PZ Cussons CDP response 2013 - RSPO - Roundtable on ... · Carbon Disclosure Project CDP 2013...

43

Carbon Disclosure Project CDP 2013 Investor CDP 2013 Information Request PZ Cussons Module: Introduction Page: Introduction 0.1 Introduction Please give a general description and introduction to your organization PZ Cussons operates in Africa, Asia and Europe with its strategy built on four core principles. Strategy We operate in selected categories where our brands have a strategic advantage and offer profitable growth opportunities. We succeed through understanding local consumer needs, being first to market and being unconstrained by big company bureaucracy. Faster and continuous innovation will ensure our brands occupy leading positions in these categories. Selected geographies We operate in specific geographies through our own infrastructure or in partnership. In these geographies we tailor our channel approach for each category. Flexible supply chain We operate an ever evolving supply chain designed to service our categories. We deliver innovative products to our customers from various sources, quickly and efficiently. Our supply chain significantly contributes to Group profitability. CAN DO people We work with people who share our unique CAN DO values. Our CAN DO culture is the unifying strength that binds together our diverse businesses around the world. We are responsible, demanding and have a sense of fun! European Categories and Brands Operations are located in the UK – PZ Cussons UK and PZ Cussons Beauty, in Poland, and in Greece (Minerva edible oils) Personal Care Within this category are leading brands such as Original Source, Imperial Leather, Carex, luksja and the Mum and Me range. With products such as Foamburst & SkinKind and also ranges of hand wash, foam bath and bar soaps. . PZ Cussons Beauty includes well know personal care brands such as St Tropez, Charles Worthington, Sanctuary Spa and Fudge.

Transcript of PZ Cussons CDP response 2013 - RSPO - Roundtable on ... · Carbon Disclosure Project CDP 2013...

Carbon Disclosure Project CDP 2013 Investor CDP 2013 Information Request

PZ Cussons

Module: Introduction

Page: Introduction

0.1

Introduction Please give a general description and introduction to your organization PZ Cussons operates in Africa, Asia and Europe with its strategy built on four core principles. Strategy We operate in selected categories where our brands have a strategic advantage and offer profitable growth opportunities. We succeed through understanding local consumer needs, being first to market and being unconstrained by big company bureaucracy. Faster and continuous innovation will ensure our brands occupy leading positions in these categories. Selected geographies We operate in specific geographies through our own infrastructure or in partnership. In these geographies we tailor our channel approach for each category. Flexible supply chain We operate an ever evolving supply chain designed to service our categories. We deliver innovative products to our customers from various sources, quickly and efficiently. Our supply chain significantly contributes to Group profitability. CAN DO people We work with people who share our unique CAN DO values. Our CAN DO culture is the unifying strength that binds together our diverse businesses around the world. We are responsible, demanding and have a sense of fun! European Categories and Brands Operations are located in the UK – PZ Cussons UK and PZ Cussons Beauty, in Poland, and in Greece (Minerva edible oils) Personal Care Within this category are leading brands such as Original Source, Imperial Leather, Carex, luksja and the Mum and Me range. With products such as Foamburst & SkinKind and also ranges of hand wash, foam bath and bar soaps. . PZ Cussons Beauty includes well know personal care brands such as St Tropez, Charles Worthington, Sanctuary Spa and Fudge.

Food and nutrition This product category consists of edible oils, butter, margarine and Feta cheese manufactured by Minerva SA in Greece. Home Care Products are manufactured in both the UK and Poland and include brands such as Morning Fresh, ‘E’ and includes a range of fabric wash / conditioning products. African Categories and Brands Operations are located in Nigeria, Ghana and Kenya Home Care The Home Care portfolio forms the backbone of the African business, its products include laundry and toilet soap and bulk and branded detergents such as Morning Fresh and Zip – a White Specialist detergent. The HPZ operation (a joint venture with Haier) in Nigeria offers a range of electrical goods which include fridges, freezers, washing machines, televisions, DVD players, mobile phones and air conditioning units. Personal Care This unit has a variety of local brands such as Premier, Imperial Leather, Venus, Robb which includes hair care and skincare products, medicated rubs and pharmaceutical products. Food and nutrition The food and nutrition unit, which manufactures milk and nutritional products is a joint venture with our Glanbia Plc and includes the NuNu and Bliss brands. Also a joint venture with Wilmar re edible palm oil manufacture is now in place with manufacture just commenced Asia categories and Brands Operations are located in Australia, Thailand and Indonesia. A group sourcing centre in Thailand services the bar soap requirements of our UK and Australian markets. Babycare Cussons baby is a comprehensive range of products including soaps, lotions, shampoos, talcum powder and rubs. Home Care This region has a diverse range of products within this category. Examples include detergents, manual dishwash products and automatic dishwash products under the Morning Fresh and Radiant brands. Personal Care Products falling within this category include soaps, deodorants, bodywashes, talcum powders, gels, creams and colognes. The diverse product range, which includes a number of leading local brands such as Extreme, is distributed across the Asian market . The global Imperial Leather brand, which is associated with personal wash products, has a high profile in Thailand through the sales of bar soap.

0.2

Reporting Year Please state the start and end date of the year for which you are reporting data. The current reporting year is the latest/most recent 12-month period for which data is reported. Enter the dates of this year first. We request data for more than one reporting period for some emission accounting questions. Please provide data for the three years prior to the current reporting year if you have not provided this information before, or if this is the first time you have answered a CDP information request. (This does not apply if you have been offered and selected the option of answering the shorter questionnaire). If you are going to provide additional years of data, please give the dates of those reporting periods here. Work backwards from the most recent reporting year. Please enter dates in following format: day(DD)/month(MM)/year(YYYY) (i.e. 31/01/2001).

Enter Periods that will be disclosed

Fri 01 Jun 2012 - Fri 31 May 2013

0.3

Country list configuration Please select the countries for which you will be supplying data. This selection will be carried forward to assist you in completing your response

Select country

Australia

Indonesia

Thailand

China

India

United Arab Emirates

Nigeria

Kenya

Ghana

Greece

Select country

Poland

United Kingdom

0.4

Currency selection Please select the currency in which you would like to submit your response. All financial information contained in the response should be in this currency. GBP(£)

0.6

Modules As part of the request for information on behalf of investors, electric utilities, companies with electric utility activities or assets, companies in the automobile or auto component manufacture sectors, companies in the oil and gas industry and companies in the information technology and telecommunications sectors should complete supplementary questions in addition to the main questionnaire. If you are in these sectors (according to the Global Industry Classification Standard (GICS)), the corresponding sector modules will not appear below but will automatically appear in the navigation bar when you save this page. If you want to query your classification, please email [email protected]. If you have not been presented with a sector module that you consider would be appropriate for your company to answer, please select the module below. If you wish to view the questions first, please see https://www.cdproject.net/en-US/Programmes/Pages/More-questionnaires.aspx.

Module: Management [Investor]

Page: 1. Governance

1.1

Where is the highest level of direct responsibility for climate change within your company? Individual/Sub-set of the Board or other committee appointed by the Board

1.1a

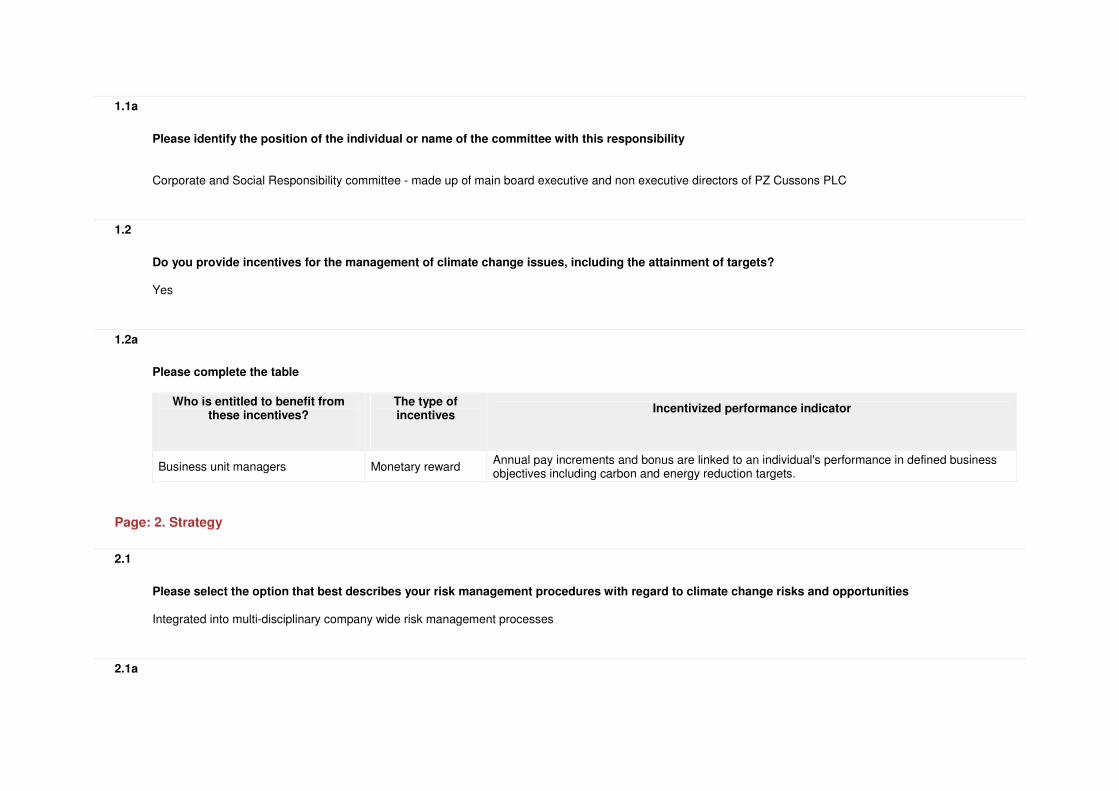

Please identify the position of the individual or name of the committee with this responsibility Corporate and Social Responsibility committee - made up of main board executive and non executive directors of PZ Cussons PLC

1.2

Do you provide incentives for the management of climate change issues, including the attainment of targets? Yes

1.2a

Please complete the table

Who is entitled to benefit from these incentives?

The type of incentives

Incentivized performance indicator

Business unit managers Monetary reward Annual pay increments and bonus are linked to an individual's performance in defined business objectives including carbon and energy reduction targets.

Page: 2. Strategy

2.1

Please select the option that best describes your risk management procedures with regard to climate change risks and opportunities Integrated into multi-disciplinary company wide risk management processes

2.1a

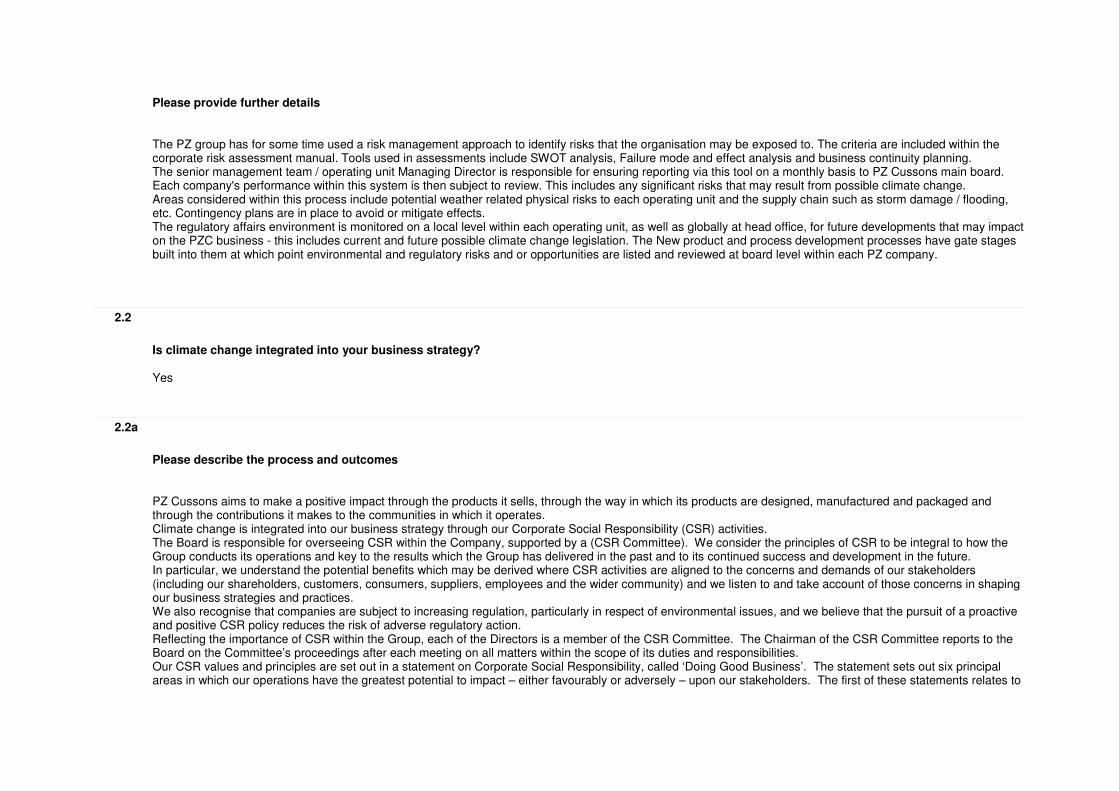

Please provide further details The PZ group has for some time used a risk management approach to identify risks that the organisation may be exposed to. The criteria are included within the corporate risk assessment manual. Tools used in assessments include SWOT analysis, Failure mode and effect analysis and business continuity planning. The senior management team / operating unit Managing Director is responsible for ensuring reporting via this tool on a monthly basis to PZ Cussons main board. Each company's performance within this system is then subject to review. This includes any significant risks that may result from possible climate change. Areas considered within this process include potential weather related physical risks to each operating unit and the supply chain such as storm damage / flooding, etc. Contingency plans are in place to avoid or mitigate effects. The regulatory affairs environment is monitored on a local level within each operating unit, as well as globally at head office, for future developments that may impact on the PZC business - this includes current and future possible climate change legislation. The New product and process development processes have gate stages built into them at which point environmental and regulatory risks and or opportunities are listed and reviewed at board level within each PZ company.

