. State of digitalization at recruitment agencies

Inthecomplexworldoftheemploymentmarket,thesymbiosisofhumanandmachineatrecruitmentagenciesisareality.Themain-tenanceofpersonalcontactsandtheperfectmatchingofcandidateandopenjobrequirespersonnelconsultants;theirroleaslisteners,coaches,andserviceproviderscanhardlybeautomated.Ontheotherhand,computerscanhelppersonnelconsultantswiththeirdailywork.AnexampleisawagesystemthatmapsthecomplexSwissem-ploymentmarketwithallgenerally-applicablecollectivebargainingagreements.Withmostindustrysoftwareprograms,itiscurrentlynotpossibletoprintanemploymentcontractthatdoesnotcomplywithSwissemploymentlaw.

Theinterplayofhumanandmachineisreflectedinthemanagers’re-sponsesabouttheirdegreeofdigitalization.At60%ofcompanies,fre-quentmanualentriesinthecomputersystemarenecessary.Personalcontact with hiring companies and temporary workers is of great significanceto95%ofrespondents.Withrespecttodigitalinfrastruc-ture,58%ofrecruitmentagenciesarenetworkedwithoneanotherviavarioussoftwaresystems.Athalfofthecompanies,thecorecorporateprocessesarelargelyautomated.

Thepictureismixedwithrespecttodataevaluation.Whileongoingbusinessismonitoredinrealtimeat60%oftherecruitmentagencies,thedigitalpossibilitiesforobtainingregularemployeeandcustomerfeedbackareusedbyjust40%ofthecompanies.

20% 40% 60% 80% 100%

Increase added value of the service for temporary workers

Make internal processes more efficient

Increase added value for hiring companies

Market information

Additional digital services

New digital services

Restructuring ofthe business model

0%

66%

72%

51%

33%

75%

80%

82%

Ranking of the most important goals for digitalization projects for recruitment agencies according to the estimation of their managers Scalevalues4&5combined

Number of respondents: dependingonthevariable,between117and122

1very low

2 3 4 5very high

Provision of new services

New digital services 7% 16% 26% 29% 22%

Additional digital services 1% 7% 20% 40% 32%

Restructuring of the business model 14% 22% 31% 26% 7%

Market information 2% 11% 21% 37% 29%

Improvement of the service quality

Increase added value of personnel placement for hiring companies

2% 2% 14% 39% 43%

Increase added value of personnel placement for temporary workers

2% 8% 15% 38% 37%

Make internal processes more efficient

0% 8% 12% 26% 54%

The significance of various goals for digi-talization projects for recruitment agencies according to their managers’ estimation Number of respondents: depending onthevariable,between117and122

