Q1 2015 Conference Call - Moodle - Université Lille...

63

Q1 2015 Conference Call April 30, 2015

Transcript of Q1 2015 Conference Call - Moodle - Université Lille...

Q1 2015 Conference CallApril 30, 2015

Agenda

Mark Alles, President & Chief Operating Officer

Peter Kellogg, Chief Financial Officer

Jackie Fouse, President, Global Hematology & Oncology

Scott Smith, President, Global I&I

B b H i Ch i & Chi f E ti Offi

Q&A

Bob Hugin, Chairman & Chief Executive Officer

2

Q&A

Forward Looking Statements and Adjusted Financial Information

This presentation contains forward-looking statements, which are generally statements that are nothistorical facts. Forward-looking statements can be identified by the words “expects,” “anticipates,”“believes,” “intends,” “estimates,” “plans,” “will,” “outlook” and similar expressions. Forward-looking, , , p , , p gstatements are based on management’s current plans, estimates, assumptions and projections, andspeak only as of the date they are made. We undertake no obligation to update any forward-lookingstatement in light of new information or future events, except as otherwise required by law. Forward-looking statements involve inherent risks and uncertainties, most of which are difficult to predict andare generally beyond our control Actual results or outcomes may differ materially from those impliedare generally beyond our control. Actual results or outcomes may differ materially from those impliedby the forward-looking statements as a result of the impact of a number of factors, many of whichare discussed in more detail in our Annual Report on Form 10-K and our other reports filed with theSecurities and Exchange Commission.

In addition to financial information prepared in accordance with U.S. GAAP, this presentation alsocontains adjusted financial measures that we believe provide investors and management withsupplemental information relating to operating performance and trends that facilitate comparisonsbetween periods and with respect to projected information. These adjusted financial measures arenon-GAAP and should be considered in addition to but not as a substitute for the informationnon GAAP and should be considered in addition to, but not as a substitute for, the informationprepared in accordance with U.S. GAAP. We typically exclude certain GAAP items thatmanagement does not believe affect our basic operations and that do not meet the GAAP definitionof unusual or non-recurring items. Other companies may define these measures in different ways.Further information relevant to the interpretation of adjusted financial measures, and reconciliations

f th dj t d fi i l t th t bl GAAP b f d

3

of these adjusted financial measures to the most comparable GAAP measures, may be found onCelgene’s website at www.Celgene.com in the “Investor Relations” section.

Mark Alles

Q1 2015: Strong Growth and Investment for the Future

Outstanding Financial ResultsOutstanding Financial Results

– Strong top- and bottom-line growth – Continued operating momentum with improving adjusted margins

– Growth of key products driven by increased market share and duration

Strong Performance Across All Operating MetricsStrong Performance Across All Operating Metrics

– Significant global regulatory approvals across the portfolio

Building for the FutureBuilding for the Future

– Advancing early- to mid-stage pipeline programs– Investing in next generation growth drivers

gg

5

Peter Kellogg

Q1 2015 Financial Highlights

Strong Q1 E ec tion Pro ides Fo ndation for F t re Gro thStrong Q1 E ec tion Pro ides Fo ndation for F t re Gro thStrong Q1 Execution Provides Foundation for Future GrowthStrong Q1 Execution Provides Foundation for Future Growth

Q1 Product Approvals Provide New Growth DriversQ1 Product Approvals Provide New Growth Drivers

Investing in Next-Generation Growth DriversInvesting in Next-Generation Growth Drivers

Executing a Balanced Capital Allocation StrategyExecuting a Balanced Capital Allocation Strategy

7

Executing a Balanced Capital Allocation Strategy Executing a Balanced Capital Allocation Strategy

Total Net Product Sales(Growth Rates = Growth vs. Prior Year Period)

$1,708

$2,055

s

$1,429

$ M

illio

ns

↑15% ↑19% ↑20%

Q1:13 Q1:14 Q1:15

8

Volume Drove Q1 2015 Growth

Contribution to Q1:15 Net Product Sales Growth(Growth Rates = Growth vs. Prior Year Period)

$2 000

↑20.4%↓1.6%↑19.3% ↑2.7%

$1,500

$2,000

lions

$1,000

Mill

$0

$500

$0Q1:14 Volume Price Fx / Hedge Q1:15

9

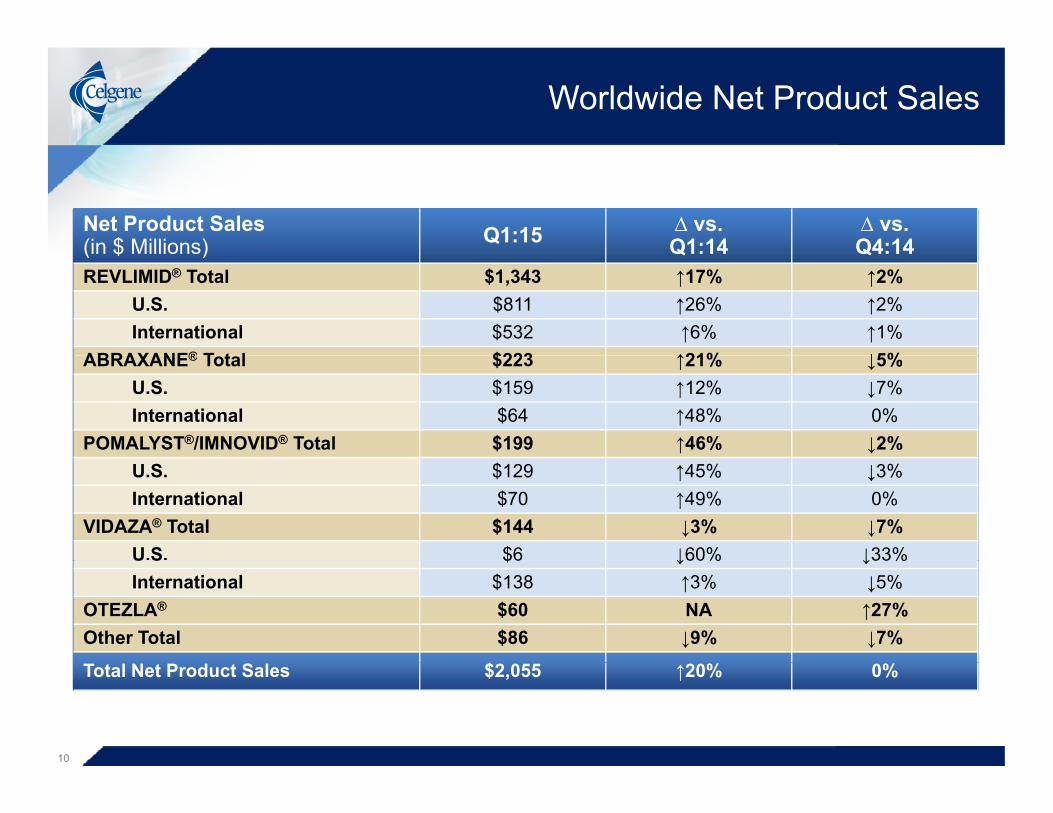

Worldwide Net Product Sales

Net Product Sales(in $ Millions) Q1:15 ∆ vs.

Q1:14∆ vs.Q4:14(in $ Millions) Q1:14 Q4:14

REVLIMID® Total $1,343 ↑17% ↑2%U.S. $811 ↑26% ↑2%International $532 ↑6% ↑1%

ABRAXANE® T t l $223 ↑21% ↓5%ABRAXANE® Total $223 ↑21% ↓5%U.S. $159 ↑12% ↓7%International $64 ↑48% 0%

POMALYST®/IMNOVID® Total $199 ↑46% ↓2%U.S. $129 ↑45% ↓3%International $70 ↑49% 0%

VIDAZA® Total $144 ↓3% ↓7%U.S. $6 ↓60% ↓33%U S $6 ↓60% ↓33%International $138 ↑3% ↓5%

OTEZLA® $60 NA ↑27%Other Total $86 ↓9% ↓7%

$

10

Total Net Product Sales $2,055 ↑20% 0%

Adjusted Diluted Earnings Per Share(Growth Rate = Growth vs. Prior Year Period)

$1 07

$0.83

$1.07

e

$0.68$

Per S

hare

↑27% ↑22%Dol

lars

↑29%

Q1:13 Q1:14 Q1:15

11

Footnote: Adjusted EPS is split-adjusted for Q1:13 and Q1:14

Key P&L Line Items (Adjusted)

Q1:15 ∆ vs. ∆ vs.Q1:15 Q1:14 Q4:14

Product Gross Margin 95.3% 0 bps 0 bps

R&D expenses% of revenue

$431M 20.7%

0 bps ↓220 bps

SG&A expenses $463MSG&A expenses% of revenue

$463M 22.3%

↓190 bps ↓70 bps

Operating Margin 52.4% ↑190 bps ↑280 bps

Effective Tax Rate 15.7% ↓90 bps ↑40 bps

12

Q1 2015 Adjusted Diluted EPS Growth Driven by Increased Operating Income

Contribution to Q1:15 Adjusted Diluted EPS

$1.07$0.21$0.83 $0.01 $0.02$0.00

Shar

eD

olla

rs P

er

Q1:14 Operating Financial Tax Rate Share Q1:15

D

Q p gIncome Income /

ExpenseCount

Q

13

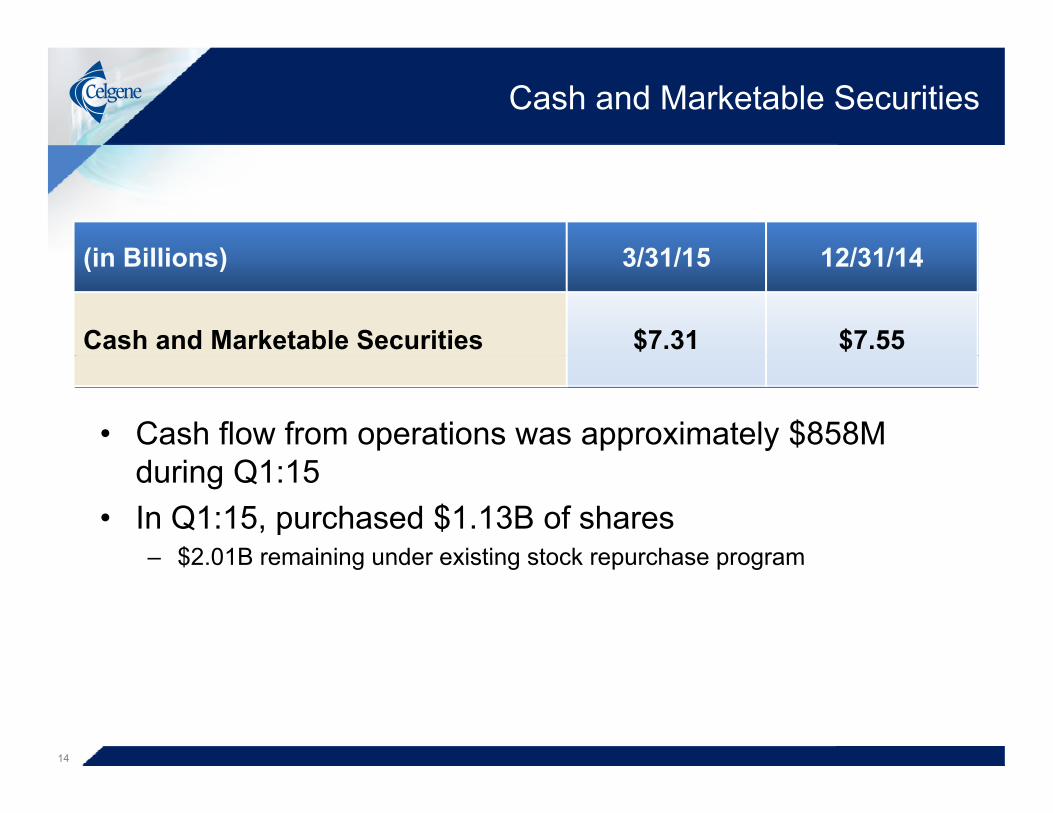

Cash and Marketable Securities

(in Billions) 3/31/15 12/31/14(in Billions) 3/31/15 12/31/14

Cash and Marketable Securities $7.31 $7.55

• Cash flow from operations was approximately $858M during Q1:15

• In Q1:15, purchased $1.13B of shares– $2 01B remaining under existing stock repurchase program$2.01B remaining under existing stock repurchase program

14

Focused on Returns

45 0%$14 0

ROIC

35.0%

40.0%

45.0%

$10.0

$12.0

$14.0

20.0%

25.0%

30.0%

$6.0

$8.0

$10.0

illio

n

5 0%

10.0%

15.0%

$2.0

$4.0

$ B

i

Average Invested Capital0.0%

5.0%

$0.02009 2010 2011 2012 2013 2014 2015 (TTM)

Capital Base Excluding Cash* Capital Base ROIC Excluding Cash* ROIC

Average Invested Capital

Cap ta ase c ud g Cas Cap ta ase O C c ud g Cas O C

15

* For purposes of this calculation, cash includes cash and cash equivalents and marketable securities available for sale.

