Q3 2017 Update: The State Of Distributed Solar to grow at a faster rate than Tesla/SolarCity, SunRun...

24

0 Perea - State of U.S. Solar Austin Perea Analyst, U.S. Solar [email protected] Q3 2017 Update: The State Of Distributed Solar

Transcript of Q3 2017 Update: The State Of Distributed Solar to grow at a faster rate than Tesla/SolarCity, SunRun...

0Perea - State of U.S. Solar

Austin Perea

Analyst, U.S. Solar

Q3 2017 Update: The State Of Distributed Solar

1Perea - State of U.S. Solar

The U.S. solar PV market installed over

2 GW

• Up 12% year-over-year

• Up 8% quarter-over-quarter

Utility PV – 1.4 GW

• ~60% of U.S. solar capacity in Q2 2017

DG remains smallest share of overall

quarterly capacity additions

Non-Residential – 436 MW

• Up 10% over Q1 2017

• Up 31% year-over-year

Residential – 563 MW

• Up 1% over Q1 2017

• Down 17% year-over-year

National-Level Market Overview – H1 2017

747941 964

2,110

1,364 1,287 1,395

2,205

1,342 1,434 1,430

3,285

2,0902,203

4,151

6,582

2,1322,387

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Inst

alla

tio

ns

(MW

dc)

Residential Non-Residential Utility

2Perea - State of U.S. Solar

Unpacking Residential Solar’s Slowdown

3Perea - State of U.S. Solar

Residential solar continues to face challenges Quarterly Residential PV Installed Capacity (MWdc) Q1 2012-Q2 2017

111 128

148 169 171

195

261 249 279

328

410

461

501

593 612

672 679

607 638

555 563

-

100

200

300

400

500

600

700

800

Cap

acit

y (M

Wd

c)