18

5.3. Reasons for the failure of digitalization projects

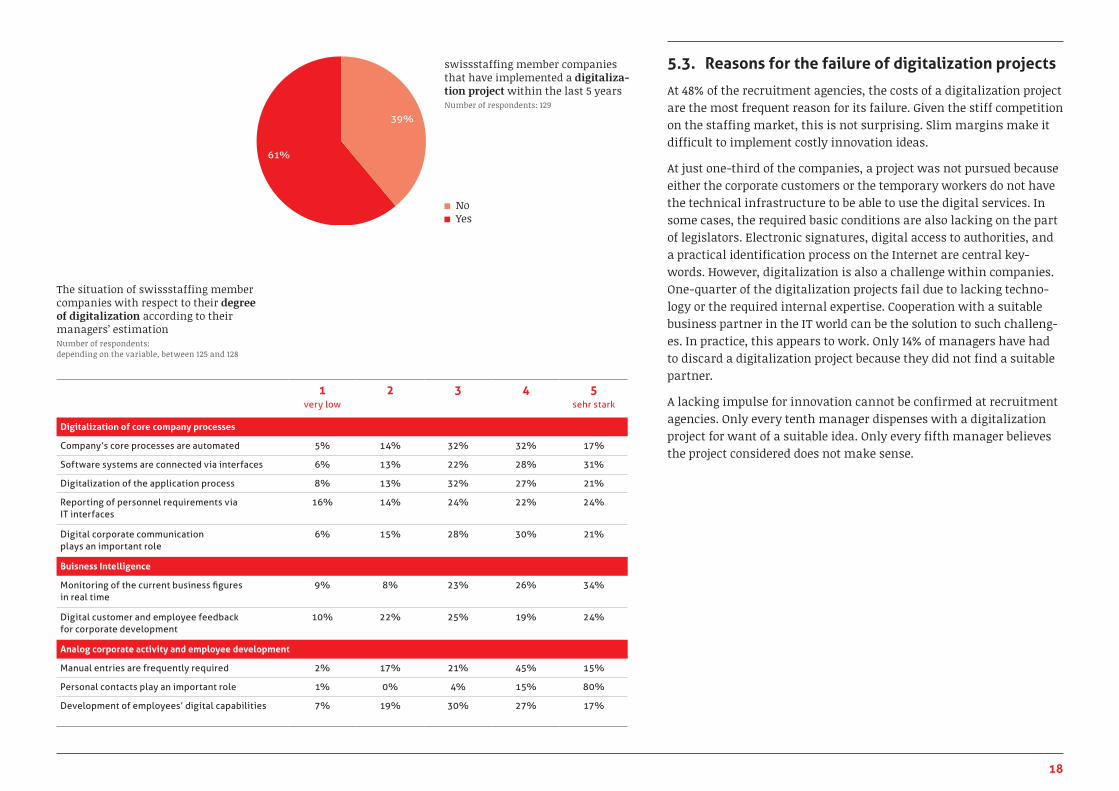

At48%oftherecruitmentagencies,thecostsofadigitalizationprojectarethemostfrequentreasonforitsfailure.Giventhestiffcompetitiononthestaffingmarket,thisisnotsurprising.Slimmarginsmakeitdifficulttoimplementcostlyinnovationideas.

Atjustone-thirdofthecompanies,aprojectwasnotpursuedbecauseeither the corporate customers or the temporary workers do not have thetechnicalinfrastructuretobeabletousethedigitalservices.Insomecases,therequiredbasicconditionsarealsolackingonthepartoflegislators.Electronicsignatures,digitalaccesstoauthorities,andapracticalidentificationprocessontheInternetarecentralkey-words.However,digitalizationisalsoachallengewithincompanies.One-quarterofthedigitalizationprojectsfailduetolackingtechno-logyortherequiredinternalexpertise.CooperationwithasuitablebusinesspartnerintheITworldcanbethesolutiontosuchchalleng-es.Inpractice,thisappearstowork.Only14%ofmanagershavehadtodiscardadigitalizationprojectbecausetheydidnotfindasuitablepartner.

Alackingimpulseforinnovationcannotbeconfirmedatrecruitmentagencies.Onlyeverytenthmanagerdispenseswithadigitalizationprojectforwantofasuitableidea.Onlyeveryfifthmanagerbelievestheprojectconsidereddoesnotmakesense.

No Yes

swissstaffingmembercompaniesthathaveimplementedadigitaliza-tion projectwithinthelast5yearsNumberofrespondents:129

39%

61%

1very low

2 3 4 5sehr stark

Digitalization of core company processes

Company’s core processes are automated 5% 14% 32% 32% 17%

Software systems are connected via interfaces 6% 13% 22% 28% 31%

Digitalization of the application process 8% 13% 32% 27% 21%

Reporting of personnel requirements via IT interfaces

16% 14% 24% 22% 24%

Digital corporate communication plays an important role

6% 15% 28% 30% 21%

Buisness Intelligence

Monitoring of the current business figures in real time

9% 8% 23% 26% 34%

Digital customer and employee feedback for corporate development

10% 22% 25% 19% 24%

Analog corporate activity and employee development

Manual entries are frequently required 2% 17% 21% 45% 15%

Personal contacts play an important role 1% 0% 4% 15% 80%

Development of employees’ digital capabilities 7% 19% 30% 27% 17%

Thesituationofswissstaffingmembercompanies with respect to their degree of digitalization according to their managers’ estimation Number of respondents: dependingonthevariable,between125and128

