RECORDS, RETURNS AND BONDS UNDER CENTRAL EXCISE. INTRODUCTION Excise records include all the records...

31

RECORDS, RETURNS AND BONDS UNDER CENTRAL EXCISE

-

Upload

jaydon-haugh -

Category

Documents

-

view

224 -

download

0

Transcript of RECORDS, RETURNS AND BONDS UNDER CENTRAL EXCISE. INTRODUCTION Excise records include all the records...

RECORDS, RETURNS AND BONDS UNDER CENTRAL

EXCISE

INTRODUCTION

Excise records include all the records prepared or maintained by the assessee for recording and reporting of transactions with regard to receipt, purchase, manufacture, storage, sale or delivery of the goods including inputs and capital goods. All accounts, agreements, invoices, price-lists, returns, statement or any other source document, whether in writing or even in electronic form is treated as Records.

CLASSIFICATION

Excise records can be classified into two categories–

(1) Mandatory records– Maintaining mandatory records are essential and compulsory under Excise Act failure to do so invites action.

(2) Discretionary– These are to be followed generally. Tribunals may take lenient view in case of lapse in following discretionary procedure. Whether a particular procedure is mandatory or discretionary- there can not be any fast and hard rule. It is upto tribunal to decide the category.

The records under Excise duty are broadly divided into two categories—

(a) Statutory records– Prior to 1.4.2000, Central Excise Rules 1944 had prescribed a number of statutory records to be maintained and submitted by assessee.

(b) Private records– While framing Central Excise Rules 2002, Cenvat Credit Rules, 2004 and other rules issued recently, the government has continued with the policy of relying more and more on private records of assessee.

The record maintainance for purchasing finished goods can be understood in a systematic way after studying basic excise procedures.

The private records relevant for Central Excise including the Daily Stock Account maintained in compliance with the provisions of said Rules shall necessarily be kept in the factory to which they pertain.

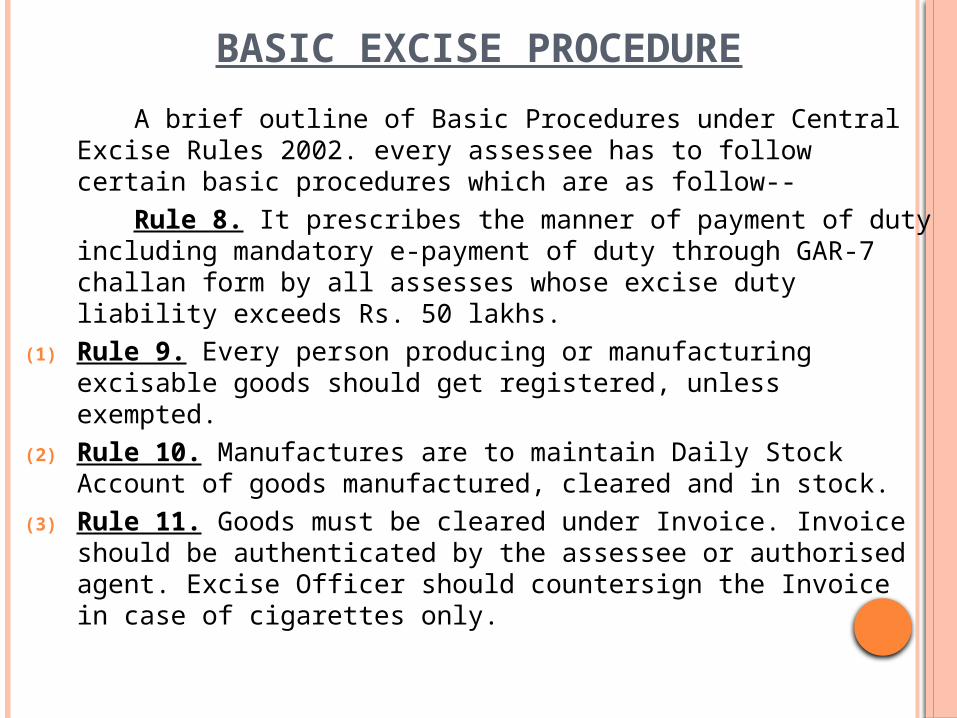

BASIC EXCISE PROCEDURE

A brief outline of Basic Procedures under Central Excise Rules 2002. every assessee has to follow certain basic procedures which are as follow--

Rule 8. It prescribes the manner of payment of duty including mandatory e-payment of duty through GAR-7 challan form by all assesses whose excise duty liability exceeds Rs. 50 lakhs.

(1) Rule 9. Every person producing or manufacturing excisable goods should get registered, unless exempted.

(2) Rule 10. Manufactures are to maintain Daily Stock Account of goods manufactured, cleared and in stock.

(3) Rule 11. Goods must be cleared under Invoice. Invoice should be authenticated by the assessee or authorised agent. Excise Officer should countersign the Invoice in case of cigarettes only.