Footnote: Refer to reconciliation tables for ROIC calculation methodology. Calculation revised in 2015 for all prior periods to reflect amortization of certain charges excluded from 2008 calculation.

Q1 2015 Summary

Q1 P f D i b S l V l G th d O ti LQ1 P f D i b S l V l G th d O ti LQ1 Performance Driven by Sales Volume Growth and Operating LeverageQ1 Performance Driven by Sales Volume Growth and Operating Leverage

Q1 Product Approvals Expected to Begin Contributing in Q2 and BeyondQ1 Product Approvals Expected to Begin Contributing in Q2 and Beyond

Investments in Next-Generation Growth Drivers On-GoingInvestments in Next-Generation Growth Drivers On-Going

Reaffirming 2015 Adjusted GuidanceReaffirming 2015 Adjusted Guidance

16

g jg j

Jackie Fouse

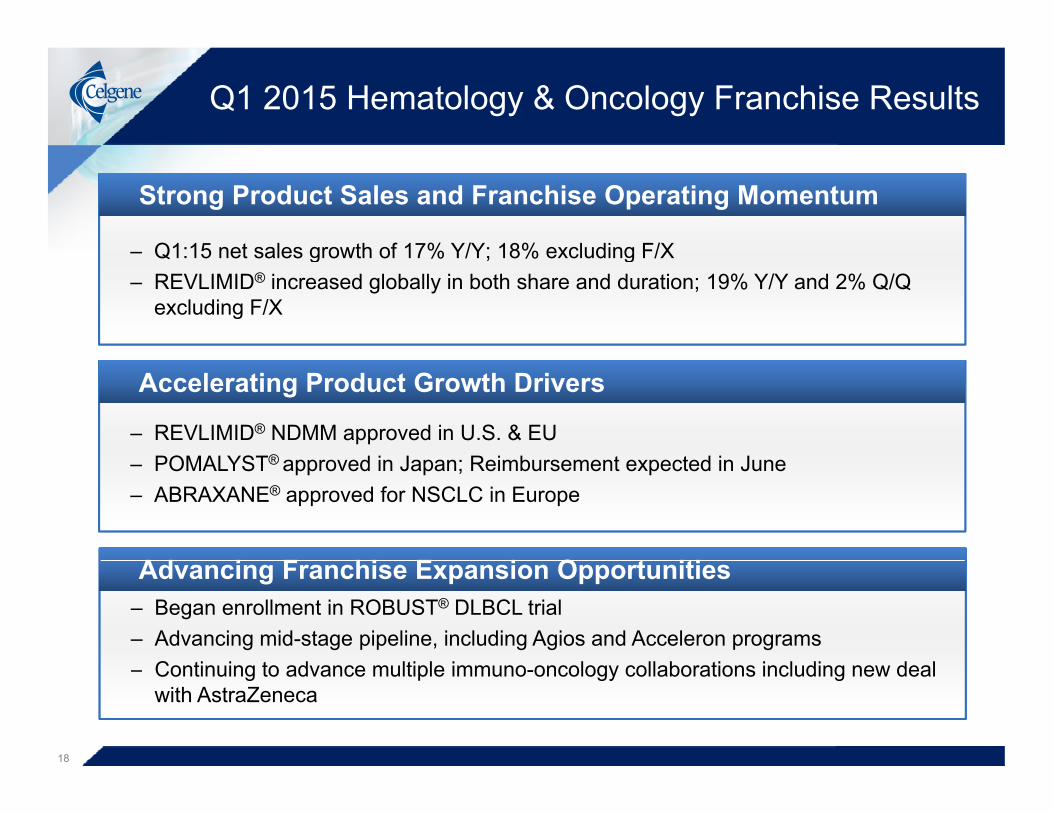

Q1 2015 Hematology & Oncology Franchise Results

– Q1:15 net sales growth of 17% Y/Y; 18% excluding F/X

Strong Product Sales and Franchise Operating MomentumStrong Product Sales and Franchise Operating Momentum

– Q1:15 net sales growth of 17% Y/Y; 18% excluding F/X– REVLIMID® increased globally in both share and duration; 19% Y/Y and 2% Q/Q

excluding F/X

– REVLIMID® NDMM approved in U.S. & EUPOMALYST® d i J R i b t t d i J

Accelerating Product Growth DriversAccelerating Product Growth Drivers

– POMALYST® approved in Japan; Reimbursement expected in June– ABRAXANE® approved for NSCLC in Europe

Ad i F hi E i O t itiAd i F hi E i O t iti– Began enrollment in ROBUST® DLBCL trial– Advancing mid-stage pipeline, including Agios and Acceleron programs

C ti i t d lti l i l ll b ti i l di d l

Advancing Franchise Expansion OpportunitiesAdvancing Franchise Expansion Opportunities

18

– Continuing to advance multiple immuno-oncology collaborations including new deal with AstraZeneca

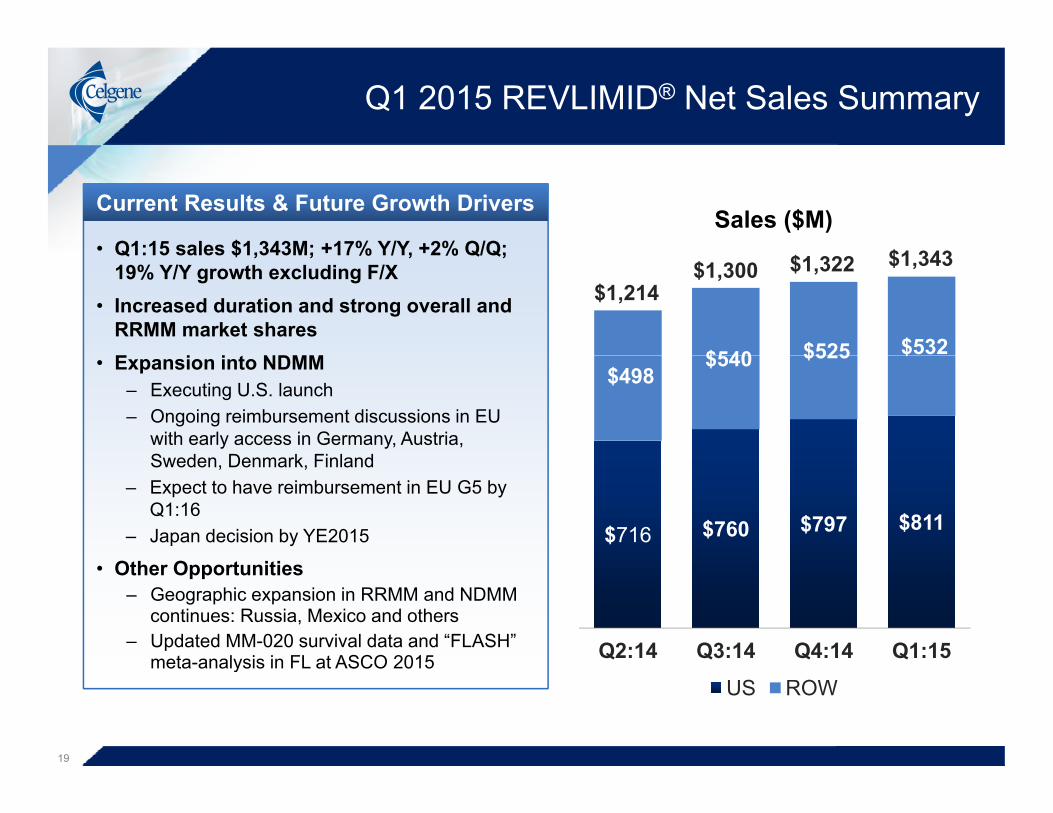

Q1 2015 REVLIMID® Net Sales Summary

Current Results & Future Growth DriversCurrent Results & Future Growth Drivers

• Q1:15 sales $1,343M; +17% Y/Y, +2% Q/Q;Sales ($M)

$1 343Q1:15 sales $1,343M; +17% Y/Y, +2% Q/Q; 19% Y/Y growth excluding F/X

• Increased duration and strong overall and RRMM market shares E i i NDMM $540 $525 $532

$1,214$1,300 $1,322 $1,343

• Expansion into NDMM– Executing U.S. launch – Ongoing reimbursement discussions in EU

with early access in Germany, Austria, Sweden Denmark Finland

$498 $540 $525 $

Sweden, Denmark, Finland– Expect to have reimbursement in EU G5 by

Q1:16– Japan decision by YE2015 $716 $760 $797 $811

• Other Opportunities– Geographic expansion in RRMM and NDMM

continues: Russia, Mexico and others– Updated MM-020 survival data and “FLASH”

meta-analysis in FL at ASCO 2015 Q2:14 Q3:14 Q4:14 Q1:15

19

meta-analysis in FL at ASCO 2015US ROW

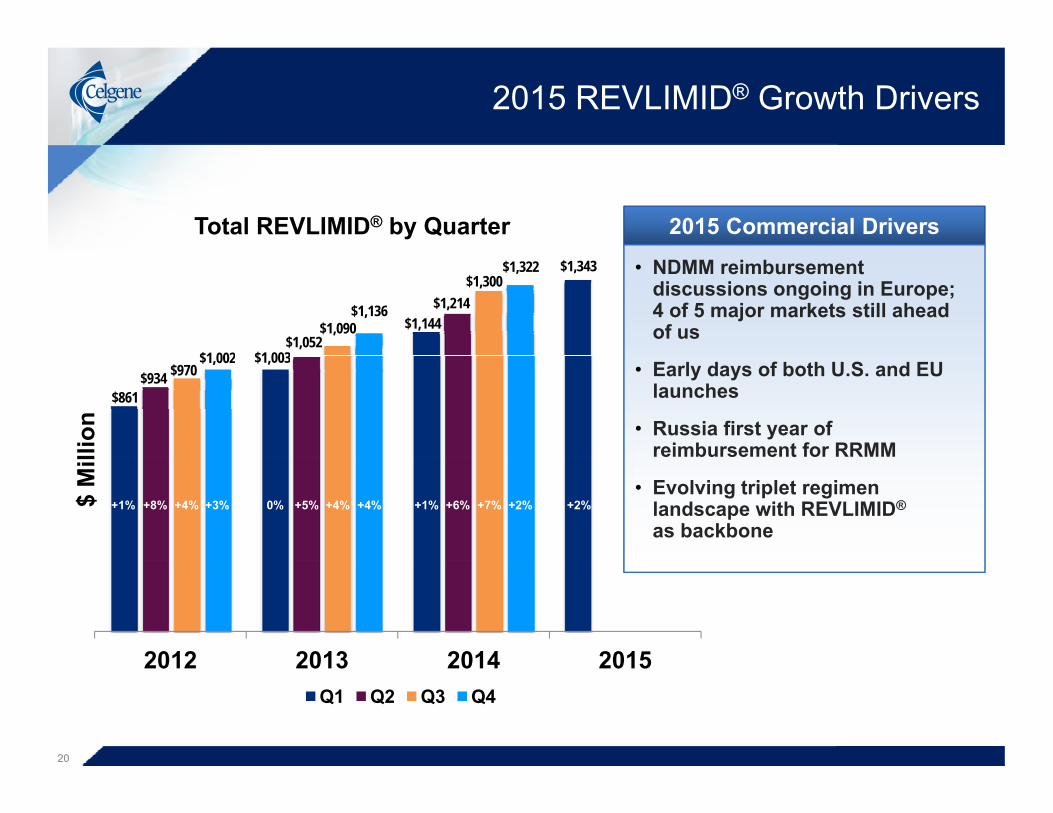

2015 REVLIMID® Growth Drivers

Total REVLIMID® by Quarter 2015 Commercial Drivers

$1 003

$1,144

$1,343

$1,052

$1,214$1,090

$1,300

$1 002

$1,136

$1,322 • NDMM reimbursement discussions ongoing in Europe; 4 of 5 major markets still ahead of us

