RE-ACT Newsletter April14

13

LATE NOTICE IN REINSURANCE – THE “BAD FAITH” EXCEPTION BY: NICK SCOTT, QBE RE Virtually all insurance policies require prompt notice of occurrences that may result in claims. Such notice af- fords the insurer an opportunity to investigate claims and establish adequate reserves. An insurer’s ability to enforce a notice clause varies; some states require strict compliance for coverage to attach while others require the insurer to show that it was prejudiced by delayed notice in order to successfully deny coverage. Similarly, reinsurance contracts usually require a cedent to notify its reinsurer when a claim is likely to impact the reinsurance (or when certain criteria are met). Historically, the “late notice” defense has not been [continued on page 3] APRIL 2014 RE-ACT A U.S. REINSURANCE UNDER 40S AND BERMUDA UNDER 40S RE/INSURANCE GROUP COLLABORATION THANK YOU TO OUR SPONSORS INSIDE THIS ISSUE: LATE NOTICE IN REIN- SURANCE—THE “BAD FAITH” EXCEPTION, BY NICK SCOTT 1 INTERVIEW WITH DOMINIC ADDESSO, PRESIDENT & CEO OF EVEREST RE 6 RE EDUCATION 8 MEMBER SPOTLIGHT: HART MOEDE 2 INTERVIEW WITH ROBERT KENNEDY, PRESIDENT & COO OF RESOURCE INTERME- DIARIES 6 SOCIAL EVENT RECAP 10 BERMUDA UNDER 40S UPCOMING EVENTS 4 CYBERLIABILITY DE- VELOPMENTS IN BER- MUDA AND OTHER OFFSHORE JURISDIC- TIONS, BY ALEX 7 MEET YOUR 2013- 2014 BOARD MEM- BERS 13

-

Upload

elizabethnussbaumedelstein -

Category

Documents

-

view

220 -

download

0

Transcript of RE-ACT Newsletter April14

L A T E N O T I C E I N R E I N S U R A N C E – T H E “ B A D F A I T H ” E X C E P T I O N B Y : N I C K S C O T T , Q B E R E

Virtually all insurance policies require prompt notice of occurrences that may result in claims. Such notice af-fords the insurer an opportunity to investigate claims and establish adequate reserves. An insurer’s ability to enforce a notice clause varies; some states require strict compliance for coverage to attach while others require the insurer to show that it was prejudiced by delayed notice in order to successfully deny coverage.

Similarly, reinsurance contracts usually require a cedent to notify its reinsurer when a claim is likely to impact the reinsurance (or when certain criteria are met). Historically, the “late notice” defense has not been

[continued on page 3]

A P R I L 2 0 1 4

R E - A C T A U . S . R E I N S U R A N C E U N D E R 4 0 S A N D B E R M U D A U N D E R 4 0 S R E / I N S U R A N C E G R O U P C O L L A B O R A T I O N

T H A N K Y O U T O O U R S P O N S O R S

I N S I D E T H I S I S S U E :

L A T E N O T I C E I N R E I N -S U R A N C E — T H E “ B A D F A I T H ” E X C E P T I O N , B Y N I C K S C O T T

1 I N T E R V I E W W I T H D O M I N I C A D D E S S O , P R E S I D E N T & C E O O F E V E R E S T R E

6 R E E D U C A T I O N 8

M E M B E R S P O T L I G H T : H A R T M O E D E

2 I N T E R V I E W W I T H R O B E R T K E N N E D Y , P R E S I D E N T & C O O O F R E S O U R C E I N T E R M E -D I A R I E S

6 S O C I A L E V E N T R E C A P 1 0

B E R M U D A U N D E R 4 0 S U P C O M I N G E V E N T S

4 C Y B E R L I A B I L I T Y D E -V E L O P M E N T S I N B E R -M U D A A N D O T H E R O F F S H O R E J U R I S D I C -T I O N S , B Y A L E X

7 M E E T Y O U R 2 0 1 3 -2 0 1 4 B O A R D M E M -B E R S

1 3

Page 2 R E - A C T

Q: How did you get involved with the re/insurance industry? How long have you been in the industry?

A: I was in graduate school in London and was applying to general positions in the finan-cial services and consulting world. I was somewhat aware of Lloyd’s of London. During one of my breaks between terms, I assisted with the delivery of a yacht to Malmo, Sweden. I spent almost two weeks on a forty foot boat with a captain, who had some experience in the marine industry. He encouraged me to look at Lloyd’s generally and marine insurance specifically.

I applied to positions in Lloyd’s but was unable to obtain a work visa for the U.K. Sadly, the current economic downturn in Europe has made it difficult to get the right to work in the U.K. Therefore, I started also looking back in the United States and found a great group of marine underwriters based in New York City with ProSight Specialty. The rest is history. I will have been working with the group for two years in July.

Q: What type of work do you do? How did you get to where you are now, in a nutshell? A: As I noted previously, I’m fairly new to the industry. My journey to my current position is largely described above. My official title is Marine Underwriter. As a marine underwriter, I handle risks across a fairly broad spectrum. My main focus is on excess liabilities for the marine and energy industries. I also deal with hull accounts, essentially property on vessels, and take following lines on packages for offshore drill rigs and platforms. The packages are often facultative reinsurance placements out of Lon-don.

My main goal on the job is to learn as much as possible from those senior to me. I still have plenty to learn. Funny enough, my direct boss started at Mutual Marine Office, the company bought by ProSight, as a marine underwriter six days before I was born, and he is one of the younger underwriters.

