REC Markets and Trading 101 - Homepage | WSPP · REC Markets and Trading 101 Peter Toomey Manager,...

23

REC Markets and Trading 101 Peter Toomey Manager, Environmental Markets Iberdrola Renewables, Inc. 2011 WSPP SPRING OPERATING COMMITTEE MEETING BANFF, ALBERTA | MARCH 21, 2011

Transcript of REC Markets and Trading 101 - Homepage | WSPP · REC Markets and Trading 101 Peter Toomey Manager,...

REC Markets and Trading 101

Peter Toomey

Manager, Environmental Markets

Iberdrola Renewables, Inc.

2011 WSPP SPRING OPERATING COMMITTEE MEETING

BANFF, ALBERTA | MARCH 21, 2011

Iberdrola Renewables - Assets and Customers

February 15, 2011

Wind projects owned or controlled

Thermal generation

Biomass cogeneration

Mountain View III 22.44 MW owned

SDG&E

Dillon 45 MW owned

SCE

High Winds 162 MW PPASMUD, Merced, Modesto

Palo Alto, Alameda, SCPPA

Shiloh 150 MW ownedPG&E, Palo Alto, MID

Pleasant Valley

144 MW PPA

LADWP, Anaheim,

Glendale, Burbank,

UAMPS

Twin Buttes

75 MW owned

Public Service

Co. of CO (Xcel)

Colorado Green

81 MW owned

(162 MW project)

Public Service Co.

of CO (Xcel)

Lempster

24 MW owned

Southern NH

University

Elk River

150 MW owned

Empire Dist. Electric Co.

Dry Lake63 MW owned

Salt River Project

1 - Klondike III a

76.5 MW owned

PG&E

2 - Hay Canyon

100.8 MW owned

Snohomish PUD

3 - Klondike

24 MW owned

BPA

4 - Klondike III

223.6 MW owned

PG&E, PSE, BPA,

EWEB

5 - Star Point

99 MW owned

Modesto Irrig. Dist.

6 - Klondike II

75 MW owned

PGE

7 - Big Horn

199.5 MW owned

Modesto, Santa

Clara, Redding

8 - Big Horn II

199.5 MW owned

Modesta, Santa

Clara, Redding

9 - Pebble Springs

98.7 MW owned

SCPPA

1 2 3

4 6 5 8

Peñascal 202 MW ownedCity of Antonio,South Texas Electric Co-op

Barton Chapel120 MW owned

Locust Ridge

26 MW owned

PPL Energy Trust

Locust Ridge II

102 MW owned

PPL and many others

Casselman

34.5 MW owned

First Energy

Maple Ridge 1

115.5 MW owned

(231 MW project)

NYSERDA

Maple Ridge II

45.4 MW owned

(91 MW project)

NY Power Authority

Rugby149.1 MW ownedMissouri River Energy Services

Farmers City 146 MW owned

Providence Heights

72 MW owned

Streator Cayuga Ridge

300 MW ownedTVA

Peñascal II 202 MW ownedBTU (City of Bryan, Texas)

7

WINDPROJECTS

WECC – Western Electricity Coordinating Council

MISO – Midwest Independent Transmission System Operator

SPP – Southwest Power Pool

PJM – Pennsylvania New Jersey Maryland Interconnection

ERCOT – Electric Reliability Council of Texas

NYISO – New York Independent System Operator

NEPOOL – New England Power Pool

Simpson Biomass 43 MW

SMUD

Electric Power Markets

Klamath Cogen

536 MW

Klamath Generating

100 MW

WINDPROJECTS

1

4 3 6 85 7

2

9 10 11 12

1 - Buffalo Ridge 50.4 MW owned

NIPSCO

2 - Buffalo Ridge II 210 MW owned

NIPSCO

3 - MinnDakota 150 MW owned

Northern States Power (Xcel)

4 - Moraine 51 MW owned

Northern States Power (Xcel)

5 - Moraine II 49.5 MW owned

Northern States Power (Xcel)

6 - Elm Creek 99 MW owned

Great River Energy

7 - Elm Creek II 148.4 MW owned

Great River Energy

8 - Trimont 101 MW owned

Great River Energy

9 - Flying Cloud 43.5 MW owned

Alliant

10 - Winnebago 20 MW owned

DairlyLand Power

11 - Top of Iowa II 80 MW owned

Madison Gas and Electric, Wisconsin Public Power

12 - Barton 160 MW owned

NIPSCO, WI Public Power, Ino, WE Energies

Dry Lake II65.1 MW owned

Salt River Project

4,634 MW of Operating Wind Assets

Presentation Objectives

1. Basic overview of RECs and REC Markets

2. Provide “flavor” for these markets from a transactional perspective

3. Stimulate questions and conversation

…Please interrupt me if you have questions, comments, etc.!!!