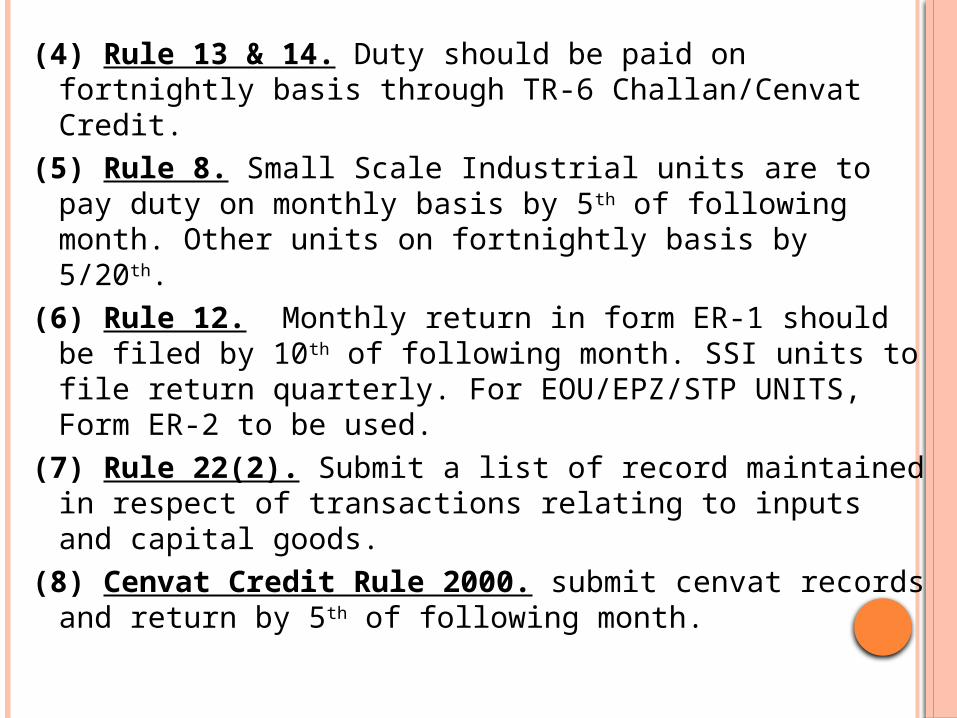

(4) Rule 13 & 14. Duty should be paid on fortnightly basis through TR-6 Challan/Cenvat Credit.

(5) Rule 8. Small Scale Industrial units are to pay duty on monthly basis by 5th of following month. Other units on fortnightly basis by 5/20th.

(6) Rule 12. Monthly return in form ER-1 should be filed by 10th of following month. SSI units to file return quarterly. For EOU/EPZ/STP UNITS, Form ER-2 to be used.

(7) Rule 22(2). Submit a list of record maintained in respect of transactions relating to inputs and capital goods.

(8) Cenvat Credit Rule 2000. submit cenvat records and return by 5th of following month.

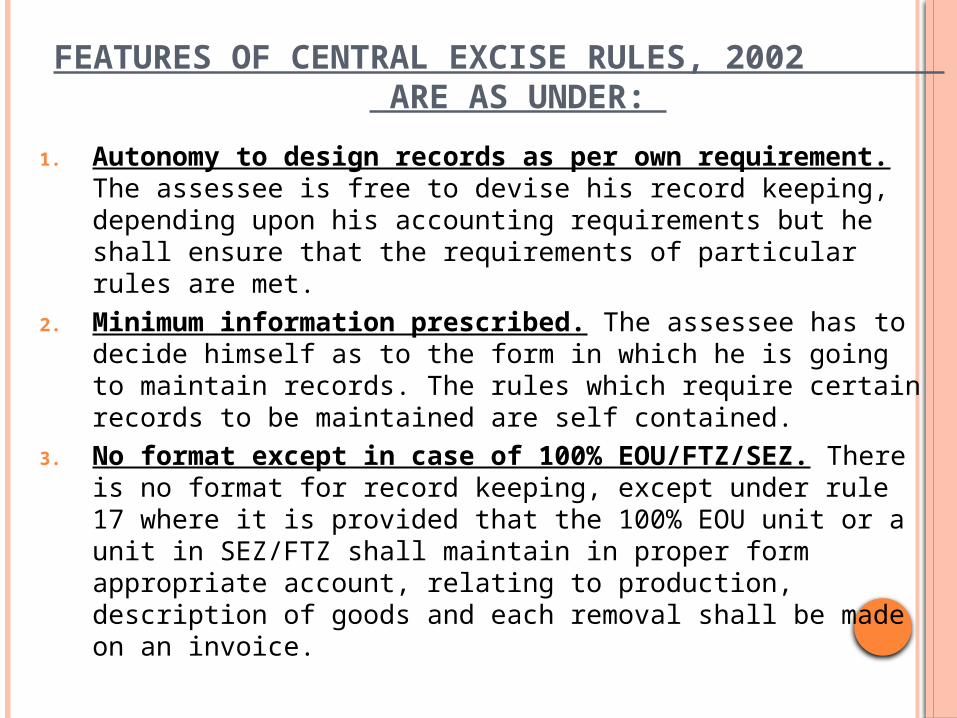

FEATURES OF CENTRAL EXCISE RULES, 2002 ARE AS UNDER:

1. Autonomy to design records as per own requirement. The assessee is free to devise his record keeping, depending upon his accounting requirements but he shall ensure that the requirements of particular rules are met.

2. Minimum information prescribed. The assessee has to decide himself as to the form in which he is going to maintain records. The rules which require certain records to be maintained are self contained.

3. No format except in case of 100% EOU/FTZ/SEZ. There is no format for record keeping, except under rule 17 where it is provided that the 100% EOU unit or a unit in SEZ/FTZ shall maintain in proper form appropriate account, relating to production, description of goods and each removal shall be made on an invoice.

