Questerre Energy Corporation CorporatePresentation Pareto Oil & Offshore Conference September 10-11,...

33

Questerre Questerre Energy Energy Corporation Corporation Corporate Corporate Presentation Presentation Pareto Oil & Offshore Pareto Oil & Offshore Conference Conference September 10-11, 2008 September 10-11, 2008

-

date post

18-Dec-2015 -

Category

Documents

-

view

216 -

download

1

Transcript of Questerre Energy Corporation CorporatePresentation Pareto Oil & Offshore Conference September 10-11,...

Questerre Questerre Energy Energy

CorporationCorporation

CorporateCorporatePresentationPresentation

Pareto Oil & Offshore Pareto Oil & Offshore ConferenceConference

September 10-11, 2008September 10-11, 2008

Forward Looking StatementForward Looking Statement

This presentation contains forward-looking information. Implicit in this information are assumptions regarding oil and natural gas prices,

production, royalties and expenses that, although considered reasonable by Questerre at the time of preparation, may prove to be incorrect. These

forward-looking statements are based on certain assumptions that involve a number of risks and uncertainties and are not guarantees of future

performance. Actual results could differ materially as a result of changes in Questerre’s plans, changes in commodity prices, general economic, market, regulatory and business conditions as well as production, development and

operating performance and other risks associated with oil and gas operations.

There is no guarantee by Questerre that actual results achieved will be the same as those forecast herein. Estimated values in this presentation do not

represent fair market value.

Presentation OutlinePresentation Outline

• Company Overview

– Business plan & asset overview– Management & Board– Capitalization – Second quarter results

• Area Overview

– St. Lawrence Lowlands, Quebec– Northeast British Columbia– Antler

• Outlook

– Near term goals– Investment summary

Business StrategyBusiness Strategy

Superior risk/reward in the Canadian frontier

“Big gas and big markets”

Buy early• Acquire significant land positions in overlooked or

underdeveloped areas

Add value• Leverage technical expertise to “understand the rocks” and

high grade land positions

Reduce risk• Farm-out to partners and create a diversified portfolio of

upsides

Create shareholder value• Prove up reserves and production

Successes to DateSuccesses to Date

• Major new shale gas discovery in Quebec

• Additional exploration targets in Quebec being evaluated in 2008/2009

• Partnerships with several seniors including Talisman, EnCana and Forest Oil

• Company value enhanced by current production of over 1,300 boe per day

Asset OverviewAsset Overview

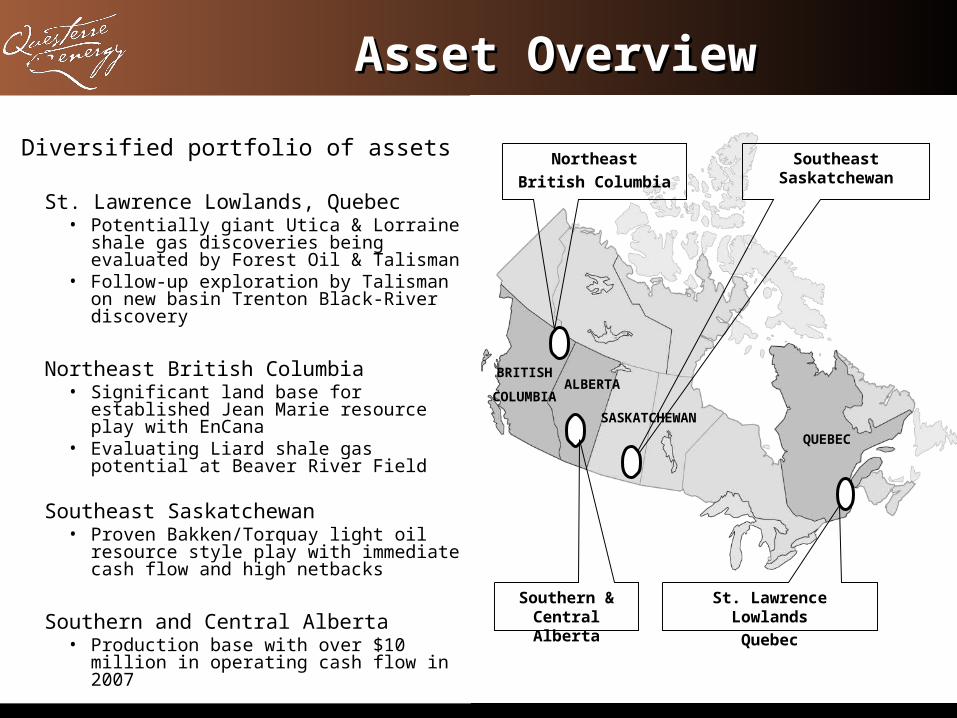

Diversified portfolio of assets

St. Lawrence Lowlands, Quebec• Potentially giant Utica & Lorraine shale

gas discoveries being evaluated by Forest Oil & Talisman

• Follow-up exploration by Talisman on new basin Trenton Black-River discovery

Northeast British Columbia• Significant land base for established

Jean Marie resource play with EnCana• Evaluating Liard shale gas potential at

Beaver River Field

Southeast Saskatchewan• Proven Bakken/Torquay light oil

resource style play with immediate cash flow and high netbacks

Southern and Central Alberta• Production base with over $10 million

in operating cash flow in 2007

St. Lawrence LowlandsQuebec

Southern & Central Alberta

QUEBEC

ALBERTA

NortheastBritish Columbia

Southeast Saskatchewan

BRITISH

COLUMBIA

SASKATCHEWAN

ManagementManagement

Senior multi-disciplinary team experienced in large-scale projects in the WCSB have invested together with directors $12 million

Michael Binnion, President & CEOJohn Brodylo, VP Exploration (Nexen)Peter Coldham, VP Engineering & Operations

(Chevron)Jason D’Silva, VP Finance (CanArgo, Flowing)Richard Mindus, Operations Manager (Nexen)Ian Nicholson, Manager, Alberta (Beau Canada, Kerr

McGee)Maria Rees, Corporate Secretary (CanArgo, Flowing)Rick Tityk, VP Land (Hunt Oil)