Q: What aspect of your job do you enjoy the most? A: The most enjoyable aspect of my work is listening to stories of the senior guys in my group. I discuss almost every risk with another underwriter in the office, and these discussions almost always result in a story. Sometimes the story is about how policy wording changed back in 1986. Other times, it is about how a risk, maybe like the one we are discussing, went very wrong. These stories are always entertaining, funny, and most importantly informative.

Q: Have you had any mentors or anyone who provided useful guidance as you made your way to where you are now? If so, is there anything you learned that you would pass on to others making their way in the industry? A: My mentors, industry wise, are the underwriters, with whom I am currently working. The most important lesson they’ve taught me is the importance of old-fashioned underwriting. We work in a line of business that is hard to model. Therefore, the im-portance of underwriting a risk or portfolio of risks on a micro level is incredibly important. An understanding of the exposures, the wordings, and making certain you are getting the proper rate on line is essential. One cannot rely on any simple formula or outline.

Q: If you weren’t working in re/insurance, what would you be doing? A: This is a hard question to answer. I suppose I have quite a hobbyist interest in politics. I could see myself working in that realm. I don’t think, however, that my work in insurance necessarily precludes participation in such activities down the road.

[continued on page 4]

M E M B E R S P O T L I G H T : H A R T M O E D E

In an effort to become more familiar with our members, we highlight one member in each issue of our newsletter. If you are interested in being interviewed for the Member Spotlight section, please email us at [email protected].

Re Under 40s caught up with Hart Moede, Marine Underwriter with ProSight Specialty. Here’s what he had to say:

perceived to be as strong in reinsurance as in the direct insurance context and, therefore, a reinsurer must typically demon-strate it was prejudiced by the lack of timely notice. Arbitrators and courts set a high bar as to what constitutes “prejudice” in this context. Although the majority of courts require a reinsurer to show prejudice before denying late-noticed claims – and notwithstanding the contrary position held in several jurisdictions – a federal judge in New York, predicting California law, recently reiterated an exception: prejudice is not required when the ceding company has acted in bad faith. ICSOP v. Argonaut In ICSOP v. Argonaut, 2013 WL 4005109 (S.D.N.Y. 2013), ICSOP sued its reinsurer, Argonaut, which denied coverage for asbes-tos bodily injury claims under a facultative certificate. After finding that ICSOP failed to provide timely notice of the claims, the court ruled “whether ICSOP’s gross negligence or bad faith excuses Argonaut from demonstrating prejudice” would be deter-mined at trial. In opening the door for the “bad faith exception” (which was first developed by the Second Circuit in 1992’s Uni-gard Security v. North River) to apply in California, the court relied on the facts that: (1) the reinsurance relationship involves a duty of utmost good faith; and (2) insurers are familiar with the concept of prompt notice because of what they require from their own policyholders. The ICSOP ruling is important not merely because the court acknowledged the validity of a late notice defense without a showing of prejudice (which not unprecedented), but because it reiterates the type of conduct that may trigger the exception and ex-pands the doctrine to a jurisdiction in which it had not previously been applied in the reinsurance context. Under the exception, a reinsurer is excused from proving prejudice if its cedent intentionally deceives the reinsurer or fails to implement routine proto-cols to notify the reinsurer of reportable claims. It is unsurprising that deception or fraud implicates the exception; it is, howev-er, noteworthy that a cedent’s failure to implement procedures designed to prevent late notice may rise to the level of bad faith. In that regard, the court stated “a requirement that the reinsured implement adequate practices and controls with respect to the provision of notice is minimally burdensome and consistent with the expectation of parties entering into a reinsurance agree-ment.” The federal courts in New York are regarded as leading judicial authorities on reinsurance and thus this decision may carry influ-ence beyond its own precedent. Following ICSOP, it is likely that courts will further explore the “bad faith exception” and, in the process, shed light on what constitutes proper reinsurance claim reporting protocols. Takeaways and Practical Considerations Although it behooves reinsurers and cedents alike to develop proper and businesslike practices relevant to their good faith rela-tionship, below are several specific suggestions: Reporting Procedures – A cedent should establish procedures for notifying reinsurers of reportable claims. There must be

clear logic in the cedent’s systems and/or staff that ensures proper reporting. Further, procedures should be documented; a dispute over the “bad faith exception” may entail a fact-intensive analysis (analogous to the extensive discovery seen in bad faith insurance litigation) and, thus, a case may be decided on documentary evidence. Also, insurers ought to invest in functional systems; it is not unusual for systems to break down or become obsolete, and the failure to maintain an ade-quate system could be fatal to recovering late-noticed claims.

Reinsurance Audits – Reinsurers should utilize their audit rights to not only examine underwriting practices and large expo-sures, but to closely inspect the cedent’s systems and claim reporting protocols. Findings should be documented and com-municated to facilitate proper reporting.

Treaty Wordings – Reinsurance contracts should articulate each party’s expectation as to what – and when – losses must be reported. It may be advisable to define concepts such as “promptly” and “as soon as is reasonably practical.” Addition-ally, reinsurers should maintain their contractual “right to associate” in underlying claims; while the ICSOP court did not find that the loss of this right alone demonstrates prejudice, losing this right may undercut the equities associated with a rein-surer’s late notice argument.

Commutations – In ICSOP, the reinsurer argued it was harmed because it did not adequately value commutations of its own (retro)ceded contracts, which were priced before it learned of the late-noticed claims. Reinsurers must consider the risk of commuting their own reinsurance when “slow” or “no” reporting by their cedents is a concern.