4Perea - State of U.S. Solar

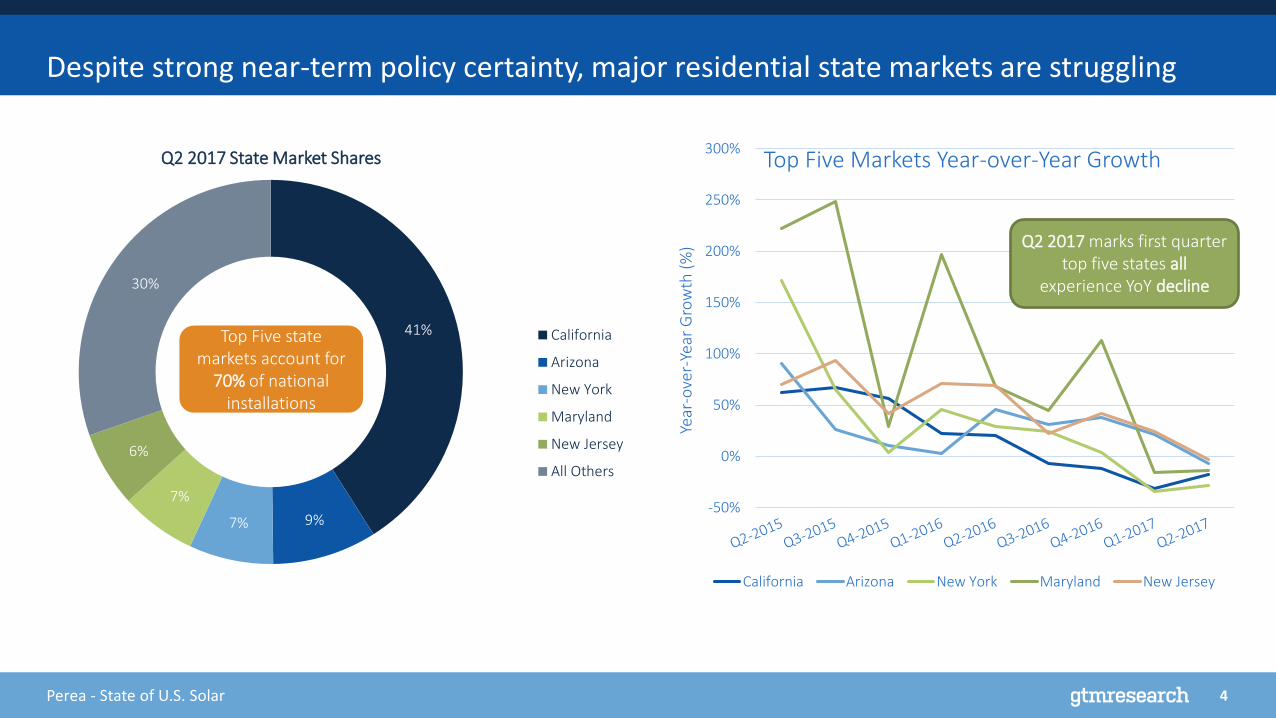

Despite strong near-term policy certainty, major residential state markets are struggling

-50%

0%

50%

100%

150%

200%

250%

300%

Year

-ove

r-Ye

ar G

row

th (

%)

Top Five Markets Year-over-Year Growth

California Arizona New York Maryland New Jersey

Q2 2017 marks first quarter top five states all

experience YoY decline

41%

9%7%

7%

6%

30%

Q2 2017 State Market Shares

California

Arizona

New York

Maryland

New Jersey

All Others

Top Five state markets account for

70% of national installations

5Perea - State of U.S. Solar

Residential solar slowdown began in California in 2016…

0 kW

10,000 kW

20,000 kW

30,000 kW

40,000 kW

50,000 kW

60,000 kW

70,000 kW

80,000 kW

90,000 kW

100,000 kW

Sub-1 MW 1-2 MW 2-10MW 10 MW+

Inst

alle

d C

apac

ity

(kW

dc)

Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

20

40

60

80

100

120

140

160

180

200

Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017

Year-over-Year G

row

th

MW

Inst

alle

d

SolarCity All Others

SCTY YoY Growth All Others YoY Growth

California Installation Volumes by Installer SizeSolarCity vs. All Other Installers in California:

Capacity and Year-over-Year Growth

Residential solar slowdown began in California in 2016…

6Perea - State of U.S. Solar

…and hit Northeast markets in full force in H1 2017

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

New York Maryland New Jersey Massachusetts

Year

-ove

r-Ye

ar G

row

th (

%)

Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

New York Maryland New Jersey Massachusetts

Cap

acit

y (M

Wd

c)

Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017

Northeast Markets Q2 2016-Q2 2017 Residential Installations Northeast Markets Q2 2016-Q2 2017 Year-over-Year Growth

7Perea - State of U.S. Solar

Growing pains among the national residential solar providers…Transitioning away from unabated market share capture to profitable growth

90%106%

66%

-1%

45%24%

78%

45%

-20%0%

20%40%60%80%

100%120%

2013 2014 2015 2016An

nu

al G

row

th (

%)

Growth Rate (SolarCity, Sunrun, Vivint Solar)

Growth Rate (Rest of Residential Market)

$0.00$0.10$0.20$0.30$0.40$0.50$0.60$0.70$0.80

SolarCity,Vivint Solar,

Sunrun

Large Regional(over 2

MW/quarter)

Mid-SizeRegional (1-2MW/quarter)

Large Local(100 kw-1

MW/quarter)

Long Tail

20

16

Avg

Co

st (

$/W

)

0%

20%

40%

60%

80%

100%

SolarCity Vivint Solar Sunrun All Others

Shar

e o

f To

tal

Dep

loym

ents

Third-Party Owned Customer Owned

Source: GTM Research

Annual Growth Rates: SCTY+RUN+VSLR vs. Rest of Residential PV Market Quarterly Residential PV TPO Market Shares in 2016: National vs. California

Source: GTM Research

2016: TPO Market Shares by Residential PV Company

Source: GTM Research

In aggregate: National residential PV companies have a more than 3x higher costof customer acquisition than the long tail of installers

