Raymond James Quarterly Global Energy Report for … · Raymond James Quarterly Global Energy...

40

Global Research Published by Raymond James & Associates Please read domestic and foreign disclosure/risk information beginning on page 37 and Analyst Certification on page 37. © 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved. International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 Energy July 14, 2015 Industry Brief Pavel Molchanov, RJA, (713) 278-5270, [email protected] J. Marshall Adkins, RJA, (713) 789-3551, [email protected] Andrew Bradford, CFA, RJL, 403.509.0503, [email protected] Bertrand Hodée, Research Analyst, RJEE, (33 1) 45 64 05 46, [email protected] Santiago Wesenack, CFA, RJ LatAm, (54 11) 4850-2537, [email protected] Energy: Quarterly News _________________________________________________________________________________________ Raymond James Quarterly Global Energy Report for 2Q15 This quarterly report aggregates energy research highlights from Raymond James & Associates and our affiliates: Raymond James Ltd. (Canada), Raymond James European Equities, and Raymond James Latin America. Quarterly Highlights Crude Oil After 1Q15 marked the bottom of the oil price meltdown – with both WTI and Brent averaging their lowest levels since the first half of 2009 – 2Q15 was not as bleak, albeit hardly bullish. Until the very end of the quarter, when the Greek debt crisis and Chinese equity selloff suddenly escalated, oil price volatility was subdued, with prices mostly range-bound. The 2Q averages came in at $62/Bbl for Brent (up 13% sequentially) and $58/Bbl for WTI (up 19% sequentially). The Brent-WTI price spread, $4/Bbl, was slightly narrower than in 1Q. Following the recovery since January’s trough, we anticipate prices will remain broadly on par with recent levels through year-end 2015, followed by further gains in 2016. Barring a truly major economic crisis (to be clear, “Grexit” in and of itself would not count), we don’t envision oil prices falling back to the lows of 1Q. See page 4 for details on our oil price assumptions. Natural Gas With 1Q15 being considerably warmer than the year-ago winter, the quarterly Henry Hub average came in at $2.97/Mcf – down not just year-over-year but again sequentially as well. Not surprisingly, seasonality in 2Q15 exerted further pressure on gas prices, and the quarterly average of $2.67/Mcf was the lowest since 2Q12. Production growth is still outstripping demand growth for the time being – even with collapse in liquids drilling activity and the resulting effect on gas volumes from liquids-rich resource plays. Growth in industrial gas demand has been frustratingly slow, and LNG exports will not be needle-moving until 2017 at the earliest. We project flattish prices through year-end 2015, with only modest recovery in 2016. See page 4 for details on our gas price assumptions. Stocks During most of 2Q15, similar to 1Q, broader U.S. markets were mostly range-bound, with low-volatility action in equities. At the end of June, however, volatility reared its head again, as troubling headlines from Greece and China caused a global sell-off in equities and commodities alike, with some spillover into July. Even so, the S&P 500 edged down merely 0.2% for the full quarter, essentially canceling out 1Q’s gain of 0.4%. Energy stocks were mixed – in the wake, of course, of having been the S&P 500’s worst-performing sector in 2014. The two broadest energy subsector indices, E&P and oil service, posted a 2Q loss of 6% and gain of 5%, respectively. See the chart on page 3 for details on the performance of various energy indices.

Transcript of Raymond James Quarterly Global Energy Report for … · Raymond James Quarterly Global Energy...

Global Research Published by Raymond James & Associates

Please read domestic and foreign disclosure/risk information beginning on page 37 and Analyst Certification on page 37.

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863

Energy July 14, 2015

Industry Brief Pavel Molchanov, RJA, (713) 278-5270, [email protected]

J. Marshall Adkins, RJA, (713) 789-3551, [email protected]

Andrew Bradford, CFA, RJL, 403.509.0503, [email protected]

Bertrand Hodée, Research Analyst, RJEE, (33 1) 45 64 05 46, [email protected]

Santiago Wesenack, CFA, RJ LatAm, (54 11) 4850-2537, [email protected]

Energy: Quarterly News _________________________________________________________________________________________

Raymond James Quarterly Global Energy Report for 2Q15

This quarterly report aggregates energy research highlights from Raymond James & Associates and our affiliates: Raymond James Ltd. (Canada), Raymond James European Equities, and Raymond James Latin America.

Quarterly Highlights

Crude Oil

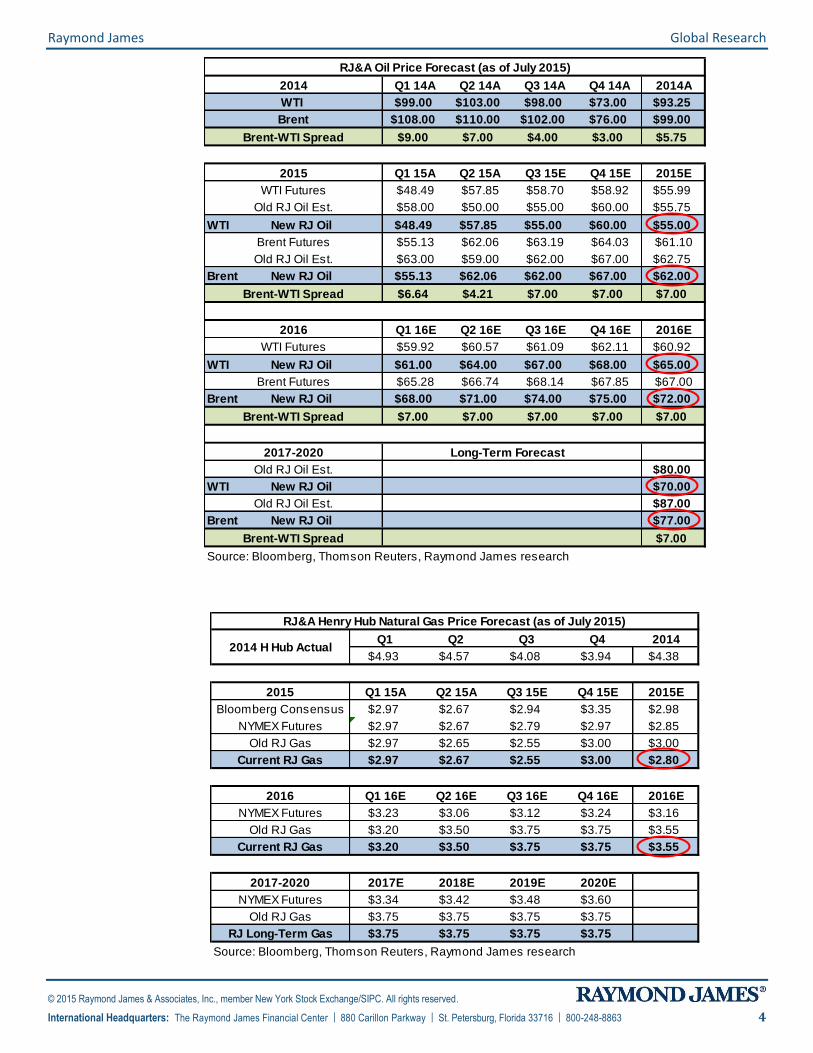

After 1Q15 marked the bottom of the oil price meltdown – with both WTI and Brent averaging their lowest levels since the first half of 2009 – 2Q15 was not as bleak, albeit hardly bullish. Until the very end of the quarter, when the Greek debt crisis and Chinese equity selloff suddenly escalated, oil price volatility was subdued, with prices mostly range-bound. The 2Q averages came in at $62/Bbl for Brent (up 13% sequentially) and $58/Bbl for WTI (up 19% sequentially). The Brent-WTI price spread, $4/Bbl, was slightly narrower than in 1Q. Following the recovery since January’s trough, we anticipate prices will remain broadly on par with recent levels through year-end 2015, followed by further gains in 2016. Barring a truly major economic crisis (to be clear, “Grexit” in and of itself would not count), we don’t envision oil prices falling back to the lows of 1Q. See page 4 for details on our oil price assumptions.

Natural Gas

With 1Q15 being considerably warmer than the year-ago winter, the quarterly Henry Hub average came in at $2.97/Mcf – down not just year-over-year but again sequentially as well. Not surprisingly, seasonality in 2Q15 exerted further pressure on gas prices, and the quarterly average of $2.67/Mcf was the lowest since 2Q12. Production growth is still outstripping demand growth for the time being – even with collapse in liquids drilling activity and the resulting effect on gas volumes from liquids-rich resource plays. Growth in industrial gas demand has been frustratingly slow, and LNG exports will not be needle-moving until 2017 at the earliest. We project flattish prices through year-end 2015, with only modest recovery in 2016. See page 4 for details on our gas price assumptions.

Stocks

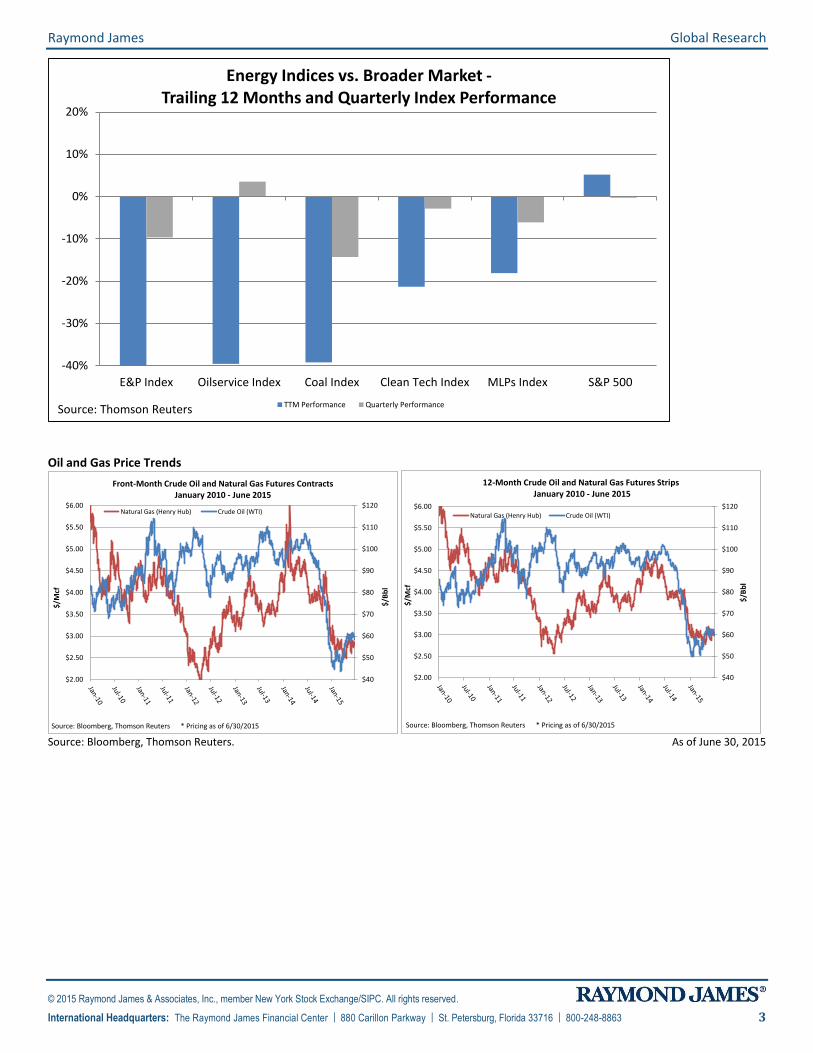

During most of 2Q15, similar to 1Q, broader U.S. markets were mostly range-bound, with low-volatility action in equities. At the end of June, however, volatility reared its head again, as troubling headlines from Greece and China caused a global sell-off in equities and commodities alike, with some spillover into July. Even so, the S&P 500 edged down merely 0.2% for the full quarter, essentially canceling out 1Q’s gain of 0.4%. Energy stocks were mixed – in the wake, of course, of having been the S&P 500’s worst-performing sector in 2014. The two broadest energy subsector indices, E&P and oil service, posted a 2Q loss of 6% and gain of 5%, respectively. See the chart on page 3 for details on the performance of various energy indices.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 2

Contents

Stats of the Week .................................................................... 5

Global Research Highlights ...................................................... 6

Exploration and Production ..................................................... 7

Oilfield Services ..................................................................... 15

Integrated Oil and Gas / Independent Refiners .................... 18

Renewable Energy and Clean Technology ............................. 23

Canadian Oil and Gas............................................................. 31

European Oil and Gas ............................................................ 34

Argentinean Oil and Gas ........................................................ 36

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 3

-40%

-30%

-20%

-10%

0%

10%

20%

E&P Index Oilservice Index Coal Index Clean Tech Index MLPs Index S&P 500

Energy Indices vs. Broader Market -Trailing 12 Months and Quarterly Index Performance

TTM Performance Quarterly PerformanceSource: Thomson Reuters

Oil and Gas Price Trends

$40

$50

$60

$70

$80

$90

$100

$110

$120

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$/B

bl

$/M

cf

Front-Month Crude Oil and Natural Gas Futures ContractsJanuary 2010 - June 2015

Natural Gas (Henry Hub) Crude Oil (WTI)