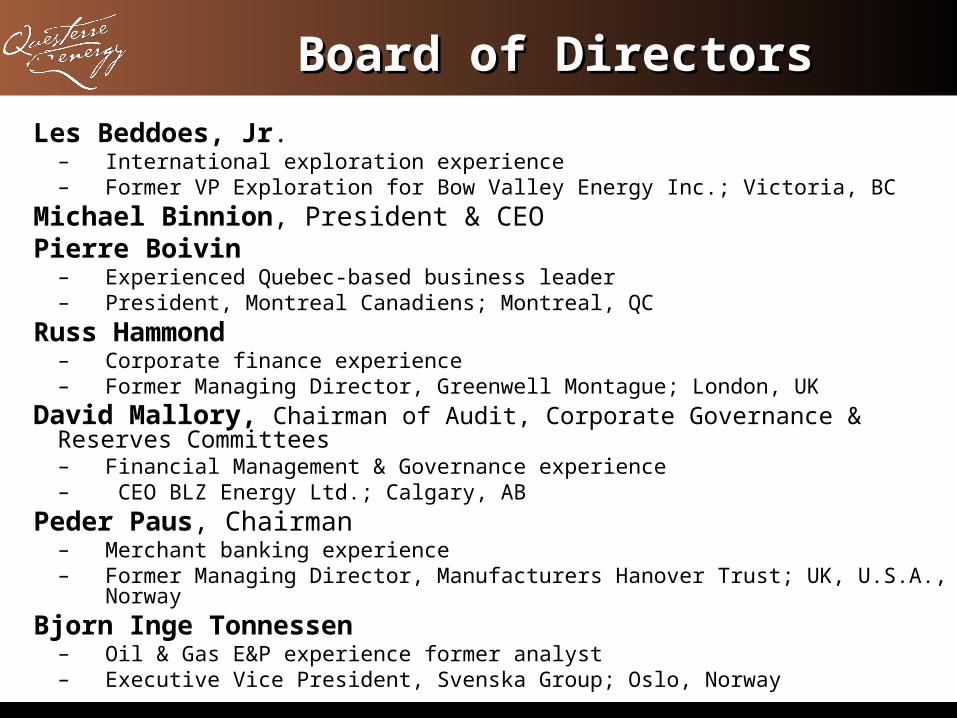

Board of DirectorsBoard of DirectorsLes Beddoes, Jr.

– International exploration experience– Former VP Exploration for Bow Valley Energy Inc.; Victoria, BC

Michael Binnion, President & CEOPierre Boivin

– Experienced Quebec-based business leader– President, Montreal Canadiens; Montreal, QC

Russ Hammond– Corporate finance experience– Former Managing Director, Greenwell Montague; London, UK

David Mallory, Chairman of Audit, Corporate Governance & Reserves Committees– Financial Management & Governance experience– CEO BLZ Energy Ltd.; Calgary, AB

Peder Paus, Chairman– Merchant banking experience– Former Managing Director, Manufacturers Hanover Trust; UK, U.S.A., Norway

Bjorn Inge Tonnessen– Oil & Gas E&P experience former analyst– Executive Vice President, Svenska Group; Oslo, Norway

CapitalizationCapitalization

Insiders 27,719,743 15%

Free Float 168,930,470 85%

Total (1) 196,650,213

Options (Average exercise price $1.21) 17,086,671

Average daily trading volume (OSE plus TSX) 8,592,007(1) Includes pending cancellation of 10,698,785 shares held by Terrenex, recently acquired by Questerre

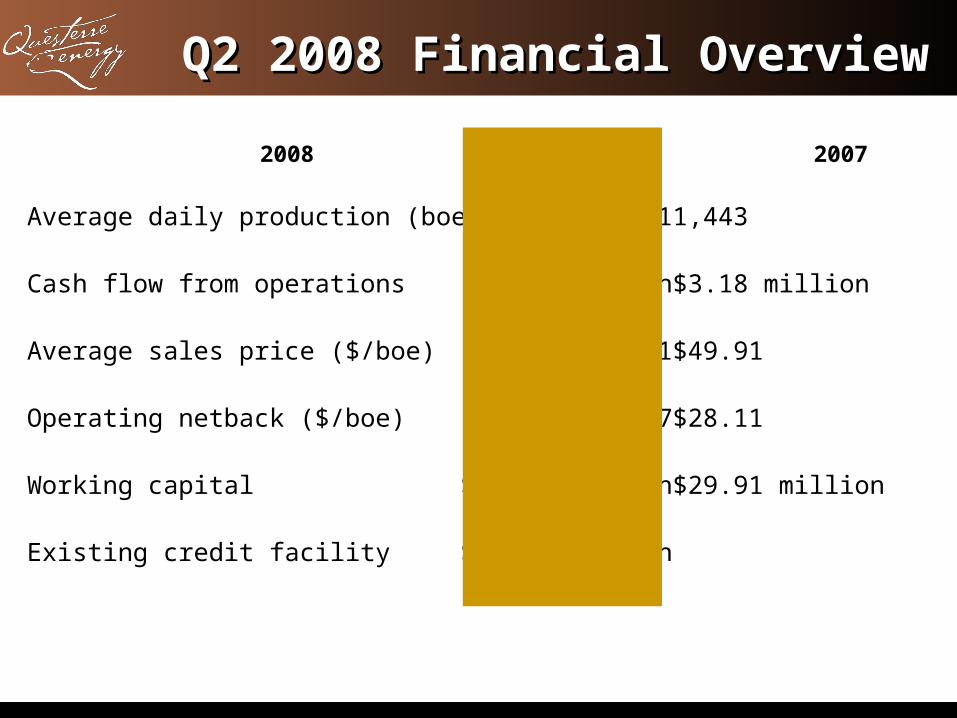

Q2 2008 Financial OverviewQ2 2008 Financial Overview

20082007

Average daily production (boe/d) 1,241 1,443

Cash flow from operations $5.14 million $3.18 million

Average sales price ($/boe) $80.01 $49.91

Operating netback ($/boe) $51.07 $28.11

Working capital $68.45 million $29.91 million

Existing credit facility $11.25 million

St. Lawrence St. Lawrence Lowlands, QuebecLowlands, Quebec

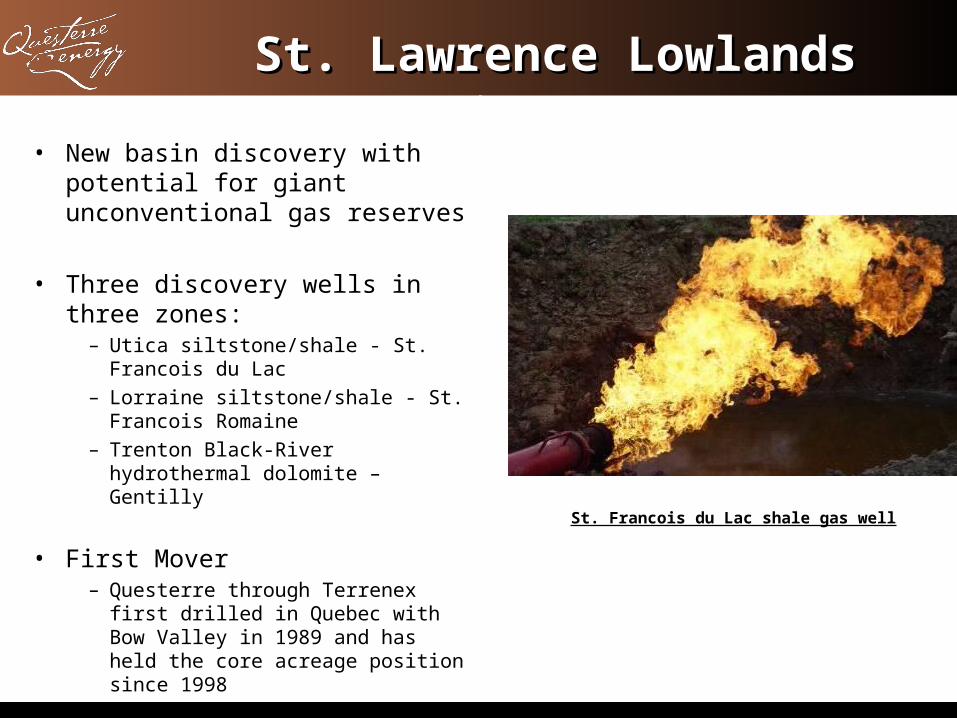

St. Lawrence LowlandsSt. Lawrence Lowlands

• New basin discovery with potential for giant unconventional gas reserves

• Three discovery wells in three zones:

– Utica siltstone/shale - St. Francois du Lac

– Lorraine siltstone/shale - St. Francois Romaine

– Trenton Black-River hydrothermal dolomite – Gentilly

• First Mover– Questerre through Terrenex first

drilled in Quebec with Bow Valley in 1989 and has held the core acreage position since 1998

St. Francois du Lac shale gas well

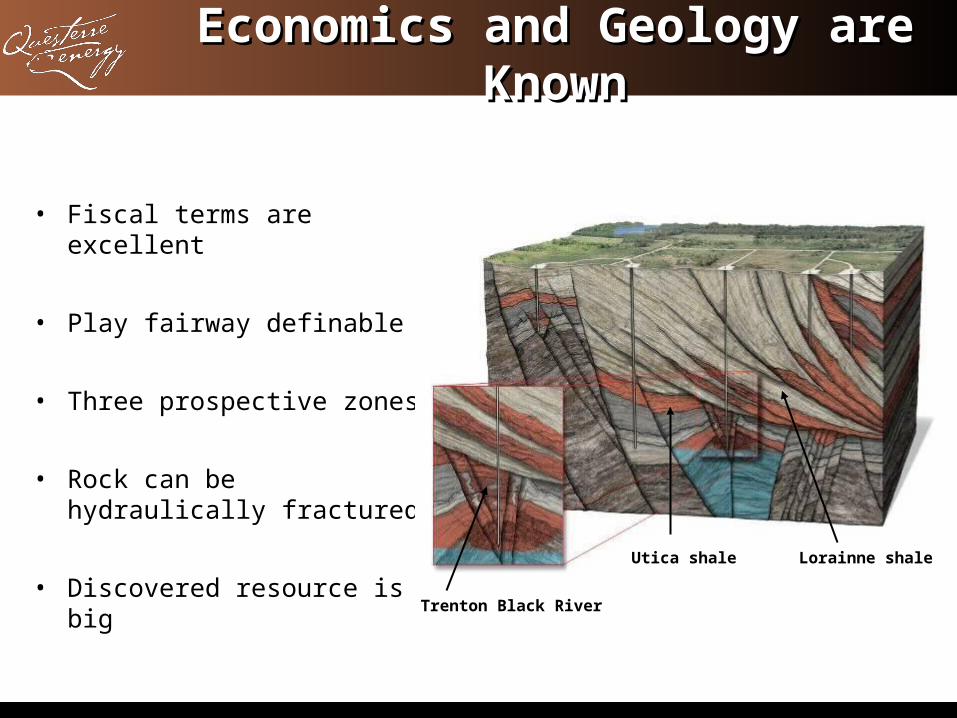

Economics and Geology are Economics and Geology are KnownKnown

• Fiscal terms are excellent

• Play fairway definable

• Three prospective zones

• Rock can be hydraulically fractured

• Discovered resource is big

Lorainne shale

Trenton Black River

Utica shale

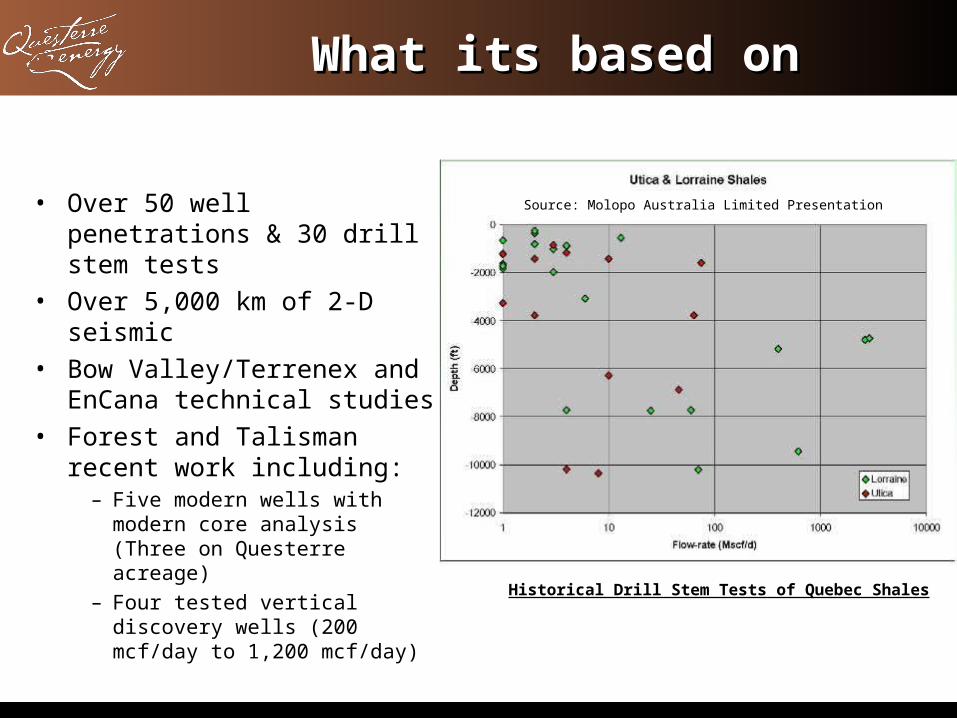

What its based onWhat its based on

• Over 50 well penetrations & 30 drill stem tests

• Over 5,000 km of 2-D seismic

• Bow Valley/Terrenex and EnCana technical studies

• Forest and Talisman recent work including:

– Five modern wells with modern core analysis (Three on Questerre acreage)

– Four tested vertical discovery wells (200 mcf/day to 1,200 mcf/day)