8Perea - State of U.S. Solar

Emerging Markets – Quarterly Installed Capacity Q1 2015-Q2 2017

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Utah South Carolina Texas Florida Pennsylvania

Cap

acit

y (M

Wd

c)

Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017

9Perea - State of U.S. Solar

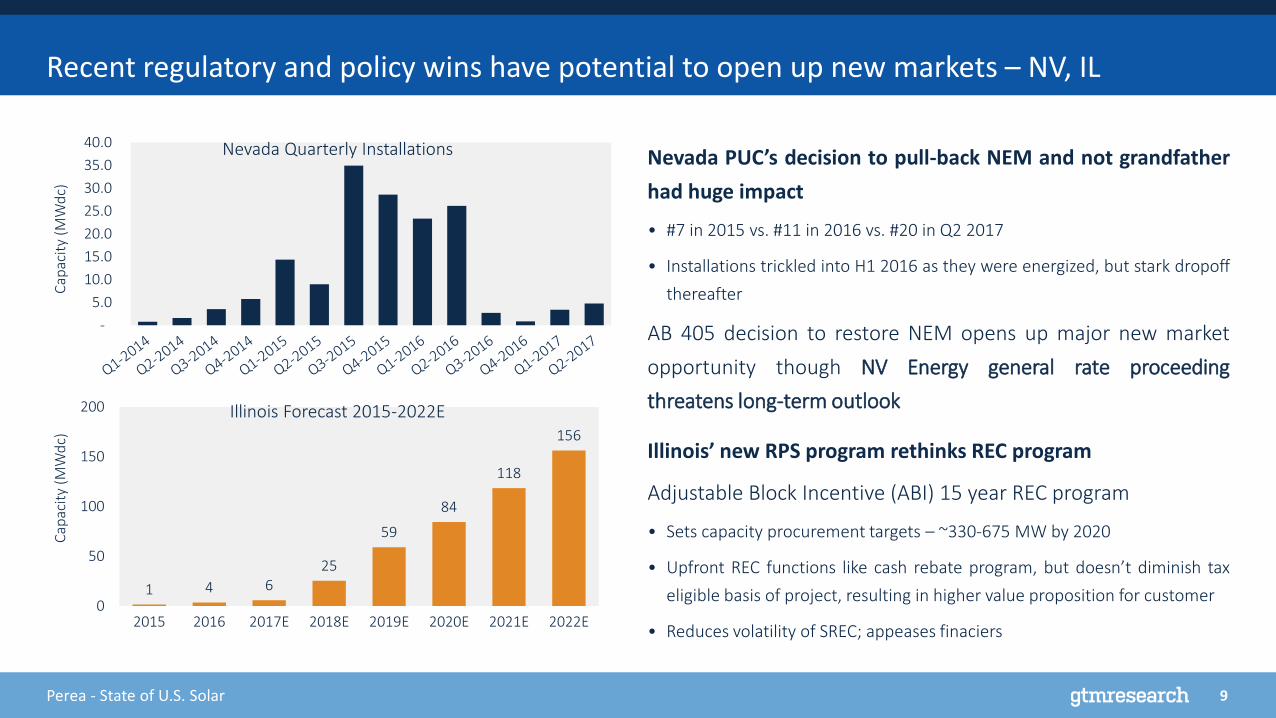

Recent regulatory and policy wins have potential to open up new markets – NV, IL

Nevada PUC’s decision to pull-back NEM and not grandfather

had huge impact

• #7 in 2015 vs. #11 in 2016 vs. #20 in Q2 2017

• Installations trickled into H1 2016 as they were energized, but stark dropoff

thereafter

AB 405 decision to restore NEM opens up major new market

opportunity though NV Energy general rate proceeding

threatens long-term outlook

Illinois’ new RPS program rethinks REC program

Adjustable Block Incentive (ABI) 15 year REC program

• Sets capacity procurement targets – ~330-675 MW by 2020

• Upfront REC functions like cash rebate program, but doesn’t diminish tax

eligible basis of project, resulting in higher value proposition for customer

• Reduces volatility of SREC; appeases finaciers

1 4 625

59

84

118

156

0

50

100

150

200

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

Cap

acit

y (M

Wd

c)