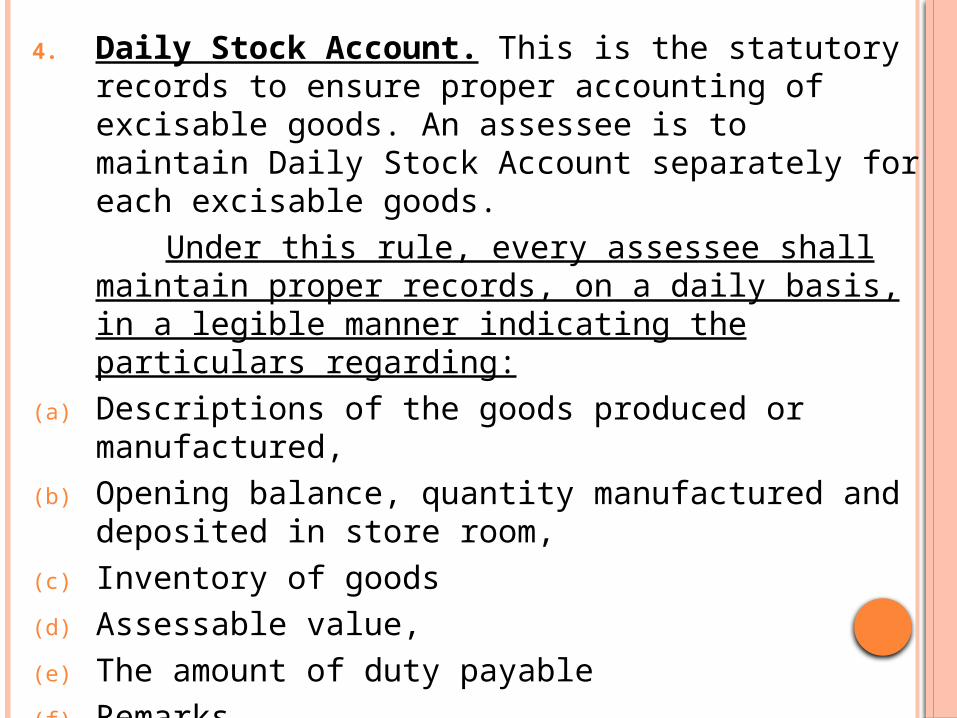

4. Daily Stock Account. This is the statutory records to ensure proper accounting of excisable goods. An assessee is to maintain Daily Stock Account separately for each excisable goods.

Under this rule, every assessee shall maintain proper records, on a daily basis, in a legible manner indicating the particulars regarding:

(a) Descriptions of the goods produced or manufactured,

(b) Opening balance, quantity manufactured and deposited in store room,

(c) Inventory of goods(d) Assessable value,(e) The amount of duty payable(f) Remarks.

5. Compulsory to maintain private records. Every assessee has to compulsorily maintain private records.

6. Authentication by assessee himself. The private records shall be authenticated on the first and last page by the assessee himself in the same manner as Daily Stock Account.

7. Submission of list of records. Every assessee is statutorily required to furnish to the Range Officer, a list in duplicate, of all records prepared or maintained by him for accounting of transaction.

8. Produce records on demand. Every assessee is under an obligation to produce on demand, to the Range Officer duly empowered by Commissioner or the audit party deputed by the Commissioner or the Comptroller and Audit General of India.

ELECTRONIC MAINTENANCE OF RECORDS

Features:(1) No need of special permission. No specific

permission from the Central Excise Department is required for electronic maintenance of records.

(2) Electronically readable form. The records, returns and documents should be in electronically readable format.

(3) Back up records. The person must ensure that proper back up records are also maintained and preserved so that in the event of destruction due to unavoidable accidents or natural causes, the information can be restored.

(4) Recording in “Scrutiny Register”. The department will record in “Scrutiny Register” or any other record indicating a person’s profile the fact that such person is electronically maintaining records using computer.

(5) Production of records. It shall be upon a person maintaining electronic records, to produce, on demand, the relevant records, returns or documents, in hard copy or in tapes or floppies or cartridges or compact disk or any other media in an electronically readable form.

(6) Audit trail and inter linkage. He shall also provide account of the audit trail and inter linkages including the source documents, whether paper or electronic, and the financial accounts record layout, data dictionary and explanation for codes used.

INVOICE

Invoice has replaced gate pass as a clearance document from 1.4.04. the invoice must be serially numbered and in bound form. The invoice is the manufacturer’s own document and pre-authentication by an authorized officer is not required.

features:(1) Removal only on invoice. Central Excise Rules, 2002

provides that no excisable goods can be removed from a factory or a warehouse except under an invoice signed by the owner of the factory.

(2) Serially numbered invoice. The invoice shall be serially numbered shall contain the registration number, description, classification and the duty payable thereon.

(3) Number of invoice copies. (a) the original copy to be marked as ORIGINAL FOR

BUYER;(b) the duplicate copy to be marked as DUPLICATE FOR

TRANSPORTER;(c) the triplicate copy to be marked as TRIPLICATE FOR

ASSESSEE.(4) Number of invoice book. Rule 11 provides that

only one invoice book shall be in used at a time, unless otherwise allowed by the Deputy commissioner of Central Excise in the special facts and circumstances of each case.

