Received by MLaMar December 11, 2014 December 11, 2014 District/CA Northern Humboldt Union... ·...

89

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT COUNTY OF HUMBOLDT MCKINLEYVILLE, CALIFORNIA ANNUAL FINANCIAL REPORT JUNE 30, 2014 ROBERTSON & ASSOCIATES, CPAs A Professional Corporation Received by MLaMar December 11, 2014 Received by MLaMar December 11, 2014 Received by MLaMar December 11, 2014

Transcript of Received by MLaMar December 11, 2014 December 11, 2014 District/CA Northern Humboldt Union... ·...

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT

COUNTY OF HUMBOLDT MCKINLEYVILLE, CALIFORNIA

ANNUAL FINANCIAL REPORT

JUNE 30, 2014

ROBERTSON & ASSOCIATES, CPAs A Professional Corporation

Received by MLaMar December 11, 2014Received by MLaMar December 11, 2014Received by MLaMar December 11, 2014

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT ORGANIZATION

JUNE 30, 2014

Northern Humboldt Union High School District (District) was established in 1925 and is comprised of two four-year high schools, two small continuation high schools, one charter school, one alternative high school, one mental health high school program and an adult school. There were no changes in the boundaries of the District during the year.

ADDRESS OF DISTRICT OFFICE

McKinleyville, CA 955192755 McKinleyville Avenue

Mr. Roger Macdonald

Mr. Nic Collart Principal - Six Rivers Charter 2 Years

Principal - MHS

Ms. Cindy Vickers Director of Fiscal Services 3 YearsMr. Dave Navarre Principal - Arcata High 3 Years

Mr. Chris Hartley Superintendent 2 YearsMr. Dave Lonn Executive Director 2 Years

Mr. Dan Johnson Trustee December, 2015

ADMINISTRATION

Name Title Tenure

Ms. Colleen Toste Trustee December, 2017Mr. Brian Lovell Trustee December, 2017

Office Term Expires

Mr. Dan Collen President December, 2015Ms. Dana Silvernale Clerk December, 2017

BOARD OF TRUSTEES

2 YearsMr. Sam Razo Principal - Tsurai 8 YearsMr. Jon Larson Principal - Pacific Coast 1 Year

Name

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT JUNE 30, 2014

TABLE OF CONTENTS

Page

1 - 3

4 - 16

17

18

19

20

21

22

23

24

25

26

27 - 52

53

54

55

Notes to Financial Statements

REQUIRED SUPPLEMENTARY INFORMATION SECTION

Schedule of Other Postemployment Benefits Funding Progress

Budgetary Comparison Schedule - General Fund

Proprietary Funds

Statement of Net Position

Statement of Revenues, Expenses and Changes in Fund Net Position

Statement of Cash Flows

Fiduciary Funds

Statement of Fiduciary Net Position

Statement of Revenues, Expenditures and Changes in Fund Balances

Reconciliation of the Governmental Funds Statement of Revenues,Expenditures and Changes in Fund Balances to the Statement ofActivities

FINANCIAL SECTION

Basic Financial Statements

Government-Wide

Statement of Net Position

Statement of Activities

Governmental Funds

Notes to Required Supplementary Information

INTRODUCTORY SECTION

Title Page

Organization

Table of Contents

INDEPENDENT AUDITOR'S REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

Balance Sheet

Reconciliation of the Governmental Funds Balance Sheet to theStatement of Net Position

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT JUNE 30, 2014

TABLE OF CONTENTS

Page

56

57

58

59 - 60

61

62

63

64

65

66 - 67

68 - 69

70 - 71

72 - 74

75

76 - 78

79

80

Combining Statement of Revenues, Expenditures and Changes inFund Balances

Fiduciary Funds Financial Statements

Summary Schedule of Prior Audit Findings

Independent Auditor's Report on Compliance for Each Major FederalProgram; Report on Internal Control Over Compliance; and Report onthe Schedule of Expenditures of Federal Awards Required by OMBCircular A-133

Independent Auditor's Report on State Compliance

FINDINGS AND QUESTIONED COSTS SECTION

Schedule of Audit Findings and Questioned Costs

Corrective Action Plan

Findings and Questioned Costs

Schedule of Average Daily Attendance

Schedule of Instructional Time

Schedule of Financial Trends and Analysis

Schedule of Expenditures of Federal Awards

Reconciliation of Annual Financial and Budget Report (SACS) withAudited Financial Statements

Schedule of Charter Schools

Notes to Supplementary Information

OTHER INDEPENDENT AUDITOR'S REPORTS

Independent Auditor's Report on Internal Control Over FinancialReporting and on Compliance and Other Matters Based on an Audit ofFinancial Statements Performed in Accordance With Government Auditing Standards

SUPPLEMENTARY INFORMATION SECTION

Other Governmental Funds Financial Statements

Combining Balance Sheet

Combining Schedule of Changes

ROBERTSON & ASSOCIATES, CPAs

A PROFESSIONAL CORPORATION 55 FIRST STREET, BOX G, SUITE 306 WWW.ROBERTSONCPA.COM LAKEPORT: (707) 263-9012 FAX: (707) 263-6001 LAKEPORT, CA 95453 TOLL FREE (800) 619-4762

- 1 -

INDEPENDENT AUDITOR’S REPORT

Board of Trustees Northern Humboldt Union High School District McKinleyville, California

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Northern Humboldt Union High School District (District), as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the District’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal controls relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the District’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the District’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

- 2 -

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Northern Humboldt Union High School District, as of June 30, 2014, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis, budgetary comparison information and schedule of funding progress, on pages 4 through 16 and 53 through 54, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the District’s basic financial statements. The combining nonmajor fund financial statements and schedule of expenditures of federal awards, as required by Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and the District’s introductory section are presented for purposes of additional analysis and are not a required part of the financial statements. The accompanying supplementary information as listed in the table of contents are required by the Standards and Procedures for Audits of California K-12 Local Educational Agencies 2013/2014 (published by the Education Audit Appeals Panel), are presented for purposes of additional analysis, and are not a required part of the basic financial statements.

This information, as listed in the table of contents, is the responsibility of management and was derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining nonmajor fund financial statements, and schedule of expenditures of federal awards and accompanying supplementary information as listed in the table of contents is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

- 3 -

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated December 05, 2014 on our consideration of the District's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the District’s internal control over financial reporting and compliance.

Lakeport, California December 05, 2014

Northern Humboldt Union High School District Management’s Discussion and Analysis

June 30, 2014

- 4 -

INTRODUCTION

Our discussion and analysis of Northern Humboldt Union High School District (District’s) financial performance provides an overview of the District’s financial activities for the year ended June 30, 2014. It should be read in conjunction with the District’s financial statements, which follow this section. FINANCIAL HIGHLIGHTS

Total net position was $16,503,602 at June 30, 2014. This was a decrease of $785,098 over the prior year’s restated net position. Net position was restated at June 30, 2013 for capital assets, net of accumulated depreciation and current liabilities in the amount of $1,092,353 (decrease to net position).

Overall revenues were $17,874,555, overall expenses were $18,659,653. OVERVIEW OF FINANCIAL STATEMENTS

Components of the Financials Section

Summary Detail

Management's Discussion and

Analysis

BasicFinancial

Statements

Required Supplementary

Information

Government-wideFinancial

Statements

FundFinancial

Statements

Notes to theFinancial

Statements

- 5 -

This annual report consists of three parts – Management’s Discussion and Analysis (this section), the basic financial statements, and required supplementary information. The three sections together provide a comprehensive overview of the District. The basic financial statements are comprised of two kinds of statements that present financial information from different perspectives:

Government-wide financial statements, which comprise the first two statements, provide both short-term and long-term information about the District’s overall financial position.