Source: Bloomberg, Thomson Reuters * Pricing as of 6/30/2015

$40

$50

$60

$70

$80

$90

$100

$110

$120

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$/B

bl

$/M

cf

12-Month Crude Oil and Natural Gas Futures StripsJanuary 2010 - June 2015

Natural Gas (Henry Hub) Crude Oil (WTI)

Source: Bloomberg, Thomson Reuters * Pricing as of 6/30/2015

Source: Bloomberg, Thomson Reuters. As of June 30, 2015

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 4

Q1 14A Q2 14A Q3 14A Q4 14A 2014A

$99.00 $103.00 $98.00 $73.00 $93.25

$108.00 $110.00 $102.00 $76.00 $99.00

$9.00 $7.00 $4.00 $3.00 $5.75

Q1 15A Q2 15A Q3 15E Q4 15E 2015E

$48.49 $57.85 $58.70 $58.92 $55.99

$58.00 $50.00 $55.00 $60.00 $55.75

WTI New RJ Oil $48.49 $57.85 $55.00 $60.00 $55.00

$55.13 $62.06 $63.19 $64.03 $61.10

$63.00 $59.00 $62.00 $67.00 $62.75

Brent New RJ Oil $55.13 $62.06 $62.00 $67.00 $62.00

$6.64 $4.21 $7.00 $7.00 $7.00

Q1 16E Q2 16E Q3 16E Q4 16E 2016E

$59.92 $60.57 $61.09 $62.11 $60.92

WTI New RJ Oil $61.00 $64.00 $67.00 $68.00 $65.00

$65.28 $66.74 $68.14 $67.85 $67.00

Brent New RJ Oil $68.00 $71.00 $74.00 $75.00 $72.00

$7.00 $7.00 $7.00 $7.00 $7.00

Long-Term Forecast

$80.00

WTI New RJ Oil $70.00

$87.00

Brent New RJ Oil $77.00

$7.00

Source: Bloomberg, Thomson Reuters, Raymond James research

2017-2020

Brent-WTI Spread

Old RJ Oil Est.

Old RJ Oil Est.

Brent Futures

2016

WTI Futures

Brent-WTI Spread

WTI Futures

Old RJ Oil Est.

Old RJ Oil Est.

WTI

Brent

2015

RJ&A Oil Price Forecast (as of July 2015)

Brent-WTI Spread

2014

Brent Futures

Brent-WTI Spread

Q1 Q2 Q3 Q4 2014

$4.93 $4.57 $4.08 $3.94 $4.38

Q1 15A Q2 15A Q3 15E Q4 15E 2015E

$2.97 $2.67 $2.94 $3.35 $2.98

$2.97 $2.67 $2.79 $2.97 $2.85

$2.97 $2.65 $2.55 $3.00 $3.00

$2.97 $2.67 $2.55 $3.00 $2.80

Q1 16E Q2 16E Q3 16E Q4 16E 2016E

$3.23 $3.06 $3.12 $3.24 $3.16

$3.20 $3.50 $3.75 $3.75 $3.55

$3.20 $3.50 $3.75 $3.75 $3.55

2017E 2018E 2019E 2020E

$3.34 $3.42 $3.48 $3.60

$3.75 $3.75 $3.75 $3.75

$3.75 $3.75 $3.75 $3.75

Source: Bloomberg, Thomson Reuters, Raymond James research

2015

Current RJ Gas

Old RJ Gas

Old RJ Gas

2014 H Hub Actual

RJ&A Henry Hub Natural Gas Price Forecast (as of July 2015)

NYMEX Futures

Bloomberg Consensus

2016

2017-2020

RJ Long-Term Gas

Current RJ Gas

NYMEX Futures

Old RJ Gas

NYMEX Futures

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 5

Stats of the Week

In Case You Missed It… Here is a Recap of All the Energy Stats of the Week from 2Q15

April 6: Bakken Production Outlook; Estimating Timing of Roll-Over and Rebound

April 13: U.S. Rig Count - When Will It Bottom and Is There Anything to Get Excited About?

April 20: Oil's "Junk Rally" Can't Hide the Near-Term Risk; Lowering 2015, 2016, L-T Price Deck

April 27: Despite Shell/BG Record, Don't Bank on a Surge in Corporate Upstream M&A

May 4: Waiting for a Rebound in U.S. Gas Prices? Industrial Demand Will Keep You Waiting

May 11: OTC - Market Uncertainty Still Pulls Sizeable Crowd Despite Downturn

May 18: Despite Oil Meltdown, Frontier Exploration Is More Robust Than You Might Think

May 26: NAPTP MLP Conference Bolsters Confidence in Continued LT Infrastructure Development

June 1: Small-Cap Managers Do Your Homework, Benchmark Energy Weighting Set to Increase

June 8: Permian Conference Takeaways - This Basin Is Hot With 2H15 Activity Set to Climb

June 15: What Are "Missing Barrels" and What Do They Mean for Oil Prices?

June 22: Missing Barrels, Part Deux - Zeroing in on Chinese Demand and Floating Storage

June 29: When Will U.S. Crude Production Roll Over? It Already Has!

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 6

Global Research Highlights

In Case You Missed It… The List Below Highlights One Featured 2Q15 Report from Each RJ Energy Analyst

Marshall Adkins: Newpark: Upgrading to Strong Buy; Sell-Off on Revised Guidance Excessive

Andrew Bradford: Enerflex: Record Low Bookings Overshadow Largely In-Line 1Q15

Andrew Coleman: RRC: Upgrading to Outperform; Truing up 2Q15 on Commodity Prices

Chris Cox: Initiating Coverage on Canada's Midstream Players

John Freeman: Memorial Resource: Thoughts from the Road; Remains a Top Pick

Cory Garcia: Refining Monthly Crack Check, June 2015: Despite Margin Strength, Stocks Still Stuck in a Rut

Bertrand Hodee: Saipem: Strong deleveraging in sight, intrinsic recovery story, upgrade to Outperform

Darren Horowitz: NGL Update: Reconciling 1H15 Volatility in Attempt to Manage 2H15 Expectations

Pavel Molchanov: A Letter from Prison: Highlights from a Tour of the Alcatraz Microgrid with Princeton Power

Kurt Molnar: Boulder Energy: A Hefty Opportunity

Praveen Narra: Lack of Contracting Should Put Lid on Offshore Drilling Rally

Kevin Smith: Black Stone Minerals: Delivering 'Stone' Cold Dist. Growth; Initiating With an Outperform

Santiago Wesenack: YPF & Petronas to Invest Jointly in Shale Oil at La Amarga Chica

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 7

Exploration and Production

Stock Performance in 2Q15 and YTD

-80% -60% -40% -20% 0% 20% 40%

4-CRK3-GDP4-SFY4-SD2-PQ

3-CHK4-REN2-BCEI3-CNX

4-HK4-WTI4-BBG3-SGY4-DNR3-EXXI2-OAS

3-CWEI2-AR

3-SWN2-QEP

4-MUR3-UPL3-NFG3-NBL2-APA2-RRC3-COP2-TGA

2-MRO2-HES2-WLL2-PXD1-OXY2-DVN2-EOG2-APC

S&P Energy3-KOS

3-ROSE2-CLR3-CRC

2-WPX3-EGN3-XEC

3-COG3-NOG

2-IOCS&P 500

2-RSPP3-LPI3-SM

2-CXO2-FANG

YTD Stock Price Performance

-60% -40% -20% 0% 20% 40% 60% 80%

4-SD3-GDP3-EXXI

4-HK2-BCEI3-CRC3-CHK3-CNX3-UPL2-PXD

3-NOG2-PQ

3-SGY4-DNR

4-MUR3-NBL3-SM

2-QEP2-CLR2-APC4-CRK4-SFY3-LPI

3-XEC2-APA2-RRC2-EOG2-CXO2-DVN2-HES3-NFG

2-ARS&P Energy

2-FANG3-COP

3-SWN2-MRO3-NFX

S&P 5004-BBG3-EGN3-KOS1-OXY2-WLL4-WTI3-COG

2-PE2-MRD2-TGA2-OAS2-WPX2-RSPP3-CWEI

2-IOC3-ROSE

4-REN

2Q15 Stock Price Performance

RJ Ratings: 1 = Strong Buy, 2 = Outperform, 3 = Market Perform, 4 = Underperform, S = Suspended This analysis does not include transaction costs and tax considerations. If included, these costs would reduce an investor’s return. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. A complete record of our Exploration & Production stock recommendations for the trailing 12 months is available upon request.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 8

Last Quarter’s E&P Results

In 2Q15, the EPX was down 7%, whereas oil was up 19% and S&P 500 ended up settling flat. The best performers during the quarter were Resolute Energy (REN), Rosetta Resources (ROSE), InterOil (IOC), and Clayton Williams (CWEI). The worst performers for the quarter were SandRidge (SD), Goodrich Petroleum (GDP), Energy XXI (EXXI), and Halcon (HK).

E&P Outlook and Investment Thesis

Following the oil price collapse of late 2014 to early 2015, the second quarter was witness to a strong rally in crude markets. West Texas Intermediate was up 19% on the quarter, settling around $60. While crude prices give us an understanding of where top-line levels will materialize, we believe rig count is a strong proxy for where well costs are headed in the E&P space. Watching the Baker Hughes rig count, we have seen a 55% decline in U.S. onshore rigs from the peak in October of last year. While not completely in lock-step, well costs have largely followed this decline throughout the major U.S. basins, particularly in the Permian and Bakken. Coupled with well cost reduction has been a tide of companies focused on high-grading and improving efficiency across basins. Higher IP-30’s and EURs throughout the majority of unconventional plays is largely a result of these efforts. As such, while U.S. E&P’s have cut spending nearly 40% y/y, production is expected to remain largely flat due to the dual effects of lower costs and higher well productivity.

The paradigm shift has helped differentiate acreage in terms of grading for most of the plays. We have seen the focus shift toward the Permian as companies re-structure their drilling activity toward the play because of its immense stacked pay potential and the prospective upside in the form of efficiency improvements. Accordingly, Permian-heavy names have witnessed stock outperformance relative to peers. We expect to see this play help drive a significant portion of the U.S. oil production growth in the coming years.

Oil prices have been falling for over three quarters now, and the futures curve has been forced from being backwardated to being in contango. On the hedging front, the E&P companies have not had enough time to engage in 2015 and 2016 hedges since the mid-2014 oil price collapse; however, some companies are still well hedged for 2015 (e.g., Bill Barrett-100%, Laredo-99%, Pioneer-92%, Antero-97%, and Memorial-89%). On a cumulative basis, ~22% of our E&P coverage universe’s 2015E oil production is hedged; however, large caps are not as well-hedged as SMid caps, and quite a few companies have no hedges at all. Therefore, for companies involved in hedges, on average, ~57% of their 2015E oil production is hedged. Similarly, on a cumulative basis, 23% of our coverage universe’s 2015E gas production is hedged. For companies involved in hedges, ~48% of their 2015E gas production is hedged.

During the second half of 2015, we expect oil prices to solidify around $60 and gas prices to approach $3 by year’s end. Therefore, commodity price pressure remains high in the second quarter, and the stocks should rebound once prices start firming up in the second half of the year. In our coverage universe, our only Strong Buy-rated E&P name is Occidental Petroleum (OXY). We currently have the following Outperform-rated E&P names: Anadarko Petroleum (APC), Antero (AR), Apache (APA), Cimarex (XEC), Concho Resources (CXO), Continental Resources (CLR), Devon Energy (DVN), EOG Resources (EOG), Hess Corp. (HES), Marathon Oil (MRO), Pioneer Natural Resources (PXD), QEP Resources (QEP), Range Resources (RRC), Whiting Petroleum (WLL), Bonanza Creek (BCEI), Diamondback Energy (FANG), InterOil Corp. (IOC), Memorial Resource Development (MRD), Oasis Petroleum (OAS), Parsley Energy (PE), PetroQuest Energy (PQ), RSP Permian (RSPP), TransGlobe Energy (TGA), and WPX Energy (WPX).

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 9

The large-cap stocks trading at the lowest 2015E EV/EBITDA multiples are Whiting (WLL), QEP Resources (QEP), Murphy (MUR), Apache Corp (APA). The small-cap stocks trading at the lowest 2015E EV/EBITDA multiples are TransGlobe Energy (TGA), SM Energy (SM), Northern Oil and Gas (NOG), and Bill Barrett (BBG).

Large Caps: EV/EBITDA Multiples vs. Reserve Life

0

4

8

12

16

20

24

28

32

36

40

44

48

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0xW

LL

QEP

MU

R

APA

SW

N

APC

HES

MRO

RRC

NBL

CLR

DN

R

CXO

CO

P

OXY

CH

K

DVN

XEC

EO

G

PXD

CO

G

AR

Years

EV / 2015E EBITDA Reserve Life

Source: FactSet, Raymond James research. As of July 10, 2015.

