Q3 presentation 20 October Final utan speaker notes · • Lower marketing spend in Latvia ... •...

15

1 JOHAN DENNELIND, PRESIDENT & CEO INTERIM REPORT JANUARY – SEPTEMBER 2016 Q3 Q3 SLOWDOWN IN LINE WITH PROJECTIONS - CONTINUING OPERATIONS 2 SERVICE REVENUE GROWTH EBITDA* GROWTH FREE CASH FLOW Reported -0.7 Organic -1.1 Reported -1.5 Organic -1.6 SEK 3.3 billion *Excluding non-recurring items Reported -0.9 Organic -0.7 Reported +3.9 Organic +4.2 SEK 7.1 billion Q3 2016 9M 2016

Transcript of Q3 presentation 20 October Final utan speaker notes · • Lower marketing spend in Latvia ... •...

1

JOHAN DENNELIND, PRESIDENT & CEO

INTERIM REPORT JANUARY – SEPTEMBER 2016 Q3

Q3 SLOWDOWN IN LINE WITH PROJECTIONS - CONTINUING OPERATIONS

2

S E R V I C E R E V E N U E G R O W T H

E B I T D A * G R O W T H

F R E E C A S H F L O W

Reported -0.7Organic -1.1

Reported -1.5 Organic -1.6

SEK 3.3 billion

*Excluding non-recurring items

Reported -0.9Organic -0.7

Reported +3.9 Organic +4.2

SEK 7.1 billion

Q3 2016 9M 2016

2

THIRD QUARTER IN BRIEF

3

Proposed settlement

amount received from U.S. and

Dutch authorities related to entry in Uzbekistan

Core business on track

TV proposition strengthened

Focus on value loading offerings

Rebalancing continues - focus

on Nordics & Baltics

Full Eurasia exit demands more

time

Full year guidance reiterated

SETTLEMENT PROPOSAL RECEIVED FROM AUTHORITIES

4

• Global resolution (US & Dutch authorities) with proposed settlement of USD 1.45 billion

• Related to Telia Company’s entry into Uzbekistan in 2007

• Provision made in accordance with the proposed settlement amount

• Telia Company in discussions with authorities

3

ACTIVE SUSTAINABILITY AGENDA

5

NEW “CODE OF RESPONSIBLE BUSINESS

CONDUCT”

AVAILABLE AT TELIACOMPANY.COM

“SUSTAINABILITY UPDATE” REPORT RELEASED

AVAILABLE AT

TELIACOMPANY.COM

“ACCELERATING SUSTAINABLE GROWTH” REPORT RELEASED

AVAILABLE AT

TELIACOMPANY.COM

“LAW ENFORCEMENT DISCLOSURE” REPORT RELEASED

AVAILABLE AT

TELIACOMPANY.COM

“HUMAN RIGHTS IMPACT ASSESSMENT” REPORT RELEASED

AVAILABLE AT

TELIACOMPANY.COM

RECENTLY DIVESTED ASSETS

DIVESTMENTS ONGOING

6

• Divested to Aga Khan Fund for Economic Development. Closing estimated before year-end

REMAINING EURASIAN ASSETS

• Exploring divestment of Fintur Holdings together with the minority owner Turkcell

• More time needed to fully exit region Eurasia

• Divested to Axiata. Transaction closed in Q2

• Divested to MÁSMÓVIL. Completed on October 5

• Divested to Marginalen. Closing estimated before year-end

4

SERVICE REVENUESOrganic growth, external service revenues

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

Sweden Europe Continuing operations

-1.6%-1.6%

-1.1%-1.1%

+0.8%+0.8%

-4.0%

1.3%

-1.6%

Q315

Q316

Q315

Q316

Q315

Q316

CORE BUSINESS ON TRACK

7

EBITDAOrganic growth, excluding non-recurring items

• Less support from fiber revenues and a negative B2B segment in Sweden

• Stable growth in Europe as mobile service revenues offset pressure on fixed

• EBITDA erosion in Sweden from service revenue decline

• Europe benefits from service revenue growth and overall solid cost control

Continuing

operationsEuropeSweden

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

Telia passed, not connectedCommunication operatorTelia connected (MDUs + SDUs)

