RATINGS FINANCIAL INSTITUTIONS - Swedbankgs/@ir/documents/article/cid_2400691.pdf · FINANCIAL...

10

FINANCIAL INSTITUTIONS CREDIT OPINION 7 September 2017 Update RATINGS Swedbank AB Domicile Sweden Long Term Debt Aa3 Type Senior Unsecured - Fgn Curr Outlook Stable Long Term Deposit Aa3 Type LT Bank Deposits - Fgn Curr Outlook Stable Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Louise Lundberg 46-8-5025-6568 VP-Sr Credit Officer [email protected] Niclas Boheman 44-20-7772-1643 AVP-Analyst [email protected] Aleksandar Hristov 44-20-7772-1071 Associate Analyst [email protected] Jean-Francois Tremblay 44-20-7772-5653 Associate Managing Director [email protected] Sean Marion 44-20-7772-1056 MD-Financial Institutions [email protected] Swedbank AB Update Following Macro Profile Change Summary We assign an a3 baseline credit assessment (BCA) and Aa3 long-term deposits and senior unsecured debt ratings to Swedbank AB (Swedbank). We also assign a long-term and short- term counterparty risk assessment (CRA) of Aa2(cr)/Prime-1(cr) to the bank. On 1 September 2017, we affirmed Swedbank's ratings as we expect the bank to be broadly resilient to the elevated risks in the residential housing market and household sector in Sweden (as reflected in our lowering of the Macro Profile for Swedish banks). Swedbank's a3 BCA reflects the bank’s strong credit quality, solid regulatory capital and stable earnings, underpinned by its established franchise in Sweden (Aaa stable) and the Baltic countries. However, similarly to many Nordic peers, the BCA is constrained by the bank’s high reliance on market funding, which renders it vulnerable to changes in investor sentiment and market conditions. Swedbank's Aa3 long-term deposit and senior debt ratings include a two-notch uplift resulting from our advanced Loss Given Failure (LGF) analysis, reflecting our view that the bank’s junior depositors and senior unsecured creditors face a very low loss given failure. In addition, our moderate assessment of government support translates into a further notch uplift included in the relevant ratings. Exhibit 1 Rating Scorecard - Key Financial Ratios 0.6% 29.6% 0.8% 36.3% 18.3% 0% 5% 10% 15% 20% 25% 30% 35% 40% 0% 5% 10% 15% 20% 25% 30% 35% Asset Risk: Problem Loans/ Gross Loans Capital: Tangible Common Equity/Risk-Weighted Assets Profitability: Net Income/ Tangible Assets Funding Structure: Market Funds/ Tangible Banking Assets Liquid Resources: Liquid Banking Assets/Tangible Banking Assets Solvency Factors (LHS) Liquidity Factors (RHS) Swedbank AB (BCA: a3) Median a3-rated banks Solvency Factors Liquidity Factors Source: Moody's Financial Metrics THIS REPORT WAS REPUBLISHED ON 11 SEPTEMBER 2017 WITH A CORRECTED PROFITABILITY SCORE IN THE BCA SCORECARD.

Transcript of RATINGS FINANCIAL INSTITUTIONS - Swedbankgs/@ir/documents/article/cid_2400691.pdf · FINANCIAL...

FINANCIAL INSTITUTIONS

CREDIT OPINION7 September 2017

Update

RATINGS

Swedbank ABDomicile Sweden

Long Term Debt Aa3

Type Senior Unsecured - FgnCurr

Outlook Stable

Long Term Deposit Aa3

Type LT Bank Deposits - FgnCurr

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Louise Lundberg 46-8-5025-6568VP-Sr Credit [email protected]

Niclas Boheman [email protected]

Aleksandar Hristov 44-20-7772-1071Associate [email protected]

Jean-FrancoisTremblay

44-20-7772-5653

Associate [email protected]

Sean Marion [email protected]

Swedbank ABUpdate Following Macro Profile Change

SummaryWe assign an a3 baseline credit assessment (BCA) and Aa3 long-term deposits and seniorunsecured debt ratings to Swedbank AB (Swedbank). We also assign a long-term and short-term counterparty risk assessment (CRA) of Aa2(cr)/Prime-1(cr) to the bank.