(5) Cancellation of invoices. As per the board’s guidelines, when an assessee is compelled to cancel invoice, the following actions should be taken:

a. Intimation of a cancelled invoice should be sent to Range Superintendent on the same date;

b. The original copy of cancelled invoice should be sent. And triplicate copy should be retained by the assessee.

RETURNS

Monthly/Quarterly Returns. Rule 12 provides that every assessee shall submit to the Superintendent of Central Excise a monthly return in proper form of production and removal of goods and other relevant particulars, within ten days after the close of the month to which the return relates.

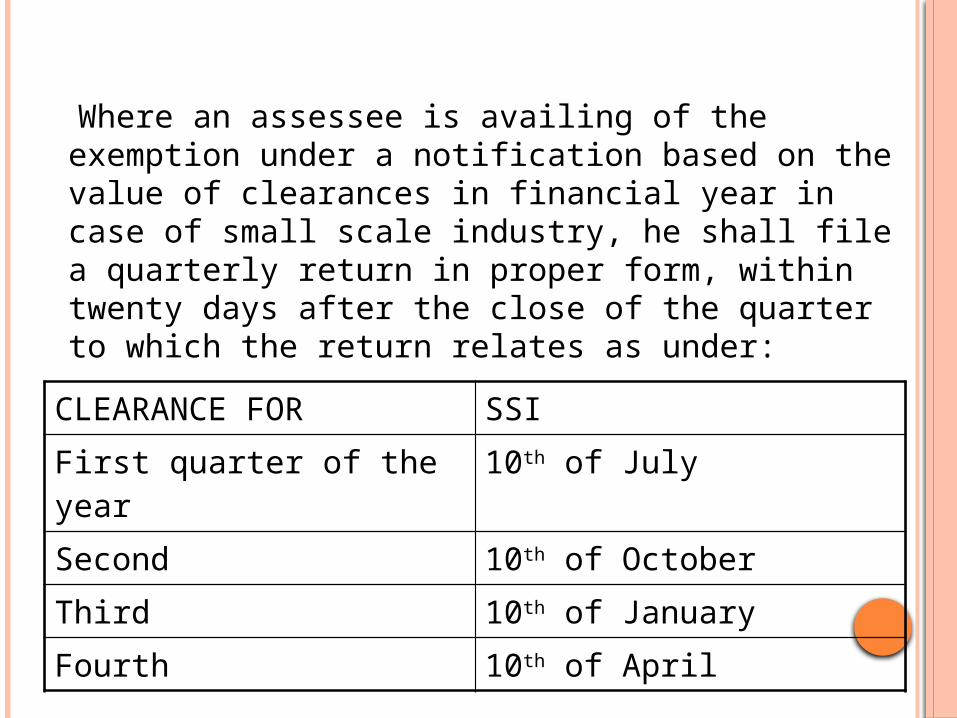

Where an assessee is availing of the exemption

under a notification based on the value of clearances in financial year in case of small scale industry, he shall file a quarterly return in proper form, within twenty days after the close of the quarter to which the return relates as under:

CLEARANCE FOR SSI

First quarter of the year 10th of July

Second 10th of October

Third 10th of January

Fourth 10th of April

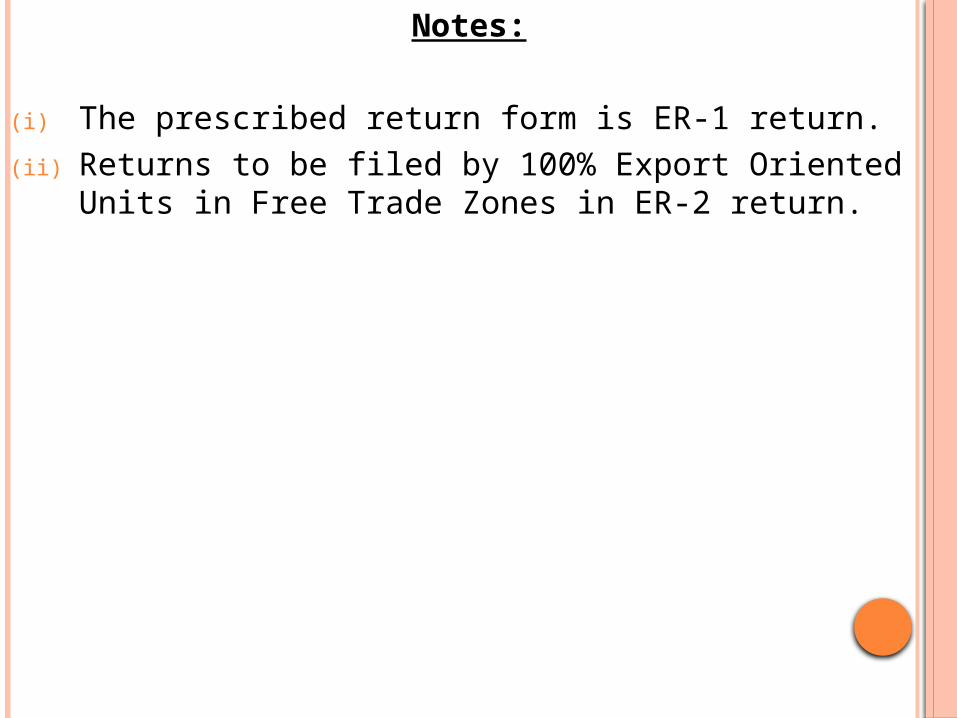

Notes:

(i) The prescribed return form is ER-1 return.(ii) Returns to be filed by 100% Export Oriented Units in

Free Trade Zones in ER-2 return.

