Real Estate Invt Trust

30

A comprehensive study on REITs (Real Estate Investment Trusts) & their credit analysis 1

-

Upload

pratik-mittal -

Category

Documents

-

view

232 -

download

0

Transcript of Real Estate Invt Trust

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 1/30

A comprehensive study on REITs (Real Estate Investment Trusts) & their credit analysis

1

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 2/30

This project report in the Area of Finance based on the in-depth study of the project theme is submitted in March,

2010 to the Sydenham Institute of Management Studies and Research and Entrepreneurship Education, B-Road,

Churchgate, Mumbai-400 020, in partial fulfillment of the requirements for the award of the diploma of Post

Graduate Diploma in Business Management (PGDBM), recognized by Government of Maharashtra.

Submitted By

NAME: NIKHIL GARG ROLL NO: 822

Through

Name of the guide: Mahesh Godse

ACKNOWLEDGEMENT

I would like to take this opportunity to thank my project guide Mahesh Godse Sir for his constant support and

guidance during the project

2

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 3/30

Contents

A comprehensive study on REITs (Real Estate Investment Trusts) & their credit analysis ......................... .............. .. 1

ACKNOWLEDGEMENT ............................................................................................................................................ 2

3

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 4/30

Contents .................................................................................................................................................................... 3

List of tables ......................................................................................................................................................... ..... 4

Introduction to REITS ...................................................................................................................................... ..... ..... 6

What is REITS ............................................................................................................................................... ........ 6

Formation of REITS .......................................................................................................................................... ..... 7

Types of REIT ...................................................................................................................................................... .. 7

Valuing REITs ................................................................................................................................................. ..... ... 10

Explaining FFO ........................................................................................................................................... .........10

FFO versus Net Income .......................................................................................................................... .........10

Multiples used for valuing REITs ................................................................................................................. .........13

Credit Analysis of REITs:......................................................................................................................................... 16

Operational performance:.................................................................................................................................... 17

Sources of Repayment....................................................................................................................................... .19

Risk Assessment................................................................................................................................................. 20

Real Estate in India .................................................................................................................................................21

Is India ready for REITs ................................................................................................................. .............. ..... ... 23

Conclusion ....................................................................................................................................................... ......25

APPENDIX ......................................................................................................................................................... ..... 25

Appendix 1: Balance Sheet.................................................................................................................................. 26

Appendix 2: Income Statement............................................................................................................................ 27

Appendix 3: Cash Flow Statement...................................................................................................................... .28

Appendix 4: Fund From Operations ............................................................................................. ..... ..... .............. 29

References ..............................................................................................................................................................30

List of tables

Table 1: Straight Line Rent Adjustment

4

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 5/30

Table 2 : Key Operating Parameters

Table 3: Financial Projections

Chart 1 : Type of REITs

Chart 2 : Equity REITS(US)

Executive Summary

Objective of the project:

5

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 6/30

Real Estate Funds are one of the attractive products in the developed world as an investment tool. They have

become a rage in the developed world mainly because it does not have any correlation with the movements in the

equity markets and thus providing diversification benefits to the investors along with stable returns.

This rage has yet not reached Indian Shores as of now mainly due to government regulations but now it won’t be

long before they are introduced in India and grow exponentially.

The objective of this project is to study the concept of REITs and its unique characteristics. It also aims at doing a

credit analysis for a REITS company from a banks perspective

Proposed coverage and depth

Then initial section of the project would describe the concept of REITS across various geographies. This would

cover the REITS structure, tax implications, dividend distribution norms etc. An in-depth analysis of various types of

REITS and their characteristics would also be done.The subsequent sections would cover the credit analysis of

REITS. This would involve understanding certain concepts unique to the real estate industry. A detailed

explanation of these concepts (FFO, AFFO etc) would be described. The valuation techniques of REITs would also

be dealt with. Following this, a REITS company would be selected and analyzed from a credit perspective. This

would involve valuation of REITS, determining repayment capability of the company and risk assessment. Various

metrics unique to real estate would be considered and a detailed credit report would be prepared

Then the project would cover the importance of REITS in India and various developments over the year for

formation of REITS.