$861

$1,003$934 $970

$1,002 • Early days of both U.S. and EU launches

• Russia first year of reimbursement for RRMMlli

on

+2%+1% +6% +7% +2% +2%+5% +4% +4% +1%+8% +4% +3% 0%

• Evolving triplet regimen landscape with REVLIMID®

as backbone

$ M

il

2012 2013 2014 20150%

2012 2013 2014 2015Q1 Q2 Q3 Q4

20

Q1 2015 POMALYST®/IMNOVID® Sales Summary

Current Results & Future Growth DriversCurrent Results & Future Growth Drivers

$202• Q1:15 sales $199M; +46% Y/Y -2% Q/QSales ($M)

$70 $70 $161$181

$202 $199Q1:15 sales $199M; +46% Y/Y, -2% Q/Q

• Expansion of POMALYST®/IMNOVID®

continues – Approval in Japan 18 months ahead of

t ti R i b t t d i J

$57 $63 expectations; Reimbursement expected in June

– U.S. label update with OS– Strong U.S. POMALYST® 3rd line+ share– Duration has been steadily increasing in the

$104 $118 $132 $129

Duration has been steadily increasing in the U.S. since launch

– EU IMNOVID® achieving rapid penetration of 3rd line+ market

• Continue to advance POMALYST®/IMNOVID®

Q2:14 Q3:14 Q4:14 Q1:15

• Continue to advance POMALYST®/IMNOVID®

combinations with other novel agents– Phase II trials with checkpoint inhibitors, HDAC

inhibitors, proteasome inhibitors enrolling

21

US ROW

2015 POMALYST®/IMNOVID® Growth Drivers

Total POMALYST®/IMNOVID® by Quarter 2015 Commercial Drivers

$199

$161

$181

$202 • Reimbursement coming for Italy, Finland, Ireland and Netherlands

• Increasing duration of treatment globally

$136

$90

$121

g y

• Japan launch in H2

• Strong growth in other markets (Australia, Canada)lli

on

$66

$90• Potential from combination data

$ M

il

$29

2013 2014 20152013 2014 2015Q1 Q2 Q3 Q4

22

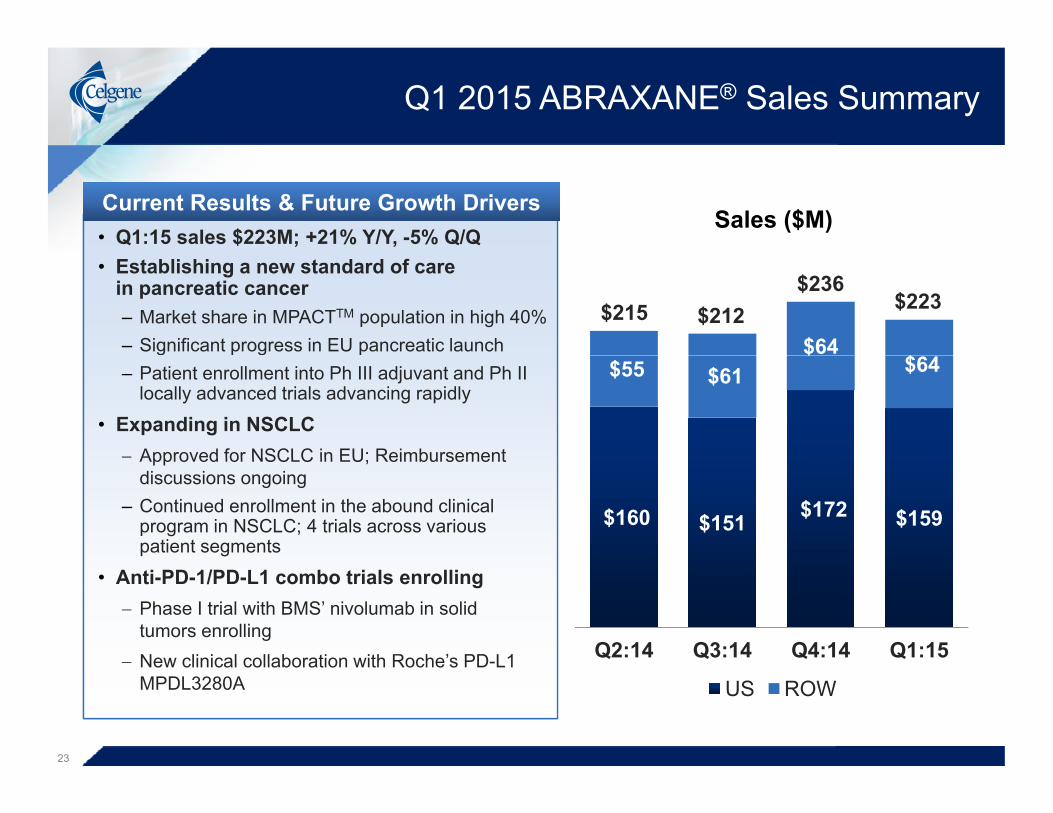

Q1 2015 ABRAXANE® Sales Summary

• Q1:15 sales $223M; +21% Y/Y, -5% Q/QCurrent Results & Future Growth DriversCurrent Results & Future Growth Drivers

Sales ($M)

$64$

$215 $212$236

$223• Establishing a new standard of care

in pancreatic cancer– Market share in MPACTTM population in high 40%– Significant progress in EU pancreatic launch

$55 $61 $

$64 – Patient enrollment into Ph III adjuvant and Ph II locally advanced trials advancing rapidly

• Expanding in NSCLC Approved for NSCLC in EU; Reimbursement

$160 $151 $172 $159

Approved for NSCLC in EU; Reimbursement discussions ongoing

– Continued enrollment in the abound clinical program in NSCLC; 4 trials across various patient segments

Q2:14 Q3:14 Q4:14 Q1:15

• Anti-PD-1/PD-L1 combo trials enrolling Phase I trial with BMS’ nivolumab in solid

tumors enrolling New clinical collaboration with Roche’s PD-L1

23

US ROWNew clinical collaboration with Roche s PD-L1 MPDL3280A

2015 ABRAXANE® Growth Drivers

$236

2015 Commercial DriversTotal ABRAXANE® by Quarter

$185

$223$215

$170

$212$202

$236 • Early days of EU pancreatic launch

• Reimbursement for PanC in Spain, Italy Q1; France, Belgium

$104

$123$110

$155

$106

$170

$106

p , y Q ; , gand others to come

• Launching in EU for NSCLC in early access markets with others still to comelli

on

$104 $106 $106

+2%

+1% +16% -1% +11% -6%+26% +10% +19% -8%+5% -3% 0% +15%• Potential in I/O combinations as

well as data readouts from ongoing Celgene trials

$ M

il

2012 2013 2014 20150%

2012 2013 2014 2015Q1 Q2 Q3 Q4

24

Clinical Data Across the Portfolio to Be Presented at Major Medical Congresses

~65 Abstracts Accepted

• Hematology®• Updated OS from FIRST®

• FLASH analysis correlating CR with PFS in 1st Line FL

• MM triplet data

ASCOASCOAcceptancesAcceptances

June 2015June 2015• Oncology

• Phase I data on demcizumab• Emerging combination data with immuno-

therapeutics

29 Abstracts Accepted

2 Oral Presentations:• Phase II data on sotatercept in lower risk MDS

MDS MDS Foundation Foundation

AcceptancesAcceptances• Phase II data on luspatercept in MDSApril 2015April 2015

49 Abstracts SubmittedPh I d PK/PD d t AG 221 i IDH 2

EHAEHASubmissionsSubmissions • Phase I and PK/PD data on AG-221 in IDH-2

mutant malignanciesSubmissionsSubmissions

June 2015June 2015

25

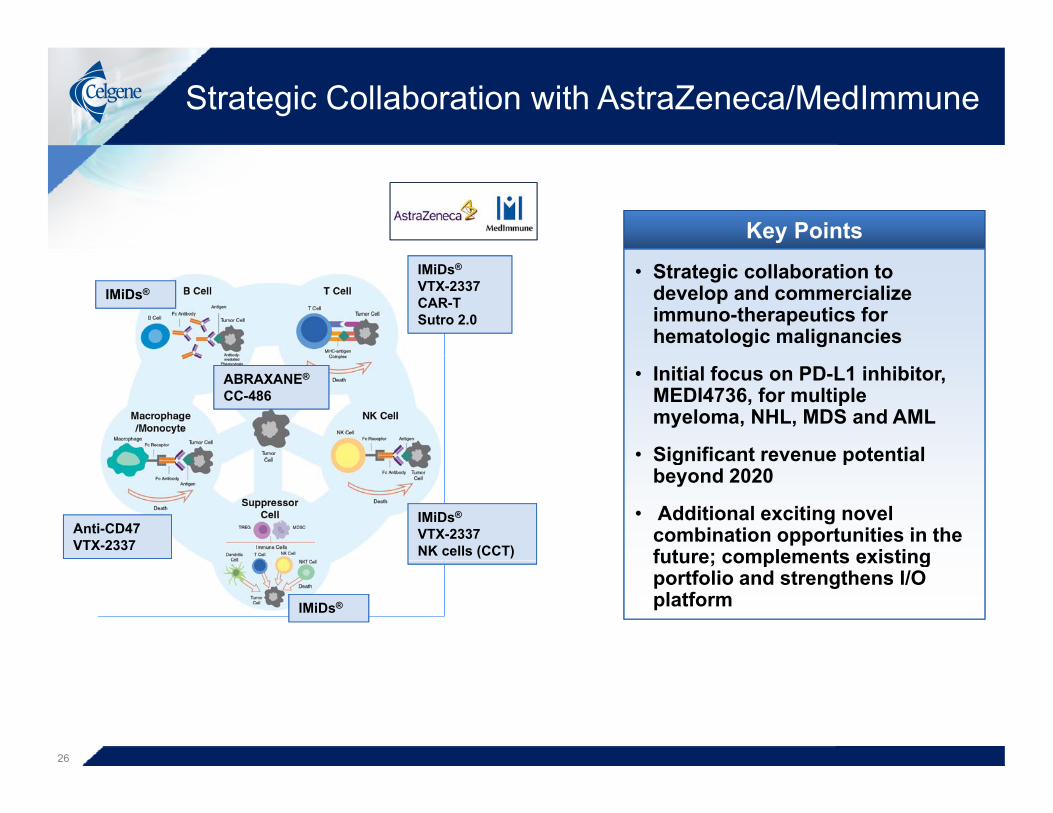

Strategic Collaboration with AstraZeneca/MedImmune

Key PointsIMiDs®

VTX-2337CAR-TSutro 2.0

IMiDs®

• Strategic collaboration to develop and commercialize immuno-therapeutics for hematologic malignancies

ABRAXANE®

CC-486• Initial focus on PD-L1 inhibitor,

MEDI4736, for multiple myeloma, NHL, MDS and AML

• Significant revenue potential

IMiDs®

VTX-2337NK cells (CCT)

Anti-CD47VTX-2337

Significant revenue potential beyond 2020

• Additional exciting novel combination opportunities in the future; complements existing

IMiDs®

future; complements existing portfolio and strengthens I/O platform

26

Scott Smith

Q1 2015 I&I Franchise Update

– Entrenching brand position in both PsA and psoriasis; Q1:15 sales $60M

Executing “Best in Class” U.S. Launch for OTEZLA®Executing “Best in Class” U.S. Launch for OTEZLA®

Entrenching brand position in both PsA and psoriasis; Q1:15 sales $60M– Over ~40,000 patients in the U.S. have been treated with OTEZLA® since launch

Expanding OTEZLA®’s Geographic FootprintExpanding OTEZLA®’s Geographic Footprint

– EU launch off to strong start• Positive early feedback from commercial launch in Germany, the UK and Nordics

Expanding OTEZLA® s Geographic FootprintExpanding OTEZLA® s Geographic Footprint

• Access broadening to increasing number of European markets– OTEZLA® approved in Australia and Canada

– Expanding lifecycle applications for OTEZLA®

– Executing pivotal program for GED-0301

Advancing Development of I&I PipelineAdvancing Development of I&I Pipeline

28

Executing pivotal program for GED 0301– Developing new products – sotatercept and CC-220

Leading Indicators Favorable for Future Growth

Source of Business Predominantly Non-BiologicLast Therapy Prior to OTEZLA®* for Psoriasis