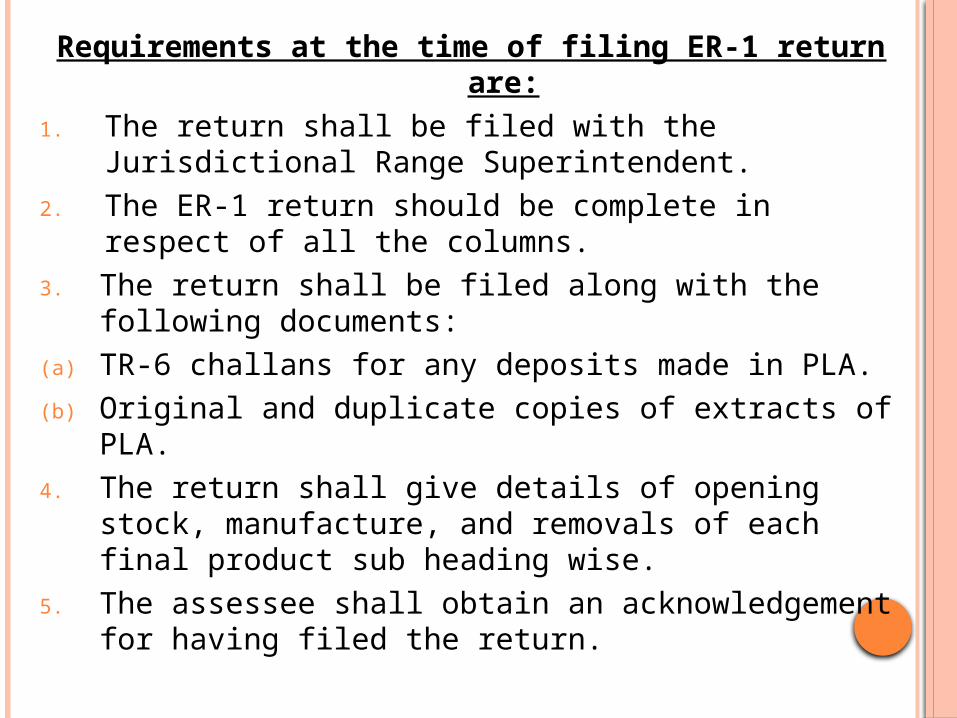

Requirements at the time of filing ER-1 return are:

1. The return shall be filed with the Jurisdictional Range Superintendent.

2. The ER-1 return should be complete in respect of all the columns.

3. The return shall be filed along with the following documents:

(a) TR-6 challans for any deposits made in PLA.(b) Original and duplicate copies of extracts of PLA.4. The return shall give details of opening stock,

manufacture, and removals of each final product sub heading wise.

5. The assessee shall obtain an acknowledgement for having filed the return.

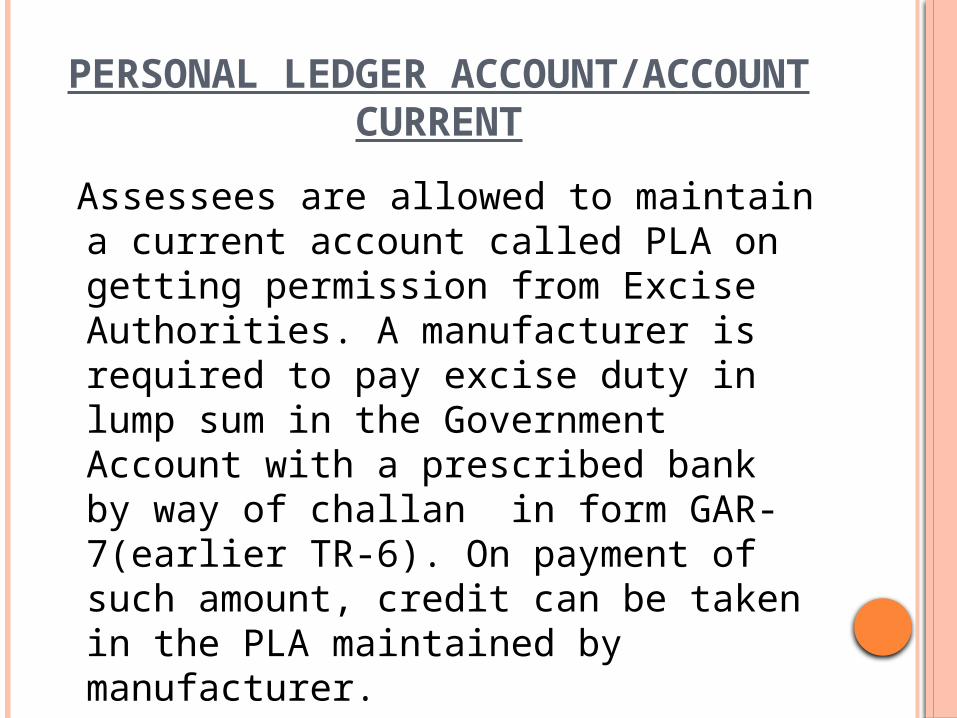

PERSONAL LEDGER ACCOUNT/ACCOUNT CURRENT

Assessees are allowed to maintain a current account called PLA on getting permission from Excise Authorities. A manufacturer is required to pay excise duty in lump sum in the Government Account with a prescribed bank by way of challan in form GAR-7(earlier TR-6). On payment of such amount, credit can be taken in the PLA maintained by manufacturer.