Illinois Forecast 2015-2022E

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Cap

acit

y (M

Wd

c)

Nevada Quarterly Installations

10Perea - State of U.S. Solar

Major Trends Defining Residential Solar in 2017

• The “long tail” of installers, with cheaper customer acquisition costs, are on

track to grow at a faster rate than Tesla/SolarCity, SunRun and Vivint

collectively

• And the “Big Three’s” pursuit of profitable sales and lower customer

acquisition costs will result in a the market contacting 3% from 2016

• Major markets continue to struggle despite strong policy environment

2017 marks the first time…

• California will fall on annual basis this decade

• Direct ownership will drive the majority of annual installations since 2011

• More than half of all states in the U.S. will be at grid parity in H2 2017

◦ Emerging state markets outside the top 5 (CA, AZ, NJ, NY and MD) to

grow 20% in a year of flat national level demand

◦ Q2 2017 second consecutive quarter in which emerging state (Utah,

Texas) replaces major state (MA) at #6 largest market

The Near Term Residential PV Outlook: Defined by market transitions

109%

15%

52%

65%

50%

95%

38%

54%

64%

75%

82%

72%

5%

45%

23%20%

-13%

2%5%

-3%

-20%

0%

20%

40%

60%

80%

100%

120%

California Next Five States All Other States Total

Axi

s Ti

tle

2013 2014 2015 2016 2017E

11Perea - State of U.S. Solar

Non-Residential Solar’s Reboot: Growth Beyond Standalone Onsite Solar to Community Solar

12Perea - State of U.S. Solar

Policy and Incentive Driven Bubbles Support 2017 Rebound

The Top 4 States: Partly fueled by short lived market drivers

• California: The closure of solar-friendly rate structures

• Massachusetts: Pull-in of demand amidst closure of SREC programs

• New Jersey: RPS driven demand for SRECs pulled in from future years

• New York: Depleting pipeline of virtual/remote NEM projects

What’s driving a reboot in all other states?

• The emergence of community solar: 220 MW+ installed in 2016

◦ Utility led community solar: Drove more than 60% of community solar

◦ Top 3 community solar states in 2017: CA, MA and MN

After 3 Consecutive Years of Flat Demand: Non-Residential PV Grew by 50%+ in 2016, expected to grow 9% in 2017E

0

100

200

300

400

500

600

700

800

Cap

acit

y (M

Wd

c)

2013 2014 2015 2016 2017E

13Perea - State of U.S. Solar

Emergence of Community Solar: Legislative and Voluntary Segments Both Set to Scale

126 9 6

2952

223

410

0

100

200

300

400

500

600

700

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

An

nu

al In

stal

lati

on

s (M

Wd

c)

Third Party Led Utility Led

3744

62

26

227

113

0

50

100

150

200

250

Coop IOU Muni

Uti

lity

Led

Co

mm

un

ity

Sola

r (M

Wd

c)

Operating In Development

Source: <Insert source>

Community Solar Installation Outlook:Third Party Led vs Utility Led Community Solar

Source: <Insert source>

Within Utility Led Community Solar:Emergence of IOUs Procuring Large Scale Community Solar