19

5.4. Who digitizes how?

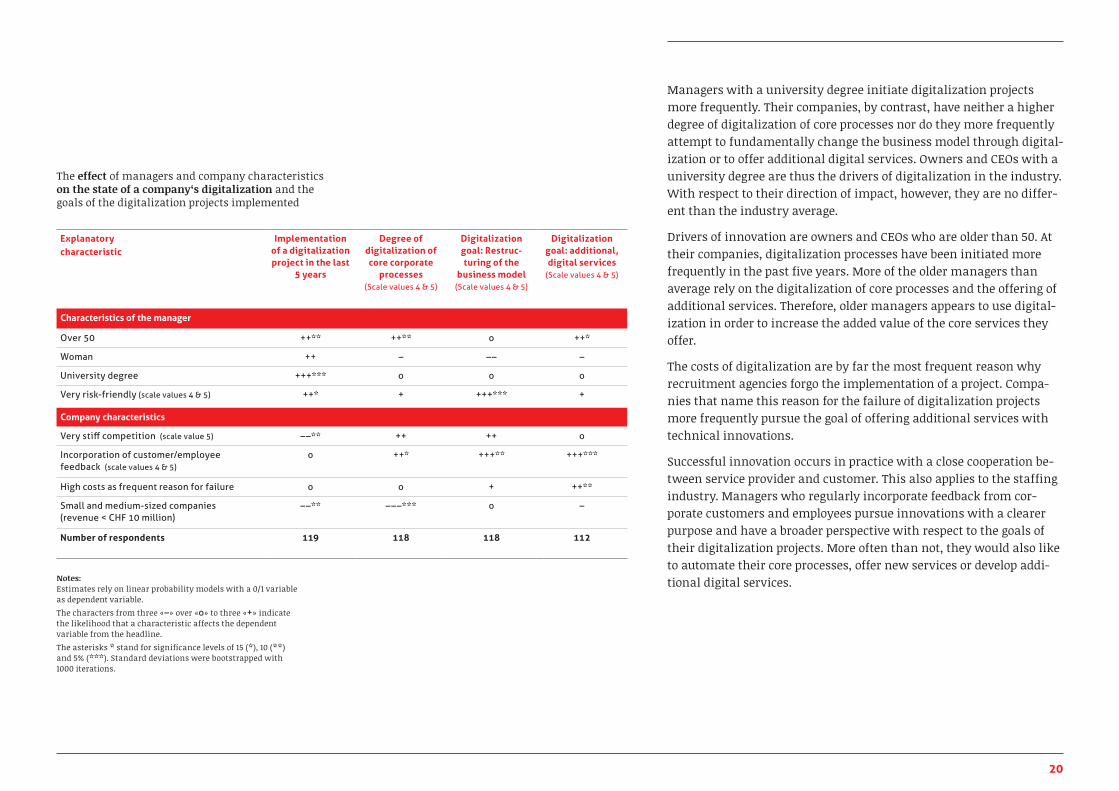

Economicmethodsprovideamorepreciselookatthesurvey’sdata.Inordertobetterunderstandtheinnovationdynamicintheindustry,itisworthwhiletotakeanotherlookandunderstandwhichmanage-mentinnovationsadvancewhichgoal(s).5

61%oftherecruitmentagencieshaveimplementedadigitalizationprojectattheircompanyinthelast5years.Amorepreciseanalysisshowsthatwithrisk-friendlymanagers,itwasmuchmorelikelythattheyimplementedadigitalizationproject.Inaddition,therisk-friend-lymanagersmorefrequentlypursuedthegoalofestablishingnewbusinessmodels.Therefore,itisalsotrueinthestaffingindustrythatrisk-friendlyentrepreneursareimportantinnovatorswhoadvancetheeconomyandtheindustry.

Digitalizationisachallengeforsmallandmedium-sizedcompanies.Inthelastfiveyears,theyinitiateddigitalizationprojectsmuchlessoften.Giventhisbackground,themuchlowerdegreeofdigitaliza-tionofcorecorporateprocessesishardlysurprising.Processesaredigitalizedatsmallandmedium-sizedcompaniesmuchlessoftenthanatlargerrecruitmentagencieswithrevenueofmorethanCHF10million.Especiallychallengedarecompaniesthatalsobelievetheyaresubjecttostiffcompetitivepressure.Lackingprofitsmaketheimplementationofcostlyprojectsthatcouldmakethecompanyfitforthefuturemoredifficult.