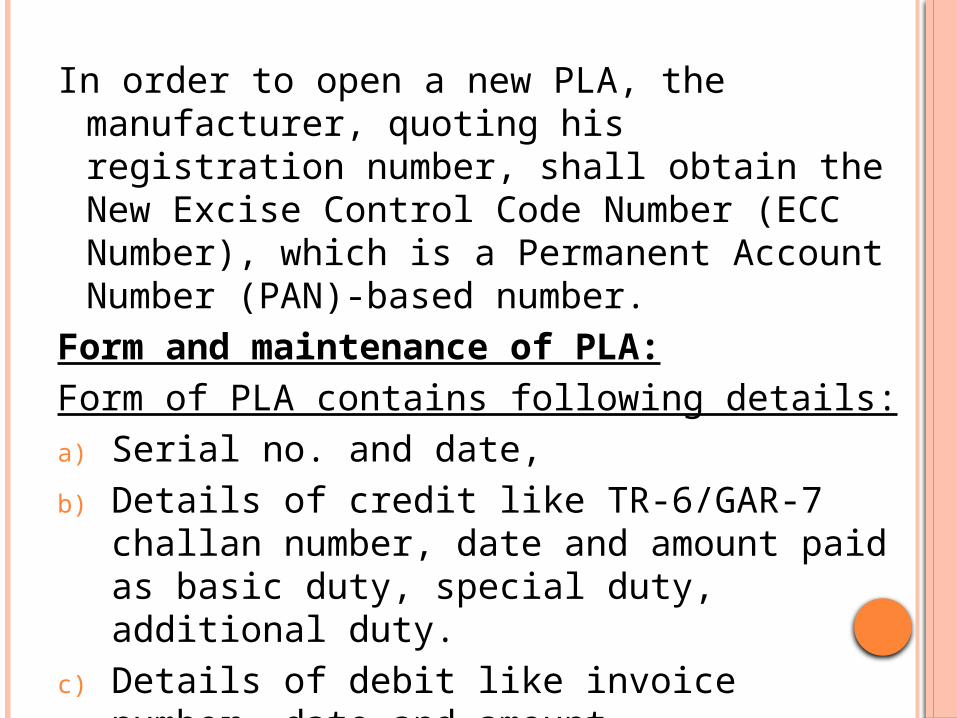

In order to open a new PLA, the manufacturer, quoting his registration number, shall obtain the New Excise Control Code Number (ECC Number), which is a Permanent Account Number (PAN)-based number.

Form and maintenance of PLA:Form of PLA contains following details:a) Serial no. and date,b) Details of credit like TR-6/GAR-7 challan

number, date and amount paid as basic duty, special duty, additional duty.

c) Details of debit like invoice number, date and amount,

d) Balance

Maintenance Of PLA:PLA must be maintained in triplicate using

indelible pencil and both sided carbon.Assessee manufacturers are required to

maintain separate PLA for each chapter. The assessee may transfer credit balance in one PLA to another.

BONDS UNDER CENTRAL EXCISE

Bond is an instrument by which the obligation to pay the money is created expressly. It is also a legal agreement and a collateral security. The primary purpose of the bond is to secure due compliance with the rules and procedures laid down under the Excise Law.

Types of bonds:Bonds are of two types: Surety Bond Security Bond.

Surety Bond: Surety Bonds are covered under the provisions of Contract Act. Under a surety bond, another person stands as surety to guarantee the performance on the part of obligor. Surety should be of full value of bond and the person standing as a surety should be solvent to the extent of the bond amount. A company can stand as surety for another company.

Surety can at any time revoke the surety but such revocation can be only prospective and cannot affect the past transactions.

Security Bond: Security Bonds are executed where security is offered instead of guarantee. Security can be in nature of Post Office Saving Deposit, National Saving Certificate, or similar realisable Government papers of Central or State Government. Bank deposit receipt of large scheduled banks is also acceptable. Security can also be furnished by cash deposit.