Strong Prescription GrowthWeekly TRx

Strong Prescription GrowthWeekly TRx

2014 2015

OTEZLA (PsA/PSOR)XELJANZ (RA)CIMZIA (Crohn's)SIMPONI (RA/PsA/AS)STELARA (PsO)

15%

11%29%

Biologic

Oral Systemic

Topical

Patient Access

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

Week Since Product Launch

Depth of Prescribing

45%Naïve (No tx in prior 12 months)

30%1 TRx

Patient Access

99%Formulary Covered

Depth of PrescribingNumber of TRx per Trialist

30%

17%53%

2 TRx

≥ 3 TRx

72%

0% 20% 40% 60% 80% 100%

Adjudicated OTEZLA® Claims**

Note: STELARA TRx launch aligned based on 4 week trailing average; TRx reflects total number of new and refill prescriptions to-date; Symphony data subject to restatement; Source of Business includes both add-on and switch patients; *Based on 12-month window. **Includes titration, bridge and PAP. Source: IMS SMART. through week ending April 17, 2015; Symphony Prescriber; through week ending March 20, 2015; SHA PTD claims data (Jan’15 feed for month ending Nov’14)

29

0% 20% 40% 60% 80% 100%

In “New-to-Brand” Patient Share, OTEZLA® Achieved Lead Positions in Both PsA and Psoriasis

New to Brand Share – PsA(Normalized Patient Equivalents)

45%

New to Brand Share – Psoriasis(Normalized Patient Equivalents)

OTEZLA®45%

OTEZLA®

33%

30%

35%

40%OTEZLA®

39%

30%

35%

40%

15%

20%

25%

15%

20%

25%

0%

5%

10%

0%

5%

10%

0%

ENBREL SIMPONI HUMIRACIMZIA STELARA Sulfasalazine

0%

Acitretin Cyclosporine HUMIRAENBREL STELARA OTEZLA

30

CIMZIA STELARA SulfasalazineMethotrexate Leflunomide OTEZLA

ENBREL STELARA OTEZLAMethotrexate

Note: Symphony data is subject to restatementSource: SHA PTD claims data (March 2015 feed for month ending January 2015)

Robust Data Rollout Planned for Upcoming Congresses

All 7 Abstracts Accepted2 Oral Presentations:

• Efficacy in difficult-to-treat PSOR manifestationsWCD WCD

AcceptancesAcceptances

All 11 Abstracts Accepted

y• MAPP global survey results

Other Abstracts Focused on PSOR Long-term Data

AcceptancesAcceptancesJune 2015June 2015

All 11 Abstracts Accepted

2 Oral Presentations:• 2 year enthesitis and dactylitis in PsA• CC-220 pre-clinical and Ph I data in healthy

EULAR EULAR AcceptancesAcceptances

volunteers

Other Abstracts focused on OTEZLA® PsA long-term Data and PSOR Overview Results

June 2015June 2015

9 Abstracts Submitted• 32 week efficacy PSOR

(post-hoc comparison to etanercept)• 32 week safety PSOR

EADV EADV SubmissionsSubmissionsO t b 2015O t b 2015

y• New composite efficacy measure• Metabolic parameters

October 2015October 2015

31

GED-0301 Development Highlights

Program Updates– Registration-enabling endoscopy trial underway– Startup activities for phase III registration trials ongoing;

study initiation expected mid-year– Ulcerative colitis phase II to begin H2:15

P i f d l t i di t i C h ’ di– Preparing for development in pediatric Crohn’s disease

Data Dissemination– Phase II manuscript published in The New England p p g

Journal of Medicine (March 18, 2015)– 2 abstracts accepted for presentation at DDW

(Digestive Disease Week) May 2015 Congress; i l d 1 l t ti d 1 t t tiincludes 1 oral presentation and 1 poster presentation

– Special encore of UEGW oral presentation

Upcoming Analyst & Investor Event

32

p g yGED-0301 “Deep Dive”

May 17, 2015

I&I Franchise Momentum Accelerating

Successfully launch OTEZLA® in the U.S., EU, and expand into additional key geographies

Maximizing the OTEZLA® Opportunity

geographies Completion and top-line results from PsA Ph IIIb and Japan registration trials Development of OTEZLA® in new indications (Behçet’s disease, atopic dermatitis,

and ulcerative colitis)

Complete enrollment of registration-enabling endoscopy trial for GED-0301 in

Moving GED-0301 Forward

Crohn’s disease Initiate enrollment in Ph III trials of GED-0301 in adults and adolescents with

Crohn’s disease Initiate clinical program in ulcerative colitis for GED-0301Initiate clinical program in ulcerative colitis for GED 0301

Complete Ph IIb enrollment for sotatercept in ESRD patients with anemia

New Products Furthering the I&I PipelineNew Products Furthering the I&I Pipeline

33

Complete Ph IIb enrollment for sotatercept in ESRD patients with anemia Complete enrollment in Ph IIa trial with CC-220 in patients with SLE

Bob Hugin

O U R F O C U S

Executing on Five Strategic Imperatives

Operational excellenceOperational excellenceOperational excellenceOperational excellence

Capitalizing on strength in HematologyCapitalizing on strength in HematologyCapitalizing on strength in HematologyCapitalizing on strength in Hematology

Expanding the Oncology franchiseExpanding the Oncology franchiseExpanding the Oncology franchise Expanding the Oncology franchise

Building an Immunology & Inflammation franchiseBuilding an Immunology & Inflammation franchise

Sustaining innovation and long-term growthSustaining innovation and long-term growth

Building an Immunology & Inflammation franchiseBuilding an Immunology & Inflammation franchise

35

Sustaining innovation and long term growthSustaining innovation and long term growth

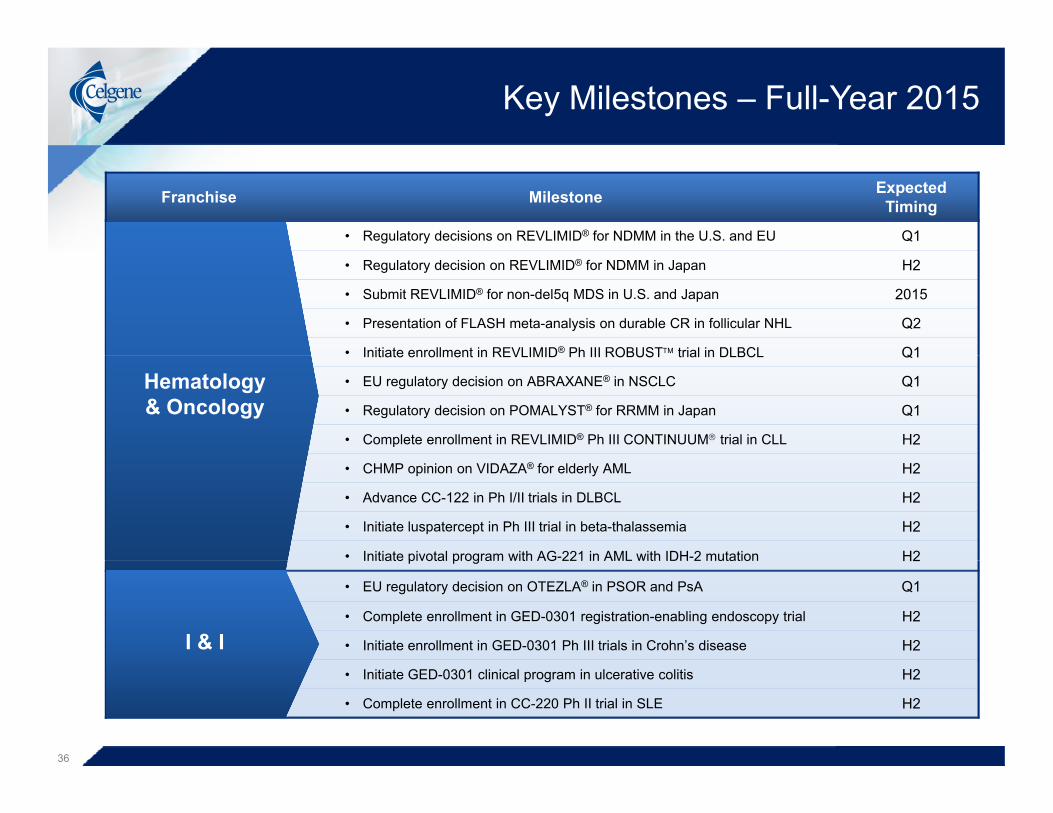

Key Milestones – Full-Year 2015

Franchise Milestone ExpectedTiming

• Regulatory decisions on REVLIMID® for NDMM in the U.S. and EU Q1

• Regulatory decision on REVLIMID® for NDMM in Japan H2

• Submit REVLIMID® for non-del5q MDS in U.S. and Japan 2015

• Presentation of FLASH meta-analysis on durable CR in follicular NHL Q2

• Initiate enrollment in REVLIMID® Ph III ROBUST trial in DLBCL Q1Initiate enrollment in REVLIMID Ph III ROBUST trial in DLBCL Q1

• EU regulatory decision on ABRAXANE® in NSCLC Q1

• Regulatory decision on POMALYST® for RRMM in Japan Q1

• Complete enrollment in REVLIMID® Ph III CONTINUUM trial in CLL H2

Hematology& Oncology

• CHMP opinion on VIDAZA® for elderly AML H2

• Advance CC-122 in Ph I/II trials in DLBCL H2

• Initiate luspatercept in Ph III trial in beta-thalassemia H2

• Initiate pivotal program with AG-221 in AML with IDH-2 mutation H2Initiate pivotal program with AG 221 in AML with IDH 2 mutation H2

• EU regulatory decision on OTEZLA® in PSOR and PsA Q1

• Complete enrollment in GED-0301 registration-enabling endoscopy trial H2

• Initiate enrollment in GED-0301 Ph III trials in Crohn’s disease H2I & I• Initiate GED-0301 clinical program in ulcerative colitis H2

• Complete enrollment in CC-220 Ph II trial in SLE H2

36

Q1 2015 Conference CallApril 30, 2015

ReconciliationReconciliation Tables

Reconciliation Tables

2014 1,

707.

5$

22

.5

1,73

0.0

86.1

713.

7

49

4.1

65.7

8.

6

1,

368.

2

361.

8

6.4

(29.

3)

(6.6

)

33

2.3

52.6

279.

7$

0.

34$

0.

33$

81

1.5

845.

1

Dec

embe

r 31,

2014 7,

546.

7$

17,3

40.1

60

5.9

6,26

5.7

6,

524.

8

8, 2

014,

to

nd e

ffec

t a tw

o-fo

r-re

sent

ed h

erei

n

31,

erio

ds E

nded

2015 2,

055.

2$

25

.6

2,08

0.8

104.

0

50

6.0

529.

2

63.6

19

.0

1,22

1.8

859.

0

9.0

(49.

2)

8.3

827.

1

10

8.2

718.

9$

0.90

$

0.

86$

798.

9

83

4.1

Mar

ch 3

1,20

15 7,31

3.5

$

17

,480

.5

504.

4

6,30

3.0

6,

764.