2.2

Is climate change integrated into your business strategy? Yes

2.2a

Please describe the process and outcomes PZ Cussons aims to make a positive impact through the products it sells, through the way in which its products are designed, manufactured and packaged and through the contributions it makes to the communities in which it operates. Climate change is integrated into our business strategy through our Corporate Social Responsibility (CSR) activities. The Board is responsible for overseeing CSR within the Company, supported by a (CSR Committee). We consider the principles of CSR to be integral to how the Group conducts its operations and key to the results which the Group has delivered in the past and to its continued success and development in the future. In particular, we understand the potential benefits which may be derived where CSR activities are aligned to the concerns and demands of our stakeholders (including our shareholders, customers, consumers, suppliers, employees and the wider community) and we listen to and take account of those concerns in shaping our business strategies and practices. We also recognise that companies are subject to increasing regulation, particularly in respect of environmental issues, and we believe that the pursuit of a proactive and positive CSR policy reduces the risk of adverse regulatory action. Reflecting the importance of CSR within the Group, each of the Directors is a member of the CSR Committee. The Chairman of the CSR Committee reports to the Board on the Committee’s proceedings after each meeting on all matters within the scope of its duties and responsibilities. Our CSR values and principles are set out in a statement on Corporate Social Responsibility, called ‘Doing Good Business’. The statement sets out six principal areas in which our operations have the greatest potential to impact – either favourably or adversely – upon our stakeholders. The first of these statements relates to

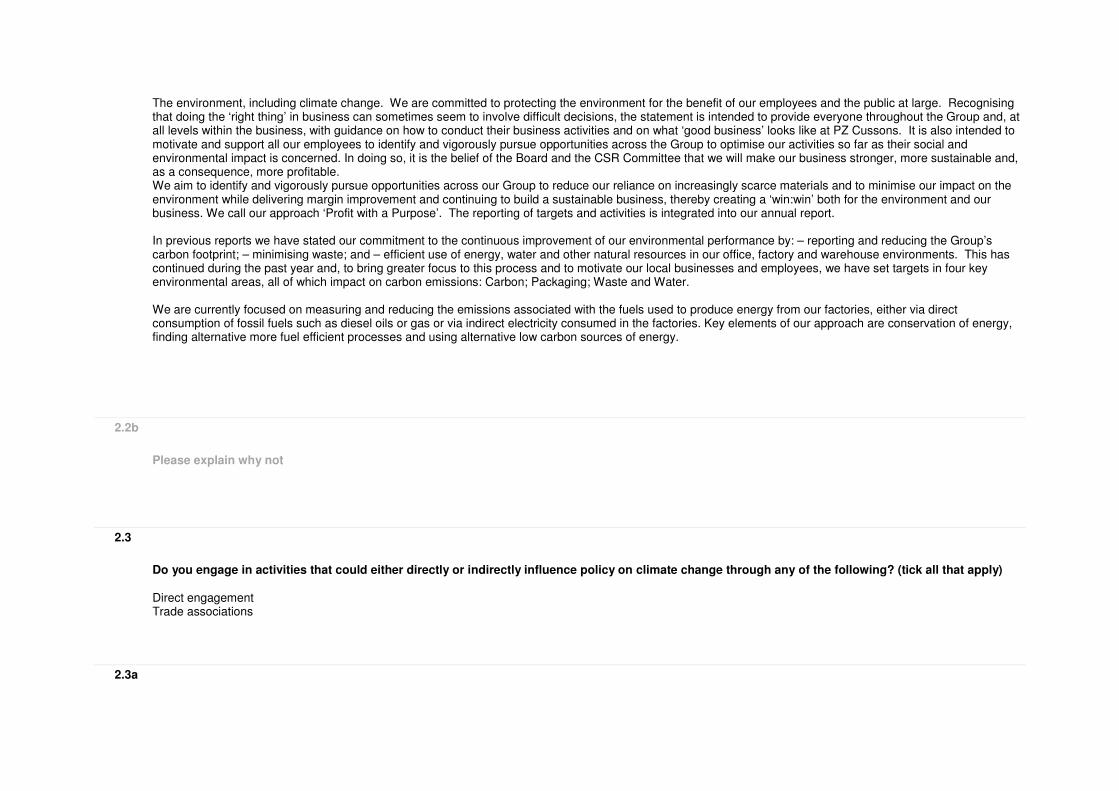

The environment, including climate change. We are committed to protecting the environment for the benefit of our employees and the public at large. Recognising that doing the ‘right thing’ in business can sometimes seem to involve difficult decisions, the statement is intended to provide everyone throughout the Group and, at all levels within the business, with guidance on how to conduct their business activities and on what ‘good business’ looks like at PZ Cussons. It is also intended to motivate and support all our employees to identify and vigorously pursue opportunities across the Group to optimise our activities so far as their social and environmental impact is concerned. In doing so, it is the belief of the Board and the CSR Committee that we will make our business stronger, more sustainable and, as a consequence, more profitable. We aim to identify and vigorously pursue opportunities across our Group to reduce our reliance on increasingly scarce materials and to minimise our impact on the environment while delivering margin improvement and continuing to build a sustainable business, thereby creating a ‘win:win’ both for the environment and our business. We call our approach ‘Profit with a Purpose’. The reporting of targets and activities is integrated into our annual report. In previous reports we have stated our commitment to the continuous improvement of our environmental performance by: – reporting and reducing the Group’s carbon footprint; – minimising waste; and – efficient use of energy, water and other natural resources in our office, factory and warehouse environments. This has continued during the past year and, to bring greater focus to this process and to motivate our local businesses and employees, we have set targets in four key environmental areas, all of which impact on carbon emissions: Carbon; Packaging; Waste and Water. We are currently focused on measuring and reducing the emissions associated with the fuels used to produce energy from our factories, either via direct consumption of fossil fuels such as diesel oils or gas or via indirect electricity consumed in the factories. Key elements of our approach are conservation of energy, finding alternative more fuel efficient processes and using alternative low carbon sources of energy.

2.2b

Please explain why not

2.3

Do you engage in activities that could either directly or indirectly influence policy on climate change through any of the following? (tick all that apply) Direct engagement Trade associations

2.3a

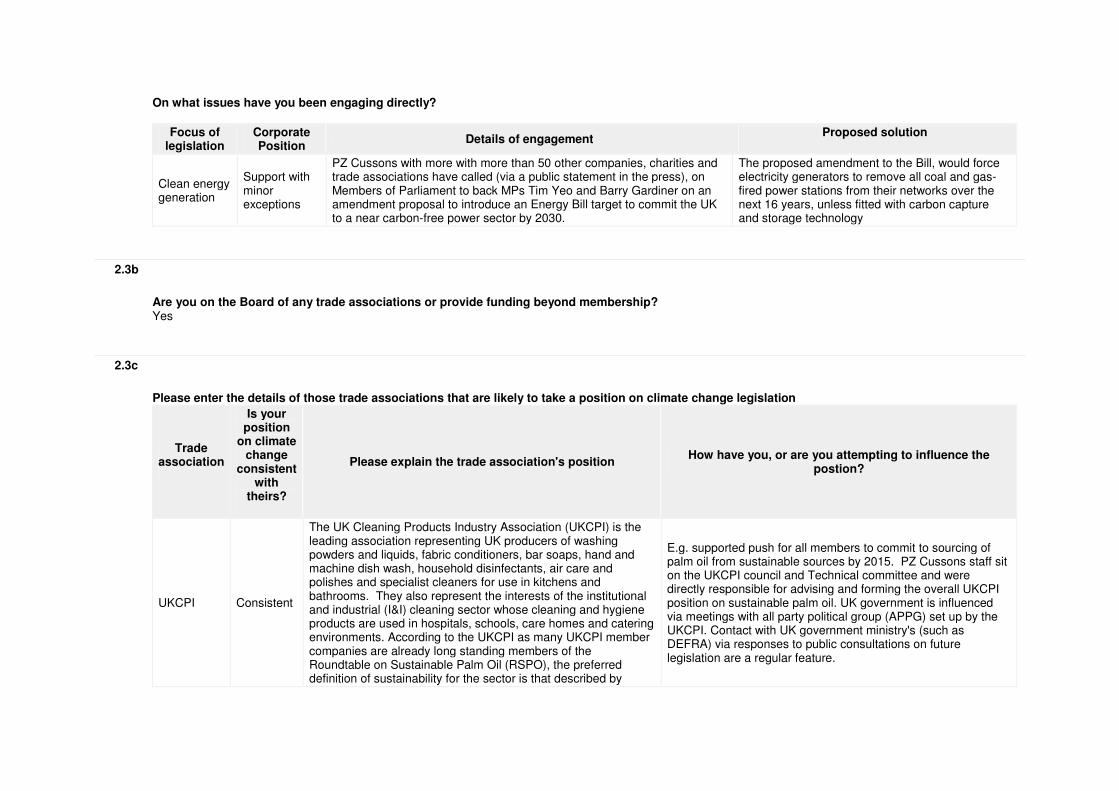

On what issues have you been engaging directly?

Focus of legislation

Corporate Position

Details of engagement Proposed solution

Clean energy generation

Support with minor exceptions

PZ Cussons with more with more than 50 other companies, charities and trade associations have called (via a public statement in the press), on Members of Parliament to back MPs Tim Yeo and Barry Gardiner on an amendment proposal to introduce an Energy Bill target to commit the UK to a near carbon-free power sector by 2030.

The proposed amendment to the Bill, would force electricity generators to remove all coal and gas-fired power stations from their networks over the next 16 years, unless fitted with carbon capture and storage technology

2.3b

Are you on the Board of any trade associations or provide funding beyond membership? Yes

2.3c

Please enter the details of those trade associations that are likely to take a position on climate change legislation

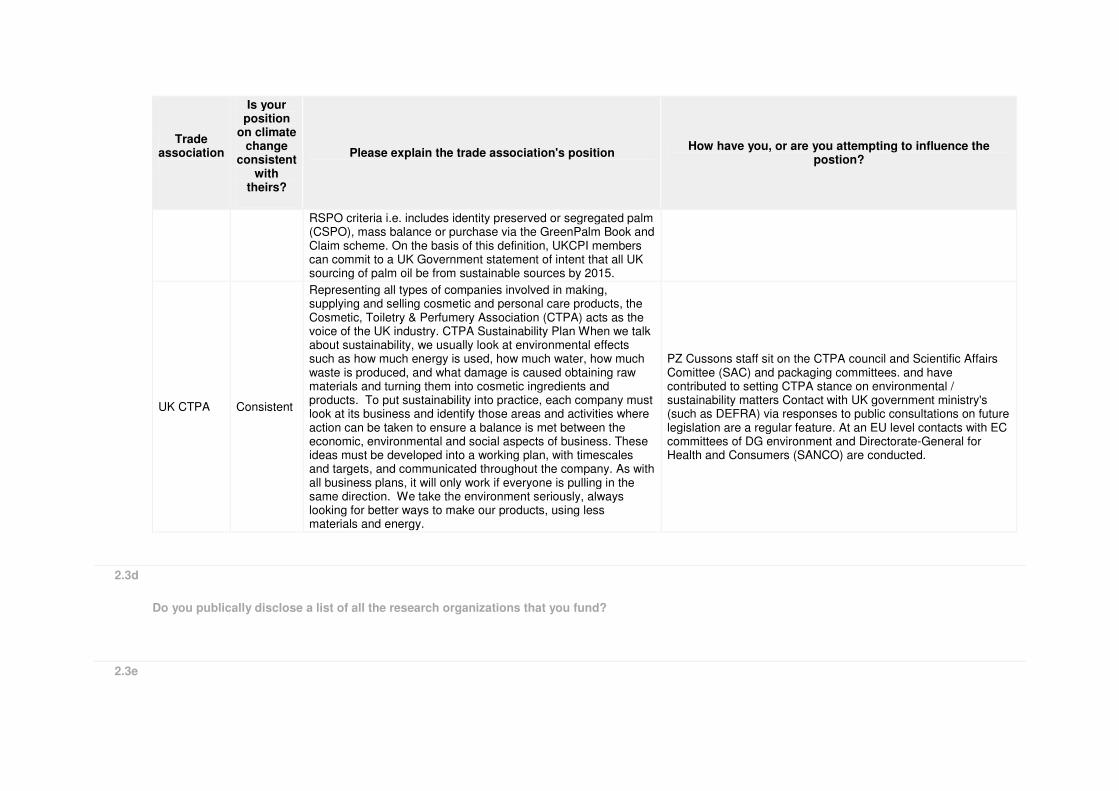

Trade association

Is your position

on climate change

consistent with

theirs?

Please explain the trade association's position How have you, or are you attempting to influence the

postion?

UKCPI Consistent

The UK Cleaning Products Industry Association (UKCPI) is the leading association representing UK producers of washing powders and liquids, fabric conditioners, bar soaps, hand and machine dish wash, household disinfectants, air care and polishes and specialist cleaners for use in kitchens and bathrooms. They also represent the interests of the institutional and industrial (I&I) cleaning sector whose cleaning and hygiene products are used in hospitals, schools, care homes and catering environments. According to the UKCPI as many UKCPI member companies are already long standing members of the Roundtable on Sustainable Palm Oil (RSPO), the preferred definition of sustainability for the sector is that described by

E.g. supported push for all members to commit to sourcing of palm oil from sustainable sources by 2015. PZ Cussons staff sit on the UKCPI council and Technical committee and were directly responsible for advising and forming the overall UKCPI position on sustainable palm oil. UK government is influenced via meetings with all party political group (APPG) set up by the UKCPI. Contact with UK government ministry's (such as DEFRA) via responses to public consultations on future legislation are a regular feature.

Trade association

Is your position

on climate change

consistent with

theirs?

Please explain the trade association's position How have you, or are you attempting to influence the

postion?

RSPO criteria i.e. includes identity preserved or segregated palm (CSPO), mass balance or purchase via the GreenPalm Book and Claim scheme. On the basis of this definition, UKCPI members can commit to a UK Government statement of intent that all UK sourcing of palm oil be from sustainable sources by 2015.

UK CTPA Consistent

Representing all types of companies involved in making, supplying and selling cosmetic and personal care products, the Cosmetic, Toiletry & Perfumery Association (CTPA) acts as the voice of the UK industry. CTPA Sustainability Plan When we talk about sustainability, we usually look at environmental effects such as how much energy is used, how much water, how much waste is produced, and what damage is caused obtaining raw materials and turning them into cosmetic ingredients and products. To put sustainability into practice, each company must look at its business and identify those areas and activities where action can be taken to ensure a balance is met between the economic, environmental and social aspects of business. These ideas must be developed into a working plan, with timescales and targets, and communicated throughout the company. As with all business plans, it will only work if everyone is pulling in the same direction. We take the environment seriously, always looking for better ways to make our products, using less materials and energy.

PZ Cussons staff sit on the CTPA council and Scientific Affairs Comittee (SAC) and packaging committees. and have contributed to setting CTPA stance on environmental / sustainability matters Contact with UK government ministry's (such as DEFRA) via responses to public consultations on future legislation are a regular feature. At an EU level contacts with EC committees of DG environment and Directorate-General for Health and Consumers (SANCO) are conducted.

2.3d

Do you publically disclose a list of all the research organizations that you fund?

2.3e

Do you fund any research organizations to produce public work on climate change?

2.3f

Please describe the work and how it aligns with your own strategy on climate change

2.3g

Please provide details of the other engagement activities that you undertake

2.3h

What processes do you have in place to ensure that all of your direct and indirect activities that influence policy are consistent with your overall climate change strategy? The PZ group main board CSR committee via the relevant stream leaders and their teams liaise closely to ensure consistency in the cascade down through the organisation of environmental policies objectives and targets to ensure consistency

2.3i

Please explain why you do not engage with policy makers

Page: 3. Targets and Initiatives

3.1

Did you have an emissions reduction target that was active (ongoing or reached completion) in the reporting year?

Absolute target

3.1a

Please provide details of your absolute target

ID

Scope

% of emissions in

scope

% reduction from base

year

Base year

Base year emissions

(metric tonnes CO2e)

Target year

Comment

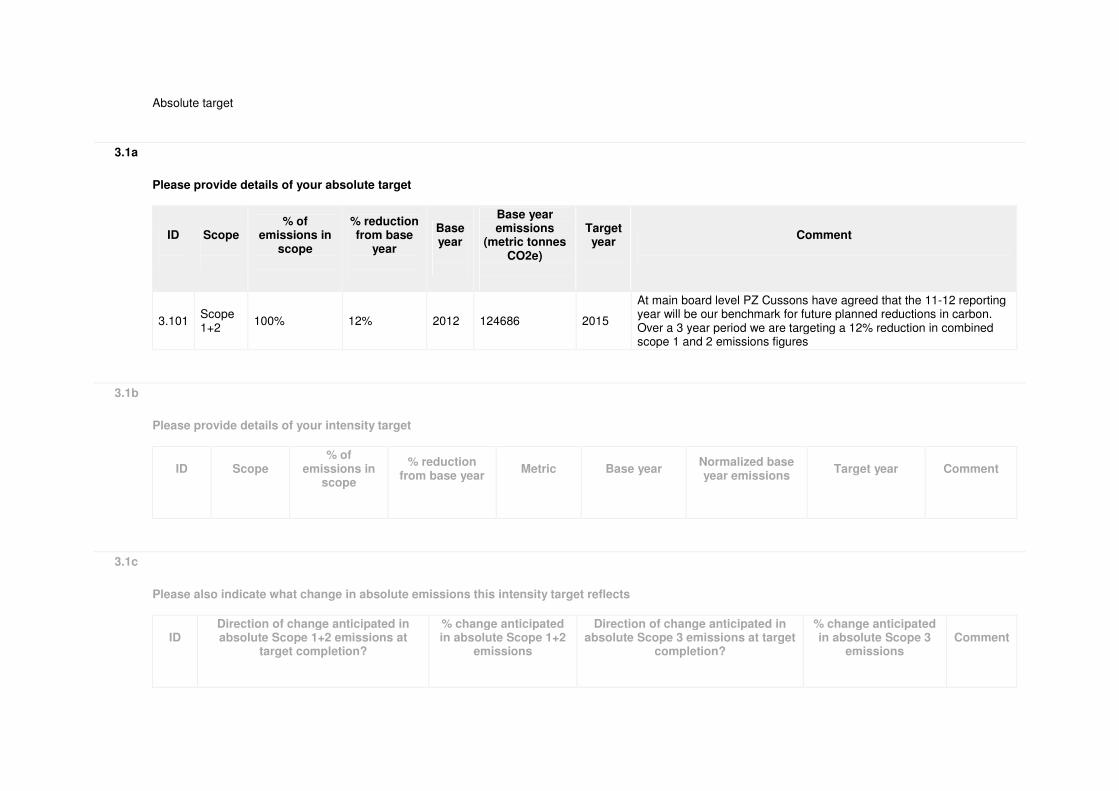

3.101 Scope 1+2

100% 12% 2012 124686 2015

At main board level PZ Cussons have agreed that the 11-12 reporting year will be our benchmark for future planned reductions in carbon. Over a 3 year period we are targeting a 12% reduction in combined scope 1 and 2 emissions figures

3.1b

Please provide details of your intensity target

ID

Scope

% of emissions in

scope

% reduction from base year

Metric

Base year

Normalized base year emissions

Target year

Comment

3.1c

Please also indicate what change in absolute emissions this intensity target reflects

ID

Direction of change anticipated in absolute Scope 1+2 emissions at

target completion?