Presentation Outline

What is a Renewable Energy Credit?

The RPS markets.

Basics of buying and selling.

REC Price Overview.

Focus on California.

General REC market observations.

Questions?

What is a REC? – the basics

•NO SINGLE DEFINITION – defined by governing institution (state, non-profit, etc.)

•Synonymous with Green Tag, Green Certificate, Tradable Green Certificate , etc.

•Intangible commodity embodying environmental attributes of renewable energy

oAttributes include offset emissions, reduced water use, env. claims, etc.

•1 MWH of electricity is granted 1 REC (there are exceptions)

•Tracked and traded separate from physical electricity, generally via:

oElectronic tracking systems (i.e. WREGIS, PJM GATS, etc.)

oPaper attestation

•Purpose:

•Ease of tracking ownership of environmental attributes

•Provide incremental revenue stream to renewable sources

•Two primary sources of demand

oCompliance market (i.e. State RPS programs)

oVoluntary market (Green-e, utility green pricing programs, etc.)

What is a REC? - Sample Definition

“Renewable Energy Certificates” or “RECs” means all right, title and interest in

and to Environmental Attributes. “Environmental Attributes” means any and all

certificates, credits, benefits, emissions reductions, environmental air

quality credits, and emissions reduction credits, offsets, claims, and

allowances, howsoever entitled, resulting from the avoidance of the emission of

any gas, chemical, or other substance attributable to the generation of the

specified energy by the Specified Resource, but specifically excluding only the

wind production tax credits. One REC represents the Environmental Attributes

made available by the generation of 1 megawatt-hour (“MWh”) of specified

energy by the Specified Resource

From Iberdrola Renewables “one-off” REC contract:

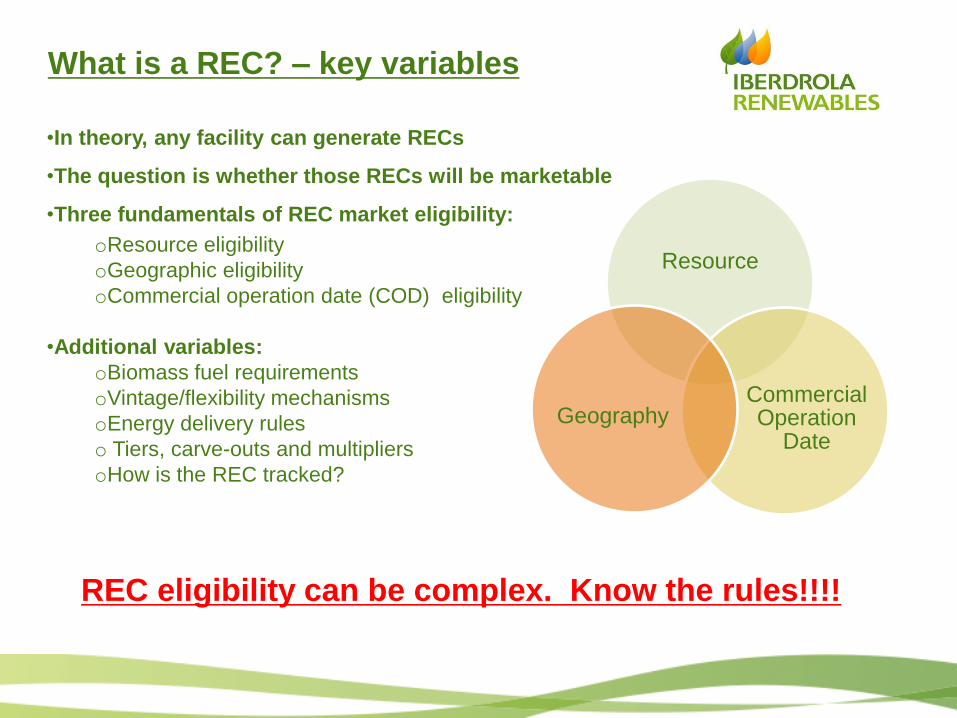

What is a REC? – key variables

•In theory, any facility can generate RECs

•The question is whether those RECs will be marketable

•Three fundamentals of REC market eligibility:

oResource eligibility

oGeographic eligibility

oCommercial operation date (COD) eligibility

•Additional variables:

oBiomass fuel requirements

oVintage/flexibility mechanisms

oEnergy delivery rules

o Tiers, carve-outs and multipliers

oHow is the REC tracked?

Resource

Commercial Operation

DateGeography

REC eligibility can be complex. Know the rules!!!!