Fund financial statements focus on reporting the individual parts of District operations in more detail. The fund financial statements comprise the remaining statements.

o Governmental fund statements tell how general government services were financed in the short term as well as what remains for future spending.

o Proprietary fund statements provide both short and long-term information about the District’s enterprise employment services fund.

o Fiduciary fund statements provide information about the financial relationships in which the District acts solely as the trustee or agent for the benefit of others, to whom the resources belong.

The financial statements also include notes that explain some of the information in the statements and provide more detailed data. The basic financial statements are followed by a section of required and other supplementary information that further explain and support the financial statements. Government-Wide Statements

The government-wide statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The statement of net position includes all of the government’s assets and liabilities. All of the current year’s revenues and expenses are accounted for in the statement of activities, regardless of when cash is received or paid.

The two government-wide statements report the District’s net position and how they have changed. Net position, the difference between assets and liabilities, is one way to measure the District’s financial health or position.

Over time, increases or decreases in the District’s net position are an indicator of whether its financial health is improving or deteriorating, respectively. The net position of the District has decreased by 5% in the past year. This is due primarily to the on-going Measure Q Bond activities. The Bond fund balance has decreased by $2,189,620.

To assess the overall health of the District, one needs to consider additional non-financial factors such as changes in enrollment, changes in the property tax base, and changes in program funding by the Federal and State governments, and condition of facilities. The District’s P-2 average daily attendance has increased by 34.29 ADA in the past year and is expected to remain stable. The District needs to be cautious regarding future state funding, which is contingent upon temporary taxes created by Proposition 30. The District has been able to make major upgrades to facilities with Measure Q funds. In addition, the District has a healthy set aside in the General Fund for Deferred Maintenance, should the need arise.

The government-wide statements of the District include all governmental activities. All of the District’s basic services are included here, such as regular education, food service, maintenance and general administration. Revenue limit funding and federal and state grants finance most of these activities.

- 6 -

FINANCIAL ANALYSIS OF THE DISTRICT’S FUNDS

Fund Financial Statements

The fund financial statements provide more detailed information about the District’s most significant governmental funds, not the District as a whole. Funds are accounting devices that the District uses to keep track of specific sources of funding and spending for particular programs.

Some funds are required to be established by State law and by bond covenants.

The governing board establishes other funds to control and manage money for particular purposes or to show that the District is meeting legal responsibilities for using certain revenues.

The District has three types of funds:

Governmental funds – All of the District’s basic services are included in governmental funds, which generally focus on: (1) how cash and other financial assets that can readily be converted to cash flow in and out, and (2) the balances left at year-end that are available for spending. Consequently, the governmental funds’ statements provide a detailed short-term view that helps determine whether there are more or fewer financial resources than previously to finance the District’s programs. Because this information does not encompass the additional long-term focus of the government-wide statements, we provide additional information following the governmental funds’ statements that explains the relationship (or differences) between them.

Proprietary funds – One type of proprietary fund, the enterprise fund, reports the business-type activities, but provides more detail and additional information, such as cash flows.

o The District’s Enterprise Fund reports activities for which a fee is charged to external users for goods or services. The Enterprise Fund of the District accounts for the financial transactions related to the services rendered to external users.

Fiduciary funds – For assets that belong to others, such as student activities funds, the District acts as the trustee, or fiduciary. The District is responsible for ensuring that the assets reported in these funds are used only for their intended purposes and by those to whom the assets belong. A separate statement of fiduciary net position, a statement of changes in fiduciary net position, or a statement of changes in agency assets and liabilities reports the District’s fiduciary activities. These activities are excluded from the government-wide financial statements, as the assets cannot be used by the District to finance its operations.

The financial performance of the District is reflected in its governmental funds as well. As the District completed the year, its governmental funds reported a combined fund balance of $13,156,952 as compared to the prior year’s ending fund balance of $15,789,973. The District’s proprietary fund reported a fund balance of $126,018 as compared to the prior year’s ending fund balance of $131,743. The District’s fiduciary funds reported an asset and a corresponding liability of $454,220 as compared to the prior year’s balances of $358,883.

- 7 -

FINANCIAL ANALYSIS OF THE ENTITY AS A WHOLE Net Position The District’s combined net position was $16,503,602 at June 30, 2014.

2014 2013 Net Change

ASSETSCash and Equivalents 12,259,599$ 15,187,013$ (2,927,414)$ Other Current Assets 1,196,923 1,745,775 (548,852) Capital Assets,

Net of Accumulated Depreciation 17,426,121 15,784,629 1,641,492

TOTAL ASSETS 30,882,643$ 32,717,417$ (1,834,774)$

LIABILITIESCurrent Liabilities 328,586$ 1,249,407$ (920,821)$ Long-Term Liabilities 14,050,455 14,179,310 (128,855)

TOTAL LIABILITIES 14,379,041$ 15,428,717$ (1,049,676)$

NET POSITIONInvested in Capital Assets,

Net of Related Debt 4,641,877$ 11,405,409$ (6,763,532)$ Restricted 8,018,394 1,382,960 6,635,434 Unrestricted 3,843,331 4,500,331 (657,000)

TOTAL NET POSITION 16,503,602$ 17,288,700$ (785,098)$

Primary Government

The June 30, 2013 capital assets, net of accumulated depreciation, current liabilities and net position have been restated.

- 8 -

Changes in Net Position

2014 2013 Net Change

REVENUESProgram Revenues:

Charges for Services 229,874$ 504,560$ (274,686)$ Operating Grants and Contributions 3,150,532 3,182,109 (31,577)

General Revenues:Property Taxes 5,963,867 5,970,840 (6,973) Unrestricted Federal and State Aid 6,877,215 5,865,748 1,011,467 Miscellaneous and Other Local 1,653,067 1,197,358 455,709

TOTAL REVENUES 17,874,555 16,720,615 1,153,940

EXPENSESInstruction 10,803,274 10,209,995 593,279 Instruction-Related Services 1,694,507 1,678,143 16,364 Pupil Services 2,030,435 2,022,190 8,245 General Administration 1,447,329 1,386,826 60,503 Plant Services 1,317,618 1,392,664 (75,046) Ancillary Services 323,256 306,500 16,756 Enterprise Services 3,919 4,028 (109) Transfers Between Agencies 105,204 46,374 58,830 Interest on Long-Term Debt 537,170 512,103 25,067

Enterprise Services 396,941 408,187 (11,246)

TOTAL EXPENSES 18,659,653 17,967,010 692,643

INCREASE (DECREASE) IN NET POSITION (785,098) (1,246,395) 461,297

NET POSITION - BEGINNING 17,288,700 18,535,095 (1,246,395)

NET POSITION - ENDING 16,503,602$ 17,288,700$ (785,098)$

Primary Government

Net position has been restated at July 1, 2012.