% change anticipated in absolute Scope 1+2

emissions

Direction of change anticipated in absolute Scope 3 emissions at target

completion?

% change anticipated in absolute Scope 3

emissions

Comment

3.1d

Please provide details on your progress against this target made in the reporting year

ID

% complete (time)

% complete (emissions)

Comment

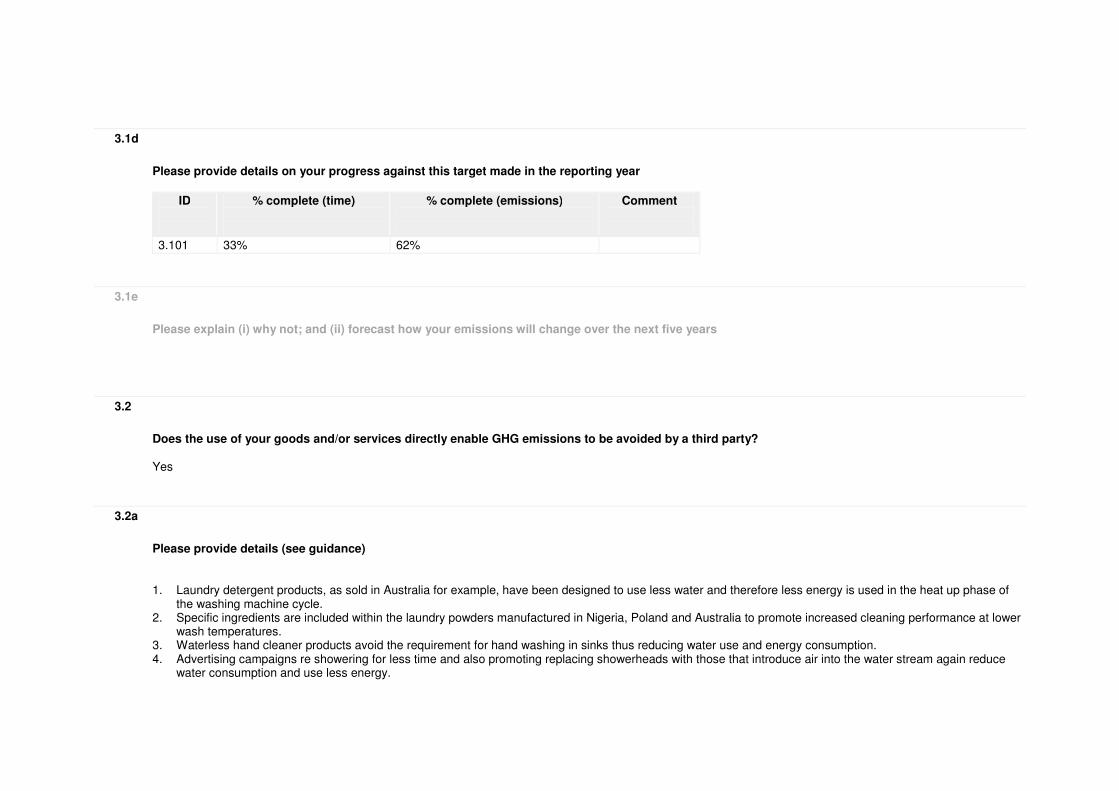

3.101 33% 62%

3.1e

Please explain (i) why not; and (ii) forecast how your emissions will change over the next five years

3.2

Does the use of your goods and/or services directly enable GHG emissions to be avoided by a third party? Yes

3.2a

Please provide details (see guidance) 1. Laundry detergent products, as sold in Australia for example, have been designed to use less water and therefore less energy is used in the heat up phase of

the washing machine cycle. 2. Specific ingredients are included within the laundry powders manufactured in Nigeria, Poland and Australia to promote increased cleaning performance at lower

wash temperatures. 3. Waterless hand cleaner products avoid the requirement for hand washing in sinks thus reducing water use and energy consumption. 4. Advertising campaigns re showering for less time and also promoting replacing showerheads with those that introduce air into the water stream again reduce

water consumption and use less energy.

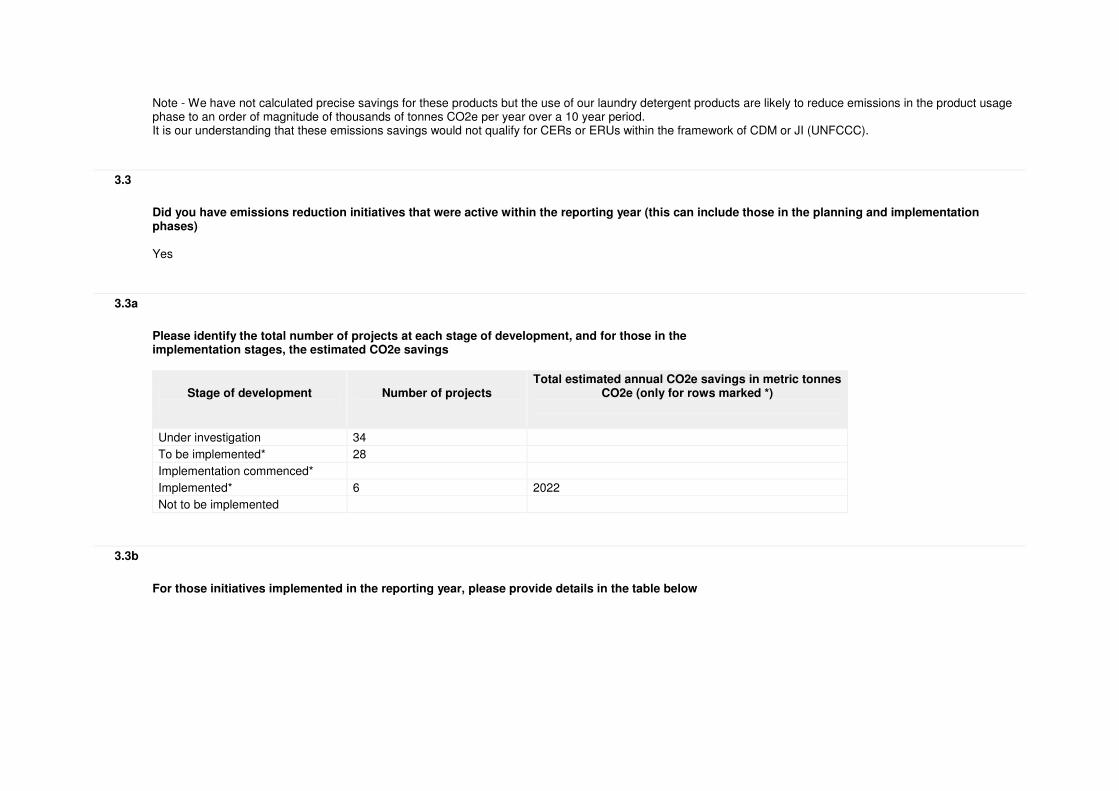

Note - We have not calculated precise savings for these products but the use of our laundry detergent products are likely to reduce emissions in the product usage phase to an order of magnitude of thousands of tonnes CO2e per year over a 10 year period. It is our understanding that these emissions savings would not qualify for CERs or ERUs within the framework of CDM or JI (UNFCCC).

3.3

Did you have emissions reduction initiatives that were active within the reporting year (this can include those in the planning and implementation phases) Yes

3.3a

Please identify the total number of projects at each stage of development, and for those in the implementation stages, the estimated CO2e savings

Stage of development

Number of projects

Total estimated annual CO2e savings in metric tonnes CO2e (only for rows marked *)

Under investigation 34

To be implemented* 28

Implementation commenced*

Implemented* 6 2022

Not to be implemented

3.3b

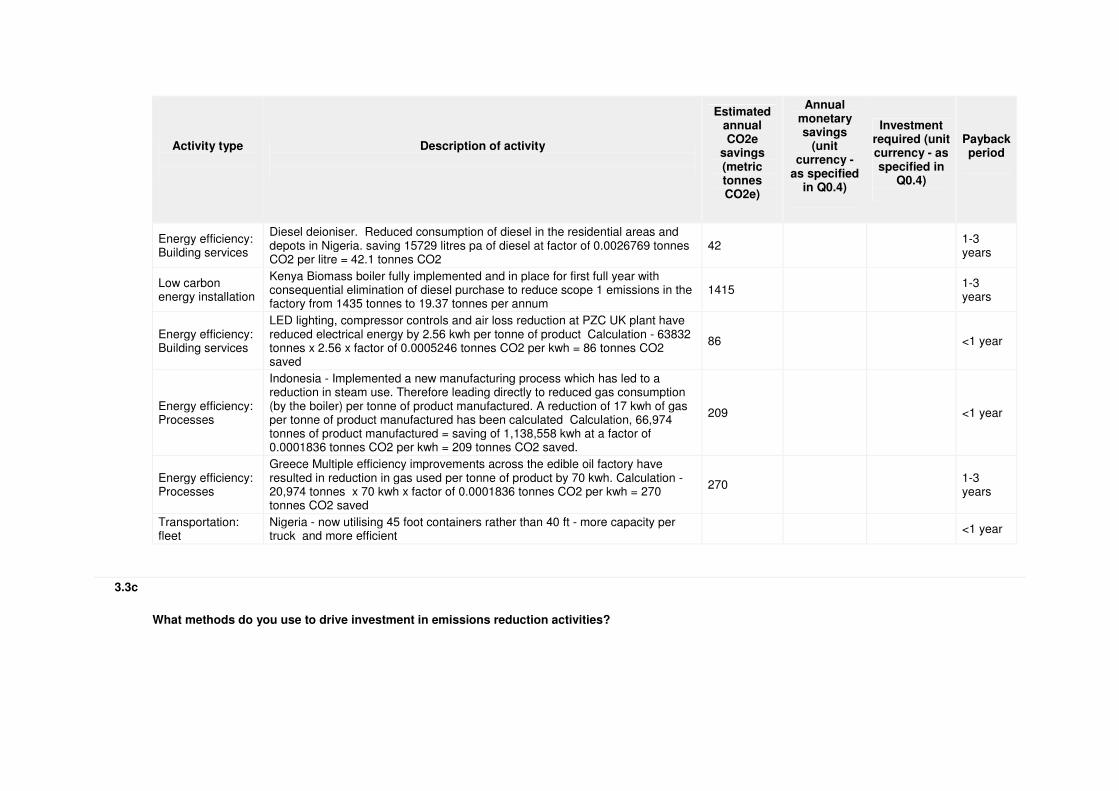

For those initiatives implemented in the reporting year, please provide details in the table below

Activity type

Description of activity

Estimated annual CO2e

savings (metric tonnes CO2e)

Annual monetary savings

(unit currency -

as specified in Q0.4)

Investment required (unit currency - as specified in

Q0.4)

Payback period

Energy efficiency: Building services

Diesel deioniser. Reduced consumption of diesel in the residential areas and depots in Nigeria. saving 15729 litres pa of diesel at factor of 0.0026769 tonnes CO2 per litre = 42.1 tonnes CO2

42

1-3 years

Low carbon energy installation

Kenya Biomass boiler fully implemented and in place for first full year with consequential elimination of diesel purchase to reduce scope 1 emissions in the factory from 1435 tonnes to 19.37 tonnes per annum

1415

1-3 years

Energy efficiency: Building services

LED lighting, compressor controls and air loss reduction at PZC UK plant have reduced electrical energy by 2.56 kwh per tonne of product Calculation - 63832 tonnes x 2.56 x factor of 0.0005246 tonnes CO2 per kwh = 86 tonnes CO2 saved

86

<1 year

Energy efficiency: Processes

Indonesia - Implemented a new manufacturing process which has led to a reduction in steam use. Therefore leading directly to reduced gas consumption (by the boiler) per tonne of product manufactured. A reduction of 17 kwh of gas per tonne of product manufactured has been calculated Calculation, 66,974 tonnes of product manufactured = saving of 1,138,558 kwh at a factor of 0.0001836 tonnes CO2 per kwh = 209 tonnes CO2 saved.

209

<1 year

Energy efficiency: Processes

Greece Multiple efficiency improvements across the edible oil factory have resulted in reduction in gas used per tonne of product by 70 kwh. Calculation - 20,974 tonnes x 70 kwh x factor of 0.0001836 tonnes CO2 per kwh = 270 tonnes CO2 saved

270

1-3 years

Transportation: fleet

Nigeria - now utilising 45 foot containers rather than 40 ft - more capacity per truck and more efficient

<1 year

3.3c

What methods do you use to drive investment in emissions reduction activities?

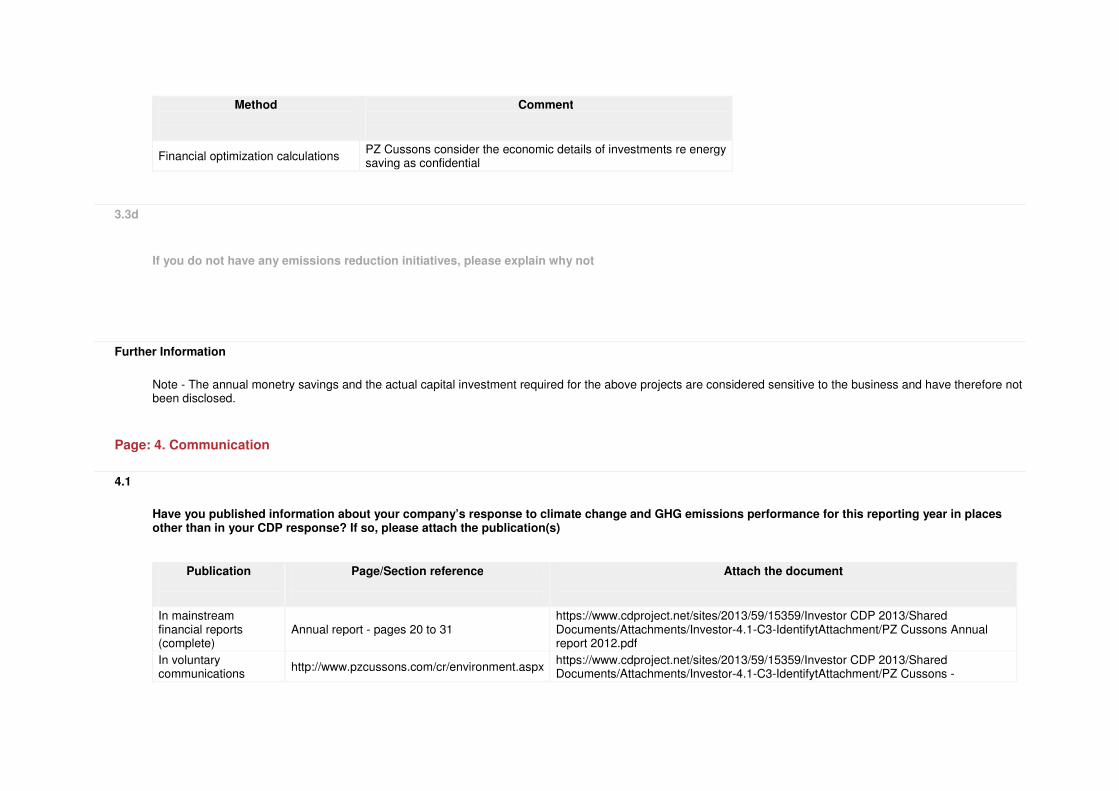

Method

Comment

Financial optimization calculations PZ Cussons consider the economic details of investments re energy saving as confidential

3.3d

If you do not have any emissions reduction initiatives, please explain why not

Further Information

Note - The annual monetry savings and the actual capital investment required for the above projects are considered sensitive to the business and have therefore not been disclosed.

