Real Estate Market Report Munich - wirtschaft … · Real Estate Market Report Munich ... München...

9

11/12 Immobilienmarktbericht München Real Estate Market Report Munich Wir unterstützen die Bewerbung www.immo .de

Transcript of Real Estate Market Report Munich - wirtschaft … · Real Estate Market Report Munich ... München...

11/12Immobilienmarktbericht MünchenReal Estate Market Report Munich

Wir unterstützen die Bewerbung

www.immo .de

The Business Location of Munich

Munich – Still top even after the crisis Having success-fully weathered the financial and economic crisis, Munich remains Germany’s economically most potent city – and the one with the most attractive future prospects. National and international rankings reflecting the general economic situation, the attractiveness of real estate locations and quality of life issues all put the Bavarian capital right at the top. Munich seems to exert a magnetic pull on highly qualified and well educated people from all over Germany and beyond. The people who come here work for global players (seven of the companies listed in the DAX 30 index of Germany’s top blue-chip firms are headquartered here), established SMEs or one of the city’s countless up-and-coming start-ups. Munich’s automotive, information and communication technology, life sciences, aerospace, corporate services and financial clusters deliver a steady stream of innovative stimulus. Such favorable conditions – the proverbial “Munich mix” – are rooted in the city’s balanced and highly diverse economic structure, besides reflecting its long-standing and enviable prosperity.

Knowledge, creativity and innovation – Munich’s recipe for success Knowledge and innovation are vital resources in a world of global competition. Munich has earned itself a deserved reputation as a modern hub of technology and science and has, in the process, repeatedly reinvented itself. An impressive public and semi-public research in-frastructure, no fewer than 14 universities, the Max Planck Society, the Fraunhofer Society, the Munich Helmholtz Association and the Leibniz Association together play a key role by creating an ideal climate for innovation. Ludwig-Maximilians Universität (LMU) and Technische Universität München (TUM) are definitely in the vanguard of German and European university research. Both also occupy lead-ing positions in the battle to attract funding. In addition, some 59,000 R&D employees firmly establish the Munich Metropolitan Region (MMR) as Germany’s foremost knowl-edge region. The presence of the European Patent Office and the German Patent and Trade Mark Office naturally also facilitates the direct translation of knowledge into innovation. Local government organizations too are keen to drive innovation. By the year 2025, Stadtwerke München, the city’s utility company, plans to supply all corporate and private customers solely with electricity generated locally from renewable sources. Every private household in Munich should indeed be supplied with green power from renewable sources as early as 2015. The Bavarian capital thus aims to become the first German city to meet these ambitious power generation and climate protection goals. The support provided by the City of Munich to promote innovation draws international acclaim. The worldwide Technopolicy Network, for example, recently singled out the Munich Technology Center (MTZ) as one of the world’s leading science incubators. Over the past 16 years, more than 300 young companies have seen their businesses flourish and grow at the MTZ, creating at least 1,000 new jobs inthe process.

Openness, tolerance – and an outstanding quality of lifeA city’s attractiveness is critical to its economic success; and precious few urban centers manage to combine busi-ness with pleasure and traditional values with leading-edge dynamism the way Munich does. In 2010, Britain’s Monocle magazine picked Munich as “the world’s most livable city”. Understandably: The city on the Isar River boasts an excellent infrastructure, a low crime rate and a truly enviable quality of life. It is no wonder, then, that Munich attracts more young and skilled labor and more tourists year for year than any other German city. Visitors and residents alike find inspiration in a wealth of artistic and cultural offerings of international standing. Generously dimensioned parks and open spaces in the heart of the city, the Isar itself, nearby lakes and the stunningly beautiful Alpine foothills combine to create the perfect setting for recreation and leisure. Having hosted soccer’s FIFA World Cup in 2006, celebrated its 850th anniversary in 2008 and celebrated 200 years of the Oktoberfest in 2010, Munich is now also a candidate city for the 2018 Winter Olympic and Paralympic Games.

Der Wirtschaftsstandort München

München – auch nach der Krise wieder top

München hat die globale Finanz- und Wirtschaftskrise erfolgreich überstanden und bleibt weiterhin

Deutschlands wirtschaftsstärkste und zukunftsfähigste Großstadt. In nationalen und internationalen

Rankings zur allgemeinen Wirtschaftslage, zur Attraktivität des Immobilienstandortes oder zur

Lebensqualität ist die Stadt immer ganz vorne mit dabei. Der Wirtschaftsstandort zieht wie ein Magnet

hochqualifizierte und gut ausgebildete Arbeitskräfte aus Deutschland und dem Ausland an. Sie arbeiten

bei den Global Playern – sieben im DAX 30 notierte Unternehmen haben ihren Hauptsitz in München –, im

Mittelstand oder bei einer der vielen aufstrebenden Start-up-Firmen. Die Münchner Cluster Automotive,

Informations- und Kommunikationstechnologie, Life-Sciences, Luft- und Raumfahrttechnik, unterneh-

mensnahe Dienstleistungen und Finanzwirtschaft sorgen für nachhaltige Innovationsimpulse. Diese

günstigen Voraussetzungen, bekannt als die „Münchner Mischung“, stehen für eine ausgewogene und

vielseitige Wirtschaftsstruktur sowie ein langfristig hohes Wohlstandsniveau.

Wissen, Kreativität und Innovation – die Erfolgsfaktoren Münchens

Im globalen Wettbewerb sind Wissen und Innovation wichtige Ressourcen. München ist es gelungen,

sich als moderner Technologie- und Wissenschaftsstandort zu profilieren und immer wieder neu zu

erfinden. Dazu tragen erheblich die öffentliche und halböffentliche Forschungsinfrastruktur, die 14

Hochschulen, die Max-Planck-Gesellschaft, die Fraunhofer-Gesellschaft, das Helmholtz-Zentrum

München und die Leibniz-Gemeinschaft bei: Sie schaffen ein optimales Klima für Innovationen. Die

Ludwig-Maximilians-Universität München und die Technische Universität München zählen zu den for-

schungsstärksten Hochschulen in Deutschland und Europa. Beide Universitäten erreichen Spitzenplätze

bei der Einwerbung von Fördermitteln. Die Europäische Metropolregion München (EMM) ist zudem mit

rund 59.000 Beschäftigten im Bereich Forschung und Entwicklung Deutschlands führende Wissensre-

gion. Die direkte Umsetzung von Wissen in Innovation wird durch das Europäische Patentamt und das

Deutsche Patent- und Markenamt ermöglicht. Auch die Stadt selbst präsentiert sich als Innovationstrei-

ber. Bis zum Jahr 2025 wollen die Stadtwerke München alle Geschäfts- und Privatkunden ausschließlich

mit selbst erzeugtem Strom aus erneuerbaren Energiequellen versorgen. Bereits bis 2015 sollen alle

Münchner Privathaushalte mit Ökostrom aus erneuerbaren Energien beliefert werden. München will

damit als erste deutsche Großstadt diese Ziele der Energiegewinnung und des Klimaschutzes erfüllen.

Die Innovationsförderung der Landeshauptstadt genießt auch internationale Anerkennung. Das global

agierende Technopolicy Network hat das Münchner Technologiezentrum (MTZ) als einen der weltweit

führenden Wissenschaftsinkubatoren ausgezeichnet. Über 300 junge Betriebe sind in den vergangenen

16 Jahren im MTZ groß geworden und haben dabei mindestens 1.000 Arbeitsplätze geschaffen.

Lebensqualität kombiniert mit Offenheit und Toleranz

Die Attraktivität einer Stadt ist mitentscheidend für ihren wirtschaftlichen Erfolg. Und kaum eine Metro-

pole verbindet Arbeit mit Freizeit und Tradition mit Moderne so wie die bayerische Landeshauptstadt.

Das britische Monocle Magazin wählte München 2010 zur lebenswertesten Stadt weltweit. Nicht zu

Unrecht, denn die Stadt verfügt über eine hervorragende Infrastruktur, niedrige Kriminalitätsraten und

ein hohes Maß an Lebensqualität. München zieht so Jahr für Jahr mehr junge Fachkräfte und Touristen

an als irgendeine andere deutsche Stadt. Inspiration finden sie in einem reichhaltigen Kunst- und Kultur-

angebot von internationalem Rang. Die zahlreichen Parks und Grünflächen direkt in der Stadt, die Isar,

die oberbayerischen Seen sowie die reizvolle Voralpenlandschaft sind ein optimales Umfeld für Freizeit

und Erholung. Nach den Großereignissen FIFA Weltmeisterschaft 2006, 850. Stadtgeburtstag im Jahr

2008 und 200 Jahre Oktoberfest 2010 ist München Candidate City für die Olympischen und Paralym-

pischen Winterspiele 2018.

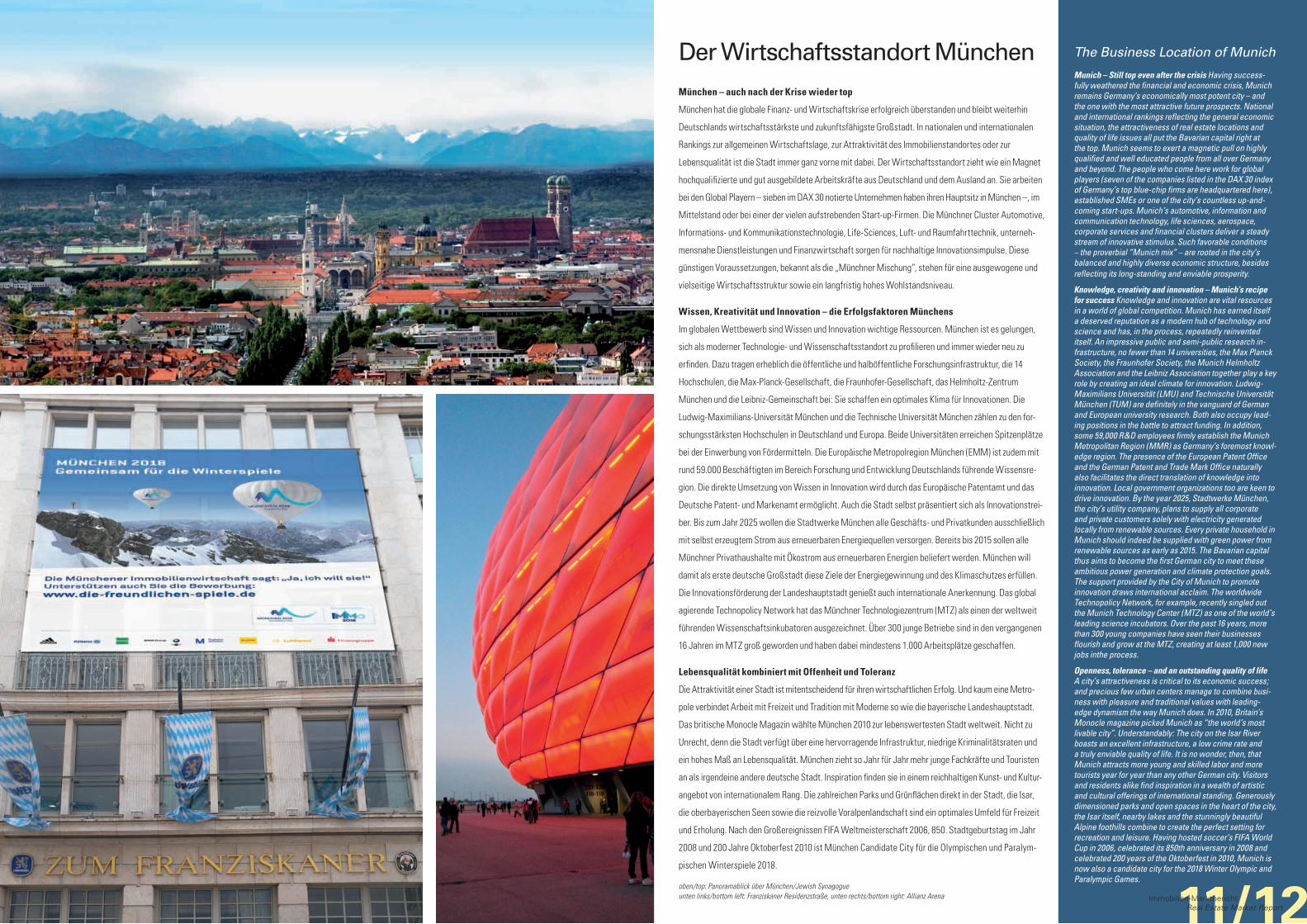

oben/top: Panoramablick über München/Jewish Synagogueunten links/bottom left: Franziskaner Residenzstraße, unten rechts/bottom right: Allianz Arena 11/12Immobilien-Marktbericht