On 1 September 2017, we affirmed Swedbank's ratings as we expect the bank to be broadlyresilient to the elevated risks in the residential housing market and household sector in Sweden(as reflected in our lowering of the Macro Profile for Swedish banks). Swedbank's a3 BCA reflectsthe bank’s strong credit quality, solid regulatory capital and stable earnings, underpinned byits established franchise in Sweden (Aaa stable) and the Baltic countries. However, similarlyto many Nordic peers, the BCA is constrained by the bank’s high reliance on market funding,which renders it vulnerable to changes in investor sentiment and market conditions.

Swedbank's Aa3 long-term deposit and senior debt ratings include a two-notch uplift resultingfrom our advanced Loss Given Failure (LGF) analysis, reflecting our view that the bank’s juniordepositors and senior unsecured creditors face a very low loss given failure. In addition, ourmoderate assessment of government support translates into a further notch uplift included inthe relevant ratings.

Exhibit 1

Rating Scorecard - Key Financial Ratios

0.6% 29.6%

0.8%

36.3% 18.3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

5%

10%

15%

20%

25%

30%

35%

Asset Risk:Problem Loans/

Gross Loans

Capital:Tangible Common

Equity/Risk-WeightedAssets

Profitability:Net Income/

Tangible Assets

Funding Structure:Market Funds/

Tangible BankingAssets

Liquid Resources:Liquid BankingAssets/TangibleBanking Assets

Solvency Factors (LHS) Liquidity Factors (RHS)

Swedbank AB (BCA: a3) Median a3-rated banks

So

lve

ncy F

acto

rs

Liq

uid

ity F

acto

rs

Source: Moody's Financial Metrics

THIS REPORT WAS REPUBLISHED ON 11 SEPTEMBER 2017 WITH A CORRECTED PROFITABILITY SCORE IN THE BCASCORECARD.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Credit Strengths

» Leading retail & SME and good corporate banking market positions in Sweden and the Baltic countries

» Strong credit quality and solid regulatory capitalisation

» Cost discipline, strong market position in mortgage lending and asset management support profitability

» Our advanced LGF analysis indicates a very low loss given failure for junior depositors and senior unsecured creditors, resulting in atwo-notch uplift in the relevant ratings, from the firm’s a3 adjusted BCA

» The long-term deposit and senior unsecured debt ratings incorporate one notch of government support uplift

Credit Challenges

» Elevated risks in the residential housing market and household sector in Sweden, although broadly contained by underwritingstandards, high wealth levels and a very strong repayment culture

» High reliance on confidence-sensitive market funding, which is partly mitigated by proven access to debt markets, a resilientdomestic covered bond market, and strong liquidity

Rating OutlookThe ratings outlook on Swedbank is stable, as we expect the bank to continue to be able to offset negative profitability pressures in theprolonged low interest rate environment, over the next 12-18 months.

Factors that Could Lead to an UpgradeThe BCA could be upgraded if the bank significantly (1) reduces its reliance on market funding, (2) improves its profitability, and/or (3)increases its liquidity position. A higher BCA would likely lead to a ratings upgrade.