Source: Molopo Australia Limited Presentation

Historical Drill Stem Tests of Quebec Shales

What is being definedWhat is being defined

• Recovery per well

• Production profile from stimulated horizontal wells

• Ultimate costs on a development program basis

• Optimization techniques/strategy

Testing of Gentilly #1 Discovery well

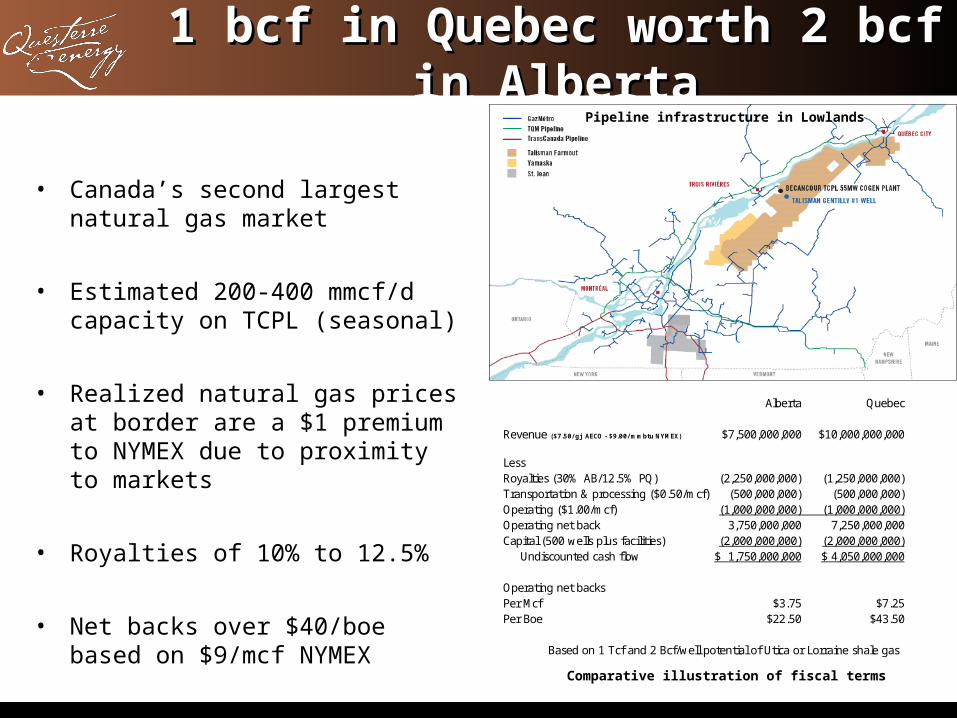

1 bcf in Quebec worth 2 bcf 1 bcf in Quebec worth 2 bcf in Albertain Alberta

• Canada’s second largest natural gas market

• Estimated 200-400 mmcf/d capacity on TCPL (seasonal)

• Realized natural gas prices at border are a $1 premium to NYMEX due to proximity to markets

• Royalties of 10% to 12.5%

• Net backs over $40/boe based on $9/mcf NYMEX

Alberta Quebec

Revenue ($7.50/ gj AECO - $9.00/ mmbtu NYMEX) $7,500,000,000 $10,000,000,000

LessRoyalties (30% AB/12.5% PQ) (2,250,000,000) (1,250,000,000)Transportation & processing ($0.50/mcf) (500,000,000) (500,000,000)Operating ($1.00/mcf) (1,000,000,000) (1,000,000,000)Operating net back 3,750,000,000 7,250,000,000Capital (500 wells plus facilities) (2,000,000,000) (2,000,000,000)

Undiscounted cash flow $ 1,750,000,000 $ 4,050,000,000

Operating net backsPer Mcf $3.75 $7.25Per Boe $22.50 $43.50

Based on 1 Tcf and 2 Bcf/well potential of Utica or Lorraine shale gas

Pipeline infrastructure in Lowlands

Comparative illustration of fiscal terms

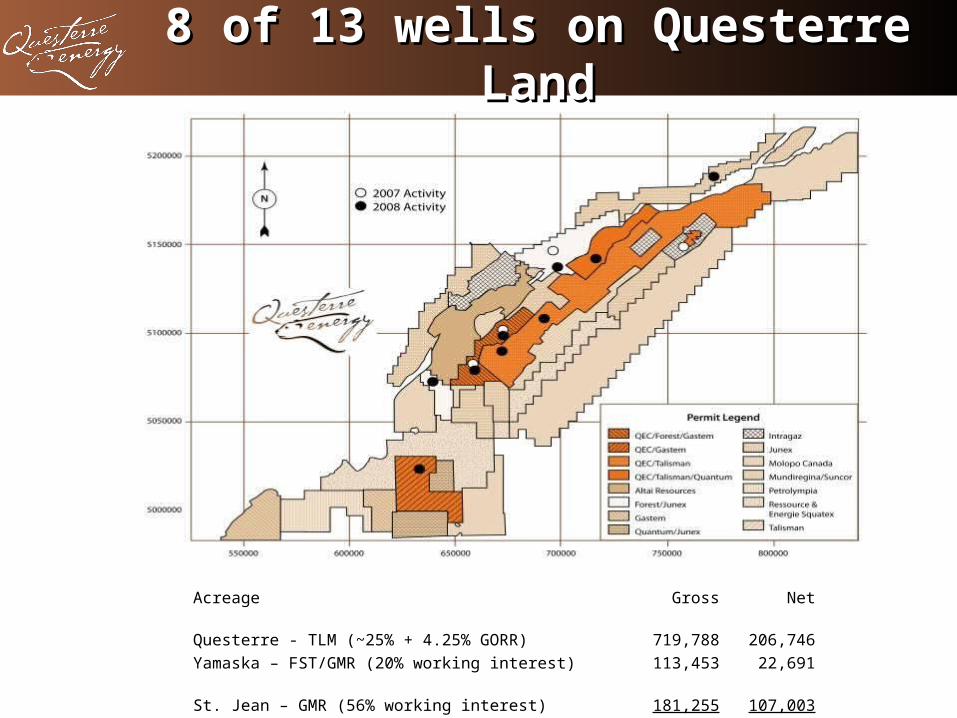

8 of 13 wells on Questerre 8 of 13 wells on Questerre LandLand

Acreage Gross Net

Questerre - TLM (~25% + 4.25% GORR) 719,788 206,746Yamaska – FST/GMR (20% working interest) 113,453 22,691