5Fromhereon,onlyinfluenceswillbediscussedthathaveastatisticallysignificantinfluencewithacertaintyofatleast15%.Withtheotherinfluences,itcannotbeexclud-edwithsufficientcertaintythattheydonotariseduetoaccidentalfluctuationsinthedataset.

10% 20% 30% 40% 50%

Lacking technology

Lacking infrastructure

High costs

Not a sensible project

Lacking expertise

Lacking partner

No innovation idea

0%

20%

23%

14%

9%

25%

31%

48%

Ranking of the most important reasons for the failure of digitalization projects for recruitment agencies by their managers’ estimation Scalevalues4&5combined

Numberofrespondents:129

20

Managerswithauniversitydegreeinitiatedigitalizationprojectsmorefrequently.Theircompanies,bycontrast,haveneitherahigherdegreeofdigitalizationofcoreprocessesnordotheymorefrequentlyattempttofundamentallychangethebusinessmodelthroughdigital-izationortoofferadditionaldigitalservices.OwnersandCEOswithauniversitydegreearethusthedriversofdigitalizationintheindustry.Withrespecttotheirdirectionofimpact,however,theyarenodiffer-entthantheindustryaverage.

DriversofinnovationareownersandCEOswhoareolderthan50.Attheircompanies,digitalizationprocesseshavebeeninitiatedmorefrequentlyinthepastfiveyears.Moreoftheoldermanagersthanaveragerelyonthedigitalizationofcoreprocessesandtheofferingofadditionalservices.Therefore,oldermanagersappearstousedigital-izationinordertoincreasetheaddedvalueofthecoreservicestheyoffer.

Thecostsofdigitalizationarebyfarthemostfrequentreasonwhyrecruitmentagenciesforgotheimplementationofaproject.Compa-niesthatnamethisreasonforthefailureofdigitalizationprojectsmorefrequentlypursuethegoalofofferingadditionalserviceswithtechnicalinnovations.

Successfulinnovationoccursinpracticewithaclosecooperationbe-tweenserviceproviderandcustomer.Thisalsoappliestothestaffingindustry.Managerswhoregularlyincorporatefeedbackfromcor-poratecustomersandemployeespursueinnovationswithaclearerpurposeandhaveabroaderperspectivewithrespecttothegoalsoftheirdigitalizationprojects.Moreoftenthannot,theywouldalsoliketoautomatetheircoreprocesses,offernewservicesordevelopaddi-tionaldigitalservices.

The effect of managers and company characteristics on the state of a company‘s digitalization and the goalsofthedigitalizationprojectsimplemented

Notes: Estimatesrelyonlinearprobabilitymodelswitha0/1variableasdependentvariable.

The characters from three «–»over«o»tothree«+»indicatethelikelihoodthatacharacteristicaffectsthedependentvariablefromtheheadline.

The asterisks *standforsignificancelevelsof15 (*),10 (**)and5%(***).Standarddeviationswerebootstrappedwith1000iterations.

Explanatorycharacteristic

Implementation of a digitalization project in the last

5 years

Degree of digitalization of core corporate

processes(Scale values 4 & 5)

Digitalization goal: Restruc-turing of the

business model(Scale values 4 & 5)

Digitalization goal:additional,digital services

(Scale values 4 & 5)

Characteristics of the manager

Over 50 ++** ++** o ++*

Woman ++ – –– –

University degree +++*** o o o

Very risk-friendly (scale values 4 & 5) ++* + +++*** +

Company characteristics

Very stiff competition (scale value 5) ––** ++ ++ o

Incorporation of customer/employee feedback (scale values 4 & 5)

o ++* +++** +++***

High costs as frequent reason for failure o o + ++**

Small and medium-sized companies (revenue < CHF 10 million)