Small and Mid-Caps: EV/EBITDA Multiples vs. Reserve Life

0

5

10

15

20

25

30

35

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

TG

A

SM

NO

G

BBG

SG

Y

NFX

OAS

BCEI

RO

SE

CRC

CRK

GD

P

SD

HK

WTI

PQ

UPL

LPI

EG

N

CW

EI

KO

S

EXXI

SFY

NFG

RSPP

REN

FAN

G

MRD PE

Years

EV / 2015E EBITDA Reserve Life

Source: FactSet, Raymond James research. As of July 10, 2015.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 10

The large-cap stocks trading at the lowest proved reserve multiples are Chesapeake (CHK), QEP Resources (QEP), Denbury (DNR), and Range Resources (RRC). The small-cap stocks trading at the lowest proved reserve multiples are Swift (SFY), Resolute (REN), Energy XXI (EXXI), and Goodrich Petroleum (GDP).

Large Caps: Enterprise Value/Proved Reserves vs. Reserve Life

0

5

10

15

20

25

30

35

40

45

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

CH

K

DN

R

QEP

RRC

AR

SW

N

APA

MRO

DVN

CO

P

MU

R

WLL

NBL

CLR

CO

G

HES

APC

OXY

XEC

EO

G

CXO

PXD

Years

Enterprise Value/Mcfe Reserve Life (Years)

Source: Company Reports , FactSet and RJ&A Estimates.Source: Company Reports , FactSet and RJ&A Estimates.Source: Company Reports , FactSet and RJ&A Estimates.

Source: FactSet, Raymond James research. As of July 10, 2015.

Small and Mid-Caps: Enterprise Value/Proved Reserves vs. Reserve Life

0

5

10

15

20

25

30

35

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

SFY

EXXI

REN

GD

P

CRK

BBG

PQ

UPL

CRC

WTI

NO

G

SG

Y

HK

RO

SE

SD

OAS

SM

NFX

LPI

BCEI

CW

EI

TG

A

EG

N

NFG

MRD PE

RSPP

FAN

G

KO

S

Years

Enterprise Value/Mcfe Reserve Life (Years)

Source: Company Reports , FactSet and RJ&A Estimates.Source: Company Reports , FactSet and RJ&A Estimates.Source: Company Reports , FactSet and RJ&A Estimates.

Source: FactSet, Raymond James research. As of July 10, 2015.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 11

The large-cap stocks trading at the lowest percentage of proved NAV/share are Murphy (MUR), Marathon (MRO), Hess (HES), and QEP (QEP). The small-cap stocks trading at the lowest percentage of proved NAV/share are InterOil (IOC), Northern Oil and Gas (NOG), Energy XXI (EXXI), and California Resources (CRC).

Large Caps: % of Proved NAV/Share

0%

100%

200%

300%

400%

500%

600%

700%M

UR

MRO

HES

QEP

APA

SW

N

RRC

CO

P

APC

CH

K

OXY

DVN

NBL

CO

G

EO

G

CLR

WLL

XEC

PXD

CXO

Source: FactSet, Raymond James research. As of July, 2015.

Small and Mid-Caps: % of Proved NAV/Share

0%

100%

200%

300%

400%

500%

600%

700%

IOC

NO

G

CRC

EXXI

TG

A

NFG

CW

EI

EG

N

FAN

G

BCEI

WTI

SM

KO

S

RSPP

MRD

RO

SE

PE

Source: FactSet, Raymond James research. As of July 10, 2015.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 12

Production Growth per Debt-Adjusted Share

The following chart ranks our coverage universe on production growth per debt-adjusted share over the time period indicated. We suggest investors use this tool to screen for potentially top-performing stocks, in addition to other relevant factors, including: 1) absolute and relative valuations; 2) leverage to changes in commodity prices; and 3) company-specific financial and operational risk profiles.

According to our analysis, the companies with the highest projected production growth per debt-adjusted share over the 2014-2016 period are Memorial Resource Development (MRD), RSP Permian (RSPP), Antero (AR), and Diamondback (FANG).

Raymond James E&P Research Universe – Market Valuation Database

Raymond James E&P Comps Sheet - Large CapsPriced Enterprise EV / EBITDA Multiples (RJ) EV / EBITDA Multiples (Consensus) Y/Y Production Growth Debt Adjusted Production Commodity Mix Value per

Name Ticker Analyst Rating 7/10/2015 Value ($mm) 2014 2015 2016 2014 2015 2016 2014 2015 2016 Growth 2014 - 2016 Oil Gas NGLs Flowing BarrelLarge Caps

Anadarko Petroleum Corp. APC AC MO-2 $75.71 59,711 5.0x 12.0x 9.1x 5.2x 11.5x 9.3x 7% -1% 1% -10.2% 36% 49% 15% $64,390.54

Antero Resources AR JF MO-2 $30.19 12,097 10.3x 9.6x 7.4x 10.5x 10.1x 8.4x 93% 41% 28% 15.8% 2% 84% 15% $48,875.73

Apache Corporation APA JF MO-2 $52.94 29,220 3.6x 6.6x 5.6x 3.0x 6.6x 5.7x -15% -15% -12% -6.2% 50% 40% 10% $45,197.39

Cabot Oil & Gas COG AC MP-3 $29.30 13,190 9.4x 13.9x 10.0x 9.0x 13.7x 10.8x 29% 14% 14% 12.5% 6% 94% 0% $41,563.13

Chesapeake Energy CHK JF MP-3 $11.37 23,670 3.7x 11.2x 10.6x 4.7x 9.0x 10.1x 6% -9% -4% -26.0% 18% 71% 11% $34,489.65

Cimarex Energy XEC AC MP-3 $105.28 10,720 6.9x 14.3x 11.1x 6.6x 12.9x 9.5x 25% 8% -6% -4.7% 32% 47% 20% $67,941.19

Concho Resources CXO JF MO-2 $108.44 17,731 8.4x 11.5x 9.0x 8.8x 10.3x 9.6x 22% 20% 6% 5.6% 68% 32% 0% $134,136.13

ConocoPhill ips COP PM MP-3 $59.13 110,156 5.1x 8.6x 6.2x 5.4x 9.8x 6.9x 1% 2% 6% -2.1% 58% 42% 0% $68,441.28

Continental Resources CLR AC MO-2 $37.36 20,490 5.4x 9.6x 6.9x 5.7x 10.3x 7.8x 28% 22% 10% 4.4% 71% 29% 0% $105,913.94

Denbury Resources DNR AC MU-4 $5.30 5,222 3.9x 6.0x 7.6x 3.9x 5.3x 6.7x 6% 0% -1% -24.5% 95% 5% 0% $70,225.81

Devon Energy DVN AC MO-2 $55.85 48,282 4.7x 10.0x 9.6x 6.8x 9.4x 10.4x -3% -1% 0% 4.1% 40% 40% 20% $70,467.60

EOG Resources EOG AC MO-2 $84.54 51,728 5.5x 11.1x 8.9x 5.8x 11.4x 8.9x 17% -3% 8% 1.7% 51% 37% 13% $85,186.81

Hess Corp. HES PM MO-2 $64.34 26,557 3.8x 7.9x 5.7x 4.1x 8.2x 6.8x -2% 10% 4% 4.1% 73% 27% 0% $73,634.17

Marathon Oil MRO PM MO-2 $24.46 25,182 4.2x 7.7x 5.7x 4.5x 9.1x 7.1x -12% 0% 2% -4.9% 71% 29% 0% $54,861.66

Murphy Oil MUR PM MU-4 $40.06 10,572 2.7x 5.5x 4.8x 3.0x 7.0x 5.8x 10% -11% -1% -13.7% 68% 32% 0% $47,715.49

Noble Energy NBL JF MP-3 $39.06 21,353 5.8x 9.9x 6.6x 5.9x 8.2x 6.7x 0% 12% 10% -5.7% 33% 57% 10% $67,148.99

Occidental Petroleum OXY PM SB-1 $73.31 62,263 5.5x 10.5x 7.8x 4.7x 10.2x 7.6x -7% -7% 3% -2.9% 76% 24% 0% $96,582.28

Pioneer Natural Resources PXD JF MO-2 $134.46 22,451 9.0x 13.2x 10.7x 8.9x 13.1x 11.1x 9% 8% 15% 7.4% 51% 31% 18% $115,830.31

QEP Resources QEP AC MO-2 $16.18 4,830 3.1x 5.7x 4.6x 3.1x 5.4x 5.4x 4% -7% 7% -15.1% 36% 57% 8% $34,693.30

Range Resources RRC AC MO-2 $45.27 12,241 9.1x 12.5x 10.7x 9.7x 13.0x 12.1x 24% 19% 16% 8.1% 6% 67% 27% $55,321.68

*Southwestern SWN AC MP-3 $20.92 13,490 5.8x 7.3x 6.0x 5.9x 7.8x 6.7x 17% 24% 11% -4.8% 1% 94% 5% $31,282.58

Whiting Petroleum WLL JF MO-2 $30.11 11,753 5.5x 8.7x 5.5x 5.5x 8.3x 6.5x 22% 42% 5% -10.5% 81% 12% 7% $70,407.03

Median 20,922 5.4x 9.8x 7.4x 5.6x 9.6x 7.7x 8% 5% 5% -3.8% 50% 40% 7% $67,545.09

Mean 27,860 5.7x 9.6x 7.7x 5.9x 9.6x 8.2x 13% 8% 6% -3.1% 46% 45% 8% $67,468.49 Source: Thomson Reuters, Raymond James research.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 13

Raymond James E&P Comps Sheet - SMID CapsPriced Enterprise EV / EBITDA Multiples (RJ) EV / EBITDA Multiples (Consensus) Y/Y Production Growth Debt Adjusted Production Commodity Mix Value per

Name Ticker Analyst Rating 7/10/2015 Value ($mm) 2014 2015 2016 2014 2015 2016 2014 2015 2016 Growth 2014 - 2016 Oil Gas NGLs Flowing Barrel0

Bill Barrett BBG JF MU-4 $7.39 1,046 5.9x 3.9x 4.3x 3.7x 4.3x 5.2x -37% -32% 13% -36.8% 71% 19% 10% $59,556.98

Bonanza Creek BCEI AC MO-2 $13.76 1,400 3.6x 5.1x 4.8x 3.6x 5.3x 5.1x 45% 23% 2% -19.7% 60% 24% 16% $50,881.36

California Resources CRC PM MP-3 $5.26 9,118 3.8x 9.1x 6.3x 3.7x 9.6x 7.1x 4% 0% -2% -8.4% 76% 24% 0% $54,816.71

Clayton Williams CWEI AC MP-3 $48.55 1,441 4.8x 13.5x 10.2x 4.8x 12.8x 9.9x 10% -6% -15% -27.4% 76% 15% 9% $83,797.75

Comstock Resources CRK JF MU-4 $2.01 1,306 3.1x 6.9x 6.6x 3.0x 7.5x 6.4x -8% 2% 4% -59.6% 43% 57% 0% $48,906.23

Diamondback Energy FANG JF MO-2 $70.89 3,438 8.5x 7.9x 6.8x 8.6x 7.8x 7.0x 166% 59% 13% 28.7% 77% 10% 13% $112,210.52

Energen Corporation EGN JF MP-3 $61.72 5,557 5.1x 8.1x 9.9x 6.2x 7.7x 8.0x 1% -14% 0% -16.7% 51% 35% 14% $79,274.84Energy XXI EXXI AC MP-3 $2.22 4,847 5.9x 10.0x 8.5x 6.7x 7.5x 10.9x 13% 14% -3% -58.7% 69% 31% 0% $80,830.65Goodrich Petroleum GDP JF MP-3 $1.57 750 6.4x 7.4x 8.9x 5.4x 6.8x 8.4x -10% -21% -20% -67.2% 56% 44% 0% $86,545.93Halcon Resources HK AC MU-4 $1.12 4,446 5.7x 6.6x 7.6x 5.8x 6.5x 8.0x 27% -3% -1% -44.1% 81% 10% 8% $96,507.98InterOil Corp. IOC PM MO-2 $50.60 1,915 N/A N/A N/A N/A N/A N/A 0% 0% 0% 0.0% N/A N/A N/A N/A

Kosmos Energy KOS PM MP-3 $7.87 3,352 5.3x 6.8x 5.4x 5.5x 10.5x 6.0x 11% 0% 21% -2.6% 100% 0% 0% $158,841.30

Laredo Petroleum LPI JF MP-3 $11.19 3,252 6.1x 6.0x 6.3x 6.2x 7.4x 8.2x 23% 14% -3% -8.6% 51% 26% 23% $68,470.76

Memorial Resource Development MRD JF MO-2 $17.62 4,076 13.3x 10.4x 6.7x 12.0x 10.2x 6.8x 84% 55% 59% 56.4% 7% 81% 12% $88,349.81

Northern Oil and Gas NOG JF MP-3 $5.82 1,133 3.7x 4.3x 5.0x 3.7x 4.2x 5.7x 29% -1% -3% -35.4% 87% 13% 0% $66,666.19

Newfield Exploration NFX AC MP-3 $35.47 7,771 5.2x 5.7x 5.5x 5.5x 6.5x 5.4x -1% 14% -7% 3.2% 48% 37% 15% $57,070.87