L A T E N O T I C E I N R E I N S U R A N C E – T H E “ B A D F A I T H ” E X C E P T I O N [ C O N T I N U E D F R O M P A G E 1 ]

Page 3 A P R I L 2 0 1 4

Q: If you could have any superpower what would it be? A: I would most certainly want to be able to read other people’s minds.

Q: List 5 personal items in your office. A: 1) A New York Review of Books or several of them more accurately.

2) A paper plane with a toy baby from a king cake sitting on top of it. A quick explanation: The King Cake is from a broker in New Orleans. King Cakes have a small baby in them, and whoever gets them is supposed to purchase a cake next year at Mardi Gras. The plane was a work up on a risk that I spent way too much time on that went nowhere. They seemed to go together at the time.

3) A waterproof jacket for sailing. I sail after work in the warmer months with the Manhattan Yacht Club. 4) A gym bag with either running attire or my clothes from the previous day in it. On Mondays I run with the Reservoir Dogs Running Club in Central Park and randomly throughout the week will run home after work. 5) A small cartoon from The New Yorker of two swans in a pond. One swan is covered in armor, has a helmet on and has a catapult on its back. The other is just a swan and is looking at the other suspiciously. The caption says, “People don’t give me bread crumbs, I take them.”

Q: What were the most embarrassing moment and proudest achievement of your career? A: Luckily, I haven’t had any major embarrassing moments in my career. I certainly have had situations where I missed obvi-ous details of a submission or misstated a coverage in a discussion. I’m certain something major will happen one day, and I’d assume it would involve a loss. In much the same way, I don’t necessarily think I have something to be overly proud of as of yet. It’s been quite an honor to be a part of a group with such a great reputation in our industry and that has done so well over the past few years. I, however, don’t feel comfortable taking any substantial amount of credit for that.

Q: What advice would you give to new professionals entering the re/insurance industry? A: Listen. There are a lot of older, more experienced individuals in this industry, who will probably be retiring in the relatively near future. They have ton of knowledge to give and most are quite eager to pass it onto those eager to receive it. Not only will you learn, but you’ll probably, as I discussed above, enjoy it.

M E M B E R S P O T L I G H T : H A R T M O E D E

[ C O N T I N U E D F R O M P A G E 2 ]

Page 4 R E - A C T

B E R M U D A U N D E R 4 0 S U P C O M I N G E V E N T S

APRIL 24th @ 6PM: Quiz Night – Outback Sports Bar MAY 14th @ 5:45PM: Financial Planning with Julian Wheddon at BF&M dock JULY 4th @ 1:00PM: Annual July 4th Golf Day – Tuckers Point Club (Shot Gun) SEPTEMBER 8th — 12th: NYC Market Tour, “Post Sandy”

Page 5 A P R I L 2 0 1 4

H O W C A N Y O U S U P P O R T U . S . R E U N D E R 4 0 S ?

In order to bring as many people in the industry together as we can, we have never charged for membership and we do not have any plans to do so in the future. We rely on our friends in the industry – people like you – to help support our Group.

On that note, we respectfully ask you if your organization is interested in becoming a sponsor for Re Under 40s. We have received several sponsorships over the years from insurers/reinsurers, brokers, consultants and law firms, but one of our most significant challenges is raising funds (or continued sponsorships) to ensure that the Group can achieve its goals moving forward.

We have several types of sponsorships. Our education events are always sponsored so that our members can attend, and learn, without any cost. Others have made financial contributions by providing funds that we utilize for our operating expenses. We recognize our sponsors at events, in our Newsletter, and on our website. Social events and Tour participation can also be spon-sored, and we would be happy to discuss other opportunities with you.

We look forward to your contributions in order to continue to make the U.S. Reinsurance Under 40s Group a cornerstone for ambitious professionals looking to expand their knowledge base and relation-ships within the (re)insurance industry.

INSURANCEDAYSUMMITBERMUDANow in its eighth year, the Insurance Day Summit Bermuda is the premier annual event for the insurance

sector. The 2014 event will take place over June 24 and 25 at the Fairmont Hamilton Princess hotel on the

island and is brought to you by the team at www.insuranceday.com.

The Summit offers a unique opportunity to hear from, and interact with, all the major insurance industry

stakeholders in Bermuda and the U.S. Gain genuine strategic insight into a number of internal and external

risk factors from our carefully selected keynote speakers and panelists.

All Bermuda Under 40s members will receive a 20% discount on the registration fee.

To register for the conference, please contact Benali Hamdache on +44 (0)20 701 77999 or email

[email protected]. Quote the Bermuda Under 40s code ‘UNDER40’ to receive your 20%

discount.

1. With 2013 seeing a record amount of alternative capacity flowing into the market, what kinds of innovation do you foresee within the traditional reinsur-ance market to remain competitive? Innovation is more likely to come to tra-ditional reinsurers in terms of capital formation and management. Alternative capital will no doubt reshape how com-panies manage their balance sheets. The addition of alternative capital to existing equity and debt constructs will potentially lower the overall cost of capi-

tal. The alternative model for Cat has been somewhat proven over the last two years. We all know it is effective to transfer standardized, modeled, non-correlating risk in highly exposed layers to un-rated capital providers. Most reinsurers use this ability to reduce their own risk, to make a market for new products, or both. However, there is a lot of opportunity outside that narrow environ-ment, even in Property. There are classes and perils that don’t fit the standard models, risks that do correlate with the overall capital market, risks with high attachments, in smaller zones or with broad reinstatements that are attractive to smart, hardworking underwrit-ers at well-rated companies. Going after this business is more than just running AIR or RMS. It requires more data about more kinds of risks and about the ceding companies themselves. Those chal-lenges are barriers that let companies distinguish themselves, and Everest is investing in these opportunities. Another kind of innovation comes from risks that were comfortably held within bank and investor balance sheets before the 2008 financial downturn and new financial regulations. These risks are finding a better fit on insurance balance sheets, including some asset, credit and mortgage areas. These risks have different fea-tures and need different types of analysis and controls. There’s more hard work there, but chances for new rewards as well. 2. Which emerging markets do you anticipate will become major

buyers of re/insurance? What steps can be taken to influence the purchasing habits and appetite of countries where insur-ance is seen as a luxury or may not exist at all?