SWEDEN- STABLE B2C BUT STILL CHALLENGES IN B2B

Q3 15 Q3 16

+1.4%+1.4%

-6.6%-6.6%

+0.6%+0.6%

B2B

B2CExcl. fiber installation revenues

Incl. fiber installation revenues

1.45 million1.45 million

TELIA FIBER HOUSEHOLDSSERVICE REVENUES BY SEGMENTOrganic growth, external service revenues

• Stable B2C development but lower contribution from fiber installation revenues

• Positive development in SME/SoHo but continued price pressure in B2B large

• Deliveries impacted by increased permit lead time and sub-contractor delays

• Targeted full year order book achieved although some deliveries will spill over to 2017

• Target of 1.9 million homes reached by end of 2018 intact

1.25 million1.25 million

8

5

18 PERCENT TV REVENUE GROWTH IN SWEDEN

9

1.1%

5.9%

12.1%

Q315

Q316

Q315

Q316

Q315

Q316

TV

ARPU DEVELOPMENTGrowth y-o-y, B2C and B2B

• Increasing mobile ARPU from improved offerings despite continued price pressure in B2B

• Fixed broadband and TV ARPUs benefitting from price changes earlier this year

Fixed broadbandMobile

• Partnering with leading content and hardware suppliers

• New generation TV box launched

• Telia Play+ available in Apple TV

• Chromecast enabling “on any screen” experience

ENHANCED TV PROPOSITION

6.1%

2.9%

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

Mobile billed service revenues Total mobile service revenues2,758 2,784

Q3 15 Q3 16

0.0%0.0%

ACCELERATED MOBILE REVENUE GROWTH IN FINLAND

10* External service revenues **Excluding non-recurring items

Service revenues EBITDA

= Organic growth

SERVICE REVENUES* & EBITDA**SEK million, reported currency

MOBILE SERVICE REVENUES*Organic growth

• Mobile billed service revenue growth mitigated lower interconnect and fixed broadband revenues

• Stable profitability

• Successful data monetization and price increases in B2C boost mobile billed revenue growth

• Lower interconnect revenues behind lower growth in total mobile service revenues

1,048 1,055

Q3 15 Q3 16

+0.1%+0.1%

6

GOOD FOCUS AND EBITDA GROWTH IN NORWAY

11

862 890

Q3 15 Q3 16

+5.5%+5.5%

Service revenues EBITDA

SERVICE REVENUES* & EBITDA**SEK million, reported currency

• Lower interconnect revenues and disposal of fixed telephony customer base in Q4 2015

• EBITDA growth from mainly reduced SAC in Q3

* External service revenues **Excluding non-recurring items = Organic growth

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

Mobile billed service revenues Total mobile service revenues

MOBILE SERVICE REVENUES*Organic growth

• Flat mobile service revenues as growth in wholesale was offset by lower billed revenues and roaming

2,003 1,949

Q3 15 Q3 16

-1.5%-1.5%

-0.5%-0.5%

0.0%0.0%

12

256217

275295

148166

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

Estonia Lithuania Latvia

Q3 15 Q3 16Lithuania

Q3 15 Q3 16Latvia

+6.2%+6.2%

Q3 15 Q3 16Estonia

MIXED DEVELOPMENT IN THE BALTICS

-15.9%-15.9%

+11.6%+11.6%0.0%0.0%

+4.6%+4.6%

-4.3%-4.3%

SERVICE REVENUES*Organic growth

EBITDA**SEK million

• Growth in Lithuania from solid development in both mobile and fixed service revenues