National Fuel Gas NFG KS MP-3 $55.19 7,207 7.6x 8.2x 7.3x 7.5x 8.7x 8.0x 33% 12% -2% -5.1% 10% 90% 0% $82,540.22

Oasis Petroleum OAS AC MO-2 $12.51 4,091 4.4x 5.4x 6.7x 4.4x 5.7x 7.1x 35% 6% -4% -29.1% 89% 11% 0% $81,588.76

Parsley Energy PE JF MO-2 $16.65 2,969 14.2x 16.4x 9.5x 14.2x 15.6x 10.1x 184% 45% 39% 21.9% 59% 23% 18% $156,922.23

PetroQuest Energy PQ AC MO-2 $1.72 686 4.8x 13.2x 11.9x 4.5x 10.8x 11.0x 14% -21% -13% -29.3% 9% 76% 15% $35,686.41

Resolute Energy REN JF MU-4 $0.74 838 6.2x 6.0x 6.9x 5.7x 7.0x 8.5x 4% -2% 3% -56.2% 72% 20% 8% $62,079.19

Rosetta Resources ROSE JF MP-3 $21.14 3,214 4.5x 7.4x 5.7x 3.9x 7.7x 8.2x 32% -9% -1% -21.1% 28% 38% 34% $48,880.43

RSP Permian RSPP JF MO-2 $26.65 2,475 11.5x 10.0x 8.2x 11.5x 9.6x 8.6x 63% 54% 29% 24.8% 48% 43% 9% $99,652.09

SandRidge Energy SD JF MU-4 $0.71 5,006 5.1x 8.0x 10.4x 5.4x 9.0x 10.9x -11% 3% -15% -60.3% 34% 50% 16% $57,075.01

SM Energy SM AC MP-3 $42.47 5,462 3.4x 4.5x 4.3x 3.3x 5.0x 4.9x 14% 17% -7% -6.5% 32% 45% 23% $31,069.68

Stone Energy SGY JF MP-3 $10.93 1,768 3.7x 5.1x 4.7x 3.8x 5.2x 6.0x -8% -4% -1% -37.6% 39% 45% 16% $38,203.62

Swift Energy SFY AC MU-4 $1.41 1,309 3.9x 11.3x 9.3x 3.7x 12.1x 9.6x 5% -7% -4% -61.4% 22% 64% 14% $38,437.66

TransGlobe Energy TGA PM MO-2 $3.62 156 0.8x 3.5x 2.2x 0.9x N/A N/A -12% -11% 3% 0.3% 100% 0% 0% $10,285.84

Ultra Petroleum UPL AC MP-3 $10.44 5,384 6.6x 8.4x 7.2x 6.6x 8.4x 8.0x 7% 15% 2% -15.6% 8% 92% 0% $41,287.68

W&T Offshore WTI JF MU-4 $4.67 1,804 3.1x 6.9x 4.6x 3.2x 8.7x 5.9x -2% -1% 0% -33.4% 43% 47% 10% $36,940.79

WPX Energy WPX AC MO-2 $11.22 4,323 3.8x 4.4x 5.4x 3.7x 4.7x 6.2x -9% -18% -7% -13.9% 20% 70% 10% $25,581.05

Median 3,214 5.1x 7.4x 6.8x 5.4x 7.7x 8.0x 11% 0% -1% -19.7% 51% 36% 9% $64,372.69

Mean 3,316 5.7x 7.9x 7.1x 5.7x 8.3x 7.8x 26% 8% 3% -19.6% 53% 38% 10% $69,779.30 Source: Thomson Reuters, Raymond James research.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 14

Raymond James E&P Debt Comps - Large CapsPriced Market Net Debt Net Debt / TTM EBITDA Interest Net Debt / Boe Net Debt /

Name Ticker Analyst Rating 7/10/2015 Cap ($MM)) ($MM) Most Recent 2014 2015 2016 Coverage Proved Developed PV-10

Anadarko Petroleum Corp. APC AC MO $75.71 38,358 14,057 1.6x 0.7x 3.1x 2.6x 4.1x $4.92 $7.14 0.3x

Antero Resources AR JF MO $30.19 8,009 3,987 1.3x 3.5x 3.8x 3.5x 6.9x $1.89 $6.29 0.4x

Apache Corporation APA JF MO $52.94 19,958 9,446 0.4x 1.3x 0.7x 0.5x 61.1x $3.94 $5.72 0.2x

Cabot Oil & Gas COG AC MP $29.30 12,111 1,863 1.4x 1.2x 2.0x 1.5x 16.4x $1.51 $2.48 0.2x

Chesapeake Energy CHK JF MP $11.37 8,823 10,740 1.9x 1.6x 5.6x 5.6x 55.4x $4.01 $5.94 0.5x

Cimarex Energy XEC AC MP $105.28 9,030 1,379 1.0x 0.7x 2.0x 1.5x 31.9x $2.64 $3.44 0.2x

Concho Resources CXO JF MO $108.44 12,721 3,396 1.8x 1.7x 2.2x 2.0x 8.7x $5.33 $9.01 0.3x

ConocoPhill ips COP PM MP $59.13 73,648 19,847 1.1x 0.8x 1.8x 1.4x 26.6x $2.22 $3.47 0.1x

Continental Resources CLR AC MO $37.36 13,844 5,971 1.6x 1.6x 3.3x 2.5x 13.3x $4.42 $11.88 0.3x

Denbury Resources DNR AC MU $5.30 1,859 3,590 3.0x 2.6x 4.0x 5.0x 7.0x $8.20 $10.60 0.4x

Devon Energy DVN AC MO $55.85 23,066 9,891 1.0x 1.0x 1.4x 1.1x -18.6x $3.59 $4.79 0.4x

EOG Resources EOG AC MO $84.54 46,074 4,266 0.5x 0.4x 0.8x 0.8x 16.3x $0.85 $1.58 0.1x

Hess Corp. HES PM MO $64.34 18,240 4,474 0.8x 0.5x 1.6x 1.4x 18.0x $3.13 $5.87 0.1x

Marathon Oil MRO PM MO $24.46 16,511 5,268 1.2x 0.7x 1.6x 1.2x 19.3x $2.40 $3.58 0.2x

Murphy Oil MUR PM MU $40.06 7,140 1,633 0.5x 0.5x 1.1x 1.4x 29.1x $2.14 $3.42 0.1x

Noble Energy NBL JF MP $39.06 14,569 5,278 1.8x 1.4x 2.5x 2.2x -13.6x $4.14 $6.53 0.3x

Occidental Petroleum OXY PM SB $73.31 56,419 4,686 0.5x 0.3x 0.9x 0.8x 111.9x $1.66 $2.36 0.1x

Pioneer Natural Resources PXD JF MO $134.46 20,035 2,285 0.8x 0.7x 1.2x 1.3x 12.6x $2.86 $3.54 0.2x

QEP Resources QEP AC MO $16.18 2,851 1,718 1.2x 0.7x 2.2x 1.9x 8.5x $2.62 $4.69 0.2x

Range Resources RRC AC MO $45.27 7,518 3,261 1.0x 2.3x 3.3x 2.8x 7.2x $1.90 $5.25 0.3x

Southwestern SWN AC MP $20.92 7,857 4,646 2.1x 0.8x 2.3x 2.1x 22.8x $2.59 $4.68 0.5x

Whiting Petroleum WLL JF MO $30.11 6,242 5,130 1.2x 2.6x 3.9x 2.4x 9.7x $11.70 $22.43 0.6x

Median 13,282 4,560 1.2x 0.9x 2.1x 1.7x 14.8x $2.75 $5.02 0.3x

Mean 19,313 5,764 1.3x 1.2x 2.3x 2.1x 20.7x $3.58 $6.12 0.3x

Raymond James E&P Debt Comps - SMID CapsPriced Market Net Debt Net Debt / TTM EBITDA Interest Net Debt / Boe Net Debt /

Name Ticker Analyst Rating 7/10/2015 Cap ($MM)) ($MM) Most Recent 2014 2015 2016 Coverage Proved Developed PV-10

Bill Barrett BBG JF MU $7.39 356 769 2.5x 3.6x 3.7x 2.8x 4.4x $9.89 $20.06 0.3x

Bonanza Creek BCEI AC MO $13.76 613 737 1.9x 2.1x 2.9x 3.0x 3.1x $8.22 $15.92 0.5x

California Resources CRC PM MP $5.26 2,010 6,476 3.5x 2.7x 6.2x 4.2x 12.4x $8.44 $11.73 0.4x

Clayton Will iams CWEI AC MP $48.55 591 739 3.0x 2.3x 7.1x 5.6x 4.8x $9.80 $15.04 0.5x

Comstock Resources CRK JF MU $2.01 93 1,180 3.3x 2.5x 5.9x 6.1x 5.4x $11.41 $14.30 1.0x

Diamondback Energy FANG JF MO $70.89 4,156 579 1.3x 1.6x 1.1x 1.2x 11.2x $5.14 $8.72 0.2x

Energen Corporation EGN JF MP $61.72 4,495 1,237 1.2x 0.9x 2.0x 3.9x 24.2x $3.32 $4.68 0.2x

Energy XXI EXXI AC MP $2.22 210 3,994 5.2x 4.7x 8.3x 7.4x 2.9x $16.50 $25.38 0.8x

Goodrich Petroleum GDP JF MP $1.57 89 581 4.4x 4.9x 6.0x 7.8x 2.8x $12.75 $19.62 0.9x

Halcon Resources HK AC MU $1.12 604 3,703 4.7x 4.7x 5.8x 7.0x 5.4x $19.58 $33.15 0.8x

InterOil Corp. IOC PM MO $50.60 2,502 (221) 3.9x 12.2x 1.3x -7.2x -2.3x N/A N/A N/A

Kosmos Energy KOS PM MP $7.87 2,993 434 0.9x 0.4x 1.6x 1.6x 12.1x $5.76 $9.75 0.1x

Laredo Petroleum LPI JF MP $11.19 1,818 731 1.4x 3.3x 1.6x 1.5x 4.3x $2.96 $7.27 0.2x

Memorial Resource Development MRD JF MO $17.62 3,361 741 2.5x 2.5x 1.7x 1.0x 7.1x $2.72 $8.30 0.3x

Northern Oil and Gas NOG JF MP $5.82 352 790 2.6x 1.4x 2.9x 3.9x -7.0x $56.31 $133.56 0.5x

Newfield Exploration NFX AC MP $35.47 5,143 2,363 1.7x 1.9x 1.6x 1.4x 9.4x $3.66 $6.98 0.3x

National Fuel Gas NFG KS MP $55.19 4,698 1,605 0.8x 1.7x 2.3x 2.6x 10.7x $5.03 $5.20 0.5x

Oasis Petroleum OAS AC MO $12.51 1,248 2,654 2.8x 2.8x 3.1x 3.9x 5.9x $9.75 $18.14 0.5x

Parsley Energy PE JF MO $16.65 2,224 530 2.6x 3.0x 3.1x 2.2x 4.8x $5.83 $11.53 0.4x

PetroQuest Energy PQ AC MO $1.72 111 421 3.5x 2.9x 4.1x 3.8x 4.1x $6.36 $10.62 0.7x

Resolute Energy REN JF MU $0.74 55 766 2.0x 5.7x 5.0x 5.6x 4.3x $10.32 $18.47 0.8x

Rosetta Resources ROSE JF MP $21.14 1,355 1,831 2.8x 2.8x 4.1x 3.0x 7.9x $6.50 $13.23 0.6x

RSP Permian RSPP JF MO $26.65 2,084 397 0.7x 2.1x 2.4x 2.6x 13.0x $3.73 $9.47 0.3x

SandRidge Energy SD JF MU $0.71 392 4,470 5.1x 3.0x 5.8x 8.3x 3.5x $212.81 $336.92 0.8x

SM Energy SM AC MP $42.47 2,868 2,366 1.5x 1.5x 1.9x 1.9x 16.5x $4.32 $8.73 0.4x

Stone Energy SGY JF MP $10.93 614 883 0.6x 1.7x 3.1x 3.7x 13.3x $5.79 $10.72 0.5x

Swift Energy SFY AC MU $1.41 62 1,124 4.1x 3.2x 9.6x 8.5x 3.7x $5.80 $16.96 0.6x

TransGlobe Energy TGA PM MO $3.62 297 (61) -0.4x -0.4x -1.4x -0.8x 18.6x -$2.74 -$3.48 -0.1x

Ultra Petroleum UPL AC MP $10.44 1,626 3,345 4.5x 4.0x 5.2x 4.4x 5.2x $3.74 $8.12 0.5x

W&T Offshore WTI JF MU $4.67 354 1,256 2.4x 2.2x 4.8x 3.6x 6.5x $10.47 $17.32 0.5x

WPX Energy WPX AC MO $11.22 2,310 1,918 1.8x 2.0x 1.4x 1.6x 8.6x $2.64 $4.24 0.4x

Median 1,248 883 2.6x 2.5x 3.1x 3.7x 5.4x $6.09 $11.63 0.5x

Mean 1,621 1,574 2.6x 2.9x 3.8x 3.5x 7.4x $16.22 $28.44 0.5x Source: Thomson Reuters, Raymond James research.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 15