St. Jean – GMR (56% working interest) 181,255 107,003

Total 1,014,496 336,440

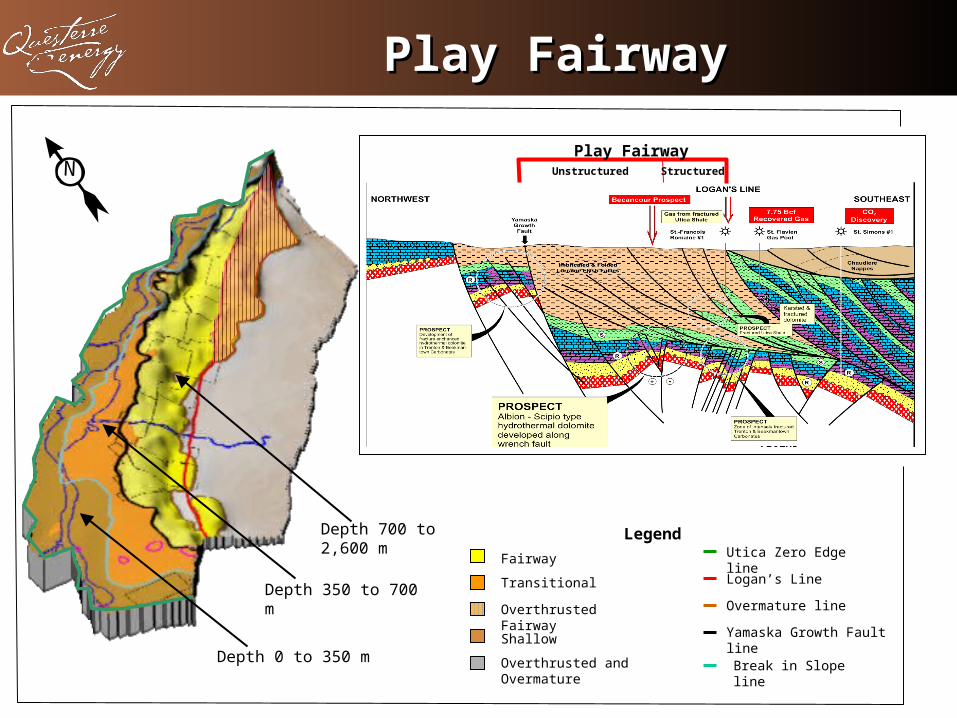

Play FairwayPlay Fairway

N

Depth 350 to 700 m

Depth 0 to 350 m

Depth 700 to 2,600 m

Unstructured Structured

Play Fairway

Legend

Overthrusted Fairway

Overthrusted and Overmature

Fairway

Transitional

Shallow

Logan’s Line

Yamaska Growth Fault line

Overmature line

Break in Slope line

Utica Zero Edge line

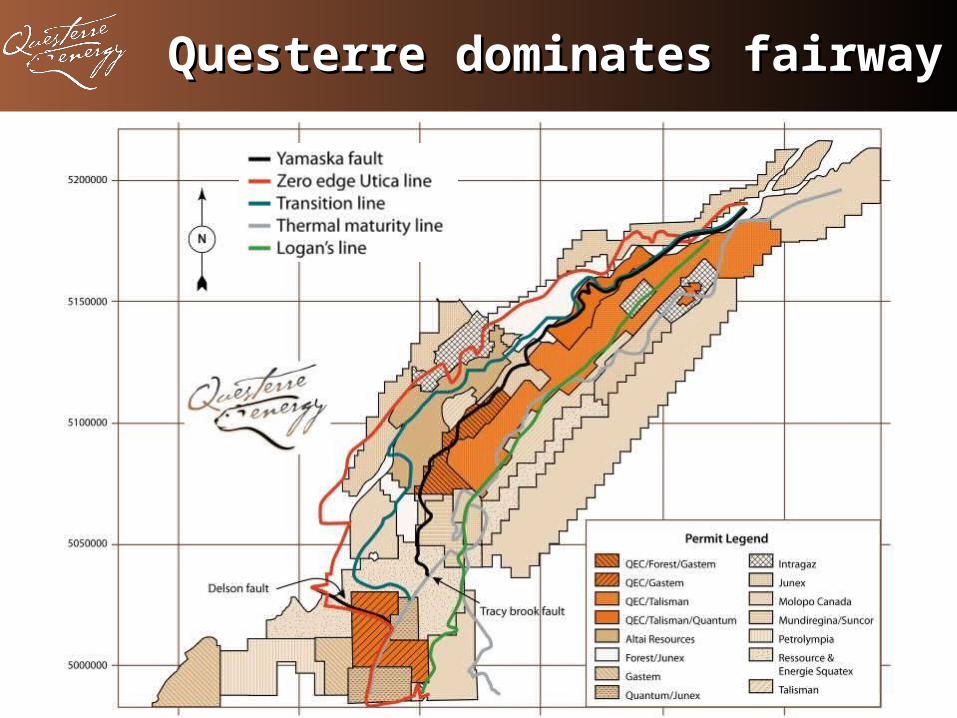

Questerre dominates Questerre dominates fairwayfairway

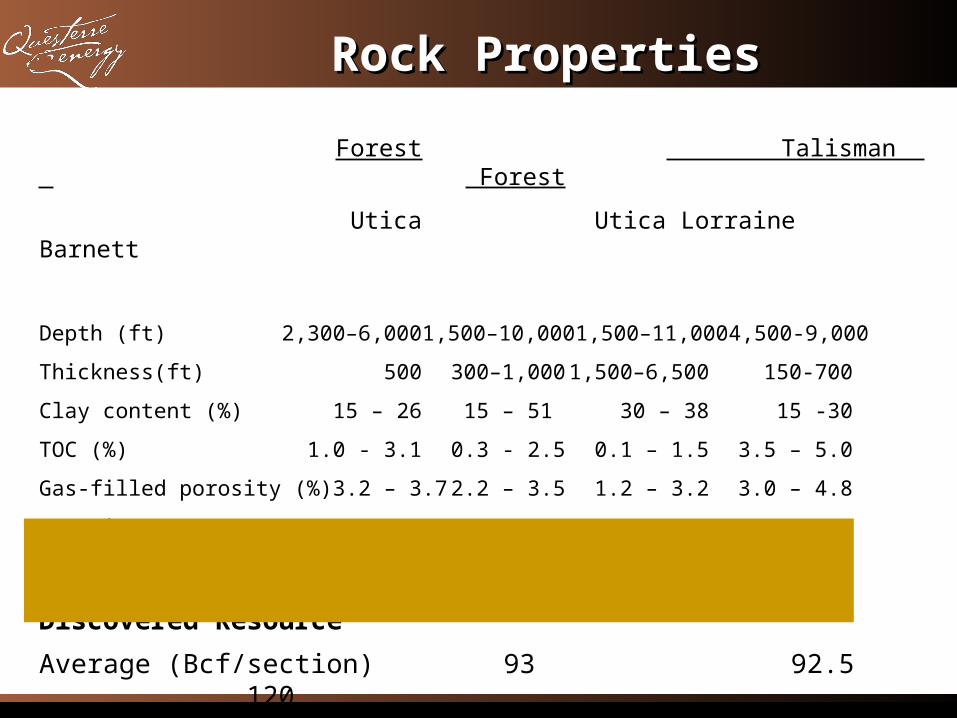

Rock PropertiesRock Properties

Forest Talisman Forest

Utica Utica Lorraine Barnett

Depth (ft) 2,300–6,0001,500–10,0001,500–11,000 4,500-9,000

Thickness(ft) 500 300–1,000 1,500–6,500 150-700

Clay content (%) 15 – 26 15 – 51 30 – 38 15 -30

TOC (%) 1.0 - 3.1 0.3 - 2.5 0.1 – 1.5 3.5 – 5.0

Gas-filled porosity (%) 3.2 – 3.7 2.2 – 3.5 1.2 – 3.2 3.0 – 4.8

Maturity (Ro) 1.3 – 2.0 1.1 – 4.0 1.1 – 4.0 1.0 – 2.2

Discovered Resource

Average (Bcf/section) 93 92.5 120

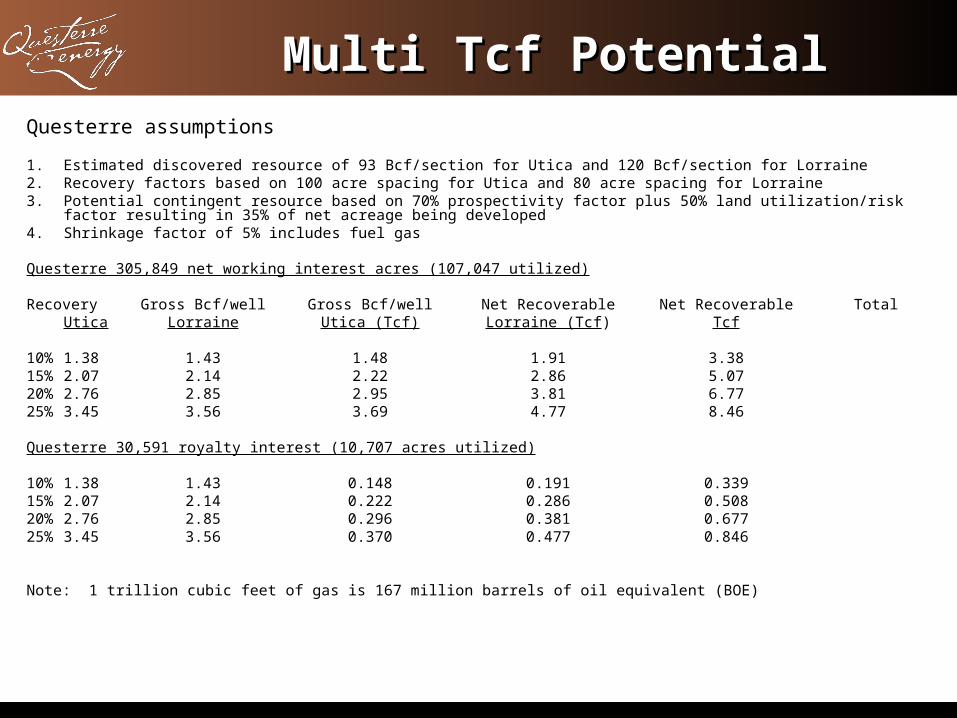

Multi Tcf PotentialMulti Tcf PotentialQuesterre assumptions

1. Estimated discovered resource of 93 Bcf/section for Utica and 120 Bcf/section for Lorraine2. Recovery factors based on 100 acre spacing for Utica and 80 acre spacing for Lorraine3. Potential contingent resource based on 70% prospectivity factor plus 50% land utilization/risk factor resulting in 35%

of net acreage being developed4. Shrinkage factor of 5% includes fuel gas