Real Estate Market Report

Market Conditions

Munich remains the German city with the brightest future prospects. Witness the latest city ranking list pub- lished by INSM (the Initiative New Social Market Eco-nomy) in cooperation with influential business weekly WirtschaftsWoche. And, also, the Future Atlas plotted every three years by business research firm Prognos AG comes to exactly the same conclusion. The City of Munich scores particularly high marks for its forceful competitive edge, its impressive purchasing power and its proven in-novative capabilities. Then there is the fact that Munich’s jobless rate – around 5 percent – is the lowest of any German major city. More than a million employees pay compulsory social insurance contributions in Munich, a close second to Berlin as the country’s largest venue for regular employment.To continue to thrive in global competition, it is impor-tant to be perceived by the international community as an important and successful business region. That is precisely the reason why the City of Munich and its outlying districts and counties joined forces to form the Munich Metropolitan Region (MMR). The MMR pools the resources and energies of the public sector, various chambers, the business community, society at large and the scientific community. Accounting for 44 percent of Bavaria’s population and nearly 50 percent of its GDP, this region is unquestionably the economic engine of the Free State. The MMR’s strong position within Germany is like-wise reflected in the latest Prognos Future Atlas, whichinvestigated the sustainable future outlook for all 412 districts and counties in Germany. Of the 30 member regions that make up the MMR, 20 ranked among the top 80 districts and counties in Germany with regard to their future prospects.Bucking the national trend, Munich is also forecast to experience significant population growth. The Bavarian capital set a new birth record in 2010. Over the next 20 years, the number of residents is projected to increase by nearly 11 percent to 1.5 million. A substantial chunk of this growth will be attributable to inward migration both from other parts of Germany and from abroad. Well educatedyoung people between the ages of 18 and 30 in particular are keen to move to the Bavarian metropolis.Such considerable net inward migration confronts the city in general and the real estate industry in particular with major challenges. Despite the efforts of “Wohnen in München” (Living in Munich), the country’s largest local government housing construction program, housing in the city is growing scarce. Permission was granted for the construction of 7,000 new dwellings in 2010; fewer than half were actually built, however.A total of 13,000 homes are now in planning or under construction in 2011. The biggest individual projects include Freiham Nord (approximately 3,000 homes), the conversion of the former industrial estate on Paul-Ger-hardt-Allee (2,000 homes) and the revitalization of former military barracks. Right now, the City of Munich has suitable plots of land capable of accommodating around 50,000 new homes.In January 2011, application company München 2018 submitted its bid book for the 2018 Winter Olympic and Paralympic Games to the International Olympic Committee (IOC). The decision will be taken on July 6, 2011. Should the region’s bid win, Munich would become the first city in the world ever to host both the Summer and Winter Olympic Games. As with the 1972 Summer Olympics, the city and its residents stand to gain enor-mous and lasting benefits. Construction of the Olympic village alone would create 1,300 new apartments, built to the very highest ecological standards. Moreover, what German automobile association ADAC already describes as the best regional traffic network in Europe would be further optimized. Some of the plans to expand the main commuter rail line between Isartor and Laim have already been concluded.

Die MarktbedingungenMünchen bleibt die deutsche Großstadt mit den besten Zukunftsaussichten. Das belegen sowohl der

aktuelle Städtevergleich der Initiative Neue Soziale Marktwirtschaft (INSM) in Kooperation mit der

WirtschaftsWoche als auch der alle drei Jahre erscheinende Zukunftsatlas des Wirtschaftsforschungs-

unternehmens Prognos AG. Die Landeshauptstadt konnte vor allem durch ihre gute Wettbewerbsfähig-

keit, die hohe Kaufkraft und ihre Innovationsstärke überzeugen. Hinzu kommt, dass München mit rund

5 Prozent die niedrigste Arbeitslosenquote unter den deutschen Metropolen hat. Mit über einer Million

sozialversicherungspflichtig Beschäftigten ist der Arbeitsamtsbezirk München knapp hinter Berlin der

zweitgrößte Beschäftigungsstandort Deutschlands.

Um im globalen Wettbewerb bestehen zu können, ist es wichtig, international als bedeutende und

erfolgreiche Wirtschaftsregion wahrgenommen zu werden. Aus diesem Grund hat die Landeshauptstadt

zusammen mit den umliegenden Landkreisen und kreisfreien Städten die Europäische Metropolregion

München (EMM) gegründet. Die EMM bündelt Kräfte aus öffentlicher Hand, Kammern, Wirtschaft,

Gesellschaft und Wissenschaft. Mit 44 Prozent der Bevölkerung und knapp 50 Prozent des BIP ist die

Region der Wirtschaftsmotor Bayerns. Wie stark die EMM innerhalb Deutschlands aufgestellt ist, zeigt

der aktuelle Prognos Zukunftsatlas, in dem alle 412 deutschen Kreise und kreisfreien Städte auf ihre

Zukunftsfähigkeit geprüft wurden. Von den insgesamt 30 EMM-Mitgliedsregionen kamen 20 unter die

besten 80 Kreise Deutschland mit hohen bis besten Zukunftschancen.

Entgegen dem allgemeinen Bundestrend wird München weiterhin ein deutliches Bevölkerungswachs-

tum prognostiziert. Im Jahr 2010 schaffte die Landeshauptstadt wieder einen neuen Geburtenrekord

und in den nächsten 20 Jahren soll die Einwohnerzahl um knapp 11 Prozent auf 1,5 Millionen ansteigen.

Ein beträchtlicher Anteil dieses Wachstums erfolgt auch durch Zuwanderung aus anderen Regionen

Deutschlands und aus dem Ausland. Besonders junge und gut ausgebildete Leute zwischen 18 und 30

Jahren zieht es in die bayerische Metropole. Das hohe Zuwanderungsplus stellt die Stadt und die

Immobilienwirtschaft vor besondere Herausforderungen. Trotz des größten kommunalen Wohnungs-

bauprogramms „Wohnen in München“ wird der Wohnraum in der Landeshauptstadt knapp. Die Stadt

hat 2010 Genehmigungen für 7.000 Wohnungen ausgewiesen. De facto wurden jedoch weniger als die

Hälfte gebaut.

Für 2011 sind insgesamt 13.000 Wohnungen in Planung und Bau. Zu den größten Einzelobjekten zählen

der Wohnstandort Freiham Nord mit ca. 3.000 Wohnungen, die Umwandlung des bisherigen Gewerbe-

gebietes an der Paul-Gerhardt-Allee in ein Wohngebiet mit 2.000 Wohnungen und die Flächenrevita-

lisierung ehemaliger Kasernenareale. Aktuell besteht in der Stadt ein Gesamtangebot an geeigneten

Grundstücken für rund 50.000 Wohnungen.

Im Januar 2011 hat die Bewerbungsgesellschaft München 2018 ihr Bid Book für die Olympischen und

Paralympischen Winterspiele 2018 dem Internationalen Olympischen Komitee (IOC) vorgelegt. Am

6.Juli 2011 wird die Entscheidung fallen. Bei einem Zuschlag wäre München der erste Austragungsort

der Welt, in dem sowohl Sommer- als auch Winterspiele abgehalten wurden. Die Stadt und ihre Ein-

wohner könnten wie bereits bei der Olympiade 1972 davon auch langfristig enorm profitieren. Durch

den Bau des olympischen Dorfes würden 1.300 neue Wohnungen auf höchstem ökologischem Niveau

entstehen. Zudem wird das ohnehin schon laut einer ADAC-Studie beste Nahverkehrsnetz Europas

noch weiter optimiert werden. Für den Ausbau der Stammstrecke zwischen Isartor und Laim sind die

Planungen zum Teil schon abgeschlossen.

0

200000

400000

600000

800000

1000000

1200000

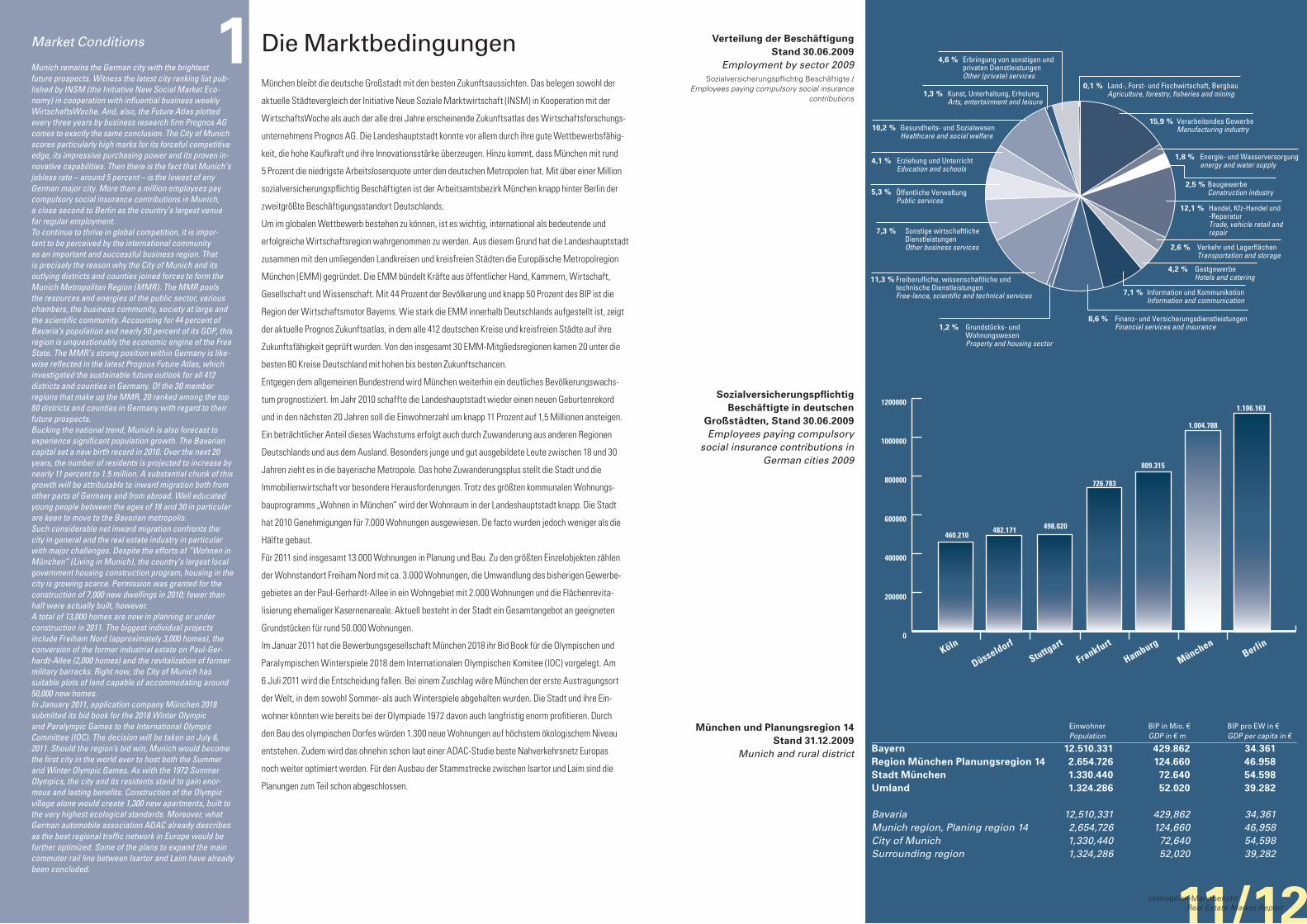

460.210 482.171 498.020

726.783

809.315

1.004.788

1.106.163

Köln

Düsseldorf

Stuttgart

Frankfurt

Hamburg

MünchenBerlin

0,1 %

Land-, Forst- und Fischwirtschaft, BergbauAgriculture, forestry, fisheries and mining