Introduction to REITS

What is REITS

A REIT (real estate investment trust) is a company that owns, and in most cases, operates income-producing real

estate such as apartments, office buildings, warehouses, shopping centers, regional malls, or hotels. 1960, the US

Congress authorized legislation for the formation of REITs, which enabled investors to benefit from direct

investment in large-scale real estate investments

6

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 7/30

Formation of REITS

REITs were formed in 1960 when Congress passed legislation that provided small investors access to the

ownership of income producing assets. The primary benefit of the REIT structure is that the entity does not pay

corporate income taxes in exchange for distributing at least 90% of their taxable net income as dividends to

shareholders annually. Therefore, taxes are paid only once and are the responsibility of the shareholder.

In order to qualify as a REIT, the company must meet and maintain certain provisions within the tax code

including:

•

Have a minimum of 100 shareholders;

• No more than 50% of its shares can be held by five or fewer individuals;

• The entity must invest at least 75% of its assets in real estate (equity or debt);

• Derive at least 75% of its gross income from rents on real property or interest on its mortgage investments;

and

• Not more than 20% of its assets can consist of stocks in taxable REIT subsidiaries (TRS). As an aside, the

taxable REIT subsidiary was created through the REIT Modernization Act (RMA) which took effect on January 1,

2001. By forming a TRS, REITs can engage in ancillary business activities that were previously prohibited by the

IRS. These business activities, which are fully taxed, allow REITs to potentially boost their earnings stream by

providing services that their clients need and/or want.

Types of REIT

There are many different types of REITs including Equity REITs, Mortgage REITs, and Hybrid REITs. In addition,

REITs can be public or private.

7

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 8/30

• Equity – An Equity REIT is an entity that owns and operates income producing assets. Many of these

companies are fully integrated organizations meaning they engage in the acquisition, development, and

management of commercial real estate for their own account.

• Mortgage – A Mortgage REIT is an entity that lends money to an owner of real estate and therefore does

not have direct ownership of the asset.

• Hybrid – A hybrid REIT is a cross between and Equity and a Mortgage REIT.

• Public vs. Private – REITs can either be publicly traded (most are listed on the NYSE) or privately held.

According to the National Association of Real Estate Investment Trusts (the REIT sector’s trade organization) there

are 151 publicly traded REITs of which 118 are equity REITs, 28 are mortgage REITs and 5 are hybrid REITs as of

March 2008.

Fig 1

Equity REITs Sectors

8

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 9/30

REITs typically invest in only one class of real estate. Broadly, these include office, industrial,

retail, residential, health care and lodging properties:

• Office / Industrial = (Office, Industrial, Mixed)

• Retail = (Shopping centers, Regional malls, Free standing)

• Residential = (Apartments, Manufactured Housing)

• Healthcare

• Lodging

• Self storage

• Diversified

• Specialty

Fig 2

9

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 10/30

• Office REITs lease office space, typically either in commercial business districts or in suburban locations.

• Industrial REITs lease warehouse space for manufacturing, distribution and other uses.

• Retail REITs own and operate malls and other shopping centers. They typically receive base rents from

tenants, reimbursements from tenants for operating expenses and percentage rents based on sales volumes.

• Multifamily REITs lease apartments, which have the disadvantage of being leased on only one year terms,

versus significantly longer leases for REITs investing in other classes of real estate.

• Healthcare REITs typically own properties leased to one or more of the following types of healthcare

providers: hospitals, professionals, researchers, and senior housing facilities.

•

Lodging REITs own hotels and other hospitality facilities.