- 9 -

Governmental Activities Net cost is total cost less fees generated by the related activity. The net cost reflects amounts funded by charges for services, operating grants and capital grants and contributions. Net Cost of Services

2014 2013 Net Change

NET COST OF SERVICESInstruction 8,053,814$ 7,694,884$ 358,930$ Instruction-Related Services 1,605,441 1,580,616 24,825 Pupil Services 1,817,655 1,145,128 672,527 General Administration 1,297,803 1,251,714 46,089 Plant Services 1,188,565 1,348,792 (160,227) Ancillary Services 323,256 306,500 16,756 Enterprise Services 3,919 4,028 (109) Transfers Between Agencies 54,683 28,389 26,294 Interest on Long-Term Debt 537,170 512,103 25,067 Business-Type Activities:

Enterprise Services 396,941 408,187 (11,246)

TOTAL NET COSTS OF SERVICES 15,279,247$ 14,280,341$ 1,010,152$

Net Cost of Services

2013/2014 Summary of Revenues for Governmental Activities

Charges for Services 1.3%

Operating Grants & Contributions 17.6%

Property Taxes 33.4%

Unrestricted Federal & State Aid 38.5%

Other General Revenues 9.2%

- 10 -

2013/2014 Summary of Expenses for Governmental Activities

Instruction 57.8%

Instruction-Related Services 9.1%

Pupil Services 10.9%

General Administration 7.8%

Plant Services 7.1%

Ancillary Services 1.7%

Transfers Between Agencies 0.6%

Interest on Long-Term Debt 2.9%

Business-Type Activities 2.1%

Fund Balance Comparison The District currently maintains the following funds:

2014 2013 Net Change

FUNDSGovernmental:

General 5,625,864$ 5,886,614$ (260,750)$ Charter Schools Special Revenue 430,258 450,528 (20,270) Cafeteria Special Revenue 26,439 19,441 6,998 Building 6,434,101 8,621,003 (2,186,902) Special Reserve Fund for Capital Outlay Projects 125,555 127,755 (2,200) Bond Interest and Redemption 514,735 684,632 (169,897)

Total Governmental 13,156,952 15,789,973 (2,633,021)

Proprietary:Enterprise:

Other Enterprise 126,018 131,743 (5,725)

Total Proprietary 126,018 131,743 (5,725)

TOTAL FUNDS 13,282,970$ 15,921,716$ (2,638,746)$

Ending Fund Balance

- 11 -

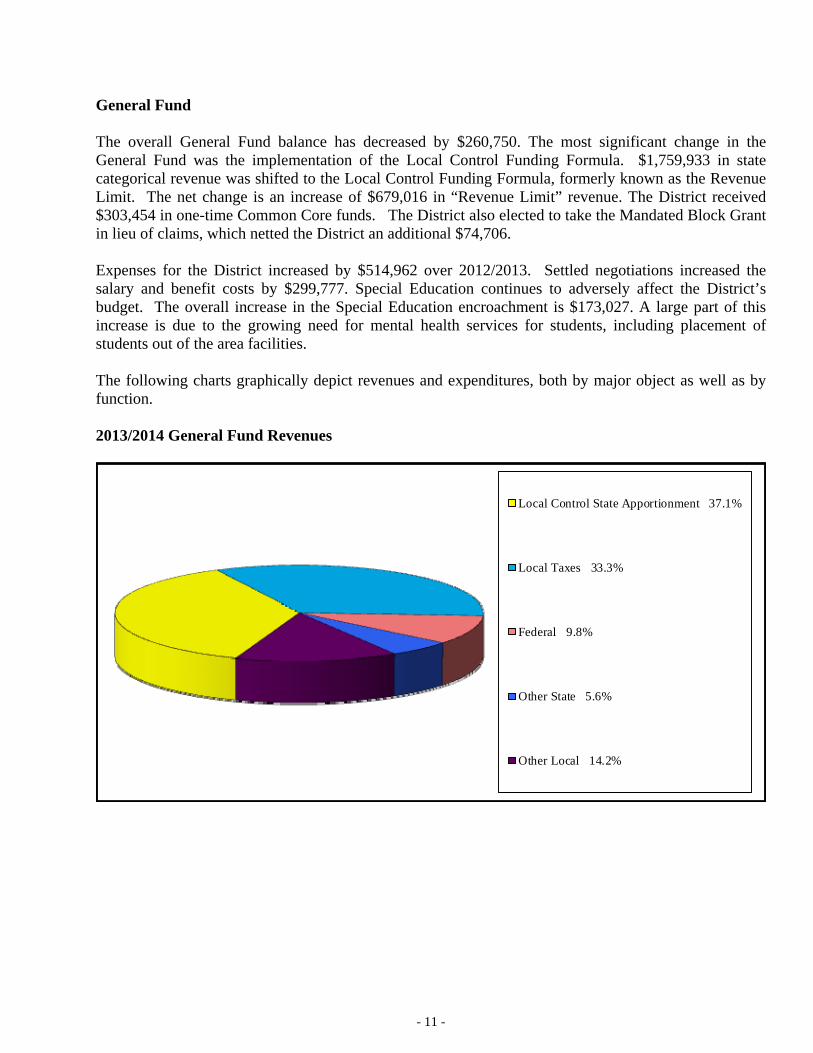

General Fund The overall General Fund balance has decreased by $260,750. The most significant change in the General Fund was the implementation of the Local Control Funding Formula. $1,759,933 in state categorical revenue was shifted to the Local Control Funding Formula, formerly known as the Revenue Limit. The net change is an increase of $679,016 in “Revenue Limit” revenue. The District received $303,454 in one-time Common Core funds. The District also elected to take the Mandated Block Grant in lieu of claims, which netted the District an additional $74,706. Expenses for the District increased by $514,962 over 2012/2013. Settled negotiations increased the salary and benefit costs by $299,777. Special Education continues to adversely affect the District’s budget. The overall increase in the Special Education encroachment is $173,027. A large part of this increase is due to the growing need for mental health services for students, including placement of students out of the area facilities. The following charts graphically depict revenues and expenditures, both by major object as well as by function. 2013/2014 General Fund Revenues

Local Control State Apportionment 37.1%

Local Taxes 33.3%

Federal 9.8%

Other State 5.6%

Other Local 14.2%

- 12 -

2013/2014 General Fund Expenditures by Object

Certificated Salaries 46.8%

Classified Salaries 15.3%

Employee Benefits 22.4%

Books & Supplies 4.7%

Services & Operating Expenses 9.9%

Capital Outlay 0.2%

Other Outgo 0.7%

2013/2014 General Fund Expenditures by Function

Instruction 60.2%

Instruction-Related Service 9.8%

Pupil Services 10.8%

General Administration 8.9%

Plant Services 7.6%

Ancillary Services 2.0%

Transfers Between Agencies 0.7%

- 13 -

Other Governmental Funds Other governmental funds had the following activity and changes for the year ended June 30, 2014:

The Special Reserve Fund had no significant changes. Six Rivers Charter School fund balance has decreased by $22,369. This is due to increases in Salary and benefits as a result of negotiations and the agreement to pay for the full cost of Health and Welfare on a year to year basis. The Cafeteria Special Revenue Fund balance has actually increased by $6,998. In 2012/2013, the Cafeteria Program was operating at a deficit of $24,932. In 2013/2014, the deficit has been reduced to $13,465. The District made operational changes in 2013/2014 to mitigate the encroachment on the General Fund and was somewhat successful. The changes made in 2013/2014 have not yet been fully realized. The Building Fund balance has decreased by $2,189,620. The District did not sell bonds in 2013/2014. The decrease is attributed to on-going project expenditures. The District continues to monitor the project costs and cash flow closely to ensure bond projects are finished timely and within budget. The Special Reserve Fund for Capital Outlay Projects had no significant changes. The Bond Interest and Redemption Fund is maintained by the Humboldt County Treasurer’s office as the District’s paying agent. The fund balance decreased by $167,179. The Enterprise Fund, also known as the Employment Services Fund showed a decrease of $5,092. The program typically operates at a surplus. However, in 2013/2014 the program generated less revenue. The program has a large ending balance, so the loss was easily absorbed. The District will continue to monitor the program for viability, but has no real concern about the program’s sustainability and believes the loss was an anomaly. The Student Body Fund had no significant changes and continues to be a self-sustained fund for the benefit of our students.