Factors that Could Lead to a DowngradeThe ratings could be downgraded if the bank’s (1) operating environment deteriorates beyond our current expectations, and/or (2) assetrisk increases more than we anticipate, for example due a stark weakening in credit quality or an increase in risk appetite, leading toriskier lending.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Key Indicators

Exhibit 2

Swedbank AB (Consolidated Financials) [1]6-172 12-162 12-152 12-142 12-133 CAGR/Avg.4

Total Assets (SEK million) 2,397,985 2,117,895 2,109,242 2,057,903 1,781,797 8.95

Total Assets (EUR million) 249,270 221,028 230,314 217,248 201,334 6.35

Total Assets (USD million) 284,305 233,130 250,189 262,882 277,426 0.75

Tangible Common Equity (SEK million) 120,243 126,378 115,721 102,989 96,021 6.65

Tangible Common Equity (EUR million) 12,499 13,189 12,636 10,872 10,850 4.15

Tangible Common Equity (USD million) 14,256 13,911 13,726 13,156 14,950 -1.35

Problem Loans / Gross Loans (%) 0.6 0.6 0.5 0.5 0.7 0.66

Tangible Common Equity / Risk Weighted Assets (%) 29.6 32.1 29.7 24.9 21.2 29.17

Problem Loans / (Tangible Common Equity + Loan Loss Reserve) (%) 7.1 6.6 5.6 6.7 8.5 6.96

Net Interest Margin (%) 1.1 1.1 1.1 1.2 1.2 1.16

PPI / Average RWA (%) 6.1 5.8 5.1 3.4 3.0 5.17

Net Income / Tangible Assets (%) 0.8 0.9 0.8 0.8 0.7 0.86

Cost / Income Ratio (%) 39.3 41.7 43.9 45.7 45.9 43.36

Market Funds / Tangible Banking Assets (%) 38.0 36.3 38.5 43.6 39.1 39.16

Liquid Banking Assets / Tangible Banking Assets (%) 27.6 18.3 22.9 21.4 20.0 22.06

Gross Loans / Due to Customers (%) 167.8 190.6 189.4 208.0 204.5 192.16

[1] All figures and ratios are adjusted using Moody's standard adjustments [2] Basel III - fully-loaded or transitional phase-in; IFRS [3] Basel II; IFRS [4] May include rounding differences dueto scale of reported amounts [5] Compound Annual Growth Rate (%) based on time period presented for the latest accounting regime [6] Simple average of periods presented for the latestaccounting regime. [7] Simple average of Basel III periods presentedSource: Moody's Financial Metrics

Detailed Credit ConsiderationsSwedbank's BCA is supported by its 'Strong+' Macro ProfileSwedbank has the bulk of its operations in Sweden, which accounted for 86% of its gross lending as of June 2017. As such, its 'strong+' Macro Profile is in line with that of Sweden.

Swedish banks benefit from a diverse and competitive economy, robust public institutions and a stable political environment thatsupports consensus-oriented policy making. However, we view Swedish household debt levels and the multi-year growth of householddebt, as key vulnerabilities to the financial system, as reflected in our Macro Profile.

Leading retail, SME and good corporate banking positions in Sweden and the Baltic countries provide stable and recurringearningsWe expect Swedbank's solid customer base and local brand recognition to continue to support its stable earnings generation capacity.Swedbank's good franchise is underpinned by large, sustainable market shares in its core markets of Sweden and the three Baltic countries,Estonia (A1 stable), Latvia (A3 stable) and Lithuania (A3 stable). As the largest retail bank in Sweden and the Baltic countries, it hassubstantial market shares in domestic mortgages, cards, retail deposits and fund management (through its franchise Robur, unrated).

The bank has a co-operation agreement with 58 Swedish savings banks, which extends the domestic distribution network of Swedbankwho in return provides central clearing service and IT solutions to the member savings banks. Currently, around 30% of Swedbank'stotal domestic product sales are conducted through the savings banks. During H1 2017, the largest contributor for the financial resultsof Swedbank was the Swedish business segment (covering Swedish retail and SMEs) which accounted for 67% of pre-tax income and55% of total assets. The combined Baltic operations of Swedbank, which is the key international exposure of the group, accounted for19% of pre-tax income but only 8% of total assets, while the Large Corporates & Institutions (LC&I) segment accounted for 11.5% ofpre-tax profit and 20% of total assets.

