Rakesh Dogra NBFC

16

Strategy, Development & Growth Name: Rakesh Kumar Dogra Contact No: Email: N B F C

-

Upload

rakesh-dogra -

Category

Documents

-

view

14 -

download

0

Transcript of Rakesh Dogra NBFC

Strategy, Development & Growth Name: Rakesh Kumar DograContact No: Email:

N B F C

Market ScenarioMarket Scenario Interested members seeking loan are required to submit

prescribed application form duly filled in along with all supporting documents attached.

Unsecured loans (loans and bill purchase within the limit prescribed by Company)

Secured Loans (within the max. limit wherever prescribed by Company)1) Transport, Business, DCG, Plant and Machinery loans2) Gold Loans 3) Loans against KVP4) General loan-(Loan against property) 5) Car Loan

Loan sanctioning authoritiesi) Companyii) Credit Manageriii) CM will sanction loans up to the power delegated by the Company

2

Target MarketsTarget Markets Present and prospective owners of shops/ offices/

show-rooms/ training centres/ service centres/ garages/ offices for Chartered Accountants/ Consultants for the purchase / refurbishment of the existing property

General / Grocery stores Government Employees with salary of 10K to 30K. Micro enterprises including SSI units, small business enterprises,

professional and self employed persons, small retail traders, transport operators etc for meeting any kind of credit requirement including purchase of shops, maximum limit being Rs 10 lakhs including term loan & working capital loan. The loan will be sanctioned for 3 years with an annual review. This product will simplify sanction process without requirement of elaborate

financial data.3

Target MarketsTarget Markets Used cars Loan Loans for purchase of cars, passenger jeeps, multi utility

vehicles etc., to his name as per the choice of the customer.

Electronic Dealer Finance Scheme The scheme provides for financing purchases of product to

consumer that is customer to Shop Keepers from Dealers to Corporate /Industry Majors.

It is a completely web based solution with customized MIS provided to the stakeholders. The Industry Major enjoys timely availability of funds. The Shop Keepers / dealer can make effective utilization on working capital funds. Both Industry Major and dealer can make use of improved cash flow forecasting

4

Target MarketsTarget Markets Loan against NSC/KVP/IVP

Up to 75% of the face value in case of NSC/KVP/IVP and in the case of

LIC policy 75% of the surrender value.

Normally general loan (unsecured loan) for ceremonial,

consumption and other domestic purposes against

security of another member is given up to maximum Rs.

2/- lacs on the basis of income parameters. However, such

type of loans up to maximum Rs. 10/- lacs can be

considered as General Loan – Secured against the

mortgage of property and repaying capacity. The security

percentage of the mortgaged property will be taken as per

the rules framed by the Company from time to time.5

Business PlansBusiness Plans Marketing Activity and Demographic study Events Management and Training Miscellaneous Promotional Activities

a) Flyerb) Advertisement (Space marketing)c) Classifiedd) Sales and Product Supporte) An Active Customer Base-To Help Drive Revenuef) Networking- Regional Meetings

Annual Convention In each micro market ; Identify and leverage new

growth opportunities such as new Area of Work Fast-growth support and optimization in order to

maximize long-term potential gains in revenue, margins, and market share ◦ Areas being adequately covered by us

6

Criteria while Sanctioning Criteria while Sanctioning Each and every loan request to be examined at three stages

◦ Branch Head / Manager / Loan Officer to provide the necessary information on the credit appraisal form along with his comments/observations. Thereafter it will be examined by Credit Manager

◦ Along with comments/observations of Branch Head / Manager / Loan Officer before placing at the Loan Sanctioning Committees. Physical verification of Shop/Stock will be done by….or any other official.

◦ The maximum credit limit of a member will be determined by the Company as per the guidelines after finalization of the…….

Processing charges will be taken as per the rates decided by the Company from time to time which will also be conveyed to the loanee member in advance.

7

Recovery / DefaultRecovery / Default If any Loan Default by Member. We need two Member's as

a guarantee. In case of default, surety or guarantee Member will be equally liable for the re-payment of his or her dues

In case of default the following actions can be taken against the defaulting member: To write to the employer u/s 52 Act 2003 for the recovery of the dues. To initiate arbitration proceedings To file case under section 138 of Negotiable Instruments Act To file case under SARFAESI Act

These actions should be taken as per the guidelines laid in the recovery policy.

8

Rate Of InterestRate Of Interest The rate of interest on all loans / credit facilities will be on

reducing rate basis which is decided by the Company from time to time. The change in the rate of interest is applicable for fresh loans disbursed from its effective date and will not be applicable for loans disbursed earlier.

The repayment of loan will be accepted through deposit of post dated cheques and submission of mandate for electronic clearance transfer services (ECS) which will be handed over to officer at the time of disbursement of loan.

However, repayment of loan can also be accepted in cash or pay order or demand draft if situation so warrants.