8

corp

orat

ion

on J

une

18llio

n to

1.1

50 b

illion

an

d pe

r sha

re a

mou

nts

pr

iari

esof

Inco

me

Mar

ch

Thre

e-M

onth

Pe

rm d

ebt

ded

its c

ertif

icat

e of

inc

n st

ock

from

575

.0 m

ilco

rdin

gly,

all

shar

e an

d

tion

and

Subs

idi

ted

Stat

emen

ts o

naud

ited)

xcep

t per

sha

re d

ata)

izatio

n of

asse

ts

keta

ble

secu

ritie

s

rren

t por

tion

of lo

ng-te

l, th

e C

ompa

ny a

men

dize

d sh

ares

of c

omm

onng

com

mon

sto

ck. A

ccsp

lit.

elge

ne C

orpo

rat

ense

d C

onso

lidat (Un

(In m

illio

ns, e

x

ales

e venu

e

sold

(exc

ludi

ng a

mor

tin

tang

ible

ass

ets)

deve

lopm

ent

al a

nd a

dmin

istra

tive

of a

cqui

red

inta

ngib

le a

late

d ch

arge

s, ne

tst

s an

d ex

pens

es

ome

nves

tmen

t inc

ome,

net

nse)

(exp

ense

), ne

t

e in

com

e ta

xes

ovisi

on

er c

omm

on s

hare

:(1)

rage

sha

res:(1

)

et it

ems:

sh e

quiv

alen

ts &

mar

ket

sm

bor

row

ings

and

cur

m d

ebt

ckho

lder

s' eq

uity

g st

ockh

olde

r app

rova

lth

e nu

mbe

r of a

utho

rizk

split

of i

ts o

utst

andi

nhe

impa

ct o

f the

sto

ck Ce

Con

de

39

Net

pro

duct

sa

Oth

er re

venu

eTo

tal r

ev

Cos

t of g

oods

ac

quire

d R

esea

rch

and

Sellin

g, g

ener

aA

mor

tizat

ion

oA

cqui

sitio

n re

lTo

tal c

os

Ope

ratin

g in

co

Inte

rest

and

inIn

tere

st (e

xpen

Oth

er in

com

e

Inco

me

befo

r e

Inco

me

tax

pro

Net

inco

me

Net

inco

me

peB

asic

Dilu

ted

Wei

ghte

d av

e rB

asic

Dilu

ted

Bal

ance

she

eC

ash,

cas

Tota

l ass

Shor

t-ter

mLo

ng-te

rmTo

tal s

toc

(1)

Follo

win

gin

crea

se

one

stoc

kre

flect

th

Reconciliation Tables

2014 27

9.7

6.1

47

.0

30

9.0

51

.3

25

.0

65

.7

8.6

(87

.5)

70

4.9

0.87

0.83

lso co

ntains

lin

form

ation

th

resp

ect to

ed

in ad

dition

lly

exclu

de

meet

the

n diff

eren

t

ds E

nded

2015 71

8.9$

$

6.7

56.2

19

.0

65.9

-

63.6

19.0

(58.3)

89

1.0$

$

1.12

$

$

1.07

$

$

P, th

is pr

ess r

eleas

e al

ment

with

supp

lemen

tal

twee

n per

iods a

nd w

itnd

shou

ld be

cons

idere

U.S.

GAAP

. We t

ypica

ation

s and

that

do no

t efi

ne th

ese m

easu

res i

ries

t Inc

ome

Three

-Mon

th Pe

rioM

arch 3

1,

(1) (1) (2) (1) (3) (4) (5) (6)

danc

e with

U.S.

GAA

Pve

stors

and m

anag

emilit

ate co

mpar

isons

bet

ures

are n

on-G

AAP

and i

n acc

orda

nce w

ith U

affec

t our

basic

oper

athe

r com

panie

s may

de

tion a

nd Su

bsidi

aP

to Ad

justed

Ne

cept

per s

hare

data)

g amo

rtizati

onts)

: n exp

ense

n exp

ense

ense

rative

:n e

xpen

seob

ligati

on

angib

le as

sets

net:

ontin

gent

cons

iderat

ion

Adjus

ted

ion pr

epar

ed in

acco

rdwe

belie

ve pr

ovide

ince

and t

rend

s tha

t fac

ius

ted fi

nanc

ial m

easu

e inf

orma

tion p

repa

red

ment

does

not b

eliev

e aon

-recu

rring

items

. Ot

Celge

ne C

orpo

rat

ncilia

tion o

f GAA

P(In

mill

ions,

exc

- GAA

P

e tax

adjus

tmen

ts:of

good

s sold

(exc

ludin g

cquir

ed in

tangib

le as

setha

re-ba

sed c

ompe

nsati

on

arch a

nd de

velop

ment:

hare-

base

d com

pens

ation

pfron

t coll

abora

tion e

xpe

ng, g

enera

l and

admi

nistr

hare-

base

d com

pens

ation

ttleme

nt of

conti

ngen

t o

rtizati

on of

acqu

ired i

nta

uisitio

n rela

ted ch

arges

, nha

nge i

n fair

value

of co

come

tax a

djustm

ents

- Ad

justed

per c

ommo

n sha

re -

A

d to fin

ancia

l info

rmati

nanc

ial m

easu

res t

hat

oper

ating

perfo

rman

cnf

orma

tion.

Thes

e adj

as a

subs

titute

for,

theAP

items

that

mana

gem

nition

of un

usua

l or n

oCRe

con

40

Net in

come

Befor

e C

ost

of

a

Sh

Res

ea

Sh

U

p

Sell

in

Sh

S

e

Amo

r

Acq

u

Ch

Net in

cNe

t inco

me

Net in

come

Ba

sicDi

lute d

In ad

dition

ad

juste

d fin

relat

ing to

opr

ojec

ted in

to, bu

t not

ace

rtain

GAA

GAAP

defin

ways

.

Reconciliation Tables

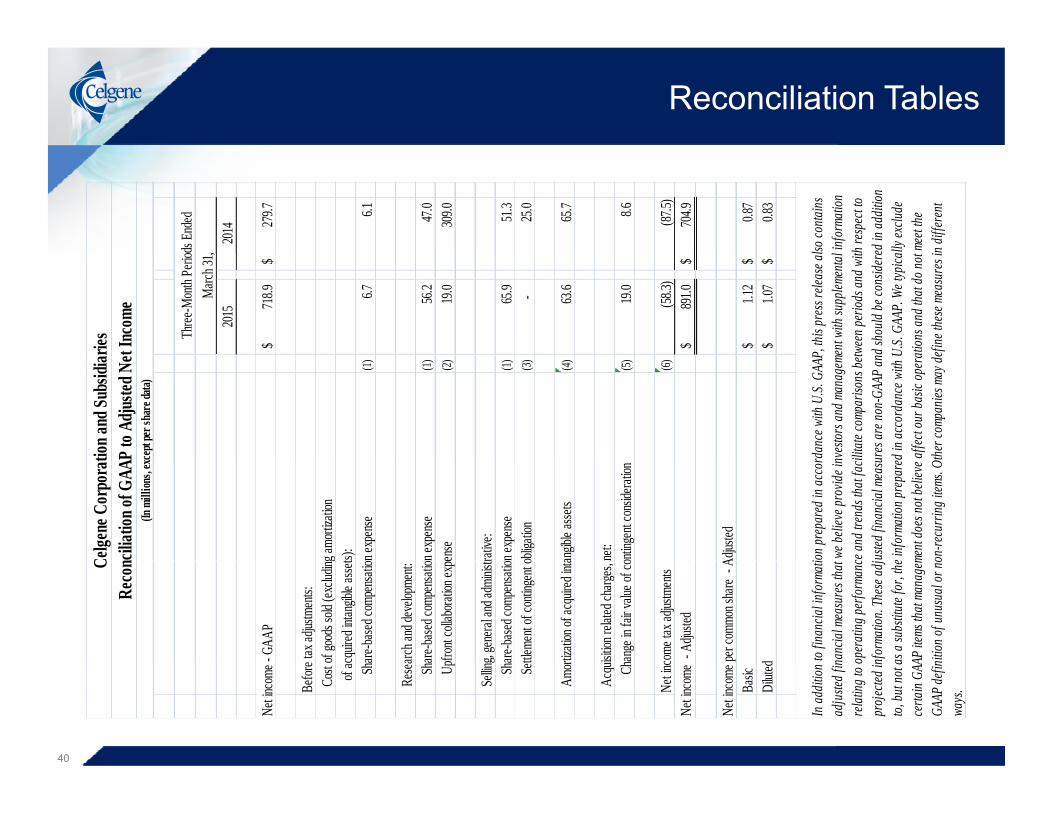

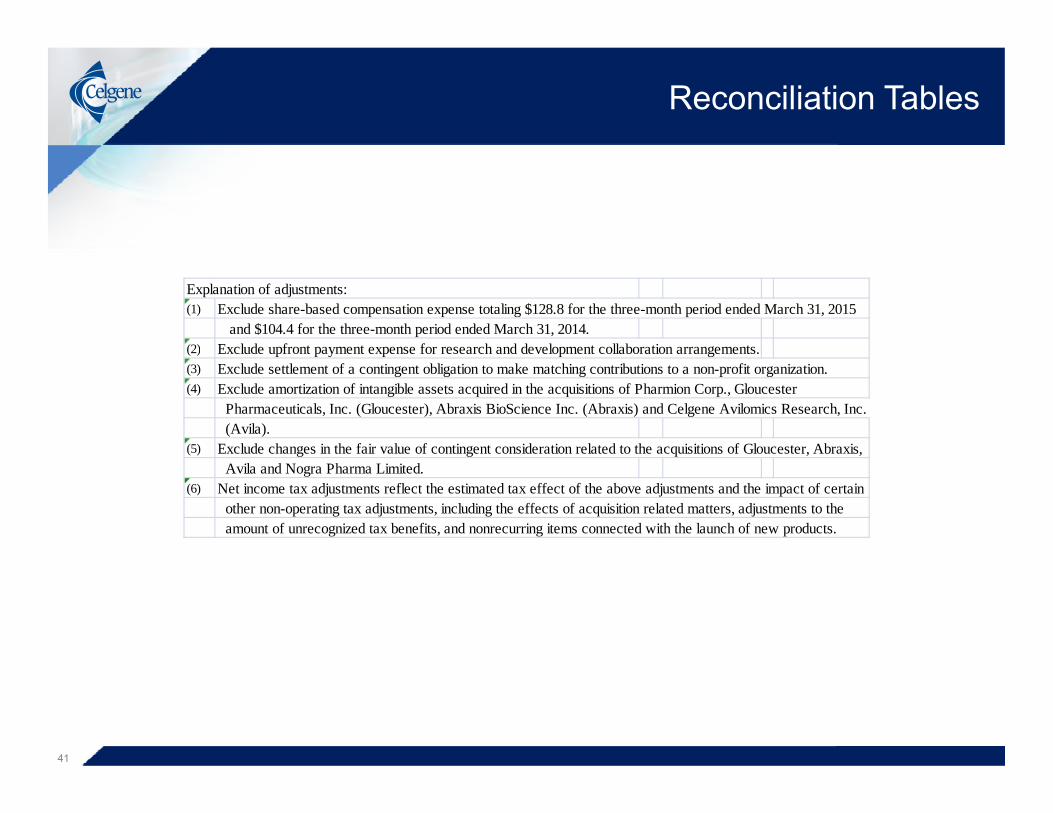

Explanation of adjustments:(1) Exclude share-based compensation expense totaling $128.8 for the three-month period ended March 31, 2015

and $104.4 for the three-month period ended March 31, 2014. (2) Exclude upfront payment expense for research and development collaboration arrangements.( ) p p y p p g(3) Exclude settlement of a contingent obligation to make matching contributions to a non-profit organization.(4) Exclude amortization of intangible assets acquired in the acquisitions of Pharmion Corp., Gloucester

Pharmaceuticals, Inc. (Gloucester), Abraxis BioScience Inc. (Abraxis) and Celgene Avilomics Research, Inc. (Avila).

(5) Exclude changes in the fair value of contingent consideration related to the acquisitions of Gloucester, Abraxis, Avila and Nogra Pharma Limited.

(6) Net income tax adjustments reflect the estimated tax effect of the above adjustments and the impact of certain other non-operating tax adjustments, including the effects of acquisition related matters, adjustments to the amount of unrecognized tax benefits, and nonrecurring items connected with the launch of new products.