15,9 %

Verarbeitendes GewerbeManufacturing industry

2,5 % Baugewerbe Construction industry

12,1 % Handel, Kfz-Handel und -ReparaturTrade, vehicle retail and repair

4,2 % GastgewerbeHotels and catering

7,1 % Information und KommunikationInformation and communication

11,3 % Freiberufliche, wissenschaftliche und technische DienstleistungenFree-lance, scientific and technical services

4,6 % Erbringung von sonstigen und privaten DienstleistungenOther (private) services

1,3 % Kunst, Unterhaltung, ErholungArts, entertainment and leisure

4,1 % Erziehung und UnterrichtEducation and schools

5,3 % Öffentliche VerwaltungPublic services

10,2 % Gesundheits- und SozialwesenHealthcare and social welfare

8,6 % Finanz- und VersicherungsdienstleistungenFinancial services and insurance1,2 % Grundstücks- und

WohnungswesenProperty and housing sector

7,3 % Sonstige wirtschaftliche DienstleistungenOther business services

1,8 % Energie- und Wasserversorgungenergy and water supply

2,6 % Verkehr und Lagerflächen Transportation and storage

1 Verteilung der Beschäftigung Stand 30.06.2009

Employment by sector 2009Sozialversicherungspflichtig Beschäftigte /

Employees paying compulsory social insurance contributions

Sozialversicherungspflichtig Beschäftigte in deutschen

Großstädten, Stand 30.06.2009Employees paying compulsory

social insurance contributions in German cities 2009

München und Planungsregion 14 Stand 31.12.2009

Munich and rural district

Einwohner BIP in Mio. € BIP pro EW in € Population GDP in € m GDP per capita in €

Bayern 12.510.331 429.862 34.361Region München Planungsregion 14 2.654.726 124.660 46.958Stadt München 1.330.440 72.640 54.598Umland 1.324.286 52.020 39.282

Bavaria 12,510,331 429,862 34,361Munich region, Planing region 14 2,654,726 124,660 46,958City of Munich 1,330,440 72,640 54,598Surrounding region 1,324,286 52,020 39,282

11/12Immobilien-Marktbericht Real Estate Market Report

�

�

�

�

=

=

Garmisch-P.

Salzburg

Lind

auA

ugsb

urg,

Stu

ttga

rtAB-Kreuz Neufahrn Berlin, NürnbergS2

S5

S4

S3

MÜNCHEN

STARNBERG

DACHAU

Germering

Unter-schleißheim

Karlsfeld

Gröben- zell

Gräfelfing

GautingUnter-haching Ottobrunn

Haar

Grasbrunn

Ismaning

Garching

Taufkirchen

Oberhaching

Unter-

Feldkirchen

föhring

b. München

-

-

471

2

AB-Dr. M.-Feldmoching

AB-Kr. M.-Nord

AB-Dr.Starnberg

AB-Kr. M. Brunnthal

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

SS

S

S

S

S

S

S

S

S

S

S S

S

S

S S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

S

SS

S

S

S

S

S S

S

S

S

S

S

S

S

S

S

92 9

8

8

95

96

Messe

AB-Kr.M.-Ost

94

99

E52

Altstadtring

Mittlerer Ring

Mittlerer Ring

Schwabing

Neuhausen

EnglischerGarten

Bogenhausen

Nymphenburg

PasingLaim

Sendling

Perlach

Giesing

0 1 2 5 km3 4

N

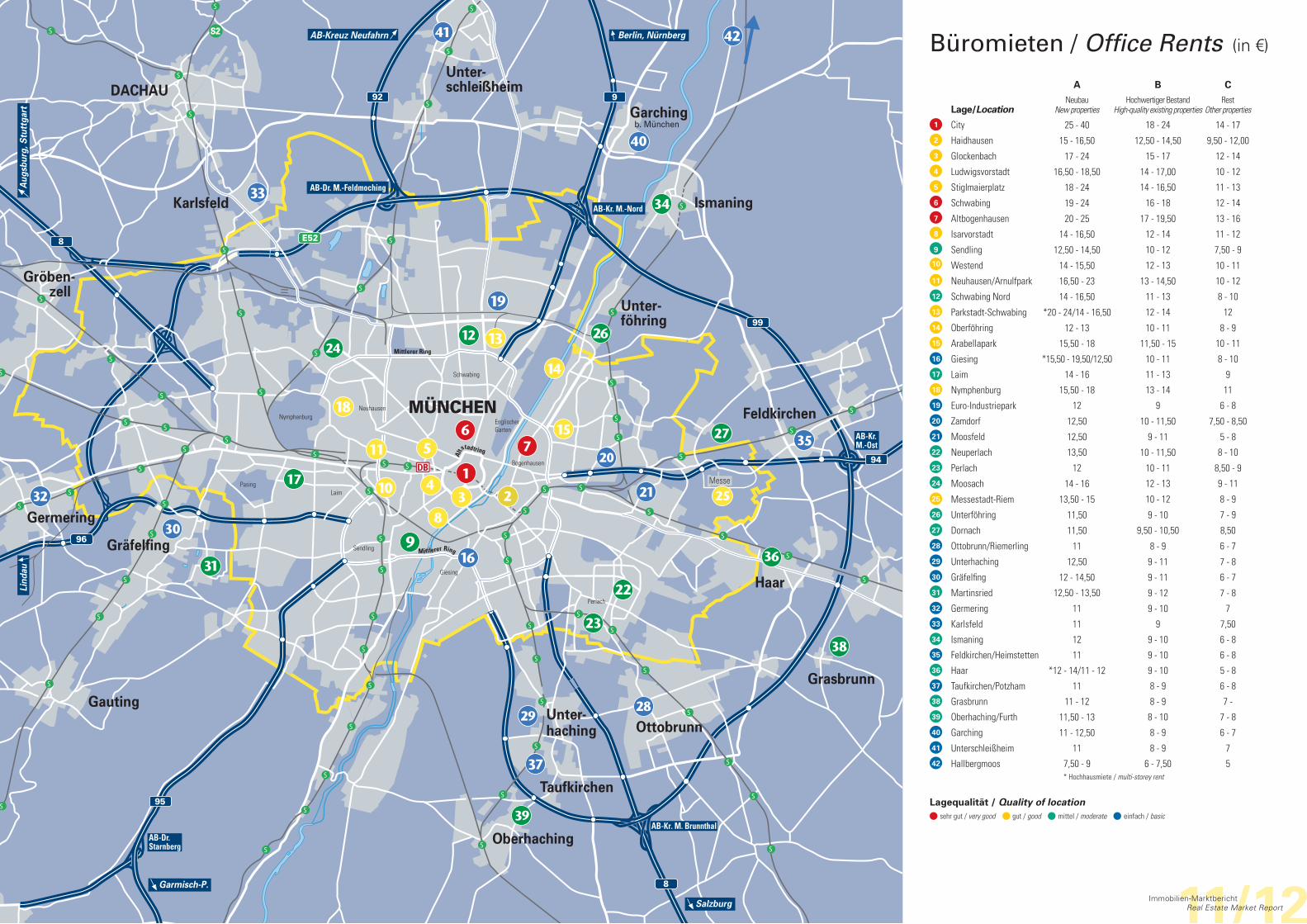

Büromieten / Office Rents (in u)

* Hochhausmiete / multi-storey rent

Lagequalität / Quality of location sehr gut / very good gut / good mittel / moderate einfach / basic

11/12Immobilien-Marktbericht Real Estate Market Report

A B C

Lage/LocationNeubau

New propertiesHochwertiger Bestand

High-quality existing propertiesRest

Other properties

1 City 25 - 40 18 - 24 14 - 172 Haidhausen 15 - 16,50 12,50 - 14,50 9,50 - 12,003 Glockenbach 17 - 24 15 - 17 12 - 144 Ludwigsvorstadt 16,50 - 18,50 14 - 17,00 10 - 125 Stiglmaierplatz 18 - 24 14 - 16,50 11 - 136 Schwabing 19 - 24 16 - 18 12 - 147 Altbogenhausen 20 - 25 17 - 19,50 13 - 168 Isarvorstadt 14 - 16,50 12 - 14 11 - 129 Sendling 12,50 - 14,50 10 - 12 7,50 - 910 Westend 14 - 15,50 12 - 13 10 - 1111 Neuhausen/Arnulfpark 16,50 - 23 13 - 14,50 10 - 1212 Schwabing Nord 14 - 16,50 11 - 13 8 - 1013 Parkstadt-Schwabing *20 - 24/14 - 16,50 12 - 14 1214 Oberföhring 12 - 13 10 - 11 8 - 915 Arabellapark 15,50 - 18 11,50 - 15 10 - 1116 Giesing *15,50 - 19,50/12,50 10 - 11 8 - 1017 Laim 14 - 16 11 - 13 918 Nymphenburg 15,50 - 18 13 - 14 1119 Euro-Industriepark 12 9 6 - 820 Zamdorf 12,50 10 - 11,50 7,50 - 8,5021 Moosfeld 12,50 9 - 11 5 - 822 Neuperlach 13,50 10 - 11,50 8 - 1023 Perlach 12 10 - 11 8,50 - 924 Moosach 14 - 16 12 - 13 9 - 1125 Messestadt-Riem 13,50 - 15 10 - 12 8 - 926 Unterföhring 11,50 9 - 10 7 - 927 Dornach 11,50 9,50 - 10,50 8,5028 Ottobrunn/Riemerling 11 8 - 9 6 - 729 Unterhaching 12,50 9 - 11 7 - 830 Gräfelfing 12 - 14,50 9 - 11 6 - 731 Martinsried 12,50 - 13,50 9 - 12 7 - 832 Germering 11 9 - 10 733 Karlsfeld 11 9 7,5034 Ismaning 12 9 - 10 6 - 835 Feldkirchen/Heimstetten 11 9 - 10 6 - 836 Haar *12 - 14/11 - 12 9 - 10 5 - 837 Taufkirchen/Potzham 11 8 - 9 6 - 838 Grasbrunn 11 - 12 8 - 9 7 - 39 Oberhaching/Furth 11,50 - 13 8 - 10 7 - 840 Garching 11 - 12,50 8 - 9 6 - 741 Unterschleißheim 11 8 - 9 742 Hallbergmoos 7,50 - 9 6 - 7,50 5

DemandCompanies in the consulting sector generated the greatest demand in 2010, in terms of both the amount of space leased (about 146,000 m², or approximately 25.2% of total take-up of space) and the number of new leases signed (233 new leases, or 27.8% of all leases signed during the period). Companies in the information and telecommunications sectors followed, accounting for some 124,500 m² of office space taken up (21.5% of the total volume) and 145 new leases recorded (17.3% of all leases signed), trailed by manufacturing-sector companies, which accounted for nearly 58,900 m² of newly leased space (10.2% of total take-up of space) and 76 signed leases (percentage of the total: 9.1%). While the volume of requests for the full year 2009 was just under 900,000 m², the figure rose slightly, by 3.6%, to about 932,000 m² by the end of 2010. Viewed on a quarterly basis, it is striking to note that new requests showed little variation by quarter, ranging from 230,000 to 250,000 m². By com-parison with the previous year, when new requests totaling about 280,000 m² were registered in the first quarter, but the figure had dwindled to only about 170,000 m² by the final quarter of the year, this serves as further indication that the Munich leasing market has regained some degree of continuity. The quality of the requests has also risen from the previous year, further evidence that businesses have emerged from their reluctance to make decisions.

