R. DHAWAN Jan 1411

26

Is Federal Reserve Bank Policy Working in the US? DR. RAJEEV DHAWAN Director, Economic Forecasting Center Georgia State University Presented at the Global Interdependence Center’s Meeting at the Central Bank of Chile in Santiago • January 17, 2011

-

Upload

global-interdependence-center -

Category

Documents

-

view

227 -

download

1

description

DR. RAJEEV DHAWAN Director, Economic Forecasting Center Georgia State University Presented at the Global Interdependence Center’s Meeting at the Central Bank of Chile in Santiago • January 17, 2011 AGENDA 1. Define the latest Federal Reserve Bank policy aka Quantitative Easing 2. Effectiveness metrics 3. Impediments to boosting aggregate demand; what creates job growth? 4. Ability and willingness of commercial banks to make loans to businesses (especially to small firms) 5. Concluding remarks

Transcript of R. DHAWAN Jan 1411

Is Federal Reserve Bank Policy

Working in the US?DR. RAJEEV DHAWAN

Director,

Economic Forecasting Center

Georgia State University

Presented at the Global Interdependence Center’s Meeting at the

Central Bank of Chile in Santiago • January 17, 2011

1. Define the latest Federal Reserve Bank policy aka Quantitative Easing

2. Effectiveness metrics

3. Impediments to boosting aggregate demand; what creates job growth?

4. Ability and willingness of commercial banks to make loans to businesses (especially to small firms)

5. Concluding remarks

AGENDA

• Quantitative Easing refers to changes in the composition and/or size of a central bank’s balance sheet that are designed to ease liquidity and/or credit constraints (Blinder 2010)

• The central bank hopes that by reducing interest rate spreads/risk premiums the central bank can boost aggregate demand even at the zero lower bound for the policy interest rate

Quantitative Easing: The Second Round (QE2)

Jim Bullard’s Fear and Solution

The FOMC’s “extended period” language may be increasing the probability of a Japanese-style outcome for the United States.

…on balance, the U.S. quantitative easing program offers the best tool to avoid such an outcome.

Source : James Bullard, “Seven Faces of “the Peril”, September/October 2010

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82

US Deflator (starting in 2000)

Japan Deflator (starting in 1990)

(%, PCHYA)

U.S. Inflation Compared to Japan

FOMC’s December Statement

Source: FOMC statement & FRB of NY, November 3, 2010

To promote a stronger pace of economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate…. The Committee…. intends to purchase a further $600 billion of longer-term Treasury securities by the end of the second quarter of 2011.

QE2’s Effectiveness:

Inflation, Spreads

& Side Effects

JANOCTJULAPRJANOCTJULAPRJANOCTJULAPRJANOCTJULAPRJANOCTJULAPRJAN

201120102009200820072006

4

3

2

1

0

-1

(%)

Expected vs. Actual Inflation

10-Y Bon d Ra t e Less T IPS Ra t e

Core In fla t ion (3-m ont h A n n . Growt h )

DECJULFEBSEPAPRNOVJUNJANAUGMAROCT

20102009200820072006

12

10

8

6

4

2

0

(%)

Risk Premium in Investment Grade BondsBB+ Corporate v s. 10-Year T-Bond

JANDECNOVOCTSEPAUG20112010

12000

11500

11000

10500

10000

9500

1450

1400

1350

1300

1250

1200

1150

($/Troy ounce)

Stock Market and Gold

DOW30 (Left) Gol d (Ri ght)

Instead of Flattening

the Yield Curve

has steepened

JANDECNOV

20112010

1.50

1.40

1.30

1.20

1.10

1.00

0.90

(%)

Long-Term Rates: Germany vs. Japan vs. US vs. UK

German 10-Y Bond UK 10-Y Bond

US 10-Y Bond Japanese 10-Y Bond

NOVSEPJULMAYMARJANNOVSEPJULMAYMARJAN

20102009

-20

-25

-30

-35

-40

-45

-50

-55

($ bil.)