We believe that Swedbank's strong credit quality and stable earnings, which are underpinned by its strong franchise in Sweden and theBaltic countries, position the bank well to manage challenges in its operating environment. These include a prolonged period of lowinterest rates, combined with the intensifying competition from mobile and digital banking solutions and asset managers (which hashistorically been very profitable).

3 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Strong credit quality and solid regulatory capitalisationSwedbank has a strong credit quality and solid regulatory capitalisation relative to global peers, reflecting conservative underwritingstandards, effective risk management and good internal capital generation. As of June 2017, the bank's problem loan ratio (for its continuingoperations and including impaired loans plus 60+ day overdue loans that were not impaired) was 0.6%, broadly in line with end-2016.Our asset risk assessment, which leads to an assigned score of a1, also takes into account the bank's concentration to the propertymanagement sector and the relatively low problem loans coverage ratio (52% as of June 2017), which is somewhat mitigated by thecollateral available to the bank against these exposures.

Swedbank's strong credit quality in its domestic loan portfolio is underpinned by a relatively diversified loan book with around 63%of lending to private individuals as of June 2017, as well as strong macroeconomic fundamentals. The riskier portions of the bank'sloan portfolio relate to its Swedish corporate and Baltic loan books. Non-retail exposures are concentrated on the Swedish propertymanagement sector which we see as a cyclical sector, making it more prone to volatility and swings in asset quality in an economicdownturn. As of June 2017, loans to the property management sector accounted for about 42% of Swedbank's corporate book, and 14%of all loans to the public. Around 21% of these loans are to Swedish residential properties (housing cooperatives), which have had verylow default rates compared to commercial real estate subsectors. Baltic lending remains limited in a historical comparison, at around9.4% of total lending as of June 2017. Nonetheless, despite the economic recovery which has been observed in the Baltic region in recentyears, we continue to view this banking book as higher risk as the operating environment is less stable, mortgages have high LTVs andfinancial buffers are lower (lower levels of household wealth, for instance).

Swedbank’s regulatory capitalisation is strong, as evidenced by its Common Equity Tier 1 (CET1) ratio and Tier 1 capital ratio under BaselIII/CRDIV of 24.6% and 27.8% as of June 2017, respectively. We calculate a tangible common equity to risk weighted assets of 29.6% asof the same date. Swedbank's tangible common equity stood at 5.4% of tangible banking assets as of June 2017.

Swedbank already meets its increased capital requirement, resulting from the conclusion of the bank's annual supervisory and evaluationprocess (SREP), which includes a Pillar 2 capital surcharge for increased risk weights for corporate exposures and the introduction ofa maturity floor for these exposures, based on the Swedish FSA's preliminary calculations. Once validated, the higher risk weights forcorporate exposures will be transitioned to the bank's Pillar 1 capital requirement from Pillar 2.

We note that a substantial part of Swedbank's loan book is composed of residential mortgages (around 55% of total lending as of end-June 2017), carrying comparatively low risk weights. In line with other Swedish banks, Swedbank's capital ratios look comparatively higheras the SFSA prefer to put additional capital guidance within pillar II. Our assigned capital score of a1 considers the lower density of RWAscompared to rated European peers.

Cost discipline and profitable fund management operations support profitability, which continues to be under pressure inthe prolonged low interest environmentThe baa1 assigned score for profitability in our BCA scorecard reflects Swedbank's consistent good level of profitability, which compareswell with its Nordic peer group, and which the bank has achieved despite the prolonged low interest-rate environment.

Since early 2014, the Swedish central bank has been lowering the key policy rate, which is currently in negative territory. Swedbank andthe other domestic banks have so far been able to mitigate the low interest rate environment pressures by not fully transferring theinterest rate reduction to their clients. In addition, market funding rates have also declined which has been supportive to earnings.

Swedbank, being one of the two largest mortgage lenders in Sweden, is one of the most reliant on net interest income (see Exhibit 3),which makes its income more sensitive to changes in mortgage margins than peers.