Rental pricesThe average rent for the entire Munich market area, adjusted for available space, is n13.98/m² as of the end of 2010. Measured by the first six months of the year, the figure slid only slightly, by just 4 cents per m², but it represents a more significant gain, of 58 cents per m², from the previous year. The focus on city center locations among customers, and the generally higher level of rents in those locations, are evident in this figure. Some users obviously seized a favorable opportunity and used the pronounced buyer’s market conditions to lease space in the area bounded by the Mittlerer Ring or the Altstadtring on attractive terms and conditions, a situation that is not always reflected in a low nominal contractual rent alone. A detailed consideration of the different loca-tions bears out this general impression: The rent level in the surrounding areas has softened by some 5%, or 52 cents per m², to n 9.75/m² since the first half of 2010, while in the city center, for instance (sub-segment 1), the rent level rose from n 19.76/m² to n 19.88/m² during the same period. The prime rent has fallen by n 1.50/m², to n 28.00/m², since the start of 2010. While various new leases were signed at rents considerably higher than n 20/m² in 2010, some of them for large spaces, there was hardly any sign of absolute top rents like those reached in years past. The top value was represented by two new leases for smaller spaces in the city center of Munich, each of them atn 35.00/m².

Summary and forecastThe positive development of take-up of space in 2010, especially in the second half of the year, meant that the Munich office leasing market closed the year better than expected at the start of the year. Since the overall economic situation in Ger- many – and with it, the situation in the business sector – has developed much bet-ter than many had expected, we assume that if the positive mood holds, the trend will also be reflected in figures for take-up of office space in 2011. We expect to see take-up volume of 570,000 m² to 610,000 m², including owner-occupants. Va-cancy rates are also expected to decline again in the coming year, since relatively little newly constructed space that has not yet been leased will be completed

during this period.

Flächenumsatz

Für den Münchener Büroflächenmarkt kann rückblickend auf das Jahr 2010 eines fest-

gestellt werden: Während das erste Halbjahr mit einem Büroflächenumsatz (inkl. Eigen-

nutzerumsatz) von 255.900 m² bzw. einem Vermietungsumsatz (exkl. Eigennutzerum-

satz) von 251.700 m² noch einige Prozentpunkte unter den Vorjahreswerten rangierte,

hat die Umsatztätigkeit im zweiten Halbjahr deutlich an Fahrt gewonnen. Im Vorjahres-

vergleich stehen nunmehr ein Plus von 9,4 % beim Flächenumsatz (578.400 m²) und

sogar ein Plus von 12,4 % beim Vermietungsumsatz (564.800 m², exkl. Eigennutzerum-

satz) zu Buche. Die differenzierte Umsatzentwicklung im Jahresverlauf ist durch die zu-

nehmende Zuversicht auf Unternehmerseite zu erklären. Anders als noch zu Jahresbe-

ginn ist offensichtlich vielerorts wieder mehr Planungssicherheit über eigene Umsätze

und die allgemeine wirtschaftliche Entwicklung eingekehrt, was es umzugswilligen

Unternehmen einfacher gemacht hat, Entscheidungen zu treffen. Ein Trend hat sich

dabei über den Jahresverlauf nicht nur manifestiert, sondern kontinuierlich verstärkt.

Die Lagen innerhalb des Mittleren Rings (Teilmärkte 1 bis 5) haben zunehmend Zu-

spruch seitens der Mieter erfahren, sodass am Ende dieses Jahres annähernd 47 %

allen Flächenumsatzes hier stattgefunden hat. Zum Halbjahr lag dieser Wert noch bei

knapp 43 %, im Jahr 2009 bei nicht ganz 42 %. Aus den sonstigen Stadt- und Umland-

lagen konnte vor allem das nordöstliche Umland hervortreten. Hier wurden knapp

79.200 m² Bürofläche umgesetzt. Den Umsatzschwerpunkt bildeten insbesondere die

kleineren Flächeneinheiten bis 500 m². Auf diese entfielen knapp 140.000 m² des

Büroflächenumsatzes (Umsatzanteil: 24 %). Dicht dahinter folgen nahezu gleichauf

die Größenbereiche 500 m² bis 1.000 m² und 1.000 m² bis 2.000 m², welche rd.

124.000 m² bzw. rd. 125.500 m² des Flächenumsatzes generierten (Umsatzanteil:

21,4 % bzw. 21,7 %). Größere Vermietungen über 5.000 m² gab es zwölf an der Zahl,

wobei die Anmietung der Scout 24 Holding GmbH aus dem ersten Quartal die größte

geblieben ist.

Angebot und Leerstand

Da der überwiegende Anteil bereits fertiggestellter und noch unvermieteter Neubau-

flächen in den ersten sechs Monaten des Jahres 2010 auf den Markt gelangte, war bis

zu diesem Zeitpunkt auch der größte Leerstandsanstieg zu verzeichnen. Die Leerstands-

quote erhöhte sich seit Jahresbeginn um 0,5 % und liegt seit Mitte des Jahres konstant

bei 7,9 %. In absoluten Zahlen ausgedrückt heißt dies, dass auf dem Münchener Büro-

flächenmarkt aktuell rd. 1,76 Mio. m² Fläche (inkl. Untermietflächen) kurzfristig zur An-

mietung stehen. Das Flächenpotenzial – also jene Büroflächen, die innerhalb von drei

bis zwölf Monaten bezogen werden können – hinzugerechnet, summiert sich das Ge-

samtangebot auf gut 1,96 Mio. m² Bürofläche. Im Vergleich zum Vorjahresstand hat sich

dieser Wert um gut 116.000 m² oder rd. 5,5 % verringert! Der Gesamtbüroflächenbe-

stand in München und im Umland von heute rd. 22,26 Mio. m² wird sich im kommen-

den Jahr allerdings nochmals um annähernd 177.000 m² erhöhen. Mit ca. 68 % ist der

größte Teil dieser Neubauflächen bereits vorvermietet oder für die Eigennutzung be-

stimmt. Bei einer anhaltend positiven Entwicklung der Büroflächenumsätze ist des-

wegen zu erwarten, dass der bislang noch vakante Teil dieser Flächen Abnehmer

finden wird und sich die Leerstandsquote im Laufe des kommenden Jahres wieder ab-

senkt. Von einer anhaltenden Überproduktion an Büroflächen ist somit für 2011 und aus

heutiger Sicht auch für 2012 nicht mehr zu sprechen.

Büromarkt München 2011

Nachfrage

Unternehmen aus dem Beratungsumfeld haben im Jahr 2010 sowohl in Bezug auf die

angemietete Fläche (rd. 146.000 m² bzw. rd. 25,2 % Umsatzanteil) als auch die Anzahl

abgeschlossener Mietverträge betreffend (233 Anmietungen bzw. 27,8 % aller Miet-

verträge) für die meiste Nachfrage gesorgt. Es folgen mit gut 124.500 m² Büroflächen-

umsatz (21,5 % Umsatzanteil) und 145 registrierten Anmietungen (17,3 % aller Miet-

verträge) Unternehmen aus der Informations- und Telekommunikationsbranche sowie

Unternehmen aus dem verarbeitenden Gewerbe mit annähernd 58.900 m² neu an-

gemieteter Flächen (10,2 % Umsatzanteil) und 76 geschlossenen Mietverträgen (Anteil

an allen Mietverträgen: 9,1 %). Lag das über das Gesamtjahr aufgelaufene Gesuchs-

volumen Ende 2009 noch knapp unter 900.000 m², hat sich dieses Ende 2010 leicht

um 3,6 % auf rd. 932.000 m² erhöht. In der quartalsweisen Betrachtung fällt auf, dass

die Summe der Neuanfragen nur wenig schwankend zwischen 230.000 bis 250.000 m²

liegt. Verglichen mit dem Vorjahr, in dem im ersten Quartal in Summe noch rd. 280.000 m²

Neugesuche registriert wurden und im Schlussquartal nur mehr ca. 170.000 m², ist

auch dies ein Hinweis darauf, dass sich wieder mehr Kontinuität am Münchener Ver-

mietungsmarkt eingestellt hat. Zudem ist im Vorjahresvergleich eine gestiegene Ge-

suchsqualität zu konstatieren, die in der Regel zeitnah zu Anmietentscheidungen führt.

Mietpreise

Die flächengewichtete Durchschnittsmiete für das gesamte Münchener Marktgebiet

liegt am Ende des Jahres 2010 bei 13,98 K/m². Gemessen an den ersten sechs Monaten

des Jahres hat sich diese nur unwesentlich um 4 Cent/m² abgesenkt. Im Vorjahresver-

gleich ist sie dagegen um 58 Cent/m² deutlich angestiegen. Hier macht sich die Fokus-

sierung der Nachfrager auf die Zentrumslagen und das dort allgemein höhere Miet-

niveau bemerkbar. Offensichtlich haben einige Nutzer die Gunst des ausgeprägten

Nachfragermarktes genutzt, um Flächen innerhalb des Mittleren Rings oder des Alt-

stadtrings zu attraktiven Konditionen anzumieten, die sich nicht immer nur in einer

nominal günstigen Vertragsmiete widerspiegeln. Dieser Eindruck bestätigt sich, wenn

die Lagen differenziert betrachtet werden: Das Mietniveau in den Umlandlagen hat seit

dem ersten Halbjahr 2010 um gut 5 % oder 52 Cent/m² auf 9,75 K/m² nachgegeben,

wohingegen etwa im Zentrum (Teilmarkt 1) das Mietniveau im gleichen Zeitraum von

19,76 K/m² auf 19,88 K/m² angestiegen ist. Die Spitzenmiete hat seit Jahresbeginn

2010 um 1,50 K/m² auf 28,00 K/m² nachgegeben. Zwar gab es in 2010 verschiedene,

z.T. auch großflächige Anmietungen, welche deutlich über 20 K/m² lagen, absolute

Höchstmieten wie sie in vergangenen Jahren erreicht wurden, waren jedoch kaum zu

verzeichnen. Den festgestellten Topwert bildeten zwei Anmietungen kleinerer Flächen

im Zentrum Münchens mit jeweils 35,00 K/m².

Fazit und Prognose

Durch die positive Umsatzentwicklung insbesondere im zweiten Halbjahr 2010 konnte

der Bürovermietungsmarkt Münchens etwas besser abschließen als noch zu Jahresbe-

ginn angenommen. Da sich die allgemeine wirtschaftliche Situation Deutschlands und

damit einhergehend auch die Lage der Unternehmen sehr viel besser entwickelt hat

als von vielen angenommen, rechnen wir damit, dass sich bei anhaltend guter Stimmung

dies auch in den Büroflächenumsätzen 2011 widerspiegeln wird. Wir erwarten ein Um-

satzvolumen von 570.000 m² bis 610.000 m² inklusive Eigennutzern. Für das kommende

Jahr ist zudem davon auszugehen, dass sich die Leerstandsquote wieder nach unten

bewegen wird, da nur vergleichsweise wenige bislang noch unvermietete Neubauflä-

chen fertiggestellt werden.

METRIS, Lage/Location: Arnulfpark PALAIS AN dER OPER, Lage/Location: Zentrum

2

Munich Office Space Market 2011

Take-up of spaceFor the Munich market for office space, one thing is clear when we look back over the year 2010: While the first half of the year came in a few percentage points below the previous year’s values, with total take-up of office space (in- cluding by owner-occupants) at 255,900 m² and take-up of leased space (not including owner-occupants) at 251,700 m², take-up activities gained consider-able momentum in the second half of the year. Annual figures now show year- on-year gains of 9.4% in take-up of space (578,400 m²) and an even bigger climb of 12.4% in leasing take-up (564,800 m², excluding take-up of space by owner-occupants). The varied picture for take-up of space over the year is due to increasing confidence in the business sector. In contrast to the uncertainty that was still prevalent at the start of the year, many sectors have evidently seen a return to greater certainty for longer-term planning purposes regarding their own sales volumes and the development of the economy as a whole, which has made decisions easier for companies planning to relocate. Over the course of the year, one trend not only made its mark, but continued to gain ground. Locations within the Mittlerer Ring (sub-segments 1 through 5) became increasingly popular with tenants, so by the end of the year, nearly 47% of all space taken up in 2010 was in this area. At midyear, the figure was just under 43%, up from nearly 42% in 2009. The area to the northeast of the city was a particular highlight among the other urban locations and surrounding areas, with nearly 79,200 m² of office space taken up there.Take-up activities focused in particular on smaller units of up to 500 m², which accounted for almost 140,000 m² of all office space taken up (percentage of take-up: 24%). This segment is closely followed by two other size ranges, nearly tied: 500 m² to 1,000 m², at about 124,000 m² overall (percentage: 21.4%), and 1,000 m² to 2,000 m², generating about 125,500 m² of the total volume (21.7%). There were twelve larger leases signed for more than 5,000 m² of space, with the lease signed by Scout 24 Holding GmbH in the first quarter emerging as the largest such transaction of the year.