[continued on page 9]

Page 6 R E - A C T

1. With 2013 seeing a record amount of alternative capacity flowing into the market, what kinds of innovation do you fore-see within the traditional reinsurance market to remain com-petitive?

It is important to differentiate the nature of the capacity being created and both where and how that capacity is being deployed. A healthy insurance/reinsurance market should include the creation and capitalization of primary insurers seeking to capitalize on in-creasing demand for risk-transfer insurance/reinsurance products as might evolve from a bourgeoning economy or the emergence of new and different insurable risks. The industry is not devoid of such developments but much of the capacity is being generated for either roll-up strategies (I can buy what I cannot otherwise grow) or an investment strategy in which insurance or reinsurance is largely a cash generator and underwriting profitability is largely an “Investment return enhancer.” Without being judgmental about the value and virtues of any insur-er or reinsurer’s business strategy or to suggest they fit easily into type-cast categories I believe it is evident that the market is evolv-ing into what is effectively two tectonic plates acting independently but in reaction to many of the same influences. They often overlap each other or grind against one another. It is admittedly an over-simplification but what differentiates these types of reinsurers is that one group views itself as a reinsurer of companies (client orientation) who provide their products and bear (and wish to share) the ensuing economic consequences. This includes developing an understanding of the nuances and peculi-arities of those clients, the decision-makers and the myriad propri-etary issues and decisions of individual clients. The other views itself as the reinsurer of products or events (commodity orienta-tion) where there can take larger and broader bets based on prod-ucts and events that are less nuanced and less dependent upon individual cedant’s underwriting skills and knowledge. There is a continuing need for both types of reinsurers. The insurer with a need to buy working layer reinsurance is likely to prefer to do so from someone who understands their business and the peo-ple, appreciates the value of long-term relationships, the need for reasonable returns and is prepared to provide advice, services and other support beyond the sale of a reinsurance product. Likewise, there will continue to be a need for commodity-type products by [continued on page 9]

Re Under 40s and Bermuda Under 40s asked Dominic Addesso, Chief Executive Officer (“CEO”) of Everest Re Group, Ltd., and Robert Kennedy, Chief Operating Officer (“COO”)

of Resource Intermediaries, to share their views regarding the current state of the reinsurance marketplace. We thank both highly-esteemed participants for their time,

valuable insight and willingness to contribute to the Re Under 40s newsletter.

I N T E R V I E W W I T H D O M I N I C A D D E S S O , P R E S I D E N T A N D C E O O F E V E R E S T R E G R O U P L T D .

I N T E R V I E W W I T H R O B E R T K E N N E D Y , P R E S I D E N T A N D C O O O F R E S O U R C E I N T E R M E D I A R I E S

Page 7 A P R I L 2 0 1 4

C Y B E R L I A B I L I T Y D E V E L O P M E N T S I N B E R M U D A A N D O T H E R O F F S H O R E J U R I S D I C T I O N S

B Y A L E X P O T T S , S E D G W I C K C H U D L E I G H

Offshore jurisdictions such as Bermuda, the BVI, and the Cayman Islands are catching up fast with the US and the UK on legal issues relating to cybercrime, cyberliability, and the use and discovery of electronic docu-ments. In the wake of the embarrassing leak in April 2013 of about 2.5 million electronic client files allegedly held by Portcullis TrustNet and Commonwealth Trust Limited (two trust companies with links to the BVI, Singapore and the Cook Islands), the BVI government has just passed a new law, called the Computer Misuse and Cy-bercrime Act 2014, following a second reading before the BVI House of Assembly. The Act is designed to prevent the illegal access and misuse of computers, and other cybercrime offences in the BVI, although it also seeks to have extraterritorial effect. The Act updates the legal definitions for various computer-related crimes and it increases the penalties for illegally accessing, copying, intercepting, transfer-ring, erasing or publishing unlawfully obtained data. The penalties imposed by the Computer Misuse and Cybercrime Act 2014 range from $10,000 to $1 million fines, and 2- to 20-year custodial sentences. The maximum fines can be tripled if the crime involves data tak-en from a “protected computer”, threatening the BVI’s national security, criminal investigations, financial ser-vices businesses, public infrastructure or essential emergency services. The BVI government has explained, in a recent press release, that the legislation is designed to “assure rele-vant stakeholders, both domestic and international, that the integrity and safety of their personal and business data is protected as they continue to undertake legitimate business transactions”. In the face of criticism by international media organisations and investigative journalists, the BVI government has sought to downplay the significance of the new Act, arguing that it simply seeks to improve upon amendments previously intro-duced to the BVI Criminal Code in 2007. The BVI government has acknowledged, however, that the April 2013 data leak has triggered the new law, since “the recent theft and unlawful publication of confidential information obtained through computer-generated systems has revealed the shortcomings in the 2007 amendments to the Criminal Code”. The BVI government has sought to stress that the new Act is not about: • protecting secrecy or shady dealings in the BVI; • witch hunting anybody involved in previous data leaks; • muzzling the press; • covering up any act of corruption; or • preventing anybody from making a disclosure to a law enforcement authority about any suspicion of the commission or of an attempt to commit an offence. The Act still has to be approved by the BVI Governor before it is brought into force. Other offshore jurisdictions already have laws in place regulating the misuse of computers and electronic da-ta, such as Bermuda’s Computer Misuse Act 1996 and the Cayman Islands’ Computer Misuse Law (2000 re-vision), although these are not as draconian as the BVI’s new legislation. These laws complement legislation that exists in offshore jurisdictions to encourage transactions being conducted electronically, and that allows offshore business documents to be stored electronically and admitted in evidence in legal proceedings, such [continued on page 12]

