Rare and Minor Metals Company Review Exploration, Development & Production RM… · Rare and Minor...

36

Rare and Minor Metals Company Review Exploration, Development & Production December Quarter 2010

-

Upload

trinhkhanh -

Category

Documents

-

view

220 -

download

2

Transcript of Rare and Minor Metals Company Review Exploration, Development & Production RM… · Rare and Minor...

Rare and Minor Metals Company ReviewExploration, Development & ProductionDecember Quarter 2010

Resource Capital Research

Resource Capital Research

Suite 1306 183 Kent Street Sydney, NSW 2000

Tel: +612 9252 9405 Fax: +612 9251 2859 Email: [email protected]: www.rcresearch.com.au

Resource Capital Research ACN 111 622 489

Rare and Minor Metals Company ReviewDecember Quarter 2010

Resource Analyst (Rare and Minor Metals): Dr Trent Allen

Resource Analyst: Dr Tony Parry

Resource Analyst: John Wilson

This report is subject to copyright and may not be redistributed without written permission from RCR. The information contained in this report is for use by US, Canadian and Australian residents only. Copies are available for purchase from RCR.

17 November 2010

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 2

Contents Contents .............................................................................................................................. 2 Overview and Investment Comment ........................................................................................ 3 RCR December Quarter 2010 Featured Company Summary ........................................................ 4 [Explorers‟ Development Cycle Chart, December Q 2010 ............................................................. ] [Comparative Charts ............................................................................................................... ] Financial Data ....................................................................................................................... 5 Company Statistics ................................................................................................................ 5 Reserves, Resources and Historic Mineralisation ........................................................................ 6 Valuation and Performance Data ............................................................................................. 6

Exploration, Development and Production Companies

[Alkane Exploration Limited ........................................................................................... ] Arafura Resources Limited ............................................................................................ 7 Avalon Rare Metals Inc ................................................................................................. 9 Crossland Uranium Mines Limited ................................................................................ 11 Globe Metals & Mining Limited .................................................................................... 13 Greenland Minerals & Energy Limited ........................................................................... 15 [Gippsland Limited ........................................................................................................ ] Gunson Resources Limited .......................................................................................... 17 Galaxy Resources Limited ........................................................................................... 19 [Icon Resources Limited ................................................................................................ ] [King Island Scheelite Limited ........................................................................................ ] [Rodinia Lithium Inc ...................................................................................................... ] [TNR Gold Corp ............................................................................................................ ]

Market Update: Lithium ........................................................................................................ 20 Market Update: Niobium ...................................................................................................... 23 Market Update: Tantalum ..................................................................................................... 25 Market Update: Tungsten ..................................................................................................... 27 Market update: Rare Earth Elements ...................................................................................... 29 Market Update: Zirconium and Zircon .................................................................................... 31

[Selected rare and minor metal price data and production statistics .............................................. ] [Exchange rates of some rare and minor metals producers and consumers. ................................... ] [Rare and minor metal mompany share performance tables ......................................................... ]

Report Contributors ............................................................................................................. 33 Disclosure and Disclaimer ..................................................................................................... 34

[This is the Abridged Report version of the December Quarter RCR Rare and Minor Metals Company Review. The

purchase price of RCR‟s December quarter Subscriber Reports (including uranium, gold, rare and minor metals,

and iron ore) is A$110. The annual rate for RCR reports – commodities covered may vary from quarter to

quarter – is A$440. Purchase details and research services for institutional investors can be found at

www.rcresearch.com.au]

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 3

Overview and Investment Comment

The outlook for rare and minor metals

Analyst: Dr Trent Allen

The past three months have seen considerable share price gains for some

rare and minor metals (RMM) equities, as investors become aware of the

potential for future supply shortages and consequent high metal prices.

Speculation has cooled in the past month, but companies that have quality

projects should retain some of their recent gains while prices remain above

their pre-2H10 levels.

The main market driver is China, which is reforming its RMM sectors, by

raising tariffs, reducing export quotas, and encouraging consolidation and

vertical integration of production. China‟s stated aims are to increase

domestic value-adding and use of the RMM, conserve resources, and

improve industry monitoring and efficiency. China‟s actions could boost

global RMM production.

Some examples of commodities with a stable to strong outlook for the next

several years:

Lithium: Increasing intensity of use is expected to require additional

supply beyond 2014.

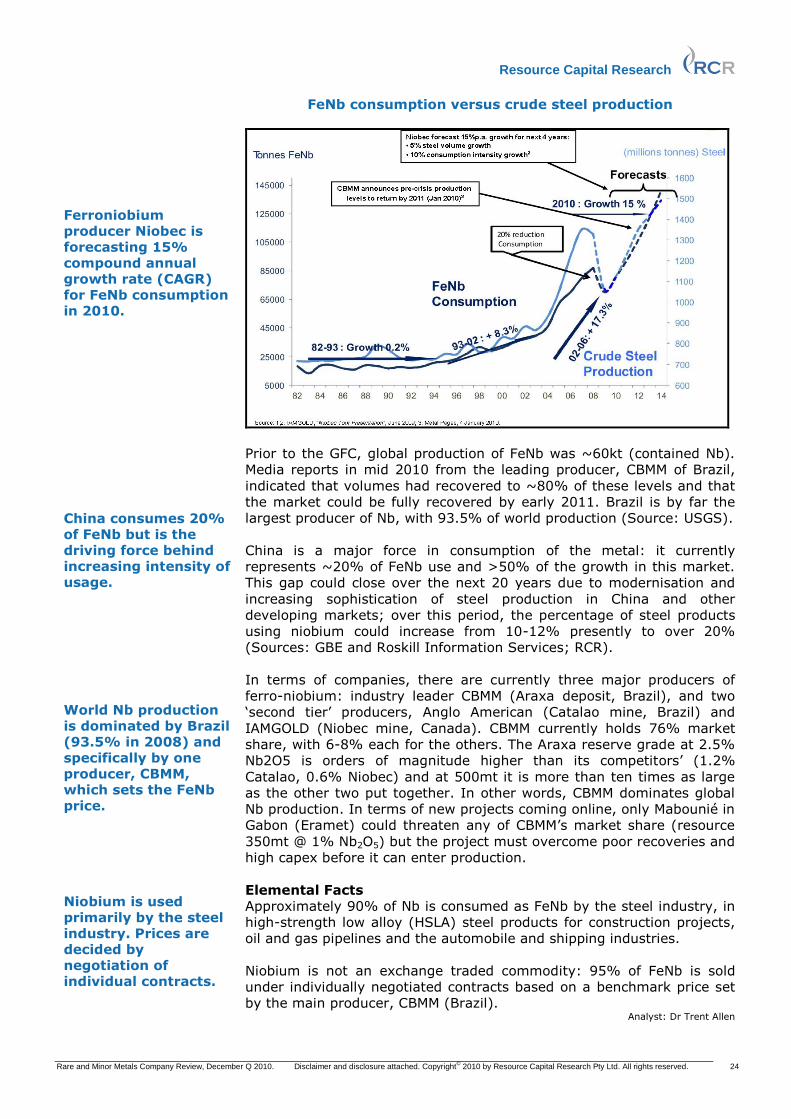

Niobium: Industry forecasts are for FeNb consumption growth of ~15%

per annum to 2014.

Rare earth elements (REE): Forecasts are for 20-30% CAGR in prices

to 2015. Export prices (China) up 510% year-on-year.

Tantalum: A supply shortfall is expected to hand a competitive

advantage to companies that provide a long-term supply of ethically

produced tantalum.

Tungsten: Supply shortages are indicated from 2013.

Zircon/zirconium: A lack of greenfields projects could create supply

shortages and boost prices in the near to medium term (1-3 yrs).

RMM deposits can take 5+ years to develop as mines, sometimes due to

their geochemical complexity, and the challenge of financing projects that

are considered to be outside the resources mainstream.

This provides an opportunity for companies with projects that are advanced

or can be fast-tracked, e.g. due to location, favourable chemistry, size

and/or high grades).

Equity performances

Globally, RMM stocks have outperformed most exchange-based indices in

the past 12 months. Share price performances have been studied, for 336

exchange-listed companies with one or more RMM projects (in six

commodity groups: lithium, REE, tungsten, zirconium, niobium, tantalum).

The unweighted average performance over 1 month (to November 17) was

+11%, compared to 1% for Australia‟s ASX S&P300 Metals and Mining

Index, and 0.1% for the ASX All Ords. Twelve-month performance was

+56% (S&P300 MM, 12%). The average RMM company share price is 33%

below its 12-month high and 155% above a 12-month low.

RMM stocks have

climbed this quarter,

in line with expected

metal shortages and

price rises.

The current market

driver is China‟s

policy of squeezing

exports.

Strong medium to

long term market

and price growth is

likely for many RMMs

Companies with

strong projects

should continue to

benefit from the

buoyant RMM

markets.

Share prices of rare

and minor metal

companies have

outperformed the

ASX over the past

year, with +56% annual growth.

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 4

RCR December Quarter 2010 Featured Company Summary AUSTRALIA

Company Code Commodities Comment

Alkane Exploration Limited ALK Definitive Feasibility Study

ALK shares have gained 45% in three months, driven by the REE market. The world class Dubbo

Zirconia Project (DZP) could be producing Zr, Nb and REE (up to 6.5ktpa) by 4Q12. A Definitive

Feasibility Study of 840koz Au Tomingley is expected 4Q10.

Arafura Resources Limited ARU Bankable Feasibility Study

ARU has raised A$90m at A$1.20/share to fund advanced development of the Nolans Rare Earths

Phosphate Project (NT) and an REE processing plant at Whyalla (SA). Recent share price trend

(+44% in 3 months) could continue: mid-term target is +A$3.00/share.

Crossland Uranium Mines Limited CUX Mid Exploration

CUX is exploring for large scale, low opex unconformity (Chilling) and "Rossing Style" (Charley Ck)

uranium targets located in the NT. Initial drill program at Charley Ck (results awaited) - potential for

significant discovery. Extensive alluvial REE confirmed (Nov '10).

Galaxy Resources Limited GXY Production

Mt Cattlin began Li concentrate production in Oct '10, with full output expected to be ~8.2ktpa Li2O.

GXY has strenghtened its ties to China, via an A$91m share and bond issue, and listing in Hong

Kong, ahead of building the Jiangsu Lithium Carbonate Plant.

Gippsland Limited GIP Bankable Feasibilty Study

Placing A$3.2m shares in Oct '10 means working capital for the Abu Dabbab (Egypt) tantulum-tin

project, where a 10-year offtake agreement is being re-negotiated (possible production 2013). An

ASX spin-off could unlock value in Tasmania and Eritrea.

Globe Metals & Mining Limited GBE Bankable Feasibility Study (BFS)

GBE's share price has jumped 88% in 3 months due to the strong rare metals market - REE

exploration results expected Oct '10. An A$41m deal could see China's ECE gain 51% of GBE, with

an eye to the 60Mt Kanyika Niobium Project (Malawi, BFS expected 2011).