• Lower sale of travel related products in Estonia

• Growing revenues coupled with synergies in Lithuania

• Lower marketing spend in Latvia

* External service revenues = Organic growth ** Excluding non-recurring items

7

SUMMARY Q3

13

PROVIS ION OF SEK 12 .5 B I LL ION

CORE BUS INESS ON TRACK

SHAPING OF NORDIC AND BALT IC FOOTPRINT

14

CHRISTIAN LUIGA,

SENIOR VICE PRESIDENT & CFO

INTERIM REPORT

JANUARY – SEPTEMBER 2016 Q1Q2Q3

8

15

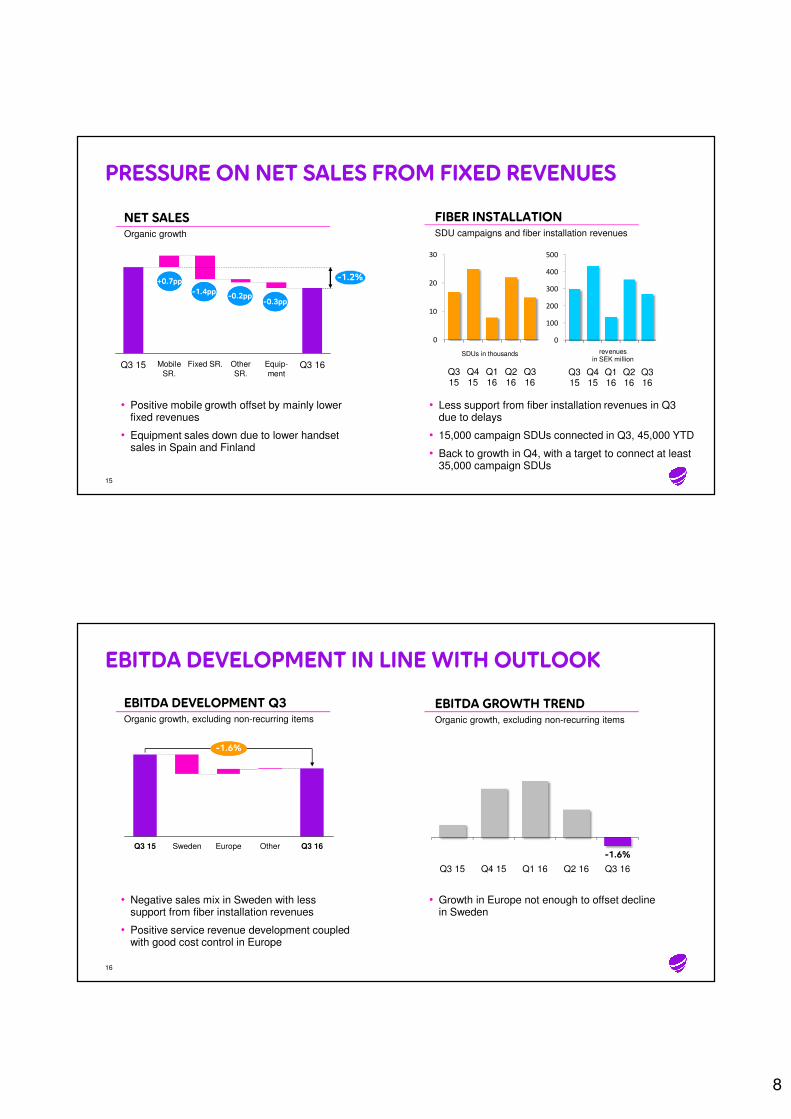

PRESSURE ON NET SALES FROM FIXED REVENUES

NET SALESOrganic growth

Q3 15 Fixed SR.Mobile SR.

Other SR.

