Q2 2018 Investor Presentation -...

22

ServiceMaster Q2 2018 Investor Presentation May 2018

Transcript of Q2 2018 Investor Presentation -...

ServiceMaster

Q2 2018 Investor Presentation

May 2018

1

Cautionary Statements

Safe Harbor Statement

This presentation contains “forward-looking statements,” including 2018 revenue and Adjusted EBITDA outlook, organic revenue growth

projections, as well as statements with respect to the potential separation of AHS from ServiceMaster and the distribution of AHS shares

to ServiceMaster shareholders, that are based on management’s beliefs and assumptions and on information currently available to

management. Most forward-looking statements contain words that identify them as forward-looking, such as “anticipates,” “believes,”

“continues,” “could,” “seeks,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “will,” “would” or

similar expressions and the negatives of those terms that relate to future events. Forward-looking statements involve known and unknown

risks, uncertainties and other factors that may cause ServiceMaster’s actual results, performance or achievements to be materially

different from any projected results, performance or achievements expressed or implied by the forward-looking statements. Forward-

looking statements represent the beliefs and assumptions of ServiceMaster only as of the date of this presentation and ServiceMaster

undertakes no obligation to update or revise publicly any such forward-looking statements, whether as a result of new information, future

events or otherwise. As such, ServiceMaster’s future results may vary from any expectations or goals expressed in, or implied by, the

forward-looking statements included in this presentation, possibly to a material degree. ServiceMaster cannot assure you that the

assumptions made in preparing any of the forward-looking statements will prove accurate or that any long-term financial or operational

goals and targets will be realized. For a discussion of some of the important factors that could cause ServiceMaster’s results to differ

materially from those expressed in, or implied by, the forward-looking statements included in this presentation, investors should refer to the

disclosure contained under the heading “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2017 and our

other filings with the SEC.

Note to Non-GAAP Financial Measures

This presentation contains certain non-GAAP financial measures. Non-GAAP measures should not be considered as an alternative to

GAAP financial measures. Non-GAAP measures may not be calculated or comparable to similarly titled measures of other companies.

See non-GAAP reconciliations below in this presentation for a reconciliation of these measures to the most directly comparable GAAP

financial measures. Adjusted EBITDA, adjusted net income, adjusted earnings per share and free cash flow are not measurements of the

Company’s financial performance under GAAP and should not be considered as an alternative to net income, net cash provided by

operating activities from continuing operations or any other performance or liquidity measures derived in accordance with GAAP.

Management uses these non-GAAP financial measures to facilitate operating performance and liquidity comparisons, as applicable, from

period to period. We believe these non-GAAP financial measures are useful for investors, analysts and other interested parties as they

facilitate company-to-company operating performance and liquidity comparisons, as applicable, by excluding potential differences caused

by variations in capital structures, taxation, the age and book depreciation of facilities and equipment, restructuring initiatives and equity-

based, long-term incentive plans.

2

ServiceMaster At A Glance

$2.9B Revenue

$685M Adjusted

EBITDA

8 years Consecutive

Revenue &

Adjusted EBITDA

Growth

23%Adjusted

EBITDA

Margin

Selected Q1 2018 LTM Financial Data

ServiceMaster helps make the

homeowner’s life easier every step of the

way. Our extensive portfolio of home and

commercial services include cleaning,

disaster restoration, home warranties,

furniture and cabinet restoration,

inspections, mold remediation, pest

control and fire and water damage

restoration. Our unmatched network of

trusted employees, technicians,

contractors and franchisees reach into

more than 75,000 homes and businesses

each day.

3

Q1 2018 Investment Highlights

1See Appendix for Non-GAAP Reconciliations and Non-GAAP Reconciliation Definitions.

2Adjusted earnings per share (EPS) is calculated as adjusted net income divided by the diluted share counts of 135.4M shares and 137.3M shares for full-year 2017 and 2016, respectively.