Greenland Minerals & Energy Limited GGG Pre-Feasibility Study

A 33% one-month gain for GGG is due to a buoyant REE market, and Greenland allowing uranium

to be included in economic assessment of the Kvanefjeld Project (forecast REE 43.7kt/yr, U3O8

3.9kt/yr). Share price target A$1.46 with considerable upside.

Gunson Resources Limited GUN DFS, Advanced Exploration

GUN could soon announce a development partner for its ~A$170m Coburn Zircon Project in WA,

which could provide a 'fast track ' to production, as a projected global zircon supply deficit starts to

bite. This step should highlight a still undervalued share price.

Icon Resources Limited III Scoping Study

An expanded tungsten resource at Mt Carbine (QLD) includes a high-grade component of 57.5kt

WO3 @ 0.14% and is a 40% increase on the previous model. Treatment of historic tailings could

start 1Q11 and be followed by hard rock mining in 2013.

King Island Scheelite Limited KIS Feasibility

KIS should soon be debt-free and hold 100% of its King Island tungsten project, after the termination

of a joint venture. The project could produce 3.3kt/yr WO3 from a reserve grading 1.3% WO3, within

three years of funding.

CANADA

Avalon Rare Metals Inc AVL Bankable Feasibility Study (PFS)

The Nechalcho REE Project (Canada) has the second largest REE and third largest Nb resources in

the world. A Bankable Feasibility Study is expected in 2Q12 and the project could be producing

10ktpa total REO in 2015, along with Nb, Ta and Zr. Share price +38% over six months.

Rodinia Lithium Inc RM Early to Mid Exploration

Rodinia is anticipating initial resource statements in 4Q10-1Q11 at two lithium brine projects in the

US and Argentina. The strategy is to explore salars near high grade Li and pre-existing

infrastructure. Strong exploration results have led to share price +63% in 3 months.

TNR Gold Corp TNR Early to Advanced Exploration

TNR is exploring for gold, copper, lithium and rare earth elements (REE) in both North and South

America. A TSX spin-out of International Lithium Corp (ILC) should add value to its Li and REE

assets, and leave TNR with highly prospective Au-(Cu) targets.

Lithium, Tantalum,

Manganese, Iron

Tungsten, Gold,

Base Metals, PGE

Uranium, Gold,

REE, Base Metals,

Diamonds

Tungsten, Copper,

Gold

Rare Earths,

Niobium, Tantalum,

Zirconium

Lithium

Gold, Copper,

Lithium, Rare

Earths

Gold, Rare Earths,

Zirconium, Base

Metals

Rare Earths,

Phosphorus,

Uranium, Gold

Niobium, Tantalum,

Rare Earths,

Uranium, Fluorine

Rare Earths,

Uranium, Zinc,

Sodium Fluoride

Tantalum, Tin, Gold

Zircon, Titanium,

Copper, Gold,

Nickel

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 5

Financial Data

C OM P A N Y Aust Canada USA Europe other

Listed

opt ions Share Price (LC$/share)3

2 Fully

Diluted

M arket

Cap Book

Enterprise

Value

Code Status1

Yr End 52 week Current Shares Opt+W2

C. Notes2

Shares (undiluted) Cash Debt Value (Undiluted)

17 N o vember 2010 Hi Low (m) (m) (m) (m) (LC$m)3

(LC$m)3

(LC$m)3

(LC$m)3

(LC$m)3

AUSTRALIA (A$)

Alkane Explorat ion Limited Equinox M inAZXls LimitedALK E Dec ASX ARUO 1.19 0.23 0.68 249 0 0 249 168 3.6 0.0 46 168

Arafura Resources Limited ARU E June ASX 1.79 0.38 1.07 335 17 0 352 358 90.7 0.0 140 358

Crossland Uranium M ines Limited CUX E June ASX 0.31 0.08 0.21 115 9 0 124 24 5.7 0.0 12 24

Galaxy Resources Limited GXY P June ASX GXYO 1.66 0.91 1.45 191 24 0 215 277 104.8 146.3 107 423

Gippsland Limited GIP E June ASX GIX 0.09 0.03 0.05 624 56 0 680 29 2.6 0.0 7 29

Globe M etals & M ining Limited GBE E June ASX 0.51 0.12 0.32 94 3 0 97 30 3.9 0.0 19 30

Greenland M inerals & Energy Limited GGG E Dec ASX GGGO 1.10 0.31 0.82 270 154 0 424 220 10.5 0.0 59 220

Gunson Resources Limited Uranex NLGUN E June ASX 0.20 0.06 0.17 178 4 0 182 29 0.2 0.0 25 29

Icon Resources Limited III I June ASX 0.23 0.06 0.13 119 23 0 142 15 1.3 0.0 7 15

King Island Scheelite Limited KIS I June ASX 0.28 0.14 0.15 62 5 0 67 9 2.0 0.0 31 9

Total : (A$) 225.3 146.3 452.8 1306

CANADA (C$)

Avalon Rare M etals Inc AVL E Aug TSX OTCQX 5.00 1.89 3.14 92 11 0 103 290 38.8 0.0 77 290

Rodinia Lithium Inc RM E Dec TSX.V OTCQX 0.68 0.25 0.48 65 29 0 94 31 4.3 0.0 15 31

TNR Gold Corp TNR E Dec TSX.V 0.38 0.15 0.18 131 21 0 152 24 3.5 0.0 20 24

Total : (C$) 46.6 0.0 112.1 345

(1) P: Producer; E: Explorer; I: Imminent - includes companies with bankable feasibility studies and likely to be in production within 3 years (2) Fully Diluted (shares, opt ions + warrants (opt. + w), convert ible notes (Conv. N), other obligat ions)

(3) L.C. - Local Currency unit ; Nov '10F (4) AUD/USD:1.01; CAN/USD: 0.99 Colour code: Actuals in black, forecasts in blue. Numbers for FY2010 can be either, depending on when the FY ends and companies' report ing schedules.

Exchanges

Company Statistics

C OM P A N Y

Code Land (A)/(A+B) %

17 N o vember 2010 ('000 ha) Sep-10 Dec-10 2010 2011 Sep-10 Dec-10 2010 2011 Sep-10 Dec-10 2010 2011 Dec-10 2010 2011

AUSTRALIA (A$)

Alkane Explorat ion Limited ALK 181 3.8 3.8 21.2 15.0 1.9 2.0 7.7 6.0 0.3 0.3 1.2 1.0 89 86 86

Arafura Resources Limited ARU 500 6.3 6.3 15.0 25.0 3.0 5.3 13.2 14.3 1.3 2.3 6.0 7.1 70 69 67

Crossland Uranium M ines Limited CUX 964 0.7 2.0 0.0 18.7 1.9 0.4 1.6 3.5 0.3 0.3 0.6 1.0 61 71 77

Galaxy Resources Limited GXY 145 5.0 5.0 21.8 20.0 1.2 0.5 7.1 3.7 3.2 2.0 8.9 9.2 20 44 29

Gippsland Limited GIP 1,330 0.0 0.0 2.0 2.0 0.1 0.5 0.3 1.4 0.5 0.6 2.4 2.2 46 10 40

Globe M etals & M ining Limited GBE 279 1.7 3.0 20.0 14.7 0.8 0.3 5.4 2.1 0.3 0.4 1.0 1.3 46 84 61

Greenland M inerals & Energy Limited GGG 211 1.0 1.0 8.0 4.0 2.6 0.7 6.6 6.0 1.7 1.1 5.3 5.4 39 56 53

Gunson Resources Limited GUN 273 0.5 0.5 4.9 2.0 0.4 0.4 2.2 1.7 0.2 0.2 0.6 0.6 70 79 73

Icon Resources Limited III 441 1.0 1.0 8.0 4.0 0.6 0.2 2.2 1.2 0.1 0.1 0.3 0.4 67 88 77

King Island Scheelite Limited KIS 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.7 0.8 0.2 0.2 1.1 0.8 45 38 49

4323 19.9 22.5 100.8 105.4 12.5 10.4 46.9 40.6 8.0 7.3 27.4 29.0 55 63 61

CANADA (C$)

Avalon Rare M etals Inc AVL 4 8.8 5.0 22.2 23.8 3.0 3.0 19.2 12.0 0.5 0.5 2.1 2.0 86 90 86

Rodinia Lithium Inc RM 31 0.6 0.6 2.3 2.4 0.8 0.8 3.0 3.2 0.4 0.4 1.6 1.6 67 65 67

TNR Gold Corp TNR 34 1.0 0.5 2.3 3.5 0.7 0.7 2.2 2.7 0.3 0.3 2.6 1.3 73 46 68

Total or Average: 69 10 6 26.8 29.7 4 4 24.4 17.9 1 1.2 6.3 4.9 75 67 74

(A) Explorat ion (L.C.$m) (B) Corporate (L.C.$m)Drilling ('000 m)