- 14 -

CAPITAL ASSETS AND DEBT ADMINISTRATION Capital Assets At June 30, 2014, the District had $17,426,121 invested, net of accumulated depreciation, in capital assets. Current year depreciation expense is $534,256. The Most significant changes in the Capital Assets is the Construction In Progress. This is directly connected to on-going Measure Q projects that have yet to be finalized. Most projects will be finalized in the 2014/2015 fiscal year, with the exception of the Fine Arts Facility.

2014 2013 Net Change

CAPITAL ASSETSLand 359,816$ 359,816$ -$ Construction In Progress 5,259,661 3,112,696 2,146,965 Land Improvements 1,491,453 1,491,453 - Buildings And Improvements 23,133,732 23,133,732 - Equipment 3,022,434 2,993,651 28,783 Accumulated Depreciation (15,840,975) (15,306,719) (534,256)

NET CAPITAL ASSETS 17,426,121$ 15,784,629$ 1,641,492$

Primary Government

The June 30, 2013 capital assets have been restated.

Long-Term Debt At year end, the District had $14,050,455 in long-term debt. The District had a decrease of $262,386 in General Obligations Bonds Payable. The District did not incur any new debt for Measure Q and simply made its required annual payment. The District also showed an increase in its OPEB obligation of $146,838. The OPEB liability is the difference between the actual required contribution and the actual payment made. The calculation is based on the future obligation of the District to pay for retiree health insurance as defined in the existing contract between the district and our employment groups.

2014 2013 Net Change

LONG-TERM DEBTGeneral Obligation Bonds Payable 12,784,244$ 13,046,630$ (262,386)$

Premium on Issuance 534,664 555,955 (21,291) Net OPEB Obligation 665,300 518,462 146,838 Compensated Absences 66,247 58,263 7,984

TOTAL LONG-TERM DEBT 14,050,455$ 14,179,310$ (128,855)$

Primary Government

The June 30, 2013 premium on issuance has been restated.

- 15 -

GENERAL FUND BUDGETARY HIGHLIGHTS The difference in the original versus final budget amounts and actual versus budget amounts is primarily due to the following:

The District always takes a conservative approach to budgeting. However, the District updates the budget throughout the year, whenever significant changes can be confirmed. Typically, by the end of the year, the budget closely reflects its actuals. Revenues - The Adopted Budget is based on projections by our County Office of Education. At the time our budget is adopted by the Governing Board, the State has yet to finalize its budget. This makes it nearly impossible to have an accurate estimate. The variance between Adopted Budget and Final Budget is 3.33%. By comparison, the District actuals to final budget showed a variance of .36%. This is less than one percent and not significant. Expenses - The expense side of the budget is always impacted by negotiations, which have historically not been settled at the time of adoption. The variance between the Adopted Budget and the final Budget is 2.69%. The variance between the actual and the final budget is 1.49%. Interfund transfers in – The most significant variance is in the area of interfund transfers. The District always budgets that a transfer from the Retiree Fund will be required to pay for retiree benefits. At the end of the fiscal year, the District evaluates the need for the transfer and for the past two years has decided the transfer is not necessary. In 2013/2014, the variance between the actual and the final budget is 88.04%. A transfer of $200,319 from the Retiree Fund was not completed.

Over the course of the year, the District revises its annual budget to reflect unexpected changes in revenues and expenditures. The final amendment to the budget was approved September 9, 2014. A schedule of the District’s General Fund original and final budget amounts compared with actual revenues and expenditures is provided with the basic financial statements in the audited financial report. ECONOMIC FACTORS AND NEXT YEAR’S BUDGETS AND RATES At the time these financial statements were prepared and audited, the District was aware of several circumstances that could affect its future financial health:

The District has started the year with slightly increased enrollment and is projecting increased Average Daily Attendance. This is important because attendance drives the majority of our funding. The District has successfully settled negotiations with the Certificated Bargaining Unit. Although this is an increased cost, the District is confident that the agreement can be supported by the District’s strong financial health. Negotiations are still unsettled with the Classified Bargaining unit. The District is hopeful we will be settled before the end of the calendar year. The biggest issue impacting the District is the uncertain funding generated by the Local Control Funding Formula (LCFF). There are wide differences between the Department of Finance and School Services of California’s estimates for future funding. The District is yet again budgeting with uncertainty and continues to take a conservative approach.

- 16 -

The Local Control Funding comes with increased accountability in the form of the Local Control Accountability Plan (LCAP). The District is now required to tie budget expenditures to state mandated goals. There is increased emphasis placed on Economically Disadvantaged, English Learner, and Foster Youth students. The District is receiving funds that must be specifically used to benefit those students. There is a lot of uncertainty regarding how much funding we will receive and how much of that funding will be restricted to serve the above mention student groups. The District received over $303,454 in one-time Common Core funds in 2013/2014. There are no additional funds available in 2014/2015. The District will need to fund this shift to Common Core utilizing its own funds. In addition, the District has had the benefit of the THRIVE grant. 2014/2015 is the final year of the grant, which will significantly affect our Federal revenue. The District is showing significant increases in Special Education costs. There has been an increased need for Non-Public School placements. This creates an incredibly large expense attributed to only a few students. It is difficult to predict when these needs will arise, and therefore difficult to plan for financially. Lastly, a serious issue facing our District is the impact of the Affordable Care Act. Our District will be working closely with our bargaining units to ensure compliance with the new regulations. The District is participating on a committee to ensure Humboldt County Schools, including our District, are fully complying with all the required regulations. At this time the financial impact is still unknown. There will be an increased workload associated with all the tracking and reporting requirements of the Affordable Care Act. But, at this point, it is unclear if additional staffing will be required. Although our District is facing significant challenges, I am confident that our Administration, working closely with all employees, can accomplish what needs to be done in the coming years.

CONTACTING THE DISTRICT’S FINANCIAL MANAGEMENT This financial report is designed to provide our citizens, taxpayers, parents, participants, investors and creditors with a general overview of the District’s finances and to demonstrate the District’s accountability for the money it receives. If you have questions about this report, or need additional financial information, contact Cindy Vickers, 2755 McKinleyville Avenue, McKinleyville, CA 95519, phone 707-839-6470.

FINANCIAL SECTION

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT STATEMENT OF NET POSITION

JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 17 -

PrimaryGovernmental Business-type Government

Activities Activities Total

ASSETSCash and equivalents 12,154,657$ 104,942$ 12,259,599$ Accounts receivable 1,166,316 30,034 1,196,350 Stores inventories 573 - 573 Capital assets:

Non-depreciable 5,619,477 - 5,619,477 Depreciable, net of accumulated depreciation 11,806,644 - 11,806,644

Total Assets 30,747,667$ 134,976$ 30,882,643$

LIABILITIESAccounts payable 164,594$ 6,050$ 170,644$ Accrued interest payable 157,942 - 157,942 Long-term debt:

Due within one year 108,959 582 109,541 Due after one year 13,938,588 2,326 13,940,914

Total Liabilities 14,370,083$ 8,958$ 14,379,041$

NET POSITIONNet Investment in capital assets 4,641,877$ -$ 4,641,877$ Restricted for:

Capital projects 6,434,101 - 6,434,101 Debt service 514,735 - 514,735 Educational programs 486,843 - 486,843 Other purposes (expendable) 456,697 - 456,697 Enterprise Activites - 126,018 126,018