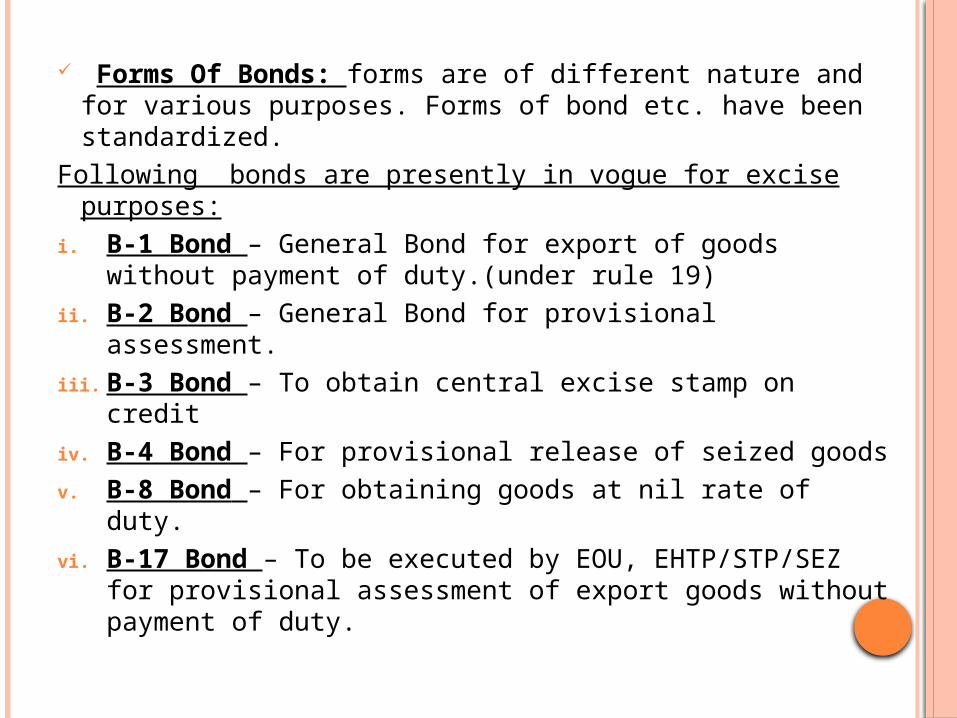

Forms Of Bonds: forms are of different nature and for various purposes. Forms of bond etc. have been standardized.

Following bonds are presently in vogue for excise purposes:

i. B-1 Bond – General Bond for export of goods without payment of duty.(under rule 19)

ii. B-2 Bond – General Bond for provisional assessment.

iii. B-3 Bond – To obtain central excise stamp on creditiv. B-4 Bond – For provisional release of seized goodsv. B-8 Bond – For obtaining goods at nil rate of duty.vi. B-17 Bond – To be executed by EOU, EHTP/STP/SEZ

for provisional assessment of export goods without payment of duty.

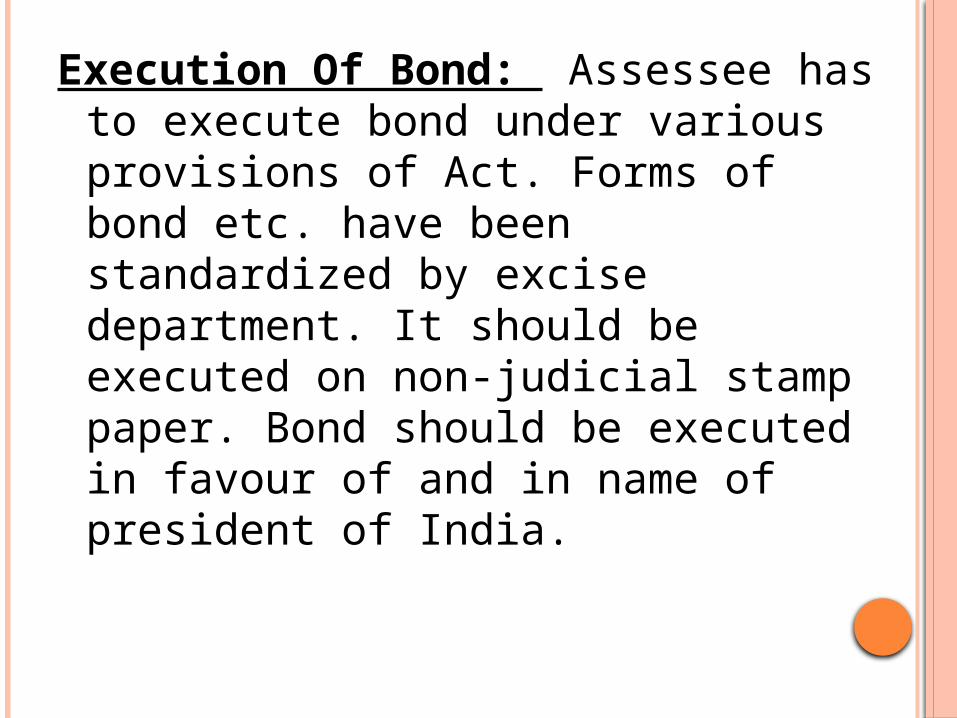

Execution Of Bond: Assessee has to execute bond under various provisions of Act. Forms of bond etc. have been standardized by excise department. It should be executed on non-judicial stamp paper. Bond should be executed in favour of and in name of president of India.