Valuing REITs

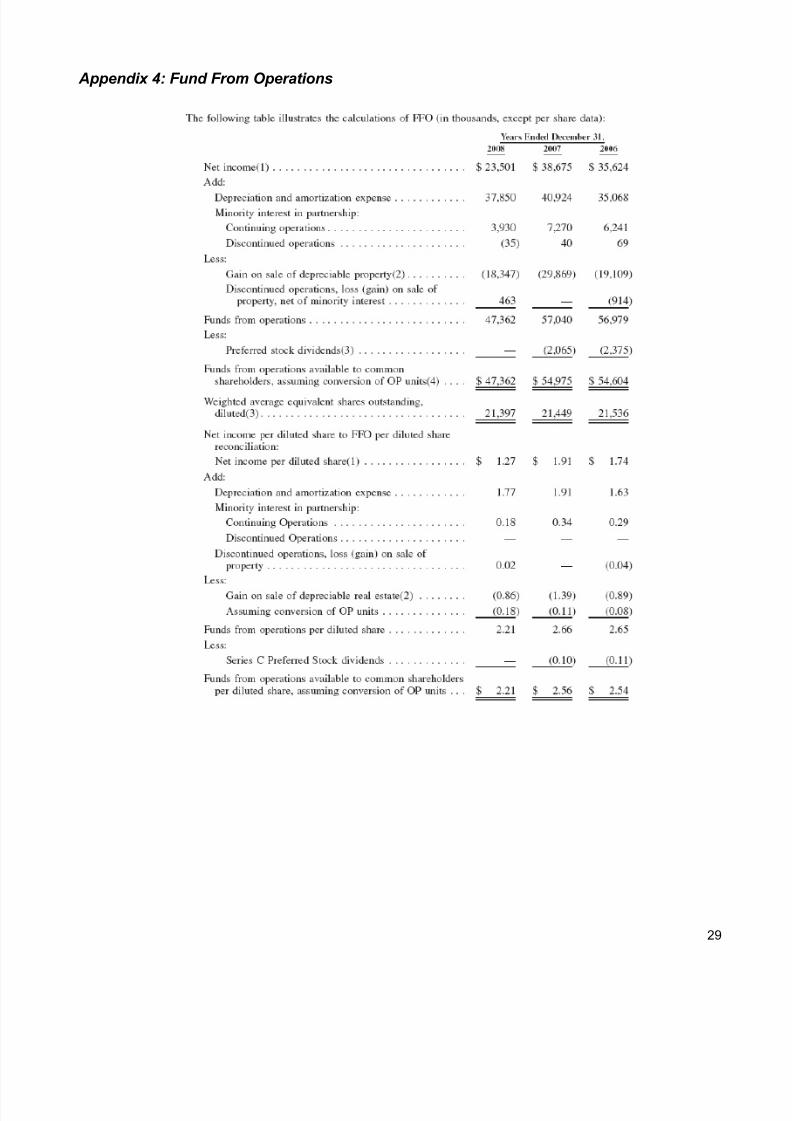

Explaining FFO

This section addresses the following

• Defining Funs from Operations (FFO) and explaining how it differs from net income

• Reported v/s Normalized FFO

• Adjusted FFO

FFO versus Net Income

Funds From Operations is defined as net income (calculated in accordance with generally accepted accounting

principles), excluding gains (or losses) from sales of property (but including asset impairment charges), plus

10

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 11/30

depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. The

adjustments for unconsolidated joint-venture partnerships will be computed to reflect FFO on the same basis.

Historical cost accounting for real estate assumes that the value of real estate assets diminishes predictably over

time. Since real estate values have historically risen or fallen with changes in market conditions, many analysts and

investors have considered operating results for real estate companies that use historical cost accounting to be

misleading.

The term Funds From Operations was created to address this problem. It was intended to be a supplemental

measure of REIT operating performance that excluded historical cost depreciation from GAAP net income (i.e., it

was added back).

Reported V/s Normalized FFO

While most REITs adhere to the strict definition of FFO when disseminating their quarterly and annual results, this

figure can be distorted due to accounting principles. As a result, a second FFO definition termed Normalized FFO

is used which gives a clearer picture of the company’s operating performance

The two adjustments we make in computing Normalized FFO are:

• Topic D-42 charges: This charge occurs when a company redeems an existing series of preferred stock

outstanding. As part of the redemption process, a company must write off the original issuance cost related to the

preferred stock that the REIT capitalized onto the balance sheet at the time of the offering. Since this charge is

non-cash in nature, it distorts a company’s true earnings power.

• Impairment losses

11

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 12/30

In a nutshell

Normalized FFO= Reported FFO + Topic D-42 changes + Impairment Losses*

*Please note that these adjustments can vary as per GAAP prevalent in the country whose REITs is being

analyzed. For general understanding US GAAP has been followed in the explanation

Adjusted FFO (AFFO)

Although FFO is a starting point for measuring a REIT’s profitability over time, it overstates the economic

profitability for three reasons that are described below. As a result, we believe that Adjusted Funds From

Operations (AFFO) is a better measure of economic profitability for REITs. The deductions made in FFO to arrive

at AFFO are:

• Recurring capital expenditures which are necessary to maintain the current status of the buildings.

• Straight-line rent which makes the revenue figure more closely aligned with the actual cash collected.