Supply and vacancy rateSince the majority of the newly constructed space that had already been com- pleted but had not yet been leased came onto the market during the first six months of the year, the largest increase in vacancies also took place in the same period. The vacancy rate rose by 0.5% from the start of the year, and has been holding steady at 7.9% since midyear. Expressed in absolute figures, that means that the Munich office space market currently has about 1.76 million m² of space (including space available for subleasing) available for leasing in the short term. If we add the potential space – meaning those office spaces available for occu- pancy within three to twelve months – the total supply comes to some 1.96 million m² of office space, a drop of some 116,000 m², or about 5.5%, from the previous year. At the same time, however, the total volume of existing office space in Munich and the surrounding area, currently about 22.26 million m², is expected to rise again in the coming year, this time by nearly 177,000 m². The majority of this newly construc- ted space, about 68%, has already been leased in advance or is intended for owner occupancy. As a result, we expect that if take-up of office space continues to rise, tenants will be found for the portion of this space that is currently still vacant, driv- ing the vacancy rate back down in the course of the year. That means that the situ-ation can no longer be said to involve continued overproduction of office space – either for 2011 or, as things currently stand, even for 2012.less expected to grow. 11/12Immobilien-Marktbericht

Real Estate Market Report

The Market for Building Land

The market for commercial building land in Munich was noticeably more active in 2010 than during the same period of the previous year, and experienced growth for the first time since 2007. The advisory committee of the City of Munich documented 27 contracts of sale; 21 of these properties were in the office and commercial building segment. Turnover and take-up have trebled in comparison to 2009. The supply of commercial and industrial sites in Munich changed very little in 2010; in the previous year relatively few structural plans for large sites came into force. Residential construction contin-ued to play the most significant role in the market for building land. The steady influx of population to the city of Munich means that planning permission for new housing must is re-quired on an ongoing basis. The demand for owner-occupier flats, overwhelming from private investors, continues to be high; this means that demand from building contractors and project developers for residential sites in the city of Munich also remains high. This is due, not least, to favourable interest rates and limited supply. This imbalance in 2010 led to sub-stantial increases in prices (turnover: plus 28 %) and take-up (plus 44 %) for residential sites. Retail development sites in Munich and in the Munich metropolitan area are also enjoy-ing ongoing high demand. Planning permission, especially in Munich, is strictly regulated by the authorities, which leads to a low supply of suitable sites.

The Investment Market

There was a significant increase in transaction volume of 27 % compared to the previous year. Two-thirds of all registered transactions took place in the second half of 2010. The total volume of activated investments in commercial properties was € 1.715 billion, while investment in residential properties attained a transaction volume of € 579 million. The majority of investment in 2010 was in the range up to € 15 million. The average transaction throughout the year was thus only around €15.3 million. Last year, most of the demand concentrated on low-risk core and core-plus properties. Very little opportunistic investment was recorded. The main turnover generators in 2010 were private investors, family offices and high-equity open and closed funds. Around € 421 million of the transaction volume (percentage of turnover: 24.5 %) was attributed to pri- vate investors and family offices; for diverse funds this was around € 530 million of the overall amount invested (percent-age of turnover: 30.9 %). When it came to the property sales, the spotlight was on building contractors and developers. These sold properties and sites to a value of around € 428 mil-lion and thus attained around one-quarter of all turnover. This was followed by pension funds with around € 330 million and private and family offices with a total sales volume of around € 228 million. In 2010 commercial properties continued to be the most popular asset class. With an investment volume of just under € 1.09 billion and almost 64 % of turnover, these con- stituted the highest contribution to total transaction sales by far. Almost all investment was in fully-let or almost fully-let properties in central locations in Munich. Initial return on in- vestment was in the area of 4.40 % to 6.35 %. With six regis-tered investments and just under 11% of turnover (investment volume: € 182 million) retail properties were the next most pop-ular investment properties. The highest return on investment attained for premium office properties was 4.5 % at the end of 2010 was thus 25 base points below the level of the beginning of the year. The same applied for top return on investment for retail properties. This was 4.25 % at the beginning of the year; it is now 25 base points lower. The perspective for 2011 pro-vides grounds for optimism. Investment by foreign investors has now increased significantly, with investments up to € 30 million. With regard to the continuing favourable interest rates in 2011 and a reactivating economy as well as an investment volume of up to € 1 .9 billion, we are of the opinion that we will see more opportunistic investment in 2011.

Der Investmentmarkt

Die Steigerung des Transaktionsvolumens ist 2010 mit einem Plus von etwa 27 % gegenüber dem Vorjahr

deutlich ausgefallen. Zwei Drittel aller registrierten Transaktionen fand dabei im zweiten Halbjahr 2010

statt: Das Gesamtvolumen getätigter Investments in gewerblich genutzte Immobilien beläuft sich auf gut

1,715 Mrd. K, wobei Investments in Wohnimmobilien für nochmals rd. 579 Mio. K Transaktionsumsatz

sorgten. Die meisten Investments fanden 2010 in einem Bereich bis 15 Mio. K statt. Die durchschnittliche

Transaktionsgröße lag im Jahresverlauf so auch nur bei ca. 15,3 Mio. K. Im abgelaufenen Jahr konzen-

trierte sich ein Großteil der Nachfrage auf risikoarme Core- und Core-Plus-Immobilien. Opportunistische

Investments waren nur ganz eingeschränkt zu verzeichnen. Zu den Hauptumsatzträgern zählten 2010 vor

allem Privatinvestoren, Family-Offices und eigenkapitalstarke offene und geschlossene Fonds. Auf die

Gruppe der Privatanleger und Family-Offices entfielen etwa 421 Mio. K des Transaktionsvolumens (Um-

satzanteil: 24,5 %), die diversen Fonds kamen sogar auf rd. 530 Mio. K Gesamtanlagesumme (Umsatzan-

teil: 30,9 %). Auf der Verkäuferseite stand ganz besonders die Gruppe der Bauträger und Entwickler im

Blickpunkt. Diese veräußerten Immobilien und Grundstücke im Wert von ca. 428 Mio. K und sorgten somit

für etwa ein Viertel aller Umsätze. Es folgen die Pensionskassen mit gut 330 Mio. K und die Gruppe der

Private- und Family-Offices mit insgesamt rd. 228 Mio. K Verkaufsvolumen. Auch 2010 waren hauptsäch-

lich bürogenutzte Immobilien wieder die beliebteste Assetklasse. Diese leisteten bei knapp 1,09 Mrd. K

Investitionssumme und annähernd 64 % Umsatzanteil den mit Abstand größten Beitrag zum gesamten

Transaktionsumsatz. Das investierte Geld floss fast vorwiegend in gänzlich oder nahezu vollvermietete

Objekte in den Münchener Zentrumslagen. Die Anfangsrenditen bewegten sich dabei in einem Bereich

von 4,40 % bis 6,35 %. Bei sechs registrierten Investments und knapp 11 % Umsatzanteil (182 Mio.

K Anlagevolumen) folgen bei den beliebtesten Investitionsobjekten die rein einzelhandelsgenutzten

Immobilien. Die erzielbare Spitzenrendite für Top-Büroimmobilien liegt Ende 2010 bei 4,5 % und somit 25

Basis-punkte unter dem Niveau vom Beginn des Jahres. Gleiches gilt für die Spitzenrendite für Einzelhan-

delsobjekte: Während diese Anfang 2010 noch bei 4,25 % lag, notiert sie mittlerweile 25 Basispunkte

niedriger. Die Perspektive für 2011 verspricht Anlass zu Optimismus: Die Vergabebereitschaft seitens

der Fremdkapitalgeber ist bei überschaubaren Investitionssummen bis zu 30 Mio. K zwischenzeitlich

wieder merklich gestiegen. Angesichts des wohl auch noch 2011 anhaltend günstigen Zinsumfeldes

und einer sich weiter belebenden Wirtschaft gehen wir davon aus, dass bei einem Investitionsvolumen

von bis zu 1,9 Mrd. K 2011 auch wieder mehr opportunistische Investments zu sehen sein werden.

The Retail Space Market

Retail properties were some of the most popular invest-ment properties throughout Germany. This is certainly due to stable and even increased consumer confidence in 2010 as well as the unexpectedly positive labour market. It should be noted that not only properties in prime locations in the largest German cities were of interest to inves-tors, specialist retailers and entire portfolios of discount supermarkets also attracted a great deal of interest, if long-term tenancy agreements were agreed. In the rental market, in prime locations and the main shopping streets in the large German cities, the demand for space was higher than available supply. This has affected the next level of locations and certain districts in Munich. Consequently the majority of the rents in these locations in Munich are stable or have increased slightly.The “Palais an der Oper” project, due for completion in 2012, also clearly illustrates limited supply in Munich’s prime locations. All of the planned retail and restau-rant space has already been leased. Although no final decision has been made, the rezoning of the Sendlinger Straße conversion remains an exciting prospect for the retail sector in Munich.

Der EinzelhandelsmarktDeutschlandweit zählten Einzelhandelsimmobilien mit zu den begehrtesten Anlageobjekten. Der

Grund hierfür ist sicherlich der 2010 stabilen bis gestiegenen Konsumfreude sowie einem unerwartet

positiven Arbeitsmarkt geschuldet. Dabei gelangten nicht nur Immobilien in den 1a-Lagen der großen

deutschen Metropolen in den Fokus des Investoreninteresses, sondern insbesondere auch Fach-

märkte und ganze Portfolios von Discountermärkten – langlaufende Mietverträge vorausgesetzt.

Auf der Vermietungsseite ist nach wie vor für die Toplagen bzw. Haupteinkaufsstraßen der großen

deutschen Städte eine über das Angebot an Flächen hinausgehende Nachfrage zu konstatieren,

die sich bisweilen auch auf die 1b-Lagen und besondere Stadtteillagen auswirkt. Die Mietpreise in

eben diesen Lagen Münchens sind infolgedessen weitgehend stabil geblieben bzw. weiterhin leicht

angestiegen.

Der Nachfrageüberhang in Münchens Toplagen zeigt sich am Beispiel des bis Ende 2012 fertig-

gestellten Projekts „Palais an der Oper“ in der Maximilianstraße sehr deutlich. Von den geplanten

Verkaufs- und Gastronomieflächen sind bereits heute alle vermietet. Auch wenn der letzte Beschluss

dazu noch aussteht, ist das Vorhaben der Umwidmung und des Umbaus der Sendlinger Straße für das

Einzelhandelsgeschehen Münchens ein spannendes.

The Market for Industrial and Storage Space

The real estate market for industrial and logistics space in the Munich metropolitan area stabilised more quickly than expected in 2010 and the level of demand remained stable. With around 281,000 m2 of industrial and logistics space transactions (new rental agreements, excluding owner-occupiers and adjacent office space), the increase of almost 28 % is well above the level of the previous year. The leases signed for two large spaces were the main reasons for the high level of take-up last year in Bergkirchen, the Rossmann health and beauty retail chain leased around 26,000 m2 and in Langenbach, DSV the logistics services provider, decided to lease around 20,000 m2. The take-up is also due to the continual increase in demand for modern logistics space, especially in the second half of the year.At around 56 %, over one half of take-up was for space up to 3,000 m2. The weakest segment was the 3,000 m2 to 5,000 m2 range; this was only 13 % of total take-up. The traditional status of locations in the northeast and northwest as the most popular was affirmed in 2010. In total, take-up here was around 27 % and 17 % respectively.These positive market developments mean that just under 34,000 m2 of modern new-generation logistics space was available for rent at short-notice at the end of 2010. The total area available of this type of space in the Munich real estate market is around 1.321 million m2; this means that the va-cancy rate is extremely low at 2.6 %. This scarcity of space maintained rent levels throughout the year: Premium rents for logistics space remain in the range of 5.65 to 6.30 €/m2. The average rent level of these spaces is almost unchanged at 5.00 to 5.50 €/m2. Premium rents for production and ser-vice space reach up to 7.95 €/m2 for existing properties and up to 9.00 €/m2 for new builds.2011 is also expected to be a successful year with a similar level of take-up. Project developments will take on more significance throughout the year, although speculative new builds are not expected as yet.