Unrestricted 3,843,331 - 3,843,331

Total Net Position 16,377,584$ 126,018$ 16,503,602$

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 18 -

Operating PrimaryCharges for Grants and Governmental Business-type Government

Functions Expenses Services Contributions Activities Activities Total

GOVERNMENTAL ACTIVITIESInstruction 10,803,274$ 163,249$ 2,586,211$ (8,053,814)$ (8,053,814)$ Instruction-related services:

Supervision of instruction 10,932 - 2,450 (8,482) (8,482) Instructional library, media and technology 252,298 - 8,373 (243,925) (243,925) School site administration 1,431,277 - 78,243 (1,353,034) (1,353,034)

Pupil services:Home-to-school transportation 857,562 - - (857,562) (857,562) Food services 179,951 37,727 121,009 (21,215) (21,215) All other pupil services 992,922 - 54,044 (938,878) (938,878)

General administration:Data processing 36,157 - - (36,157) (36,157) All other general administration 1,411,172 - 149,526 (1,261,646) (1,261,646)

Plant services 1,317,618 - 129,053 (1,188,565) (1,188,565) Ancillary services 323,256 - - (323,256) (323,256) Enterprise services 3,919 - - (3,919) (3,919) Transfers between agencies 105,204 28,898 21,623 (54,683) (54,683) Interest on long-term debt 537,170 - - (537,170) (537,170)

Total Governmental Activities 18,262,712$ 229,874$ 3,150,532$ (14,882,306) (14,882,306)

BUSINESS-TYPE ACTIVITIESEnterprise services 396,941$ -$ -$ (396,941)$ (396,941)

Total Business-Type Activities 396,941$ -$ -$ (396,941) (396,941)

GENERAL REVENUESTaxes and subventions:

Property taxes levied for general purposes 5,232,583 - 5,232,583 Property taxes levied for debt service 731,284 - 731,284

Federal and state aid not restricted to specific purposes 6,877,215 - 6,877,215 Interest and investment earnings 46,281 666 46,947 Interagency revenues 837,911 - 837,911 Miscellaneous 377,659 390,550 768,209

Total General Revenues 14,102,933 391,216 14,494,149

Change in Net Position (779,373) (5,725) (785,098)

Net Position - Beginning 17,156,957 131,743 17,288,700

Net Position - Ending 16,377,584$ 126,018$ 16,503,602$

Program RevenuesChange in

Net Position

Net (Expense)Revenue and

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT GOVERNMENTAL FUNDS

BALANCE SHEET JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 19 -

Other TotalGeneral Building Governmental Governmental

Fund Fund Funds FundsASSETS

Cash and equivalents 4,691,923$ 6,429,240$ 1,033,494$ 12,154,657$ Accounts receivable 1,087,561 10,806 67,949 1,166,316 Stores inventories - - 573 573

Total Assets 5,779,484$ 6,440,046$ 1,102,016$ 13,321,546$

LIABILITIESAccounts payable 153,620$ 5,945$ 5,029$ 164,594$

Total Liabilities 153,620 5,945 5,029 164,594

FUND BALANCESNon spendable

Cash in revolving fund 2,500 - - 2,500 Stores inventories - - 573 573

Restricted 486,843 6,434,101 562,925 7,483,869 Assigned

Other assignments 3,053,251 - 533,489 3,586,740 Unassigned

Reserve for economic uncertainties 2,083,270 - - 2,083,270

Total Fund Balance 5,625,864 6,434,101 1,096,987 13,156,952

Total Liabilities and Fund Balance 5,779,484$ 6,440,046$ 1,102,016$ 13,321,546$

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT RECONCILIATION OF THE GOVERNMENTAL FUNDS

BALANCE SHEET TO THE STATEMENT OF NET POSITION JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 20 -

Detail Total

13,156,952$

Historical cost of capital assets 33,267,096$ Accumulated depreciation (15,840,975)

17,426,121

(665,300)

(157,942)

General obligation bonds payable (13,318,908) Compensated absences (63,339)

(13,382,247)

126,018

16,503,602$

and, therefore, are not reported as liabilities in thegovernmental funds. Long-term liabilities, net of unamortizedpremiums, discounts, and deferred charges, are included inthe Statement of Net Position.

The District uses an internal service fund to charge the costs ofcertain activities to individual funds. The assets and liabilitiesof the internal service fund are reported with governmentalactivities in the Statement of Net Position.

Total net position, governmental activities

Interest on long-term debt is not reported in the governmental

funds until the period in which it matures and is paid. In thegovernment-wide statement of activities, it is recognized inthe period that it is incurred. The additional liabilities for theunmatured interest owing at the end of the period are includedon the Statement of Net Position.

Long-term liabilities are not due and payable in the current period

Total fund balances - governmental funds

Amounts reported for governmental activities in the Statement ofNet Position differ from amounts reported in governmental fundsas follows:

Capital Assets used in governmental activities are not financialresources and, therefore, are not reported in the governmentalfunds.

The cumulative difference in the Annual Required Contributions

(ARC) and actual OPEB contributions made is reported as along-term liability in the government-wide statements on theStatement of Net Position. When the cumulative contributionsexceed the ARC, a Net OPEB Asset exists and is reported asan asset on the Statement of Net Position.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT GOVERNMENTAL FUNDS

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 21 -

Other TotalGeneral Building Governmental Governmental

Fund Fund Funds FundsREVENUES

Local control sources:State apportionments 5,823,661$ -$ 389,229$ 6,212,890$ Local sources 5,232,583 - 276,360 5,508,943

Federal 1,544,832 - 155,067 1,699,899 Other state 875,945 - 66,369 942,314 Other local 2,231,484 49,621 838,188 3,119,293

Total Revenues 15,708,505 49,621 1,725,213 17,483,339

EXPENDITURESInstruction 9,639,128 - 671,316 10,310,444 Instruction related services:

Supervision of instruction 9,668 - - 9,668 Instructional library, media, and technology 229,550 - 8,232 237,782 School site administration 1,326,805 - 81,761 1,408,566

Pupil services:Home-to-school transportation 801,775 - - 801,775 Food services - - 172,200 172,200 All other pupil services 928,293 - 28,742 957,035

General administration:Data processing 36,157 - - 36,157 All other general administration 1,387,722 - 1,404 1,389,126

Plant services 1,212,137 92,581 12,686 1,317,404 Facility acquisition and construction - 2,143,942 3,023 2,146,965 Ancillary services 320,518 - - 320,518 Transfers between agencies 105,204 - - 105,204 Principal on long-term debt - - 285,000 285,000 Interest on long-term debt - - 618,516 618,516

Total Expenditures 15,996,957 2,236,523 1,882,880 20,116,360

Excess (deficiency) of revenues over (under) expenditures (288,452) (2,186,902) (157,667) (2,633,021)

OTHER FINANCING SOURCES (USES)Operating transfers in 48,165 - 20,463 68,628 Operating transfers out (20,463) - (48,165) (68,628)

Total Other Financing Sources (Uses) 27,702 - (27,702) -

Excess of revenues and other financing sources over (under) expenditures and other financing sources (uses) (260,750) (2,186,902) (185,369) (2,633,021)

Fund Balance - Beginning 5,886,614 8,621,003 1,282,356 15,789,973

Fund Balance - Ending 5,625,864$ 6,434,101$ 1,096,987$ 13,156,952$

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT RECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT

OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES TO THE STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 22 -

Detail Total

(2,633,021)$

Capital outlay 2,175,748$ Depreciation expense (534,256)

1,641,492

(22,614)

Amortization Expense 21,291

General obligation bonds payable 285,000

Contributions made during the year 168,032 Annual OPEB Cost (314,870)

(146,838)

Increases to compensated absences (7,352)

82,669

Change in net position of governmental activities (779,373)$

Increases in the liability for compensated absences are not

recorded as expenditures in governmental funds because theyare not expected to be liquidated with current financialresources. In the statement of activities, compensatedabsences are recognized as expenses when earned.