4

$80

$100

$120

$140

$160

$180

$200

$220

$240

$260

$280

$300

$320

6/2

6/2

01

4

12/3

1/2

01

4

12/3

1/2

01

5

12/3

0/2

01

6

12/2

9/2

01

7

5/3

/20

18

SERV S&P 500 Index S&P 400 Consumer Service Index

Delivering Significant Returns To Shareholders

195%

Data From: June 26, 2014 – May 3, 2018

62%

45%

S & P 400 Consumer

Services Index

S & P 500 Index

We continue to outperform the major indices

Scale

: June 2

6,

2014 p

rices =

$100

5

Tax-Free American Home Shield Spin

6

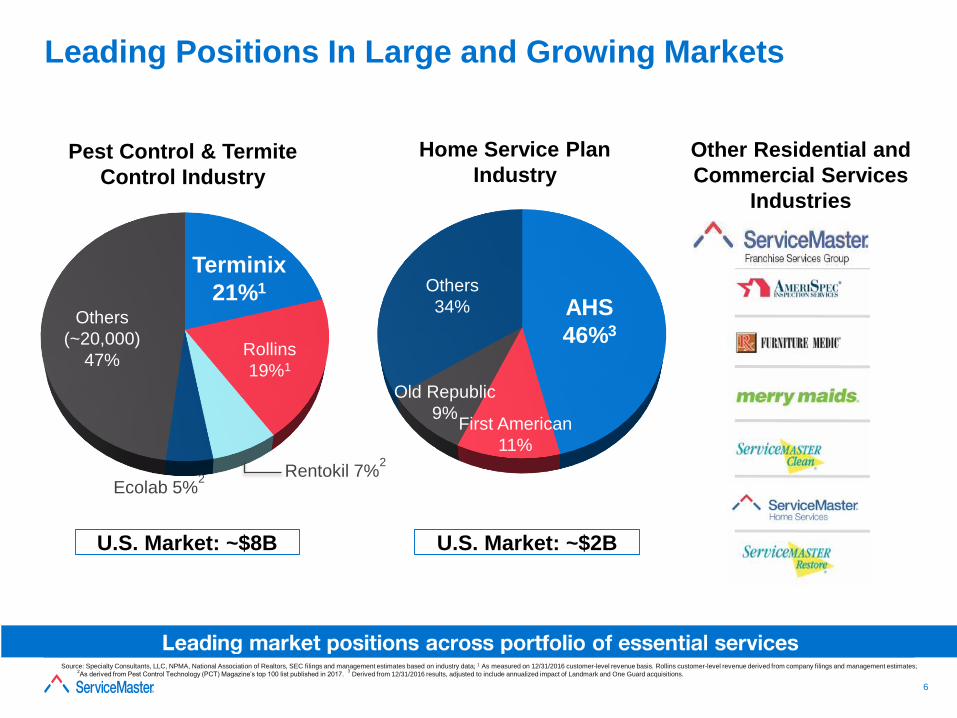

Source: Specialty Consultants, LLC, NPMA, National Association of Realtors, SEC filings and management estimates based on industry data; 1 As measured on 12/31/2016 customer-level revenue basis. Rollins customer-level revenue derived from company filings and management estimates; 2As derived from Pest Control Technology (PCT) Magazine’s top 100 list published in 2017.

3Derived from 12/31/2016 results, adjusted to include annualized impact of Landmark and One Guard acquisitions.

Terminix

21%1

Rollins

19%1

Others

(~20,000)

47%

U.S. Market: ~$8B U.S. Market: ~$2B

AHS

46%3

First American

11%

Old Republic

9%

Others

34%

Rentokil 7%2

Ecolab 5%2

Leading Positions In Large and Growing Markets

Pest Control & Termite

Control Industry

Home Service Plan

Industry

Other Residential and

Commercial Services

Industries

7

Terminix Overview

Q1’18LTM Revenue/CLR: $1.5B/$1.9B Q1’18LTM Adj. EBITDA: $335M Q1’18LTM Adj. EBITDA margin: 22%

Leading provider of U.S extermination services

Operate in 19 countries and 47 U.S. states

U.S. locations include ~400 company-owned and

franchise branches

Large and attractive U.S. market (~$8B)

Competitive strengths include scale and expertise

Positioned for growth in core and new services

1,3701,444

1,524 1,541 1,544

23%24% 24%

21% 22%

10%

20%

30%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2014 2015 2016 2017 Q1'18LTM

Revenue ($millions) Adj. EBITDA Margin

Historical Revenue and Adj. EBITDA Margin

8

Implement disciplined, Lean Six Sigma

approach

Rebuild a strong commercial business

Reinforce accountability

Empower our technicians to deliver an

exceptional customer experience

Build a strong leadership team

Progress on Terminix Business Transformation

9

• Driving strong focus on the

commercial pest control space:

- Adding strong leadership

- Investing in process control and

technology

- Driving systematic efforts to

improve service capabilities

- Rebuilding relationships with key

customers

• Leveraging best-in-class

capabilities, leadership and process

from our newest Copesan brands

Rebuild a Strong Commercial Business

10

American Home Shield Overview

Q1’18LTM Revenue: $1.2B Q1’18LTM Adj. EBITDA: $262M Q1’18LTM Adj. EBITDA Margin: 22%

Leading provider of home warranties in the U.S.