Equip-ment

-1.2%

Q3 16

-1.4pp-1.4pp

+0.7pp+0.7pp

-0.2pp-0.2pp-0.3pp-0.3pp

0

100

200

300

400

500

Q315

Q415

Q116

Q216

Q316

revenuesin SEK million

FIBER INSTALLATIONSDU campaigns and fiber installation revenues

• Positive mobile growth offset by mainly lower fixed revenues

• Equipment sales down due to lower handset sales in Spain and Finland

• Less support from fiber installation revenues in Q3 due to delays

• 15,000 campaign SDUs connected in Q3, 45,000 YTD

• Back to growth in Q4, with a target to connect at least 35,000 campaign SDUs

0

10

20

30

Q315

Q415

Q116

Q216

Q316

SDUs in thousands

16

EBITDA DEVELOPMENT IN LINE WITH OUTLOOK

EBITDA DEVELOPMENT Q3Organic growth, excluding non-recurring items

EBITDA GROWTH TRENDOrganic growth, excluding non-recurring items

-1.6%-1.6%

Q3 16OtherEuropeSwedenQ3 15-1.6%

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

• Negative sales mix in Sweden with less support from fiber installation revenues

• Positive service revenue development coupled with good cost control in Europe

• Growth in Europe not enough to offset decline in Sweden

9

REVENUE GROWTH AND COST CONTROL IN EUROPE

17

EBITDAOrganic growth, excluding non-recurring items

ESTLITDENNORFINQ3 15

+1.3%+1.3%

Q3 16SPALAT

• Strong mobile billed revenue growth in Finland offset by lower interconnect and fixed revenues

• Norway impacted by divestment of fixed base in Q4 2015

• Mobile and fixed revenue growth in Lithuania

SERVICE REVENUESOrganic growth, external service revenues

• Growing mobile service revenues and lower OPEX in most markets support EBITDA

• Lower SAC in Norway

+0.8%+0.8%

Q3 16SPAQ3 15 LATESTLITDENNORFIN

-0.4%-0.4%

If excluding Spain

+1.0%+1.0%

If excluding Spain

18

EASING REVENUE PRESSURE IN EURASIA

FINANCIAL DEVELOPMENT Q3Organic growth

-12%

-6%

19%

1%

-25%

-11%

1%

-9%

Kazakhstan Azerbaijan Uzbekistan Eurasia

Service revenues*

EBITDA**

• Service revenue growth in 4 of 6 markets

• Less pressure on revenues in Kazakhstan but still high competition in the market

• EBITDA impacted by weaker local currencies in the region

• Trends are improving

* External service revenues **Excluding non-recurring items

TRENDS IN EURASIAOrganic growth, excluding Nepal

-3% -2%

1%

-27%-24%

-9%

Q1 16 Q2 16 Q3 16

Service revenues*

EBITDA**

10

19

COST DEVELOPMENT UNDER CONTROL

• Sweden and Spain key drivers behind lower OPEX H1 2016

• Increased transformation and commercial activities drive OPEX in Sweden Q3 2016

0.6%

Q3 15* Q4 15* Q1 16* Q2 16* Q3 16*

OPEX DEVELOPMENTOrganic growth, excluding Norway

* Norway excluded for comparison reasons due to Tele2 acquisition

OPEX represents ~40 percent of total cost base

2015 YTD Q32016

2016e 2017e

Sweden

Finland

Central funtions

INVEST TO SAVE PHASINGSEK billion, savings run-rate at period/year-end

0.6

0.91.1

2.0

• Program on track

1.4 1.7

1.21.1

0.60.8

0.0

1.0

2.0

3.0

4.0

Q3 15 Q3 16

Other operations

Europe

Sweden

TRANSFORMATION AND FIBER ROLL-OUT DRIVE CAPEX

20

= In relation to external service revenues

16.9%16.9% 19.8%19.8%

CAPEX EXCLUDING LICENSESSEK billion, continuing operations

• Higher CAPEX in Sweden driven by fiber and business transformation

• Group function IT investments main reason for higher CAPEX in Other operations

• Full year CAPEX likely to be in the high-end of guidance range

• Spectrum acquired in Denmark in the quarter -license auctions upcoming in Sweden and Finland