Oilfield Services

Stock Performance in 2Q15 and TTM

-35% -25% -15% -5% 5% 15% 25%

MP3-PACD

MP3-ORIG

MP3-HLX

MO2-HCLP

SB1-NR

MO2-EXLP

SB1-CCLP

MO2-USAC

MO2-OIS

MP3-ATW

SB1-SPN

MP3-DO

MO2-NOV

MP3-UNT

SB1-BHI

SB1-HAL

MP3-KEG

DJIA

MP3-WFT

SB1-PTEN

MO2-TTI

MP3-SLB

OSX

MP3-ESV

MO2-NBR

MP3-NE

MP3-BAS

MU4-RIG

MP3-FTI

MO2-CAM

MU4-PES

MO2-RDC

MO2-CELP

RJ Oilservice Universe - 2Q15Stock Performance

Source: Thomson ReutersSource: Thomson ReutersSource: Thomson Reuters

-28%

-90% -80% -70% -60% -50% -40% -30% -20% -10% 0% 10%

MP3-KEG

MP3-BAS

MP3-ORIG

MU4-PES

MP3-PACD

MU4-RIG

MP3-UNT

MP3-ESV

MO2-HCLP

MO2-NBR

MP3-ATW

MP3-HLX

MP3-DO

MP3-NE

MP3-WFT

SB1-PTEN

MO2-NOV

MO2-TTI

SB1-SPN

MO2-OIS

SB1-HAL

OSX

MO2-RDC

MP3-FTI

SB1-CCLP

SB1-NR

MO2-CELP

MP3-SLB

MO2-CAM

MO2-USAC

MO2-EXLP

SB1-BHI

DJIA

RJ Oilservice Universe - 12 Month Trailing Stock Performance

Source: Thomson Reuters

-84%

This analysis does not include transaction costs and tax considerations. If included these costs would reduce an investor’s return. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. A complete record of our Oil Service stock recommendations for the trailing 12 months is available upon request.

On average, oil service stocks gained modestly in 2Q15 but have since backtracked with oil to around 52-week lows. For 2Q15, the OSX gained 5%, as oil prices grew towards a plateau of ~$60 throughout the quarter. As oil prices rose early in the quarter, oil service stocks recovered quickly; however, as oil prices hit a plateau of $60 and began to show signs of weakness, stocks dipped late in the quarter. Investors remained very selective throughout the last quarter, with some names seeing strong performances and others remaining weak. The top performer in the quarter in our coverage was CELP, up 28%. The manufacturing group held up pretty well, with CAM (+15%) and FTI (+12%) as two of the top five performers in our coverage. There were strong and weak performers across most oil service subgroups, but companies more exposed to commodity prices, such as PES, KEG, and some offshore drillers, received a boost in the quarter from the uplift in crude prices. Not surprisingly, many stocks that were the best performers in 2Q15 are some of the worst performers over the past 12 months. Valuations are less stretched since retracement; North American onshore recovery still looks like the best play. We believe a bottom has formed within North American land activity, but the upturn will be slow and largely dependent on commodity prices. There has been substantial pricing pressure and overcapacity in many business lines (drilling and pressure pumping come to mind) that will take quite some time to work though; however, robust cost reduction efforts should begin to take hold in 2Q and 3Q to relatively maintain margins, and we believe margins begin to improve in the back half of the year. While we believe most investors understand that a U.S. land recovery is a matter of time, many remain concerned that low oil prices may delay a recovery. Internationally, we expect a much less sharp but somewhat more prolonged downturn. In 1Q, we saw pricing take a larger toll than activity, but throughout the remainder of the year we expect reduced activity levels to slowly slide before a late 2016 recovery. Offshore activity, on the other hand, is unlikely to see even a moderate uptick in activity for several years without severe changes to the cost structure. While valuations aren’t quite as attractive on 2015/2016

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 16

numbers, investors must understand they are not only buying the land-oriented group for service recovery, but also for a commodity price recovery. Oil price movements are the single largest driver of service stock performances, and although we remain cautious in the short-term due to dollar-based movements and strong OPEC production, we are optimistic on the intermediate-/long-term outlook. Keeping these factors in mind, our key oil service themes are: 1) activity will be decidedly weak in 2015, with substantial rig count declines and price concessions across all oil service sectors; 2) cost reductions for service companies from wage/headcount reductions and supply chain optimization should counteract much of this pricing weakness; 3) we believe a recovery in U.S. onshore is inevitable and timing remains largely dependent on commodity prices; and 4) capital spending declines and an oversupplied offshore rig market are likely to put substantial downward pressure on the offshore space for several years.

What are the most attractive oil service stocks in our view?

In today’s market, we believe the top names to own are high quality, North American land-oriented names with good balance sheets. These names include: 1) Strong Buy-rated Baker Hughes/Halliburton, given leverage to the North American land recovery and positive long-term trends from the acquisition; 2) Strong Buy-rated Newpark Resources, given strong growth avenues and market share gain potential; 3) Strong Buy-rated Superior, given a strong balance sheet and its free cash flow generation; 4) Strong Buy-rated CSI Compressco Partners, given its distribution growth outlook, high yield, and stable contract compression services, and 5) other North American land-leveraged names with strong ties to commodity prices, including Strong Buy-rated Patterson-UTI.

7/10/2015 Total Thomson Estimates Thomson Estimates Enterprise Value/

7/10/2015 Fisc. Ent. Revs Cap./ -Fiscal EPS- P/E Ratio -Fiscal EBITDA- EBITDA Total Total Debt to EBITDA

Symbol Company Price Year Value LTM Revs 2014 2015E 2016E 2014 2015E 2016E 2014 2015E 2016E 2014 2015E 2016E Debt 2014 2015E 2016E

DIVERSIFIEDS

BHI BHI* BAKER HUGHES $59.71 Dec. 28,423 $23,414 1.2 3.86 (0.09) 1.11 15.4 NM 53.6 4,662 2,109 4,969.6 6.1 13.5 5.7 4,055 0.9x 1.9x 0.8x

HAL HAL* HALLIBURTON $41.33 Dec. 40,636 $32,572 1.2 3.94 1.37 1.83 10.5 30.2 22.6 7,168 4,316 10,618.9 5.7 9.4 3.8 7,841 1.1x 1.8x 0.7x

SLB SLB* SCHLUM BERGER $83.96 Dec. 112,527 $47,642 2.4 5.51 3.45 3.82 15.2 24.3 22.0 13,694 10,044 2,140.8 8.2 11.2 52.6 12,726 0.9x 1.3x 5.9x

WFT WFT* WEATHERFORD INTERNATIONAL $11.33 Dec. 16,084 $14,109 1.1 1.00 (0.17) 0.33 11.4 NM 34.8 3,005 1,673 0.0 5.4 9.6 NA 7,832 2.6x 4.7x N/A

GROUP M ean 1.5 13.1 27.2 33.2 6.3 10.9 20.7 1.4x 2.4x 2.5x

MANUFACTURERS

CAM CAM * CAM ERON INTERNATIONAL $50.86 Dec. 10,829 $10,396 1.0 4.09 3.13 2.89 12.4 16.2 17.6 1,629 1,359 40.0 6.6 8.0 271.0 2,844 1.7x 2.1x 71.2x

CRR CRR CARBO CERAM ICS $35.74 Dec. 811 $574 1.4 3.26 (2.07) (0.55) 11.0 NM NM 159 -20 444.7 5.1 NA 1.8 75 0.5x -3.8x 0.2x

DRC DRC* DRESSER RAND GROUP $85.18 Dec. 7,458 $2,630 2.8 2.42 2.47 2.63 35.2 34.5 32.4 461 446 227.3 16.2 16.7 32.8 1,019 2.2x 2.3x 4.5x

DRQ DRQ DRIL QUIP $70.43 Dec. 2,368 $953 2.5 5.02 4.80 3.88 14.0 14.7 18.2 300 278 224.1 7.9 8.5 10.6 0 0.0x 0.0x 0.0x

FET FET FORUM ENERGY TECHNOLOGIES $18.50 Dec. 2,050 $1,684 1.2 1.86 0.84 1.01 10.0 22.0 18.3 347 200 996.1 5.9 10.3 2.1 469 1.3x 2.3x 0.5x

FTI FTI* FM C TECHNOLOGIES $37.45 Dec. 9,008 $7,797 1.2 2.85 2.53 2.22 13.1 14.8 16.9 1,313 1,065 2,311.4 6.9 8.5 3.9 1,316 1.0x 1.2x 0.6x

NOV NOV* NATIONAL OILWELL VARCO $44.99 Dec. 18,945 $21,371 0.9 6.00 2.98 2.53 7.5 15.1 17.8 4,573 2,668 694.1 4.1 7.1 27.3 4,245 0.9x 1.6x 6.1x

OII OII OCEANEERING INTERNATIONAL $44.30 Dec. 4,820 $3,606 1.3 3.99 2.87 2.94 11.1 15.4 15.1 858 682 219.7 5.6 7.1 21.9 750 0.9x 1.1x 3.4x

OIS OIS* OIL STATES INTERNATIONAL $34.14 Dec. 1,896 $1,752 1.1 3.62 0.66 1.03 9.4 51.4 33.3 447 192 49.7 4.2 9.9 38.2 206 0.5x 1.1x 4.2x

TESO TESO TESCO $10.02 Dec. 314 $513 0.6 0.91 (0.18) 0.12 11.0 NM NM 99 35 25.0 3.2 8.9 NA 0 0.0x 0.0x 0.0x

TWIN TWIN TWIN DISC $17.88 Dec. 190 $272 0.7 0.43 1.08 0.92 41.6 16.6 19.4 21 27 0.0 NA 7.0 NA 12 0.6x 0.5x N/A

GROUP M ean 1.3 16.0 22.3 21.0 6.6 9.2 45.5 0.9x 0.8x 9.1x

ONSHORE DRILLERS

HP HP HELM ERICH & PAYNE $64.11 Dec. 6,755 $3,877 1.7 6.29 2.90 0.90 10.2 22.1 71.4 1,568 1,131 1,144.9 4.3 6.0 5.9 572 0.4x 0.5x 0.5x

NBR NBR* NABORS INDUSTRIES $13.36 Dec. 7,089 $6,641 1.1 1.16 (0.21) (0.12) 11.5 NM NM 1,774 1,154 102.3 4.0 6.1 69.3 3,825 2.2x 3.3x 37.4x

PES PES* PIONEER DRILLING $4.71 Dec. 697 $1,010 0.7 0.38 (0.80) (0.87) 12.4 NM NM 261 114 570.9 2.7 6.1 1.2 430 1.7x 3.8x 0.8x

PDS PDS PRECISION DRILLING $5.79 Dec. 3,256 $2,190 1.5 0.76 (0.28) (0.10) 7.7 NM NM 811 485 149.4 4.0 6.7 21.8 2,010 2.5x 4.1x 13.5x

PKD PKD PARKER DRILLING $3.03 Dec. 842 $944 0.9 0.29 (0.30) (0.14) 10.3 NM NM 256 141 532.7 3.3 6.0 1.6 585 2.3x 4.1x 1.1x

PTEN PTEN* PATTERSON UTI ENERGY $17.71 Dec. 3,387 $3,162 1.1 1.55 (0.85) (0.91) 11.4 NM NM 988 530 461.5 3.4 6.4 7.3 880 0.9x 1.7x 1.9x

UNT UNT* UNIT $24.61 Dec. 2,170 $1,440 1.5 4.31 (0.37) 0.28 5.7 NM 89.2 767 385 0.0 2.8 5.6 NA 957 1.2x 2.5x N/A

GROUP M ean 1.2 9.9 22.1 80.3 3.5 6.1 17.9 1.6x 2.9x 9.2x OFFSHORE DRILLERS

ATW ATW* ATWOOD OCEANICS $24.30 Dec. 3,079 $1,318 2.3 4.91 7.14 4.70 5.0 3.4 5.2 544 746 699.3 5.7 4.1 4.4 1,607 3.0x 2.2x 2.3x

DO DO* DIAM OND OFFSHORE DRILLING $24.32 Dec. 11,770 $2,725 4.3 3.14 1.98 0.44 7.8 12.3 55.3 1,093 926 1,618.0 10.8 12.7 7.3 2,245 2.1x 2.4x 1.4x

ESV ESV* ENSCO $20.39 Dec. 7,814 $2,980 2.6 6.00 3.95 2.69 3.4 5.2 7.6 2,376 1,916 60.2 3.3 4.1 129.7 4,138 1.7x 2.2x 68.7x

HERO HERO* HERCULES OFFSHORE $0.21 Dec. 1,026 $766 1.3 (0.15) (1.59) (1.26) NM NM NM 238 -14 1,319.9 4.3 NA 0.8 1,211 5.1x -84.5x 0.9x

NE NE* NOBLE $14.29 Dec. 8,588 $3,678 2.3 2.98 2.17 1.16 4.8 6.6 12.3 2,017 1,594 796.8 4.3 5.4 10.8 5,212 2.6x 3.3x 6.5x