Page 8 R E - A C T

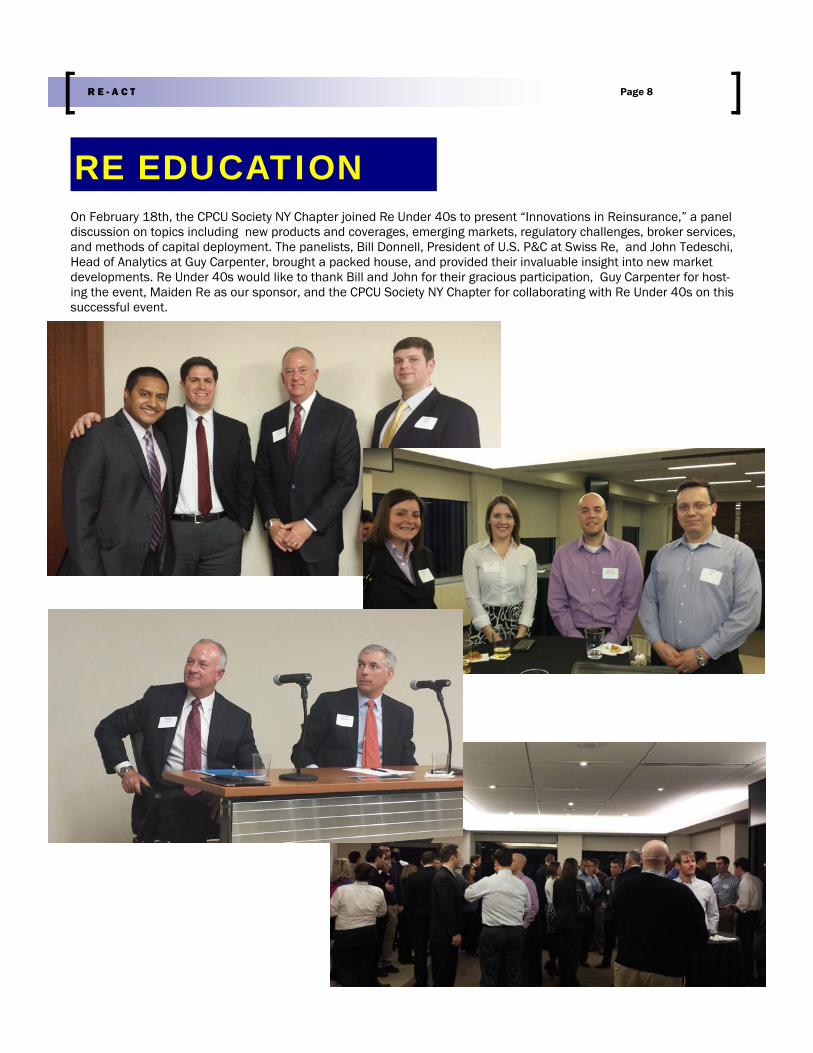

On February 18th, the CPCU Society NY Chapter joined Re Under 40s to present “Innovations in Reinsurance,” a panel discussion on topics including new products and coverages, emerging markets, regulatory challenges, broker services, and methods of capital deployment. The panelists, Bill Donnell, President of U.S. P&C at Swiss Re, and John Tedeschi, Head of Analytics at Guy Carpenter, brought a packed house, and provided their invaluable insight into new market developments. Re Under 40s would like to thank Bill and John for their gracious participation, Guy Carpenter for host-ing the event, Maiden Re as our sponsor, and the CPCU Society NY Chapter for collaborating with Re Under 40s on this successful event.

RE EDUCATION

Page 9 A P R I L 2 0 1 4

It is somewhat difficult to predict a particular emerging market that will become the major buyer. The most recent financial crisis has somewhat interrupted the meteoric rise in many countries, particu-larly those that are commodity based economies. In the short term, the beneficiaries, if there are any, may in fact be the more devel-oped nations. However, over the long term, population growth and a rising middle class in many emerging markets will be hard to ignore as demands for goods and services rise. Rather than select one winner at this stage, it is best to stay active in all of these mar-kets and scale accordingly. Many early bets on particular regions have yet to pay off. In terms of demand, this will of course evolve naturally as econo-mies develop. Rising property values and of course increased eco-nomic activity creates a natural demand, and these coverages tend to be the bulk of what is sought today. Demand for liability cover-age will only rise as societies mature and become more litigious themselves or as their business ventures expand globally exposing them to liabilities from other venues. This will come with time, and while there may be little we can do to influence this, we certainly should be educating the market on the value we bring in terms of supporting economic growth by helping to manage risk. We should never forget to ask our customers what their business risks are, and can we craft a solution to help manage that. 3. What is your view on the likelihood that TRIA will be renewed

in some form, and if it is not renewed or coverage is materially reduced, whether there is enough capacity in the private mar-ket to absorb the shortfall for terrorism insurance? What sort of innovative products might be developed to cover terrorism in the absence of a federal backstop?