4 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Exhibit 3

Net Interest Income Represents The Bulk Of Swedbank's IncomeSwedbank: Income breakdown

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 Q2 2017

Net interest income Net Fees and commissions Other non interest income

Source: Moody's Financial Metrics

Swedbank has implemented cost rationalisation initiatives to offset profitability pressures, which have proven effective so far. In addition,the bank has maintained a large and stable commission income stream (average of 29% of net revenues over the last three years), whichprovides a good degree of diversification to its earnings. Swedbank’s leading fund management franchise Robur had a large market shareof 21% in Sweden as of June 2017.

High reliance on confidence-sensitive market funding which is partially mitigated by proven access to capital markets, aresilient domestic covered bond market and strong liquiditySwedbank maintains broad access to capital markets and has a large liquidity buffer, mitigating its high reliance on market funding, whichin our view remains one of its key credit weaknesses. Although this is a common feature among the large Nordic banks, it exposes the banksto changes in market conditions, and renders them more sensitive to swings in investor confidence than some of their international peers.

As of June 2017, market funding accounted for 38% of tangible banking assets. Like the other large Swedish banks, Swedbank's wholesalefunding is diversified and includes covered bonds (50%), senior unsecured debt (18%), commercial paper/certificates of deposit (15%),interbank funding (14%) and subordinated debt (3%). As indicated in our banks methodology, we reflect the greater stability of coveredbonds compared to unsecured market funding through a standard adjustment to the funding structure ratio. Given the long history ofthe Swedish covered bond markets, local currency and deep domestic investor base, we make additional (positive) adjustments for localcurrency (LC) denominated covered bonds issued in this market.

Swedbank’s high reliance on wholesale funding is mitigated by its strong liquidity position. As of June 2017, liquid resources covered allmarket funding maturing over the following 18 months (see Exhibit 4 for long-term debt maturity and liquidity reserves). Swedbank’sliquidity pool (SEK559 billion, or 23% of total assets at the same date) consisted of balances with central banks (78%), sovereign andmunicipal securities (12%) and covered bonds (11%). As of June 2017, Swedbank had an overall Liquidity Coverage Ratio (LCR) of 121%overall under the CRR definition of LCR. Its Net Stable Funding Ratio (NSFR) was 110% as at the same reporting date, which is evidenceof its strong funding and liquidity positions.