Trade Balance

Source: May 2005, Forecast of the Nation, EFC@GSU

10-Year Bond Regression

10-Year Bond Rate and Trade Deficit

20102009200820072006200520042003200220012000

120

110

100

90

80

70

(Index 2000 = 100)

US Trade Weighted Currency Index

Emerging Currencies

Major Currencies

Impediments to

Boosting Aggregate

Demand

DECAUGAPRDECAUGAPRDECAUGAPRDECAUGAPRDECAUGAPR

20102009200820072006

120

100

80

60

40

20

16000

14000

12000

10000

8000

6000

(Index 1966 = 100)

Consumer Confidence and Stock Market Wealth

Consu m er Confiden ce (Left ) Wilsh ire 5000 (Righ t )20102009200820072006200520042003200220012000199919981997

200

180

160

140

120

100

80

Hom e Prices: Case-Shiller National Average

Home Price Expectations Survey

Source: MaroMarkets Home Price Expectations Survey, December 2010

EFC

Median

Low

High

Employment Recovery

So What

Creates Jobs?

2010200820062004200220001998199619941992199019881986198419821980

5.0

4.5

4.0

3.5

3.0

2.5

2.0

(%)

Investment in Tech Equipment andSoftware as a % of GDP

Golden 90’s

Job Growth:

240K/Month

2003-2007

Job Growth:

132K/Month

12%

6%

-15%2008-2009

Job Loss:

400K/Month

+19%

2010 YTD:

87K/Month

Rajeev DhawanProfessor & DirectorEconomic Forecasting CenterGeorgia State University

Harold Vasquez Research Specialist

Economic Forecasting CenterGeorgia State University

Source: “U.S. Employment Growth and Tech Investment: A New Link” By Rajeev Dhawan & Harold Vasquez, 2010

The improvements in CEO’s perceptions about the future increases TECH investment spending.

TECH investment significantly increases employment growth via durable goods ORDERS channel.

Employment growth

(Job additions)

CEO:1% CEO 0.034% TECH

1% CEO 0.11% ORDERS

TECH:

1% TECH 0.059% EMP:

ORDERS:1% ORDERS 0.45% TECH

Job Growth and Tech Investment

IVIIIVIIIVIIIVIIIVIIIVIIIVIIIVIIIVIIIVIIIVIIIVII201020092008200720062005200420032002200120001999

70

60

50

40

30

20

10

0

-10

-20

-30

-40

(%, Y -O-Y )

Chief Executive Confidence & Durable Goods OrdersExpectati ons of Busi ness Condi ti ons i n Own Industry 6 Months Ahead

CEO Confi dence (Left) Durabl e Goods Orders Growth (Ri ght)

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2500

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2001 2002 2003 2004 2005 2006 2007 2008 09q1 09q2 09q3 09q4 10q1 10q2 10q3

DOW 30 (Left) Private Job Gains (Right)

(‘000 Jobs)(%, Y-O-Y)