Page: 4. Communication

4.1

Have you published information about your company’s response to climate change and GHG emissions performance for this reporting year in places other than in your CDP response? If so, please attach the publication(s)

Publication

Page/Section reference

Attach the document

In mainstream financial reports (complete)

Annual report - pages 20 to 31 https://www.cdproject.net/sites/2013/59/15359/Investor CDP 2013/Shared Documents/Attachments/Investor-4.1-C3-IdentifytAttachment/PZ Cussons Annual report 2012.pdf

In voluntary communications

http://www.pzcussons.com/cr/environment.aspx https://www.cdproject.net/sites/2013/59/15359/Investor CDP 2013/Shared Documents/Attachments/Investor-4.1-C3-IdentifytAttachment/PZ Cussons -

Publication

Page/Section reference

Attach the document

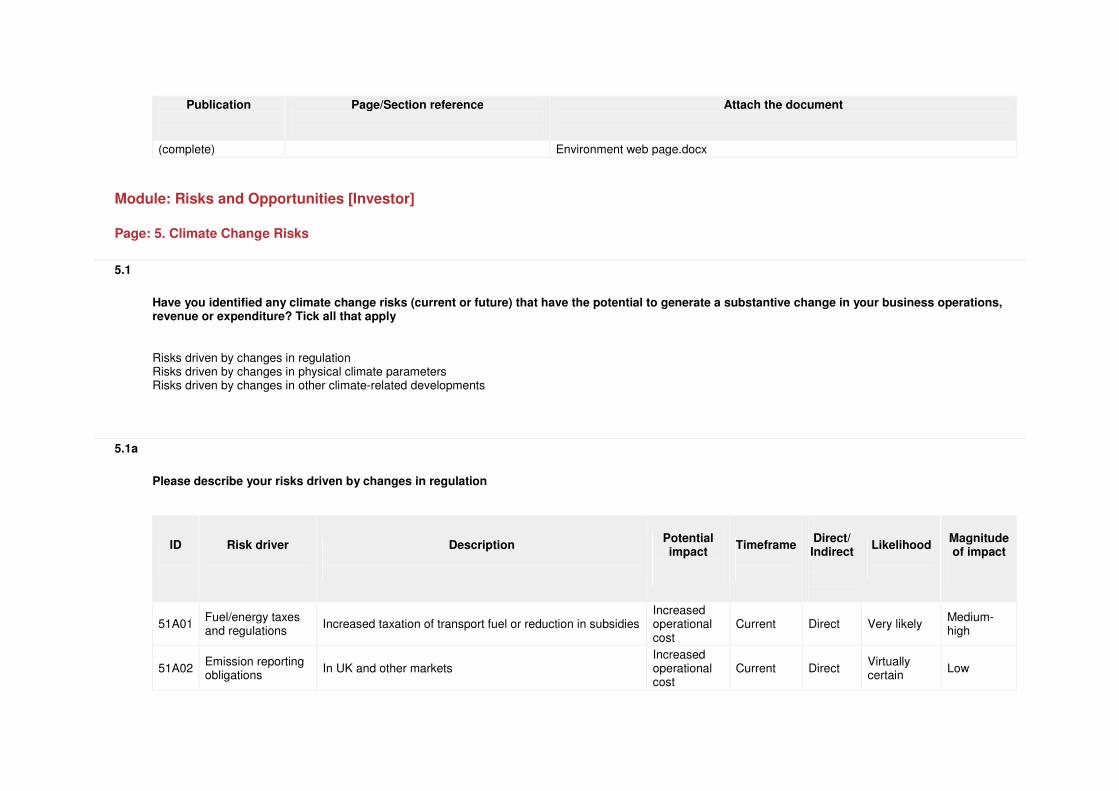

(complete) Environment web page.docx

Module: Risks and Opportunities [Investor]

Page: 5. Climate Change Risks

5.1

Have you identified any climate change risks (current or future) that have the potential to generate a substantive change in your business operations, revenue or expenditure? Tick all that apply Risks driven by changes in regulation Risks driven by changes in physical climate parameters Risks driven by changes in other climate-related developments

5.1a

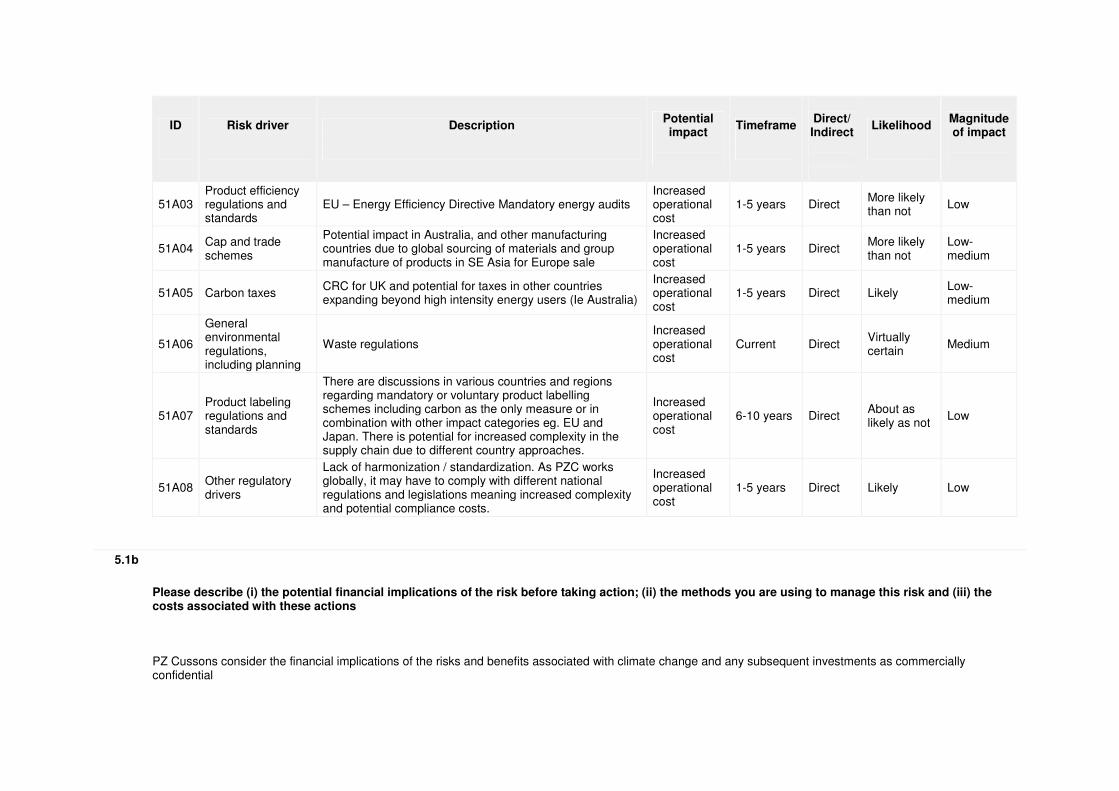

Please describe your risks driven by changes in regulation

ID

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

51A01 Fuel/energy taxes and regulations

Increased taxation of transport fuel or reduction in subsidies Increased operational cost

Current Direct Very likely Medium-high

51A02 Emission reporting obligations

In UK and other markets Increased operational cost

Current Direct Virtually certain

Low

ID

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

51A03 Product efficiency regulations and standards

EU – Energy Efficiency Directive Mandatory energy audits Increased operational cost

1-5 years Direct More likely than not

Low

51A04 Cap and trade schemes

Potential impact in Australia, and other manufacturing countries due to global sourcing of materials and group manufacture of products in SE Asia for Europe sale

Increased operational cost

1-5 years Direct More likely than not

Low-medium

51A05 Carbon taxes CRC for UK and potential for taxes in other countries expanding beyond high intensity energy users (Ie Australia)

Increased operational cost

1-5 years Direct Likely Low-medium

51A06

General environmental regulations, including planning

Waste regulations Increased operational cost

Current Direct Virtually certain

Medium

51A07 Product labeling regulations and standards

There are discussions in various countries and regions regarding mandatory or voluntary product labelling schemes including carbon as the only measure or in combination with other impact categories eg. EU and Japan. There is potential for increased complexity in the supply chain due to different country approaches.

Increased operational cost

6-10 years Direct About as likely as not

Low

51A08 Other regulatory drivers

Lack of harmonization / standardization. As PZC works globally, it may have to comply with different national regulations and legislations meaning increased complexity and potential compliance costs.

Increased operational cost

1-5 years Direct Likely Low

5.1b

Please describe (i) the potential financial implications of the risk before taking action; (ii) the methods you are using to manage this risk and (iii) the costs associated with these actions PZ Cussons consider the financial implications of the risks and benefits associated with climate change and any subsequent investments as commercially confidential

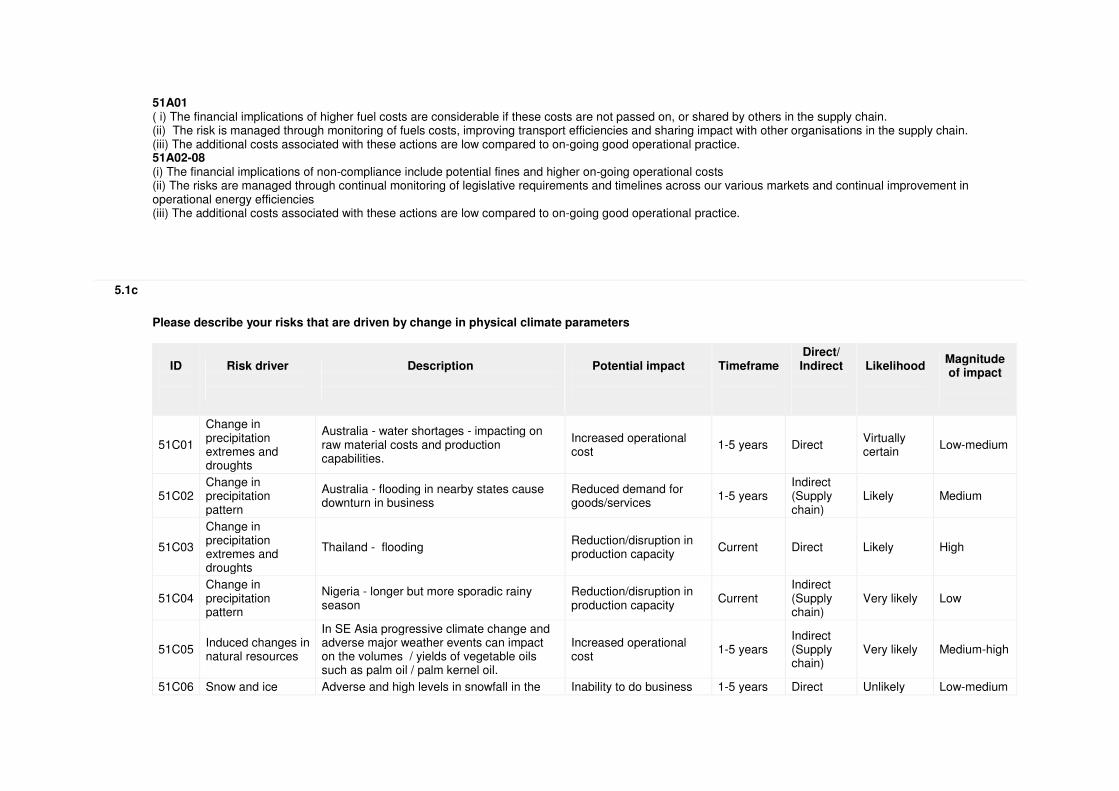

51A01 ( i) The financial implications of higher fuel costs are considerable if these costs are not passed on, or shared by others in the supply chain. (ii) The risk is managed through monitoring of fuels costs, improving transport efficiencies and sharing impact with other organisations in the supply chain. (iii) The additional costs associated with these actions are low compared to on-going good operational practice. 51A02-08 (i) The financial implications of non-compliance include potential fines and higher on-going operational costs (ii) The risks are managed through continual monitoring of legislative requirements and timelines across our various markets and continual improvement in operational energy efficiencies (iii) The additional costs associated with these actions are low compared to on-going good operational practice.

5.1c

Please describe your risks that are driven by change in physical climate parameters

ID

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

51C01

Change in precipitation extremes and droughts

Australia - water shortages - impacting on raw material costs and production capabilities.

Increased operational cost

1-5 years Direct Virtually certain

Low-medium

51C02 Change in precipitation pattern

Australia - flooding in nearby states cause downturn in business

Reduced demand for goods/services

1-5 years Indirect (Supply chain)

Likely Medium

51C03

Change in precipitation extremes and droughts

Thailand - flooding Reduction/disruption in production capacity

Current Direct Likely High

51C04 Change in precipitation pattern

Nigeria - longer but more sporadic rainy season

Reduction/disruption in production capacity

Current Indirect (Supply chain)

Very likely Low

51C05 Induced changes in natural resources

In SE Asia progressive climate change and adverse major weather events can impact on the volumes / yields of vegetable oils such as palm oil / palm kernel oil.

Increased operational cost

1-5 years Indirect (Supply chain)

Very likely Medium-high

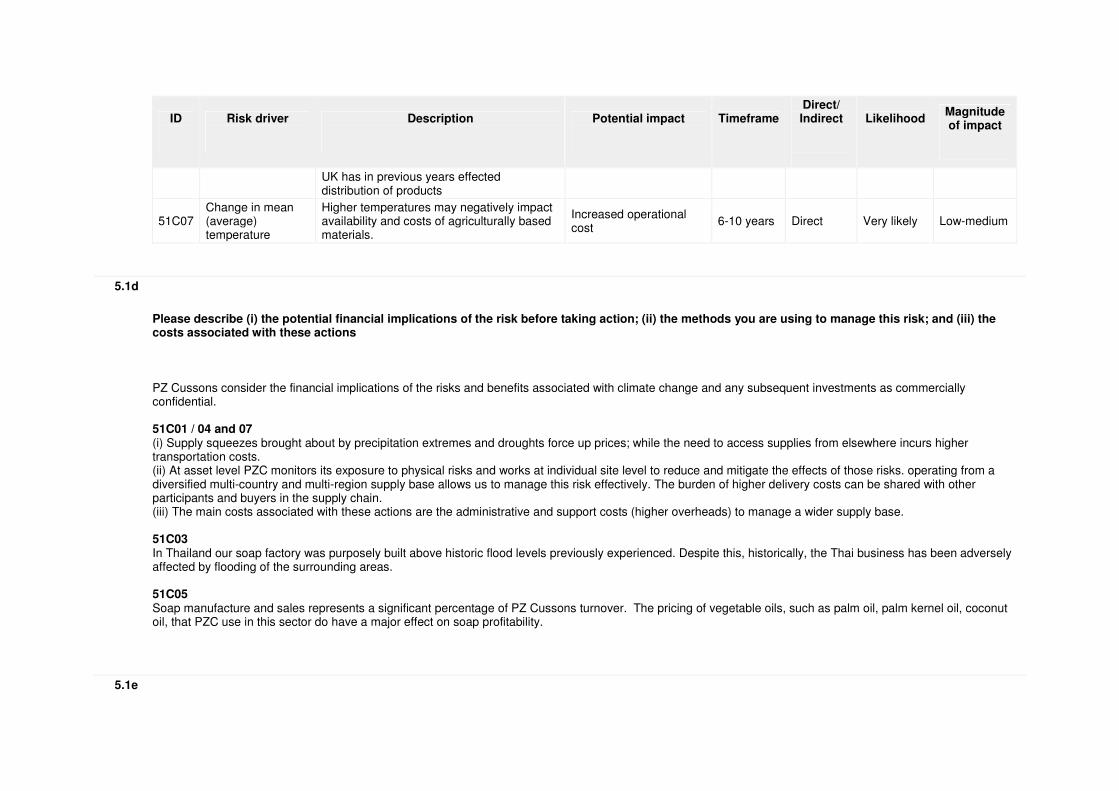

51C06 Snow and ice Adverse and high levels in snowfall in the Inability to do business 1-5 years Direct Unlikely Low-medium

ID

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

UK has in previous years effected distribution of products

51C07 Change in mean (average) temperature

Higher temperatures may negatively impact availability and costs of agriculturally based materials.