3.1

3.6

11

21

TOTAL EPS IMPACTED BY PROVISION

EPS - TOTALSEK

• Flat EPS in continuing operations

• Lower EPS in discontinued operations due mainly to SEK 12.5 billion settlement proposal provision

* Excluding income from associates and non-recurring items

-2.03

0.021.06

Oth

er

-0.12

Non

-rec

urrin

g

0.16

Ope

ratin

gin

com

e*

-0.06

Q3 15

Ass

ocia

tes

-3.09

Dis

cont

inue

dop

erat

ions Q3 16

0.000.00

Continuing operations

STABLE FREE CASH FLOW

FREE CASH FLOW Q3 SEK billion, continuing operations

• EBITDA in Eurasia impacted by Ncelldeconsolidation, erosion of local currencies and operational taxes

• MegaFon dividend of SEK 1.1 billion net of tax received in the quarter

* Excluding non-recurring items ** Net of tax

-0.2

EBITDA*

-0.1

Dividend associates

**

3.2

Q3 15

0.00.0

Q3 16

3.3

Interest Other

-0.5-0.4

Change in WC

-0.2

Tax Cash CAPEX

0.9 0.6

0

4

8

12

16

20

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

Discontinued operations Dividends from associates net of taxes Continuing operations excl. associates Continuing operations incl. associates