Questerre 305,849 net working interest acres (107,047 utilized)

Recovery Gross Bcf/well Gross Bcf/well Net Recoverable Net Recoverable TotalUtica Lorraine Utica (Tcf) Lorraine (Tcf) Tcf

10% 1.38 1.43 1.48 1.91 3.3815% 2.07 2.14 2.22 2.86 5.0720% 2.76 2.85 2.95 3.81 6.7725% 3.45 3.56 3.69 4.77 8.46

Questerre 30,591 royalty interest (10,707 acres utilized)

10% 1.38 1.43 0.148 0.191 0.33915% 2.07 2.14 0.222 0.286 0.50820% 2.76 2.85 0.296 0.381 0.67725% 3.45 3.56 0.370 0.477 0.846

Note: 1 trillion cubic feet of gas is 167 million barrels of oil equivalent (BOE)

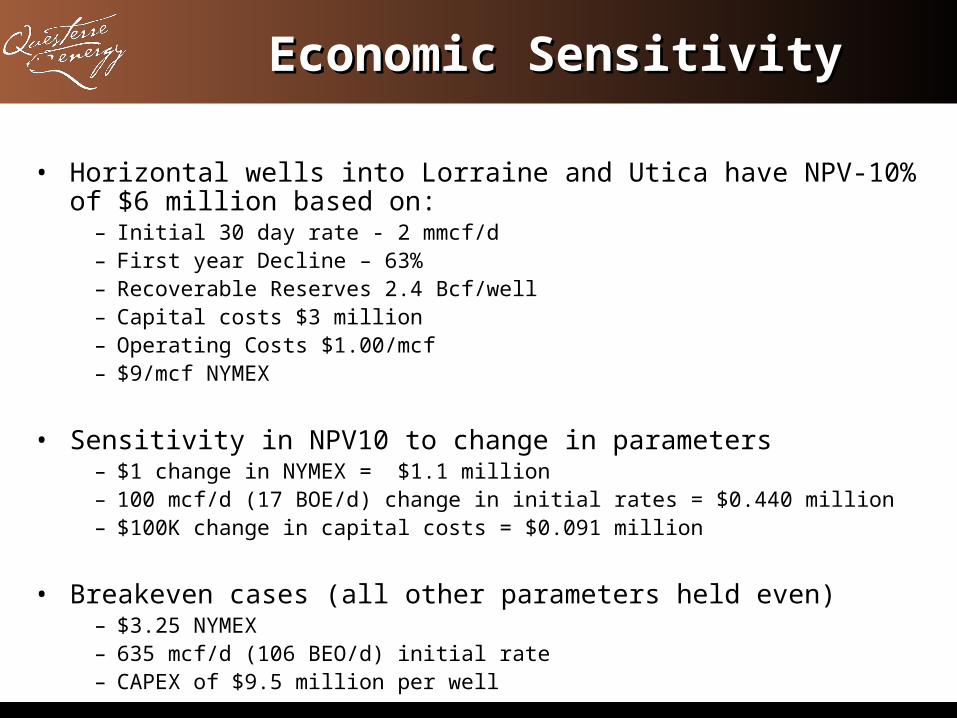

Economic SensitivityEconomic Sensitivity

• Horizontal wells into Lorraine and Utica have NPV-10% of $6 million based on:

– Initial 30 day rate - 2 mmcf/d– First year Decline – 63%– Recoverable Reserves 2.4 Bcf/well– Capital costs $3 million– Operating Costs $1.00/mcf– $9/mcf NYMEX

• Sensitivity in NPV10 to change in parameters– $1 change in NYMEX = $1.1 million– 100 mcf/d (17 BOE/d) change in initial rates = $0.440 million– $100K change in capital costs = $0.091 million

• Breakeven cases (all other parameters held even)– $3.25 NYMEX– 635 mcf/d (106 BEO/d) initial rate– CAPEX of $9.5 million per well

Pilot ProgramsPilot Programs

Over next 18 months QEC will participate in pilot programs to establish commerciality of unconventional gas in St. Lawrence Lowlands at an estimated cost of $40 million to $50 million net to Questerre with first gas estimated by second half of 2009 and full development in 2010 based on results achieved