41

Reconciliation Tables

High 2,6

51.5

$

34.0

25

5.4

499.0

29

2.1

254.6

91

.0

(135.1

)

3,9

42.5

$

3.19

$

4.7

5$

830.0

ge n agre

emen

ts,

as pa

rt of

the

Inco

me

Low

1)2,4

68.2

$

36.5

26

8.9

499.0

30

4.0

254.6

11

6.2

(129.4

)

3,8

18.0

$

2.97

$

4.6

0$

830.0

Ran g

mbina

tions

, coll

abora

tion

e of o

ur CV

Rs is

sued

s p

ress r

eleas

e.

iaries

to A

djus

ted N

et

(1

uired ed ct of

any b

usine

ss co

mha

nges

in th

e fair

value

prior

to the

date

of thi

s

tion a

nd S

ubsid

iro

jected

GAA

P t

xcep

t per

shar

e data

)

g amo

rtizati

on of

acqu

on ex

pens

e

on ex

pens

e pe

nse

rative

:on

expe

nse

ngibl

e asse

ts

net:

nting

ent c

onsid

eratio

n

mmon

share

- GA

AP

mmon

share

- A

djuste

share

s

o not

includ

e the

effec

sset im

pairm

ents,

or ch

y occ

ur aft

er the

day p

elgen

e Cor

pora

tull

-Yea

r 201

5 Pr

(In m

illion

s, ex

incom

e - G

AAP

ax ad

justm

ents:

f goo

ds so

ld (ex

cludin

gan

gible

asse

ts):

are-ba

sed c

ompe

nsati

o

rch an

d dev

elopm

ent:

are-ba

sed c

ompe

nsati

ofro

nt co

llabo

ration

exp

, gen

eral a

nd ad

minis

trare

-base

d com

pens

atio

zatio

n of a

cquir

ed in

tan

ition r

elated

charg

es, n

ge in

fair v

alue o

f con

me ta

x adju

stmen

ts

incom

e - A

djuste

d

incom

e per

dilute

d com

incom

e per

dilute

d com

ghted

avera

ge di

luted

ected

2015

earni

ngs d

oqu

isition

s, int

angib

le as

on of

Abra

xis th

at ma

yCeon

ciliat

ion of

Fu

42

Proje

cted n

et i

Befor

e ta

Cost

of

inta

Sha

Rese

ar S

ha U

pf

Sellin

g, S

ha

Amo

rtiz

Acq

uisi

Cha

ng

Net in

com

Proje

cted n

et i

Proje

cted n

et i

Proje

cted n

et i

Proje

cted w

eig

(1)Ou

r proj

eas

set a

cqac

quisit

io

Reco

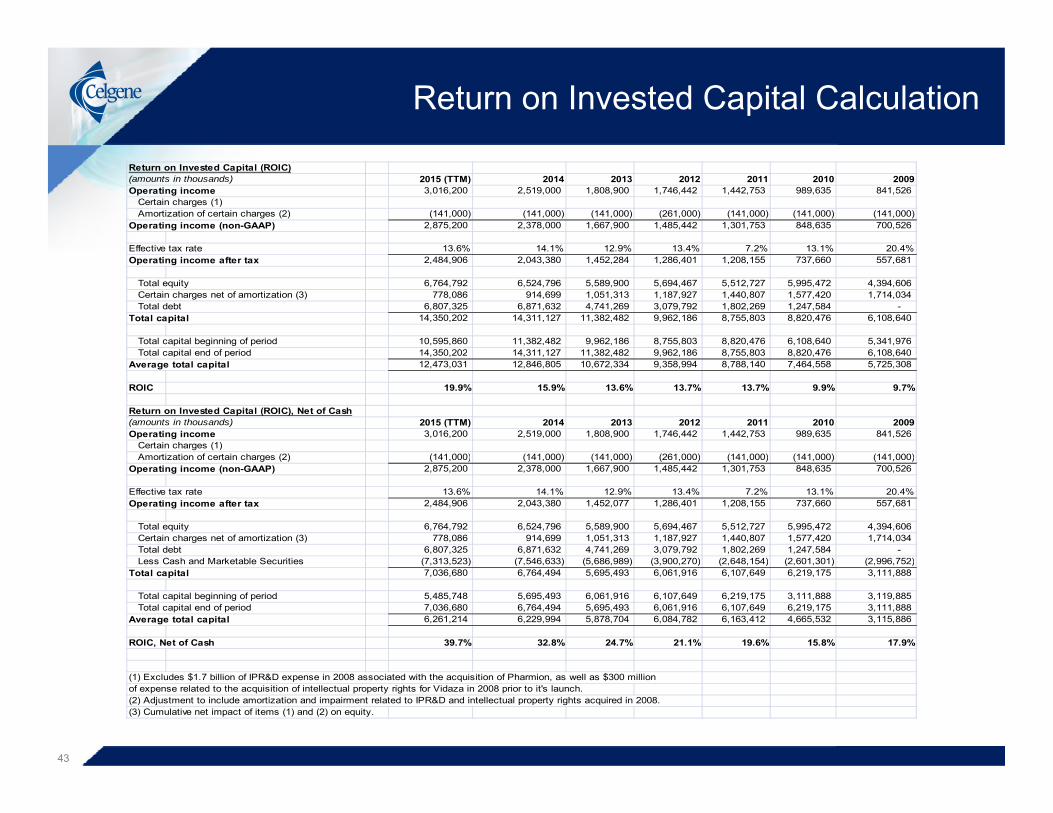

Return on Invested Capital Calculation

Return on Invested Capital (ROIC)(amounts in thousands) 2015 (TTM) 2014 2013 2012 2011 2010 2009Operating income 3,016,200 2,519,000 1,808,900 1,746,442 1,442,753 989,635 841,526

Certain charges (1)Amortization of certain charges (2) (141,000) (141,000) (141,000) (261,000) (141,000) (141,000) (141,000)

Operating income (non-GAAP) 2,875,200 2,378,000 1,667,900 1,485,442 1,301,753 848,635 700,526

Effective tax rate 13.6% 14.1% 12.9% 13.4% 7.2% 13.1% 20.4%Operating income after tax 2,484,906 2,043,380 1,452,284 1,286,401 1,208,155 737,660 557,681

Total equity 6,764,792 6,524,796 5,589,900 5,694,467 5,512,727 5,995,472 4,394,606 Certain charges net of amortization (3) 778,086 914,699 1,051,313 1,187,927 1,440,807 1,577,420 1,714,034 Total debt 6,807,325 6,871,632 4,741,269 3,079,792 1,802,269 1,247,584 -

Total capital 14,350,202 14,311,127 11,382,482 9,962,186 8,755,803 8,820,476 6,108,640

Total capital beginning of period 10,595,860 11,382,482 9,962,186 8,755,803 8,820,476 6,108,640 5,341,976 Total capital end of period 14,350,202 14,311,127 11,382,482 9,962,186 8,755,803 8,820,476 6,108,640Total capital end of period 14,350,202 14,311,127 11,382,482 9,962,186 8,755,803 8,820,476 6,108,640

Average total capital 12,473,031 12,846,805 10,672,334 9,358,994 8,788,140 7,464,558 5,725,308

ROIC 19.9% 15.9% 13.6% 13.7% 13.7% 9.9% 9.7%

Return on Invested Capital (ROIC), Net of Cash(amounts in thousands) 2015 (TTM) 2014 2013 2012 2011 2010 2009Operating income 3,016,200 2,519,000 1,808,900 1,746,442 1,442,753 989,635 841,526

Certain charges (1)Amortization of certain charges (2) (141 000) (141 000) (141 000) (261 000) (141 000) (141 000) (141 000)Amortization of certain charges (2) (141,000) (141,000) (141,000) (261,000) (141,000) (141,000) (141,000)

Operating income (non-GAAP) 2,875,200 2,378,000 1,667,900 1,485,442 1,301,753 848,635 700,526

Effective tax rate 13.6% 14.1% 12.9% 13.4% 7.2% 13.1% 20.4%Operating income after tax 2,484,906 2,043,380 1,452,077 1,286,401 1,208,155 737,660 557,681

Total equity 6,764,792 6,524,796 5,589,900 5,694,467 5,512,727 5,995,472 4,394,606 Certain charges net of amortization (3) 778,086 914,699 1,051,313 1,187,927 1,440,807 1,577,420 1,714,034 Total debt 6,807,325 6,871,632 4,741,269 3,079,792 1,802,269 1,247,584 - Less Cash and Marketable Securities (7 313 523) (7 546 633) (5 686 989) (3 900 270) (2 648 154) (2 601 301) (2 996 752)Less Cash and Marketable Securities (7,313,523) (7,546,633) (5,686,989) (3,900,270) (2,648,154) (2,601,301) (2,996,752)

Total capital 7,036,680 6,764,494 5,695,493 6,061,916 6,107,649 6,219,175 3,111,888

Total capital beginning of period 5,485,748 5,695,493 6,061,916 6,107,649 6,219,175 3,111,888 3,119,885 Total capital end of period 7,036,680 6,764,494 5,695,493 6,061,916 6,107,649 6,219,175 3,111,888

Average total capital 6,261,214 6,229,994 5,878,704 6,084,782 6,163,412 4,665,532 3,115,886

ROIC, Net of Cash 39.7% 32.8% 24.7% 21.1% 19.6% 15.8% 17.9%

43

(1) Excludes $1.7 billion of IPR&D expense in 2008 associated with the acquisition of Pharmion, as well as $300 millionof expense related to the acquisition of intellectual property rights for Vidaza in 2008 prior to it's launch. (2) Adjustment to include amortization and impairment related to IPR&D and intellectual property rights acquired in 2008.(3) Cumulative net impact of items (1) and (2) on equity.

Appendix

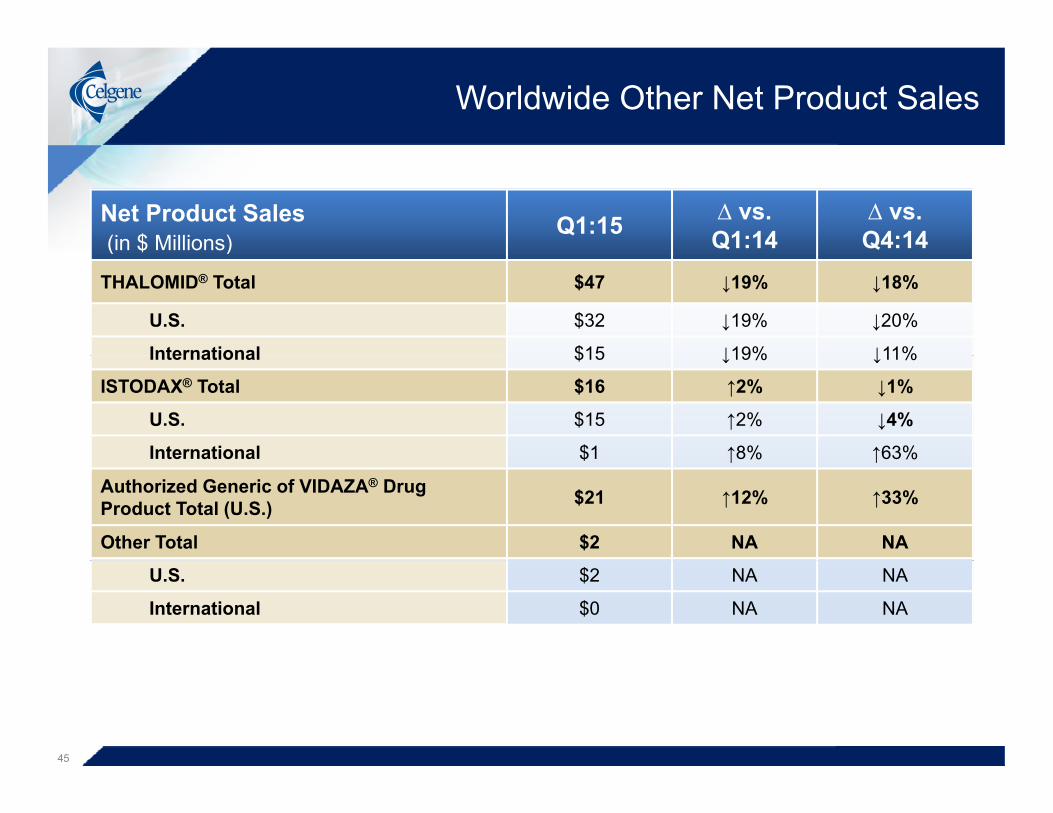

Worldwide Other Net Product Sales

Net Product Sales(in $ Millions)

Q1:15 ∆ vs.Q1:14

∆ vs.Q4:14( )

THALOMID® Total $47 ↓19% ↓18%

U.S. $32 ↓19% ↓20%

International $15 ↓19% ↓11%International $15 ↓19% ↓11%

ISTODAX® Total $16 ↑2% ↓1%

U.S. $15 ↑2% ↓4%

International $1 ↑8% ↑63%International $1 ↑8% ↑63%

Authorized Generic of VIDAZA® Drug Product Total (U.S.) $21 ↑12% ↑33%

Other Total $2 NA NA

U.S. $2 NA NA

International $0 NA NA

45

Celgene Pipeline

46

Celgene Pipeline

47

Celgene Pipeline

48

Celgene Pipeline

49

REVLIMID® Multiple Myeloma Late Stage Programs

Patient Population NDMM Non-ASCT Eligible NDMM Non-ASCT Eligible

Trial Name MM-015MM-020

Trial Name MM-015FIRST®

Phase III III

Target Enrollment 459 1,623

Design

Arm A: REVLIMID® (10mg)/melphalan/ prednisone for 9 cycles followed by REVLIMID® (10mg) maintenance to

disease progressionArm B: REVLIMID® (10mg)/melphalan/

prednisone for 9 cycles followed by placebo

Arm A: REVLIMID® (25mg)/low-dose dexamethasone until disease progression

Arm B: REVLIMID® (25mg)/low-dose dexamethasone for 18 4-week cycles g prednisone for 9 cycles followed by placebo

maintenance to disease progressionArm C: Melphalan/prednisone for 9 cycles

followed by placebo maintenance to disease progression

(72 weeks)Arm C: THALOMID®/melphalan/prednisone

for 12 6-week cycles (72 weeks)

P i E d i tPrimary Endpoint Progression Free Survival Progression Free Survival

Status

Study met primary endpoint July 2009Data presented at ASH 2009 with follow-up data at ASCO 2010, ASH and IMW 2011,

ASH 2012 and IMW 2013 PFS2 presented

Enrollment completeTrial met primary endpoint for PFS

Final PFS and interim OS presented at ASH 2013ASH 2012 and IMW 2013. PFS2 presented

at ASH 2013. Published in NEJM May 2012Follow-up continuing

ASH 2013REVLIMID® approved for NDMM in U.S. and

EU

50

REVLIMID® Multiple Myeloma Late Stage Programs

Patient Population Maintenance Post-ASCT Maintenance Post-ASCT

Trial Name CALGB 100104 IFM 2005-02

Phase III III

Target Enrollment 459 614

DesignArm A: REVLIMID® (10mg) until disease

progression Arm B: Placebo until disease progression

Arm A: REVLIMID® consolidation (25mg) for 2 cycles followed by REVLIMID®

(10-15mg) until disease progressionArm B: REVLIMID® consolidation (25mg)

for 2 cycles followed by placebo until disease progressiondisease progression

Primary Endpoint Time to Progression Progression Free Survival

Trial met primary endpoint in Dec 2009Data presented at ASCO 2010. Follow-up

Trial met primary endpoint in June 2010Data presented at ASCO 2010. Follow-up

StatusData presented at ASCO 2010. Follow up

data at ASH 2010, IMW 2011 and IMW 2013.