TRIA is currently scheduled to expire on a cut-off basis at the end of this year, a congressional election year. Many voices in Washing-ton are making good cases for a continuation or extension, and pushing for something to happen over the next few months, before Congress adjourns to campaign. Will that happen? Maybe. We do know that brokers are showing us a few more requests for multi-year coverage in case it doesn’t happen on time. If there is a delay or a shortfall, the magnitude of the coverage need is manageable. TRIA has several components, including com-pany participations, industry pooling, a Federal layer and then an annual aggregate cap on total liability of $100 billion. The Federal-ly funded piece sounds like a very big number, but it is actually less than the reinsurance industry provides today in Florida. Gauging form experience, the cost to cover it will probably be less than Flori-da insurers pay for their protection, but it will not be free, which is what Washington is charging for it. The price and coverage of the insurance product will have to change to reflect that, and that is probably a good thing for the economy in the long term.

[continued on page 10]

I N T E R V I E W W I T H D O M I N I C A D D E S S O [ C O N T I N U E D F R O M P A G E 6 ]

I N T E R V I E W W I T H R O B E R T K E N N E D Y [ C O N T I N U E D F R O M P A G E 6 ]

large institutional buyers of what is largely property catastrophe reinsurance or surplus relief oriented. The key to a competitive traditional market is the recognition of how and why it is different than the commodity market, an under-standing of the role it plays and how it can address the unique needs of certain reinsurance buyers better than the commodity reinsurers. 2. Which emerging markets do you anticipate will become major

buyers of re/insurance? What steps can be taken to influence the purchasing habits and appetite of countries where insur-ance is seen as a luxury or may not exist at all?

I am not sure there is a good answer to this question. Businesses are generally motivated by fear and greed. If insurance or reinsur-ance is perceived as a profit enhancer or a cost-effective risk man-agement tool, it will be used. If not, it is irrelevant. I am unaware of anywhere globally where economic grow has been stunted by an unavailability of insurance or reinsurance. 3. What is your view on the likelihood that TRIA will be renewed

in some form, and if it is not renewed or coverage is materially reduced, whether there is enough capacity in the private mar-ket to absorb the shortfall for terrorism insurance? What sort of innovative products might be developed to cover terrorism in the absence of a federal backstop?

I believe that there is a high likelihood that TRIA will be renewed to both commercial and political reasons. However, if it is not re-newed I believe that there is more than ample private market ca-pacity currently available or primed to enter the market to absorb the product demand. The issue of insurance for this peril is not new and has been in the collective consciences of the industry and its leader for many years. If TRIA is not renewed one might specu-late that there would be a period of supply shortage and a period price fluctuation and uncertainty as the market finds its equilibri-um. However within a reasonable period of time I believe the open market can and will fill the need. 4. Do you believe there are any “sleepers” on the horizon, that is,

is there a significant trend, issue, or opportunity relevant to the re/insurance market that currently is not being discussed or broadcasted by the press that you think deserves atten-tion?

Yes, the geo-political environment is tumultuous and risky as evi-denced by the events in Ukraine, Venezuela, Syria and China. His-torically this level of international angst has resulted in heightened concerns about foreign investments and worries over political risk issues including the nationalization, expropriation, contract repudi-ation, confiscation and currency inconvertibility. This could acceler-ate the small but growing trend towards the re-importation of

[continued on page 11]

Page 10 R E - A C T

If there is more demand for Terror coverage, it will tend to go to traditional reinsurers, not alternative capital. Investors look back to 2001 and saw that the markets closed for a week, and most stocks re-opened at sharply lower values, roughly 20% lower. That risk is too subjective and too systemic for most fund investors. Cat bonds and ILS funds avoid terrorism coverage. Terror coverage could be anoth-er great opportunity for a smart, well controlled traditional reinsurer. 4. Do you believe there are any “sleepers” on the horizon, that is, is there a significant trend, issue, or opportunity relevant to the

re/insurance market that currently is not being discussed or broadcasted by the press that you think deserves attention? Of course, there are “sleepers.” The problem is just that they are still asleep. As an industry, we do a great job recalibrating our businesses after our last big mistake, although that exact mistake never happens again. Yes, we should learn from the past, and be sensible in excluding known exposures to loss, like tobacco and lead paint, so that if they are the “next asbestos” they will stay out of our results. But, we also have to be prepared for new risks in forms and places that the experts can’t predict. At Everest, we track and limit our liabil-ity and asset accumulations in various ways, such as industry and insured. We deliberately keep our leverage lower than the rating agen-cies accept for highly rated companies. We disregard the potential for diversification in modeling our “tail” scenarios, to be sure that un-seen correlations are safely managed. Maintaining that strength across the business cycle gives us the capacity to pursue emerging opportunities when they arise. 5. If television aired a special called “A Day in the Life of Dom,” what would viewers see as it relates to your day-to-day work? My day is a lot about reaching out to people, and while some of that is surely formal meetings, it is so much more. Walking the halls, so to speak, is so important to get a genuine feel for what is going on in your business and with your employees, customers and brokers. I try to not just rely on filtered information. 6. As technology advances and the use of analytics and models increase, what skills would you recommend to young professionals that

are pertinent to move ahead in their careers? Each of us more than likely comes from a different technical background, whether it is underwriting, actuarial, finance, accounting, etc. Obviously, if you wanted to remain in a particular discipline, one needs to stay current in that field, however, as one moves along in their career in any discipline, the other technical aspects of the business become equally important. Learning at least the basics of all the jobs in your company is key. Beyond the obvious which is a good base in statistics, underwriting and finance, I would recommend that young executives not lose sight of communication skills, both written and oral, and people/management skills. 7. What steps have you taken in your career that helped you the most to get to where you are now? I have always tried to keep learning and challenging myself by taking on new roles that might initially have been outside my comfort zone.