Prepared by Dr Trent Allen

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 6

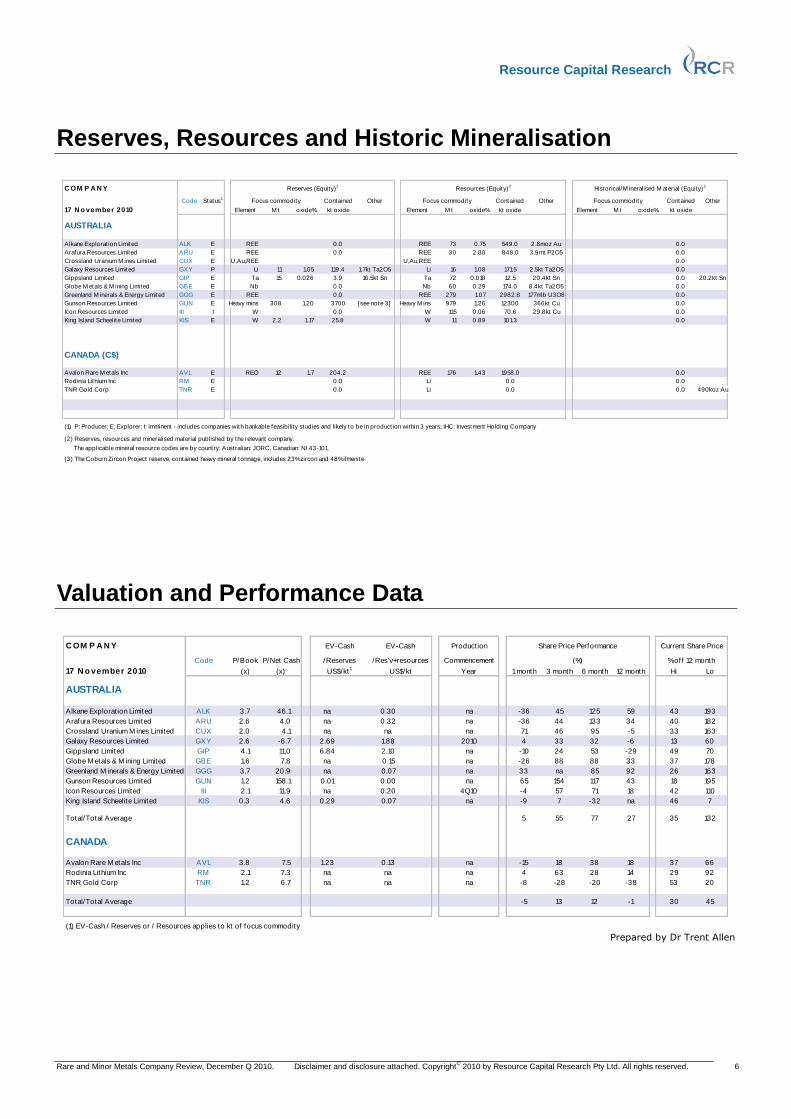

Reserves, Resources and Historic Mineralisation

C OM P A N Y

Code Status1

Contained Other Contained Other Contained Other

17 N o vember 2010 Element M t oxide% kt oxide Element M t oxide% kt oxide Element M t oxide% kt oxide

AUSTRALIA

Alkane Explorat ion Limited ALK E REE 0.0 REE 73 0.75 549.0 2.8moz Au 0.0

Arafura Resources Limited ARU E REE 0.0 REE 30 2.80 848.0 3.9mt P2O5 0.0

Crossland Uranium M ines Limited CUX E U,Au,REE U,Au,REE 0.0

Galaxy Resources Limited GXY P Li 11 1.05 119.4 1.7kt Ta2O5 Li 16 1.08 171.5 2.5kt Ta2O5 0.0

Gippsland Limited GIP E Ta 15 0.026 3.9 16.5kt Sn Ta 72 0.018 12.5 20.4kt Sn 0.0 20.2kt Sn

Globe M etals & M ining Limited GBE E Nb 0.0 Nb 60 0.29 174.0 8.4kt Ta2O5 0.0

Greenland M inerals & Energy Limited GGG E REE 0.0 REE 279 1.07 2982.8 177mlb U3O8 0.0

Gunson Resources Limited GUN E Heavy mins 308 1.20 3700 [see note 3] Heavy M ins 979 1.26 12300 366kt Cu 0.0

Icon Resources Limited III I W 0.0 W 115 0.06 70.6 29.8kt Cu 0.0

King Island Scheelite Limited KIS E W 2.2 1.17 25.8 W 11 0.89 101.3 0.0

CANADA (C$)

Avalon Rare M etals Inc AVL E REO 12 1.7 204.2 REE 176 1.43 1958.0 0.0

Rodinia Lithium Inc RM E 0.0 Li 0.0 0.0

TNR Gold Corp TNR E 0.0 Li 0.0 0.0 490koz Au

(1) P: Producer; E: Explorer; I: Imminent - includes companies with bankable feasibility studies and likely to be in production within 3 years; IHC: Investment Holding Company

(2) Reserves, resources and mineralised material published by the relevant company.

The applicable mineral resource codes are by country: Australian: JORC, Canadian: NI 43-101.

(3) The Coburn Zircon Project reserve, contained heavy mineral tonnage, includes 23% zircon and 48% ilmenite

Focus commodity Focus commodity Focus commodity

Reserves (Equity)2

Resources (Equity)2

Historical/M ineralised M aterial (Equity)2

Valuation and Performance Data

C OM P A N Y EV-Cash EV-Cash Production

Code P/Book P/Net Cash /Reserves /Res'v+resources Commencement

17 N o vember 2010 (x) (x) US$/kt1

US$/kt Year 1 month 3 month 6 month 12 month Hi Lo

AUSTRALIA

Alkane Explorat ion Limited ALK 3.7 46.1 na 0.30 na -36 45 125 59 43 193

Arafura Resources Limited ARU 2.6 4.0 na 0.32 na -36 44 133 34 40 182

Crossland Uranium M ines Limited CUX 2.0 4.1 na na na 71 46 95 -5 33 163

Galaxy Resources Limited GXY 2.6 -6.7 2.69 1.88 2010 4 33 32 -6 13 60

Gippsland Limited GIP 4.1 11.0 6.84 2.10 na -10 24 53 -29 49 70

Globe M etals & M ining Limited GBE 1.6 7.8 na 0.15 na -26 88 88 33 37 178

Greenland M inerals & Energy Limited GGG 3.7 20.9 na 0.07 na 33 na 85 92 26 163

Gunson Resources Limited GUN 1.2 158.1 0.01 0.00 na 65 154 117 43 18 195

Icon Resources Limited III 2.1 11.9 na 0.20 4Q10 -4 57 71 18 42 110

King Island Scheelite Limited KIS 0.3 4.6 0.29 0.07 na -9 7 -32 na 46 7

Total/Total Average 5 55 77 27 35 132

CANADA

Avalon Rare M etals Inc AVL 3.8 7.5 1.23 0.13 na -15 18 38 18 37 66

Rodinia Lithium Inc RM 2.1 7.3 na na na 4 63 28 14 29 92

TNR Gold Corp TNR 1.2 6.7 na na na -8 -28 -20 -38 53 20

Total/Total Average -5 13 12 -1 30 45

(1) EV-Cash / Reserves or / Resources applies to kt of focus commodity

(%)

Share Price Performance Current Share Price

% off 12 month

Prepared by Dr Trent Allen

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 7

Arafura Resources Limited

1.79

Debt (A$m) - Dec 10F

Enterprise value (A$m)

Avg monthly volume (m)

Cash (A$m) - Dec 10F

Price/Cash (x) Cash (A$m)

Price/Book (x)

Listed company options: Net asset backing (Ac/share)

*Quarters refer to calendar year. ^Raising capex A$950m in 4Q11, assumed 50/50 equity/debt.

Resources

Mineralised Material (est., non compliant with JORC)

Contacts Directors

Dr Steve Ward

Managing Director, CEO

Tel: +61 (0) 8 6210 7666

Perth, WA, Australia

Analyst: Dr Trent Allen

Capital raisings (A$m)^

Equity %

-

165.7

124.5

Drilling - Other/Diamond (m) 15,0006,250

291.3

Drilling - RAB (m) 0

Shares on issue (pr end) (m shares)

na

Arafura Resources Limited

40.34.0

0 0

A$ 1.07

Production and Financial Forecasts

2012F

486.4

0

Company Comment

0.0

163

Classification Project c/off

(JORC)

Ore

30.3

0.355

U

Mt

P2O5

2.60

2.80

12.3

Reserves and Resources/Mineralised MaterialCode for reporting mineral resources - Australian:

REO

1.0

Measured

Indicated 1.0

Location

REE %

1.0

0.00 0.0

1.7 g/t Au

2.98

Sep-10a

6,250

13.255.30

366.3

Partner Type

100% (Au)

-

0.0

23.518.4

0.0

Key Projects

500

0.0

0.00

na

Tenement costs ($k per year) -

Vein

na

na

M Muir (Non Exec)

(Non Exec)

www.arafuraresources.com.au

East China Min Expl & Devel Bureau (ECE, 22.2%)

I Laurance (Chairman)

Investment Points

Land holding ('000 ha)

Funding from JV partners (A$m)

No

90.7

"

Nolans Total

Mt Porter

ARU.AU

358.4

to

0.0

334.9Number of shares (m)

17.1Options and warrants (m)

Capital Profile

17 November 2010

30

Fully diluted (m)

358.4

World-class rare earth element (REE) deposit at Nolans

Project, with total resources of 30.3mt and production

expected in 2013.

Nolans Project valuation of A$1,967m and NAV

A$3.16/share (10% nom, exchange 0.8, post dilution) at

REO blend value US$30/kg, current is +US$50/kg.

Good infrastructure at NT mine site (railway, gas,

highway). Downstream chemical plant site will be at

Whyalla port in SA: given Major Project status by State.

Mine life +20 years with production of 20ktpa rare earth

oxides (REO), plus phosphoric acid, uranium, gypsum.

REO blend has high proportions of desirable "magnet

feed" REE: Nd, Pr and Dy. Value was US$51/kg in mid

October 2010, up 319% since Dec '09 in strong market.

Project risk should further decrease through 2011 with

final technology demonstration, mine and chemical plant

EIS/approvals, BFS and project finance (both 4Q11).

A$90m placement at A$1.20/share to fund BFS,

resource drilling. Shareholding of ECE will be diluted.

Market capitalisation (undiluted) (A$m)

Major shareholders: JP Morgan Nominees (29.5%)

0.0

Australia

Bankable Feasibility Study

Exchanges: ASX:ARU

Share price (A$) 1.07

S Ward (MD, CEO)

4.0

52 week range (A$/share)

Convertible notes (m)

0.38

352.0

2.6

Aust (NT)

Ni,Cu

Au

100% Au

A Losada-Calderon 100%

100%Kurinelli

Rare Earth Elements, Phosphorus, Uranium, Gold

Corporate (A$m)

5.6333

5.3

Funding duration at current burn (years)

1.32

ARU has raised A$90m at A$1.20/share to fund advanced development

of the Nolans Rare Earths Phosphate Project (NT) and an REE

processing plant at Whyalla (SA). Recent share price trend (+44% in 3

months) could continue: mid-term target is +A$3.00/share.

1.2

12.00

YEAR END: June*

8.007.07

Exploration and evaluation (A$m)

Exploration/(Expl.+ Corporate) (%) 69 6970 60

Dec-10F

25,000

0

500

290.6

2010a 2011F

14.28

347.9

500 500

33.92

2.25

67

5.99

90.00

- -

25,000

500

806.0

21.4 40.438.2

90.7

24.6

20.8

8.1

475

0.0 0.0

Cash backing (Ac/share) 6.3

I Kowalick (Non Exec)

none

Aileron / Reynolds 100%/(40%)

Indicated, inferred

L Shasha (Exec)

T Jackson (Non Exec)

Nolans

Hammer Hill

Mt Porter / Frances Ck

REE, P, Fe

100% REE, P, U

REO

1.7

Aust (NT)Mid Expl.

Early Expl.

na

Leach

none

none

none

Sulphide

Reef

Aust (NT)

M'morphic

Various

Aust (NT)

(Ngalia)

Aust (NT)

na

Early Expl.