9

Product KnowledgeProduct Knowledge Surety loan eligibility on completion of one month

membership. ◦ One month up to one year maximum surety loan entitlement up to Rs. 1/-

Lacs.◦ Above one year maximum surety loan entitlement up to Rs. 2/- Lacs. and

that will be change time to time. Unsecured (Surety ) loan

◦ Up to Rs. maximum 2,00,000/- Eligibility criteria : When no other loan has been taken:

◦ 10 times of take home salary (two latest salary slips required in case of salaried persons)

◦ 8 times of ITR income – (Two latest ITRs to be submitted)◦ Where ITR or proper salary certificates are not provided – max. 7 times of the

declared income subject to max. Rs.1,00,000/- for the first time and up to max. Rs. 1,25,000/- from 2nd time onwards subject to the condition that the member has not taken any other loan and he has been a good paymaster.

Surety for unsecured loan above Rs. 1,00,000/- invariably from a member in govt. service or from a member having residential house on his/her own name or on the name of spouse or two house owner regular paymaster sureties.

10

Product KnowledgeProduct Knowledge When a member does not have residential house on his

own name or on the name of his spouse but the house is owned by father, mother, son, brother, father-in-law, mother-in-law in case of lady member and the member lives with them in the same house then the surety stood by such a member will be treated as a house owner surety.

The following types of secured loans can be considered :

Consumer Durables Loan for consumer durables such as Computers, TV, Fridge, Mobile,

AC etc up to 80% of the cost or Rs. 1,00,000/- whichever is less. Loan amount to be disbursed direct to the vendor/supplier after taking the margin money. Advance payment will not be allowed.

Loan will be recovered in 6/12/24/36 equal monthly instalments. Minimum one surety from a regular paymaster member of the services is required. Item to be purchased will remain hypothecated to the. 5% of the loan is taken as security for giving post loan disbursement papers. This amount on request will be returned immediately on receipt of papers.

11

Product KnowledgeProduct Knowledge Vehicle Loans

Up to 100% of the ex-showroom price of the new vehicle. Minimum one surety from a regular paymaster member of the Bank.

Loan will be paid direct to the vendor/supplier/dealer. The loan will be considered on the Performa invoice in favour of the member. Margin money and loan processing charges will be taken. Name of the bank will be written on the RC and the vehicle will be insured jointly with the bank during the continuation of the loan. If the name of the vehicle could not be written on RC, disclaimer certificate should be obtained from the transport authority.

For new LMV the maximum repayment period will be 36 EMI EMIs. However, for new vehicle for personal use the repayment

period can be extended up to 60 EMIs on the request of the member. Security – Hypothecation of vehicle in favour of the

Company. While considering request for transport loans, repaying

capacity is not considered presuming that income will be generated only after the purchase of vehicle. If the member applies for any term loan after taking transport loans, then for calculating repaying capacity for the requested term loan EMIs being paid for the existing transport loans will be taken into consideration.

12

Product KnowledgeProduct Knowledge Loan for plant and machinery

◦ If the loan is needed for the purchase of new machinery, Performa invoice to be provided and loan limit will be up to 70% of the cost or Rs. 2/- lacs whichever is less without collateral security but with one or two house owner/govt. surety(ies). Above Rs. 2/- lacs with collateral security of property duly evaluated from the approved valuer and with search report from the advocate on the approved panel.

◦ In case of old machinery the valuation of machinery from the approved valuer required. The loan limit for old machinery shall be maximum 50% of its value. For loans up to Rs. 2/- lacs security will be hypothecation and joint insurance of machinery and personal surety. For old plant and machinery security will be hypothecation of machinery and mortgage of property. Joint insurance of machinery and property required separately and both jointly with the Company.