I N T E R V I E W W I T H D O M I N I C A D D E S S O [ C O N T I N U E D F R O M P A G E 9 ]

April 9th, Field House —in support of the St. Baldrick’s Foundation

January 29th, Three Sheets Saloon

NEW YORK PHILADELPHIA

Page 11 A P R I L 2 0 1 4

previously exported jobs to the U.S. Perhaps it means an increase in U.S. manufacturing that will result in higher payroll in higher rated Workers Compensation rating classification and the therefore a rise in Workers Compensation premium. “Fracking” in natural gas production has become almost ubiquitous in spite of the warning and concerns. It is already a major change agent in our economy and in our industry with a potential of eclipsing earlier pervasive industry issues such as asbestosis, black-lung and silicosis. Whether viewing this negatively including the resultant direct damage to the environment, human and animal health, contamina-tion of ground-water or view positively as a burgeoning industry with a massive need for continued infra-structure for processing, pipelines, refineries, liquefying planting, shipping ports, construction of LNG container ships and port terminals, the U.S. economy is significantly and permanently altered as a result of this phenomenon and the insurance and reinsurance are likely to share in the outcome; good or bad. 5. If television aired a special called “A Day in the Life of Bob,” what would viewers see as it relates to your day-to-day work? I’m not sure there was ever a time when our business was “Easy” but I believe that we have experienced a convergence of factor that has made it extremely difficult for insurer to make a reasonable risk-adjusted return on equity and even more difficult for the decision-makers to lead their companies safely and successfully through what is an extremely unforgiving environment. Make a wrong move, fall behind your peer-group in an important rating criteria, face a rating down-grade, lose business and find it harder to attract new business, watch ROE deteriorate, find yourself of a list of companies for sale. My business, that of a reinsurance intermediary, is not as much about the placement of reinsurance as it is about the proffering of advice, counsel, a vested but otherwise independent opinion, the need and willingness to share insight and intelligence and to act as a sounding board for management that wants to hear more feedback than the sound of their own echoes. The day-to-day work is talking with clients about threats and opportunities including how one might go about analyzing them and whether or not there is a rational and cost-effective strategy for buffering the risk of adverse outcomes. Often these issues only tangentially relate to reinsurance in any form but they generally represent the value that an intermediary brings to its clients even if it is the placement of tradi-tional reinsurance and the occasional “Alternative” problem-solution that yields revenue. 6. As technology advances and the use of analytics and models increase, what skills would you recommend to young professionals that

are pertinent to move ahead in their careers? The question is somewhat specious since it implies that there is something new and different in the form of analytics and modeling. I would suggest that this has been a slow and somewhat begrudging evolution and not a revolution. It is largely an adaptation of the kind of analyt-ics that has been used in other sectors of the financial services industry for generations, albeit a very welcome adaptation. For young professionals I would make the same suggestion I would have made regardless of the evolution or revolution of analytics and technological advances; be on the same plane of thought as your customers. It is not about the technology. It is about the decisions. The very best technology does not necessarily imply the avoidance of a disastrous decision and vice versa. Where are they in their technological evolution? How are they using technology to aide their decision-making? How would they like to use it if they could? More importantly, what decisions do we have to make and what tools are available to us to make a better and more informed decisions. 7. What steps have you taken in your career that helped you the most to get to where you are now? Read everything. Your greatest value to your clients is your ability to help them connect the dots and that means having a specific un-

derstanding of them and how they do or can relate their market, to the industry and to economy at large. Ask basic questions. You cannot think for your clients but you have to understand how they think, what they think about and why they

think it. Become multi-disciplined. As reinsurance brokers we’re not accountants but I would defy anyone to help a client make a good reinsur-

ance decision without understanding the impact on that client’s financial statements. We’re not lawyers but we deal in contracts that relate to contracts that often relate to tort issues. We’re not actuaries but actuarial science drives many decisions on both the buy and sell sides of the transaction. We’re not economists but we have to see our clients in the context of a complex economy.

Assume it can be done and it is just a matter of you finding out how to do it and with whom. Be proactively empathetic. If you understand what all the parties to a transaction need and want, where they may or may not find ob-

jection, where the friction points are likely to appear and what they each need to get to a “Yes” you will be successful more often than not.

I N T E R V I E W W I T H R O B E R T K E N N E D Y [ C O N T I N U E D F R O M P A G E 9 ]

Page 12 A P R I L 2 0 1 4

Thank you to our editors:

Kelly Nickerson, FTI Consulting

Michael Kurtis, Nelson Levine de Luca & Hamilton

Victoria Cunningham, Tokio Millennium Re

Cindy Hooper, Everest Reinsurance (Bermuda) Ltd.