5 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

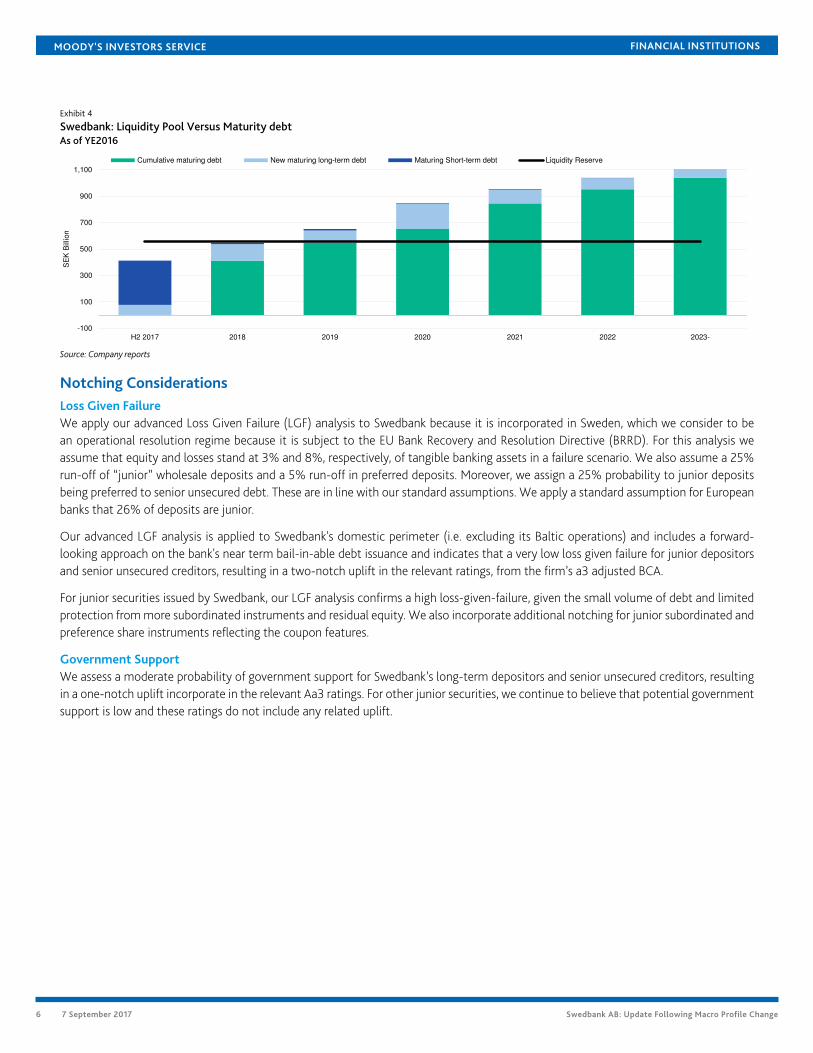

Exhibit 4

Swedbank: Liquidity Pool Versus Maturity debtAs of YE2016

-100

100

300

500

700

900

1,100

H2 2017 2018 2019 2020 2021 2022 2023-

SE

K B

illion

Cumulative maturing debt New maturing long-term debt Maturing Short-term debt Liquidity Reserve

Source: Company reports

Notching ConsiderationsLoss Given FailureWe apply our advanced Loss Given Failure (LGF) analysis to Swedbank because it is incorporated in Sweden, which we consider to bean operational resolution regime because it is subject to the EU Bank Recovery and Resolution Directive (BRRD). For this analysis weassume that equity and losses stand at 3% and 8%, respectively, of tangible banking assets in a failure scenario. We also assume a 25%run-off of “junior” wholesale deposits and a 5% run-off in preferred deposits. Moreover, we assign a 25% probability to junior depositsbeing preferred to senior unsecured debt. These are in line with our standard assumptions. We apply a standard assumption for Europeanbanks that 26% of deposits are junior.

Our advanced LGF analysis is applied to Swedbank's domestic perimeter (i.e. excluding its Baltic operations) and includes a forward-looking approach on the bank's near term bail-in-able debt issuance and indicates that a very low loss given failure for junior depositorsand senior unsecured creditors, resulting in a two-notch uplift in the relevant ratings, from the firm’s a3 adjusted BCA.

For junior securities issued by Swedbank, our LGF analysis confirms a high loss-given-failure, given the small volume of debt and limitedprotection from more subordinated instruments and residual equity. We also incorporate additional notching for junior subordinated andpreference share instruments reflecting the coupon features.

Government SupportWe assess a moderate probability of government support for Swedbank’s long-term depositors and senior unsecured creditors, resultingin a one-notch uplift incorporate in the relevant Aa3 ratings. For other junior securities, we continue to believe that potential governmentsupport is low and these ratings do not include any related uplift.

6 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Rating Methodology and Scorecard Factors

Exhibit 5

Swedbank ABMacro FactorsWeighted Macro Profile Strong + 100%

Factor HistoricRatio

MacroAdjusted

Score

CreditTrend

Assigned Score Key driver #1 Key driver #2

SolvencyAsset RiskProblem Loans / Gross Loans 0.6% aa2 ← → a1 Sector concentration

CapitalTCE / RWA 29.6% aa1 ← → a1 Risk-weighted

capitalisationProfitabilityNet Income / Tangible Assets 0.8% baa1 ← → baa1 Return on assets

Combined Solvency Score aa3 a2LiquidityFunding StructureMarket Funds / Tangible Banking Assets 36.3% ba2 ← → baa2 Market

funding qualityLiquid ResourcesLiquid Banking Assets / Tangible Banking Assets 18.3% baa2 ← → baa2 Stock of liquid assets