13

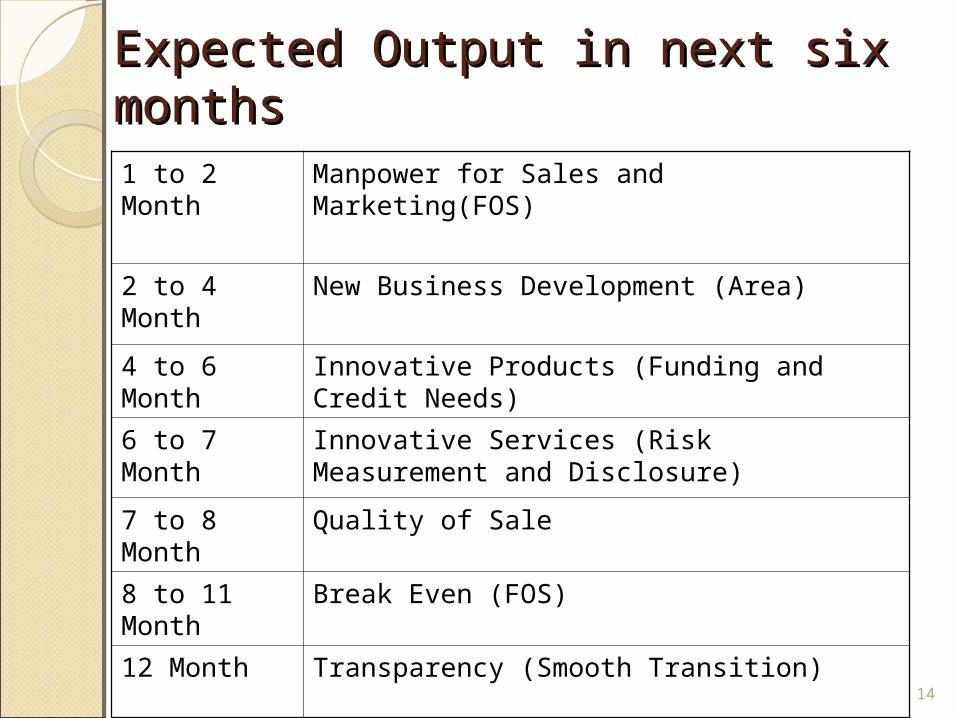

Expected Output in next six Expected Output in next six monthsmonths

14

1 to 2 Month Manpower for Sales and Marketing(FOS)

2 to 4 Month New Business Development (Area)

4 to 6 Month Innovative Products (Funding and Credit Needs)

6 to 7 Month Innovative Services (Risk Measurement and Disclosure)

7 to 8 Month Quality of Sale

8 to 11 Month

Break Even (FOS)

12 Month Transparency (Smooth Transition)

15

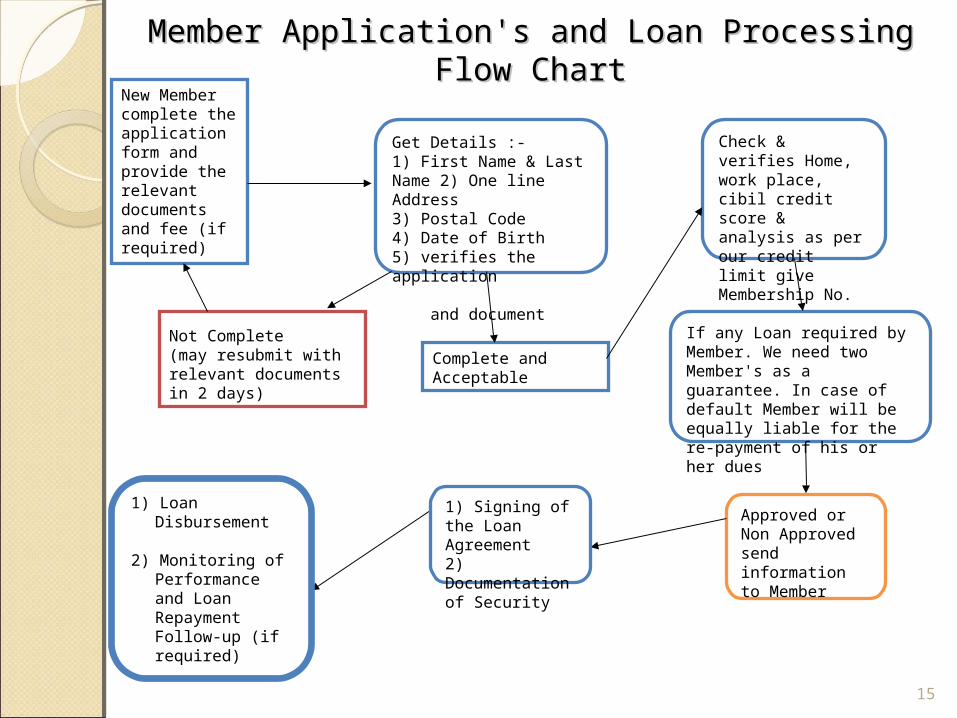

New Member complete the application form and provide the relevant documents and fee (if required)

Get Details :- 1) First Name & Last Name 2) One line Address 3) Postal Code 4) Date of Birth 5) verifies the application and document

Not Complete(may resubmit with relevant documents in 2 days)

Check & verifies Home, work place, cibil credit score & analysis as per our credit limit give Membership No.

Complete and Acceptable

Approved or Non Approved send information to Member

1) Signing of the Loan Agreement2) Documentation of Security

1) Loan Disbursement

2) Monitoring of Performance and Loan Repayment Follow-up (if required)

If any Loan required by Member. We need two Member's as a guarantee. In case of default Member will be equally liable for the re-payment of his or her dues

Member Application's and Loan Processing Flow Member Application's and Loan Processing Flow ChartChart

Thank YouThank You

16

BY RAKESH KUMAR DOGRA