Der Markt für Industrie- und LagerflächenDer Immobilienmarkt für Industrie- und Logistikflächen im Großraum München hat sich 2010 schnel-

ler als erwartet stabilisiert und ein gutes, stabiles Nachfrageniveau erreicht. Mit ca. 281.000 m²

(Neuvermietungen, ohne Eigennutzer und anteilige Büroflächen) umgesetzter Industrie- und Logistik-

flächen ist der Anstieg mit fast 28 % gegenüber dem Vorjahr deutlich ausgefallen.

Die Hauptgründe für dieses umsatzstarke Jahr sind zwei großflächige Mietvertragsabschlüsse – in

Bergkirchen hat die Drogeriemarktkette Rossmann ca. 26.000 m² angemietet und in Langenbach hat

der Logistikdienstleister DSV eine Anmietentscheidung für rd. 20.000 m² Fläche getroffen – sowie

die insbesondere in der zweiten Jahreshälfte kontinuierlich gestiegene Nachfrage nach modernen

Logistikflächen.

Mit rd. 56 % liegt mehr als die Hälfte des Flächenumsatzes in einer Größenordnung bis zu 3.000 m².

Das nach wie vor schwächste Segment bildet der Größenbereich von 3.000 m² bis 5.000 m². Hier

wurden lediglich knapp 13 % des Umsatzes erzielt. Dass die Lagen im Münchener Nordosten und

Nordwesten traditionell die nachgefragtesten sind, hat sich auch 2010 bestätigt. In Summe konnte

hier ein Umsatzanteil von rd. 27 % bzw. 17 % festgestellt werden.

Die positive Marktentwicklung hat dazu geführt, dass nur mehr knapp 34.000 m² an modernen Logistik-

flächen der neuesten Generation am Ende des Jahres 2010 zur kurzfristigen Anmietung bereitstehen.

Bei einem Gesamtbestand solcher Flächen im Münchener Marktgebiet von ca. 1,321 Mio. m² bedeutet

dies eine äußerst geringe Leerstandsrate von 2,6 %. Diese Flächenknappheit führt zu einem im Jahres-

verlauf sehr konstanten Mietniveau: Die Spitzenmieten für Logistikflächen verharren bei einer Spanne

von 5,65 - 6,30 K/m². Das Durchschnittsmietniveau dieser Flächen liegt nahezu unverändert bei 5,00 –

5,50 K/m². Für Produktions- und Serviceflächen werden daneben Spitzenmieten von bis zu 7,95 K/m²

für Bestandsimmobilien bzw. bis zu 9,00 K/m² für Neubauten erzielt.

Es ist zu erwarten, dass auch 2011 ein erfolgreiches Jahr mit einem ähnlichen Umsatzniveau sein

wird. Projektentwicklungen werden im Laufe des Jahres dabei immer stärker in den Fokus rücken – mit

spekulativen Neubauten ist allerdings noch nicht zu rechnen.

Der Markt für BaugrundstückeDer Markt für gewerblich genutzte Baugrundstücke in München war im Jahr 2010 wieder deutlich lebhaf-

ter als im Vorjahreszeitraum und verzeichnete seit 2007 erstmals wieder Zuwächse. Der Gutachteraus-

schuss der Stadt München hat insgesamt 27 Kaufverträge dokumentiert, wovon 21 Objekte dem Segment

Büro- und Geschäftshaus zuzuordnen sind. Der Geld- und der Flächenumsatz haben sich gegenüber 2009

jeweils verdreifacht. Das Angebot an Gewerbe- oder Industriegrundstücken in München hat sich im Jahr

2010 nur unwesentlich verändert, da im vergangenen Jahr nur verhältnismäßig wenige Bebauungspläne

für größere Areale rechtskräftig wurden. Die immer noch wesentlichste Rolle auf dem Markt für Baugrund-

stücke spielten jene für den Wohnungsbau. Der stetige Zuzug in das Stadtgebiet München erfordert die

kontinuierliche Schaffung von Baurecht für neue Wohnungen. Die Nachfrage nach Eigentumswohnungen

von überwiegend privaten Kapitalanlegern und somit auch die Nachfrage der Bauträger und Projektent-

wickler nach Wohnbaugrundstücken im Stadtgebiet ist nicht zuletzt aufgrund der günstigen Zinssituation

ungebrochen hoch und das Angebot nach wie vor sehr gering. Dieses Ungleichgewicht führte im Jahr 2010

zu einem enormen Anstieg der Preise (Geldumsatz plus 28 %) und des Flächenumsatzes (plus 44 %) für

Wohnbaugrundstücke. Weiterhin hoher Nachfrage erfreuen sich auch Entwicklungsgrundstücke für

den Einzelhandel in München und im Großraum München. Die Zulässigkeit dieser Vorhaben ist insbeson-

dere im Stadtgebiet München durch die Behörden streng kontrolliert, was wiederum ein geringes Angebot an

geeigneten Grundstücken zur Folge hat.

3

4

5

6

11/12Immobilien-Marktbericht Real Estate Market Report

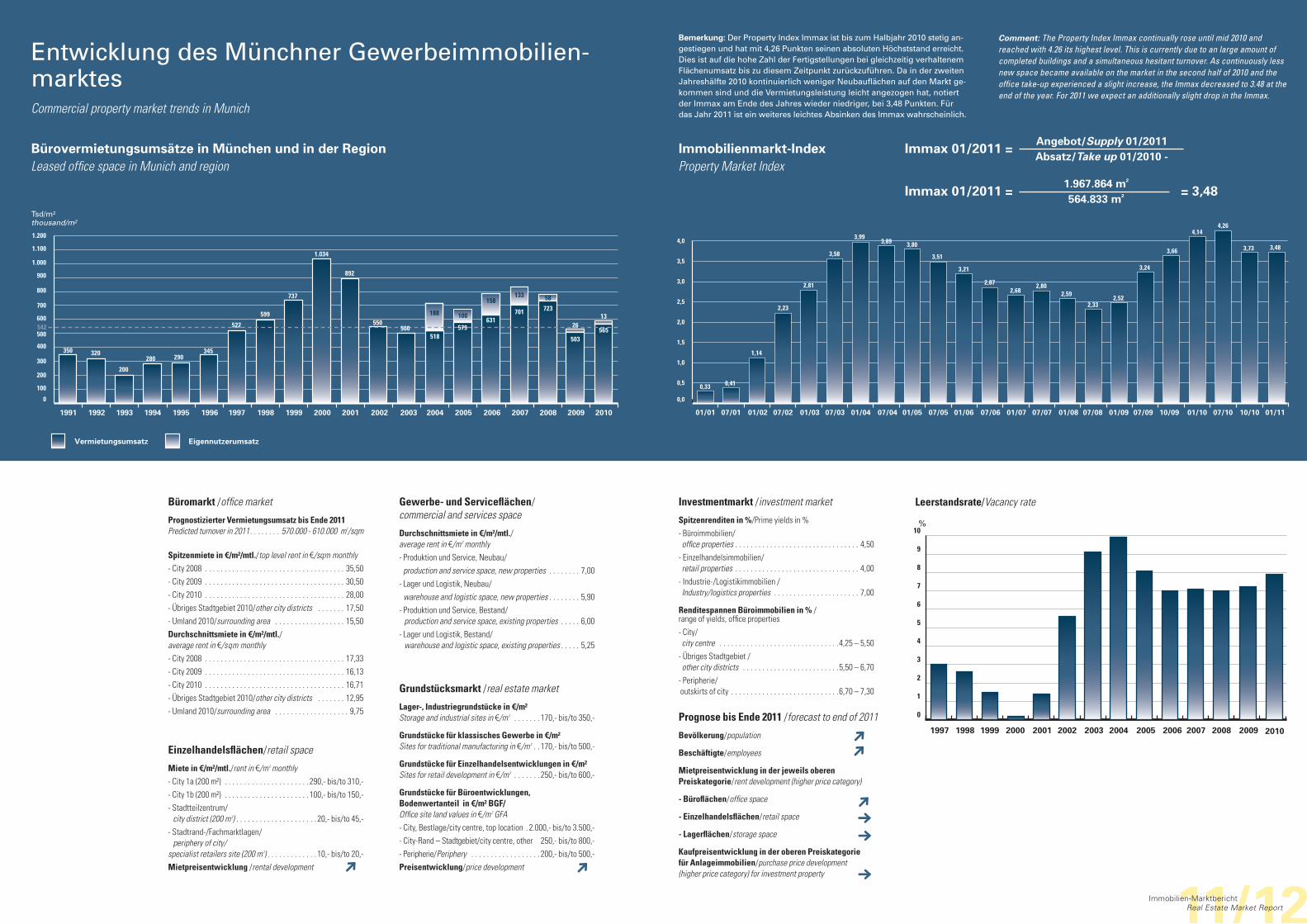

Büromarkt /office market

Prognostizierter Vermietungsumsatz bis Ende 2011Predicted turnover in 2011 . . . . . . . . 570 .000 - 610 .000 m²/sqm Spitzenmiete in w/m²/mtl./top level rent in u/sqm monthly- City 2008 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35,50- City 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30,50- City 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28,00- Übriges Stadtgebiet 2010/other city districts . . . . . . . 17,50- Umland 2010/surrounding area . . . . . . . . . . . . . . . . . . 15,50durchschnittsmiete in w/m²/mtl./average rent in u/sqm monthly- City 2008 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17,33- City 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,13- City 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,71- Übriges Stadtgebiet 2010/other city districts . . . . . . . 12,95- Umland 2010/surrounding area . . . . . . . . . . . . . . . . . . . 9,75

Einzelhandelsflächen/retail space

Miete in w/m²/mtl./rent in u/m² monthly- City 1a (200 m²) . . . . . . . . . . . . . . . . . . . . . . 290,- bis/to 310,-- City 1b (200 m²) . . . . . . . . . . . . . . . . . . . . . . 100,- bis/to 150,-- Stadtteilzentrum/ city district (200 m²) . . . . . . . . . . . . . . . . . . . . . 20,- bis/to 45,-- Stadtrand-/Fachmarktlagen/ periphery of city/ specialist retailers site (200 m²) . . . . . . . . . . . . . 10,- bis/to 20,-Mietpreisentwicklung /rental development

Gewerbe- und Serviceflächen/ commercial and services space

durchschnittsmiete in w/m²/mtl./average rent in u/m² monthly- Produktion und Service, Neubau/

production and service space, new properties . . . . . . . . 7,00- Lager und Logistik, Neubau/

warehouse and logistic space, new properties . . . . . . . . 5,90- Produktion und Service, Bestand/ production and service space, existing properties . . . . . 6,00- Lager und Logistik, Bestand/ warehouse and logistic space, existing properties . . . . . 5,25

Grundstücksmarkt /real estate market

Lager-, Industriegrundstücke in w/m²Storage and industrial sites in u/m² . . . . . . . 170,- bis/to 350,-

Grundstücke für klassisches Gewerbe in w/m²Sites for traditional manufacturing in u/m² . . 170,- bis/to 500,-

Grundstücke für Einzelhandelsentwicklungen in w/m²Sites for retail development in u/m² . . . . . . . 250,- bis/to 600,-

Grundstücke für Büroentwicklungen, Bodenwertanteil in w/m² BGF/Office site land values in u/m² GFA- City, Bestlage/city centre, top location . 2.000,- bis/to 3.500,-- City-Rand – Stadtgebiet/city centre, other 250,- bis/to 800,-- Peripherie/Periphery . . . . . . . . . . . . . . . . . . 200,- bis/to 500,-Preisentwicklung/price development

Investmentmarkt /investment market

Spitzenrenditen in %/Prime yields in %- Büroimmobilien/ office properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,50- Einzelhandelsimmobilien/ retail properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,00- Industrie-/Logistikimmobilien / Industry/logistics properties . . . . . . . . . . . . . . . . . . . . . . 7,00