14Perea - State of U.S. Solar

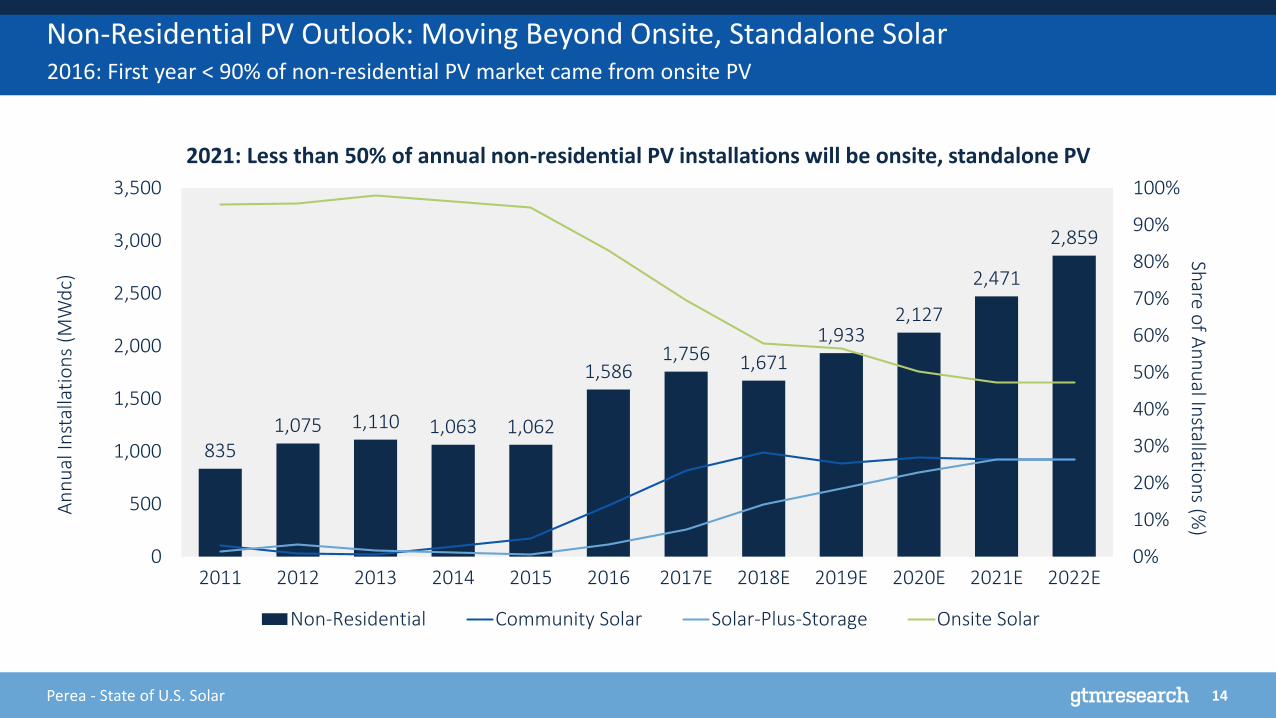

Non-Residential PV Outlook: Moving Beyond Onsite, Standalone Solar

8351,075 1,110 1,063 1,062

1,5861,756 1,671

1,9332,127

2,471

2,859

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

Share o

f An

nu

al Installatio

ns (%

)A

nn

ual

Inst

alla

tio

ns

(MW

dc)

Non-Residential Community Solar Solar-Plus-Storage Onsite Solar

2021: Less than 50% of annual non-residential PV installations will be onsite, standalone PV

2016: First year < 90% of non-residential PV market came from onsite PV

15Perea - State of U.S. Solar

The Next 5 Years of U.S. Solar

16Perea - State of U.S. Solar

1. Macro level uncertainty: Solar trade dispute, corporate tax reform, NEM and rate reform risk

What comes next for U.S. solar?

17Perea - State of U.S. Solar

1. Macro level uncertainty: Solar trade dispute, corporate tax reform, NEM and rate reform risk

2. Residential Solar: Near term contraction, sub 12% annual growth in a more fragmented installer landscape, paired with the emergence of loans and cash sales collectively outpacing third party owned leases and PPAs

3. Non-Residential Solar: Continued growth hinges on community solar (near term) and solar-plus-storage (long term) amidst state incentive reductions and TOU rate reforms across major markets

What comes next for U.S. solar?