This adjustment to FFO is to deduct the amount of “non-cash” revenue that the company recognized in the period

as a result of contractual step-ups in its leases. This non-cash revenue is known as straight-line rent and occurs

when a landlord enters into a long-term lease with a tenant and the lease contains contractual rent increases over

the life of the lease. Based on GAAP accounting, the company must “straight-line” the entire revenue stream over

the term of the lease rather than recognize revenue as the cash is collected each period. The table below provides

an example of how a lease overstates the actual cash collected during the early portion of the lease and

understates the cash collected during the later part of the lease.

12

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 13/30

Cash Rents St-Line Rents S-L Rent Adj

Year 1 50 55 -5

Year 2 55 55 0

Year 3 60 55 5

Total Collections 165 165 0

Straight-line rent adjustment

Table 1

Multiples used for valuing REITs

Unlike traditional companies, which are valued on EPS or book value, REITs are valued under different criteria

including FFO and AFFO and Net Asset Value (NAV). The reason these metrics are used is that real estate is

purchased in the private sector based on cash flow streams from the asset, not on GAAP earnings or historical

book values. As a result, several metrics were created to evaluate REITs in the early ‘90’s. Below are outlined the

valuation metrics

The valuation metrics are:

• Price-to-AFFO multiples (i.e., price to cash flow)

• Price-to-NAV and Price-to Forward NAV

• Yield Spread – REIT dividend yield vs 10-year Treasury Yield

• Yield Spread – REIT dividend yield vs. BBB Corporate Bonds

Net Asset Value

One valuation metric that investors use in evaluating public companies is price-to book ratios. Unfortunately, price-

to-book ratios are not useful valuation yardsticks for REITs since a company’s book value is based on its historical

13

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 14/30

costs and therefore does not reflect the appreciation in property prices over the past decade. As a result, NAVs

(Net Asset Values) as a surrogate for the underlying values of REITs.

The framework used in calculating NAVs is presented below

• Determine a company’s forward 12-month cash net operating income : The reason for choosing this

period is that purchasers of real estate focus on the earnings potential of a property, not its past performance, and

cap rates are generally defined as a consequence of income over the next 12 months.

• Divide the company’s cash NOI figure by an appropriate cap rate. A cap rate is simply an inverse of a

cash flow multiple; i.e. dividing a cash flow estimate by a 10% cap rate is the same as applying a 10x multiple to

the cash flow. To derive the cap rate for each company we generally run a 5-year IRR model for each portfolio in

order to account for different return hurdles and future growth rates, both of which significantly influence the cap

rate calculation.

• Determine value of third party income. After determining the actual cash flow derived from a company’s

ancillary businesses, apply a cap rate to the income stream. Since management contracts are typically cancelable

on short notice often 30 days’ notice, ascribe a lower valuation to fee income than to rental income. Use a cap rate

from a high of 20% to a low of 7% for fee income versus property level cap rates that range from the mid 5s to the

low 9s.

• Determine gross market value of assets. After adding the results from steps 2 & 3 together, then add

cash and cash equivalents, other assets, land held for development, value of unleased space, and existing

development projects (valued at cost) to derive the gross market value of assets.

•

Determine net market value of assets.Subtract total liabilities (including preferred stock) from the gross

market value of assets. Included in the total liabilities is a "mark-to-market" figure for the company's total fixed-rate

debt outstanding.

• Determine NAV per share. Divide the net market value of assets by the total number of shares outstanding

to derive the net asset value per share.

14

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 15/30

Price to Forward NAV

Another metric to compute and analyze to form an investment opinion is concept of price to forward NAV. Forward

NAV concept seeks to capture expected NAV growth from development or redevelopment activity as well as from

internal growth over the next twelve months. The forward NAV concept also allows adjustment for expected

changes in cap rates over the next year

This forward NAV metric is useful because expected NAV growth may explain why one REIT trades at a higher

premium to NAV versus another REIT. In general, REITs with higher NAV growth should trade at larger premiums

to their current NAV and vice versa. If this relationship is inconsistent when comparing two REITs or a group of

REITs, then it may provide an opportunity to identify expected outperformance for a REIT or a group of REITs.

Table 7 details the P/NAV and P/Forward NAVs for each of the major property sectors. This table also provides the

growth rate in our current NAV versus the year ago period, as well as the implied growth rate from our current NAV

to forward NAV and the expected long-term FFO growth rate for each sector.