Unmatured interest on long-term debt is recognized ingovernmental funds in the period when it is due. However, inthe statement of activities, unmatured interest on long-termdebt is accrued at year end.

Debt issued at a premium or at a discount is recognized as an

Other Financing Source or Other Financing Use in the periodit is incurred in the governmental funds. In the government-wide statements, the premium or discount is amortized asinterest over the life of the debt.

Repayment of the principal of long-term debt is reported as anexpenditure in governmental funds. However, the repaymentreduces long-term liabilities in the statement of net position.

In governmental funds, contributions to a trust fund and premiumpayments for OPEB are recorded as expenditures. However,in the Statement of Activities, the annual OPEB Cost isexpensed.

Accreted interest on capital appreciation bonds is accrued aslong-term debt in the government wide financials, increasinginterest expense.

Total change in fund balances - governmental funds

Amounts reported for governmental activities differ from amounts reported in governmental funds as follows:

Capital Outlays are reported as expenditures in governmentalfunds. However, in the statement of activities, the cost ofthose assets is allocated over their estimated useful lives asdepreciation expense.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT PROPRIETARY FUNDS

STATEMENT OF NET POSITION FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 23 -

Business-typeActivities

Enterprise Fund

ASSETSCash and equivalents 104,942$ Accounts receivable 30,034

Total Assets 134,976$

LIABILITIESAccounts payable 6,050$ Long-term debt:

Due within one year 582 Due after one year 2,326

Total Liabilities 8,958$

NET POSITIONUnrestricted 126,018$

Total Net Position 126,018$

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT PROPRIETARY FUNDS

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN FUND NET POSITION

FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 24 -

Business-typeActivities

Enterprise FundOPERATING REVENUES

Fees and Contracts 354,105$ Other operating revenues 36,445

Total Operating Revenues 390,550

OPERATING EXPENSESClassified salaries 289,402Employee benefits 75,730Books, supplies and equipment 10,632 Services and other operating expenditures 21,177

Total Operating Expenses 396,941

Operating income (loss) (6,391)

NON-OPERATING REVENUES (EXPENSES)Interest income 666

Total Non-Operating Revenue (Expenses) 666

Change in Net Position (5,725)

Net Position - Beginning 131,743

Net Position - Ending 126,018$

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT PROPRIETARY FUNDS

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 25 -

Business-typeActivities

Enterprise Fund

CASH FLOWS FROM OPERATING ACTIVITIESCash received from contract services 396,851$ Cash paid for services (400,047)

Net cash provided (used) by operating activities (3,196)

CASH FLOWS FROM INVESTING ACTIVITIESInterest on investments 666

Net cash provided (used) by investing activities 666

Net increase (decrease) in cash and cash equivalents (2,530)

Cash and Cash Equivalents - Beginning 107,472

Cash and Cash Equivalents - Ending 104,942$

Reconciliation of net operating income (loss) to net cash provided (used)by operating activities:

Operating income (loss) (6,391)$ Adjustments to reconcile net operating income (loss) to net cash provided

(used) by operating activities: Changes in assets and liabilities:

Receivables 6,301 Accounts payable (3,738) Compensated absences 632

Net cash provided (used) by operating activities (3,196)$

NON CASH TRANSACTIONS There were no non-cash investing, capital, or financing activities.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT FIDUCIARY FUNDS

STATEMENT OF FIDUCIARY NET POSITION FOR THE YEAR ENDED JUNE 30, 2014

The accompanying notes are an integral part of these financial statements. - 26 -

McKineleyville High School

Arcata High School

Total Fiduciary Funds

ASSETS

Cash and equivalents 165,834$ 257,758$ 423,592$

Total Assets 165,834$ 257,758$ 423,592$

LIABILITIES

Due to student groups 165,834$ 257,758$ 423,592$

Total Liabilities 165,834$ 257,758$ 423,592$

Agency Funds

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 27 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES A. General Statement

The Northern Humboldt Union High School District (District) is a public educational agency operating under the applicable laws and regulations of the State of California. It is governed by a five member Board of Trustees (Board) elected by registered voters of the District, which comprises an area in Northern Humboldt County. The District was established in 1925 and serves students in grades nine through twelve.

B. Accounting Policies

The District prepares its basic financial statements in conformity with generally accepted accounting principles as prescribed by the Governmental Accounting Standards Board (GASB) and the American Institute of Certified Public Accountants (AICPA) and complies with the policies and procedures of the Department of Education’s California School Accounting Manual.

C. Reporting Entity

The Board is elected by the public and it has the authority to make decisions, appoint administrators and managers, and significantly influence operations. It also has the primary accountability for fiscal matters. The District is therefore a financial reporting entity as defined by the GASB in its Statement No. 14, The Financial Reporting Entity, as amended by GASB 39, Determining Whether Certain Organizations Are Component Units. The District has reviewed criteria to determine whether other entities with activities that benefit the District should be included within its financial reporting entity. The criteria include, but are not limited to: whether the District exercises oversight responsibility (which includes financial interdependency, selection of governing authority, designation of management, ability to significantly influence operations, and accountability for fiscal matters), the scope of public service, and a special financing relationship.

The District has determined that no outside entity meets the above criteria, and therefore, no agency has been included as a component unit in the District’s general-purpose financial statements. In addition, the District is not aware of any entity that would exercise such oversight responsibility that would result in the District being considered a component unit of that entity.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 28 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued) D. Future Implementation of New Accounting Pronouncements

The following is a summary of the upcoming GASB Statements that may have an impact on the District’s future reporting at the time of this report in order of implementation date: Statement Number Title

Effective for Periods beginning after: Description

GASB 69 Government Combinations and Disposals of Government Operations

December 15, 2013 This Statement establishes accounting and financial reportingstandards related to government combinations and disposals ofgovernment operations. As used in this Statement, the termgovernment combinations includes a variety of transactions referredto as mergers, acquisitions, and transfers of operations.

GASB 68 Accounting and Financial Reporting for Pensions - an amendment of GASB Statement No. 27

June 15, 2014 This Statement replaces the requirements of Statement No. 27,Accounting for Pensions by State and Local GovernmentalEmployers, as well as the requirements of Statement No. 50, PensionDisclosures, as they relate to pensions that are provided throughpension plans administered as trusts or equivalent arrangements(hereafter jointly referred to as trusts) that meet certain criteria. Therequirements of Statement Nos. 27 and 50 remain applicable forpensions that are not covered by the scope of this Statement.

This Statement and Statement No. 67 establish a definition of apension plan that reflects the primary activities associated with thepension arrangement - determining pensions, accumulating andmanaging assets dedicated for pensions, and paying benefits to planmembers as they come due.

This Statement requires single and agent employers to present inrequired supplementary information the following information,determined as of the measurement date, for each of the 10 mostrecent fiscal years.

GASB 71 Pension Transition for ContributionsMade Subsequent to the MeasurementDate – an amendment to GASBStatement No. 68.

June 15, 2014 The objective of this Statement is to address an issue regardingapplication of the transition provisions of Statement No. 68,Accounting and Financial Reporting for Pensions. The issue relatesto amounts associated with contributions, if any, made by a state orlocal government employer or nonemployer contributing entity to adefined benefit pension plan after the measurement date of thegovernment’s beginning net pension liability.