Increased operational cost

6-10 years Direct Very likely Low-medium

5.1d

Please describe (i) the potential financial implications of the risk before taking action; (ii) the methods you are using to manage this risk; and (iii) the costs associated with these actions PZ Cussons consider the financial implications of the risks and benefits associated with climate change and any subsequent investments as commercially confidential. 51C01 / 04 and 07 (i) Supply squeezes brought about by precipitation extremes and droughts force up prices; while the need to access supplies from elsewhere incurs higher transportation costs. (ii) At asset level PZC monitors its exposure to physical risks and works at individual site level to reduce and mitigate the effects of those risks. operating from a diversified multi-country and multi-region supply base allows us to manage this risk effectively. The burden of higher delivery costs can be shared with other participants and buyers in the supply chain. (iii) The main costs associated with these actions are the administrative and support costs (higher overheads) to manage a wider supply base. 51C03 In Thailand our soap factory was purposely built above historic flood levels previously experienced. Despite this, historically, the Thai business has been adversely affected by flooding of the surrounding areas. 51C05 Soap manufacture and sales represents a significant percentage of PZ Cussons turnover. The pricing of vegetable oils, such as palm oil, palm kernel oil, coconut oil, that PZC use in this sector do have a major effect on soap profitability.

5.1e

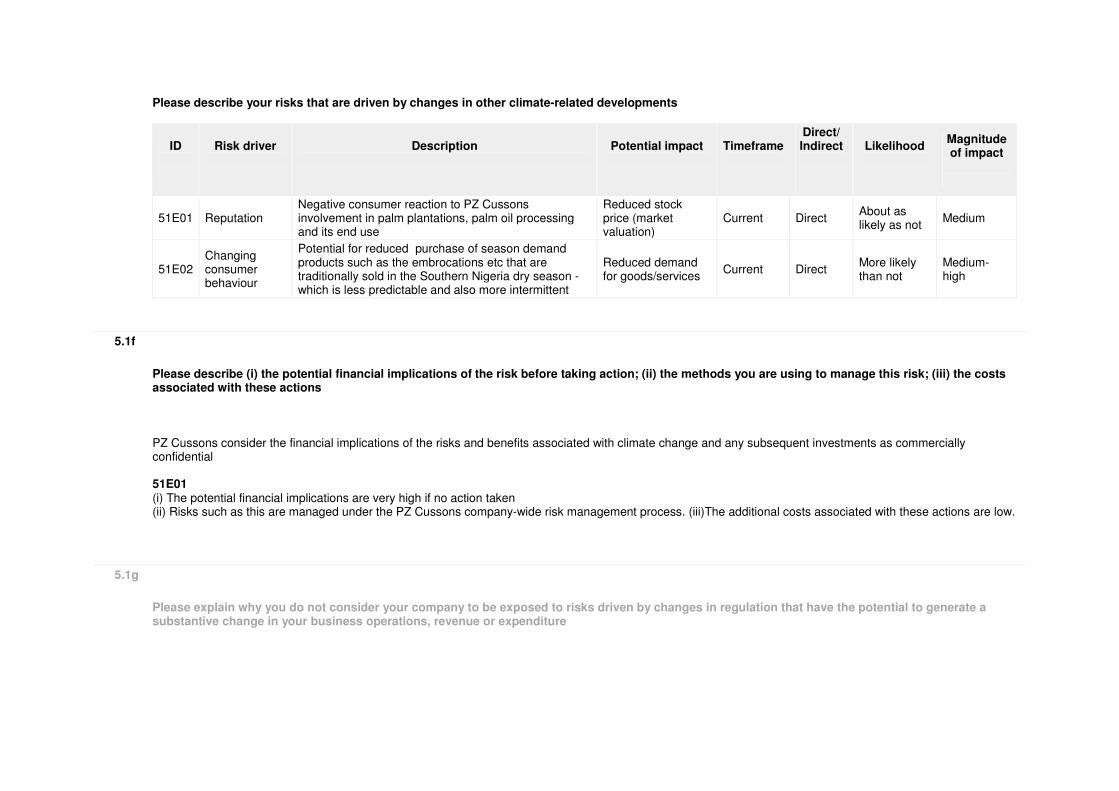

Please describe your risks that are driven by changes in other climate-related developments

ID

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

51E01 Reputation Negative consumer reaction to PZ Cussons involvement in palm plantations, palm oil processing and its end use

Reduced stock price (market valuation)

Current Direct About as likely as not

Medium

51E02 Changing consumer behaviour

Potential for reduced purchase of season demand products such as the embrocations etc that are traditionally sold in the Southern Nigeria dry season - which is less predictable and also more intermittent

Reduced demand for goods/services

Current Direct More likely than not

Medium-high

5.1f

Please describe (i) the potential financial implications of the risk before taking action; (ii) the methods you are using to manage this risk; (iii) the costs associated with these actions PZ Cussons consider the financial implications of the risks and benefits associated with climate change and any subsequent investments as commercially confidential 51E01 (i) The potential financial implications are very high if no action taken (ii) Risks such as this are managed under the PZ Cussons company-wide risk management process. (iii)The additional costs associated with these actions are low.

5.1g

Please explain why you do not consider your company to be exposed to risks driven by changes in regulation that have the potential to generate a substantive change in your business operations, revenue or expenditure

5.1h

Please explain why you do not consider your company to be exposed to risks driven by physical climate parameters that have the potential to generate a substantive change in your business operations, revenue or expenditure

5.1i

Please explain why you do not consider your company to be exposed to risks driven by changes in other climate-related developments that have the potential to generate a substantive change in your business operations, revenue or expenditure

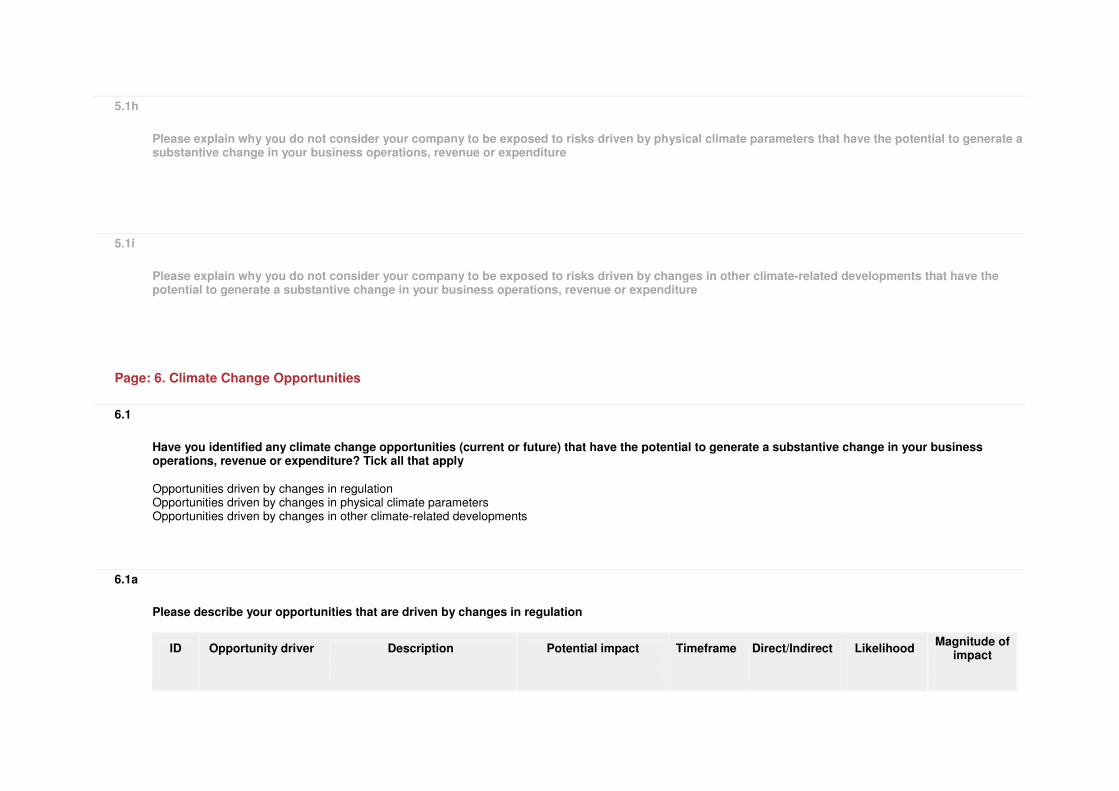

Page: 6. Climate Change Opportunities

6.1

Have you identified any climate change opportunities (current or future) that have the potential to generate a substantive change in your business operations, revenue or expenditure? Tick all that apply Opportunities driven by changes in regulation Opportunities driven by changes in physical climate parameters Opportunities driven by changes in other climate-related developments

6.1a

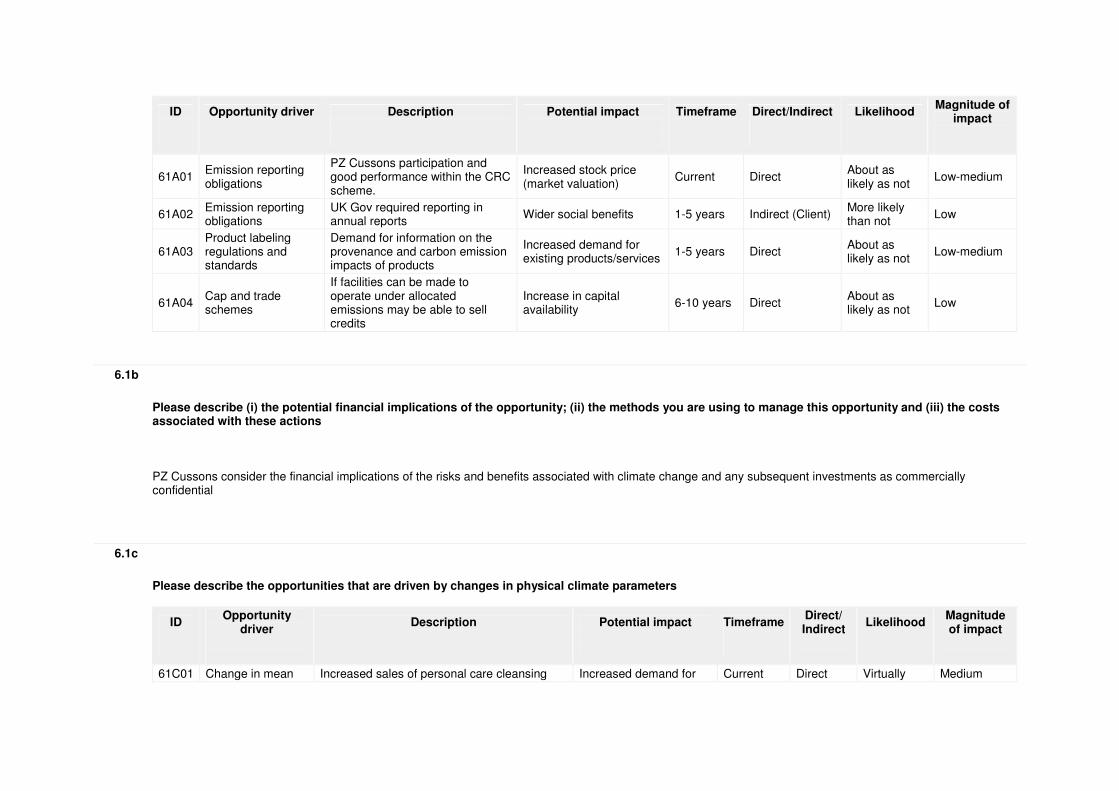

Please describe your opportunities that are driven by changes in regulation

ID

Opportunity driver

Description

Potential impact

Timeframe

Direct/Indirect

Likelihood

Magnitude of impact

ID

Opportunity driver

Description

Potential impact

Timeframe

Direct/Indirect

Likelihood

Magnitude of impact

61A01 Emission reporting obligations

PZ Cussons participation and good performance within the CRC scheme.

Increased stock price (market valuation)

Current Direct About as likely as not

Low-medium

61A02 Emission reporting obligations

UK Gov required reporting in annual reports

Wider social benefits 1-5 years Indirect (Client) More likely than not

Low

61A03 Product labeling regulations and standards

Demand for information on the provenance and carbon emission impacts of products

Increased demand for existing products/services

1-5 years Direct About as likely as not

Low-medium

61A04 Cap and trade schemes

If facilities can be made to operate under allocated emissions may be able to sell credits

Increase in capital availability

6-10 years Direct About as likely as not

Low

6.1b

Please describe (i) the potential financial implications of the opportunity; (ii) the methods you are using to manage this opportunity and (iii) the costs associated with these actions PZ Cussons consider the financial implications of the risks and benefits associated with climate change and any subsequent investments as commercially confidential

6.1c

Please describe the opportunities that are driven by changes in physical climate parameters

ID

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

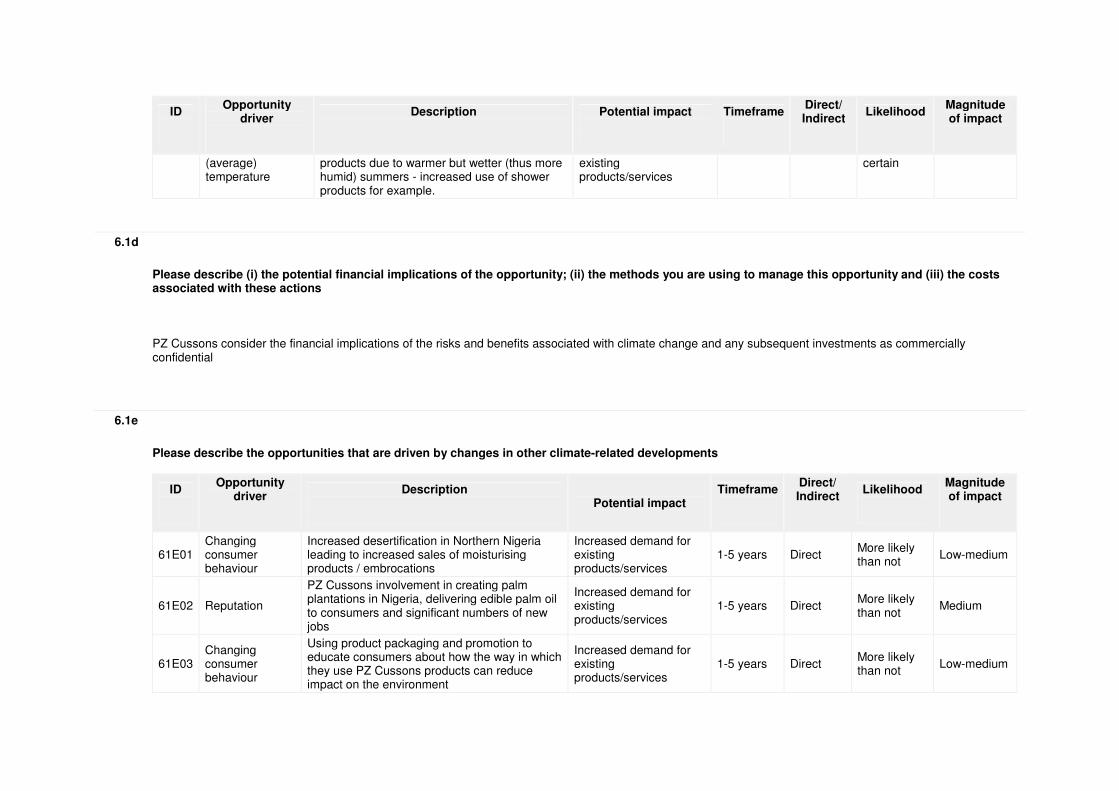

61C01 Change in mean Increased sales of personal care cleansing Increased demand for Current Direct Virtually Medium

ID

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

(average) temperature

products due to warmer but wetter (thus more humid) summers - increased use of shower products for example.

existing products/services

certain

6.1d

Please describe (i) the potential financial implications of the opportunity; (ii) the methods you are using to manage this opportunity and (iii) the costs associated with these actions PZ Cussons consider the financial implications of the risks and benefits associated with climate change and any subsequent investments as commercially confidential

6.1e

Please describe the opportunities that are driven by changes in other climate-related developments

ID

Opportunity driver

Description

Potential impact Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

61E01 Changing consumer behaviour

Increased desertification in Northern Nigeria leading to increased sales of moisturising products / embrocations

Increased demand for existing products/services

1-5 years Direct More likely than not

Low-medium

61E02 Reputation

PZ Cussons involvement in creating palm plantations in Nigeria, delivering edible palm oil to consumers and significant numbers of new jobs

Increased demand for existing products/services

1-5 years Direct More likely than not

Medium

61E03 Changing consumer behaviour

Using product packaging and promotion to educate consumers about how the way in which they use PZ Cussons products can reduce impact on the environment