State RPS Markets – The Patchwork

29 states + D.C.

8 states with nonbinding goals

State RPS State RPS Goal

HI40% - 2030

(Includes existing)

MT

15% - 2015

NV

25% - 2025CA

33% -

2020

AZ

15% - 2025

CO

30% - 2020 (IOU)

10% - 2020

(Muni/Coop)

NM

20% - 2020 (IOU)

10% - 2020 (Coop)

TX

5,880 MW - 2015

IA

105 MW

MN

25% - 2025

Xcel: 30% - 2020

WI

10% -

2015

IL

25% -

2025

NY29% - 2015

PA8% - 2020

„Tier 1‟

MA 15% - 2020

ME

10% - 2017 “New”

VTLoad growth by 2012

20% - 2017

WA

15% - 2020

OR

25% - 2025 (LG)

5-10% - 2025 (SM)

NH23.8% - 2025

NC

12.5% - 2021 (IOU)

10% - 2018 (Muni/Coop)

MO

15% - 2021

VA15% - 2025

ND

10% - 2015

SD

10% - 2015

UT

20%- 2025

OH12.5% -2025

Updated December 2010

MD 20% - 2022

DE 20% - 2019

NJ 22.5% - 2020

CT 20% - 2020

RI 16% - 2020

DC 20% - 2020

MI

10% - 2015

Detroit Ed: 600MW – 2015

Consumers: 500MW - 2015

KS

20% - 2020

*peak demand capacity

WV25% - 2025

OK

15% - 2015

LA

350 MW - 2015

There is also a national voluntary market, with some regional preferences.

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

P01018

Rectangle

The RPS Markets - Complexity

Illinois

Pennsylvania

Providence Heights - 72MW

Locust Ridge II - 102MW

•RPS eligibility rules not always reciprocal

•Create regional price variation due to supply/demand characteristics

•Still oversimplification!

New Jersey

Ohio

PH RECs eligible for PA & NJ

LRII RECs NOT eligible for IL

LRII RECs eligible for OH

PH RECs NOT eligible for OH

Eligibility rules complex ,non-intuitive, and unstable!!!

RPS Markets – Recent Developments

•Various factors contributing to reconsideration of RPS policies

oRatepayer impacts, particularly during down economy

oLack of in-state projects (i.e. local economic development benefits)

oRealization that original design may be flawed

•Specific Examples

oConnecticut contemplating reduced RPS mandate

oMassachusetts recently mandated long-term bundled contracts

oNumerous eastern states considering off-shore carve-outs

MA, RI, NY, NJ, MD, DE, NC, VA

oMissouri (rulemaking) and Indiana (legislation) not going well

oBills introduced to restructure IL RPS by adding LTC component

oOngoing saga in California (will be discussed)

Buying and Selling RECs

•Almost exclusively a bilateral market

•Most sales are short-term (spot market – 3 years)

•Brokers play major role due to lack of transparency/market fragmentation

oEx. Evolution Markets, ICAP, TFS, Spectron, Amerex, etc.

•Efforts at creating exchanges have had very limited success

oEx. Chicago Climate Futures Exchange (CCFE)

•Regulated utilities often procure via RFP process approved by commission

•Widely varying creditworthiness among counterparties

•Contract standardization limited, though various efforts have been made

oABA/ACORE/EMA, ISDA, EEI

•REC title transferred via electronic tracking system; cash settled separately

oAll 6 regional tracking systems built by same company

oAPX, Inc., which was recently purchased by NYSE Euronext

REC Tracking System – Screen Shot

Key deal terms

Term Description

Product What programs will the REC qualify for? Project specific?

Volume Are you selling a firm block, a unit contingent percent of output, etc.?

Price $/MWH

Vintage Do the RECs need to be generated during a specific time period?

Term Spot, multi-year, etc.

Delivery Will the RECs be transferred via a tracking system? When?

Payment Pre-pay vs perform?

Change in Law

Is buyer or seller subject to risk if there is a change in eligibility rules?

What if the RPS is voted down?

Default Provisions

Can seller provide replacement RECs? How are market damages

calculated?

•Characteristics of physical commodity/financial product (not a derivative)

•Somewhat unique in that value driven primarily by regulation

•Regulatory risk often at core of contract negotiations

Sample REC Confirm (NJ RPS)

Trade Date: March 21, 2011

Transaction Reference(s): ABC123

Seller: Iberdrola Renewables, Inc.

Buyer: New Jersey Utility Inc.