This Statement amends paragraph 137 of Statement 68 to requirethat, at transition, a government recognize a beginning deferredoutflow of resources for its pension contributions, if any, madesubsequent to the measurement date of the beginning net pensionliability. Statement 68, as amended, continues to require thatbeginning balances for other deferred outflows of resources anddeferred inflows of resources related to pensions be reported attransition only if it is practical to determine all such amounts.

The provisions of these Statements generally are required to be applied retroactively for all periods presented. Early application, if allowable, was not adopted.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 29 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued) E. Basis of Presentation

1. Government-Wide Financial Statements

The government-wide financial statements (i.e., the statement of net position and the statement of activities) report information on all of the nonfiduciary activities of the District and its component units. Governmental activities, which normally are supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support. Likewise, the primary government is reported separately from certain legally separate component units for which the primary government is financially accountable. The government-wide statement of activities presents a comparison between direct expenses and program revenues for each function or program of the District’s governmental activities. Direct expenses are those that are specifically associated with a service, program, or department and are therefore clearly identifiable to a particular function. The District does not allocate indirect expenses to functions in the statement of activities. Program revenues include charges paid by the recipients of goods or services offered by a program, as well as grants and contributions that are restricted to meeting the operational or capital requirements of a particular program. Revenues which are not classified as program revenues are presented as general revenues of the District, with certain limited exceptions. The comparison of direct expenses with program revenues identifies the extent to which each governmental function is self-financing or draws from the general revenues of the District.

2. Fund Financial Statements

The financial transactions of the District are reported in individual funds in the fund financial statements. Each fund is accounted for by providing a separate set of self-balancing accounts that comprises its assets, liabilities, reserves, fund equity, revenues and expenditures or expenses, as appropriate. The emphasis in fund financial statements is on the major funds in either the governmental or business-type activities categories. Non-major funds by category are summarized in to a single column. GASB Statement No. 34 sets forth minimum criteria (percentage of the assets, liabilities, revenues or expenditures/expenses of either fund category or the governmental and enterprise funds combined) for the determination of major funds. The non-major funds are combined in a column in the fund financial statements.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 30 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

The District’s accounts are organized into major, non-major governmental, proprietary funds, and fiduciary funds as follows: a. Major Governmental Funds

The General Fund is the general operating fund of the District. It is used to account for all financial resources except those required to be accounted for in another fund. The Building Fund is used to account for the acquisition of major governmental capital facilities and buildings funded primarily with proceeds from the sale of bonds.

b. Non-major Governmental Funds

Special Revenue Funds are used to account for the proceeds of specific revenue sources that are legally restricted to expenditures for specific purposes. The District maintains the following non-major special revenue funds:

The Charter School Fund is used to account for the resources committed to and expenditures incurred by the District chartered Six Rivers Charter High School. The Cafeteria Fund is used to account for revenues and expenditures associated with the District’s food service program.

Capital Projects Funds are used to account for the acquisition and construction of all major governmental capital assets. The District maintains the following non-major capital projects fund:

The Special Reserve Fund for Capital Outlay Projects is used to account for the financial resources used for the acquisition or construction of major capital projects.

Debt Service Funds are used to account for the accumulation of resources for, and the debt service payments related to, the District’s debt issuances. The District maintains the following non-major debt service fund:

The Bond Interest and Redemption Fund is maintained by the County Treasurer and is used to account for both the accumulation of resources from ad valorem tax levies and the interest payments and redemption of principal of the District’s general obligation bond issuance as discussed later in the Notes to Financial Statements.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 31 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

c. Proprietary Funds

Operating revenues in the proprietary funds are those revenues that are generated from the primary operations of the fund. All other revenues are reported as non-operating revenues. Operating expenses are those expenses that are essential to the primary operations of the fund. All other expenses are reported as non-operating expenses. For purposes of the statement of cash flows, the District considers all highly liquid investments (including restricted assets) with a maturity when purchased of three months or less and all local government investment pools to be cash equivalents. Enterprise Funds are used to account for services provided to users on a cost-recovery basis. The District maintains the following non-major enterprise fund:

The Enterprise Fund is used to account for the District’s employment services program for which a fee is charged to external users of goods or services. The Enterprise Fund of the District accounts for financial transactions related to the services rendered to external users.

d. Agency Funds

Agency Funds are used to account for assets of others for which the District acts as an agent. The Student Body Fund is used to account for the proceeds of Board approved student activities and student body approved expenditures. The District maintains two agency funds, one for each high school’s Student Body.

F. Basis of Accounting

Basis of accounting refers to when transactions are recorded in the financial records and reported in the financial statements. The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, as are the proprietary fund and fiduciary fund financial statements. Governmental funds are reported using the current financial resources measurement focus and the modified accrual basis of accounting.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 32 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

1. Revenues - Exchange and Non-exchange Transactions

Revenue resulting from exchange transactions, in which each party gives and receives essentially equal value, is recorded under the accrual basis when the exchange takes place. Under the modified accrual basis, revenue is recorded in the fiscal year in which the resources are measurable and become available. “Available” means the resources will be collected within the current fiscal year or are expected to be collected soon enough thereafter to be used to pay liabilities of the current fiscal year. For the District, “available” means collectable within the current period or with 45, 60, 90 days after year-end, depending on the revenue source. However, to achieve comparability of reporting among California Districts and so as not to distort normal revenue patterns, with specific respect to reimbursement grants and corrections to state aid apportionments, the California Department of Education has defined available as collectible within one year. Non-exchange transactions are those in which the District receives value without directly giving equal value in return, include property taxes, grants, and entitlements. Under the accrual basis, revenue from property taxes is recognized in the fiscal year for which the taxes are levied. Revenue from grants and entitlements is recognized in the fiscal year in which all eligibility requirements have been satisfied. Eligibility requirements include timing requirements, which specify the year when the resources are to be used or the fiscal year when use is first permitted; matching requirements, in which the District must provide local resources to be used for a specific purpose; and expenditure requirements, in which the resources are provided to the District on a reimbursement basis. Under the modified accrual basis, revenue from non-exchange transactions must also be available before it can be recognized.

2. Unearned Revenue

Unearned revenue arises when assets are received before revenue recognition criteria have been satisfied. Grants and entitlements received before eligibility requirements are met are recorded as unearned revenue. On governmental fund financial statements, receivables associated with non-exchange transactions that will not be collected within the availability period have also been recorded as unearned revenue.

3. Expenses/Expenditures

Under the accrual basis of accounting, expenses are recognized at the time they are incurred. However, the measurement focus of governmental fund accounting is on decreases in the net financial resources (expenditures) rather than expenses. Expenditures are generally recognized in the accounting period in which the related fund liability is incurred, if measurable. Allocations of cost, such as depreciation and amortization, are not recognized on governmental fund financial statements.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 33 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued) G. Budgets and Budgetary Accounting

Annual budgets are adopted on a basis consistent with accounting principles generally accepted in the United States of America for all governmental funds. By state law, the District’s governing board must adopt a final budget no later than July 1. A public hearing must be conducted to receive comments prior to adoption. The District’s governing board satisfied these requirements. These budgets are revised by the District’s governing board and District superintendent during the year to give consideration to unanticipated revenue and expenditures. The original and final revised budgets for the General Fund are presented as required supplementary information in these financial statements. Formal budgetary integration was employed as a management control device during the year for all budgeted funds. The District employs budget control by minor object and by individual appropriation accounts. Expenditures cannot legally exceed appropriations by major object account.

H. Encumbrances

Encumbrance accounting is used in all budgeted funds to reserve portions of applicable appropriations for which commitments have been made. Encumbrances are recorded for purchase orders, contracts, and other commitments when they are written. Encumbrances are liquidated when the commitments are paid. All encumbrances are liquidated on June 30.