Renditespannen Büroimmobilien in % / range of yields, office properties- City/ city centre . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4,25 – 5,50- Übriges Stadtgebiet / other city districts . . . . . . . . . . . . . . . . . . . . . . . . .5,50 – 6,70- Peripherie/ outskirts of city . . . . . . . . . . . . . . . . . . . . . . . . . . . .6,70 – 7,30

Prognose bis Ende 2011 /forecast to end of 2011

Bevölkerung/population

Beschäftigte/employees

Mietpreisentwicklung in der jeweils oberenPreiskategorie/rent development (higher price category)

- Büroflächen/office space

- Einzelhandelsflächen/retail space

- Lagerflächen/storage space

Kaufpreisentwicklung in der oberen Preiskategoriefür Anlageimmobilien/purchase price development(higher price category) for investment property

Bürovermietungsumsätze in München und in der RegionLeased office space in Munich and region

542

0

100

200

300

400

500

600

700

800

900

1.000

1.100

1.200

Vermietungsumsatz

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Tsd/m2

thousand/m2

Eigennutzerumsatz

350 320

200

280 290345

522

737

1.034

550500

892

599 701

133

723

58

503

26631

579

188

518

100

158

2010

565

13

Entwicklung des Münchner Gewerbeimmobilien-marktesCommercial property market trends in Munich

0

1

2

3

4

5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

0,33 0,41

2,23

2,81

3,58

3,993,89 3,80

3,51

3,21

2,872,68

2,802,59

2,33

3,24

2,52

4,14

3,66

4,26

3,73 3,48

01/01 07/01 01/02 07/02 01/03 07/03 01/04 07/04 01/05 07/05 01/06 07/06 01/07 01/08 07/08 01/09 07/09 10/0907/07 01/10 07/10 10/10

1,14

01/11

Immobilienmarkt-IndexProperty Market Index

Immax 01/2011 =Angebot/Supply 01/2011Absatz/Take up 01/2010 -

Immax 01/2011 =1.967.864 m²

564.833 m² = 3,48

%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2008 2009

0

1

2

3

4

5

6

7

8

9

10

2007 2010

Leerstandsrate/Vacancy rate

Bemerkung: Der Property Index Immax ist bis zum Halbjahr 2010 stetig an- gestiegen und hat mit 4,26 Punkten seinen absoluten Höchststand erreicht. Dies ist auf die hohe Zahl der Fertigstellungen bei gleichzeitig verhaltenem Flächenumsatz bis zu diesem Zeitpunkt zurückzuführen. Da in der zweiten Jahreshälfte 2010 kontinuierlich weniger Neubauflächen auf den Markt ge-kommen sind und die Vermietungsleistung leicht angezogen hat, notiert der Immax am Ende des Jahres wieder niedriger, bei 3,48 Punkten. Für das Jahr 2011 ist ein weiteres leichtes Absinken des Immax wahrscheinlich.

Comment: The Property Index Immax continually rose until mid 2010 and reached with 4.26 its highest level. This is currently due to an large amount of completed buildings and a simultaneous hesitant turnover. As continuously less new space became available on the market in the second half of 2010 and the office take-up experienced a slight increase, the Immax decreased to 3.48 at the end of the year. For 2011 we expect an additionally slight drop in the Immax.

11/12Immobilien-Marktbericht Real Estate Market Report

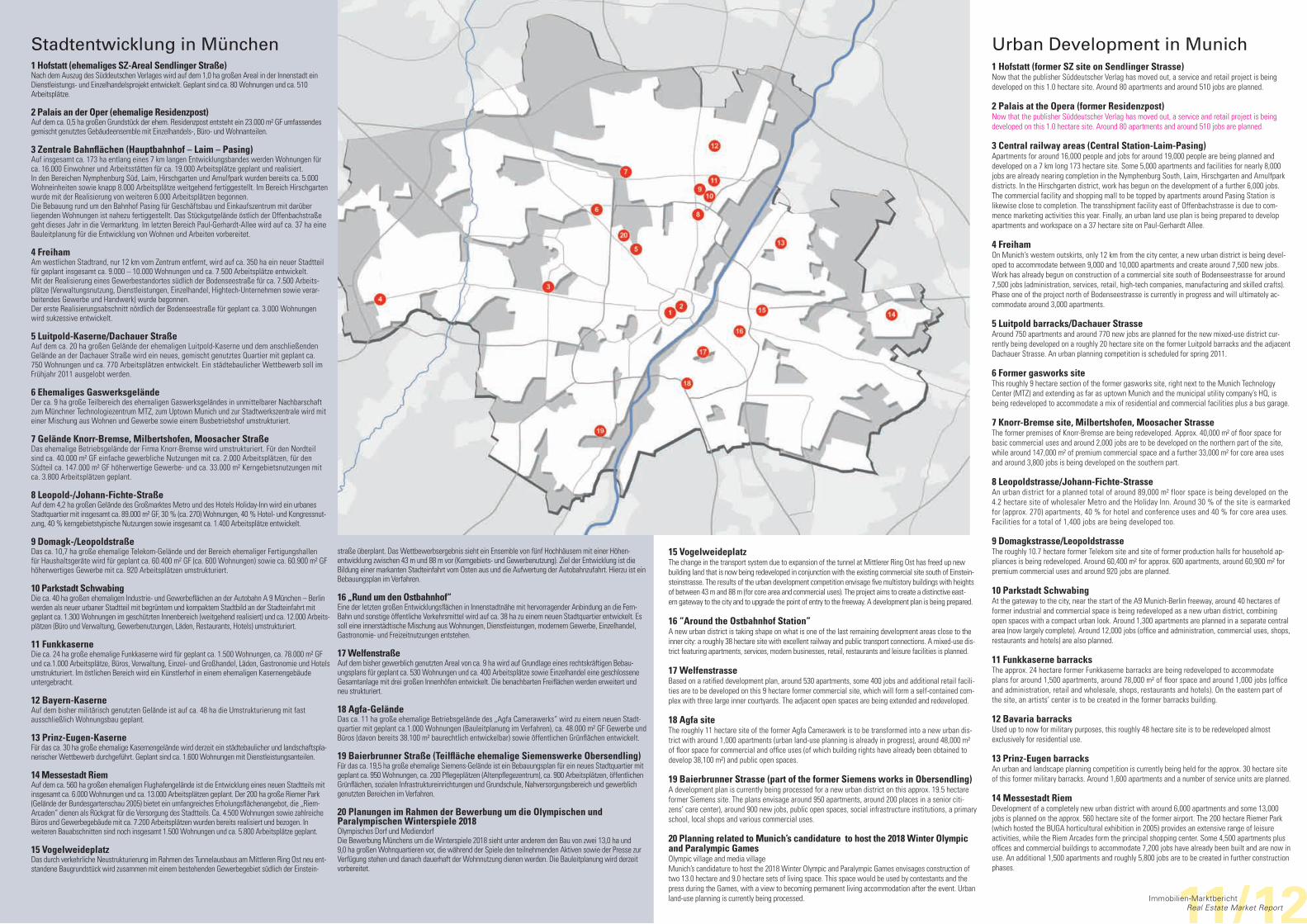

Stadtentwicklung in München1 Hofstatt (ehemaliges SZ-Areal Sendlinger Straße)Nach dem Auszug des Süddeutschen Verlages wird auf dem 1,0 ha großen Areal in der Innenstadt ein Dienstleistungs- und Einzelhandelsprojekt entwickelt. Geplant sind ca. 80 Wohnungen und ca. 510 Arbeitsplätze.

2 Palais an der Oper (ehemalige Residenzpost)Auf dem ca. 0,5 ha großen Grundstück der ehem. Residenzpost entsteht ein 23.000 m² GF umfassendes gemischt genutztes Gebäudeensemble mit Einzelhandels-, Büro- und Wohnanteilen.

3 Zentrale Bahnflächen (Hauptbahnhof – Laim – Pasing)Auf insgesamt ca. 173 ha entlang eines 7 km langen Entwicklungsbandes werden Wohnungen für ca. 16.000 Einwohner und Arbeitsstätten für ca. 19.000 Arbeitsplätze geplant und realisiert.In den Bereichen Nymphenburg Süd, Laim, Hirschgarten und Arnulfpark wurden bereits ca. 5.000 Wohneinheiten sowie knapp 8.000 Arbeitsplätze weitgehend fertiggestellt. Im Bereich Hirschgarten wurde mit der Realisierung von weiteren 6.000 Arbeitsplätzen begonnen.Die Bebauung rund um den Bahnhof Pasing für Geschäftsbau und Einkaufszentrum mit darüber liegenden Wohnungen ist nahezu fertiggestellt. Das Stückgutgelände östlich der Offenbachstraße geht dieses Jahr in die Vermarktung. Im letzten Bereich Paul-Gerhardt-Allee wird auf ca. 37 ha eine Bauleitplanung für die Entwicklung von Wohnen und Arbeiten vorbereitet.

4 FreihamAm westlichen Stadtrand, nur 12 km vom Zentrum entfernt, wird auf ca. 350 ha ein neuer Stadtteil für geplant insgesamt ca. 9.000 – 10.000 Wohnungen und ca. 7.500 Arbeitsplätze entwickelt.Mit der Realisierung eines Gewerbestandortes südlich der Bodenseestraße für ca. 7.500 Arbeits-plätze (Verwaltungsnutzung, Dienstleistungen, Einzelhandel, Hightech-Unternehmen sowie verar-beitendes Gewerbe und Handwerk) wurde begonnen.Der erste Realisierungsabschnitt nördlich der Bodenseestraße für geplant ca. 3.000 Wohnungen wird sukzessive entwickelt.

5 Luitpold-Kaserne/dachauer StraßeAuf dem ca. 20 ha großen Gelände der ehemaligen Luitpold-Kaserne und dem anschließenden Gelände an der Dachauer Straße wird ein neues, gemischt genutztes Quartier mit geplant ca. 750 Wohnungen und ca. 770 Arbeitsplätzen entwickelt. Ein städtebaulicher Wettbewerb soll im Frühjahr 2011 ausgelobt werden.

6 Ehemaliges GaswerksgeländeDer ca. 9 ha große Teilbereich des ehemaligen Gaswerksgeländes in unmittelbarer Nachbarschaft zum Münchner Technologiezentrum MTZ, zum Uptown Munich und zur Stadtwerkszentrale wird mit einer Mischung aus Wohnen und Gewerbe sowie einem Busbetriebshof umstrukturiert.

7 Gelände Knorr-Bremse, Milbertshofen, Moosacher StraßeDas ehemalige Betriebsgelände der Firma Knorr-Bremse wird umstrukturiert. Für den Nordteil sind ca. 40.000 m² GF einfache gewerbliche Nutzungen mit ca. 2.000 Arbeitsplätzen, für den Südteil ca. 147.000 m² GF höherwertige Gewerbe- und ca. 33.000 m² Kerngebietsnutzungen mit ca. 3.800 Arbeitsplätzen geplant.

8 Leopold-/Johann-Fichte-StraßeAuf dem 4,2 ha großen Gelände des Großmarktes Metro und des Hotels Holiday-Inn wird ein urbanes Stadtquartier mit insgesamt ca. 89.000 m² GF, 30 % (ca. 270) Wohnungen, 40 % Hotel- und Kongressnut-zung, 40 % kerngebietstypische Nutzungen sowie insgesamt ca. 1.400 Arbeitsplätze entwickelt.

9 domagk-/LeopoldstraßeDas ca. 10,7 ha große ehemalige Telekom-Gelände und der Bereich ehemaliger Fertigungshallen für Haushaltsgeräte wird für geplant ca. 60.400 m² GF (ca. 600 Wohnungen) sowie ca. 60.900 m² GF höherwertiges Gewerbe mit ca. 920 Arbeitsplätzen umstrukturiert.

10 Parkstadt SchwabingDie ca. 40 ha großen ehemaligen Industrie- und Gewerbeflächen an der Autobahn A 9 München – Berlin werden als neuer urbaner Stadtteil mit begrüntem und kompaktem Stadtbild an der Stadteinfahrt mit geplant ca. 1.300 Wohnungen im geschützten Innenbereich (weitgehend realisiert) und ca. 12.000 Arbeits-plätzen (Büro und Verwaltung, Gewerbenutzungen, Läden, Restaurants, Hotels) umstrukturiert.