4. Utility Solar: On track for another boom in procurement heading into 2019 in response to the scheduled stepdown of the 30% federal ITC, supporting growth in the 2019-2021 timeframe

18Perea - State of U.S. Solar

Total Installed Capacity triples by 2022, reaches 16 GW annually

September 29, 2017www.seia.org18

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

Year

ly In

stal

led

So

lar

Cap

acit

y (M

Wd

c)

U.S. Solar PV Deployment Forecast

Residential (PV) Non-residential (PV) Utility (PV)Source: SEIA/GTM

Research U.S. Solar Market

Insight

20Perea - State of U.S. Solar

Appendix: Utility-Scale Trends

21Perea - State of U.S. Solar

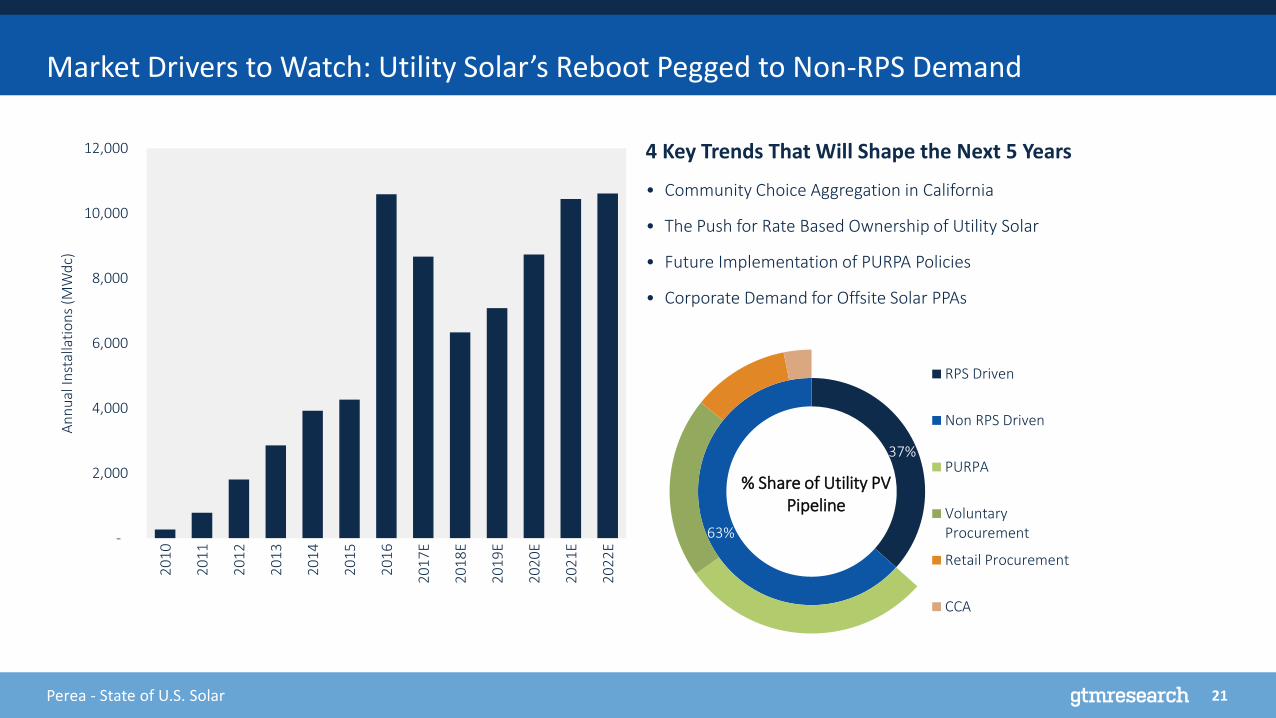

4 Key Trends That Will Shape the Next 5 Years

• Community Choice Aggregation in California

• The Push for Rate Based Ownership of Utility Solar

• Future Implementation of PURPA Policies

• Corporate Demand for Offsite Solar PPAs

Market Drivers to Watch: Utility Solar’s Reboot Pegged to Non-RPS Demand

37%

63%

RPS Driven

Non RPS Driven

PURPA

VoluntaryProcurement

Retail Procurement

CCA

% Share of Utility PV Pipeline

-

2,000

4,000

6,000

8,000

10,000

12,0002

01

0

20

11

20

12

20

13

20

14

20

15

20

16

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

An

nu

al In

stal

lati

on

s (M

Wd

c)