Adv Expl.

na

Feasibility

Aust (NT)

1.6

kt mlb

848 3.9

2.9 0.7

Option Metal

91.96

ProjectJV

85.7

24.8

Rare Earth Elements

Reserves

2.80

ProcessOwnership/ Target

"

3 g/t Au

Project StatusRoute

344

A free, in-depth report about Arafura Resources Ltd, dated 18 December 2009, is available from w w w .rcresearch.com.au, as are recent quarterly updates

100% Fe, V M'morphicnone Mid. Expl.Jervois

Inferred

Nolans Project 100% 1.05.1 3.20

12.8

34.2koz Au

0.0 0.0 0.0

13.3

mt

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Nov-

09

Dec-

09

Jan-1

0

Mar-

10

Apr-

10

May-

10

Jun-1

0

Jul-10

Aug-1

0

Sep-1

0

Oct-10

Sh

are

Pri

ce

($/S

hare

)

ARU - Arafura Resources Limited

Source: Bloomberg

Introduction: Arafura‟s flagship is the Nolans Rare Earths-Phosphate-Uranium Project (NT), 135km NNW of Alice Springs. The deposit has a JORC resource of 30.3mt containing 848kt of rare earth oxides (REO), 3.9mt of phosphate (P2O5), and 13.3mlbs of uranium (U3O8), with potential to expand. A Bankable Feasibility Study (BFS) is expected in 4Q11. Mining is planned for 2013, when the Nolans Project could supply ~10% of the global rare earths market. ARU holds +5,000km

2 of grassroots to advanced exploration +projects (REE, Au, Fe, Ni) in the NT.

Nolans Project: Planned annual production from Nolans is 20kt REO, 80kt P2O5 (as phosphoric acid), 0.5mt CaSO4 (gypsum) and 0.33mlbs (150t) U3O8, with 400kt CaCl2 as residue that could be recycled into the chemical process. Mining rate, by open cut, will be 1mtpa with mine life +20 years. Processing will be in three broad stages: concentration; acid leaching into RE/uranium and phosphate streams; and production of final commodities such as REOs. Key inputs are chloralkali and sulphuric acid. The waste material would include Th, which is slightly radioactive (alpha) and must be stored appropriately. Forecast capital costs are A$950m (@ A/US 0.95) with 20% contingency, including A$690m for the chemical plant. Opex could be A$376mpa (chem. plant A$291mpa), i.e. US$376/t ore at 1mtpa. Infrastructure, includes a railway and gas pipeline. Road distance to the Darwin-Adelaide rail line is 65km. On-site concentrate production would precede rail transport to a chemical plant. Whyalla Rare Earths Complex (SA): The major industrial port of Whyalla (1400km rail from Nolans) was chosen in Sep „10 as location for the chemical plant. ARU has signed an Exclusivity Deed for 800ha land with OneSteel (ASX:OST), which controls the port. The purchase is expected to be finalised in 4Q10. The Complex will include facilities for producing feed chemicals and final products. The SA Gov‟t has granted Major Project status, providing certainty for work programs. A final decision to build should follow the BFS and project finance. Development schedule: The Nolans Bankable Feasibility Study (BFS) is now expected in 4Q11 after the scope was broadened due to improving credit markets. Announcements in 4Q10 should include a Mine Optimisation Study with mining reserves. Groundwater studies began 2Q10 ahead of an EIS for the mine site in 2Q11. Process de-risking via pilot and demonstration plant testing is under way, focused on beneficiation, the RE/REO stream, and acid recycling. Subject to finance in 4Q11, construction could begin in 2012 and production in 2013. Valuation: NAV is highly sensitive to REO prices. At a long term US$30/kg for the Nolans REO blend (current +US$50/kg), with U3O8 at US$50/lb, phosphate US$750/t and gypsum US$25/t, revenue would be US$689m/yr. Using opex/capex from the Oct ‟10 economic update and a 30% pre-BFS discount, Nolans after-tax NPV is A$1,967m (10% DR, AU/US 0.8). NAV could be A$3.31/share (fully diluted, with cash and exploration assets), assuming dilution from raising 50% of A$950m at a nominal A$2.00/share. Risks to the valuation (both upside and downside) include exchange rates and the China-controlled REO market, especially elevated LREE prices. There is upside risk from an increase in the Nolans resource, and downside in delays (process, permits, finance). Investment Comment: ARU‟s share price has increased 44% in the past three months due to high REE prices and well-received news about the Whyalla chemical complex, although it has backed off the Oct ‟10 high of A$1.79/share due to profit taking and stabilisation of an overheated REE equity market. If ARU keeps meeting its development milestones, a price of +A$3.00/share could be reached after project finance is established (expected 4Q11). The force driving Nolans to production will continue to be increasing REE demand (7%-9%pa) over the next 5 years, against a background of supply constraint and export quotas in China.

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 8

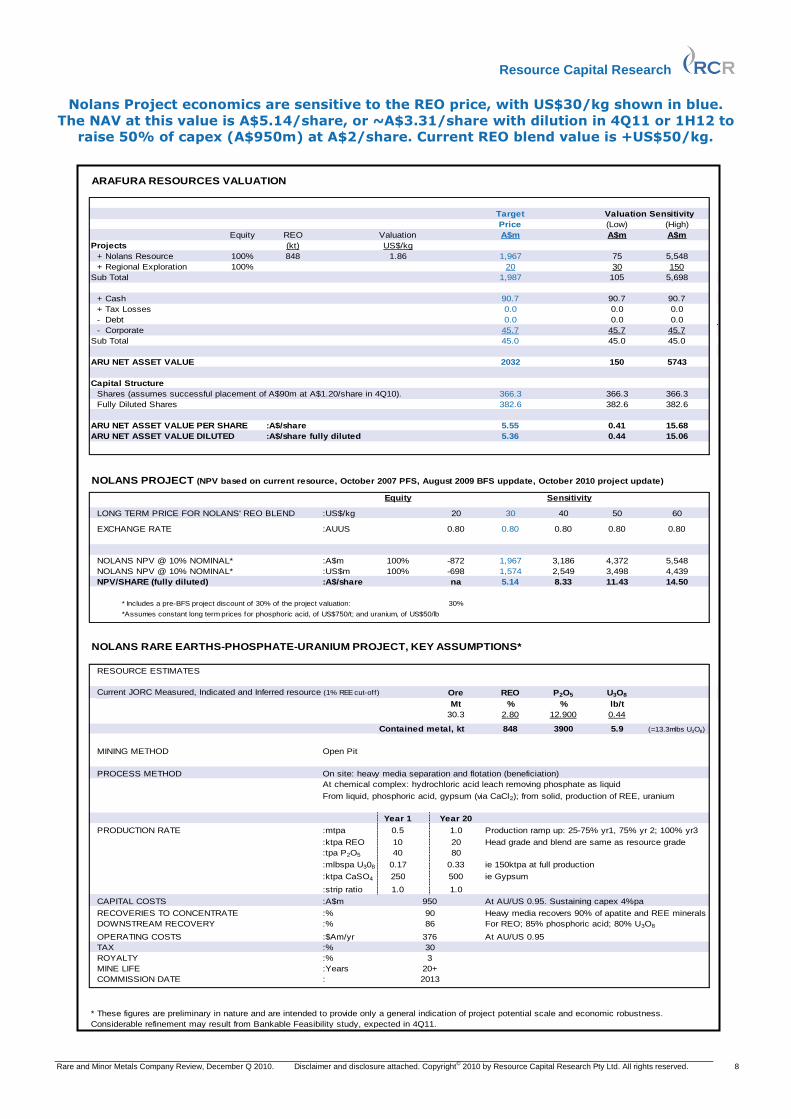

Nolans Project economics are sensitive to the REO price, with US$30/kg shown in blue.

The NAV at this value is A$5.14/share, or ~A$3.31/share with dilution in 4Q11 or 1H12 to

raise 50% of capex (A$950m) at A$2/share. Current REO blend value is +US$50/kg.

ARAFURA RESOURCES VALUATION

Target

Price (Low) (High)

Equity REO Valuation A$m A$m A$m

Projects (kt) US$/kg

+ Nolans Resource 100% 848 1.86 1,967 75 5,548

+ Regional Exploration 100% 20 30 150

Sub Total 1,987 105 5,698

+ Cash 90.7 90.7 90.7

+ Tax Losses 0.0 0.0 0.0

- Debt 0.0 0.0 0.0

- Corporate 45.7 45.7 45.7

Sub Total 45.0 45.0 45.0

ARU NET ASSET VALUE 2032 150 5743

Capital Structure

Shares (assumes successful placement of A$90m at A$1.20/share in 4Q10). 366.3 366.3 366.3

Fully Diluted Shares 382.6 382.6 382.6

ARU NET ASSET VALUE PER SHARE :A$/share 5.55 0.41 15.68

ARU NET ASSET VALUE DILUTED :A$/share fully diluted 5.36 0.44 15.06

NOLANS PROJECT (NPV based on current resource, October 2007 PFS, August 2009 BFS uppdate, October 2010 project update)

Equity

LONG TERM PRICE FOR NOLANS' REO BLEND :US$/kg 20 30 40 50 60

EXCHANGE RATE :AUUS 0.80 0.80 0.80 0.80 0.80

NOLANS NPV @ 10% NOMINAL* :A$m 100% -872 1,967 3,186 4,372 5,548

NOLANS NPV @ 10% NOMINAL* :US$m 100% -698 1,574 2,549 3,498 4,439

NPV/SHARE (fully diluted) :A$/share na 5.14 8.33 11.43 14.50

* Includes a pre-BFS project discount of 30% of the project valuation: 30%

*Assumes constant long term prices for phosphoric acid, of US$750/t; and uranium, of US$50/lb

NOLANS RARE EARTHS-PHOSPHATE-URANIUM PROJECT, KEY ASSUMPTIONS*

RESOURCE ESTIMATES

Current JORC Measured, Indicated and Inferred resource (1% REE cut-off) Ore REO P2O5 U3O8

Mt % % lb/t

30.3 2.80 12.900 0.44

Contained metal, kt 848 3900 5.9 (=13.3mlbs U3O8)

MINING METHOD Open Pit

PROCESS METHOD On site: heavy media separation and flotation (beneficiation)

At chemical complex: hydrochloric acid leach removing phosphate as liquid

From liquid, phosphoric acid, gypsum (via CaCl2); from solid, production of REE, uranium

Year 1 Year 20

PRODUCTION RATE :mtpa 0.5 1.0 Production ramp up: 25-75% yr1, 75% yr 2; 100% yr3

:ktpa REO 10 20 Head grade and blend are same as resource grade

:tpa P2O5 40 80

:mlbspa U308 0.17 0.33 ie 150ktpa at full production

:ktpa CaSO4 250 500 ie Gypsum

:strip ratio 1.0 1.0

CAPITAL COSTS :A$m At AU/US 0.95. Sustaining capex 4%pa

RECOVERIES TO CONCENTRATE :% Heavy media recovers 90% of apatite and REE minerals

DOWNSTREAM RECOVERY :% For REO; 85% phosphoric acid; 80% U3O8

OPERATING COSTS :$Am/yr At AU/US 0.95

TAX :%

ROYALTY :%

MINE LIFE :Years

COMMISSION DATE :

950

90

86

* These figures are preliminary in nature and are intended to provide only a general indication of project potential scale and economic robustness.

Considerable refinement may result from Bankable Feasibility study, expected in 4Q11.