ORIG ORIG* OCEAN RIG $4.71 Dec. 4,503 $12,579 0.4 2.29 1.45 0.96 2.1 3.3 4.9 933 890 437.5 4.8 5.1 10.3 4,377 4.7x 4.9x 10.0x

PACD PACD* PACIFIC DRILLING $2.61 Dec. 3,264 $919 3.6 0.84 0.54 (0.36) 3.1 4.9 NM 557 545 896.7 5.9 6.0 3.6 2,835 5.1x 5.2x 3.2x

RDC RDC* ROWAN COM PANIES $19.41 Dec. 5,172 $1,994 2.6 2.14 2.76 2.34 9.1 7.0 8.3 694 914 1,545.0 7.5 5.7 3.3 2,807 4.0x 3.1x 1.8x

RIG RIG* TRANSOCEAN $14.62 Dec. 12,650 $8,878 1.4 4.79 2.33 (0.34) 3.1 6.3 NM 3,696 2,731 2,390.7 3.4 4.6 5.3 10,020 2.7x 3.7x 4.2x

SDRL SDRL SEADRILL $9.38 Dec. 15,968 $5,020 3.2 2.68 2.33 1.99 3.5 4.0 4.7 2,685 2,512 279.9 5.9 6.4 57.0 12,558 4.7x 5.0x 44.9x

VTG VTG VANTAGE DRILLING $0.16 Dec. 2,620 $861 3.0 0.14 0.10 (0.28) NM NM NM 422 397 0.0 6.2 6.6 NA 2,650 6.3x 6.7x N/A

GROUP M ean 2.5 4.6 5.9 14.0 5.6 6.1 23.3 3.8x -4.2x 14.4x

OFFSHORE CONSTRUCTION

GIFI GIFI* GULF ISLAND FABRICATION $11.24 Dec. 113 $471 0.2 1.36 0.15 0.10 8.3 NM NM 57 29 280.4 2.0 3.9 0.4 0 0.0x 0.0x 0.0x

HLX HLX* HELIX ENERGY SOLUTIONS GROUP $12.36 Dec. 1,440 $1,043 1.4 1.95 0.67 0.87 6.3 18.4 14.2 396 218 241.9 3.6 6.6 6.0 546 1.4x 2.5x 2.3x

M DR M DR M CDERM OTT INTERNATIONAL $5.07 Dec. 1,269 $2,248 0.6 (0.48) (0.14) 0.08 NM NM NM 53 176 0.0 23.8 7.2 NA 861 16.1x 4.9x N/A

GROUP M ean 0.7 7.3 18.4 14.2 9.8 5.9 2.2 5.8x 2.5x 0.8x

OFFSHORE SUPPLY/TRANSPORT

BRS BRS BRISTOW GROUP $50.58 Dec. 2,597 $1,771 1.5 4.34 4.13 4.12 11.6 12.3 12.3 316 334 165.3 8.2 7.8 15.7 939 3.0x 2.8x 5.7x

HELI HELI* CHC GROUP $0.63 Dec. 1,713 $1,708 1.0 (1.44) (1.53) (2.19) NM NM NM 240 207 248.0 7.1 8.3 6.9 1,219 5.1x 5.9x 4.9x

CKH CKH SEACOR HOLDINGS $68.42 Dec. 1,624 $1,270 1.3 1.60 2.02 3.45 42.8 34.0 19.8 236 199 74.3 6.9 8.2 21.9 880 3.7x 4.4x 11.8x

GLF GLF GULFM ARK OFFSHORE $10.30 Dec. 765 $465 1.6 2.37 (1.40) (1.20) 4.3 NM NM 171 54 211.2 4.5 14.2 3.6 561 3.3x 10.4x 2.7x

HOS HOS HORNBECK OFFSHORE SERVICES $19.24 Dec. 1,483 $633 2.3 2.47 0.95 0.66 7.8 20.2 29.0 292 215 619.7 5.1 6.9 2.4 1,076 3.7x 5.0x 1.7x

KEX KEX KIRBY $77.26 Dec. 5,118 $2,565 2.0 4.91 4.23 4.67 15.7 18.3 16.6 640 581 N/A 8.0 8.8 NA 819 1.3x 1.4x N/A

PHII PHII PETROLEUM HELICOPTERS $30.60 Dec. 435 $843 0.5 N/A N/A N/A NA NA NA N/A N/A 247.9 NA NA 1.8 540 N/A N/A 2.2x

TDW TDW TIDEWATER $22.35 Dec. 2,462 $1,539 1.6 3.55 3.32 0.64 6.3 6.7 34.9 413 421 0.0 6.0 5.9 NA 1,491 3.6x 3.5x N/A

GROUP M ean 1.5 14.8 18.3 22.5 6.5 8.6 8.7 3.4x 4.8x 4.8x Source: Thomson Reuters, Raymond James research.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 17

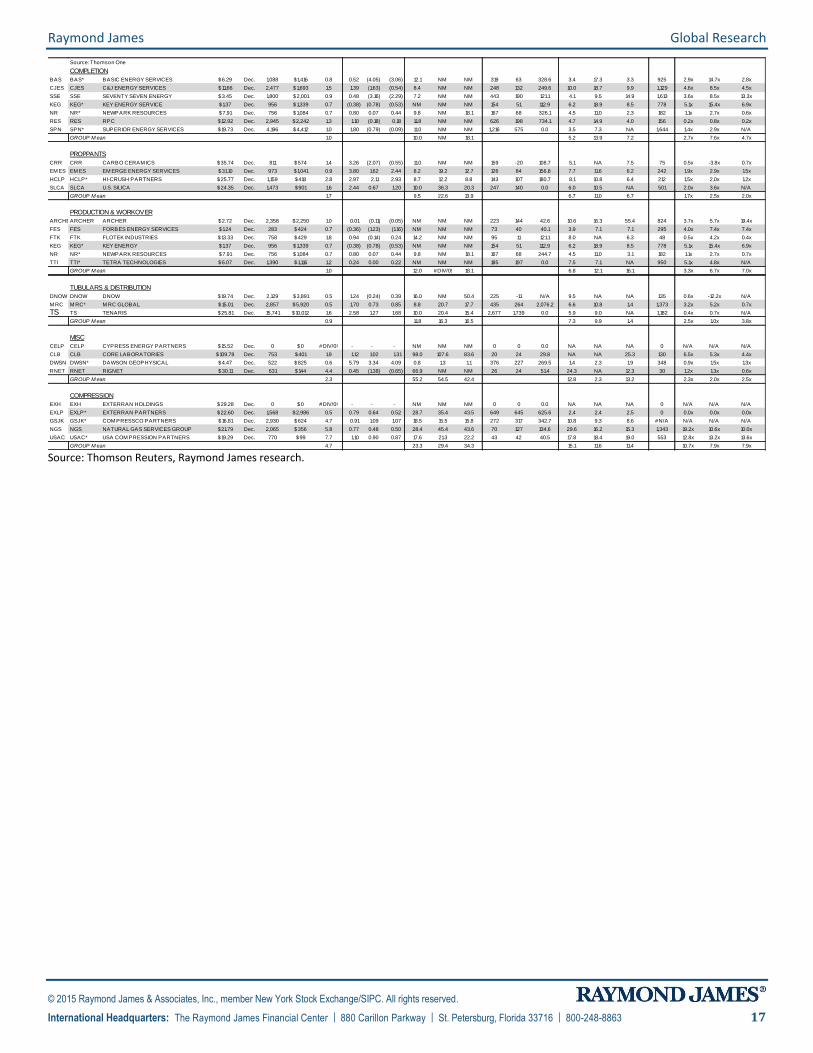

Source: Thomson One

COMPLETION

BAS BAS* BASIC ENERGY SERVICES $6.29 Dec. 1,088 $1,416 0.8 0.52 (4.05) (3.06) 12.1 NM NM 319 63 328.6 3.4 17.3 3.3 925 2.9x 14.7x 2.8x

CJES CJES C&J ENERGY SERVICES $11.66 Dec. 2,477 $1,693 1.5 1.39 (1.63) (0.54) 8.4 NM NM 248 132 249.6 10.0 18.7 9.9 1,129 4.6x 8.5x 4.5x

SSE SSE SEVENTY SEVEN ENERGY $3.45 Dec. 1,800 $2,001 0.9 0.48 (3.16) (2.29) 7.2 NM NM 443 190 121.1 4.1 9.5 14.9 1,613 3.6x 8.5x 13.3x

KEG KEG* KEY ENERGY SERVICE $1.37 Dec. 956 $1,339 0.7 (0.38) (0.78) (0.53) NM NM NM 154 51 112.9 6.2 18.9 8.5 778 5.1x 15.4x 6.9x

NR NR* NEWPARK RESOURCES $7.91 Dec. 756 $1,084 0.7 0.80 0.07 0.44 9.8 NM 18.1 167 68 326.1 4.5 11.0 2.3 182 1.1x 2.7x 0.6x

RES RES RPC $12.92 Dec. 2,945 $2,242 1.3 1.10 (0.18) 0.18 11.8 NM NM 626 198 734.1 4.7 14.9 4.0 156 0.2x 0.8x 0.2x

SPN SPN* SUPERIOR ENERGY SERVICES $19.73 Dec. 4,196 $4,412 1.0 1.80 (0.79) (0.09) 11.0 NM NM 1,216 575 0.0 3.5 7.3 NA 1,644 1.4x 2.9x N/A

GROUP M ean 1.0 10.0 NM 18.1 5.2 13.9 7.2 2.7x 7.6x 4.7x

PROPPANTS

CRR CRR CARBO CERAM ICS $35.74 Dec. 811 $574 1.4 3.26 (2.07) (0.55) 11.0 NM NM 159 -20 108.7 5.1 NA 7.5 75 0.5x -3.8x 0.7x

EM ES EM ES EM ERGE ENERGY SERVICES $31.10 Dec. 973 $1,041 0.9 3.80 1.62 2.44 8.2 19.2 12.7 126 84 156.8 7.7 11.6 6.2 242 1.9x 2.9x 1.5x

HCLP HCLP* HI-CRUSH PARTNERS $25.77 Dec. 1,159 $418 2.8 2.97 2.11 2.93 8.7 12.2 8.8 143 107 180.7 8.1 10.8 6.4 212 1.5x 2.0x 1.2x

SLCA SLCA U.S. SILICA $24.35 Dec. 1,473 $901 1.6 2.44 0.67 1.20 10.0 36.3 20.3 247 140 0.0 6.0 10.5 NA 501 2.0x 3.6x N/A

GROUP M ean 1.7 9.5 22.6 13.9 6.7 11.0 6.7 1.7x 2.5x 2.0x

PRODUCTION & WORKOVER

ARCHERARCHER ARCHER $2.72 Dec. 2,358 $2,250 1.0 0.01 (0.11) (0.05) NM NM NM 223 144 42.6 10.6 16.3 55.4 824 3.7x 5.7x 19.4x

FES FES FORBES ENERGY SERVICES $1.24 Dec. 283 $424 0.7 (0.36) (1.23) (1.16) NM NM NM 73 40 40.1 3.9 7.1 7.1 295 4.0x 7.4x 7.4x

FTK FTK FLOTEK INDUSTRIES $13.33 Dec. 758 $429 1.8 0.94 (0.14) 0.24 14.2 NM NM 95 11 121.1 8.0 NA 6.3 48 0.5x 4.2x 0.4x

KEG KEG* KEY ENERGY $1.37 Dec. 956 $1,339 0.7 (0.38) (0.78) (0.53) NM NM NM 154 51 112.9 6.2 18.9 8.5 778 5.1x 15.4x 6.9x

NR NR* NEWPARK RESOURCES $7.91 Dec. 756 $1,084 0.7 0.80 0.07 0.44 9.8 NM 18.1 167 68 244.7 4.5 11.0 3.1 182 1.1x 2.7x 0.7x

TTI TTI* TETRA TECHNOLOGIES $6.07 Dec. 1,390 $1,116 1.2 0.24 0.00 0.22 NM NM NM 185 197 0.0 7.5 7.1 NA 950 5.1x 4.8x N/A

GROUP M ean 1.0 12.0 #DIV/0! 18.1 6.8 12.1 16.1 3.3x 6.7x 7.0x TUBULARS & DISTRIBUTION

DNOW DNOW DNOW $19.74 Dec. 2,129 $3,891 0.5 1.24 (0.24) 0.39 16.0 NM 50.4 225 -11 N/A 9.5 NA NA 135 0.6x -12.2x N/A

M RC M RC* M RC GLOBAL $15.01 Dec. 2,857 $5,920 0.5 1.70 0.73 0.85 8.8 20.7 17.7 435 264 2,076.2 6.6 10.8 1.4 1,373 3.2x 5.2x 0.7x

TS TS TENARIS $25.81 Dec. 15,741 $10,012 1.6 2.58 1.27 1.68 10.0 20.4 15.4 2,677 1,739 0.0 5.9 9.0 NA 1,182 0.4x 0.7x N/A