I. Assets, Liabilities, and Equity

1. Cash and Equivalents

The District considers all highly liquid investments with a maturity of three months or less at the time of purchase to be cash equivalents.

2. Receivables

Accounts receivable in governmental fund types consist primarily of receivables from federal, state and local governments for various programs.

3. Stores Inventories

Inventories are recorded using the purchases method, in that inventory acquisitions are initially charged as expenditures when acquired. The inventory (asset) account is adjusted to the physical count at year-end. Reported inventories are equally offset by a fund balance reserve, which indicates that these amounts are not “available for appropriation and expenditure” even though they are a component of net current assets.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 34 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

4. Prepaid Expenditures

The District has the option of reporting expenditures for prepaid items in governmental funds either when paid or during the benefiting period. The District has chosen to report the expenditure when paid and, therefore, no asset is reported.

5. Capital Assets

Capital assets are those purchased or acquired with an original cost of $5,000 or more and are reported at historical cost or estimated historical cost. Contributed assets are reported at fair market value as of the date received. Additions, improvements, and other capital outlays that significantly extend the useful life of an asset are capitalized. The costs of normal maintenance and repairs that do not add to the value of the assets or materially extend the asset’s lives are not capitalized, but are expensed as incurred. Depreciation on all capital assets is computed using a straight-line basis and an annual convention over the following estimated useful lives:

Land improvements 10 - 25Buildings and improvements 10 - 50Equipment 5 - 15

6. Compensated Absences

All vacation pay is accrued when incurred in the government-wide financial statements. A liability for these amounts is reported in the governmental funds only if they have matured, for example, as a result of employee resignations and retirements.

Accumulated sick leave benefits are not recognized as liabilities of the District. The District’s policy is to record sick leave as an operating expense in the period taken, since such benefits do not vest, nor is payment probable; however, unused sick leave is added to the creditable service period for calculation of retirement benefits when the employee retires.

7. Other Postemployment Benefits

As provided in applicable negotiated contracts, employees meeting the established criteria may participate in the District’s postemployment group health and insurance program as described later in the Notes to Financial Statements. The cumulative difference since the implementation of GASB Statement No. 45 between the annual OPEB cost and the District’s contributions is recognized as a long-term liability in the statement of net position. If the cumulative difference of contributions exceeds costs, an asset is reported.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 35 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

1. Accrued Liabilities and Long-Term Obligations

All payables, accrued liabilities and long-term obligations are reported in the government-wide and proprietary fund financial statements. In general, governmental fund payables and accrued liabilities that, once incurred, are paid in a timely manner and in full from current financial resources are reported as obligations of the funds. The District reports long-term obligations of governmental funds at face value in the government-wide financial statements. In the fund financial statements, governmental funds recognize bond premiums and discounts as well as bond issuance costs, during the current period. The face amount of the debt issued is reported as other financing sources.

2. Fund Balance Classifications

The governmental fund financial statements present fund balances based on a classification hierarchy that depicts the extent to which the District is bound by spending constraints imposed on the use of its resources. The classifications used in the governmental fund financial statements are as follows: a. Nonspendable Fund Balance

The nonspendable fund balance classification reflects amounts that are not in spendable form. Examples include inventory and prepaid items. This classification also reflects amounts that are in spendable form but that are legally or contractually required to remain intact.

b. Restricted Fund Balance

The restricted fund balance classification reflects amounts subject to externally imposed and legally enforceable constraints. Such constraints may be imposed by creditors, grantors, contributors, or laws or regulations of other governments, or may be imposed by law through constitutional provisions or enabling legislation. These are the same restrictions used to determine restricted net position as reported in the government-wide, proprietary fund, and fiduciary trust fund statements.

c. Committed Fund Balance

The committed fund balance classification reflects amounts subject to internal constraints self-imposed by formal action of the highest level of decision-making authority. The governing board is the highest level of decision-making authority for the District. Commitments may be established, modified, or rescinded only through resolutions or other action as approved by the governing board. The District has no committed fund balances.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 36 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

d. Assigned Fund Balance

The assigned fund balance classification reflects amounts that the District intends to be used for specific purposes. Assignments may be established either by the Board of Trustees or by a designee of the Board of Trustees, and are subject to neither the restricted nor committed levels of constraint. Constraints giving rise to assigned fund balance are not required to be imposed, modified, or removed by formal action of the highest level of decision-making authority. The action may be delegated to another body or official.

e. Unassigned Fund Balance and Minimum Fund Balance Policy

In the General Fund only, the unassigned fund balance classification reflects the residual balance that has not been assigned to other funds and that is not restricted, committed, or assigned to specific purposes. The Reserve for Economic Uncertainties maintained by the District pursuant to the Criteria and Standards for fiscal solvency adopted by the State Board of Education is a stabilization-like arrangement of the "minimum fund balance policy" type. The Reserve for Economic Uncertainties does not meet the criteria to be reported as either restricted or committed because it is not an externally enforceable legal requirement, and because even where the Reserve for Economic Uncertainties is established by formal action of the District’s highest level of decision-making authority, the circumstances in which the Reserve for Economic Uncertainties might be spent are by their nature neither specific nor non-routine. For this reason, the Reserve for Economic Uncertainties is reported as unassigned fund balance. The District is committed to maintaining a prudent level of financial resources to protect against the need to reduce service levels because of temporary revenue shortfalls or unpredicted expenditures. The District’s Minimum Fund Balance Policy requires a Reserve for Economic Uncertainties, consisting of unassigned amounts, equal to no less than two months of General Fund operating expenditures, or three percent (3%) of General Fund expenditures and other financing uses. The District passed a resolution May 10, 2011 to establish classification of fund balances in Governmental Funds, as required by GASB 54. The resolution delegates authorization to the Superintendent and/or designee to identify intended uses of assigned funds. The District’s policy regarding the order in which spendable fund balances are spent when more than one classification is available for a specific purpose is that they are spent in restricted, committed, assigned, and then unassigned order.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 37 -

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES (Continued)

3. Property Taxes

Secured property taxes attach as an enforceable lien on property as of January 1, and are payable in two installments on December 10 and April 10. Unsecured property taxes are payable in one installment on or before August 31. The County of Humboldt bills and collects the taxes for the District. Tax revenues are recognized by the District when received.

J. Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and reported amounts of revenues and expenditures during the reporting period. Actual amounts could differ from those estimates.

NOTE 2. CASH AND EQUIVALENTS Cash and Equivalents at June 30, 2014 are classified in the accompanying financial statements as follows:

PrimaryGovernmental Business-type Government Fiduciary

Activities Activities Total Funds

Cash and EquivalentsPooled Funds:

Cash in county treasury 12,152,157$ 104,942$ 12,257,099$ -$ Deposits:

Cash on hand and in banks - - - 423,592 Cash in revolving fund 2,500 - 2,500 -

Total Cash and Equivalents 12,154,657$ 104,942$ 12,259,599$ 423,592$

A. Cash in County Treasury

In accordance with Education Code 41001, the District maintains substantially all of its cash in the Humboldt County Treasury (the Treasury). The Treasury pools these funds with those of other districts in the County and invests the cash. The share of each fund in the pooled cash account is separately accounted for and interest earned is apportioned quarterly to funds that are legally required to receive interest based on the relationship of a fund’s daily balance to the total of pooled cash and investments.

NORTHERN HUMBOLDT UNION HIGH SCHOOL DISTRICT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014

- 38 -

NOTE 2. CASH AND EQUIVALENTS (Continued)