22Perea - State of U.S. Solar

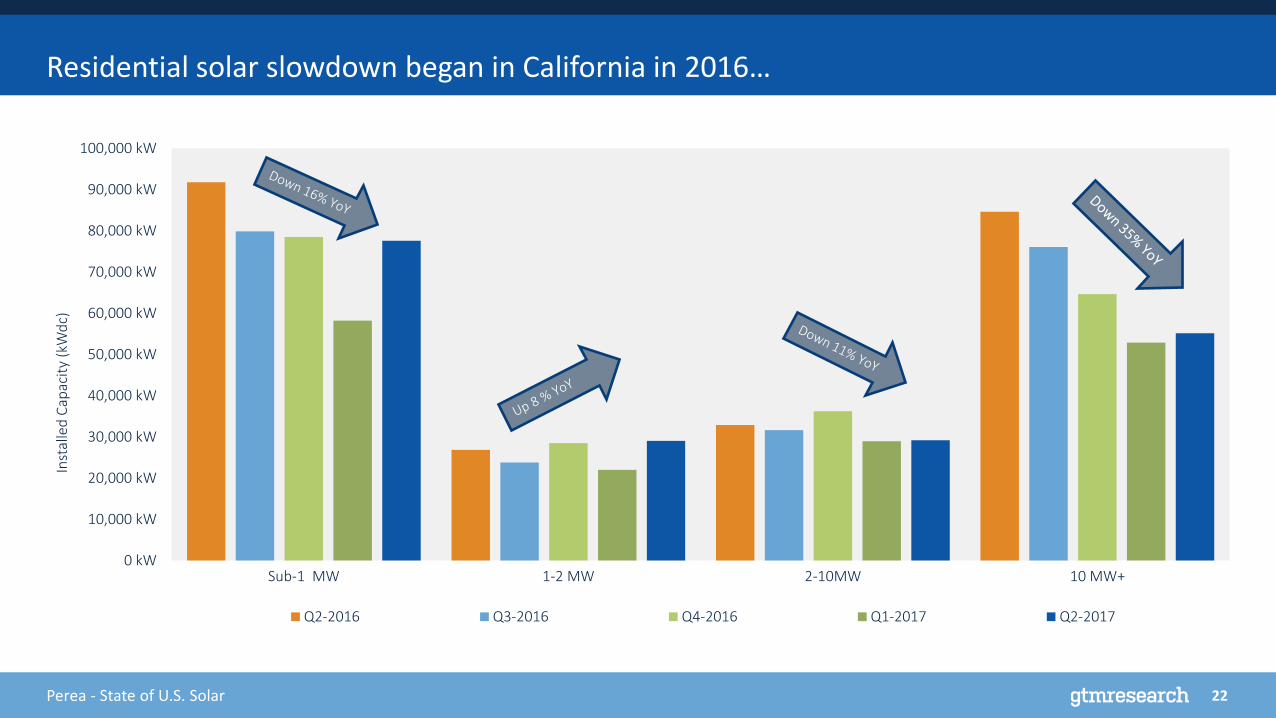

Residential solar slowdown began in California in 2016…

0 kW

10,000 kW

20,000 kW

30,000 kW

40,000 kW

50,000 kW

60,000 kW

70,000 kW

80,000 kW

90,000 kW

100,000 kW

Sub-1 MW 1-2 MW 2-10MW 10 MW+

Inst

alle

d C

apac

ity

(kW

dc)

Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017

23Perea - State of U.S. Solar

U.S. Solar Market Outlook: Resumption of market growth in 2019

0.9 1.9

3.4

4.8

6.2 7.5

15.0

12.5

11.1

13.1

15.0 16.3

17.4

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

An

nu

al P

V In

stal

lati

on

s (G

Wd

c)

Residential Non-Residential Utility

Resumption of total market growth

Return to 2016 installation levels