GROUP M ean 0.9 11.8 16.3 16.5 7.3 9.9 1.4 2.5x 1.0x 3.8x

MISC

CELP CELP CYPRESS ENERGY PARTNERS $15.52 Dec. 0 $0 #DIV/0! - - - NM NM NM 0 0 0.0 NA NA NA 0 N/A N/A N/A

CLB CLB CORE LABORATORIES $109.78 Dec. 753 $401 1.9 1.12 1.02 1.31 98.0 107.6 83.6 20 24 29.8 NA NA 25.3 130 6.5x 5.3x 4.4x

DWSN DWSN* DAWSON GEOPHYSICAL $4.47 Dec. 522 $825 0.6 5.79 3.34 4.09 0.8 1.3 1.1 376 227 269.5 1.4 2.3 1.9 348 0.9x 1.5x 1.3x

RNET RNET RIGNET $30.11 Dec. 631 $144 4.4 0.45 (1.38) (0.65) 66.9 NM NM 26 24 51.4 24.3 NA 12.3 30 1.2x 1.3x 0.6x

GROUP M ean 2.3 55.2 54.5 42.4 12.8 2.3 13.2 2.3x 2.0x 2.5x

COMPRESSION

EXH EXH EXTERRAN HOLDINGS $29.28 Dec. 0 $0 #DIV/0! - - - NM NM NM 0 0 0.0 NA NA NA 0 N/A N/A N/A

EXLP EXLP* EXTERRAN PARTNERS $22.60 Dec. 1,568 $2,986 0.5 0.79 0.64 0.52 28.7 35.4 43.5 649 645 625.6 2.4 2.4 2.5 0 0.0x 0.0x 0.0x

GSJK GSJK* COM PRESSCO PARTNERS $16.81 Dec. 2,930 $624 4.7 0.91 1.09 1.07 18.5 15.5 15.8 272 317 342.7 10.8 9.3 8.6 #N/A N/A N/A N/A

NGS NGS NATURAL GAS SERVICES GROUP $21.79 Dec. 2,065 $356 5.8 0.77 0.48 0.50 28.4 45.4 43.6 70 127 134.6 29.6 16.2 15.3 1,343 19.2x 10.6x 10.0x

USAC USAC* USA COM PRESSION PARTNERS $19.29 Dec. 770 $99 7.7 1.10 0.90 0.87 17.6 21.3 22.2 43 42 40.5 17.8 18.4 19.0 553 12.8x 13.2x 13.6x

GROUP M ean 4.7 23.3 29.4 34.3 15.1 11.6 11.4 10.7x 7.9x 7.9x Source: Thomson Reuters, Raymond James research.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 18

Integrated Oil and Gas / Independent Refiners

Stock Performance in 2Q15 and TTM

RJ Integrated Oil & Gas and Refiners Universe

Quarterly Stock Price Performance TTM Stock Price Performance

-20% 0% 20% 40% 60%

MP3 - PBF

MP3 - EC

MP3 - WNR

MO2 - CVX

MP3 - TSO

MP3 - DK

MP3 - XOM

MO2 - VLO

S&P 500

MP3 - BP

MO2 - MPC

MO2 - PSX

MP3 - HFC

MP3 - PBR

RJ Integrateds and Refiners Universe -Quarterly Stock Price Performance

Source: Thomson Reuters

-80% -60% -40% -20% 0% 20% 40% 60%

MP3 - EC

MP3 - PBR

MO2 - CVX

MP3 - BP

MP3 - XOM

MP3 - HFC

MO2 - PSX

S&P 500

MP3 - PBF

MP3 - WNR

MO2 - VLO

MP3 - DK

MO2 - MPC

MP3 - TSO

RJ Integrateds and Refiners Universe -TTM Stock Price Performance

Source: Thomson Reuters

This analysis does not include transaction costs and tax considerations. If included these costs would reduce an investor’s return. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. A complete record of our stock recommendations for the trailing 12 months is available upon request.

Outlook on the Refining Industry

The U.S. refining industry has been one of the primary beneficiaries of growing domestic crude supply. As such, we are structurally constructive on the space, given the competitive advantage afforded by the discounted U.S. crude landscape, which should serve to moderate some of the industry’s cyclicality – some, not all. In the coming months, we fully expect that the WTI-Brent spread will continue to experience volatility as oil inventories continue to balloon and the dramatic fall in oil prices affects regional production characteristics. We envision WTI trading at a continued discount to seaborne international crudes, albeit to a more modest degree.

Meanwhile, global cracks priced off seaborne crudes remain relatively strong, particularly on the gasoline front. Indeed, the gasoline market has defied the typical seasonality and cracks continue to surprise to the upside, particularly against fears that the worldwide crude oil glut would soon turn into a refined product glut. A stronger-than-expected demand response (at least relative to consensus), especially in the U.S., has kept gasoline inventories from ballooning despite high refinery runs; however, lower crude oil differentials and weaker diesel cracks have reined in some – not all – of the strength in gasoline. Furthermore, the global refining arena still faces fundamental headwinds on an intermediate-term basis: structural overcapacity in weaker markets (i.e., Europe) and a wave of new refinery projects (mainly in Asia-Pacific and the Mid-East). A greater degree of refinery shutdowns, above and beyond the recent examples of rationalization and project delays (especially in Latin America), is a must to stave off the creep towards overcapacity.

As shown in the following chart, the U.S. benchmark crack spread has tracked above historical averages for much of the past two-plus years, largely driven by the disconnect in crude pricing between WTI and Brent; however, crack spreads have recently been nicely above year-ago levels for much of 2015 (after rebounding from the January lows). We continue to expect the Brent-WTI spread to be volatile in 3Q15, particularly as the global crude oil market remains in oversupply and inventories continue to need to find a market – in other words, expect the roller coaster ride to continue.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 19

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Ja

n-1

5

Feb

-15

Ma

r-15

Apr-

15

Ma

y-1

5

Ju

n-1

5

Jul-

15

Aug-1

5

Sep-1

5

Oct-

15

Nov-1

5

Dec-1

5

$ / B

bl

U.S. - NYMEX WTI 3-2-1 Crack Spread

5-Yr. Range 2013 2014 2015Source: Bloomberg

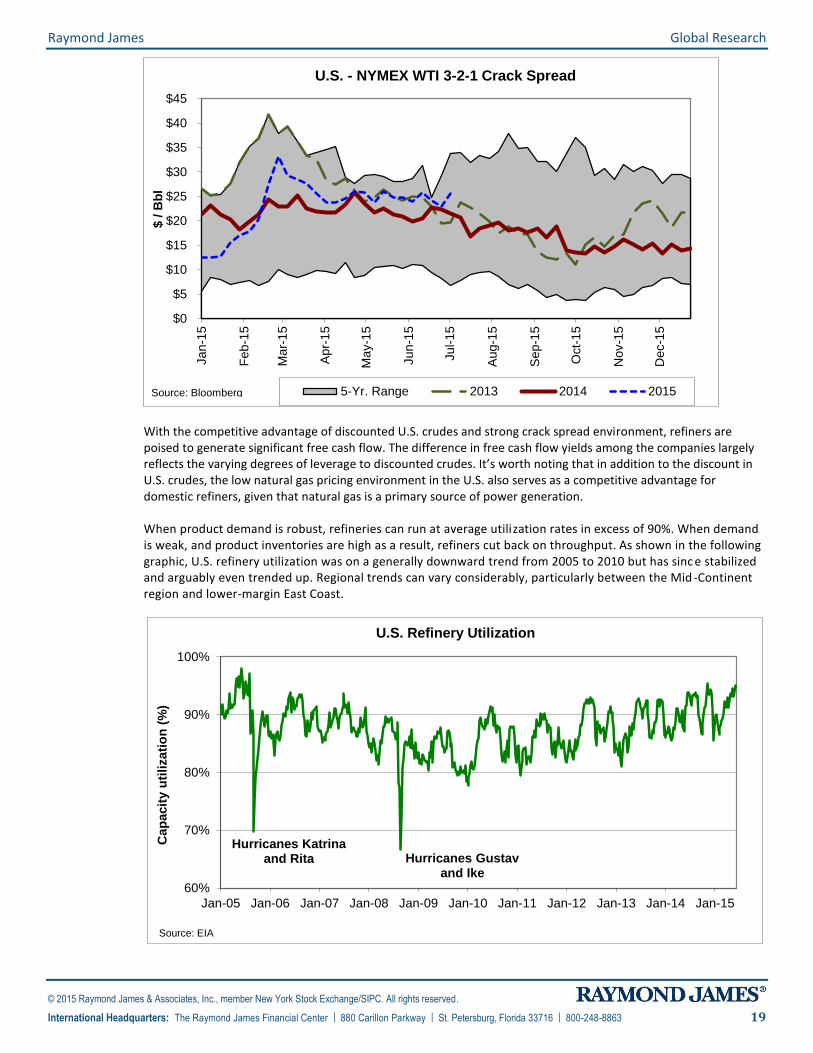

With the competitive advantage of discounted U.S. crudes and strong crack spread environment, refiners are poised to generate significant free cash flow. The difference in free cash flow yields among the companies largely reflects the varying degrees of leverage to discounted crudes. It’s worth noting that in addition to the discount in U.S. crudes, the low natural gas pricing environment in the U.S. also serves as a competitive advantage for domestic refiners, given that natural gas is a primary source of power generation. When product demand is robust, refineries can run at average utilization rates in excess of 90%. When demand is weak, and product inventories are high as a result, refiners cut back on throughput. As shown in the following graphic, U.S. refinery utilization was on a generally downward trend from 2005 to 2010 but has sinc e stabilized and arguably even trended up. Regional trends can vary considerably, particularly between the Mid -Continent region and lower-margin East Coast.

60%

70%

80%

90%

100%

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Ca

pa

cit

y u

tili

za

tio

n (

%)

U.S. Refinery Utilization

Source: EIA

Hurricanes Katrina and Rita Hurricanes Gustav

and Ike

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 20

Our benchmark crack spread assumptions are shown in the following table. We would caution that these crack spreads (left table) are based off Brent and do not represent the actual margin capture expected for any given refinery.

Q1 '02-'12 Q2 '02-'12 Q3 '02-'12 Q4 '02-'12 FY '02-'12

$7.50 $13.50 $11.00 $7.00 $9.75

Q1 13A Q2 13A Q3 13A Q4 13A 2013A

$14.33 $16.01 $14.72 $8.15 $13.30

Q1 14A Q2 14A Q3 14A Q4 14A 2014A

$12.80 $12.59 $14.27 $14.84 $13.63

Gasoline $7.45 $11.87 $13.16 $11.33 $10.95

Diesel $23.51 $14.04 $16.49 $21.86 $18.98

Q1 15A Q2 15A Q3 15E Q4 15E 2015E

Current RJ est. $14.92 $18.03 $14.50 $9.00 $14.11

Gasoline $10.68 $18.32 $13.75 $5.50 $12.06

Diesel $23.41 $17.44 $16.00 $16.00 $18.21

Q1 16E Q2 16E Q3 16E Q4 16E 2016E

Current RJ est. $10.00 $13.50 $12.00 $9.50 $11.25

Gasoline $6.50 $11.75 $9.75 $6.00 $8.50

Diesel $17.00 $17.00 $16.50 $16.50 $16.75

Source: Bloomberg, Thomson Reuters, Raymond James research

Note: Actuals are calculated by averaging w eekly closing prices

U.S. East Coast Seaborne-based 3-2-1 Crack Spread Estimates

U.S. - NYMEX WTI Europe - Spot Brent

3-2-1 Crack Spread 2-1-1 Crack Spread

($/Bbl) ($/Bbl)

2008 $10.20 $14.10

2009 $8.62 $8.48

2010 $9.96 $9.27

2011 $25.09 $9.48

2012 $29.54 $12.61

2013 $23.69 $10.82

2014 $19.21 $11.03

2015E $20.11 $15.14

Source: Bloomberg, Raymond James research

Note: Actuals are calculated by averaging w eekly closing margins

Actual and Forecasted Refining Margins

Outlook on Independent Refiners

The earnings uplift generated by the WTI discount has been a massive tailwind for the independent refining group, with the benefit extending beyond those refiners in the Mid-Continent. While we expect continued volatility in the WTI-Brent spread (currently ~$5-6/Bbl), we expect the spread to gradually widen throughout the year, with the growth in higher value cash flow streams (i.e., midstream and retail) and the associated sum of the parts valuation providing a solid backstop. Thus, we remain structurally bullish on most of the stocks. While a hazy outlook for continued global oil demand and rising refining capacity in emerging markets could present longer-term headwinds, we believe the competitive advantage afforded by the discount in onshore crudes outweighs these potential challenges.

While it is tough to wrap a precise band around the forward P/E multiples of independent refiners, given the sharp volatility of crack spreads (and hence earnings), we believe a range of about 6-10x reflects average historical valuations, as shown in the chart that follows. Currently, refiners are trading at median 2015 and 2016 EPS multiples of roughly 11.7x and 12.4x (based on consensus estimates).

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 21

0

4

8

12

16

20

24

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

P/E

mu

ltip

le

Independent Refiners: Consensus Forward-Year P/E Multiples

Valuation Range MedianSource: FactSet, Thomson Reuters Priced as of 7/10/2015

The following valuation table provides more detail on individual company multiples as well as our ratings.