Combined Liquidity Score ba1 baa2Financial Profile a3

Business Diversification 0Opacity and Complexity 0Corporate Behavior 0

Total Qualitative Adjustments 0Sovereign or Affiliate constraint: AaaScorecard Calculated BCA range a2-baa1Assigned BCA a3Affiliate Support notching 0Adjusted BCA a3

Balance Sheet in-scope(SEK million)

% in-scope at-failure(SEK million)

% at-failure

Other liabilities 989,047 49.6% 1,063,894 53.3%Deposits 733,802 36.8% 658,954 33.0%

Preferred deposits 543,014 27.2% 515,863 25.8%Junior Deposits 190,789 9.6% 143,091 7.2%

Senior unsecured bank debt 191,682 9.6% 191,682 9.6%Dated subordinated bank debt 21,475 1.1% 21,475 1.1%Equity 59,877 3.0% 59,877 3.0%Total Tangible Banking Assets 1,995,882 100% 1,995,882 100%

7 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

De Jure waterfall De Facto waterfall NotchingDebt classInstrumentvolume +

subordination

Sub-ordination

Instrumentvolume +

subordination

Sub-ordination

De Jure De FactoLGF

NotchingGuidance

vs.Adjusted

BCA

AssignedLGF

notching

Additionalnotching

PreliminaryRating

Assessment

Counterparty Risk Assessment 20.8% 20.8% 20.8% 20.8% 3 3 3 3 0 aa3 (cr)Deposits 20.8% 4.1% 20.8% 13.7% 2 3 2 2 0 a1Senior unsecured bank debt 20.8% 4.1% 13.7% 4.1% 2 1 2 2 0 a1Dated subordinated bank debt 4.1% 3.0% 4.1% 3.0% -1 -1 -1 -1 0 baa1Cumulative bank preference shares 3.0% 3.0% 3.0% 3.0% -1 -1 -1 -1 -2 baa3 (hyb)Non-cumulative bank preference shares 3.0% 3.0% 3.0% 3.0% -1 -1 -1 -1 -2 baa3 (hyb)

Instrument class Loss GivenFailure notching

AdditionalNotching

Preliminary RatingAssessment

GovernmentSupport notching

Local CurrencyRating

ForeignCurrency

RatingCounterparty Risk Assessment 3 0 aa3 (cr) 1 Aa2 (cr) --Deposits 2 0 a1 1 Aa3 Aa3Senior unsecured bank debt 2 0 a1 1 Aa3 Aa3Dated subordinated bank debt -1 0 baa1 0 -- Baa1Cumulative bank preference shares -1 -2 baa3 (hyb) 0 Baa3 (hyb) --Non-cumulative bank preference shares -1 -2 baa3 (hyb) 0 -- Baa3 (hyb)Source: Moody's Financial Metrics

Ratings

Exhibit 6Category Moody's RatingSWEDBANK AB

Outlook StableBank Deposits Aa3/P-1Baseline Credit Assessment a3Adjusted Baseline Credit Assessment a3Counterparty Risk Assessment Aa2(cr)/P-1(cr)Issuer Rating Aa3Senior Unsecured Aa3Subordinate Baa1Pref. Stock -Dom Curr Baa3 (hyb)Pref. Stock Non-cumulative Baa3 (hyb)Commercial Paper P-1Other Short Term (P)P-1

SWEDBANK MORTGAGE AB

Outlook StableCounterparty Risk Assessment Aa2(cr)/P-1(cr)Issuer Rating Aa3Bkd Sr Unsec MTN (P)Aa3Bkd Commercial Paper P-1Bkd Other Short Term (P)P-1

Source: Moody's Investors Service

8 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1088495

9 7 September 2017 Swedbank AB: Update Following Macro Profile Change

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

10 7 September 2017 Swedbank AB: Update Following Macro Profile Change