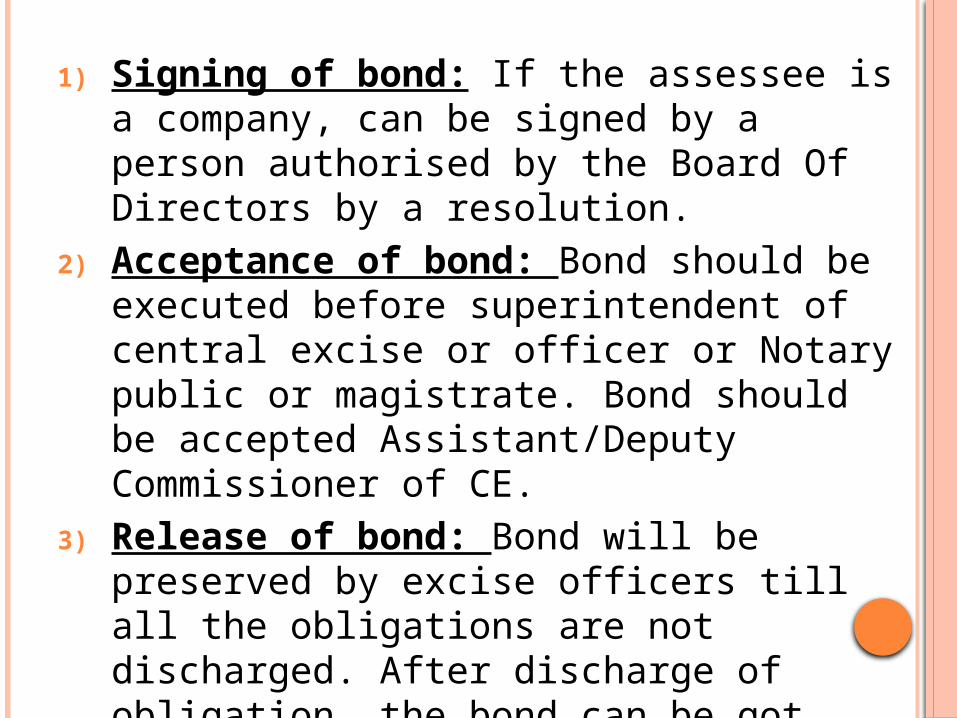

1) Signing of bond: If the assessee is a company, can be signed by a person authorised by the Board Of Directors by a resolution.

2) Acceptance of bond: Bond should be executed before superintendent of central excise or officer or Notary public or magistrate. Bond should be accepted Assistant/Deputy Commissioner of CE.

3) Release of bond: Bond will be preserved by excise officers till all the obligations are not discharged. After discharge of obligation, the bond can be got released.

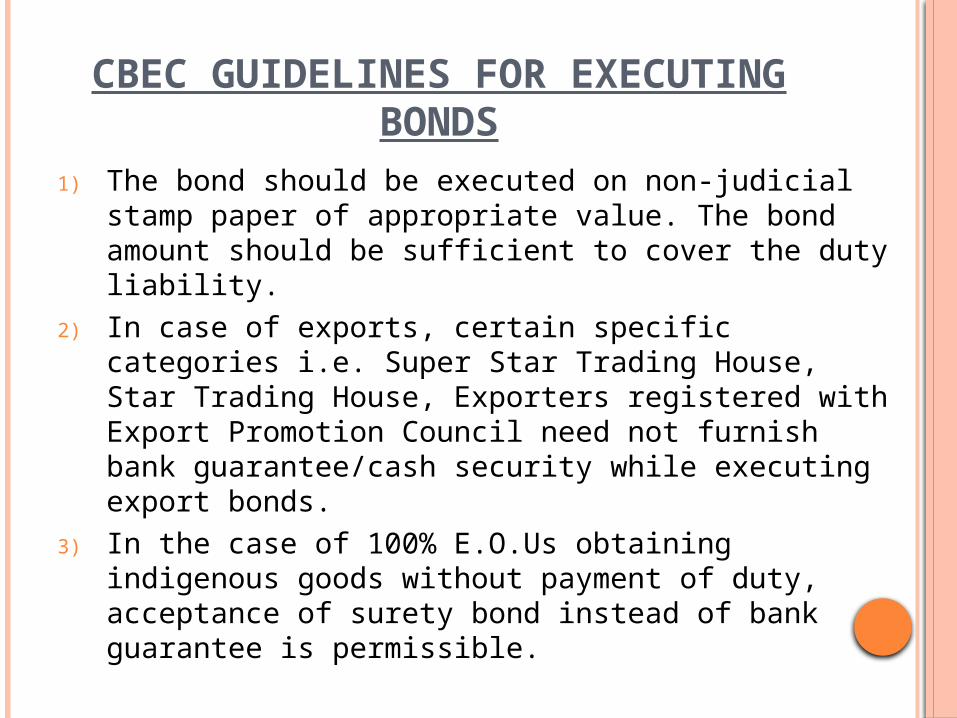

CBEC GUIDELINES FOR EXECUTING BONDS

1) The bond should be executed on non-judicial stamp paper of appropriate value. The bond amount should be sufficient to cover the duty liability.

2) In case of exports, certain specific categories i.e. Super Star Trading House, Star Trading House, Exporters registered with Export Promotion Council need not furnish bank guarantee/cash security while executing export bonds.

3) In the case of 100% E.O.Us obtaining indigenous goods without payment of duty, acceptance of surety bond instead of bank guarantee is permissible.

4) Bonds for provisional assessment is required.

5) Stamps on Bond: All Bonds must bear stamps on the scale prescribed by article 37 of schedule 1 of the Indian Stamp Act, 1899, modified as may be, by State Legislation.

6) Execution of bond by Government Undertaking or Autonomous Corporations: Every Undertaking owned and managed directly through any ministry, directorate or directorates by the Central Government is exempt from the execution of any bond.

7) Security: Security can be in nature of cash, Bank deposit, Government Promissory Notes, Post Office Saving Deposit, National Saving Certificate, or similar realisable Government papers of Central or State Government.

8) Surety: Under a surety bond, another person stands as surety to guarantee the performance on the part of obligor. Surety should be of full value of bond and the person standing as a surety should be solvent to the extent of the bond amount. A company can stand as surety for another company.

9) Guarantee Bond executed by bank: When any scheduled bank gives a guarantee for a registered person with or without deposit of security, the guarantee bond should provide a period of validity during which obligations arising may be enforced.