––** –––*** o –

Number of respondents 119 118 118 112

21

6. Recruitment agencies look into the future

6.1. The employment world – today and tomorrow

Withaviewtothefuture,themanagersofrecruitmentagenciesallagree:theybelieveinpeopleandtheirabilitytowork.Despiteallthegloomypredictionsoffutureresearchersandpoliticiansofvariousstripes,only22%arecountingonalong-termincreaseinunemploy-ment.Only17%believethatrecruitmentagencieswillrentrobotsinthefuture.However,fromthemanagers’pointofview,theemploy-mentworldwillneverthelesschange.75%ofthosesurveyedbelievethatflexibleworkinSwitzerlandwillincrease.And40%expectthattraditionalemploymentrelationshipswillincreasinglybereplacedbycontractrelationships.CrowdsourcingandthegigeconomyinthesenseofUberandAirbnbarecentralkeywords. Inthiscontext,thequestionmustbeposedtowhatextentthegigeconomyhasalreadybecomerealityinthestaffingindustry.At40%ofmembercompanies,onlyone-quarteroftheplacementsorfewerarebrief–uptofourweeks.Atanother30%ofmembercompanies,theshareofbriefplacementsisbetween25and50%.Thefiguresshowthatthemajorityofplacementsareforlongerperiods.However,briefplacementsinthesenseofthegigeconomyarealreadybeinghandledwithtemporarywork.Incontrasttoothernewbusinessmodelsandformsofwork,establishedtemporaryworkoffersthefullprotectionofsocialinsuranceandthepersonnelplacementcollectivebargainingagreementwithsimultaneousflexibility.

20%10% 30% 50%40% 60% 70% 80%

Digital services are acompetitive advantage

The significance ofHR consulting will increase

Flexible work will increase

The traditional employment relationshipwill be replaced by the contract relationship

The staffing industry will bechanged by digitalization

Personnel consultants will be digitalized

Unemployment will increase

Recruitment agencies will place/rent robots in the future

0%

40%

48%

25%

22%

17%

49%

61%

75%

Ranking of the most important future employment market developments in the estimation of the managers of recruitment agenciesScalevalues4&5combined

Number of respondents: dependingonthevariable,between117and125

20%10% 30% 40%

50 to 75% of placements with a duration of less than 4 weeks

25 to 50% of placements with a duration of less than 4 weeks

0 to 25% of placements with a duration of less than 4 weeks

75 to 100% of placements with a duration of less than 4 weeks

0%

13%

16%

30%

40%

Share of the short-term placements of less than 4 weeksamongswissstaffingmembercompaniesaccordingtodetailsfromtheirmanagersExample of how to read the first line: At40%ofswissstaffingmembercompanies,theshareofshort-termplacementsofupto4weeksislessthan25%.

Numberofrespondents:129

22

6.2. The future of the industry

There is a difference of opinion among managers about the future of theindustry.48%ofthosesurveyedassumethatdigitalizationwillchangetheindustry.Thusitisnotsurprisingthateveryotherper-sonseesafuturecompetitiveadvantageindigitalservices.However,accordingtothemanagers’estimation,therewillnotbeacompleterevolution.Onlyeveryfourthpersonbelievesinacompletedigitali-zationofpersonnelconsulting.ApossiblereasonforthisresultmightbethatthemanagersanticipateasharpincreaseinHRconsulting,anareainwhichexpertpersonnelconsultantswillplayakeyrolenowasbefore.

Interesting is a more precise examination of which managers think howaboutthefutureoftheindustry.6Managerswhoarerisk-friendlybelievemorefrequentlythanaverageincompetitiveadvantagesduetodigitalservices.Otherwise,therearehardlyanystatisticallysig-nificantdistinctionsbetweenthemanagerswithrespecttotheothercharacteristics.Thisalsoapplieswithaviewtoarevolutionofthestaffingindustryandtheincreaseofcontractrelationships.Memberswhoregardthemselvesassubjecttostiffcompetitionfromtheircom-petitorsbelieveinsharpchangesinbothoftheseareas.Furthermore,risk-friendlymanagersbelieveespeciallyfrequentlyinasignificantincreaseincontractrelationshipsontheemploymentmarket.