Dividend Yield

During the early stages of the modern REIT era starting in 1990, the comparison between REIT dividend yields vs

treasury yields was accepted as the standard valuation metric. As REITs were considered an alternative asset

class that offered investors a high level of dividends, the sector was often compared to treasury yields to gauge

value. Since 1990, REIT dividend yields, on average, yielded 140bp above the 10-year treasury. This relationship

broke down most recently during the real estate boom of 2006–07, due to the abundant availability of cheap capital

that drove REIT valuations to record levels. REIT dividend yields reached an all time high of 12.8% on October

1990, and reached an all time low of 3.8% on January 2007. Today, with the advent of the credit crisis, REIT

dividend yields stand at 8.4% and have dramatically widened vs. treasuries, offering 610bp over treasuries.

15

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 16/30

Credit Analysis of REITs:

This section covers the various steps in judging the credit worthiness of a REITS. Each step would be explained by

an example for better understanding.

The basic steps in credit analysis of a REITs are as follows

1) Operational Performance

2) Sources of repayment

3) Risk assessment

Each of these steps will be explained in detail

Case study:

The following case will be used in doing the credit analysis

16

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 17/30

About the company

RG Properties Trust is a fully integrated, self-administered, publicly-traded real estate investment trust (“REIT”)

organized on October 2, 1997.

It owns, develops, acquires, manages and leases community shopping centers and one regional mall, in the

Midwestern, Southeastern and Mid-Atlantic regions of the United States. At December 31, 2008, they owned

interests in 89 shopping centers, comprised of 65 community centers, 21 power centers, two single tenant retail

properties, and one enclosed regional mall, totaling approximately 20.0 million square feet of gross leaseable area

Shopping centers can generally be organized in five categories: convenience, neighborhood, community, regional

and super regional centers. Shopping centers are distinguished by various characteristics, including center size,

the number and type of anchor tenants and the types of products sold. Community shopping centers provide

convenience goods and personal services offered by neighborhood centers, but with a wider range of soft and hard

line goods. The community shopping center may include a grocery store, discount department store, super drug

store, and several specialty stores.

For the financial statements of the company please refer Appendix . For detailed report visit

http://216.139.227.101/interactive/rpt2008/

Operational performance:

This section covers the operational performance of the company during a particular year. Certain line items like

revenues, expenses, NOI, EBITDA, FFO are compared to study the trend and performance. Also a liquidity

analysis is done to check the liquidity position of the company. In this, the liquid assets (Cash and Cash

equivalents, credit facility) are determined and checked to see whether they are sufficient to cover the future

obligations of the company. Then a future outlook is formed based on the company and the sector to gauge its

growth potential

The following table highlights key operating statistics for RG Properties

17

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 18/30

Item FYE08 % of Revenues FYE07 % of Revenues YOY CHG

Total Revenues 132,724 100% 140,971 100% -5.9%

Operating Expenses 52,155 39% 48,362 34% 7.8%

Property NOI 80,569 61% 92,609 66% -13.0%

Net Income 23,501 18% 38,675 27% -39.2%

EBITDA 76,939 58% 92,420 66% -16.8%FFO 47,362 36% 57,040 40% -17.0%

Table 2

Please note: FYE07 Nos. are taken from 2007 Annual report not included here

• Property revenues for FY08 decreased by $8.3 mn or 5.9% primarily due to a $5.7 mn decrease in

minimum rents and a $2.6 mn decrease in tenant recoveries as a result of dispositions

• Same center revenues increased by $2 mn or 1.9% in FY08 due to an increase in minimum rents and

tenant recoveries

• Property operating expenses increased by 7.8% while same centre operating expenses increased by 5.4%

• NOI decreased by 13%, while same store NOI increased 0.1% to &70.7 mn.

• FFO before preference dividends fell 17% to $47.4 mn for FY08 compared to $57 mn for the same period

prior year. This decline was primarily attributable to non-cash impairment charges, accounts receivable write-offs

and pre-development cost write-offs.

Liquidity Analysis

• As of 31/12/2008 RG had cash of $5.3mn and $18.7mn available under its revolving credit facility,

• RG had approximately $215 mn of pro rata share of total debt maturing through YE2009. It has 5.7% of

debt maturing in 2009, See below for summary of debt maturities

18

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 19/30

Based on the chart RG has insufficient liquidity to cover its capital needs in 2009 and 2010. The company will need

to access the capital markets for raising further capital

Sources of Repayment

This is the most important section of credit analysis. In this the future cash position of the company is forecasted.