Valuation Sensitivity

Sensitivity

376

30

3

20+

2013

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 9

Avalon Rare Metals Inc

4.99

Debt (C$m) - Aug 10F

Enterprise value (C$m)

Avg monthly volume (m)

Cash (C$m) -Aug 10F

Price/Cash (x) Cash (C$m)

Price/Book (x)

Listed company warrants: Net asset backing (Cc/share)

Quarters refer to calendar year.

Contacts Directors

Mr Donald Bubar

President, Director, CEO

Tel: +1 (416) 364 4938

Toronto, ON, Canada

Analyst: Dr Trent Allen

Capital raisings (C$m)

-

35.5

0.0 0.0

* Cut offs defined on basis of Net Metal Return (NMR) in PFS financial modelling. ^ Inferred total has 0.21% HREO, 2.7% ZrO2, 300ppm Ga2O5.

to

D Bubar (Pres, CEO)

D Connelly

7.6

3.25

1.89

A Ferry (Non Exec Chair)

LocationType

Investment Points

Land holding ('000 ha)*

Funding from JV partners (C$m)

AVL.WT

c/off

feldspar

-

0.0

MFC Global Investment Management US, LLC (15.6%)

Igneous

Partner

2.30.3

Drilling - Other/Diamond (m) 10,2725,000

92.3

0

23,757

79.1

Drilling - RAB (m)

C$ 3.25

Production and Financial Forecasts

2011F2009a 2010F

Avalon Rare Metals Inc

Shares on issue (pr end) (m shares) 79.0 79.1 70.8

0 00

10.39 3.00

Corporate (C$m)

May-10a Aug-10F

95

Exploration and evaluation (C$m)

Exploration/(Expl.+ Corporate) (%)

AVL.CN

300.0

0.0

92.3Number of shares (m)

10.7Options and warrants (m)

Capital Profile

52 week range (C$/share)

Exchanges: TSX:AVL, OTCQX:AVARF

25

Fully diluted (m)

300.0

Nechalcho Project: world's second largest REE

resource (Canada, NWT), includes ~2.5mt of Total REE

Oxides (TREO) grading 1.4%.

Rare earths in Basal Zone of the deposit are 23% heavy

rare earths, implying a high value ore. Recent 40%

upgrade in Inferred resource (Sep '10).

Thor Lake Pre-Feasibility Study (June 2010): capex

C$900m, opex C$267/t (mined) for 10ktpa TREO, LOM

18yrs, pre-tax NPV (10%) of C$246m (C$2.78/share).

A viable metallurgical process has been defined for

REE, with valuable by-products (zirconium, niobium,

gallium). Low thorium, no significant contaminants.

Well-funded to finish BFS in 1H12, with Oct '10 cash

C$42m (and no debt) after C$30m share placement and

C$9.6m exercise of warrants.

Three-month share price +18% in tight REE market, with

industry-wide speculation followed by pullback.

Market capitalisation (undiluted) (C$m)

Major shareholders:

0.0

Canada

Bankable Feasibility Study (BFS)

Share price (C$)

6.81

The Nechalcho REE Project (Canada) has the second largest REE and third

largest Nb resources in the world. A Bankable Feasibility Study is expected

in 2Q12 and the project could be producing 10ktpa total REO in 2015, along

with Nb, Ta and Zr. Share price +38% over six months.

0.4

12.0019.24

YEAR END: August

17 November 2010

Funding duration at current burn (years)

0.56

Convertible notes (m)

103.0

Rare Metals

2.002.120.50

90

3.22

6886 86

0

4

5,000

4

3.9416.11 0.00

44

Tenement costs ($k per year)

5.8

32.8

9.2

4

22,217

- - -

39.62

41.2

Cash backing (Cc/share) 13.3

10.5

0.0

7.3

0.07.3

50.4

Company Comment

49.949.9 35.4 83.3

Ta

Separation Rapids Igneous

Process

P Fontaine

H Panday Canada (ON)Exploration

Permitting

na

na

none

P McCarter

BD MacEachenwww.avalonraremetals.com

100%

100%

100%

none

none

REE,Nb,Ta100%

100%

Sn,In,Ga

Li

none

none

Option Metal

48.89

Project

7.3

9.2

4.1

JV

Lilypad Lakes Igneous

IgneousWarren Township

Ownership/ Target

Project

East Kemptville

Nechalacho

Canada (ON)

na

Route

Financing

Scoping

na

PFS Canada (NWT)Float, hydromet

Status

Canada (ON)

Canada (NS)

Key Projects

Igneous

TREO

Equity Mt %

Reserves - Nechalacho

Reserves and Resources/Mineralised MaterialCode for reporting mineral resources - Canadian: NI 43-101

Rare Metals Classification Project Ore Nb2O5 Ta2O5TREO

kt

260 204.2

% ppmC$/t NMR*

20.5 1.75 260

0.41 410100% 12.0 1.70

Resources - Nechalacho

358 0.42 139Basal Zone Indicated 100%

Upper Zone Indicated 100% 10.0 1.43 260 143 0.28 169

Basal Zone Inferred 100% 84.2 1.53 260 1,288 0.43 131

Upper Zone Inferred 100% 98.4 1.29 260 1,269 0.36 171

2,556 0.39Total as Inferred^ 182.6 1531.40

Mineralised Material (est., non compliant with JORC) 0.0 0.0 0.0

1

1.5

2

2.5

3

3.5

4

4.5

5

Dec-

09

Jan-1

0

Feb

-10

Mar-

10

Apr-

10

May-

10

Jun-1

0

Aug-1

0

Sep-1

0

Oct-10

Share

Price (

$/S

hare

)

AVL - Avalon Rare Metals Inc

Source: Bloomberg

Introduction: AVL owns five rare metals and minerals projects in Canada, of which four are at advanced stages of development. Its main asset is the 100% owned Nechalacho Rare Earth Element Deposit. Nechalacho (REE, Nb, Ta, Zr): The project is at Thor Lake, 100km SE of Yellowknife. The deposit, an igneous intrusion, is enriched in valuable HREE (heavy rare earth elements). Since 2005, Avalon has spent C$25m on exploration and development. It is focusing on high-grade, HREE-rich resources in the large Basal Zone, which (as of September 2010) contains Indicated Resources of 20.45mt @ 1.75% TREO (total rare earth oxides) with 23% HREO/TREO. Total Inferred Resources are 182.6mt @ 1.4% TREO. The deposit also contains Ta, Nb, Zr, Hf and Ga. Less than 10% of the property has been drilled. Recent discoveries include a near-surface zone (North Tardiff) with 11m @ 10.78% TREO. Assays from summer drilling are pending. The main deposit is open in three directions. Pre-Feasibility Study: This June 2010 study was of an 18-year mine life, operating underground (~200m depth) on a 12mt reserve in the deposit‟s Basal Zone, ramping from 5ktpa up to 10ktpa TREO (total rare earth oxides), 18ktpa ZrO2, 1.7ktpa Nb2O5 and 100t Ta2O5. Opex is expected to be C$267/t. Capex is C$899.7m with 22% contingency, including C$589.3m for an underground mine, onsite mill (crush, flotation; 8.4MW by diesel at 2,000tpd) and offsite hydrometallurgical separation plant. The PFS contemplates a plant in the tailings area of an historic mine (Pine Point), to reduce environmental impacts and allow hydroelectric power during summer (7.3MW). In this scenario, concentrate will be barged in summer from Thor Lake via Great Slave Lake to the plant. Combined recoveries are 84.6% for flotation, 90% for the hydro plant. A more recent Scoping Study of plant costs (Oct ‟10) estimates capex at C$346m. The PFS estimates pre-tax net cash flow of C$2.1bn ($1.5bn post tax), with IRR 14%, and pre-tax NPV @ 10% of C$246m (C$/US$ 0.9) and NPV @ 5% of C$826m. REEs contribute ~56% of revenue at US$21.94/kg TREO. Development: Possible start date for full capacity production is 2015, with 24-30 months construction from 2013 upon receipt of land and water permits and financing. A flotation pilot plant could be constructed from September 2010 and a Bankable Feasibility Study is expected in 1H12, ahead of project financing. Permitting: Avalon commenced application for Type A Land Use Permit and Water Licence, in 2Q10 – an Environmental Assessment can take ~1.5-2.5 years to complete, prior to official review and approval. Other Projects: There are three other advanced projects in Canada, i.e. Separation Rapids (lithium, Ontario), Warren Township (calcium feldspar; Ontario; currently inactive pending resolution of permitting issue) and East Kemptville (tin-indium-gallium-germanium; Nova Scotia). A fifth project, Lilypad Lakes (tantalum; Ontario) is early stage. These projects could move forward under Joint Venture or be monetised while AVL develops Nechalacho. Investment Comment: Nechalacho has the second largest REE resource in the world, and the third largest niobium resource. If Nechalacho comes on line in 2015 it would fill <5% of anticipated world REE demand, even at the full rate of 10ktpa, so any downward pressure on global REE prices due to extra supply should be moderate. The NPV of Nechalacho, of C$246m (from the PFS), is close to AVL‟s market capitalisation of ~C$410m but the ore value will have increased since July 2010 (e.g. cerium oxide value +500% in 3 months). In line with other REE equities, the share price increased dramatically after July 2010 due to dramatic cuts in Chinese rare earth exports, and pulled back due to profit taking and stabilisation of the market; AVL remains highly leveraged to REE prices.

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 10

Avalon Rare Metals Inc project location map: from a recent company presentation, this

graphic shows the main focus is on Thor Lake, where AVL has the Nechalacho and North T

Deposits. Total resources include 2mt of Rare Earth Oxides (REO).

Thor Lake, schedule to production: Avalon plans to have the Nechalacho REE Deposit in

production in late 2015. The project is expected to progress along four lines: community

engagement, permitting, marketing and Bankable Feasibility Study (BFS).

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 11

Crossland Uranium Mines Limited

0.31

Debt (A$m) - Dec 10F

Enterprise value (A$m)

Major shareholders: Gaden Nominees (6.14%); ANZ Nominees (5.7%)

Avg monthly volume (m)

Cash (A$m) - Dec 10F

Price/Cash (x) Cash (A$m)

Price/Book (x)

Listed company options: Net asset backing (Ac/share)

*Uranium prospective tenements only; held and under application. Quarters refer to calendar year.

Contacts Directors

Mr Geoff Eupene

Executive Director

Tel: 61 (0) 8 8981 5911

North Sydney, NSW, Australia

U3O8 Eq

Mlb

Status

Kt

0.0 0.0

P Walker (Non Exec Dir)

1.1

3.3

0.0

Process

Charley Creek

Analyst: John Wilson

Granite

Target

www.crosslanduranium.com.au R Richardson (Non Exec Dir)

5.00

Equity

U3O8Cut Off

P Elliott (Non Exec Dir)

R Cleary (Non Exec Ch)

G Eupene (Exec Dir)

Mineralised Material (est., non compliant w ith JORC)

Project Metal

4.1

0.2

8.4

Cash backing (Ac/share)

1.2

Early Expl. Aus (NT)

Early Expl.