Serves 2M customers in 50 states

Significant market leadership: 4x larger than nearest

competitors

75% customer retention rates

National network of ~15,000 contractors

Significant direct-to-consumer marketing and lead

generation capabilities

828917

1,020

1,157 1,176

22% 22% 22% 22% 22%

10%

20%

30%

0

200

400

600

800

1,000

1,200

1,400

2014 2015 2016 2017 Q1'18LTM

Revenue ($millions) Adjusted EBITDA Margin

Historical Revenue and Adj. EBITDA Margin

11

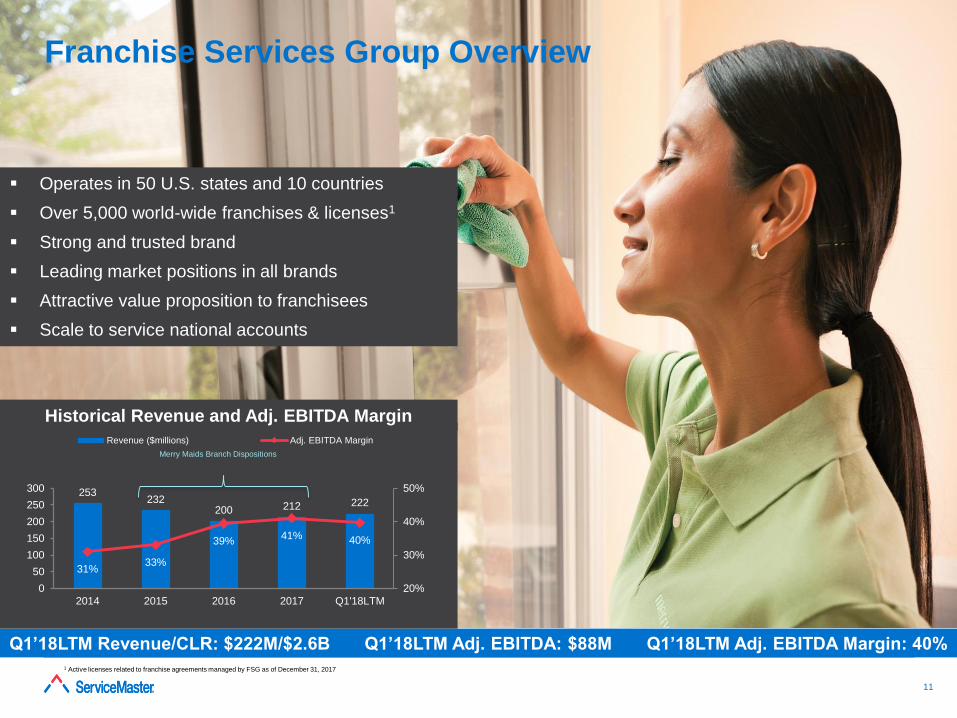

1 Active licenses related to franchise agreements managed by FSG as of December 31, 2017

Franchise Services Group Overview

Q1’18LTM Revenue/CLR: $222M/$2.6B Q1’18LTM Adj. EBITDA: $88M Q1’18LTM Adj. EBITDA Margin: 40%

Operates in 50 U.S. states and 10 countries

Over 5,000 world-wide franchises & licenses1

Strong and trusted brand

Leading market positions in all brands

Attractive value proposition to franchisees

Scale to service national accounts

253232

200 212 222

31%33%

39%41% 40%

20%

30%

40%

50%

0

50

100

150

200

250

300

2014 2015 2016 2017 Q1'18LTM

Revenue ($millions) Adj. EBITDA Margin

Merry Maids Branch Dispositions

Historical Revenue and Adj. EBITDA Margin

12

557

622667

678 685

23% 24% 24% 23% 23%

2014 2015 2016 2017 Q1'18 LTM

Ad

j. E

BIT

DA

Ma

rgin

274

3583262 338

348

49%

58%

49% 50% 51%

2014 2015 2016 2017 1Q'18 LTM

% o

f A

dj. E

BIT

DA

Revenue ($millions)

2,4572,594

2,7462,912 2,944

2014 2015 2016 2017 Q1'18 LTM

CAGR = 5.7% Adjusted EBITDA ($millions) CAGR = 6.6%

Free Cash Flow1,2 ($millions) Net Debt / Adjusted EBITDA

5.0x

4.2x 4.1x

3.7x 3.7x

2014 2015 2016 2017 1Q'18 LTM

Consistent Financial Performance

1 Free Cash Flow is defined in the appendix. 2 2016 Free Cash Flow excludes the impact of $56 million, net of tax in payments, on fumigation related matters.