22

FREE CASH FLOW, R12 MONTHSSEK billion, continuing and discontinued operations

11.4

16.016.615.5

9.0

10.3

12

23

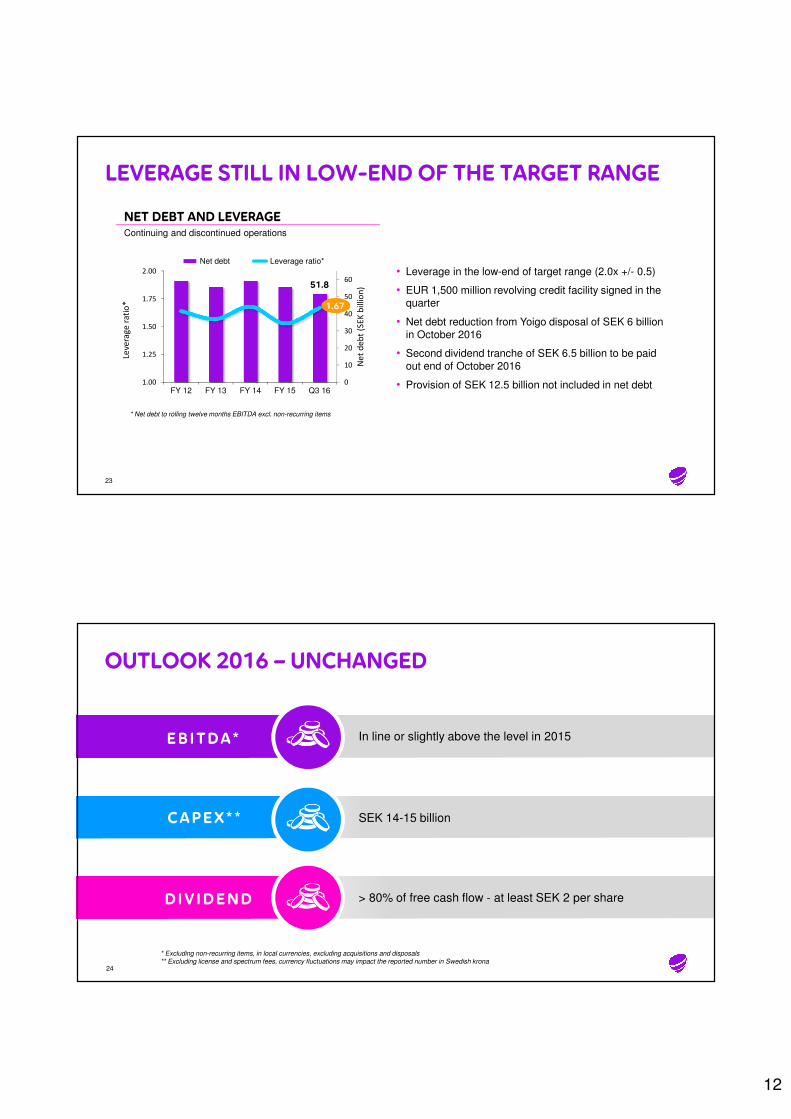

LEVERAGE STILL IN LOW-END OF THE TARGET RANGE

NET DEBT AND LEVERAGEContinuing and discontinued operations

51.8

0

10

20

30

40

50

60

1.00

1.25

1.50

1.75

2.00

FY 12 FY 13 FY 14 FY 15 Q3 16

Ne

t d

eb

t (S

EK

billio

n)

Leve

rag

e r

ati

o*

Net debt Leverage ratio*

* Net debt to rolling twelve months EBITDA excl. non-recurring items

1.67

• Leverage in the low-end of target range (2.0x +/- 0.5)

• EUR 1,500 million revolving credit facility signed in the quarter

• Net debt reduction from Yoigo disposal of SEK 6 billion in October 2016

• Second dividend tranche of SEK 6.5 billion to be paid out end of October 2016

• Provision of SEK 12.5 billion not included in net debt

OUTLOOK 2016 – UNCHANGED

* Excluding non-recurring items, in local currencies, excluding acquisitions and disposals** Excluding license and spectrum fees, currency fluctuations may impact the reported number in Swedish krona

24

In line or slightly above the level in 2015EB ITDA *

SEK 14-15 billion

> 80% of free cash flow - at least SEK 2 per share

CAPEX * *

DIV IDEND

13

Q&A

DEBT MATURITY SCHEDULE MMO

0

1

2

3

4

5

6

7

8

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-76

May-17

Jun-17

Jul-17

Aug-17

Sep-17

0

2

4

6

8

10

12

2016 2019 2022 2025 2028 2031 2034 2037 2040 2043 2046 2049 2052 2055 2058 2061 2064

26

DEBT MATURING NEXT 12 MONTHS

DEBT PORTFOLIO MATURITY SCHEDULE – 2016 AND ONWARDS

SEK billion

SEK billion

14

FINANCIAL SUMMARY Q3 2016

27

* Excluding non-recurring items

Q3 2016 Q3 2015 CHANGE (%)

Net sales (SEK million) 21,524 21,712 -0.9

Change local organic (%) -1.2

Service revenues (SEK million) 18,413 18,549 -0.7

Change local organic (%) -1.1

EBITDA* (SEK million) 6,850 6,957 -1.5

Change local organic (%) -1.6

EBITDA* Margin (%) 31.8 32.0

Total EPS (SEK) -2.03 1.06

Total free cash flow (SEK million) 3,657 4,699 -22.2

28

SEP 30, 2016 DEC 31, 2015

Return on equity*, % Negative 9.3

Return on capital employed*, % 2.6 8.9

Equity/assets ratio, % 31.5 35.1

Net debt/equity ratio, % 63.3 62.5

Net debt/EBITDA** ratio, multiple 1.67 1.53

Net debt/assets ratio, % 19.9 21.9

* Rolling 12 months ** Rolling 12 months, excluding non-recurring items

FINANCIAL KEY RATIOS Q3 2016

15

FORWARD-LOOKING STATEMENTS

Statements made in this document relating to future status or circumstances, including future performance and other trend projections are forward-looking statements. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There can be no assurance that actual results will not differ materially from those expressed or implied by these forward-looking statements due to many factors, many of which are outside the control of Telia Company.