0.00

Aus (NT)

Aus (SA)

16,000

0.00

Lake Woods

Type

Unconf

Project

IOCGU

Chilling Project

Ownership/

Kalabity 30%

TSX.V:PUC

JV

Option Partner

Diamonds

5.7

Reserves and Resources/Mineralised Material

Key Projects

0.0

U3O8

U3O8Classification

U

TSX.V:PUC

50%

50%

100%

na

Project

Route

na

NT uranium focus - 90%. Exploration budget ~A$3mpa.

Charley Creek (near Alice Springs, NT): strategic holding

(4,111km2); large radiometric anomaly. Cockroach Dam

drilling 4Q10 for "Rossing Style" granite hosted uranium.

Charley Creek sediment basins: Shallow, high percentage

heavy REE (contained in 39% REO). Likely extractable

with exisiting technology. Potential JORC 4Q11.

Chilling (NT): Shallow unconformity style targets in Pine

Creek Orogen. Similar stratigraphy to Rum Jungle.

Marchfly Zone (Chilling): best drill intercept 0.5m @

0.816% U3O8 (2009). Drilling 1H11(2,000m).

Exploration team experienced in Australian uranium

unconformity style deposits - chief geologist for Ranger

Mine development and Ranger 68 discovery.

Uranium

Code for reporting mineral resources - Australian:

Reserves

Aus (NT)

0.0

U Platsearch

U, REE

na

5

-

140.5

2,730

964

Company Comment

9.3

4.6

140.5

17,000

964

Location

Early Expl.

na

Early Expl.

na

0.00.0

24.3

125

Eupene Nominees (5.20%)

0.0

Market capitalisation (undiluted) (A$m)

1.2

0

Fully diluted (m)

24.3

964

4.2

Investment Points

Convertible notes (m)

YEAR END: Dec

5.7

-

2.1

No

Share price (A$)

Number of shares (m) 115

Options and warrants (m)

0.21

0.08

CUX.AU

9

Uranium, Gold, REE, Base Metals, Diamonds

Australia (NT,SA)

Mid Exploration

Exchanges: ASX:CUX

Capital Profile

52 week range (A$/share) to

17 November 2010

0 Exploration/(Expl.+ Corporate) (%)

2.2

Ore U3O8

Mt

-

140.5

%

0.0

115.5

0.00

0

0

0

ppm

-

85 70

0.40

0.26

80

1.3

0.970.44 1.04

1.85

0.27Corporate (A$m)

2.55 2.403.86

A$ 0.21

Production and Financial Forecasts

2011FDec-10F

CUX is exploring for large scale, low opex unconformity (Chilling)

and "Rossing Style" (Charley Ck) uranium targets located in the NT.

Initial drill program at Charley Ck (results awaited) - potential for

significant discovery. Extensive alluvial REE confirmed (Nov '10).

61

Land holding ('000 ha)*

Drilling - RAB (m)

Shares on issue (pr end) (m shares)

Funding duration at current burn (years)

Drilling - Other/Diamond (m)

Exploration and evaluation - gross (A$m)

Funding from JV partners (A$m)

8.4

Capital raisings (A$m)

Tenement costs ($k per year)

7.7

-

964

0

2,000

5.6

3.2 4.1

(JORC)

5.7

Resources

Mlb

0.0

2.2

5.00

1.0

3.1

3.7

Crossland Uranium Mines Limited

87

115.5

0

730

1.3

2009aSep-10a 2010F

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Nov-

09

Dec-

09

Jan-1

0

Mar-

10

Apr-

10

May-

10

Jun-1

0

Jul-10

Aug-1

0

Sep-1

0

Nov-

10

Sh

are

Pri

ce

($/S

hare

)

CUX - Crossland Uranium Mines Limited

Source: Bloomberg

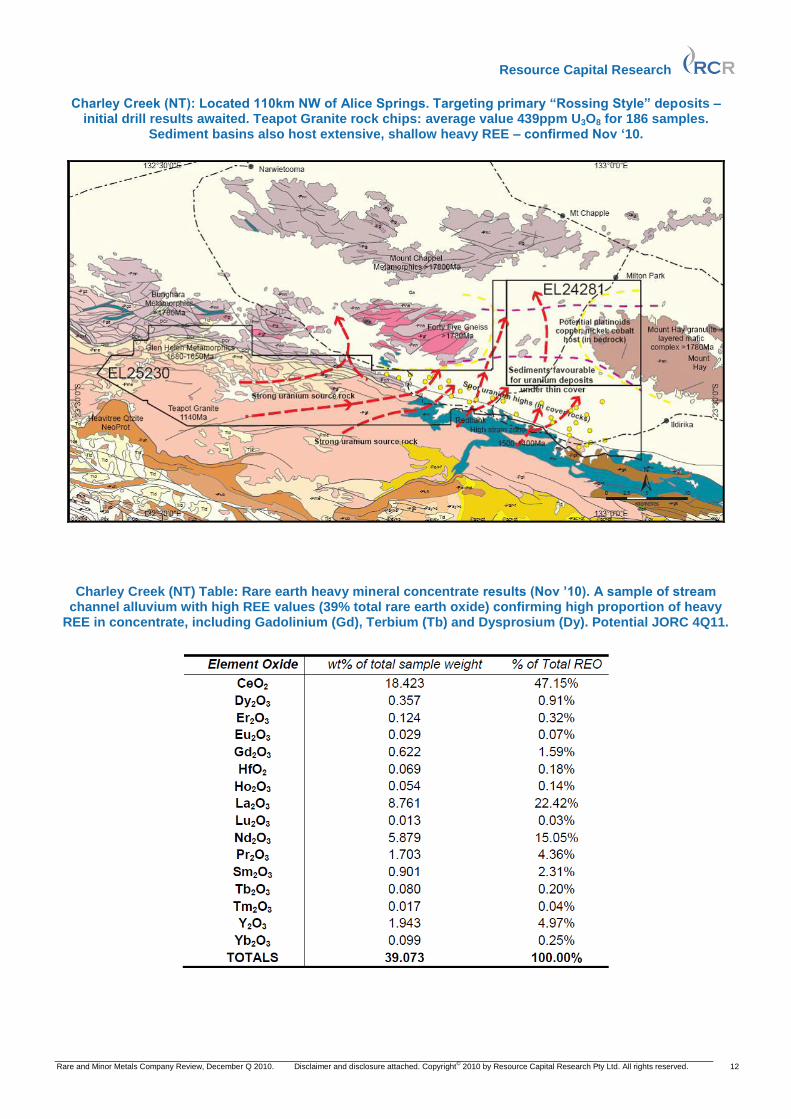

Overview: Crossland Uranium Mines formed as the merger of Klondike Source Limited (KSL) and Crossland Mines Pty Ltd, in May 2006. It listed on the ASX April 2007. Pancontinental holds a contributing 50% stake in most CUX projects (U/REE/base metals). Crossland‟s directors and management are one of the most experienced uranium teams in Australia. Charley Creek project (NT): (4,111km

2 granted) Located 110km north-west of Alice Springs, prospective for

a variety of mineralisation styles, including primary and secondary uranium, heavy rare earth elements and intrusive related copper, nickel and platinoids. Granite hosted uranium - CUX is currently drilling “hot” granites – targeting large, low grade uranium deposit styles, the closest analogy being “Rossing Style” deposits in Namibia. Rock chip samples have returned values up to 0.54% U3O8, with an average of 439ppm for 186 samples. The area has received little, or no, previous exploration attention. Permits were granted mid July and drilling commenced August (1,500m, 10 holes @ 150m) – targeting areas within the Teapot Granite (~50km

2) at Cockroach Dam, Cockroach East, and Cockroach Central. CUX expanded Charley

Creek holding and announced a JV with Western Desert (ASX:WDR, Aug „10). Drainage and Sediment Basins: prospective for palaeochannel and calcrete uranium deposits. Airborne EM conducted in 2007 identified palaeochannels - drilling expected 1H11 subject to approvals. Rare Earth Elements (REE, NT): Initial assays and met test work produced a heavy mineral concentrate from stream channel alluvium. Initial samples contained 39% REO, including a high proportion of heavy REE (Gd, Tb, and Dy, refer table) which are in global short supply. Initial exploration suggests these REE ratios could be widely reported throughout the Cockroach Dam area. CUX expects, due to the shallow nature and likely established process routes for this type of REE mineralogy (phosphate mineral) that there is potential for a low capex project to produce several thousand tonnes pa of heavy REE concentrate. Expansion of REE exploration is expected 2011 - auger drilling (10,000m) 1Q11 to test for depth extensions and consistency of heavy REE RAB/RC drilling (10,000m) expected 2Q11. Chilling (NT): (2904km

2). Located 20km SSW of Rum Jungle on the west side of the Pine Creek Orogen -

targeting large scale, high grade unconformity style uranium deposits. Chilling contains 130km of prospective unconformity strike length and potential 110km extension under cover. Airborne geophysical survey completed 2007 and regional AEM identified 43 priority anomalies, followed up with ground surveys and some initial air-core drilling. Buchanan Window - Increasing focus of CUX activity prospective for uranium and base metals. Confirmed basal Pine Creek Orogen stratigraphy as at Rum Jungle. Drilling 1Q11 (1,500m) – targeting bedrock to 250m depth (10 drill targets). Allia Window - drilling EM anomalies 1Q11 (1,000m). Marchfly - initial drill program 2009 (11 holes) - highest grade intersection - CHDD12: 0.816% U3O8 over 0.5m. Investment Comment: CUX has potential for large scale uranium discovery in established (Chilling, Pine Creek Orogen) and new (Charley Creek) districts. Near term share price catalysts could be Initial drill results from primary uranium targets at Charley Creek - expected Nov-Dec ‟10; and REE auger results 1Q11. The share price doubled from $0.15 with REE announcement 1 November. CUX offers an attractive risk/reward trade-off, with upside to large scale uranium discovery, REE and base metals. Cash A$5.7m Dec ‟10F; capital raising expected 1H11.

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 12

Charley Creek (NT): Located 110km NW of Alice Springs. Targeting primary “Rossing Style” deposits – initial drill results awaited. Teapot Granite rock chips: average value 439ppm U3O8 for 186 samples.

Sediment basins also host extensive, shallow heavy REE – confirmed Nov „10.

Charley Creek (NT) Table: Rare earth heavy mineral concentrate results (Nov ‟10). A sample of stream channel alluvium with high REE values (39% total rare earth oxide) confirming high proportion of heavy

REE in concentrate, including Gadolinium (Gd), Terbium (Tb) and Dysprosium (Dy). Potential JORC 4Q11.