Raymond James - Independent Refiners Research Universe

Market Valuation Database

Consensus Valuation Ratios

Price 3-Month Equity Ent.

Company Ticker Rating 07/10/15 Volume Value Value Capacity EDC 2015 2016 2015 2016 2015 2016 2015 2016

Alon USA Energy ALJ NC $18.77 902,930 1,320 1,713 6,851 1,124 5.1x 5.1x 21.5x 25.0x

CVR Energy CVI NC $39.65 287,842 3,443 3,078 26,763 3,253 4.6x 5.0x 14.7x 20.9x

Delek US Holdings DK MP3 $37.84 981,481 2,213 2,356 5,319 936 5.6x 4.4x 12.8x 10.8x 5.5x 4.7x 13.7x 12.3x

HollyFrontier Corp. HFC MP3 $45.26 2,527,709 8,831 8,365 18,883 3,324 4.9x 5.2x 10.7x 11.3x 5.0x 5.6x 11.1x 12.4x

Marathon Petroleum MPC MO2 $54.49 4,518,255 29,969 33,229 20,213 1,699 4.8x 5.5x 8.8x 10.9x 5.0x 5.8x 9.4x 10.9x

PBF Energy PBF MP3 $31.10 1,543,473 2,851 3,191 5,910 523 3.7x 2.9x 9.0x 6.9x 3.7x 3.6x 8.7x 7.8x

Phillips 66 PSX MO2 $81.49 3,078,495 45,010 47,644 21,656 1,900 6.3x 5.7x 11.5x 10.2x 7.0x 6.7x 12.6x 11.5x

Tesoro Corp. TSO MP3 $98.40 2,213,559 12,487 15,674 23,588 2,470 5.6x 5.4x 13.1x 12.7x 5.9x 6.1x 12.3x 13.2x

Valero Energy VLO MO2 $65.85 5,870,018 33,979 33,049 12,815 1,068 4.3x 4.5x 9.1x 9.8x 4.3x 4.8x 9.2x 10.5x

Western Refining WNR MP3 $46.54 1,369,759 4,453 5,060 33,510 6,571 4.3x 4.5x 10.2x 10.9x 4.9x 5.6x 10.6x 12.6x

Median $6,642 $6,713 19,548 1,799 4.8x 4.8x 10.4x 10.8x 5.0x 5.3x 11.7x 12.4x

Mean $14,456 $15,336 17,551 2,287 4.9x 4.8x 10.6x 10.4x 5.1x 5.3x 12.4x 13.7x

SB1 = Strong Buy; M O2 = Outperform; M P3 = M arket Perform; M U4 = Underperform; NC = Not Covered EDC = Equivalent Distillation Capacity

Source: Thomson Reuters, Oil & Gas Journal, Raymond James research Long-term debt on a GAAP basis includes non-recourse debt associated with respective M LPs

Price /

Bbl of Daily EBITDA EPS EBITDA EPS

Market Valuation Raymond James Valuation Ratios

($ MM) Enterprise Value / Price / Ent. Value /

Outlook on Integrated Oil and Gas

Integrated oil and gas companies are certainly not immune from oil price weakness, and many tend to trade in tandem with larger-cap E&Ps, though their downstream operations tend to provide a natural hedge. Furthermore, these companies – Petrobras being a notable exception – typically generate significant free cash flow (at least in less-challenged oil price environments) that supports above-average dividend yields and share buyback. These factors support relative outperformance vs. more aggressive energy stocks amid volatile markets, especially on a total return basis. On the flip side, these companies face structural challenges, including 1) constrained access to resources, especially amid resource nationalism and greater competition from state-controlled oil and gas companies, and 2) pressures on downstream divisions from a secular decline in oil demand in developed economies. Our ratings reflect mainly thematic differences between individual companies, including business segment weightings (upstream vs. downstream), commodity mix (oil/ overseas gas vs. North American gas), cash flow allocation (capital spending vs. dividends/share buyback), and balance sheet quality. We also take high-impact exploration and other potential catalysts into account.

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 22

While recognizing a significant amount of variance among the integrated companies, we can peg a historical average P/E multiple range of 8-12x. Currently, the group is trading at median EPS multiples of roughly 15.7x for 2015 and 13.4x for 2016 (based on consensus estimates).

0

4

8

12

16

20

24

28

32

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

P/E

mu

ltip

le

Integrated Oil and Gas: Consensus Forward-Year P/E Multiples

Valuation Range Median

Source: FactSet, Thomson Reuters Priced as of 7/10/2015

The following valuation table provides more detail on individual company multiples as well as our ratings.

Raymond James - Integrated Oil and Gas Research Universe

Market Valuation Database

Equity

Price 3-Month Value Price /

Company Ticker Rating 07/10/15 Volume ($ MM) 2015 2016 2015 2016 Proved NAV 2015 2016 2015 2016

BP plc ** BP MP3 $39.90 5,184,038 121,553 5.3x 4.5x 15.9x 13.6x

Cenovus Energy * CVE MO2 $14.36 2,057,391 11,896 8.7x 7.3x NM 268.8x

Chevron Corp. CVX MO2 $94.41 6,869,005 177,160 6.4x 5.4x 24.4x 17.4x 168.8% 6.3x 5.0x 23.3x 15.1x

China Petroleum & Chemical SNP NC $80.07 166,262 70,293 4.5x 3.8x 14.1x 10.8x

CNOOC Ltd. CEO NC $131.29 172,105 58,618 4.1x 3.7x 12.3x 8.3x

Ecopetrol S.A. EC MP3 $12.17 781,592 25,019 6.4x 5.0x 36.2x 13.8x 224.5% 6.0x 4.4x 12.3x 7.4x

Eni SpA * E MO2 $35.23 535,899 64,016 3.6x 3.0x 21.3x 14.2x

Exxon Mobil Corp. XOM MP3 $82.22 10,628,877 346,228 8.2x 6.8x 21.7x 17.6x 240.9% 7.7x 6.6x 18.7x 15.4x

Imperial Oil * IMO MP3 $36.71 285,617 31,115 12.5x 12.8x 23.2x 16.4x

Petrobras Argentina * PZE MP3 $6.64 108,796 1,341 - - - -

PetroChina Co. PTR NC $104.54 164,529 191,330 5.7x 5.0x 18.5x 13.4x

Petróleo Brasileiro PBR MP3 $8.38 35,260,190 54,656 6.0x 5.9x 14.0x 14.4x 90.8% 6.1x 5.5x 9.8x 7.5x

Royal Dutch Shell plc * RDS'A MO2 $56.84 2,533,390 174,184 - - - -

Statoil ASA STO NC $17.23 2,227,078 54,940 3.0x 2.7x 15.4x 11.8x

Suncor Energy * SU MO2 $26.80 3,706,093 38,752 7.4x 6.3x 43.1x 19.8x

Total S.A. * TOT MO2 $49.74 1,174,916 119,164 5.0x 4.5x 13.4x 13.0x

YPF S.A. * YPF MO2 $25.71 1,056,405 10,111 3.3x 2.8x 11.1x 8.1x

Median $58,618 6.4x 5.6x 23.1x 15.9x 196.7% 5.7x 4.5x 15.7x 13.4x

Mean $91,199 6.8x 5.7x 24.1x 15.8x 181.3% 5.9x 5.2x 18.0x 29.6x

SB1 = Strong Buy; M O2 = Outperform; M P3 = M arket Perform; M U4 = Underperform; NC = Not Covered ** BP is co-covered with RJ Euro Equities.

Source: Thomson Reuters, Raymond James research * CVE, IM O and SU are covered by RJ Ltd. PZE and YPF are covered by RJ Latin America.

*E, RDS.A and TOT are covered by RJ Euro Equities.

Raymond James Valuation Ratios Consensus Valuation Ratios

EV / EBITDA Price / EPS EV / EBITDA Price / EPS

Raymond James Global Research

© 2015 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800-248-8863 23

Renewable Energy and Clean Technology

Stock Performance in 2Q15 and TTM

-40% -20% 0% 20% 40%

MP3 - ENPH

MP3 - FSLR

MP3 - AMRS

SB1 - ENOC

MO2 - CAFD

MO2 - EVA

MO2 - SPWR

MP3 - TSL

ECO Index

MO2 - GTLS

MO2 - SCTY

MU4 - CLNE

SB1 - AEIS

MO2 - SZYM

MP3 - WPRT

MO2 - SSNI

RJ Clean Tech Universe -Quarterly Stock Price Performance

Source: Thomson Reuters

-100% -50% 0% 50%

MP3 - WPRT

MO2 - SZYM

MO2 - GTLS

MU4 - CLNE

SB1 - ENOC

MP3 - AMRS

MP3 - FSLR

MO2 - SPWR

MO2 - SCTY

ECO Index

MO2 - CAFD

MP3 - ENPH

MO2 - EVA

MP3 - TSL

MO2 - SSNI

SB1 - AEIS

RJ Clean Tech Universe -TTM Stock Price Performance

Source: Thomson Reuters

This analysis does not include transaction costs and tax considerations. If included these costs would reduce an investor’s return. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. A complete record of our stock recommendations for the trailing 12 months is available upon request.

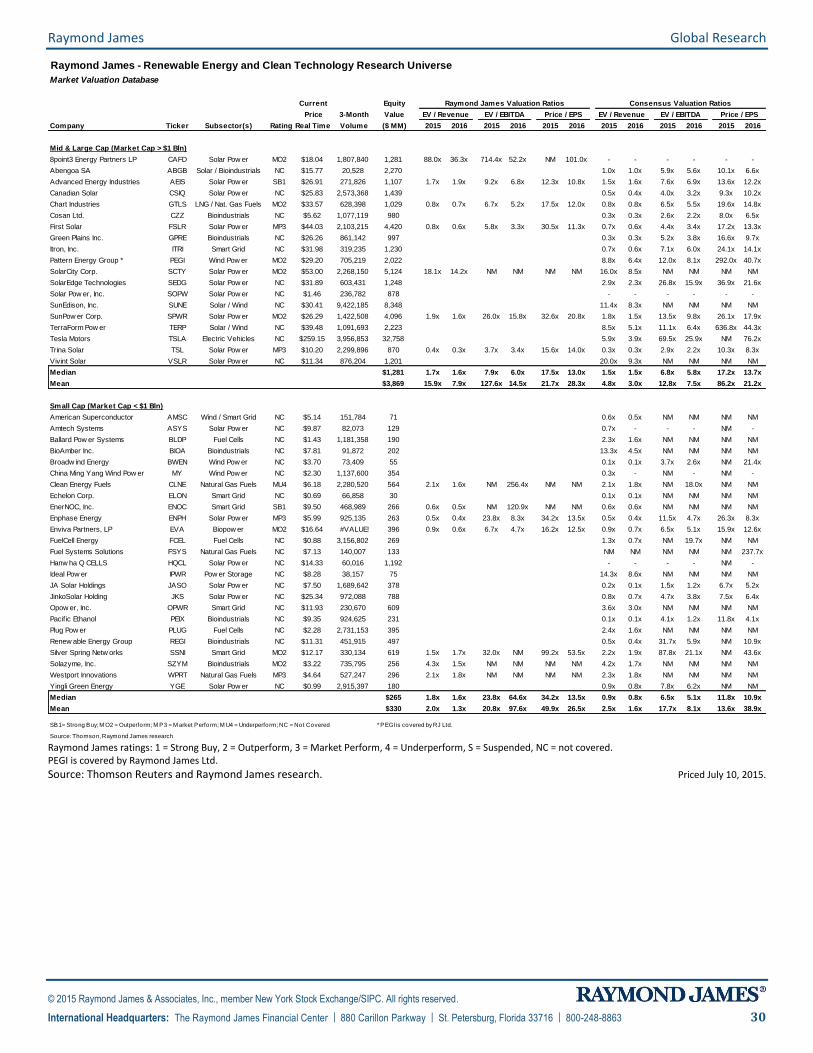

Outlook on Solar Power

The global photovoltaic (PV) industry is exhibiting secular growth in electricity market penetration, albeit with volatile margins across the value chain. While Europe has historically comprised the bulk of global PV demand, the European market has markedly slowed down, and growth is increasingly coming from China, Japan, the U.S., and other geographies. Capacity rationalization in China and elsewhere has reduced overcapacity, though import tariffs (e.g., the U.S.-China solar trade war) and other trade barriers can further complicate supply/demand dynamics.

Policy support for PV demand is evolving. The European Union and over 25 U.S. states have renewable portfolio standards, and some jurisdictions have “carve-out” mandates for PV. Tax credits or rebates, such as the federal Investment Tax Credit (ITC), provide more direct financial support. The most effective policy structure is the feed-in tariff, which is most common in Europe but has materialized elsewhere, including China and Japan. Widespread feed-in tariff reductions in Europe have forced developers and manufacturers to adapt to the lower economics.

0

20,000

40,000

60,000

2008 2009 2010 2011 2012 2013 2014 2015E 2016E

Me

ga

wa

tts

Global PV Demand