Increased demand for existing products/services

1-5 years Direct More likely than not

Low-medium

6.1f

Please describe (i) the potential financial implications of the opportunity; (ii) the methods you are using to manage this opportunity; (iii) the costs associated with these actions PZ Cussons consider the financial implications of the risks and benefits associated with climate change and any subsequent investments as commercially confidential

6.1g

Please explain why you do not consider your company to be exposed to opportunities driven by changes in regulation that have the potential to generate a substantive change in your business operations, revenue or expenditure

6.1h

Please explain why you do not consider your company to be exposed to opportunities driven by physical climate parameters that have the potential to generate a substantive change in your business operations, revenue or expenditure

6.1i

Please explain why you do not consider your company to be exposed to opportunities driven by changes in other climate-related developments that have the potential to generate a substantive change in your business operations, revenue or expenditure

Module: GHG Emissions Accounting, Energy and Fuel Use, and Trading [Investor]

Page: 7. Emissions Methodology

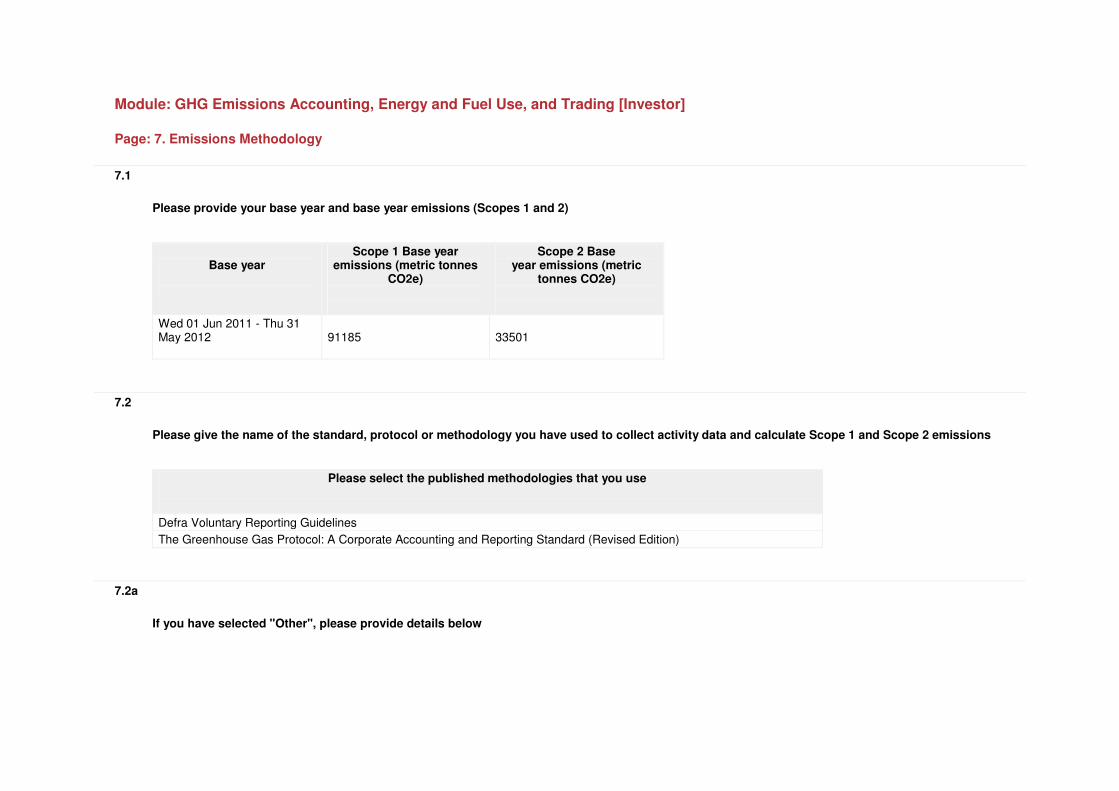

7.1

Please provide your base year and base year emissions (Scopes 1 and 2)

Base year

Scope 1 Base year emissions (metric tonnes

CO2e)

Scope 2 Base year emissions (metric

tonnes CO2e)

Wed 01 Jun 2011 - Thu 31 May 2012

91185 33501

7.2

Please give the name of the standard, protocol or methodology you have used to collect activity data and calculate Scope 1 and Scope 2 emissions

Please select the published methodologies that you use

Defra Voluntary Reporting Guidelines

The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (Revised Edition)

7.2a

If you have selected "Other", please provide details below

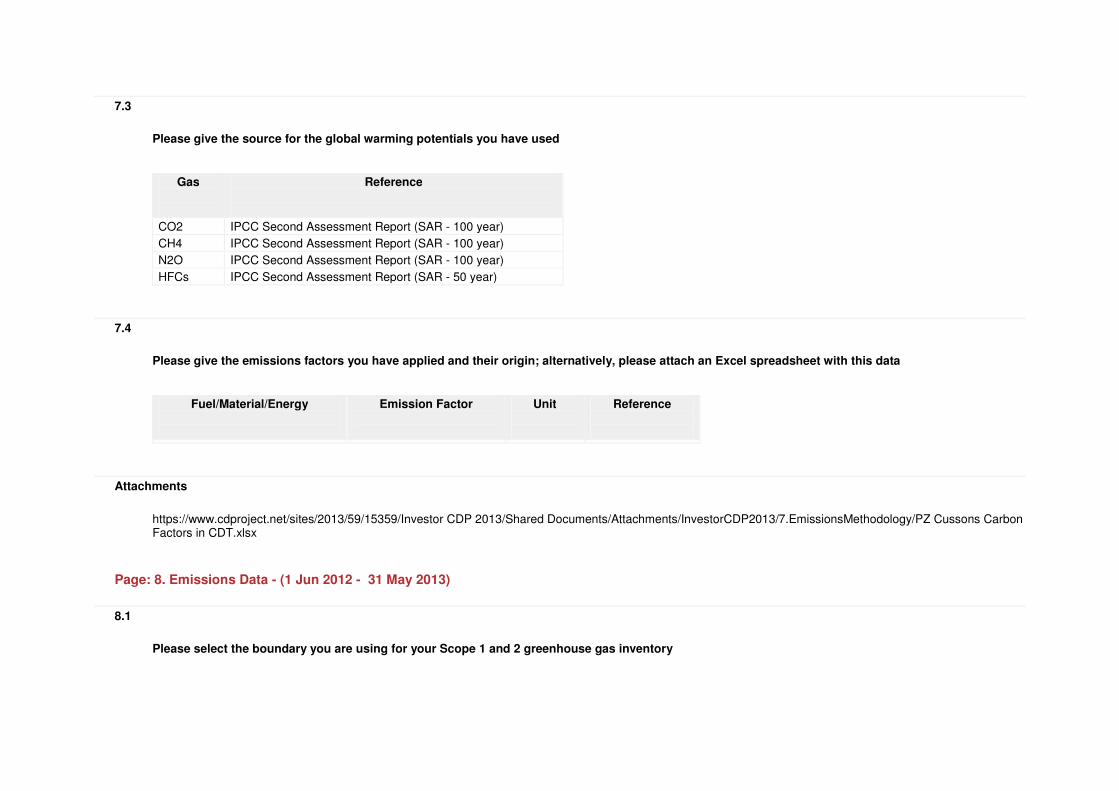

7.3

Please give the source for the global warming potentials you have used

Gas

Reference

CO2 IPCC Second Assessment Report (SAR - 100 year)

CH4 IPCC Second Assessment Report (SAR - 100 year)

N2O IPCC Second Assessment Report (SAR - 100 year)

HFCs IPCC Second Assessment Report (SAR - 50 year)

7.4

Please give the emissions factors you have applied and their origin; alternatively, please attach an Excel spreadsheet with this data

Fuel/Material/Energy

Emission Factor

Unit

Reference

Attachments

https://www.cdproject.net/sites/2013/59/15359/Investor CDP 2013/Shared Documents/Attachments/InvestorCDP2013/7.EmissionsMethodology/PZ Cussons Carbon Factors in CDT.xlsx

Page: 8. Emissions Data - (1 Jun 2012 - 31 May 2013)

8.1

Please select the boundary you are using for your Scope 1 and 2 greenhouse gas inventory

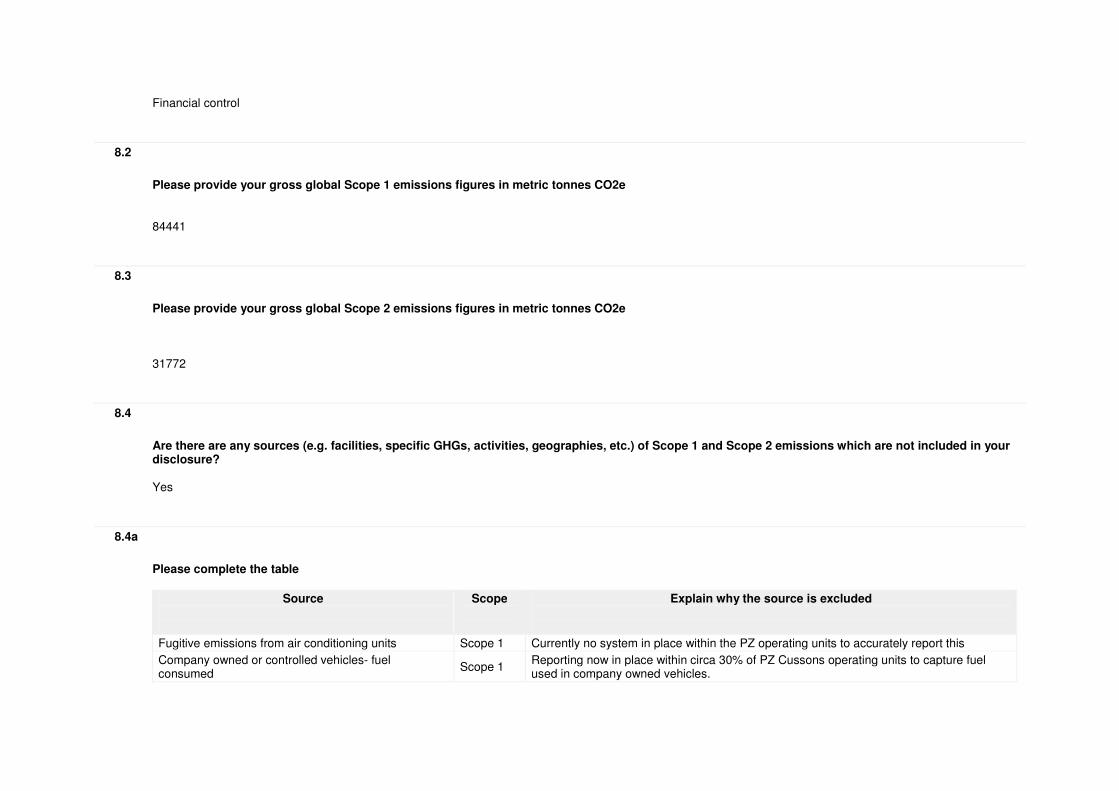

Financial control

8.2

Please provide your gross global Scope 1 emissions figures in metric tonnes CO2e 84441

8.3

Please provide your gross global Scope 2 emissions figures in metric tonnes CO2e 31772

8.4

Are there are any sources (e.g. facilities, specific GHGs, activities, geographies, etc.) of Scope 1 and Scope 2 emissions which are not included in your disclosure? Yes

8.4a

Please complete the table

Source

Scope

Explain why the source is excluded

Fugitive emissions from air conditioning units Scope 1 Currently no system in place within the PZ operating units to accurately report this

Company owned or controlled vehicles- fuel consumed

Scope 1 Reporting now in place within circa 30% of PZ Cussons operating units to capture fuel used in company owned vehicles.

Source

Scope

Explain why the source is excluded

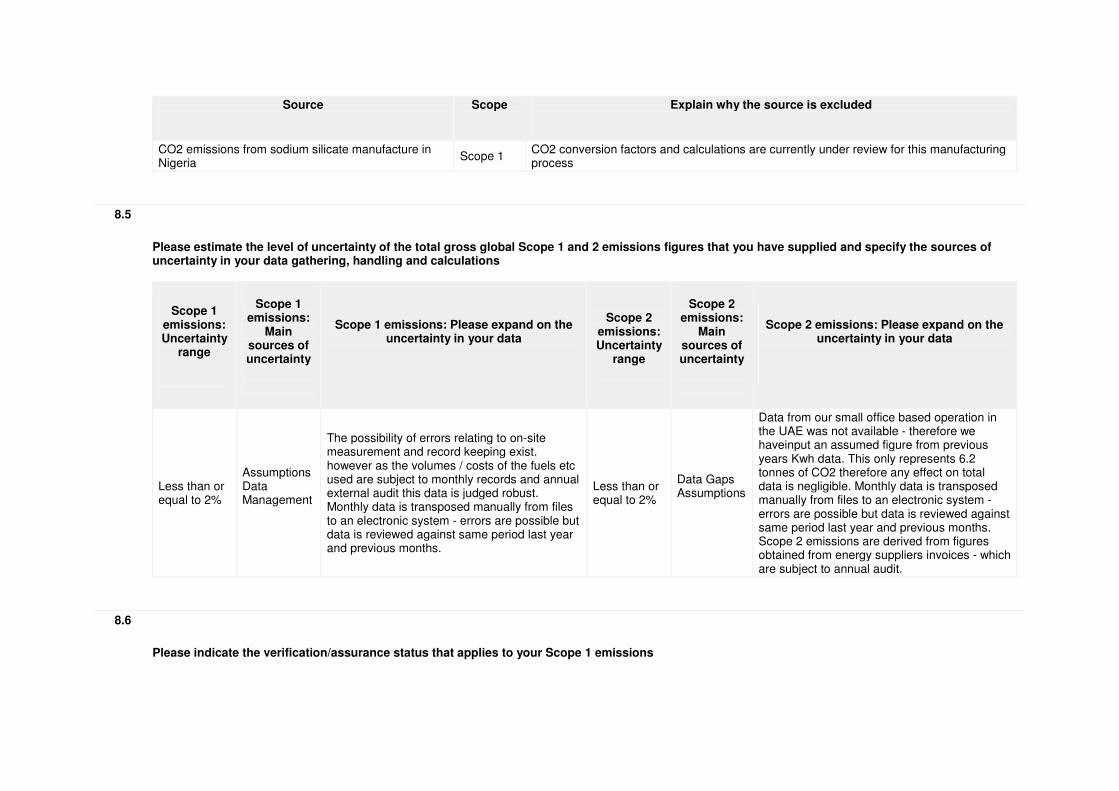

CO2 emissions from sodium silicate manufacture in Nigeria

Scope 1 CO2 conversion factors and calculations are currently under review for this manufacturing process

8.5

Please estimate the level of uncertainty of the total gross global Scope 1 and 2 emissions figures that you have supplied and specify the sources of uncertainty in your data gathering, handling and calculations

Scope 1

emissions: Uncertainty

range

Scope 1

emissions: Main

sources of uncertainty

Scope 1 emissions: Please expand on the

uncertainty in your data

Scope 2

emissions: Uncertainty

range

Scope 2

emissions: Main

sources of uncertainty

Scope 2 emissions: Please expand on the

uncertainty in your data

Less than or equal to 2%

Assumptions Data Management

The possibility of errors relating to on-site measurement and record keeping exist. however as the volumes / costs of the fuels etc used are subject to monthly records and annual external audit this data is judged robust. Monthly data is transposed manually from files to an electronic system - errors are possible but data is reviewed against same period last year and previous months.

Less than or equal to 2%

Data Gaps Assumptions

Data from our small office based operation in the UAE was not available - therefore we haveinput an assumed figure from previous years Kwh data. This only represents 6.2 tonnes of CO2 therefore any effect on total data is negligible. Monthly data is transposed manually from files to an electronic system - errors are possible but data is reviewed against same period last year and previous months. Scope 2 emissions are derived from figures obtained from energy suppliers invoices - which are subject to annual audit.