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 13

Globe Metals & Mining Limited

0.51

Debt (A$m) - Dec 10F

Enterprise value (A$m)

Avg monthly volume (m)

Cash (A$m) - Dec 10F

Price/Cash (x) Cash (A$m)

Price/Book (x)

Listed company options Net asset backing (Ac/share)

Quarters refer to calendar year.

Resources

Mineralised Material (est., non compliant with JORC)

*5Mt measured, 18Mt Indicated, 37Mt Inferred

Contacts Directors

Mr Mark Sumich

Managing Director

Tel: +61 (0) 8 9486 1779

West Perth, WA, Australia

MW100%/20% U ASX:RSL S'stone na Adv Expl

0.0 0.0 0.0

174.00.29 0.15 0.014 0.009Kanyika Meas, Ind, Inf* 100% 60.0

% %

Reserves 0.0 0.0

Equity Mt

c/off

% Nb2O5%

Code for reporting mineral resources - Australian:(JORC)

Nb, Ta, U Classification Project Ore Nb2O5

0.00.0 0.00

Ta2O5 U3O8 Nb2O5

kt

0.0

Key Projects

0.00

Status

Target ProcessOwnership/

BFS MW

Mid Expl

MW

Analyst: Dr Trent Allen

0.0

18.4

(JORC)

1.6

1.5

Company Comment

36.2

100.1

11.2

Option Metal

44.50

Project

0.0

Early Expl

na

93.75

5.9

1.401.34

MW

MZ

Early Expl

F, REE Carb'tite

Salambidwe

Mount Muambe

J Stephens (Non Exec)

W Hayden (Non Exec)

Livingstonia

Reserves and Resources/Mineralised Material

5.29

2.5

0.00 3.50

17.5

0.0

Type

ASX:RSL

none

Partner

JV

Project

Machinga

Kanyika 100%

164.1

1,688

279

No

3.9

17.3

2.37.8

Cash backing (Ac/share) 3.6

0.35

61

1.03

8446

17 November 2010

0.12

Rare Metals, Uranium, Fluorine

Exchanges: ASX:GBE

Share price (A$)

0.29

73

Exploration and evaluation (A$m)*

Exploration/(Expl.+ Corporate) (%)Performance shares (m)

102 1.4

5.36

0.32

GBE's share price has jumped 88% in 3 months due to the strong

rare metals market - REE exploration results expected Oct '10. An

A$41m deal could see China's ECE gain 51% of GBE, with an eye to

the 60Mt Kanyika Niobium Project (Malawi, BFS expected 2011).

0.4

2.002.09

59

Sep-10a 2011F

Funding duration at current burn (years)

11

Fully diluted (m)

30.1

Valuation gap: Globe NAV (10% nom, 4Q10) based on

scoping/feasibility study is A$315m or ~A$1.78/share post

development funding - current market cap ~A$30m.

Kanyika Project BFS results expected 2011. Scoping

Study (Jun '08, Coffey; update May „09) - 4ktpa Nb as

FeNb, opex US$13/kg-US$20/kg Nb, capex US$155m.

Key economic driver is niobium, used in steel. Nb price is

extremely stable, LT forecast US$39/kg in FeNb, current

US$42/kg. Nb 70-85% revenue; tantalum 15-30%.

Planned 51% investment by China's ECE could bring

initial A$41m and lead to project funding, subject to

government, shareholder approvals (possible Jan '11).

MOU's for offtake covering 45% of forecast production.

Portfolio of exploration projects in Africa. Drilling results

expected Nov '10 from Machinga Project (REE,Nb,Ta).

Kanyika resource of 60mt has 174kt Nb2O5 grading

0.29%, with 18.5mlbs tantalum as Ta2O5 and 11.9mlbs

Market capitalisation (undiluted) (A$m)

Major shareholders: HSBC Custody Nom (7.6%)

0.0

Malawi, Mozambique

Bankable Feasibility Study (BFS)

GBE.AU

30.1

to

5

94Number of shares (m)

3.2Options and warrants (m)

Capital Profile

52 week range (A$/share)

Shares on issue (pr end) (m shares)

YEAR END: June

0.79 0.30

Corporate (A$m)

A$ 0.32

Production and Financial Forecasts

2012FDec-10F 2010a

Globe Metals & Mining Limited

Drilling - Other/Diamond (m)

92.9

00

20,000

108.2

3,000

94.2

Drilling - RAB (m) 0

29.45.4

279

5.9

320.8

0

20,00014,688

0

279

Ragusa Investments (6.7%), JP Morgan Nom (6.3%)

M Sumich (Exec Chair, MD)

Investment Points

1.6

Code for reporting mineral resources - Australian:

Land holding ('000 ha)* 279

-

279

Tenement costs ($k per year) -

3.9

Acid leachU (Nb,Ta)

REE0%/80%

none

ASX:RSL100%

0%/90%

Location

na

Granitoid

Pegmatite

na

Route

Pegmatite

REEwww.globemetalsandmining.com.au

D Sumich (Non Exec)

-

31.2

46.8

- -

16.9

Capital raisings (A$m)

Funding from JV partners (A$m) 0.0

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Nov-

09

Dec-

09

Jan-1

0

Mar-

10

Apr-

10

May-

10

Jun-1

0

Jul-10

Aug-1

0

Sep-1

0

Oct-10

Sh

are

Pri

ce

($/S

hare

)

GBE - Globe Metals & Mining Limited

Source: Bloomberg

Introduction: Globe Metals & Mining listed on the ASX in December 2005. It is an African-focused rare metals resource company. Its main project is the multi-commodity Kanyika Niobium Project. Globe also has exploration projects focused on rare metals, fluorite and uranium projects. Investment by ECE: A A$41m buy-in at A$0.345/share could see the East China Mineral Exploration and Development Bureau own 51% of GBE. China consumes ~35% of global ferroniobium (FeNb) and ECE (a holder in ASX-listed REE player Arafura) plans to help GBE with project finance and development. Approval is needed from Malawi, China, Australia, shareholders (EGM called for Jan ‟10). Kanyika (uranium, central Malawi): GBE is targeting rare metals (niobium, tantalum), zirconium and uranium mineralisation in an alkalic granitoid in central Malawi. The main ore minerals are disseminated pyrochlore (Nb, Ta, U) and zircon (Zr). GBE aims to bring Kanyika into production in late 2012, or 2013. Resource and grade – The current resource is 60mt, with a recent 77% increase in Measured and Indicated tonnes (now 23Mt). The resource is defined to 300m width, 250m depth and 2.3km of ~3.8km known strike within 5 zones: 60mt @ 0.29% Nb2O5 (174kt), 0.009% U3O8 (11.9mlbs), 0.014% Ta2O5 (18.5mlbs) and 0.5% ZrSiO4. There is a high-grade resource at 3,000ppm Nb2O5 cut-off, of 21mt with 0.41% Nb2O5 of which 10mt is M&I grading 0.47% Nb2O5 The deposit is open along strike in both directions (N-S). There is a high-grade Exploration Target of 40-50Mt @ 0.37-0.4% Nb2O5. Metallurgy – GBE aims to produce ferro-niobium (FeNb) for the steel industry, as well as oxides of niobium, tantalum and uranium, and possibly magnetite (iron oxide) and zircon. Studies commenced in 2008: two initial phases reported encouraging costs and recoveries, and work is entering Stage 3 (bulk testing pilot program). Studies were on hold (dispute with former JV partner) but could restart in 4Q10. Mining Potential - The deposit could be mined open-pit with low strip ratio of 0.5-0.9. Higher-grade, near surface Measured and Indicated resources could be targeted first (critical for early payback of capex). A Scoping Study (Coffey, Jun ‟08; updated May „09) examined 4ktpa Nb production as FeNb alloy, with 59tpa Ta2O5 and 11.4-13.7ktpa ZrSiO4 (processing 2.2-3.5mtpa) with a 20yr LOM. Uranium would report to aluminous slag for potential future processing. Current (revised) model prefers mining 1.5mt-2.5mtpa, for 3,000tpa Nb and 192tpa Ta2O5 over life-of-mine. Capex US$155m, opex US$40.3/t. A Bankable Feasibility Study (BFS) is in progress, and a pit design should be completed 4Q10 (Coffey Mining). Other Projects: GBE has exploration projects in Malawi and Mozambique that could provide positive newsflow in the near term. The main focus is Machinga (Southern Malawi), for pegmatite-hosted REE-Nb-Ta-Zr. Trenching in 2Q10 incl. 10m @ 1% TREO (total REO) and 0.5% Nb2O5, with 0.34% HREO. Drilling results expected early Nov „10. The Mount Muambe Project (REE-Fluorite) could be drilled in 4Q10 – surface sampling and re-sampling in 3Q10 turned up high REE values (peak >1.2% TREO) with av. 50% HREO/TREO in fluorite samples, including 168ppm dysprosium (a high-value element). Investment Comment: GBE‟s share price has benefitted from the jump in REE prices in 3Q10. Our NAV for the company is A$315m, or A$1.78/share based on funding 50% of capex at A$1.00/share. The sale of 51% to ECE for A$41m at A$0.375/share moves this NAV to A$0.59/share, close to the 4Q07 high of +A$0.60/share and a reasonable target, subject to ECE‟s investment and a successful BFS.

Resource Capital Research

Rare and Minor Metals Company Review, December Q 2010. Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 14

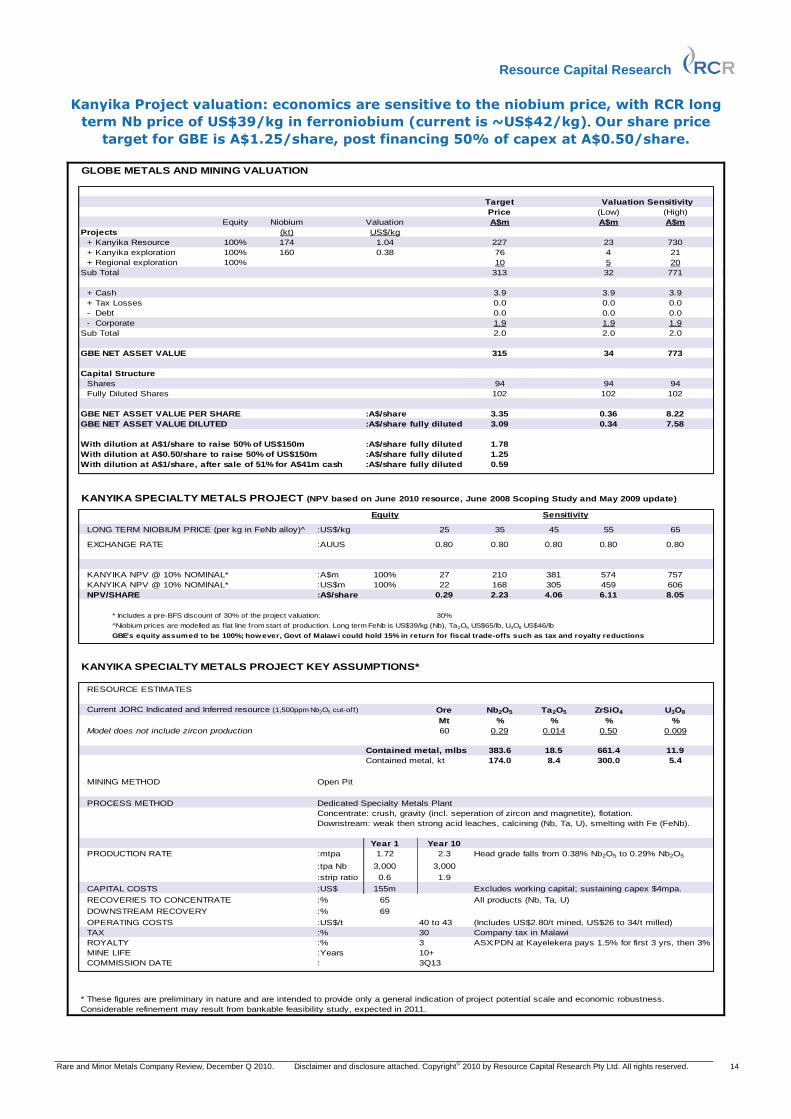

Kanyika Project valuation: economics are sensitive to the niobium price, with RCR long

term Nb price of US$39/kg in ferroniobium (current is ~US$42/kg). Our share price

target for GBE is A$1.25/share, post financing 50% of capex at A$0.50/share.