C Y B E R L I A B I L I T Y D E V E L O P M E N T S I N B E R M U D A A N D O T H E R O F F S H O R E J U R I S D I C T I O N S

[ C O N T I N U E D F R O M P A G E 7 ]

as Bermuda’s Electronic Transactions Act 1999, Jersey’s Electronic Communications (Jersey) Law 2000, and the Cayman Is-lands’ Electronic Communications Law (2003 Revision). So far as rules regulating the conduct of electronic discovery in civil litigation are concerned, the offshore jurisdictions have not yet caught up with legal developments in onshore jurisdictions such as the UK and the USA. However, in a recent unreported decision, the Supreme Court of Bermuda has confirmed that it has the inherent jurisdiction to regulate the parties’ approach to electronic discovery, even in the absence of a specific set of rules. The Bermuda judiciary is willing, therefore, to bring active case management techniques to bear as appropriate, following recent guidance provided by the English courts and set out in the English civil procedure rules, with a view to avoiding an unnecessary and disproportionate waste of costs associated with an unregulated electronic discovery exercise. The offshore courts have also had to start grappling with other cyberliability issues in recent years. For example, in Bermuda Restaurants Ltd v Daspin and Convergex Global Markets Limited [2009] Bda LR 7, the Supreme Court of Bermuda considered the issue of an employer's potential vicarious liability for defamatory emails sent by an employee on the employer’s computer system. The Court held that the employee was acting on a “frolic of his own”, and that the employer was not responsible for the defamatory publication. More recently, in Richardson v Raynor [2011] Bda LR 52, the Supreme Court of Bermuda held that a Facebook posting to a limited circle of Facebook “friends” did not give rise to criminal liability for defamation, although the court did not address the issue of potential civil liability. If all this recent activity is any guide to the future, offshore cyberliability claims and issues look set to grow.

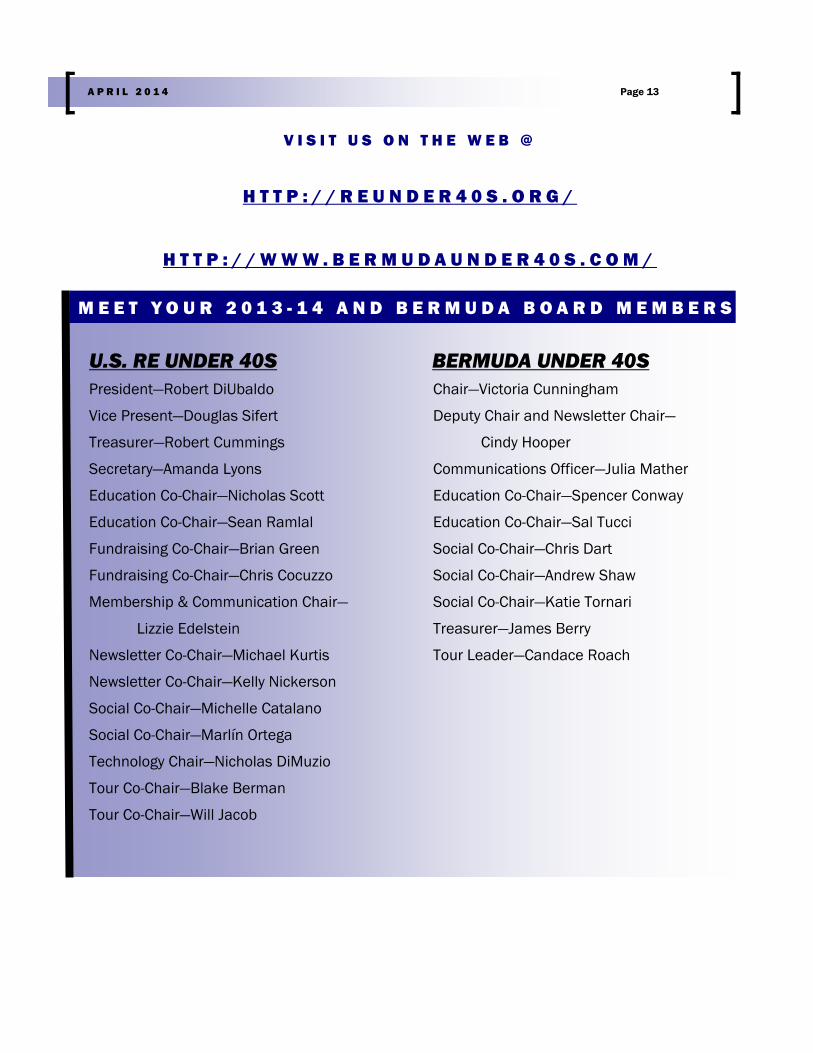

President—Robert DiUbaldo

Vice Present—Douglas Sifert

Treasurer—Robert Cummings

Secretary—Amanda Lyons

Education Co-Chair—Nicholas Scott

Education Co-Chair—Sean Ramlal

Fundraising Co-Chair—Brian Green

Fundraising Co-Chair—Chris Cocuzzo

Membership & Communication Chair—

Lizzie Edelstein

Newsletter Co-Chair—Michael Kurtis

Newsletter Co-Chair—Kelly Nickerson

Social Co-Chair—Michelle Catalano

Social Co-Chair—Marlín Ortega

Technology Chair—Nicholas DiMuzio

Tour Co-Chair—Blake Berman

Tour Co-Chair—Will Jacob

M E E T Y O U R 2 0 1 3 - 1 4 A N D B E R M U D A B O A R D M E M B E R S

Page 13 A P R I L 2 0 1 4

V I S I T U S O N T H E W E B @

H T T P : / / R E U N D E R 4 0 S . O R G /

H T T P : / / W W W . B E R M U D A U N D E R 4 0 S . C O M /

U.S. RE UNDER 40S BERMUDA UNDER 40S Chair—Victoria Cunningham

Deputy Chair and Newsletter Chair—

Cindy Hooper

Communications Officer—Julia Mather

Education Co-Chair—Spencer Conway

Education Co-Chair—Sal Tucci

Social Co-Chair—Chris Dart

Social Co-Chair—Andrew Shaw

Social Co-Chair—Katie Tornari

Treasurer—James Berry

Tour Leader—Candace Roach