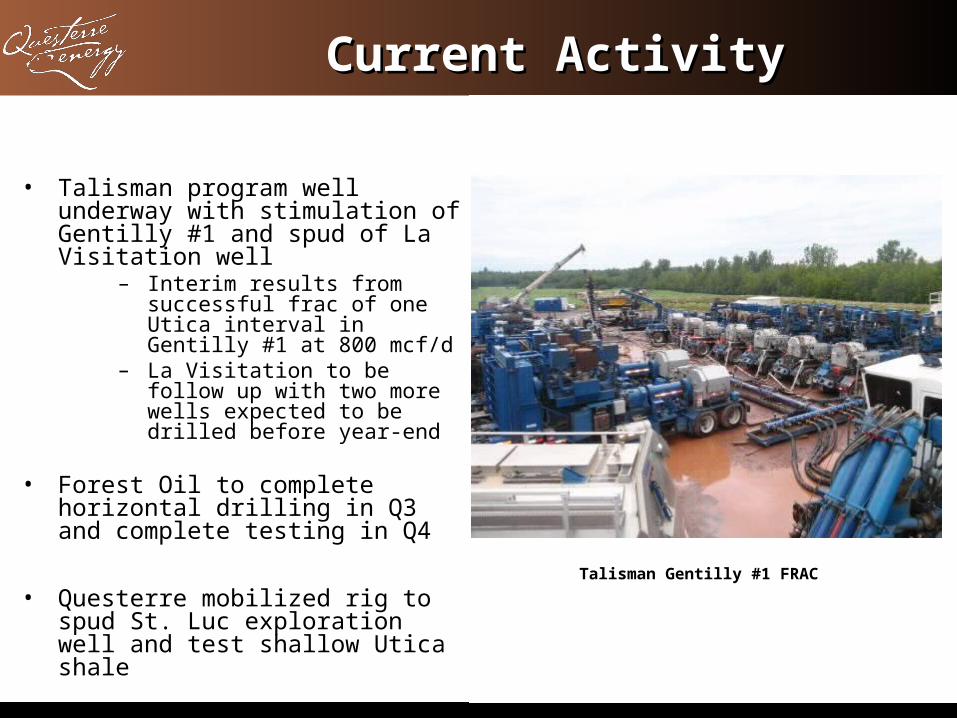

Current ActivityCurrent Activity

Talisman Gentilly #1 FRAC

• Talisman program well underway with stimulation of Gentilly #1 and spud of La Visitation well

– Interim results from successful frac of one Utica interval in Gentilly #1 at 800 mcf/d

– La Visitation to be follow up with two more wells expected to be drilled before year-end

• Forest Oil to complete horizontal drilling in Q3 and complete testing in Q4

• Questerre mobilized rig to spud St. Luc exploration well and test shallow Utica shale

Northeast British Northeast British ColumbiaColumbia

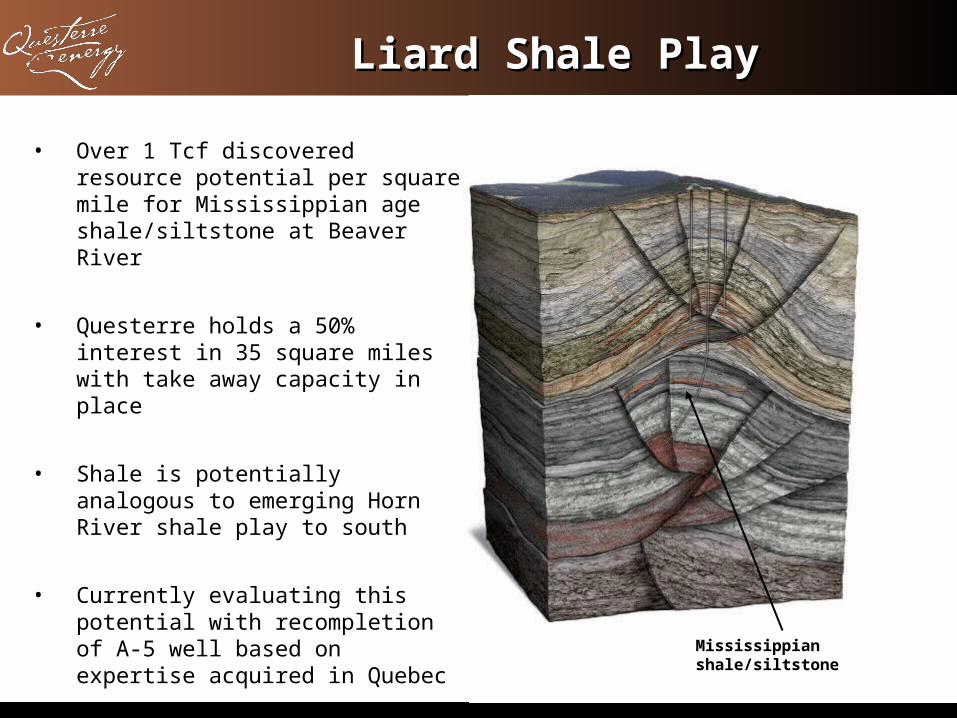

Liard Shale PlayLiard Shale Play

• Over 1 Tcf discovered resource potential per square mile for Mississippian age shale/siltstone at Beaver River

• Questerre holds a 50% interest in 35 square miles with take away capacity in place

• Shale is potentially analogous to emerging Horn River shale play to south

• Currently evaluating this potential with recompletion of A-5 well based on expertise acquired in Quebec Mississippian

shale/siltstone

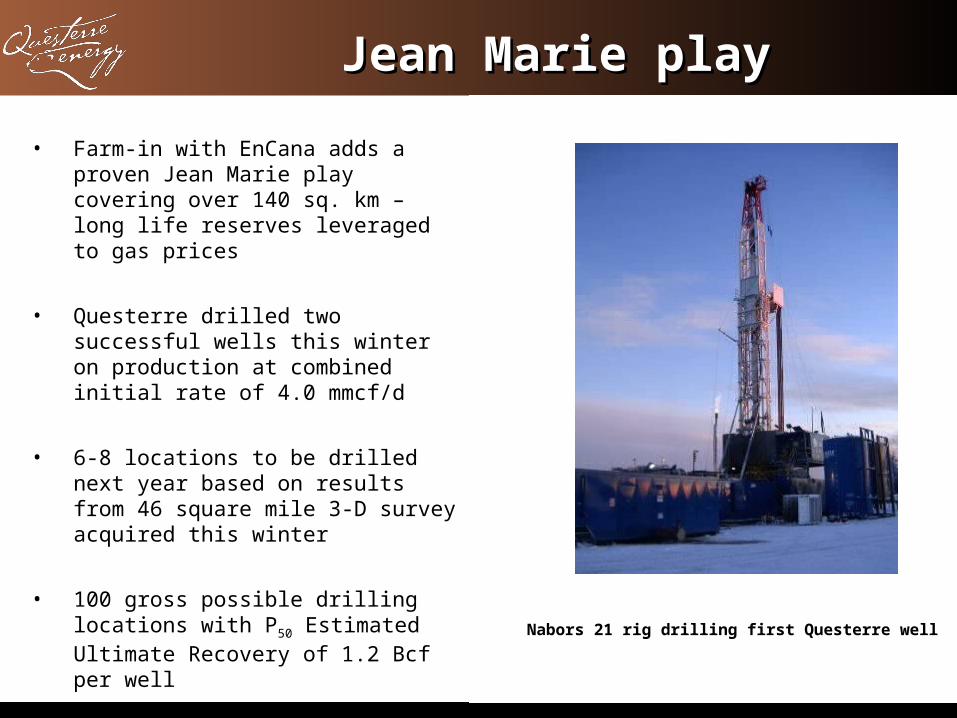

Jean Marie playJean Marie play

• Farm-in with EnCana adds a proven Jean Marie play covering over 140 sq. km – long life reserves leveraged to gas prices

• Questerre drilled two successful wells this winter on production at combined initial rate of 4.0 mmcf/d

• 6-8 locations to be drilled next year based on results from 46 square mile 3-D survey acquired this winter

• 100 gross possible drilling locations with P50 Estimated Ultimate Recovery of 1.2 Bcf per well