6Fromhereon,onlyinfluenceswillbediscussedthathaveastatisticallysignificantinfluencewithacertaintyofatleast15%.Withtheotherinfluences,itcannotbeexclud-edwithsufficientcertaintythattheydonotariseduetoaccidentalfluctuationsinthedataset.

1very low

2 3 4 5very high

The future of the employment market

Unemployment will increase 22% 24% 32% 15% 7%

The traditional employment relation-ship will be replaced by the contract relationship

3% 22% 35% 32% 8%

Flexible work will increase 2% 4% 19% 42% 33%

Recruitment agencies will place/rent robots in the future

42% 25% 16% 12% 5%

The future of the industry

The staffing industry will be changed by digitalization

8% 16% 28% 25% 23%

Personnel consultants will be digitalized 22% 28% 25% 20% 5%

Digital services are a competitive advantage

5% 14% 32% 26% 23%

The significance of HR consulting will increase

0% 14% 25% 36% 25%

The view of the future from the point of view of the manager of swissstaffingmembercompanies Number of respondents: dependingonthevariable,between117and125

23

WithregardtotheincreasingsignificanceofHRconsulting,therearesignificantdifferencesamongmembercompanies.ManagersofsmallcompanieswithrevenueoflessthanCHF10millionbelievelessfrequentlyinthefutureofHRconsulting.Thisalsoappliesforcom-paniesforwhichhighcostsarethereasonforthefailureofdigitali-zationprojects.ThesefigurescanbeunderstoodasanindicationthattheintroductionofservicesintheHRconsultingsectorisespeciallydifficultforsmallcompanies,andinsomecasesassociatedwithhighcosts.Whenfacedwithdigitalization,onereasonmaybethatBigDatawillbeakeytoolinHRconsulting,whichiscomplextouseandespeciallyapplicableatlargecompanies. Furthermore,themanagersoverage50believemorestronglyinafutureofHRconsulting,asdothosecompanieswhereincorporationofcustomerandemployeefeedbackistakenseriously.ThelatterishardlysurprisingsincethesystematicobtainingoffeedbackisabasicprerequisiteforentryintoprofessionalHRconsulting.

The effect of managers’ and companies’ cha-racteristics on the managers’ opinion with regardtofutureindustrydevelopment

Notes: Estimatesrelyonlinearprobabilitymodelswitha0/1variableasdependentvariable.

The characters from three «–»over«o»tothree«+»indicatethelikelihoodthatacharacteristicaffectsthedependentvariablefromtheheadline.

The asterisks *standforsignificancelevelsof15 (*),10 (**)and5%(***).Standarddeviationswerebootstrappedwith1000iterations.

Explanatorycharacteristic

Revolution ofthestaffing

industry

Increase: Contract

relationship

Competitive advantage:

Digital service

Increase: HR consulting

Characteristics of the manager

Over 50 o o + ++**

Woman - – ++ o

University degree ++ o ++ –

Very risk-friendly (scale values 4 & 5) ++ +++*** +++*** +

Company characteristics

Very stiff competition (scale value 5) +++*** +++** o ++*

Incorporation of customer/employee feedback (scale values 4 & 5

o + o ++*

High costs as frequent reason for failure o o o ––**

Small and medium-sized companies (revenue < CHF 10 million)

–– o –– ––***

Number of respondents 102 107 108 105

24

Legal notices

swissstaffingSwiss Association of Recruitment AgenciesStettbachstrasse 10CH-8600DübendorfTel:+41(0)[email protected]

SurveyThecombinedonlineandtelephonesurveywasconductedby gfs-zürich.

Editorial staffDr.rer.pol.MariusOsterfeld,Economist,swissstaffing

InformationDr.MariusOsterfeld,Economist,[email protected]

TranslationDr.LindaL.Gaus,MadDocsLLC

DesignAndreaChanteiroGmünder,feinformgrafikwww.feinform.ch

Documentavailableatwww.swissstaffing.chReprinting,alsoinexcerpt,permittedwithindicationofsource.©swissstaffingPublishedinMarch2018

byswissstaffing,theSwissassociationof Recruitment Agencies

www.swissstaffing.ch

swissstaffingStettbachstrasse 10CH-8600Dübendorf