Published in NEJM May 2012Follow-up for survival continuing

Data presented at ASCO 2010. Follow up data at ASH 2010, IMW 2011 and

ASH 2013.Published in NEJM May 2012

Follow-up for survival continuing

51

REVLIMID® Multiple Myeloma Late Stage Programs

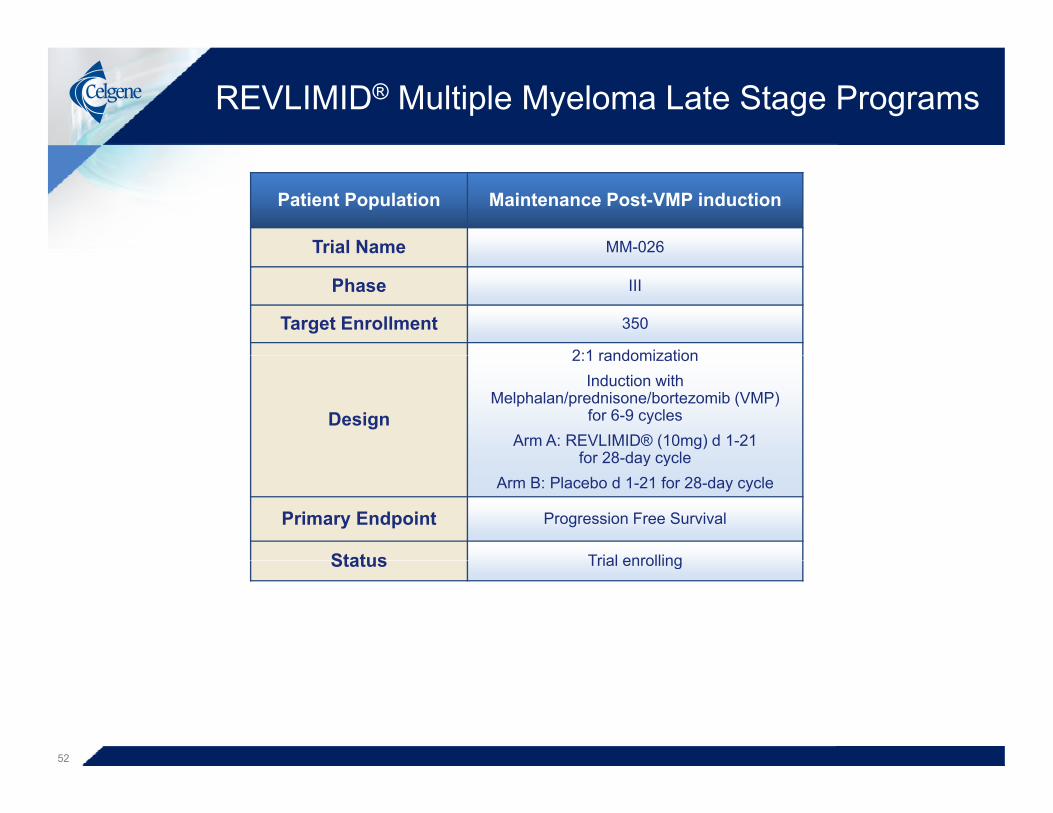

Patient Population Maintenance Post-VMP induction

Trial Name MM-026Trial Name

Phase III

Target Enrollment 350

2:1 randomization

Design

2:1 randomizationInduction with

Melphalan/prednisone/bortezomib (VMP) for 6-9 cycles

Arm A: REVLIMID® (10mg) d 1-21 for 28 day cyclefor 28-day cycle

Arm B: Placebo d 1-21 for 28-day cycle

Primary Endpoint Progression Free Survival

Status Trial enrollingStatus Trial enrolling

52

REVLIMID® Multiple Myeloma Late Stage Programs

Patient Population Maintenance in ASCT EligibleTrial Name MYELOMA XI

Phase III

Target Enrollment 3,970

Arm A: Cyclophosphamide (500mg) d1,8,15; THALOMID® (100mg d1-21 then 200mg daily), Dexamethasone (40mg) d1-4, 12-15 for minimum of 4 21-day cycle

Arm B: REVLIMID® (25mg) d 1-21, Cyclophosphamde (500mg) d1,8, dexamethasone (40mg)

Design

( g) y ( g) ( g)d1-4,12-15 for minimum of 4 28-day cycles

Arm C: Cyclophosphamde (500mg) d1,8, Carfilzomib (20 mg/m2) d 1,2 cycle 1 then (36 mg/m2) d 1,2,8,9,15,16, REVLIMID® (25mg) d1-21, Dexamethasone (40mg) d 1-

4,8,9,15,16 for 4 21-day cyclesPatients with no change, progressive disease, PR or MR randomized toDesign

Arm A: Bortezomib (1.3mg/m2) d 1,4,8,11, Cyclophosphamide (500mg) d 1,8,15, Dexamethasone (20mg) d 1,2,4,5,8,9,11,12 for max of 8 21-day cycles

Arm B: No treatmentAll patients go to SCT

After SCT randomization to:Arm A: REVLIMID® (10mg) d 1-21 for 28-day cycle to disease progression

Arm B: No maintenance

Primary Endpoint Overall Survival and Progression Free Survival

StatusTrial enrolling

Possible interim data in mid-2015E

53

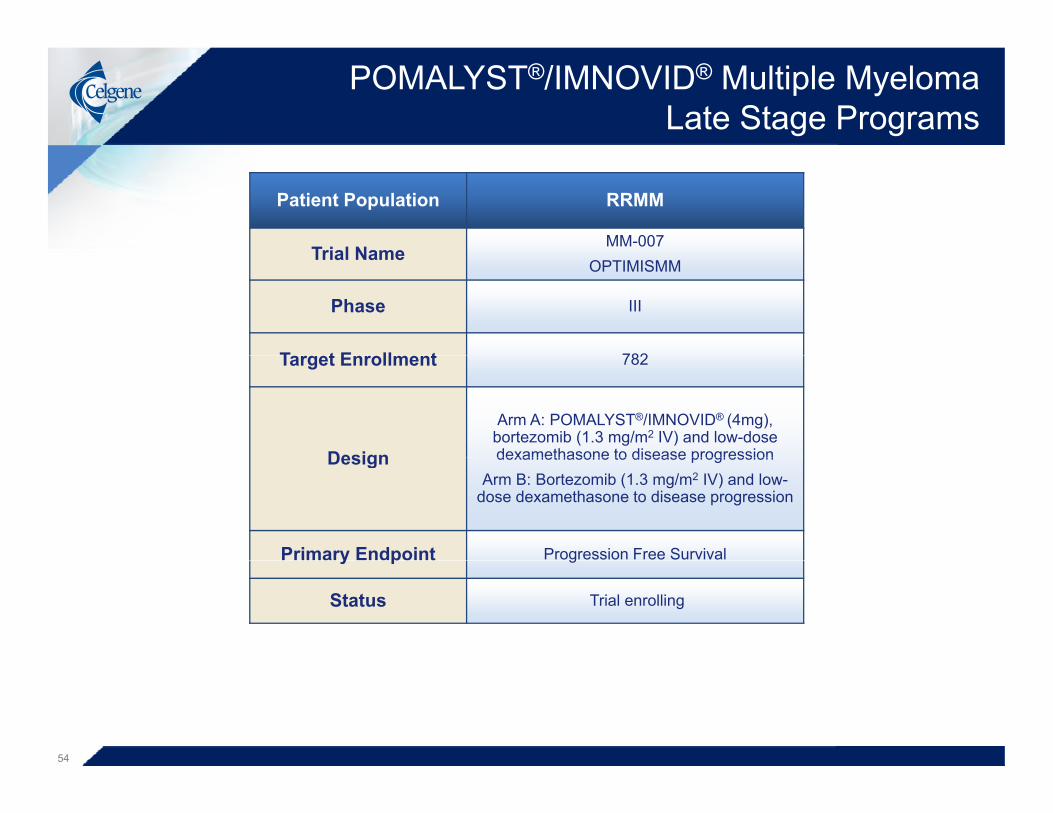

POMALYST®/IMNOVID® Multiple Myeloma Late Stage Programs

Patient Population RRMM

Trial NameMM-007

Trial NameOPTIMISMM

Phase III

T t E ll t 782Target Enrollment 782

Design

Arm A: POMALYST®/IMNOVID® (4mg), bortezomib (1.3 mg/m2 IV) and low-dose dexamethasone to disease progressionDesign dexamethasone to disease progression

Arm B: Bortezomib (1.3 mg/m2 IV) and low-dose dexamethasone to disease progression

Primary Endpoint Progression Free Survivaly p g

Status Trial enrolling

54

MDS/AML/MF Late Stage Programs

Patient Population Non-del5Q low risk/INT-1 transfusion-dependent MDS

Low risk/INT-1 transfusion-dependent MDS

CC 486Molecule REVLIMID®

CC-486(Oral Azacitidine)

Trial Name MDS-005 AZA-MDS-003

Phase III III

Target Enrollment 239 386g

DesignArm A: REVLIMID® (10mg)

Arm B: PlaceboArm A: CC-486 (150mg or 200mg)

Arm B: Placebo

Primary Endpoint RBC-transfusion independencefor at least 8 weeks

RBC-transfusion independence for more than 12 weeks

Primary endpoint metStatus

yData presented at ASH 2014

Submission to FDA expected in 2015Trial enrolling

55

MDS/AML/MF Late Stage Programs

Patient Population Elderly Newly Diagnosed AML Post induction AML Maintenance

MoleculeVIDAZA® CC-486

Molecule(azacitidine) (oral azacitidine)