Dow30 Revenue Growth and Job Gains

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

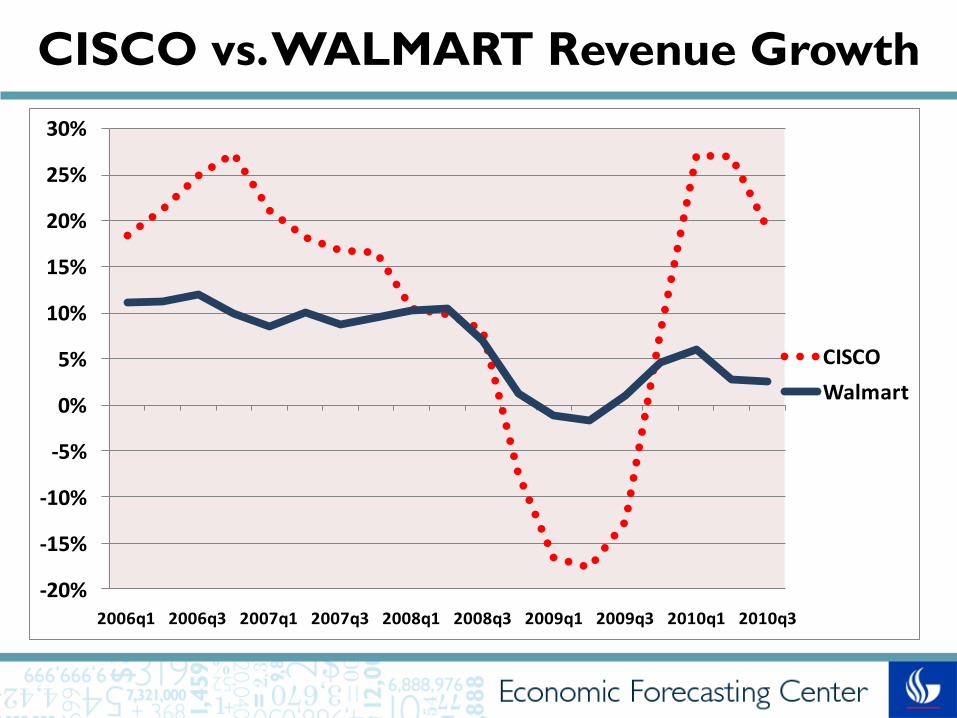

2006q1 2006q3 2007q1 2007q3 2008q1 2008q3 2009q1 2009q3 2010q1 2010q3

CISCO

Walmart

CISCO vs. WALMART Revenue Growth

WALMART CEO Mike Duke

Source: Bloomberg Businessweek, December 6, 2010

Three issues that we often talk about: tax, trade, and health care.

But What About the

Ability/Willingness

of Banks to Lend?

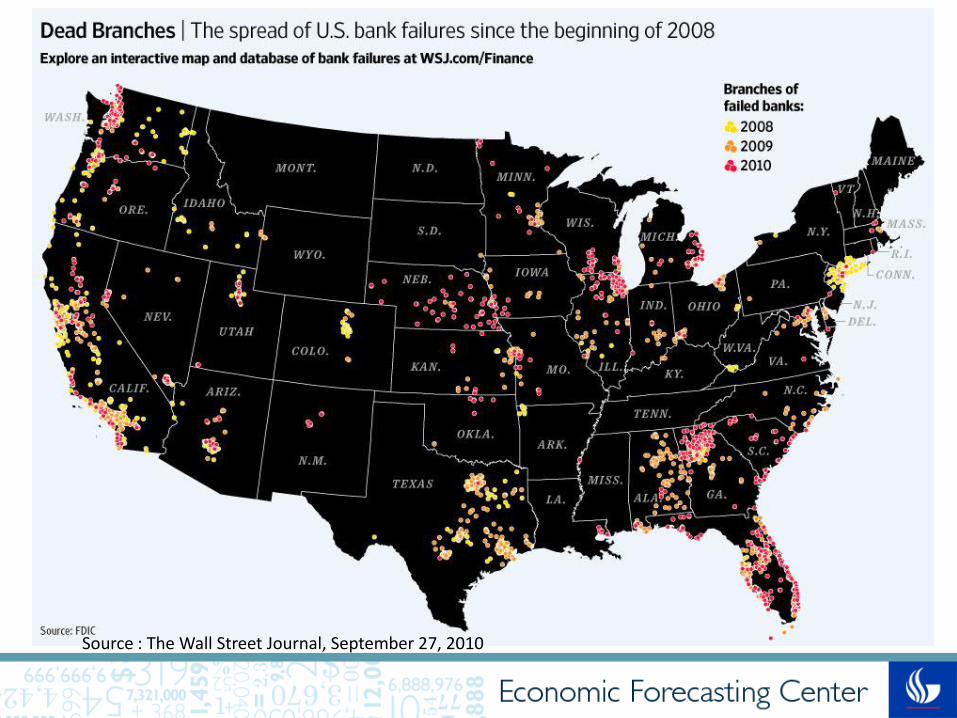

Source : The Wall Street Journal, September 27, 2010

DECOCTAUGJUNAPRFEBDECOCTAUGJUNAPRFEBDECOCTAUG

201020092008

1200

1000

800

600

400

200

0

-200

($ Bil.)

Excess Reserves of Depository Institutions

an “overhang” of impaired banks that may be

forced to sell soon can reduce the current price of illiquid securities sufficiently that banks have no interest in selling. This

creates high expected returns to holding cash for potential buyers and an aversion to making term loans.

Source: NBER working paper #14925, April 2009

Douglas Diamond Professor of FinanceUniversity of Chicago

Raghuram Rajan Professor of Finance

University of Chicago

Fear of Fire Sales and

the Credit Freeze

• Job growth is a function of “tech” investment that in turn is dependent upon confidence levels (CEO’s and consumers)

• Can a central bank do anything here? • Not directly, but by easing the flow of credit it

can help small firms that are primarily bank finance dependent

• How to do it? • Clean up the toxic debt by using the QE power

(Explore setting up a Resolution Trust Corporation as in early 90’s? Reviving Treasury’s PPIP?)

Food-For-Thought

Special Thanks to the Center’s

Carl R. ZwernerChair of Family

Owned Businesses

Executive Sponsors

Sponsors