13

Leverage relationships with insurance companies

Accelerate national accounts growth

Extend reach & growth beyond core areas

Extend current product offerings

Expand into adjacent markets

Increase market penetration using world-class service

Achieve world-class customer service

Expand commercial business

Execute business transformation

Strategic Growth Priorities

14

We Deliver

We Care

We Serve

ServiceMaster Shared Vision

Appendix

16

2Adjusted earnings per share (EPS) is calculated as adjusted net income divided by the diluted share counts of 135.6M shares and 136.0M shares for the first quarter of 2018

and 2017, respectively.

1See Non-GAAP Reconciliations and Non-GAAP Reconciliation Definitions.

• Continued strong organic revenue growth at AHS driven by new unit sales growth

and improved price realization

• Strong revenue growth at FSG, driven by higher disaster restoration royalty fees and

janitorial national accounts revenue growth

• Terminix improved margins, primarily due to benefits from business productivity

initiatives

($ millions, except EPS) Q1 2018 Q1 2017

Revenue 675$ 643$ 32$ 5%

Adjusted EBITDA1

141$ 134$ 7$ 5%

Margin 20.9% 20.8%

Adjusted Net Income1

59$ 46$ 14$ 30%

Margin 8.8% 7.2%

Adjusted EPS1,2 0.44$ 0.34$ 0.10$ 30%

Variance

Q1 2018 Consolidated Financial Summary

17

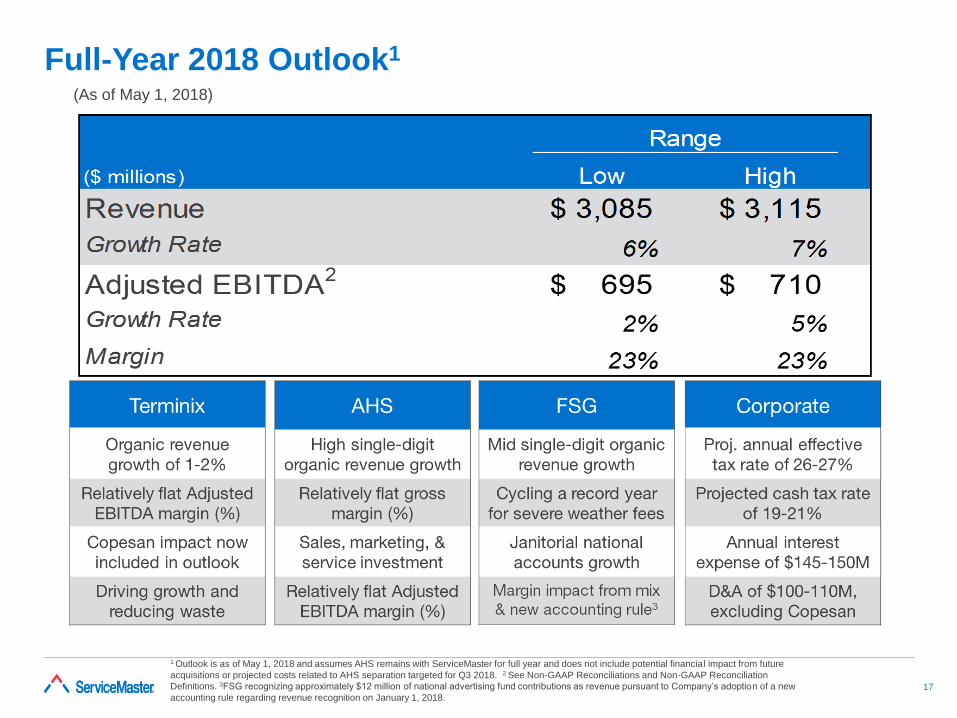

Full-Year 2018 Outlook1

1 Outlook is as of May 1, 2018 and assumes AHS remains with ServiceMaster for full year and does not include potential financial impact from future

acquisitions or projected costs related to AHS separation targeted for Q3 2018. 2 See Non-GAAP Reconciliations and Non-GAAP Reconciliation

Definitions. 3FSG recognizing approximately $12 million of national advertising fund contributions as revenue pursuant to Company’s adoption of a new

accounting rule regarding revenue recognition on January 1, 2018.

(As of May 1, 2018)

18

Non-GAAP Reconciliation Definitions

Adjusted EBITDA is defined as net income before: depreciation and amortization expense;

401(k) Plan corrective contribution; fumigation related matters; insurance reserve

adjustment; non-cash stock-based compensation expense; restructuring charges; American

Home Shield spin-off charges; gain on sale of Merry Maids branches; non-cash impairment

of software and other related costs; (income) loss from discontinued operations, net of

income taxes; provision for income taxes; loss on extinguishment of debt; management and

consulting fees; consulting agreement termination fees; other non-operating expenses and

interest expense.