GLOBE METALS AND MINING VALUATION

Target

Price (Low) (High)

Equity Niobium Valuation A$m A$m A$m

Projects (kt) US$/kg

+ Kanyika Resource 100% 174 1.04 227 23 730

+ Kanyika exploration 100% 160 0.38 76 4 21

+ Regional exploration 100% 10 5 20

Sub Total 313 32 771

+ Cash 3.9 3.9 3.9

+ Tax Losses 0.0 0.0 0.0

- Debt 0.0 0.0 0.0

- Corporate 1.9 1.9 1.9

Sub Total 2.0 2.0 2.0

GBE NET ASSET VALUE 315 34 773

Capital Structure

Shares 94 94 94

Fully Diluted Shares 102 102 102

GBE NET ASSET VALUE PER SHARE :A$/share 3.35 0.36 8.22

GBE NET ASSET VALUE DILUTED :A$/share fully diluted 3.09 0.34 7.58

With dilution at A$1/share to raise 50% of US$150m :A$/share fully diluted 1.78

With dilution at A$0.50/share to raise 50% of US$150m :A$/share fully diluted 1.25

With dilution at A$1/share, after sale of 51% for A$41m cash :A$/share fully diluted 0.59

KANYIKA SPECIALTY METALS PROJECT (NPV based on June 2010 resource, June 2008 Scoping Study and May 2009 update)

Equity

LONG TERM NIOBIUM PRICE (per kg in FeNb alloy)^ :US$/kg 25 35 45 55 65

EXCHANGE RATE :AUUS 0.80 0.80 0.80 0.80 0.80

KANYIKA NPV @ 10% NOMINAL* :A$m 100% 27 210 381 574 757

KANYIKA NPV @ 10% NOMINAL* :US$m 100% 22 168 305 459 606

NPV/SHARE :A$/share 0.29 2.23 4.06 6.11 8.05

* Includes a pre-BFS discount of 30% of the project valuation: 30%

^Niobium prices are modelled as f lat line from start of production. Long term FeNb is US$39/kg (Nb), Ta2O5 US$65/lb, U3O8 US$46/lb

GBE's equity assumed to be 100%; however, Govt of Malawi could hold 15% in return for fiscal trade-offs such as tax and royalty reductions

KANYIKA SPECIALTY METALS PROJECT KEY ASSUMPTIONS*

RESOURCE ESTIMATES

Current JORC Indicated and Inferred resource (1,500ppm Nb2O5 cut-off) Ore Nb2O5 Ta2O5 ZrSiO4 U3O8

Mt % % % %

Model does not include zircon production 60 0.29 0.014 0.50 0.009

Contained metal, mlbs 383.6 18.5 661.4 11.9

Contained metal, kt 174.0 8.4 300.0 5.4

MINING METHOD Open Pit

PROCESS METHOD Dedicated Specialty Metals Plant

Concentrate: crush, gravity (incl. seperation of zircon and magnetite), flotation.

Downstream: weak then strong acid leaches, calcining (Nb, Ta, U), smelting with Fe (FeNb).

Year 1 Year 10

PRODUCTION RATE :mtpa 1.72 2.3 Head grade falls from 0.38% Nb2O5 to 0.29% Nb2O5

:tpa Nb 3,000 3,000

:strip ratio 0.6 1.9

CAPITAL COSTS :US$ 155m Excludes working capital; sustaining capex $4mpa.

RECOVERIES TO CONCENTRATE :% 65 All products (Nb, Ta, U)

DOWNSTREAM RECOVERY :% 69

OPERATING COSTS :US$/t 40 to 43 (Includes US$2.80/t mined, US$26 to 34/t milled)

TAX :% 30 Company tax in Malawi

ROYALTY :% 3 ASX:PDN at Kayelekera pays 1.5% for first 3 yrs, then 3%

MINE LIFE :Years 10+

COMMISSION DATE : 3Q13

Valuation Sensitivity

Sensitivity

* These figures are preliminary in nature and are intended to provide only a general indication of project potential scale and economic robustness.

Considerable refinement may result from bankable feasibility study, expected in 2011.

Resource Capital Research

Rare and Minor Metals Review, 4Q10 Disclaimer and disclosure attached. Copyright© 2010 by Resource Capital Research Pty Ltd. All rights reserved. 1

1.10

Debt (A$m) - Dec 10F

Enterprise value (A$m)

Avg monthly volume (m)

Cash (A$m) - Dec 10F

Price/Cash (x) Cash (A$m)

Price/Book (x)

Listed company options: Net asset backing (Ac/share)

* Uranium prospective properties only.

Mineralised Material (est., non compliant w ith JORC)

Contacts Directors

Mr Roderick McIllree M Hutchinson (Chair)

Managing Director

Tel: 61 (0) 8 9226 1100 S Cato (Exec Dir)

West Perth, WA, Australia J Whybrow (Expl Dir)

Analyst: Dr Trent Allen

T Ho (Non-Exec)www.ggg.gl

10.5

Uranium

Code for reporting mineral resources - Australian:

0.0

na

Key Projects

20.9

Investment Points

3.7

GGGO

R McIllree (MD)

Reserves

Type Location

Target

Multi-element focus at Kvanefjeld - uranium component

valued in-ground (4Q10) at ~US$17.5 billion (US$62/lb)

and REE at ~US$146 billion (US$30/kg).

Potential to be one of the world's largest REE and U

deposits - plus economic potential NaF, Zn and Sn.

Resource includes 283mlbs U3O8, 4.9mt REO, 1mt Zn

and 3.1mt NaF- defined over 2km x 1km; open at depth

(>300m) and along strike, regional prospectivity is high.

Metallurgical studies are advanced: process flow sheet

includes alkaline/carbonate pressure leach for uranium,

and separate flotation and leach for REO.

Pre-feasibility study, Feb '10: processing 10.8mtpa for 23

years, producing 43.7ktpa REO and 8.6mlbspa U3O8 .

Capex is US$2.31bn, opex US$41/t. NPV US$2.18bn.

Greenland Government has amended exploration licence

structure to allow for investigation of uranium, signalling

willingness to consider allowing uranium mining.

Indicated, inferred

Project

150

0.0

Route

61%/100%

Partner

Resources

Kvanefjeld*

Project

0.0

Kvanefjeld Advanced Expl

Ownership/

Option Status

JV

U, REO

Metal

Greenland

457 1.0761%

IgneousWestrip

%Mt

Process

Classification

0

*Also uranium (283mlbs contained @ 0.028%), Zn (0.99mt contained @ 0.22%) and NaF (3.09mt contained @ 0.85% NaF).

0.0

10,780

ppm

U3O8

1.6

10.5

3.4

7.6

31.9

(JORC)

Reserves and Resources/Mineralised Material

TREOCut OffOre

0.71

-

211

Cash backing (Ac/share)

211

Funding from JV partners (A$m)

TREO

0

3.9

6.3 10.5

21.9

Project

2.5

1

211

2011F

32.2

7.6

20.5

5.40

6.00

58

Company Comment

424.3

2.8

Sep-10a 2009aDec-10FYear End: December

Land holding ('000 ha)

13.2

7,000 4,000

0

Greenland Minerals and Energy Ltd

1.10

Funding duration at current burn (years)

-

6.8

JP Morgan Nom (15.9%), HSBC Nom (7.6%), Westrip Hold. (6.9%)

22 November 2010

Exchanges: ASX:GGG

0.31 to

Share price (A$) 0.82

Convertible notes (m) 0.0

52 week range (A$/share)

GGG.AU

Rare Earth Elements, Uranium, Zinc, Sodium Fluoride

Greenland

Pre-Feasibility Study

Production and Financial Forecasts Capital Profile

A 33% one-month gain for GGG is due to a buoyant REE market,

and Greenland allowing uranium to be included in economic

assessment of the Kvanefjeld Project (forecast REE 43.7kt/yr,

U3O8 3.9kt/yr). Share price target A$1.46 with considerable upside.

61

211

-

Capital raisings (A$m)

Tenement costs ($k per year)

39

270.4

0

270.4 226.8

211

0

Market capitalisation (undiluted) (A$m)

Major shareholders: Citicorp Nom (16.7%), National Nom (16.7%),

220.4

220.4

1,000

0

1,000

21.9

3.9

2

21.6 20.7

0

-

6.06.1

2.63

Exploration/(Expl.+ Corporate) (%)

Corporate (A$m)

31

1.65

424.3

250.5

Drilling - Other/Diamond (m)

Drilling - RAB (m)

10.47 6.64

0

56

5.28

0.9

6

65

153.9

Number of shares (m) 270.4 Exploration and evaluation (A$m)

Options and warrants (m)

U3O8

Fully diluted (m)

Shares on issue (pr end) (m shares)

0.0

4,000

Equity

0.0

-

Kt Kt

A$ 0.82

Mlb

TREO Eqty

2010F

2,983

TREO

4,890

0.0

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Nov-

09

Dec-

09

Jan-1

0

Mar-

10

Apr-

10

May-

10

Jun-1

0

Aug-1

0

Sep-1

0

Oct-10

Sh

are

Pri

ce

($/S

hare

)

GGG - Greenland Minerals and Energy Limited

Source: Bloomberg

Overview: Greenland Minerals and Energy Limited listed on the ASX in June 2006 (ASX:GGG). It is evaluating the uranium-rich Kvanefjeld multi-element project in Greenland. Kvanefjeld (uranium, Greenland): The project (80km

2) is located on the SW tip of Greenland, at