8.6

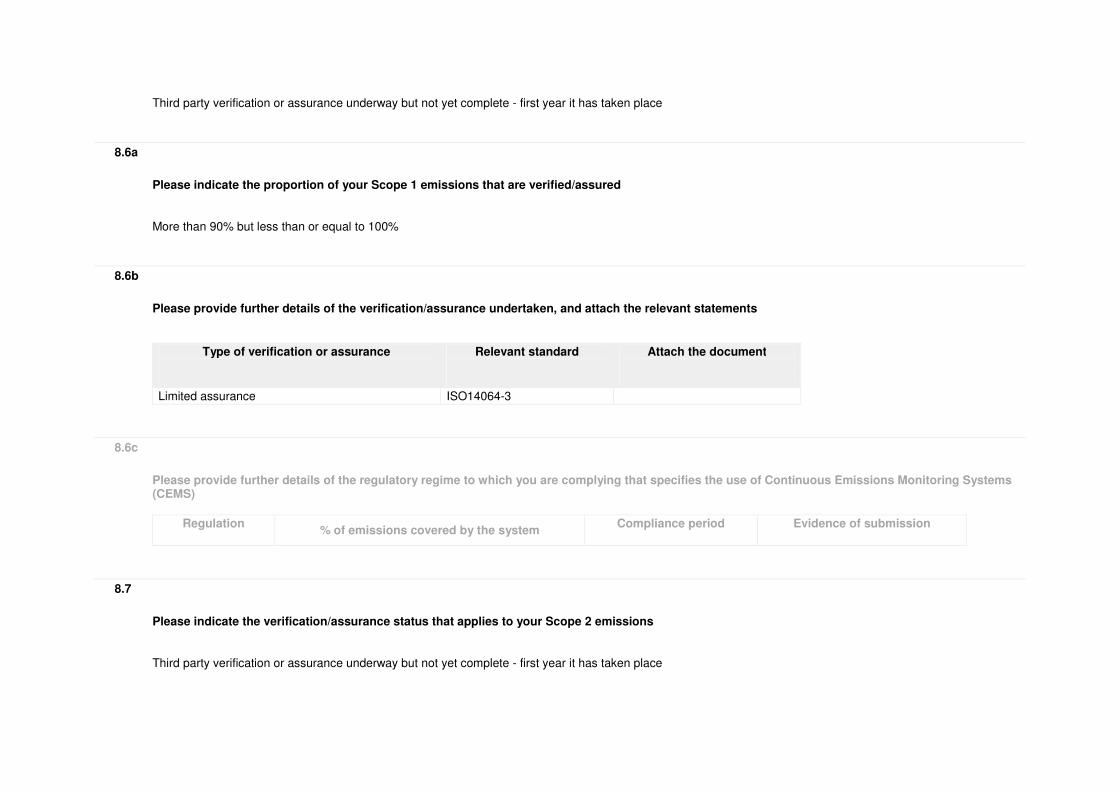

Please indicate the verification/assurance status that applies to your Scope 1 emissions

Third party verification or assurance underway but not yet complete - first year it has taken place

8.6a

Please indicate the proportion of your Scope 1 emissions that are verified/assured More than 90% but less than or equal to 100%

8.6b

Please provide further details of the verification/assurance undertaken, and attach the relevant statements

Type of verification or assurance

Relevant standard

Attach the document

Limited assurance ISO14064-3

8.6c

Please provide further details of the regulatory regime to which you are complying that specifies the use of Continuous Emissions Monitoring Systems (CEMS)

Regulation

% of emissions covered by the system Compliance period

Evidence of submission

8.7

Please indicate the verification/assurance status that applies to your Scope 2 emissions Third party verification or assurance underway but not yet complete - first year it has taken place

8.7a

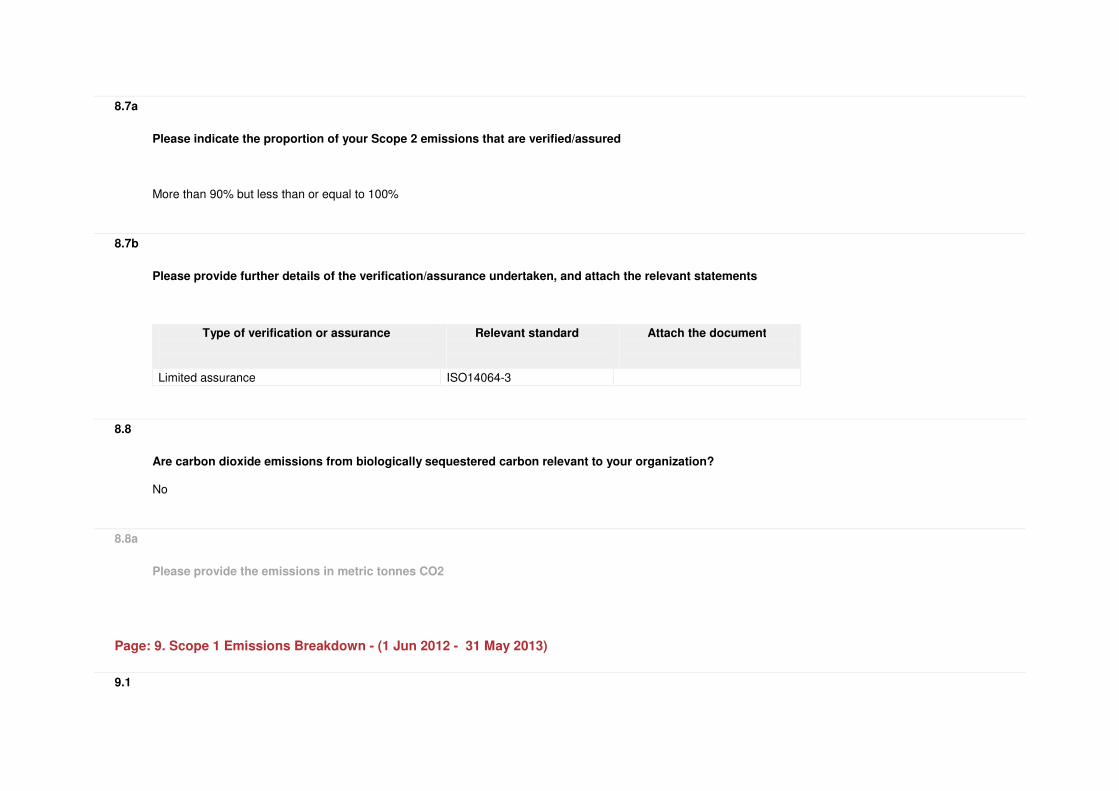

Please indicate the proportion of your Scope 2 emissions that are verified/assured More than 90% but less than or equal to 100%

8.7b

Please provide further details of the verification/assurance undertaken, and attach the relevant statements

Type of verification or assurance

Relevant standard

Attach the document

Limited assurance ISO14064-3

8.8

Are carbon dioxide emissions from biologically sequestered carbon relevant to your organization? No

8.8a

Please provide the emissions in metric tonnes CO2

Page: 9. Scope 1 Emissions Breakdown - (1 Jun 2012 - 31 May 2013)

9.1

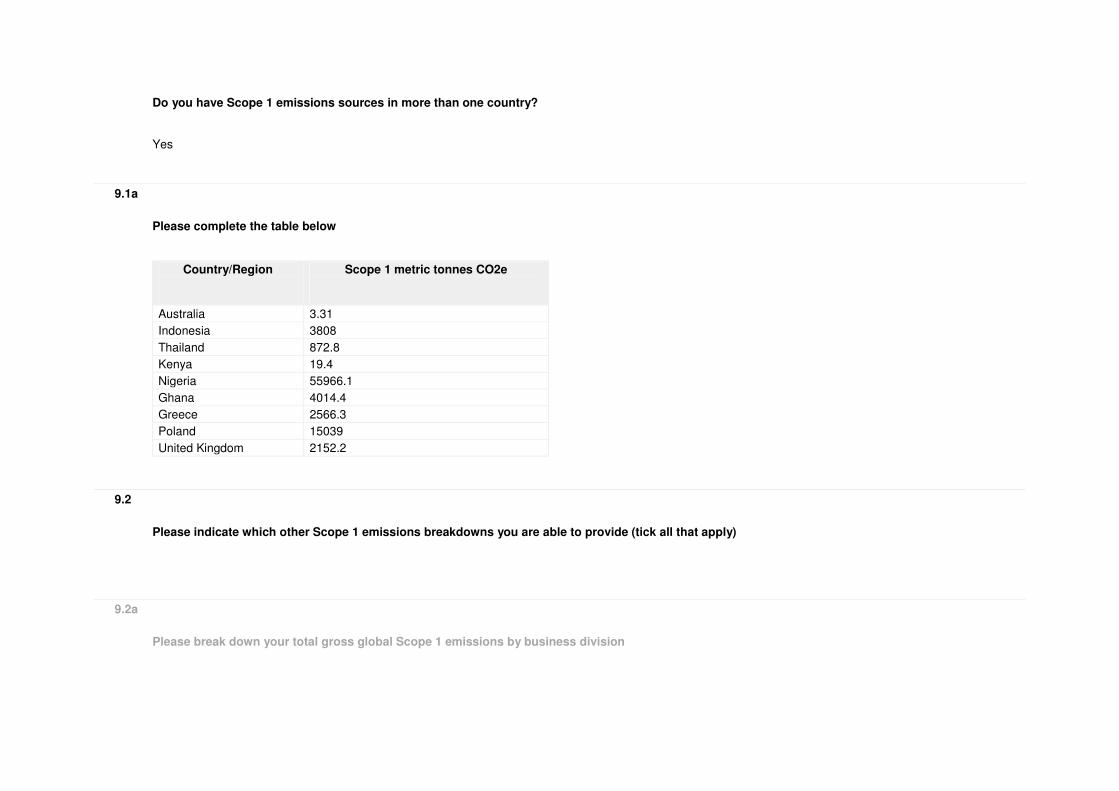

Do you have Scope 1 emissions sources in more than one country? Yes

9.1a

Please complete the table below

Country/Region

Scope 1 metric tonnes CO2e

Australia 3.31

Indonesia 3808

Thailand 872.8

Kenya 19.4

Nigeria 55966.1

Ghana 4014.4

Greece 2566.3

Poland 15039

United Kingdom 2152.2

9.2

Please indicate which other Scope 1 emissions breakdowns you are able to provide (tick all that apply)

9.2a

Please break down your total gross global Scope 1 emissions by business division

Business division

Scope 1 emissions (metric tonnes CO2e)

9.2b

Please break down your total gross global Scope 1 emissions by facility

Facility

Scope 1 emissions (metric tonnes CO2e)

Latitude

Longitude

9.2c

Please break down your total gross global Scope 1 emissions by GHG type

GHG type

Scope 1 emissions (metric tonnes CO2e)

9.2d

Please break down your total gross global Scope 1 emissions by activity

Activity

Scope 1 emissions (metric tonnes CO2e)

9.2e

Please break down your total gross global Scope 1 emissions by legal structure

Legal structure

Scope 1 emissions (metric tonnes CO2e)

Page: 10. Scope 2 Emissions Breakdown - (1 Jun 2012 - 31 May 2013)

10.1

Do you have Scope 2 emissions sources in more than one country? Yes

10.1a

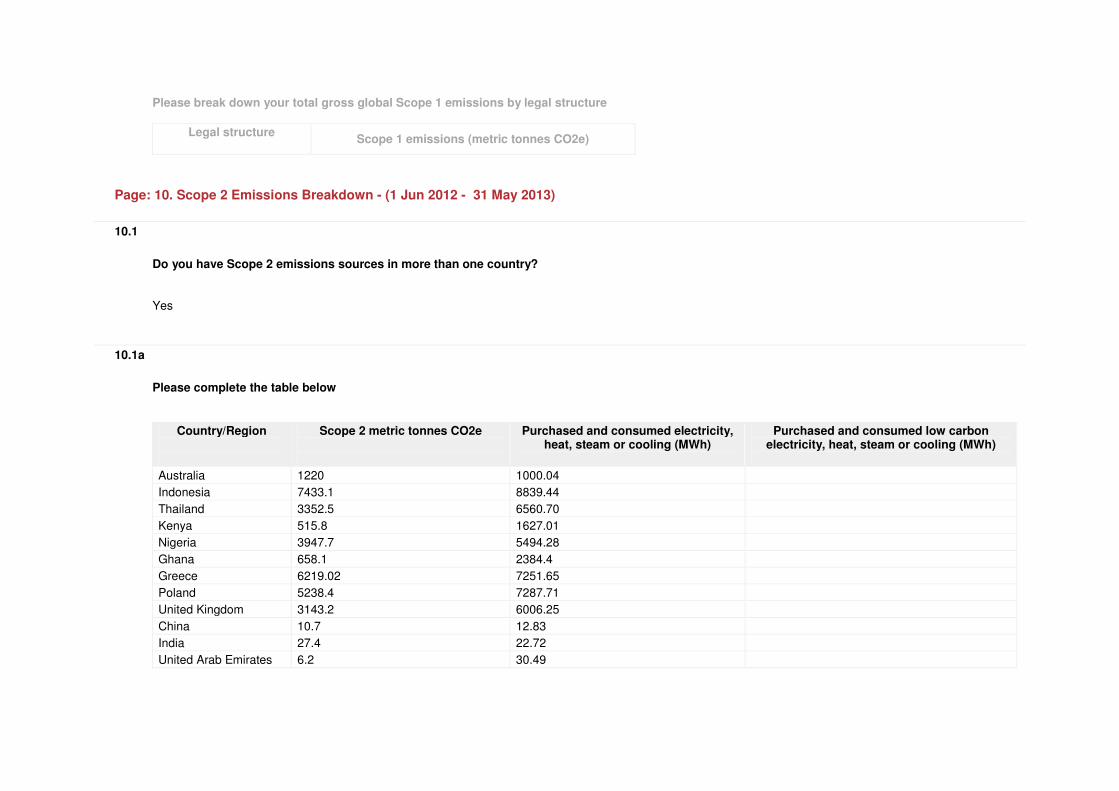

Please complete the table below

Country/Region

Scope 2 metric tonnes CO2e

Purchased and consumed electricity, heat, steam or cooling (MWh)

Purchased and consumed low carbon electricity, heat, steam or cooling (MWh)

Australia 1220 1000.04

Indonesia 7433.1 8839.44

Thailand 3352.5 6560.70

Kenya 515.8 1627.01

Nigeria 3947.7 5494.28

Ghana 658.1 2384.4

Greece 6219.02 7251.65

Poland 5238.4 7287.71

United Kingdom 3143.2 6006.25

China 10.7 12.83

India 27.4 22.72

United Arab Emirates 6.2 30.49

10.2

Please indicate which other Scope 2 emissions breakdowns you are able to provide (tick all that apply)

10.2a

Please break down your total gross global Scope 2 emissions by business division

Business division

Scope 2 emissions (metric tonnes CO2e)

10.2b

Please break down your total gross global Scope 2 emissions by facility

Facility

Scope 2 emissions (metric tonnes CO2e)

10.2c

Please break down your total gross global Scope 2 emissions by activity

Activity

Scope 2 emissions (metric tonnes CO2e)

10.2d

Please break down your total gross global Scope 2 emissions by legal structure

Legal structure

Scope 2 emissions (metric tonnes CO2e)

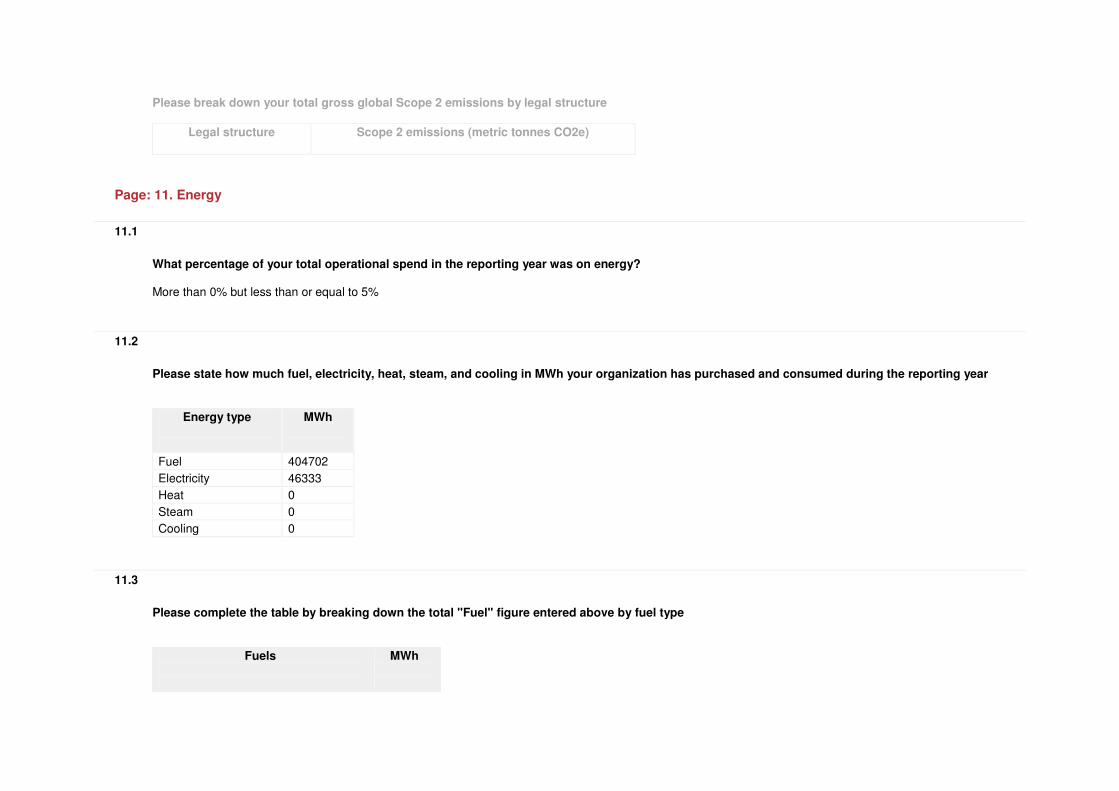

Page: 11. Energy

11.1

What percentage of your total operational spend in the reporting year was on energy? More than 0% but less than or equal to 5%