Adjusted net income is defined as net income before: amortization expense; 401(k) Plan

corrective contribution; fumigation related matters; insurance reserve adjustment;

restructuring charges; American Home Shield spin-off charges; gain on sale of Merry Maids

branches; impairment of software and other related costs; (income) loss from discontinued

operations, net of income taxes; loss on extinguishment of debt; the tax impact of the

aforementioned adjustments and the impact of the tax law changes on deferred taxes.

Adjusted earnings per share is calculated as adjusted net income divided by the

weighted-average diluted common shares outstanding.

Free Cash Flow is defined as net cash provided from operating activities from continuing

operations; plus cash paid for consulting agreement termination fees; less property

additions, net of government grant fundings for property additions.

19

Adjusted EBITDA Reconciliation

2014 2015 2016 2017Q1 2018

LTMNet Income (Loss) ($57) $160 $155 $510 $511

Reconciliation to Adjusted EBITDA:

(Income) Loss from discontinued operations, net of income taxes 100 2 1 (0) 0

Depreciation & amortization expense 100 85 94 103 103

401(k) Plan corrective contribution - 23 2 (3) (3)

Fumigation related matters - 9 93 4 4

Insurance reserve adjustment - - 23 - -

Non-cash stock-based compensation expense 8 10 13 12 11

Management and consulting fees 4 - - - -

Consulting agreement termination fees 21 - - - -

Non-cash impairment of software and other related costs 47 - 1 2 -

Restructuring charges 11 5 17 34 44

American Home Shield spin-off charges - - - - 7

(Benefit) Provision for income taxes 40 107 85 (139) (149)

Interest expense 219 167 153 150 151

Loss on extinguishment of debt 65 58 32 6 6

Gain on sale of Merry Maids branches (1) (7) (2) 0 (0)

Other non-operating expenses - 3 - 0 0

Total Adjustments 613 462 512 168 174

Adjusted EBITDA $557 $622 $667 $678 $685

Terminix 309 347 371 330 335

American Home Shield 179 205 220 260 262

Franchise Services Group 78 77 79 87 88

Other Operations & Headquarters (9) (9) (3) 1 1

Adjusted EBITDA $557 $622 $667 $678 $685

20

2014 2015 2016 2017 Q1 2018 LTM

Net Cash Provided from Operating Activities from Continuing Operations1 $289 $398 $325 $413 $428

Reconciliation to Free Cash Flow:

Cash paid for consulting agreement termination fees 21 - - - -

Property additions, net of government grant fundings for property additions (35) (40) (56) (75) (80)

Free Cash Flow2 $274 $358 $270 $338 $348

1 As a result of the early adoption of Accounting Standards Updates 2016-09 and 2016-15, $13 million of excess tax benefits for 2015 were retrospectively presented as an

operating activity, and $49 million, and $35 million of call premium paid on retirement of debt, net of premium received on issuance of debt for 2015, and 2014 respectively, were

retrospectively presented as financing activities. 2 2016 Free Cash Flow includes the impact of $56 million, net of tax, in payments on fumigation related matters

Free Cash Flow Reconciliation

21

Q1 2018 Net Income to Adjusted EBITDA and Adjusted Net Income Reconciliations

$ millions, except per share data

Net Income $ 40 $ 39

Depreciation and amortization expense 25 25

Fumigation related matters — 1

Non-cash stock-based compensation expense 4 5

Restructuring charges 12 2

American Home Shield spin-off charges 7 —

Non-cash impairment of software and other related costs — 2

Income from discontinued operations, net of income taxes — (1)

Provision for income taxes 14 24

Interest expense 37 37

Adjusted EBITDA $ 141 $ 134

Terminix $ 86 $ 81

American Home Shield 32 31

Franchise Services Group 23 21

Corporate — —

Adjusted EBITDA $ 141 $ 134

Net Income $ 40 $ 39

Amortization expense 5 7

Fumigation related matters — 1

Restructuring charges 12 2

American Home Shield spin-off charges 7 —

Impairment of software and other related costs — 2

Income from discontinued operations, net of income taxes — (1)

Tax impact of adjustments (6) (5)

Adjusted Net Income $ 59 $ 46

Weighted-average diluted common shares outstanding 135.6 136.0

Adjusted Earnings Per Share $ 0.44 $ 0.34

First Quarter

2018 2017