This is done by analyzing the company, its growth plans and past history. Using this, it is determined whether the

company is generating enough cash to repay its debt obligations. If the cash flows are adequate then the

repayment capability of the company is strong. This projection forms the base case of the company

A stress case is also prepared. Based on certain guidelines a few line items (eg. Sales, CapEx) are stressed to

gauge the effect on the cash position of the company. On basis of both the base case and stress case the

company’s credit capability is determined and appropriate suggestions are made to strengthen its credit capability

19

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 20/30

The table below captures the base and stress case. These figures have been arrived at by studying the industry

and company’s growth plans. The source for this information were latest analyst reports and company website

Base Case Stress Case Base Case Stress Case

EBITDA 76,939 69,245 76,939 69,245

Cap Ex(10% of NOI) (7,694) (6,925) (7,694) (6,925)

Straight Line Rent (1,641) (1,641) (1,641) (1,641)

Adjusted EBITDA 67,604 60,679 67,604 60,679

Interest (36,518) (36,518) (36,518) (36,518)

Prin Amount (5,139) (5,139) (4,014) (4,014)

Dividends Paid (34,844) (34,844) (19,849) (19,849)

FCF 6,063 (871) 7,178 254

2009 2010

Table 3

• Due to the economic downturn expected to continue in 2009 the company’s operations would be affected.

The company needs in 2009 will consist of around $46mn of secured debt

• Free cash flow is expected to be $6 mn for FYE 09

So the source of repayment to pay off its obligations would be refinance in the bank debt market

augmented by cash flow from operations

Risk Assessment

Here the key credit risks of the company are highlighted along with their mitigants.

The key credit risks for this company are as follows

• Refinancing Risk : The deteriorating economy combined with a constrained capital market provides a

difficult environment in which access debt and equity

Mitigants:

20

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 21/30

o The debt obligations are of a long term. So till the refinancing need arises the capital markets will return to

normal

• Weak Retail Environment

Consumer spending and consumer confidence has deteriorated, thereby putting significant pressure on company’s

operating performance

Mitigants:

o The company is well diversified and is lesser affected by consumer spending

Real Estate in India

The talk of launching REITs in India in a structure similar to what exists in the United States has been going on for

many years. What should be realized, however, is that many aspects of real estate in India must be addressed

before one could even think of introducing such a product to the investment community.

The factors which are favorable to investment in real estate in India are:

• Current macro economic background is extremely attractive

• Broadening industrial and commercial growth beyond IT and BPO

• Large demand foreseeable in commercial, residential and hospitality sectors. Retail sector might be slightly

erratic.

• FDI has opened up and is evolving

• Gradual evolution of secondary market, longer leases and financing sophistication should be increasingly

evident

21

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 22/30

In the present scenario, focus would be on following types of investments:

• Commercial : Offices and Parks

• Hospitality : Hotels, Leisure and Healthcare

• Retail : Large Malls

• Industrial

• Mixed use development sites : Including Residential

Several groups are actively working to improve the real estate investment options and establish a REIT industry in

India. The Associated Chambers of Commerce and Industry of India (ASSOCHAM) has proposed to create REITs

to ensure that India's property markets are suitably expanded with proper regulation.

The Securities and Exchange Board of India (SEBI) Advisory Committee on Mutual Funds has considered the

subject of mutual funds launching specialized real estate products (REMFs) on the lines of German open-end

funds.

The SEBI guidelines will enable retail investors to participate in the real estate market via real estate-dedicated

mutual funds. The new guidelines will enable mutual funds to invest in the real estate sector and thereby will also

allow small investors to own property.

The Association of Mutual Funds of India (AMFI) has constituted a committee for an in-depth study of relevant legal

and operational aspects. At present, 38 companies have been licensed to operate as mutual funds in India,

including well-known international names like Alliance Capital, Deutsche Bank, Merrill Lynch, Fidelity, HSBC,

Morgan Stanley, Quantum and ING. These firms have already floated more than 500 funds and could be in line to

offer a real estate fund.