Trial Name AZA-AML-001 CC-486-AML-001

Phase III III

Target Enrollment 488 460

Arm A: VIDAZA®

(75 mg/m2 SC) daily for D1-7 of a 28-day cycle until disease progression

Designcycle until disease progression

Arm B: Conventional Care Regimen (intensive chemotherapy, low-dose

cytarabine or best supportive care) to disease progression

Arm A: CC-486 (150mg or 200mg)Arm B: Best Supportive Care

Primary Endpoint Overall Survival Overall Survival

StatusData presented at EHA 2014 and ASH 2014

S b itt d t EU i 2014Trial enrolling

Submitted to EU in 2014g

56

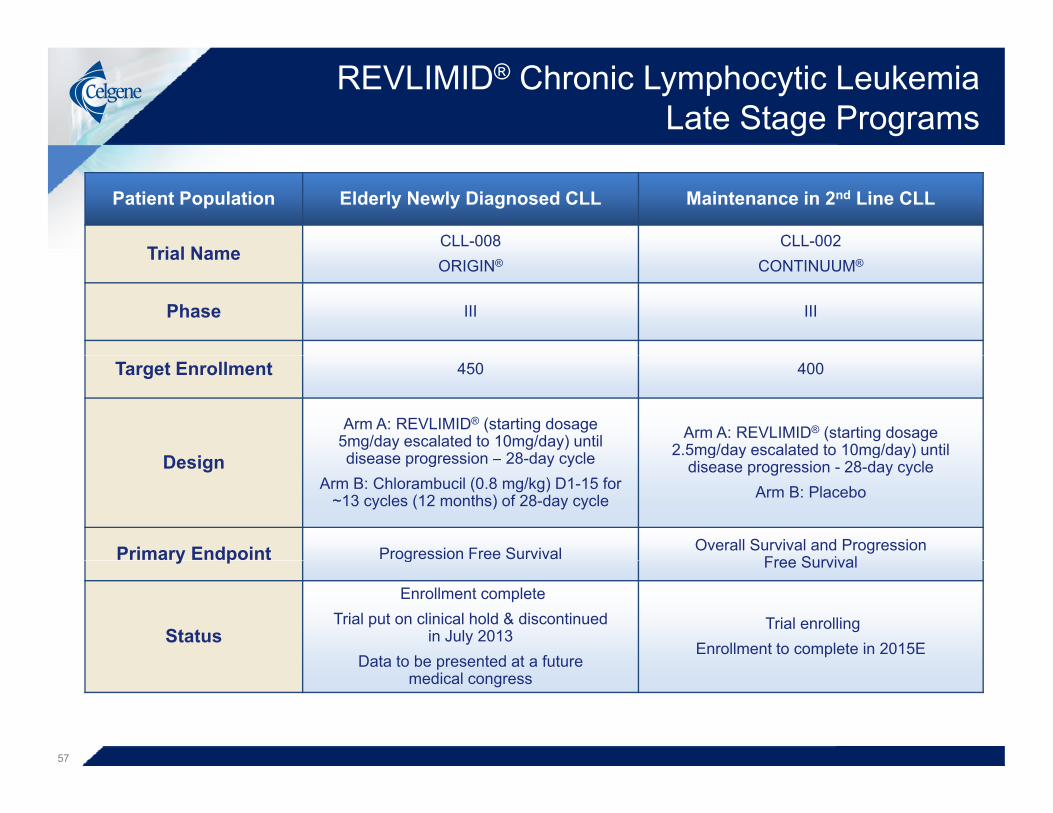

REVLIMID® Chronic Lymphocytic Leukemia Late Stage Programs

Patient Population Elderly Newly Diagnosed CLL Maintenance in 2nd Line CLL

Trial NameCLL-008 CLL-002

Trial NameORIGIN® CONTINUUM®

Phase III III

Target Enrollment 450 400

D i

Arm A: REVLIMID® (starting dosage 5mg/day escalated to 10mg/day) until disease progression 28 day cycle

Arm A: REVLIMID® (starting dosage 2.5mg/day escalated to 10mg/day) until

Design disease progression – 28-day cycleArm B: Chlorambucil (0.8 mg/kg) D1-15 for

~13 cycles (12 months) of 28-day cycle

g y g y)disease progression - 28-day cycle

Arm B: Placebo

Primary Endpoint Progression Free Survival Overall Survival and ProgressionFree Survivaly p g Free Survival

Status

Enrollment completeTrial put on clinical hold & discontinued

in July 2013Data to be presented at a future

Trial enrollingEnrollment to complete in 2015E

Data to be presented at a future medical congress

57

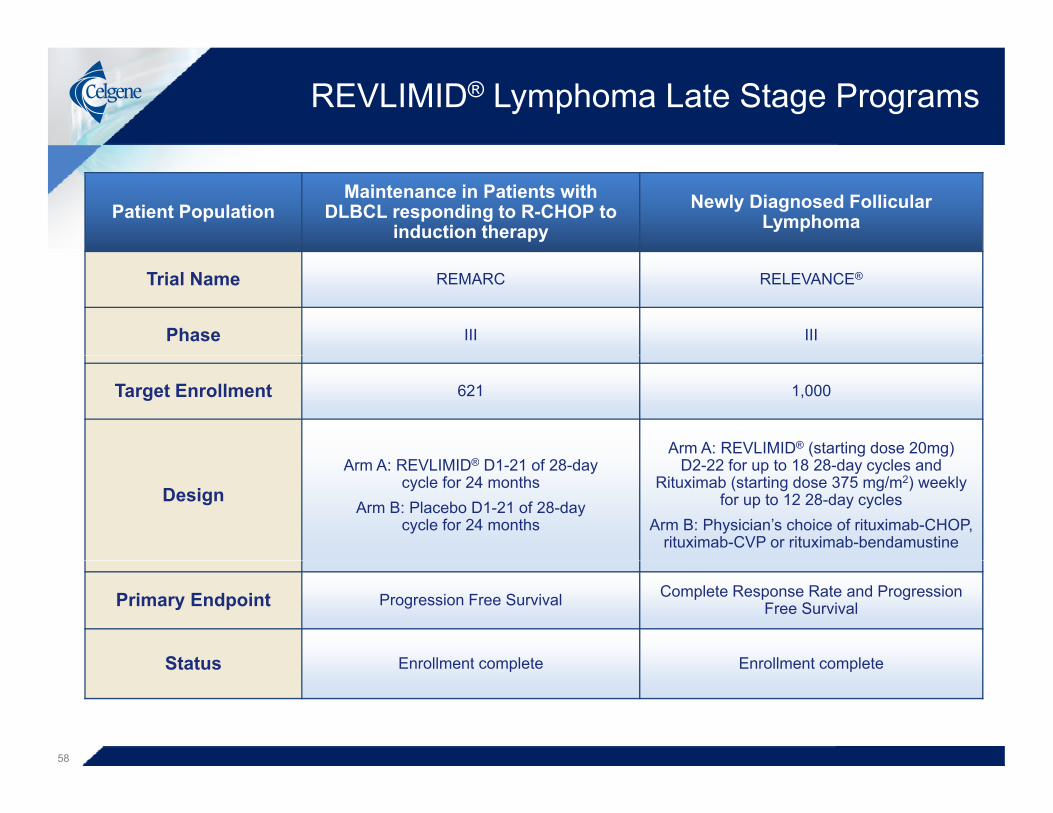

REVLIMID® Lymphoma Late Stage Programs

Patient PopulationMaintenance in Patients with

DLBCL responding to R-CHOP to induction therapy

Newly Diagnosed Follicular Lymphoma

Trial Name REMARC RELEVANCE®

Phase III III

Target Enrollment 621 1,000

Arm A: REVLIMID® (starting dose 20mg)

DesignArm A: REVLIMID® D1-21 of 28-day

cycle for 24 monthsArm B: Placebo D1-21 of 28-day

cycle for 24 months

D2-22 for up to 18 28-day cycles and Rituximab (starting dose 375 mg/m2) weekly

for up to 12 28-day cyclesArm B: Physician’s choice of rituximab-CHOP,

rituximab-CVP or rituximab-bendamustine

Primary Endpoint Progression Free Survival Complete Response Rate and Progression Free Survival

Status Enrollment complete Enrollment completeStatus Enrollment complete Enrollment complete

58

REVLIMID® Lymphoma Late Stage Programs

Patient Population Relapsed or Refractory Follicular Lymphoma

Untreated Activated B-Cell DLBCL

T i l NAUGMENTTM ROBUSTTM

Trial NameNHL-007 DLC-002

Phase III III

Target Enrollment 500 560Target Enrollment 500 560

Design

Arm A: REVLIMID® (10-20mg) D1-21 / Rituximab 375 mg/m2 weekly for cycle 1

then D 1 of cycles 2-5 for 5 28-day cycles Arm a: REVLIMID® (15mg) D1-14/+ R-CHOP21 for 6 21-day cyclesDesign

Arm B: Placebo D1-21, / Rituximab 375 mg/m2 weekly for cycle 1 then D 1 of

cycles 2-5 for 5 28-day cycles

CHOP21 for 6 21 day cyclesArm B: Placebo + R-CHOP21 for 6 cycles

Primary Endpoint Progression Free Survival Progression Free Survival

Status Trial enrolling Trial enrolling

59

REVLIMID® Lymphoma Late Stage Programs

Patient Population Relapsed or Refractory Indolent Lymphoma

Trial NameMAGNIFYTM

NHL-008

Phase III

T t E ll t 500Target Enrollment 500

D i

Arm A: REVLIMID® (10-20mg) D1-21 / Rituximab 375 mg/m2 weekly for cycle 1 then D 1 of cycles 3, 5, 7,9 and 11 for 12 28-day cycles followed by REVLIMID® (10mg) D1-21 / Rituximab 375 mg/m2 D 1 of cycles 13, 15, 17,19, 21, 23, 25, 27 and 29 for

18 28-day cycles followed by REVLIMID® (10mg) D 1-21 until disease progression –28 day cycleDesign 28 day cycle

Arm B: REVLIMID® (10-20mg) D1-21 / Rituximab 375 mg/m2 weekly for cycle 1 then D 1 of cycles 3, 5, 7,9 and 11 for 12 28-day cycles followed by REVLIMID® (10mg) D1-21 / Rituximab 375 mg/m2 D 1 of cycles 13, 15, 17,19, 21, 23, 25, 27 and 29 for

18 28-day cycles

Primary Endpoint Progression Free Survival

Status Trial enrolling

60

ABRAXANE® Solid Tumor Late Stage Programs

Patient PopulationMaintenance After Induction in

Squamous Non-Small Cell Lung Cancer

Adjuvant Therapy in Surgically Resected Pancreatic Cancer

Trial Name NSCL-003 PANC-003

Phase III III

Target Enrollment 540 800

Induction: ABRAXANE® (100 mg/m2) D 1, 8,and 15 / Carboplatin (6 mg min/mL) D 1 for

4 21-day cycles A A ABRAXANE® (125 / 2) / G it bi

Design

4 21-day cyclesMaintenance:

Arm A: ABRAXANE® (100 mg/m2) D 1 and 8 plus BSC until disease progression –

21-day cycle

Arm A: ABRAXANE® (125 mg/m2) / Gemcitabine (1000 mg/m2) D 1, 8 and 15 for 6 28-day cyclesArm B: Gemcitabine (1000 mg/m2) D 1, 8 and

15 for 6 28-day cycles.

Arm B: BSC until disease progression

Primary Endpoint Progression Free Survival Disease Free Survival

Status Trial enrolling Trial enrolling

61

ABRAXANE® Solid Tumor Late Stage Programs

Patient Population First-Line Triple Negative Metastatic Breast Cancer

tnAcity™Trial Name

tnAcity™ABI-007-MBC-001

Phase II/III

Target Enrollment 240/550Target Enrollment 240/550

Phase IIArm A: ABRAXANE® 1(25mg/m2) / Gemcitabine

(1000 mg/m2) D 1 and 8 – 21-day cycleArm B: ABRAXANE® (125mg/m2) / Carboplatin

DesignAUC 2 IV, D 1 and 8 – 21-day cycle

Arm C: Gemcitabine (1000 mg/m2) / Carboplatin AUC 2 IV, D 1 and 8 – 21-day cycle

Phase IIIArm 1: Selected phase II ABRAXANE® armp

Arm 2: Gemcitabine (1000 mg/m2) / Carboplatin AUC 2 IV, D 1 and 8 – 21-day cycle

Primary Endpoint Progression Free Survival

Status Trial enrolling

62

I&I Late Stage Programs

Patient Population

Untreated Moderate-to-Severe

Late Stage Psoriatic Arthritis

Moderate-to-Severe Plaque Psoriasis Active Behçet’s Disease

Molecule OTEZLA® OTEZLA® OTEZLA®

Trial Name PSA-006 PSOR-010BCT-002RELIEFTM

Phase III IIIb III

Target Enrollment 214 240 204

Arm A: OTEZLA® single agent (30mg)

Arm A: OTEZLA® (30 mg) twice daily

Arm A; Placebo for 12 weeks followed by 30mg OTEZLA®

i d il f 2 kDesign(30mg)

twice dailyArm B: Placebo

Arm B: Etanercept (50 mg subcutaneous) once weekly

Arm C: Placebo

twice daily for 52-weeksArm B: 30mg OTEZLA® twice

daily for 64 weeks

Primary ACR 20 t W k 16 PASI75Area under the curve (AUC) for th b f l l fPrimary

Endpoint ACR 20 at Week 16 PASI75 the number of oral ulcers from baseline through week 12

Status EnrollingEnrollment complete

Trial enrollingStatus gData presented at AAD 2015

g

63