Nabors 21 rig drilling first Questerre well

Antler, Antler, SaskatchewanSaskatchewan

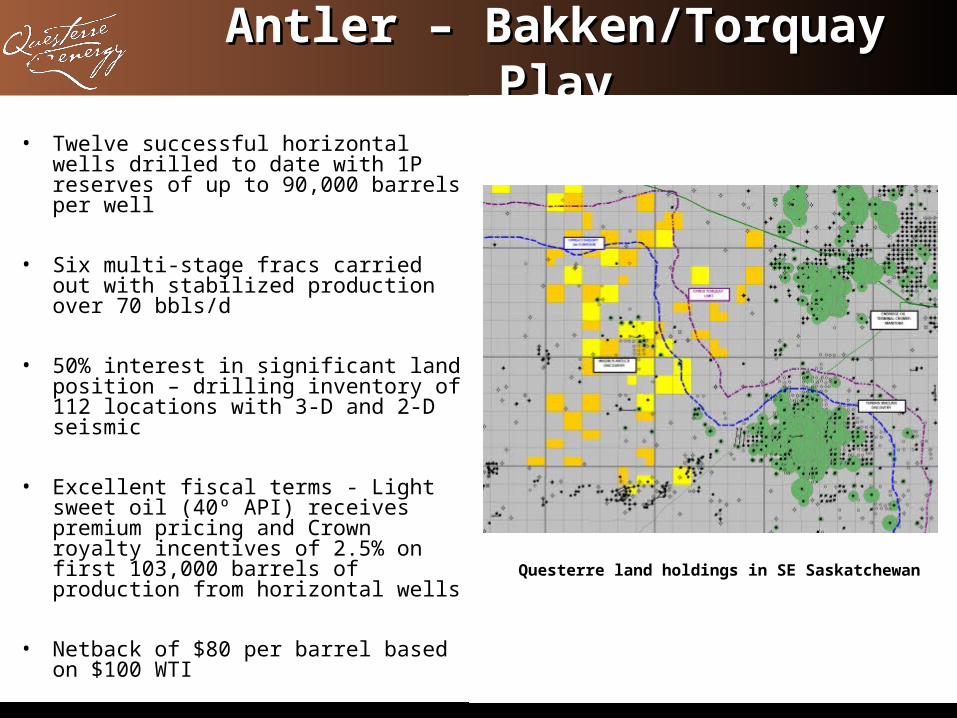

Antler – Bakken/Torquay Antler – Bakken/Torquay PlayPlay

Questerre land holdings in SE Saskatchewan

• Twelve successful horizontal wells drilled to date with 1P reserves of up to 90,000 barrels per well

• Six multi-stage fracs carried out with stabilized production over 70 bbls/d

• 50% interest in significant land position – drilling inventory of 112 locations with 3-D and 2-D seismic

• Excellent fiscal terms - Light sweet oil (40º API) receives premium pricing and Crown royalty incentives of 2.5% on first 103,000 barrels of production from horizontal wells

• Netback of $80 per barrel based on $100 WTI

Company OutlookCompany Outlook

Company OutlookCompany Outlook

• St. Lawrence Lowlands, Eastern Canada– Talisman exploration program for the

Trenton Black River underway - three wells scheduled for 2008 - results in early 2009

– Talisman $100 million plus Utica and Lorraine shale gas evaluation and pilot program underway - results in fourth quarter

– Forest Oil to fracture stimulate two pilot production horizontal wells - results in fourth quarter

– Shallow Utica/Trenton Black River well to be operated by Questerre in fall 2008 on St Jean

• Northeast British Columbia– Evaluate results from A-5 recompletion for

Liard shale potential– Six well program anticipated in Greater

Sierra based on interpretation of 3-D seismic acquisition program

• Antler, Saskatchewan– Drill, complete and fracture stimulate nine

additional wells and stimulate two existing wells over second half of 2008

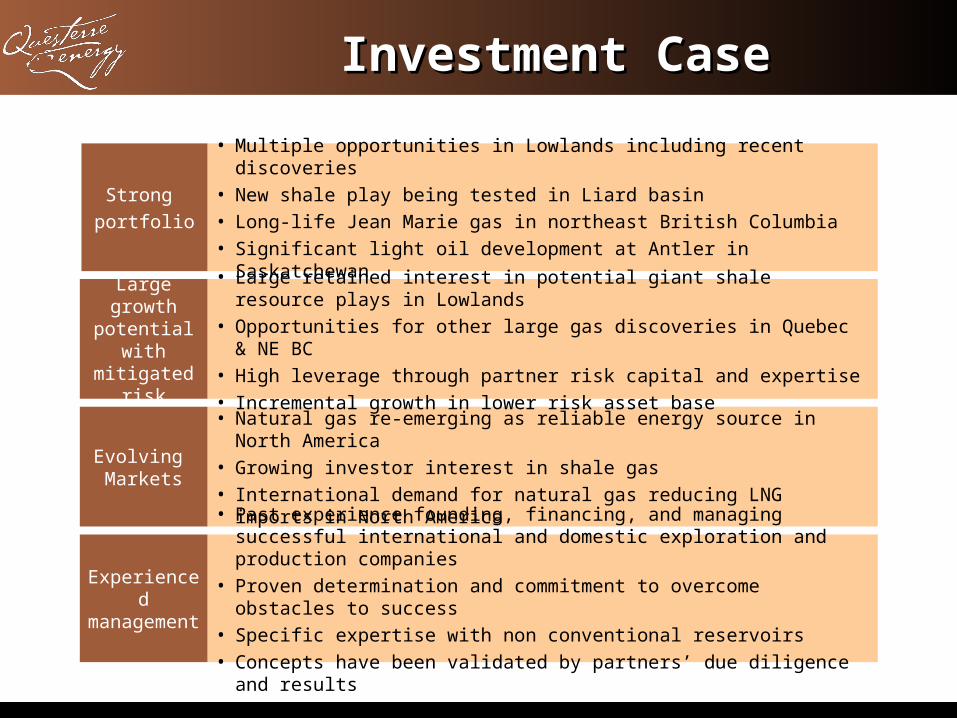

Investment CaseInvestment Case

• Multiple opportunities in Lowlands including recent discoveries• New shale play being tested in Liard basin• Long-life Jean Marie gas in northeast British Columbia• Significant light oil development at Antler in Saskatchewan

Strong portfolio

• Natural gas re-emerging as reliable energy source in North America

• Growing investor interest in shale gas• International demand for natural gas reducing LNG imports in

North America

Evolving Markets

• Past experience founding, financing, and managing successful international and domestic exploration and production companies

• Proven determination and commitment to overcome obstacles to success

• Specific expertise with non conventional reservoirs• Concepts have been validated by partners’ due diligence and

results

Experienced

management

• Large retained interest in potential giant shale resource plays in Lowlands

• Opportunities for other large gas discoveries in Quebec & NE BC• High leverage through partner risk capital and expertise• Incremental growth in lower risk asset base

Large growth

potential with

mitigated risk

1650 AMEC Place1650 AMEC Place

801 Sixth Avenue SW801 Sixth Avenue SW

Calgary, Alberta T2P 3W2 Calgary, Alberta T2P 3W2 CanadaCanada

Tel : (403) 777-1185Tel : (403) 777-1185

Fax : (403) 777-1578Fax : (403) 777-1578

Web: www.questerre.comWeb: www.questerre.com

Email : [email protected] : [email protected]