11.2

Please state how much fuel, electricity, heat, steam, and cooling in MWh your organization has purchased and consumed during the reporting year

Energy type

MWh

Fuel 404702

Electricity 46333

Heat 0

Steam 0

Cooling 0

11.3

Please complete the table by breaking down the total "Fuel" figure entered above by fuel type

Fuels

MWh

Fuels

MWh

Residual fuel oil 14667

Bituminous coal 47725

Diesel/Gas oil 25918

Natural gas 305263

Liquefied petroleum gas (LPG) 800

Other: petrol 5725

Other: miscellaneous fuel 4604

11.4

Please provide details of the electricity, heat, steam or cooling amounts that were accounted at a low carbon emission factor

Basis for applying a low carbon emission factor

MWh associated with low carbon electricity, heat, steam or cooling

Comments

Page: 12. Emissions Performance

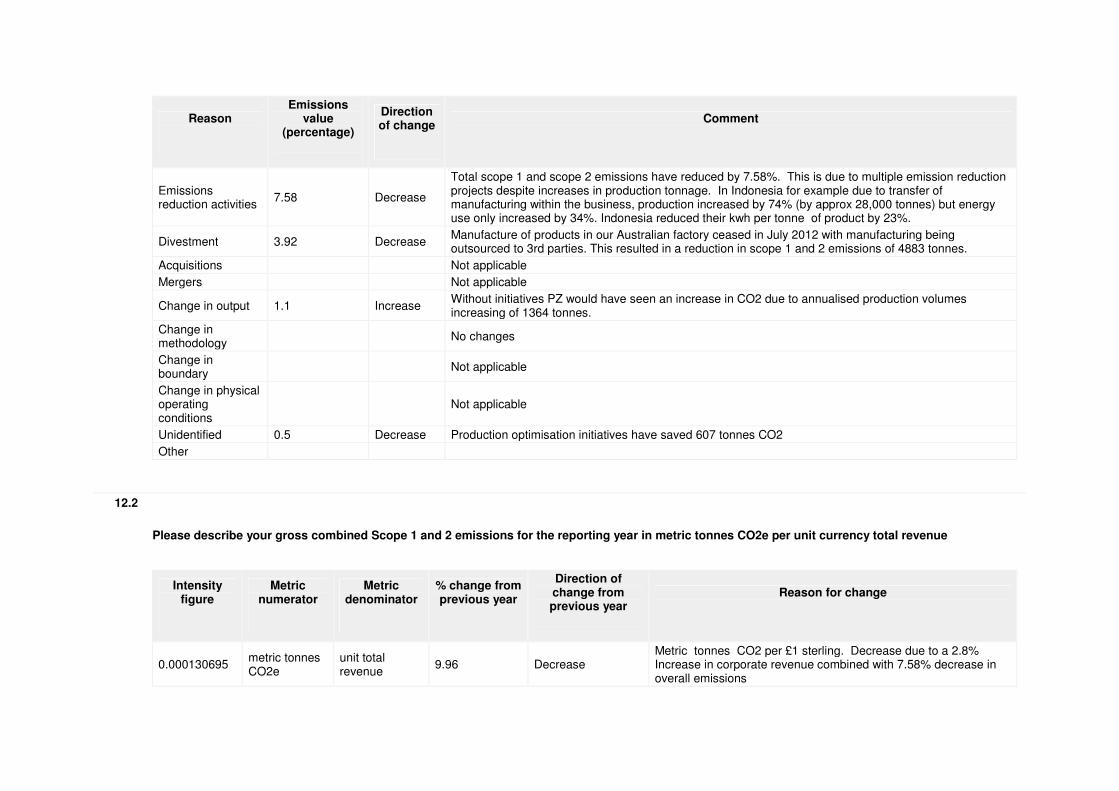

12.1

How do your absolute emissions (Scope 1 and 2 combined) for the reporting year compare to the previous year? Decreased

12.1a

Please complete the table

Reason

Emissions value

(percentage)

Direction of change

Comment

Emissions reduction activities

7.58 Decrease

Total scope 1 and scope 2 emissions have reduced by 7.58%. This is due to multiple emission reduction projects despite increases in production tonnage. In Indonesia for example due to transfer of manufacturing within the business, production increased by 74% (by approx 28,000 tonnes) but energy use only increased by 34%. Indonesia reduced their kwh per tonne of product by 23%.

Divestment 3.92 Decrease Manufacture of products in our Australian factory ceased in July 2012 with manufacturing being outsourced to 3rd parties. This resulted in a reduction in scope 1 and 2 emissions of 4883 tonnes.

Acquisitions

Not applicable

Mergers

Not applicable

Change in output 1.1 Increase Without initiatives PZ would have seen an increase in CO2 due to annualised production volumes increasing of 1364 tonnes.

Change in methodology

No changes

Change in boundary

Not applicable

Change in physical operating conditions

Not applicable

Unidentified 0.5 Decrease Production optimisation initiatives have saved 607 tonnes CO2

Other

12.2

Please describe your gross combined Scope 1 and 2 emissions for the reporting year in metric tonnes CO2e per unit currency total revenue

Intensity figure

Metric numerator

Metric denominator

% change from previous year

Direction of change from previous year

Reason for change

0.000130695 metric tonnes CO2e

unit total revenue

9.96 Decrease Metric tonnes CO2 per £1 sterling. Decrease due to a 2.8% Increase in corporate revenue combined with 7.58% decrease in overall emissions

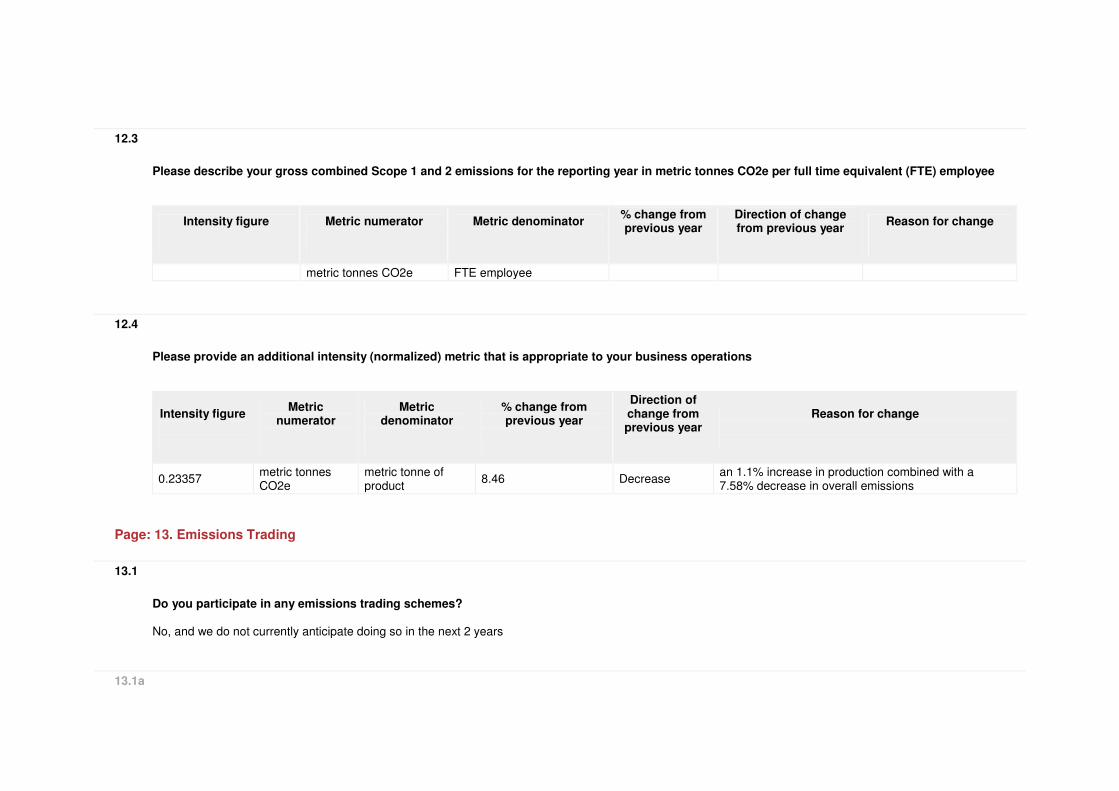

12.3

Please describe your gross combined Scope 1 and 2 emissions for the reporting year in metric tonnes CO2e per full time equivalent (FTE) employee

Intensity figure

Metric numerator

Metric denominator

% change from previous year

Direction of change from previous year

Reason for change

metric tonnes CO2e FTE employee

12.4

Please provide an additional intensity (normalized) metric that is appropriate to your business operations

Intensity figure

Metric numerator

Metric denominator

% change from previous year

Direction of change from previous year

Reason for change

0.23357 metric tonnes CO2e

metric tonne of product

8.46 Decrease an 1.1% increase in production combined with a 7.58% decrease in overall emissions

Page: 13. Emissions Trading

13.1

Do you participate in any emissions trading schemes? No, and we do not currently anticipate doing so in the next 2 years

13.1a

Please complete the following table for each of the emission trading schemes in which you participate

Scheme name

Period for which data is supplied

Allowances allocated

Allowances purchased

Verified emissions in metric tonnes CO2e

Details of ownership

13.1b

What is your strategy for complying with the schemes in which you participate or anticipate participating?

13.2

Has your company originated any project-based carbon credits or purchased any within the reporting period? No

13.2a

Please complete the table

Credit origination

or credit purchase

Project type

Project identification

Verified to which standard

Number of credits (metric

tonnes of CO2e)

Number of credits (metric tonnes

CO2e): Risk adjusted volume

Credits retired

Purpose, e.g. compliance

Page: 14. Scope 3 Emissions

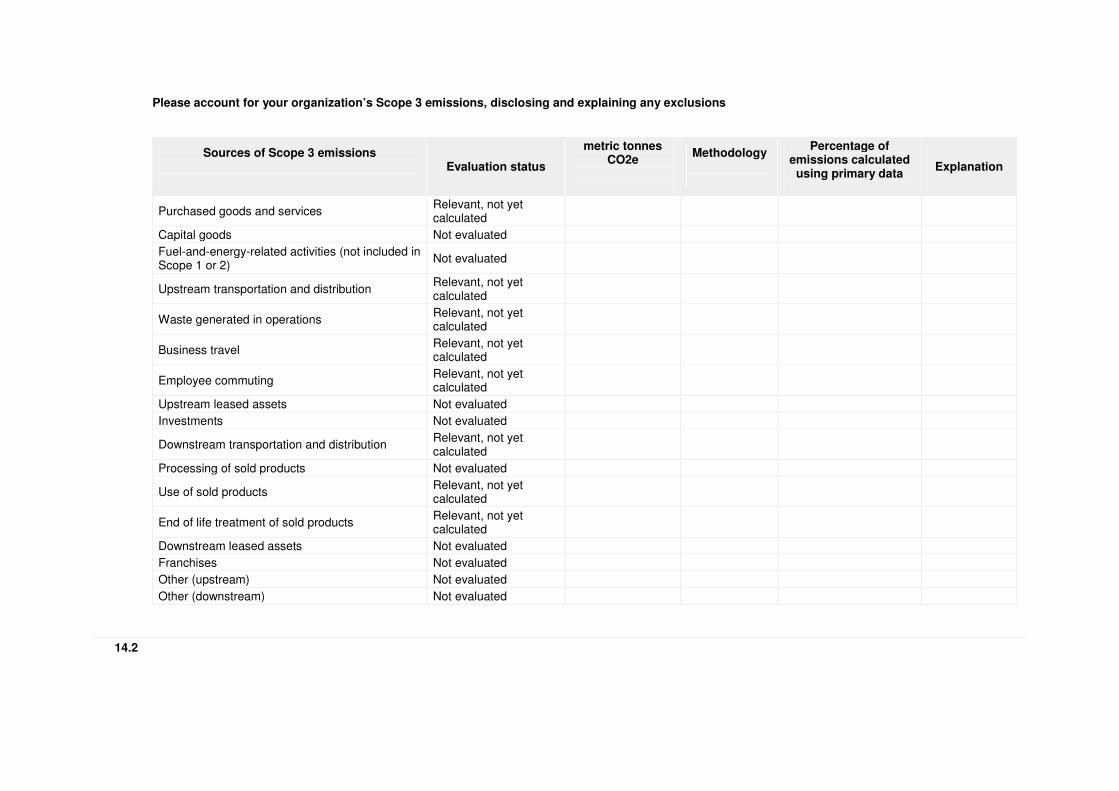

14.1

Please account for your organization’s Scope 3 emissions, disclosing and explaining any exclusions

Sources of Scope 3 emissions

Evaluation status

metric tonnes CO2e

Methodology

Percentage of emissions calculated

using primary data

Explanation

Purchased goods and services Relevant, not yet calculated

Capital goods Not evaluated

Fuel-and-energy-related activities (not included in Scope 1 or 2)

Not evaluated

Upstream transportation and distribution Relevant, not yet calculated

Waste generated in operations Relevant, not yet calculated

Business travel Relevant, not yet calculated

Employee commuting Relevant, not yet calculated

Upstream leased assets Not evaluated

Investments Not evaluated

Downstream transportation and distribution Relevant, not yet calculated

Processing of sold products Not evaluated

Use of sold products Relevant, not yet calculated

End of life treatment of sold products Relevant, not yet calculated

Downstream leased assets Not evaluated

Franchises Not evaluated

Other (upstream) Not evaluated

Other (downstream) Not evaluated

14.2

Please indicate the verification/assurance status that applies to your Scope 3 emissions No emissions data provided

14.2a

Please indicate the proportion of your Scope 3 emissions that are verified/assured

14.2b

Please provide further details of the verification/assurance undertaken, and attach the relevant statements

Type of verification or assurance

Relevant standard

Attach the document

14.3

Are you able to compare your Scope 3 emissions for the reporting year with those for the previous year for any sources? No, we don’t have any emissions data

14.3a

Please complete the table

Sources of Scope 3

emissions

Reason for change

Emissions value

(percentage)

Direction of change

Comment

14.4

Do you engage with any of the elements of your value chain on GHG emissions and climate change strategies? (Tick all that apply) No, we do not engage

14.4a

Please give details of methods of engagement, your strategy for prioritizing engagements and measures of success

14.4b

To give a sense of scale of this engagement, please give the number of suppliers with whom you are engaging and the proportion of your total spend that they represent

Number of suppliers

% of total spend Comment

14.4c

If you have data on your suppliers’ GHG emissions and climate change strategies, please explain how you make use of that data

How you make use of the data

Please give details

14.4d

Please explain why not and any plans you have to develop an engagement strategy in the future PZ Cussons plan to report on relevant scope 3 emissions in future CDP reports. Areas we are considering as a priority are emissions from products manufactured on our behalf by 3rd parties, corporate travel, and downstream distribution of good

Module: Sign Off

Page: Sign Off

Please enter the name of the individual that has signed off (approved) the response and their job title Duncan Cooper Halliwell PZ group Quality and Regulatory Affairs Executive

CDP