Product: New Jersey Class I Eligible Renewable Energy Credits (“RECs”)

Vintage(s): Reporting Year 2012 (i.e. June 2011-May 2012)

Contract Price ($/MWh): $5.00

Product Quantity: 50,000 RECs

Total Contract Price: $250,000.00

Facility: N/A

Eligible Renewable Resource Type: Any

Geography: Any

Delivery Deadline: July 15, 2012 via PJM Generation Attributes Tracking System (GATS)

*Many terms would be defined in the master, such as definition of NJ Class I REC, etc.

REC Price Overview

$-

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

Connecticut Massachusetts New Jersey Pennsylvania Texas Vol - National Vol - WECC

Historical OTC REC Prices - Select REC Markets

Current Price

*Prices are indicative and derived using broker information and simplified methodology. Near term vintages only.

• In theory, prices should equal marginal cost less energy price

• In practice, driven by short term supply/demand balance

• Regional variation, but most markets have trended lower recently

• Conventional wisdom is that in short-term, markets well supplied

• Lack of long-term liquidity due to market design/regulatory uncertainty

• Prices below reflect markets that “trade” – not value embedded in PPAs

• WARNING - Transparency limited due to low liquidity/high volatility

California – RPS Overview

•One of strongest programs in nation, but…

•Has come to define regulatory uncertainty

•Constantly under review for better part of last decade

•Three parallel RPS regimes currently relevant

oSB 107: law of the land (20% by 2020)

oExecutive Order 2-21-09: CARB/AB32 (33% by 2020)

oSBX 1-2:pending (33% by 2020)

SB 107

• Original RPS

• Passed in 2002

• 20% by 2020

• Applies to IOUs

• Administered by CEC/CPUC

• Law of land

E.O.

• Signed in 9/2009

• 20% by 2010

• 33% by 2020

• Linked to AB 32

• Administered by CARB

• Rulemaking in progress

SBX 1-2

• Sitting in Assembly

• 20% by 2013

• 33% by 2020

• Would be prevailing program

• Likely to pass soon

California RPS – REC/TRECs

•Role of REC/TRECs is a long unsettled issue in CA

•First, pending tracking system and CPUC rulemaking

•Significant political pressure to limit imports to spur in-state projects

•Interminable rulemakings, hearings, re-hearings, etc. ensued

•Nonetheless, key issues are:

oWhat counts as an unbundled TREC transaction?

oWhat percentage of RPS compliance can be met with TRECs?

•Recent CPUC decision comes to a different conclusion then pending legislation

•CARB rulemaking could come to entirely different conclusion as well.

•Pending legislation, if enacted, would prevail

California RPS – REC/TREC Issues

Recent CPUC Decision (1/13/2011)

• 25% cap on use of TRECs for RPS compliance by IOUs

• Also created $50/REC price cap

• Caps expire 12/31/2013

• TRECs essentially defined as everything but a bundled transaction

o Still a requirement that an equivalent volume of energy is delivered annually

• Bundled transaction defined as a transaction where either:

1. The RPS eligible generator’s first point of interconnection with the WECC

interconnected transmission system is with a California balancing authority,

or;

2. RPS eligible energy from the transaction is dynamically transferred to a

California balancing authority.

• No clear definition of dynamically transferred exists!!

• Existing contract grandfathered, but may count towards cap

California RPS – REC/TREC Issues

Pending Legislation (SBX 1-2)

• Increases RPS to 33% by 2020

• Creates 3 categories of RPS-eligible transactions (i.e. buckets)

• Buckets apply to all retail sellers of electricity

• Bucket 1

o Bundled transactions with projects interconnected with a CA BA

o Bundled transactions scheduled from unit directly to a CA BA

o Bundled transactions dynamically transferred into state

o Minimum of 50% by end of 2013, 65% by end 2016, 75% thereafter

• Bucket 2

o Firmed and shaped transactions providing incremental energy into CA

o Maximum of 50%, 35%, 25%

• Bucket 3

o Anything that isn’t in 1 or 2, including TRECs

o Max of 25%, 15%, 10%

• Still does not clearly define DYNAMICALLY TRANSFERRED

General Market Observations

•Defined by regulation and regulatory uncertainty

•In short term, have little impact on power prices per se

•Bimodal prices due to vertical demand curve (i.e. boom/bust)

oNotably, even in markets with banking and other flexibility mechanisms

•Dominated by short-term transactions, which limits hedge value for developers

oResult of power market structure and buyer risk aversion

•Trading/arbitrage opportunities emanate from:

o overlapping RPS eligibility, lack of transparency, regulatory inflection points

•Back-office nightmare due to lack of standardization/systems

•As developer, I would probably argue for enhanced design to stimulate LTC

Peter Toomey

Manager, Environmental Markets

1115 Broadway, 12th Floor

New York, NY 20016

(646) 770 - 1679

Questions?