11 FunkkaserneDie ca. 24 ha große ehemalige Funkkaserne wird für geplant ca. 1.500 Wohnungen, ca. 78.000 m² GF und ca.1.000 Arbeitsplätze, Büros, Verwaltung, Einzel- und Großhandel, Läden, Gastronomie und Hotels umstrukturiert. Im östlichen Bereich wird ein Künstlerhof in einem ehemaligen Kasernengebäude untergebracht.

12 Bayern-KaserneAuf dem bisher militärisch genutzten Gelände ist auf ca. 48 ha die Umstrukturierung mit fast ausschließlich Wohnungsbau geplant.

13 Prinz-Eugen-KaserneFür das ca. 30 ha große ehemalige Kasernengelände wird derzeit ein städtebaulicher und landschaftspla-nerischer Wettbewerb durchgeführt. Geplant sind ca. 1.600 Wohnungen mit Dienstleistungsanteilen.

14 Messestadt RiemAuf dem ca. 560 ha großen ehemaligen Flughafengelände ist die Entwicklung eines neuen Stadtteils mit insgesamt ca. 6.000 Wohnungen und ca. 13.000 Arbeitsplätzen geplant. Der 200 ha große Riemer Park (Gelände der Bundesgartenschau 2005) bietet ein umfangreiches Erholungsflächenangebot, die „Riem-Arcaden“ dienen als Rückgrat für die Versorgung des Stadtteils. Ca. 4.500 Wohnungen sowie zahlreiche Büros und Gewerbegebäude mit ca. 7.200 Arbeitsplätzen wurden bereits realisiert und bezogen. In weiteren Bauabschnitten sind noch insgesamt 1.500 Wohnungen und ca. 5.800 Arbeitsplätze geplant.

15 VogelweideplatzDas durch verkehrliche Neustrukturierung im Rahmen des Tunnelausbaus am Mittleren Ring Ost neu ent- standene Baugrundstück wird zusammen mit einem bestehenden Gewerbegebiet südlich der Einstein-

straße überplant. Das Wettbewerbsergebnis sieht ein Ensemble von fünf Hochhäusern mit einer Höhen-entwicklung zwischen 43 m und 88 m vor (Kerngebiets- und Gewerbenutzung). Ziel der Entwicklung ist die Bildung einer markanten Stadteinfahrt vom Osten aus und die Aufwertung der Autobahnzufahrt. Hierzu ist ein Bebauungsplan im Verfahren.

16 „Rund um den Ostbahnhof“Eine der letzten großen Entwicklungsflächen in Innenstadtnähe mit hervorragender Anbindung an die Fern-Bahn und sonstige öffentliche Verkehrsmittel wird auf ca. 38 ha zu einem neuen Stadtquartier entwickelt. Es soll eine innerstädtische Mischung aus Wohnungen, Dienstleistungen, modernem Gewerbe, Einzelhandel, Gastronomie- und Freizeitnutzungen entstehen.

17 WelfenstraßeAuf dem bisher gewerblich genutzten Areal von ca. 9 ha wird auf Grundlage eines rechtskräftigen Bebau-ungsplans für geplant ca. 530 Wohnungen und ca. 400 Arbeitsplätze sowie Einzelhandel eine geschlossene Gesamtanlage mit drei großen Innenhöfen entwickelt. Die benachbarten Freiflächen werden erweitert und neu strukturiert.

18 Agfa-GeländeDas ca. 11 ha große ehemalige Betriebsgelände des „Agfa Camerawerks“ wird zu einem neuen Stadt-quartier mit geplant ca.1.000 Wohnungen (Bauleitplanung im Verfahren), ca. 48.000 m² GF Gewerbe und Büros (davon bereits 38.100 m² baurechtlich entwickelbar) sowie öffentlichen Grünflächen entwickelt.

19 Baierbrunner Straße (Teilfläche ehemalige Siemenswerke Obersendling)Für das ca. 19,5 ha große ehemalige Siemens-Gelände ist ein Bebauungsplan für ein neues Stadtquartier mit geplant ca. 950 Wohnungen, ca. 200 Pflegeplätzen (Altenpflegezentrum), ca. 900 Arbeitsplätzen, öffentlichen Grünflächen, sozialen Infrastruktureinrichtungen und Grundschule, Nahversorgungsbereich und gewerblich genutzten Bereichen im Verfahren.

20 Planungen im Rahmen der Bewerbung um die Olympischen und Paralympischen Winterspiele 2018Olympisches Dorf und MediendorfDie Bewerbung Münchens um die Winterspiele 2018 sieht unter anderem den Bau von zwei 13,0 ha und 9,0 ha großen Wohnquartieren vor, die während der Spiele den teilnehmenden Aktiven sowie der Presse zur Verfügung stehen und danach dauerhaft der Wohnnutzung dienen werden. Die Bauleitplanung wird derzeit vorbereitet.

Urban Development in Munich1 Hofstatt (former SZ site on Sendlinger Strasse) Now that the publisher Süddeutscher Verlag has moved out, a service and retail project is being developed on this 1.0 hectare site. Around 80 apartments and around 510 jobs are planned.

2 Palais at the Opera (former Residenzpost) Now that the publisher Süddeutscher Verlag has moved out, a service and retail project is being developed on this 1.0 hectare site. Around 80 apartments and around 510 jobs are planned.

3 Central railway areas (Central Station-Laim-Pasing) Apartments for around 16,000 people and jobs for around 19,000 people are being planned and developed on a 7 km long 173 hectare site. Some 5,000 apartments and facilities for nearly 8,000 jobs are already nearing completion in the Nymphenburg South, Laim, Hirschgarten and Arnulfpark districts. In the Hirschgarten district, work has begun on the development of a further 6,000 jobs. The commercial facility and shopping mall to be topped by apartments around Pasing Station is likewise close to completion. The transshipment facility east of Offenbachstrasse is due to com-mence marketing activities this year. Finally, an urban land use plan is being prepared to develop apartments and workspace on a 37 hectare site on Paul-Gerhardt Allee.

4 Freiham On Munich’s western outskirts, only 12 km from the city center, a new urban district is being devel-oped to accommodate between 9,000 and 10,000 apartments and create around 7,500 new jobs. Work has already begun on construction of a commercial site south of Bodenseestrasse for around 7,500 jobs (administration, services, retail, high-tech companies, manufacturing and skilled crafts). Phase one of the project north of Bodenseestrasse is currently in progress and will ultimately ac-commodate around 3,000 apartments.

5 Luitpold barracks/dachauer Strasse Around 750 apartments and around 770 new jobs are planned for the new mixed-use district cur-rently being developed on a roughly 20 hectare site on the former Luitpold barracks and the adjacent Dachauer Strasse. An urban planning competition is scheduled for spring 2011.

6 Former gasworks site This roughly 9 hectare section of the former gasworks site, right next to the Munich Technology Center (MTZ) and extending as far as uptown Munich and the municipal utility company’s HQ, is being redeveloped to accommodate a mix of residential and commercial facilities plus a bus garage.

7 Knorr-Bremse site, Milbertshofen, Moosacher Strasse The former premises of Knorr-Bremse are being redeveloped. Approx. 40,000 m² of floor space for basic commercial uses and around 2,000 jobs are to be developed on the northern part of the site, while around 147,000 m² of premium commercial space and a further 33,000 m² for core area uses and around 3,800 jobs is being developed on the southern part.

8 Leopoldstrasse/Johann-Fichte-Strasse An urban district for a planned total of around 89,000 m² floor space is being developed on the 4.2 hectare site of wholesaler Metro and the Holiday Inn. Around 30 % of the site is earmarked for (approx. 270) apartments, 40 % for hotel and conference uses and 40 % for core area uses. Facilities for a total of 1,400 jobs are being developed too.

9 domagkstrasse/Leopoldstrasse The roughly 10.7 hectare former Telekom site and site of former production halls for household ap-pliances is being redeveloped. Around 60,400 m² for approx. 600 apartments, around 60,900 m² for premium commercial uses and around 920 jobs are planned.

10 Parkstadt Schwabing At the gateway to the city, near the start of the A9 Munich-Berlin freeway, around 40 hectares of former industrial and commercial space is being redeveloped as a new urban district, combining open spaces with a compact urban look. Around 1,300 apartments are planned in a separate central area (now largely complete). Around 12,000 jobs (office and administration, commercial uses, shops, restaurants and hotels) are also planned.

11 Funkkaserne barracks The approx. 24 hectare former Funkkaserne barracks are being redeveloped to accommodate plans for around 1,500 apartments, around 78,000 m² of floor space and around 1,000 jobs (office and administration, retail and wholesale, shops, restaurants and hotels). On the eastern part of the site, an artists’ center is to be created in the former barracks building.

12 Bavaria barracks Used up to now for military purposes, this roughly 48 hectare site is to be redeveloped almost exclusively for residential use.

13 Prinz-Eugen barracks An urban and landscape planning competition is currently being held for the approx. 30 hectare site of this former military barracks. Around 1,600 apartments and a number of service units are planned.

14 Messestadt Riem Development of a completely new urban district with around 6,000 apartments and some 13,000 jobs is planned on the approx. 560 hectare site of the former airport. The 200 hectare Riemer Park (which hosted the BUGA horticultural exhibition in 2005) provides an extensive range of leisure activities, while the Riem Arcades form the principal shopping center. Some 4,500 apartments plus offices and commercial buildings to accommodate 7,200 jobs have already been built and are now in use. An additional 1,500 apartments and roughly 5,800 jobs are to be created in further construction phases.

15 Vogelweideplatz The change in the transport system due to expansion of the tunnel at Mittlerer Ring Ost has freed up new building land that is now being redeveloped in conjunction with the existing commercial site south of Einstein- steinstrasse. The results of the urban development competition envisage five multistory buildings with heights of between 43 m and 88 m (for core area and commercial uses). The project aims to create a distinctive east- ern gateway to the city and to upgrade the point of entry to the freeway. A development plan is being prepared.

16 “Around the Ostbahnhof Station” A new urban district is taking shape on what is one of the last remaining development areas close to the inner city: a roughly 38 hectare site with excellent railway and public transport connections. A mixed-use dis- trict featuring apartments, services, modern businesses, retail, restaurants and leisure facilities is planned.

17 Welfenstrasse Based on a ratified development plan, around 530 apartments, some 400 jobs and additional retail facili-ties are to be developed on this 9 hectare former commercial site, which will form a self-contained com-plex with three large inner courtyards. The adjacent open spaces are being extended and redeveloped.

18 Agfa site The roughly 11 hectare site of the former Agfa Camerawerk is to be transformed into a new urban dis-trict with around 1,000 apartments (urban land-use planning is already in progress), around 48,000 m² of floor space for commercial and office uses (of which building rights have already been obtained to develop 38,100 m²) and public open spaces.

19 Baierbrunner Strasse (part of the former Siemens works in Obersendling) A development plan is currently being processed for a new urban district on this approx. 19.5 hectare former Siemens site. The plans envisage around 950 apartments, around 200 places in a senior citi-zens’ care center), around 900 new jobs, public open spaces, social infrastructure institutions, a primary school, local shops and various commercial uses.

20 Planning related to Munich’s candidature to host the 2018 Winter Olympic and Paralympic Games Olympic village and media village Munich’s candidature to host the 2018 Winter Olympic and Paralympic Games envisages construction of two 13.0 hectare and 9.0 hectare sets of living space. This space would be used by contestants and the press during the Games, with a view to becoming permanent living accommodation after the event. Urban land-use planning is currently being processed. 11/12Immobilien-Marktbericht

Real Estate Market Report

COLLIERS SChauER & SChöLL GmbhDachauer Straße 63 | 80335 münchen | Germany

Telefon +49 89 624294-0 | Telefax +49 89 [email protected] | www.colliers.com

hERauSGEbER/EDITOR:

Die Colliers Schauer & Schöll GmbH ist ein rechtlich selbstständiges Mitglied der Colliers International Property Consultants mit 480 Büros in über 61 Ländern weltweit.

Colliers Schauer & Schöll GmbH is an independently owned and operated affiliate of Colliers International Property Consultants with 480 offices throughout more than 61 countries worldwide.

Stand März 2011