22

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 23/30

A Citigroup Research report on real estate investment trust (REIT) strategy has identified over $15 billion of capital

raised by opportunity funds targeted at India. In March 2005, the Union Government allowed FDI in real-estate

development sector under automatic approval route for large projects

Is India ready for REITs

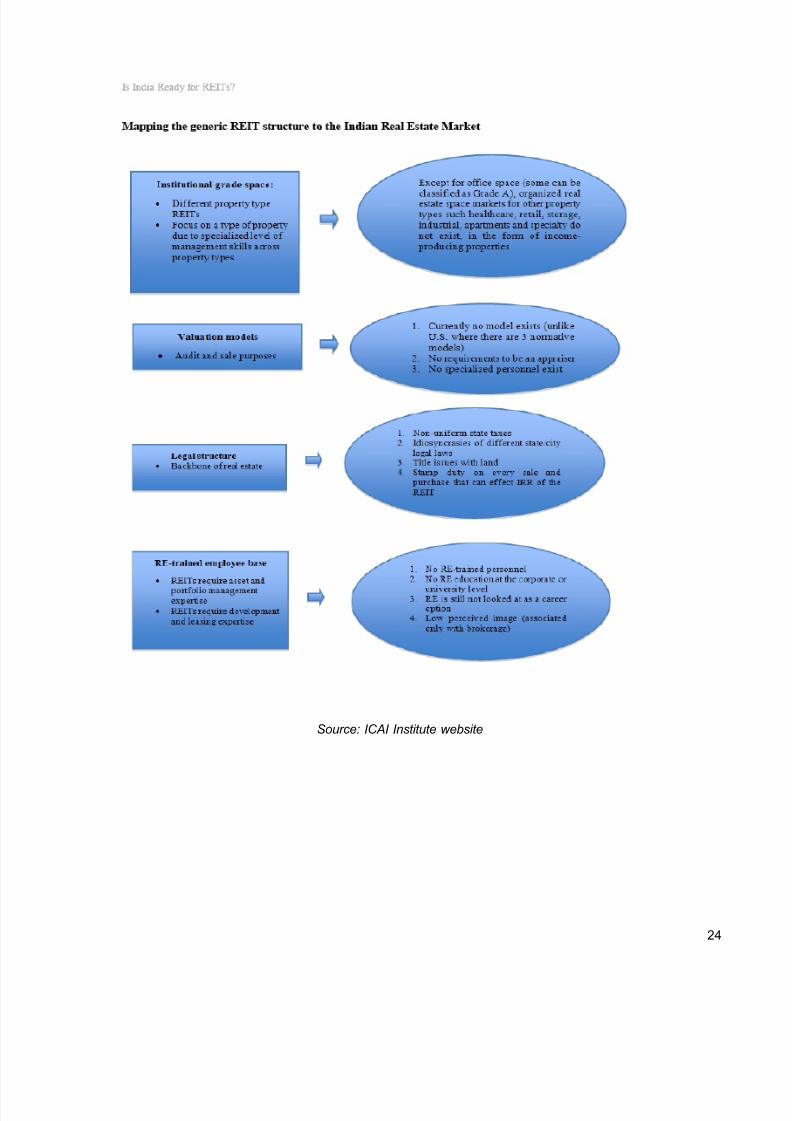

The dual nature of REITs emphasizes their dependence on the real estate asset/physical space market. Without

an organized real estate market, REITs can’t deploy the funds they raise. The model below shows the various

components of an efficient REIT market and what India is lacking. The model shows the absence of various

aspects of real estate in India that would be required for the efficient functioning of REITs in India. The absence of

even one of these elements could lead to an inefficient REIT market and trigger a collapse in the entire system.

Rather than a failed attempt, it would be wise to build up each of the elements over time before initiating any

discussion of REITs in India. A failed attempt would be a detriment to the globalization of REITs and discourage

any foreign REIT, such as a U.S. REIT, from launching in India in the future.

23

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 24/30

Source: ICAI Institute website

24

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 25/30

Conclusion

With the current economic slowdown largely attributed to the real estate market, credit analysis of real estate

companies has become very crucial. REITs has been in US since a very long time and have given healthy returns

to investors beating the index by a high margin. In a developing market like India , where real estate development

is essential a REITS like concept will be very useful. This project successfully puts forth the concept of REITs in US

and its analysis. Using a similar approach in Indian REITs will help in analyzing credit worthiness of companies andgive a better picture of the real estate industry

APPENDIX

25

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 26/30

Appendix 1: Balance Sheet

26

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 27/30

Appendix 2: Income Statement

27

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 28/30

Appendix 3: Cash Flow Statement

28

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 29/30

Appendix 4: Fund From Operations

29

8/2/2019 Real Estate Invt Trust

http://slidepdf.com/reader/full/real-estate-invt-trust 30/30

References

www.investopedia.com

www.icainstitute.org

www.nareit.com

REIT-Industry Primer – Macquarie Research